As filed with the Securities and Exchange Commission on May 2, 2018

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22842

FORUM FUNDS II

Three Canal Plaza, Suite 600

Portland, Maine 04101

Jessica Chase, Principal Executive Officer

Three Canal Plaza, Suite 600

Portland, Maine 04101

207-347-2000

Date of fiscal year end: February 28

Date of reporting period: March 1, 2017 – February 28, 2018

ITEM 1. REPORT TO STOCKHOLDERS.

NWS INTERNATIONAL PROPERTY FUND

NWS GLOBAL PROPERTY FUND

Annual Report

February 28, 2018

NWS INTERNATIONAL PROPERTY FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

FEBRUARY 28, 2018

The real estate markets globally continued to perform well as economic growth remained supportive of fundamentals. However, publicly listed real estate company performance was varied as the prospects for rising interest rates and a gradual reduction of quantitative easing weighed on stock performance, especially in the US where the Fed has already begun the process of normalization. As the year progressed, it became clearer that long-term rates were not rising as expected in the US in particular. The net result is that the public real estate market in the US and most of the world is trading well below the value of the underlying assets and demand for property by global investors is supportive of much higher valuations. The year was also characterized by a widening of dispersion in performance which favors active management, and the NWS International Property Fund (the “Fund”) outperformed its benchmark by 10%.

The Asian property markets, excluding Japan, were among the strongest performers having started 2017 at extreme levels of discounts to NAV as the public markets attempted to discount a China recession/economic meltdown. This has not occurred and it appears that the Chinese government has managed to engineer a modest slowdown while seeking to moderate the rising debt levels of consumers and local governments. Demand for residential property was stronger than expected and the Chinese developers were by far the best performing stocks worldwide. We would expect this trend to continue as the latest economic data for China has been better than expected and demand for property that is well-built and located is very strong, with companies trading at 30-50% discounts to NAV.

Hong Kong and Singapore property companies experienced strong gains throughout much of 2017. In Hong Kong, office demand has been very strong all year and the lack of supply has resulted in rental rates that are now the highest in the world. Singapore is benefiting from strong demand for office space which has absorbed the excess supply that had been developed recently at a far faster pace than expected. The residential market is also experiencing a surge in demand and low inventories, which led to a rapid rise in home prices. The public company share prices have yet to fully catch up to the rise in property values and are trading at 20-30% discounts to NAV. The Australian market has been the laggard, suffering from a slow-paced economic recovery and the fear that the central bank will tighten ahead of the recovery. As a result, the Aussie REITs have been trading at unusually wide discounts to NAV with dividend yields of 5-7%.

European property companies have been benefiting from an improving economic environment, strong demand for property, and very limited new supply. However, the property companies appear to be trading below the value of their portfolios which may be attributable to the political turmoil and concerns about the unwinding of quantitative easing. Political uncertainty in Spain, Italy, Germany, and of course the Brexit issue, provide ample support for caution while at the same time, the economic data continues to improve. Given these seemingly countervailing forces, stock selection has been paramount and the Fund has benefited from holdings in Germany, Spain and Sweden where the property markets have been performing well. Despite the challenges of Brexit, the UK real estate market is performing well, especially those companies that are either in the industrial/logistics sector or other non-traditional forms of real estate like student housing and storage.

For the 12 months ended 2/28/18, the Fund was up 23.69% compared to 13.50% for the FTSE EPRA/NAREIT Developed ex-US Total Return Index. The very strong relative outperformance was driven by stock selection in Japan where the Fund’s investments outperformed the Japanese real estate securities market in aggregate by over 20%. In addition, the Fund’s out-of-benchmark investments in China and Thailand were major drivers of absolute and relative performance, surging over 50% and 60%, respectively. The Fund’s European exposure also contributed positively primarily due to stock selection in the UK and investment in German residential specialist ADO Properties, which gained over 40% in US dollar terms.

Looking forward, there are several common themes to consider for this most heterogeneous and inefficient sector including:

|

●

|

Demand for real estate is well-supported. Recent surveys of institutional investors suggest that the future appetite for real estate is increasing despite expectations for lower returns. This is in addition to the current surfeit of capital already committed but not yet invested.

|

|

●

|

Attractive relative valuation. As compared with other asset classes, real estate securities in particular are trading at levels that are appreciably lower in terms of multiples/valuations. As compared with private real estate, we believe the public companies are priced from 10-50% below the value of their underlying assets.

|

|

●

|

Retail-oriented companies are oversold. While it is difficult to assess the ultimate impact of ecommerce and Millennial buying habits, all companies that are engaged in the retail sector worldwide are not homogeneous and yet they are priced as if they were.

|

|

●

|

Dispersion in performance will likely continue, providing opportunities for active management to continue to outperform.

|

|

●

|

Supply largely in check but pockets of oversupply need to be monitored. Property types with the lowest reproduction costs and fastest time to market like warehouses, self-storage, apartments and retail centers (excluding malls) should be most at risk.

|

|

●

|

Interest rate increases continue to weigh on the sector. As has been the case in the past, REITs in the US and Australia in particular will trade down as rates are rising – which has been occurring during the past 2 years – and then recover when either economic growth drives rents higher and/or it becomes clear that the rise in interest rates has peaked.

|

1

NWS INTERNATIONAL PROPERTY FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

FEBRUARY 28, 2018

Because the Fund concentrates its net assets in the real estate industry (by investing in equity REITs and other companies that invest in real estate assets), it is particularly vulnerable to the risks of the real estate industry, including those specific to equity REITs. Declines in real estate values, changes in interest rates, economic downturns, overbuilding and changes in zoning laws and government regulations can have a significant negative effect on companies in the real estate industry. Extended vacancies, a decline in rental income, failure to collect rents, increased competition from other properties and poor management can also affect the value and performance of equity REITs and companies that invest in real estate assets. The Fund is non-diversified, which means that the Fund may hold larger positions in fewer securities than other funds. Investing overseas involves special risks, including the volatility of currency exchange rates, and in some cases, political and economic instability, and relatively illiquid markets.

Emerging markets involve greater risks than more developed markets as they may be more volatile and less liquid. The Fund may invest in small and mid-sized capitalization companies meaning that these companies carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock.

2

NWS INTERNATIONAL PROPERTY FUND

PERFORMANCE CHART AND ANALYSIS (Unaudited)

FEBRUARY 28, 2018

The following chart reflects the change in the value of a hypothetical $1,000,000 investment in Institutional Shares, including reinvested dividends and distributions, in the NWS International Property Fund (the “Fund”) compared with the performance of the benchmark, the FTSE EPRA/NAREIT Developed ex-US Total Return Index (“Developed ex-US”), since inception. The Developed ex-US is an unmanaged subset of the FTSE EPRA/NAREIT Developed Index that incorporates Real Estate Investment Trusts (REITs) and Real Estate Holding & Development companies. The total return of the index includes the reinvestment of dividends and income. The total return of the Fund includes operating expenses that reduce returns, while the total return of the index does not include expenses. The Fund is professionally managed, while the index is unmanaged and is not available for investment.

Comparison of Change in Value of a $1,000,000 Investment

NWS International Property Fund vs. FTSE EPRA/NAREIT Developed ex-US Total Return Index

|

Average Annual Total Returns

Periods Ended February 28, 2018

|

One Year

|

Since Inception 03/31/15

|

|

NWS International Property Fund

|

23.69%

|

5.84%

|

|

FTSE EPRA/NAREIT Developed ex-US Total Return Index

|

13.50%

|

4.36%

|

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than original cost. As stated in the Fund’s prospectus, the annual operating Expense ratio (gross) is 4.41%. However, the Fund’s adviser has contractually agreed to waive its fee and/or reimburse Fund expenses to limit Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement (excluding all taxes, interest, portfolio transaction expenses, acquired fund fees and expenses, proxy expenses and extraordinary expenses) to 1.00%, through at least June 30, 2019 (the “Expense Cap”). The adviser may be reimbursed by the Fund for fees waived and expenses reimbursed by the adviser pursuant to the Expense Cap if such payment is approved by the Board, made within three years of the fee waiver or expense reimbursement, and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current expense cap, or (ii) the expense cap in place at the time the fees/expenses were waived/reimbursed. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. Shares redeemed or exchanged within 90 days of purchase will be charged a 1.50% redemption fee. The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns greater than one year are annualized. For the most recent month-end performance, please call (844) 218-5182.

3

NWS INTERNATIONAL PROPERTY FUND

SCHEDULE OF INVESTMENTS

FEBRUARY 28, 2018

|

Shares

|

Security Description

|

Value

|

||||

|

Common Stock - 95.2%

|

||||||

|

Australia - 9.6%

|

||||||

|

100,500

|

Mirvac Group REIT

|

$

|

165,484

|

|||

|

57,070

|

Stockland REIT

|

179,078

|

||||

|

36,270

|

The GPT Group REIT

|

134,094

|

||||

|

46,400

|

Vicinity Centres REIT

|

89,376

|

||||

|

568,032

|

||||||

|

Belgium - 2.1%

|

||||||

|

1,580

|

VGP NV (a)

|

123,366

|

||||

|

China - 8.4%

|

||||||

|

58,000

|

China Overseas Land & Investment, Ltd.

|

203,810

|

||||

|

46,000

|

China Resources Land, Ltd.

|

164,288

|

||||

|

91,992

|

KWG Property Holding, Ltd.

|

129,068

|

||||

|

497,166

|

||||||

|

France - 5.3%

|

||||||

|

6,800

|

Carmila SA REIT

|

198,275

|

||||

|

2,760

|

Klepierre SA REIT

|

114,249

|

||||

|

312,524

|

||||||

|

Germany - 3.4%

|

||||||

|

3,880

|

ADO Properties SA (b)

|

202,503

|

||||

|

Hong Kong - 16.0%

|

||||||

|

81,800

|

Hang Lung Properties, Ltd.

|

195,461

|

||||

|

13,500

|

Hongkong Land Holdings, Ltd.

|

93,015

|

||||

|

47,000

|

Hysan Development Co., Ltd.

|

272,358

|

||||

|

42,000

|

Kerry Properties, Ltd.

|

190,790

|

||||

|

131,245

|

New World Development Co., Ltd.

|

199,906

|

||||

|

951,530

|

||||||

|

Indonesia - 1.2%

|

||||||

|

868,100

|

Summarecon Agung Tbk PT

|

70,087

|

||||

|

Ireland - 2.0%

|

||||||

|

62,100

|

Green REIT PLC

|

116,370

|

||||

|

Japan - 18.0%

|

||||||

|

5,500

|

Aeon Mall Co., Ltd.

|

115,315

|

||||

|

6,000

|

Daiwa House Industry Co., Ltd.

|

223,647

|

||||

|

11,000

|

Mitsui Fudosan Co., Ltd.

|

265,785

|

||||

|

8,000

|

Sumitomo Realty & Development Co., Ltd.

|

292,497

|

||||

|

23,000

|

Tokyu Fudosan Holdings Corp.

|

170,730

|

||||

|

1,067,974

|

||||||

|

Netherlands - 6.5%

|

||||||

|

1,650

|

Unibail-Rodamco SE REIT

|

385,993

|

||||

|

Singapore - 6.6%

|

||||||

|

68,000

|

CapitaLand, Ltd.

|

186,330

|

||||

|

21,600

|

City Developments, Ltd.

|

208,051

|

||||

|

394,381

|

||||||

|

Spain - 2.6%

|

||||||

|

10,766

|

Merlin Properties Socimi SA REIT

|

154,528

|

||||

|

Sweden - 3.0%

|

||||||

|

8,200

|

Fabege AB

|

178,104

|

||||

|

Thailand - 3.7%

|

||||||

|

32,300

|

Central Pattana PCL, NVDR

|

86,692

|

||||

|

371,200

|

Land & Houses PCL, NVDR

|

130,080

|

||||

|

216,772

|

||||||

|

United Kingdom - 6.8%

|

||||||

|

16,063

|

Great Portland Estates PLC REIT

|

138,875

|

||||

|

7,781

|

Land Securities Group PLC REIT

|

99,301

|

||||

|

10,000

|

The UNITE Group PLC REIT

|

104,836

|

||||

|

15,100

|

Urban & Civic PLC

|

63,404

|

||||

|

406,416

|

||||||

|

Total Common Stock (Cost $4,815,038)

|

5,645,746

|

|||||

|

Investments, at value - 95.2% (Cost $4,815,038)

|

$

|

5,645,746

|

||||

|

Other Assets & Liabilities, Net - 4.8%

|

283,944

|

|||||

|

Net Assets - 100.0%

|

$

|

5,929,690

|

||||

| NVDR |

Non-Voting Depositary Receipt

|

| PCL |

Public Company Limited

|

| PLC |

Public Limited Company

|

| REIT |

Real Estate Investment Trust

|

| (a) |

Non-income producing security.

|

| (b) |

Security exempt from registration under Rule 144A under the Securities Act of 1933. At the period end, the value of these securities amounted to $202,503 or 3.4% of net assets.

|

The following is a summary of the inputs used to value the Fund’s investments as of February 28, 2018.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in Note 2 of the accompanying Notes to Financial Statements.

|

Valuation Inputs

|

Investments in Securities

|

|||

|

Level 1 - Quoted Prices

|

$

|

5,645,746

|

||

|

Level 2 - Other Significant Observable Inputs

|

–

|

|||

|

Level 3 - Significant Unobservable Inputs

|

–

|

|||

|

Total

|

$

|

5,645,746

|

||

The Level 1 value displayed in this table is Common Stock. Refer to this Schedule of Investments for a further breakout of each security by country.

The Fund utilizes the end of period methodology when determining transfers. There were no transfers among Level 1, Level 2 and Level 3 for the year ended February 28, 2018.

PORTFOLIO HOLDINGS (Unaudited)

|

% of Total Net Assets

|

|

|

Australia

|

9.6%

|

|

Belgium

|

2.1%

|

|

China

|

8.4%

|

|

France

|

5.3%

|

|

Germany

|

3.4%

|

|

Hong Kong

|

16.0%

|

|

Indonesia

|

1.2%

|

|

Ireland

|

2.0%

|

|

Japan

|

18.0%

|

|

Netherlands

|

6.5%

|

|

Singapore

|

6.6%

|

|

Spain

|

2.6%

|

|

Sweden

|

3.0%

|

|

Thailand

|

3.7%

|

|

United Kingdom

|

6.8%

|

|

Other Assets & Liabilities, Net

|

4.8%

|

|

|

100.0 %

|

See Notes Financial Statements.

4

NWS INTERNATIONAL PROPERTY FUND

STATEMENT OF ASSETS AND LIABILITIES

FEBRUARY 28, 2018

|

ASSETS

|

||||

|

Investments, at value (Cost $4,815,038)

|

$

|

5,645,746

|

||

|

Cash

|

310,255

|

|||

|

Receivables:

|

||||

|

Dividends and interest

|

5,683

|

|||

|

From investment adviser

|

1,968

|

|||

|

Prepaid expenses

|

7,865

|

|||

|

Total Assets

|

5,971,517

|

|||

|

LIABILITIES

|

||||

|

Payables:

|

||||

|

Foreign capital gains tax payable

|

8,029

|

|||

|

Accrued Liabilities:

|

||||

|

Fund services fees

|

7,101

|

|||

|

Other expenses

|

26,697

|

|||

|

Total Liabilities

|

41,827

|

|||

|

NET ASSETS

|

$

|

5,929,690

|

||

|

COMPONENTS OF NET ASSETS

|

||||

|

Paid-in capital

|

$

|

5,959,338

|

||

|

Distributions in excess of net investment income

|

(544,611

|

)

|

||

|

Accumulated net realized loss

|

(308,107

|

)

|

||

|

Net unrealized appreciation

|

823,070

|

|||

|

NET ASSETS

|

$

|

5,929,690

|

||

|

SHARES OF BENEFICIAL INTEREST AT NO PAR VALUE (UNLIMITED SHARES AUTHORIZED)

|

638,904

|

|||

|

NET ASSET VALUE, OFFERING AND REDEMPTION PRICE PER SHARE*

|

$

|

9.28

|

||

| * |

Shares redeemed or exchanged within 90 days of purchase are charged a 1.50% redemption fee.

|

See Notes Financial Statements.

5

NWS INTERNATIONAL PROPERTY FUND

STATEMENT OF OPERATIONS

YEAR ENDED FEBRAURY 28, 2018

|

INVESTMENT INCOME

|

||||

|

Dividend income (Net of foreign withholding taxes of$13,754)

|

$

|

162,787

|

||

|

Interest income

|

1,621

|

|||

|

Total Investment Income

|

164,408

|

|||

|

EXPENSES

|

||||

|

Investment adviser fees

|

41,679

|

|||

|

Fund services fees

|

98,337

|

|||

|

Custodian fees

|

10,417

|

|||

|

Registration fees

|

10,018

|

|||

|

Professional fees

|

25,157

|

|||

|

Trustees’ fees and expenses

|

2,199

|

|||

|

Other expenses

|

20,167

|

|||

|

Total Expenses

|

207,974

|

|||

|

Fees waived and expenses reimbursed

|

(152,401

|

)

|

||

|

Net Expenses

|

55,573

|

|||

|

NET INVESTMENT INCOME

|

108,835

|

|||

|

NET REALIZED AND UNREALIZED GAIN (LOSS)

|

||||

|

Net realized gain on:

|

||||

|

Investments (Net of foreign withholding taxes of $6,646)

|

289,625

|

|||

|

Foreign currency transactions

|

523

|

|||

|

Net realized gain

|

290,148

|

|||

|

Net change in unrealized appreciation (depreciation) on:

|

||||

|

Investments

|

772,432

|

|||

|

Deferred foreign capital gains taxes

|

(4,208

|

)

|

||

|

Foreign currency translations

|

323

|

|||

|

Net change in unrealized appreciation (depreciation)

|

768,547

|

|||

|

NET REALIZED AND UNREALIZED GAIN

|

1,058,695

|

|||

|

INCREASE IN NET ASSETS RESULTING FROM OPERATIONS

|

$

|

1,167,530

|

||

See Notes to Financial Statements.

6

NWS INTERNATIONAL PROPERTY FUND

STATEMENTS OF CHANGES IN NET ASSETS

|

For the

Year Ended February 28, 2018 |

For the

Year Ended February 28, 2017 |

|||||||

|

OPERATIONS

|

||||||||

|

Net investment income

|

$

|

108,835

|

$

|

82,168

|

||||

|

Net realized gain (loss)

|

290,148

|

(193,324

|

)

|

|||||

|

Net change in unrealized appreciation (depreciation)

|

768,547

|

507,855

|

||||||

|

Increase in Net Assets Resulting from Operations

|

1,167,530

|

396,699

|

||||||

|

DISTRIBUTIONS TO SHAREHOLDERS FROM

|

||||||||

|

Net investment income

|

(670,176

|

)

|

(339,897

|

)

|

||||

|

Total Distributions to Shareholders

|

(670,176

|

)

|

(339,897

|

)

|

||||

|

CAPITAL SHARE TRANSACTIONS

|

||||||||

|

Reinvestment of distributions

|

670,176

|

336,010

|

||||||

|

Redemption of shares

|

(222,268

|

)

|

(318,151

|

)

|

||||

|

Increase in Net Assets from Capital Share Transactions

|

447,908

|

17,859

|

||||||

|

Increase in Net Assets

|

945,262

|

74,661

|

||||||

|

NET ASSETS

|

||||||||

|

Beginning of Year

|

4,984,428

|

4,909,767

|

||||||

|

End of Year (Including line (a))

|

$

|

5,929,690

|

$

|

4,984,428

|

||||

|

SHARE TRANSACTIONS

|

||||||||

|

Reinvestment of distributions

|

73,646

|

42,532

|

||||||

|

Redemption of shares

|

(22,497

|

)

|

(40,069

|

)

|

||||

|

Increase in Shares

|

51,149

|

2,463

|

||||||

|

(a) Distributions in excess of net investment income

|

$

|

(544,611

|

)

|

$

|

(270,300

|

)

|

||

See Notes to Financial Statements.

7

NWS INTERNATIONAL PROPERTY FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each period.

|

For the Years Ended February 28,

|

March 31,

2015 (a) Through |

|||||||||||

|

2018

|

2017

|

February 29, 2016

|

||||||||||

|

INSTITUTIONAL SHARES

|

||||||||||||

|

NET ASSET VALUE, Beginning of Period

|

$

|

8.48

|

$

|

8.39

|

$

|

10.00

|

||||||

|

INVESTMENT OPERATIONS

|

||||||||||||

|

Net investment income (b)

|

0.18

|

0.14

|

0.05

|

|||||||||

|

Net realized and unrealized gain (loss)

|

1.81

|

0.53

|

(1.23

|

)

|

||||||||

|

Total from Investment Operations

|

1.99

|

0.67

|

(1.18

|

)

|

||||||||

|

DISTRIBUTIONS TO SHAREHOLDERS FROM

|

||||||||||||

|

Net investment income

|

(1.19

|

)

|

(0.58

|

)

|

(0.43

|

)

|

||||||

|

Total Distributions to Shareholders

|

(1.19

|

)

|

(0.58

|

)

|

(0.43

|

)

|

||||||

|

NET ASSET VALUE, End of Period

|

$

|

9.28

|

$

|

8.48

|

$

|

8.39

|

||||||

|

TOTAL RETURN

|

23.69

|

%

|

8.50

|

%

|

(12.09

|

)%(c)

|

||||||

|

RATIOS/SUPPLEMENTARY DATA

|

||||||||||||

|

Net Assets at End of Period (000s omitted)

|

$

|

5,930

|

$

|

4,984

|

$

|

4,910

|

||||||

|

Ratios to Average Net Assets:

|

||||||||||||

|

Net investment income

|

1.96

|

%

|

1.59

|

%

|

0.55

|

%(d)

|

||||||

|

Net expenses

|

1.00

|

%

|

1.00

|

%

|

1.00

|

%(d)

|

||||||

|

Gross expenses (e)

|

3.74

|

%

|

4.41

|

%

|

8.26

|

%(d)

|

||||||

|

PORTFOLIO TURNOVER RATE

|

38

|

%

|

30

|

%

|

17

|

%(c)

|

||||||

|

(a)

|

Commencement of operations.

|

|

(b)

|

Calculated based on average shares outstanding during each period.

|

|

(c)

|

Not annualized.

|

|

(d)

|

Annualized.

|

|

(e)

|

Reflects the expense ratio excluding any waivers and/or reimbursements.

|

See Notes to Financial Statements.

8

NWS GLOBAL PROPERTY FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

FEBRUARY 28, 2018

The real estate markets globally continued to perform well as economic growth remained supportive of fundamentals. However, publicly listed real estate company performance was varied as the prospects for rising interest rates and a gradual reduction of quantitative easing weighed on stock performance, especially in the US where the Fed has already begun the process of normalization. As the year progressed, it became clearer that long-term rates were not rising as expected in the US in particular. The net result is that the public real estate market in the US and most of the world is trading well below the value of the underlying assets and demand for property by global investors is supportive of much higher valuations. The year was also characterized by a widening of dispersion in performance which favors active management, and the NWS Global Property Fund (the “Fund”) outperformed its benchmark by nearly 4% despite the challenging environment.

The US REIT market was expected to be most directly affected by the expectation of rising interest rates throughout much of 2017, but the greatest impact occurred in the first two months of 2018 when the 10-year Treasury bond surged 55bps, from 2.4% to 2.95%. The speed of this increase, not necessarily the magnitude, may have been responsible for the sharp decline in REITs (10%) and other yield-sensitive investments. Over the past 12 months, REITs that focus on retail have been the hardest hit and are trading at the widest discounts to NAV (up to 40%) while the industrial/logistics REITs are the star performers - and are trading above NAVs. This is being referred to as the Amazon effect, where delivery of goods now takes precedence over the retail experience of shopping in physical stores. Warehouse/logistics REITs rose 10-25% while some of the retail REITs declined by an equally large amount. The hotel sector also performed well, but this was more a function of recovering from significant declines in 2016 rather than dramatically improving market conditions. Office and apartment REITs struggled throughout the year but for different reasons and the performance was highly dependent on each company’s target markets. Apartment supply has been rising over the past several years and rental growth is slowing, especially in New York, while office demand has been improving but the impact of WeWork and similar sharing concepts as well as general tenant resistance to rent increases has affected rental growth. Given the relatively modest growth in office supply since the 2008 recession and the increase in employment, we would have expected greater rental growth at this point in the cycle but this has yet to materialize. The US REIT market overall is trading at a 15% discount to NAV which is especially unusual given the strong underlying demand for property and the relative lack of supply.

The Asian property markets, excluding Japan, were among the strongest performers having started 2017 at extreme levels of discounts to NAV as the public markets attempted to discount a China recession/economic meltdown. This has not occurred and it appears that the Chinese government has managed to engineer a modest slowdown while seeking to moderate the rising debt levels of consumers and local governments. Demand for residential property was stronger than expected and the Chinese developers were by far the best performing stocks worldwide. We would expect this trend to continue as the latest economic data for China has been better than expected and demand for property that is well-built and located is very strong, with companies trading at 30-50% discounts to NAV.

Hong Kong and Singapore property companies experienced strong gains throughout much of 2017. In Hong Kong, office demand has been very strong all year and the lack of supply has resulted in rental rates that are now the highest in the world. Singapore is benefiting from strong demand for office space which has absorbed the excess supply that had been developed recently at a far faster pace than expected. The residential market is also experiencing a surge in demand and low inventories, which led to a rapid rise in home prices. The public company share prices have yet to fully catch up to the rise in property values and are trading at 20-30% discounts to NAV. The Australian market has been the laggard, suffering from a slow-paced economic recovery and the fear that the central bank will tighten ahead of the recovery. As a result, the Aussie REITs have been trading at unusually wide discounts to NAV with dividend yields of 5-7%.

European property companies have been benefiting from an improving economic environment, strong demand for property, and very limited new supply. However, the property companies appear to be trading below the value of their portfolios which may be attributable to the political turmoil and concerns about the unwinding of quantitative easing. Political uncertainty in Spain, Italy, Germany, and of course the Brexit issue, provide ample support for caution while at the same time, the economic data continues to improve. Given these seemingly countervailing forces, stock selection has been paramount and the Fund has benefited from holdings in Germany, Spain and Sweden where the property markets have been performing well. Despite the challenges of Brexit, the UK real estate market is performing well, especially those companies that are either in the industrial/logistics sector or other non-traditional forms of real estate like student housing and storage.

For the 12 months ended 2/28/18, the Fund was up 4.02% compared to 0.27% for the FTSE EPRA/NAREIT Developed Total Return Index. The relative outperformance was driven by stock selection in Asia and the US, and to a lesser extent Europe. The Fund’s investments in Japan contributed most, followed by HK/China and Singapore, with stocks gaining over 20%, 30% and 40%, respectively. Although the US market overall was down for the period, the Fund’s investments in the manufactured housing and industrial sectors were up single and double digits, respectively, and contributed to both relative and absolute performance. German residential specialist ADO Properties was the largest contributor in Europe, returning over 40% in US dollar terms.

9

NWS GLOBAL PROPERTY FUND

A MESSAGE TO OUR SHAREHOLDERS (Unaudited)

FEBRUARY 28, 2018

Looking forward, there are several common themes to consider for this most heterogeneous and inefficient sector including:

| • |

Demand for real estate is well-supported. Recent surveys of institutional investors suggest that the future appetite for real estate is increasing despite expectations for lower returns. This is in addition to the current surfeit of capital already committed but not yet invested.

|

| • |

Attractive relative valuation. As compared with other asset classes, real estate securities in particular are trading at levels that are appreciably lower in terms of multiples/valuations. As compared with private real estate, we believe the public companies are priced from 10-50% below the value of their underlying assets.

|

| • |

Retail-oriented companies are oversold. While it is difficult to assess the ultimate impact of ecommerce and Millennial buying habits, all companies that are engaged in the retail sector worldwide are not homogeneous and yet they are priced as if they were.

|

| • |

Dispersion in performance will likely continue, providing opportunities for active management to continue to outperform.

|

| • |

Supply largely in check but pockets of oversupply need to be monitored. Property types with the lowest reproduction costs and fastest time to market like warehouses, self-storage, apartments and retail centers (excluding malls) should be most at risk.

|

| • |

Interest rate increases continue to weigh on the sector. As has been the case in the past, REITs in the US and Australia in particular will trade down as rates are rising - which has been occurring during the past 2 years - and then recover when either economic growth drives rents higher and/or it becomes clear that the rise in interest rates has peaked.

|

Because the Fund concentrates its net assets in the real estate industry (by investing in equity REITs and other companies that invest in real estate assets), it is particularly vulnerable to the risks of the real estate industry, including those specific to equity REITs. Declines in real estate values, changes in interest rates, economic downturns, overbuilding and changes in zoning laws and government regulations can have a significant negative effect on companies in the real estate industry. Extended vacancies, a decline in rental income, failure to collect rents, increased competition from other properties and poor management can also affect the value and performance of equity REITs and companies that invest in real estate assets. The Fund is non-diversified, which means that the Fund may hold larger positions in fewer securities than other funds. Investing overseas involves special risks, including the volatility of currency exchange rates, and in some cases, political and economic instability, and relatively illiquid markets.

Emerging markets involve greater risks than more developed markets as they may be more volatile and less liquid. The Fund may invest in small and mid-sized capitalization companies meaning that these companies carry greater risk than is customarily associated with larger companies for various reasons such as narrower markets, limited financial resources and less liquid stock.

10

NWS GLOBAL PROPERTY FUND

PERFORMANCE CHART AND ANALYSIS (Unaudited)

FEBRUARY 28, 2018

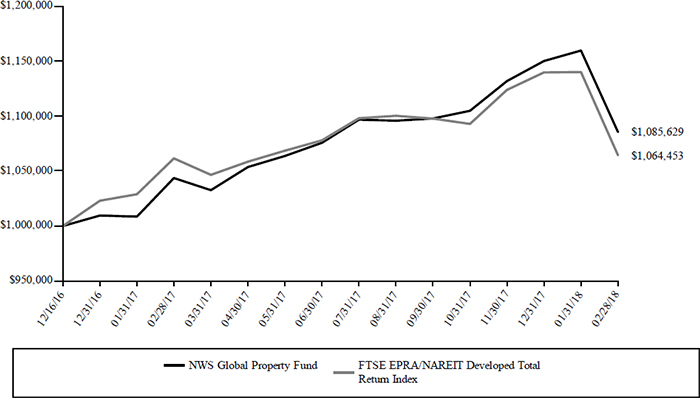

The following chart reflects the change in the value of a hypothetical $1,000,000 investment in Institutional Shares, including reinvested dividends and distributions, in the NWS Global Property Fund (the “Fund”) compared with the performance of the benchmark, FTSE EPRA/NAREIT Developed Total Return Index (“Developed Index”), since inception. The Developed Index incorporates Real Estate Investment Trusts (REITs) and Real Estate Holding & Development companies. The total return of the index includes the reinvestment of dividends and income. The total return of the Fund includes operating expenses that reduce returns, while the total return of the index does not include expenses. The Fund is professionally managed, while the index is unmanaged and is not available for investment.

Comparison of Change in Value of a $1,000,000 Investment

NWS Global Property Fund vs. FTSE EPRA/NAREIT Developed Total Return Index

NWS Global Property Fund vs. FTSE EPRA/NAREIT Developed Total Return Index

|

Average Annual Total Returns

Periods Ended February 28, 2018

|

One Year

|

Since Inception 12/16/16

|

|

NWS Global Property Fund

|

4.02%

|

7.07%

|

|

FTSE EPRA/NAREIT Developed Total Return Index

|

0.27%

|

5.33%

|

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than the performance data quoted. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than original cost. As stated in the Fund’s prospectus, the annual operating Expense ratio (gross) is 33.40%. However, the Fund’s adviser has contractually agreed to waive its fee and/or reimburse Fund expenses to limit Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement (excluding all taxes, interest, portfolio transaction expenses, acquired fund fees and expenses, proxy expenses and extraordinary expenses) to 0.90%, through at least June 30, 2019 (the “Expense Cap”). The adviser may be reimbursed by the Fund for fees waived and expenses reimbursed by the adviser pursuant to the Expense Cap if such payment is approved by the Board, made within three years of the fee waiver or expense reimbursement, and does not cause the Total Annual Fund Operating Expenses After Fee Waiver and/or Expense Reimbursement to exceed the lesser of (i) the then-current expense cap, or (ii) the expense cap in place at the time the fees/expenses were waived/reimbursed. During the period, certain fees were waived and/or expenses reimbursed; otherwise, returns would have been lower. Shares redeemed or exchanged within 90 days of purchase will be charged a 1.50% redemption fee. The performance table and graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Returns greater than one year are annualized. For the most recent month-end performance, please call (844) 218-5182.

11

NWS GLOBAL PROPERTY FUND

SCHEDULE OF INVESTMENTS

FEBRUARY 28, 2018

|

Shares

|

Security Description | Value | ||||

|

Common Stock - 90.7%

|

||||||

|

Australia - 4.6%

|

||||||

|

66,900

|

Mirvac Group REIT

|

$

|

110,158

|

|||

|

34,800

|

Stockland REIT

|

109,198

|

||||

|

56,900

|

Vicinity Centres REIT

|

109,601

|

||||

|

328,957

|

||||||

|

Belgium - 1.3%

|

||||||

|

1,220

|

VGP NV (a)

|

95,258

|

||||

|

China - 4.1%

|

||||||

|

41,000

|

China Overseas Land & Investment, Ltd.

|

144,073

|

||||

|

42,000

|

China Resources Land, Ltd.

|

150,002

|

||||

|

294,075

|

||||||

|

France - 2.3%

|

||||||

|

5,760

|

Carmila SA REIT

|

167,950

|

||||

|

Germany - 2.4%

|

||||||

|

3,330

|

ADO Properties SA (b)

|

173,798

|

||||

|

Hong Kong - 5.7%

|

||||||

|

24,000

|

Hysan Development Co., Ltd.

|

139,077

|

||||

|

30,000

|

Kerry Properties, Ltd.

|

136,278

|

||||

|

90,531

|

New World Development Co., Ltd.

|

137,892

|

||||

|

413,247

|

||||||

|

Ireland - 1.4%

|

||||||

|

52,800

|

Green REIT PLC

|

98,943

|

||||

|

Japan - 8.9%

|

||||||

|

6,400

|

Aeon Mall Co., Ltd.

|

134,184

|

||||

|

4,200

|

Daiwa House Industry Co., Ltd.

|

156,553

|

||||

|

7,000

|

Mitsui Fudosan Co., Ltd.

|

169,136

|

||||

|

5,000

|

Sumitomo Realty & Development Co., Ltd.

|

182,811

|

||||

|

642,684

|

||||||

|

Netherlands - 2.8%

|

||||||

|

860

|

Unibail-Rodamco SE REIT

|

201,184

|

||||

|

Singapore - 2.2%

|

||||||

|

16,300

|

City Developments, Ltd.

|

157,002

|

||||

|

Spain - 1.6%

|

||||||

|

7,800

|

Merlin Properties Socimi SA REIT

|

111,956

|

||||

|

Sweden - 2.0%

|

||||||

|

6,570

|

Fabege AB

|

142,700

|

||||

|

United Kingdom - 3.9%

|

||||||

|

8,984

|

Great Portland Estates PLC REIT

|

77,673

|

||||

|

4,911

|

Land Securities Group PLC REIT

|

62,674

|

||||

|

6,690

|

The UNITE Group PLC REIT

|

70,135

|

||||

|

15,997

|

Urban & Civic PLC

|

67,170

|

||||

|

277,652

|

||||||

|

United States - 47.5%

|

||||||

|

2,850

|

Agree Realty Corp. REIT

|

134,235

|

||||

|

870

|

AvalonBay Communities, Inc. REIT

|

135,737

|

||||

|

7,750

|

CareTrust REIT, Inc.

|

102,687

|

||||

|

17,440

|

Cousins Properties, Inc. REIT

|

145,450

|

||||

|

2,660

|

DCT Industrial Trust, Inc. REIT

|

147,231

|

||||

|

17,960

|

DDR Corp. REIT

|

140,088

|

||||

|

3,770

|

Douglas Emmett, Inc. REIT

|

134,777

|

||||

|

3,900

|

Education Realty Trust, Inc. REIT

|

121,446

|

||||

|

2,030

|

Equity LifeStyle Properties, Inc. REIT

|

171,758

|

||||

|

1,570

|

Extra Space Storage, Inc. REIT

|

133,529

|

||||

|

7,880

|

Healthcare Trust of America, Inc., Class A REIT

|

195,818

|

||||

|

2,830

|

Highwoods Properties, Inc. REIT

|

121,718

|

||||

|

1,280

|

Life Storage, Inc. REIT

|

100,557

|

||||

|

1,570

|

Mid-America Apartment Communities, Inc. REIT

|

134,737

|

||||

|

2,150

|

National Health Investors, Inc. REIT

|

139,471

|

||||

|

Shares

|

Security Description | Value | |||||

|

United States - 47.5% (continued)

|

|||||||

|

5,306

|

NexPoint Residential Trust, Inc. REIT

|

$

|

127,928

|

||||

|

9,240

|

Paramount Group, Inc. REIT

|

128,898

|

|||||

|

2,615

|

Regency Centers Corp. REIT

|

151,958

|

|||||

|

1,160

|

Simon Property Group, Inc. REIT

|

178,072

|

|||||

|

9,040

|

Summit Hotel Properties, Inc. REIT

|

119,057

|

|||||

|

1,740

|

Sun Communities, Inc. REIT

|

152,354

|

|||||

|

7,690

|

Sunstone Hotel Investors, Inc. REIT

|

110,967

|

|||||

|

3,880

|

Taubman Centers, Inc. REIT

|

226,825

|

|||||

|

4,700

|

Terreno Realty Corp. REIT

|

156,557

|

|||||

|

|

3,411,855

|

||||||

| Total Common Stock (Cost $6,629,170) |

6,517,261

|

||||||

| Investments, at value - 90.7% (Cost $6,629,170) |

$

|

6,517,261

|

|||||

| Other Assets & Liabilities, Net - 9.3% |

665,232

|

||||||

|

Net Assets - 100.0%

|

$

|

7,182,493

|

|||||

|

PLC

|

Public Limited Company

|

|

REIT

|

Real Estate Investment Trust

|

|

(a)

|

Non-income producing security.

|

|

(b)

|

Security exempt from registration under Rule 144A under the Securities Act of 1933. At the period end, the value of these securities amounted to $173,798 or 2.4% of net assets.

|

The following is a summary of the inputs used to value the Fund’s investments as of February 28, 2018.

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. For more information on valuation inputs, and their aggregation into the levels used in the table below, please refer to the Security Valuation section in Note 2 of the accompanying Notes to Financial Statements.

|

Valuation Inputs

|

Investments in Securities

|

|||

|

Level 1 - Quoted Prices

|

$

|

6,517,261

|

||

|

Level 2 - Other Significant Observable Inputs

|

–

|

|||

|

Level 3 - Significant Unobservable Inputs

|

–

|

|||

|

Total

|

$

|

6,517,261

|

||

The Level 1 value displayed in this table is Common Stock. Refer to this Schedule of Investments for a further breakout of each security by country.

The Fund utilizes the end of period methodology when determining transfers. There were no transfers among Level 1, Level 2 and Level 3 for the year ended February 28, 2018.

|

PORTFOLIO HOLDINGS (Unaudited)

|

|

|

% of Total Net Assets

|

|

|

Australia

|

4.6%

|

|

Belgium

|

1.3%

|

|

China

|

4.1%

|

|

France

|

2.3%

|

|

Germany

|

2.4%

|

|

Hong Kong

|

5.7%

|

|

Ireland

|

1.4%

|

|

Japan

|

8.9%

|

|

Netherlands

|

2.8%

|

|

Singapore

|

2.2%

|

|

Spain

|

1.6%

|

|

Sweden

|

2.0%

|

|

United Kingdom

|

3.9%

|

|

United States

|

47.5%

|

|

Other Assets & Liabilities, Net

|

9.3%

|

|

100.0%

|

See Notes to Financial Statements.

12

NWS GLOBAL PROPERTY FUND

STATEMENT OF ASSETS AND LIABILITIES

FEBRUARY 28, 2018

|

ASSETS

|

||||

|

Investments, at value (Cost $6,629,170)

|

$

|

6,517,261

|

||

|

Cash

|

1,916,605

|

|||

|

Receivables:

|

||||

|

Fund shares sold

|

985

|

|||

|

Dividends and interest

|

816

|

|||

|

From investment adviser

|

12,269

|

|||

|

Prepaid expenses

|

5,725

|

|||

|

Total Assets

|

8,453,661

|

|||

|

LIABILITIES

|

||||

|

Payables:

|

||||

|

Investment securities purchased

|

1,237,660

|

|||

|

Accrued Liabilities:

|

||||

|

Fund services fees

|

6,150

|

|||

|

Other expenses

|

27,358

|

|||

|

Total Liabilities

|

1,271,168

|

|||

|

NET ASSETS

|

$

|

7,182,493

|

||

|

COMPONENTS OF NET ASSETS

|

||||

|

Paid-in capital

|

$

|

7,334,143

|

||

|

Distributions in excess of net investment income

|

(39,684

|

)

|

||

|

Accumulated net realized loss

|

(354

|

)

|

||

|

Net unrealized depreciation

|

(111,612

|

)

|

||

|

NET ASSETS

|

$

|

7,182,493

|

||

|

SHARES OF BENEFICIAL INTEREST AT NO PAR VALUE (UNLIMITED SHARES AUTHORIZED)

|

701,091

|

|||

|

NET ASSET VALUE, OFFERING AND REDEMPTION PRICE PER SHARE*

|

$

|

10.24

|

||

|

*

|

Shares redeemed or exchanged within 90 days of purchase are charged a 1.50% redemption fee.

|

See Notes to Financial Statements.

13

NWS GLOBAL PROPERTY FUND

STATEMENT OF OPERATIONS

YEAR ENDED FEBRUARY 28, 2018

|

INVESTMENT INCOME

|

||||

|

Dividend income (Net of foreign withholding taxes of $1,458)

|

$

|

30,131

|

||

|

Interest income

|

415

|

|||

|

Total Investment Income

|

30,546

|

|||

|

EXPENSES

|

||||

|

Investment adviser fees

|

7,927

|

|||

|

Fund services fees

|

84,663

|

|||

|

Custodian fees

|

10,174

|

|||

|

Registration fees

|

4,889

|

|||

|

Professional fees

|

30,607

|

|||

|

Trustees' fees and expenses

|

2,011

|

|||

|

Offering costs

|

22,436

|

|||

|

Other expenses

|

18,575

|

|||

|

Total Expenses

|

181,282

|

|||

|

Fees waived and expenses reimbursed

|

(170,943

|

)

|

||

|

Net Expenses

|

10,339

|

|||

|

NET INVESTMENT INCOME

|

20,207

|

|||

|

NET REALIZED AND UNREALIZED GAIN (LOSS)

|

||||

|

Net realized gain on:

|

||||

|

Investments

|

5,728

|

|||

|

Foreign currency transactions

|

694

|

|||

|

Net realized gain

|

6,422

|

|||

|

Net change in unrealized appreciation (depreciation) on:

|

||||

|

Investments

|

(139,353

|

)

|

||

|

Foreign currency translations

|

286

|

|||

|

Net change in unrealized appreciation (depreciation)

|

(139,067

|

)

|

||

|

NET REALIZED AND UNREALIZED LOSS

|

(132,645

|

)

|

||

|

DECREASE IN NET ASSETS RESULTING FROM OPERATIONS

|

$

|

(112,438

|

)

|

|

See Notes to Financial Statements.

14

NWS GLOBAL PROPERTY FUND

STATEMENTS OF CHANGES IN NET ASSETS

|

For the

Year Ended February 28, 2018 |

December 16,

2016* Through February 28, 2017 |

|||||||

|

OPERATIONS

|

||||||||

|

Net investment income

|

$

|

20,207

|

$

|

2,885

|

||||

|

Net realized gain

|

6,422

|

1,333

|

||||||

|

Net change in unrealized appreciation (depreciation)

|

(139,067

|

)

|

27,455

|

|||||

|

Increase (Decrease) in Net Assets Resulting from Operations

|

(112,438

|

)

|

31,673

|

|||||

|

DISTRIBUTIONS TO SHAREHOLDERS FROM

|

||||||||

|

Net investment income

|

(67,043

|

)

|

(2,554

|

)

|

||||

|

Net realized gain

|

(1,288

|

)

|

–

|

|||||

|

Total Distributions to Shareholders

|

(68,331

|

)

|

(2,554

|

)

|

||||

|

CAPITAL SHARE TRANSACTIONS

|

||||||||

|

Sale of shares

|

6,548,542

|

718,161

|

||||||

|

Reinvestment of distributions

|

65,075

|

2,365

|

||||||

|

Increase in Net Assets from Capital Share Transactions

|

6,613,617

|

720,526

|

||||||

|

Increase in Net Assets

|

6,432,848

|

749,645

|

||||||

|

NET ASSETS

|

||||||||

|

Beginning of Year

|

749,645

|

–

|

||||||

|

End of Year (Including line (a))

|

$

|

7,182,493

|

$

|

749,645

|

||||

|

SHARE TRANSACTIONS

|

||||||||

|

Sale of shares

|

623,045

|

71,816

|

||||||

|

Reinvestment of distributions

|

5,992

|

238

|

||||||

|

Increase in Shares

|

629,037

|

72,054

|

||||||

|

(a) Undistributed (distributions in excess of ) net investment income

|

$

|

(39,684

|

)

|

$

|

355

|

|||

|

*

|

Commencement of operations.

|

See Notes to Financial Statements.

15

NWS GLOBAL PROPERTY FUND

FINANCIAL HIGHLIGHTS

These financial highlights reflect selected data for a share outstanding throughout each period.

|

For the

Year Ended February 28, 2018 |

December 16,

2016 (a) Through February 28, 2017 |

|||||||

|

INSTITUTIONAL SHARES

|

||||||||

|

NET ASSET VALUE, Beginning of Period

|

$

|

10.40

|

$

|

10.00

|

||||

|

INVESTMENT OPERATIONS

|

||||||||

|

Net investment income (b)

|

0.20

|

0.04

|

||||||

|

Net realized and unrealized gain

|

0.25

|

(c)

|

0.40

|

|||||

|

Total from Investment Operations

|

0.45

|

0.44

|

||||||

|

DISTRIBUTIONS TO SHAREHOLDERS FROM

|

||||||||

|

Net investment income

|

(0.60

|

)

|

(0.04

|

)

|

||||

|

Net realized gain

|

(0.01

|

)

|

–

|

|||||

|

Total Distributions to Shareholders

|

(0.61

|

)

|

(0.04

|

)

|

||||

|

NET ASSET VALUE, End of Period

|

$

|

10.24

|

$

|

10.40

|

||||

|

TOTAL RETURN

|

4.02

|

%

|

4.37

|

%(d)

|

||||

|

RATIOS/SUPPLEMENTARY DATA

|

||||||||

|

Net Assets at End of Period (000s omitted)

|

$

|

7,182

|

$

|

750

|

||||

|

Ratios to Average Net Assets:

|

||||||||

|

Net investment income

|

1.91

|

%

|

1.98

|

%(e)

|

||||

|

Net expenses

|

0.98

|

%

|

1.00

|

%(e)

|

||||

|

Gross expenses (f)

|

17.15

|

%

|

33.40

|

%(e)

|

||||

|

PORTFOLIO TURNOVER RATE

|

27

|

%

|

17

|

%(d)

|

||||

|

(a)

|

Commencement of operations.

|

|

(b)

|

Calculated based on average shares outstanding during each period.

|

|

(c)

|

Per share amount does not accord with the amount reported in the statement of operations due to the timing of Fund share sales and the amount per share of realized and unrealized gains and losses at such time.

|

|

(d)

|

Not annualized.

|

|

(e)

|

Annualized.

|

|

(f)

|

Reflects the expense ratio excluding any waivers and/or reimbursements.

|

See Notes to Financial Statements.

16

NWS FUNDS

NOTES TO FINANCIAL STATEMENTS

FEBRUARY 28, 2018

Note 1. Organization

NWS International Property Fund and NWS Global Property Fund (individually, a “Fund” and collectively, the “Funds”) are non-diversified portfolios of Forum Funds II (the “Trust”). The Trust is a Delaware statutory trust that is registered as an open-end, management investment company under the Investment Company Act of 1940, as amended (the “Act”). Under its Trust Instrument, the Trust is authorized to issue an unlimited number of each Fund’s shares of beneficial interest without par value. The NWS International Property Fund and NWS Global Property Fund commenced operations on March 31, 2015, and December 16, 2016, respectively. Each Fund currently offers one class of shares: Institutional Shares. Each Fund seeks to generate maximum total return through current income and capital appreciation by investing in real estate-related and equity-linked securities internationally.

Note 2. Summary of Significant Accounting Policies

The Funds are investment companies and follow accounting and reporting guidance under Financial Accounting Standards Board (“FASB”) Accounting Standards Codification (“ASC”) Topic 946, “Financial Services-Investment Companies”. These financial statements are prepared in accordance with accounting principles generally accepted in the United States of America (“GAAP”), which require management to make estimates and assumptions that affect the reported amounts of assets and liabilities, the disclosure of contingent liabilities at the date of the financial statements, and the reported amounts of increases and decreases in net assets from operations during the fiscal year. Actual amounts could differ from those estimates. The following summarizes the significant accounting policies of each Fund:

Security Valuation - Securities are valued at market prices using the last quoted trade or official closing price from the principal exchange where the security is traded, as provided by independent pricing services on each Fund business day. In the absence of a last trade, securities are valued at the mean of the last bid and ask price provided by the pricing service. Shares of non-exchange traded open-end mutual funds are valued at net asset value (“NAV”). Short-term investments that mature in sixty days or less may be valued at amortized cost.

Each Fund values its investments at fair value pursuant to procedures adopted by the Trust’s Board of Trustees (the “Board”) if (1) market quotations are not readily available or (2) the Adviser, as defined in Note 4, believes that the values available are unreliable. The Trust’s Valuation Committee, as defined in each Fund’s registration statement, performs certain functions as they relate to the administration and oversight of each Fund’s valuation procedures. Under these procedures, the Valuation Committee convenes on a regular and ad hoc basis to review such investments and considers a number of factors, including valuation methodologies and significant unobservable inputs, when arriving at fair value.

The Valuation Committee may work with the Adviser to provide valuation inputs. In determining fair valuations, inputs may include market-based analytics that may consider related or comparable assets or liabilities, recent transactions, market multiples, book values and other relevant investment information. Adviser inputs may include an income-based approach in which the anticipated future cash flows of the investment are discounted in determining fair value. Discounts may also be applied based on the nature or duration of any restrictions on the disposition of the investments. The Valuation Committee performs regular reviews of valuation methodologies, key inputs and assumptions, disposition analysis and market activity.

Fair valuation is based on subjective factors and, as a result, the fair value price of an investment may differ from the security’s market price and may not be the price at which the asset may be sold. Fair valuation could result in a different NAV than a NAV determined by using market quotes.

GAAP has a three-tier fair value hierarchy. The basis of the tiers is dependent upon the various “inputs” used to determine the value of each Fund’s investments. These inputs are summarized in the three broad levels listed below:

Level 1 - Quoted prices in active markets for identical assets and liabilities

Level 2 - Prices determined using significant other observable inputs (including quoted prices for similar securities, interest rates, prepayment speeds, credit risk, etc.). Short-term securities with maturities of sixty days or less are valued at amortized cost, which approximates market value, and are categorized as Level 2 in the hierarchy. Municipal securities, long-term U.S. government obligations and corporate debt securities are valued in accordance with the evaluated price supplied by the pricing service and generally categorized as Level 2 in the hierarchy. Other securities that are categorized as Level 2 in the hierarchy include, but are not limited to, warrants that do not trade on an exchange, securities valued at the mean between the last reported bid and ask quotation and international equity

17

NWS FUNDS

NOTES TO FINANCIAL STATEMENTS

FEBRUARY 28, 2018

securities valued by an independent third party with adjustments for changes in value between the time of the securities respective local market closes and the close of the U.S. market.

Level 3 - Significant unobservable inputs (including each Fund’s own assumptions in determining the fair value of investments)

The aggregate value by input level, as of February 28, 2018, for each Fund’s investments is included in each Fund’s Schedule of Investments.

Security Transactions, Investment Income and Realized Gain and Loss - Investment transactions are accounted for on the trade date. Dividend income are recorded on the ex-dividend date. Foreign dividend income are recorded on the ex-dividend date or as soon as possible after determining the existence of a dividend declaration after exercising reasonable due diligence. Income and capital gains on some foreign securities may be subject to foreign withholding taxes, which are accrued as applicable. Interest income is recorded on an accrual basis. Premium is amortized and discount is accreted using the effective interest method. Identified cost of investments sold is used to determine the gain and loss for both financial statement and federal income tax purposes.

Foreign Currency Translations - Foreign currency amounts are translated into U.S. dollars as follows: (1) assets and liabilities at the rate of exchange at the end of the respective period; and (2) purchases and sales of securities and income and expenses at the rate of exchange prevailing on the dates of such transactions. The portion of the results of operations arising from changes in the exchange rates and the portion due to fluctuations arising from changes in the market prices of securities are not isolated. Such fluctuations are included with the net realized and unrealized gain or loss on investments.

Foreign Currency Transactions - Each Fund may enter into transactions to purchase or sell foreign currency contracts and options on foreign currency. Forward currency contracts are agreements to exchange one currency for another at a future date and at a specified price. A fund may use forward currency contracts to facilitate transactions in foreign securities, to manage a fund’s foreign currency exposure and to protect the U.S. dollar value of its underlying portfolio securities against the effect of possible adverse movements in foreign exchange rates. These contracts are intrinsically valued daily based on forward rates, and a fund’s net equity therein, representing unrealized gain or loss on the contracts as measured by the difference between the forward foreign exchange rates at the dates of entry into the contracts and the forward rates at the reporting date, is recorded as a component of NAV. These instruments involve market risk, credit risk, or both kinds of risks, in excess of the amount recognized in the Statements of Assets and Liabilities. Risks arise from the possible inability of counterparties to meet the terms of their contracts and from movement in currency and securities values and interest rates. Due to the risks associated with these transactions, a fund could incur losses up to the entire contract amount, which may exceed the net unrealized value included in its NAV.

Distributions to Shareholders - Each Fund declares any dividends from net investment income and pays them annually. Any net capital gains and foreign currency gains realized by the Funds are distributed at least annually. Distributions to shareholders are recorded on the ex-dividend date. Distributions are based on amounts calculated in accordance with applicable federal income tax regulations, which may differ from GAAP. These differences are due primarily to differing treatments of income and gain on various investment securities held by each Fund, timing differences and differing characterizations of distributions made by each Fund.

Federal Taxes - Each Fund intends to continue to qualify each year as a regulated investment company under Subchapter M of Chapter 1, Subtitle A, of the Internal Revenue Code of 1986, as amended (“Code”), and to distribute all of their taxable income to shareholders. In addition, by distributing in each calendar year substantially all of their net investment income and capital gains, if any, the Funds will not be subject to a federal excise tax. Therefore, no federal income or excise tax provision is required. Each Fund will file a U.S. federal income and excise tax return as required. Each Fund’s federal income tax returns are subject to examination by the Internal Revenue Service for a period of three fiscal years after they are filed. As of February 28, 2018, there are no uncertain tax positions that would require financial statement recognition, de-recognition or disclosure.

In addition to the requirements of the Code, each Fund may also be subject to capital gains tax in Thailand on gains realized upon sale of Thai securities, payable upon repatriation of sales proceeds. Funds with exposure to Thai securities accrue a deferred liability for unrealized gains based on existing tax rates of the securities. As of February 28, 2018, the NWS International Property Fund recorded Thai capital gains tax in the amount of $6,646 which is included in the line item Net realized gain(loss) on investments and a deferred liability for potential future Thai capital gains taxes of $8,029.

REITs - Each Fund has made certain investments in real estate investment trusts (“REITs”) which pay dividends to their shareholders based upon funds available from operations. It is quite common for these dividends to exceed the REIT’s taxable earnings and profits

18

NWS FUNDS

NOTES TO FINANCIAL STATEMENTS

FEBRUARY 28, 2018

resulting in the excess portion of such dividends being designated as a return of capital. Each Fund may include the gross dividends from such REITs in income or may utilize estimates of any potential REIT dividend reclassifications in each Fund’s annual distributions to shareholders and, accordingly, a portion of each Fund’s distributions may be designated as a return of capital, require reclassification, or be under distributed on an excise basis and subject to excise tax.

Income and Expense Allocation - The Trust accounts separately for the assets, liabilities and operations of each of its investment portfolios. Expenses that are directly attributable to more than one investment portfolio are allocated among the respective investment portfolios in an equitable manner.

Offering Costs - Offering costs for the NWS Global Property Fund of $29,915 consisted of fees related to the mailing and printing of the initial prospectus, certain startup legal costs, and initial registration filings. Such costs are amortized over a twelve-month period beginning with the commencement of operations of the NWS Global Property Fund. During the year ended February 28, 2018, the NWS Global Property Fund expensed $22,436.

Redemption Fees - A shareholder who redeems or exchanges shares within 90 days of purchase will incur a redemption fee of 1.50% of the current NAV of shares redeemed or exchanged, subject to certain limitations. The fee is charged for the benefit of the remaining shareholders and will be paid to each Fund to help offset transaction costs. The fee is accounted for as an addition to paid-in capital. Each Fund reserves the right to modify the terms of or terminate the fee at any time. There are limited exceptions to the imposition of the redemption fee. Redemption fees incurred for the Funds, if any, are reflected on the Statements of Changes in Net Assets.

Commitments and Contingencies - In the normal course of business, each Fund enters into contracts that provide general indemnifications by each Fund to the counterparty to the contract. Each Fund’s maximum exposure under these arrangements is dependent on future claims that may be made against each Fund and, therefore, cannot be estimated; however, based on experience, the risk of loss from such claims is considered remote. Each Fund has determined that none of these arrangements requires disclosure on each Fund’s balance sheet.

Note 3. Cash - Concentration in Uninsured Account

For cash management purposes, each Fund may concentrate cash with each Fund’s custodian. This typically results in cash balances exceeding the Federal Deposit Insurance Corporation (“FDIC”) insurance limits. As of February 28, 2018, the NWS International Property Fund and NWS Global Property Fund had $60,255 and $1,666,605, respectively, as cash reserves at MUFG Union Bank, N.A. that exceeded the FDIC insurance limit.

Note 4. Fees and Expenses

Investment Adviser - Northwood Securities LLC (the “Adviser”) is the investment adviser to each Fund. Pursuant to an investment advisory agreement, the Adviser receives an advisory fee, payable monthly, from each Fund at an annual rate of 0.75% of each Fund’s average daily net assets.

Distribution - Foreside Fund Services, LLC serves as each Fund’s distributor (the “Distributor”). The Funds do not have a distribution (12b-1) plan; accordingly, the Distributor does not receive compensation from the Funds for its distribution services. The Adviser compensates the Distributor directly for its services. The Distributor is not affiliated with the Adviser or Atlantic Fund Administration, LLC (d/b/a Atlantic Fund Services) (“Atlantic”) or their affiliates.