As filed with the Securities and Exchange Commission on June 17, 2013

Registration No. 333-187164

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________

AMENDMENT NO. 8

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

_____________________

Truett-Hurst, Inc.

(Exact Name of Registrant as Specified in Its Charter)

|

Delaware

|

2080

|

46-1561499

|

|

(State or Other Jurisdiction of

Incorporation or Organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification Number)

|

|

5610 Dry Creek Road

Healdsburg, CA 95448

(707) 433-9545

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

|

|

Phillip L. Hurst

President and Chief Executive Officer

Truett-Hurst, Inc.

5610 Dry Creek Road

Healdsburg, CA 95448

(707) 433-9545

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

|

Copies to:

|

Anna T. Pinedo, Esq.

James R. Tanenbaum, Esq.

Morrison & Foerster LLP

1290 Avenue of the Americas

New York, New York 10104

Tel: (212) 468-8000

|

Michael A. Hedge, Esq.

Gary J. Kocher, Esq.

K&L Gates LLP

925 Fourth Avenue, Suite 2900

Seattle, Washington 98104

Tel: (206) 623-7580

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer o

|

Accelerated filer o

|

| Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company x |

_____________________

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of

Securities to be Registered

|

Amount to be

Registered (1) |

Proposed Maximum

Aggregate

Offering Price (2)

|

Amount of

Registration Fee

|

|

Class A Common Stock, par value $0.001 per share

|

2,700,000

|

$21,600,000

|

$5,939.00(3) |

|

(1)

|

This Registration Statement also covers the re-offer and sale of Class A common stock on an ongoing basis after their initial sale in market-making transactions by WRHambrecht + Co, LLC, an affiliate of the Registrant. All such market-making transactions with respect to these shares of Class A common stock are being made pursuant to this Registration Statement.

|

|

(2)

|

Estimated solely for the purposes of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

|

|

(3)

|

Previously estimated and paid based on the registration of 2,902,557 shares of Class A common stock.

|

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the Securities and Exchange Commission declares our registration statement effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JUNE 17, 2013.

|

Truett-Hurst, Inc.

2,700,000 Shares of

Class A Common Stock

|

||

|

This is our initial public offering and no public market currently exists for our shares. We are selling 2,700,000 shares of our Class A common stock. We expect that the initial public offering price will be between $6.00 and $8.00 per share. Immediately following this offering, our Class A common stock will collectively represent 100% of the economic interests in Truett-Hurst, Inc. and approximately 38.3% of the voting power of Truett-Hurst, Inc. Our Class B common stock will represent approximately 58.2% of the voting power of Truett-Hurst, Inc. Certain of our existing owners may purchase in this offering up to 7.0%, or 189,608 shares, of the Class A common stock to be outstanding following the offering in order to meet the all or none sales threshold of 2,700,000 shares.

Our Class A common stock has been approved for listing on the Nasdaq Capital Market under the symbol “THST.”

We are an “emerging growth company” as defined in the Jumpstart Our Business Startups Act and, as such, may elect to comply with certain reduced reporting requirements after this offering.

|

OpenIPO® and Best Efforts Offering: The method of distribution being used by the underwriters in this offering differs somewhat from that traditionally employed in underwritten public offerings. The public offering price and allocation of shares will be determined primarily by an auction process conducted by the underwriters participating in this offering. The underwriters have agreed to use their best efforts to procure potential purchasers for the shares of Class A common stock offered pursuant to this prospectus. The shares are being offered on an all or none basis. All investor funds received prior to the closing will be deposited into a non-interest bearing escrow account with an escrow agent until closing. If investor funds for the full amount of the offering are not received at closing, the offering will terminate and any funds received will be returned promptly.

The auction will close and a public offering price will be determined after the registration statement becomes effective. The auction will remain open no longer than 30 days following effectiveness. The minimum size of any bid is 100 shares.

A more detailed description of this process is included in “The OpenIPO Auction Process” beginning on page 25 and in “Plan of Distribution” beginning on page 113.

|

||

|

THE OFFERING

|

PER SHARE

|

TOTAL

|

|

|

Initial Public Offering Price

|

$

|

$

|

|

|

Placement Agents’ Fee

|

$

|

$

|

|

|

Proceeds to Truett-Hurst, Inc.

|

$

|

$

|

|

|

The underwriters expect to deliver the shares of Class A common stock on , 2013.

|

|||

|

Investing in our Class A common stock involves a high degree of risk. See “Risk Factors” beginning on page 12. |

|

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense. |

|

CSCA | Feltl and Company | Sidoti & Company, LLC |

The date of this prospectus is , 2013.

TABLE OF CONTENTS

|

Page

|

|

|

Prospectus Summary

|

1

|

|

Risk Factors

|

12

|

|

Special Note Regarding Forward-Looking Statements

|

24

|

|

Industry Data

|

24

|

|

The OpenIPO Auction Process

|

25

|

|

Use of Proceeds

|

34

|

|

Dividend Policy

|

35

|

|

Capitalization

|

36

|

|

Dilution

|

37

|

| Unaudited Pro Forma Consolidated Financial Information | 39 |

|

Selected Consolidated Financial Data

|

47

|

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

48

|

|

Business

|

61

|

|

History and Formation Transactions

|

80

|

|

Directors and Executive Officers

|

85

|

|

Executive Compensation

|

89

|

|

Certain Relationships and Related Party Transactions

|

92

|

|

Principal Stockholders

|

98

|

|

Description of Capital Stock

|

102

|

|

Shares Eligible for Future Sale

|

106

|

|

Material U.S. Federal Tax Consequences to Non-U.S. Holders

|

109

|

|

Plan of Distribution

|

113

|

|

Conflicts of Interest

|

115

|

|

Legal Matters

|

116

|

|

Experts

|

116

|

|

Where You Can Find Additional Information

|

116

|

|

Index to Consolidated Financial Statements

|

|

You should rely only on the information contained in this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document. Our business and financial condition may have changed since that date.

Neither we nor any of the underwriters have done anything that would permit a public offering of the shares of our Class A common stock or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of Class A common stock and the distribution of this prospectus outside of the United States.

i

Unless the context suggests otherwise, references in this prospectus to "Truett-Hurst," the "Company," "we," "us" and "our" refer (1) prior to the consummation of the offering transactions described under "History and Formation Transactions—Organizational Structure," to H.D.D. LLC and its consolidated subsidiaries and (2) after the offering transactions described under "History and Formation Transactions—Organizational Structure," to Truett-Hurst, Inc. and its consolidated subsidiaries. We refer to the owners of membership interests in H.D.D. LLC prior to the offering transactions, collectively, as our "existing owners."

ii

PROSPECTUS SUMMARY

This summary highlights the information contained elsewhere in this prospectus, and is qualified in its entirety by reference to the more detailed information and financial statements appearing elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information that may be important to you. Before investing in our Class A common stock, you should read this entire prospectus, including the information set forth under the heading “Risk Factors” and the financial statements and the notes thereto.

Truett-Hurst is an innovative and fast-growing Super-premium and Ultra-premium wine sales, marketing and production company based in the acclaimed Dry Creek and Russian River Valleys of Sonoma County, California. The core of our business is a combination of direct to consumer sales, traditional brand sales and “custom label” partnerships with major retailers, such as Trader Joe’s and Safeway. We work closely with our retail partners to develop tailored brands to be sold to the discovery-oriented wine consumer. We offer a top quality product at a reasonable price, a result of our competitive grape sourcing, high-quality wine making and world-class packaging and label design. Our “custom label” model allows us to own the brands that we create, which we believe differentiates us from the traditional private label model and allows us to potentially expand the brands into the broad market, further building brand equity. Our retail partners value their relationships with us because they collaborate in the development of the products and ultimately benefit from the higher margins that we offer them. We believe that we have attracted these partners as a result of our rapid brand development cycles, our ability to quickly adjust to market demand and because we can bypass many traditional distribution layers to offer higher margin products for our partners’ key target customers.

We have had a limited number of quarters or years of profitability and historically raised additional capital to meet our growth needs. We expect to make significant future investment in order to develop and expand our business and become a public company, which will result in additional sales, marketing and general and administrative expenses that will require increased sales to recover these additional costs.

Nielsen estimates that 22% of consumer products sold by food and drug retailers in the United States are private label. However, in the U.S. wine sector, only 3.7% of sales are made through private labels. Other more mature wine markets, such as the U.K. and Australia, have much higher penetration of private label wine sales (19% and 16%, respectively). Given the $33 billion market for wine sales in the United States, the private label business represents a market opportunity of many billions of dollars.

The California wine industry, which accounts for 90% of total U.S. wine production, is dominated by a few producers who make up the vast majority of sales. The top four wine producers in California control approximately 65% of unit shipments of California wine. Our business approach seeks to disrupt this oligopoly by providing high quality wine at a reasonable cost, in part by avoiding an expensive and competitive distribution system. Likewise, our large chain partners have turned to private label and custom label as a way to gain margin, customer loyalty and differentiation that allows them to compete with powerful producers and suppliers for this growing market.

In addition to our focus on our custom label business model, we also have business operations in the direct to consumer and traditional three-tier distribution channels. Our direct to consumer channel consists of sales through our tasting rooms and wine clubs, which serve as strong tools for increasing brand visibility and loyalty, and through our ownership interest in The Wine Spies, LLC (“The Wine Spies”), an internet wine retailer specializing in short-lived “flash” sales. Our more traditional three-tier distribution business consists of sales of our wine under four fully-owned labels, Truett-Hurst, VML, Healdsburg Ranches and Bradford Mountain, through a variety of distributor channels.

Market Opportunity

A combination of fundamental market changes in the United States created an opportunity for us, including:

|

|

·

|

Steady growth in the U.S. wine market: The U.S. wine market has grown at an average annual rate of 5% over the past decade and is now the largest in the world (although per capita consumption remains relatively low). In the recent past, growth in wine sales has been focused in domestic brands; from 2007 to 2011, wine imports have only grown by 1.6% per year. According to the 2011 Gomberg-Fredrikson & Associates Annual Wine Industry Review for the twelve months ended December 2011, two of the three fastest growing price points are the $7-$14 (“Super-premium”) and over-$14 (“Ultra-premium”) segments. We have focused on the higher end of the Super-premium segment and also have a significant presence in the Ultra-premium segment, which together accounted for 66% of industry-wide revenue in 2011.

|

1

|

|

·

|

Market ripe for disruption: Food retailers account for roughly 65% of wine sales, with a high concentration of market share among only a handful of major wine producers and distributors. The top four wine producers in California control approximately 65% of unit shipments of California wine. In order to compete with powerful producers and suppliers for this growing profit pool, food and grocery retailers have turned to private label programs as a way of gaining margin, customer loyalty, category growth and differentiation.

|

|

|

·

|

Retailer focus on innovation: Increased market competition has heightened for retailers the emphasis on increasing consumer traffic to grow same store sales year over year. In order to create excitement in their stores, major global retail chains and top wine retailers in the United States have made wine and packaging innovations, including “earth-friendly” elements, a key strategic initiative for 2013 and beyond. Our core values are aligned with our retail partners’ initiatives and consumer consciousness as we strive to make our products in a way that minimizes waste and fossil fuel usage and increases recyclability.

|

|

|

·

|

Private label model remains in its infancy: Nielsen estimates that, in the United States, only 3.7% of wines, by dollar value, were sold through private labels in the year to date, as of August 2010, which was a 20% increase compared to the prior year. Other mature wine markets have experienced considerably higher penetration; for example, private label wine sales make up 19% and 16% of total wine sales in the U.K. and Australia, respectively. The U.S. market appears poised for growth in this segment.

|

|

|

·

|

Declining brand loyalty: Along with robust growth, the U.S. wine market has also witnessed a proliferation of new brands. In 2010 alone, the United States approved 120,000 new wine labels. Consumers have shown an increasing appetite to sample new labels and varietals, which can be promoted cost-effectively on an in-store basis. For example, relatively new brands like Cupcake, Ménage à Trois and E.&J. Gallo Winery’s Apothic grew by 55%, 18% and 258%, respectively, in 2011. Food retailers are well-positioned to manage this promotion as they control the shelf space and brand positioning in their stores. In an ever more crowded market, this advantage has become increasingly valuable.

|

|

|

·

|

Rapid growth of internet retailing: Small but rapidly growing, we expect the internet segment to continue to outpace brick and mortar retailer sales, and we believe it is poised to surpass winery direct sales.

|

|

|

·

|

“Premiumization” of the market: Following years of explosive growth in the late 1980s and early 1990s, the U.S. market experienced a supply glut which resulted in severe pricing pressure from so-called “value brands.” Due to significant consumption growth of California wines and the reduction of imported wines, as well as changes in exchange rates and taste preferences, this trend has reversed in the current cycle, with the Super-premium and Ultra-premium segments among those experiencing the highest growth.

|

|

|

·

|

Significant direct to consumer sales growth: Tasting room and wine club sales are typically the highest gross margin sales for a winery. Our direct to consumer net sales increased 54% for the fiscal year ended June 30, 2012 as compared to the prior fiscal year and 52% for the nine months ended March 31, 2013 as compared to the prior-year period, with gross margins averaging approximately 60%, which we believe is generally consistent with industry averages.

|

2

Our Strategy

Recognizing the opportunity created by these trends, our founders developed a strategy focused on the following key elements:

|

|

·

|

Model scalability will drive growth: We combine the best of deep experience in the wine industry and the speed and agility of a start-up to work with both retailers and distributors to develop and market new brands. Because we are smaller, more agile and less prone to layers of decision making and because we have a world-class brand development/creative team in house, we are able to launch innovative new brands faster and more cost-effectively. This allows us and our partners to respond rapidly to market opportunities.

|

|

|

·

|

Highly collaborative channel partnerships: Our management believes that it is critical to support multiple players in the distribution system in order for a young company to defend a sustainable market position. This includes a strong collaboration with well-known and reputable retailers who are looking for innovative, higher-margin brands to market. Our reputation has been enhanced by our success with these channel partners, leading to new opportunities in brand development, including selling some of our brands via traditional three-tier distribution at a reduced cost.

|

Currently, we have a small share of this sizeable market. For example, for the first nine months of fiscal year 2013, our sales to Safeway were less than $5.0 million, which is less than 1% of Safeway’s 2012 annual wine sales. Our goal is to expand our sales with our existing retailer partners, including large businesses such as Trader Joe’s, Safeway and Total Wine & More, as well as increase the number of new major retailers that we partner with, including The Kroger Company, Publix and Wal-Mart.

|

|

·

|

Collaborative and rapid brand development: Our development process with our partners is highly collaborative and our products are developed based on our partners’ market data and understanding of what their customers want. Instead of developing a brand and bringing it to market based on consultants’ input and wine maker reputation, we exploit our retail partners’ quantitative data about brands, price points, packaging and varietals that its customers are buying. When we initiate a partnership, we approach a retailer with numerous concepts; an agreement to move forward typically includes multiple brands, varietals and price points that are launched in tandem. This allows the retailer to test various concepts, with the expectation that about half of the brands will be successful and further developed, while the other half will be scaled back or discontinued. Typically, it takes six months from the initial conversations with a retailer until the product is on their shelves.

|

|

|

·

|

Quality focused on the robust premium sector: The private label business has historically focused on the generic, Sub-premium category (below $7 per bottle retail price), with wine quality consistent with the price points. However, recognizing the opportunity for growth, we have positioned ourselves in the Super-premium and Ultra-premium segments. In order to support our premium strategy, we have identified and contracted premium grape sources from Paso Robles, Sonoma and Mendocino Counties. Our founders’ diverse and extensive experience in the industry allows us to leverage longstanding relationships with California growers, an increasingly important asset as grape supplies tighten globally. We are also able to source grapes on a priority basis from our founders and members of our management team, who collectively control 500 acres of vineyards in Sonoma and Mendocino Counties. In addition, we have hired a top-quality winemaking staff and invested in state of the art systems and equipment.

|

While we have focused primarily on the higher end of the Super-premium segment, we also have a significant presence in the Ultra-premium segment of the industry.

3

|

|

·

|

Innovative packaging and label design: Given the proliferation of brands and the need to “rise above the noise” in wine displays, innovative labeling and packaging is increasingly important to success in launching new wine brands. Our founders and Kevin Shaw, an independent contractor who serves as our creative director, have world-class experience in this area and are establishing a reputation as market leaders with novel packaging, such as evocative paper-wrapping, unique bottle shapes and the world’s first paper-based bottles.

|

|

|

o

|

Evocative wine wraps: We have developed, produced and sold one of the world’s first “wine wrap” packaging concepts to Safeway, one of the country’s largest wine retailers. We have applied for trademarks on the wine wrap brands and a patent on the unique packaging.

|

|

|

o

|

The world’s first paper bottle: In 2013, we entered into a seven-year exclusive agreement with the producer of what we believe to be the first ever paper wine bottle. We intend to begin selling wine in the paper bottle in the first quarter of fiscal year 2014 and are in discussions with several of the top U.S. retailers and distributors, including Safeway, The Kroger Company and Southern Wine & Spirits, to sell the product.

|

|

|

o

|

Proprietary square bottle: We have designed a unique square-shaped glass bottle and created a brand that will “own” this concept. We have applied for a trademark on the brand and a patent on the design. Five of the top U.S. wine retailers are vying for the product, and we anticipate establishing a partnership for launch in spring 2013. We have partnered with one of the country’s fastest growing and most important wine retail chains, Total Wine & More, to produce and sell 40,000 cases (generating approximately $3.5 million in sales) in fiscal year 2014.

|

|

|

·

|

Management team and key personnel: The founding team of Phil Hurst and Paul Dolan represents decades of experience in the wine industry and success at building businesses to scale, typically only seen in much larger, global players in the wine and spirits industry.

|

|

|

o

|

Phillip L. Hurst, Co-Founder, President and Chief Executive Officer: co-founded and helped build Winery Exchange Inc. into a global private label beer, spirits and wine company with more than $100 million in sales.

|

|

|

o

|

Paul E. Dolan, III, Co-Founder: worked at Fetzer Vineyards for 27 years, initially as wine maker and later as President, and scaled the business from 30,000 cases to over 4 million cases sold per year.

|

|

|

o

|

Virginia Marie Lambrix, Director of Winemaking: experience making wine for such leading producers as De Loach Vineyards, La Follette and Hendry Ranch.

|

|

|

o

|

Heath E. Dolan, Co-Founder, Director of Vineyard Operations: has 16 years of experience in the wine business, including managing cellar operations for Fetzer Vineyards.

|

|

|

o

|

Kevin Shaw, Independent Contractor/Creative Director: has nearly 20 years of experience as a designer. As proprietor and founder of Stranger and Stranger design agency, he received the 2012 Harpers Wine & Spirits Magazine Design Award for “Best Design Agency.” Kevin designs over 100 beverage brands every year in markets all around the world, including Jack Daniels, Avion Tequila, Lillet and The Kraken Spiced Rum. Collectively, his brands sell over a billion bottles a year.

|

|

|

o

|

James D. Bielenberg, Chief Financial Officer: has more than 30 years of public and private accounting experience. After gaining public accounting experience with Arthur Young (now Ernst & Young), he has spent the last 25 years working in wine-making operations with such well known firms as Kendall-Jackson Wine Estates, Francis Ford Coppola Winery, Ascentia Wine Estates, LLC and Rodney Strong Vineyards.

|

4

|

|

o

|

Daniel A. Carroll, Director: retired partner of TPG Capital, where he was a founder of the firm's Asian operations (formerly Newbridge Capital). Prior to 1995, he spent nine years with Hambrecht & Quist Group.

|

|

|

o

|

William R. Hambrecht, Director: after selling Hambrecht & Quist Group in 1998, Bill founded WR Hambrecht + Co, LLC (“WR Hambrecht + Co”) where he is now Chairman and Co-CEO. He has been actively involved in the wine business for 40 years as an owner and operator of vineyards and wineries.

|

Our Structure

The net proceeds from this offering will be used by Truett-Hurst, Inc. to purchase 2,700,000 newly-issued LLC units (“LLC Units”) from H.D.D. LLC (the “LLC”) at a purchase price per unit equal to the initial public offering price per share of Class A common stock in this offering, as described under "History and Formation Transactions—Organizational Structure—Offering Transactions." The LLC will use these proceeds to pay down amounts owed on our credit facility, for working capital, capital expenditures, hiring additional personnel, and other general corporate purposes, as further described under “Use of Proceeds.” After the offering, Truett-Hurst, Inc. will hold 2,700,000 LLC Units, representing a 39.7% equity interest in the LLC. Truett-Hurst, Inc. will not purchase for cash in this offering any LLC Units held by members of the LLC.

Truett-Hurst, Inc. is a Delaware corporation formed to serve as a holding company that will hold an interest in the LLC. Truett-Hurst, Inc. has not engaged in any business or other activities other than in connection with its formation. The current board of directors of Truett-Hurst, Inc. is made up of six members of the LLC, as well as two individuals meeting the criteria for independence under the rules of the Nasdaq Capital Market (“Nasdaq”) and the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These LLC members will remain controlling holders of Truett-Hurst, Inc. following the offering. See “Directors and Executive Officers.” Following this offering, Truett-Hurst, Inc. will remain a holding company and its sole asset will be this equity interest in the LLC. Truett-Hurst, Inc. will become the sole managing member of the LLC, will operate and control all of its business and affairs and consolidate its financial results. The limited liability company agreement of the LLC will be amended and restated to, among other things, modify its capital structure by replacing the different classes of interests currently held by our existing owners with a single new class of LLC Units and to provide that the conduct, control and management of the LLC shall be vested exclusively in Truett-Hurst, Inc., as sole managing member. The other members of the LLC will not have the right to remove the sole managing member for any reason.

We and our existing owners will also enter into an exchange agreement under which (subject to the terms of the exchange agreement) they will have the right to exchange their LLC Units for shares of our Class A common stock on a one-for-one basis, subject to customary conversion rate adjustments for stock splits, stock dividends and reclassifications, or for cash, at our election. See "Certain Relationships and Related Party Transactions— Exchange Agreement."

In connection with the offering, one share of Class B common stock of Truett-Hurst, Inc. will be distributed to each existing holder of LLC Units, each of which provides its owner with no economic rights but entitles the holder, without regard to the number of shares of Class B common stock held by such holder, to one vote on matters presented to stockholders of Truett-Hurst, Inc. for each LLC Unit held by such holder, as described in "Description of Capital Stock—Common Stock—Voting Rights." Holders of our Class A common stock and Class B common stock vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law.

Immediately following this offering and the application of net proceeds from this offering, our existing owners will control approximately 62.6% of the combined voting power of our outstanding Class A and Class B common stock. Accordingly, our existing owners will have the ability to elect all of the members of our board of directors, and thereby to control our management and affairs.

As a result of these transactions:

|

|

·

|

The investors in this offering will collectively own 2,700,000 shares of our Class A common stock and Truett-Hurst, Inc. will hold 2,700,000 LLC Units;

|

|

|

·

|

Our existing owners will hold 4,102,644 LLC Units;

|

|

|

·

|

Our Class A common stock will collectively represent approximately 38.3% of the voting power in Truett-Hurst, Inc.;

|

|

|

·

|

Our Class B common stock will collectively represent approximately 58.2% of the voting power in Truett-Hurst, Inc.; and

|

|

|

·

|

Truett-Hurst, Inc. will own approximately 39.7% of the economic interest in the LLC and will exercise exclusive control over the LLC, as its sole managing member.

|

In addition, James D. Bielenberg, our Chief Financial Officer, holds 42,000 shares of restricted Class A common stock and Kevin Shaw, an independent contractor who acts as our creative director, holds 210,000 shares of restricted Class A common stock. These shares of restricted Class A common stock were granted in December 2012 and February 2013, respectively, and vest over a three-year period. Mr. Bielenberg and Mr. Shaw are entitled to vote these shares prior to vesting. In the aggregate, these shares will represent approximately 3.6% of the voting power of the Class A common stock outstanding after the offering.

5

The diagram below depicts our organizational structure immediately following this offering:

The voting power of the Class A holders shown in the above diagram includes up to an aggregate 189,608 shares of our Class A common stock to be purchased by certain of our existing owners and a third party in this offering. These shares of our Class A common stock will be purchased for investment purposes, and not with a view to a distribution or resale, and will be purchased at the clearing price established through the OpenIPO process. See “The OpenIPO Auction Process.” In order to avoid having these potential purchases influence the auction outcome, the existing owners and the third party will not submit their indications through the OpenIPO website, but will agree to purchase at the clearing price set through the auction process.

In connection with the offering, Truett-Hurst, Inc. will enter into a tax receivable agreement with our existing owners that provides for the payment from time to time by Truett-Hurst, Inc. to our existing owners of 90% of the amount of the benefits, if any, that Truett-Hurst, Inc. is deemed to realize as a result of (i) increases in tax basis resulting from our exchange of LLC Units and (ii) certain other tax benefits related to our entering into the tax receivable agreement, including tax benefits attributable to payments under the tax receivable agreement. The actual increase in tax basis, as well as the amount and timing of any payments under the tax receivable agreement, will vary depending upon a number of factors, including the timing of exchanges, the price of shares of our Class A common stock at the time of the exchange, the extent to which such exchanges are taxable, and the amount and timing of our income. A chart estimating the amounts of such payments appears on page 93 of this prospectus. See “Certain Relationships and Related Party Transactions—Tax Receivable Agreement.”

The LLC’s fiscal year-end is currently December 31, while the fiscal year-end of Truett-Hurst, Inc. is June 30. For purposes of comparability, we have presented audited financial statements of the LLC as of June 30, 2011 and 2012 and for each of the years in the two-year period ended June 30, 2012 so that these will be comparable with the audited consolidated financial statements of Truett-Hurst, Inc. upon completion of this offering. The LLC will amend its operating agreement to change its fiscal year end to June 30 after the offering.

Recent Developments

Financial results for periods subsequent to March 31, 2013 are not currently available. However, we expect to report between $4.0 million and $4.9 million in net sales for the three months ending June 30, 2013, compared to net sales of $2.3 million for the three months ended June 30, 2012. In addition, we expect to report between $16.1 million and $17.0 million in net sales for the fiscal year ending June 30, 2013, compared to net sales of $12.7 million for the fiscal year ended June 30, 2012. Based on the high end of the range above, for the fourth quarter and fiscal year ending June 30, 2013, these amounts would represent increases of $2.6 million and $4.3 million, respectively, versus the prior periods. Anticipated increases in net sales compared to the prior periods are consistent with the Company’s rate of growth to date, but reflect the relatively small base of sales in prior periods used for comparison. Therefore, investors should not attribute undue significance to the growth in sales discussed above, as there can be no assurance that the Company will continue to grow at these rates, or that its final results will be consistent with these estimates.

The anticipated increase in net sales for the three months and fiscal year ending June 30, 2013 is attributable to the introduction of new brands, additional distributors, increased market penetration in the wholesale and direct sales segments, and increased net sales from the acquisition of a fifty percent interest in The Wine Spies LLC. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

We recognize revenue when our products are shipped. Our current estimates of net sales for the three months ending June 30, 2013 are based on (i) actual shipments to date, (ii) open sales orders with shipment dates prior to quarter-end, and (iii) anticipated sales orders (and the shipment dates of those orders) based on discussions with our distributors. Actual net sales for the period will be subject to the actual shipment schedules of our products, which are determined by our distributors and customers. No additional material assumptions were used to calculate the projected net sales for the periods described above.

We expect to report between $115,000 in net loss attributable to H.D.D. LLC members and $145,000 in net income attributable to H.D.D. LLC members for the three months ending June 30, 2013, compared to a net loss attributable to H.D.D. LLC members of $224,000 for the three months ended June 30, 2012. In addition, we expect to report between $595,000 and $335,000 in net loss attributable to H.D.D. LLC members for the fiscal year ending June 30, 2013 compared to net income attributable to H.D.D. LLC members of $26,462 for the fiscal year ended June 30, 2012.

The minimum and maximum net income (loss) spread approximates $260,000, which we believe is reasonable based on the following information known to us: (i) net sales methodology described above, less (ii) actual related cost of sales, (iii) actual sales and marketing, general and administrative expenses and one-time expenses related to the Offering Transactions, and (iv) projected one-time expenses related to the Offering Transactions for the defined periods. Projected one-time expenses related to the offering were determined through discussions with certain service providers involved with the offering.

Any material fluctuations in the net income (loss) range is subject to actual shipments, related cost of sales for shipments and related shipping and sales and marketing expenses for the defined periods. Actual revenue recognized and associated expenses incurred vary based upon sales orders, sales mix and related shipping dates placed by our customers. No additional material assumptions were used to calculate the projected net income (loss) for the defined periods.

After giving effect to the Recapitalization and the Offering Transactions, we expect to have 7,054,644 shares of Class A common stock outstanding (assumes the exchange of all LLC Units for shares of Class A common stock). We expect to report, on a weighted average basis, between $0.02 in losses per share and $0.02 in earnings per share on an estimated $115,000 in net loss attributable to H.D.D. LLC members and $145,000 in net income attributable to H.D.D. LLC members for the three months ending June 30, 2013, respectively. In addition, we expect to report, on a weighted average basis, between $0.08 and $0.05 in losses per share on an estimated $595,000 and $335,000 in net loss attributable to H.D.D. LLC members for the fiscal year ending June 30, 2013, respectively. No additional material assumptions were used to calculate the earnings or loss from continuing operations per share for the defined periods.

For the three months and fiscal year ended June 30, 2012, respectively, net income (loss) attributable to H.D.D. LLC members totaled approximately $(224,000) and $26,000, respectively. We estimate for the fourth quarter and fiscal year ending June 30, 2013, the high end of the range of net loss attributable to H.D.D. LLC members will be approximately $115,000 and $595,000, respectively. The anticipated change from profitability to a loss as compared to the previous periods is due primarily to one-time expenses associated with the Offering Transactions and increased personnel costs in preparation for becoming a publicly held company. For additional information regarding operating expenses and period changes see “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The ranges provided for the defined periods are, in management’s estimation, the most probable for the financial items presented based on the methodologies applied. These are only estimated results and investors should not attribute undue certainty to them. Our actual results depend on many factors, and may differ from these estimates. In addition we face risks that may adversely impact our business and results of operations. See “Risk Factors.”

The foregoing represents our estimates as of the date of this prospectus. We do not intend to furnish investors with any updated projections after the date hereof.

Summary of Risk Factors

Our business is subject to numerous risks, which are described in the section entitled “Risk Factors” immediately following this prospectus summary on page 12. You should carefully consider these risks before making an investment. In particular, the following considerations, among others, may offset our competitive strengths or have a negative effect on our growth strategy, which could cause a decline in the price of our Class A common stock and result in a loss of all or a portion of your investment:

|

|

·

|

A reduction in the supply of grapes and bulk wine available to us from the independent grape growers and bulk wine suppliers could reduce our annual production of wine.

|

|

|

·

|

We face significant competition which could adversely affect our profitability.

|

|

|

·

|

The estimates of our financial performance for the three months and fiscal year ending June 30, 2013 contained in this prospectus are subject to inherent risks.

|

|

|

·

|

Because a significant amount of our business is made through our direct to retailer partnerships, any change in our relationships with them could harm our business.

|

|

|

·

|

We have a history of losses and we may not achieve or maintain profitability in the future.

|

|

|

·

|

The loss of Mr. Hurst, Mr. Bielenberg, Ms. Lambrix, Mr. Dolan or other key employees would damage our reputation and business.

|

|

|

·

|

A reduction in our access to, or an increase in the cost of, the third-party services we use to produce our wine could harm our business.

|

|

|

·

|

The terms of our credit facility may restrict our current and future operations; we have breached our existing loan covenants under the terms of this facility.

|

|

|

·

|

Because our existing owners will retain significant control over Truett-Hurst after this offering, new investors will not have as much influence on corporate decisions as they would if control were less concentrated.

|

|

|

·

|

Many of our transactions are with related parties, including our founders, executive officers, principal stockholders and other related parties, and present conflicts of interest.

|

|

|

·

|

Several of our executive officers and key team members have outside business interests which may create conflicts of interest.

|

6

|

|

·

|

We depend upon our trademarks and proprietary rights, and any failure to protect our intellectual property rights or any claims that we are infringing upon the rights of others may adversely affect our competitive position and brand equity.

|

|

|

·

|

We are controlled by our existing owners, whose interests may differ from those of our public stockholders.

|

|

|

·

|

We are a “controlled company” within the meaning of the corporate governance standards of Nasdaq and, as a result, expect to qualify for, and rely on, exemptions from certain corporate governance requirements.

|

Emerging Growth Company Status

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act, enacted on April 5, 2012 (“JOBS Act”). For as long as we are an “emerging growth company,” we may take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies,” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404(b) of the Sarbanes-Oxley Act, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding stockholder advisory “say-on-pay” votes on executive compensation and stockholder advisory votes on golden parachute compensation.

Under the JOBS Act, we will remain an “emerging growth company” until the earliest of:

|

|

·

|

the last day of the fiscal year during which we have total annual gross revenues of $1 billion or more;

|

|

|

·

|

the last day of the fiscal year following the fifth anniversary of the completion of this offering;

|

|

|

·

|

the date on which we have, during the previous three-year period, issued more than $1 billion in non-convertible debt; and

|

|

|

·

|

the date on which we are deemed to be a “large accelerated filer” under the Exchange Act (we will qualify as a large accelerated filer as of the first day of the first fiscal year after we have (i) more than $700 million in outstanding common equity held by our non-affiliates and (ii) been public for at least 12 months; the value of our outstanding common equity will be measured each year on the last day of our second fiscal quarter).

|

The JOBS Act also provides that an “emerging growth company” can utilize the extended transition period provided in Section 7(a)(2)(B) of the Securities Act of 1933, as amended (the “Securities Act”) for complying with new or revised accounting standards. However, we are choosing to “opt out” of such extended transition period, and, as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for companies that are not “emerging growth companies.” Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Corporate Information

We were originally formed as a limited liability company in the State of California in 2007. Following this offering, Truett-Hurst, Inc. will be a holding company, and its sole asset will be its equity interest in the LLC. Our principal executive offices are located at 5610 Dry Creek Road, Healdsburg, California 95448. Our telephone number is (707) 433-9545. Our website address is www.truetthurst.com. The reference to our website is an inactive textual reference only, the information that can be accessed through our website is not part of this prospectus, and investors should not rely on any such information in deciding whether to purchase our Class A common stock.

7

Trade Names

We sell our products under a number of trademarks that we own. As of June 17, 2013, we had 21 registered, 16 published and six pending material U.S. trademarks.

8

THE OFFERING

|

Class A common stock offered

by us

|

2,700,000 shares.

|

|

Class A common stock to be

outstanding after the offering

|

2,700,000 shares (or 6,802,644 shares if all outstanding LLC Units held by our existing owners were exchanged for newly-issued shares of Class A common stock on a one-for-one basis).

|

|

Class B common stock

outstanding after the offering

|

Ten shares, or one share for every holder of LLC Units.

|

|

Price per share

|

$

|

|

Use of proceeds

|

We intend to use the net proceeds from this offering to purchase LLC Units from the LLC, and we will cause the LLC to use these proceeds to pay down amounts owed on our credit facility and for working capital, capital expenditures, hiring additional personnel and other general corporate purposes. See “Use of Proceeds.”

|

|

Voting rights

|

Each share of our Class A common stock, including any share of restricted Class A common stock granted pursuant to the 2012 Stock Incentive Plan (the “2012 Plan”), entitles its holder to one vote on all matters to be voted on by stockholders generally.

After the offering, each existing owner of the LLC will hold one share of Class B common stock. The shares of Class B common stock have no economic rights but entitle the holder, without regard to the number of shares of Class B common stock held, to a number of votes on matters presented to stockholders of Truett-Hurst, Inc. that is equal to the aggregate number of LLC Units held by such holder. See "Description of Capital Stock—Common Stock—Voting Rights."

Holders of our Class A common stock and Class B common stock vote together as a single class on all matters presented to our stockholders for their vote or approval, except as otherwise required by applicable law.

|

|

Exchange rights of holders of

LLC Units

|

Prior to the closing of this offering, we will enter into an exchange agreement with our existing owners so that they may (subject to the terms of the exchange agreement) exchange their LLC Units for shares of Class A common stock of Truett-Hurst, Inc. on a one-for-one basis, subject to customary conversion rate adjustments for stock splits, stock dividends and reclassifications, or for cash, at our election.

|

9

|

Underwriters

|

WR Hambrecht + Co

CSCA Capital Advisors, LLC

Feltl and Company, Inc.

Sidoti & Company, LLC

|

|

Risk Factors

|

Investing in our Class A common stock involves a high degree of risk. Before buying any shares, you should read the discussion of material risks of investing in our Class A common stock in “Risk factors” beginning on page 12.

|

|

Conflicts of Interest

|

William R. Hambrecht and Barrie Graham each serve as an officer, and Mr. Hambrecht serves as a director, of WR Hambrecht + Co, an underwriter in this offering. Both Mr. Hambrecht and Mr. Graham serve on our board of directors and have the power to influence or cause the direction of our management and policies. Additionally, Hambrecht Wine Group, L.P., which is approximately 83.7% beneficially owned by a trust for the benefit of Mr. Hambrecht and his family members and as to which Mr. Hambrecht is a trustee, owns 12.94% of the combined voting power of our Class A and Class B common stock prior to this offering and will own 7.99% of the combined voting power of our Class A and Class B common stock after this offering. Mr. Hambrecht is deemed to beneficially own all of the equity interest held by Hambrecht Wine Group, L.P. Because of the foregoing, WR Hambrecht + Co is deemed to have a “conflict of interest” under Rule 5121 of the Financial Industry Regulatory Authority, Inc. (“FINRA”). Accordingly, this offering will be made in compliance with the applicable provisions of Rule 5121. Rule 5121 requires that a “qualified independent underwriter” meeting certain standards participate in the preparation of the registration statement and prospectus and exercise the usual standards of due diligence with respect thereto. CSCA Capital Advisors, LLC has agreed to act as a “qualified independent underwriter” within the meaning of Rule 5121 in connection with this offering. WR Hambrecht + Co will not confirm sales of the shares to any account over which it exercises discretionary authority without the prior written approval of the customer.

|

|

Nasdaq Symbol

|

THST

|

In this prospectus, unless otherwise indicated, the number of shares of Class A common stock outstanding and the other information based thereon reflects a 1-for-14 stock split effected on April 18, 2013 and does not reflect:

|

|

·

|

4,102,644 shares of Class A common stock issuable upon exchange of 4,102,644 LLC Units;

|

|

|

·

|

42,000 shares of restricted Class A common stock granted to James D. Bielenberg, our Chief Financial Officer, and 210,000 shares of restricted Class A common stock granted to Kevin Shaw, an independent contractor who acts as our creative director, in each case pursuant to the 2012 Plan; these shares of restricted Class A common stock were granted in December 2012 and February 2013, respectively, and vest over a three-year period; and

|

|

|

·

|

shares available for grant under the automatic increase provisions of the 2012 Plan (see “Executive Compensation—Employee Benefit and Stock Plans—2012 Stock Incentive Plan”).

|

10

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL INFORMATION

The following summary historical consolidated financial and other data of the LLC should be read together with “History and Formation Transactions—Organizational Structure,” “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our Financial Statements and related notes, all included elsewhere in this prospectus.

We have derived the consolidated statement of operations data for the fiscal years ended June 30, 2011 and 2012 and our consolidated balance sheet data as of June 30, 2011 and 2012 from our audited consolidated financial statements and related notes included elsewhere in this prospectus. We derived the consolidated statement of operations data for the nine months ended March 31, 2012 and 2013 and our consolidated balance sheet data as of March 31, 2013 from our unaudited consolidated financial statements included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future.

Consolidated Statement of Operations Data:

|

Fiscal Year Ended

|

Nine Months Ended

|

|||||||||||||||

|

|

June 30,

|

March 31,

|

||||||||||||||

|

2011

|

2012

|

2012

|

2013

|

|||||||||||||

| (unaudited) | ||||||||||||||||

|

Net sales

|

$ | 5,402,045 | $ | 12,693,395 | $ |

10,345,052

|

$ |

12,144,144

|

||||||||

|

Cost of sales

|

3,900,942 | 9,618,065 |

7,943,664

|

8,092,552

|

||||||||||||

|

Gross profit

|

1,501,103 | 3,075,330 |

2,401,388

|

4,051,592

|

||||||||||||

|

Operating expenses:

|

||||||||||||||||

|

Sales and marketing

|

595,226 | 1,387,321 |

1,069,654

|

1,956,193

|

||||||||||||

|

Gain on sale of assets

|

(111,150 | ) | (6,945 | ) | (465 | ) | - | |||||||||

|

General and administrative

|

1,435,908 | 1,194,353 |

745,878

|

2,347,136

|

||||||||||||

|

Total operating expenses

|

1,919,984 | 2,574,729 |

1,815,067

|

4,303,329

|

||||||||||||

|

Income (loss) from operations

|

(418,881 | ) | 500,601 |

586,321

|

(251,737

|

) | ||||||||||

|

Other income (expense):

|

||||||||||||||||

|

Interest expense

|

(401,134 | ) | (463,339 | ) |

(334,961

|

) |

(253,368

|

) | ||||||||

|

Warrant re-valuation

|

- | (10,000 | ) | - |

-

|

|||||||||||

|

Gain on exercise of warrant

|

- | - | - | 10,000 | ||||||||||||

|

Unrealized loss on interest rate swap

|

- | - | - | (28,500 | ) | |||||||||||

|

Gain on foreign currency

|

- | - | - | 1,802 | ||||||||||||

|

Total other expense

|

(401,134 | ) | (473,339 | ) |

(334,961

|

) |

(270,066

|

) | ||||||||

|

Income (loss) before provision for

income taxes |

(820,015 | ) | 27,262 |

251,360

|

(521,803

|

) | ||||||||||

|

Provision for income taxes

|

800 | 800 |

800

|

1,600

|

||||||||||||

|

Net income (loss) before

noncontrolling interest |

(820,815 | ) | 26,462 |

250,560

|

(523,403

|

) | ||||||||||

|

Loss attributable to noncontrolling

interest |

- | - | - |

(43,540

|

) | |||||||||||

|

Net income (loss) attributable to

H.D.D. LLC members |

$ | (820,815 | ) | $ | 26,462 | $ |

250,560

|

$ |

(479,863

|

) | ||||||

|

Consolidated Balance

|

At June 30,

|

At March 31,

|

||||||||||

|

Sheet Data:

|

2011

|

2012

|

2013 | |||||||||

|

(unaudited)

|

||||||||||||

|

Cash and cash equivalents

|

$ | 274,422 | $ | 167,309 | $ |

170,680

|

||||||

|

Total assets

|

10,099,873 | 14,082,617 |

21,244,784

|

|||||||||

|

Total liabilities

|

7,394,347 | 8,823,364 |

15,397,662

|

|||||||||

|

Total members’ equity (deficit)

|

(3,540,625 | ) | (626,898 | ) |

5,565,703

|

|||||||

11

RISK FACTORS

Investing in our Class A common stock involves a high degree of risk. You should carefully consider the following risk factors, as well as other information in this prospectus, before deciding whether to invest in shares of our Class A common stock. The occurrence of any of the events described below could harm our business, financial condition, results of operations and growth prospects. In such an event, the trading price of our Class A common stock may decline and you may lose all or part of your investment.

Risks Related to our Business and Strategy

A reduction in the supply of grapes and bulk wine available to us from the independent grape growers and bulk wine suppliers could reduce our annual production of wine.

We rely on annual contracts with over 20 independent growers to purchase substantially all of the grapes used in our wine production. Our business would be harmed if we are unable to contract for the purchase of grapes at acceptable prices from these or other suppliers in the future. The terms of many of our purchase agreements also constrain our ability to discontinue purchasing grapes in circumstances where we might want to do so.

Some of these agreements provide that either party may terminate the agreement prior to the beginning of each harvest year.

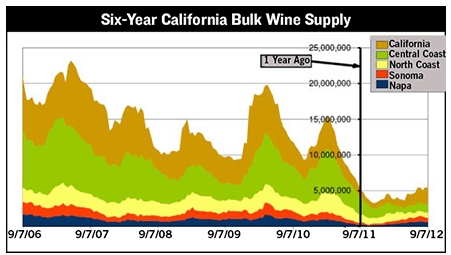

We depend on bulk wine suppliers for the production of several of our wines, particularly our direct to retailer designated labels. We have contracts with some wineries to provide us with bulk wine for a four-year term at specified prices and terms. These contracts will provide us with limited growth opportunities for the next two years. Further growth beyond our grape and wine contracts depends on the availability of bulk wine at the right price and quality for our labels.

The price, quality and available quantity of bulk wine has fluctuated in the past. It is possible that we will not be able to purchase bulk wine of acceptable quality at acceptable prices and quantities in the future, which could increase the cost or reduce the amount of wine we produce for sale. This could reduce our sales and profits.

In fiscal year 2012, E&J Gallo Winery and Robert Hall Winery were our largest suppliers of bulk wine. It is possible that we will not be able to source wine from these or comparable suppliers in the future, which could reduce our annual production of wine and harm our sales and profits.

We have a history of losses, and we may not achieve or maintain profitability in the future.

We have had a limited number of quarters or years of profitability and historically raised additional capital to meet our growth needs. We expect to make significant future investment in order to develop and expand our business and become a public company, which will result in additional sales, marketing and general and administrative expenses that will require increased sales to recover these additional costs. In addition, as we prepare to become a public company, we have incurred and expect that we will continue to incur significant legal, accounting, and other administrative expenses that we did not incur as a private company. As a result of our sales and marketing expenses as well as these increased expenditures, we must generate and sustain increased revenue to achieve and maintain future profitability. While our revenue has grown in recent periods, this growth may not be sustainable. In the event that we do not complete this offering, we expect to reduce our planned sales and marketing expenses, scale back our business plan and seek to terminate certain of our supply agreements, including those with affiliates.

We may not generate sufficient revenue to achieve or maintain profitability. We may incur significant losses in the future for a number of reasons, including slowing demand for our products and increasing competition, as well as the other risks described in this prospectus, and we may encounter unforeseen expenses, difficulties, complications and delays, and other unknown factors in the expansion of our business. Accordingly, we may not be able to achieve or maintain profitability and, we may incur significant losses in the future, and this could cause the price of our Class A common stock to decline.

We face significant competition which could adversely affect our profitability.

The wine industry is intensely competitive. Our wines compete in several Super-premium and Ultra-premium wine market segments with many other Super-premium and Ultra-premium domestic and foreign wines, with imported wines coming from the Burgundy and Bordeaux regions of France, as well as Italy, Chile, Argentina, South Africa and Australia. Our wines also compete with popularly-priced generic wines and with other alcoholic and, to a lesser degree, non-alcoholic beverages, for shelf space in retail stores and for marketing focus by our independent distributors, many of which carry extensive brand portfolios. A result of this intense competition has been and may continue to be upward pressure on our selling and promotional expenses. In addition, the wine industry has experienced significant consolidation. Many of our competitors have greater financial, technical, marketing and public relations resources than we do. Our sales may be harmed to the extent we are not able to compete successfully against such wine or alternative beverage producers’ costs. There can be no assurance that in the future we will be able to successfully compete with our current competitors or that we will not face greater competition from other wineries and beverage manufacturers.

The estimates of our financial performance for the three months and fiscal year ending June 30, 2013 contained in this prospectus are subject to inherent risks.

This prospectus contains certain estimates by our management, including, but not limited to, estimates relating to net sales, net income (loss) and earnings (losses) per share for the three months and fiscal year ending June 30, 2013. These estimates reflect numerous assumptions made by management, including assumptions with respect to our specific as well as general business, economic, market and financial conditions, all of which are difficult to predict and many of which are beyond our control. Accordingly, there is a risk that the assumptions made in preparing the estimates, and/or the estimates themselves, will prove inaccurate. There will likely be differences between actual and projected results, and actual results may differ materially from those contained in the estimates. The inclusion of the estimates in this prospectus should not be regarded as an indication that we or our management or representatives considered or consider the estimates to be a reliable prediction of future events, and the estimates should not be relied upon as such.

12

Because a significant amount of our business is made through our direct to retailer partnerships, any change in our relationship with them could harm our business.

In fiscal year 2011, approximately 83% of our gross wholesale sales were made through our direct retailer relationships to Trader Joe’s and Total Wine & More. In fiscal year 2012, 89% was concentrated in these two accounts. For the first nine months of fiscal year 2013, 77% was concentrated in Trader Joe’s, Safeway, Inc. and Total Wine & More.

Our agreements with our direct retail partners are informal and therefore subject to change. If one or more of our direct retail partners chose to purchase fewer of our products, or we were forced to reduce the prices at which we sell our products to these partners, our sales and profits would be reduced and our business would be harmed.

The loss of Mr. Hurst, Mr. Bielenberg, Ms. Lambrix, Mr. Dolan or other key employees or personnel would damage our reputation and business.

We believe that our success largely depends on the continued employment of a number of our key employees, including Phil Hurst, our Chief Executive Officer, James Bielenberg, our Chief Financial Officer, Virginia Lambrix, our Winemaker, Paul Dolan, one of our co-founders and Kevin Shaw, an independent contractor who serves as our creative director. Any inability or unwillingness of Mr. Hurst, Mr. Bielenberg, Ms. Lambrix, Mr. Dolan, Mr. Shaw or other key management team members to continue in their present capacities could harm our business and our reputation.

A reduction in our access to, or an increase in the cost of, the third-party services we use to produce our wine could harm our business.

We utilize several third-party facilities, of which there is a limited supply, for the production of our wines. Our inability in the future to use these or alternative facilities, at reasonable prices or at all, could increase the cost or reduce the amount of our production, which could reduce our sales and our profits. We do not have long-term agreements with any of these facilities, and they may provide services to our competitors at a price above what we are willing to pay. The activities conducted at outside facilities include crushing, fermentation, storage, blending and bottling. Our reliance on these third parties varies according to the type of production activity. As production increases, we must increasingly rely upon these third-party production facilities. Reliance on third parties will also vary with annual harvest volumes.

In addition, we have limited control over the quality control and quality assurance of these third-party manufacturers. If our suppliers are not able to deliver products that satisfy our requirements, we may be forced to seek alternative providers for these goods and services, which may not be available at the same price, or at all, which would harm our financial results.

The terms of our credit facility with Bank of the West may restrict our current and future operations, which could adversely affect our ability to respond to changes in our business and to manage our operations; we have breached our existing loan covenants.

Our senior credit facility includes a number of customary restrictive covenants that could impair our financing and operational flexibility and make it difficult for us to react to market conditions and satisfy our ongoing capital needs and unanticipated cash requirements. The credit facility contains usual and customary covenants, including, without limitation:

|

·

|

limitation on incurring senior indebtedness;

|

|

·

|

limitation on making loans and advances;

|

|

·

|

limitation on investments, acquisitions and capital expenditures;

|

|

·

|

limitation on liens, mergers and sales of assets; and

|

|

·

|

limitations on activities of Truett-Hurst.

|

In addition, the credit facility contains negative and financial covenants, including, without limitation, a minimum current assets to current liabilities ratio (measured quarterly), debt to effective tangible net worth ratio (measured quarterly) and debt service coverage ratio (measured annually).

We were not in compliance with the minimum current assets to current liabilities ratio at September 30, 2012, December 31, 2012 or March 31, 2013. We were not in compliance with the debt to effective tangible net worth at December 31, 2012 or March 31, 2013. In March 2013 and again in May 2013, as a condition to receiving waivers from Bank of the West, we entered into certain transactions with our members as described in “Management’s Discussion and Analysis of Financial Condition and Result of Operations-Indebtedness.”

Our ability to comply with the covenants and other terms of our senior credit facility will depend on our future operating performance and, in addition, may be affected by events beyond our control, and we may not meet them. If we fail to comply with such covenants and terms, we would be required to obtain waivers from our lenders or agree with our lenders to an amendment of the facility's terms to maintain compliance under such facility. If we are unable to obtain any necessary waivers and the debt under our senior credit facility is accelerated, it would have a material adverse effect on our financial condition and future operating performance, and we may be required to limit our activities.

Because our existing owners will retain significant control over Truett-Hurst after this offering, new investors will not have as much influence on corporate decisions as they would if control were less concentrated.

Following this offering and assuming that all LLC Units held by our existing owners and their respective affiliates, if any, have been converted, our directors and executive officers and their respective affiliates will beneficially own 4,056,233 shares of our outstanding Class A common stock, or approximately 59.6% of our outstanding Class A common stock. Prior to conversion of their LLC Units, each holder of LLC Units will hold a single share of our Class B common stock. Although these shares have no economic rights, they will allow our existing owners to exercise voting power over Truett-Hurst, Inc., the managing member of the LLC, at a level that is consistent with their overall equity ownership of our business. As a result, our existing owners and their respective affiliates have significant influence in the election of directors and the approval of corporate actions that must be submitted for a vote of stockholders.

In addition, certain existing owners, as well as certain trusts and other entities under their control, have entered into guarantee agreements in connection with our credit facility with Bank of the West. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Indebtedness.”

The interests of these affiliates may conflict with the interests of other stockholders, and the actions they take or approve may be contrary to those desired by the other stockholders. This concentration of ownership may also have the effect of delaying, preventing or deterring an acquisition of Truett-Hurst by a third party.

13

Many of our transactions are with related parties, including our founders, executive officers and other related parties, and present conflicts of interest.

We routinely source bulk wine and grapes for our products from vineyards owned by our founders, executive officers, and principal stockholders. We also engage in other transactions with affiliates. The interests of these affiliates in such transactions may be contrary to those desired by stockholders. Although we intend to put in place policies related to mitigating the risk associated with such transactions, stockholders may be harmed by self-dealing with affiliates and our loss of corporate opportunity. See “Certain Relationships and Related Party Transactions.”

In addition, from time to time we enter into transactions for goods and services with entities in which our executive officers, directors and/or affiliates have interests, as further described under “Certain Relationships and Related Party Transactions.” For example, we lease our VML Winery facility, including all of the buildings, grounds, parking areas and other facilities and equipment located at VML Winery, from Hambrecht Wine Group, a member of the LLC.

We also enter into grape and bulk wine purchase agreements from time to time with entities in which our executives and/or founders have financial interests. We have entered into such arrangements with:

|

|

·

|

Hambrecht Vineyards, which is owned by the Hambrecht 1980 Revocable Trust (the “Hambrecht Trust”), of which William R. Hambrecht, a director of the LLC and Truett-Hurst, Inc., serves as trustee. The manager of Hambrecht Vineyards is Forrester R. Hambrecht, a member of the LLC and the grandson of William R. Hambrecht.

|

|

|

·

|

Ghianda Rose Vineyard, which is owned by Diana Fetzer, wife of Paul E. Dolan, III a member of our board of directors.

|

|

|

·

|

Gobbi Street Vineyards, which is partly owned by Diana Fetzer, and Paul E. Dolan, III’s daughter, Nya Kusakabe.

|

|

|

·

|

Mendo Farming Company, which is managed by Heath E. Dolan and owned by the following members: (i) Phillip L. Hurst and Sylvia M. Hurst as trustees of The Hurst Family Revocable Trust Dated August 1, 2004 (the “Hurst Trust”) (33.333% interest); (ii) Paul E. Dolan III, as trustee of The Dolan 2003 Family Trust Dated June 5, 2003 (the “Dolan 2003 Trust”) (30.334% interest); (iii) Peter E. Dolan (17.333% interest); (iv) Heath E. Dolan and Robin A. Dolan, as trustees of The Dolan 2005 Family Trust Dated August 24, 2005 (the “Dolan 2005 Trust”) (9.500% interest); and (v) Zachary Y. Schat and Melissa Schat, as trustees of The Zachary Schat Trust U/D/T Dated September 1, 2004 (the “Schat Trust”) (9.500% interest). Peter E. Dolan is the brother of Paul E. Dolan, III.

|

We believe these arrangements reflect substantially the same market terms we would receive in transactions with unaffiliated third parties. However, if we fail to receive market terms for these transactions or other similar transactions in the future, our profits could be reduced.