UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | Annual report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2017

or

| ¨ | Transition report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number 001-35853

BIOSTAGE, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 45-5210462 | |

| (State or other jurisdiction of | (I.R.S. Employer | |

| Incorporation or organization) | Identification No.) |

84 October Hill Road, Suite 11, Holliston, Massachusetts 01746

(Address of Principal Executive Offices, including zip code)

(774)233-7300

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $0.01 par value

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ¨ NO x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. YES ¨ NO x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES x NO ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). YES x NO ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company x | |

| Emerging growth company x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act. YES ¨ NO x

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant, computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of June 30, 2017 was approximately $15,081,053. Shares of the registrant’s common stock held by each officer and director and each person known to the registrant to own 10% or more of the outstanding voting power of the registrant have been excluded in that such persons may be deemed affiliates. This determination of affiliate status is not a determination for other purposes.

At March 30, 2018, there were 2,859,419 shares of the registrant’s common stock issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the Company’s definitive Proxy Statement in connection with the 2018 Annual Meeting of Stockholders (the “Proxy Statement”), to be filed within 120 days after the end of the Registrant’s fiscal year, are incorporated by reference into Part III of this Form 10-K. Except with respect to information specifically incorporated by reference in this Form 10-K, the Proxy Statement is not deemed to be filed as part hereof.

BIOSTAGE, INC.

TABLE OF CONTENTS

ANNUAL REPORT ON FORM 10-K

For the Year Ended December 31, 2017

INDEX

| i |

This Annual Report on Form 10-K contains statements that are not statements of historical fact and are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934 (the “Exchange Act”), each as amended. The forward-looking statements are principally, but not exclusively, contained in “Item 1: Business” and “Item 7: Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by the forward-looking statements. Forward-looking statements include, but are not limited to, statements about management’s confidence or expectations and our plans, objectives, expectations and intentions that are not historical facts. In some cases, you can identify forward-looking statements by terms such as “may,” “will,” “should,” “could,” “would,” “seek,” “expect,” “plans,” “aim,” “anticipates,” “believes,” “estimates,” “projects,” “predicts,” “intends,” “think,” “continue,” “potential,” “is likely,” “permit,” “objectives,” “optimistic,” “new,” “goal,” “target,” “strategy” and similar expressions intended to identify forward-looking statements. These statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements. We discuss many of these risks in detail under the heading “Item 1A. Risk Factors” beginning on page 18 of this Annual Report on Form 10-K. You should carefully review all of these factors, as well as other risks described in our public filings, and you should be aware that there may be other factors, including factors of which we are not currently aware, that could cause these differences. Also, these forward-looking statements represent our estimates and assumptions only as of the date of this report. We may not update these forward-looking statements, even though our situation may change in the future, unless we have obligations under the federal securities laws to update and disclose material developments related to previously disclosed information. Biostage, Inc. is referred to herein as “we,” “our,” “us,” and “the Company.”

| 1 |

| Item 1. | Business. |

BUSINESS

We are a biotechnology company developing bioengineered organ implants based on our novel CellframeTM technology. Our Cellframe technology is comprised of a biocompatible scaffold seeded with the patient’s own stem cells. Our platform technology is being developed to treat life-threatening conditions of the esophagus, bronchus and trachea. By focusing on these underserved patients, we hope to dramatically improve the treatment paradigm for these patients. Our unique Cellframe technology combines the clinically proven principles of tissue engineering, cell biology and material science.

We believe that our Cellframe technology may provide surgeons a new paradigm to address life-threatening conditions of the esophagus, bronchus, and trachea due to cancer, infection, trauma or congenital abnormalities. Our novel technology harnesses the body’s response and modulates it toward the healing process to regenerate tissue and restore the continuity and integrity of the organ. We are pursuing the Cellspan TM esophageal implant as our first product candidates to address pediatric esophageal atresia and esophageal cancer, and we are also developing our technology’s applications to address conditions of the bronchus and trachea.

In collaboration with world-class institutions, such as Mayo Clinic and Connecticut Children’s Medical Center, we are advancing our technology toward filing an Investigational New Drug (IND) application with the U.S. Food and Drug Administration (FDA) for our Cellspan esophageal implant product candidates. We plan to conduct additional pre-clinical studies in 2018 for our pediatric esophageal atresia program as well as our adult esophageal cancer indication. In 2019, we plan to file an IND with the FDA for each of these esophageal indications.

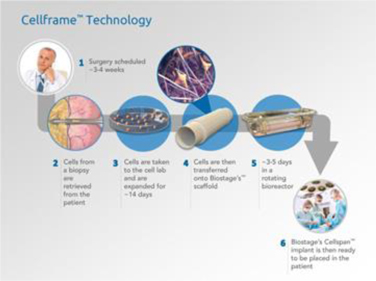

Our Cellframe technology platform: how it works

Our Cellframe process begins with the collection of an adipose (fat) tissue biopsy from the patient followed by the use of standard tissue culture techniques to isolate and expand the patient’s own (autologous) mesenchymal (multipotent) stem cells, or MSC. The cells are seeded onto a proprietary biocompatible, synthetic scaffold, produced to mimic the dimensions of the organ to be regenerated, and incubated in a proprietary organ bioreactor. The scaffold is electrospun from polyurethane (PU) to form a non-woven, hollow tube. The specific microstructures of the Cellspan implants are designed to allow the cultured cells to attach to and cover the scaffold fibers.

| 2 |

We have conducted large-animal studies to investigate the use of the Cellspan implants for the reconstitution of the continuity and integrity of tubular shape organs, such as the esophagus and the large airways, following a full circumferential resection of a clinically relevant segment, just as would occur in a clinical setting. We announced favorable preliminary preclinical results of large-animal studies for the esophagus, bronchus and trachea in November 2015. Based on the results of those studies, we chose the esophagus to be the initial focus for our organ regeneration technology.

Illustration of intersection of Cellspan esophageal implant and native

esophagus at time of implant and proposed mechanism of action

In May 2016, we reported an update of results from additional, confirmatory pre-clinical large-animal studies. We disclosed that the studies had demonstrated in a predictive large-animal model the ability of our Cellspan organ implant to successfully stimulate the regeneration of a section of esophagus that had been surgically removed. Cellspan esophageal implants, consisting of a proprietary biocompatible synthetic scaffold seeded with the recipient animal’s own stem cells, were surgically implanted in place of the esophagus section that had been removed. After the surgical full circumferential resection of a portion of the thoracic esophagus, the Cellspan implant stimulated the reconstitution of full esophageal structural integrity and continuity.

Illustration of esophageal reconstitution over Cellspan esophageal

implant following time of implant and proposed mechanism of action

Study animals were returned to a solid diet three weeks after the implantation surgery. The scaffold portions of the Cellspan implants, which are intended to be in place only temporarily, were retrieved approximately three weeks post-surgery via the animal’s mouth in a non-surgical endoscopic procedure. Within 2.5 to 3 months, a complete inner epithelium layer and other specialized esophagus tissue layers were regenerated. Two animals in the study were kept in life for almost two years to evaluate the long-term viability of the newly regenerated tubular conduit and were then sacrificed for histological data. Prior to their sacrifice, these animals demonstrated normal weight gain, appeared healthy and free of any significant side effects and received no specialized care.

| 3 |

Platform technology in life-threatening orphan indications

In November 2016, we were granted Orphan Drug Designation for our Cellspan esophageal implant by the FDA to restore the structure and function of the esophagus subsequent to esophageal damage due to cancer, injury or congenital abnormalities. Orphan drug designation provides a seven-year marketing exclusivity period against competition in the U.S. from the date of a product’s approval for marketing. This exclusivity would be in addition to any exclusivity we may obtain from our patents. Additionally, orphan designation provides certain incentives, including tax credits and a waiver of the Biologics License Application fee. We also plan to apply for orphan drug designation for our Cellspan esophageal implant in Europe. Orphan drug designation in Europe provides market exclusivity in Europe for ten years from the date of the product’s approval for marketing.

We are now advancing the development of our Cellframe technology, specifically a Cellspan esophageal implant, in large-animal studies with collaborators. In order to seek approval for the initiation of clinical trials for Biostage Cellspan esophageal implants in humans, GLP studies to support the safety of the Cellspan esophageal implant are required to submit an Investigational New Drug (IND) application with the FDA. As we believe that our recent studies provided sufficient confirmatory proof of concept data, we have initiated the Good Laboratory Practice (GLP) studies to demonstrate that our technology, personnel, systems and practices are sufficient for advancing into human clinical trials. We have conducted a number of IND-enabling GLP studies demonstrating safety and feasibility of the Cellspan implant. These studies were done primarily in pursuit of our adult esophageal cancer program. Additional GLP studies are necessary in support of the adult esophageal cancer program, which will also be supportive of an IND for the pediatric esophageal atresia program. We intend to perform those studies in 2018. We will also pursue additional non-GLP studies for the pediatric esophageal atresia program in 2018 to optimize that product candidate.

First-In-Human Use of Esophageal Implant Product Candidate

On August 7, 2017, we announced the use of our Cellspan Esophageal Implant product candidate in a patient at a major U.S. hospital via an FDA-approved single-use expanded access application. The patient was a 75-year old male with a life-threatening cancerous mass in his chest that spanned his heart, a lung and his esophagus. The surgery was performed in May 2017 to remove the tumor, repair the heart, part of one lung, and a section of the esophagus. The Cellspan Esophageal Implant was interpositioned into the gap in the esophagus created by the removal of the tumor. The patient’s surgeon informed us at that time that the surgery was a success and the patient was later discharged from the hospital. In February 2018 the surgeon informed us that the patient had died after living approximately eight months after surgery. The surgeon stated that the cause of death was a stroke, and that the stroke was unrelated to the esophageal implant. The surgeon also informed us that a preliminary autopsy had shown that the esophageal implant resulted in a regenerated esophageal tube in the patient, except for a very small (approximately 5mm) hole on the lateral wall that was right up against a synthetic graft inserted as part of the patient’s heart repair on the pericardium in that same surgery. The synthetic graft on the pericardium was not related to our esophageal implant product and may have acted as an irritant to esophageal regeneration where it contacted the esophageal implant. The surgeon also informed us that the esophageal regeneration in this patient was consistent with the regeneration previously observed in our large-animal studies. The surgeon informed us that following completion of the autopsy the hospital will pursue a publication and we expect to be in a position to release additional information on this landmark case at that time.

Our product candidates are currently in development and have not yet received regulatory approval for sale anywhere in the world.

Changing the surgical treatment of Esophageal Cancer

|

|

| |

| Illustration of esophageal cancer site | Illustration of potential human application of Cellspan esophageal implant at site of esophageal cancer (depicting implant prior to esophageal tissue reconstitution over implant) |

According to the World Health Organization’s International Agency for Research on Cancer, there are approximately 450,000 new cases of esophageal cancer worldwide each year. A portion of all patients diagnosed with esophageal cancer are treated via a surgical procedure known as an esophagectomy. The current standard of care for an esophagectomy requires a complex surgical procedure that involves moving the patient’s stomach or a portion of their colon into the chest to replace the portion of esophagus resected by the removal of the tumor. These current procedures have high rates of complications and can lead to a severely diminished quality of life and require costly ongoing care. Our Cellspan esophageal implants aim to provide a simpler surgical procedure, with reduced complications, that may result in a better quality of life after the operation and reduce the overall cost of these patients to the healthcare system.

| 4 |

Focus on Pediatric Esophageal Atresia: a congenital abnormality in need of a better solution

Each year, several thousand children worldwide are born with a congenital abnormality known as esophageal atresia, a condition where the baby is born with an esophagus that does not extend completely from the mouth to the stomach. When a long segment of the esophagus is lacking, the current standard of care is a series of surgical procedures where surgical sutures are applied to both ends of the esophagus in an attempt to stretch them and pull them together so they can be connected at a later date. This process can take weeks and the procedure is plagued by serious complications and may carry high rates of failure. Such approach also requires, in time, at least two separate surgical interventions. Other options include the use of the child’s stomach or intestine that would be pulled up into the chest to allow a connection to the mouth. We are working to develop a Cellspan esophageal implant solution to address the complications of esophageal atresia, that could potentially be life-changing or organ-sparing, or both.

Our Mission and Our Strategy

Our mission is to revolutionize regenerative medicine by bioengineering patient-specific Cellspan implants that use the patient’s own cells to stimulate organ regeneration and restore an organ’s structure and continuity. Our business strategy to accomplish this mission includes:

Targeting life-threatening medical conditions. We are focused on creating products to help physicians treat life-threatening conditions like esophageal cancer, central lung cancer and damage to the trachea caused by cancer, trauma or infection. We are also developing products for the treatment of congenital abnormalities of the esophagus and the airways. We are not targeting less severe conditions that have reasonable existing treatment options. Solutions for life-threatening medical conditions present a favorable therapeutic index, or risk/benefit relationship, by providing the opportunity of a significant medical benefit for patients who have poor or no treatment alternatives. We believe that product candidates targeting life-threatening medical conditions may be eligible for review and approval by regulatory authorities under established expedited review programs, which may result in savings of time in the regulatory approval process. Also, we believe that products targeting life-threatening medical conditions may be more likely to receive favorable reimbursement compared with treatments for less critical medical conditions.

Developing products that have a relatively short time to market. Since the number of patients diagnosed with esophageal cancer in the U.S. each year is relatively small, we expect the number of patients that we would likely need to enroll in a clinical trial will also be relatively small. A small number of patients implies a relatively fast enrollment time and a less expensive clinical development program. Therefore, we expect to be able to conduct a clinical trial in a relatively short period of time compared to clinical trials in indications with larger patient populations. We intend to work closely with regulatory agencies and clinical experts to design and size the clinical studies appropriately based on the specific conditions our products are intended to treat.

Using our Cellframe technology as a platform to address multiple organs. We believe that pre-clinical data we have produced to date may suggest that our Cellframe technology is a novel and innovative approach to restoring organ function that may provide an ability to develop products that would address life-threatening conditions impacting organs like the esophagus, bronchus and trachea, and perhaps lower portions of the gastrointestinal (GI) tract. We believe that our Cellframe technology may allow physicians to treat certain life-threatening conditions in ways not currently possible, and in some combination, to save patients’ lives, avoid or reduce complications experienced in the current standard of care, and improve the patients’ quality of life, while at the same time reducing the overall cost of patient care to the healthcare system.

Supplying the finished organ implant to the surgeon. Our technology includes our proprietary organ bioreactor, as well as our proprietary biocompatible scaffold that is seeded with the patient’s own cells. We believe there is considerable value in supplying the final cell-seeded scaffold implant to the surgeon so that the hospital and surgeon may focus solely on performing the implantation.

Collaborating with leading medical and research institutions. We have and will continue to collaborate with leading medical and research institutions. We have a co-development initiative with Mayo Clinic for regenerative medicine organ implant products for the esophagus and airways based on our Cellframe technology. We are also collaborating with Connecticut Children’s Medical Center on a co-development project to translate our Cellframe technology for pediatric esophageal atresia from pre-clinical studies to clinical trials. We believe the use of our product candidates by leading surgeons and institutions will increase the likelihood that other surgeons and institutions will use our products.

| 5 |

Our Technology

Our Cellframe technology is comprised of our proprietary bioengineered organ scaffold seeded with the patient’s own stem cells in our proprietary organ bioreactor prior to implantation. We believe that our Cellframe technology combines a highly-engineered, biocompatible scaffold and a robust population of cells that, by tapping into the stem cell niche of the surrounding native tissue after implantation, may potentially enable a tubular organ to remodel or regenerate tissue to close the gap created by a surgical resection of a portion of that organ. This unique combination of technologies, developed through our extensive testing performed during the last few years, may potentially provide solutions to life-threatening conditions for patients with unmet medical needs.

We believe that our technology is unique, in that its mode of action appears to be different from other tissue engineering organ scaffold products developed previously, of which we are aware. Prior to our development of the Cellframe technology, our approach attempted to implant an organ scaffold that would be incorporated into the patient’s body by the surrounding native tissue growing into the scaffold. To our knowledge, all previous research and development efforts by other investigators were based on that same concept. Our Cellframe technology appears to work very differently. We believe that the unique combination of our highly-engineered organ scaffold with a population of the patient’s own mesenchymal stem cells enables an organ to develop new native tissue around our scaffold, but not into it, so the scaffold acts as a type of frame or staging for the new tissue. As a result, our scaffold is not incorporated into the body. Instead, it is retrieved from the body via an endoscopic procedure, not surgically, after sufficient tissue remodeling and regeneration has occurred to restore the organ’s integrity and function.

A Cellframe technology-based organ implant includes two key components: a biocompatible synthetic scaffold and the patient’s own stem cells.

Biocompatible Scaffold Component

Our proprietary biocompatible scaffold component of the Cellspan esophageal implant is constructed primarily of polyurethane (PU; a plastic polymer). This material was chosen based on extensive testing of various materials. The scaffold is made using a manufacturing process known as electrospinning. The combination of the electrospinning process, which provides control over the desired microstructure of the scaffold fabric, with the PU results in a scaffold that we believe has favorable biocompatibility characteristics.

The Patient’s Cells

Based on current pre-clinical development efforts, the cells we seed onto the scaffold are obtained from the patient’s adipose tissue (abdominal fat). This fat tissue is obtained from a standard biopsy before the implant surgery. Mesenchymal stem cells are extracted and isolated from the adipose tissue biopsy. The isolated cells are then expanded, or grown, for a short period prior to surgery in order to derive a sufficient cell population to be seeded on the scaffold. The cells are then seeded on the scaffold in our proprietary organ bioreactor and incubated there before the implant surgery.

We believe the Cellspan esophageal implant has the potential to provide a major advance over the current therapeutic options for treating esophageal cancer, damage from infection or trauma and congenital abnormalities. We believe our Cellframe technology has the potential to overcome the major challenges in restoring organ function for a damaged esophagus. With our Cellspan esophageal implant we are developing a surgical procedure that has the objective of reconstituting the continuity of the patient’s esophagus without having to relocate another organ in its place. In addition, by reducing or eliminating complications that occur in the current standard of care, we expect to reduce the costs of addressing and treating those additional complications. Because these substantial costs can be reduced or even eliminated with our technology, we believe our products, if successfully developed, can help save lives, improve the quality of life for patients and reduce overall healthcare costs.

| 6 |

Unmet Patient Needs and Cellspan Implant Solutions

Esophageal Cancer

There are approximately 456,000 new diagnoses of esophageal cancer globally each year, according to the World Health Organization’s International Agency for Research on Cancer. According to the American Cancer Society, there are approximately 17,000 new diagnoses of esophageal cancer in the U.S. each year, and there are more than 15,000 deaths from esophageal cancer each year. Esophageal cancer is very deadly - the five-year survival rate for people with esophageal cancer is 18% in the U.S. Approximately 5,000 esophagectomy surgeries occur in the U.S. annually to treat esophageal cancer, and approximately 10,000 esophagectomies occur in Europe annually. We believe that approximately one half of the world’s esophageal cancer cases occur in China, which would represent the largest patient population for our adult esophageal product candidate. We believe that our Cellspan esophageal implant, if approved, has the potential to provide a major advance over the current esophagectomy procedures for addressing esophageal cancer, which have high complication and morbidity rates.

The current standard of care for the esophagectomy requires either (A) a gastric pull-up, where the stomach is cut and sutured into a tubular shape, then pulled up through the diaphragm to replace a portion of the esophagus resected by the removal of the cancerous tumor; or (B) a colon interposition, where a portion of the colon is resected and used to replace the portion of the esophagus resected by the removal of the cancerous tumor. Esophagectomies have 90-day mortality rates of up to 19%. Serious complications, such as leakage at the anastomoses, which can lead to infections and sepsis, and pulmonary complications, such as impaired pulmonary function or pneumonia, occur in up to 30% of esophagectomy cases. Other complications from esophagectomies, such as a narrowing of the esophagus post-surgery, gastroesophageal reflux and dumping syndrome (repetitive nausea, dizziness and vomiting) can also pose significant quality of life issues for patients.

We believe that the Cellspan esophageal implant has the potential to provide physicians a new, simpler procedure to restore organ function while significantly reducing complication and morbidity rates compared with the current standard of care, and without creating significant quality of life issues for patients.

Esophageal Atresia

Esophageal Atresia (EA) is a rare congenital abnormality in which a baby is born without part of the esophagus. About 1 in 4,000 babies in the U.S. is born with EA. In some cases, the two sections can be connected surgically. However, in cases where the gap is too great for a simple surgical reconnection, the current standard of care is a gastric pull-up, a colon interposition, or a procedure known as the Foker process. In the Foker process, traction devices are surgically attached to the two ends of the esophagus. Traction is then applied, usually for several weeks during which time the baby remains in an Intensive Care Unit, to stimulate the ends of the esophagus to grow and narrow the gap. If the Foker process is successful in narrowing the gap sufficiently, a second surgery is necessary to connect the two ends of the esophagus. In addition to the Foker process being complex, it is also a very expensive procedure, because the baby will normally be several months in hospital for the process.

We believe that a pediatric Cellspan esophageal implant may provide pediatric surgeons with a better procedure to treat EA that would result in a connected esophagus with higher success rates, lower complications and lower overall costs to the healthcare system.

Central Lung Cancer

Lung cancer is the most common form of cancer and the most common cause of death from cancer worldwide. There are more than 450,000 new lung cancer diagnoses annually in the U.S. and Europe. In approximately 25% of all lung cancer cases, the cancerous tumor resides only in a bronchus and not in the lobes of the lungs, and is known as central lung cancer. Approximately 33,000 central lung cancer cases diagnosed in the U.S. and Europe are Stage I and II and are considered eligible for surgical resection, often with adjuvant chemotherapy and radiation. Approximately 5,000 of those patients are treated via pneumonectomy, a surgical procedure involving the resection of the cancer tumor, the whole bronchus below the tumor and the entire lung to which it is connected. It is a complex surgery and, due to the removal of a lung, results in a 50% reduction in the patient’s respiratory capacity. The procedure has reported rates of post-surgical (in hospital) mortality of 8% to 15%. Complication rates associated with pneumonectomy are reported as high as 50%, and include post-operative pneumonia, supraventricular arrhythmias and anastomotic leakage, placing patients at significant mortality risk post-discharge.

We believe that a Cellspan bronchial implant, once developed and approved for marketing, has the potential to provide physicians a treatment alternative superior to the sleeve pneumonectomy to address central lung cancer, a simpler procedure to restore organ function of the bronchus without sacrificing one of the patient’s lungs, resulting in fewer post-surgery complications, improved mortality rates and improved quality of life for the patient.

Life-threatening conditions of the Trachea

There are approximately 8,000 patients per year in the U.S. and Europe who suffer from a condition of the trachea that put the patient at high risk of death. These conditions can be due to tracheal trauma, tracheal stenosis or trachea cancer. There are approximately 40,000 tracheal trauma patients diagnosed each year in the U.S. Of those, approximately 1,000 are severe enough to need surgical resection procedures. Tracheal stenosis is a rare complication from tracheostomies, but may have a devastating impact on respiratory function for patients. Approximately 2,000 patients are diagnosed with stenosis from tracheostomy in the U.S. each year. Trachea cancer is a very rare but extremely deadly cancer. Trachea cancer patients in the U.S. have a median survival of 10 months from diagnosis and a 5-year survival of only 27%. There were approximately 200 cases of primary trachea cancer diagnosed in the U.S. in 2013. Based on these facts, we estimate that there are approximately 8,000 patients in the U.S. and Europe with conditions of the trachea that put them at high risk of death, but for whom there is currently no clinically effective tracheal implant or replacement method currently available.

We believe that a Cellspan tracheal implant may potentially provide physicians a treatment to re-establish the structural integrity and function of a damaged or diseased trachea to address life-threatening conditions due tracheal trauma, stenosis or cancer.

| 7 |

Our History

We were incorporated under the laws of the State of Delaware on May 3, 2012 by Harvard Bioscience, Inc. (“Harvard Bioscience”) to provide a means for separating its regenerative medicine business from its other businesses. Harvard Bioscience decided to separate its regenerative medicine business into our company, a separate corporate entity (the “Separation”), and it spun off its interest in our business to its stockholders in November 2013. Since the Separation we have been a separately-traded public company and Harvard Bioscience has not been a stockholder of our common stock or controlled our operations. Following the Separation, we continued to innovate our bioreactors based on our physiology expertise, we developed our materials science capabilities and we investigated and developed a synthetic tracheal scaffold. By that time, we had built and staffed cell biology laboratories at our Holliston facility, to give ourselves the ability to perform and control our scientific investigation and developments internally. At that point, we began the second phase of our company’s development.

In mid-2014, we increased the pace of our scientifically-based internal analysis and development of our first-generation tracheal implant product, the HART-Trachea. From large-animal studies conducted thereafter we found that the product elicited an unfavorable inflammatory response after implantation, which required additional development and testing. These requirements extended our expectations regarding our regulatory milestones and we announced the additional testing and extended milestone expectations in January 2015. During 2015 we isolated and tested all major variables of the organ scaffold and the cell source and protocols, examining the effects of alternatives against the then-existing product approach. Through extensive in vitro preclinical studies, and small-animal and large-animal studies, we made dramatic improvements, and discovered that the mechanism of action of this new approach was very different from our hypothesis regarding that of the first-generation product. We call this new implant approach our Cellframe technology. Our Cellframe technology uses a different scaffold material and microstructure, a different source and concentration of the patient’s cells and several other changes from our earlier trachea initiative. We believe that our Cellframe technology, although built on learnings from our earlier-generation product initiative, represents a new technology platform resulting from our rigorous science and development. We see the development of our Cellframe technology platform as the beginning of a new, third phase in our company’s progression.

We discontinued development of our earlier initiative in 2014; that first-generation product approach was significantly different from our new Cellframe technology and Cellspan product candidates currently in development. We have focused our development efforts on our Cellframe technology and Cellspan product candidates, which we have and will continue to develop internally, and with our collaborators, via a rigorous scientific development process.

Clinical Trials

Our Esophageal Cellspan Implant has been designated by the FDA as a combination product biologic. We believe that this is a favorable designation as it allows for orphan designation and a more participatory path to approval. To date, we have conducted numerous pre-clinical studies in our esophageal implant programs and continue to see consistent regeneration. We are analyzing these data and our human experience to better ascertain what specific pre-clinical studies are still needed prior to conducting a phase I human clinical trial. We are pursuing two indications in parallel. The two complementary indications we are pursuing are esophageal cancer and pediatric esophageal atresia. In order to market our product candidates, we will need to successfully complete clinical trials. The initial indication for which we intend to seek FDA approval will be to restore the function of the esophagus subsequent to esophageal damage or stenosis due to cancer, injury or infection.

Because esophageal cancer affects only approximately 17,000 patients per year in the U.S. we anticipate that our clinical trials will involve relatively few patients. Therefore, once commenced, we expect to be able to conduct a clinical trial in a relatively short period of time compared to clinical trials in indications with larger patient populations. We intend to work closely with regulatory agencies and clinical experts to design and size the clinical studies appropriately based on the specific conditions our products are intended to treat. We also intend to request expedited review from the FDA for the Cellspan esophageal implant product. Receipt of expedited review would reduce the overall time through the regulatory approval process. These expedited requests are submitted during the IND process.

We believe that we have excellent pre-clinical and clinical support of the pediatric atresia program through our collaboration with Connecticut Children’s Medical Center and our primary investigator Dr. Christine Finck. Essentially, we liken the pediatric atresia market to a rare disease market. Accordingly, the clinical trial population should reflect the ultra-orphan nature of the disease state.

We intend to pursue regulatory approval for the Cellspan esophageal implant in the U.S., initially. Following clinical trials in other foreign markets, we expect to pursue regulatory approval for the Cellspan esophageal implant in those foreign markets, as well. We believe that approximately one half of the world’s esophageal cancer cases occur in China, which would represent the largest potential patient population for our adult esophageal implant product candidate, and we are consequently beginning to prepare to address that market.

Research and Development

Our primary research and development activities are focused in three areas: materials science, cell biology and engineering. In materials science, we focus on designing and testing biocompatible organ scaffolds, testing the structural integrity and the cellularization capacities of the scaffolds. In cell biology, we focus on developing and testing isolation and expansion protocols, cell characterization and fate studies, investigating the effects of various cell types and concentrations, evaluating the biocompatibility of scaffolds, experimenting with different cell seeding methodologies, and developing protocols for implantation experiments. Our engineering group supports the materials science and cell biology groups across an array of their activities, i.e. designing, engineering and making our proprietary organ bioreactors. All three of our R&D groups combine to plan and execute the in vitro studies. A fundamental part of our R&D effort in developing the Cellframe technology has been dedicated to the discovery and development of small and large animal model studies. The large-animal model employs the use of Yucatan mini-pigs. Our Cellspan scaffolds were implanted in the cervical portion as well as the thoracic portion of the esophagus and the airways in studies to date.

Following the failure to receive the funding with respect to a securities purchase agreement in August 2017, and in an effort to conserve cash, we completed a reduction in headcount of 20 persons during October and November 2017, of whom 18 were directly involved in research and development activities. As a result, we had one research and development employee as of December 31, 2017. Following our raising additional capital in December 2017, January 2018 and February 2018, we re-hired four of our former research and development employees into key scientific and engineering positions, and retained two others as consultants, in January 2018. We believe that our new staffing level after those hires, combined with our consultant and co-development collaborator resources, is sufficient to pursue both of our esophageal programs.

In addition to our in-house engineering and scientific development team, we collaborate with leaders in the field of regenerative medicine who are performing the fundamental research and surgeries in this field to develop and test new products that will advance and improve the procedures being performed. We will work with our collaborators to further enhance our products to make them more efficient and easier to use by surgeons. In the U.S., our principal collaborations have been with Mayo Clinic and Connecticut Children’s Medical Center. Collaboration typically involves us developing new technologies specifically to address issues these researchers and clinicians face, and then working together to translate our technology from pre-clinical studies to clinical trials. In certain instances, we have entered into agreements that govern the ownership of the technologies developed in connection with these collaborations.

| 8 |

We incurred approximately $7.7 million and $7.6 million of research and development expenses in 2017 and 2016, respectively. As we have not yet applied for or received regulatory approval to market any clinical products and sales of our research bioreactor products have not been significant in relation to our operating costs, no significant amount of these research and development costs have been passed on to our customers.

Manufacturing

Biostage has developed a comprehensive manufacturing process for our product candidates, including: cell biology, scaffold production, cell isolation and expansion, seeding of cells on the scaffold, incubation and expansion processes in the bioreactor and product transportation. We currently perform certain manufacturing steps in-house and subcontract certain processes and activities, primarily those related to cell expansion, seeding and incubation, to experienced partners.

For our scaffolds we use a process called electrospinning to create the fabric part of the scaffold. Electrospinning is a well-known fabrication process. It is useful for cell culture applications as it can create extremely thin fibers (much thinner than a human hair) that can make a fabric with pores approximately the same size as a cell. The electrospinning process parameters can be tuned to create a structure that is very similar to the natural structure of the collagen fibers in human extracellular matrix. Our process and end product have been developed over many years and involve many trade secrets and proprietary know-how. Our Cellspan scaffolds are made from polyurethane, an inert polymer that is not bioresorbable. However, we also perform studies on the use of scaffolds made from bioresorbable materials. While we do not manufacture the cells, as they will come from the patient’s adipose tissue, for regulatory purposes we are responsible for the quality control of the cells and the seeding of the cells onto the scaffold in the bioreactor. For this we have, in collaboration with our partners, developed standard operating procedures for the seeding of cells on the scaffold. For U.S. clinical trials we anticipate that the seeding will be performed in an automated version of our bioreactor at a pre-qualified third-party contract manufacturer using current Good Manufacturing Procedures (cGMP) using our proprietary protocol and under the supervision of our staff.

For our scaffolds, our primary materials are medical-grade plastic resins and solvents used to liquefy the resins in our manufacturing process. These materials are readily available from a variety of suppliers and do not currently represent a large proportion of our total costs. For our bioreactors, we perform final assembly and testing of components that we buy from third parties like machine shops, parts distributors, molding facilities and printed circuit board manufacturers. These operations are performed primarily at our Holliston, MA headquarters.

Sales and Marketing

We expect that most surgeries using the Cellspan esophageal implant product will be performed at a relatively small number of major hospitals in the U.S., Canada and European countries that will establish themselves as specialized centers of excellence. We believe that a relatively small number of centers of excellence in each country would be able to treat a very large percentage of that country’s patients annually, given the expected number of patients to be treated each year. So, we expect our markets to be served by a concentrated number of treatment centers. Further, our three Cellspan product candidates are for the esophagus, the bronchi and the trachea, three organs all treated by thoracic surgeons. Therefore, all three products, once approved, would be marketed primarily to physicians practicing in a single surgical specialty, so we expect that the total number of physicians using our products will be a much smaller population than if our products were to be used by physicians in multiple areas of surgical specialties. Due to our expectation of a population of physicians in one surgical specialty being the primary users of our products in a concentrated number of centers of excellence in each national market, we expect to be able to support our markets with a fairly small field sales force.

We expect to price the product commensurate with the medical value created for the patient and the costs avoided with the use of our product. We further expect to be paid by the hospital that buys the product from us. Finally, we expect that the hospital would seek reimbursement from payers for the entire transplant procedure, including the use of our products.

Harvard Bioscience is the exclusive distributor for the research versions of our organ bioreactors. Harvard Bioscience can only sell those products to the research markets in accordance with the terms of our distribution agreement. We retain all rights to manufacture and sell all our products for clinical use.

| 9 |

Intellectual Property and Related Agreements

We actively seek to protect our products and proprietary information by means of U.S. and foreign patents, trademarks and contractual arrangements. Our success will depend in part on our ability to obtain and enforce patents on our products, processes and technologies to preserve our trade secrets and other proprietary information and to avoid infringing on the patents or proprietary rights of others.

We anticipate that we will sell products in various markets in the United States and various jurisdictions under brand name, logo and product design trademarks and service marks and that these marks will attain material importance in the future.

We also own select U.S. Patents as well as certain patents in Germany. These patents cover aspects of device and processes currently under development by our company. Patents for various processes and devices extend for varying periods according to the date of patent filing or grant and the legal term of patents in the country or countries in which the patent was obtained. The actual protection afforded by a patent can vary from country to country and depends on factors such as the type of patent, scope of protection and available legal remedies.

In addition to issued patents, we have several pending patent applications in the U.S. and key target jurisdictions. We believe that one or more of these pending patent applications may be of importance to material position depending upon factors such as the relevant patent jurisdiction, type of patent granted, and scope of patent claims ultimately allowed in a given jurisdiction. Depending upon factors such as the type of grant and the date on which the patent application was filed, we anticipate that the term of certain pending patents may extend to 2036.

We also rely on unpatented proprietary technologies in the development and commercialization of our products. We also depend upon the skills, knowledge and experience of our scientific and technical personnel, as well as those of our advisors, consultants and other contractors. To help protect our proprietary know-how that may not be patentable, and our inventions for which patents may be difficult to enforce, we rely on trade secret protection and confidentiality agreements to protect our interests. To this end, we require employees, consultants and advisors to enter into agreements that prohibit the disclosure of confidential information and, where applicable, require disclosure and assignment to us of the ideas, developments, discoveries and inventions that arise from their activities for us. Additionally, these confidentiality agreements require that our employees, consultants and advisors do not bring to us, or use without proper authorization, any third party’s proprietary technology.

| 10 |

Exclusive License Agreement and Sponsored Research Agreement - InBreath Bioreactor

We entered into a sponsored research agreement with Sara Mantero, Maria Adelaide Asnaghi, and the Department of Bioengineering of the Politecnico Di Milano, or PDM. Under the terms of this agreement, PDM was required to use its facilities and best efforts to conduct a research program relating to the development of bioreactors, clinical applications, and automated seeding processes. We were required to provide engineering support to PDM with respect to bioreactor designs. Intellectual property developed by PDM or its employees, including Dr. Mantero or Ms. Asnaghi, under this sponsored research agreement will be owned by Dr. Mantero or Ms. Asnaghi and covered by our exclusive license agreement described above. In addition, we have an option to an exclusive license for intellectual property relating to new technology that may not be covered by the exclusive license agreement. We will own any inventions and discoveries that we solely develop in connection with the research program and any inventions and discoveries that are jointly developed in connection with the research program will be owned jointly by the parties. We terminated the sponsored research agreement in 2017.

Sublicense Agreement with Harvard Bioscience

We have entered into a sublicense agreement with Harvard Bioscience pursuant to which Harvard Bioscience has granted us a perpetual, worldwide, royalty-free, exclusive, except as to Harvard Bioscience and its subsidiaries, license to use the mark “Harvard Apparatus” in the name Harvard Apparatus Regenerative Technology. The mark “Harvard Apparatus” is used under a license agreement between Harvard Bioscience and Harvard University, and we have agreed to be bound by such license agreement in accordance with our sublicense agreement. We currently have no affiliation with Harvard University.

Separation Agreements with Harvard Bioscience

On November 1, 2013, to effect the Separation, Harvard Bioscience distributed all of the shares of our common stock to the Harvard Bioscience stockholders (the “Distribution”). Prior to the Distribution Harvard Bioscience contributed the assets of its regenerative medicine business, and approximately $15 million in cash, to our company to fund our operations following the Distribution.

In connection with the Separation and immediately prior to the Distribution, we entered into a Separation and Distribution Agreement, Intellectual Property Matters Agreement, Product Distribution Agreement, Tax Sharing Agreement, Transition Services Agreement, and Sublicense Agreement with Harvard Bioscience to effect the Separation and Distribution and provide a framework for our relationship with Harvard Bioscience after the Separation. These agreements govern the current relationships among us and Harvard Bioscience and provided for the allocation among us and Harvard Bioscience of Harvard Bioscience’s assets, liabilities and obligations (including employee benefits and tax-related assets and liabilities) attributable to periods prior to the Separation.

Government Regulation

Any product that we may develop based on our Cellframe technology, and any other clinical products that we may develop, will be subject to considerable regulation by governments. We were in the past informed by the FDA that our previous-generation tracheal product candidate would be regulated under the Biologics License Application, or BLA, pathway in the U.S. and we were informed by the European Medicines Agency (EMA) that the previous generation tracheal product would be regulated under the Advanced Therapy Medicinal Products(ATMP), pathway in the EU. On October 18, 2016, we also received written confirmation from FDA’s Center for Biologics Evaluation and Research(CBER), that FDA intends to regulate our Cellspan esophageal implant as a combination product under the primary jurisdiction of CBER. We further understand that CBER may choose to consult or collaborate with the FDA’s Center for Devices and Radiological Health (CDRH), with respect to the characteristics of the synthetic scaffold component of our product based on CBER’s determination of need for such assistance. Although our Cellframe technology differs in design and performance from the first-generation product candidate, we expect that Cellframe-based products will be regulated by the FDA and EMA under the same pathways as the first-generation tracheal product candidate. This expectation is based on the fact that the Cellframe technology is centered on the delivery of the patient’s own cells seeded on an implanted synthetic scaffold in order to restore organ function and our belief that the cells provide the primary mode of action. Of course, it is possible that some of our current and future products may use alternative regulatory pathways.

| 11 |

Regulatory Strategy

Domestic Regulation of Our Products and Business

The testing, manufacturing, and potential labeling, advertising, promotion, distribution, import and marketing of our products are subject to extensive regulation by governmental authorities in the U.S. and in other countries. In the U.S., the FDA, under the Public Health Service Act, the Federal Food, Drug and Cosmetic Act, and its implementing regulations, regulates biologics and medical device products.

The labeling, advertising, promotion, marketing and distribution of biopharmaceuticals, or biologics and medical devices also must be in compliance with the FDA and U.S. Federal Trade Commission (FTC), requirements which include, among others, standards and regulations for off-label promotion, industry sponsored scientific and educational activities, promotional activities involving the internet, and direct-to-consumer advertising. The FDA and FTC have very broad enforcement authority, and failure to abide by these regulations can result in penalties, including the issuance of a warning letter directing us to correct deviations from regulatory standards and enforcement actions that can include seizures, injunctions and criminal prosecution. Further, we are required to meet regulatory requirements in countries outside the U.S., which can change rapidly with relatively short notice.

| 12 |

We have been informed by the FDA that our Cellspan esophageal implant product candidates are combination biologic/device products. Biological products must satisfy the requirements of the Public Health Services Act and the Food, Drug and Cosmetics Act and their implementing regulations. In order for a biologic product to be legally marketed in the U.S., the product must have a BLA approved by the FDA.

The BLA Approval Process

The steps for obtaining FDA approval of a BLA to market a biopharmaceutical, or biologic product in the U.S. include:

| • | completion of pre-clinical laboratory tests, animal studies and formulation studies under the FDA’s GLP regulations; |

| • | submission to the FDA of an IND application, for human clinical testing, which must become effective before human clinical trials may begin and which must include Institutional Review Board (IRB), approval at each clinical site before the trials may be initiated; |

| • | performance of adequate and well-controlled clinical trials in accordance with Good Clinical Practices (GCP), to establish the safety and efficacy of the product for each indication; |

| • | submission to the FDA of a BLA, which contains detailed information about the chemistry, manufacturing and controls for the product, extensive pre-clinical information, reports of the outcomes of the clinical trials, and proposed labeling and packaging for the product; |

| • | the FDA’s acceptance of the BLA for filing; |

| • | satisfactory review of the contents of the BLA by the FDA, including the satisfactory resolution of any questions raised during the review or by the advisory committee, if applicable; |

| • | satisfactory completion of an FDA inspection of the manufacturing facility or facilities at which the product is produced to assess compliance with cGMP regulations, to assure that the facilities, methods and controls are adequate to ensure the product’s identity, strength, quality and purity; and |

| • | FDA approval of the BLA. |

Based on preliminary discussions with the FDA, we expect the clinical trials for our esophageal implant product candidates to be conducted in two sequential phases:

| · | A Phase 1, or Pilot Trial, where our product would be tested on a small number, perhaps five or six, of patients to demonstrate the product’s safety. If successful, that study would be followed by, |

| · | A Phase II Registration, or Pivotal Trial to test the product’s efficacy. We believe that the nature of our esophageal products and the sizes of their targeted patient populations would lead to a small number of patients in this trial, relative to most biotechnology clinical trials. |

| 13 |

Clinical testing may not be completed successfully within any specified time period, if at all. The FDA closely monitors the progress of each of the phases of clinical trials that are conducted under an IND and may, at its discretion, reevaluate, alter, suspend, or terminate the testing based upon the data accumulated to that point and the FDA’s assessment of the risk/benefit ratio to the patient. The FDA or the sponsor may suspend or terminate clinical trials at any time for various reasons, including a finding that the subjects or patients are being exposed to an unacceptable health risk. The FDA can also request that additional pre-clinical studies or clinical trials be conducted as a condition to product approval.

Companies also may seek Fast Track or Breakthrough Therapy designation for their products. Fast Track or Breakthrough Therapy products are those that are intended for the treatment of a serious or life-threatening condition and that demonstrate the potential to address unmet medical needs for such a condition. If awarded, the Fast Track or Breakthrough Therapy designation applies to the product only for the indication for which the designation was received.

If the FDA determines after review of preliminary clinical data submitted by the sponsor that a Fast Track or Breakthrough Therapy product may be effective, it may begin review of portions of a BLA before the sponsor submits the complete BLA (rolling review), thereby accelerating the date on which review of a portion of the BLA can begin. There can be no assurance that any of our products will be granted Fast Track or Breakthrough Therapy designation. And even if they are designated as Fast Track or Breakthrough Therapy products, we cannot assure you that our products will be reviewed or approved more expeditiously for their Fast Track or Breakthrough Therapy indications than would otherwise have been the case or will be approved promptly, or at all. Furthermore, the FDA can revoke Fast Track or Breakthrough Therapy designation at any time.

| 14 |

In addition, products studied for their safety and effectiveness in treating serious or life-threatening illnesses and that provide meaningful therapeutic benefit over existing treatments may receive Accelerated Approval and may be approved on the basis of adequate and well-controlled clinical trials establishing that the product has an effect on a surrogate endpoint that is reasonably likely to predict clinical benefit or on the basis of an effect on a clinical endpoint other than survival or irreversible morbidity. As a condition of approval, the FDA may require that a sponsor of a product receiving Accelerated Approval perform adequate and well-controlled post-approval clinical trials to verify and further define the product’s clinical benefit and safety profile. There can be no assurance that any of our products will receive Accelerated Approval. Even if Accelerated Approval is granted, the FDA may withdraw such approval if the sponsor fails to conduct the required post-approval clinical trials, or if the post-approval clinical trials fail to confirm the early benefits seen during the accelerated approval process.

Priority Review Voucher

Fast Track or Breakthrough Therapy designation and Accelerated Approval should be distinguished from Priority Review designation although products awarded Fast Track or Breakthrough Therapy designation may also be eligible for Priority Review designation.

Products regulated by the CBER may receive Priority Review designation if they provide significant improvement in the safety or effectiveness of the treatment, diagnosis, or prevention of a serious or life-threatening disease. The agency has agreed to the performance goal of reviewing products awarded Priority Review designation within six months, whereas products under standard review receive a ten-month target. The review process, however, can be significantly extended by FDA requests for additional information or clarification regarding information already provided in the submission. Priority Review designation is requested at the time the BLA is submitted, and the FDA makes a decision as part of the agency’s review of the application for filing.

Separately, but somewhat related, is a product’s ability to qualify its sponsor to receive a Priority Review Voucher, or PRV. For a product aimed at prevention or treatment of a “rare pediatric disease” as defined by Food, Drug and Cosmetics Act at 21 USC 360ff, and that also meets certain other qualifying attributes, the product’s sponsor may qualify, apply for and receive a PRV, from the FDA. A PRV entitles its holder to Priority Review for a drug application, and the PRV is transferable. Some companies who have received PRV’s have sold their PRV’s to other companies who have then used the PRV to receive Priority Review for a drug application with the FDA. Recent transfers of PRV’s from one company to another have occurred at prices in the $125 – 150 million range. We intend to apply for rare pediatric disease designation for our pediatric esophageal implant product candidate as a first step in pursuit of a PRV. A PRV is earned only upon marketing approval of the product. There is no certainty that our pediatric esophageal product will achieve marketing approval from the FDA, or that if it does, that FDA would award us a PRV. Further, if received, there is no certainty that the value of a PRV at that future date will compare favorably with the values reflected in recent transfers of PRV’s.

| 15 |

Orphan Drug Designations

The Orphan Drug Act provides incentives to manufacturers to develop and market drugs and biologics for rare diseases and conditions affecting fewer than 200,000 persons in the U.S. at the time of application for orphan drug designation.. In September 2014 the FDA granted orphan designation to our HART-Trachea product in the U.S. In November 2016, we were granted Orphan Drug Designation for our Cellspan esophageal implant by the FDA to restore the structure and function of the esophagus subsequent to esophageal damage due to cancer, injury or congenital abnormalities. The first developer to receive FDA marketing approval for an orphan biologic is entitled to a seven-year exclusive marketing period in the U.S. for that product. The marketing exclusivity prevents FDA approval of another application for the same product for the same indication for a period of seven years. Orphan status also entitles the product’s sponsor to certain other benefits, such as a waiver of the BLA user fee, which is currently a $2 million value. Orphan product designation does not convey any advantage in or shorten the duration of the regulatory review and approval process.

International

We plan to seek required regulatory approvals and comply with extensive regulations governing product safety, quality, manufacturing and reimbursement processes in order to market our products in other major foreign markets. The regulation of our products in the Asian and European markets, and in other foreign markets varies significantly from one jurisdiction to another. The classification of the particular products and related approval or CE marking procedures can involve additional product testing and additional administrative review periods. The time required to obtain these foreign approvals or to CE mark our products may be longer or shorter than that required in the U.S., and requirements for approval may differ from the FDA requirements. Regulatory approval in one country does not ensure regulatory approval in another, but a failure or delay in obtaining regulatory approval in one country may negatively impact the regulatory process in others.

Legislation similar to the Orphan Drug Act has been enacted in other jurisdictions, including the EU. The orphan legislation in the EU is available for therapies addressing conditions that affect five or fewer out of 10,000 persons. The marketing exclusivity period is for ten years, although that period can be reduced to six years if, at the end of the fifth year, available evidence establishes that the product is sufficiently profitable not to justify maintenance of market exclusivity.

Employees

At December 31, 2017, we had 5 employees working in our business, of whom 4 were full-time and one was part-time. At that date, all of our employees were based in the U.S. None of our employees are unionized. In general, we consider our relations with our employees to be good.

Competition

We are not aware of any companies whose products are directly competitive with our cell-seeded biocompatible synthetic scaffold system. However, in our key markets we may in the future compete with multiple pharmaceutical, biotechnology, and medical device, including, among others, Aldagen, Asterias Biotherapeutics, Athersys, BioTime, Caladrius Biosciences, Celgene, Cytori Therapeutics, E. I. du Pont de Nemours and Company, InVivo Therapeutics, Mesoblast, Miramatrix Medical, Nanofiber Solutions, Neuralstem, Organovo, Osiris Therapeutics, Pluristem, Smiths Medical, Tissue Genesis, Inc., Tissue Growth Technologies, United Therapeutics, Vericel Corporation and W.L. Gore and Associates. In addition, there are many academic and clinical centers that are developing regenerative technologies that may one day become competitors with us.

Many of our potential competitors have substantially greater financial, technological, research and development, marketing, and personnel resources than we do. We cannot forecast if or when these or other companies may develop competitive products.

| 16 |

We expect that other products will compete with products and potential products based on efficacy, safety, cost, and intellectual property positions. While we believe that these will be the primary competitive factors, other factors include, in certain instances, obtaining marketing exclusivity under the Orphan Drug Act, availability of supply, manufacturing, marketing and sales expertise and capability, and reimbursement coverage.

Executive Officers of the Registrant

The following table shows information about our executive officers as of December 31, 2017.

| Name | Age | Position(s) | ||

| James McGorry | 61 | Chief Executive Officer and Member of the Board of Directors | ||

| Thomas McNaughton | 57 | Chief Financial Officer |

James McGorry - Chief Executive Officer and Director

Mr. McGorry has served as our President and Chief Executive Officer (CEO) since July 6, 2015. He has served as a Member of our Board of Directors since February 2013. Mr. McGorry has more than 30 years of experience as a life science business leader in biologics, personalized medicine and medical devices, including multiple product launches. Prior to becoming President and CEO at Biostage, Mr. McGorry most recently served as Executive Vice President and General Manager, Translational Oncology Solutions for Champions Oncology and previously was Executive Vice President of Commercial Operations at Accellent. During a 12-year tenure at Genzyme, he held leadership positions across several therapeutic areas, including Bio Surgery, Cardiac Surgery, Oncology and Transplant. Mr. McGorry also was President of Clineffect Systems, an electronic medical records company. He began his life sciences career with Baxter Healthcare Corporation, where he spent 11 years in positions of increasing responsibility. Mr. McGorry also served as an officer in the United States Army for six years, including commanding a special operations Green Beret SCUBA detachment. Mr. McGorry has an MBA with a concentration in healthcare from Duke University, Fuqua School of Business, and a B.S. in engineering from the United States Military Academy at West Point where he was the president of his class. We believe Mr. McGorry’s qualifications to sit on our Board of Directors include his extensive executive leadership positions at several biotechnology and healthcare companies over the past 25 years.

Thomas McNaughton - Chief Financial Officer

Mr. McNaughton has served as our Chief Financial Officer since May 3, 2012. Mr. McNaughton joined Harvard Bioscience as its Chief Financial Officer in September 2008, and served in that role until the spin-off of our company from Harvard Bioscience on November 1, 2013. During 2008 and prior to joining Harvard Bioscience, Mr. McNaughton was a consultant providing services primarily to an angel-investing group and a silicon manufacturing start-up. From 2005 to 2007, he served as Vice President of Finance and Chief Financial Officer for Tivoli Audio, LLC, a venture capital-backed global manufacturer of premium audio systems. From 1990 to 2005, Mr. McNaughton served in various managerial positions in the areas of financial reporting, treasury, investor relations, and acquisitions within Cabot Corporation, a global manufacturer of fine particulate products, and served from 2002 to 2005 as Finance Director, Chief Financial Officer of Cabot Supermetals, a $350 million Cabot division that provided high purity tantalum and niobium products to the electronics and semiconductor industries. Mr. McNaughton practiced from 1982 to 1990 as a Certified Public Accountant in the audit services group of Deloitte & Touche, LLP. He holds a B.S. in accounting and finance with distinction from Babson College.

Available Information and Website

Our website address is www.biostage.com. Our Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and exhibits and amendments to those reports filed or furnished with the Securities and Exchange Commission pursuant to Section 13(a) of the Exchange Act are available for review on our website and the Securities and Exchange Commission’s (“SEC”) website at www.sec.gov. Any such materials that we file with, or furnish to, the SEC in the future will be available on our website as soon as reasonably practicable after they are electronically filed with, or furnished to, the SEC. The information on our website is not incorporated by reference into this Annual Report on Form 10-K.

| 17 |

| Item 1A. | Risk Factors. |

The following factors should be reviewed carefully, in conjunction with the other information contained in this Annual Report on Form 10-K. As previously discussed, our actual results could differ materially from our forward-looking statements. Our business faces a variety of risks. We describe below what we believe are currently the material risks and uncertainties we face, but they are not the only risks and uncertainties we face. Additional risks and uncertainties of which we are unaware, or that we currently believe are not material, may also become important factors that adversely affect our business. In addition, past financial performance may not be a reliable indicator of future performance and historical trends should not be used to anticipate results or trends in future periods. If any of the following risks and uncertainties develops into actual events, these events could have a material adverse effect on our business, financial condition or results of operations. In such case, the trading price of our common stock could decline, and you may lose all or part of your investment in our securities. The risk factors generally have been separated into three groups: (i) risks relating to our business, (ii) risks relating to the Separation and (iii) risks relating to our common stock. These risk factors should be read in conjunction with the other information in this Annual Report on Form 10-K.

Risks Relating To Our Business

Risks Associated with Clinical Trials and Pre-Clinical Development

The results of our clinical trials or pre-clinical development efforts may not support our product claims or may result in the discovery of adverse side effects.

Even if our pre-clinical development efforts or clinical trials are completed as planned, we cannot be certain that their results will support our product claims or that the FDA, foreign regulatory authorities or notified bodies will agree with our conclusions regarding them. Although we have obtained some positive results from the use of our scaffolds and bioreactors for trachea transplants performed to date, we also discovered that our first-generation trachea product design encountered certain body response issues that we have sought to resolve with our ongoing development of our Cellframe implant design. We cannot be certain that our Cellframe implant design or any future modifications or improvements with respect thereto will support our claims, and any such developments may result in the discovery of further adverse side effects. We also may not see positive results when our products undergo clinical testing in humans in the future. Success in pre-clinical studies and early clinical trials does not ensure that later clinical trials will be successful, and we cannot be sure that the later trials will replicate the results of prior trials and pre-clinical studies. Our pre-clinical development efforts and any clinical trial process may fail to demonstrate that our products are safe and effective for the proposed indicated uses, which could cause us to abandon a product and may delay development of others. Also, patients receiving surgeries using our products under compassionate use or in clinical trials may experience significant adverse events following the surgeries, including serious health complications or death, which may or may not be related to materials provided by us. Our current Cellframe technology has never been used in humans. We provided a previous generation trachea implant that was used in human patients under compassionate use. To date, we believe that at least four of the six patients who received that first-generation implant have died. While we believe that none of them have died because of a failure of the first-generation implant, these and any other such adverse events have and may cause or contribute to the delay or termination of our clinical trials or pre-clinical development efforts. Any delay or termination of our pre-clinical development efforts or clinical trials will delay the filing of our product submissions and, ultimately, our ability to commercialize our products and generate revenues. It is also possible that patients enrolled in clinical trials will experience adverse side effects that are not currently part of the product’s profile.

Clinical trials necessary to support a biological product license or other marketing authorization for our products will be expensive and will require the enrollment of sufficient patients to adequately demonstrate safety and efficacy for the product’s target populations. Suitable patients may be difficult to identify and recruit. Delays or failures in our clinical trials will prevent us from commercializing any products and will adversely affect our business, operating results and prospects.