| Exhibit 99.1

|

Exhibit 99.1

ANALYST FIELD TRIP

June 23-24

GERMANY

|

|

Introduction

Paul BLALOCK

|

|

Forward-looking statements

Certain statements contained in this press release may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. This press release may contain “forward-looking statements” with respect to our business, results of operations and financial condition, and our expectations or beliefs concerning future events and conditions. You can identify certain forward-looking statements because they contain words such as, but not limited to, “believes”, “expects”, “may”, “should”, “approximately”, “anticipates”, “estimates”, “intends”, “plans”, “targets”, “likely”, “will”, “would”, “could”, and similar expressions (or the negative of these terminologies or expressions). All forward-looking statements involve risks and uncertainties. Many risks and uncertainties are inherent in our industry and markets. Others are more specific to our business and operations. These risks and uncertainties include, but are not limited to, those set forth under the heading “Risk Factors” in our Annual Report on Form 20-F, and described from time to time in subsequent reports, filed with the U.S. Securities and Exchange Commission, and include risks relating to the finalization of our U.S. Body-in-White joint venture, including the failure to receive required regulatory approvals. The occurrence of the events described and the achievement of the expected results depend on many events, some or all of which are not predictable or within our control. Consequently, actual results may differ materially from the forward-looking statements contained in this press release. We undertake no obligation to publicly update or revise any forward-looking statements as a result of new information, future events or otherwise, expects as required by law.

3

|

|

Non-GAAP measures

This presentation includes information regarding certain non-GAAP financial measures, including, Adjusted EBITDA, Adjusted EBITA per metric ton, Adjusted Free Cash Flow and Net Debt. These measures are presented because management uses this information to monitor and evaluate financial results and trends and believes this information to also be useful for investors. Adjusted EBITDA measures are frequently used by securities analysts, investors and other interested parties in their evaluation of Constellium and in comparison to other companies, many of which present an adjusted EBITDA-related performance measure when reporting their results. Adjusted EBITDA, Adjusted EBITDA per Metric Ton, Adjusted Free Cash Flow and Net Debt are not presentations made in accordance with IFRS and may not be comparable to similarly titled measures of other companies. These non-GAAP financial measures supplement our IFRS disclosures and should not be considered an alternative to the IFRS measures. This presentation provides a reconciliation of non-GAAP financial measures to the most directly comparable GAAP financial measures.

4

|

|

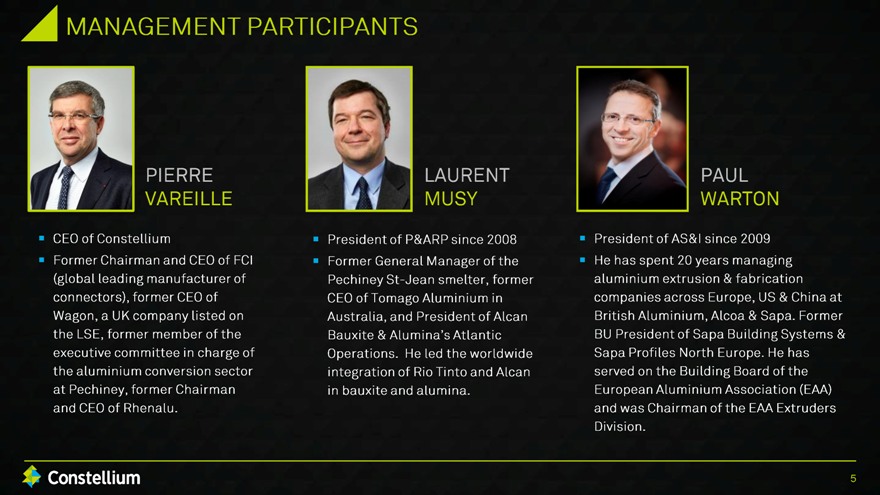

MANAGEMENT PARTICIPANTS

PIERRE VAREILLE

LAURENT MUSY

PAUL WARTON

CEO of Constellium

Former Chairman and CEO of FCI (global leading manufacturer of connectors), former CEO of Wagon, a UK company listed on the LSE, former member of the executive committee in charge of the aluminium conversion sector at Pechiney, former Chairman and CEO of Rhenalu.

President of P&ARP since 2008

Former General Manager of the Pechiney St-Jean smelter, former CEO of Tomago Aluminium in Australia, and President of Alcan Bauxite & Alumina’s Atlantic Operations. He led the worldwide integration of Rio Tinto and Alcan in bauxite and alumina.

President of AS&I since 2009

He has spent 20 years managing aluminium extrusion & fabrication companies across Europe, US & China at British Aluminium, Alcoa & Sapa. Former BU President of Sapa Building Systems & Sapa Profiles North Europe. He has served on the Building Board of the European Aluminium Association (EAA) and was Chairman of the EAA Extruders Division.

5

|

|

AUTOMOTIVE FOCUS

Robust & Global Growth

Pierre VAREILLE Chief Executive Officer

|

|

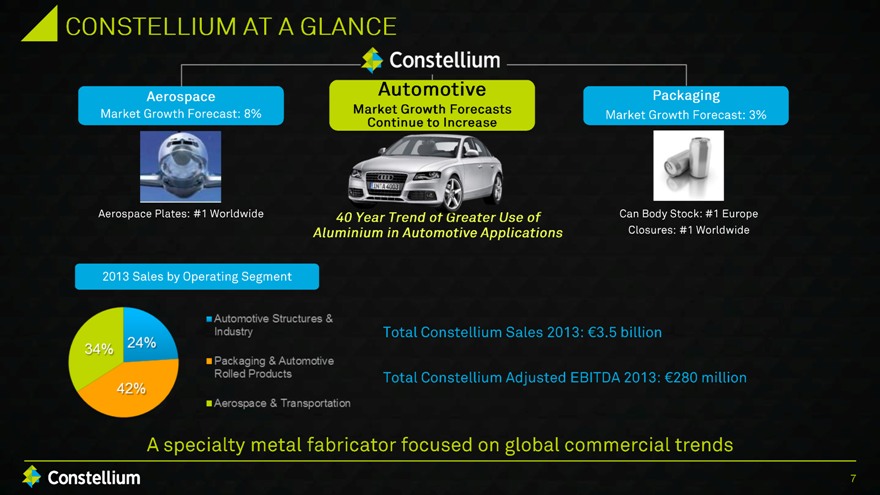

CONSTELLIUM AT A GLANCE

Aerospace Market Growth Forecast: 8% Aerospace Plates: #1 Worldwide

Automotive Market Growth Forecasts Continue to Increase 40 Year Trend of Greater Use of Aluminium in Automotive Applications

Packaging Market Growth Forecast: 3% Can Body Stock: #1 Europe Closures: #1 Worldwide

2013 Sales by Operating Segment

34% 24% 42%

Automotive Structures & Industry

Packaging & Automotive Rolled Products

Aerospace & Transportation

Total Constellium Sales 2013: €3.5 billion

Total Constellium Adjusted EBITDA 2013: €280 million

A specialty metal fabricator focused on global commercial trends

7

|

|

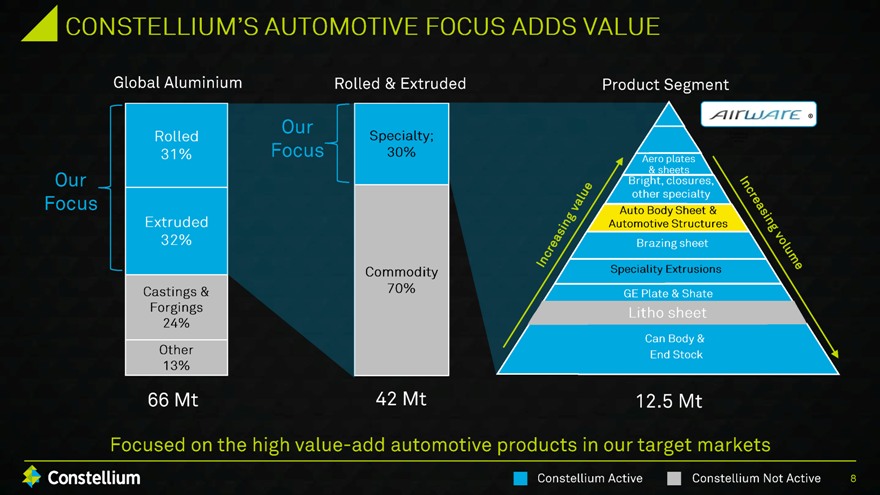

CONSTELLIUM’S AUTOMOTIVE FOCUS ADDS VALUE

Our Focus

Global Aluminium

Rolled 31% Extruded 32% Castings & Forgings 24% Other 13% 66 Mt

Rolled & Extruded

Our Focus

Specialty; 30% Commodity: 70% 42 Mt

Product Segment

Increasing Value

Aero plates & sheets Bright, closures, other specialty Auto Body Sheet & Automotive Structures Brazing sheet Speciality Extrusions GE Plate & Shate Litho sheet Can Body & End Stock 12.5 Mt Increasing Volume

Focused on the high value-add automotive products in our target markets

Constellium Active Constellium Not Active

8

|

|

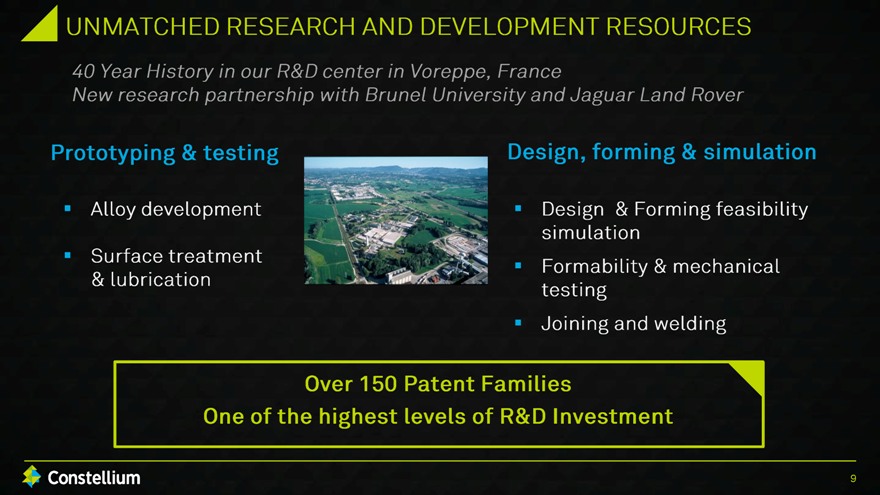

UNMATCHED RESEARCH AND DEVELOPMENT RESOURCES

40 Year History in our R&D center in Voreppe, France New research partnership with Brunel University and Jaguar Land Rover

Prototyping & testing

Alloy development Surface treatment & lubrication

Design, forming & simulation

Design & Forming feasibility simulation Formability & mechanical testing Joining and welding

Over 150 Patent Families One of the highest levels of R&D Investment

9

|

|

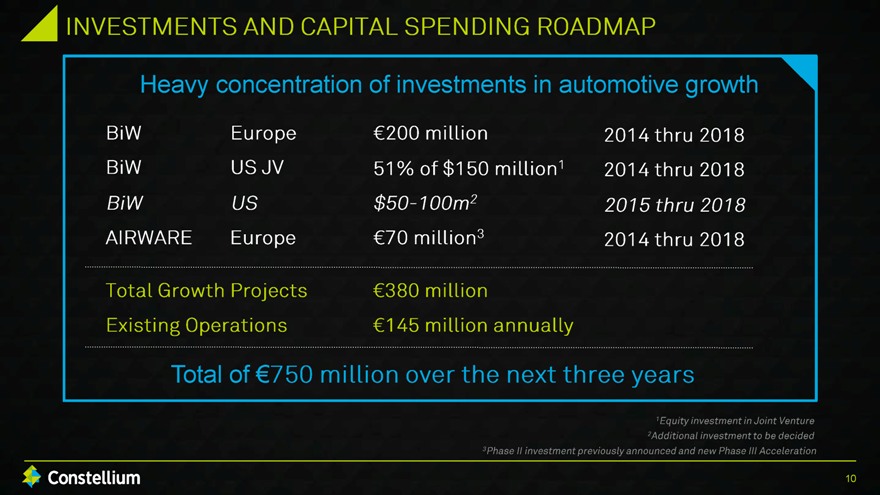

INVESTMENT AND CAPITAL SPENDING ROADMAP

Heavy concentration of investments in automotive growth

BiW Europe €200 million 2014 thru 2018

BiW US JV 51% of $150 million1 2014 thru 2018

BiW US $50-100m2 2015 thru 2018

AIRWARE Europe €70 million3 2014 thru 2018

Total Growth Projects €380 million

Existing Operations €145 million annually

Total of €750 million over the next three years

1 Equity investment in Joint Venture

2 Additional investment to be decided

3 Phase II investment previously announced and new Phase III Accelearation

10

|

|

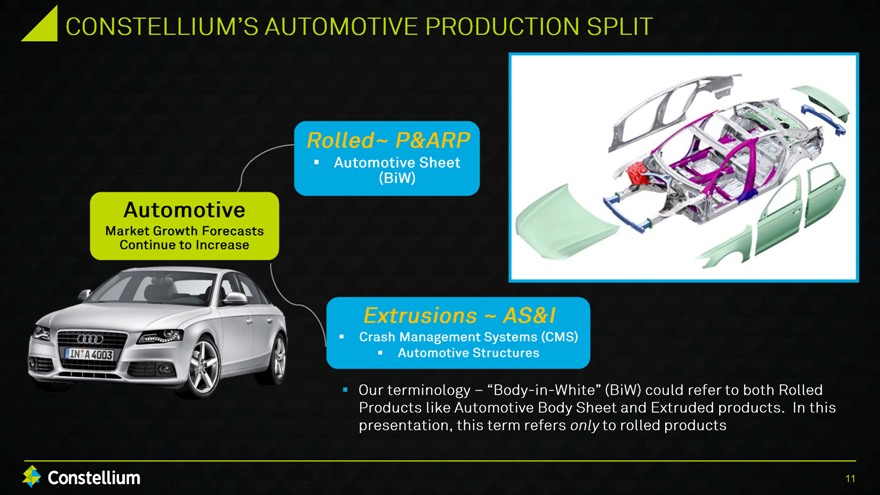

CONSTELLIUM’S AUTOMOTIVE PRODUCTION SPLIT

Rolled – P&ARP

Automotive Sheet

(BiW)

Automotive

Market Growth Forecasts

Continue to Increase

Extrusions – AS&I

Crash Management Systems (CMS)

Automotive Structures

Our terminology – “Body-in-White” (BiW) could refer to both Rolled

Products like Automotive Body Sheet and Extruded products. In this

Presentation, this term refers only to rolled products

11

|

|

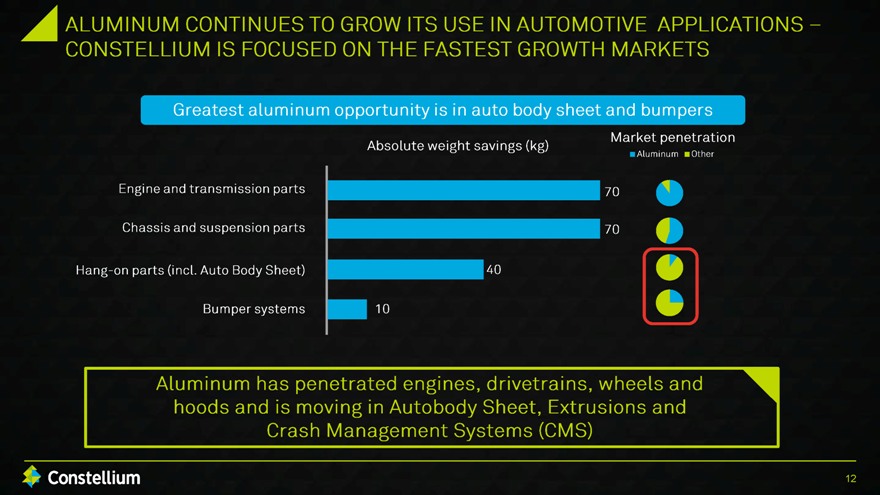

ALUMINUM CONTINUES TO GROW ITS USE IN AUTOMOTIVE APPLICATIONS – CONSTELLIUM IS FOCUSED ON THE FASTEST GROWTH MARKETS

Greatest aluminum opportunity is in auto body sheet and bumpers

Absolute weight savings (kg)

Market penetration

Aluminum Other

Engine and transmission parts

Chassis and suspension parts

Hang-on parts (incl. Auto Body Sheet)

Bumper systems

70

70

40

10

Aluminum has penetrated engines, drivetrains, wheels and hoods and is moving in Autobody Sheets, Extrusions and Crash Management Systems (CMS)

12

|

|

AUTOMOTIVE APPLICATIONS CONTINUING TO INCREASE ALUMINUM CONSUMPTION

The consumption of aluminum in automotive applications has consistently increased for the last 40 years!

2015 through 2025 will reach an explosive period of new growth in body parts, doors and closures

Global light vehicle aluminum content is projected to increase 2X to 4X per vehicle over the next decade

In North America alone, the demand for aluminum sheet is projected to grow 20X over the next decade (from 200 million pounds in 2013 to nearly 4 billion pounds in 2025)

Research performed by Ducker Worldwide on behalf of the Aluminum Association (U.S.)

13

|

|

AUTOMOTIVE FOCUS

Laurent MUSY

President, Packaging & Automotive Rolled Products

|

|

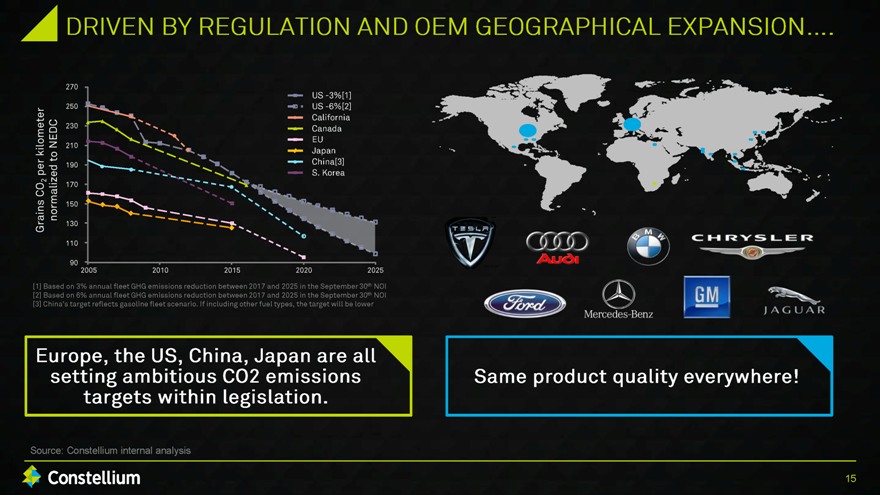

DRIVEN BY REGULATION AND OEM GEOGRAPHICAL EXPANSION….

Grains CO2 per kilometer normalized to NEDC

US-3%[1]

US-6%[2]

California

Canada

EU

Japan

China[3]

S. Korea

270

250

230

210

190

170

150

130

110

90

2005

2010

2015

2020

2025

[1] Based on 3% annual fleet GHG emissions reduction between 2017 and 2025 in the September 30th NOI

[2] Based on 6% annual fleet GHG emissions reduction between 2017 and 2025 in the September 30th NOI

[3] China’s target reflects gasoline fleet scenario. If including other fuel types, the target will be lower

Same product quality everywhere!

Source: Constellium internal analysis

Europe, the US, China, Japan are all setting ambitious CO2 emissions targets within legislation.

15

|

|

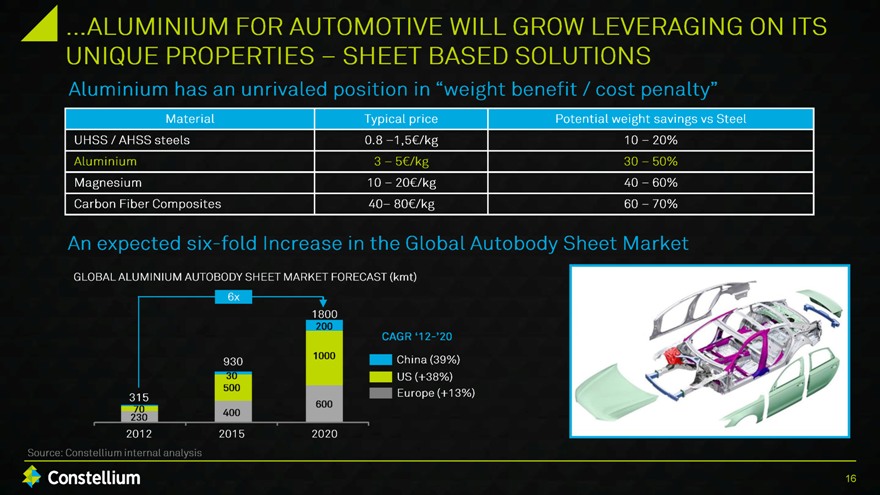

ALUMINIUM FOR AUTOMOTIVE WILL GROW LEVERAGING ON ITS UNIQUE PROPERTIES – SHEET BASED SOLUTIONS

Aluminium has an unrivaled position in “weight benefit / cost penalty”

Material Typical price Potential weight savings vs Steel

UHSS / AHSS steels 0.8 – 1, 5€/kg 10 – 20%

Aluminium 3 – 5€/kg 30 – 50%

Magnesium 10 – 20€/kg 40 – 60%

Carbon Fiber Composites 40 – 80€/kg 60 – 70%

An expected six-fold Increase in the Global Autobody Sheet Market

GLOBAL ALUMINIUM AUTOBODY SHEET MARKET FORECAST (kmt)

6x

315

70

230

930

30

500

400

1800

200

1000

600

CAGR ‘12-’20

China (39%)

US (+38%)

Europe(+13%)

2012

2015

2020

Source: Constellium internal analysis 16

|

|

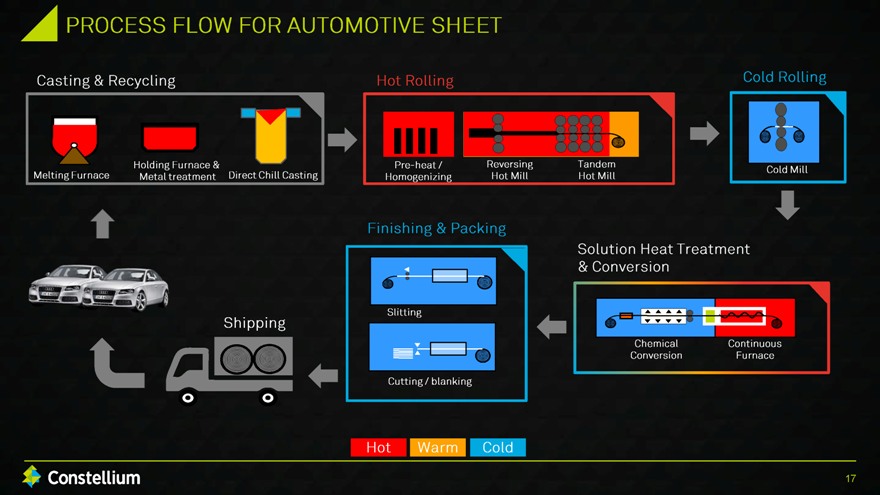

PROCESS FLOW FOR AUTOMOTIVE SHEET

Casting & Recycling

Melting Furnace Holding Furnace & Metal treatment Direct Chill Casting

Hot Rolling

Pre-heat / Homogenizing Reversing Hot Mill Tandem Hot Mill

Cold Rolling

Cold Mill

Shipping

Finishing & Packing

Slitting

Cutting / blanking

Solution Heat Treatment & Conversion

Chemical Conversion Continuous Furnace

Hot Warm Cold

17

|

|

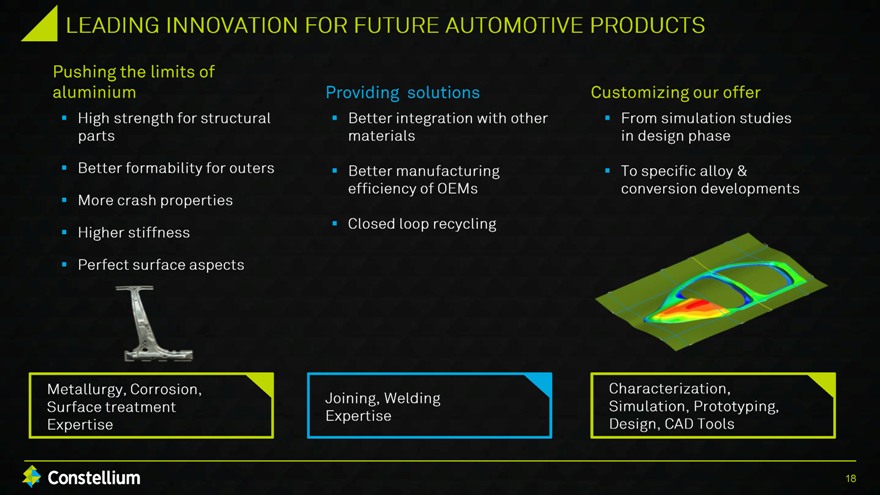

LEADING INNOVATION FOR FUTURE AUTOMOTIVE PRODUCTS

Pushing the limits of aluminium

High strength for structural parts

Better formability for outers

More crash properties

Higher stiffness

Perfect surface aspects

Providing solutions

Better integration with other materials

Better manufacturing efficiency of OEMs

Closed loop recycling

Customizing our offer

From simulation studies in design phase

To specific alloy & conversion developments

Metallurgy, Corrosion, Surface treatment Expertise

Joining, Welding Expertise

Characterization, Simulation, Prototyping, Design, CAD Tools

18

|

|

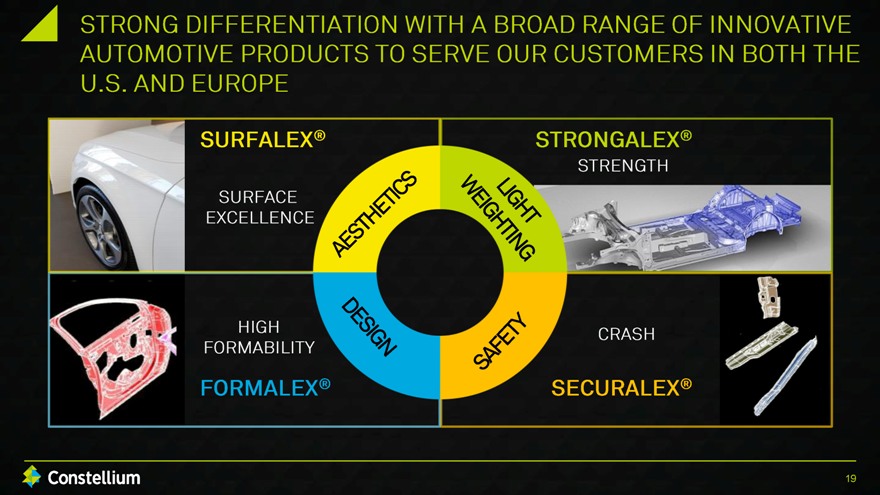

STRONG DIFFERENTIATION WITH A BROAD RANGE OF INNOVATIVE AUTOMOTIVE PRODUCTS TO SERVE OUR CUSTOMERS IN BOTH THE U.S. AND EUROPE

SURFALEX® SURFACE EXCELLENCE

STRONGALEX® STRENGTH

HIGH FORMABILITY FORMALEX®

CRASH SECURALEX®

AESTHETICS

LIGHT WEIGHTING

DESIGN

SAFETY

19

|

|

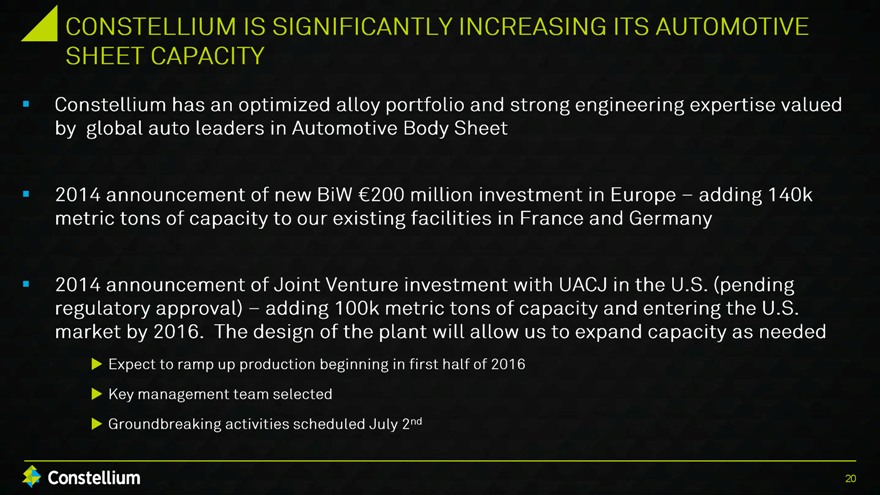

CONSTELLIUM IS SIGNIFICANTLY INCREASING ITS AUTOMOTIVE SHEET CAPACITY

Constellium has an optimized alloy portfolio and strong engineering expertise valued by global auto leaders in Automotive Body Sheet

2014 announcement of new BiW €200 million investment in Europe – adding 140k metric tons of capacity to our existing facilities in France and Germany

2014 announcement of Joint Venture investment with UACJ in the U.S. (pending regulatory approval) – adding 100k metric tons of capacity and entering the U.S. market by 2016. The design of the plant will allow us to expand capacity as needed

Expect to ramp up production beginning in first half of 2016

Key management team selected

Groundbreaking activities scheduled July 2nd

20

|

|

A GLOBAL LEADER IN AUTOMOTIVE SHEET – Key Takeaways

Long term “lightweighting” trend in the global automotive industry driven by regulation

Initial lightweighting allows indirect additional lightweighting and cost saving by OEMs

Cars in the future will be multi-material. Aluminium will be the material of choice for closure parts and gain market share in body structures, especially but not excluding large and premium automobile

Aluminium continues to advance into more auto models and parts per vehicle

Leveraging our world-class R&D and technical capabilities and alloys to partner with OEMs to meet local needs and meet sustainability objectives

Significantly expanding our capacity in BiW in Europe by 2016

Joint Venture with UACJ in the U.S. building finishing capacity in Bowling Green, Kentucky

Industry capacity will likely drive the pace of meeting strong long term demand

21

|

|

AUTOMOTIVE FOCUS

Paul WARTON

President, Automotive Structures & Industry

|

|

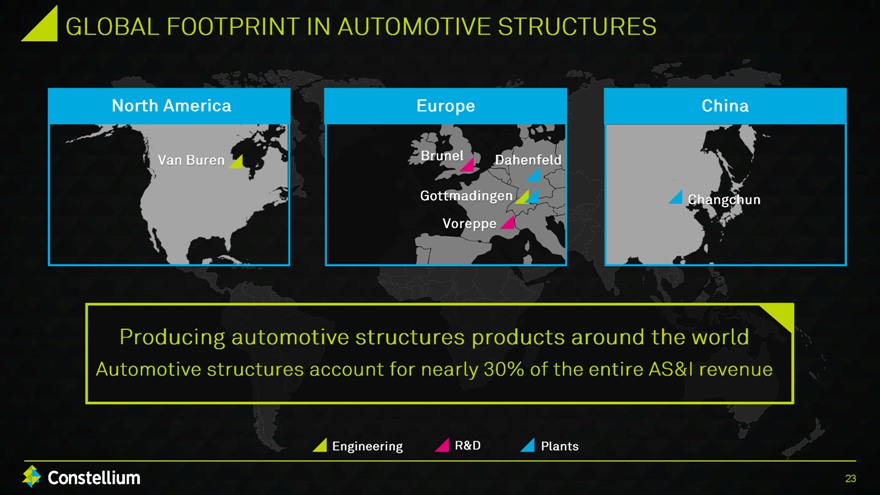

GLOBAL FOOTPRINT IN AUTOMOTIVE STRUCTURES

North America

Van Buren

Europe

Brunel Dahenfeld Gottmadingen Voreppe

China

Changchun

Producing automotive structures products around the world

Automotive structures account for nearly 30% of the entire AS&I revenue

Engineering R&D Plants

23

|

|

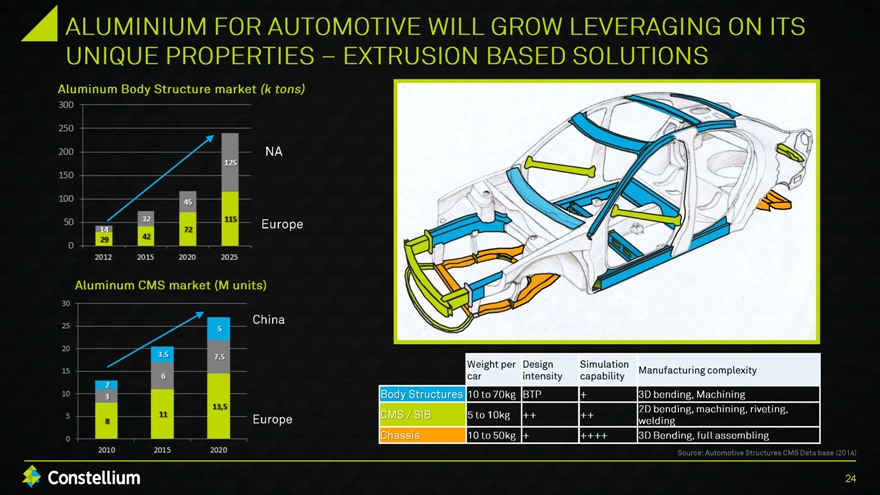

ALUMINIUM FOR AUTOMOTIVE WILL GROW LEVERAGING ON ITS UNIQUE PROPERTIES – EXTRUSION BASED SOLUTIONS

Aluminum Body Structure market (k tons)

300 250 200 150 100 50 0

2012 2015 2020 2025

29 42 72 115

14 32 45 125

NA

Europe

Aluminum CMS market (M units)

30 25 20 15 10 5 0

2010 2015 2020

8 11 13,5

2 3 3.5 6 5 7.5

China

Europe

Weight per car Design intensity Simulation capability Manufacturing complexity

Body Structures 10 to 70kg BTP + 3D bending, Machining

CMS / SIB 5 to 10kg ++ ++ 2D bending, machining, riveting, welding

Chassis 10 to 50kg + ++++ 3D Bending, full assembling

Source: Automotive Structures CMS Data base (2014)

24

|

|

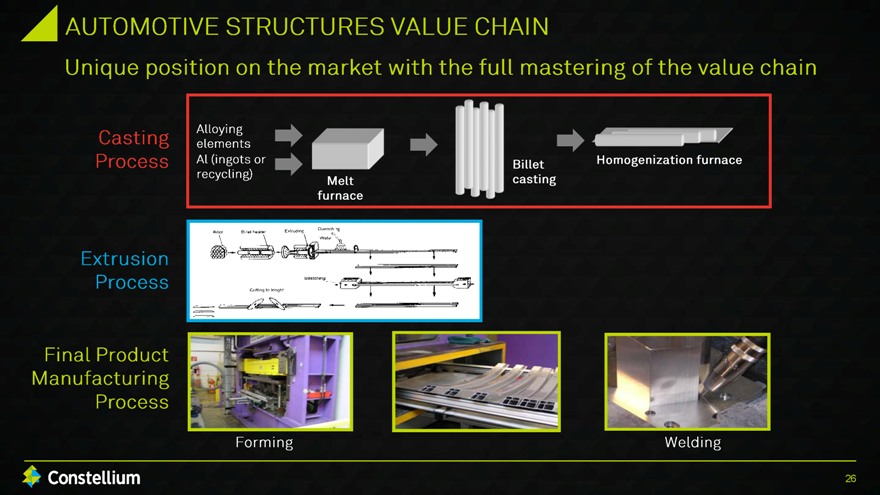

AUTOMOTIVE STRUCTURES VALUE CHAIN

Unique position on the market with the full mastering of the value chain

Casting Process Alloying elements Al (ingots or recycling) Melt furnace Billet casting Homogenization furnace

Extrusion Process Final Product Manufacturing Process Forming Welding

26

|

|

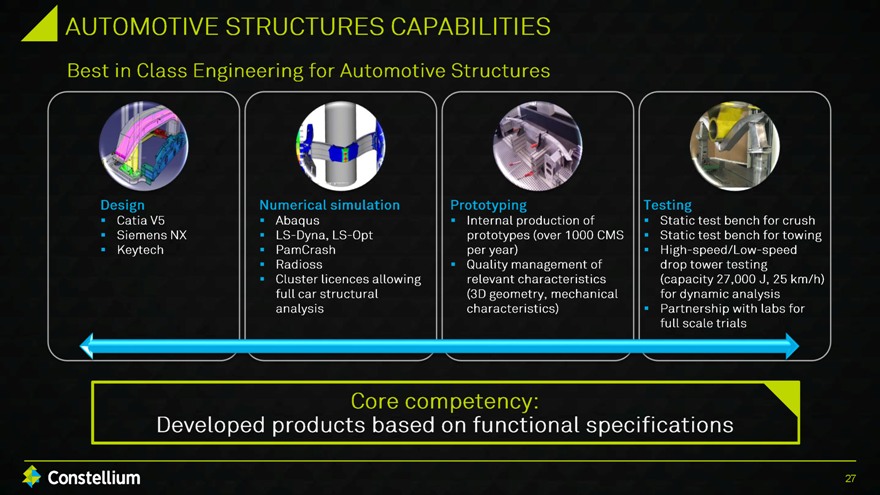

AUTOMOTIVE STRUCTURES CAPABILITIES

Best in Class Engineering for Automotive Structures

Design Catia V5 Siemens NX Keytech Numerical simulation Abaqus LS-Dyna, LS-Opt PamCrash Radioss Cluster licences allowing full car structural analysis

Prototyping Internal production of prototypes (over 1000 CMS per year) Quality management of relevant characteristics (3D geometry, mechanical characteristics)

Testing Static test bench for crush Static test bench for towing High-speed/Low-speed drop tower testing (capacity 27,000 J, 25 km/h)for dynamic analysis Partnership with labs for full scale trials

Core competency: Developed products based on functional specifications

27

|

|

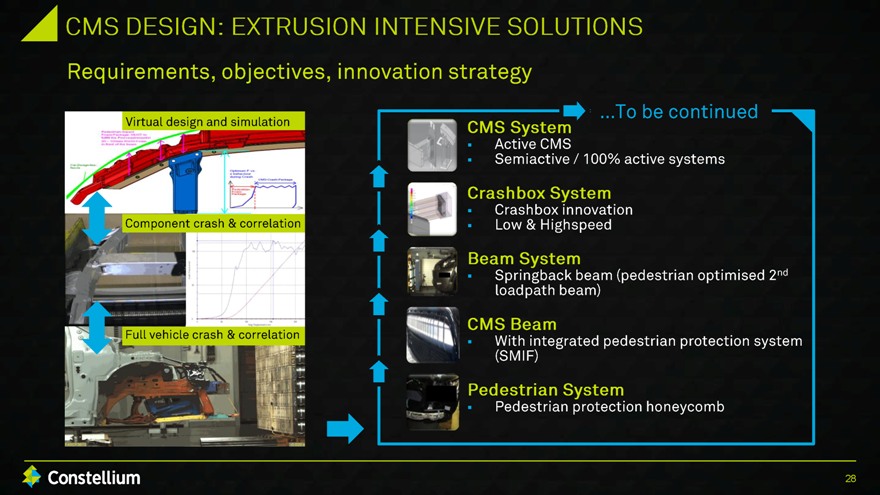

CMS DESIGN: EXTRUSION INTENSIVE SOLUTIONS

Requirements, objectives, innovation strategy

Virtual design and simulation Component crash & correlation Full vehicle crash & correlation

…To be continued

CMS System Active CMS Semiactive / 100% active systems

Crashbox System Crashbox innovation Low & Highspeed

Beam System Springback beam (pedestrian optimised 2nd loadpath beam

CMS Beam With integrated pedestrian protection system (SMIF)

Pedestrian System Pedestrian protection honeycomb

28

|

|

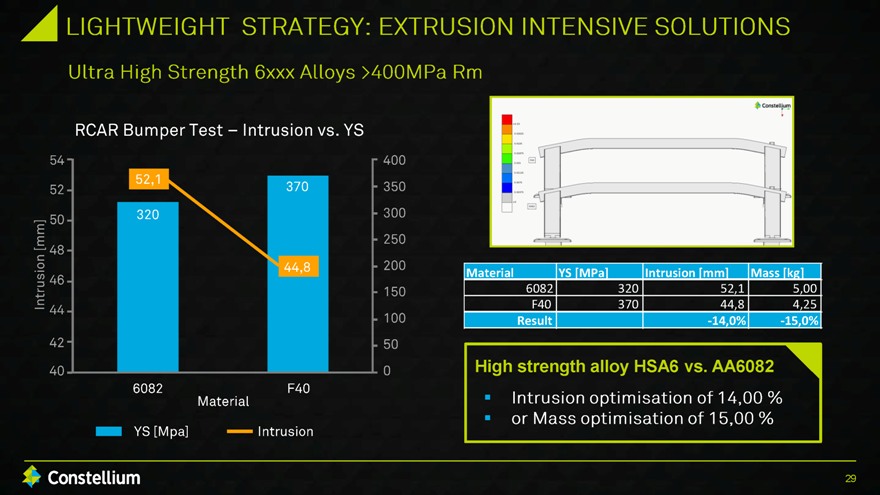

LIGHTWEIGHT STRATEGY: EXTRUSION INTENSIVE SOLUTIONS

Ultra High Strength 6xxx Alloys >400MPa Rm

RCAR Bumper Test – Intrusion vs. YS

54 52 50 48 46 44 42 40

6082 F40

400 350 300 250 200 150 100 50 0

52,1 320 370 44,8

Material YS[Mpa] Intrusion

Material YS [MPa] Intrusion [mm] Mass [kg]

6082 320 52,1 5,00

F40 370 44,8 4,25

Result -14,0% -15,0%

High strength alloy HSA6 vs. AA6082

Intrusion optimisation of14,00%

or Mass optimisation of 15,00%

29

|

|

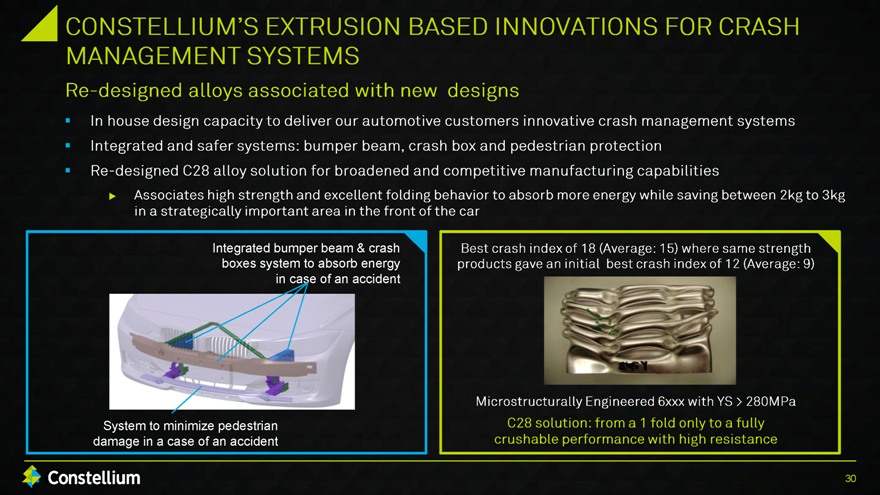

CONSTELLIUNM’S EXTRUSION BASED INNOVATIONS FOR CASH MANAGEMENT SYSTEMS

Re-designed alloys associated with new designs

In house design capacity to deliver our automotive customers innovative crash management systems

Integrated and safer systems: bumper beam, crash box and pedestrian protection

Re-designed C28 alloy solution for broadened and competitive manufacturing capabilities

Associates high strength and excellent folding behavior to absorb more energy while saving between 2kg to 3kg in a strategically important area in the front of the car

Integrated bumper beam & crash boxes system to absorb energy in case of an accident

Best Crash index of 18 (Average:15) where same strength products gave an initial best crash index of 12 (Average:9)

System to minimize pedestrian damage in a case of an accident

Microstructurally Engineered 6xxx with YS>280MPa

C28 solution: from a 1 fold only to fully crushable performance with high resistance

30

|

|

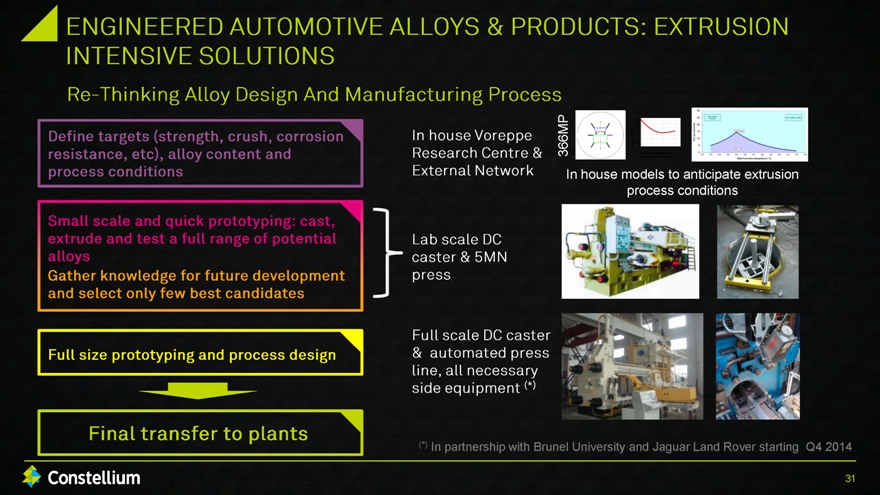

ENGINEERED AUTOMOTIVE ALLOYS & PRODUCTS: EXTRUSION INTENSIVE SOLUTIONS

Re-Thinking Alloy Design And Manufacturing Process

Define targets (Strength, crush, corrosion resistance, etc), alloy content and process conditions

Small scale and quick prototyping: cast, extrude and test a full range of potential alloys Gather knowledge for future development and select only few best candidates

Full size prototyping and process design

Final transfer to plants

366MP

In house Voreppe Research Centre & External Network

In house models to anticipate extrusion process conditions

Lab scale DC caster & 5MN press

Full scale DC caster & automated press line, all necessary side equipment (*)

(*) In partnership with Brunel University and Jaguar Land Rover starting Q4 2014

31

|

|

CONSTELLIUM IS INCREASING ITS EXTRUSION BASED AUTOMOTIVE CAPACITY

Finishing capacity across 3 continents (China, U.S. and Europe)

Strong long term customer relationships with leading OEMs

Development partner to certain OEMs in producing and manufacturing the designed solutions

2013 Automotive Extrusion production of 70kmt

Adding 10,000 metric ton expansion in Decin, Czech Republic

32

|

|

AUTOMOTIVE STRUCTURES OPPORTUNITY – KEY TAKEAWAYS

Long term high growth opportunities in Auto Body Structures, Crash Management Systems and Chassis from global OEMs

Unique global footprint with plants in Asia, Europe and the U.S.

Strong competencies in high strength alloys designed to meet customer needs

A very compelling Automotive Structures Business Model

Constellium

33

|

|

Conclusion

Pierre VAREILLE

|

|

CONSTELLIUM’S AUTOMOTIVE FOCUS WILL DRIVE A DECADE OF LONG TERM GROWTH – KEY TAKEWAYS

Long term relationships with global “blue chip” automotive customers

Unmatched portfolio of alloys along with technical research and capabilities

Global manufacturing footprint

Strong sustainability and recycling capabilities

Project economics accretive to segment financials

Targeting high growth projects in automotive applications

Constellium is uniquely positioned to be a top global supplier of automotive products

35

|

|

Questions & Answers

|

|

ANALYST

FIELD TRIP

June 23-24 GERMANY

|

|

Appendix

|

|

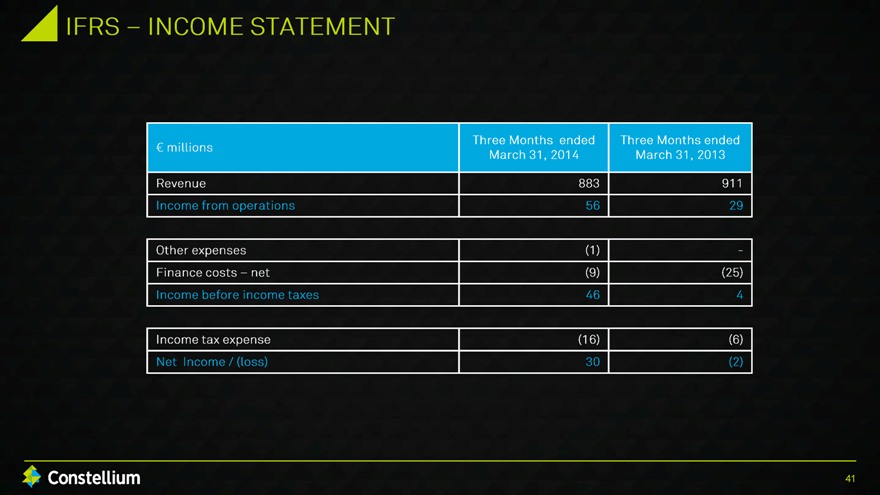

IFRS – INCOME STATEMENT

€ millions

Three Months ended March 31, 2014

Three Months ended March 31, 2013

Revenue 883 911

Income from operations 56 29

Other expenses (1) –

Finance costs- net (9) (25)

Income before income taxes 46 4

Income tax expense (16) (6)

Net Income/(loss) 30 (2)

41

|

|

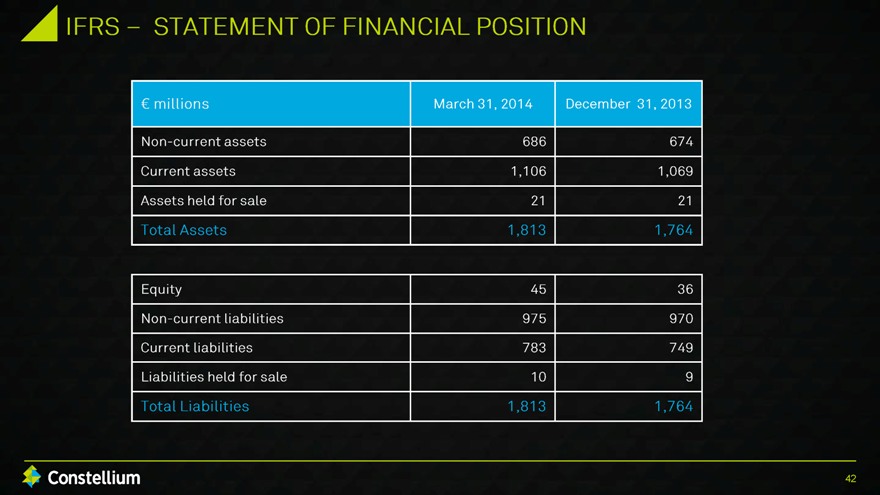

IFRS –STATEMENT OF FINANCIAL POSITION

€ millions

March 31, 2014 December 31, 2013

Non-current assets 686 674

Current assets 1,106 1,069

Assets held for sale 21 21

Total Assets 1,813 1,764

Equity 45 36

Non-current liabilities 975,970

Current liabilities 783 749

Liabilities held for sale 10 9

Total Liabilities 1,813 1,764

42

|

|

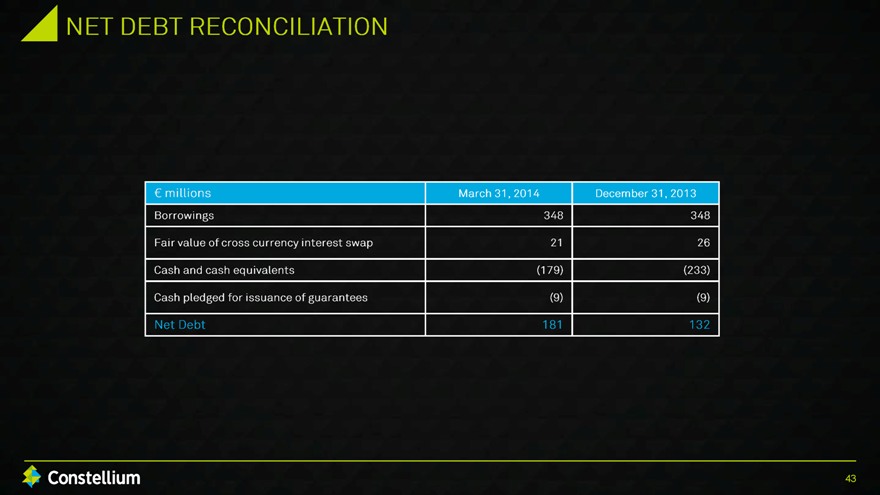

NET DEBT RECONCILIATION

€ millions

March 31, 2014 December 31, 2013

Borrowings 348 348 Fair value of cross currency interest swap 21 26

Cash and cash equivalents (179) (233)

Cash pledged for issuance of guarantees (9) (9)

Net Debt 181 132

43

|

|

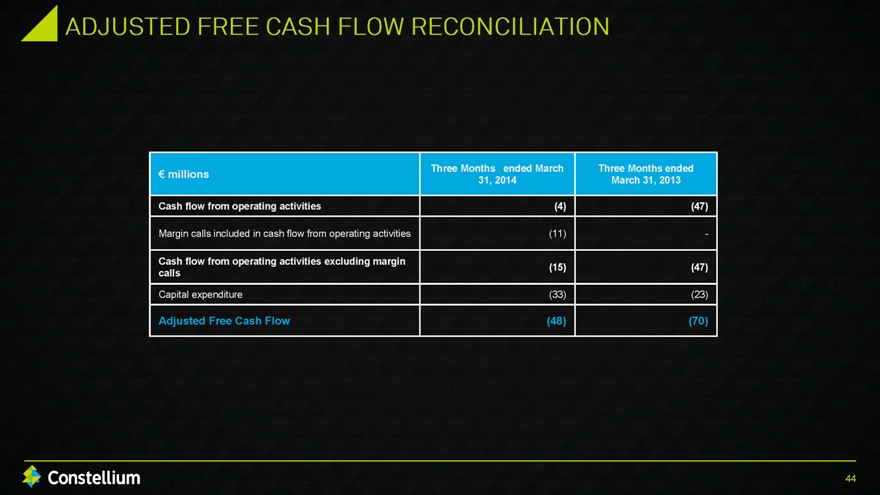

ADJUSTED FREE CASH FLOW RECONCILIATION

€ millions

Three Months ended March 31, 2014

Three Months ended March 31, 2013

Cash flow from operating activities (4) (47)

Margin calls included in cash flow from operating activities (11) -

Cash flow from operating activities excluding margin calls (15) (47)

Capital expenditure (33) (23)

Adjusted Free Cash Flow (48) (70)

44

|

|

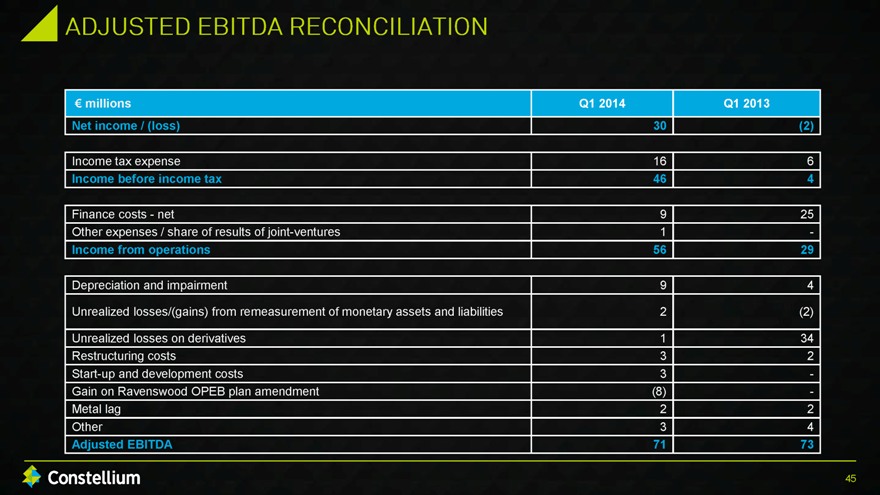

ADJUSTED EBITDA RECONCILIATION

€ millions Q1 2014 Q1 2013

Net income / (loss)30 (2)

Income tax expense 16 6

Income before income tax 46 4

Finance costs - net 9 25

Other expenses / share of results of joint-ventures 1-

Income from operations 56 29

Depreciation and impairment 9 4

Unrealized losses/(gains) from remeasurement of monetary assets and liabilities 2 (2)

Unrealized losses on derivatives 1 34

Restructuring costs3 2

Start-up and development costs 3 -

Gain on Ravenswood OPEB plan amendment (8) -

Metal lag 2 2

Other 3 4

Adjusted EBITDA 71 73

45

|

|

ANALYST

FIELD TRIP

June 23-24 GERMANY