UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

for the fiscal year ended

For the transition period from: _____________ to _____________

Commission file number:

(Exact Name of Registrant as Specified in Its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

(Address of Principal Executive Offices, including Zip Code)

Tel No.:

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| None | None | None |

Securities registered pursuant to Section 12(g) of the Act:

| (Title of class) |

Indicate by check mark if the registrant is a well-known

seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required

to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has

filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months

(or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Indicate by check mark whether the registrant has submitted

electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405

of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller reporting company | |

| Emerging growth company |

If an emerging growth company, indicate by check mark

if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards

provided pursuant to Section 13(a) of the Exchange Act.

Indicate by checkmark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the regular public accounting firm that prepared or issued its audit report. ☐

Indicate by check mark whether the registrant is a shell

company (as defined in Rule 12b-2 of the Act). Yes ☐

As of December 31, 2022, the last business day of

the registrant’s most recently completed fiscal quarter, the aggregate market value of the common stock held by non-affiliates

of the registrant was $

The number of shares outstanding of the registrant’s classes of common stock as of March 22, 2023 was shares.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| i |

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

Certain statements contained in this Report may contain "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, as amended. Such forward-looking statements include, but are not limited to, statements regarding our Company and management’s expectations, hopes, beliefs, intentions, or strategies regarding the future, including our financial condition and results of operations. In addition, any statements that refer to projections, forecasts, or other characterizations of future events or circumstances, including any underlying assumptions, are forward-looking statements. The words “anticipates,” “believes,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “might,” “plans,” “possible,” “potential,” “predicts,” “projects,” “seeks,” “should,” “will,” “would” and similar expressions, or the negatives of such terms, may identify forward-looking statements, but the absence of these words does not mean that a statement is not forward-looking.

Forward-looking statements are subject to significant risks and uncertainties. Investors are cautioned against placing undue reliance on such statements. Actual results may differ materially from those set forth in the forward-looking statements. Other important factors that we think could cause our actual results to differ materially from expected results are summarized below, including the still ongoing impact of the current outbreak of the novel coronavirus ("COVID-19"), on the U.S., regional and global economies, the U.S. sustainable energy market, and the broader financial markets. The current outbreak of COVID-19 has also impacted, and is likely to continue to impact, directly or indirectly, many of the other important factors below and the risks described in this Form 10-K and in our subsequent filings under the Exchange Act. Other factors besides those listed could also adversely affect us. In addition, we cannot assess the impact of each factor on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. In particular, it is difficult to fully assess the impact of COVID-19 at this time due to, among other factors, uncertainty regarding the severity and duration of the outbreak domestically and internationally, uncertainty regarding the effectiveness of federal, state and local governments’ efforts to contain the spread of COVID-19 and respond to its direct and indirect impact on the global economy and economic activity, including the timing of the successful distribution of an effective vaccine.

Statements regarding the following subjects, among others, may be forward-looking:

| · | negative impacts from a continued spread of COVID-19, including on the U.S. or global economy or on our business, financial position, or results of operations; | |

| · | market trends in our industry, energy markets, commodity prices, interest rates, the debt and lending markets, or the general economy; | |

| · | our plans and expectations regarding future financial results, expected operating results; | |

| · | the sufficiency of our cash and our liquidity; | |

| · | development of new products and improvements to our existing products; | |

| · | our manufacturing capacity and manufacturing costs; | |

| · | the adequacy of our agreements with our suppliers; | |

| · | our ability to obtain financing, our ability to comply with debt covenants or cure any defaults; | |

| · | availability of opportunities to participate in climate solutions including energy efficiency and renewable energy projects and our ability to complete potential new opportunities in our pipeline; | |

| · | actions and initiatives of federal, state and local governments and changes to federal, state and local government policies, regulations, tax laws and rates and the execution and impact of these actions, initiatives and policies; | |

| · | our ability to obtain and maintain financing arrangements on favorable terms, including securitizations; | |

| · | general volatility of the securities markets in which we participate; | |

| · | the impact of weather conditions, natural disasters, accidents or equipment failures, or other events that disrupt our operations or negatively impact the value of our assets; | |

| · | availability of and our ability to attract and retain qualified personnel; and | |

| · | our understanding of our competition. |

| ii |

Forward-looking statements are based on beliefs, assumptions and expectations as of the date of this Form 10-K. Any forward-looking statement speaks only as of the date on which it is made. New risks and uncertainties arise over time, and it is not possible for us to predict those events or how they may affect us. Except as required by law, we are not obligated to, and do not intend to, update or revise any forward-looking statements after the date of this Form 10-K, whether as a result of new information, future events or otherwise.

The risks included here are not exhaustive. Other sections of this Form 10-K may include additional factors that could adversely affect our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for management to predict all such risk factors, nor can it assess the impact of all such risk factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. Given these risks and uncertainties, investors should not place undue reliance on forward-looking statements as a prediction of actual results.

| iii |

PART I

ITEM 1. BUSINESS.

Company Overview

Energy and Water Development Corp. (the “Company” or “EAWD”) was originally incorporated as a Delaware corporation named Wealthhound.com, Inc. in 2000 and was converted to a Florida corporation under the name Eagle International Holdings Group Inc. on December 14, 2007.

On March 10, 2008, the Company changed its name to Eurosport Active World Corporation and on March 17, 2008, the Company entered into an Agreement and Plan of Acquisition (the “Acquisition Agreement”) with Inko Sport America, LLC (“ISA”), a privately-held Florida limited liability company wherein all of the certified owners of ISA exchanged their ownership interests in ISA for shares of the Company. In connection with the closing of the Acquisition Agreement, the Company adopted ISA’s business plan and the Company’s registered current directors were elected to their positions. This transaction was accounted for as a recapitalization effected by a share exchange, wherein ISA was considered the acquirer for accounting and financial reporting purposes. ISA was administratively dissolved in September 2010.

In September 2019, the Company changed its name to Energy and Water Development Corp. to more accurately reflect the Company’s purpose and business sector and the Company has registered its logo “EAWD” with the United States Patent and Trademark Office, the European Union Intellectual Property Office and the World Intellectual Property Organization (WIPO) to secure its corporate identity.

To ensure the Company is positioned to service its growing business in one of the EU’s most environmentally progressive countries, the Company has a branch registered to conduct business in Germany and two wholly-owned German subsidiaries: Energy and Water Development Deutschland GmbH (“EAWD Deutschland”) and EAWD Logistik GmbH (“EAWD Logistik”).

The Business

We are an engineering services company formed as an outsourcing green tech platform, focused on sustainable water and energy solutions.

| · | EAWD builds water and energy systems out of existing, proven technologies, utilizing our patent pending systems configuration and our technical know-how to customize solutions to meet our clients’ needs. To date, two water systems have been sold and deployed in Mexico and Germany. | |

| · | Using its patent pending design, EAWD is working to design, build, and operate Off-Grid EV Charging Stations in Germany. | |

| · | EAWD commercializes proven technologies for the sustainable generation of energy and water. The first unit has been built and tested in Germany and the Company is working to fulfill additional orders. | |

| · | EAWD is a United Nations “accredited vendor” and offers design, construction, maintenance and specialty consulting services to private companies, government entities and non-government organizations (NGOs) for the sustainable supply of energy and water. |

In view of the increased world-wide demand for water and energy, our business goals are focused on self-sufficient energy supplied water generation and green energy production. To accomplish this, we set out to establish an outsourcing green tech platform to commercialize the Company’s state-of-the-art technologies while providing engineering and technical consultation services to design the most sustainable technological solutions that can provide water and energy. We also intend to secure all required technical, maintenance, education, and training related to the identified technology solutions. To this end the Company has sought potential collaboration with green tech research and development centers in Europe and has established its operating subsidiaries in Hamburg Germany, where we have started to assemble our patent-pending innovative off-grid, self-sufficient energy supply atmosphere water generation (“AWG”) systems (EAWD Off-Grid AWG Systems). EAWD Deutschland and EAWD Logistik operate in Hamburg, Germany to meet the increasing demands of water and energy generation projects around the world as well as to operate the solar powered EAWD Off-Grid EV Charging Stations, EAWD’s newest product, in Germany.

| 1 |

The green tech industry is constantly evolving due to ongoing and increasing water scarcity as well as increased energy needs in the world. Therefore, we believe that by designing sustainable and renewable solutions to these problems, EAWD will become an essential component of a rapidly growing industry with many new markets.

The green tech industry is complex because it still requires increased promotion and public education about its potential. Furthermore, regulations in each country are different and, in many cases, several segments are regulated by both national and local (state, provincial, municipal) governments. EAWD’s approach seeks to assist businesses with the growth and development of their general operations by ensuring the efficient, profitable, and sustainable supply/generation of water and energy allowing our potential customers to focus on their business while adopting strategies of sustainability. Using our own EAWD Off-Grid AWG Systems, EAWD Off-Grid EV Charging Stations, EAWD Off-Grid Power Systems, EAWD Off-Grid Water Purification Systems, and other identified technology, products, and services licensed or purchased from third party sources, we are delivering and installing a product set that suits the green technology water and/or energy needs of our customers. By using the state-of-the art technological solutions and technologies identified, designed, and provided by EAWD and its collaborators, we believe that our potential clients will be free to focus on the performance of their operations as well as with the water and energy consumption or generation regulations within their industry. Our clients may be businesses seeking to upgrade their business processes, NGOs or governmental entities seeking to apply green technology solutions for the water and energy they supply to their constituencies.

We continue to be a development stage company. The Company presently assembles its EAWD Off-Grid AWG Systems and EAWD Off-Grid EV Charging Stations at its workshop in Germany and outsources most of its engineering and technical services as well as services relating to the promotion, selling, and distribution of its products. We presently have only nine employees: Ms. Velazquez, our Chief Executive Officer, Vice-Chairman of the Board of Directors, and a significant stockholder, Mr. Hofmeier, our Chief Technology Officer, Chairman of the Board of Directors, and a significant stockholder, two engineers, two technicians, one accountant assistant, and two assemblers. Ms. Velazquez and Mr. Hofmeier are married.

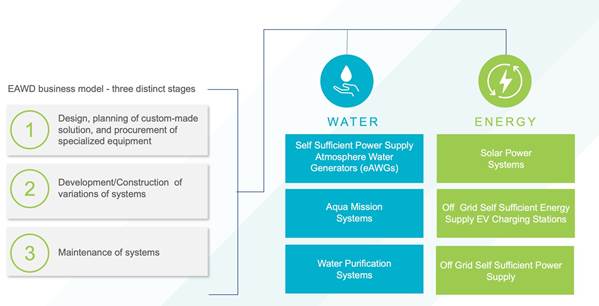

We seek to focus on three main aspects of the water and energy business: (1) generation, (2) supply, and (3) maintenance. We seek to assist private companies, government entities and municipalities, and NGOs to build profitable and sustainable supplies/generation capabilities of water and energy as required by selling them the required technology or technical service to enhance their productivity/operability. With its outsourced technical arm and its commission-based global network of distributors, the Company expects to create sustainable added value to each project it takes on while generating revenue from the sale of own EAWD Off-Grid AWG Systems, EAWD Off-Grid EV Charging Stations, EAWD Off-Grid Power Systems, and EAWD Off-Grid Water Purification Systems, royalties from the commercialization of energy and water in certain cases, and the licensing of our innovated technologies; as well as from its engineering, technical consulting, and project management services.

The following table depicts the Company’s service and product offerings to its clients.

| 2 |

We plan to provide customized technology solutions and technical services, based upon client need and preference, which may include any or all of the following:

| · | water and energy generation | |

| · | off-grid electric vehicle charging stations | |

| · | technical assistance | |

| · | strategic and financial partnering | |

| · | project management |

The Company also plans to focus on addressing areas of the industry which concentrate on new technological and engineering concepts relating to water and energy generation and those related components that assist in advancing the green tech industry. These include:

| · | advancement of EAWD Off-Grid AWG Systems | |

| · | development of techniques to attain self-sufficient supply of energy | |

| · | advancement of new ideas on energy generation, storage and management implementation | |

| · | designing, prototyping, and arranging the manufacture of new water and energy generation systems | |

| · | designing and prototyping off-grid self-sufficient power systems | |

| · | designing and prototyping solar powered charging stations for electric vehicles |

Our Vision

The size of the global market for atmospheric water generators was estimated at USD 959.85 million in 2020, reached USD 1,074.01 million in 2021, and at a compound annual growth rate (CAGR) of 14.75%, is expected to reach USD 2,515.19 million by 2027. (Source: Atmospheric Water Generator Market 2022 Report published by 360i Research)

The main market dynamics to consider are the growing numbers of AWGs across various end-use verticals and versus the high energy consumption, production cost, and high carbon footprint of such technology. Our research and development activities in AWG technology have led us to develop novel technologies that overcome these negative dynamics (such as our EAWD Off-Grid AWG Systems).

The mission of EAWD is to provide sustainable water generation systems based on high efficiency, renewable sources and to provide off-grid self-sufficient energy supply solutions. Through a combination of the best design and configuration of state-of-the-art technology-assisted solutions, EAWD has created a completely self-sufficient off the grid energy generation and water production system, which can be simultaneously used to meet potable water requirements and the electrical energy needs of the industrial sector.

EAWD promotes and commercializes its green technology solutions via commission-based distributers and agents worldwide.

Through our BlueTech Alliance for Water Generation, established in December 2020, we have state-of-the-art technology partners, technology transfer agreements, and technology representation agreements in place relating to aspects of renewable energy and water supply. These unique key relationships offer important selling features and capabilities that differentiated EAWD from its competitors.

The Company plans to generate revenue from the sale of EAWD Off-Grid AWG Systems, the development, sale, and operation of the EAWD Off-Grid EV Charging Stations, sale of EAWD Off-Grid Power Systems, and EAWD Off-Grid Water Purification Systems, royalties from the commercialization of energy and water in certain cases, and the licensing of our innovated technologies; as well as from its engineering, technical consulting, and project management services.

| 3 |

Our Products

The technological solutions offered by our Company are the following:

EAWD Off-Grid AWG Systems

Today, atmospheric water generators (AWGs) are standard equipment in many places; however, operating AWGs requires high amounts of energy that is often not available in the places where they are needed most, making the price for the generated water very high. Our innovative EAWD Off-Grid AWG Systems are designed to have an internal power supply and ability to generate power. Our EAWD Off-Grid AWG Systems produce sufficient quantities of potable water even in very dry and hot climate conditions and can be scaled to almost any size, community, and/or population. Presently, AWGs are largely used in Asian and African countries. The majority of manufacturers of AWGs, which rely on dehumidifying, are located in China. Almost every U.S. based AWG brand is also supplied by manufacturers in China.

By contrast, EAWD uses a proven German technology for condensate water from the air based on A/C technology. We believe that this method allows higher, more efficient, sustainable performance and a larger quantity of water generation because of its internal power supply and because it does not require high humidity to function. EAWD has licensed the rights to use this German AWG technology for ninety-nine years; however, thanks to our continued research and development efforts, the Company has designed a new, innovative and more efficient configuration that allows the substantial amount of energy required to operate the equipment to be supplied by the equipment itself. Our EAWD Off-Grid AWG Systems line is different in size from the standard AWG line. Our EAWD Off-Grid AWG Systems are energy self-sufficient and can condense large amounts of water out of the atmosphere and we believe they could be a solution in countries around the world that deal with issues of water scarcity.

Our EAWD Off-Grid AWG System with an internal power supply, works by first “inhaling” large volumes of air, then cooling the air down to the dew point, and finally collecting, filtering, and mineralizing the resulting condensed water. Through this process, pure drinking water is created that meets the quality standards of the World Health Organization (WHO). In regions with high temperatures and high humidity levels, a single system can generate more than 300,000 liters of water per day. Our EAWD Off-Grid AWG Systems line starts at 2,640 gallons/day and can expand the water supply to one acre-feet/day, which we believe, in effect, is essentially the ability to produce an unlimited supply of water. As a certified vendor of the United Nations (UN) Global Marketplace, EAWD is introducing the EAWD Off-Grid AWG and Power Systems to the UN with the hopes of initially supplying the equipment to large cluster of agencies established in key locations for humanitarian response as well as refugee camps around the world in need of fresh water.

EAWD Off-Grid Water Purification Systems

EAWD also seeks to respond to the growing need for drinking water by proposing a water purification solution utilizing solar, photovoltaic energy and, when applicable, a mini-windmill or other alternate source of renewable energy. The design of the system is ready to be built and delivered on demand.

Generally, drinking water is produced by passing sea water, lake water, river water, or stagnant water through several stages of purification and treatment until it is rendered drinkable in accordance with WHO standards. In the case of sea or stagnant water, we recommend a treatment via reverse osmosis membranes, which permits the retention of dissolved solids and results in obtaining water of drinking quality. If the water being treated emanates from lakes or rivers, we recommend treatment via an ultrafiltration membrane which functions by retaining suspended materials such as colloids, viruses and bacteria. The systems proposed by EAWD are containerized and contain all the equipment necessary to function autonomously, in part due to an automatic cleansing system that can be accessed remotely via satellite or the internet. Moreover, the machines use available renewable energy sources such as solar or wind to function.

| 4 |

EAWD Off-Grid EV Charging Stations

The global electric vehicle market was valued at $162.34 billion in 2019, and is projected to reach $802.81 billion by 2027, registering a CAGR of 22.6%. Asia-Pacific was the highest revenue contributor, accounting for $84.84 billion in 2019, and is estimated to reach $357.81 billion by 2027, with a CAGR of 20.1%. North America is estimated to reach $194.20 billion by 2027, at a significant CAGR of 27.5%. Asia- Pacific and Europe collectively accounted for around 74.8% share in 2019, with the former constituting around 52.3% share. North America and Europe are expected to witness considerable CAGRs of 27.5% and 25.3%, respectively, during the forecast period. The cumulative share of these two segments was 40.1% in 2019, and is anticipated to reach 51.0% by 2027. (Source: Electric Vehicle Fluids Market Global Forecast to 2030 2021 Report from Markets and Markets.)

There is also an increasing consensus among European truck manufacturers and industry stakeholders that battery electric trucks (BETs) will play a dominant role in the decarbonization of the road freight sector. Most truck makers including Daimler, DAF, MAN, Scania and Volvo are now focusing on bringing BETs to the mass market for all vehicle segments, including long-haul, starting from 2024. For this, a network of public high-power and overnight charging points needs to be rolled out across Europe no later than 2024.

Based on our patent-pending Off-Grid Power System, EAWD has developed an innovative design and configuration of off-grid charging stations for BETs and electric vehicles in Germany. Our product is the first off-grid solution available in Europe for charging the BETs and electric passenger vehicles that are currently on the roads of Europe. EAWD plans to establish up to 1,700 charging stations throughout the USA, Mexico and Germany starting with 40 locations scheduled to be deployed in the fourth quarter of 2024.

EAWD Off-Grid Power Systems

Today, batteries for stationary storage have become a commodity, but in order to reduce the duration, complexity and cost of the installation, and to increase its capacity or relocate a system over time as well as to reduce its carbon footprint and environmental impact, we offer a complete Electrical Energy Storage System (EESS) and Energy Management System (EMS) for a wide range of customers and applications, including microgrids and EV fast charging stations. A highly capable energy management system which secures the efficient energy supply and storage of energy. Example: with elements such as software and Battery Management System (BMS) our systems can allow controlled and optimized battery cell management.

This product portfolio includes systems and complete services for solar power generation in the building envelope. A high-quality frameless glass solar panel with a super-matte surface, which secures a high-performance energy source.

In contrast to classic solar systems on the roof, EAWD combines the highest standards of aesthetics with high efficiency energy generation. With these solutions, EAWD supports its customers on their way to CO2 neutrality and the search for alternative renewable energies.

Current Projects

COVID-19 is an incomparable global public health emergency that has affected almost every industry and has caused the worst global economic contraction of the past 80 years (IMF) and the current war in Ukraine has also caused significant changes in consumer behavior and purchasing patterns, supply chain routing, the dynamics of current market forces, and government oversight and intervention. As a consequence of the foregoing, the following projects have been delayed; however the Company continues to make progress on their fulfillment:

Germany

The Company has leased 24,000 sq. mi of land in Kassel, Germany, where it is establishing the first large off-grid charging station location for electric trucks and passenger vehicles in Germany and Europe. With enough solar panels installed, each charging station is proposed to generate at least five MWh of solar energy per day and have a total capacity of at least one MWp. More than 2,400 MWh of energy storage capacity will be used in lithium battery systems (LFP), to ensure the continuous use and availability of energy. The system is low voltage AC coupled, which will ensure easy integration and expansion of the system in the future. The different elements of EAWD’s system form a “micro grid” that is isolated and independent from the public power grid. It will have a capacity up to one MW of instant and continuous power. The charging points will be of 300 KW of power, with the capacity to charge two trucks simultaneously of 150 KW each, of course it will also be able to charge any other electric vehicle since it has the most common and standard connections/adapters in Europe.

| 5 |

The Company has completed the manufacture and installation of the first of forty planned solar powered EAWD Off-Grid EV Charging Stations for electric long-haul trucks in Hamburg, Germany. Our charging stations are the first off-grid charging station available for these e-trucks in Europe and the Company plans to contract with companies that own these electric long-haul trucks to provide fleet charging as well as to install them in public places for per-use fees.

A solar powered EAWD Off-Grid AWG System has also been built in Hamburg, Germany and the Company plans to use it to showcase the system’s ability to generate water for large projects throughout Germany where it is expected to produce up to two million gallons of water per day. The Company expects these systems to be operated throughout Germany, the United States of America, Mexico and Latin America.

Mexico

In 2020, our Mexican distributor placed a USD $550,000 initial order for a solar powered EAWD Off-Grid AWG System which was built in Germany

and delivered to the customer in accordance with the purchase agreement. The Company is currently negotiating the purchase of three additional

units by the same customer. The foregoing description of the purchase contract does not purport to be complete and is qualified in its

entirety by reference to the copy of such contract filed as Exhibit 10.4 to this report on Form 10-K.

South Africa

On May 8, 2019, the Company signed a sales contract for the sale of a solar powered EAWD Off-Grid AWG System to a South African customer for a purchase price of $2,800,000. The build out of the equipment began in the fourth quarter of 2019, however because of delays due to COVID-19 and the global supply chain, the expected completion date has been pushed to late 2023. The foregoing description of the purchase contract does not purport to be complete and is qualified in its entirety by reference to the copy of such contract filed as Exhibit 10.3 to this report on Form 10-K.

Worldwide Business Relationships

EAWD has commission-based independent agents and distributors strategically placed around the world in Germany, Mexico, United States, India, Canada, Australia, Colombia, Nepal, Kenya, Morocco, and Thailand to promote and sell EAWD’s technology solutions.

We believe that this worldwide presence through our agents and distributors will provide us access to the most important markets in need of water, energy, and energy management solutions.

Competition

The market witnesses the presence of a diversified array of large and small scale manufacturers resulting in a significant level of competition in the global market. The competition in the market, both in the residential and commercial sectors, is projected to grow in intensity and is characterized by the demand for advanced and reliable atmospheric water generator units. Rising demand for industrial-size eAWGs, particularly in regions facing water shortages, is expected to create opportunities for new market players such as EAWD through 2027. Moreover, current research that is focused on increasing overall product efficiency in the industry is anticipated to open new avenues for market players over the coming years. According to an atmospheric water generator market size report [published by Grand View Research in 2020], some of the prominent players in the atmospheric water generator (AWG) market include: Akvo Atmospheric Water Systems Pvt. Ltd., Dew Point Manufacturing, Saisons Trade & Industry Private Limited, Water Maker India Pvt. Ltd., Planets Water, Water Technologies International, Inc. (WTII), Drinkable Air, Hendrx Water, Atlantis Solar, GENAQ Technologies S.L., Air2Water LLC, EcoloBlue, Inc and Watergen. On some level, each of these companies faces the two main industry challenges: carbon footprint and high-power requirement.

| 6 |

We compete by providing innovative systems assembled with state-of-the-art technologies and that contain self-sufficient power supplies, which make them more sustainable and profitable than the traditional solutions. We also set ourselves apart by providing services that are valued by our customers such as reliable sales relationships, product innovations, and responses to changing market/business needs.

Corporate Information

We were incorporated in Florida in 2008 and have operations based in Hamburg, Germany.

Our website is www.energy-water.com. Our website and the information contained therein, or connected thereto, are not intended to be incorporated into this report on Form 10-K.

Our principal executive offices are located at 7901 4th Street N STE #4174, St Petersburg, Florida. Our telephone number is 727-677-9408, and our website is www.energy-water.com. Our operations in Germany are located at the office address Ballindamm 3, 20095 Hamburg. Our Telephone number is +49 40 809 08 1354.

The transfer agent for our common stock is Worldwide Stock Transfer, LLC, located at One University Plaza, Suite 505, Hackensack, NJ 07601, Phone: (201) 820-2008, Fax: (201) 820-2010. We intend to engage Worldwide Stock Transfer, LLC as transfer agent for the Warrants as well.

Government Regulation

The manufacturing, processing, testing, packaging, labeling, and advertising of the technologies that we sell may be subject to regulation by one or more U.S. federal agencies, including the Food and Drug Administration, the Federal Trade Commission, the U.S. Department of Agriculture, the Environmental Protection Agency, and by the standards provided by the U.S. Department of Health and Human Services and the World Health Organization for drinking water. Our operations may also be regulated by various agencies of states, localities, and foreign countries in which consumers reside. Currently, the technologies we intend to use in our solutions and our services are not subject to any governmental regulation in the United States although it is possible that the FDA may choose to regulate the quality of water produced from atmospheric water generating machines in the near future.

Since the Company may be subject to a wide range of regulation covering every aspect of our business as mentioned above, we cannot predict the nature of any future U.S. laws, regulations, interpretations or applications, nor can we determine what effect additional governmental regulations or administrative orders, when and if promulgated, would have on the business in the future. Although the regulation of water is less restrictive than that of drugs and food additives, we cannot offer assurance that the current statutory scheme and regulations applicable to water will remain less restrictive. Further, we cannot assure you that, under existing laws and regulations, or if more stringent statutes are enacted, regulations are promulgated, or enforcement policies are adopted, we are or will be in compliance with these new statutes, regulations or enforcement policies without incurring material expenses or adjusting our business strategy. Any laws, regulations, enforcement policies, interpretations or applications applicable to our business could require the reformulation of products, all of which are supplied by third parties, to meet new standards or the recall or discontinuance of certain products not capable of reformulation, additional record keeping, expanded documentation of the properties of certain products, expanded or different labeling or scientific substantiation.

Employees

As of December 31, 2022, we had four full-time employees. Over time, we will be required to hire employees or continue to engage independent contractors in order to execute the projects necessary to grow and develop the business. These decisions will be made by our officers and directors, if and when appropriate. We work with 34 commission-based agents and distributors to promote and sell the Company’s technology solutions. These agents and distributors are independent contractors with whom we have contractual relationships and are compensated solely based on commission.

| 7 |

JOBS Act and the Implications of Being an Emerging Growth Company

We are an “emerging growth company” as defined in Section 2(a)(19) of the Securities Act, as modified by the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). As such, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements, and exemptions from the requirements of holding a non-binding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved. We elected to take advantage of all of these exemptions.

In addition, Section 107 of the JOBS Act also provides that an “emerging growth company” can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards, and delay compliance with new or revised accounting standards until those standards are applicable to private companies. We have elected to take advantage of the benefits of this extended transition period.

We will be an emerging growth company until the last day of the first fiscal year following the fifth anniversary of our first common equity offering, although we will lose that status earlier if our annual revenues exceed $1.0 billion, if we issue more than $1.0 billion in non-convertible debt in any three-year period or if we become a “large accelerated filer” as defined in Rule 12b-2 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). We will qualify as a “large accelerated filer” as of the first day of the first fiscal year after we have (i) more than $700,000,000 in outstanding common equity held by our non-affiliates as of the last day of our most recently completed second fiscal quarter; (ii) been a public company for at least 12 months; and (iii) filed at least one annual report with the SEC. The value of our outstanding common equity will be measured each year on the last day of our second fiscal quarter.

COVID-19 Pandemic Update and the War in Ukraine

The outbreak of Coronavirus (COVID-19) has caused significant disruptions to national and global economies and government activities. However, during this time, we have continued to conduct our operations to the fullest extent possible, while responding to the outbreak with actions that include:

| ● | coordinating closely with our suppliers and customers; | |

| ● | instituting various aspects of our business continuity programs; and | |

| ● | planning for and working aggressively to mitigate disruptions that may occur. |

COVID-19 is an incomparable global public health emergency that has affected almost every industry and has caused the worst global economic contraction of the past 80 years (IMF) and the current war in Ukraine has also caused significant changes in consumer behavior and purchasing patterns, supply chain routing, the dynamics of current market forces, and government oversight and intervention.. Disruptive activities could include the temporary closure of our manufacturing facilities and those used in our supply chain processes, restrictions on the export or shipment of our products, significant cutback of ocean container delivery from Germany, business closures in impacted areas, and restrictions on our employees’ and consultants’ ability to travel and to meet with customers. The extent to which COVID-19 or the war in Ukraine impacts our results will depend on future developments, which still uncertain and cannot be predicted, including new information which may emerge concerning the severity of the current conflict as well as virus variants and the actions to contain it or treat its impact, among others. COVID-19 and the war in Ukraine could also continue to result in social, economic and labor instability in the countries in which we or our customers and suppliers operate.

If workers at one or more of our offices or the offices of our suppliers or manufacturers become ill or are quarantined and in either or both events are therefore unable to work, our operations could be subject to disruption. Further, if our manufacturers become unable to obtain necessary raw materials or components, we may incur higher supply costs or our manufacturers may be required to reduce production levels, either of which may negatively affect our financial condition or results of operations.

In light of these challenges, the Company is focusing its efforts on supporting key areas of our business that will help us to stabilize in the new environment and strategize for what comes next. Those key areas are: crisis management and response, workforce, operation and supply chain, finance and liquidity, tax, trade and regulatory, as well as strategy and brand.

Intellectual Property

We rely on a combination of trademarks, copyrights, trade secrets and patents and contractual provisions, to protect our proprietary technology and our brands.

| · | The Company has registered its logo as a trademark with the United States Patent and Trademark Office (USPTO, the European Union Intellectual Property Office and the World Intellectual Property Organization (WIPO) to secure its corporate identity. |

| · | The Company has filed an application to patent its EAWD Off-Grid AWG Systems with the USPTO and WIPO. |

| · | The Company has filed an application to patent its EAWD Off Grid Self Sufficient Electric Vehicle Charging Station with the USPTO and WIPO. |

| 8 |

ITEM 1A. RISK FACTORS.

As a Smaller Reporting Company, the Company is not required to include the disclosure required under this Item 1A.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

Not applicable.

ITEM 2. PROPERTIES.

Our registered office is located at 7901 4th Street N STE #4174, St. Petersburg, Florida 33702. Our telephone number is +1 (727) 677-9408. Office services are contracted for on a month-to-month basis in this address. Since October 2020, the Company had an official registered Branch, which became an officially registered subsidiary in Hamburg Germany; the office address Bellindam 3, 20095 Hamburg. Our Telephone number is +49 40 809 08 1354.

We do not own any real property. We may procure additional space as we add employees and expand geographically. We believe that our current facilities are adequate to meet our needs for the immediate future and that, should it be needed, suitable additional space will be available to accommodate expansion of our operations.

ITEM 3. LEGAL PROCEEDINGS.

EAWD vs Packard and Co-Defendant Nick Norwood - Case number 18-031011 CA-01 Miami-Dade County Circuit Court. The Company is demanding proof of payment for shares issued in 2008.

EAWD vs Nerve Smart Systems ApS (“Nerve”) Case number BS-15264/2022– The Court of Roskilde, Denmark. On April 2022, the Company filed a claim against Nerve demanding the return of amounts paid by the Company for a Battery Energy Storage System that was never delivered by Nerve to the Company, and therefore Nerve did not meet the requirements and specifications of the contract with the Company. The Company is confident there will be a positive outcome. This matter is not expected to be resolved prior to 2024 due to the long waiting times of the Danish court System.

EAWD vs NPP Niethammer, Posewang & Partner GmbH Wirtschaftsprüfungsgesellschaft Steuerberatungsgesellschaft (“NPP”) – Case number 322 O 159/22 – On November 28, 2022, by court settlement, the legal dispute again NPP was settled. The subject matter of the legal dispute was NPP’s fee claims against the Company in the amount of EUR 45,500, which is approximately $48,160, plus interest. On November 28, 2022, the Company agreed to pay NPP an amount of EUR 22,749, which is approximately $23,214. The costs of the legal dispute were set off against each other in the settlement. There is still an outstanding fee claim against the Company according to an invoice dated January 25, 2023 in the amount of EUR 4,986, which is approximately $5,277.

Due to the nature of the Company's business, the Company may at times be subject to claims and legal actions. The Company accrues liabilities when it is probable that future costs will be incurred, and such costs can be reasonably estimated. Such accruals are based on developments to date and the Company’s estimates of the outcomes of these matters. Except as set forth above, as of December 31, 2022 we are not currently subject to any legal proceedings, nor to the knowledge of management are any legal proceedings threatened that are likely to have a material adverse effect on our financial position, results of operations or cash flows.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

| 9 |

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Our common stock is currently quoted on the OTCQB tier of the OTC Market under the symbol “EAWD” There is currently a limited market for our common stock and the volume of our common stock traded on any day may vary significantly from one day to another. Trading in stock quoted on the OTC Market’s OTCQB is often thin and characterized by wide fluctuations in trading prices due to many factors that may have little to do with our operations or business prospects. The availability of buyers and sellers represented by this volatility could lead to a market price for our common stock that is unrelated to operating performance. Moreover, the OTC Market’s OTCQB is not a stock exchange, and trading of securities quoted on the OTC Market’s OTCQB is often more sporadic than the trading of securities listed on a stock exchange like NASDAQ. There is no assurance that there will be a sufficient market in our stock, in which case it could be difficult for our stockholders to resell their shares.

On March 28, 2023 , the closing price of our common stock was $0.04 per share as reported on the OTC QB Market maintained by OTC Markets Group, Inc.

The following table sets forth for the respective periods indicated the prices of our common stock in this market as reported and summarized by the OTC Markets. Such prices are based on inter-dealer bid and asked prices, without markup, markdown, commissions, or adjustments and may not represent actual transactions.

| HIGH | LOW | |||||||

| Fiscal Year 2022: | ||||||||

| First Quarter | $ | 0.45 | $ | 0.15 | ||||

| Second Quarter | $ | 0.25 | $ | 0.16 | ||||

| Third Quarter | $ | 0.21 | $ | 0.05 | ||||

| Fourth Quarter | $ | 0.08 | $ | 0.02 | ||||

| Fiscal Year 2021: | ||||||||

| First Quarter | $ | 0.76 | $ | 0.15 | ||||

| Second Quarter | $ | 0.45 | $ | 0.17 | ||||

| Third Quarter | $ | 0.59 | $ | 0.05 | ||||

| Fourth Quarter | $ | 1.00 | $ | 0.0001 | ||||

Penny Stock

The SEC has adopted rules that regulate broker-dealer practices in connection with transactions in penny stocks. Penny stocks are generally equity securities with a market price of less than $5.00, other than securities registered on certain national securities exchanges or quoted on the NASDAQ system, provided that current price and volume information with respect to transactions in such securities is provided by the exchange or system. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock, to deliver a standardized risk disclosure document prepared by the SEC, that: (a) contains a description of the nature and level of risk in the market for penny stocks in both public offerings and secondary trading; (b) contains a description of the broker’s or dealer’s duties to the customer and of the rights and remedies available to the customer with respect to a violation of such duties or other requirements of the securities laws; (c) contains a brief, clear, narrative description of a dealer market, including bid and ask prices for penny stocks and the significance of the spread between the bid and ask price; (d) contains a toll-free telephone number for inquiries on disciplinary actions; (e) defines significant terms in the disclosure document or in the conduct of trading in penny stocks; and (f) contains such other information and is in such form, including language, type size and format, as the SEC shall require by rule or regulation.

The broker-dealer also must provide, prior to effecting any transaction in a penny stock, the customer with (a) bid and offer quotations for the penny stock; (b) the compensation of the broker-dealer and its salesperson in the transaction; (c) the number of shares to which such bid and ask prices apply, or other comparable information relating to the depth and liquidity of the market for such stock; and (d) a monthly account statement showing the market value of each penny stock held in the customer’s account.

| 10 |

In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from those rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written acknowledgment of the receipt of a risk disclosure statement, a written agreement as to transactions involving penny stocks, and a signed and dated copy of a written suitability statement.

These disclosure requirements may have the effect of reducing the trading activity for our common stock. Therefore, shareholders may have difficulty selling our securities.

Holders

As of December 31, 2022, we had 846 record holders of our common stock, holding 182,934,483 shares of common stock. The number of record holders was determined from the records of our transfer agent and does not include beneficial owners of common stock whose shares are held in the names of bank, brokers and other nominees.

Dividends

We have never declared nor paid any cash dividends on our common stock, and currently intend to retain all of our cash and any earnings for use in our business and, therefore, do not anticipate paying any cash dividends in the foreseeable future. Any future determination to pay cash dividends on our common stock will be at the discretion of the Board of Directors and will be dependent upon our consolidated financial condition, results of operations, capital requirements and such other factors as the Board of Directors deems relevant.

Securities authorized for issuance under equity compensation plans

Reference is made to “Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters—Securities Authorized for Issuance under Equity Compensation Plans” for the information required by this item.

Recent Sales of Unregistered Securities

During the fiscal years ended December 31, 2022 and 2021, the Company issued $178,000 and $404,000 in convertible debentures, respectively. The holders of certain of such instruments had the option to convert these convertible debentures into the Company’s common stock at conversion prices ranging from $0.01 to $0.20.

During 2022 and 2021, holders of convertible debentures exercised their conversion options on convertible debentures amounting to $50,000 and $270,000, respectively in exchange for 540,716 and 4,671,167 shares of common stock, respectively.

During the year ended December 31, 2022, the Company engaged in the following equity events:

Sale of Common Stock and Subscriptions

On February 18, 2022, the Company received a deposit in the amount of $300,000 for 1,875,000 common shares to be issued pursuant to a securities purchase agreement. These common shares were issued on July 4, 2022.

From January 1, 2022 through March 31, 2022, the Company has issued 14,953,000 common shares related to subscriptions outstanding at December 31, 2021 for total cash consideration of $747,650.

From April 1, 2022 through June 30, 2022, the Company has issued 8,527,947 common shares related to subscriptions outstanding at March 31, 2022 for total cash consideration of $437,450.

| 11 |

Shares issued pursuant to ELOC

On January 26, 2022 the Company entered into a two year equity line of credit (“ELOC”) with an investor to provide up to $5 million. As of March 31, 2022, 500,000 common shares had been issued pursuant to this agreement as the commitment fee at a fair value of $80,000.

On January 26, 2022, the Company entered into a Securities Purchase Agreement with an investor. As of March 31, 2022, 2,000,000 common shares were issued pursuant to this agreement for a purchase price of $300,000. In the third quarter of 2022, an additional 4,023,368 common shares were issued pursuant to ELOC for a purchase price of $450,000.

In the fourth quarter of 2022, the Company issued an additional 5,064,421 shares of the Company’s common stock pursuant to the ELOC for total cash consideration of $187,000.

Shares issued upon conversion of convertible debt

On January 14, 2022, the Company completed a conversion of our outstanding convertible debt by exchanging $53,222 cash for retiring $50,000 in convertible debt along with $3,222 in interest for a total of 575,558 common shares.

Shares issued for services

On February 2, 2022, the Company issued 20,000 shares of the Company’s common stock to a vendor for services valued at $3,600.

On February 3, 2022, the Company issued 500,000 shares of the Company’s common stock to a vendor for services valued at $85,000.

On April 27, 2022, the Company issued 227,273 shares of the Company’s common stock to a vendor for services valued at $50,000.

On August 11, 2022, the Company issued 600,000 shares of the Company’s common stock to a vendor for services valued at $79,500.

On September 9, 2022, the Company issued 227,273 shares of the Company’s common stock to a vendor for services valued at $50,000.

The sale and the issuance of the foregoing securities were offered and sold in reliance upon exemptions from registration pursuant to Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”) and Rule 506 of Regulation D promulgated under the Securities Act (“Regulation D”). We made this determination based on the representations of each recipient, as applicable, which included, in pertinent part, that each such investor was either (a) an “accredited investor” within the meaning of Rule 501 of Regulation D or (b) a “qualified institutional buyer” within the meaning of Rule 144A under the Securities Act and upon such further representations from each investor that (i) such investor acquired the securities for his, her or its own account for investment and not for the account of any other person and not with a view to or for distribution, assignment or resale in connection with any distribution within the meaning of the Securities Act, (ii) such investor agreed not to sell or otherwise transfer the purchased securities unless they are registered under the Securities Act and any applicable state securities laws, or an exemption or exemptions from such registration are available, (iii) such investor had knowledge and experience in financial and business matters such that he, she or it was capable of evaluating the merits and risks of an investment in us, (iv) such investor had access to all of our documents, records, and books pertaining to the investment and was provided the opportunity to ask questions and receive answers regarding the terms and conditions of the offering and to obtain any additional information which we possessed or were able to acquire without unreasonable effort and expense, and (v) such investor had no need for the liquidity in its investment in us and could afford the complete loss of such investment. In addition, there was no general solicitation or advertising for such securities issued in reliance upon these exemptions.

| 12 |

ITEM 6. [RESERVED]

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

Introductory Statement

The following discussion and analysis of the results of operations and financial condition for the fiscal years ended December 31, 2022 and 2021 should be read in conjunction with our financial statements and the notes to those financial statements that are included elsewhere in this Report. This discussion contains forward-looking statements and information relating to our business that reflect our current views and assumptions with respect to future events and are subject to risks and uncertainties that may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

These forward-looking statements speak only as of the date of this report. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, or achievements. Except as required by applicable law, including the securities laws of the United States, we expressly disclaim any obligation or undertaking to disseminate any update or revisions of any of the forward-looking statements to reflect any change in our expectations with regard thereto or to conform these statements to actual results.

Addressing Challenges Post-COVID-19 and the Current War in Ukraine

COVID-19 is an incomparable global public health emergency that has affected almost every industry and has caused the worst global economic contraction of the past 80 years (IMF) and the current war in Ukraine has also caused significant changes in consumer behavior and purchasing patterns, supply chain routing, the dynamics of current market forces, and government oversight and intervention. Disruptive activities could include the temporary closure of our manufacturing facilities and those used in our supply chain processes, restrictions on the export or shipment of our products, significant cutback of ocean container delivery from Germany, business closures in impacted areas, and restrictions on our employees’ and consultants’ ability to travel and to meet with customers. The extent to which COVID-19 or the war in Ukraine impacts our results will depend on future developments, which still uncertain and cannot be predicted, including new information which may emerge concerning the severity of the current conflict as well as virus variants and the actions to contain it or treat its impact, among others. COVID-19 and the war in Ukraine could also continue to result in social, economic and labor instability in the countries in which we or our customers and suppliers operate.

If workers at one or more of our offices or the offices of our suppliers or manufacturers become ill or are quarantined and in either or both events are therefore unable to work, our operations could be subject to disruption. Further, if our manufacturers become unable to obtain necessary raw materials or components, we may incur higher supply costs or our manufacturers may be required to reduce production levels, either of which may negatively affect our financial condition or results of operations.

In light of these challenges, the Company is focusing its efforts on supporting key areas of our business that will help us to stabilize in the new environment and strategize for what comes next. Those key areas are: crisis management and response, workforce, operation and supply chain, finance and liquidity, tax, trade and regulatory, as well as strategy and brand.

Critical Accounting Policies and Estimates

Our financial statements have been prepared in accordance with accounting principles generally accepted in the United States of America. The preparation of these financial statements requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities and expenses. Note 2 of the Notes to Financial Statements describes the significant accounting policies used in the preparation of the financial statements. Certain of these significant accounting policies are considered to be critical accounting policies, as defined below.

| 13 |

A critical accounting policy is defined as one that is both material to the presentation of our financial statements and requires management to make difficult, subjective or complex judgments that could have a material effect on our financial condition and results of operations. Specifically, critical accounting estimates have the following attributes: 1) we are required to make assumptions about matters that are highly uncertain at the time of the estimate; and 2) different estimates we could reasonably have used, or changes in the estimate that are reasonably likely to occur, would have a material effect on our financial condition or results of operations.

Estimates and assumptions about future events and their effects cannot be determined with certainty. We base our estimates on historical experience and on various other assumptions believed to be applicable and reasonable under the circumstances. These estimates may change as new events occur, as additional information is obtained and as our operating environment changes. These changes have historically been minor and have been included in the financial statements as soon as they became known. Based on a critical assessment of our accounting policies and the underlying judgments and uncertainties affecting the application of those policies, management believes that our financial statements are fairly stated in accordance with accounting principles generally accepted in the United States and present a meaningful presentation of our financial condition and results of operations. We believe the following critical accounting policies reflect our more significant estimates and assumptions used in the preparation of our financial statements:

Risks and Uncertainties – The Company’s business could be impacted by price pressure on its product manufacturing, acceptance of its products in the marketplace, new competitors, changes in federal and/or state legislation and other factors and new technology. If the Company is unsuccessful in securing adequate liquidity, its plans may be curtailed. Adverse changes in these areas could negatively impact the Company’s financial position, results of operations and cash flows.

Basis of Presentation

The consolidated financial statements include the accounts of Energy and Water Development Corp and have been prepared in accordance with accounting principles generally accepted in the United States of America and the rules of the Securities and Exchange Commission. In the opinion of management, all adjustments, consisting of normal recurring adjustments, necessary for a fair presentation of financial position and the results of operations for the periods presented have been reflected herein.

Use of Estimates

The preparation of financial statements in accordance with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of expenses during the reporting periods. Actual results could differ from those estimates. Estimates which are particularly significant to the financial statements include estimates relating to the determination of impairment of assets, assessment of going concern, the useful life of property and equipment, the determination of the fair value of stock-based compensation, and the recoverability of deferred income tax assets.

Leases

Effective January 1, 2019, the Company adopted ASC 842- Leases (“ASC 842”). The lease standard provided a number of optional practical expedients in transition. The Company elected the package of practical expedients. As such, the Company did not have to reassess whether expired or existing contracts are or contain a lease; did not have to reassess the lease classifications or reassess the initial direct costs associated with expired or existing leases. The lease standard also provides practical expedients for an entity’s ongoing accounting. The Company elected the short-term lease recognition exemption under which the Company will not recognize right-of-use (“ROU”) assets or lease liabilities, and this includes not recognizing ROU assets or lease liabilities for existing short-term leases. The Company elected the practical expedient to not separate lease and non-lease components for certain classes of assets (facilities).

At the inception of an arrangement, the Company determines whether the arrangement is or contains a lease based on the unique facts and circumstances present in the arrangement. Leases with a term greater than one year are recognized on the balance sheet as right-of-use assets and short-term and long-term lease liabilities, as applicable.

| 14 |

Income Taxes

Income taxes are accounted for under the asset and liability method as stipulated by ASC 740, “Accounting for Income Taxes”. Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of existing assets and liabilities and their respective tax bases and operating loss and tax credit carry forwards. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled. Under ASC 740, the effect on deferred tax assets and liabilities or a change in tax rate is recognized in income in the period that includes the enactment date. Deferred tax assets are reduced to estimated amounts to be realized by the use of the valuation allowance. A valuation allowance is applied when in management’s view it is more likely than not (50%) that such deferred tax will not be utilized.

ASC 740 provides interpretative guidance for the financial statement recognition and measurement of a tax position taken or expected to be taken in a tax return. In the unlikely event that an uncertain tax position exists in which the Corporation could incur income taxes, the Corporation would evaluate whether there is a probability that the uncertain tax position taken would be sustained upon examination by the taxing authorities. A liability for uncertain tax positions would then be recorded if the Corporation determined it is more likely than not that a position would not be sustained upon examination or if a payment would have to be made to a taxing authority and the amount is reasonably estimable.

As of December 31, 2022 and 2021, the Corporation does not believe any uncertain tax positions exist that would result in the Corporation having a liability to the taxing authorities. The Corporation’s policy is to classify interest and penalties related to unrecognized tax benefits, if and when required, as part of interest expense and general and administrative expense, respectively, in the statement of operations. The Corporation’s tax returns for the years ended 2012 through 2020 are subject to examination by the federal and state tax authorities. The Corporation’s tax returns for the tax year ended 2021 have not been filed.

We record our provision for income taxes in our consolidated statements of operations and comprehensive loss by estimating our taxes in each of the jurisdictions in which we operate. We estimate our actual current tax exposure together with assessing temporary differences arising from differing treatment of items recognized for financial reporting versus tax return purposes. These differences result in deferred tax assets, which are included in our balance sheets. In general, deferred tax assets represent future tax benefits to be received when certain expenses previously recognized in our consolidated statements of operations and comprehensive loss become deductible expenses under applicable income tax laws, or loss or credit carry forwards are utilized. Valuation allowances are recorded when necessary to reduce deferred tax assets to the amount expected to be realized.

Significant management judgment is required in determining our provision for income taxes, our deferred tax assets and liabilities and any valuation allowance recorded against our net deferred tax assets. We make these estimates and judgments about our future taxable income that are based on assumptions that are consistent with our future plans. As of December 31, 2022 and 2021, we had recorded a full valuation allowance on our U.S. net deferred tax assets because we expect that it is more likely than not that our deferred tax assets will not be realized in the foreseeable future. Should the actual amounts differ from our estimates, the amount of our valuation allowance could be materially impacted.

Revenue Recognition

The Company recognizes revenue in accordance with ASC 606, Revenue from Contracts with Customers, the core principle of which is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled to receive in exchange for those goods or services.

To achieve this core principle, five basic criteria must be met before revenue can be recognized: (1) identify the contract with a customer; (2) identify the performance obligations in the contract; (3) determine the transaction price; (4) allocate the transaction price to performance obligations in the contract; and (5) recognize revenue when or as the Company satisfies a performance obligation. During the year ended December 31, 2021, the Company recognized $550,000 in revenue as a result of meeting the above criteria. The Company recognized no revenue during the year ended December 31, 2022.

| 15 |

Fair Value of Financial Instruments

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at a measurement date. A fair value hierarchy requires an entity to maximize the use of observable inputs, where available, and minimize the use of unobservable inputs when measuring fair value.

Described below are the three levels of inputs that may be used to measure fair value:

Level 1 – Quoted prices in active markets that are accessible at the measurement date for identical assets or liabilities,

Level 2 – Observable prices that are based on inputs not quoted on active markets, but corroborated by market data,

Level 3 – Unobservable inputs are used when little or no market data is available.

Certain assets and liabilities are required to be recorded at fair value on a recurring basis. The Company adjusts derivative financial instruments to fair value on a recurring basis. The fair value for other assets and liabilities such as cash, accounts receivable, prepaid expenses and other current assets, accounts payable and accrued expenses, customer/investor deposit have been determined to approximate carrying amounts due to the short maturities of these instruments. The Company believes that its indebtedness approximates fair value based on current yields for debt instruments with similar terms.

Stock-Based Payments

The Company adopted Accounting Standards Update 2018-07 (“ASU 2018-07”), “Improvement to Nonemployee Share Based Payment Accounting”, which expanded the scope of ASC 718 to include share-based payment transactions for acquiring goods and services from nonemployees. The guidance was applied prospectively to all new awards granted after the date of adoption. In addition, the guidance was applied to all existing equity-classified awards for which a measurement date has not been established under ASC 505-50 by the adoption date by remeasuring at fair value as of the adoption date and recording a cumulative effect adjustment to opening accumulated deficit on January 1, 2019.

For the Company’s equity-classified awards for which a measurement date has not been established under ASC 505-50, the fair value on January 1, 2019, the adoption date, approximated the value assigned on December 31, 2018, therefore no cumulative adjustment to opening accumulated deficit was required.

Under the revised guidance, the accounting for awards issued to non-employees will be similar to the model for employee awards, except that ASU 2018-07:

| ● | allows the Company to elect on an award-by-award basis to use the contractual term as the expected term assumption in the option pricing model, and | |

| ● | the cost of the grant is recognized in the same period(s) and in the same manner as if the grantor had paid cash. |

Employee and Non-Employee Share Based Compensation

The Company applies ASC 718-10, “Share - Based Payment,” which requires the measurement and recognition of compensation expenses for all share-based payment awards made to employees and directors including employee stock options under the Company’s stock plans and equity awards issued to non-employees based on estimated fair values.

ASC 718-10 requires companies to estimate the fair value of equity-based option awards on the date of grant using an option-pricing model. The fair value of the award is recognized as an expense on a straight-line basis over the requisite service periods. The Company recognizes share based award forfeitures as they occur.

| 16 |

The Company estimates the fair value of granted option equity awards using a Black-Scholes options pricing model. The option-pricing model requires a number of assumptions, of which the most significant are share price, expected volatility and the expected option term (the time from the grant date until the options are exercised or expire). Expected volatility is estimated based on volatility of similar companies in the technology sector. The Company has historically not paid dividends and has no foreseeable plans to issue dividends. The risk-free interest rate is based on the yield from governmental zero-coupon bonds with an equivalent term. The expected option term is calculated for options granted to employees and directors using the “simplified” method. Grants to non-employees are based on the contractual term. Changes in the determination of each of the inputs can affect the fair value of the options granted and the results of operations of the Company.

Recent Accounting Pronouncements

On January 1, 2022, the Company adopted ASU No. 2020-06, Debt with Conversion and Other Options (Subtopic 470-20) and Derivatives and Hedging - Contracts in Entity’s Own Equity (Subtopic 815-40). This standard eliminates the beneficial conversion and cash conversion accounting models for convertible instruments. It also amends the accounting for certain contracts in an entity’s own equity that are currently accounted for as derivatives because of specific settlement provisions. In addition, the new guidance modifies how particular convertible instruments and certain contracts that may be settled in cash or shares impact the diluted EPS computation. The adoption of ASU 2020-06 did not have a material impact on the Company’s consolidated financial statements.

On January 1, 2022, the Company adopted ASU No. 2021-04, Earnings Per Share (Topic 260), Debt – Modifications and Extinguishments (Subtopic 470-50), Compensation – Stock Compensation (Topic 718), and Derivatives and Hedging – Contracts in Entity’s Own Equity (Subtopic 815-40): Issuer’s Accounting for Certain Modification or Exchanges of Freestanding Equity-Classified Written Call Options (“ASU 2021-04”), which will clarify and reduce diversity in practice. Specifically, the new standard includes a recognition model comprising four categories of transactions and corresponding accounting treatment for each category. The category that would apply to a modification or an exchange of an equity-classified warrant would depend on the substance of the modification transaction (e.g., a financing transaction to raise equity versus one to raise debt). This recognition model is premised on the idea that the accounting for the transaction should not differ from what it would have been had the issuer of the warrants paid cash instead of modifying the warrants. The adoption of ASU 2021-04 did not have a material impact on the Company’s consolidated financial statements.