UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K/A

(Amendment No. 1)

☒ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the Fiscal Year Ended August 31, 2020

or

☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Commission File Number: 000-55991

PETROTEQ ENERGY INC.

(Exact name of registrant as specified in its charter)

| Ontario | None | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) | |

15315 W. Magnolia Blvd, Suite 120 Sherman Oaks, California |

91403 | |

| (Address of principal executive offices) | (Zip code) |

(866) 571-9613

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the act: None

| Title of each class: | Trading Symbol(s): | Name of each exchange on which registered: | ||

| N/A | N/A | N/A |

Securities registered pursuant to section 12(g) of the Act:

| Common Shares, without par value |

| (Title of Class) |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Non-accelerated filer ☒ | Smaller reporting company ☒ |

| Emerging growth company ☒ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold on the TSX Venture Exchange as of the last business day of the registrant’s most recently completed second fiscal quarter (CAD$0.0950 converted to US$0.0707 on February 28, 2020) was approximately: $13,793,616

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date:

Number of shares of common stock outstanding as of December 14, 2020 was 385,609,435.

Documents incorporated by reference: None.

PETROTEQ ENERGY INC.

EXPLANATORY NOTE

This Amendment No. 1 to our Annual Report on Form 10-K/A for the fiscal year ended August 31, 2020, as filed with the Securities and Exchange Commission on December 23, 2020, is being filed for the following purposes: (a) to provide on the face page of this Amendment No. 1 (i) the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold on the TSX Venture Exchange as of the last business day of our Company’s most recently completed second fiscal quarter, and (ii) the number of shares of common stock outstanding as of December 14, 2020, as such information was inadvertently omitted from the original Form 10-K; (b) to replace all references to “Petroteq Oil Sands Recovery, LLC” with “Petroteq Oil Recovery, LLC” (being the correct name of that entity); (c) to furnish the List of Subsidiaries as Exhibit 21.1, which was inadvertently omitted from the original Form 10-K; (d) to amend the exhibit table to include references to the Extensible Business Reporting Language (XBRL) exhibits included in the original Form 10-K filing and this Amendment No.1; (e) to replace the Certification of Chief Executive Officer filed pursuant to Rule 13a-14(a) of the Exchange Act as Exhibit 31.1 to the original Form 10-K; and (f) to replace the Certification of Chief Executive Officer furnished pursuant to Rule 13a-14(b) as Exhibit 32.1 to the original Form 10-K. Due to an administrative error, the EDGAR versions of Exhibits 31.1 and 32.1 incorrectly identified David Sealock, our Company’s former Chief Executive Officer, as the certifying officer. New Certifications of Chief Executive Officer are filed and furnished herewith as Exhibits 31.1 and 32.1 hereto.

No other changes have been made to the Form 10-K. This Amendment No. 1 to the Form 10-K/A speaks as of the original filing date of the Form 10-K, does not reflect events that may have occurred subsequent to the original filing date, and does not modify or update in any way disclosures made in the original Form 10-K.

NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K/A contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). In particular, statements contained in this Annual Report on Form 10-K/A, including but not limited to, statements regarding the sufficiency of our cash, our ability to finance our operations and business initiatives and obtain funding for such activities; our future results of operations and financial position, business strategy and plan prospects are forward looking statements. These forward-looking statements relate to our future plans, objectives, expectations and intentions and may be identified by words such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “intends,” “targets,” “projects,” “contemplates,” “believes,” “seeks,” “goals,” “estimates,” “predicts,” “potential” and “continue” or similar words. Readers are cautioned that these forward-looking statements are based on our current beliefs, expectations and assumptions and are subject to risks, uncertainties, and assumptions that are difficult to predict, including those identified below, under Part I, Item 1A. “Risk Factors” and elsewhere in this Annual Report on Form 10-K/A. Therefore, actual results may differ materially and adversely from those expressed, projected or implied in any forward-looking statements. We undertake no obligation to revise or update any forward-looking statements for any reason.

NOTE REGARDING COMPANY REFERENCES

Throughout this Annual Report on Form 10-K/A, “Petroteq,” the “Company,” “we,” “us” and “our” refer to Petroteq Energy Inc.

PETROTEQ ENERGY INC.

FORM 10-K/A

TABLE OF CONTENTS

i

BUSINESS OVERVIEW

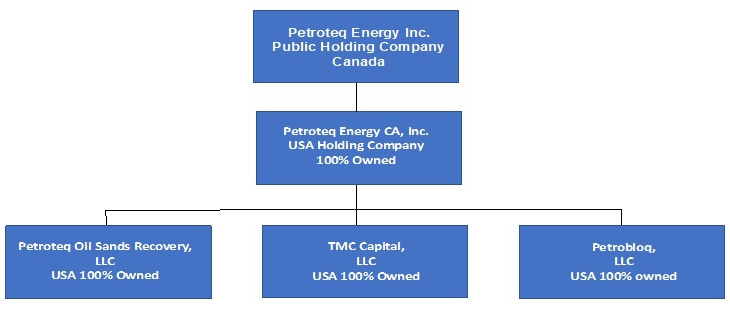

We are a holding company organized under the laws of Ontario, Canada, that is engaged in various aspects of the oil and gas industry. Our primary focus is on the development and implementation of our proprietary oil sands mining and processing technology to recover oil from surface mined bitumen deposits. Our wholly-owned subsidiary, Petroteq Energy CA, Inc., a California corporation (“PCA”), conducts our oil sands extraction business through two wholly owned operating companies, Petroteq Oil Recovery, LLC, a Utah limited liability company (“POSR”), and TMC Capital, LLC, a Utah limited liability company (“TMC”). Another subsidiary, Petrobloq LLC, a California limited liability company (“Petrobloq”), also wholly owned by Petroteq, is currently dormant.

OIL SANDS MINING & PROCESSING

Through our wholly-owned subsidiary PCA, and its two subsidiaries POSR and TMC, we are in the business of oil sands mining operations on the TMC Mineral Lease (as defined and described below) in Uintah County, Utah, where we process mined oil sands ores using our proprietary extraction technology (the “Extraction Technology”) to produce crude oil and hydrocarbon products. Our primary extraction and processing operations are conducted at our Asphalt Ridge processing facility, which is owned by POSR.

Petroteq owns the intellectual property rights to the Extraction Technology which is used at our Asphalt ridge processing facility to extract and produce crude oil from oil sands utilizing a closed-loop solvent based extraction system.

The processing facility, which initially commenced operations as a pilot plant in 2015, was relocated from its original site near Maeser, Utah, to the lands then covered by a Mining and Mineral Lease Agreement dated as of July 1, 2013, between Asphalt Ridge, Inc., as lessor, and TMC, as lessee, (the “Original TMC Mineral Lease”), near our Asphalt Ridge Mine, in 2017 to improve logistical and processing efficiencies in the oil sands recovery process. The relocation of our processing facility occurred during a temporary suspension of our oil sands mining and processing operations that we had initiated in 2016 in the face of a sharp decline in world oil prices. We restarted operations at the end of May 2018, and completed expansion work on the processing facility to increase production to 400-500 barrels of oil per day during the last quarter of fiscal 2019 (the quarter ended August 31, 2019). We continued testing the expanded plant in the first quarter of fiscal 2020 (the quarter ended November 30, 2019) and determined that a number of equipment upgrades were required to support continuous operation of the plant. As discussed below, such upgrades were completed by Greenfield Energy LLC (“Greenfield”) in December 2020.

We had expected to generate revenue from the sale of hydrocarbon products commencing in the third quarter ended May 31, 2020. However, due to the COVID-19 pandemic and volatility in oil prices, we reduced operations to a single shift per day during the quarter ended February 29, 2020, and ultimately suspended production of hydrocarbon products during the quarter ended May 31, 2020.

1

On July 2, 2020, TomCo Energy PLC (“TomCo”) announced that, following the establishment by TomCo of Greenfield as a joint venture company with Valkor LLC (“Valkor”) on June 17, 2020, Greenfield would take over the management and operations of our Asphalt Ridge processing facility. Valkor remains party to a non-exclusive technology licensing agreement with Petroteq dated July 2, 2019, as amended, in respect of the plant.

Since assuming responsibility for the management of the Asphalt Ridge facility in July 2020, Greenfield has made certain upgrades to the plant to improve its capacity and reliability, and is undertaking tests to assess its potential commerciality. All critical equipment has been received and installed at the plant. In addition, buildings have been erected over the nitrogen system and the vapor recovery system, and wind-walls have been erected at the mixing tank area and decanter deck, to better allow for operations during winter months. Pressure testing of piping systems is currently underway as part of plant pre-commissioning activities in preparation for plant start-up, which is expected to occur in late December 2020.

The Company expects that Greenfield will also be in a position to restart mining and ore handling operations in late December 2020. All site personnel completed mandatory Mine Safety and Health Administration (MSHA) training in late November 2020, and rental equipment needed for ore crushing and handling has arrived on site. Valkor has completed its evaluation of recently received mining quotations and has selected a mining contractor. The mining contract has been executed and the mining contractor has already begun mobilizing equipment to site. After initial work to prepare the site, it is expected that mining of oil sands ore will begin in late December 2020.

Even once we resume production, we anticipate that our revenue will be limited until we are at full production. We expect that we will require additional capital to continue our operations and planned growth.

As announced by TomCo on September 16, 2020, the board of TomCo believes that the Pre-FEED (Front-End Engineering and Design) Report prepared by Crosstrails Engineering LLC, a subsidiary of Valkor, provides a high level of confidence that the processes being utilized at the Asphalt Ridge processing facility can be scaled up to enable commercial production of 10,000 barrels of oil per day from a single site. Proof of commerciality though is subject to the successful completion of the upgrade works to the plant, that are currently being completed prior to its restart, and the associated trials to demonstrate the commerciality of the processes used in Petroteq’s Extraction Technology process and the identification and securing of a suitable site for a commercial scale plant.

Once the Asphalt Ridge processing facility has been restarted, Petroteq intends to undertake a series of associated tests and trials, to be verified by an independent third party, to demonstrate both the commerciality of the Extraction Technology process and validate the proposed design for the commercial scale plant, thereby enabling Greenfield to move forward with the final FEED report for a 10,000 barrels of oil per day plant.

In addition, Greenfield has announced that, following the restart of the Asphalt Ridge processing facility, it intends to start working with Quadrise Fuels International plc, regarding a trial of Quadrise’s MSAR® technology at the plant. This will initially comprise the supply of oil samples produced by at the plant to Quadrise to enable them to undertake test work in the United Kingdom to finalize the required MSAR® formulations, before the planned on-site demonstration trial to produce approximately 600 barrels (100 tonnes) of MSAR®. MSAR® is a low viscosity oil-in-water emulsified synthetic heavy fuel oil (“HFO”). It is manufactured using Quadrise’s proprietary technology to mix heavy residual oils with small amounts of specialist chemicals and water to a bespoke formulation. According to Quadrise, the resulting emulsion contains approximately 30% water and less than 1% chemicals. The emulsion is a low viscosity liquid at room temperature, which makes it easier to handle and reduces the heating costs for storing, transportation and use in comparison to HFOs.

As announced by the Company on November 17, 2020, Greenfield has executed a non-exclusive, multi-site license with Petroteq (the “Greenfield License”). The Greenfield License has been granted in consideration for the funding that Greenfield has provided to date in respect of the upgrades to the Asphalt Ridge processing facility, in the aggregate amount of $2,000,000. The Greenfield License will allow Greenfield to use the Extraction Technology in any future oil sands plants built by Greenfield in the United States. The Greenfield License also clarifies the ownership of any intellectual property developed as a result of the Asphalt Ridge processing facility upgrade and associated trials or otherwise developed by Greenfield in the future. Any such intellectual property will be the property of Petroteq and pursuant to the Greenfield License, Petroteq will grant Greenfield the ability to utilize such intellectual property, together with any additional intellectual property developed by Petroteq, in accordance with the terms of the Greenfield License.

For any future oil sands plants built by Greenfield utilizing the Greenfield License, Greenfield will pay Petroteq a 5% royalty of net revenues received from oil products produced from oil sand resources.

2

Oil Sands Exploration and Processing Plant

In June 2011, Petroteq commenced the development of an oil sands extraction facility near Maeser, Utah and entered into construction and equipment fabrication contracts for the purpose of evaluating the Extraction Technology in producing crude oil from the extraction and processing of oil sands mined from the TMC Mineral Lease and from other deposits located in the Asphalt Ridge area. By January 2014 our initial processing facility, designed as a pilot plant having processing capacity of 250 barrels per day, was fully permitted and construction was completed by October 1, 2014. Operations conducted at this initial pilot plant during 2015 allowed us to test and evaluate the Extraction Technology at or near the plant’s capacity. During 2015, the plant produced approximately 10,000 (gross) barrels of oil from the local oil sands ores, including oil sands deposits located within our TMC Mineral Lease. From this production, 7,777.33 barrels of finished crude oil were sold to an oil and gas distributor for resale to its refinery customers, with the balance of the produced oil used internally to power generators for the plant. The initial processing plant was flexible in that it had the ability to produce both high quality heavy crude oil as well as lighter oil if needed.

In 2015, with the sharp decline in world oil prices, Petroteq determined that the transportation costs of hauling mined ore from our mine site to the processing facility, a distance of approximately 17 miles, were adversely affecting the economics of our processing operations. For that reason, we temporarily suspended operations in 2016, and, in 2017, the plant was disassembled and moved from its original location to the site of our Temple Mountain mining site (referred to as the Asphalt Ridge Mine #1) located within the TMC Mineral Lease. During the reassembly of the facility, additional equipment was installed to increase the plant’s capacity from 250 barrels per day to 400-500 barrels per day. In May 2018, mining operations at the Asphalt Ridge Mine #1 recommenced, and the new processing plant commenced a test production phase of heavy crude oil from oil sands deposits at this site. Work to increase the plant’s capacity to 400-500 barrels per day was completed during the last quarter of fiscal 2019 (the quarter ended August 31, 2019). Testing, which continued into the first quarter of fiscal 2020 (the quarter ended November 30, 2019), determined that a number of equipment upgrades were required to support continuous operation of the plant.

Greenfield, a joint venture company established by TomCo and Valkor, assumed responsibility for the management and operations of our Asphalt Ridge processing facility in July 2020. As discussed above, Greenfield has made certain upgrades to the plant to improve its capacity and reliability, and is undertaking tests to assess its potential commerciality.

Resources and Mining Operations

Through its acquisition of TMC in June 2015, Petroteq indirectly acquired certain mineral rights under the TMC Mineral Lease, consisting of the Original TMC Mineral Lease covering approximately 1,229.82 acres of land in the Asphalt Ridge area of Uintah County, Utah. In June 2018, Petroteq, acting through POSR, acquired additional mineral rights under two mineral leases entitled “Utah State Mineral Lease for Bituminous-Asphaltic Sands”, each dated June 1, 2018, between the State of Utah’s School and Institutional Trust Land Administration (“SITLA”), as lessor, and POSR, as lessee, covering lands that largely adjoin the lands covered by the TMC Mineral Lease ( “SITLA Leases”). More recently, in April 2019 and in July 2019, in two separate transactions, TMC acquired an initial 50% and then the remaining 50% of the operating rights under five (5) federal (U.S.) oil and gas leases, administered by the (U.S.) Department of Interior’s Bureau of Land Management (“BLM”), covering lands located in eastern and south-eastern Utah (“BLM Leases”).

As described in more detail below, the Original TMC Mineral Lease was terminated effective August 10, 2020, and a new Short-Term Mining Lease agreement dated as of that date was entered into between Asphalt Ridge, Inc., as lessor, and Valkor as lessee. Valkor and TMC have entered into a Short-Term Mining and Mineral Sub-Lease dated August 20, 2020 (the “TMC Mineral Sub-Lease”) whereby all of the rights and obligations of Valkor, as lessee, have been sub-let to TMC. At this time, Petroteq (through its subsidiaries) holds mineral leases (or the operating rights under leases) covering approximately 8,501.76 net acres within the State of Utah, consisting of 1,229.82 acres held under the TMC Mineral Lease, 1,311.94 acres held under the SITLA Leases and 5.960 acres under the BLM Leases.

The SEC permits oil and gas companies that are subject to domestic issuer reporting requirements under U.S. federal securities law, in their filings with the SEC, to disclose only estimated proved, probable and possible reserves that meet the SEC’s definitions of such terms. The Company has not yet established any reserves.

Between March 14, 2019 and May 31, 2020, we made cash deposits of $1,907,000, included in prepaid expenses and other current assets on the consolidated balance sheets for the acquisition of 100% of the operating rights under U.S. federal oil and gas leases, administered by the BLM in Garfield and Wayne Counties covering approximately 8,480 gross acres in P.R. Springs and the Tar Sands Triangle within the State of Utah. The total consideration of $3,000,000 has been partially settled by the $1,907,000 cash deposit, with the balance of $1,093,000 still outstanding.

3

The following table sets forth the gross/net developed and undeveloped acreage held under the TMC Mineral Sub-Lease.

TMC Mineral Lease Developed/Undeveloped Acreage (Gross/Net) | |

| Total Acreage | |

| Gross Acres | 1,229.82 acres |

| Net Acres | 1,229.82 acres |

| Developed Acreage | |

| Asphalt Ridge Mine #1/Permit Boundaries | |

| Gross Acres | 174.00 acres |

| Net Acres | 174.00 acres |

| Undeveloped Acreage | |

| Acreage Outside Asphalt Ridge Mine #1/Permit Boundaries | |

| Gross Acres | 1,055.82 acres |

| Net Acres | 1,055.82 acres |

The TMC Mineral Lease covers lands situated in or near Utah’s Asphalt Ridge, an area located along the northern edge of the Uintah Basin and containing oil sands deposits located at or near the surface. Most of the oil-impregnated reservoirs or deposits in the Asphalt Ridge area are found in the Rimrock Sandstone (Mesaverde Group Formations) and in the (Tertiary) Duchense River Formation. Substantial bitumen deposits in the Rimrock and Duchense River Formations extend from the northwest in a south-easterly direction through a substantial part of the lands included in the TMC Mineral Lease, particularly the acreage located in T5S-R21E (Section 25) and T5S-R22E (Section 31) where our Asphalt Ridge Mine #1 is located. Bitumen-saturated pay thicknesses in lands covered by the TMC Mineral Lease generally range from 50-200 feet, with some deposits approaching 300 feet in pay thickness. Petroteq believes that oil sands deposits in this area may be mined economically at depths up to 250-300 feet below the surface.

As announced by the Company on October 29, 2020, a recent survey of Petroteq’s lease properties has identified three key areas where the oil sands ore appears to have higher oil saturations than what was previously mined. Samples were taken from each location and lab assays of the samples showed that the ore was a higher quality to that mined previously. These areas are currently anticipated to be the focus of Petroteq’s mining efforts during the initial operation of the Asphalt Ridge processing facility following its restart. In addition, six corehole locations were staked and, subject to rig availability, will be drilled during January. This work is expected to allow Petroteq’s mining consultant to develop a detailed mining plan which would direct future mining operations for extended plant operation. No additional exploratory work has been performed in the preceding three years.

The following tables set forth the gross/net undeveloped acreage held under the SITLA Leases and BLM Leases, respectively.

| SITLA Leases | |

| Developed/Undeveloped Acreage (Gross/Net) | |

| SITLA Lease #53806 | |

| Gross Acres | 833.03 acres |

| Net Acres | 833.03 acres |

| SITLA Lease #53807 | |

| Gross Acres | 478.91 acres |

| Net Acres | 478.91 acres |

| All Acreage is Currently Undeveloped | |

4

BLM Leases Developed/Undeveloped Acreage (Gross/Net) | |

| BLM Lease #U-38071 | |

| Gross Acres | 1,920.00 acres |

| Net Acres | 1,920.00 acres |

| BLM Lease #U-08291G | |

| Gross Acres | 160.00 acres |

| Net Acres | 160.00 acres |

| BLM Lease #U-17781 | |

| Gross Acres | 1,880.00 acres |

| Net Acres | 1,880.00 acres |

| BLM Lease #U-17979 | |

| Gross Acres | 720.00 acres |

| Net Acres | 720.00 acres |

| BLM Lease #U-20860 | |

| Gross Acres | 1,280.00 acres |

| Net Acres | 1,280.00 acres |

| All Acreage is Currently Undeveloped | |

The BLM Leases include lands located either in the P.R. Springs or Tar Sands Triangle areas of Utah, geographic areas that have been designated as a “Special Tar Sands Area” by the (U.S.) Department of Interior.

5

The TMC Mineral Lease

The Original TMC Mineral Lease has been terminated and replaced with (a) a new Short-Term Mining Lease agreement dated as of August 20, 2020 between Asphalt Ridge, Inc., as lessor, and Valkor as lessee, and (b) the TMC Mineral Sub-Lease whereby all of the rights and obligations of Valkor, as lessee, have been sub-let to TMC, as sub-lessee. TMC has the exclusive right to explore for, mine and produce oil and other minerals associated with oil sands, subject to certain depth limits. For ease of reference, the term “TMC Mineral Lease” is used to refer to the Original TMC Mineral Lease or the TMC Mineral Sub-Lease, as applicable.

Previously, TMC was the direct lessee under the TMC Mineral Lease with Asphalt Ridge, Inc., as lessor, which was amended on October 1, 2015 and further amended on March 1, 2016, on February 1, 2018, and most recently on November 21, 2018. The primary term of the TMC Mineral Lease, as amended, commenced July 1, 2013 and continued for six years until June 30, 2019, subject to extension.

The TMC Mineral Sub-Lease it is to remain in effect for a term that coincides and is co-extensive with the term of the Short-Term Mining Lease between Asphalt Ridge, Inc. and Valkor, including any extension or renewal to the term thereof; provided, however, that the TMC Mineral Sub-Lease provides for a termination date of June 30, 2021. The initial term of the Short-Term Mining Lease between Asphalt Ridge, Inc. and Valkor will expire on December 31, 2020, provided that Valkor may extend the term for an additional period of up to 6 months subject to certain conditions, but in no event beyond June 30, 2021.

TMC paid Valkor an initial rental fee in the amount of $25,000 on commencement of the TMC Mineral Sub-Lease, and is obligated to pay Valkor a monthly rental fee of $15,000 during the term of the TMC Mineral Sub-Lease. TMC is also obligated to pay production royalties as follows:

| (a) | For “Bitumen Product” produced from oil sands mined or otherwise extracted from the property, a production royalty equal to 8% of the gross sales revenue received by TMC from the sale of such Bitumen Product. “Bitumen Product” is defined to mean naturally occurring oil in the oil sands that is sold in whatever form, including run-of-mine, screened, processed, or after the addition of any additives and/or upgrading of the Bitumen Product; |

| (b) | Subject to the production royalty described in paragraph (a) above on sales of Bitumen Product that are fully accounted for, a production royalty of 8% of the gross sales revenue received by TMC on all other minerals produced from Bitumen Product mined or otherwise extracted from the property and sold; provided that where sales occur to a third party purchaser that is engaged in marketing a variety of products or by-products made from such materials, and payments to TMC therefore vary, and if TMC’s receipts are measurably greater than comparable sales by others of similar products or by-products which may be due to the nature of high end by-products such as frac sands produced and sold by the third party, the production royalty will be the greater of a 5% royalty on the gross value of the product and by-products sold by the third party or 50% of the gross revenue received by TMC from the sale of such products or by-products, as the case may be; and |

| (c) | On oil and gas, and associated hydrocarbons produced by TMC using standard oil and gas drilling recovery techniques above 3000 feet MSL (mean sea level) and sold, a production royalty of 1/6 of the gross market value. |

6

During the year ended August 31, 2020, we received (gross) proceeds of $290,809 from the sale of upgraded or finished oil produced at our Asphalt Ridge processing facility from oil sands mined under the TMC Mineral Lease. During our fiscal years ending August 31, 2019 we had sales of $59,335 and for the years ended August 31, 2018 and 2017 and 2016, we had no sales of produced oil since, during this period, we temporarily suspended our mining and processing operations during the relocation, reassembly and expansion of our process facility to a new site located within the TMC Mineral Lease.

During the last five (5) months of 2015, we produced approximately 10,000 barrels of oil, with 2,222 barrels consumed as fuel in plant operations and 7,777.33 barrels sold and delivered to an independent purchaser at our processing facility. Our use of produced oil as a fuel source for plant generators in 2015 is no longer necessary since the plant’s power supply is now provided by a local power company.

The costs associated with extraction and processing operations at our Asphalt Ridge processing facility which are used in determining our “Average Production Costs” include the costs of oil sands ore, natural gas liquids, aromatic solvent, operator labor, electricity, propane, nitrogen, water, diesel fuel and rental equipment. The primary costs are the costs of mining oil sands ore, natural gas liquids, aromatic solvents, and labor costs. Other than the aromatic solvents, the condensate used as both a solvent and a feedstock in the processing operations at our Asphalt Ridge facility is produced by processing natural gas liquids through a distillation column, with aromatic solvents then added to the distillate. In addition:

| ● | Our fixed costs generally remain constant without regard to the API gravity of our upgraded crude oil; |

| ● | Our oil sands ore costs, which include our mining costs, the cost of transporting mined ore to our processing facility, and pre-processing costs (crushing etc.) incurred in preparing mined ore for processing, do not vary with the API gravity of the oil produced at our facility, but will decrease over time (subject to economies of scale) as our mining operations expand and oil production increases; and |

| ● | Solvent and condensate costs are based on the market prices that exist for each category of product, which are usually determined by a monthly average of prevailing prices in effect during the month of delivery. Solvent and condensate costs typically increase as the target API gravity for our finished crude oil increases. |

7

During the period of August 2018 through December 2018, our “Average Production Costs” decreased to $27 per barrel of oil produced at our Asphalt Ridge facility. During this period, our fixed costs did not differ materially from our August 2015 to December 2015 fixed costs. We do anticipate that we will experience a decrease in fixed costs per barrel as we increase our capacity and operate at full capacity.

With respect to variable costs, our oil sands ore cost during the 2018 period increased to an average of $6.65 per barrel, due primarily to the quantity and quality of ore processed, but with cost-savings resulting from the relocation of our processing facility to the mine site located within our TMC Mineral Lease. In addition, during the 2018 period, our average cost of aromatic solvent decreased to $0.47 per gallon and the average cost of condensate was substantially lower at $2.75 per barrel, due primarily to our production of heavier oil with an API gravity of between 15 and 25 degrees.

We do not expect our operating costs to materially change as the depth of the Asphalt Ridge #1 Mine increases with additional mining over time. We further anticipate that increased efficiencies in our mining operations and various economies of scale (such as bulk quantity purchases of aromatic solvents at quantity/price discounts), will assist in managing and potentially reducing our average production costs as production at our Asphalt Ridge facility increases over time.

The API gravity for the raw heavy oil or bitumen extracted from oil sands ores initially treated at our Asphalt Ridge processing facility averages approximately 10 degrees. Through the application of the Extraction Technology at our plant, we expect to produce a crude oil having a range of API gravity of between 10 degrees and 12 degrees. Through our solvent formulation and the select distillation capabilities, the plant is able to craft a final crude oil product to meet the specifications of a range of customers.

The finished crude oil produced at our Asphalt Ridge processing facility is currently sold to an independent purchaser under short-term or spot delivery contracts where the purchaser takes delivery of finished crude oil at or near the plant and transports it for resale to a refinery in Nevada. The specifications of the oil produced at the plant are effectively tailored to meet customer (pipeline and refinery) specifications and requirements. From time to time we sell oil produced at our Asphalt Ridge facility pursuant to the terms of product off take agreements However, none of our agreements with our current purchaser and none of the offtake agreements are firm commitments requiring the purchaser to acquire a specified quantity of our produced oil. If we increase our production beyond the needs of our current purchaser, we expect to attempt to find additional purchasers for such additional production. Although we believe that larger production quantities will attract certain purchasers that only purchase larger quantities of product and will require transportation of our products to locations closer to our processing facility, resulting in lower transportation costs, to date we have only had preliminary discussions with such purchasers and have no purchase commitments from such purchasers. If purchasers located closer to our processing facility are not interested in acquiring such additional quantities produced, we may sell our product to purchasers that may require transportation of our products to locations that are further from our processing facility, which would result in higher transportation costs and lower profit margins for us.

Generally, the finished oil produced at our Asphalt Ridge processing facility is sold at a price representing a discount off an average of published prices for West Texas Intermediate (WTI) crude oil for a specified period. WTI crude oil is commonly used as a benchmark in pricing oil under oil sales/purchase contracts, particularly in the United States. The discount off the WTI benchmark price is based on a number of factors, including differences that may exist between the specifications of our crude oil and those of WTI crude oil together with the cost of transporting our crude oil to delivery points. Since WTI crude oil generally has an API gravity of between 37-42 degrees, a heavier oil having a lower API gravity in the range of the oil produced at our processing facility will be valued and sold at a price reflecting a discount off the WTI benchmark price.

We anticipate that, as production from our oil sands facility increases, longer term contracts will be secured by POSR utilizing market-based pricing formulas.

8

The SITLA Leases

The SITLA Leases have a primary term of ten (10) years and will remain in effect thereafter for as long as (a) bituminous sands are produced in paying quantities, or (b) POSR is otherwise engaged in diligent operations, exploration or development activity and certain other conditions are satisfied. Generally, the term of the SITLA Leases may not be extended beyond the twentieth year of their effective dates except by production in paying quantities. An annual minimum royalty of $10 an acre must be paid during the first ten years of the SITLA Leases; from and after the 11th year of the leases, the annual minimum royalty may be adjusted by the lessor based on certain “readjustment” provisions in the SITLA Leases. Annual minimum royalties paid in any lease year may be credited against production royalties accruing in the same year.

The BLM Leases

In April 2019, TMC acquired an undivided 50% of the operating rights under the BLM Leases, consisting of the right to explore for and produce oil from oil sands formations and deposits from the surface down to a subsurface depth of 1,000 feet. The operating rights assigned and transferred to TMC under certain of the BLM Leases also grant to TMC the right, subject to similar depth limitation, to explore for and produce oil and gas from conventional sources. Each of the BLM Leases includes lands that are located within a “Special Tar Sands Area” or “STSA”, a geographic area that has been designated by the (U.S.) Department of Interior as containing substantial deposits of oil sands.

The BLM Leases were originally issued by BLM under the Mineral Leasing Act of 1920 (the “MLA”). However, because the definition of “oil” in the MLA prior to 1981 did not include oil produced from oil sands, the BLM Leases (and all other federal onshore mineral leases issued prior to 1981) did not authorize the development and recovery of oil from oil sands, tar sands and bitumen-impregnated rocks and sediments. The Combined Hydrocarbon Leasing Act of 1981 (“CHL Act”) expanded the definition of “oil” to include oil produced from oil sands and bitumen deposits and authorized the issuance of new “combined hydrocarbon leases” or “CHLs” that permit exploration and production of oil and gas from both conventional sources and from oil sands deposits.

For federal onshore mineral leases that were in effect on November 16, 1981 (the CHL Act’s enactment date) and included lands located within an STSA, the CHL Act granted to lessees the right to convert such leases to new CHLs. Upon issuance by BLM, each CHL will constitute a new lease that will remain in effect for a primary term of ten (10) years and thereafter for as long as oil or gas is produced in paying quantities.

Each of the BLM Leases has been included in an application to BLM requesting their conversion to new CHLs. During the pendency of such applications, the term (and any operations) of the BLM Leases are in “suspension status” under BLM regulations until the new CHLs are issued.

Summary of Production Royalties Payable

Technology Transfer Agreement

Pursuant to the terms of a technology transfer agreement dated November 7, 2011 that we entered into with Vladimir Podlipskiy, the developer of the Extraction Technology, we are obligated to pay Mr. Podlipskiy a royalty on production from each processing plant that we own or operate that uses the Extraction Technology, starting with the construction and operation of a second plant. The royalty, if and at such time as it becomes payable, will consist of 2% of gross sales if the price of heavy oil is below $60.00 per barrel; 3% of gross sales if the price of heavy oil is between $60.00 and $69.99 per barrel; 3.5% of gross sales if the price of heavy oil is between $70.00 and $79.99 and 4% of gross sales if the price of heavy oil is greater than $80.00 per barrel.

TMC Mineral Lease

Under the TMC Mineral Lease, TMC holds 100% of the working interests (subject to a 1.6 % overriding royalty previously granted to Temple Mountain Energy, Inc.).

In addition, TMC was required to make certain advance royalty payments to the lessor. During the period from July 1, 2018 to June 30, 2020, the minimum payments were $100,000 per quarter. The minimum payments were to increase to $150,000 per quarter with effect from July 1, 2020. The TMC mineral lease was terminated during August 2020, and replaced with a sub-lease entered into with Valkor.

Production royalties payable under the sub-lease with Valkor are 8% of the gross sales revenue, subject to certain adjustments.

9

SITLA Leases

The SITLA Leases provide that Petroteq must pay: (i) an annual rent equal to the greater of $1 an acre or a fixed sum of $500 (without regard to acreage); and (ii) a production royalty of 8% of the market price received for products produced from the leases at the point of first sale, less reasonable actual costs of transportation to the point of first sale. After the tenth year of the Leases, the lessor may increase the royalty rate by as much as one percent (1%) per year up to a maximum of 12.5%, subject to a proviso that production royalties under the leases shall never be less than $3.00/bbl during the term of the Leases. As the sole lessee under the SITLA Leases, POSR owns 100% of the working interests under the Leases, subject to payment of annual rentals, advance annual minimum royalties, and production royalties.

BLM Leases

Under the BLM Leases, production royalties are governed by BLM regulations and are payable to the U.S. Department of Interior at the rate of 12.5% of the amount or value of the production removed and sold. The interests acquired by TMC under the BLM Leases are also subject to a 6.25% overriding royalty reserved by predecessors-in-title.

Permits and Taxes

On September 15, 2008, a large mining permit was granted to TME Asphalt Ridge, LLC by the State of Utah Division of Oil, Gas, and Mining (“UDOGM”) for the mining and development of the Asphalt Ridge Mine #1, an open pit mine located on land included within the TMC Mineral Lease.

On or about July 9, 2015, UDOGM approved an application filed by TMC to transfer the “Notice of Intention to Commence Large Mining Operations” for the Asphalt Ridge Mine #1 (Permit # M/047/0089) from TME Asphalt Ridge LLC to TMC. On October 27, 2017, UDOGM granted final approval to TMC’s “Amended Notice of Intention to Commence Large Mining Operations” and issued final Permit # M/047/0089 authorizing TMC to conduct operations at Asphalt Ridge Mine #1.

Mining operations, including the initial development of the mine at the property and removal of a portion of the overburden soil layer, have already been performed. In addition to the mining permits, all environmental, construction, utility and other local permits necessary for the construction of the plant and the processing of the oil sands have been granted to Petroteq.

Specifically, a Groundwater Discharge Permit was issued by the Utah Department of Environmental Quality (Division of Water Quality, Water Quality Board) (“UDEQ”), on July 26, 2016 (expiration on July 27, 2021), covering disposal of tailings from ore sands produced from the land area encompassed by the Asphalt Ridge Mine #1. This permit was required by Utah law even though our processing facility does not use a water-based process, and authorizes a return of residual sand tailings to the mine for backfill and capping. A Small Source Registration air permit was issued by UDEQ by a letter dated November 2, 2018. The letter confirms that our processing facility at Asphalt Ridge is exempt from any requirement of additional air quality permits since the facility produces less emissions than the level that would require a special air permit. A Conditional Use Permit (“CUP”) was issued by the Uintah County (Utah) Commission to us on January 29, 2018, for the operation of our current processing facility. The CUP is a right/interest in land under Utah law and will continue in effect in perpetuity.

The oil and gas properties (including plants, equipment etc.) included in or under the TMC Mineral Lease are subject to the State of Utah’s property (ad valorem) tax. The actual tax rate is established by each county in the State (and therefore may vary) and is generally assessed against the “fair market value” of the property. Under Utah Code § 59-2-1103, the oil and gas properties included in the SITLA Leases are exempt from the State’s property (ad valorem) tax (although this exemption does not apply to improvements on state lands).

Under Utah Code § 59-5-120, beginning January 1, 2006 and ending June 30, 2026, no severance (production) tax will be imposed on oil and gas produced from oil sands (tar sands). Accordingly, severance tax will not be owed to the State of Utah on the production of oil and hydrocarbon substances from the TMC Mineral Lease or the SITLA Leases until after June 30, 2026.

10

Extraction Technology

Petroteq intends to continue to develop its operations by processing native oil sands ore produced through the mining operations of its subsidiary (TMC) and potentially through purchased native oil sands ore, using its patented closed loop, continuous flow, scalable and environmentally safe Extraction Technology. The Extraction Technology process allows the extraction of hydrocarbons from a wide range of oil sands deposits and other hydrocarbon sediment types. Petroteq’s oil extraction process takes place in a completely closed loop system that continuously recirculates and recycles the solvent after it has separated the bitumen and heavy oils from the oil sands. The closed loop system is capable of recovering up to 99% of all hydrocarbons from the oil sands. The only two end products of the process are high quality heavy oil and clean sand, making this technology environmentally benign.

The Extraction Technology, which has been modified since 2015 and unlike the technology utilized in 2015, utilizes no water in the process, is anticipated to produce minimal greenhouse gases, and is expected to extract up to 99% of all hydrocarbon content and recycle up to 95% of the solvents. The proprietary solvent composition is expected to dissolve up to 99% of heavy bitumen/asphalt and other lighter hydrocarbons from the oil sands and prevent their precipitation during the extraction process. Solvents used in this composition form an azeotropic mixture which has a low boiling point of 50 – 65 °C (degrees Celsius) and it is expected to allow recycling of over 95% of the solvent.

In the oil extraction and upgrade process utilized at our Asphalt Ridge processing facility, the bitumen crude oil that we extract from mined oil sands has an average API gravity of 9-12 degrees.

No diluents or blending agents are used to reduce the viscosity of the heavy oil extracted from bitumen saturated ores. Instead, varying amounts of solvent are introduced into an extraction tank containing raw oil sands ore that has been crushed prior to being added to the extraction tank. The solvent is designed to release the crude oil from bitumen-saturated ore during the initial extraction process.

The crude oil containing solvent is then introduced or subjected to a simple flash distillation process where virtually all of the solvent is recovered and recycled for future use.

The oil extraction process, as it exists in the pilot plant, has a Feed/Bottoms heat exchanger, a Solvent Vaporizer (heat exchanger), a Solvent Scrubber (vessel), air-cooled condensers, an air-cooled product cooler, a Bitumen Product Pump, and an oil heater plus a propane tank as the energy source. The bitumen/solvent slurry is routed via a pump to the Feed/Bottoms Exchanger where it is pre-heated both to cool the exiting product as well as to integrate the heat available from the flash distillation process. This pre-heated slurry is then heated in the Solvent Vaporizer to approximately 405°F to vaporize essentially all of the solvent from the bitumen product. This two-phase stream is then flashed across a control valve and routed to the Solvent Scrubber where the gaseous solvent stream exits the vessel and is routed to air-cooled condensers where it will be liquified and returned to the storage vessel to be re-used. The resultant hot bitumen is pumped through the Feed/Bottoms exchanger via the Bitumen Product Pump and cooled prior to entering an air-cooled exchanger where it is cooled to 180°F, the temperature at which the product is stored. If it is desired that solvent be left in the bitumen for transportation purposes, the temperature of that back end flash distillation process can be controlled.

11

Petroteq has received patents in the United States, Canada and Russia that protect the claims and processes embodied in the Extraction Technology. See “Intellectual Property” below.

INTELLECTUAL PROPERTY

On March 27, 2013, Petroteq entered into an intellectual property license agreement in a private arm’s length transaction with a Canadian company, TS Energy Ltd., which has agreed to act as the sole and exclusive licensee of the Extraction Technology within Canada and the Republic of Trinidad and Tobago.

On July 2, 2019, Petroteq entered into an intellectual property license agreement with Valkor LLC, a company based in Katy, Texas, for the non-exclusive, non-transferable use of the Extraction Technology worldwide (subject to any exclusive license agreements in effect) in the engineering, construction and operation of oil sands extraction plants. The agreement requires Valkor to invest (or secure investment of) a minimum of US$20 million towards the construction of an oilsands plant by December 2020, and to have in production a minimum of 1,000 barrels per day. The agreement also requires Valkor to pay a one-time non-refundable license fee of US$2 million per oil sands plant commissioned, with 50% payable upon start of construction and the remainder payable upon first production. The agreement further provides that Valkor will pay a five percent (5%) royalty based on annual gross sales for so long as the licensed technology is covered by a valid claim in the country in which it is used.

We rely upon patents to protect our intellectual property. We have obtained patents in the United States, Canada and Russia that protect the Extraction Technology. The following sets forth details of our issued patents.

| DOCKET | TITLE | COUNTRY | DATE FILED SERIAL NO. |

DATE ISSUED PATENT NO./STATUS | ||||

| 1492.2 | Oil From Oil Sands Extraction Process |

USA | 09/26/12 13/627,518 ----------------------- 10/07/11 61/545,034 |

02/06/18 9,884,997 Expires: 10/07/31 |

Summary: A system for extracting bitumen from oil sands includes an extractor tank which incorporates a plurality of jet injectors. Operationally, the jet injectors provide jet streams of an extractant in the extractor tank that creates a fluidized bed of the extractant. A reaction between crushed oil sands and the fluidized bed then separates bitumen from the oil sands.

12

Corresponding Foreign Patent Properties

| DOCKET | TITLE | COUNTRY |

DATE FILED SERIAL NO. |

DATE ISSUED PATENT NO./STATUS | ||||

| 11492.2a | Oil Extraction Process | Canada | 09/30/11 2,754,355 | Received Notice of Allowance; patent payment submitted to Commission of Patents | ||||

| 11492.2d | Oil From Oil Sands Extraction Process | Russia | 04/28/14 2014117162 | 12/20/15 2571827 Expires: 09/27/2032 |

THE OIL SANDS MARKET

As an unconventional hydrocarbon resource, oil sands hold hundreds of billions of barrels of oil on a worldwide basis. Although Canada is the only country that is currently extracting large quantities of oil from its oil sands deposits, the United States also has large oil sands resources that can be developed. In a 2007 Report entitled “A Technical, Economic, and Legal Assessment of North American Oil Shale, Oil Sands, and Heavy Oil Resources In Response to Energy Policy Act of 2005 Section 369(p)” (September 2007), prepared by the Utah Heavy Oil Program, Institute For Clean and Secure Energy and The University of Utah for the U.S. Department of Energy (the “2007 Report”), the authors reported the following estimates, which estimates were based upon source material published in 1979, 1987 and 1993:

| ● | The United States has an estimated 76 billion barrels of oil-in-place (“OIP”) (OIP are not estimates of reserves or recoverable resources) from bitumen and heavy oil contained in oil sands resources; |

| ● | In the United States, Utah is known to have the largest oil sands deposits, with total resource estimates ranging from 23 to 32 billion barrels of OIP from bitumen and heavy oil contained in oil sands formations and deposits; and |

| ● | Within the state of Utah, the region that has experienced the most oil sands development, both in terms of existing oil production and supporting infrastructure, is the Asphalt Ridge area located on the northern edge of the Uintah Basin in eastern Utah. In the 2007 Report, it is estimated that about one (1) billion barrels of OIP exist in the form of bitumen and heavy oil contained in oil sands formations and deposits in the Asphalt Ridge area. |

From our own investigation of the oil sands deposits in the Asphalt Ridge area of Utah, we believe that a substantial part of the oil sands deposits in this area are accessible through outcroppings or in shallow depths with limited or no overburden. In our view, the location and accessibility of oil sands deposits in Asphalt Ridge create an opportunity for commercial development, supported by positive economics, using surface mining techniques and our extraction technology.

The worldwide growing demand for heavy crude oil and the recent decline in heavy crude oil production in countries such as Venezuela makes the high quality, low Sulphur, heavy oil found in oil sands deposits in the United States a valuable resource that has been underdeveloped to date. The development of “tight shale” oil plays in the United States has produced significant quantities of light, sweet crude oil reserves, but heavy oil development in the United States has lagged. To date, oil sands development has been limited by the absence of a viable technology that can extract heavy oil and bitumen from the oil sands deposits in an economical and environmentally responsible manner. To that end, Petroteq has developed and patented an extraction technology that aims to develop oil sands reserves in an economical and environmentally responsible manner. Petroteq is currently expanding its commercial oil sands extraction operations in the Asphalt Ridge area, utilizing a process that is economical, environmentally benign and produces high quality heavy oil.

13

We have tested our Extraction Technology both at Asphalt Ridge and with oil sands sourced from different parts of the world and having different hydrocarbon chemical compositions. To date, we have conducted tests with oil sands from Russia, China, Indonesia and the Middle East. Our tests with Russian oil sands, which were the only tests of our Extraction Technology with oil sands from different parts of the world that were conducted by third parties, were conducted in Ufa, Bashkorkostan (Russia) by a third party (KVADRA) retained by us to perform the tests using a multi-ton pilot plant, used the local oil sands ore with oil saturation in a range of 7-10%, and resulted in industrial quantities of heavy oil. From the tests conducted in Ufa, an average of 70 metric tons of raw oil sands material were processed per day resulting in 5,475 kg of heavy asphaltenic oil per day. Other tests, consisting of oil sands samples from China, Indonesia and Jordan, were conducted internally at Petroteq’s laboratory in San Diego using lab bench testing with our own solvent blend that produced approximately one to two pound quantities. By introducing the solvent mixture to crushed and treated ore containing bitumen oil, the oil was separated by recycling the solvent with a laboratory-scale rotor vacuum evaporator. Sand tailings were separated by centrifuge and dried under the vacuum.

Through our testing of oil sands sourced from different countries, we found that the efficiency and consistency of Petroteq’s extraction technology are not affected by differences in the chemical composition of the oil/bitumen in the oil sands. Despite relatively significant differences in oil/bitumen chemistry, both the efficiency and consistency of our extraction technology remained intact, resulting in an oil recovery efficiency that in each test exceeded 99%. We believe that this testing demonstrates that the Extraction Process is universal in its application and does not depend on the material source or the hydrocarbon content or fingerprint.

REGULATION

Exploration and production operations are subject to various types of regulation at the federal, state and local levels. This regulation includes requiring permits to drill wells, maintaining bonding requirements to drill or operate wells, and regulating the location of wells, the method of drilling and casing wells, the surface use and restoration of properties on which wells are drilled, and the plugging and abandoning of wells. Full mining permits have been granted to POSR from the State of Utah Division of Oil, Gas, and Mining for the mining and development of the Asphalt Ridge Mine #1 located in the Asphalt Ridge area of Utah. In addition to the mining permits, all environmental, construction, utility and other local permits necessary for the construction of the plant and the processing of the oil sands have been granted to POSR. Our operations are also subject to various conservation laws and regulations.

Typically, oil enhancements such as hydraulic fracturing operations are overseen by state regulators as part of their oil and gas regulatory programs; however, the (U.S.) Environmental Protection Agency (“EPA”) has asserted federal regulatory authority over certain hydraulic fracturing activities involving diesel under the Safe Drinking Water Act and has released draft permitting guidance for hydraulic fracturing activities that use diesel in fracturing fluids in those states where EPA is the permitting authority. As a result, we may be subject to additional permitting requirements for our operations. These permitting requirements and restrictions could result in delays in operations at well sites as well as increased costs to make wells productive. In addition, legislation introduced in Congress provides for federal regulation of hydraulic fracturing under the Safe Drinking Water Act and requires the public disclosure of certain information regarding the chemical makeup of hydraulic fracturing fluids. Moreover, on November 23, 2011, the EPA announced that it was granting in part a petition to initiate a rulemaking under the Toxic Substances Control Act, relating to chemical substances and mixtures used in oil and gas exploration and production. Further, on May 4, 2012, the BLM issued a proposed rule to regulate hydraulic fracturing on public and Indian land.

On August 16, 2012, the EPA published final rules that establish new air emission control requirements for natural gas and NGL production, processing and transportation activities, including New Source Performance Standards to address emissions of sulphur dioxide and volatile organic compounds, and National Emission Standards for Hazardous Air Pollutants (NESHAP) to address hazardous air pollutants frequently associated with gas production and processing activities. Among other things, these final rules require the reduction of volatile organic compound emissions from natural gas wells through the use of reduced emission completions or “green completions” on all hydraulically fractured wells constructed or refractured after January 1, 2015. In addition, gas wells are required to use completion combustion device equipment (e.g., flaring) by October 15, 2012 if emissions cannot be directed to a gathering line. Further, the final rules under NESHAP include maximum achievable control technology (MACT) standards for “small” glycol dehydrators that are located at major sources of hazardous air pollutants and modifications to the leak detection standards for valves. Compliance with these requirements, especially the imposition of these green completion requirements, may require modifications to certain of our operations, including the installation of new equipment to control emissions at the well site that could result in significant costs, including increased capital expenditures and operating costs, and could adversely impact our business.

14

In addition to these federal legislative and regulatory proposals, some states such as Pennsylvania, West Virginia, Texas, Kansas, Louisiana and Montana, and certain local governments have adopted, and others are considering adopting, regulations that could restrict hydraulic fracturing in certain circumstances, including requirements regarding chemical disclosure, casing and cementing of wells, withdrawal of water for use in high-volume hydraulic fracturing of horizontal wells, baseline testing of nearby water wells, and restrictions on the type of additives that may be used in hydraulic fracturing operations. For example, the Railroad Commission of Texas adopted rules in December 2011 requiring disclosure of certain information regarding the components used in the hydraulic fracturing process. In addition, Pennsylvania’s Act 13 of 2012 became law on February 14, 2012 and amended the state’s Oil and Gas Act to impose an impact fee for drilling, increase setbacks from certain water sources, require water management plans, increase civil penalties, strengthen the Pennsylvania Department of Environmental Protection’s (PaDEP) authority over the issuance of drilling permits, and require the disclosure of chemical information regarding the components in hydraulic fracturing fluids.

We believe that the technologies we use are cleaner and environmentally friendlier than the known fracking or tar sand technologies. Regulatory and social resistance sometimes prohibits fracking recovery methods in some states.

OSHA and Other Laws and Regulations.

We are subject to the requirements of the federal Occupational Safety and Health Act (OSHA), and comparable state laws. The OSHA hazard communication standard, the EPA community right-to-know regulations under the Title III of CERCLA and similar state laws require that we organize and/or disclose information about hazardous materials used or produced in our operations. Also, pursuant to OSHA, the Occupational Safety and Health Administration has established a variety of standards related to workplace exposure to hazardous substances and employee health and safety.

Oil Pollution Act.

The Federal Oil Pollution Act of 1990 (“OPA”) and resulting regulations impose a variety of obligations on responsible parties related to the prevention of oil spills and liability for damages resulting from such spills in waters of the United States. The term “waters of the United States” has been broadly defined to include inland water bodies, including wetlands and intermittent streams. The OPA assigns joint and several strict liability to each responsible party for oil removal costs and a variety of public and private damages. We believe that we are in compliance with the OPA and the federal regulations promulgated thereunder in the conduct of our operations.

Clean Water Act.

The Federal Water Pollution Control Act (Clean Water Act) and resulting regulations, which are primarily implemented through a system of permits, also govern the discharge of certain contaminants into waters of the United States. Sanctions for failure to comply strictly with the Clean Water Act are generally resolved by payment of fines and correction of any identified deficiencies. However, regulatory agencies could require us to cease construction or operation of certain facilities or to cease hauling wastewaters to facilities owned by others that are the source of water discharges. We believe that we substantially comply with the Clean Water Act and related federal and state regulations.

COMPETITION

Competition in the oil industry is intense. We compete with other companies seeking to acquire sub economic oil fields, many with substantial financial and other resources. We will also compete with technologies such as gas injection, polymer flooding, microbial injection and thermal methods. As a new technology, we also compete with many of the other technologies that have been proven to be economically successful in enhancing oil production in the United States. As a result of this competition, we may be unable to attract the necessary funding or qualified personnel. If we are unable to successfully compete for funding or for qualified personnel, our activities may be slowed, suspended or terminated, any of which would have a material adverse effect on our ability to continue operations. However due to the innovative nature of our technology and the ecological benefit it provides, while remaining economically efficient, we believe that competition will not be a significant impediment to our operations or expansion.

15

IMPLICATIONS OF BEING AN EMERGING GROWTH COMPANY

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”), and therefore we intend to take advantage of certain exemptions from various public company reporting requirements, including not being required to have our internal controls over financial reporting audited by our independent registered public accounting firm pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”) even if we cease to be a smaller reporting company with annual revenues of less than $100 million, reduced disclosure obligations regarding executive compensation in our periodic reports and proxy statements and exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and any golden parachute payments. We may take advantage of these exemptions until we are no longer an “emerging growth company.” In addition, the JOBS Act provides that an “emerging growth company” can delay adopting new or revised accounting standards until such time as those standards apply to private companies. We have elected to use the extended transition period for complying with new or revised accounting standards under the JOBS Act. This election allows us to delay the adoption of new or revised accounting standards that have different effective dates for public and private companies until those standards apply to private companies. As a result of this election, our financial statements may not be comparable to companies that comply with public company effective dates.

We will remain an “emerging growth company” until the earlier of (1) the last day of the fiscal year: (a) following the fifth anniversary of the date of the first sale of our common shares pursuant to an effective registration statement filed under the Securities Act; (b) in which we have total annual gross revenue of at least $1.07 billion; or (c) in which we are deemed to be a large accelerated filer, which generally means the market value of our common shares that is held by non-affiliates exceeded $700.0 million as of the last business day of our most recently completed second fiscal quarter, and (2) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period. References herein to “emerging growth company” have the meaning associated with that term in the JOBS Act.

ENFORCEABILITY OF CIVIL LIABILITIES

We are a company incorporated in Ontario, Canada. Certain of our directors and officers named in this registration statement reside outside the U.S. In addition, some of our assets and the assets of our directors and officers are located outside of the United States. As a result, it may be difficult for investors who reside in the United States to effect service of process upon these persons in the United States. You may also have difficulty enforcing, both in and outside the United States, judgments you may obtain in U.S. courts against us or these persons in any action, including actions based upon the civil liability provisions of U.S. federal or state securities laws.

Furthermore, there is substantial doubt whether an action could be brought in Canada in the first instance predicated solely upon U.S. federal securities laws. Canadian courts may refuse to hear a claim based on an alleged violation of U.S. securities laws against us or these persons on the grounds that Canada is not the most appropriate forum in which to bring such a claim. Even if a Canadian court agrees to hear a claim, it may determine that Canadian law and not U.S. law is applicable to the claim. If U.S. law is found to be applicable, the content of applicable U.S. law must be proved as a fact, which can be a time-consuming and costly process. Certain matters of procedure will also be governed by Canadian law.

History and Development of the Company

We were incorporated as “AXEA Capital Corp.” on January 4, 2008 pursuant to the Business Corporations Act (British Columbia). On October 15, 2012, MCW Energy Group Limited (“MCW NB”), a corporation incorporated in the Province of New Brunswick, completed a reverse acquisition of AXEA Capital Corp. (the “RTO”) and as a result MCW NB became a wholly owned subsidiary of AXEA Capital Corp. which also changed its name from “AXEA Capital Corp.” to “MCW Enterprises Ltd.” Pursuant to articles of continuance filed on December 7, 2012, MCW NB changed its jurisdiction of governance by continuing from the Province of New Brunswick into the Province of Ontario. Pursuant to articles of continuance filed on December 12, 2012, MCW Enterprises Ltd. changed its jurisdiction of governance by continuing from the Province of British Columbia into the Province of Ontario and changed its name to MCW Enterprises Continuance Ltd. Pursuant to a certificate of amalgamation dated December 12, 2012, MCW Enterprises Continuance Ltd. and MCW NB amalgamated in the Province of Ontario and continued under the name “MCW Energy Group Limited”.

We are governed by the Business Corporations Act (Ontario) and our registered office is located at Suite 6000, 1 First Canadian Place, PO Box 367, 100 King Street West, Toronto, Ontario M5X 1E2, Canada. Our executive office is located at 15315 W. Magnolia Blvd., Suite 120, Sherman Oaks, California 91403. Our telephone number is (866) 571-9613.

16

Our common shares are publicly traded on the TSX Venture Exchange (the “TSXV”) under the trading symbol “PQE”, the Frankfurt Exchange under the trading symbol PQCF.F and on the OTC Pink under the trading symbol “PQEFF”.

Pursuant to articles of amendment filed on May 5, 2017, we changed our name from “MCW Energy Group Limited” to “Petroteq Energy Inc.” and we changed our TSXV trading symbol from MCW to PQE. On June 2, 2017, our OTCQX trading symbol was changed from MCW to PQEFF. Since March 15, 2018, our stock has traded on the OTC Pink market when it no longer traded on the OTCQX International Market.

On May 5, 2017, we effected a share consolidation (reverse stock split) on a 1-for-30 basis. Unless otherwise included, all shares amounts and per share amounts in this registration statement have been prepared on a pro forma basis to reflect the 1-for-30 reverse stock split of our outstanding common shares. On November 23, 2018, our shareholders approved a resolution authorizing our Board of Directors to consolidate our shares on a basis of up to ten for one. No consolidation has been effected to date.

We determined that the Company ceased to qualify as a foreign private issuer (as defined in Rule 405 under the Securities Act of 1933, as amended, and Rule 3b-4 under the Securities Exchange Act of 1934, as amended) as of February 28, 2019 (being the last business day of the second fiscal quarter of the fiscal year ended August 31, 2019), and therefore ceased to be eligible to rely on the rules and forms available to foreign private issuers on August 31, 2019.

Additional information related to our company may be found on our website at www.petroteq.energy. Information contained in our website does not form part of the registration statement and is intended for informational purposes only.

The following risks relate specifically to our business and should be considered carefully. Our business, financial condition and results of operations could be harmed by any of the following risks. As a result, the trading price of our common shares could decline and the holders could lose part or all of their investment.

We face business disruption and related risks resulting from the recent outbreak of the novel coronavirus 2019 (“COVID-19”), which could have a material adverse effect on our business and results of operations.

In an effort to contain and mitigate the spread of COVID-19, many countries, including the United States and Canada, have imposed unprecedented restrictions on travel, and there have been business closures and a substantial reduction in economic activity in countries that have had significant outbreaks of COVID-19. The pandemic has had a material adverse effect on our operations. We have scaled back to a skeleton crew and we have suspended production of hydrocarbon products, because of the effects of the recent decline in oil pricing, we are no longer operating (in terms of the cost to produce and sell oil, excluding G&A) on a breakeven basis. We do not plan to resume production until oil prices return to sustainable profitable levels.

Significant uncertainty remains as to the potential impact of the COVID-19 pandemic on our operations, and on the global economy as a whole. Government-imposed restrictions on travel and other “social-distancing” measures such restrictions on assembly of groups of persons, have the potential to disrupt supply chains for parts and sales channels for our products, and may result in labor shortages.

It is currently not possible to predict how long the pandemic will last or the time that it will take for economic activity to return to prior levels. We will continue to monitor the COVID-19 situation closely, and intend to follow health and safety guidelines as they evolve.

We expect the ultimate significance of the impact of these disruptions, including the extent of their adverse impact on our financial and operational results, will be dictated by the length of time that such disruptions continue, which will, in turn, depend on the currently unknowable duration of the COVID-19 pandemic and the impact of governmental regulations that might be imposed in response. Our business could also be impacted should the disruptions from COVID-19 lead to changes in commercial behavior. The COVID-19 impact on the capital markets could impact our cost of borrowing. There are certain limitations on our ability to mitigate the adverse financial impact of these items, including the fixed costs of our operations. COVID-19 also makes it more challenging for management to estimate future performance of our businesses, particularly over the near to medium term.

17

We have a limited operating history, and may not be successful in developing profitable business operations.

Our oil extraction segment has a limited operating history. We have generated limited revenue from our oil sands mining and processing activities, and do not anticipate generating any significant revenue from these activities until our Asphalt Ridge processing facility is fully operational. Even once we are fully operational, our business operations must be considered in light of the risks, expenses and difficulties frequently encountered in establishing a business in the oil extraction business.

We have an insufficient history at this time on which to base an assumption that our oil sands mining and processing operations will prove to be successful in the long-term. Our future operating results will depend on many factors, including:

| ● | our ability to raise adequate working capital; |

| ● | the success of our development and exploration; |

| ● | the demand for oil; |

| ● | the level of our competition; |

| ● | our ability to attract and maintain key management and employees; and |

| ● | our ability to efficiently explore, develop, produce or acquire sufficient quantities of marketable gas or oil in a highly competitive and speculative environment while maintaining quality and controlling costs. |

To achieve profitable operations in the future, we must, alone or with others, successfully manage the factors stated above, as well as continue to develop ways to enhance or increase the efficiency of our mining and processing operations that are being conducted in the Asphalt Ridge area in eastern Utah. Despite our best efforts, we may not be successful in our exploration or development efforts or obtain the regulatory approvals required to conduct our operations.

We have suffered operating losses since inception and we may not be able to achieve profitability.

At August 31, 2020, August 31, 2019 and August 31, 2018, we had an accumulated deficit of ($90,664,349), ($78,285,282) and ($62,497,396), respectively and we expect to continue to incur increasing expenses in the foreseeable future as we develop our oil extraction business. We incurred a net loss of ($12,379,067) and ($15,787,886) for the years ended August 31, 2020 and August 31, 2019, respectively. As a result, we are sustaining substantial operating and net losses, and it is possible that we will never be able to develop or sustain the revenue levels necessary to attain profitability.