UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| ☒ | ANNUAL REPORT UNDER TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

or

| ☐ | TRANSITIONAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transitional period from _____________ to ______________

Commission file number 333-189731

DIEGO PELLICER WORLDWIDE, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 33-1223037 | |

| (State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

6160 Plumas Street, Suite 100, Reno, NV 89519

(Address of principal executive offices) (Zip Code)

(516) 900-3799

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class registered: | Name of each exchange on which registered: | |

| None | None |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act: Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 day. Yes ☐ No ☒

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulations S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 if the Exchange Act.

| Large Accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☒ | Smaller reporting company | ☒ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

There was no active public trading market as of the last business day of the Company's second fiscal quarter, so there was no aggregate market value of common stock held by non-affiliates.

As of May 26, 2020, the registrant had 130,247,932 shares issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None.

TABLE OF CONTENTS

| 2 |

CAUTIONARY NOTE REGARDING FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K (the "Annual Report") contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, or the Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Forward-looking statements discuss matters that are not historical facts. Because they discuss future events or conditions, forward-looking statements may include words such as “anticipate,” “believe,” “estimate,” “intend,” “could,” “should,” “would,” “may,” “seek,” “plan,” “might,” “will,” “expect,” “anticipate,” “predict,” “project,” “forecast,” “potential,” “continue” negatives thereof or similar expressions. Forward-looking statements speak only as of the date they are made, are based on various underlying assumptions and current expectations about the future and are not guarantees. Such statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, level of activity, performance or achievement to be materially different from the results of operations or plans expressed or implied by such forward-looking statements.

We cannot predict all of the risks and uncertainties. Accordingly, such information should not be regarded as representations that the results or conditions described in such statements or that our objectives and plans will be achieved and we do not assume any responsibility for the accuracy or completeness of any of these forward-looking statements. These forward-looking statements are found at various places throughout this Annual Report on Form 10-K and include information concerning possible or assumed future results of our operations, including statements about potential acquisition or merger targets; business strategies; future cash flows; financing plans; plans and objectives of management; any other statements regarding future acquisitions, future cash needs, future operations, business plans and future financial results, and any other statements that are not historical facts.

These forward-looking statements represent our intentions, plans, expectations, assumptions and beliefs about future events and are subject to risks, uncertainties and other factors. Many of those factors are outside of our control and could cause actual results to differ materially from the results expressed or implied by those forward-looking statements. In light of these risks, uncertainties and assumptions, the events described in the forward-looking statements might not occur or might occur to a different extent or at a different time than we have described. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of the Annual Report on Form 10-K. All subsequent written and oral forward-looking statements concerning other matters addressed in this Annual Report on Form 10-K and attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this Annual Report on Form 10-K.

Unless otherwise provided in this Annual Report, references to the “Company,” “Diego,” “we,” “us” and “our” refer to Diego Pellicer Worldwide, Inc.

| 3 |

Explanatory Note

Diego Pellicer Worldwide, Inc. (the “Company”) disclosed in its Form 8-K filed on March 30, 2020 that it would be relying on the March 4, 2020 Securities and Exchange Commission Order under Section 36 of the Securities Exchange Act of 1934 Granting Exemptions from Specified Provisions of the Exchange Act and Certain Rules Thereunder, the Partnership (as superseded by the order dated March 25, 2020) delayed the filing of this Annual Report on Form 10-K, originally due Monday, March 30, 2020. The primary reasons for the delay were due to the circumstances related to COVID-19. COVID-19-related shelter-in-place orders and office closures severely affected transportation and limited access to the facilities of the Company and staff. This resulted in disruptions to the Company’s staff which delayed our ability to complete our audit and the Company’s ability to prepare the Report. The Company was unable, without unreasonable effort or expense, to file its Annual Report on Form 10-K for the year ended December 31, 2019 (the “Annual Report”) by the May 29, 2020 extended deadline (which is 60 days from the Report’s original filing deadline of March 30, 2020).

| 4 |

PART I

Overview of the Market

The cannabis market has a multi-billion dollar potential. The industry is in its infancy and is rapidly being propelled towards its potential by the state legalization and the rush by suppliers to meet the pent-up demand. Most suppliers are small unsophisticated but capable operators. The federal legal constraints provide an opportunity to those companies early to the market to gain a first mover advantage and to the successful ones, an opportunity to be a consolidator in the industry. How can a company establish itself as a prestigious national brand when federal laws prohibit the sale of these products? How can a legitimate company respect these laws and be the first mover in the retail and wholesale trade in this industry?

What is Diego's Strategy, Phases One and Two?

Diego is a real estate and a consumer retail development company that is focused on high quality recurring revenues resulting from leasing real estate to licensed cannabis operators, and the management of operations for these and other third party cannabis operators deriving income from management and royalty fees. Diego provides a competitive advantage to these operators by developing “Diego Pellicer” as the world’s first premium marijuana brand and by establishing the highest quality standards for its facilities and products.

The Company's first phase strategy is to lease and develop the most prominent and convenient real estate locations for the purposes of leasing them to state licensed operators in the cannabis industry. Diego's first phase revenues result from leasing real estate and selling non-cannabis related accessories to our tenants. The Company has developed a brand name strategy, providing training, design services, branded accessories, systems and systems training, locational selection, and other advisory services to their tenants. We enter into branding agreements with our tenants. In addition, part of the vetting process in finding the proper tenant is selecting a tenant that shares the Company's values and strictly complies with state laws, follows strict safety and testing requirements and provides consistent, high-quality products. If the tenants do not comply, they will not be allowed to use the brand.

The second phase of our strategy is to secure options to purchase the tenant's operations. When mutually advantageous for Diego and the tenant, Diego will negotiate acquisition contracts with selected Diego operators/tenants. When it becomes federally legal to do so, Diego will execute the acquisition contracts, consolidate our selected tenants and become a nationally branded marijuana retailer and producer concurrent with the change of federal law.

Diego Pellicer Management Company, will license the upscale Diego Pellicer brand to qualified operators and receive royalty payments, while providing expertise in retail, product and manufacturing from Diego’s accomplished management team with extensive industry experience

Value Proposition

Value proposition 1: By providing branding, management experience, training, unique accessories, purchasing services, locational experience, standardized design, and experienced construction supervision, the tenant reduces his startup time, reduces cash drain, increases his efficiency, and builds his gross margin. Diego provides the capital for preopening lease costs and tenant improvements. This results in a turnkey retail location for the tenant. Thus, Diego’s real estate, management, consulting and accessory sales are positioned to deliver a premium return on our investment.

Value proposition 2: With each lease, Diego negotiates an acquisition contract with selected licensed tenants to acquire their operations. This contract will be executed at Diego's option, and upon changes to federal law , introduces our second value proposition-ownership of operations in an industry that is projected to exceed $8 billion by 2019.

Revenue Generation and Growth

Diego generates current revenue and stages future revenue streams through the following processes:

| ● | Acquire target properties to be improved for the growing, processing, distribution, and sale of medical and recreational marijuana, extracts and ancillary products. |

| ● | Build and lease turnkey Retail, Processing and/or Growing facilities. |

| ● | The Company may choose to secure management contracts with other retail and grow facilities to manage the business the “Diego Way.” This will generate additional revenue with which we can further expand our network of stores. |

| 5 |

| ● | Negotiate merger agreements with favored partners that will trigger when marijuana commerce becomes legal federally. |

| ● | Own DP Brands and other intellectual property. |

| ● | Charge reasonable rents and management fees to tenants or operators to recover all build-out, start-up investment plus profit margin, and management expertise over the lease term. |

| ● | Sell non-cannabis branded products lines such as apparel and edibles to Diego stores. |

| ● | Create an e-commerce platform selling non-cannabis branded merchandise |

| ● | Continue to build and market the brand utilizing all forms of media including traditional and digital media, social media, e-commerce, and strategic partners. |

Why We Believe this is a Winning Strategy

When the US and countries around the world legalize the commerce of marijuana on a national and international platform, Diego is positioning itself to be a dominate player in the marijuana marketplace. Diego will accomplish this by being a fully integrated marijuana retail operation and premium brand, capitalizing on the beautifully designed retail stores offering the finest quality products at competitive prices.

Most industries evolve through the same business cycle. Many small independent companies initially operate in fragmented markets in the early stages. Then there is a consolidation of the industry, with the consolidators thriving and the independent companies dwindling. The larger companies have access to cheaper capital, lower costs, better merchandising, brand name recognition, and more efficient operations. This what we offer out tenants when negotiating the lease: an agreement to acquire them when marijuana is legalized. This gives the tenant the ultimate opportunity to participate in the rapid consolidation that we believe will happen when marijuana is legalized. This consolidation will result in companies that have heretofore been unable to participate in the rapidly growing industry to be scrambling to enter the space. Diego and its tenants will already be established and consolidated. As an exit strategy, we want to position Diego to be a likely candidate for acquisition or a major player in the marketplace.

What we accomplished in 2019

2019 was a time of continued growth and a change of focus for the Company. An effective and experienced team was assembled from within our operators to develop our newly formed management company, and to complement the current executives with knowledge and experience in real estate operations, banking, site selection, branding, facility design, corporate finance, investor relations, store management, and grow expertise, Additional capital needed to be raised in order to have sufficient capital to help support our operators expand within their markets, and to begin the expansion into different markets in the US. Much of the Company’s debt was renegotiated, and additional commitments were formalized for the expansion in the Colorado market. New markets had to be explored, new alliances forged, and opportunities prioritized.

New markets were explored. Three facilities continued to see year upon year increases in revenues, which lead to increased rental revenue cash-flow to the Company. In 2019, Diego focused on our Colorado operations, and divested itself from the Washington tenant, citing restrictive rules and regulations for public company involvement in any part of the Washington State marijuana industry. Diego received revenues from three Colorado facilities, and the first quarter for our Washington store. Diego now had four facilities generating rent in 2019 for the year and we have actively been expanding in the Colorado markets with potential acquisitions for our tenants, and our management company. The tenants growing their sales and improving operational efficiency. Diego worked with these tenants, partially forbearing on their rent so as to allow these operators to strengthen their position and become capable of paying full rents. The properties generating rents in 2019 are as follows:

Table 1: Property Portfolio

| Purpose | Size | City | State | |||||||||

| Retail store (recreational and medical) | 3,300 sq. | Denver | CO | |||||||||

| Cultivation warehouse | 18,600 sq. | Denver | CO | |||||||||

| Cultivation warehouse | 14,800 sq. | Denver | CO | |||||||||

| Retail store (recreational and medical) - Sold | 4,500 sq. | Seattle | WA |

Diego’s Washington tenant opened our first flagship store in Seattle in October 2016. On May 6, 2019, the Company entered into an agreement with a third party, which the Company sold the Seattle leased location provided $550,000 in capital and executive resources for expansion which the company allocated to its efforts in a new location and cannabis grow facilities in Colorado. The Colorado tenant opened the Diego Denver branded flagship store in February 2017. In addition, Diego’s two cultivation facilities in Denver, CO began production in late 2016. The retail facilities have shown steady growth in sales since their opening. The three Colorado properties were subleased to a single entity. The Company is currently is exploring the acquisition of this entity.

| 6 |

Diego Pellicer Denver

| 7 |

Diego will continue this strategy in states where recreational or medical marijuana sales and cultivation is legal under state law. Our business model is recurring lease revenue, royalties, management fees, and is entirely scalable. Our success will dependent upon continuing to raise capital for expansion, continual improvement of our business model, standardizing store design, controlling costs, new store management opportunities, and continuing to develop the brand.

What does our premium branding accomplish?

A very important aspect of our marketing plan is to build Diego Pellicer as a luxury brand. This not only enables us to establish a premium brand, but also to generate significant revenues from non- cannabis products.

| 8 |

The Company is establishing several levels of branding and will use these to appeal to the various segments of the marketplace depending upon the location, competition, legal constraints, and budget. Standard store templates are being developed, complimentary accessories selectively designed, and customer preferences and segments analyzed.

| 9 |

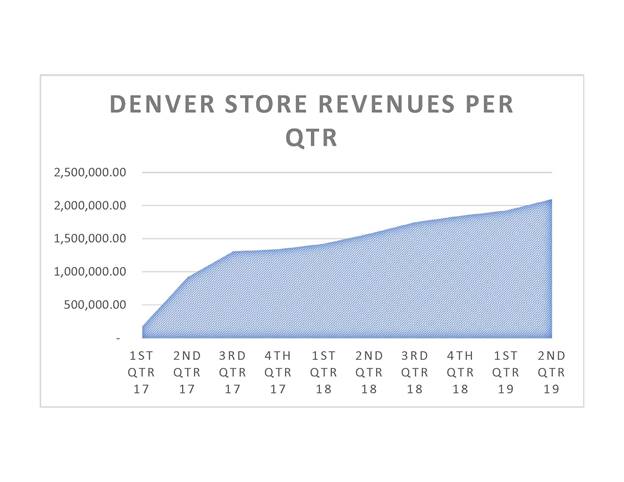

Our Seattle and Denver stores have been met with enthusiastic demand growing revenues quickly. This is proving the initial Diego concept.

The Industry: Retail Sales Continue to Rise Rapidly

Legalization of marijuana is a very recent movement. California was the first to legalize in 1996 when medical marijuana was approved. Nine states and the District of Columbia have legalized the drug for recreational purposes, according to the National Conference of State Legislatures. More than half the states (31) – plus the District of Columbia, Guam and Puerto Rico – have legalized it for medical purposes. The list of states that have legalized marijuana could expand this November. Voters in Michigan and North Dakota will decide whether to allow recreational use. Marijuana remains illegal under U.S. federal law.

| 10 |

Source: 2018 Marijuana Business Daily, a division of Anne Holland Ventures Inc.

| 11 |

The growth in public support for legal marijuana comes as a growing number of states have legalized the drug for medical or recreational purposes in recent years.

About six-in-ten Americans (62%) say the use of marijuana should be legalized, reflecting a steady increase over the past decade, according to a new Pew Research Center survey. The share of U.S. adults who support marijuana legalization is little changed from about a year ago – when 61% favored it – but it is double what it was in 2000 (31%).

| 12 |

As in the past, there are wide generational and partisan differences in views of marijuana legalization. Majorities of Millennials (74%), Gen Xers (63%) and Baby Boomers (54%) say the use of marijuana should be legal. Members of the Silent Generation continue to be the least supportive of legalization (39%), but they have become more supportive in the past year.

Source: Pew Research Center

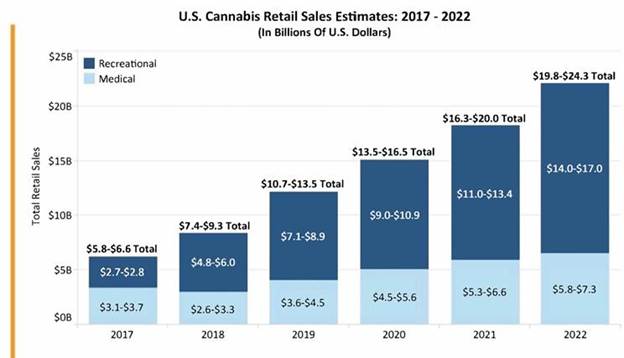

Annual cannabis retail sales continue to grow year-over-year as new markets emerge and more states legalize medical and recreational marijuana. Sales in 2018 are projected to increase by roughly 35% from 2017, on pace to reach more than $8 billion by the end of the year.

By 2022, annual retail marijuana sales in the United States could top $22 billion, which would represent more than a 250% increase from 2017.

| 13 |

Source: 2018 Marijuana Business Daily, a division of Anne Holland Ventures Inc.

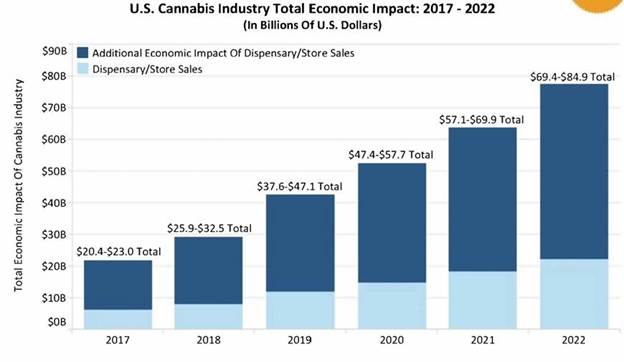

The retail and medical marijuana industry brought in an estimated $39 - $48 billion of economic impact in 2019 just in the USA. By 2023, we expect the potential for the industry to surpass $100 billion in annual economic benefit.

Estimates for economic impact are based on an impact multiplier of 3.5. This means that for every $1 a consumers spend at dispensaries or recreational stores, another $2.50 in economic benefit will be created in the cities, states and ultimately the nation.

Here are some of the factors in this overall economic impact:

| · | The launch of new businesses |

| · | Hundreds of millions of dollars in state and local taxes |

| · | Real estate investments |

| · | Visiting tourists spending money to legally consume |

| · | Marijuana employees circulating earnings back into the economy |

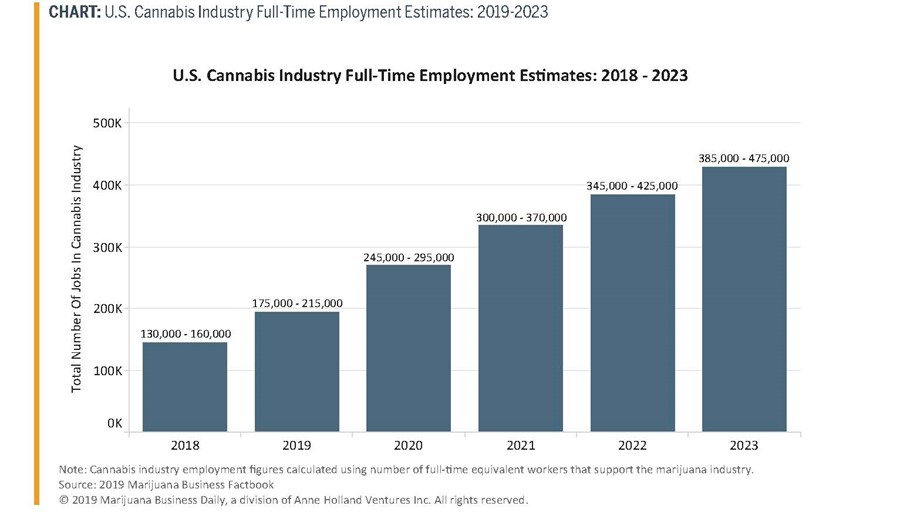

Overall the marijuana labor market has increased about 34% over last year with marijuana industry supporting about 175,000-215,000 employees. A majority of this growth has come in California, which is the next market Diego is focusing it’s attention on acquisitions, and branding agreements. In 2019, marijuana employment surpassed that of the technology industry of web developers and is fast approaching the number of clergy in the USA.

The continued growth in the cannabis market, including legalizing the growing and retailing of hemp based products has boosted the rapid growth in employees and retail sales. The industry is expected to add more than 235,000 full-time jobs between now and 2023 with compounding annual growth rates of 22% and should lead to over 475,000 jobs by 2023.

Outside of California, however, sales are expected to continue climbing, bolstered by ongoing growth in mature markets like New Mexico and Arizona, increased patient access in Florida and new MMJ programs coming online in Maryland and Pennsylvania. The transition to fully regulated, state-licensed MMJ sales in Michigan has caused some short-term instability, but it remains one of the largest medical markets in the country and will likely continue to form the foundation of the MMJ industry for years to come.

As more states continue to legalize medical and recreational marijuana sales, an ever increasing number of adults are introduced, or re-introduced to the product. Continued research into the benefits of CBD derived from both the Marijuana and hemp plants, has catapulted the cannabis industry into the mainstream media. Legal sales of recreational and medical marijuana reached about $8.6 - $10 billion in sales for 2018, about twice that spent on tobacco cigarettes. It is estimated that total demand for cannabis including legally produced product is in excess of $50 - $60 billion

By 2023, we project total retail and medical marijuana sales in the United States will reach approximately $28 billion annually - more than a threefold increase from estimated annual sales in 2017. Our estimates account for the fact that more states will likely legalize medical or adult-use marijuana in the coming years - though it's difficult to predict when that will happen and how big those markets will be. Using a range of estimates that incorporate several factors - such as the likelihood of a given state passing a legalization measure, the size of the customer/patient base and time frame for the launch of sales - helps account for this uncertainty. Our approach is refined over time as more information becomes available.

It's important to point out that the marijuana industry has a big and growing impact on the economy at large as the revenue it generates ripples across a community, city and/ or state - as well as the nation. To understand an industry's economic impact, traditional macroeconomic multipliers can range anywhere from 10 to 20 times the original dollar spent. Based on new data from other industries, we've settled on a standard multiplier of 3.5 for the marijuana industry - a slight revision from last year's multiplier of four.

In other words, for every $1 consumers/patients spend at dispensaries and rec stores, an additional $2.50 of economic value will be injected into the economy - much of it at the local level.

| 14 |

Source: 2018 Marijuana Business Daily, a division of Anne Holland Ventures Inc. (Note that our goal is to provide conservative, realistic financial forecasts that reflect the high degree of uncertainty in the industry. Total cannabis sales in any given calendar year are highly dependent upon progress made - or not made - in each individual state. California is currently the big wild card, as the slow rollout of its statewide regulatory system makes it difficult to get a handle on the exact size of this enormous market. As more information comes to light over time, it could change our estimates for California and, therefore, the industry at large.)

Where are the Greatest Market Opportunities?

All eyes are on California.

That's the reality for nearly everyone involved in the global marijuana market. Companies around the world - from Europe to Canada to Israel and beyond - want a piece of the California market. But there are plenty of practical ramifications. No other state or federal government in the world has tried to implement such a wide-ranging regulatory system that affects tens of thousands of existing black- and gray-market businesses.

The bottom line: The sheer immensity of the California cannabis market is topped only by its complexity. And that complexity has led to major struggles and big wait times for entrepreneurs looking to tap the California market potential. California's MJ regulatory system covers a population of 40 million and includes incentives for existing businesses to transition to the licit tax-paying industry.

There are plenty of other hurdles for existing and future businesses as well, including local license caps from towns and counties that are hesitant to grant permits to any type of cannabis companies. As of early October 2018, only a fraction of local governments had opted to allow rec companies to set up shop within their borders, and state business permits are dependent on a company first obtaining local authorization of some sort. Plenty of companies are striving to play by the rules, but they're often unable to stay in business while doing so because they haven't been able to find locations that fit all the legal parameters for licensing.

The same is true for thousands of small-scale growers in California, as well as edibles makers, concentrate producers and other plant-touching businesses. One option for such companies, at least for now, is to focus on the medical marijuana market instead of rec. Far more local governments allow limited medical companies than adult-use businesses. Obtaining such permits could be a stopgap move, because as time goes on, it's likely that more and more local governments will decide to permit rec. Another option could be to pivot into an alternate cannabis sector, such as distribution or testing labs, given that there's a dearth of both key business types in the state.

Hemp and CBD

Hemp was once prized for making rope. Two hundred years later, the plant still has us tied in knots. From a patchwork of state hemp rules to confusion among cannabis entrepreneurs about the definition of hemp, uncertainty reigns in the hemp industry. Hemp has long been bedeviled by its conflation with marijuana, and the Controlled Substances Act banned its production for decades. That changed in 2014, when the U.S. Farm Bill opened the door for a hemp revival in states willing to experiment (and control) the crop's return to legal production. The federal government defines hemp as cannabis sativa with a THC content at or below 0.3%.

| 15 |

The Farm Bill set off an explosion of hemp production and experimentation and has given cannabis entrepreneurs new opportunities to grow, sell and buy cannabis in a nonintoxicating form. As of October 2018, hemp production is legal under at least limited circumstances in 41 states. The Farm Bill allows limited interstate commerce for hemp - something still off-limits to marijuana entrepreneurs. And hemp businesses report fewer banking and regulatory headaches (though barriers certainly exist in these areas), compared to their marijuana-producing colleagues.

The U.S. hemp experiment is still unfolding. Market conditions vary widely. Some states ban all hemp production; others allow some but not all farmers to grow it; and a handful of states invite all farmers to try hemp and even offer to help market the crop and find companies to process it. U.S. agriculture authorities consider hemp legal only if it is grown as part of a state-backed pilot project, so the USDA keeps no records of the nation's nascent hemp industry.

Not all U.S. states use the federal THC guidelines to define hemp, and the 0.3% THC threshold has little basis in science, meaning that scientists don't agree how much THC a plant needs to produce a high when heated and consumed. Cannabis plants have more than 100 cannabinoids, of which THC is only one, and hemp products with no detectable THC can still be considered psychoactive if they contain cannabinoids that relieve anxiety or depression. At least one state, Iowa, explicitly dictates that cannabidiol is legal but highTHC marijuana is not legal - then goes on to say it accepts cannabidiol with a THC limit 10 times higher than the federal threshold for legal hemp.

Still, the 0.3% THC threshold is a useful metric for dividing marijuana from hemp, and it is the standard used in this Factbook.

Longtime hemp prohibition in the United States has left the industry frozen in time. There is little modern agricultural equipment appropriate for hemp harvesting and processing, and the crop likely won't match the market share it enjoyed before the Industrial Revolution, when hemp fibers were commonly used in commercial fabrics. Today, hemp's value comes mostly from its flower, rich in cannabinoids beyond THC. The most valuable as of this report is CBD, a cannabinoid with established therapeutic uses including pain relief and reducing muscle spasms associated with epilepsy or muscular sclerosis.

Hemp Industry Daily estimates that the U.S. market for hemp-derived CBD will hit approximately $500 million in 2018, with the potential to eclipse $3 billion annually by 2022 - a 500% increase in just four years.

Expect hemp-derived cannabinoid products low in THC to take increasing market share (and media attention) in the overall cannabis industry.

Source: 2018 Marijuana Business Daily, a division of Anne Holland Ventures Inc.

What Benchmarks could Diego be Measured Against?

Diego was one of the first to the market with a real estate holding and branding business model; however, other companies have since adopted similar strategies. Key differentiators between Diego and its competitors are superior branding, optimized build-out and turnkey grow and retail development, pre-negotiated acquisition contracts, and most importantly a branded management company. Table 4 provides a financial benchmark of other cannabis.

Table 4: Financial Benchmark-millions

| Market Cap at 5/28/2020 | Most Recent Revenue | Cost of Revenue | Gross Margin % | Net Profit | For the year ended | |||||||||||||||||||||||||||||||||

| General Cannabis Corp(CANN) | $ | 21.60 | M | $ | 3,666 | $ | 2,467 | 33 | % | $ | (12,462 | ) | 12/31/2019 | |||||||||||||||||||||||||

| Mountain High Acquisitions Corp. (MYHI) | 3.35 | M | 141 | 0 | 100 | % | (5,434 | ) | 3/31/2019 | |||||||||||||||||||||||||||||

| Innovative Industrial Properties, Inc.(IIPR) | 1,461.32 | M | 44,667 | 1,315 | 97 | % | (23,475 | ) | 12/31/2019 | |||||||||||||||||||||||||||||

M J Holdings Inc.(MJNE) |

11.83 | M | 8 | 10 | N/A | (5,007 | ) | 12/31/2018 | ||||||||||||||||||||||||||||||

| 16 |

Status of Federal Law

While marijuana is legal under the laws of several U.S. States, at the present time the concept of “medical marijuana” and “retail marijuana” do not exist under U.S. federal law. The United States Federal Controlled Substance Act classifies marijuana as a Schedule I drug. As defined under U.S. federal law, a Schedule I drug or substance has a high potential for abuse, no accepted medical use in the United States, and a lack of safety for the use of the drug under medical supervision.

The United States Supreme Court has ruled in several cases that the federal government does not violate the federal constitution by regulating and criminalizing cannabis, even for medical purposes. Therefore, federal law criminalizing the use of marijuana pre-empts state laws that legalizes its use for medicinal and recreational purposes.

Attorney General Jeff Sessions' January 2018 decision to rescind the Cole Memo raised some concerns in the marijuana industry that federal officials may try to interfere with legal cannabis. Those concerns, for the most part, haven't materialized, but the scare did get many marijuana businesses thinking about the possibility of federal interference and what could be done about it.

The memo was drafted during the Obama administration by former U.S. Deputy Attorney General James Cole in 2013 as a way to minimize the threat of federal crackdowns against legal marijuana businesses. The document essentially instructed federal law enforcement not to interfere with state-licensed marijuana businesses complying with state laws and certain conditions, such as not selling product to minors or into the black market.

While the Cole Memo clearly expressed an Obama administration policy of leaving legal marijuana businesses alone, it was not a legal change - which only Congress can do. Therefore, the Cole Memo technically allowed U.S. attorneys to go after marijuana businesses if they wanted. With the sending of the Cole Memo to the proverbial shredder, U.S. attorneys no longer have guidelines on how to deal with state-licensed marijuana businesses. But in an April 2018 conversation with Republican U.S. Sen. Cory Gardner, President Donald Trump pledged to keep the Department of Justice from interfering with state cannabis laws and, perhaps more significantly, support legislation protecting state-legal marijuana businesses. White House officials later confirmed the president's policy stance.

The news is being celebrated by advocates working to reform marijuana laws, but many are wary of taking President Trump at his word as nothing has been codified that would prevent him from reversing course.

Several bills have been introduced to Congress seeking to reform federal marijuana laws in different ways, including the removal of cannabis from the list of controlled substances, allowing MJ companies to access traditional banking services and amending the IRS code to more fairly tax cannabis businesses. Similar bills have been introduced in previous sessions of Congress, but none have gained significant traction. This time, however, may be different, as marijuana reform has become a bipartisan issue that has the support of many prominent Republicans.

Senate Majority Leader Mitch McConnell, for example, introduced a bill in April to remove federal barriers on hemp, while former Republican House Speaker John Boehner recently disclosed his involvement with a large, multistate cannabis company.

Whether any significant reform of federal marijuana policy happens in 2018 and what shape it could take remains an open question, but it's clear that attitudes toward cannabis on Capitol Hill are shifting.

Source: 2018 Marijuana Business Daily, a division of Anne Holland Ventures Inc.

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide the information under this item.

None.

Our principal executive office is located at 9030 Seward Park Ave S. #501, Seattle, Washington 98118.

We currently are not a party to any material litigation or other material legal proceedings. From time to time, we may become involved in various lawsuits and legal proceedings which arise in the ordinary course of business. However, litigation is subject to inherent uncertainties and an adverse result in these or other matters may arise from time to time that may harm our business. We are currently not aware of any such legal proceedings or claims that we believe will have a material adverse effect on our business, financial condition or operating results.

Not applicable.

| 17 |

PART II

Item 5. Market for Registrant's Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

There is no established public trading market for our common stock. As of the date of this Report, there are outstanding options and warrants to purchase 374,305 shares of common stock of the Registrant.

The table below sets forth the range of quarterly high and low closing sales prices for its common stock for 2019 and 2018. The quotations below reflect inter-dealer prices, without retail mark-up, mark-down or commission and may not represent actual transactions:

| High | Low | |||||||

| Year ended December 31, 2019 | ||||||||

| First Quarter | $ | 0.02 | $ | 0.01 | ||||

| Second Quarter | $ | 0.03 | $ | 0.01 | ||||

| Third Quarter | $ | 0.06 | $ | 0.02 | ||||

| Fourth Quarter | $ | 0.12 | $ | 0.05 | ||||

| High | Low | |||||||

| Year ended December 31, 2018 | ||||||||

| First Quarter | $ | 1.80 | $ | 0.58 | ||||

| Second Quarter | $ | 0.50 | $ | 0.17 | ||||

| Third Quarter | $ | 0.24 | $ | 0.11 | ||||

| Fourth Quarter | $ | 0.25 | $ | 0.02 | ||||

Record Holders

As of April 30, 2020, there were approximately 201 shareholders of record holding a total of 127,693,963 shares of common stock. The holders of the common stock are entitled to one vote for each share held of record on all matters submitted to a vote of shareholders. Holders of the common stock have no preemptive rights and no right to convert their common stock into any other securities. There are no redemption or sinking fund provisions applicable to the common stock.

Dividends

The Registrant has not declared any cash dividends since inception and does not anticipate paying any dividends in the foreseeable future. The payment of dividends is within the discretion of the Board of Directors and will depend on the Company's earnings, capital requirements, financial condition, and other relevant factors. There are no restrictions that currently limit the Registrant's ability to pay dividends on its common stock other than those generally imposed by applicable state law.

Unregistered Sale of Equity Securities

During the year ended December 31, 2019, $842,712 of notes and $60,627 of accrued interest was converted into 48,684,667 shares of common stock.

We issued 4,987,610 shares of common stock, valued at $170,348, for services.

We issued 24,566,400 shares of common stock, valued at $732,029, for related party services.

During the year ended December 31, 2019, 8,071,000 shares were issued for cashless warrant exercise.

During the year ended December 31, 2019, we issued 5,000 shares for $2,648, which were authorized in prior period.

In connection with the issuances of the foregoing securities, the Company relied on the exemptions from registration provided by Section 4(a) (2) of, and Rule 506 of Regulation D promulgated under, the Securities Act of 1933, as amended, for transactions not involving a public offering.

Item 6. Selected Financial Data

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide the information under this item.

| 18 |

Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations

The following discussion and analysis of the results of operations and financial condition of Diego Pellicer Worldwide, Inc. (the “Company”, “we”, “us” or “our”) should be read in conjunction with the financial statements of Diego Pellicer Worldwide, Inc. and the notes to those financial statements that are included elsewhere in this Form 10-K This discussion includes forward-looking statements based upon current expectations that involve risks and uncertainties, such as our plans, objectives, expectations and intentions. Actual results and the timing of events could differ materially from those anticipated in these forward-looking statements as a result of a number of factors, including those under sections in the financial statements and footnotes included in the Company’s Form 10-K filed on June 2, 2020 for the year ended December 31, 2019. Words such as “anticipate,” “estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “believe,” “intend,” “may,” “will,” “should,” “could,” and similar expressions are used to identify forward-looking statements.

Overview

Diego Pellicer Worldwide, Inc. was established on August 26, 2013 to take advantage of growing market for legalized cannabis being made possible by the escalating legislation allowing for the legalization of cannabis operations in the majority of states:

The industry is operating under stringent regulations within the various state jurisdictions. The Company’s primary business plan is twofold: First to lease various properties to licensed operators in these jurisdictions to grow, process and sell cannabis and related products, and the second the Diego Pellicer Management Company, will license the upscale Diego Pellicer brand to qualified operators and receive royalty payments, while providing expertise in retail, product and manufacturing from Diego’s accomplished management team with extensive industry experience, The Company will also provide educational training, compliance consultation, branding, and related accessories to their tenants. These leases and management agreements are expected to provide substantial streams of income. We believe that as laws evolve, it is possible that we will have the opportunity to participate directly in these operations. Accordingly, the Company will selectively negotiate an option on our tenants’ operating company.

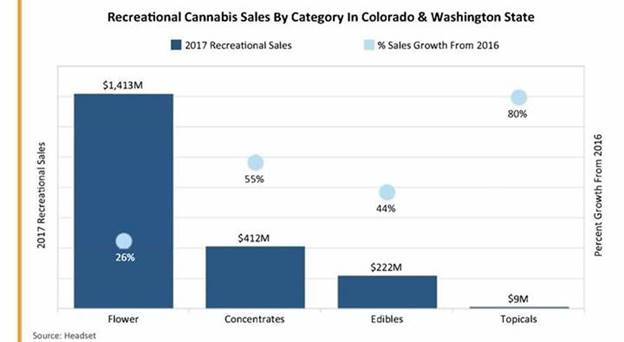

The Company has already established four facilities in markets that have experienced high growth, Washington and Colorado. This growth is illustrated in the tables below:

| 19 |

Source: Headset & 2018 Marijuana Business Daily, a division of Anne Holland Ventures Inc.

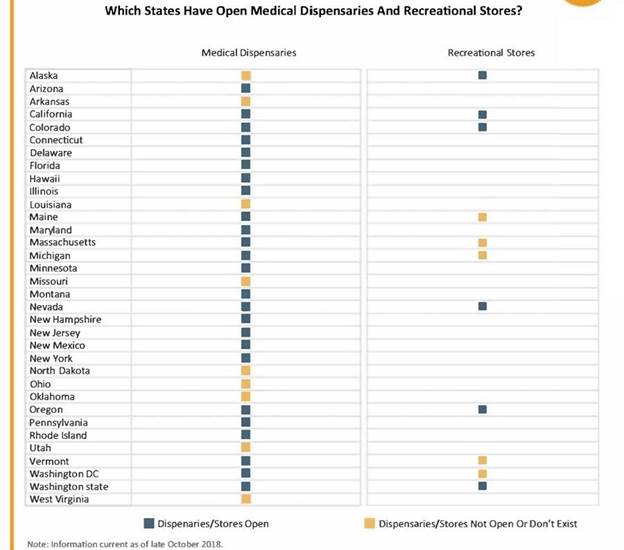

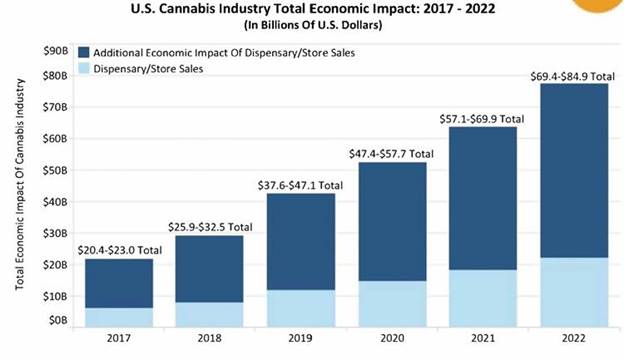

The legalization taking place in other states such as California and Florida present opportunities many times that of Washington and Colorado. The Company is exploring opportunities in Oregon, California and Florida and is getting inquiries from other potential operators in other jurisdictions.

This market is projected to grow rapidly in the future as this chart below illustrates:

| 20 |

Source: Marijuana Business Daily

Summary

The Company’s primary business objective is to lease various properties to licensed operators to grow, process and retail cannabis and related products. By developing a premium brand name, building upscale facilities, and providing quality accessories to a market where financing is difficult to obtain, these subleases are designed to provide a substantial stream of income. We believe that as laws evolve, it is possible that we will have the opportunity to participate directly in these operations as well.

2018 was a year of growth for Diego Pellicer Worldwide. All tenants were open and generating lease revenue. The tenants were showing steady revenue increases and operating improvements. The business model was being proven. The brand name was getting national recognition and garnered the “Most Valuable Brand of the Year” at the 2018 National Cannabis Business Awards beating out tough national competition including MedMen™, The Clinic, Lightshade and Olio. Diego was also honored as the “Best Retail Center” for the second year in a row, defeating other highly regarded names including LiveWell, The Clinic, The Green Solutions, Euflora and Kind Love.

2019 was a time of continued growth and a change of focus for the Company. An effective and experienced team was assembled from within our operators to develop our newly formed management company, and to complement the current executives with knowledge and experience in real estate operations, banking, site selection, branding, facility design, corporate finance, investor relations, store management, and grow expertise, Additional capital needed to be raised in order to have sufficient capital to help support our operators expand within their markets, and to begin the expansion into different markets in the US. Much of the Company’s debt was renegotiated, and additional commitments were formalized for the expansion in the Colorado market. New markets had to be explored, new alliances forged, and opportunities prioritized.

Diego is exploring opportunities in California, Colorado, Nevada, Washington and other states. The Company will continue to raise capital to finance that expansion. This should result in increased revenues for the future and increased opportunities into new markets.

Opportunity in an untapped industry with multi-billion-dollar potential

The demand for marijuana products is a multi-billion-dollar market that has only recently begun to become mainstream. Many challenges face the marijuana entrepreneur. Therein lies the opportunity.

Regulation and reality

Total demand for marijuana in the United States, including the black market, is around $52.5 billion, according to the estimates. That becomes a very conservative estimate of the size of the market in the United States. Distribution was driven underground for years by the Controlled Substance Act passed by Congress nearly 50 years ago. The favorable public opinion towards the legalization is rapidly changing the political attitude toward marijuana not only on the state level but on the federal level. If the Federal Government legalized marijuana nationwide, sales might start out around that level, but would likely rise as cannabis gained mainstream acceptance and the market evolved. Eventually, marijuana could surpass cigarette sales with the potential to rival beer in terms of overall sales.

| 21 |

Financing and banking

As doubts remain, financing is still a challenge for this industry with banks in many states not only avoiding lending to these businesses but also refusing deposits because of complicated FDIC requirements. Financing has been largely equity raises, vendor financing, and expensive convertible debt. However, with the legalization and subsequent public capital raises in Canada and the change in the political attitude, there has been an indication of more interest by institutional investors in providing capital to this industry and more banks are accepting deposits.

A fragmented industry

Most industries evolve through the same business cycle. Many small independent companies initially operate in fragmented markets in the early stages. Then there is a consolidation of the industry, with the consolidators thriving and the independent companies dwindling. The larger companies have access to less expensive capital, lower costs, better merchandising, brand name recognition, and more efficient operations. This what we offer our tenants when negotiating the lease: an agreement to acquire them when marijuana is federally legalized. This gives the tenant the ultimate opportunity to participate in the rapid consolidation that we believe will happen when marijuana is federally legalized. This consolidation will result in companies that have heretofore been unable to participate in the rapidly growing industry to be scrambling to enter the space. Diego and its tenants will already be established and consolidated. As an exit strategy, we want to position Diego to be a likely candidate for acquisition or a major player in the marketplace.

The opportunity

The first mover advantage will continue to be possible for those willing to deal with the regulatory, banking, and financial challenges in today’s market. The fragmented market, the shortage of executives skilled in challenges of the industry, scarcity of brand names, provides a company like Diego, who has proven their business model, to be a consolidator in this industry.

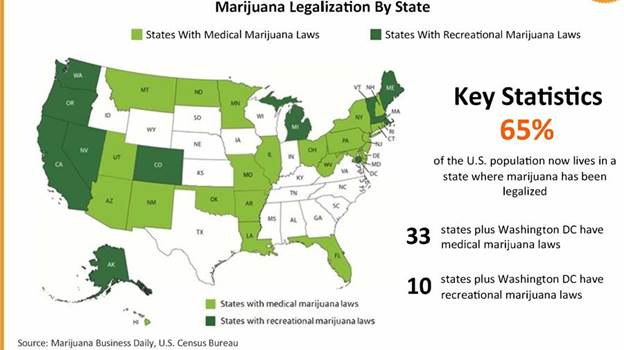

States with legalized marijuana

Thirty three states and the District of Columbia have laws broadly legalizing marijuana in some form. Ten states and the District of Columbia have legalized marijuana for recreational use with the largest market by far, California, becoming legal.

The majority of all states allow for use of medical marijuana under certain circumstances. Some states have also decriminalized the possession of small amounts of marijuana. The industry is operating under stringent regulations within the various state jurisdictions.

This map shows current state laws and recently approved ballot measures legalizing marijuana for medical or recreational purposes. 2

There are 9,397 active licenses for marijuana businesses in the U.S., according to Ed Keating, chief data officer for Cannabiz Media, which tracks marijuana licenses. This includes cultivators, manufacturers, retailers, dispensaries, distributors, deliverers and test labs. Now 306 million Americans live in a jurisdiction that has legalized some form of cannabis use.3 BDS Analytics estimates that the industry paid $1 billion in state taxes in 2016 and owes another $1.4 billion for 2017.4

| 22 |

1 “Illegal Pot Sales Topped $46.4 Billion in 2016, and that’s Good News for Marijuana Entrepreneurs,” Inc., January 17, 2017, Will Yakowicz.

2 CNN Money , “The Legal Marijuana Market is Booming,” January 31, 2018, by Aaron Smith

3 Frontier Financial Group, ‘The Cannabis Industry Annual Report: 2017 Legal Marijuana Outlook,”

4 CNN Money , “The Legal Marijuana Market is Booming,” January 31, 2018, by Aaron Smith

The recent legalization in states such as California and probable legalization in Florida present opportunities many times that of Washington and Colorado. The Company is exploring opportunities in Oregon, California and Florida and is getting inquiries from other potential operators in other jurisdictions such as Michigan.

States introducing and expanding legalized marijuana laws

The legalized cannabis market has grown considerably bigger, with Canada federally legalizing recreational marijuana in 2018 and Eastern states in the U.S. rushing towards legalization.

In May 2019, Colorado Governor Polis signed into law House Bill 19-1090. It is generally referred to as the "Public Company" bill because it allows public companies to own Colorado marijuana licenses for the first time. This law went into effect on November 1, 2019.

Recent developments at the federal level

Pressures from the states with legalized cannabis industries have been exerted by those state’s Senators and Congressmen. Both informal and formal efforts have been increased by these states. The following are the most recent:

In an April 2018 conversation with Republican U.S. Sen. Cory Gardner, President Donald Trump pledged to keep the Department of Justice from interfering with state cannabis laws and, perhaps more significantly, support legislation protecting state-legal marijuana businesses. White House officials later confirmed the president's policy stance.

Several bills have been introduced to Congress seeking to reform federal marijuana laws in different ways, including the removal of cannabis from the list of controlled substances, allowing MJ companies to access traditional banking services and amending the IRS code to more fairly tax cannabis businesses.

Similar bills have been introduced in previous sessions of Congress, but none have gained significant traction. This time, however, may be different, as marijuana reform has become a bipartisan issue that has the support of many prominent Republicans.

Senate Majority Leader Mitch McConnell, for example, introduced a bill in April to remove federal barriers on hemp, while former Republican House Speaker John Boehner recently disclosed his involvement with a large, multistate cannabis company.

Whether any significant reform of federal marijuana policy happens in 2018 and what shape it could take remains an open question, but it's clear that attitudes toward cannabis on Capitol Hill are shifting.

New York Democratic Senator Chuck Schumer introducing legislation to remove cannabis from the DEA’s list of controlled substances, to decriminalize pot at a federal level and effectively allow states to decide how to regulate the use of medical or recreational marijuana without concern for federal law.

President Trump cut a deal with Colorado Senator Corey Gardner, R-Colo. to allow states to decide what to do about cannabis.

Former Speaker of the House John Boehner became a director with cannabis company Acreage Holdings.

The Food and Drug Administration setting up for an approval of the first cannabis-based drug from GW Pharmaceuticals Plc (“ GWPH” )

The Veteran’s Administration now wants to study the effectiveness of cannabis for chronic pain and PTSD. (The Street, “Cannabis Industry Sits on Precipice of Major Expansion, March 28, 2018, by Bill Meagher)

Source: 2018 Marijuana Business Daily, a division of Anne Holland Ventures Inc.

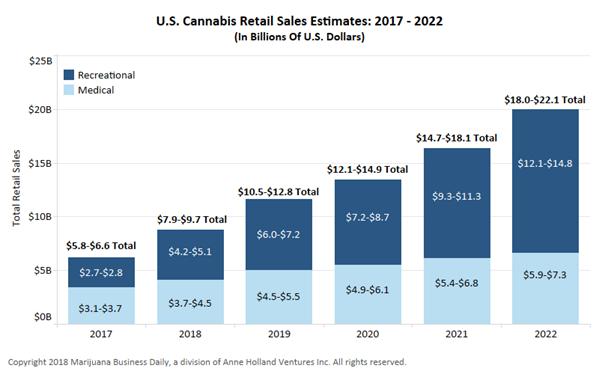

The projected U.S. cannabis industry’s growth

The Cannabis Industry’s Annual Report for 2018 projects the following robust growth of legal marijuana sales:

| 23 |

New Frontier, “The Cannabis Industry Annual Report: 2018 Legal Marijuana Outlook,”

What is Diego's Strategy, Phases One and Two?

Diego is a real estate and a consumer retail development company that is focused on high quality recurring revenues resulting from leasing real estate to licensed cannabis operators, and the management of operations for these and other third party cannabis operators deriving income from management and royalty fees. Diego provides a competitive advantage to these operators by developing “Diego Pellicer” as the world’s first premium marijuana brand and by establishing the highest quality standards for its facilities and products.

The Company's first phase strategy is to acquire or lease and develop the most prominent and convenient real estate locations for the purposes of leasing them to state licensed operators in the cannabis industry. Diego's first phase revenues result from leasing real estate and selling non-cannabis related accessories to our tenants. The Company has developed a brand name strategy, providing training, design services, branded accessories, systems and systems training, locational selection, and other advisory services to their tenants. We enter into branding agreements with our tenants. In addition, part of the vetting process in finding the proper tenant is selecting a tenant that shares the Company's values and strictly complies with state laws, follows strict safety and testing requirements and provides consistent, high-quality products. If the tenants do not comply, they will not be allowed to use the brand.

| 24 |

The second phase of our strategy is to secure options to purchase the tenant's operations. When mutually advantageous for Diego and the tenant, Diego will negotiate acquisition contracts with selected Diego operators/tenants. When it becomes federally legal to do so, Diego will execute the acquisition contracts, consolidate our selected tenants and become a nationally branded marijuana retailer and producer concurrent with the change of federal law.

Diego Pellicer Management Company, will license the upscale Diego Pellicer brand to qualified operators and receive royalty payments, while providing expertise in retail, product and manufacturing from Diego’s accomplished management team with extensive industry experience

Value Proposition

Value proposition 1: By providing branding, management experience, training, unique accessories, purchasing services, locational experience, standardized design, and experienced construction supervision, the tenant reduces his startup time, reduces cash drain, increases his efficiency, and builds his gross margin. Diego provides the capital for preopening lease costs and tenant improvements. This results in a turnkey retail location for the tenant. Thus, Diego’s real estate, management, consulting and accessory sales are positioned to deliver a premium return on our investment.

Value proposition 2: With each lease, Diego negotiates an acquisition contract with selected licensed tenants to acquire their operations. This contract will be executed at Diego's option, and upon changes to federal law ,, introduces our second value proposition-ownership of operations in an industry that is projected to exceed $8 billion by 2019.

What does our premium branding accomplish?

A very important aspect of our marketing plan is to build Diego Pellicer as a luxury brand. This not only enables us to establish a premium brand, but also to generate significant revenues from non- cannabis products.

| 25 |

The Company is establishing several levels of branding and will use these to appeal to the various segments of the marketplace depending upon the location, competition, legal constraints, and budget. Standard store templates are being developed, complimentary accessories selectively designed, and customer preferences and segments analyzed.

| 26 |

Denver stores have been met with enthusiastic demand growing revenues quickly. This is proving the initial Diego concept.

We have proven this to be a winning strategy

Diego is positioning itself to be a dominate player in the marijuana marketplace. Diego has proven this by being a fully integrated marijuana retail operation and premium brand, capitalizing on beautifully designed retail stores offering the finest quality products at competitive prices.

What we accomplished in 2019

2019 was a time of continued growth and a change of focus for the Company. An effective and experienced team was assembled from within our operators to develop our newly formed management company, and to complement the current executives with knowledge and experience in real estate operations, banking, site selection, branding, facility design, corporate finance, investor relations, store management, and grow expertise, Additional capital needed to be raised in order to have sufficient capital to help support our operators expand within their markets, and to begin the expansion into different markets in the US. Much of the Company’s debt was renegotiated, and additional commitments were formalized for the expansion in the Colorado market. New markets had to be explored, new alliances forged, and opportunities prioritized.

New markets were explored. Three facilities continued to see year upon year increases in revenues, which lead to increased rental revenue cash-flow to the Company. In 2019, Diego focused on our Colorado operations, and divested itself from the Washington Tenant, citing restrictive rules and regulations for public company involvement in any part of the Washington State marijuana industry. Diego received revenues from three Colorado facilities, and the first quarter for our Washington store. Diego now had four facilities generating rent in 2019 for the year and we have actively been expanding in the Colorado markets with potential acquisitions for our tenants, and our management company. The tenants growing their sales and improving operational efficiency. Diego worked with these tenants, partially forbearing on their rent so as to allow these operators to strengthen their position and become capable of paying full rents. The properties generating rents in 2019 are as follows:

Table 1: Property Portfolio

| Purpose | Size | City | State | |||||||||

| Retail store (recreational and medical) | 3,300 sq. | Denver | CO | |||||||||

| Cultivation warehouse | 18,600 sq. | Denver | CO | |||||||||

| Cultivation warehouse | 14,800 sq. | Denver | CO | |||||||||

| Retail store (recreational and medical) - Sold | 4,500 sq. | Seattle | WA |

Diego’s Washington tenant opened our first flagship store in Seattle in October 2016. On May 6, 2019, the Company entered into an agreement with a third party, which the Company sold the Seattle leased location provided $550,000 in capital and executive resources for expansion which the company allocated to its efforts in a new location and cannabis grow facilities in Colorado. The Colorado tenant opened the Diego Denver branded flagship store in February 2017. In addition, Diego’s two cultivation facilities in Denver, CO began production in late 2016. The retail facilities have shown steady growth in sales since their opening. The three Colorado properties were subleased to a single entity. The Company is currently is exploring the acquisition of this entity.

| 27 |

Diego Pellicer Denver

| 28 |

Diego will continue this strategy in states where recreational or medical marijuana sales and cultivation is legal under state law. Our business model is recurring lease revenue, royalties, management fees, and is entirely scalable. Our success will dependent upon continuing to raise capital for expansion, continual improvement of our business model, standardizing store design, controlling costs, new store management opportunities, and continuing to develop the brand.

RESULTS OF OPERATIONS

Year ended December 31, 2019 compared to year ended December 31, 2018

After rental expense the gross margins on the lease were as follows:

| Year Ended | Year Ended | Increase (Decrease) | ||||||||

| December 31, 2019 | December 31, 2018 | $ | % | |||||||

| Revenues | ||||||||||

| Net rental revenue | $ | 1,646,369 | $ | 1,456,939 | $ | 189,430 | 13% | |||

| Rental expense | (1,189,352) | (1,130,135) | (59,217) | 5% | ||||||

| Gross profit | 457,017 | 326,804 | 130,213 | 40% | ||||||

| General and administrative expenses | 2,521,649 | 2,786,615 | (264,966) | -10% | ||||||

| Selling expense | 52,605 | 66,511 | (13,906) | -21% | ||||||

| Depreciation expense | 139,595 | 498,400 | (358,805) | -72% | ||||||

| Loss from operations | $ | (2,256,832) | $ | (3,024,722) | $ | 767,890 | -25% | |||

Revenues. For the year ended December 31, 2019 and 2018, the Company leased three facilities to licensees in Colorado. The year ended December 31, 2019 is the beginning of the second year of operations for these licensees. Diego, however, is still forbearing on the partial premium rents contractually due from the tenant as a result of the cost of leasehold improvements and the deferral of preopening rents. These will become recorded as revenue when the Company considers the premium rents collectible considering the relative success of the tenant’s operations. These licensees have now had their opening year behind them and are experiencing increasing revenues in the second year of operations. This is a significant event for the Company. As a result, total revenue for the year ended December 31, 2019 was $1,646,369, as compared to $1,456,939 for the year ended December 31, 2018, an increase of $189,430.

| 29 |

Gross profit. Rental revenue for the periods ended December 31, 2019 increased over the prior year ended December 31, 2018, resulting in a gross profit of $457,017.

General and administrative expense. Our general and administrative expenses for the year ended December 31, 2019 were $2,521,649, compared to $2,786,615 for the year ended December 31, 2018. The decline of $264,966 was largely attributable a reduction in executive stock compensation and consulting fees during year ended December 31, 2019.

Selling expense. Our selling expenses for the year ended December 31, 2019 were $52,605, compared to $66,511 for the year ended December 31, 2018. The decline of $13,906 was due to reduction of services used related to selling and marketing

| Year Ended | Year Ended | Increase (Decrease) | ||||||||||||||

| December 31, 2019 | December 31, 2018 | $ | % | |||||||||||||

| Other income (expense) | ||||||||||||||||

| Other income (expense) | $ | 153,782 | $ | 2,984 | $ | 150,798 | 5054 | % | ||||||||

| Interest expense | (3,184,951 | ) | (2,758,160 | ) | (426,791 | ) | 15 | % | ||||||||

| Loss on debt issuance | — | (2,892,033 | ) | 2,892,033 | -100 | % | ||||||||||

| Write off of accounts receivable | — | (23,966 | ) | 23,966 | -100 | % | ||||||||||

| Gain on sale of lease | 534,649 | — | 534,649 | N/A | ||||||||||||

| Extinguishment of debt | 218,196 | 121,217 | 96,979 | 80 | % | |||||||||||

| Change in derivative liabilities | 1,948,643 | 1,493,962 | 454,681 | 30 | % | |||||||||||

| Change in value of warrants | 15,609 | 175,774 | (160,165 | ) | -91 | % | ||||||||||

| Total other income (loss) | $ | (314,072 | ) | $ | (3,880,222 | ) | $ | 3,566,150 | -92 | % | ||||||

The Net Other Income was the effect of the decline in market value of the Company’s stock had on the derivative liability of $5,024,321 offset by recording the cost of triggering technical default penalties on certain convertible notes and the financing costs of new debt incurred by the Company. Our other income for the year ended December 31, 2019 were $153,782, compared to $2,984 for the year ended December 31, 2018. The increase of $150,798 was due to income from the receivables owed by the our sublease tenant of the Company’s Colorado properties and affiliates of the tenant.

LIQUIDITY AND CAPITAL RESOURCES

| Year Ended | Year Ended | Increase (Decrease) | ||||||||||||||

| December 31, 2019 | December 31, 2018 | $ | % | |||||||||||||

| Net Cash provided (used) in operating activities | $ | (1,183,991 | ) | $ | (1,201,618 | ) | $ | 17,627 | -1 | % | ||||||

| Net Cash used in investing activities | 550,000 | — | 550,000 | N/A | ||||||||||||

| Net Cash used in financing activities | 891,000 | 1,103,353 | (212,353 | ) | -19 | % | ||||||||||

| Net Increase in Cash | 257,009 | (98,265 | ) | 355,274 | -362 | % | ||||||||||

| Cash - beginning of period | 60,437 | 158,702 | (98,265 | ) | ||||||||||||

| Cash - end of period | $ | 317,446 | $ | 60,437 | $ | 257,009 | 425 | % | ||||||||

Operating Activities. For the year ended December 31, 2019, the net cash used of $1,183,991 was an increase over the same period of the prior year of $1,201,618. The loss from operations after non-cash adjustments increased by $243,975 over the prior year, and an increase in net assets and liabilities of $261,602.

Investing Activities. For the year ended December 31, 2019, proceeds from sale of Seattle lease was $550,000. There was no investing activities for the year ended December 31, 2018.

Financing Activities. During the year ended December 31, 2019, $897,725 in proceeds were from convertible notes payable and $130,000 from the sale of preferred stock. Payments of convertible notes payable was $120,500 and debt cost was $16,225. For the year ended December 31, 2018, $1,173,750 in proceeds were from convertible notes payable and $20,872 from the sale of common stock. Payments of convertible notes payable was $135,000 and debt cost was $16,000. In 2020, we raised $117,000 from sales of preferred stocks.

| 30 |

COVID-19

On January 30, 2020, the World Health Organization (“WHO”) announced a global health emergency in response to a new strain of a coronavirus (the “COVID-19 outbreak”). In March 2020, the WHO classified the COVID-19 outbreak as a pandemic based on the rapid increase in exposure globally. The full impact of the COVID-19 outbreak continues to evolve as of the date of this report. Management is actively monitoring the global situation and its effects on the Company’s industry, financial condition, liquidity, and operations. Given the daily evolution of the COVID-19 outbreak and the global responses to curb its spread, the Company is not able to estimate the effects of the COVID-19 outbreak on its results of operations, financial condition, or liquidity for fiscal year 2020. However, if the pandemic continues, it may have a material adverse effect on the Company’s results of future operations, financial position, and liquidity in fiscal year 2020.

Critical Accounting Policies

The preparation of our financial statements requires us to make estimates and judgments that affect the reported amounts of our assets, liabilities, revenues and expenses, and related disclosures of contingent liabilities. The following are the areas that we believe require the greatest amount of judgments or estimates in the preparation of the financial statements: deferred income tax assets, accrued expenses, fair value of equity instruments and reserves for any other commitments or contingencies. Management reviews critical accounting estimates on an ongoing basis and as needed prior to the release of annual financial statements. See also Note 2 to our consolidated financial statements, which discusses the significant assumptions used in applying accounting policies.

Revenue recognition

In accordance with ASC 842, Leases , the Company recognizes rent income on a straight-line basis over the lease term to the extent that collection is considered probable. As a result the Company been recognizing rents as they become payable.

During the initial term of the lease, management has a policy of partial rent forbearance when the tenant first opens the facility to assure that the tenant has the opportunity for success. Management may be required to exercise considerable judgment in estimating revenue to be recognized.

Prior to the adoption of ASC Topic 842, Leases , the Company recognized lease revenue when the collectability is reasonably assured, in accordance with ASC Topic 840, Leases , as amended and interpreted, minimum annual rental revenue is recognized for rental revenues on a straight-line basis over the term of the related lease.

When management concludes that the Company is the owner of tenant improvements, management records the cost to construct the tenant improvements as a capital asset. In addition, management records the cost of certain tenant improvements paid for or reimbursed by tenants as capital assets when management concludes that the Company is the owner of such tenant improvements. For these tenant improvements, management records the amount funded or reimbursed by tenants as deferred revenue, which is amortized as additional rental income over the term of the related lease. When management concludes that the tenant is the owner of tenant improvements for accounting purposes, management records the Company’s contribution towards those improvements as a lease incentive, which is amortized as a reduction to rental revenue on a straight-line basis over the term of the lease.

The Company has adopted the new revenue recognition guidelines in accordance with ASC 606, Revenue from Contracts with Customers (ASC 606), commencing from the period under this report. The adoption of ASU 2016-10 did not have a material impact on the financial statements and related disclosures since the Company is primarily a lessor for revenue purposes and recognizes rent income under ASC 842, Leases.

| 31 |

The Company analyzes its contracts to assess that they are within the scope and in accordance with ASC 606. In determining the appropriate amount of revenue to be recognized as the Company fulfills its obligations under each of its agreements, whether for goods and services or licensing, the Company performs the following steps: (i) identification of the promised goods or services in the contract; (ii) determination of whether the promised goods or services are performance obligations including whether they are distinct in the context of the contract; (iii) measurement of the transaction price, including the constraint on variable consideration; (iv) allocation of the transaction price to the performance obligations based on estimated selling prices; and (v) recognition of revenue when (or as) the Company satisfies each performance obligation.

Stock-Based Compensation

The Company recognizes compensation expense for stock-based compensation in accordance with ASC Topic 718. The Company calculates the fair value of the award on the date of grant using the Black-Scholes method for stock options and the quoted price of our common stock for unrestricted shares; the expense is recognized over the service period for awards expected to vest. The estimation of stock-based awards that will ultimately vest requires judgment, and to the extent actual results or updated estimates differ from original estimates, such amounts are recorded as a cumulative adjustment in the period estimates are revised. The Company considers many factors when estimating expected forfeitures, including types of awards, employee class, and historical experience. The adoption of new standard did not have a material impact on the Company’s Consolidated Financial Statements.

Recent accounting pronouncements.

Leasing

Effective January 1, 2019 the Company adopted the Financial Accounting Standards Board's ("FASB") Accounting Standards Update No. 2016-02, “Leases (Topic 842)” which superseded previous lease guidance ASC 840, Leases. Topic 842 is a new lease model that requires a company to recognize right-of-use (“ROU”) assets and lease liabilities on the balance sheet. The Company adopted the standard using the modified retrospective approach that does not require the restatement of prior year financial statements. The adoption of Topic 842 did not have a material impact on the Company’s consolidated income statement or consolidated cash flow statement. The adoption of Topic 842 resulted in the recognition of ROU assets of $4,069,296 and corresponding lease liabilities of $4,151,427 as of January 1, 2019 for leases classified as operating leases. In addition, the deferred rent liability as of January 1, 2019, was reclassified as a reduction in the ROU assets. Topic 842 also applies to the Company's sub-lease revenues, however, the adoption of Topic 842 did not have a significant impact on the Company's accounting for its sub-lease agreements.

The Company adopted the package of practical expedients and transition provisions available for expired or existing contracts, which allowed the Company carryforward its historical assessments of 1) whether contracts are or contain leases, 2) lease classification and 3) initial direct costs. Additionally, for real estate leases, the Company adopted the practical expedient that allows lessees to treat the lease and non-lease components of leases as a single lease component. The Company also elected the hindsight practical expedient to determine the reasonably certain lease term for existing leases. Further, the Company elected the short-term lease exception policy, permitting it exclude the recognition requirements for leases with terms of 12 months or less. See Note 10 for additional information about leases.

Off-Balance Sheet Arrangements

We have no off-balance sheet arrangements.

Item 7A. Quantitative and Qualitative Disclosure about Market Risk.

We are a smaller reporting company as defined by Rule 12b-2 of the Exchange Act and are not required to provide the information under this item.

| 32 |

Item 8. Financial Statements and Supplementary Data.

Diego Pellicer Worldwide, Inc.

December 31, 2019 and 2018

Index to the Consolidated Financial Statements

| 33 |

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Shareholders and Board of Directors of

Diego Pellicer Worldwide, Inc.

Opinion on the Financial Statements

We have audited the accompanying consolidated balance sheet of Diego Pellicer Worldwide, Inc. (the “Company”), as of December 31, 2018 , and the related consolidated statements of operations, stockholders’ deficit and cash flows for each of the year ended December 31, 2018 and the related notes (collectively referred to as the “consolidated financial statements”). In our opinion, the consolidated financial statements present fairly, in all material respects, the financial position of the Company as of December 31, 2018, and the results of its operations and its cash flows for each of the year ended December 31, 2018, in conformity with accounting principles generally accepted in the United States of America.

The Company’s Ability to Continue as a Going Concern

The accompanying consolidated financial statements have been prepared assuming the Company will continue as a going concern. As discussed in Note 3 to the accompanying consolidated financial statements, the Company has suffered recurring losses from operations, generated negative cash flows from operating activities, has an accumulated deficit and that raised substantial doubt exists about Company’s ability to continue as a going concern. Management’s evaluation of the events and conditions and management’s plans in regarding these matters are also described in Note 3. The consolidated financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Basis for Opinion