UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

| For the fiscal year ended | ||||||||

or | ||||||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

| For the transition period from __________ to __________ | ||||||||

Commission File Number: 001-35797

| (Exact name of registrant as specified in its charter) | ||

| (State or other jurisdiction of | (I.R.S. Employer Identification No.) | |||||||||||||

| incorporation or organization) | ||||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

(973 )-822-7000

(Registrant’s telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of Securities Act. Yes x No ¨

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b-2 of the Exchange Act. (Check one):

x | Accelerated filer | ☐ | Non-accelerated filer | ☐ | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

The aggregate market value of the voting stock held by nonaffiliates of the registrant as of June 30, 2020, the last business day of the registrant's most recently completed second fiscal quarter, was $65,094 million. The registrant has no non-voting common stock.

The number of shares outstanding of the registrant's common stock as of February 11, 2021 was 475,166,373 shares.

DOCUMENTS INCORPORATED BY REFERENCE:

Portions of the registrant’s Proxy Statement for the 2021 Annual Meeting of Shareholders (hereinafter referred to as the “2021 Proxy Statement”) are incorporated into Part III of this Form 10-K.

TABLE OF CONTENTS

| Page | ||||||||||||||

Item 1. | ||||||||||||||

Item 1A. | ||||||||||||||

Item 1B. | ||||||||||||||

Item 2. | ||||||||||||||

Item 3. | ||||||||||||||

Item 4. | ||||||||||||||

Item 5. | ||||||||||||||

Item 7. | ||||||||||||||

| Item 7A. | ||||||||||||||

Item 8. | ||||||||||||||

Item 9. | ||||||||||||||

Item 9A. | ||||||||||||||

Item 9B. | ||||||||||||||

Item 10. | ||||||||||||||

Item 11. | ||||||||||||||

Item 12. | ||||||||||||||

Item 13. | ||||||||||||||

Item 14. | ||||||||||||||

Item 15. | ||||||||||||||

Item 16. | ||||||||||||||

PART I

Item 1. Business.

Overview

Zoetis Inc. is a global leader in the animal health industry, focused on the discovery, development, manufacture and commercialization of medicines, vaccines, diagnostic products, biodevices, genetic tests and precision livestock farming technology. We have a diversified business, commercializing products across eight core species: dogs, cats and horses (collectively, companion animals) and cattle, swine, poultry, fish and sheep (collectively, livestock); and within seven major product categories: vaccines, anti-infectives, parasiticides, dermatology, other pharmaceutical products, medicated feed additives and animal health diagnostics. For more than 65 years, we have been committed to advancing the health of animals and bringing solutions to our customers who raise and care for them.

We were incorporated in Delaware in July 2012 and prior to that the company was a business unit of Pfizer Inc. (Pfizer). The address of our principal executive offices is 10 Sylvan Way, Parsippany, New Jersey 07054. Unless the context requires otherwise, references to “Zoetis,” “the company,” “we,” “us” or “our” in this Annual Report on Form 10-K for the fiscal year ended December 31, 2020 (2020 Annual Report) refer to Zoetis Inc., a Delaware corporation, and its subsidiaries. In addition, unless the context requires otherwise, references to “Pfizer” in this 2020 Annual Report refer to Pfizer Inc., a Delaware corporation, and its subsidiaries.

Operating Segments

The animal health medicines, vaccines and diagnostics market is characterized by meaningful differences in customer needs across different regions. This is due to a variety of factors, including:

•economic differences, such as standards of living in developed markets as compared to emerging markets;

•cultural differences, such as dietary preferences for different animal proteins, pet ownership preferences and pet care standards;

•epidemiological differences, such as the prevalence of certain bacterial and viral strains and disease dynamics;

•treatment differences, such as utilization of different types of medicines and vaccines, as well as the pace of adoption of new technologies;

•environmental differences, such as seasonality, climate and the availability of arable land and fresh water; and

•regulatory differences, such as standards for product approval and manufacturing.

As a result of these differences, among other things, we organize and operate our business in two segments:

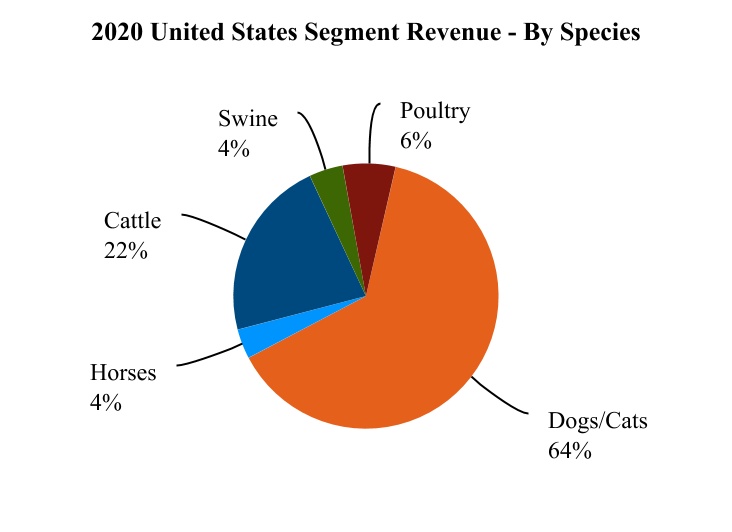

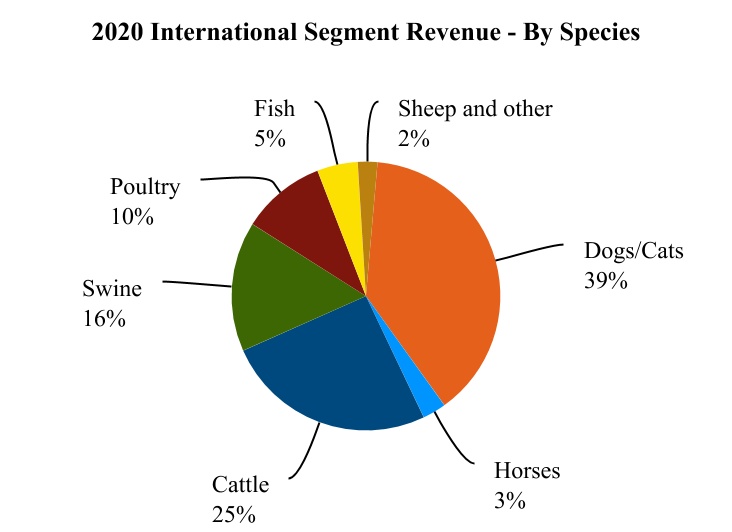

•United States (U.S.) with revenue of $3,557 million, or 53% of total revenue for the year ended December 31, 2020; and

•International with revenue of $3,035 million, or 46% of total revenue for the year ended December 31, 2020.

Within each of these operating segments, we offer a diversified product portfolio for both companion animal and livestock customers so that we can capitalize on local trends and customer needs.

In addition, our Client Supply Services (CSS) organization which provides contract manufacturing services to third parties, and our human health products, together represented approximately 1% of our total revenue for the year ended December 31, 2020.

1 |

Our 2020 revenue for the U.S. and key international markets, together with the percentage of revenue attributable to companion animal and livestock products in those markets, is as follows:

| (MILLIONS OF DOLLARS) | Revenue | Companion Animal | Livestock | ||||||||

| United States | $3,557 | 67% | 33% | ||||||||

| Australia | $207 | 46% | 54% | ||||||||

| Brazil | $258 | 30% | 70% | ||||||||

| Canada | $210 | 50% | 50% | ||||||||

| Chile | $100 | 14% | 86% | ||||||||

| China | $266 | 50% | 50% | ||||||||

| France | $118 | 48% | 52% | ||||||||

| Germany | $159 | 58% | 42% | ||||||||

| Italy | $90 | 56% | 44% | ||||||||

| Japan | $177 | 65% | 35% | ||||||||

| Mexico | $116 | 23% | 77% | ||||||||

| Spain | $112 | 35% | 65% | ||||||||

| United Kingdom | $178 | 63% | 37% | ||||||||

| Other Developed | $388 | 41% | 59% | ||||||||

| Other Emerging | $656 | 28% | 72% | ||||||||

For additional information regarding our performance in each of these operating segments and the impact of foreign exchange rates, see Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations and Item 8. Financial Statements and Supplementary Data:

Notes to Consolidated Financial Statements—Note 4. Revenue and Note 19. Segment Information. Our 2020 reported revenue for each segment, by species, is as follows:

2 |

Products

Over the course of our history, we have focused on developing a diverse portfolio of animal health products that deliver solutions across the continuum of care. We refer to all different brands of a particular product, or its dosage forms for all species, as a product line. We have approximately 300 comprehensive product lines, including products for both companion animals and livestock within each of our major product categories.

Our companion animal products help extend and improve the quality of life for pets; increase convenience and compliance for pet owners; and help veterinarians improve the quality of their care and the efficiency of their businesses. Growth in the companion animal medicines, vaccines and diagnostics sector is driven by economic development, related increases in disposable income and increases in pet ownership and spending on pet care. Companion animals are also living longer, deepening the human-animal bond, receiving increased medical treatment and benefiting from advances in animal health medicines, vaccines and diagnostics. Companion animal products represented approximately 55% of our revenue for the year ended December 31, 2020.

Our livestock products primarily help prevent or treat diseases and conditions to allow veterinarians and producers to care for their animals and to enable the cost-effective production of safe, high-quality animal protein. Human population growth and increasing standards of living are important long-term growth drivers for our livestock products in three major ways. First, population growth and increasing standards of living drive demand for improved nutrition, particularly through increased consumption of animal protein. Second, population growth leads to greater natural resource constraints driving a need for enhanced productivity. Finally, as standards of living improve and the global food chain faces increased scrutiny, there is more focus on food quality, safety and reliability of supply. Livestock products represented approximately 44% of our revenue for the year ended December 31, 2020.

In addition, our CSS organization, which provides contract manufacturing services to third parties, and our human health products, together represented approximately 1% of our total revenue for the year ended December 31, 2020.

Our major product categories are:

•vaccines: biological preparations that help prevent diseases of the respiratory, gastrointestinal and reproductive tracts or induce a specific immune response;

•anti-infectives: products that prevent, kill or slow the growth of bacteria, fungi or protozoa;

•parasiticides: products that prevent or eliminate external and internal parasites such as fleas, ticks and worms;

•dermatology products: products that relieve itch associated with allergic conditions and atopic dermatitis;

•other pharmaceutical products: pain and sedation, antiemetic, reproductive, and oncology products;

•medicated feed additives: products added to animal feed that provide medicines to livestock; and

•animal health diagnostics: portable blood and urine analysis systems and point-of-care diagnostic products, including instruments and reagents, rapid immunoassay tests, reference laboratory kits, blood glucose monitors and reference laboratory services.

Our remaining revenue is derived from other non-pharmaceutical product categories, such as nutritionals and agribusiness, as well as products and services in biodevices, genetic tests and precision livestock farming.

As part of our growth strategy, we focus on the discovery and development of new chemical, biopharmaceutical and biological entities, as well as product lifecycle innovation, primarily through our research and development (R&D) group. Historically, a substantial portion of our products and revenue has been the result of product lifecycle innovation where we actively work to broaden the value of existing products by developing claims in additional species, more convenient formulations and combinations, and by expanding usage into more countries. For example, the first product in our ceftiofur line was an anti-infective approved for treating bovine respiratory disease (BRD) in cattle that was administered via intramuscular injection. Through follow-on studies and reformulations, we have expanded the product line into additional cattle claims and administration routes, as well as other species and regions. The ceftiofur product line currently includes the brands Excede®, Excenel®, Naxcel® and Spectramast®.

The following are examples of our first-in-class and/or best-in-class products that we have launched in recent years and products that we believe may represent platforms for future product lifecycle innovation (listed alphabetically):

•Apoquel®, the first Janus kinase inhibitor for use in veterinary medicine, was approved for the control of pruritus associated with allergic dermatitis and the control of atopic dermatitis in dogs at least 12 months of age. Since January 2014, we launched Apoquel in key markets including the U.S., Europe, Japan, Brazil, Australia and China;

•Core EQ Innovator™, the first and only vaccine for horses to contain all five core equine disease antigens - West Nile, Eastern and Western Equine encephalomyelitis, tetanus and rabies - in one combination, was approved in the U.S. in 2018 and in Canada in 2019;

•Cytopoint®, the first canine monoclonal antibody (mAb) to help reduce the clinical signs of atopic dermatitis (such as itching) in dogs of any age, was licensed in the U.S. in 2016 (and was later granted an expanded indication to treat allergic dermatitis in 2018). Since 2016, the product has been approved in major markets including Canada, the European Union, New Zealand, Australia, Brazil and Mexico. An injection given once every four to eight weeks, Cytopoint neutralizes interleukin-31, a protein that has been demonstrated to trigger itching in dogs;

•Fostera® PCV MH was introduced in November 2013 in the U.S. and approved in the European Union in 2015 and Australia in 2017. It was developed to help protect pigs from porcine circovirus-associated disease (PCVAD) and enzootic pneumonia caused by M. hyopneumoniae (M. hyo). The one-bottle formulation of Fostera PCV MH allows the convenience of a one-dose program or the flexibility of a two-dose program. The Fostera franchise also includes Fostera/Suvaxyn® PRRS, which was approved in the U.S. in 2015 and in Taiwan, Vietnam and European Union countries in 2017. This vaccine offers protection against both the respiratory and reproductive forms of disease caused by porcine reproductive and respiratory syndrome (PRRS) virus. Fostera Gold PCV MH was approved in the U.S. and Canada in 2018, Brazil and Mexico in 2019 and Australia, Europe (under the name CircoMax Myco) and Japan in 2020. This is the only vaccine to contain two PCV2 genotypes and long-lasting M. hyo coverage;

3 |

•Librela® (bedinvetmab), the first injectable mAb therapy for monthly alleviation of osteoarthritis (OA) pain in dogs, was approved in the European Union and Switzerland in 2020, and Canada and Brazil in early 2021;

•Poulvac® Procerta™ HVT-ND, our first vector vaccine that helps protect against Marek’s disease and Newcastle disease, highly contagious viral infections affecting poultry, was approved in the U.S. in 2019. In 2020, we expanded our line of recombinant vector vaccines with the launch of Poulvac Procerta HVT-IBD, which provides early protection against the contemporary infectious bursal disease (IBD) viruses confronting U.S borders;

•ProHeart® 12 (moxidectin), a once-yearly injection to prevent heartworm disease in dogs 12 months of age and older, was approved in the U.S. in 2019;

•Simparica® (sarolaner) Chewables, a monthly chewable tablet for dogs to control fleas and ticks, was approved in the European Union and New Zealand in 2015, the U.S., Canada, Australia, and Brazil (Simparic) in 2016, Japan and additional European, Latin American and Asia Pacific markets in 2017, and China in 2020. Building on this franchise, in 2017, Zoetis received European Commission approval for Stronghold® Plus (selamectin/sarolaner), a topical combination product that treats ticks, fleas, ear mites, lice and gastrointestinal worms and prevents heartworm disease in cats. In 2018, this product was approved in the U.S., Japan and Canada (Revolution® Plus);

•Simparica Trio®, a triple combination parasiticide for dogs, was approved in the European Union and Canada in 2019, the U.S. and Australia in 2020, and Mexico in early 2021. This product is a key internal lifecycle innovation that combines flea and tick treatment (sarolaner) with the prevention of heartworm disease and treatment of gastrointestinal parasites;

•SolensiaTM (frunevetmab), the first injectable mAb therapy for monthly alleviation of OA pain in cats, was approved in Switzerland in 2020; and

•Vanguard®/Versican® is a market leading vaccine line for dogs intended to help prevent a range of diseases. Since 2016, Zoetis has added new and innovative enhancements to its Vanguard line in the U.S. with Vanguard crLyme, Vanguard Rapid Resp Intranasal, Vanguard B Oral, and Vanguard CIV H3N2/H3N8. In 2019, the company received approval for Versican Plus Bb Oral, the first oral vaccine for dogs in Europe. It provides long-lasting protection against Bordetella bronchiseptica, a primary component of the canine infectious respiratory disease complex (CIRDC).

We pursue the development of new vaccines for emerging infectious diseases, with an operating philosophy of “first to know and fast to market.” Examples of the successful execution of this strategy include the first equine vaccine for West Nile virus in the U.S. and European Union; the first swine vaccine for pandemic H1N1 influenza virus in the U.S.; the first fully licensed vaccine to help reduce disease caused by the Georgia 08 variant of infectious bronchitis virus (IBV) in poultry; a conditionally licensed vaccine to help fight porcine epidemic diarrhea virus (PEDv) in the U.S.; and the first conditionally licensed vaccine to help prevent the H3N2 type of canine influenza that emerged in the U.S. In 2019, Zoetis established a research facility with Texas A&M University to develop vaccines for transboundary and emerging diseases in animals, including Foot-and-Mouth Disease (FMD), a virus that can cause serious illness in cattle, pigs, and sheep. In 2020, the company opened a research lab at Colorado State University in a partnership to explore the livestock immune system and target new immunotherapies with a goal of paving the way for new alternatives to antibiotics in food-producing animals.

Additionally, the Pharmaq business of Zoetis is the global leader in vaccines and innovation for aquatic health products. Pharmaq added to its leading Alpha Ject® vaccine line with approval of Alpha Ject Micro 1 TiLa in Brazil and Colombia, and Alpha Ject Micro 1 Si in Honduras in 2019, as well as Alpha Ject Micro 4-2 in Chile in 2020. Pharmaq also launched Alpha Flux® in Chile in 2019, a parasiticide that helps salmon farmers control sea lice infestations, one of the major challenges in the aquatic health industry. In 2020, Pharmaq received approval in Norway for Alpha ERM Salar, an oil-based injectable vaccine that helps protect salmon from red mouth, a common bacterial infection. Pharmaq also established a new diagnostics lab in Norway, the country with the highest density of salmon fish farmers in the world, that will serve as a hub for research and testing. In 2020, Zoetis acquired Fish Vet Group to expand the geographic reach and enhance the diagnostics expertise and testing services of the Pharmaq business for fish farmers in major aquaculture markets.

Zoetis enhanced the portfolio of its diagnostic products with the acquisition in 2018 of Abaxis, Inc. (Abaxis), a leading provider of veterinary point-of-care diagnostic instruments. With this acquisition came the VetScan® portfolio of benchtop and handheld diagnostic instruments and consumables, which serves a large customer base of veterinary practices both in North America and international markets. In 2019, the company acquired Phoenix Central Laboratory for Veterinarians, Inc. (Phoenix Lab) and ZNLabs, LLC (ZNLabs) marking its entry into reference laboratory services and building on a strategy to develop a more comprehensive diagnostics offering with enhanced value for veterinarians. In 2020, the company acquired a third veterinary reference lab business, Ethos Diagnostic Science. The Zoetis diagnostic portfolio also includes the Witness®, Serelisa® and ProFlok® lines of immunodiagnostic kits, which provide disease detection capabilities for various species, including dogs, cats, cattle, pigs and poultry. In 2020, the company launched Vetscan Imagyst™ in Australia, Ireland, New Zealand, the U.K. and the U.S. Imagyst uses a combination of image recognition technology, algorithms and cloud-based artificial intelligence to deliver rapid testing results to veterinary clinics. Its first indication is for testing fecal samples for parasites, with the potential for broader applications to different types of testing in the future.

Zoetis also entered the field of animal nutritionals with the acquisition of Platinum Performance in 2019. The acquisition brings us premium nutritional product formulas and a unique approach to the field of scientific wellness for horses, dogs and cats.

In 2020, our top two selling products, Apoquel and Simparica/ Simparica Trio, contributed approximately 10% and 6%, respectively, of our revenue. Combined with our next three top selling products, Revolution® / Revolution Plus / Stronghold, Draxxin® and the ceftiofur line, these five products contributed approximately 31% of our revenue. In 2020, our top ten product lines contributed 44% of our revenue.

4 |

Our product lines and products that represented approximately 1% or more of our revenue in 2020, which comprise 64% of our total revenue, are as follows (listed alphabetically by product category):

Companion animal products

| Product line / product | Description | Primary species | ||||||||||||

| Vaccines | ||||||||||||||

Vanguard® L4 (4-way Lepto) | Compatible with the Vanguard line and helps protect against leptospirosis caused by Leptospira canicola, L. grippotyphosa, L. icterohaemorrhagiae and L. pomona | Dogs | ||||||||||||

Vanguard® line | Aids in preventing canine distemper caused by canine distemper virus; infectious canine hepatitis caused by canine adenovirus type 1; respiratory disease caused by canine adenovirus type 2; canine parainfluenza caused by canine parainfluenza virus; canine parvoviral enteritis caused by canine parvovirus; Lyme disease and subclinical arthritis associated with Borrelia burgdorferi, the causative agent of Lyme disease; and Rapid Resp - a group of three vaccines combating infections in dogs caused by Bordetella bronchiseptica, canine parainfluenza and canine adenovirus; canine influenza vaccines; and an oral vaccine for Bordatella bronchiseptica | Dogs | ||||||||||||

| Anti-infectives | ||||||||||||||

Clavamox® / Synulox® | A broad-spectrum antibiotic and the first potentiated penicillin approved for use in dogs and cats | Cats, dogs | ||||||||||||

Convenia® | Anti-infective for the treatment of common bacterial skin infections that provides a course of treatment in a single injection | Cats, dogs | ||||||||||||

| Parasiticides | ||||||||||||||

ProHeart® | Prevents heartworm infestation; also for treatment of existing larval and adult hookworm infections | Dogs | ||||||||||||

Revolution® / Revolution® Plus / Stronghold® line | An antiparasitic for protection against fleas, heartworm disease and ear mites in cats and dogs; sarcoptic mites and American dog tick in dogs and roundworms and hookworms for cats | Cats, dogs | ||||||||||||

Simparica®/ Simparica Trio® | A monthly chewable tablet for dogs to control fleas and ticks; Simparica Trio, also a monthly chewable tablet, is a triple combination parasiticide that delivers all-in-one protection from fleas and ticks, as well as heartworm disease, roundworms and hookworms | Dogs | ||||||||||||

| Other Pharmaceutical Products | ||||||||||||||

Cerenia® | A medication that prevents and treats acute vomiting in dogs, treats acute vomiting in cats and prevents vomiting due to motion sickness in dogs | Cats, dogs | ||||||||||||

Rimadyl® | For the relief of pain and inflammation associated with osteoarthritis and for the control of postoperative pain associated with soft tissue and orthopedic surgeries | Dogs | ||||||||||||

| Dermatology | ||||||||||||||

Apoquel® | A selective inhibitor of the Janus Kinase 1 enzyme that controls pruritus associated with allergic dermatitis and control of atopic dermatitis in dogs at least 12 months of age | Dogs | ||||||||||||

Cytopoint® | An injectable to help reduce the clinical signs such as itching of atopic dermatitis in dogs of any age | Dogs | ||||||||||||

| Animal Health Diagnostics | ||||||||||||||

VetScan® | A portfolio of benchtop and handheld diagnostic instruments, rapid tests and associated consumables | Cats, dogs | ||||||||||||

5 |

Livestock products

| Product line / product | Description | Primary species | ||||||||||||

| Vaccines | ||||||||||||||

| Improvac / Improvest / Vivax | Reduces boar taint, as an alternative to surgical castration and suppression of estrus in gilts | Swine | ||||||||||||

Rispoval® / Bovishield® line | Aids in preventing three key viruses involved in cattle pneumonia-BRSV, PI 3 virus and BVD-viruses as well as other respiratory diseases, depending on formulation | Cattle | ||||||||||||

Suvaxyn® / Fostera® | Aids in preventing or controlling diseases associated with major pig pathogens such as porcine circovirus type 2 (PCV2), porcine reproductive and respiratory syndrome virus (PRRSv) and Mycoplasma hyopneumoniae (M. hyo), depending on formulations | Swine | ||||||||||||

| Anti-infectives | ||||||||||||||

| Ceftiofur injectable line | Broad-spectrum cephalosporin antibiotic active against gram-positive and gram-negative bacteria, including ß-lactamase-producing strains, with some formulations producing a single course of therapy in one injection | Cattle, sheep, swine | ||||||||||||

Draxxin® | Single-dose low-volume antibiotic for the treatment and prevention of bovine and swine respiratory disease, infectious bovine keratoconjunctivitis and bovine foot rot | Cattle, sheep, swine | ||||||||||||

Spectramast® | Treatment of subclinical or clinical mastitis in dry or lactating dairy cattle, delivered via intramammary infusion; same active ingredient as the ceftiofur line | Cattle | ||||||||||||

Terramycin® line | Antibiotic for the treatment of susceptible infections | Cattle, poultry, sheep, swine | ||||||||||||

| Parasiticides | ||||||||||||||

Dectomax® | Injectable or pour-on endectocide, characterized by extended duration of activity, for the treatment and control of internal and external parasite infections | Cattle, swine | ||||||||||||

| Medicated Feed Additives | ||||||||||||||

Aureomycin® | Provides livestock producers control, treatment and convenience against a wide range of respiratory, enteric and reproductive diseases | Cattle, poultry, sheep, swine | ||||||||||||

BMD® | Aids in preventing and controlling enteritis; and increases rate of weight gain and improves feed efficiency in poultry and swine | Poultry, swine | ||||||||||||

| Lasalocid line | Controls coccidiosis in poultry (Avatec®) and cattle (Bovatec®) and for increased rate of weight gain and improved feed efficiency in cattle | Poultry, cattle | ||||||||||||

| Lincomycin line | Controls necrotic enteritis; treatment of dysentery (bloody scours), control of ileitis and treatment/reduction in severity of mycoplasmal pneumonia | Swine, poultry | ||||||||||||

Zoamix® | A non-ionophore anticoccidial for the prevention and control of coccidiosis in poultry | Poultry | ||||||||||||

| Other Non-Pharmaceutical Products | ||||||||||||||

Embrex® devices | Devices for enhancing hatchery operations' efficiency through in ovo detection and vaccination | Poultry | ||||||||||||

International Operations

We directly market our products in approximately 45 countries across North America, Europe, Africa, Asia, Australia and South America, and our products are sold in more than 100 countries. Operations outside the U.S. accounted for 46% of our total revenue for the year ended December 31, 2020. Through our efforts to establish an early and direct presence in many emerging markets, such as Brazil, Chile, China and Mexico, emerging markets contributed 21% of our revenue for the year ended December 31, 2020.

Our international businesses are subject, in varying degrees, to a number of risks inherent in carrying on business in other countries. These include, among other things, currency fluctuations, capital and exchange control regulations, expropriation and other restrictive government actions. See Item 1A. Risk Factors— Risks related to operating in foreign jurisdictions.

Sales and Marketing

Our sales organization includes sales representatives and technical and veterinary operations specialists. In markets where we do not have a direct commercial presence, we generally contract with distributors that provide logistics and sales and marketing support for our products.

Our sales representatives visit our customers, including veterinarians and livestock producers, to provide information and to promote and sell our products and services. Our technical and veterinary operations specialists, who generally have advanced veterinary medicine degrees, provide scientific consulting focused on disease management and herd management, training and education on diverse topics, including responsible product use. These direct relationships with customers allow us to understand the needs of our customers. Additionally, our sales representatives and technical and veterinary operations specialists partner with customers to provide training and support in areas of disease awareness and treatment protocols, including through the use of our products. As a result of these relationships, our sales and consulting visits are typically longer, more meaningful and provide us with better access to customer decision makers as compared to those in human health. As of December 31, 2020, our sales organization consisted of approximately 3,600 employees.

6 |

Our companion animal and livestock products are primarily available by prescription through a veterinarian. On a more limited basis, in certain markets, we sell certain products through retail and e-commerce outlets. We also market our products by advertising to veterinarians, livestock producers and pet owners.

Customers

We primarily sell our companion animal products to veterinarians or to third-party veterinary distributors that typically then sell our products to veterinarians, and in each case veterinarians then typically sell our products to pet owners. We sell our livestock products directly to a diverse set of livestock producers, including beef and dairy farmers as well as pork and poultry operations, and to veterinarians, third-party veterinary distributors and retail outlets that then typically sell the products to livestock producers. Our two largest customers, both distributors, represented approximately 14% and 6%, respectively, of our revenue for the year ended December 31, 2020, and no other customer represented more than 6% of our revenue for the same period.

Research and Development

Our research and development (R&D) operations are comprised of a dedicated veterinary medicine R&D organization, external alliances and other operations focused on the development, registration and regulatory maintenance of our products. In addition, we have R&D operations focused on diagnostics, devices, data, digital and other technological innovation. We incurred R&D expense of $463 million in 2020, $457 million in 2019 and $432 million in 2018.

Our R&D efforts are comprised of more than 300 programs and reflect our commitment to develop better solutions. We create new insights for predicting, preventing, detecting and treating health conditions that result in the development of new platforms of knowledge which become the basis for continuous innovation. Leveraging internal discoveries, complemented by diverse external research collaborations, results in the delivery of novel vaccine, pharmaceutical, biopharmaceutical, biodevice and diagnostic products to help our customers face their toughest challenges. While the development of new chemical, biopharmaceutical and biological entities through new product R&D plays a critical role in our growth strategies, a significant share of our R&D investment (including regulatory functions) is focused on product lifecycle innovation. A commitment to continuous innovation, based on customer need, ensures we actively work to broaden the value of existing products by developing claims in additional species, more convenient formulations, routes of administration and combinations, and by expanding usage into more countries. We also create opportunities by integrating product offerings to optimize solutions based on the totality of customer need.

We prioritize our R&D spending on an annual basis with the goal of aligning our research and business objectives, and do not disaggregate our R&D operations by research stage or by therapeutic area for purposes of managing our business. We make our strategic investments in R&D based on four criteria: strategic fit and importance to our current portfolio; technical feasibility of development and manufacture; return on investment; and the needs of customers and the market. A centralized portfolio management function links development plans with financial systems to build a comprehensive view of the status of project progression and spend. This view facilitates our ability to set targets for project timing and goals for investment efficiency. The allocation of our R&D investment between product lifecycle innovation and new product development, in addition to our ability to leverage the discoveries of our existing R&D and other industries, supports a cost-effective, efficient, sustainable and relatively predictable R&D process.

We regularly enter into agreements with external parties that enable us to collaborate on research programs or gain access to substrates and technologies (such as new devices). Some of our external partnerships involve funding from a non-governmental organization or a government grant. We are generally responsible for providing technical direction and supplemental expertise for, as well as investment in, such external partnerships. Depending on the nature of the agreement, we may act as the commercialization partner for discoveries that originate during the period of collaborative research, or we may own or have exclusive rights to any intellectual property that enables the development of proprietary products or models.

As of December 31, 2020, we employed approximately 1,250 employees in our global R&D operations. Our R&D headquarters is located in Kalamazoo, Michigan. We have R&D operations co-located with manufacturing sites in Weibern, Austria; Louvain-la-Neuve, Belgium; Campinas, Brazil; Suzhou, China; Farum, Denmark; Olot, Spain; Union City, California; Kalamazoo, Michigan; Durham, North Carolina; and Lincoln, Nebraska, U.S. We co-locate R&D operations with manufacturing sites to facilitate the efficient transfer of production processes from our laboratories to manufacturing. In addition, we maintain R&D operations in Sydney, Australia; Zaventem, Belgium; São Paulo, Brazil; Beijing, China; Navi Mumbai, India; Oslo, Norway; Hong Ngu, Vietnam; and Thanh Binh, Vietnam. Each site is designed to meet the regulatory requirements for working with chemical or infectious disease agents, as appropriate.

Manufacturing and Supply Chain

Our products are manufactured at both sites operated by us and sites operated by third-party contract manufacturing organizations, which we refer to as CMOs. We have a global manufacturing network of 29 sites.

7 |

Our global manufacturing network is comprised of the following sites:

| Site | Location | Site | Location | |||||||||||||||||

| Buellton | California, U.S. | Melbourne | Australia | |||||||||||||||||

| Campinas | Brazil | Olot | Spain | |||||||||||||||||

| Catania | Italy | Overhalla | Norway | |||||||||||||||||

| Charles City | Iowa, U.S. | Rathdrum | Ireland | |||||||||||||||||

| Chicago Heights | Illinois, U.S. | Salisbury | Maryland, U.S. | |||||||||||||||||

| Durham | North Carolina, U.S. | San Diego | California, U.S. | |||||||||||||||||

| Eagle Grove | Iowa, U.S. | Suzhou | China | |||||||||||||||||

| Farum | Denmark | Tallaght | Ireland | |||||||||||||||||

| Jilin | China | Tullamore | Ireland | |||||||||||||||||

| Kalamazoo | Michigan, U.S. | Union City | California, U.S. | |||||||||||||||||

| Klofta | Norway | Weibern | Austria | |||||||||||||||||

| Lincoln | Nebraska, U.S. | Wellington | New Zealand | |||||||||||||||||

| London | Ontario, Canada | White Hall | Illinois, U.S. | |||||||||||||||||

| Louvain-la-Neuve | Belgium | Willow Island | West Virginia, U.S. | |||||||||||||||||

| Medolla | Italy | |||||||||||||||||||

We own the majority of these sites, with the exception of our facilities in Buellton, California (U.S.), Durham, North Carolina (U.S.), Klofta (Norway), London (Canada), Medolla (Italy), Melbourne (Australia), San Diego, California (U.S.), Tullamore (Ireland), Union City, California (U.S.) and Weibern (Austria), which are leased sites.

We are currently in the process of building a second manufacturing site in Suzhou (China).

Our global manufacturing and supply chain is supported by a network of CMOs. As of December 31, 2020, this network was comprised of 144 CMOs, including those centrally managed as well as local CMOs.

We select CMOs based on several factors: (i) their ability to reliably supply products or materials that meet our quality standards at an optimized cost; (ii) their access to niche products and technologies; (iii) capacity; and (iv) financial efficiency analyses. Our regional and global manufacturing teams seek to ensure that all of the CMOs we use adhere to our standards of manufacturing quality.

We purchase certain raw materials necessary for the commercial production of our products from a variety of third-party suppliers. We utilize logistics service providers as a part of our global supply chain, primarily for shipping and logistics support.

We intend to continue our efficiency improvement programs in our manufacturing and supply chain organization, including Six Sigma and Lean capabilities, which are processes intended to improve manufacturing efficiency. We have strong globally managed and coordinated quality control and quality assurance programs in place at our global manufacturing network sites, and we regularly inspect and audit our global manufacturing network and CMO sites.

Competition

Although our business is the largest based on revenue in the animal health medicines, vaccines and diagnostics industry, we face competition in the regions in which we compete. Principal drivers of competition vary depending on the particular region, species, product category and individual product, and include new product development, quality, price, service and promotion to veterinary professionals, pet owners and livestock producers.

Our primary competitors include animal health medicines, vaccines and diagnostic companies such as Boehringer Ingelheim Animal Health Inc., the animal health division of Boehringer Ingelheim GmbH; Merck Animal Health, the animal health division of Merck & Co., Inc.; Elanco Animal Health, which includes their recent acquisition of Bayer Animal Health, the animal health division of Bayer AG; and IDEXX Laboratories. There are also several new start-up companies working in the animal health area. In addition, we compete with hundreds of other producers of animal health products throughout the world.

The level of competition from generic products varies from market to market. For example, the level of generic competition is higher in Europe and certain emerging markets than in the U.S. Unlike in the human health market, there is no large, well-capitalized company focused on generic animal health products that exists as a global competitor in the industry. The reasons for this include the relatively smaller average market size of each product opportunity, the importance of direct distribution and education to veterinarians and livestock producers and the primarily self-pay nature of the business. For more information regarding the generic competition we have and expect to encounter as patents on certain of our key products expire, see Item 1. Business - Intellectual Property. In addition, companion animal health products are often directly prescribed and dispensed by veterinarians.

The importance of quality and safety concerns to pet owners, veterinarians and livestock producers also contributes to animal health brand loyalty. As a result, we believe that significant brand loyalty to products often continues after the loss of patent-based and regulatory exclusivity.

8 |

Intellectual Property

Our technology, brands and other intellectual property are important elements of our business. We rely on patent, trademark, copyright and trade secret laws, as well as regulatory exclusivity periods and non-disclosure agreements to protect our intellectual property rights. Our policy is to vigorously protect, enforce and defend our rights to our intellectual property, as appropriate.

Our product portfolio enjoys the protection of approximately 6,100 granted patents and 1,450 pending patent applications, filed in more than 50 countries, with a focus on our major markets, including Australia, Brazil, Canada, China, Europe, Japan and the U.S., as well as other countries with strong patent systems. Many of the patents and patent applications in our portfolio are the result of our in-house research and development, while other patents and patent applications in our portfolio were wholly or partially developed by third parties and are licensed to Zoetis.

Patents for individual products expire at different times based on the date of the patent filing (or sometimes the date of patent grant) and the legal term of patents in the countries where such patents are obtained. Below is a summary of our recent and upcoming key patent expirations.

•Draxxin, containing the active ingredient tulathromycin, is covered by a formulation patent in the U.S. which expired in February 2021. Corresponding formulation patents in Europe, Canada, Australia and other key markets expired in late 2020, with the exception of the formulation patents in Brazil and Japan that both expire in 2025. The active ingredient tulathromycin is protected in Brazil until 2022 and in Japan until 2023. Generic tulathromycin products are now marketed in key markets including Europe, Canada, Mexico and Australia, as well as many smaller markets. Market entry of generic tulathromycin products in the U.S. is expected in 2021.

•Several patents covering Excede/Naxcel, part of the ceftiofur antibiotic product line, began expiring in the U.S. in 2015. The patent covering the commercial formulation of Excede in the U.S. extends to 2024, but expires in September 2021 in Europe, Canada and Australia. Corresponding patents in Japan and Brazil expire in 2026 and 2027, respectively. The commercial method of administration patent relevant to the product line expires in 2023 in the U.S., Europe and Australia. Generic versions of Excede have entered the market in Mexico and Russia. At this time, the market entry of a generic version of Excede in the U.S. is not anticipated before 2024.

•The compound patent for selamectin, the active ingredient in our parasiticides Revolution, Revolution Plus and Stronghold, expired in 2014. Formulation patents covering these products expired in important markets in 2019. Generic versions of selamectin are now sold in markets including the U.S., Europe, Australia and Canada.

•The patent for the active ingredient of Convenia has expired; however, there are formulation patents relevant to the product line which expire between November 2022 and October 2023.

•The patent for the active ingredient of Cerenia has expired; however, there are formulation patents relevant to the product line which expire between 2025 and 2028. Generic versions of Cerenia have been registered and marketed in Canada and Europe. At this time, there is no indication of an impending market entry of a generic version of Cerenia in the U.S.

•The formulation patent covering ProHeart 12 expired in the U.S. in 2019, but expires in Australia, Canada and Japan in October 2021.

Zoetis typically enforces its patents vigorously as appropriate both within and outside the U.S., including by filing infringement claims against other parties.

Additionally, many of our vaccine products are based on proprietary master seeds and proprietary or patented adjuvant formulations. We actively seek to protect our proprietary information, including our trade secrets and proprietary know-how, including by seeking to require our employees, consultants, advisors and partners to enter into confidentiality agreements and other arrangements upon the commencement of their employment or engagement.

Following our separation from Pfizer, Pfizer licenses to us the right to use certain intellectual property rights in the animal health field. We license to Pfizer the right to use certain of our trademarks and substantially all of our other intellectual property rights in the human health field and all other fields outside of animal health. In addition, Pfizer granted us a perpetual license to use certain of Pfizer's product name trademarks.

We seek to file and maintain trademarks around the world based on commercial activities in most regions where we have, or desire to have, a business presence for a particular product or service. We currently maintain more than 8,200 trademark applications and registrations in our market countries, identifying products and services dedicated to the care of companion animals and livestock.

Regulatory

The sale of animal health products is governed by the laws and regulations specific to each country in which we market our products. To maintain compliance with these regulatory requirements, we have established processes, systems and dedicated resources with end-to-end involvement from product concept to launch and maintenance in the market. Our regulatory function actively engages in dialogue with various global agencies regarding their policies that relate to animal health products. In the majority of our markets, the relevant animal health authority is separate from those governing human medicinal products.

United States

United States Food and Drug Administration (FDA). The regulatory body that is responsible for the regulation of animal health pharmaceuticals in the U.S. is the Center for Veterinary Medicine (CVM), housed within the FDA. All manufacturers of animal health pharmaceuticals must show their products to be safe, effective and produced by a consistent method of manufacture as defined under the Federal Food, Drug and Cosmetic Act. The FDA's basis for approving a drug application is documented in a Freedom of Information Summary. Post-approval monitoring of products is required by law, with reports being provided to the CVM's Surveillance and Compliance group. Reports of product quality defects, adverse events or unexpected results are produced in accordance with the law. Additionally, we are required to submit all new information for a product, regardless of the source.

United States Department of Agriculture (USDA). The regulatory body in the U.S. for veterinary vaccines is the USDA. The USDA's Center for Veterinary Biologics is responsible for the regulation of animal health vaccines, including immunotherapeutics. All manufacturers of animal health

9 |

biologicals must show their products to be pure, safe, effective and produced by a consistent method of manufacture as defined under the Virus Serum Toxin Act. Post-approval monitoring of products is required. Reports of product quality defects, adverse events or unexpected results are produced in accordance with the agency requirements.

Environmental Protection Agency (EPA). The main regulatory body in the U.S. for veterinary pesticides is the EPA. The EPA's Office of Pesticide Programs is responsible for the regulation of pesticide products applied to animals. All manufacturers of animal health pesticides must show their products will not cause “unreasonable adverse effects to man or the environment” as stated in the Federal Insecticide, Fungicide, and Rodenticide Act. Within the U.S., pesticide products that are approved by the EPA must also be approved by individual state pesticide authorities before distribution in that state. Post-approval monitoring of products is required, with reports provided to the EPA and some state regulatory agencies.

In addition, the U.S. Foreign Corrupt Practices Act (FCPA) prohibits U.S. corporations and their representatives from offering, promising, authorizing or making payments to any foreign government official, government staff member, political party or political candidate in an attempt to obtain or retain business abroad. The scope of the FCPA includes interactions with certain healthcare professionals in many countries. Other countries have enacted similar anti-corruption laws and/or regulations.

We are also subject to foreign trade controls administered by certain U.S. government agencies, including the Bureau of Industry and Security within the Commerce Department, Customs and Border Protection within the Department of Homeland Security and OFAC. As a global animal health company, we conduct business in multiple jurisdictions throughout the world. This includes supplying medicines and medical products for use in Iran and shipment of products to Iran, and conducting related activities, in accordance with a general license issued by OFAC and in line with our corporate policies. As previously disclosed, we acquired Platinum Performance (Platinum) in August 2019. During the integration process, after the closing of the acquisition, we discovered that Platinum had initiated certain transactions involving sales of food, medicine or devices to individuals or entities who may have been resident in or had ties to Iran. These sales were not conducted pursuant to a general license from OFAC and potentially violated the Iranian Transactions and Sanctions Regulations (ITSR) administered by OFAC. We submitted an initial voluntary disclosure to OFAC in February 2020 while our internal investigation was ongoing. After concluding our internal investigation, in December 2020, we submitted a final voluntary disclosure to OFAC and the U.S. Department of Justice regarding these transactions.

As a result of our acquisition of Abaxis, our product portfolio includes human medical diagnostics, which are subject to regulation in the U.S. by the FDA under the Federal Food, Drug, and Cosmetic Act, including the 1976 Medical Device Amendments and the Quality System Regulation, and the Clinical Laboratory Improvement Amendments of 1988, and by the Department of Health and Human Services Office for Civil Rights under the Health Insurance Portability and Accountability Act of 1996.

Outside the United States

European Union (EU). The European Medicines Agency (EMA) is the centralized regulatory agency of the EU. The agency is responsible for the scientific evaluation of medicines developed by healthcare companies seeking centralized approval for use in the EU. The agency has a veterinary review section distinct from the medical review section. The Committee for Medicinal Products for Veterinary Use (CVMP) is responsible for scientific and technical review of the submissions for innovative pharmaceuticals, biopharmaceuticals and vaccines. After the CVMP issues a positive opinion on the approvability of a product, the EU commission reviews the opinion and, if they agree with the CVMP, they grant the product market authorization. Once granted by the European Commission, a centralized marketing authorization is valid in all EU and European Economic Area-European Free Trade Association states. Products can also be registered in the EU via a decentralized route under the supervision of the Co-ordination Group for Mutual Recognition and Decentralized Procedures - Veterinary (CMDv). This co-ordination group is composed of one representative per member state from each national regulatory agency, including Norway, Iceland and Liechtenstein. The CMDv reviews submissions of pharmaceuticals and vaccines for authorization of a veterinary product in two or more member states in accordance with the mutual recognition or the decentralized procedure. A series of Regulations, Directives, Guidelines and EU Pharmacopeia Monographs provide the requirements for product approval in the EU. In general, these requirements are similar to those in the U.S., requiring demonstrated evidence of, safety, efficacy, and quality/consistency of manufacturing processes. We are also subject to the EU General Data Protection Regulation (GDPR) that requires us to meet enhanced requirements regarding the handling of personal data, including its use, protection and the rights of data subjects to request correction or deletion of their personal data.

Brazil. The Ministry of Agriculture, Livestock Production and Supply (MAPA) is the regulatory body in Brazil that is responsible for the regulation and control of pharmaceuticals, biologicals and medicated feed additives for animal use. MAPA's regulatory activities are conducted through the Secretary of Agricultural Defense and its Livestock Products Inspection Department. In addition, regulatory activities are conducted at a local level through the Federal Agriculture Superintendence. These activities include the inspection and licensing of both manufacturing and commercial establishments for veterinary products, as well as the submission, review and approval of pharmaceuticals, biologicals and medicated feed additives. MAPA is one of the most active regulatory agencies in Latin America, having permanent seats at several international animal health forums, such as Codex Alimentarius, World Organization for Animal Health and Committee of Veterinary Medicines for the Americas. MAPA was also invited to be a Latin American representative at meetings of the International Cooperation on Harmonisation of Technical Requirements for Registration of Veterinary Medicinal Products (VICH). Several normative instructions issued by MAPA have set regulatory trends in Latin America.

Australia. The Australian Pesticides and Veterinary Medicines Authority (APVMA) is an Australian government statutory authority established in 1993 to centralize the registration of all agricultural and veterinary products into the Australian marketplace. Previously each State and Territory government had its own system of registration. The APVMA assesses applications from companies and individuals seeking registration so they can supply their product to the marketplace. Applications undergo rigorous assessment using the expertise of the APVMA's scientific staff and drawing on the technical knowledge of other relevant scientific organizations, Commonwealth government departments and state agriculture departments. If the product works as intended and the scientific data confirms that when used as directed on the product label it will have no harmful or unintended effects on people, animals, the environment or international trade, the APVMA will register the product. As well as registering new agricultural and veterinary products, the APVMA reviews older products that have been on the market for a substantial period of time to ensure they still do the job users expect and are safe to use. The APVMA also reviews registered products when particular concerns are raised about their safety and effectiveness. The review of a product may result in confirmation of its registration, or it may see registration continue with some changes to the way the product can be used. In some cases the review may result in the registration of a product being canceled and the product taken off the market.

10 |

Rest of world. Country-specific regulatory laws have provisions that include requirements for certain labeling, safety, efficacy and manufacturers' quality control procedures (to assure the consistency of the products), as well as company records and reports. With the exception of the EU, most other countries' regulatory agencies will generally refer to the FDA, USDA, EU and other international animal health entities, including the World Organization for Animal Health and Codex Alimentarius, in establishing standards and regulations for veterinary pharmaceuticals and vaccines.

Global policy and guidance

Joint FAO/WHO Expert Committee on Food Additives. The Joint FAO/WHO Expert Committee on Food Additives is an international expert scientific committee that is administered jointly by the Food and Agriculture Organization of the United Nations (FAO) and the World Health Organization (WHO). They provide a risk assessment/safety evaluation of residues of veterinary drugs in animal products, exposure and residue definition and maximum residue limit proposals for veterinary drugs. We work with them to establish acceptable safe levels of residual product in food-producing animals after treatment. This in turn enables the calculation of appropriate withdrawal times for our products prior to an animal entering the food chain.

Advertising and promotion review. Promotion of prescription animal health products is controlled by regulations in many countries. These rules generally restrict advertising and promotion to those claims and uses that have been reviewed and endorsed by the applicable agency. We conduct a review of promotion materials for compliance with the local and regional requirements in the markets where we sell animal health products.

Food Safety Inspection Service/generally recognized as safe. The FDA is authorized to determine the safety of substances (including “generally recognized as safe” substances, food additives and color additives), as well as prescribing safe conditions of use. However, although the FDA has the responsibility for determining the safety of substances, the Food Safety and Inspection Service, the public health agency in the USDA, still retains, under the tenets of the Federal Meat Inspection Act and the Poultry Products Inspection Act and their implementing regulations, the authority to determine whether new substances and new uses of previously approved substances are suitable for use in meat and poultry products.

International Cooperation on Harmonisation of Technical Requirements for Registration of Veterinary Medicinal Products (VICH). VICH is a trilateral (EU-Japan-USA) program aimed at harmonizing technical requirements for veterinary product registration. The objectives of the VICH are as follows:

•Establish and implement harmonized technical requirements for the registration of veterinary medicinal products in the VICH regions, which meet high quality, safety and efficacy standards and minimize the use of test animals and costs of product development.

•Provide a basis for wider international harmonization of registration requirements through the VICH Outreach Forum (VOF).

•Monitor and maintain existing VICH guidelines, taking particular note of the ICH work program and, where necessary, update these VICH guidelines.

•Ensure efficient processes for maintaining and monitoring consistent interpretation of data requirements following the implementation of VICH guidelines.

•By means of a constructive dialogue between regulatory authorities and industry, provide technical guidance enabling response to significant emerging global issues and science that impact on regulatory requirements within the VICH regions.

Human Capital Management

As of December 31, 2020, we had approximately 11,300 employees worldwide, which included approximately 5,300 employees in the U.S. and approximately 6,000 in other jurisdictions. We view the strength of our team and our talented colleagues around the world as a critical component of our past and future success. We are committed to continuing to be a company our colleagues can be proud of and to attracting, retaining and developing the best talent in the industry through our focus on workplace culture and engagement, diversity, equity and inclusion, talent recruitment, development and retention, benefits and compensation, and employee health and safety. The Human Resources Committee of our Board of Directors is responsible for overseeing talent development, diversity and inclusion, and employee engagement programs and policies, and the Quality and Innovation Committee regularly reviews employee health and safety metrics.

Certain of our employees are members of unions, works councils, trade associations or are otherwise subject to collective bargaining agreements in particular jurisdictions, including a small number of employees in the U.S.

Workplace Culture and Employee Engagement

We have established Core Beliefs that are the foundation of the commitments we make to each other, our customers and our stakeholders every day:

•Our Colleagues Make the Difference

•Always Do the Right Thing

•Customer Obsessed

•Run It Like You Own It

•We are One Zoetis

We value responsibility and integrity. Our Code of Conduct contains general guidelines for conducting business with the highest standards of ethics. We are committed to an environment where open, honest communications are the expectation, not the exception. We have an Open Door Policy where colleagues are encouraged to present ideas, concerns, questions, problems or suggestions directly to any level of leadership within Zoetis, without fear of retaliation.

We assess colleague engagement and key drivers enabling organizational performance by regularly conducting employee engagement surveys. Our engagement rate in 2020 was 89%. Insights from the Company’s engagement survey are used to develop both company-wide and business function level organizational and talent development plans.

11 |

Diversity, Equity and Inclusion

We strive to create an environment where colleagues feel valued and cared for and understand the important role we play in embracing diversity to improve the quality of our innovation, collaboration and relationships. In January 2020, we appointed a new Chief Talent, Diversity, Equity & Inclusion Officer, reporting to our Chief Human Resources Officer, who oversees a team dedicated to executing on our diversity, equity and inclusion strategy, which is reviewed with our executive leadership team and Board of Directors each year.

Our diversity, equity & inclusion focus and commitment begins with our leadership team of diverse backgrounds, experiences and ethnicities (50% of the executive team, including our Chief Executive Officer, are women), and it is demonstrated in our support of our colleagues and industry. We are committed to accelerating inclusion, equity and more diverse representation across the company and have developed aspirations for change to make Zoetis and our industry more inclusive, including specific aspirations focused on increasing the representation of people of color and women within our company by the end of 2025.

•Increase representation of women at the director level and above globally from 32% to 40%;

•Increase overall representation among people of color in the U.S. from 21% to 25%;

•Increase representation of Black colleagues in the U.S. from 4% to 5%; and

•Increase representation of Latinx colleagues in the U.S. from 5% to 6%.

We established a Diversity, Equity & Inclusion Council in January 2020 that represents a diverse group of colleagues across locations, functions and communities, who serve as ambassadors and champions for diversity, equity and inclusion initiatives. In addition to the Diversity, Equity & Inclusion Council, in 2020, we also introduced six Colleague Resource Groups, which are an important catalyst to foster a diverse, inclusive environment, while positively impacting our business and community.

In 2020, we offered diversity, equity and inclusion training to all our employees.

Talent Recruitment, Development and Retention

We employ a variety of career development, employee benefits, policies and compensation programs designed to attract, develop and retain our colleagues. Employee benefits and policies are designed for diverse needs including generous parental leave policies and expanded adoption, fertility and surrogacy benefits for all colleagues equitably. We have internal programs designed to develop and retain talent, including a talent portal, mentoring programs, career planning resources, leadership development programs, performance management and training programs. In particular, our R&D team recruits scientists and research and development personnel from universities and scientific associations and forums and leverages a variety of R&D-specific talent tools. In 2020, our voluntary attrition rate was 10.6%.

Compensation and Benefits

We strive to support our colleagues’ well-being and enable them to achieve their best at work and at home. Our compensation and benefits and programs are designed to support colleague well-being including physical and mental health, financial wellness, and family and lifestyle resources. We recognize the diverse needs of our colleagues around the world and have developed comprehensive programs that vary by country and region to best address them. In the U.S., these benefits include flexible work arrangements, educational assistance, mental health support, and inclusive family-friendly benefits like fully paid parental leave, including for adoptions, fathers and same sex partners, as well as fertility and surrogacy benefits. During the COVID-19 pandemic, we enhanced our childcare benefits and our flexible work arrangements to support our colleagues in managing their work and family responsibilities.

We are proud of our continuing record of being recognized as a top employer by esteemed publications and organizations around the world.

Employee Health and Safety

We are committed to ensuring a safe working environment for our colleagues, and our Global Environmental Health and Safety (EHS) Policy standards define EHS performance requirements for each site, procedures and recommended practices. Our sites have injury prevention programs, and we strive to build a best-in-class safety culture. Our procedures emphasize the need for the cause of injuries to be investigated and for action plans to be implemented to mitigate potential recurrence.

We track health and safety performance metrics including total injury rate (TIR), lost time injury rate (LTIR), restricted work injuries and medical treatment injuries on a monthly basis for all manufacturing and research and development sites, as well as for U.S. offices, field force, fleet and logistics. Since 2018, we have tracked TIR and LTIR for all our operations worldwide. Our safety programs have resulted in strong safety performance, with TIR and LTIR rates being lower than the industry averages.

In response to the COVID-19 pandemic, we have implemented and continue to implement safety measures in all our facilities.

12 |

Information about our Executive Officers

Kristin C. Peck

Age 49

Chief Executive Officer and Director

Ms. Peck has served as our Chief Executive Officer since January 2020 and as a director since October 2019. Prior to becoming CEO, Ms. Peck was Executive Vice President and Group President, U.S. Operations, Business Development and Strategy at Zoetis from March 2018 to December 2019. Ms. Peck previously served as our Executive Vice President and President, U.S. Operations from May 2015 to February 2018 and Executive Vice President and Group President from October 2012 through April 2015. In these roles, Ms. Peck helped usher Zoetis through its Initial Public Offering in 2013 and has been a driving force of change in areas including Global Manufacturing and Supply, Global Poultry, Global Diagnostics, Corporate Development, and New Product Marketing and Global Market Research. Before joining Zoetis, Ms. Peck served as Executive Vice President, Worldwide Business Development and Innovation at Pfizer Inc. and as a member of Pfizer's Executive Leadership Team.

Glenn David

Age 49

Executive Vice President and Chief Financial Officer

Mr. David has served as our Executive Vice President and Chief Financial Officer since August 2016. With more than 25 years of experience in finance and operations, Mr. David has played a key role in leading the financial operations for Zoetis since its initial public offering in 2013. He served as our Senior Vice President of Finance Operations from 2013 to 2016 and as acting Chief Financial Officer from April 2014 through August 2014. Mr. David joined Pfizer in 1999 and held various financial roles, including Vice President of Global Finance for Pfizer Animal Health, our predecessor company, and Vice President of Finance for the U.S. Primary Care franchise.

Timothy J. Bettington

Age 47

Executive Vice President and President, U.S. Operations

Mr. Bettington has served as our Executive Vice President and President, U.S. Operations since January 2020. Mr. Bettington joined Zoetis from Boehringer Ingelheim (BI) where he served for 12 years, most recently as North American Region Head of Commercial Operations for BI’s animal health business from January 2017 to December 2019. Mr. Bettington was also BI’s Global Head of Customer Experience from August 2015 to December 2016, and Vice President of Sales and Marketing for the U.S. from April 2012 to July 2015. Prior to BI, Mr. Bettington served as Senior Manager Food Animal Marketing at Novartis Animal Health from February 2006 to March 2008. During his years at BI and Novartis Animal Health, Mr. Bettington developed a deep expertise in sales, marketing, strategy and business integration.

Heidi C. Chen

Age 54

Executive Vice President, General Counsel and Corporate Secretary

Ms. Chen has served as our Executive Vice President and General Counsel since October 2012, and as our Corporate Secretary since July 2012. Since January 2020, Ms. Chen has had oversight responsibility for our Human Health Diagnostics business. Prior to Zoetis, Ms. Chen was Vice President and Chief Counsel of Pfizer Animal Health, our predecessor company, from 2009 to 2012. Ms. Chen joined Pfizer in 1998 and held various legal and compliance positions of increasing responsibility, including lead counsel for Pfizer’s Established Products (generics) business.

Robert E. Kelly

Age 49

Executive Vice President and President, International Operations

Mr. Kelly was appointed Executive Vice President and President, International Operations in January 2020, and also oversees Pharmaq, our aquatic health business. Mr. Kelly was previously our President of International Operations from March 2018 to December 2019, Senior Vice President of the Asia-Pacific Cluster from April 2015 to February 2018 and Senior Vice President of U.S. Cattle and Equine from November 2009 to April 2015. Mr. Kelly also worked at Wyeth/Fort Dodge Animal Health and Schering Plough before joining Pfizer Animal Health as part of the Wyeth acquisition.

Catherine A. Knupp

Age 60

Executive Vice President and President of Research and Development

Dr. Knupp has served as our Executive Vice President and President of Research and Development since October 2012. From 2005 to 2012, she served as Vice President of Pfizer’s Veterinary Medicine Research and Development business unit. Dr. Knupp joined Pfizer in July 2001 and held various positions, including Vice President of Pfizer’s Michigan laboratories for Pharmacokinetics, Dynamics and Metabolism.

13 |

Roxanne Lagano

Age 56

Executive Vice President, Chief Human Resources Officer and Global Operations

Ms. Lagano has served as our Executive Vice President and Chief Human Resources Officer since November 2012 and was given responsibility for the Global Operations and Security functions in January 2020. She previously had oversight of the company’s Corporate Communications function from 2015 to 2019. Prior to joining Zoetis, Ms. Lagano was Senior Vice President, Global Compensation, Benefits and Wellness for Pfizer. Ms. Lagano joined Pfizer in 1997 and held various positions, including Senior Director, Business Transactions, Pfizer Worldwide Human Resources.

Wafaa Mamilli

Age 54

Executive Vice President and Chief Information and Digital Officer

Ms. Mamilli has served as our Executive Vice President and Chief Information and Digital Officer since January 2020. Ms. Mamilli joined Zoetis from Eli Lilly and Company where she most recently served as Global Chief Information Officer for business units from January 2019 to January 2020, where she had worldwide responsibility for digital and technology across customer experience, sales, marketing and medical affairs for diabetes, oncology, bio medicines and international business. Prior to that, she was Eli Lilly’s Chief Information Security Officer from March 2016 to March 2019 and Information Officer for the Diabetes Business Unit & Real World Evidence from May 2014 to March 2016. During her tenure at Eli Lilly, Ms. Mamilli held a variety of international and U.S. leadership positions while establishing high-performing teams to identify and deliver on opportunities at the intersection of healthcare, information technology, big data and analytics.

J. Michael McFarland

Age 62

Executive Vice President and Chief Medical Officer

Dr. McFarland was appointed Executive Vice President and Chief Medical Officer in November 2020 and also leads Global Commercial Development (GCD), Customer Experience, and Sustainability at Zoetis. Previously, Dr. McFarland served as our Executive Vice President and Group President, Accelerated Growth Businesses from January 2020 to November 2020 where he oversaw a portfolio of Zoetis businesses, including Global Diagnostics, Genetics, BioDevices, Precision Livestock Farming and Platinum Performance. Dr. McFarland previously served as our Head of U.S. Cattle Marketing and Marketing Operations from May 2019 to January 2020, after having played a similar role for the U.S. Petcare business from June 2015 to May 2019 during a period of key product launches and growth. During his career, he has led veterinary services and marketing organizations for companion animals and livestock at Zoetis and Pfizer. Dr. McFarland also worked for 15 years in private practice as a companion animal veterinarian.

Abhay Nayak

Age 33

Executive Vice President, Head of Strategy and Accelerated Growth Businesses

Mr. Nayak serves as our Executive Vice President, Head of Strategy and Accelerated Growth Businesses, where he leads our global business strategy and drives strategic alignment and execution across a group of businesses, including Global Diagnostics, Genetics, BioDevices, Precision Livestock Farming and Platinum Performance. He was appointed as our Head of Strategy and Accelerated Growth Businesses in November 2020 and became Executive Vice President in February 2021. Previously, he served as our Head of Global Strategy, Commercial Development and Customer Experience at Zoetis from January 2020 to November 2020 and as our Head of Corporate Strategy from July 2018 to December 2019. Prior to joining Zoetis, Mr. Nayak was a consultant at McKinsey & Company from July 2015 to June 2018, where he advised leading pharmaceutical and medical device companies on crafting and executing global growth strategies. Prior to that, Mr. Nayak was an Assistant Vice President at Barclays Bank Plc in their Investment Banking Division in London.

Sherry Pudloski

Age 53

Executive Vice President, Corporate Affairs and Communications

Ms. Pudloski has served as our Executive Vice President, Corporate Affairs and Communications since March 2020, overseeing Zoetis' U.S. and International Public Affairs teams and Corporate Communications organization. Ms. Pudloski joined Zoetis from Guardian Life Insurance Company where she most recently served as Chief Communications Officer. Ms. Pudloski has considerable experience in communications, corporate social responsibility and healthcare policy. She formerly held executive leadership roles with Pfizer, Novartis and Ogilvy Public Relations, where she led the global healthcare practice.

Roman Trawicki

Age 57

Executive Vice President and President of Global Manufacturing and Supply