Use these links to rapidly review the document

TABLE OF CONTENTS

Filed pursuant to Rule 424(b)(5)

Registration No. 333-194770

The information contained in this preliminary prospectus supplement is not complete and may be changed. This preliminary prospectus supplement and the accompanying prospectus are not an offer to sell these securities and are not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to completion, dated June 17, 2014

PRELIMINARY PROSPECTUS SUPPLEMENT

(To Prospectus Dated April 4, 2014)

12,500,000 Shares

COMMON STOCK

We are offering 12,500,000 shares of our common stock, par value $0.01 per share.

The net proceeds of the offering will be used by us to acquire 12,500,000 common units (or 14,375,000 common units if the underwriters exercise their option to purchase additional shares of our common stock in full, assuming one common unit will be purchased for every share of common stock issued by us in this offering) of limited partnership interests ("operating partnership units") in CyrusOne LP from a subsidiary of Cincinnati Bell Inc.

To assist us in complying with certain U.S. federal income tax requirements applicable to real estate investment trusts ("REITs"), among other purposes, our charter contains certain restrictions relating to the ownership and transfer of our stock, including an ownership limit of 9.8% of our outstanding common stock, subject to certain exceptions. See "Description of Securities—Restrictions on Ownership and Transfer" in the accompanying prospectus for a detailed description of the ownership and transfer restrictions applicable to our common stock.

Our common stock is listed on the NASDAQ Global Select Market under the symbol "CONE." On June 16, 2014, the last reported sale price of our common stock on the NASDAQ Global Select Market was $22.87 per share.

We are an "emerging growth company" under the Jumpstart Our Business Startups Act of 2012. Investing in our common stock involves risks. See "Risk Factors" beginning on page S-17 of this prospectus supplement.

|

||||

| |

Per Share |

Total |

||

|---|---|---|---|---|

Public Offering Price |

$ | $ | ||

Underwriting Discounts(1) |

$ | $ | ||

Proceeds to CyrusOne (before expenses) |

$ | $ | ||

|

||||

- (1)

- We refer you to "Underwriting" beginning on page S-23 of this prospectus supplement for additional information regarding underwriting compensation.

We have granted the underwriters the option to purchase up to an additional 1,875,000 shares of our common stock at the public offering price, less underwriting discounts, for thirty days after the date of this prospectus supplement.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We previously announced a dividend of $0.21 per share of common stock and common stock equivalent for the second quarter of 2014. The dividend will be paid on July 15, 2014, to stockholders of record at the close of business on June 27, 2014. This offering is expected to close prior to June 27, 2014, therefore purchasers of our common stock that take delivery of such stock on the closing date and continue to hold such common stock as of the close of business on June 27, 2014 will receive the dividend.

Delivery of the shares is expected to be made to investors through the book-entry delivery system of The Depository Trust Company on or about June , 2014.

Joint Book-Running Managers

| Citigroup | BofA Merrill Lynch | |||

| Barclays | Deutsche Bank Securities | Morgan Stanley |

Co-Managers

| Cantor Fitzgerald & Co. | Evercore | KeyBanc Capital Markets | Stephens Inc. | UBS Investment Bank |

The date of this prospectus supplement is June , 2014.

Neither we nor the underwriters have authorized anyone to provide any information or to make any representations other than those contained or incorporated by reference into this prospectus supplement, the accompanying prospectus or any free writing prospectus we have prepared. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. You should assume that the information appearing in this prospectus supplement, the accompanying prospectus, any free writing prospectus prepared by us and the documents incorporated by reference herein is accurate only as of their respective dates or on the date or dates that are specified in those documents regardless of the time of delivery of this prospectus supplement and the accompanying prospectus or any sale of shares of our common stock. Our business, financial condition, liquidity, results of operations and prospects may have changed since those dates.

S-i

ABOUT THIS PROSPECTUS SUPPLEMENT

This document contains two parts. The first part is this prospectus supplement, which describes the terms of this offering of common stock and also adds to and updates information contained in the accompanying prospectus and the documents incorporated by reference. The second part is the accompanying prospectus, which provides more general information, some of which may not apply to this offering. It is important for you to read and consider all information contained in this prospectus supplement and the accompanying prospectus in making your investment decision. You should also read and consider the additional information included in the documents incorporated by reference. See "Where You Can Find More Information" and "Incorporation by Reference" in this prospectus supplement. If the information in this prospectus supplement differs or varies from the information in the accompanying prospectus or the documents incorporated by reference, you should rely on the information in this prospectus supplement.

Except as otherwise indicated or required by the context, references in this prospectus supplement to (i) "CyrusOne," "we," "our," "us," "the Company" and "our company" refer to CyrusOne Inc., a Maryland corporation, together with its combined subsidiaries, including CyrusOne LP, a Maryland limited partnership (our "operating partnership" or "CyrusOne LP"), and CyrusOne GP, a Maryland statutory trust of which we are the sole beneficial owner and sole trustee and which is the sole general partner of our operating partnership ("CyrusOne GP"), (ii) "CBI" refers to Cincinnati Bell Inc., an Ohio corporation, and, unless the context otherwise requires, its consolidated subsidiaries, and (iii) the number of operating partnership units gives effect to the approximately 2.8-to-1 operating partnership unit reverse split effected immediately prior to the completion of our initial public offering in January 2013.

S-ii

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus supplement, the accompanying prospectus and the documents incorporated by reference herein contain forward-looking statements within the meaning of the federal securities laws. You can identify forward-looking statements by the use of forward-looking terminology such as "believes," "expects," "may," "will," "should," "seeks," "approximately," "intends," "plans," "estimates" or "anticipates" or the negative of these words and phrases or similar words or phrases that are predictions of or indicate future events or trends and that do not relate solely to historical matters. You can also identify forward-looking statements by discussions of strategy, plans or intentions.

Forward-looking statements involve numerous risks and uncertainties and you should not rely on them as predictions of future events. Forward-looking statements depend on assumptions, data or methods that may be incorrect or imprecise and we may not be able to realize them. The following factors, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements:

- •

- loss of key customers;

- •

- defaults on or non-renewal or early termination of leases by customers;

- •

- economic downturn, natural disaster or oversupply of data centers in the limited geographic area that we serve;

- •

- inability to supply customers with adequate electrical power;

- •

- inability to renew leases on the data center buildings in our portfolio not owned by us;

- •

- risks related to natural disasters and inadequate insurance coverage;

- •

- risks related to the failure of our physical infrastructure or services;

- •

- risks related to the development of our properties and our ability to successfully lease those properties;

- •

- risks related to third-party suppliers of power;

- •

- internet connectivity and other services;

- •

- loss of access to key third-party service providers and suppliers;

- •

- long leasing cycle for data center services;

- •

- risks related to our international activities, including expanding our international operations;

- •

- inability to identify and complete acquisitions and operate acquired properties;

- •

- customers choosing to develop their own data centers;

- •

- decrease in demand for data center services;

- •

- inability to manage growth;

- •

- our failure to obtain necessary outside financing on favorable terms, or at all;

- •

- our level of indebtedness or debt service obligations;

- •

- restrictions in the instruments governing our indebtedness;

- •

- risks related to litigation;

- •

- risks related to environmental matters;

- •

- risks related to climate change regulations;

S-iii

- •

- unknown or contingent liabilities related to acquired properties;

- •

- management's inexperience operating a REIT;

- •

- significant competition in our industry;

- •

- loss of key personnel;

- •

- obsolescence of our data center infrastructure;

- •

- valuations and impairment charges of properties;

- •

- the impact of emerging growth company status on our common stock;

- •

- risks related to our National IX Platform;

- •

- risks associated with real estate assets and the real estate industry;

- •

- risks of illiquidity of real estate investments;

- •

- rights of stockholders;

- •

- potential conflict of interest between our operating partnership and its partners;

- •

- risks related to CBI owning shares of our common stock and operating partnership units;

- •

- potential conflict of interest between CyrusOne directors who remain involved with CBI;

- •

- provisions in our charter and bylaws that may limit an acquisition of our common stock or a change in control;

- •

- provisions of Maryland law that may limit the ability of a third-party to acquire control of us;

- •

- risks related to the assumption of liabilities from the transactions relating to our formation in 2012 and initial public

offering in 2013;

- •

- failure to maintain our status as a REIT;

- •

- highly technical and complex REIT provisions of the Internal Revenue Code of 1986, as amended (the "Code");

- •

- risk that dividends payable may not qualify for reduced tax rates;

- •

- risk that REIT distribution requirements could adversely affect our ability to execute our business plan;

- •

- risk that other tax liabilities may reduce cash flow;

- •

- risk that we may have to forego other opportunities due to compliance with REIT requirements;

- •

- risk that REIT requirements could limit our ability to hedge effectively;

- •

- risk of potential penalty tax caused by CBI's future acquisition of a significant percentage of our stock;

- •

- risk of changes in U.S. tax law and other U.S. laws, whether or not specific to REITs;

- •

- risk of insufficient cash available for distribution to stockholders;

- •

- risk that future offerings of debt may adversely affect the market price of our common stock;

- •

- risk that increases in market interest rates could drive potential investors to seek higher dividend yields and reduce

demand for our common stock;

- •

- risk that shares available for future sale could affect the market price of stock;

S-iv

- •

- risk that market price and volume of stock could be volatile; and

- •

- risk that earnings and cash distributions could affect the market price of our common stock.

While forward-looking statements reflect our good faith beliefs, they are not guarantees of future performance. We disclaim any obligation to publicly update or revise any forward-looking statement to reflect changes in underlying assumptions or factors of new information, data or methods, future events or other changes. For a further discussion of these and other factors that could impact our future results, performance or transactions, see the section in this prospectus supplement and the accompanying prospectus entitled "Risk Factors," including the risks incorporated herein and therein from our most recent Annual Report on Form 10-K filed with the Securities and Exchange Commission ("SEC") on March 3, 2014, as updated by our subsequent filings.

S-v

WHERE YOU CAN FIND MORE INFORMATION

We are subject to the information and reporting requirements of the Securities Exchange Act of 1934, as amended (the "Exchange Act") and, accordingly, file annual, quarterly and periodic reports, proxy statements and other information with the SEC. You may read and copy any reports, statements or other information we file with the SEC at the Public Reference Room of the SEC, 100 F Street, NE, Washington, D.C. 20549. Please call the SEC at 1-800-SEC-0330 for further information on the operation of the Public Reference Room. You may also obtain copies of this information by mail from the Public Reference Room of the SEC, 100 F Street, NE, Washington, D.C. 20549, at prescribed rates, or from commercial document retrieval services.

We have filed with the SEC a registration statement on Form S-3, including exhibits and schedules filed with the registration statement of which this prospectus supplement is a part, under the Securities Act of 1933, as amended (the "Securities Act"), with respect to the shares of our common stock registered hereby. This prospectus supplement and the accompanying prospectus do not contain all of the information set forth in the registration statement and exhibits and schedules to the registration statement. For further information with respect to our company and our shares of common stock registered hereby, reference is made to the registration statement, including the exhibits and schedules to the registration statement. Statements contained in this prospectus supplement and the accompanying prospectus as to the contents of any contract or other document referred to in this prospectus supplement and the accompanying prospectus are not necessarily complete and, where that contract is an exhibit to the registration statement, each statement is qualified in all respects by the exhibit to which the reference relates. Copies of the registration statement, including the exhibits and schedules to the registration statement, may be examined without charge at the Public Reference Room of the SEC, in the manner described above.

Our SEC filings, including our registration statement, are also available to you, free of charge, on the SEC's website at www.sec.gov. Our SEC filings will also be available through the Investor Relations section of CyrusOne Inc.'s website at www.cyrusone.com. The information contained on or linked to or from our website is not incorporated by reference into this prospectus supplement or the accompanying prospectus and is not considered part of this prospectus supplement or the accompanying prospectus.

S-vi

The SEC allows us to "incorporate by reference" certain information into this prospectus supplement from certain documents that we filed with the SEC prior to the date of this prospectus supplement. By incorporating by reference, we are disclosing important information to you by referring you to documents we have filed separately with the SEC. The information incorporated by reference is deemed to be part of this prospectus supplement, except for information incorporated by reference that is modified or superseded by information contained in this prospectus supplement or in any other subsequently filed document that also is incorporated by reference herein. Any statement so modified or superseded will not be deemed, except as so modified or superseded, to be part of this prospectus supplement. These documents contain important information about us, our business and our finances. The following documents previously filed with the SEC are incorporated by reference into this prospectus supplement except for any document or portion thereof deemed to be "furnished" and not filed in accordance with SEC rules:

- •

- Our Annual Report on Form 10-K for the year ended December 31, 2013, filed with the SEC on March 3,

2014;

- •

- Our Definitive Proxy Statement on Schedule 14A filed with the SEC on March 19, 2014;

- •

- Our Quarterly Report on Form 10-Q for the quarter ended March 31, 2014, filed with the SEC on May 9,

2014;

- •

- Our Current Reports on Form 8-K filed with the SEC on May 6, 2014 and May 22, 2014 (but only with

respect to Item 5.02(b)); and

- •

- The description of our common stock included in our registration statement on Form 8-A filed with the SEC on January 17, 2013.

We also incorporate by reference all documents we may file with the SEC pursuant to Sections 13(a), 13(c), 14 or 15(d) of the Exchange Act on or after the date we file this prospectus supplement and prior to the termination of the offering of securities covered by this prospectus supplement, except for any document or portion thereof deemed to be "furnished" and not filed in accordance with SEC rules. The information relating to us contained in this prospectus supplement does not purport to be comprehensive and should be read together with the information contained in the documents incorporated or deemed to be incorporated by reference herein.

If you request, either orally or in writing, we will provide you with a copy of any or all documents that are incorporated by reference herein. Such documents will be provided to you free of charge, but will not contain any exhibits, unless those exhibits are incorporated by reference into the document. Requests can be made by writing to Investor Relations at 1649 West Frankford Road, Carrollton, TX 75007. The documents may also be accessed on our website under the Investor Relations tab at www.cyrusone.com. Information contained on our website is not incorporated by reference into this prospectus supplement or the accompanying prospectus and is not considered part of this prospectus supplement or the accompanying prospectus.

S-vii

The following summary contains information about us and the offering. It does not contain all of the information that may be important to you in making a decision to purchase the common stock. For a more complete understanding of us and the common stock, we urge you to read this entire prospectus supplement, the accompanying prospectus and the documents incorporated by reference herein carefully, including the "Risk Factors" section and our financial statements and the notes to those statements incorporated by reference herein. See "Where You Can Find More Information" and "Incorporation by Reference" in this prospectus supplement.

Our Company

We are an owner, operator and developer of enterprise-class, carrier-neutral data center properties. Our data center properties are purpose-built facilities with redundant power, cooling and telecommunications systems. They are not network-specific and enable customer interconnectivity to a range of telecommunications carriers. We provide mission-critical data center facilities that protect and ensure the continued operation of information technology ("IT") infrastructure for approximately 630 customers in 25 operating data centers in 10 distinct markets (8 cities in the U.S., London and Singapore) as of March 31, 2014.

Our goal is to be the preferred global data center provider to the Fortune 1000. As of March 31, 2014, our customers included nine of the Fortune 20 and 135 of the Fortune 1000 or private or foreign enterprises of equivalent size. These 135 customers provided 74% of our annualized rent as of March 31, 2014.

We cultivate long-term strategic relationships with our customers and provide them with solutions for their data center facilities and IT infrastructure challenges. Our offerings provide flexibility, reliability and security and are delivered through a tailored customer service focused platform that is designed to foster long-term relationships. We focus on attracting customers that have not historically outsourced their data center needs and providing them with solutions that address their current and future needs. Our facilities and construction design allow us to offer flexibility in density, power resiliency and the opportunity for expansion as our customers' needs grow. We also offer high-performance, low-cost data transfer and accessibility for our customers through our interconnection platform, CyrusOne National IX, which delivers interconnection across states and between metro-enabled sites within the CyrusOne facility footprint and beyond.

Our Portfolio

As of March 31, 2014, our property portfolio included 25 operating data centers in 10 distinct markets (8 cities in the U.S., London and Singapore) collectively providing approximately 2,060,000 net rentable square feet ("NRSF"), of which 83% was leased, and powered by approximately 169 MW of universal power supply capacity. We own 14 of the buildings in which our data center facilities are located. We lease the remaining 11 buildings, which account for approximately 375,000 NRSF, or approximately 18% of our total operating NRSF. These leased buildings accounted for 24% of our total annualized rent as of March 31, 2014. The weighted average remaining lease term is approximately 8 years, or approximately 17 years after giving effect to our contractual renewal rights. As of that date, we also had approximately 761,000 NRSF under development and approximately 569,000 NRSF of additional powered shell available for development, which we believe we could use to construct up to approximately 900,000 square feet of colocation space ("CSF"). In addition, we have approximately 200 acres of land upon which we believe we could develop up to approximately 3,100,000 CSF. Along with our primary product offering, leasing of colocation space, our customers are increasingly interested in ancillary office and other space. We believe our existing operating portfolio and development pipeline will allow us to meet the evolving needs of our existing customers and continue to attract new customers.

S-1

The following tables provide an overview of our operating and development properties as of March 31, 2014.

| |

|

|

|

|

|

|

|

|

|

Powered Shell Available for Future Development (NRSF)(j) |

|

||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

|

|

Operating Net Rentable Square Feet (NRSF)(a) | |

|||||||||||||||||||||||||||||

| |

|

|

Available UPS Capacity (MW)(k) |

||||||||||||||||||||||||||||||

Facilities

|

Metro Area | Annualized Rent(b) |

Colocation Square Feet (CSF)(c) |

CSF Leased(d) |

CSF Utilized(e) |

Office & Other(f) |

Office & Other Leased(g) |

Supporting Infrastructure(h) |

Total(i) | ||||||||||||||||||||||||

Westway Park Blvd. |

Houston |

$ |

51,815,783 |

112,133 |

97 |

% |

97 |

% |

10,563 |

98 |

% |

37,063 |

159,759 |

3,000 |

28 |

||||||||||||||||||

(Houston West 1) |

|||||||||||||||||||||||||||||||||

Southwest Fwy. |

Houston |

40,167,850 |

63,469 |

92 |

% |

92 |

% |

17,259 |

69 |

% |

23,203 |

103,931 |

— |

14 |

|||||||||||||||||||

(Galleria) |

|||||||||||||||||||||||||||||||||

S. State Hwy 121 |

Dallas |

37,927,019 |

108,687 |

97 |

% |

97 |

% |

11,279 |

96 |

% |

59,345 |

179,311 |

— |

18 |

|||||||||||||||||||

Business |

|||||||||||||||||||||||||||||||||

(Lewisville)* |

|||||||||||||||||||||||||||||||||

West Seventh Street |

Cincinnati |

34,442,528 |

211,718 |

90 |

% |

91 |

% |

5,744 |

100 |

% |

171,561 |

389,023 |

37,000 |

13 |

|||||||||||||||||||

(7th St.)*** |

|||||||||||||||||||||||||||||||||

Fujitec Drive |

Cincinnati |

21,001,479 |

65,303 |

79 |

% |

79 |

% |

36,261 |

90 |

% |

49,159 |

150,723 |

72,000 |

14 |

|||||||||||||||||||

(Lebanon) |

|||||||||||||||||||||||||||||||||

Westover Hills Blvd. |

San Antonio |

16,437,632 |

43,487 |

100 |

% |

100 |

% |

5,633 |

85 |

% |

45,939 |

95,058 |

11,000 |

12 |

|||||||||||||||||||

(San Antonio 1) |

|||||||||||||||||||||||||||||||||

W. Frankford Road |

Dallas |

15,339,297 |

107,616 |

69 |

% |

100 |

% |

19,706 |

20 |

% |

53,588 |

180,910 |

345,000 |

9 |

|||||||||||||||||||

(Carrollton) |

|||||||||||||||||||||||||||||||||

Industrial Road |

Cincinnati |

14,721,210 |

52,698 |

100 |

% |

100 |

% |

46,848 |

87 |

% |

40,374 |

139,920 |

— |

9 |

|||||||||||||||||||

(Florence) |

|||||||||||||||||||||||||||||||||

Knightsbridge Drive |

Cincinnati |

11,275,885 |

46,565 |

89 |

% |

89 |

% |

1,077 |

100 |

% |

35,336 |

82,978 |

— |

10 |

|||||||||||||||||||

(Hamilton)* |

|||||||||||||||||||||||||||||||||

E. Ben White Blvd. |

Austin |

6,776,994 |

16,223 |

85 |

% |

86 |

% |

21,376 |

100 |

% |

7,516 |

45,115 |

— |

2 |

|||||||||||||||||||

(Austin 1)* |

|||||||||||||||||||||||||||||||||

Parkway Dr. |

Cincinnati |

5,833,599 |

34,072 |

100 |

% |

100 |

% |

26,458 |

98 |

% |

17,193 |

77,723 |

— |

4 |

|||||||||||||||||||

(Mason) |

|||||||||||||||||||||||||||||||||

Metropolis Drive |

Austin |

5,432,430 |

37,780 |

76 |

% |

77 |

% |

4,128 |

17 |

% |

18,444 |

60,352 |

— |

5 |

|||||||||||||||||||

(Austin 2) |

|||||||||||||||||||||||||||||||||

Midway Rd.** |

Dallas |

5,397,862 |

8,390 |

100 |

% |

100 |

% |

— |

— |

— |

8,390 |

— |

1 |

||||||||||||||||||||

South Ellis Street |

Phoenix |

5,207,640 |

77,504 |

88 |

% |

93 |

% |

37,040 |

7 |

% |

32,723 |

147,267 |

31,000 |

11 |

|||||||||||||||||||

(Phoenix 1) |

|||||||||||||||||||||||||||||||||

Westway Park Blvd. |

Houston |

4,544,037 |

79,492 |

36 |

% |

42 |

% |

3,112 |

31 |

% |

30,597 |

113,201 |

12,000 |

12 |

|||||||||||||||||||

(Houston West 2) |

|||||||||||||||||||||||||||||||||

Kestral Way |

London |

3,460,588 |

10,000 |

99 |

% |

99 |

% |

— |

— |

— |

10,000 |

— |

1 |

||||||||||||||||||||

(London)** |

|||||||||||||||||||||||||||||||||

Springer Street |

Chicago |

2,403,080 |

13,516 |

47 |

% |

50 |

% |

4,115 |

100 |

% |

12,230 |

29,861 |

29,000 |

3 |

|||||||||||||||||||

(Lombard) |

|||||||||||||||||||||||||||||||||

Marsh Ln.** |

Dallas |

2,100,163 |

4,245 |

100 |

% |

100 |

% |

— |

— |

— |

4,245 |

— |

1 |

||||||||||||||||||||

Goldcoast Drive |

Cincinnati |

1,463,036 |

2,728 |

100 |

% |

100 |

% |

5,280 |

100 |

% |

16,481 |

24,489 |

14,000 |

1 |

|||||||||||||||||||

(Goldcoast) |

|||||||||||||||||||||||||||||||||

E. Monroe Street |

South Bend |

1,039,540 |

6,350 |

64 |

% |

64 |

% |

— |

— |

6,478 |

12,828 |

4,000 |

1 |

||||||||||||||||||||

(Monroe St.) |

|||||||||||||||||||||||||||||||||

Bryan St.** |

Dallas |

976,533 |

3,020 |

57 |

% |

57 |

% |

— |

— |

— |

3,020 |

— |

1 |

||||||||||||||||||||

North Fwy. |

Houston |

837,564 |

13,000 |

100 |

% |

100 |

% |

1,449 |

100 |

% |

— |

14,449 |

— |

1 |

|||||||||||||||||||

(Greenspoint)** |

|||||||||||||||||||||||||||||||||

Crescent Circle |

South Bend |

668,887 |

3,432 |

49 |

% |

49 |

% |

— |

— |

5,125 |

8,557 |

11,000 |

1 |

||||||||||||||||||||

(Blackthorn)* |

|||||||||||||||||||||||||||||||||

McAuley Place |

Cincinnati |

620,448 |

6,193 |

39 |

% |

39 |

% |

6,950 |

100 |

% |

2,166 |

15,309 |

— |

1 |

|||||||||||||||||||

(Blue Ash)* |

|||||||||||||||||||||||||||||||||

Jurong East |

Singapore |

307,680 |

3,200 |

12 |

% |

12 |

% |

— |

— |

— |

3,200 |

— |

1 |

||||||||||||||||||||

(Singapore)** |

|||||||||||||||||||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total |

$ | 290,198,764 | 1,130,821 | 84 | % | 89 | % | 264,278 | 72 | % | 664,521 | 2,059,619 | 569,000 | 169 | |||||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

- *

- Indicates

properties in which we hold a leasehold interest in the building shell and land. All data center infrastructure has been constructed by us and is

owned by us.

- **

- Indicates properties in which we hold a leasehold interest in the building shell, land, and all data center infrastructure.

S-2

- ***

- The

information provided for the West Seventh Street (7th St.) property includes data for two facilities, one of which we lease and one of which we

own.

- (a)

- Represents

the total square feet of a building under lease or available for lease based on engineers' drawings and estimates but does not include space held

for development or space used by CyrusOne.

- (b)

- Represents

monthly contractual rent (defined as cash rent including customer reimbursements for metered power) under existing customer leases as of

March 31, 2014, multiplied by 12. For the month of March 2014, our total annualized rent was $290.2 million and customer reimbursements were $30.6 million annualized and consisted

of reimbursements by customers across all facilities with separately metered power. Customer reimbursements under leases with separately metered power vary from month-to-month based on factors such as

our customers' utilization of power and the suppliers' pricing of power. From April 1, 2012 through March 31, 2014, customer reimbursements under leases with separately metered power

constituted between 8.6% and 10.6% of annualized rent. After giving effect to abatements, free rent and other straight-line adjustments, our annualized effective rent as of March 31, 2014 was

$301,286,789. Our annualized effective rent was greater than our annualized rent as of March 31, 2014 because our positive straight-line and other adjustments and amortization of deferred

revenue exceeded our negative straight-line adjustments due to factors such as the timing of contractual rent escalations and customer prepayments for services.

- (c)

- Represents

the NRSF at an operating facility that is currently leased or readily available for lease as colocation space, where customers locate their

servers and other IT equipment.

- (d)

- Percent

leased is determined based on CSF being billed to customers under signed leases as of March 31, 2014 divided by total CSF. Leases signed but

not commenced as of March 2014 are not included.

- (e)

- Utilization

is calculated by dividing CSF under signed leases for colocation space (whether or not the customer has occupied the space) by total CSF.

- (f)

- Represents

the NRSF at an operating facility that is currently leased or readily available for lease as space other than CSF, which is typically office and

other space.

- (g)

- Percent

leased is determined based on Office & Other space being billed to customers under signed leases as of March 31, 2014 divided by total

Office & Other space. Leases signed but not commenced as of March 2014 are not included.

- (h)

- Represents

infrastructure support space, including mechanical, telecommunications and utility rooms, as well as building common areas.

- (i)

- Represents

the NRSF at an operating facility that is currently leased or readily available for lease. This excludes existing vacant space held for

development.

- (j)

- Represents

space that is under roof that could be developed in the future for operating NRSF, rounded to the nearest 1,000.

- (k)

- UPS capacity (also referred to as critical load) represents the aggregate power available for lease and exclusive use by customers from the facility's installed universal power supplies (UPS) expressed in terms of megawatts. The capacity reported is for non-redundant megawatts, as we can develop flexible solutions to our customers at multiple resiliency levels. Does not sum to total due to rounding.

(square feet rounded to nearest 1,000; dollars in millions)

| |

|

NRSF Under Development(a) | |

Under Development Costs(b) | ||||||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

Facilities

|

Metro- politan Area |

Colocation Space (CSF) |

Office & Other |

Supporting Infrastructure |

Powered Shell(c) |

Total(d) | Estimated UPS MW Capacity(e) |

Actual to Date(f) |

Estimated Costs to Completion |

Total | ||||||||||||||||||||

W. Frankford Rd., |

Dallas |

60,000 |

8,000 |

28,000 |

— |

96,000 |

9.0 |

$ |

9 |

$ |

17 - 22 |

$ |

26 - 31 |

|||||||||||||||||

Westover Hills Blvd., |

San Antonio |

30,000 |

20,000 |

25,000 |

40,000 |

115,000 |

3.0 |

3 |

29 - 35 |

32 - 38 |

||||||||||||||||||||

Westway Park Blvd., |

Houston |

— |

— |

— |

320,000 |

320,000 |

— |

1 |

18 - 24 |

19 - 25 |

||||||||||||||||||||

South Ellis Street, |

Phoenix |

— |

— |

— |

— |

— |

5.0 |

3 |

1 - 3 |

4 - 6 |

||||||||||||||||||||

South Ellis Street, |

Phoenix |

— |

— |

— |

110,000 |

110,000 |

— |

— |

14 - 17 |

14 - 17 |

||||||||||||||||||||

Ridgetop Circle, |

Loudon |

30,000 |

5,000 |

30,000 |

50,000 |

115,000 |

6.0 |

— |

36 - 44 |

36 - 44 |

||||||||||||||||||||

Metropolis Dr., |

Austin |

5,000 |

— |

— |

— |

5,000 |

— |

— |

0.5 - 1.0 |

0.5 - 1.0 |

||||||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total |

125,000 |

33,000 |

83,000 |

520,000 |

761,000 |

23.0 |

$ |

16 |

$ |

115.5 - 146.0 |

$ |

131.5 - 162.0 |

||||||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

- (a)

- Represents

NRSF at a facility for which activities have commenced or are expected to commence in the next 2 quarters to prepare the space for its intended

use. Estimates and timing are subject to change. Does not include approximately 37,000 CSF or 41,000 CSF constructed in the first quarter 2014 at our Houston West 2 and Phoenix 1 facilities, which are

reflected in our operating properties table above.

- (b)

- Represents

management's estimate of the total costs required to complete the current NRSF under development. There may be an increase in costs if customers

require greater power density.

- (c)

- Represents NRSF under construction that, upon completion, will be powered shell available for future development into operating NRSF.

S-3

- (d)

- Represents

total NRSF under development. For new facilities, this represents incremental powered shell. For existing facilities, this represents the

conversion of existing powered shell into CSF, Office & Other space, and Supporting Infrastructure.

- (e)

- Represents

the aggregate power expected to be available for lease to and exclusive use by customers from the facility's installed universal power supplies

expressed in terms of megawatts. The capacity presented is for non-redundant megawatts, as we can develop flexible solutions to our customers at multiple resiliency levels.

- (f)

- Represents

the cash investment as of March 31, 2014. There may be accruals above this amount for work completed, for which cash has not yet been

paid.

- (g)

- Construction

expected to be completed in second quarter 2014.

- (h)

- Represents construction of a new facility.

Our Competitive Strengths

We believe the following competitive strengths distinguish us from other data center operators and will enable us to continue to grow our operations.

High Quality Customer Base. The high quality of our assets combined with our reputation for serving the needs of large enterprises has enabled us to focus on the Fortune 1000 to build a quality customer base. We currently have approximately 630 customers from a broad spectrum of industries, with a particular expertise serving the energy industry, which comprises 32% of our annualized rent as of March 31, 2014. We currently have nine of the Fortune 20 and 135 of the Fortune 1000 or private or foreign enterprises of equivalent size as customers. Our revenue is generated by a stable enterprise customer base, as evidenced by the following as of March 31, 2014:

- •

- 74% of our annualized rent comes from the Fortune 1000 or private or foreign enterprises of equivalent size.

- •

- 57% of our annualized rent comes from investment grade companies or their affiliates, based on the parent company's

corporate credit rating by Standard & Poor's Ratings Services.

- •

- 41% of our annualized rent comes from the Fortune 100 or private or foreign enterprises of equivalent size.

As of March 31, 2014, no single customer represented more than 7.5% of our annualized rent, and our top 10 customers represented 42% of our annualized rent.

Strategically Located Portfolio. Our portfolio is located in several domestic and international markets possessing attractive characteristics for enterprise-focused data center operations. We have domestic properties in five of the top 10 largest U.S. cities by population (Chicago, Dallas, Houston, Phoenix and San Antonio), according to the U.S. Census Bureau, and four of the top 10 cities for Fortune 500 headquarters (Chicago, Cincinnati, Dallas and Houston), according to Forbes. We believe cities with large populations or a large number of corporate headquarters are likely to produce incremental demand for IT infrastructure. In addition, we believe being located close to our current and potential customers provides chief information officers ("CIOs") with additional confidence when outsourcing their data center infrastructure to us.

Modern, High Quality Facilities. Our portfolio includes highly efficient, reliable facilities with flexibility to customize customer solutions and accessibility to hundreds of connectivity providers. To optimize the delivery of power, our properties include modern engineering technologies designed to minimize unnecessary power usage and, in our newest facilities, we are able to provide power utilization efficiency ratios we believe to be among the best in the multi-tenant data center industry. Fortune 1000 CIOs are dividing their application stacks into groups as some applications require 100% availability while others may require significant power to support complex computing or robust connectivity. Our construction design enables us to deliver different power densities and resiliencies to the same customer footprint, allowing customers to tailor solutions to meet their application needs. In

S-4

addition, the National IX Platform provides access to hundreds of telecommunication and Internet carriers.

Massively Modular® Construction Methods. Our Massively Modular® design principles allow us to efficiently stage construction on a large scale and deliver critical power and colocation square feet in a timeframe that we believe is one of the best in the industry. We acquire or build a large powered shell capable of scaling with our customers' power and colocation space needs. The powered shell can be acquired or constructed for a relatively inexpensive capital cost. Once the building shell is ready, we can build individual data center halls in portions of the building space to meet the needs of customers on a modular basis. This modular data center hall construction can be completed in less than 16 weeks to meet our customers' immediate needs. This short construction timeframe ensures a very high utilization of the assets and minimizes the time between our capital investment and the receipt of customer revenue, favorably impacting our return on investment while also translating into lower costs for our customers. Our design principles also allow us to add incremental equipment to increase power densities as our customers' power needs increase, which provides our customers with a significant amount of flexibility to manage their IT demands. We believe this Massively Modular® approach allows us to respond to rapidly evolving customer needs, to commit capital toward the highest return projects and to develop state-of-the-art data center facilities.

Significant Leasing Capability and Low Recurring Rent Churn. Our focus on the customer, our ability to scale with their needs, and our operational excellence provides us with two key benefits: embedded future growth from our customer base and low recurring rent churn. During 2013, our total annualized rent increased by approximately 22%, approximately 56% of which was provided by our existing customer base. Since December 31, 2012, we have increased our operational NRSF by approximately 343,000 square feet or 20%, while maintaining a high percentage of NRSF leased of 83% as of March 31, 2014.

Our management team focuses on minimizing recurring rent churn. We define recurring rent churn as any reduction in recurring rent due to customer terminations, net pricing reductions or service reductions as a percentage of the annualized rent at the beginning of the applicable period, excluding any impact from metered power reimbursements. For 2013, our recurring rent churn was 4.1%. For 2012 and 2011, our recurring rent churn was 4.6% and 3.0%, respectively.

Significant, Attractive Expansion Opportunities. As of March 31, 2014, we had 569,000 NRSF of powered shell available for future development and approximately 200 acres of land that were available for future data center facility development. Our current development properties and available acreage were selected based on extensive site selection criteria and the collective industry knowledge and experience of our management team with a focus on markets with a strong presence of and high demand by Fortune 1000 companies. As a result, we believe that our development portfolio contains properties that are located in markets with attractive supply and demand conditions and that possess suitable physical characteristics to support data center infrastructure.

Differentiated Reputation for Service. We believe that the decision CIOs make to outsource their data center infrastructure has material implications for their businesses, and, as such, CIOs look to third-party data center providers that have a reputation for serving similar organizations and that are able to deliver a customized solution. We take a consultative approach to understanding the unique requirements of our customers, and our design principles allow us to deliver a customized data center solution to match their needs. We believe that this approach has helped fuel our growth. Our current customers are also often the source of new contracts, with referrals being an important source of new customers.

S-5

Business and Growth Strategies

Our objective is to grow our revenue and earnings and maximize stockholder returns by continuing to expand our data center infrastructure outsourcing business.

Increasing Revenue from Existing Customers and Properties. We have historically generated a significant portion of our revenue growth from our existing customers. During 2013, our total annualized rent increased by approximately 22%, approximately 56% of which was provided by our existing customer base. We will continue to target our existing customers because we believe that many have significant data center infrastructure needs that have not yet been outsourced, and many will require additional data center space and power to support their growth and their increasing reliance on technology infrastructure in their operations. As of March 31, 2014, we had approximately 359,000 NRSF available to address new demand. We also have approximately 761,000 NRSF under development, as well as 569,000 NRSF of additional powered shell space under roof available for development. In addition, we have approximately 200 acres of land that are available for future data center shell development.

Attracting and Retaining New Customers. Increasingly, enterprises are beginning to recognize the complexities of managing data center infrastructure in the midst of rapid technological development and innovation. We believe that these complexities, brought about by the rapidly increasing levels of Internet traffic and data, obsolete existing corporate data center infrastructure, increased power and cooling requirements and increased regulatory requirements, are driving the need for companies to outsource their data center facility requirements. Consequently, this will significantly increase the percentage of companies that use third-party data center colocation services over the next several years. We believe that our high quality assets and reputation for serving large enterprises have been, and will be, key differentiators for us in attracting customers that are outsourcing their data center infrastructure needs.

We acquire customers through a variety of channels. We have historically managed our sales process through a direct-to-the-customer model, with average revenue production per sales employee increasing by approximately 45% in 2013. We are now also utilizing third-party leasing agents and indirect leasing channels to expand our universe of potential new customers. Our indirect leasing channels include value added resellers, systems integrators and hosting providers. These channels, in combination with our award-winning internal marketing team, have enabled us to build both a strong brand and outreach program to new customers. Throughout the life cycle of a customer's lease with us, we maintain a disciplined approach to monitoring their experience, with the goal of providing the highest level of customer service. This personal attention fosters a strong relationship and trust with our customers, which leads to future growth, leasing renewals and low recurring rent churn.

We also recently announced the launch of a new product line, CyrusOne Solutions, which was created in response to the growing customer demand for large-scale and innovative build-to-suit deployments. CyrusOne Solutions is a custom option for companies needing expert help with facilities that can house their mission-critical IT assets. It offers customers the flexibility to engineer larger-scale data center solutions at a range of power densities and resiliency levels with robust connectivity options and various cooling system alternatives to meet their specific business requirements.

Growing Interconnection Business. In April 2013, we launched the National IX Platform, delivering interconnection across states and between metro-enabled sites within the CyrusOne facility footprint and beyond. The platform enables high-performance, low-cost data transfer and accessibility for customers seeking to connect between CyrusOne facilities, from CyrusOne to their own private data center facility, or with one another via private peering, cross connects and/or public switching environments. Interconnection within a facility or on the National IX Platform allows our customers to share information and conduct commerce in a highly efficient manner not requiring a third-party

S-6

intermediary, and at a fraction of the cost normally required to establish such a connection between two enterprises. As of March 31, 2014, approximately 60% of our annualized rent came from customers with footprints in multiple CyrusOne data centers, and the National IX Platform provides an easy and low-cost method for these customers to connect between facilities. The demand for interconnection creates additional rental and revenue growth opportunities for us, and we believe that customer interconnections increase our likelihood of customer retention by providing an environment not easily replicated by competitors. We act as a trusted neutral party that enterprises, carriers and content companies utilize to connect to each other. We believe that the reputation and industry relationships of our executive management team place us in an ongoing trusted provider role. In 2014, we became the first colocation provider in North America to receive multi-site certification from the Open-IX Association, a non-profit industry group formed to promote better standards for data center interconnection and Internet Exchanges in North America. The six CyrusOne facilities receiving data center certification are located in the Dallas, Houston, Austin, Cincinnati and Phoenix markets.

Expanding into New Markets. Our expansion strategy focuses on developing new data centers in markets where our customers are located and in markets with a strong presence of and high demand by Fortune 1000 customers. We conduct extensive analysis to ensure an identified market displays strong data center fundamentals, independent of the demand presented by any particular customer. In addition, we consider markets where our existing customers want us to be located. We regularly meet with our customers to understand their business strategies and potential data center needs. Our strategy of broadening our geographic footprint and expanding into markets with a strong presence of and high demand by Fortune 1000 customers is what led us to our recent expansion into the Northern Virginia market. We believe that this approach combined with our Massively Modular® construction design reduces the risk associated with expansion into new markets because it provides strong visibility into our leasing opportunities and helps to ensure targeted returns on new developments. When considering a new market, we take a disciplined approach in evaluating potential business, property and site acquisitions, including a site's geographic attributes, availability of telecommunications and connectivity providers, access to power, and expected costs for development.

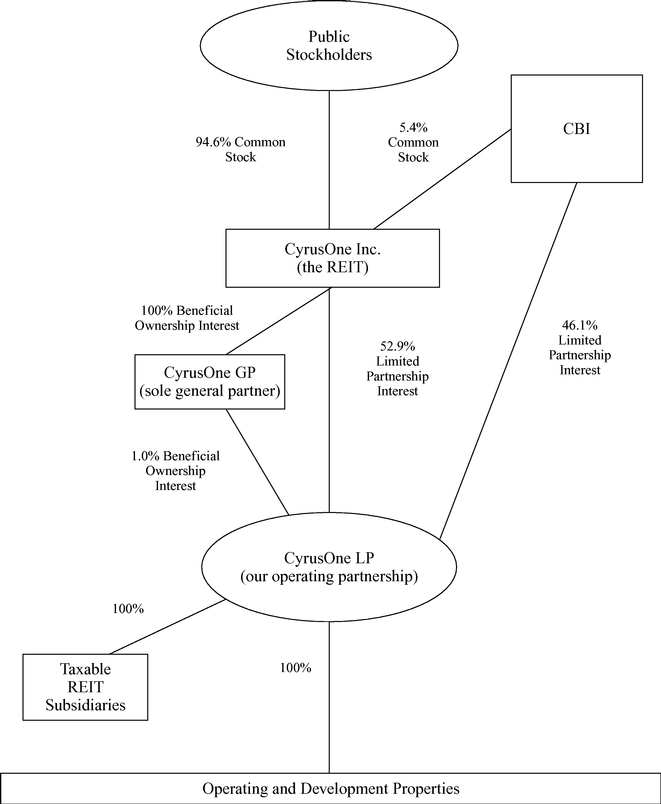

Our Structure

The proceeds of this offering are being used by us to acquire 12,500,000 CyrusOne LP operating partnership units (or 14,375,000 operating partnership units if the underwriters exercise their option to purchase additional shares of our common stock in full, assuming one operating partnership unit will be purchased for every share of common stock issued by us in this offering) from a subsidiary of CBI (the "CBI Repurchase").

S-7

The following diagram depicts our ownership structure as of May 31, 2014, after giving effect to this offering and the use of proceeds therefrom to effect the CBI Repurchase (assuming no exercise by the underwriters of their option to purchase additional shares of our common stock):

S-8

Tax Status

We intend to continue to operate in a manner that will allow us to qualify as a REIT commencing with our taxable year ended December 31, 2013, and we will make our REIT election upon filing our 2013 U.S. federal income tax return. We are required, among other things, to distribute at least 90% of our REIT taxable income, determined without regard to the dividends paid deduction and excluding any net capital gains, to our stockholders on an annual basis in order to qualify for taxation as a REIT for U.S. federal income tax purposes. As a REIT, we are generally not subject to corporate level U.S. federal income tax on the earnings distributed currently to our stockholders. If we fail to qualify as a REIT in any taxable year and do not qualify for certain statutory relief provisions, we would be subject to U.S. federal income tax at regular corporate rates and would be precluded from re-electing to be taxed as a REIT for the subsequent four taxable years following the year during which we lost our REIT qualification. Even if we qualify for taxation as a REIT, we may be subject to certain U.S. federal, state and local taxes on our income or property, and the income of our taxable REIT subsidiaries will be subject to taxation at regular corporate rates.

Restrictions on Ownership and Transfer of Our Stock

Due to limitations on the concentration of ownership of REIT stock imposed by the Code, among other purposes, our charter provides for restrictions on ownership and transfer of our shares of stock, including, in general, prohibitions on any person actually or constructively owning more than 9.8% in value or number (whichever is more restrictive) of the outstanding shares of our common stock or 9.8% in value of the outstanding shares of all classes or series of our stock. Our charter, however, permits exceptions to be made for stockholders provided that our board of directors determines such exceptions will not jeopardize our tax status as a REIT. Our board of directors has granted CBI exemptions from the ownership limits applicable to other holders of our common stock, subject to certain initial and ongoing conditions designed to protect our status as a REIT, including the receipt of an IRS private letter ruling or an opinion of counsel from a nationally recognized law firm that the exercise of any such exemption should not cause any rent payable by CBI to jeopardize our REIT status.

Corporate Information

Our principal executive offices are located at 1649 West Frankford Road, Carrollton, TX 75007. Our telephone number is (972) 350-0060.

S-9

The following summary contains basic information about this offering. It does not contain all the information that is important to you. You should read this prospectus supplement, the accompanying prospectus and the documents incorporated by reference carefully before making an investment decision.

Issuer |

CyrusOne Inc. | |

Common stock offered by us |

12,500,000 shares |

|

Common stock to be outstanding after this offering |

35,177,498 shares(1) |

|

Common stock and operating partnership units to be outstanding after this offering |

65,264,333 shares/operating partnership units(2) |

|

Use of Proceeds |

We expect the net proceeds to us from the sale of common stock in this offering, after deducting estimated underwriting discounts, will be approximately $ million (or approximately $ million if the underwriters exercise their option to purchase additional shares of common stock in full). |

|

|

We intend to use the net proceeds from this offering, after deducting estimated underwriting discounts, but before estimated offering expenses payable by us, to acquire 12,500,000 operating partnership units (or 14,375,000 operating partnership units if the underwriters exercise their option to purchase additional shares of our common stock in full, assuming one operating partnership unit will be purchased for every share of common stock issued by us in this offering) from a subsidiary of CBI. |

|

NASDAQ Symbol |

CONE |

|

Risk Factors |

See "Risk Factors" and all other information included or incorporated by reference into this prospectus supplement and the accompanying prospectus (including the "Risk Factors" under Item 1A of our Annual Report on Form 10-K for the fiscal year ended December 31, 2013, incorporated by reference herein) for a discussion of the factors you should carefully consider before deciding to invest in our common stock. |

- (1)

- Excludes

1,875,000 shares issuable upon exercise of the underwriters' option to purchase additional shares and 2,015,818 shares reserved for

issuance under our 2012 Long Term Incentive Plan.

- (2)

- Includes 30,086,835 operating partnership units outstanding pursuant to the consummation of the transactions relating to our formation in 2012 and initial public offering in 2013 that may, subject to the limits in the partnership agreement of our operating partnership, be exchanged for cash or, at our option, shares of our common stock on a one-for-one basis and excludes operating partnership units held by us and our subsidiaries.

S-10

The following tables set forth summary financial information on a consolidated and combined historical basis. The financial information for the periods prior to our initial public offering on January 24, 2013 are deemed to be the financial information of the "Predecessor" and for the periods subsequent to January 24, 2013 are deemed to be the financial information of the "Successor" company. CyrusOne Inc. was formed on July 31, 2012, and prior to our initial public offering, we had minimal activity, consisting solely of deferred offering costs. The financial information of the "Predecessor" reflect the historical financial position, results of operations and cash flows of the data center activities and holdings of CBI for all periods presented. The Predecessor's historical information has been prepared on a "carve-out" basis from CBI's consolidated financial statements using the historical results of operations, cash flows, assets and liabilities attributable to the data center business and include allocations of income, expenses, assets and liabilities from CBI. These allocations reflect significant assumptions and do not fully reflect what the Predecessor's financial position, results of operations and cash flows would have been had the Predecessor been a stand-alone company during the periods presented. As a result, historical financial information is not necessarily indicative of our future results of operations, financial position and cash flows.

The financial information presented below as of December 31, 2013 and 2012, and for the period ended January 23, 2013 (January 1, 2013 to January 23, 2013), and period ended December 31, 2013 (January 24, 2013 to December 31, 2013) and each of the years ended December 31, 2012 and 2011 has been derived from our audited consolidated and combined financial statements included in our Annual Report on Form 10-K for the fiscal year ended December 31, 2013, which is incorporated by reference into this prospectus supplement. The financial information as of December 31, 2011 has been derived from the Predecessor's combined financial statements, which have not been incorporated by reference into this prospectus supplement.

The financial information presented below as of March 31, 2014 and for the three months ended March 31, 2014, and the periods ended March 31, 2013 (January 24, 2013 to March 31, 2013) and January 23, 2013 (January 1, 2013 to January 23, 2013) has been derived from the unaudited condensed consolidated and combined financial statements included in our Quarterly Report on Form 10-Q for the quarterly period ended March 31, 2014, which is incorporated by reference into this prospectus supplement. The unaudited condensed consolidated and combined financial statements contain all normal recurring adjustments necessary, in the opinion of management, to summarize the financial position and results for the periods presented. The historical operating results of our company for the three months ended March 31, 2014 are not necessarily indicative of the results that may be expected for the full year.

You should read the following summary financial information in conjunction with our audited and unaudited condensed consolidated financial statements and the related notes and "Management's Discussion and Analysis of Financial Condition and Results of Operations" contained in our Annual Report on Form 10-K for the fiscal year ended December 31, 2013, and our Quarterly Report on Form 10-Q for the quarterly period ended March 31, 2014, which are incorporated by reference into this prospectus supplement.

S-11

| |

Successor | Predecessor | Successor | Predecessor | ||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Three Months Ended March 31, 2014 |

|

|

|

|

Year Ended December 31, |

||||||||||||||||

| |

January 24, 2013 to March 31, 2013 |

January 1, 2013 to January 23, 2013 |

January 24, 2013 to December 31, 2013 |

January 1, 2013 to January 23, 2013 |

||||||||||||||||||

| (Dollars in millions) |

2012 | 2011 | ||||||||||||||||||||

Statement of Operations Data: |

||||||||||||||||||||||

Revenue |

$ | 77.5 | $ | 45.0 | $ | 15.1 | $ | 248.4 | $ | 15.1 | $ | 220.8 | $ | 181.7 | ||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Costs and expenses: |

||||||||||||||||||||||

Property operating expenses |

27.7 | 15.3 | 4.8 | 88.4 | 4.8 | 76.0 | 58.2 | |||||||||||||||

Sales and marketing |

3.0 | 2.1 | 0.7 | 9.9 | 0.7 | 9.7 | 9.1 | |||||||||||||||

General and administrative |

7.3 | 5.4 | 1.5 | 26.5 | 1.5 | 20.7 | 12.5 | |||||||||||||||

Depreciation and amortization |

27.6 | 16.4 | 5.3 | 89.9 | 5.3 | 73.4 | 55.5 | |||||||||||||||

Restructuring costs(a) |

— | — | — | 0.7 | — | — | — | |||||||||||||||

Transaction costs(b) |

0.1 | — | 0.1 | 1.3 | 0.1 | 5.7 | 2.6 | |||||||||||||||

Transaction-related compensation |

— | — | 20.0 | — | 20.0 | — | — | |||||||||||||||

Management fees charged by CBI(c) |

— | — | — | — | — | 2.5 | 2.3 | |||||||||||||||

Loss on sale of receivables to affiliate(d) |

— | — | — | — | — | 3.2 | 3.5 | |||||||||||||||

Asset impairments(e) |

— | — | — | 2.8 | — | 13.3 | — | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Operating (loss) income |

11.8 | 5.8 | (17.3 | ) | 28.9 | (17.3 | ) | 16.3 | 38.0 | |||||||||||||

Interest expense |

10.7 | 8.4 | 2.5 | 41.2 | 2.5 | 41.8 | 32.9 | |||||||||||||||

Other income |

— | — | — | (0.1 | ) | — | — | — | ||||||||||||||

Loss on extinguishment of debt(f) |

— | — | — | 1.3 | — | — | 1.4 | |||||||||||||||

Income tax (expense) benefit |

(0.4 | ) | (0.2 | ) | (0.4 | ) | (1.9 | ) | (0.4 | ) | 5.1 | (2.2 | ) | |||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

(Loss) income from continuing operations |

0.7 | (2.8 | ) | (20.2 | ) | (15.4 | ) | (20.2 | ) | (20.4 | ) | 1.5 | ||||||||||

(Loss) gain on sale of real estate improvements(g) |

— | — | — | (0.2 | ) | — | 0.1 | — | ||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) income from continuing operations |

$ | 0.7 | $ | (2.8 | ) | $ | (20.2 | ) | $ | (15.6 | ) | $ | (20.2 | ) | $ | (20.3 | ) | $ | 1.5 | |||

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

Noncontrolling interest in net income (loss) |

0.5 | (1.9 | ) | — | 10.3 | — | — | — | ||||||||||||||

Net income (loss) attributed to common shareholders |

$ | 0.2 | $ | (0.9 | ) | — | $ | (5.3 | ) | — | — | — | ||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

Per share data: |

||||||||||||||||||||||

Basic weighted average common shares outstanding |

20.9 | 20.9 | — | 20.9 | — | — | — | |||||||||||||||

Diluted weighted average common shares outstanding |

20.9 | 20.9 | — | 20.9 | — | — | — | |||||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

Basic and diluted loss per common share |

— | (0.05 | ) | — | (0.28 | ) | — | — | — | |||||||||||||

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | |

Dividends declared per share |

$ | 0.21 | $ | 0.16 | — | $ | 0.64 | — | — | — | ||||||||||||

S-12

| |

|

|

Predecessor | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Successor | ||||||||||||

| |

As of December 31, | ||||||||||||

| |

As of March 31, 2014 |

As of December 31, 2013 |

|||||||||||

| (Dollars in millions) |

2012 | 2011 | |||||||||||

Balance Sheet Data (at period end): |

|||||||||||||

Investment in real estate, net |

$ | 924.8 | $ | 883.8 | $ | 706.9 | $ | 529.0 | |||||

Total assets |

1,528.1 | 1,506.8 | 1,210.9 | 954.7 | |||||||||

Debt(h) |

540.5 | 541.7 | 557.2 | 523.1 | |||||||||

Other financing arrangements(i) |

56.4 | 56.3 | 60.8 | 48.2 | |||||||||

CBI's net investment(j) |

$ | 447.2 | $ | 455.6 | $ | 500.1 | $ | 311.5 | |||||

| |

Three Months Ended March 31, |

Year Ended December 31, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Successor | Successor | Predecessor | |||||||||||||

| (Dollars in millions) |

2014 | 2013(k) | 2013(l) | 2012 | 2011 | |||||||||||

Other Financial Data: |

||||||||||||||||

Utilization Rate(m) |

89 | % | 81 | % | 85 | % | 78 | % | 88 | % | ||||||

Funds from operations(n) |

$ | 27.1 | $ | (2.9 | ) | $ | 54.6 | $ | 61.7 | $ | 54.2 | |||||

Funds from operations (excluding specified items)(n) |

27.2 | 17.2 | 78.7 | 67.4 | 56.8 | |||||||||||

EBITDA(o) |

39.4 | 10.2 | 105.4 | 89.8 | 92.1 | |||||||||||

Adjusted EBITDA(o) |

41.7 | 31.5 | 138.7 | 115.3 | 99.6 | |||||||||||

Capital expenditures |

$ | 49.7 | $ | 52.6 | $ | 228.6 | $ | 228.3 | $ | 117.5 | ||||||

- (a)

- Represents

a restructuring charge recognized in 2013 as a result of moving certain administrative functions to the Company's corporate office.

- (b)

- Represents

legal, accounting and consulting fees incurred in connection with the transactions relating to our formation in 2012 and initial public offering

in 2013, our qualification as a REIT and completed and potential business combinations.

- (c)

- Represents

management fees charged by CBI for services it provided to the Predecessor, including executive management, legal, treasury, human resources,

accounting, tax, internal audit and IT services. See Note 17 to our audited combined financial statements included in our Annual Report on Form 10-K for the fiscal year ended

December 31, 2013, which is incorporated by reference into this prospectus supplement.

- (d)

- Represents

the sale by the Predecessor of most of its trade and other accounts receivable to Cincinnati Bell Funding LLC, a bankruptcy-remote subsidiary of

CBI, at a 2.5% discount to the receivables' face value. Effective October 1, 2012, we terminated our participation in this program.

- (e)

- Represents

asset impairments recognized on real estate related equipment in 2013 and on a customer relationship intangible and property and equipment

primarily related to our GramTel Inc. acquisition in 2012.

- (f)

- Represents

losses attributable to the termination of financing obligations for two of our facilities when we purchased them from their former lessors during

the respective periods.

- (g)

- Represents

the (gain) loss that was recognized on the sale of chillers and generators in connection with upgrading of the equipment at various data center

facilities.

- (h)

- As

of March 31, 2014, and December 31, 2013 and 2012, debt consisted of our $525 million senior notes due 2022 and capital lease

obligations. For prior periods, debt reflects related party note payable and capital lease obligations.

- (i)

- Represents

leases of real estate where we were involved in the construction of structural improvements to develop buildings into data centers. When we bear

substantially all the construction period risk, such as managing or funding construction, we are deemed to be the accounting owner of the leased property. These transactions generally do not qualify

for sale-leaseback accounting due to our continued involvement in these data center operations. For these transactions, at the lease inception date, we recognize the fair value of the leased building

as an asset in investment in real estate and as a liability in other financing arrangements.

- (j)

- Represents CBI's net investment in CyrusOne Inc., CyrusOne GP, CyrusOne LP and its subsidiaries. Prior to November 20, 2012, these entities were not separate legal entities.

S-13

- (k)

- Represents

the combined results of the Predecessor for the period January 1, 2013 to January 23, 2013 and the Successor for the period

January 24, 2013 to March 31, 2013.

- (l)

- Represents

the combined results of the Predecessor for the period January 1, 2013 to January 23, 2013 and the Successor for the period

January 24, 2013 to December 31, 2013.

- (m)

- We

calculate utilization rate by dividing CSF under signed leases for available space (whether or not the contract has commenced billing) by total CSF.

Utilization rate differs from percent leased presented elsewhere in this prospectus supplement because utilization rate excludes office space and supporting infrastructure net rentable square footage

and includes CSF for signed leases that have not commenced billing. Management uses utilization rate as a measure of CSF leased.

- (n)

- We

calculate funds from operations ("FFO") as net income (loss) computed in accordance with U.S. GAAP before real estate depreciation and

amortization, amortization of customer relationship intangibles, real estate impairments, customer relationship intangible impairments and (gain) loss on sale of real estate improvements. Because the

value of the customer relationship intangibles is inextricably connected to the real estate acquired, we believe the amortization and impairments of such intangibles is analogous to real estate

depreciation and impairments; therefore, we add the customer relationship intangible amortization and impairments back for similar treatment with real estate depreciation and impairments. Our customer

relationship intangibles are primarily associated with the acquisition of Cyrus Networks, LLC in 2010 and, at the time of acquisition, represented 22% of the value of the assets acquired.

- We

calculate funds from operations (excluding specified items) ("FFO (excluding specified items)") as FFO plus transaction-related compensation,

(gain) loss on extinguishment of debt, restructuring charges, legal claim costs and transaction costs.

- Management

uses FFO and FFO (excluding specified items) as supplemental performance measures because they provide performance measures that,

when compared year over year, capture trends in occupancy rates, rental rates and operating costs. We also believe that, as widely recognized measures of the performance of REITs, these measures will

be used by investors as a basis to compare our operating performance with that of other REITs.

- However, because FFO and FFO (excluding specified items) exclude real estate depreciation and amortization, amortization of customer relationship intangibles, real estate impairments and customer relationship intangible impairments, and capture neither the changes in the value of our properties that result from use or from market conditions, nor the level of capital expenditures and leasing commissions necessary to maintain the operating performance of our properties, all of which have real economic effect and could materially impact our results from operations, the utility of FFO and FFO (excluding specified items) as measures of our performance is limited. Other REITs may not calculate FFO and FFO (excluding specified items) in the same manner. Accordingly, our FFO and FFO (excluding specified items) may not be comparable to others. Therefore, FFO and FFO (excluding specified items) should be considered only as supplements to net income as measures of our performance. FFO and FFO (excluding specified items) should not be used as measures of our liquidity or as indicative of funds available to fund our cash needs, including our ability to make distributions. FFO and FFO (excluding specified items) also should not be used as supplements to or substitutes for cash flow from operating activities computed in accordance with U.S. GAAP.

S-14

- A reconciliation of net income (loss) to FFO and FFO (excluding specified items) is presented below:

| |

Three Months Ended March 31, |

Year Ended December 31, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

Successor | Successor | Predecessor | |||||||||||||

| (Dollars in millions) |

2014 | 2013(k) | 2013(l) | 2012 | 2011 | |||||||||||

Net income (loss) |

$ | 0.7 | $ | (23.0 | ) | $ | (35.8 | ) | $ | (20.3 | ) | $ | 1.5 | |||

| | | | | | | | | | | | | | | | | |

Real estate depreciation and amortization |

22.2 | 15.9 | 70.6 | 52.9 | 37.7 | |||||||||||

Amortization of customer relationship intangibles |

4.2 | 4.2 | 16.8 | 16.0 | 15.0 | |||||||||||

Real estate impairments |

— | — | 2.8 | 11.7 | — | |||||||||||

Customer relationship intangible impairments |

— | — | — | 1.5 | — | |||||||||||

(Gain) loss on sale of real estate improvements |

— | — | 0.2 | (0.1 | ) | — | ||||||||||

| | | | | | | | | | | | | | | | | |

FFO |

27.1 | (2.9 | ) | 54.6 | 61.7 | 54.2 | ||||||||||

| | | | | | | | | | | | | | | | | |

Transaction-related compensation |

— | 20.0 | 20.0 | — | — | |||||||||||

Loss on extinguishment of debt |

— | — | 1.3 | — | 1.4 | |||||||||||

Restructuring charges |

— | — | 0.7 | — | — | |||||||||||

Legal claim costs |

— | — | 0.7 | — | — | |||||||||||

Transaction costs |

0.1 | 0.1 | 1.4 | 5.7 | 2.6 | |||||||||||

| | | | | | | | | | | | | | | | | |

FFO (excluding specified items) |

$ | 27.2 | $ | 17.2 | $ | 78.7 | $ | 67.4 | $ | 58.2 | ||||||

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

- (o)

- We