Exhibit 10.1

AGREEMENT OF LEASE

EMPIRE STATE BUILDING COMPANY L.L.C., Landlord

and

SHUTTERSTOCK, INC., Tenant

|

Premises: |

Portion of the 20th Floor and |

|

|

|

Entire 21st Floor |

|

|

|

Empire State Building |

|

|

|

350 Fifth Avenue |

|

|

|

New York, New York 10118 |

|

|

|

|

|

|

|

|

|

|

Date: |

As of March , 2013 |

|

TABLE OF CONTENTS

|

Article |

|

|

Page | |

|

|

1. |

COMMENCEMENT DATE; TERM; PURPOSE; ETC. |

1 | |

|

|

2. |

RENT |

4 | |

|

|

3. |

ELECTRICITY |

14 | |

|

|

4. |

ASSIGNMENT AND SUBLETTING |

19 | |

|

|

5. |

DEFAULT |

24 | |

|

|

6. |

RE-LETTING; ETC. |

25 | |

|

|

7. |

LANDLORD MAY CURE DEFAULTS |

27 | |

|

|

8. |

ALTERATIONS |

27 | |

|

|

9. |

LIENS |

30 | |

|

|

10. |

REPAIRS; DESTRUCTION |

30 | |

|

|

11. |

END OF TERM |

31 | |

|

|

12. |

SUBORDINATION AND ESTOPPEL; ETC. |

32 | |

|

|

13. |

CONDEMNATION |

34 | |

|

|

14. |

REQUIREMENTS OF LAW |

35 | |

|

|

15. |

CERTIFICATE OF OCCUPANCY |

36 | |

|

|

16. |

POSSESSION |

36 | |

|

|

17. |

QUIET ENJOYMENT |

36 | |

|

|

18. |

RIGHT OF ENTRY |

37 | |

|

|

19. |

INTENTIONALLY OMITTED |

37 | |

|

|

20. |

INDEMNITY |

37 | |

|

|

21. |

LANDLORD’S LIABILITY |

38 | |

|

|

22. |

CONDITION OF DEMISED PREMISES; BUILDING WORK; TENANT’S INITIAL INSTALLATION; ETC. |

40 | |

|

|

23. |

JURY WAIVER; DAMAGES |

45 | |

|

|

24. |

NO WAIVER; CONSTRUCTIVE EVICTION; SURVIVAL OF OBLIGATIONS; ETC. |

45 | |

|

|

25. |

OCCUPANCY AND USE BY TENANT; SIGNAGE; ETC. |

46 | |

|

|

26. |

NOTICES |

48 | |

|

|

27. |

WATER |

49 | |

|

|

28. |

SPRINKLER SYSTEM |

49 | |

|

|

29. |

SERVICES; HEAT; AIR CONDITIONING; ETC. |

49 | |

|

|

30. |

SECURITY DEPOSIT |

51 | |

|

|

31. |

RENT CONTROL |

53 | |

|

|

32. |

SHORING |

54 | |

|

|

33. |

EFFECT OF CONVEYANCE; ETC. |

54 | |

|

|

34. |

RIGHTS OF SUCCESSORS AND ASSIGNS; PARTIAL INVALIDITY |

54 | |

|

|

35. |

CAPTIONS |

54 | |

|

|

36. |

LEASE SUBMISSION |

54 | |

|

|

37. |

ELEVATORS AND LOADING |

54 | |

|

|

38. |

BROKERAGE |

55 | |

|

|

39. |

ARBITRATION |

55 | |

|

|

40. |

INSURANCE |

55 | |

|

|

41. |

TWENTY-FIRST FLOOR SETBACK |

57 | |

|

|

42. |

LATE CHARGES |

58 | |

|

|

43. |

ENVIRONMENTAL COMPLIANCE |

58 | |

|

|

44. |

LEASE FULLY NEGOTIATED |

60 | |

|

|

45. |

SMOKING RESTRICTIONS |

60 | |

|

|

46. |

ANTI-TERRORISM REQUIREMENTS |

60 | |

|

|

47. |

CONDOMINIUM PROVISIONS |

61 | |

|

|

48. |

ADDITIONAL DEFINITIONS |

62 | |

|

|

49. |

USE OF BUILDING NAME AND IMAGE |

63 | |

|

|

50. |

APPLICABLE LAW |

63 | |

|

|

51. |

COUNTERPARTS |

63 | |

|

|

52. |

CONFIDENTIALITY |

63 | |

|

|

53. |

EMERGENCY GENERATOR |

64 | |

|

|

54. |

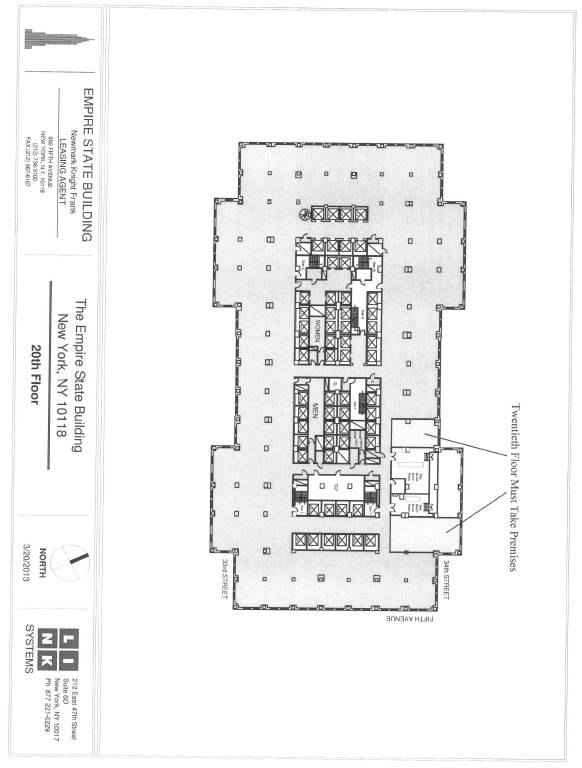

TWENTIETH FLOOR MUST TAKE PREMISES |

64 | |

|

|

56. |

OBSERVATORY PASS |

69 | |

|

|

57. |

TWENTY-SECOND FLOOR; RIGHT OF FIRST OFFER; ETC. |

69 | |

|

|

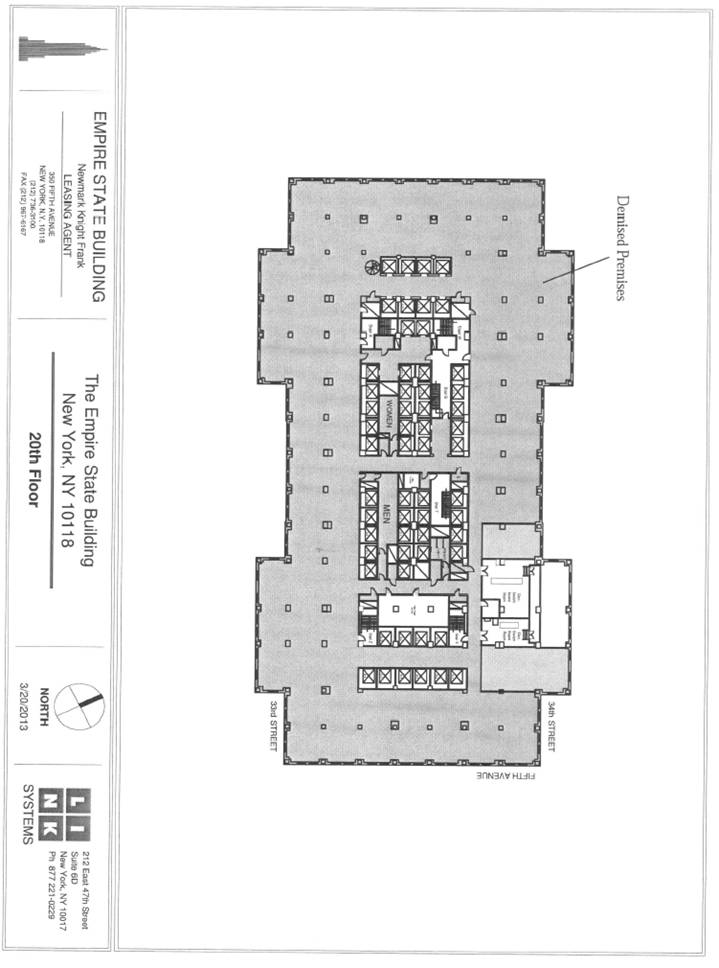

EXHIBIT A - Diagram of Demised Premises | |||

|

|

EXHIBIT B - Cleaning Schedule | |||

|

|

EXHIBIT C-1 Subordination, Non-Disturbance Agreement with Empire State Building Associates L.L.C. | |||

|

|

EXHIBIT C-2 Non-Disturbance Agreement with Empire State Building Land Associates L.L.C. | |||

|

|

EXHIBIT D - Entrance Door and Entrance Door Signage Specifications | |||

|

|

EXHIBIT E - Letter of Credit | |||

|

|

EXHIBIT F - Building Standard Energy Efficiency Guidelines | |||

|

|

EXHIBIT G - Diagram of Twentieth Floor Must Take Premises | |||

|

|

EXHIBIT H - Heat and Air-Conditioning Specifications | |||

|

|

EXHIBIT I - Critical Path Schedule for Building Work |

|

|

EXHIBIT J - Elevator Modernization Schedule for C Bank Elevators |

|

|

SCHEDULE A - Rules and Regulation |

LEASE (“Lease” or “lease”) made as of this day of March, 2013, between EMPIRE STATE BUILDING COMPANY L.L.C., a New York limited liability company, with an address at 350 Fifth Avenue, New York, New York 10118, hereinafter referred to as “Landlord” and SHUTTER STOCK, INC., a Delaware corporation with an address at 60 Broad Street, 30th Floor, New York, New York 10004, hereinafter referred to as “Tenant”.

WITNESSETH:

Landlord hereby leases to Tenant and Tenant hereby hires from Landlord certain premises consisting of a portion of the 20th floor (the “20th Floor Portion”) and the entire rentable area of the 21st floor (the “21st Floor Portion”), as more particularly depicted on Exhibit A (which is not necessarily to scale) annexed hereto and made part hereof (said premises are hereinafter collectively referred to as the “Demised Premises” or the “demised premises”), in the building known as the Empire State Building, located at 350 Fifth Avenue, New York, New York 10118 (hereinafter referred to as the “Building”), in the County, City and State of New York, for a term years, to commence on the Commencement Date (as such term is defined in Article 1A of this Lease), and to expire on the date (the “Expiration Date”) which is the last day of the eleventh Lease Year (as such term is defined in Article 1E of this Lease), both dates inclusive, upon the terms and conditions hereinafter provided. For all purposes under this Lease, the parties agree that the rentable square foot area of the Demised Premises shall be deemed to be 77,845rentable square feet, irrespective of any disparity between (i) such figure and any actual measurement of such area or (ii) the usable area thereof.

Landlord and Tenant further covenant and agree as follows:

1. COMMENCEMENT DATE; TERM; PURPOSE; ETC.

A. (i) The term of this Lease with respect to the 20th Floor Portion shall commence on the date (the “20th Floor Commencement Date”) which shall be first to occur of the following dates:

(a) the date which shall be the later to occur of (1) the date that Landlord makes vacant possession of the 20th Floor Portion available to Tenant with the Building Work (as such term is defined in Article 22B of this Lease) which is applicable to such space substantially completed (the “20th Floor Substantial Completion Date”), or (2) August 1, 2013; or

(b) the date that Tenant takes possession of the 20th Floor Portion or any portion thereof for the purpose of performing Tenant’s Initial Installation.

Landlord shall use commercially reasonable efforts to keep Tenant apprised of the anticipated 20th Floor Substantial Completion Date, as well as any possible changes to such date due to conditions relating to the performance of such work therein.

(ii) Notwithstanding anything contained herein to the contrary, if Landlord shall fail to cause the 20th Floor Substantial Completion Date to occur on or before the date that is one hundred eighty (180) days after the date that this Lease is executed and delivered by Landlord and Tenant (the “20th Floor First Outside Date”), then Tenant shall be entitled to a rent credit in the amount of $5,529.13 per day for each day after the 20th Floor First Outside Date that the 20th Floor Substantial Completion Date shall not occur; provided, however, that if Landlord shall fail to cause 20th Floor Substantial completion Date to occur on or before the date that is two hundred forty (240) days after the date that this Lease is executed and delivered by Landlord and Tenant (the “20th Floor Second Outside Date”), then the amount of such rent credit shall be increased to $11,058.26 per day for each day after the 20th Floor Second Outside Date that the 20th Floor Substantial Completion Date shall not occur. Such rent credit shall be applied, until fully exhausted, against the first fixed annual rent due under this Lease with respect to the 20th Floor Portion from and after the full application of the rent credit set forth in Article 2B(iii) of this Lease. Notwithstanding the foregoing, the 20th Floor First Outside Date and the 20th Floor Second Outside Date shall each be extended by one day for each day that the completion of the Building Work which is applicable to such space is delayed due to any of the causes set forth in Article 21A of this Lease or due to any act or omission of Tenant, its agents, employees or contractors.

(iii) The term of this Lease with respect to the 21st Floor Portion shall commence on the date (the “21st Floor Commencement Date”) which shall be first to occur of the following dates:

(a) the date which shall be the later to occur of (1) the date that Landlord makes vacant possession of the 21st Floor Portion available to Tenant with the Building Work which is applicable to such space substantially completed (the “21st Floor Substantial Completion Date”), or (2) August 1, 2013; or

(b) the date that Tenant takes possession of the 21st Floor Portion or any portion thereof for the purpose of performing Tenant’s Initial Installation therein.

Landlord shall use commercially reasonable efforts to keep Tenant apprised of the anticipated 21st Floor Substantial Completion Date, as well as any possible changes to such date due to conditions relating to the performance of such work.

(iv) Notwithstanding anything contained herein to the contrary, if Landlord shall fail to cause the 21st Floor Substantial Completion Date to occur on or before August 1, 2013 (the “21st Floor First Outside Date”), then Tenant shall be entitled to a rent credit in the amount of $4,494.75 per day for each day after the 21stFloor First Outside Date that the 21stFloor Substantial Completion Date shall not occur; provided, however, that if Landlord shall fail to cause 21stFloor Substantial completion Date to occur on or before October 1, 2013 (the “21st Floor Second Outside Date”), then then the amount of such rent credit shall be increased to $8,989.50 per day for each day after the 21stFloor Second Outside Date that the 21stFloor Substantial Completion Date shall not occur. Such rent credit shall be applied, until fully exhausted, against the first fixed annual rent due under this Lease with respect to the 21stFloor Portion from and after the full application of the rent credit set forth in Article 2B(iv) of this Lease. Notwithstanding the foregoing, the 21stFloor First Outside Date and the 21stFloor Second Outside Date shall each be extended by one day for each day that the completion of the Building Work which is applicable to such space is delayed due to any of the causes set forth in Article 21A of this Lease or due to any act or omission of Tenant, its agents, employees or contractors.

B. The Building Work shall be considered to be substantially completed if only minor insubstantial details of construction and mechanical adjustments (i.e., “punch list items”) remain to be completed, as determined and identified upon a joint inspection of the applicable portion of the Demised Premises (i.e., the 20th Floor Portion or the 21st Floor Portion, as the case may be) by representatives of Landlord and Tenant within five (5) Business Days prior to the 20th Floor Commencement Date or the 21st Floor Commencement Date, as the case may be, provided such space is accessible, reasonably usable for the purpose of performing Tenant’s Initial Installation (as such term is defined in Article 22C(i) of this Lease), and in a condition that is suitable for the issuance of any governmental permit or approval that is required in connection with such work. Landlord shall nevertheless seek to complete such punch list items with reasonable diligence, but in any event within a period of thirty (30) days after the 20th Floor Commencement Date or the 21st Floor Commencement Date, as the case may be (or, with respect to any such punch list items discovered by Tenant during the course of Tenant’s Initial Installation for which Landlord is responsible hereunder, within thirty (30) days after Landlord’s receipt of notice thereof from Tenant, provided such punch list items so discovered by Tenant shall have no effect whatsoever on the 20th Floor Commencement Date or the 21st Floor Commencement Date hereunder).

C. Landlord shall, in accordance with the foregoing, fix the 20th Floor Commencement Date and the 21st Floor Commencement Date, and shall notify Tenant of the dates so fixed. When both the 20th Floor Commencement Date and the 21st Floor Commencement Date have so been determined, the parties hereto shall, within thirty (30) days thereafter, at Landlord’s request, execute a written agreement confirming such dates as the 20th Floor Commencement Date and the 21st Floor Commencement Date. Any failure of the parties to execute such written agreement shall not affect the validity of this Lease or either such Commencement Dates as fixed and determined by Landlord, as aforesaid.

D. Tenant by entering into occupancy of the 20th Floor Portion or the 21st Floor Portion, as the case may be, shall be presumptively deemed to have agreed that Landlord up to the time of such occupancy had performed all of its obligations hereunder and that such portion of the Demised Premises was in satisfactory condition as of the date of such occupancy, unless within twenty (20) days after such date Tenant shall give written

notice (hereinafter called the “Punch List Notice”) to Landlord specifying the respects in which the same were not in satisfactory condition, in which event the 20th Floor Portion or the 21st Floor Portion, as applicable, shall be conclusively deemed to be in satisfactory condition except for the items set forth in the Punch List Notice and any latent defects which are not readily discoverable upon a reasonable inspection of such space, which latent defects shall be promptly corrected by Landlord, at its sole cost and expense, provided Tenant notifies Landlord within sixty (60) days after Tenant discovers same. The giving of the Punch List Notice shall have no effect whatsoever upon the 20th Floor Commencement Date or the 21st Floor Commencement Date.

E. The term “Lease Year” when used in this Lease shall mean the twelve (12) months commencing on the later to occur of the 20th Floor Commencement Date or the 21st Floor Commencement Date (or if the later of such two Commencement Dates is not the first day of a month, the first day of the month following the month in which occurs the later to occur of the 20th Floor Commencement Date or the 21st Floor Commencement Date), and each subsequent period of twelve (12) months. The first Lease Year shall include the period, if any, from the later to occur of the 20th Floor Commencement Date or the 21st Floor Commencement Date to the end of the month in which the later of such Commencement Dates occurs.

F. The Demised Premises shall be used by Tenant (or by any permitted assignee or sublessee of Tenant) solely as general, administrative and executive offices for the conduct of Tenant’s business, and for uses ancillary and related thereto, including, without limitation, as a data center, one or more office pantries and an exercise and/or game room (provided that the use of such exercise/game room shall not adversely affect the use or occupancy of any other tenant or occupant of the Building); and the Demised Premises shall be not be used for any other purpose, such covenant being of the essence of this Lease. The use of all or any portion of the Demised Premises for any activities not directly related to, or in furtherance of, the conduct of Tenant’s business shall be a prima facie breach of such covenant. Notwithstanding anything contained herein to the contrary, a breach of such covenant shall be deemed a material and substantial default by Tenant under this Lease, for which Landlord shall have all remedies available to it under this Lease and under the law, including, without limitation, the right to enforce such covenant by injunctive or other appropriate equitable relief. Without limiting the generality of the foregoing, it is expressly understood that no portion of the Demised Premises shall be used as, by or for (a) retail operations of any bank, trust company, savings bank, industrial bank, savings and loan association, credit union or personal loan association or other form of entity, (b) a public stenographer or typist, (c) a barber shop, beauty shop, beauty parlor or manicure parlor, (d) telephone agency, (e) a telephone, court reporting, stenographic or secretarial service, (f) a messenger service, (g) a travel or tourist agency, (h) an employment agency, (i) a restaurant or bar, (j) a commercial document reproduction or offset printing service, (k) a public vending machines operation, (l) a retail, wholesale or discount shop for sale of books, magazines, audio or video tapes, CD ROM, DVD ROM, Blueray or other devices for the recording or transmitting of audio or visual signals, images, music or speech, electronic equipment and accessories or any other merchandise, (m) a retail service shop, (n) a labor union, (o) a school or classroom, (p) a governmental or quasi-governmental bureau, department or agency, including an autonomous governmental corporation, embassy or consular office of any country or other quasi-autonomous or sovereign organization, whether or not subject to the Foreign Sovereign Immunities Act of 1976, as from time to time amended, or any successor statute, (q) an advertising agency, (r) a firm whose principal business is real estate brokerage, (s) a company engaged in the business of renting office or desk space, (t) any person, organization, association, corporation, company, partnership entity or other agency immune from service or suit in the courts of the State of New York or the assets of which may be exempt from execution by Landlord in any action for damages, (u) a factory of any kind, (v) any use to which increased security costs or insurance premiums payable by Landlord may be attributed, (w) a payroll office or check cashing operation, (x) a clinic, (y) any manufacturing purpose, (z) film, radio or video production or broadcasting studio., or (aa)any illegal purpose. Tenant shall not affix any sign to any window or exterior surface of the Demised Premises nor install or place any sign within the Demised Premises that may be seen from the outside. Notwithstanding anything to the contrary contained in this Article 1F, Tenant (or any permitted assignee or sublessee of Tenant) shall be permitted to conduct its business in the Demised Premises on an on-line basis and, in connection therewith, may sell or otherwise deal in merchandise or services on-line.

G. Neither the Demised Premises for the halls, corridors, stairways, elevators or any other portion of the Building shall be used by Tenant or Tenant’s servants, employees, licensees, invitees or visitors in connection with the aforesaid permitted use or otherwise so as to cause any congestion of the public portions of the Building or the sidewalks or roadways adjoining the Building whether by trucking or by the congregating or loitering thereon of Tenant or Tenant’s servants, employees, licensees, invitees or visitors.

2. RENT

A. General:(i) Tenant agrees to pay rent as herein provided at the office of Landlord or such other place as Landlord may designate, in United States legal tender, by good and sufficient check drawn on a bank having a branch in the Borough of Manhattan, City of New York, or by wire transfer of immediately available U.S. funds pursuant to instructions provided by Landlord, and without any notice (except as may be specifically set forth herein), credit, set-off, counterclaim, deduction or reduction whatsoever, each of the types of rent set forth in this Article 2 and Article 3.

(ii) Any sum payable hereunder, other than fixed annual rent and use and occupancy charges following any holdover, shall be deemed additional rent and due within thirty (30) days after demand or, if Landlord is not obligated to make a demand there for, on the first day of each month following notice of each amount due, unless otherwise specifically provided. Landlord shall have the same rights and remedies provided herein or by law with respect to Tenant’s non-payment of additional rent and any other charge as it has with respect to Tenant’s nonpayment of fixed annual rent. Tenant warrants that the obligation to pay rent hereunder, whether any such payment is timely made or not, is an integral part of Tenant’s business and made in the ordinary course thereof.

B. Fixed Annual Rent: (i) There is herein reserved to Landlord for the entire term of this Lease fixed annual rent equal to the aggregate amount of the sums hereinafter set forth, as calculated (a) in this Article 2 and, (b) if and so long as Landlord provides electricity to the Demised Premises on a rent inclusion basis, in Article 3.Fixed annual rent shall be paid in advance as follows: commencing on 20th Floor Commencement Date or the 21st Floor commencement Date, as applicable, and on the first day of each month thereafter throughout the term of this Lease, Tenant shall pay to Landlord, without notice, credit, counterclaim, deduction, set off or reduction (except as may be specifically set forth herein), monthly payments of fixed annual rent equal to one-twelfth (1/12th) of each of the following annual amounts (except that the first monthly installment of fixed annual rent for the entire Demised Premises, in the amount of $304,892.92, is being paid upon the execution hereof):

FOR THE 20TH FLOOR PORTION:

(a) from the 20th Floor Commencement Date through the last day of the sixth Lease Year: Two Million Eighteen Thousand One Hundred Thirty-Three and 00/100 ($2,018,133.00) Dollars perannum ($168,177.75 per month); and

(b) from the first day of the seventh Lease Year through the last day of the eleventh Lease Year: Two Million Two Hundred Thirty-Two Thousand Eight Hundred Twenty-Eight and 00/100 ($2,232,828.00) Dollars perannum ($186,069.00 per month).

FOR THE 21ST FLOOR PORTION:

(a) from the 21st Floor Commencement Date through the last day of the sixth Lease Year: One Million Six Hundred Forty Thousand Five Hundred Eighty-Two and 00/100 ($1,640,582.00) Dollars per annum ($136,715.17 per month); and

(b) from the first day of the seventh Lease Year through the last day of the eleventh Lease Year: One Million Eight Hundred Fifteen Thousand One Hundred Twelve and 00/100 ($1,815,112.00) Dollars per annum ($151,259.33 per month).

(ii) Should the Commencement Date occur on any day other than the first day of a month, then the fixed annual rent for the unexpired portion of such month shall be adjusted and prorated on a per diem basis and any overpayment of the first month’s fixed annual rent shall be credited against the next month’s installment of fixed annual rent coming due.

(iii) For so long as Tenant is not in default, beyond any applicable grace or cure period, of any monetary or other material term of this Lease (including each Exhibit hereto), Tenant shall receive a rent credit against fixed annual rent in the amount of Two Million Three Hundred Seventy-Two Thousand Five Hundred Seventy-Nine and 58/100 ($2,372,579.58) Dollars, which rent credit shall be applied, until fully exhausted, against

the first fixed annual rent payable under this Lease with respect to the 20th Floor Portion, from and after the 20th Floor Commencement Date, except the installment being paid upon execution hereof (which shall be applied against the first payment of fixed annual rent due following full depletion of the aforesaid rent credit). If the term of this Lease is terminated prior to its stated expiration date solely as a result of any uncured default by Tenant, then, in addition to all other damages, rights and remedies herein provided and provided by law for Landlord, Landlord shall be entitled to the return of the total amount of such rent credit theretofore enjoyed by Tenant, which sum shall be deemed additional rent due and owing prior to such termination of the term hereof. The obligation of Tenant to pay such additional rent to Landlord shall survive the termination of the term of this Lease. Anything in this paragraph to the contrary notwithstanding, Tenant shall be responsible for paying all additional rent and electric charges due under this Lease during the period covered by such rent credit without any credit, setoff, deduction or reduction by reason of this paragraph (except as otherwise expressly provided herein).

(iv) For so long as Tenant is not in default, beyond any applicable grace or cure period, of any monetary or other material term of this Lease(including each Exhibit hereto), Tenant shall receive a rent credit against fixed annual rent in the amount of One Million Six Hundred Forty Thousand Five Hundred Eighty-Two and 00/100 ($1,640,582.00) Dollars, which rent credit shall be applied, until fully exhausted, against the first fixed annual rent payable under this Lease with respect to the 21st Floor Portion, from and after the 21st Floor Commencement Date, except the installment being paid upon execution hereof(which shall be applied against the first payment of fixed annual rent due following full depletion of the aforesaid rent credit). If the term of this Lease is terminated prior to its stated expiration date solely as a result of any uncured default by Tenant, then, in addition to all other damages, rights and remedies herein provided and provided by law for Landlord, Landlord shall be entitled to the return of the total amount of such rent credit theretofore enjoyed by Tenant, which sum shall be deemed additional rent due and owing prior to such termination of the term hereof. The obligation of Tenant to pay such additional rent to Landlord shall survive the termination of the term of this Lease. Anything in this paragraph to the contrary notwithstanding, Tenant shall be responsible for paying all additional rent and electric charges due under this Lease during the period covered by such rent credit without any credit, setoff, deduction or reduction by reason of this paragraph (except as otherwise expressly provided herein).

C. Operating Expenses Escalations: (i) Tenant shall pay to Landlord, as additional rent, operating expense escalation in accordance with this Article 2C.

(ii) For the purposes of this Article 2C, the following definitions shall apply:

(a) The term “Base Year” as herein after set forth for the determination of operating expenses escalation, shall mean the calendar year 2014.

(b) The term “The Percentage” shall mean 3.1026 percent (3.1026%).The Percentage has been computed on the basis of a fraction, the numerator of which is the rentable square foot area of the Demised Premises (i.e., 77,845) and the denominator of which is the total rentable square foot area of the office space in the Building Project (as such term is defined in subparagraph D(ii)(a) of this Article). The parties acknowledge and agree that the total rentable square foot area of the office space in the Building Project shall be deemed to be 2,509,022 rentable square feet.

(c) The term “comparative year” shall mean each calendar year commencing on or after January 1, 2015, in which occurs any part of the term of this Lease.

(d) The term “Expenses” shall mean the total of all the costs and expenses incurred or borne by Landlord with respect to the operation and maintenance of the Building and the improvements relating thereto and the services provided tenants therein, including, but not limited to, the costs and expenses incurred for and with respect to: steam and any other fuel; water rates and sewer rents; air-conditioning; mechanical ventilation; heating; cleaning (unless and to the extent Tenant is required to contract separately for such cleaning), by contract or otherwise; window washing (interior and exterior); elevators, escalators; porter and matron service; Building electric current (Building electric current shall be deemed, for the purposes of this Article 2C, to mean all electricity purchased for the Building, except that the parties acknowledge and agree that for the purposes of calculating additional rent under this Article 2C and irrespective of the actual allocation of electric service between tenants and the Building, fifty (50%) percent of the Building’s payment to the utility company or companies for the provision,

supply and distribution to the Building of electricity shall be deemed to be payment for Building electric current); protection and security; lobby decoration; repairs, replacements and improvements which are appropriate for the continued operation of the Building in the same or an improved manner as the Building is operated on the date hereof; expenses (other than capital expenses excluded below or payable pursuant to Article 43E); for application fees, consulting, legal, architectural and engineering fees and inspection charges incurred in connection with obtaining, maintaining, renewing and/or improving any environmental rating or certification for the Building or any component part thereof or equipment or apparatus used therein (such as LEED (Leadership in Energy and Environmental Design), Green Globes or Energy Star); maintenance; painting of non-tenant areas; fire, extended coverage, boiler and machinery, sprinkler, apparatus, public liability and property damage insurance, rental and plate glass insurance and any insurance required by a mortgagee or other holder of a Superior Interest (as hereinafter defined); management fees; supplies, wages, salaries, disability benefits, pensions, hospitalization, retirement plans, and group insurance respecting employees of Landlord or Landlord’s managing agent and the wages, salaries, and benefits of employees for whom Landlord reimburses such agent, up to and including the Building manager (including a pro rata share only of such wages and benefits of employees including Landlord’s engineer, who are employed at more than one building, which pro rata share shall be determined by Landlord and shall be based upon Landlord’s estimate of the percentage of time spent by such employees at the Building Project); uniforms and working clothes for such employees and the cleaning thereof and expenses imposed pursuant to law or to any collective bargaining agreement with respect to such employees; workmen’s compensation insurance, payroll, social security, unemployment and other similar taxes with respect to such employees; contributions to any business improvement district association (whether currently existing or hereafter established) not deemed to be real estate taxes or a business improvement district assessment payable pursuant to Article 2D hereof; legal, accounting and other fees paid to professionals and consultants retained by or on behalf of Building management and not excluded pursuant to the following paragraph; maintenance and operating costs for any specialty improvement constructed or designated solely for use by tenants of the Building, including, without limitation, conference center, cafeteria, tanning salon, exercise or fitness facility, luncheon or recreational club or facility, less the amount of any rent or other usage fees received by Landlord in connection therewith; and association fees or dues payable to professional associations such as the Real Estate Board of New York, Inc. and other associations organized to promote the interests of commercial landlords.

The foregoing costs and expenses shall exclude or have deducted from them, as the case may be and as shall be appropriate: leasing commissions; managing agents’ fees or commissions in excess of the rates then customarily charged for Building management for buildings of like class and character; executives’ salaries above the grade of Building manager; debt service under any mortgage or other loan or rent under any underlying or ground lease of the Building; expenditures for capital improvements, except those required by law and enacted or first becoming effective after the date of this Lease, in which event the cost thereof shall be included in Expenses for the year (whether Base Year or a comparative year) in which the costs are incurred and subsequent comparative years, amortized on a straight line basis, to the extent that such items are amortized over the useful life of the item in question (determined in accordance with generally accepted accounting principles (“GAAP”)), with an interest factor equal to the prime rate of the JP Morgan Chase Bank, N.A. (or its successors) at the time of Landlord’s having incurred said expenditure; amounts received by Landlord through proceeds of insurance to the extent the proceeds are compensation for expenses which were previously included in Expenses hereunder, costs of repairs or replacements incurred by reason of fire or other casualty to the extent to which Landlord is compensated therefor through proceeds of insurance, or which are necessitated by the exercise of the right of eminent domain; advertising and promotional expenditures, amounts paid pursuant to Article 43E hereof; legal, auditing and other third-party fees incurred in connection with actual or anticipated litigation with any Building tenant or group of tenants to enforce any provision of their respective lease; the incremental cost of furnishing services such as overtime HVAC to any tenant at such tenant’s expense; costs incurred in performing work or furnishing services for individual tenants (including this Tenant) at such tenant’s expense; and costs of performing work or furnishing services for tenants other than this Tenant at Landlord’s expense to the extent that such work or service is in excess, on a per rentable square foot basis, of any work or service Landlord is obligated to furnish to this Tenant at Landlord’s expense. Expenses shall further exclude the following:

(1) Costs incurred in connection with the original construction or any subsequent renovation of the Building or any costs of repairing, replacing or otherwise correcting defects or deficiencies in the design, construction or components of the improvements comprising the Building;

(2) Costs incurred in connection with the investigation, removal, remediation or clean-up of Hazardous Materials from the Project or Buildings (including, without limitation, the fees of any environmental consultants);

(3) Costs incurred in connection with the sales, mortgaging, selling or change of ownership of the Building, including, without limitation, brokerage commissions, consultants’, attorneys’ and accountants’ fees, closing costs, title insurance premiums, transfer taxes and interest charges;

(4) Costs, fines, interest, penalties, legal fees or costs of litigation incurred due to the late payments of taxes, utility bills and other costs incurred by Landlord’s failure to make such payments when due;

(5) Landlord’s general corporate overhead and general and administrative expenses;

(6) Rent for Landlord’s on-site leasing office, or any other offices or spaces of Landlord or any related entity, except if such space is actually used in connection with the operation and/or management of the Building;

(7) Costs or expenses of utilities directly metered to tenants of the Building and payable separately by such tenants or electric power costs for which any tenant directly contracts with the local public service company;

(8) Costs of any above-standard electrical usage by any other tenants of the Building;

(9) Moving expense costs of tenants of the Building;

(10) Costs incurred for any item to the extent covered by a manufacturer’s, materialman’s, vendor’s or contractor’s warranty and paid by such manufacturer, materialman, vendor or contractor;

(11) Non-cash items such as deductions for depreciation and amortization of Building equipment, except as otherwise provided herein;

(12) Reserves for maintenance, repairs and replacements or any other purpose;

(13) Costs incurred by Landlord for trustee’s fees, entity organizational expenses and accounting fees except accounting fees relating to the ownership and operation of the Building (exclusive of the incremental accounting fees to the extent incurred separately to solely and exclusively report operating results to the Building’s owners or lenders);

(14) Costs of any special or extra heating, ventilating, air conditioning, janitorial or other special or extra services or work provided to tenants during non-business hours for which Landlord receives after-hours fees or charges, if applicable;

(15) Political or charitable contributions;

(16) Works of fine art;

(17) Retail operating expenses for retail space in the Building;

(18) Development fees, impact fees and similar charges;

(19) The cost of installing, operating and maintaining the Empire State Building Observatory or any other specialty improvement which is not designated solely for use by tenants of the Building; and the cost of installing any specialty improvement which is designated solely for

use by tenants of the Building, including, without limitation, conference center, cafeteria, tanning salon, exercise or fitness facility, luncheon or recreational club or facility;

(21) Any items included in real estate taxes;

(22) All items and services for which any tenant reimburses Landlord or pays third persons; and

(23) Any and all deductibles and retentions on any insurance maintained by Landlord.

(e) The “Escalation Statement” shall mean a statement in writing issued by Landlord or the Building’s managing agent, setting forth the amount payable by Tenant for a specified comparative year) pursuant to Article 2C(v) below.

(iii) If during all or part of the Base Year or of any comparative year, Landlord shall not furnish any particular item(s) of work or service (which would constitute an Expense hereunder) to portions of the Building due to the fact that such portions are not occupied or leased, or because such item of work or service is not required or desired by the tenant of such portion, or such tenant is itself obtaining and providing such item of work or service, or for other reasons, then, for the purposes of computing the additional rent payable under this Article 2C, the amount of the Expenses for such Base Year or comparative year, as applicable, shall be increased by an amount equal to the additional operating and maintenance expenses which would reasonably have been incurred during such period by Landlord if it had at its own expense furnished such item of work or services that had not been provided to such portion of the Building Project.

(iv) If there shall be any conflict or ambiguity between any provision of this Article 2C and Article 43E hereof, the provisions of said Article 43E shall take precedence and be controlling.

(v) If the Expenses for any comparative year shall be greater than the Expenses for the Base Year, Tenant shall pay to Landlord, as additional rent for such comparative year, in the manner hereinafter provided, an amount equal to The Percentage of the excess of the Expenses for such comparative year over the Expenses for the Base Year (such amount being hereinafter called the “Expense Payment”). The first payment of additional rent for the entire first comparative year shall be payable within thirty (30) days after the bill therefor is tendered. Commencing on the first day of the first comparative year and thereafter, all monthly installments of rental shall reflect one-twelfth (1/12th) of the then current annual amount of such adjustment for Expenses plus such additional amount as Landlord estimates in good faith such Expenses shall increase on account of the next ensuing comparative year and such amount shall be payable until a new adjustment becomes effective pursuant to the provisions of this Article 2C. Within thirty (30) days after the rendering of the next Escalation Statement, Tenant shall pay to Landlord on account of additional rent for the comparative year to which such Expense Statement relates, an amount equal to the excess of additional rent due on account of increases in Expenses over the amount collected on account thereof during the preceding year. If there shall have been a reduction in the Expenses during any ensuing comparative year, the excess of the amount collected by Landlord over the amount paid on account of such comparative year shall be credited against amounts payable by Tenant for the current comparative year (or if the term hereof shall have expired on its stated expiration date, promptly refunded to Tenant). If any Escalation Statement is furnished to Tenant after the commencement of such comparative year, there also shall within ten (10) days be paid by Tenant to Landlord an amount equal to the portion of such monthly adjustments allocable to the part of such comparative year which shall have lapsed prior to the first day of the calendar month next succeeding the calendar month in which said Escalation Statement is furnished to Tenant. The aforesaid monthly payments based on the total Expense Payment for the preceding calendar year or comparative year, as the case may be, shall be adjusted to reflect, if Landlord can reasonably so estimate, known increases in rates or costs, for the current comparative year, applicable to the categories involved in computing Expenses, whenever such increases become known prior to or during such current comparative year.

(vi) Following the expiration of the Base Year and each comparative year and after receipt of necessary information and computations from Landlord’s certified public accountant, Landlord shall submit to Tenant an Expense statement, as hereinafter described, setting forth the Expenses for the preceding comparative year, the Expenses for the Base Year, and the Expense Payment, if any, due to Landlord from Tenant for such

comparative year under this Article 2C. The rendition of such statement to Tenant shall constitute prima facie proof of the accuracy thereof.

(vii) The Expense Statements furnished by Landlord as provided above shall be based on Landlord’s books and records (which shall be maintained in accordance with GAAP) and information and computations made for Landlord by a certified public accountant (who may be the accountant now or then employed by Landlord for the audit of its accounts); said certified public accountant may rely on Landlord’s allocations and estimates wherever operating cost allocations or estimates are needed for this Article. The Expense Statements thus furnished to Tenant shall constitute a final determination as between Landlord and Tenant of the Expenses for the periods represented thereby, unless Tenant within one hundred eighty (180) days after any Expense Statement is furnished, time being of the essence, shall give a notice to Landlord (each an “Examination Notice”) that Tenant wishes to examine Landlord’s relevant books and records regarding the accuracy of such Expense Statement or its appropriateness, which notice may but need not specify the particular respects in which the Expense Statement is inaccurate or inappropriate and the reasons therefor. Pending the resolution of any dispute arising prior to or by virtue of such examination, Tenant shall continue to pay the additional rent to Landlord in accordance with the Expense Statements furnished by Landlord. Provided Tenant is current in the payment of all fixed rent and additional rent hereunder, Tenant, its representatives, accountants and/or attorneys shall have the right, during regular business hours, to examine Landlord’s relevant books and records with respect to the foregoing, provided such examination is commenced within thirty (30) days of the giving of an Examination Notice and concluded within five (5) Business Days after its commencement. Tenant shall keep such examination and related arbitration (described below) in strict confidence (except if disclosure is required by law), it being agreed that Tenant’s failure to do so shall be deemed a substantial and material default by Tenant under the terms of this Lease, for which Landlord shall have all remedies available to it under this Lease and under the law. IN NO EVENT MAY TENANT EMPLOY ANY PERSON OR ENTITY WHOSE COMPENSATION WHOLLY OR PARTIALLY IS CALCULATED UPON A PERCENTAGE OF ANY EXPENSES DEEMED TO BE INCORRECTLY INCLUDED IN MAKING LANDLORD’S CALCULATION OF ADDITIONAL RENT UNDER THIS ARTICLE 2C OR ANY PERCENTAGE OF SAVINGS REALIZED BY TENANT BY REASON OF DISPUTING LANDLORD’S CALCULATION OF SUCH ADDITIONAL RENT, EXCEPT A NATIONALLY OR REGIONALLY RECOGNIZED FIRM REASONABLY ACCEPTABLE TO LANDLORD. Any such dispute under this Article 2C shall be resolved by arbitration in accordance with Article 39 hereof.

D. Tax Escalation. (i) Tenant shall pay to Landlord, as additional rent, tax escalation in accordance with this Article 2D.

(ii) Definitions: For the purposes of this Article 2D, the following definitions shall apply:

(a) The term “applicable tax rate” shall mean the real estate tax rate for any fiscal tax year (or portion thereof) of the City of New York applicable to the Building, other improvements related thereto, and land upon which the Building is situated, sometimes referred to as the “Building Project”, for the purpose of computing real estate taxes.

(b) Subject to subparagraph (l) below, the term “base year taxes” shall mean the average of the real estate taxes payable with respect to the Building Project for the tax year commencing July 1, 2013 and ending June 30, 2014 and the tax year commencing July 1, 2014 and ending June 30, 2015, determined by applying the applicable tax rate to each of the two (2) tax years included in the base tax year assessment and taking the average of such two (2) numbers.

(c) Subject to subparagraph (l) below, the term “base tax year” shall mean the calendar year 2014.

(d) Subject to subparagraph (l) below, the term “base tax year assessment” means the taxable assessed value (without regard or giving effect to any abatement, exemption or credit) of the Building, other improvements related thereto and the land on which the Building Project is located, for each of the tax year commencing July 1, 2013 and ending June 30, 2014 and the tax year commencing July 1, 2014 and ending June 30, 2015.

(e) Subject to subparagraph (l) below, the term “comparative year” shall mean each calendar year commencing on or after January 1, 2015, in which occurs any part of the term of this Lease.

(f) Subject to subparagraph (l) below, the term “comparative year assessment” shall mean the actual assessed value (without regard or giving effect to any abatement, exemption or credit) of the Building Project for the relevant comparative year for which additional rent under this paragraph D is being calculated (i.e., the actual assessed value of the Building Project for each of the two (2) tax years included in such comparative year).

(g) Subject to subparagraph (l) below, the term “comparative year taxes” shall mean the real estate taxes determined by applying the applicable tax rate to the comparative year assessment (i.e., by applying such tax rate to the assessment for each of the two (2) tax years included in the comparative year assessment and taking the average of such two (2) numbers).

(h) The term “The Percentage” shall mean 2.8308 (2.8308%) percent. The Percentage has been computed on the basis of a fraction, the numerator of which is the rentable square foot area of the Demised Premises (i.e., 77,845) and the denominator of which is the total rentable square foot area of the office and commercial space in the Building Project. The parties acknowledge and agree that the total rentable square foot area of the office and commercial space in the Building Project shall be deemed to be 2,749,931 rentable square feet.

(i) The term “real estate taxes” shall mean the total of all taxes and special or other assessments levied, assessed or imposed at any time by any governmental authority upon or against the Building Project, any tax or assessment levied, assessed or imposed at any time by any governmental authority in connection with the receipt of income or rents from the Building Project, to the extent that same shall be in lieu of all or a portion of any of the aforesaid taxes or assessments, or additions or increases thereof, upon or against said Building Project, any assessment by a business improvement district (BID), and all costs incurred by Landlord to contest any assessment of the Building or any tax, charge, or other imposition levied against it. If, due to a future change in the method of taxation or in the taxing authority, or for any other reason, a franchise, income, transit, profit or other tax or governmental imposition, however designated, shall be levied against Landlord in substitution in whole or in part for the real estate taxes, or in lieu of additions to or increases of said real estate taxes (whether or not the enabling legislation states that such tax is in substitution in whole or in part for the real estate taxes, or in lieu of additions to or increases of said real estate taxes), then such franchise, income, transit, profit or other tax or governmental imposition shall be deemed to be included within the definition of “real estate taxes” for the purposes hereof. As to special assessments which are payable over a period of time extending beyond the term of this Lease, only a pro rata portion thereof covering the portion of the term of this Lease unexpired at the time of the imposition of such assessment, shall be included in “real estate taxes.” If by law, any assessment may be paid in installments, then, for the purposes hereof (a) such assessment shall be deemed to have been payable in the maximum number of installments permitted by law and (b) there shall be included in real estate taxes, for each comparative year in which such installments may be paid, the installments of such assessment so becoming payable during such comparative year, together with interest payable during such comparative year in respect of any such installment. Except as otherwise provided above, “real estate taxes” shall not include (x) state, corporate or franchise taxes, or any inheritance, estate or gift taxes, mortgage taxes, deed, stamp or transfer taxes, or interest, or (y) penalties for late payment of real estate taxes, or (z) increases in real estate taxes attributable to any reassessment of the Building Project resulting from or arising out of the Initial Public Offering (“IPO”) which is currently being contemplated by Landlord and/or its affiliate and which would involve the transfer of Landlord’s interest in the Building to the public company being formed in connection with such transaction (it being understood and agreed, however, that the burden of proving that such reassessment is due to such IPO shall be solely on Tenant).

(j) The term “tax year” means any fiscal tax year of the City of New York.

(k) Where more than one assessment is imposed by the City of New York for any tax year, whether denominated an “actual assessment” or “transitional assessment” or otherwise, then the phrases herein “assessed value” and “assessments” shall mean the actual assessed value (and not the transitional assessed value, taxable assessment or other assessment) designated by the City of New York for any comparative year and the taxable assessment for the base tax year.

(l) Notwithstanding anything contained herein to the contrary, if Landlord shall fail to cause both the 20th Floor Substantial Completion Date and the 21st Floor Substantial Completion Date to occur on or before December 31, 2013 (the “Base Tax Year Outside Date”), then the following terms shall have the following meanings herein: the term “base tax year” shall mean the tax year commencing July 1, 2014 and ending June 30, 2015; the term “base year taxes” shall mean the real estate taxes payable with respect to the Building Project for the tax year commencing July 1, 2014 and ending June 30, 2015; the term “base tax year assessment” shall mean the taxable assessed value (without regard or giving effect to any abatement, exemption or credit) of the Building, other improvements related thereto and the land on which the Building Project is located, for the tax year commencing July 1, 2014 and ending June 30, 2015; the term “comparative year” shall mean each tax year commencing on or after July 1, 2015 (or such other 12-month period commencing on or after July 1, 2015 adopted by the City of New York as its fiscal tax year); the term “comparative year assessment” shall mean the actual assessed value (without regard or giving effect to any abatement, exemption or credit) of the Building Project for the relevant comparative year for which additional rent under this paragraph D is being calculated; and the term “comparative year taxes” shall mean the real estate taxes determined by applying the applicable tax rate to the comparative year assessment. Notwithstanding the foregoing, the Base Tax Year Outside Date shall be extended by one day for each day that the completion of the Building Work is delayed due to any of the causes set forth in Article 21A of this Lease or due to any act or omission of Tenant, its agents, employees or contractors.

(iii) (a) Before or after the start of each comparative year, Landlord shall furnish to Tenant a statement of the comparative year taxes, and a statement of the real estate taxes payable during the base tax year (together with copies of the relevant real estate tax bills for such comparative year taxes and the real estate taxes payable during the base tax year). If the comparative year taxes exceed the base year taxes, additional rent for such comparative year, in an amount equal to The Percentage of the excess, shall be due from Tenant to Landlord, and such additional rent shall be payable by Tenant to Landlord at Landlord’s election (1) within thirty (30) days after receipt of the aforesaid statement or (2) in equal monthly installments each equal to one-twelfth (1/12th) of The Percentage of the excess of the relevant comparative year taxes over the base year taxes, each payable with the monthly installment of fixed annual rent. If such statement is tendered to Tenant after the commencement of any comparative year and Landlord has elected that the relevant excess be paid in accordance with item (2) of the preceding sentence, Tenant shall, notwithstanding the terms of item (2) of the preceding sentence, pay to Landlord within thirty (30) days after such statement is tendered, a lump sum equal to the product resulting from multiplying The Percentage of such excess of the comparative year taxes over the base year taxes, by a fraction the numerator of which is the number of full and partial months elapsed from the commencement of the relevant comparative year and the denominator of which is twelve (12). Thereafter, Tenant shall commence paying the monthly installments of such additional rent with the next installment of fixed annual rent next due and continue paying pursuant to said item (2) until a subsequent statement with respect thereto is rendered by Landlord. The benefit of any discount for any earlier payment or prepayment of real estate taxes shall accrue solely to the benefit of Landlord, and such discount shall not be subtracted from the real estate taxes payable for any comparative year.

(b) Should the base year taxes be reduced by final determination of legal proceedings, settlement or otherwise, then, the base year taxes shall be correspondingly revised, the additional rent theretofore paid or payable hereunder for all comparative years shall be recomputed on the basis of such reduction, and Tenant shall pay to Landlord as additional rent, within thirty (30) days after being billed therefor, any deficiency between the amount of such additional rent as theretofore computed and the amount thereof due as the result of such recomputations. Should the base year taxes be increased by such final determination of legal proceedings, settlement or otherwise, then appropriate recomputation and adjustment also shall be made, and the amount of any overpayment by Tenant shall be refunded to Tenant within thirty (30) days after such final determination (or, at Landlord’s option, applied, until fully exhausted, as a rent credit against the next rent due under this Lease).

(c) As long as Tenant is a tenant and is not in default of any material obligation hereunder, if Tenant shall have made a payment of additional rent under this paragraph and Landlord shall receive during the term hereof a refund of any portion of the real estate taxes paid for any comparative year after the base tax year on which such payment of additional rent shall have been based, as a result of a reduction of such real estate taxes by final determination of legal proceedings, settlement or otherwise, Landlord shall, promptly after receiving the refund, credit to Tenant The Percentage of the refund less The Percentage of expenses (including attorneys’ and appraisers’ fees) incurred by Landlord in connection with any such application, settlement negotiation or proceeding (unless previously included in real estate taxes for the comparative year to which such expenses relate). If prior to

the payment of taxes for any comparative year, Landlord shall have obtained a reduction of that comparative year’s assessed valuation of the Building Project, and therefore of said taxes, then the term “real estate taxes” for that comparative year shall be deemed to include the amount of Landlord’s expenses in obtaining such reduction in assessed valuation, including attorneys’ and appraisers’ fees.

(d) The statement of the real estate taxes to be furnished by Landlord as provided above shall be certified by Landlord and shall constitute a final determination as between Landlord and Tenant of the real estate taxes for the periods represented thereby, unless Tenant, within ninety (90) days after they are furnished, time being of the essence, shall give a written notice to Landlord that it disputes their accuracy or their appropriateness, which notice shall specify the particular respects in which the statement is inaccurate or inappropriate. If Tenant shall so dispute said statement then, pending the resolution of such dispute, Tenant shall pay the additional rent to Landlord in accordance with the statement furnished by Landlord. Any such dispute shall be resolved by arbitration in accordance with Article 39 hereof.

E. No Right to Apply Security: Tenant shall not have the right to apply any security deposited to assure Tenant’s faithful performance of Tenant’s obligation hereunder to the payment of any installment of fixed annual rent or additional rent.

F. No Reduction in Fixed Annual Rent, Etc.:(i) In no event shall the fixed annual rent under this Lease be reduced by virtue of any decrease in the amount of any additional rent payment under this Article or any other provision of this Lease.

(ii) If Landlord receives from Tenant any payment less than the sum of the fixed annual rent and additional rent then due and owing pursuant to this Lease, Tenant hereby waives its right, if any, to designate the items to which such payment shall be applied and agrees that Landlord in its sole discretion may apply such payment in whole or in part to any fixed annual rent, additional rent, any other charge payable hereunder or to any combination thereof then due and payable hereunder.

(iii) Unless Landlord shall otherwise expressly agree in writing, acceptance of any portion of the fixed annual rent or additional rent from anyone other than Tenant shall not relieve Tenant of any of its other obligations under this Lease, including the obligation to pay other fixed annual rent and additional rent, and Landlord shall have the right at any time, upon notice to Tenant, to require Tenant (rather than someone other than Tenant) to pay the fixed annual rent and additional rent payable hereunder directly to Landlord. Furthermore, such acceptance of fixed annual rent and additional rent shall not be deemed to constitute an assignment of this Lease, a subletting of the Demised Premises or Landlord’s consent to an assignment of this Lease or a subletting or other occupancy of the Demised Premises by anyone other than Tenant, nor a waiver of any of Landlord’s rights or Tenant’s obligations under this Lease.

G. Partial Comparative Year: If the Commencement Date shall occur during a comparative year commencing prior to the term hereof, then the additional rent due under any paragraph of this Article for the first comparative year (as defined in the relevant paragraph) shall be a proportionate share of said additional rent for the entire comparative year, said proportionate share to be based upon the length of time that the lease term will be in existence during such first comparative year. Upon the date of any expiration or termination of this Lease (except termination because of Tenant’s default) whether the same be the date herein above set forth for the expiration of the term or any prior or subsequent date, a proportionate share of said additional rent for such comparative year during which such expiration or termination occurs shall immediately become due and payable by Tenant to Landlord, if it was not theretofore already billed and paid. The said proportionate share shall be based upon the length of time that this Lease shall have been in existence during such comparative year. Landlord shall, as soon as reasonably practicable, compute the additional rent due from Tenant, as aforesaid, which computations shall either be based on that comparative year’s actual figures or be an estimate based upon the most recent statements theretofore prepared by Landlord and furnished to Tenant as may be required under any paragraph in this Article. If an estimate is used, then Landlord shall cause statements to be prepared on the basis of the comparative year’s actual figures promptly after they are available, and thereupon, Landlord and Tenant shall make appropriate adjustments of any estimated payments theretofore made.

H. ICAP:

(i) For the purposes of this Article 2H the following definitions shall apply:

(a) The term “DLS” shall mean the Division of Labor Services of the DOBS or any successor agency to or hereafter becoming responsible for all or any relevant function of DLS as such functions relate to ICAP.

(b) The term “DOBS” shall mean the New York City Department of Business Services or any successor agency to or hereafter becoming responsible for all or any relevant function of DOBS as such functions relate to ICAP.

(c) The term “DOF” shall mean the New York City Department of Finance or any successor agency to or hereafter becoming responsible for all or any relevant function of DOF as such functions relate to ICAP.

(d) The term “DSBS” shall mean the New York City Department of Small Business Services or any successor agency to or hereafter becoming responsible for all or any relevant function of DSBS as such functions relate to ICAP.

(e) The term “ICAP” shall mean Industrial and Commercial Abatement Program or any successor or alternate program to the Industrial and Commercial Abatement Program as constituted on the date of this Lease.

(ii) Landlord hereby notifies Tenant that Landlord has availed or intends to avail itself of certain exemptions and/or abatements of real estate taxes under the ICAP in connection with certain renovations and improvements made or to be made to the Building. Tenant agrees to comply with all rules and regulations of the ICAP including, but not limited to, the filing requirements of the DOF, the DSBS and the DOBS and its DLS and to cooperate with Landlord in Landlord’s compliance with the rules, regulations and requirements promulgated in connection with the ICAP by an of such departments or divisions or otherwise pursuant to law. In connection therewith, all of Tenant’s construction managers, contractors and subcontractors employed in connection with work performed by or on behalf of Tenant at the Building shall be contractually required by Tenant to comply with DSBS and DOBS and DLS and any other requirements applicable to construction projects benefiting from the ICAP. Such compliance, as of the date hereof, includes, without limitation, the following: the submission and approval of a Construction Employment Report, attendance, as requested by Landlord, at a pre-construction conference with representatives of DSBS and adherence to the provisions of Article 22 of the ICAP Rules and Regulations, the provisions of the New York City Charter, the provisions of Sections 11-256 through 11-267 of the Administrative Code of the City of New York and the provisions of Executive order No. 50 (1980) and cooperation with Landlord with respect to Landlord’s application to obtain the ICAP exemption and/or abatements and the implementation of the ICAP through the period that the program shall be in effect. Furthermore, at Landlord’s request as may be necessary to comply with ICAP rules, Tenant shall (a) direct its architect or engineer to prepare a narrative description of the project with a construction budget to be submitted to Landlord, (b) report annually to Landlord the number of workers permanently engaged in employment in the Demised Premises, the nature of each worker’s employment, and to the extent applicable, the New York City residency of each worker, (c) provide access to the Demised Premises by employees and agents of the Department (as such term is defined in the ICAP rules and regulations) at all reasonable times on reasonable prior notice, (d) enforce the contractual obligations of Tenant’s construction managers, contractors, and subcontractors to comply with the DSBS requirements and any other requirements applicable to the Industrial and Commercial Abatement Program (e) submit required ICAP documentation which shall include copies of blueprints, plans and building permits, (f) furnish to Landlord (and cause its contractors and subcontractors to so furnish), simultaneously with the submission to any agency administering the ICAP, copies of all documents submitted by Tenant or required to be submitted by Tenant in connection with the ICAP (and cause its contractors and subcontractors to do the same) and (g) submit to Landlord on completion of the work, an architect’s letter of completion, and a summary by trade of the costs incurred completing such work, certified by a reputable, independent certified public accountant. Landlord shall reimburse Tenant for any reasonable out-of-pocket costs or expenses incurred by Tenant in order to comply with the provisions

of this paragraph H, within thirty (30) days after Landlord’s receipt of an invoice and reasonable substantiation of such costs.

3. ELECTRICITY

A. Landlord shall provide electricity to the Demised Premises, in accordance with the provisions of this Article 3. The parties agree that electricity distribution shall initially be on a “submetering” basis, in accordance with the provisions of paragraph B of this Article. If the requirements of law change so that Landlord may not legally furnish electricity to Tenant on a “submetering basis”, then and in such event Landlord shall redistribute to Tenant the electricity for the Demised Premises on a “rent inclusion” basis, in accordance with the provisions of paragraph C of this Article.

B. Submetering: (i) For the purposes of this Article 3B, the following definitions shall apply:

(a) “Landlord’s Cost” for redistributed electricity means the product of (x) Landlord’s Cost Rates for the relevant Utility Billing Period multiplied by (y) Tenant’s electricity consumption (i.e., energy and demand) based on the meter readings referred to below.

(b) “Landlord’s Cost Rates” means the sum of “Landlord’s Electricity Consumption Cost” and “Landlord’s Electricity Demand Cost”.

(c) “Landlord’s Electricity Consumption,” for any given Utility Billing Period means the number of kilowatt-hours of electricity consumed in and for the Building (including common areas, tenantable areas and mechanical areas) during said Utility Billing Period, as indicated on the applicable utility bills.

(d) “Landlord’s Electricity Consumption Cost,” (Landlord’s cost per KWH) for any given Utility Billing Period means the amount arrived at by dividing (x) Landlord’s KWH cost, as indicated on the applicable utility bills (inclusive of any taxes, including any taxes included in the computation of said utility bills) for Landlord’s Electricity Consumption for said Utility Billing Period, inclusive of any fuel adjustments or rate adjustments contained in said utility bill allocable to Landlord’s Electricity Consumption, by (y) Landlord’s Electricity Consumption (KWH) as indicated on said bills.

(e) “Landlord’s Electricity Demand,” for any given Utility Billing Period means the number of kilowatts of electricity demanded in and for the Building (including, without limitation, common areas, tenantable areas and mechanical areas) during said Utility Billing Period, as indicated on the applicable utility bill.

(f) “Landlord’s Electricity Demand Cost” (Landlord’s Cost per KW) for any given Utility Billing Period means the amount arrived at by dividing (x) Landlord’s KW cost, as indicated on the applicable utility bill (inclusive of any taxes, including any taxes included in the computation of said utility bill) for Landlord’s Electricity Demand for said Utility Billing Period, inclusive of any rate adjustments contained in said utility bill allocable to Landlord’s Electricity Demand (provided that same have not been included in the computation of Landlord’s Electricity Consumption Cost), by (y) Landlord’s Electricity Demand (KW) as indicated on said bill.

(g) “Utility Billing Period” means the respective period of electricity consumption and demand for which Landlord is charged on each successive bill from the utility company furnishing electricity to the Building.

(ii) If and so long as Landlord provides electricity to the Demised Premises (with Landlord providing the Required Electrical Capacity (as such term is defined in Article 3D(viii) hereof), which shall be the maximum electric service Landlord shall be obligated to redistribute to the Demised Premises) on a submetering useable basis, Tenant covenants and agrees to purchase the same from Landlord or Landlord’s designated agent at Landlord’s Cost plus six percent (6%) thereof. Where more than one meter measures the service of Tenant in the Building, the KWH and KW recorded by each meter shall be added and the aggregate shall be billed as if measured by a single meter. Bills therefor shall be rendered at such times as Landlord may elect, but in no event more frequently than monthly, and the amount, as computed from a meter or meters and determined by

Landlord’s Electrical Consultant in accordance with this Article, shall be deemed to be, and be paid as, additional rent. For purposes of determining Landlord’s Electricity Consumption Cost and Landlord’s Electricity Demand Cost, each amount appearing on any utility bill for demand, energy, fuel or rate adjustments shall be taken into account (where it cannot be determined from the utility bill whether such amount relates to consumption or to demand, it shall be deemed to relate to demand).

(iii) The parties acknowledge that there are currently electrical submeters located in each electrical closet on the 20th and 21st floors of the Building. It is agreed that Tenant, as part of Tenant’s Initial Installation, and without imposition of any “connection” or “tap in” charge, shall effect any and all work which is necessary to connect the electrical systems and equipment servicing the Demised Premises to one or more of such submeters, so that Landlord may furnish redistributed electricity in the Required Capacity to the Demised Premises on a submetering basis in accordance with the terms of this Article. Tenant may so connect to any such existing submeter on the 21st floor, and shall only connect to the submeter reasonably designated by Landlord on the 20th floor. Landlord agrees that all such submeters within the Demised Premises shall be in proper working order on the Commencement Date. Landlord further agrees that, within thirty (30) days after Tenant furnishes Landlord with the load letter described in subparagraph D(viii) of this Article, Landlord shall provide Tenant with a report and/or diagram identifying the locations of all power sources on each floor of the Demised Premises, including voltage amounts and electrical panels.

C. Rent Inclusion: (i) If and so long as Landlord provides electricity to the Demised Premises on a rent inclusion basis, Article 3B shall not apply and Tenant agrees that the fixed annual rent shall be increased by the amount of the Electricity Rent Inclusion Factor (“ERIF”), as hereinafter defined and by the amounts as hereinafter determined. Tenant acknowledges and agrees (a) that the fixed annual rent set forth in Article 2 of this Lease does not yet, but is to include initially an ERIF of Two and 25/100 ($2.25) Dollars per rentable square foot per annum to compensate Landlord for electrical wiring and other installations necessary for, and for its obtaining and making available to Tenant, the redistribution of electric current as an additional service; and (b) that said ERIF, which shall be subject to periodic adjustments as hereinafter provided, has been partially based upon an estimate of Tenant’s connected electrical load, which shall be deemed to be the demand (KW), and hours of use thereof, which shall be deemed to be the energy (KWH) for ordinary lighting and light office equipment and the operation of typical small business machines, including copying machines, personal computers and peripheral equipment such as printers, telephone switching equipment and facsimile transmission machines (such lighting, machines and equipment are hereinafter called “Ordinary Equipment”) for fifty (50) hours per week during the hours of 8:00 a.m. to 6:00 p.m., Mondays through Fridays, including holidays (“ordinary business hours”), with Landlord providing an average demand load to the Demised Premises meeting the Required Electrical Capacity, which shall be the maximum electrical service Landlord shall be obligated to redistribute to the Demised Premises. Any installation and use of equipment other than Ordinary Equipment and/or any demand load and/or any energy usage by Tenant in excess of the foregoing shall result in adjustment of the ERIF as hereinafter provided.

(ii) If the cost to Landlord of electricity shall have been, or shall be, increased subsequent to April 30 of the year in which this Lease is dated (whether such change occurs prior to or during the term of this Lease), due to (a) any change in costs or fees paid by Landlord under any agreement for the supply and/or distribution of electricity to the Building or electric rates or service classifications applicable to Landlord, or (b) any increase, subsequent to the last such electric rate or service classification change, in market prices, in fuel adjustments or charges of any kind, or (c) any taxes, imposed or which may be imposed on Landlord’s electricity purchases, or on Landlord’s electricity redistribution, or (d) by virtue of any other reason or cause, then the ERIF, which is a portion of the fixed annual rent, shall be changed in the same percentage as any such change in cost due to changes in any of the items listed in (a) through (d) above and, also, Tenant’s payment obligation for electricity redistribution shall change from time to time so as to reflect any such increase in cost due to changes in any of the items listed in (a) through (d) of this paragraph from the date of any such increase (which may be billed retroactively). Sales taxes collectible by Landlord under applicable law in connection with the sale or re-distribution of electricity to Tenant shall be paid by Tenant to Landlord as additional rent when billed. Any such percentage change in Landlord’s cost due to changes in costs reflected in the matters referred to in (a) through (d) above shall be computed by the application of the average consumption (energy and demand) of electricity for the entire Building for the twelve (12) full months immediately prior to the effective date of any such increase in costs or any changed methods of or rules for billing of same, on a consistent basis, to the new rate and/or service classification and/or cost to the immediately prior existing rate and/or service classification and/or cost. If the average consumption of