As filed with the Securities and Exchange Commission on November 21, 2013

|

Registration No. No. 333-180741

|

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 3

TO

FORM S-11

FOR REGISTRATION UNDER THE SECURITIES ACT OF 1933

OF SECURITIES OF CERTAIN REAL ESTATE COMPANIES

MVP REIT, INC.

(Exact Name of Registrant as Specified in its Governing Instruments)

8880 West Sunset Road, Suite 220

Las Vegas, Nevada 89148

(702) 227-0965

(Address, Including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

Michael V. Shustek

MVP REIT, Inc.

8880 West Sunset Road, Suite 220

Las Vegas, Nevada 89148

(702) 227-0965

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

Copies to:

Hillel T. Cohn

David M. Lynn

Ben Chung

Morrison & Foerster LLP

555 West Fifth Street, Suite 3500

Los Angeles, California 90013

(213) 892-5500

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box.

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering.

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box.

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act (Check One):

|

Large accelerated filer

|

Accelerated filer

|

Non-accelerated filer þ

|

Smaller reporting company

|

|||

|

(Do not check if a smaller reporting company)

|

|

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

|

This Post-Effective Amendment No. 3 consists of the following:

|

|

1.

|

The Registrant’s prospectus, dated October 7, 2013, and filed with the SEC on October 8, 2013, included herewith;

|

|

|

2.

|

Supplement No. 1 to the Registrant’s prospectus dated October 7, 2013, included herewith;

|

|

|

3.

|

Part II, included herewith; and

|

|

|

4.

|

Signatures, included herewith.

|

The Company is filing this post-effective amendment pursuant to its undertaking under Item 20.D of the SEC’s Industry Guide 5.

The Company has also updated its undertaking set forth in Part II, Item 37, paragraph 4 of this post-effective amendment to its Registration Statement on Form S-11 in accordance with the SEC staff's guidance set forth in the SEC CF Disclosure Guidance: Topic No. 6 - Staff Observations Regarding Disclosures of Non-Traded Real Estate Investment Trusts.

Filed Pursuant to Rule 424(b)(4)

Registration No. 333-180741

PROSPECTUS

MVP REIT, INC.

$550,000,000 Maximum Offering

MVP REIT, Inc. is a Maryland corporation that intends to invest in a diversified portfolio of real estate secured loans and direct investments in real estate. We will focus primarily on investments in commercial real estate and loans secured by commercial real estate located throughout the United States. Based on current market conditions and other factors, we have decided that a significant focus of our investment strategy will be on self-storage facilities and parking facilities, including parking lots, parking garages and other parking structures. We may also acquire or invest in other commercial properties such as office buildings. We intend to qualify as a REIT for federal income tax purposes for the tax year ended December 31, 2013.

We are offering up to $500,000,000 in shares of our common stock, $0.001 par value per share, to the public at $9.00 per share. We are also offering up to $50,000,000 in shares of common stock pursuant to our distribution reinvestment plan at an initial price of $8.73 per share. We expect to offer shares of common stock in our primary offering until September 25, 2014, unless extended by our board of directors to September 25, 2015, in states that permit us to make this extension.

We are an “emerging growth company” under the federal securities laws and will be subject to reduced public company reporting requirements. Investing in our common stock is speculative and involves a high degree of risk. You should purchase these securities only if you can afford a complete loss of your investment. See “Risk Factors” beginning on page 23 to read about the more significant risks you should consider before buying shares of our common stock. These risks include the following:

|

•

|

We have a limited operating history, having commenced operations in December 2012.

|

||

|

•

|

Although we have acquired several properties and identified others we intend to acquire, we are effectively a “blind pool” because we have not identified, and you will not be able to evaluate, any additional investments we will make with proceeds from this offering.

|

||

|

•

|

This is a “best efforts” offering, and if we are unable to raise substantial funds then we may not be able to diversify our investments.

|

||

|

•

|

We depend upon our advisor and its affiliates to conduct our operations.

|

||

|

•

|

Our business strategy involves substantial risk as many of our investments are expected to be in real estate markets that have suffered significant declines in values over the last several years and we may seek to acquire loans made to higher risk borrowers.

|

||

|

•

|

There is no public trading market for our shares and we are not required to list or liquidate by a certain date or at all. Accordingly, our shares will lack liquidity and you may have to hold the investment indefinitely.

|

|

•

|

There are restrictions on your ability to have your shares repurchased under our share repurchase program.

|

||

|

•

|

There are substantial conflicts of interest between us and our advisor and its affiliates.

|

||

|

•

|

We may not be able to make distributions on a monthly basis and may pay distributions from sources other than cash flow from operations, including the sale of assets, borrowings or offering proceeds. We have no limits on the amounts we may pay from such sources. If we pay distributions from sources other than our cash flow from operations, the funds available to us for investments would be reduced and your share value may be diluted.

|

||

|

•

|

We may incur substantial debt, which will increase our risk and may reduce our distributions.

|

||

|

•

|

Failure to qualify as a REIT would adversely affect our ability to make distributions to our stockholders.

|

Neither the Securities Exchange Commission, the Attorney General of the State of New York nor any other state securities regulator has approved or disapproved of our common stock, determined if this prospectus is truthful or complete or passed on or endorsed the merits of this offering. Any representation to the contrary is a criminal offense. This prospectus is not an offer to sell our common stock and we are not soliciting an offer to buy our common stock in any state where the offer or sale is not permitted.

The use of projections or forecasts in this offering is prohibited. No one is authorized to make any oral or written predictions about the cash benefits or tax consequences you will receive from your investment in our shares.

|

Price To Public

|

Selling

Commissions(1)

|

Net Proceeds

(Before

Expenses)(2)

|

||||||||||

|

Primary Offering Per Share

|

$

|

9.00

|

$

|

0.27

|

$

|

8.73

|

||||||

|

Maximum Offering

|

$

|

500,000,000

|

$

|

15,000,000

|

$

|

485,000,000

|

||||||

|

Distribution Reinvestment Plan Per Share

|

$

|

8.73

|

—

|

$

|

8.73

|

|||||||

|

Total Maximum for Distribution Reinvestment Plan

|

$

|

50,000,000

|

—

|

$

|

50,000,000

|

|||||||

|

Total Maximum Offering (Primary and Distribution Reinvestment Plan)

|

$

|

550,000,000

|

$

|

15,000,000

|

$

|

535,000,000

|

||||||

|

(1)

|

Discounts are available to certain categories of purchasers.

|

|

(2)

|

Proceeds are calculated before deducting issuer costs other than selling commissions. These issuer costs consist of, among others, expenses of our organization, due diligence expenses, legal, accounting, printing, filing fees, escrow fees, and other offering-related expenses.

|

The date of this prospectus is October 7, 2013

TABLE OF CONTENTS

SUITABILITY STANDARDS

The shares of common stock we are offering are suitable only as a long-term investment for persons of adequate financial means. We do not expect to have a public market for shares of our common stock, which means that it may be difficult for you to sell your shares. On a limited basis, you may be able to have shares of our common stock repurchased through our share repurchase program, and in the future we may also consider various forms of additional liquidity. You should not buy shares of our common stock if you need to sell them immediately or if you will need to sell them quickly in the future.

In consideration of these factors, we have established suitability standards for initial stockholders and subsequent transferees. These suitability standards require that a purchaser of shares of our common stock have either:

|

•

|

a net worth (excluding the value of an investor’s home, furnishings and automobiles) of at least $250,000; or

|

||

|

•

|

a gross annual income of at least $70,000 and a net worth (excluding the value of an investor’s home, furnishings and automobiles) of at least $70,000; and

|

||

|

•

|

a net worth (excluding the value of an investor’s home, furnishings and automobiles) of at least ten times their investment in us and similar programs.

|

Certain states have established suitability requirements that may be in addition to or vary from the minimum standards described above. Shares will be sold only to investors in these states who meet the special suitability standards set forth below. Although we have listed the suitability requirements of certain states below, we will only offer to sell our common stock in these states if and when the offer or sale is permitted in such states, and we are not making an offer of our common stock in any state where the offer is not permitted.

California: Investors must have either (i) a net worth of at least $250,000, or (ii) a gross annual income of at least $75,000 and a net worth of at least $75,000.

Iowa: Investors must have (excluding the value of their home, furnishings and automobiles) either (i) a minimum net worth of $100,000 and an annual income of $70,000, or (ii) a minimum net worth of $350,000. In addition, investors may not invest, in the aggregate, more than 10% of their liquid net worth in us and all of our affiliates. “Liquid net worth” is defined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities.

Kentucky, Michigan, Oregon, and Pennsylvania: Investors must have a liquid net worth of at least ten (10) times their investment in us.

Maine: The Maine Office of Securities recommends that an investor’s aggregate investment in this offering and similar offerings not exceed 10% of the investor’s liquid net worth. For this purpose, “liquid net worth” is defined as that portion of net worth that consists of cash, cash equivalents and readily marketable securities.

Nevada: Investors must have (excluding the value of their home, furnishings and automobiles) either: (i) a minimum net worth of $75,000 and an annual income of $75,000, or (ii) a minimum net worth of $500,000. In addition, the investment in us must not exceed 10% of the investor’s net worth (exclusive of home, furnishings and automobiles).

New Jersey: Investors who reside in the state of New Jersey must have either (i) a liquid net worth of $250,000 and annual gross income of $70,000 or (ii) a minimum liquid net worth of $500,000. Additionally, a New Jersey investor’s total investment in this offering and similar direct participation investments shall not exceed 10% of his or her liquid net worth. “Liquid net worth” is defined as that portion of net worth (total assets exclusive of home, home furnishings, and automobiles minus total liabilities) that is comprised of cash, cash equivalents, and readily marketable securities.

North Dakota: Investors must have a liquid net worth of at least ten (10) times their investment in us and our affiliates.

Ohio: Investors may not invest, in the aggregate, more than 10% of their liquid net worth in us and all of our affiliates.

Pennsylvania: Because the minimum offering of our common stock is less than $50 million, Pennsylvania investors are cautioned to evaluate carefully our ability to accomplish fully our stated objectives and to inquire as to the current dollar volume of our subscription proceeds. Notwithstanding our $3.0 million minimum offering amount for other jurisdictions, we will not sell any shares to Pennsylvania investors unless we raise a minimum of $25 million in gross offering proceeds (including sales made to residents of other jurisdictions). See “Plan of Distribution – Special Notice to Pennsylvania Investors.”

Tennessee: We will not offer to sell our common stock in Tennessee unless and until the offer and sale is permitted in such state. In addition, investors must have (excluding the value of their home, home furnishings and automobile) either (i) a minimum annual gross income of $100,000 and a minimum net worth of $100,000, or (ii) a minimum net worth of $500,000. In addition, because the minimum offering of our common stock is less than $50 million, Tennessee investors are cautioned to evaluate carefully our ability to accomplish fully our stated objectives and to inquire as to the current dollar volume of our subscription proceeds. Notwithstanding our $3.0 million minimum offering amount for other jurisdictions, we will not sell any shares to Tennessee investors unless we raise a minimum of $10 million in gross offering proceeds (including sales made to residents of other jurisdictions). See “Plan of Distribution – Special Notice to Tennessee Investors.”

Our sponsor and each participating broker-dealer are responsible for determining if investors meet our minimum suitability standards and state specific suitability standards for investing in our common stock. In making this determination, our sponsor will rely on the participating broker-dealers and/or information provided by investors. In addition to the minimum suitability standards described above, each participating broker-dealer, authorized representative or any other person selling shares on our behalf, and our sponsor, is required to make every reasonable effort to determine that the purchase of shares is a suitable and appropriate investment for each investor.

It shall be the responsibility of your participating broker-dealer, authorized representative or other person selling shares on our behalf to make this determination, based on a review of the information provided by you, including your age, investment objectives, income, net worth, financial situation and other investments held by you, and consider whether you:

|

•

|

meet the minimum income and net worth standards established in your state;

|

|||||

|

•

|

can reasonably benefit from an investment in shares of our common stock based on your overall investment objectives and portfolio structure;

|

|||||

|

•

|

are able to bear the economic risk of the investment based on your net worth and overall financial situation; and

|

|||||

|

•

|

have apparent understanding of:

|

|||||

|

•

|

the fundamental risks of an investment in shares of our common stock;

|

|||||

|

•

|

the risk that you may lose your entire investment;

|

|||||

|

•

|

the lack of liquidity of shares of our common stock;

|

|||||

|

•

|

the restrictions on transferability of shares of our common stock;

|

|||||

|

•

|

the background and qualifications of our advisor; and

|

|||||

|

•

|

the tax, including ERISA, consequences of an investment in shares of our common stock.

|

|||||

Your participating broker-dealer, authorized representative or other person selling shares on our behalf must maintain records for at least six years of the information used to determine that an investment in the shares is suitable and appropriate for each investor.

HOW TO SUBSCRIBE

Subscription Procedures

Investors seeking to purchase shares of our common stock who meet the suitability standards described herein should proceed as follows:

|

•

|

Read this entire prospectus and any supplements accompanying this prospectus.

|

||

|

•

|

Complete the execution copy of the subscription agreement. A specimen copy of the subscription agreement, including instructions for completing it, is included in this prospectus as Appendix A.

|

||

|

•

|

Deliver a check for the full purchase price of the shares of our common stock being subscribed for along with the completed subscription agreement to the soliciting broker-dealer. Your check should be made payable to “MVP REIT, Inc.”

|

By executing the subscription agreement and paying the total purchase price for the shares of our common stock subscribed for, each investor agrees to be bound by all of its terms and attests that the investor meets the minimum income and net worth standards as described herein. Subscriptions will be effective only upon our acceptance, and we reserve the right to reject any subscription in whole or in part. Subscriptions will be accepted or rejected within 30 days of receipt by us, and if rejected, all funds will be returned to subscribers without interest and without deduction for any expenses within 10 business days from the date the subscription is rejected. We are not permitted to accept a subscription for shares of our common stock until at least five business days after the date you receive the final prospectus.

An approved trustee or custodian must process and forward to us subscriptions made through IRAs, Keogh plans and 401(k) plans. In the case of investments through IRAs, Keogh plans and 401(k) plans, we will send the confirmation and notice of our acceptance to the trustee.

Minimum Purchase Requirements

You must initially invest at least $4,500 in shares of our common stock, or 500 shares at the offering price of $9.00 a share, to be eligible to participate in this offering, except for IRAs and other qualified retirement plans, which must purchase a minimum of $1,350, or 150 shares at the offering price of $9.00 per share. You should note that an investment in shares of our common stock will not, in itself, create a retirement plan and that, in order to create a retirement plan, you must comply with all applicable provisions of the Internal Revenue Code of 1986, as amended, and the regulations promulgated thereunder, or the Code. If you have satisfied the applicable minimum purchase requirement, any additional purchase must be in amounts of at least $900, or 100 shares at the offering price of $9.00 per share, except for shares purchased pursuant to our distribution reinvestment plan.

Determination of Suitability

In determining suitability, participating broker-dealers who sell shares on our behalf may rely on, among other things, relevant information provided by the prospective investors. Each prospective investor should be aware that participating broker-dealers are responsible for determining suitability and will be relying on the information provided by prospective investors in making this determination. In making this determination, participating broker-dealers have a responsibility to ascertain that each prospective investor:

|

•

|

meets the minimum income and net worth standards set forth under the “Suitability Standards” section of this prospectus;

|

||

|

•

|

can reasonably benefit from an investment in shares of our common stock based on the prospective investor’s investment objectives and overall portfolio structure;

|

||

|

•

|

is able to bear the economic risk of the investment based on the prospective investor’s net worth and overall financial situation; and

|

|

•

|

has apparent understanding of:

|

|||||

|

•

|

the fundamental risks of an investment in shares of our common stock;

|

|||||

|

•

|

the risk that the prospective investor may lose his or her entire investment;

|

|||||

|

•

|

the lack of liquidity of shares of our common stock;

|

|||||

|

•

|

the restrictions on transferability of shares of our common stock;

|

|||||

|

•

|

the background and qualifications of our advisor; and

|

|||||

|

•

|

the tax consequences of an investment in shares of our common stock.

|

|||||

Participating broker-dealers are responsible for making the determinations set forth above based upon information relating to each prospective investor concerning his age, investment objectives, investment experience, income, net worth, financial situation and other investments of the prospective investor, as well as other pertinent factors. Each participating broker-dealer is required to maintain records of the information used to determine that an investment in shares is suitable and appropriate for an investor. These records are required to be maintained for a period of at least six years.

IMPORTANT INFORMATION ABOUT THIS PROSPECTUS

Please carefully read the information in this prospectus and any accompanying prospectus supplements, which we refer to collectively as the prospectus. You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. This prospectus may only be used where it is legal to sell these securities. You should not assume that the information contained in this prospectus is accurate as of any date later than the date hereof or such other dates as are stated herein or as of the respective dates of any documents or other information incorporated herein by reference.

This prospectus is part of a registration statement that we filed with the Securities and Exchange Commission, or the SEC, using a continuous offering process. Periodically, as we make material investments or have other material developments, we will provide a prospectus supplement that may add, update or change information contained in this prospectus. Any statement that we make in this prospectus will be modified or superseded by any inconsistent statement made by us in a subsequent prospectus supplement. The registration statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this prospectus. You should read this prospectus and the related exhibits filed with the SEC and any prospectus supplement, together with additional information described herein under “Additional Information.”

The registration statement containing this prospectus, including exhibits to the registration statement, provides additional information about us and the securities offered under this prospectus. The registration statement can be read at the SEC website, www.sec.gov, or at the SEC public reference room mentioned under the heading “Additional Information.”

QUESTIONS AND ANSWERS ABOUT THIS OFFERING

The following questions and answers about this offering highlight material information regarding us and this offering that is not otherwise addressed in the “Prospectus Summary” section of this prospectus. You should read this entire prospectus, including the section entitled “Risk Factors,” before deciding to purchase shares of our common stock.

|

Q:

|

What is MVP REIT, Inc.?

|

|

A:

|

MVP REIT, Inc. is a Maryland corporation incorporated in April 2012 as a hybrid real estate investment trust to invest in a diversified portfolio of real estate secured loans and real property. We will invest primarily in commercial real estate and loans secured by commercial real estate located throughout the United States. In addition, through one or more taxable REIT subsidiaries, we may invest in companies that manage real estate or mortgage investment programs. The use of the terms “MVP REIT, Inc.,” the “company,” “we,” “us” or “our” in this prospectus refer to MVP REIT, Inc. unless the context indicates otherwise.

|

|

Q:

|

What is a real estate investment trust, or REIT?

|

|||

|

A:

|

In general, a REIT is an entity that:

|

|||

|

•

|

combines the capital of many investors to acquire or provide financing for a diversified portfolio of real estate investments under professional management;

|

|||

|

•

|

is able to qualify as a “real estate investment trust” for U.S. federal income tax purposes and, therefore, generally is not subject to federal corporate income taxes on its net income or gains distributed to stockholders, substantially eliminating the “double taxation” (i.e., taxation at both the corporate and stockholder levels) that generally results from investments in a corporation; and

|

|||

|

•

|

pays distributions to investors of at least 90% of its annual REIT taxable income.

|

|||

In this prospectus, we refer to an entity that qualifies to be taxed as a real estate investment trust for U.S. federal income tax purposes as a REIT. We do not currently qualify as a REIT. However, we intend to elect treatment, and to qualify, as a REIT for U.S. federal income tax purposes commencing with our taxable year ending December 31, 2013.

REITs generally fall into three categories: equity REITs, mortgage REITs, and hybrid REITs. Equity REITs generally own and operate income-producing real estate. Mortgage REITs generally provide money to real estate owners and operators either directly in the form of mortgages or other types of real estate loans, or indirectly through the acquisition of mortgage-backed securities. Hybrid REITs generally are companies that use the investment strategies of both equity REITs and mortgage REITs. As a hybrid REIT, we seek to generate income from rent and capital gains, like an equity REIT, as well as interest, like a mortgage REIT.

|

Q:

|

Do you currently own any assets?

|

|

A:

|

Yes. As of July 31, 2013, we owned the following properties. A self-storage facility in Cedar Park, Texas containing 52,000 interior rentable square feet, comprising of 12 buildings and 376 self-storage units, together with 24 exterior RV parking spaces. A two story, 22,000 square foot office building located in Las Vegas, Nevada. A three story, 47,500 square foot office building located in Las Vegas, Nevada. A one-third interest in a 0.75 acre parking facility located in downtown Ft. Lauderdale, Florida.

|

We have identified several additional parking facilities and office buildings which we are in the process of acquiring. However, this offering should be viewed as a “blind pool” to the extent that we have not yet identified any additional specific real estate-related assets to acquire using the proceeds from this offering. We discuss the risks associated with this status under “Risk Factors.”

|

Q:

|

Will the distributions I receive be taxable?

|

|

A:

|

Distributions that you receive, including distributions that are reinvested pursuant to our distribution reinvestment plan, generally will be taxed as ordinary dividend income to the extent they are paid out of our current or accumulated earnings and profits. However, if we recognize a long-term capital gain upon the sale of one of our assets, a corresponding portion of our dividends may be designated and treated in your hands as a long-term capital gain. In addition, we expect that some portion of your distributions may not be subject to tax in the year received due to the fact that depreciation expense reduces earnings and profits but does not reduce cash available for distribution. Amounts distributed to you in excess of our earnings and profits will reduce the tax basis of your investment and will not be taxable to the extent thereof, and distributions in excess of tax basis will be taxable as an amount realized from the sale of your shares of common stock. We discuss the taxation of our distributions in greater detail below under “Material U.S. Federal Income Tax Considerations”.

|

|

Q:

|

Who will choose which investments you make?

|

|||

|

A:

|

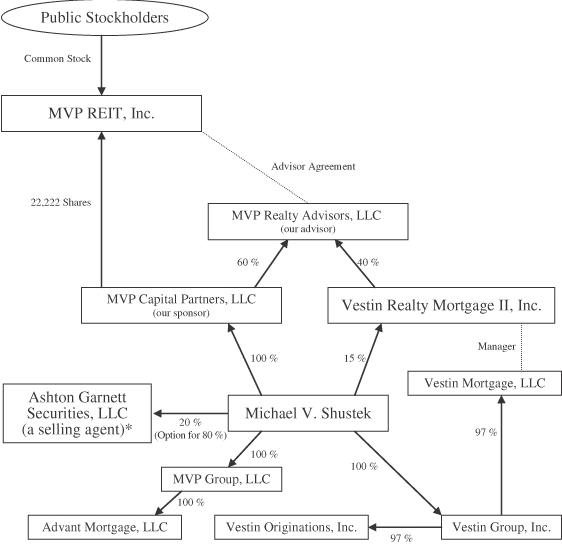

We are externally managed by MVP Realty Advisors, LLC, or our advisor. The principal of our advisor is Michael V. Shustek. Most of our advisor’s employees are associated with Vestin Mortgage, LLC, a company which manages two Nasdaq-listed companies engaged primarily in the business of investing in loans secured by commercial real estate. Our advisor will make recommendations for all of our investment decisions, which are subject to the approval of our board of directors. For additional information about the key personnel of our advisor, see the section of this prospectus captioned “Management — The Advisor.” For information about the experience of affiliates of our advisor, see the section of this prospectus captioned “Prior Performance Summary.”

|

|||

|

Q:

|

Why should I invest in a company that is focused on commercial real estate and commercial real estate secured loans?

|

|||

|

A:

|

We believe that the absence of many historical sources of debt financing for the commercial real estate market, resulting from continued uncertain economic conditions in certain markets, has and will continue to create a favorable environment for experienced commercial real estate lenders to produce attractive, risk-adjusted returns employing little or no leverage in the near term. The de-leveraging and risk assessment taking place among the large institutional banks and traditional credit providers, as well as disruptions in the market for securitized vehicles as a means of financing, has, in many cases, left real estate owners with very limited options for obtaining debt financing for acquisitions and re-financings. As a result, we believe the terms and structure of real estate secured loans have become much more favorable for lenders. At the same time, as part of this overall de-leveraging, we expect that portfolios of existing loans and debt instruments secured by real estate will continue to be offered for sale by banks and other institutions at discounts to par value and in some cases with relatively attractive seller financing. In addition, many owners of real estate face maturities on loans that have been syndicated or securitized or both, and may have difficulty due to the loan structure and servicing standards, in obtaining an extension even for performing, stabilized assets.

|

|||

|

Q:

|

Who might benefit from an investment in our shares?

|

|||

|

A:

|

An investment in our shares may be beneficial for you if you meet the minimum suitability standards described in this prospectus, seek to diversify your personal portfolio with a REIT investment focused on commercial real estate secured loans and investments in commercial real estate, seek to receive current income and are able to hold your investment indefinitely as there is no set listing or liquidation date. On the other hand, we caution persons who require immediate liquidity or who seek a short-term investment, that an investment in our shares will not meet those needs. In addition, our shares are not appropriate for investors seeking guaranteed protection of their principal or fixed, periodic distributions on their investment.

|

|||

|

Q:

|

How does a “best efforts” offering work?

|

|||

|

A:

|

When shares of common stock are offered to the public on a “best efforts” basis, the broker-dealers participating in the offering are only required to use their best efforts to sell the shares of our common stock. Broker-dealers do not have a firm commitment or obligation to purchase any of the shares of our common stock.

|

|||

|

Q:

|

Who can buy shares?

|

|||

|

A:

|

Generally, you may purchase shares if you have either:

|

|||

|

•

|

a minimum net worth (excluding the value of an investor’s home, furnishings and personal automobiles) of at least $70,000 and a minimum annual gross income of at least $70,000; or

|

|||

|

•

|

a minimum net worth (excluding the value of an investor’s home, furnishings and personal automobiles) of at least $250,000; and

|

|||

|

•

|

a net worth (excluding the value of an investor’s home, furnishings and personal automobiles) of at least ten times their investment in us and similar programs. However, these minimum levels vary from state to state, so you should carefully read the suitability requirements explained in the “Suitability Standards” section of this prospectus.

|

|||

|

Q:

|

How do I subscribe for shares of common stock?

|

|||

|

A:

|

Investors who meet the suitability standards described herein may purchase shares of our common stock. See “Suitability Standards.” Investors seeking to purchase shares of our common stock should proceed as follows:

|

|||

|

•

|

Read this entire prospectus and any appendices and supplements accompanying this prospectus.

|

|||

|

•

|

Complete the execution copy of the subscription agreement. A specimen copy of the subscription agreement, including instructions for completing it, is included in this prospectus as Appendix A.

|

|||

|

•

|

Deliver a check for the full purchase price of the shares of our common stock being subscribed for along with the completed subscription agreement to the registered broker-dealer or investment advisor. Your check should be made payable to “MVP REIT, Inc.”

|

|||

By executing the subscription agreement and paying the total purchase price for the shares of our common stock subscribed for, each investor represents that he meets the suitability standards as stated in the subscription agreement and agrees to be bound by all of its terms.

Subscriptions will be effective only upon our acceptance, and we reserve the right to reject any subscription in whole or part. Subscriptions will be accepted or rejected within 30 days of receipt by us and, if rejected, all funds shall be returned to subscribers without deduction for any expenses within 10 business days from the date the subscription is rejected. We will send purchase confirmation and notice of our acceptance if we accept a subscription to all subscribers. We are not permitted to accept a subscription for shares of our common stock until at least five business days after the date you receive the final prospectus. An approved trustee or custodian must process and forward to us subscriptions made through individual IRAs, Keough plans and 401(k) plans. In the case of investments through IRAs, Keough plans and 401(k) plans, we will send the confirmation and notice of our acceptance to the trustee or custodian.

|

Q:

|

If I buy shares, will I receive distributions and how often?

|

|

A:

|

We have adopted a distribution policy which provides for paying distributions on a monthly basis to our stockholders. Our first distribution payment was paid on February 11, 2013 to stockholders of record as of January 24, 2013. To date, such distributions have been paid from our capital contributions. We cannot predict when, if ever, we will generate sufficient cash flow to pay distributions from cash flow. We may pay distributions from sources other than cash flow from operations, including the sale of assets, borrowings or offering proceeds. We have no limits on the amounts we may pay from such sources. If we pay distributions from sources other than our cash flow from operations, the funds available to us for investments would be reduced and your share value may be diluted. We may be forced to cease paying distributions if our cash flow and other resources are insufficient to sustain such payments.

|

|

Q:

|

Will I receive a stock certificate?

|

|

A:

|

No. You will not receive a stock certificate unless expressly authorized by our board of directors. We anticipate that all shares of our common stock will be issued in book-entry form only. The use of book-entry registration protects against loss, theft or destruction of stock certificates and reduces the offering costs.

|

|

Q:

|

Is there any minimum initial investment required?

|

|

A:

|

Yes. You must initially invest at least $4,500 in shares of our common stock, or 500 shares at the offering price of $9.00 per share, except for IRAs and other qualified retirement plans, which must purchase a minimum of $1,350, or 150 shares at the offering price of $9.00 per share. After you have satisfied the minimum investment requirement, any additional purchases must be in increments of at least $900, or 100 shares at the offering price of $9.00 per share. The investment minimum for subsequent purchases does not apply to shares purchased pursuant to our distribution reinvestment plan.

|

|

Q:

|

Can I buy shares at a discount?

|

|

A:

|

A participating broker dealer may offer a qualifying purchaser who purchases more than $200,000 of our shares a volume discount by reducing the amount of its sales commission. The reduction varies from one-half percent (0.50%) to two and one-half percent (2.50%) depending upon the number of shares purchased, as specified under the “Plan of Distribution — Special Discounts.”

|

Our officers and directors and their family members, as well as officers and employees of our advisor and our advisor’s affiliates and their family members, at their option, also may purchase the shares offered hereby at a 3% discount, or at $8.73 per share, reflecting that selling commission will not be paid in connection with such sales.

We may sell shares to participating broker-dealers, their retirement plans, their representatives and the family members as described above, IRAs and qualified plans of their representatives at a purchase price of $8.73 per share, reflecting that selling commissions in the amount of $0.27 per share will not be payable in consideration of the services rendered by such broker-dealers and representatives in the offering.

The net proceeds to us from any of the foregoing sales of our shares will be the same as the net proceeds we receive from other sales of shares without a discount.

|

Q:

|

What will you do with the proceeds from your offering?

|

|

A:

|

We expect to use substantially all of the net proceeds from this offering to invest in a diversified portfolio of real estate secured loans and direct investments in real estate. We will focus primarily on investments in commercial real estate and loans secured by commercial real estate located throughout the United States. We expect to use substantially all of the net proceeds from this offering to acquire: (i) real estate secured loans, including mezzanine loans, first and second mortgage loans, subordinated mortgage loans, bridge loans, variable interest rate real estate secured loans where a portion of the return is dependent upon performance-based metrics and other loans secured by real estate; and (ii) real property that meets our investment objectives. Based on current market conditions and other factors, we have decided that a significant focus of our investment strategy will be on self-storage facilities and parking facilities, including parking lots, parking garages and other parking structures. We will also acquire or invest in other commercial properties such as office buildings.

|

In addition, until we have generated sufficient cash flow from operations, we may pay distributions from other sources, including offering proceeds, borrowings or sales of assets. We have no limits on the amounts we may pay from such sources. If we pay distributions from sources other than our cash flow from operations, the funds available to us for investments would be reduced and your share value may be diluted. As of the date of this prospectus, we have paid all of our distributions from proceeds from issuance of our common stock in the offering or under our distribution reinvestment plan.

We may not be able to promptly invest the net proceeds of this offering. In the interim, we may invest in short-term, highly liquid or other authorized investments. Such short-term investments are not anticipated to earn as high of a return as we expect to earn on our real estate investments. In the event we are not able to promptly invest the net proceeds of this offering, it may also be necessary for us to pay distributions from offering proceeds.

|

Q:

|

May I reinvest my distributions?

|

|

A:

|

Yes. Please see “Description of Capital Stock” for more information regarding our distribution reinvestment plan.

|

|

Q:

|

If I buy shares of common stock in this offering, how may I later sell them?

|

|

A:

|

There is no public trading market for our shares and we have no current intention to list our shares on any national securities exchange in the near future. As a result, if you wish to sell your shares, you may not be able to do so promptly, or at all, or you may only be able to sell them at a substantial discount from the price you paid. In general, although there is no current public market for the shares, you may sell your shares to any buyer that meets the applicable suitability standards. See “Suitability Standards” and “Description of Capital Stock.” We have adopted a share repurchase program, as discussed under “Description of Capital Stock,” which may provide limited liquidity for some of our stockholders.

|

|

Q:

|

What is your liquidity strategy?

|

|

A:

|

Our board of directors does not anticipate evaluating a transaction providing liquidity for our stockholders until the later of 2018 or three years after the date this offering closes. Our charter does not require our board of directors to pursue a liquidity event. Due to the uncertainties of market conditions in the future, we believe setting firm dates for possible, but uncertain, liquidity events may result in actions not necessarily in the best interests of our stockholders. We expect that our board of directors, in the exercise of its fiduciary duty to our stockholders, will determine to pursue a liquidity event when it believes that then-current market conditions are favorable for a liquidity event, and that such a transaction is in the best interests of our stockholders. A liquidity event could include (1) the sale of all or substantially all of our assets either on a portfolio basis or individually followed by a liquidation, in which the net proceeds are distributed to stockholders, (2) a merger or another transaction approved by our board of directors in which our stockholders will receive cash and/or shares of a publicly traded company or (3) a listing of our shares on a national securities exchange. There can be no assurance as to if and when a suitable liquidity transaction will be achievable.

|

|

Q:

|

Are there any special restrictions on the ownership of shares?

|

|

A:

|

Yes. Our charter, subject to certain exceptions, authorizes our board of directors to take such actions as are necessary and desirable to preserve our qualification as a REIT and limits any person to beneficial or constructive ownership of no more than a specified percentage of the number or value, whichever is more restrictive, of the outstanding shares of our stock. Specifically, our charter generally prohibits a person from beneficially or constructively owning more than 9.8% in value of the aggregate of our outstanding shares of stock or more than 9.8% in value or number of shares, whichever is more restrictive, of the aggregate of our outstanding common stock, unless waived by the board of directors. The ownership limit may have the effect of precluding a change in control of us by a third party, even if such change in control would be in the best interests of our stockholders (and even if such change in control would not reasonably jeopardize our REIT status).

|

|

Q:

|

What is the status of this offering and how many shares do you currently have outstanding?

|

|

A:

|

On September 25, 2012, we commenced this offering of up to $550,000,000 in shares of our common stock, including up to $50,000,000 in shares of our common stock being offered pursuant to our distribution reinvestment plan, in each case, at an initial purchase price of $9.00 per share. On December 12, 2012, we received gross offering proceeds of approximately $4.1 million, which was sufficient to satisfy the minimum offering amounts in all states where we are conducting or planning to conduct this offering except Pennsylvania and Tennessee. Accordingly, we have broken escrow with respect to subscriptions received from all states where we are conducting or planning to conduct this offering except Pennsylvania, which has a minimum offering amount of $25.0 million, and Tennessee, which has a minimum offering amount of $10.0 million. We will not offer to sell our shares in Tennessee unless and until the offer and sale is permitted in such state.

|

As of June 30, 2013, we have approximately 835,082 shares of common stock issued and outstanding and our stockholders’ equity was approximately $7.2 million.

|

Q:

|

How long will this offering last?

|

|||

|

A:

|

We currently expect that this offering will terminate on September 25, 2014 (two years after the initial effective date of the registration statement of which this prospectus is a part with a possible extension of one year with the permission of the SEC). Once we have met the minimum offering requirements, we could in some circumstances seek to continue our primary offering in accordance with SEC requirements until as late as September 25, 2015 (approximately three years after the initial effective date of this offering). If we decide to continue our primary offering beyond two years from the date of this prospectus, we will provide that information in a prospectus supplement. In certain states, this offering may continue for just one year unless we are able to renew the offering period in such states. In addition, we reserve the right to terminate this offering for any other reason at any time.

|

|||

|

Q:

|

What are some of the risks involved in investing in this offering?

|

|||

|

A:

|

Investing in our common stock involves a high degree of risk. You should carefully review the “Risk Factors” section of this prospectus, beginning on page 23, which contains a detailed discussion of the material risks that you should consider before you invest in shares of our common stock. Some of the more significant risks relating to an investment in our shares include:

|

|||

|

•

|

We have a limited operating history having commenced operations in December 2012.

|

|||

|

•

|

Although we have acquired several properties and identified others we intend to acquire, this offering should be viewed as effectively a “blind pool” because we have not identified, most of the properties we would acquire with proceeds from this offering and you will have no opportunity to evaluate such properties.

|

|||

|

•

|

This is a “best efforts” offering, and if we are unable to raise substantial funds then we may not be able to acquire a diverse portfolio of investments and the value of your shares may vary more widely with the performance of specific assets.

|

|||

|

•

|

Our business strategy involves substantial risk as many of our investments are expected to be in real estate markets that have suffered significant declines in values over the last several years and we may seek to acquire loans made to higher risk borrowers.

|

|||

|

•

|

We set the offering price of our shares arbitrarily. This offering price is unrelated to the book or net value of our assets or to our expected operating income and may be significantly in excess of share value at the time of investment because the offering price was set arbitrarily.

|

|||

|

•

|

There is no public trading market for our shares, we have no current intention to list our shares on any national securities exchange in the near future and there is no requirement to ever list or liquidate. Accordingly, our shares will lack liquidity.

|

|||

|

•

|

There are restrictions and limitations on your ability to have all or any portion of your shares of our common stock repurchased under our share repurchase program and, if you are able to have your shares repurchased, it may be at a price that is less than the price you paid for the shares.

|

|||

|

•

|

We may change our targeted investments and investment guidelines without stockholder consent, which could result in investments that are different from those described in this prospectus.

|

|||

|

•

|

We may not be able to make distributions on a monthly basis. Moreover, our distributions may exceed our earnings, particularly during the period before we have substantially invested the net proceeds from this offering. Therefore, portions of the distributions that we make may represent a return of capital to you, which will lower your tax basis in our shares. If we pay distributions from sources other than our cash flow from operations, we will have fewer funds available for investments and your overall return may be reduced. We have no limits on the amounts we may pay in distributions from sources other than cash flow from operations, including from the sale of assets or offering proceeds.

|

|||

|

•

|

We will be subject to risks incident to the ownership of real estate related assets including: changes in national, regional or local economic, demographic or real estate market conditions; changes in supply of, or demand for, similar properties in an area; increased competition for real estate assets targeted by our investment strategy; bankruptcies, financial difficulties or lease defaults by property owners and tenants; changes in interest rates and availability of financing; and changes in government rules, regulations and fiscal policies, including changes in tax, real estate, environmental and zoning laws.

|

|||

|

•

|

We may incur substantial debt and such leverage will increase the risk of loss on our investments and may reduce the cash available for distribution to our stockholders.

|

|||

|

•

|

We have issued 1,000 shares of convertible stock to our advisor, at a price of $1.00 per share. In general, upon the occurrence of certain events, our issued shares of convertible stock will convert into a number of shares of common stock representing three and one-half percent (3.50%) of the outstanding shares of our common stock immediately preceding the conversion. Upon such conversion, your interests in us will be diluted.

|

|||

|

•

|

If we fail to qualify as a REIT, it would adversely affect our operations and our ability to make distributions to our stockholders because we will be subject to U.S. federal income tax at regular corporate rates with no ability to deduct distributions made to our stockholders.

|

|||

|

•

|

Our success depends to a significant degree upon the contributions of Michael V. Shustek, who could be difficult to replace if he decides not to remain associated with our sponsor.

|

|||

|

•

|

Hedging against interest rate exposure may adversely affect our earnings, limit our gains or result in losses, which could adversely affect cash available for distributions to our stockholders.

|

|||

|

Q:

|

Will I be notified of how my investment is doing?

|

|||

|

A:

|

Yes, we will provide you with periodic updates on the performance of your investment in us, including:

|

|||

|

•

|

three quarterly financial reports;

|

|||

|

•

|

an annual report; and

|

|||

|

•

|

supplements to the prospectus, provided not less often than quarterly during the offering period.

|

|||

We will provide this information to you via one or more of the following methods, in our discretion and with your consent, if necessary:

|

•

|

U.S. mail or other courier;

|

|||

|

•

|

facsimile;

|

|||

|

•

|

electronic delivery, including email and/or CD-ROM; or

|

|||

|

•

|

posting, or providing a link, on our affiliated web site at.

|

|||

|

Q:

|

Will I receive annual tax information regarding distributions from you?

|

|||

|

A:

|

You will receive a Form 1099-DIV, if required, which will be mailed by January 31 of each year.

|

|||

|

Q:

|

Who can help answer my questions about the offering?

|

|

A:

|

If you have more questions about the offering, or if you would like additional copies of this prospectus, you should contact your registered representative or contact:

|

MVP Realty Advisors, LLC

8880 W. Sunset Road, Suite 240

Las Vegas, Nevada 89148

Attn: Investor Relations

(702) 534-5577

PROSPECTUS SUMMARY

This prospectus summary highlights material information regarding our business and this offering that is not otherwise addressed in the “Questions and Answers About this Offering” section of this prospectus and is contained elsewhere in this prospectus. Because it is a summary, it may not contain all of the information that is important to you. To understand this offering fully, you should read the entire prospectus carefully, including the “Risk Factors” section before making a decision to invest in our common stock. The use of the words “we,” “us” or “our” refers to MVP REIT, Inc. and our subsidiaries, except where the context otherwise requires. References to “shares” and “our common stock” refer to the shares of common stock offered in this offering.

MVP REIT, Inc.

MVP REIT, Inc. is a Maryland corporation formed as a hybrid real estate investment trust to invest in a diversified portfolio of real estate secured loans and direct investments in real estate. We will focus primarily on investments in commercial real estate and loans secured by commercial real estate located throughout the United States. We expect to use substantially all of the net proceeds from this offering to acquire: (i) real estate secured loans, including mezzanine loans, first and second mortgage loans, subordinated mortgage loans, bridge loans, performance-based variable interest rate real estate secured loans and other loans related to real estate; and (ii) direct investments in real estate that meets our investment objectives. In addition, through one or more taxable REIT subsidiaries, we may invest in companies that manage real estate or mortgage investment programs. We intend to operate in a manner that will allow us to qualify as a REIT for U.S. federal income tax purposes for the taxable year ended December 31, 2013. Among other requirements, REITs are required to satisfy certain gross income and asset tests, which may affect the composition of assets we acquire with the proceeds of this offering. In addition, REITs are required to distribute to stockholders at least 90% of their annual REIT taxable income (computed without regard to the dividends paid deduction and excluding net capital gain).

Investment Objectives

Our primary investment objective is to generate current income. We anticipate generating current income from interest payments on our real estate loans and from rent and other income from properties we acquire. We may also seek to realize growth in the value of our investments by timing their sale to maximize value. However, we cannot assure you that we will attain these objectives or that the value of our assets will not decrease. Furthermore, within our investment objectives and policies, our advisor will have substantial discretion with respect to the selection of specific investments and the purchase and sale of our assets. Our board of directors will review our investment policies at least annually to determine whether our investment policies continue to be in the best interests of our stockholders.

Investment Strategy

Over the past several years, commercial real estate markets have suffered a major disruption. This disruption included significant declines in value, unprecedented rates of default on real estate secured loans and reduced availability of credit for real estate projects. The disruption was particularly severe in certain markets, including Nevada, Arizona and certain portions of California, and the effects of the disruption generally persist in such markets.

We believe that the adverse developments in these real estate markets have created unique opportunities for investors willing to undertake the risk of acquiring properties or making real estate secured loans in such markets. For example, we believe Nevada, Arizona and inland California all continue to offer significant long term growth opportunities notwithstanding their current difficulties. However, because of the lingering effects of the recession in these markets, certain commercial properties may be under-valued and borrowers continue to face difficulties obtaining financing for their projects. We hope to profit from such opportunities by identifying undervalued properties in such markets. Our strategy inevitably involves significant risk. Real estate markets may be slow to recover and we may misjudge the potential value of a property or the reliability of a borrower. In this regard, it is important to note that most of our borrowers are likely to be higher risk borrowers who are currently unable or unwilling to obtain credit at traditional banks. Nonetheless, we believe that by undertaking measured risk and building a diversified portfolio of properties and real estate secured loans, we may be able to profit from the current situation in these real estate markets.

Our investment strategy is to invest substantially all of the net proceeds from this offering in a diverse portfolio of real estate secured loans and direct investments in real property. We will focus primarily on investments in commercial real estate and loans secured by commercial real estate located in the Western and Southwestern United States and other areas where our affiliates or correspondents have experience. We intend to acquire real estate secured loans, including mezzanine loans, first and second mortgage loans, subordinated mortgage loans, bridge loans, variable interest rate real estate secured loans where a portion of the return is dependent upon performance-based metrics and other loans secured by real estate. In addition, we may invest directly in real estate that, in the opinion of our board of directors, meets our investment objectives. We may acquire real property either alone or jointly with another party. When fully funded, we intend to be invested in approximately equal amounts as measured by the net proceeds of this offering in both real estate secured loans and direct investments in real estate.

We may, through one or more “taxable REIT subsidiaries,” invest in companies that manage real estate or mortgage investment programs. However, no more than 25% of the value of our assets may consist of stock or securities of one or more taxable REIT subsidiaries. See “Material Federal Income Tax Considerations — Subsidiary Entities — Taxable REIT Subsidiaries” below.

We may consider opportunities to acquire all of the equity interests or assets in another company whose operating assets are limited to real property and/or real estate secured loans. Any such acquisition would be pursued to expand our portfolio of real estate and real estate secured loans and will be undertaken only if we obtain control of the entity or substantially all of its assets. We will not make passive investments in other companies that are engaged in the real estate business.

Mortgage Program

The turmoil in the United States mortgage market that commenced in 2008 has diminished the availability of new loans for real estate, often regardless of the quality of the underlying property or the financial strength of the borrower. We believe that the continuing shortage of available financing creates a favorable investment environment for us. There is also an opportunity to acquire mortgage loans from distressed lenders at a discount to par, thereby taking advantage of borrower payoffs, loan restructurings and potential capital appreciation as markets normalize.

The management team of our advisor has extensive experience in evaluating, managing and disposing of real estate secured loans similar to the types of loans in which we intend to invest in. We will pursue a strategy similar to the strategy previously pursued by the management team. We will seek to:

|

•

|

invest in fixed rate rather than floating rate loans;

|

||

|

•

|

invest in loans expected to mature within one to five years;

|

||

|

•

|

maximize current income;

|

||

|

•

|

invest in loans not exceeding 75% of the current value of the underlying property;

|

||

|

•

|

provide diversification by property type, geographic location, tenancy and borrower;

|

||

|

•

|

source off-market transactions;

|

||

|

•

|

focus on small to mid-sized loans of $3 million to $15 million; and

|

||

|

•

|

hold investments until maturity unless, in our advisor’s judgment, market conditions warrant earlier disposition.

|

Our underwriting process will focus on the value of the underlying real estate that will serve as collateral on our real estate secured loans rather than the creditworthiness of the borrower. Many of our borrowers may be companies or individuals who are not able or willing to obtain loans from commercial banks or other traditional lenders. Accordingly, we will depend primarily upon our real estate collateral to protect us in the event of a loan default. We will seek to invest in loans not exceeding 75% of the current value of the underlying property to provide us with an equity cushion in the event real estate values decline. To assist us in estimating the value of the underlying property, we will utilize appraisals prepared by independent appraisers possessing the designation as a Member of the Appraisal Institute (“MAI”). Such appraisals will generally be as of a date not more than one year prior to the date of our proposed acquisition of the loan. We depend upon the skill of independent appraisers to value the security underlying our loans. However, notwithstanding the experience of the appraisers, they may make mistakes, or the value of the real estate may decrease due to subsequent events. Appraisals also may not reflect a decrease in the value of the real estate due to events subsequent to the date of the appraisals. If there is less security and a default occurs, we may not recover the full amount of our loan, thus reducing the amount of funds available to distribute to you.

Real Estate Program

The recession in the real estate market has created opportunities to acquire under-valued properties. We will focus on acquiring properties which meet the following criteria:

|

•

|

properties that generate current cash flow;

|

||

|

•

|

multi-tenant properties that are not dependent upon a single tenant, such as apartment buildings, self-storage facilities and parking lots;

|

||

|

•

|

properties located in markets with growth potential;

|

||

|

•

|

we will not invest in undeveloped land;

|

||

|

•

|

while we may acquire properties that require renovation, we will only do so if we anticipate the properties will be income producing within 12 months of our acquisition; and

|

||

|

•

|

when fully invested, no single property will exceed 5.00% of our total assets.

|

The foregoing criteria are guidelines and our advisor and board of directors may vary from these guidelines to acquire properties which they believe represent value opportunities. However, we will not acquire any undeveloped land as an investment.

Borrowing Policy

We intend to employ conservative levels of borrowing in order to provide more funds available for investment. Our intended targeted debt level is no more than 50% of the loan to value of our portfolio of assets. Our charter precludes us from borrowing more than the North American Securities Administrators Association’s Statement of Policy Regarding Real Estate Investment Trusts, as revised and adopted on May 7, 2007, which we refer to as the NASAA REIT Guidelines, limit of 300% of our net assets, unless a majority of our independent directors approve any borrowing in excess of 300% of our net assets and the justification for such excess borrowing is disclosed to our stockholders in our next quarterly report. Net assets for purposes of this calculation are defined to be our total assets (other than intangibles), valued at cost prior to deducting depreciation, reserves for bad debts and other non-cash reserves, less total liabilities. The preceding calculation is generally expected to approximate 75% of the aggregate cost of our assets before non-cash reserves and depreciation. We may borrow in excess of these amounts if such excess is approved by a majority of the independent directors and disclosed to stockholders in our next quarterly report, along with an explanation for such excess. In such event, we will review our debt levels at that time and take action to reduce any such excess as soon as practicable. We do not intend to exceed our charter’s leverage limit except in the early stages of our operations when the costs of our investments are most likely to exceed our net offering proceeds. Our aggregate borrowings, secured and unsecured, will be reviewed by the board of directors at least quarterly.

Summary of Risk Factors

Investing in our common stock involves a high degree of risk. You should carefully review the “Risk Factors” section of this prospectus, beginning on page 23, which contains a detailed discussion of the material risks that you should consider before you invest in shares of our common stock. Some of the more significant risks relating to an investment in our shares include:

|

•

|

We have a limited operating history having commenced operations in December 2012.

|

|||

|

•

|

Although we have acquired several properties and identified others we intend to acquire, this offering should be viewed as effectively a “blind pool” because we have not identified, most of the properties we would acquire with proceeds from this offering and you will have no opportunity to evaluate such properties.

|

|||

|

•

|

This is a “best efforts” offering, and if we are unable to raise substantial funds then we may not be able to acquire a diverse portfolio of investments and the value of your shares may vary more widely with the performance of specific assets.

|

|||

|

•

|

Our business strategy involves substantial risk as many of our investments are expected to be in real estate markets that have suffered significant declines in values over the last several years and we may seek to acquire loans made to higher risk borrowers.

|

|||

|

•

|

We set the offering price of our shares arbitrarily. This offering price is unrelated to the book or net value of our assets or to our expected operating income and may be significantly in excess of share value at the time of investment because the offering price was set arbitrarily.

|

|||

|

•

|

There is no public trading market for our shares, we have no current intention to list our shares on any national securities exchange in the near future and there is no requirement to ever list or liquidate. Accordingly, our shares will lack liquidity.

|

|||

|

•

|

There are restrictions and limitations on your ability to have all or any portion of your shares of our common stock repurchased under our share repurchase program and, if you are able to have your shares repurchased, it may be at a price that is less than the price you paid for the shares.

|

|||

|

•

|

We may change our targeted investments and investment guidelines without stockholder consent, which could result in investments that are different from those described in this prospectus.

|

|||

|

•

|

We may not be able to make distributions on a monthly basis. Moreover, our distributions may exceed our earnings, particularly during the period before we have substantially invested the net proceeds from this offering. Therefore, portions of the distributions that we make may represent a return of capital to you, which will lower your tax basis in our shares. If we pay distributions from sources other than our cash flow from operations, we will have fewer funds available for investments and your overall return may be reduced. We have no limits on the amounts we may pay in distributions from sources other than cash flow from operations, including from the sale of assets or offering proceeds.

|

|||

|

•

|

We will be subject to risks incident to the ownership of real estate related assets including: changes in national, regional or local economic, demographic or real estate market conditions; changes in supply of, or demand for, similar properties in an area; increased competition for real estate assets targeted by our investment strategy; bankruptcies, financial difficulties or lease defaults by property owners and tenants; changes in interest rates and availability of financing; and changes in government rules, regulations and fiscal policies, including changes in tax, real estate, environmental and zoning laws.

|

|||

|

•

|

We may incur substantial debt and such leverage will increase the risk of loss on our investments and may reduce the cash available for distribution to our stockholders.

|

|||

|

•

|

We have issued 1,000 shares of convertible stock to our advisor, at a price of $1.00 per share. In general, upon the occurrence of certain events, our issued shares of convertible stock will convert into a number of shares of common stock representing three and one-half percent (3.50%) of the outstanding shares of our common stock immediately preceding the conversion. Upon such conversion, your interests in us will be diluted.

|

|||

|

•

|

If we fail to qualify as a REIT, it would adversely affect our operations and our ability to make distributions to our stockholders because we will be subject to U.S. federal income tax at regular corporate rates with no ability to deduct distributions made to our stockholders.

|

||

|

•

|

Our success depends to a significant degree upon the contributions of Michael V. Shustek, who could be difficult to replace if he decides not to remain associated with our sponsor.

|

||

|

•

|

Hedging against interest rate exposure may adversely affect our earnings, limit our gains or result in losses, which could adversely affect cash available for distributions to our stockholders.

|

Conflicts of Interest

Our advisor and its affiliates will experience conflicts of interest in connection with the management of our business. Some of the material conflicts that our advisor and its affiliates will face include the following:

|

•

|

Our sponsor’s real estate, finance and securities professionals acting on behalf of our advisor must determine which investment opportunities to recommend to us and other affiliates which have investment objectives similar to this offering and are also seeking investment opportunities.

|

||

|

•

|

Our sponsor’s real estate, finance and securities professionals acting on behalf of our advisor will have to allocate their time among us, our sponsor’s business and other programs and activities in which they are involved.

|

||

|

•

|

Our advisor and its affiliates will receive fees in connection with transactions involving the purchase, origination, management and sale of our assets regardless of the quality or performance of the asset acquired or the services provided. This fee structure may cause our advisor to recommend borrowing funds in order to acquire assets or to fail to negotiate the best price for the assets we acquire.

|

||

|

•

|

The terms of the advisory agreement (including the substantial fees our advisor and its affiliates will receive thereunder) were not negotiated at arm’s length.

|

||

|

•

|

Our property manager may be an affiliate of our advisor and, as a result, may benefit from our advisor’s determination to retain our assets while our stockholders may be better served by the sale or disposition of our assets.

|

||

|

•

|

You may be more likely to sustain a loss on your investment because our sponsor does not have as strong an economic incentive to avoid losses as do sponsors who have made significant equity investments in their companies.

|

||

|

•

|