|

OMB APPROVAL

|

|

OMB Number: 3235-0570

Expires: January 31, 2017

Estimated average burden hours per response: 20.6

|

|

Investment Company Act file number

|

811-22680

|

|

Ultimus Managers Trust

|

|

(Exact name of registrant as specified in charter)

|

|

225 Pictoria Drive, Suite 450 Cincinnati, Ohio

|

45246

|

|

(Address of principal executive offices)

|

(Zip code)

|

|

Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246

|

|

(Name and address of agent for service)

|

|

Registrant's telephone number, including area code:

|

(513) 587-3400

|

|

Date of fiscal year end:

|

May 31

|

|

|

Date of reporting period:

|

May 31, 2015

|

| Item 1. | Reports to Stockholders. |

APEXcm SMALL/MID-CAP GROWTH FUND

(APSGX)

Annual Report

May 31, 2015

|

APEXcm SMALL/MID-CAP GROWTH FUND |

May 31, 2015 |

Dear APEXcm Small/Mid-Cap Growth Fund Shareholder,

APEX INVESTMENT PHILOSOPHY

We believe that the best way to provide value-added returns is to identify companies that exhibit certain favorable fundamental advantages and benefit from secular growth trends, allowing us to structure the portfolio in high-conviction areas of longer-term sustainable growth. Embedded in our portfolio construction is the recognition of companies at different stages of their growth cycle, which we designate as “stable” and “emerging” growth stocks. We are confident that having the spectrum of growth companies that are truly innovative and growing rapidly, combined with established growth companies, can provide relative stability while allowing the opportunity to drive outperformance versus our benchmark and peers over time. In addition, the SMID style provides the opportunity to invest in higher-growth companies and capture a longer period of growth as these companies mature.

FUND PERFORMANCE

The APEXcm Small/Mid-Cap Growth Fund (the “Fund”) underperformed the Fund’s benchmark, the Russell 2500TM Growth Index (the “Index”), for the 12-month period ended May 31, 2015. The Fund’s total return was 14.67% (net of fees), while the total return of the benchmark was 17.55%. While the environment has been challenging for our performance over the past year—a time period in which small-cap growth stocks outperformed mid-cap growth stocks by approximately 3%--we think our measured approach is appropriate in this more volatile setting.

MARKET ENVIRONMENT

Most domestic stock indices delivered double–digit gains in the past 12 months. The U.S. economy began to exhibit sufficient strength to allow the Federal Reserve Board (the “Fed”) to end its easing monetary policy and turn its attention to its first interest rate increase in nearly a decade. With many of the world’s economies, currencies, central banks and interest rates on very diverse paths, the advance was not consistent across sectors. Investors wrestled with the implications of a dramatic collapse of oil prices, which then punished the Energy sector, while the rapid ascent of the U.S. dollar put pressure on the earnings outlooks of many multinational firms. While these late-2014 and early-2015 macroeconomic factors hurt sectors such as Energy, Materials and Industrials, the Health Care sector delivered very strong returns that far outpaced the rest of the market. The Health Care sector was powered by a vigorous mergers and acquisitions (M&A) environment, especially within the biotechnology and specialty pharmaceutical industries.

During the first five months of 2015, the U.S. economy appeared to have hit a soft patch, restrained by an unusually harsh winter across much of the Midwest and Northeast, accompanied by a prolonged stoppage at West Coast ports, with the impact resonating in Q1 2015 as GDP output decreased to a 0.7% annualized

PORTFOLIO REVIEW

While the Index was up 17.55% for the reporting period, its performance was predominately driven by three sectors; Consumer Discretionary (up approximately 19%), Health Care (up approximately 46%), and Information Technology (up approximately 24%). These gains offset relative weakness within Financials, Materials, Consumer Staples, and Industrials, along with the dismal performance of Energy (down approximately 29%). Our portfolio structure was solid during the period as we were either equal or overweight the three best performing sectors of Health Care, Information Technology and Consumer Discretionary, which collectively added 60 basis points to the Fund’s performance versus the Index. Of equal importance was the underweight in Consumer Staples, Financials, Industrials, and Materials, which added approximately another 90 basis points to the Fund’s performance versus the Index. The Fund’s underperformance was due, in part, to our slight overweight in Energy compared to the Index, which detracted approximately 38 basis points.

Although we had strong stock selection in the Consumer Discretionary and Financials sectors, the underperformance is directly attributed to stock selection in Energy, Materials, Industrials, Health Care and Information Technology. We have noted some of the highlights below.

The Consumer Discretionary sector was a standout performer, benefitting from continued M&A activity across multiple industries. Expedia, with its acquisition of Orbitz, and Signet Jewelers acquiring Zales were cheered by investors, as these solid business models continue to deliver and add scale. PetSmart preferred the private equity path, with the intent of unlocking tremendous value in this dominant franchise. Such excellent performance was offset by unacceptable performance from Zulily. The fast growing leader in “flash sales” faced scale and distribution headwinds in maintaining the high-level growth pace. Also, Decker’s Outdoor, which manages popular footwear brands like UGGS and Teva, missed estimates and struggled with their direct-to-consumer offering. We have exited both companies given the lackluster execution.

The Financials sector contributed excess returns driven by CBRE Group, Inc. The company provides commercial real estate services and is benefitting from its ability to grow market share in an industry that is very fragmented with smaller market operators increasingly unable to compete with CBRE’s reach and service capabilities. The company also continues to benefit from increased M&A activity with its March 2015 acquisition of Johnson Controls’ Global Workplace Solutions.

The Materials sector was the Fund’s largest detractor from relative performance, as earnings prospects for most Materials sector companies diminished with the rising U.S. dollar and signs of global, especially Chinese, economic deterioration. Although

The Energy sector also detracted from performance. Energy was the only segment of the market to post negative absolute returns in the past 12 months. Although less than 5% of our holdings, we were not immune to the carnage as oil prices declined dramatically. Significant selloffs occurred in companies that support our U.S. energy independence theme, as seen with oil service companies possessing next generation technology, as well as in oil exploration companies that have key geological assets in fast growing energy regions. Our holdings in key strategic companies such as Whiting Petroleum and Helmerich & Payne underperformed the sector. With the oil rig count down approximately 50% and a slowing domestic oil supply, we proceeded with exiting the positions. We maintained positions in Carrizo Oil & Gas, favoring their key reserves in the Eagle Ford area and the low transport costs to the gulf, as well as Core Labs with their diversified business focused on reservoir monitoring and services.

The Industrials sector also detracted from relative performance. We lowered our exposure in this multifaceted sector, as companies within global-oriented industries and those tied to energy infrastructure lagged. Employment services such as our investment in Robert Half performed very well in this environment. Our biggest disappointment was United Rentals, a long-time holding of the Fund which has had stellar performance until late 2014. The timing of the Company’s decision to enhance their tool rental business into a more focused offering in energy services exacerbated the uncertainty of sustainable growth, and we reluctantly sold the position.

The Information Technology (“IT”) sector continued to contribute positively to strong relative returns, and the Fund benefitted from its overweight positioning. However, stock selection within the sector was not up to our standards, and late in the year we adjusted our holdings. During this time period where the IT sector was up in excess of 20%, we had a few names that underperformed. Capital expenditures have been choppy for companies tied to telecom and cable/digital distribution which impacted both Finisar and Rovi (down in excess of 25%). We sold Finisar, and although we continue to see expanded breadth and applicability of the patent portfolio of Rovi in the evolution of digital content, that holding was eliminated as well. Yelp was also down in excess of 25%, as the opportunity associated with relatively unpenetrated local advertising became more competitive driving up costs. Additionally, its reliance on traffic from Google added volatility to results, and we moved on to better opportunities elsewhere. As strong advocates to the value of secular themes, it is hard to argue the importance of big data, business intelligence and now cybersecurity. Our biggest winner for the time period was business intelligence software provider Tableau with its unique dashboard and pricing approach to making the mountains of data more useful. Not only has the explosion of data and our online existence provided tremendous efficiencies to individuals and businesses, the risks continue to mount to exploit the interconnectedness to our disadvantage. Cybersecurity safeguards are becoming one

The Health Care sector was the runaway winner during this one-year period. The sector continued to be fueled by M&A activity, and although stock selection was a slight detractor from performance, we are pleased with the performance of our more diverse sector holdings. Half of our top ten contributors to performance came from this sector. Two beneficiaries of the Affordable Care Act, Medicaid health care providers and hospitals, were well represented in the portfolio with Centene and Universal Health Services, respectively. Biotechnology continues to provide long-term opportunity, and our best performer for the time period was ISIS Pharmaceuticals. The strategic antisense platform continues to build its pipeline of potentially effective drugs and partnerships. Along with ISIS, Medivation partnered with Astellas in providing commercially relevant Xtandi, which provides a very attractive profile to urologists and oncologists for pre-chemo prostate cancer. Lastly, Akorn, a niche generic manufacturer in high barrier-to-entry markets (injectable, ophthalmology, etc.), has positioned itself for long-term sustainable growth.

OUTLOOK

We believe the economic weakness noted in Q1 2015 will prove to be transient, and that economic growth will resume, fueled by low inflation, a benign interest rate environment, and improving consumer spending. Some of this strength is showing up in improving home prices, employment and consumer sentiment. We continue to have faith in the strength of the U.S. economy, as well as indications of an improving recovery in Europe. We would expect higher levels of volatility to continue, as the market perceives stocks to be expensive and earnings growth weak. With the rising U.S. dollar and the associated corresponding cheaper imports, we would anticipate inflation expectations to remain subdued, allowing the Fed to be more patient in raising interest rates.

At Apex, one of the foundations of our success is focusing on the long-term sustainability of secular growth trends. The performance dichotomy across sectors highlights the importance of sharpening the focus on those industries that are able to deliver sustained earnings growth within an uncertain economic backdrop. During challenging times, we remain committed to the opportunities provided in such areas as consumer mobility, big data and cloud computing, cybersecurity, the U.S. manufacturing renaissance, personalized medicine and genomics, and energy independence. As we navigate through the early stages of the self-sustaining U.S. economy, coupled with global growth anxieties, our focus will continue to be on selective opportunities that could benefit in this environment.

Sincerely,

Nitin N. Kumbhani

President and Chief Investment Officer

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance data current to the most recent month-end are available by calling 1-888-575-4800.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus, please visit our website at www.apexcmfund.com or call 1-888-575-4800 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The APEXcm Small/Mid-Cap Growth Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed. The securities held by the Fund that are discussed in the Letter to Shareholders were held during the period covered by this Report. They do not comprise the entire investment portfolio of the Fund, may be sold at any time and may no longer be held by the Fund. The opinions of the Fund’s Adviser with respect to those securities may change at any time.

APEXcm SMALL/MID-CAP GROWTH FUND

PERFORMANCE INFORMATION

May 31, 2015 (Unaudited)

Comparison of the Change in Value of a $10,000

Investment in APEXcm Small/Mid-Cap Growth Fund

versus the Russell 2500TM Growth Index

|

Average Annual Total Returns |

|||

|

1 Year |

Since |

||

|

APEXcm Small/Mid-Cap Growth Fund(a) |

14.67% |

21.37% |

|

|

Russell 2500TM Growth Index |

17.55% |

21.09% |

|

|

(a) |

The Fund’s total return does not reflect the deduction of taxes a shareholder would pay on Fund distributions or the redemption of Fund shares. |

|

(b) |

The Fund commenced operations on June 29, 2012. |

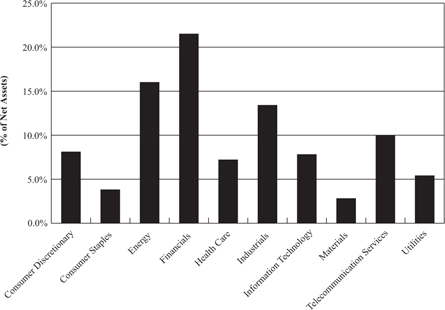

APEXcm SMALL/MID-CAP GROWTH FUND

PORTFOLIO INFORMATION

May 31, 2015 (Unaudited)

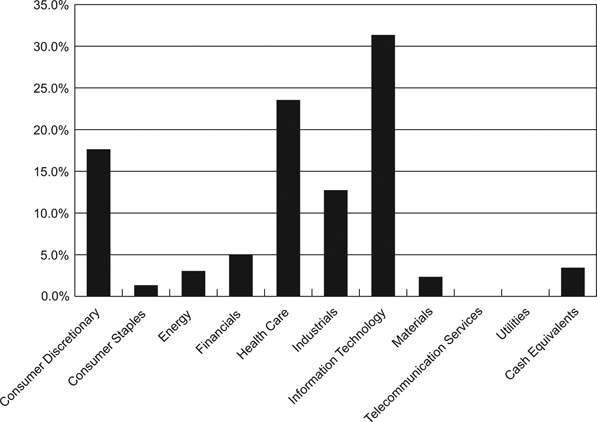

Sector Diversification (% of Net Assets)

Top 10 Equity Holdings

|

Security Description |

% of |

|

Universal Health Services, Inc. - Class B |

2.6% |

|

Wabtec Corp. |

2.3% |

|

Tableau Software, Inc. - Class A |

2.3% |

|

Autoliv, Inc. |

2.2% |

|

IAC/InterActiveCorp |

2.2% |

|

Total System Services, Inc. |

2.1% |

|

CBRE Group, Inc. - Class A |

2.1% |

|

Medivation, Inc. |

2.1% |

|

Williams-Sonoma, Inc. |

2.1% |

|

Foot Locker, Inc. |

2.1% |

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||||||

|

COMMON STOCKS — 96.6% |

Shares |

Value |

||||||

|

Consumer Discretionary — 17.6% |

||||||||

|

Auto Components — 2.2% |

||||||||

|

Autoliv, Inc. |

42,474 |

$ |

5,358,095 |

|||||

|

Hotels, Restaurants & Leisure — 2.4% |

||||||||

|

Dunkin' Brands Group, Inc. |

45,048 |

2,403,761 |

||||||

|

Wyndham Worldwide Corp. |

40,419 |

3,431,977 |

||||||

|

5,835,738 |

||||||||

|

Internet & Catalog Retail — 2.0% |

||||||||

|

Expedia, Inc. |

45,373 |

4,866,708 |

||||||

|

Media — 1.1% |

||||||||

|

IMAX, Corp. * |

64,798 |

2,613,951 |

||||||

|

Multi-Line Retail — 2.3% |

||||||||

|

Burlington Stores, Inc. * |

62,960 |

3,322,399 |

||||||

|

Dillard's, Inc. - Class A |

19,431 |

2,254,190 |

||||||

|

5,576,589 |

||||||||

|

Specialty Retail — 5.6% |

||||||||

|

Foot Locker, Inc. |

79,670 |

5,035,144 |

||||||

|

Signet Jewelers Ltd. |

25,257 |

3,266,488 |

||||||

|

Williams-Sonoma, Inc. |

64,214 |

5,047,863 |

||||||

|

13,349,495 |

||||||||

|

Textiles, Apparel & Luxury Goods — 2.0% |

||||||||

|

Carter's, Inc. |

23,520 |

2,427,735 |

||||||

|

Skechers U.S.A., Inc. - Class A * |

22,991 |

2,434,057 |

||||||

|

4,861,792 |

||||||||

|

Consumer Staples — 1.3% |

||||||||

|

Food Products — 1.3% |

||||||||

|

Hain Celestial Group, Inc. (The) * |

50,018 |

3,164,639 |

||||||

|

Energy — 2.9% |

||||||||

|

Energy Equipment & Services — 0.7% |

||||||||

|

Core Laboratories N.V. |

13,744 |

1,614,645 |

||||||

|

Oil, Gas & Consumable Fuels — 2.2% |

||||||||

|

Carrizo Oil & Gas, Inc. * |

61,063 |

3,062,920 |

||||||

|

Diamondback Energy, Inc. * |

30,153 |

2,346,205 |

||||||

|

5,409,125 |

||||||||

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||||||

|

COMMON STOCKS — 96.6% (Continued) |

Shares |

Value |

||||||

|

Financials — 4.9% |

||||||||

|

Banks — 1.7% |

||||||||

|

First Republic Bank/CA |

64,586 |

$ |

3,910,682 |

|||||

|

Diversified Financial Services — 1.1% |

||||||||

|

Interactive Brokers Group, Inc. - Class A |

39,988 |

1,427,571 |

||||||

|

MarketAxess Holdings, Inc. |

13,993 |

1,237,681 |

||||||

|

2,665,252 |

||||||||

|

Real Estate Management & Development — 2.1% |

||||||||

|

CBRE Group, Inc. - Class A * |

134,282 |

5,134,944 |

||||||

|

Health Care — 23.5% |

||||||||

|

Biotechnology — 8.3% |

||||||||

|

Agios Pharamceuticals, Inc. * |

10,952 |

1,336,363 |

||||||

|

AMAG Pharmaceuticals, Inc. * |

17,900 |

1,245,482 |

||||||

|

Enanta Pharmaceuticals, Inc. * |

64,175 |

2,623,474 |

||||||

|

Isis Pharmaceuticals, Inc. * |

62,643 |

4,217,127 |

||||||

|

Keryx Biopharmaceuticals, Inc. * |

115,693 |

1,203,207 |

||||||

|

Medivation, Inc. * |

38,837 |

5,128,426 |

||||||

|

Momenta Pharmaceuticals, Inc. * |

54,867 |

1,089,110 |

||||||

|

Receptos, Inc. * |

4,969 |

819,338 |

||||||

|

United Therapeutics Corp. * |

12,655 |

2,324,977 |

||||||

|

19,987,504 |

||||||||

|

Health Care Equipment & Supplies — 2.7% |

||||||||

|

Align Technology, Inc. * |

50,875 |

3,086,586 |

||||||

|

DexCom, Inc. * |

37,625 |

2,698,465 |

||||||

|

Tandem Diabetes Care, Inc. * |

50,017 |

603,705 |

||||||

|

6,388,756 |

||||||||

|

Health Care Providers & Services — 4.3% |

||||||||

|

Centene Corp. * |

55,648 |

4,192,520 |

||||||

|

Universal Health Services, Inc. - Class B |

47,496 |

6,154,532 |

||||||

|

10,347,052 |

||||||||

|

Health Care Technology — 1.3% |

||||||||

|

Medidata Solutions, Inc. * |

52,121 |

3,023,539 |

||||||

|

Life Sciences Tools & Services — 2.7% |

||||||||

|

ICON plc * |

43,654 |

2,831,835 |

||||||

|

WuXi PharmaTech (Cayman), Inc. - ADR * |

86,208 |

3,708,668 |

||||||

|

6,540,503 |

||||||||

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||||||

|

COMMON STOCKS — 96.6% (Continued) |

Shares |

Value |

||||||

|

Health Care — 23.5% (Continued) |

||||||||

|

Pharmaceuticals — 4.2% |

||||||||

|

Akorn, Inc. * |

93,545 |

$ |

4,293,716 |

|||||

|

Horizon Pharma plc * |

40,545 |

1,314,874 |

||||||

|

Jazz Pharmaceuticals plc * |

18,656 |

3,345,954 |

||||||

|

Supernus Pharmaceuticals, Inc. * |

88,023 |

1,251,687 |

||||||

|

10,206,231 |

||||||||

|

Industrials — 12.7% |

||||||||

|

Aerospace & Defense — 0.8% |

||||||||

|

B/E Aerospace, Inc. |

32,836 |

1,882,816 |

||||||

|

Machinery — 4.0% |

||||||||

|

Nordson Corp. |

36,555 |

2,957,665 |

||||||

|

Proto Labs, Inc. * |

15,187 |

1,050,637 |

||||||

|

Wabtec Corp. |

55,827 |

5,599,448 |

||||||

|

9,607,750 |

||||||||

|

Professional Services — 3.3% |

||||||||

|

Robert Half International, Inc. |

68,168 |

3,842,630 |

||||||

|

Towers Watson & Co. - Class A |

30,511 |

4,208,992 |

||||||

|

8,051,622 |

||||||||

|

Road & Rail — 2.8% |

||||||||

|

Avis Budget Group, Inc. * |

49,674 |

2,533,374 |

||||||

|

Old Dominion Freight Line, Inc. * |

60,423 |

4,109,368 |

||||||

|

6,642,742 |

||||||||

|

Trading Companies & Distributors — 1.8% |

||||||||

|

HD Supply Holdings, Inc. * |

136,548 |

4,430,983 |

||||||

|

Information Technology — 31.3% |

||||||||

|

Communications Equipment — 4.4% |

||||||||

|

Ciena Corp. * |

124,420 |

3,001,010 |

||||||

|

F5 Networks, Inc. * |

32,602 |

4,097,746 |

||||||

|

Infinera Corp. * |

173,341 |

3,577,758 |

||||||

|

10,676,514 |

||||||||

|

Electronic Equipment, |

||||||||

|

Dolby Laboratories, Inc. - Class A |

53,232 |

2,084,033 |

||||||

|

Internet Software & Services — 5.6% |

||||||||

|

Bitauto Holdings Ltd. - ADR * |

38,862 |

2,352,706 |

||||||

|

IAC/InterActiveCorp |

70,960 |

5,326,967 |

||||||

|

MercadoLibre, Inc. |

21,656 |

3,142,935 |

||||||

|

YY, Inc. - ADR * |

41,768 |

2,708,237 |

||||||

|

13,530,845 |

||||||||

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||||||

|

COMMON STOCKS — 96.6% (Continued) |

Shares |

Value |

||||||

|

Information Technology — 31.3% (Continued) |

||||||||

|

IT Services — 6.3% |

||||||||

|

Gartner, Inc. * |

27,354 |

$ |

2,392,928 |

|||||

|

Global Payments, Inc. |

43,861 |

4,578,211 |

||||||

|

Heartland Payment Systems, Inc. |

58,211 |

3,111,378 |

||||||

|

Total System Services, Inc. |

124,889 |

5,145,427 |

||||||

|

15,227,944 |

||||||||

|

Semiconductors & Semiconductor Equipment — 1.8% |

||||||||

|

Entegris, Inc. * |

162,211 |

2,259,599 |

||||||

|

Power Integrations, Inc. |

39,428 |

2,001,365 |

||||||

|

4,260,964 |

||||||||

|

Software — 12.3% |

||||||||

|

ACI Worldwide, Inc. * |

72,793 |

1,733,201 |

||||||

|

Advent Software, Inc. |

67,736 |

2,964,127 |

||||||

|

BroadSoft, Inc. * |

27,323 |

997,563 |

||||||

|

FireEye, Inc. * |

53,697 |

2,500,669 |

||||||

|

Fortinet, Inc. * |

96,884 |

3,881,173 |

||||||

|

Informatica Corp. * |

76,588 |

3,706,859 |

||||||

|

Manhattan Associates, Inc. * |

34,521 |

1,893,477 |

||||||

|

NetScout Systems, Inc. * |

3,664 |

146,853 |

||||||

|

Splunk, Inc.* |

57,172 |

3,865,971 |

||||||

|

Tableau Software, Inc. - Class A * |

47,888 |

5,421,401 |

||||||

|

Verint Systems, Inc. * |

37,946 |

2,453,968 |

||||||

|

29,565,262 |

||||||||

|

Materials — 2.4% |

||||||||

|

Containers & Packaging — 1.2% |

||||||||

|

Silgan Holdings, Inc. |

53,940 |

2,931,100 |

||||||

|

Paper & Forest Products — 1.2% |

||||||||

|

KapStone Paper and Packaging Corp. |

101,207 |

2,727,529 |

||||||

|

Total Common Stocks (Cost $200,912,620) |

$ |

232,475,344 |

||||||

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||||||

|

MONEY MARKET FUNDS — 4.6% |

Shares |

Value |

||||||

|

Fidelity Institutional Money Market Portfolio - Class I, 0.10% (a) (Cost $11,174,521) |

11,174,521 |

$ |

11,174,521 |

|||||

|

Total Investments at Value — 101.2% (Cost $212,087,141) |

$ |

243,649,865 |

||||||

|

Liabilities in Excess of Other Assets — (1.2%) |

(2,904,734 |

) |

||||||

|

Net Assets — 100.0% |

$ |

240,745,131 |

||||||

|

ADR - American Depositary Receipt.

|

|

|

* |

Non-income producing security. |

|

(a) |

The rate shown is the 7-day effective yield as of May 31, 2015.

|

|

See accompanying notes to financial statements. |

|

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||

|

ASSETS |

||||

|

Investments in securities: |

||||

|

At acquisition cost |

$ |

212,087,141 |

||

|

At value (Note 2) |

$ |

243,649,865 |

||

|

Dividends receivable |

152,057 |

|||

|

Receivable for capital shares sold |

1,399,249 |

|||

|

Receivable for investment securities sold |

8,057,355 |

|||

|

Other assets |

18,790 |

|||

|

Total assets |

253,277,316 |

|||

|

LIABILITIES |

||||

|

Payable for investment securities purchased |

12,310,573 |

|||

|

Payable for capital shares redeemed |

4,997 |

|||

|

Payable to Adviser (Note 4) |

165,902 |

|||

|

Payable to administrator (Note 4) |

27,890 |

|||

|

Other accrued expenses |

22,823 |

|||

|

Total liabilities |

12,532,185 |

|||

|

NET ASSETS |

$ |

240,745,131 |

||

|

NET ASSETS CONSIST OF: |

||||

|

Paid-in capital |

$ |

209,204,785 |

||

|

Accumulated net investment loss |

(395,464 |

) |

||

|

Undistributed net realized gains from security transactions |

373,086 |

|||

|

Net unrealized appreciation on investments |

31,562,724 |

|||

|

NET ASSETS |

$ |

240,745,131 |

||

|

Shares of beneficial interest outstanding |

13,808,259 |

|||

|

Net asset value, offering price and redemption price per share (Note 2) |

$ |

17.43 |

||

|

See accompanying notes to financial statements. |

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||

|

INVESTMENT INCOME |

||||

|

Dividend income (net of foreign taxes of $3,525) |

$ |

836,621 |

||

|

EXPENSES |

||||

|

Investment advisory fees (Note 4) |

1,468,496 |

|||

|

Administration fees (Note 4) |

147,153 |

|||

|

Registration and filing fees |

46,227 |

|||

|

Custody and bank service fees |

45,338 |

|||

|

Fund accounting fees (Note 4) |

44,466 |

|||

|

Professional fees |

32,861 |

|||

|

Transfer agent fees (Note 4) |

19,813 |

|||

|

Compliance fees (Note 4) |

16,773 |

|||

|

Postage and supplies |

8,690 |

|||

|

Trustees' fees and expenses (Note 4) |

7,366 |

|||

|

Insurance expense |

3,102 |

|||

|

Other expenses |

18,722 |

|||

|

Total expenses |

1,859,007 |

|||

|

Less fee waivers by the Adviser (Note 4) |

(317,860 |

) |

||

|

Net expenses |

1,541,147 |

|||

|

NET INVESTMENT LOSS |

(704,526 |

) |

||

|

REALIZED AND UNREALIZED GAINS ON INVESTMENTS |

||||

|

Net realized gains from security transactions |

830,411 |

|||

|

Net change in unrealized appreciation/depreciation on investments |

21,795,162 |

|||

|

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS |

22,625,573 |

|||

|

NET INCREASE IN NET ASSETS RESULTING FROM OPERATIONS |

$ |

21,921,047 |

||

|

See accompanying notes to financial statements. |

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||||||

|

|

Year |

Year |

||||||

|

FROM OPERATIONS |

||||||||

|

Net investment loss |

$ |

(704,526 |

) |

$ |

(192,714 |

) |

||

|

Net realized gains (losses) from security transactions |

830,411 |

(197,613 |

) |

|||||

|

Net change in unrealized appreciation on investments |

21,795,162 |

8,704,592 |

||||||

|

Net increase in net assets resulting from operations |

21,921,047 |

8,314,265 |

||||||

|

DISTRIBUTIONS TO SHAREHOLDERS |

||||||||

|

From net realized gains |

— |

(226,268 |

) |

|||||

|

CAPITAL SHARE TRANSACTIONS |

||||||||

|

Proceeds from shares sold |

154,037,822 |

74,662,709 |

||||||

|

Net asset value of shares issued in reinvestment of distributions to shareholders |

— |

162,061 |

||||||

|

Payments for shares redeemed |

(23,690,438 |

) |

(7,589,046 |

) |

||||

|

Net increase in net assets from capital share transactions |

130,347,384 |

67,235,724 |

||||||

|

TOTAL INCREASE IN NET ASSETS |

152,268,431 |

75,323,721 |

||||||

|

NET ASSETS |

||||||||

|

Beginning of year |

88,476,700 |

13,152,979 |

||||||

|

End of year |

$ |

240,745,131 |

$ |

88,476,700 |

||||

|

ACCUMULATED NET |

$ |

(395,464 |

) |

$ |

(105,388 |

) |

||

|

CAPITAL SHARE ACTIVITY |

||||||||

|

Shares sold |

9,429,777 |

5,289,946 |

||||||

|

Shares reinvested |

— |

10,768 |

||||||

|

Shares redeemed |

(1,443,740 |

) |

(515,199 |

) |

||||

|

Net increase in shares outstanding |

7,986,037 |

4,785,515 |

||||||

|

Shares outstanding at beginning of year |

5,822,222 |

1,036,707 |

||||||

|

Shares outstanding at end of year |

13,808,259 |

5,822,222 |

||||||

|

See accompanying notes to financial statements. |

|

APEXcm SMALL/MID-CAP GROWTH FUND |

||||||||||||

|

Per Share Data for a Share Outstanding Throughout Each Period |

||||||||||||

|

|

Year |

Year |

Period |

|||||||||

|

Net asset value at beginning of period |

$ |

15.20 |

$ |

12.69 |

$ |

10.00 |

||||||

|

Income (loss) from investment operations: |

||||||||||||

|

Net investment income (loss) |

(0.04 |

) |

(0.03 |

) |

0.04 |

(b) |

||||||

|

Net realized and unrealized gains on investments |

2.27 |

2.60 |

2.72 |

|||||||||

|

Total from investment operations |

2.23 |

2.57 |

2.76 |

|||||||||

|

Less distributions: |

||||||||||||

|

From net investment income |

— |

— |

(0.07 |

) |

||||||||

|

From net realized gains |

— |

(0.06 |

) |

— |

||||||||

|

Total distributions |

— |

(0.06 |

) |

(0.07 |

) |

|||||||

|

Net asset value at end of period |

$ |

17.43 |

$ |

15.20 |

$ |

12.69 |

||||||

|

Total return (c) |

14.67 |

% |

20.26 |

% |

27.65 |

%(d) |

||||||

|

Net assets at end of period (000's) |

$ |

240,745 |

$ |

88,477 |

$ |

13,153 |

||||||

|

Ratios/supplementary data: |

||||||||||||

|

Ratio of total expenses to average net assets |

1.26 |

% |

1.49 |

% |

4.87 |

%(e) |

||||||

|

Ratio of net expenses to average net assets (f) |

1.05 |

% |

1.05 |

% |

1.05 |

%(e) |

||||||

|

Ratio of net investment income (loss) to average net assets (f) |

(0.48 |

%) |

(0.38 |

%) |

0.26 |

%(e) |

||||||

|

Portfolio turnover rate |

58 |

% |

47 |

% |

18 |

%(d) |

||||||

|

(a) |

Represents the period from the commencement of operations (June 29, 2012) through May 31, 2013. |

|

(b) |

Calculated using weighted average shares outstanding during the period. |

|

(c) |

Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. The total returns would be lower if the Adviser had not waived advisory fees and/or reimbursed expenses (Note 4). |

|

(d) |

Not annualized. |

|

(e) |

Annualized. |

|

(f) |

Ratio was determined after advisory fee waivers and/or expense reimbursements (Note 4).

|

|

See accompanying notes to financial statements. |

|

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS

May 31, 2015

1. Organization

APEXcm Small/Mid-Cap Growth Fund (the “Fund”) is a diversified series of Ultimus Managers Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated February 28, 2012. Other series of the Trust are not incorporated in this report. The Fund commenced operations on June 29, 2012.

The investment objective of the Fund is long-term capital growth.

2. Significant Accounting Policies

The following is a summary of the Fund’s significant accounting policies. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). As an investment company, as defined in Financial Accounting Standards Board (“FASB”) Accounting Standards Update 2013-08, the Fund follows accounting and reporting guidance under FASB Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.”

Securities valuation – The Fund values its portfolio securities at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open for business. The pricing and valuation of portfolio securities is determined in good faith in accordance with procedures established by and under the direction of the Board of Trustees (the “Board”) of the Trust. The Fund values its listed securities on the basis of the security’s last sale price on the security’s primary exchange, if available, otherwise at the exchange’s most recently quoted bid price. NASDAQ-listed securities are valued at the NASDAQ Official Closing Price. In the event that market quotations are not readily available or are considered unreliable due to market or other events, the Fund values its securities and other assets at fair value in accordance with procedures established by and under the general supervision of the Board. Under these procedures, the securities will be classified as Level 2 or 3 within the fair value hierarchy (see below), depending on the inputs used. Unavailable or unreliable market quotes may be due to the following factors: a substantial bid-ask spread; infrequent sales resulting in stale prices; insufficient trading volume; small trade sizes; a temporary lapse in any reliable pricing source; and actions of the securities or futures markets, such as the suspension or limitation of trading. As a result, the prices of securities used to calculate the Fund’s net asset value may differ from quoted or published prices for the same securities.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value, and requires additional disclosures about fair value measurements.

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

|

● |

Level 1 – quoted prices in active markets for identical securities |

|

● |

Level 2 – other significant observable inputs |

|

● |

Level 3 – significant unobservable inputs |

The inputs or methods used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Fund’s investments as of May 31, 2015:

|

|

Level 1 |

Level 2 |

Level 3 |

Total |

||||||||||||

|

Common Stocks |

$ |

232,475,344 |

$ |

— |

$ |

— |

$ |

232,475,344 |

||||||||

|

Money Market Funds |

11,174,521 |

— |

— |

11,174,521 |

||||||||||||

|

Total |

$ |

243,649,865 |

$ |

— |

$ |

— |

$ |

243,649,865 |

||||||||

Refer to the Fund’s Schedule of Investments for a listing of the common stocks by industry type. As of May 31, 2015, the Fund did not have any transfers into and out of any Level. In addition, the Fund did not hold derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of May 31, 2015. It is the Fund’s policy to recognize transfers into and out of any Level at the end of the reporting period.

Share valuation – The net asset value per share of the Fund is calculated daily by dividing the total value of the Fund’s assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of the Fund is equal to the net asset value per share.

Investment income – Dividend income is recorded on the ex-dividend date. Interest income is accrued as earned.

Security transactions – Security transactions are accounted for on the trade date. Gains and losses on securities sold are determined on a specific identification basis.

Common expenses – Common expenses of the Trust are allocated among the Fund and the other series of the Trust based on the relative net assets of each series or the nature of the services performed and the relative applicability to each series.

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

Distributions to shareholders – The Fund will distribute to shareholders any net investment income dividends and net realized capital gains distributions at least once each year. The amount of such dividends and distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions are recorded on the ex-dividend date. The tax character of the Fund’s distributions paid during the years ended May 31, 2015 and May 31, 2014 was as follows:

|

Year Ended |

Ordinary Income |

Long-Term Capital Gains |

Total Distributions |

|||||||||

|

May 31, 2015 |

$ |

— |

$ |

— |

$ |

— |

||||||

|

May 31, 2014 |

$ |

212,871 |

$ |

13,397 |

$ |

226,268 |

||||||

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax – The Fund has qualified and intends to continue to qualify as a regulated investment company under the Internal Revenue Code of 1986 (the “Code”). Qualification generally will relieve the Fund of liability for federal income taxes to the extent 100% of its net investment income and net realized capital gains are distributed in accordance with the Code. Accordingly, no provision for income tax has been made.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended October 31) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of May 31, 2015:

|

Tax cost of portfolio investments |

$ |

212,099,228 |

||

|

Gross unrealized appreciation |

$ |

35,041,342 |

||

|

Gross unrealized depreciation |

(3,490,705 |

) |

||

|

Net unrealized appreciation |

31,550,637 |

|||

|

Qualified late year losses |

(395,464 |

) |

||

|

Undistributed long term gains |

385,173 |

|||

|

Accumulated earnings |

$ |

31,540,346 |

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

The value of the federal income tax cost of portfolio investments and the tax components of accumulated earnings and the financial statement cost of portfolio investments and components of net assets may be temporarily different (“book/tax difference”). These book/tax differences are due to the recognition of capital gains or losses under income tax regulations and GAAP, primarily due to the tax deferral of losses on wash sales.

Qualified late year losses incurred after December 31, 2014 and within the taxable year are deemed to arise on the first day of the Fund’s next taxable year. For the year ended May 31, 2015, the Fund intends to defer $395,464 of late year ordinary losses to June 1, 2015 for federal income tax purposes.

For the year ended May 31, 2015, the Fund reclassified $414,450 of accumulated net investment loss against paid-in capital on its Statement of Assets and Liabilities. Such reclassification, the result of permanent differences between financial statement and income tax reporting requirements, had no effect on the Fund’s total net assets or net asset value per share.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions for all open tax periods (periods ended May 31, 2013 through May 31, 2015) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements. The Fund identifies its major tax jurisdiction as U.S. Federal.

3. Investment Transactions

During the year ended May 31, 2015, cost of purchases and proceeds from sales of investment securities, other than short-term investments, were $208,711,369 and $82,463,546, respectively.

4. Transactions with Related Parties

INVESTMENT ADVISORY AGREEMENT

The Fund’s investments are managed by Apex Capital Management, Inc. (the “Adviser”) pursuant to the terms of an Investment Advisory Agreement. Under the Investment Advisory Agreement, the Fund pays the Adviser an advisory fee, computed and accrued daily and paid monthly, at the annual rate of 1.00% of its average daily net assets.

Pursuant to an Expense Limitation Agreement between the Fund and the Adviser, the Adviser has contractually agreed, until October 1, 2016, to waive investment advisory fees and reimburse other expenses to limit Total Annual Fund Operating Expenses (exclusive of brokerage costs, taxes, interest, acquired fund fees and expenses, extraordinary expenses such as litigation and merger or reorganization

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

costs, and other expenses not incurred in the ordinary course of the Fund’s business) to an amount not exceeding 1.05% of the Fund’s average daily net assets. Accordingly, during the year ended May 31, 2015 the Adviser waived its advisory fees in the amount of $317,860.

Under the terms of the Expense Limitation Agreement, investment advisory fee waivers and expense reimbursements by the Adviser are subject to recoupment by the Adviser for a period of three years after such fees and expenses were incurred, provided the recoupments do not cause Total Annual Fund Operating Expenses to exceed the foregoing expense limitations. As of May 31, 2015, the Adviser may seek recoupment of investment advisory fee reductions and expense reimbursements no later than the dates as stated below:

|

May 31, 2016 |

May 31, 2017 |

May 31, 2018 |

||

|

$144,876 |

$223,293 |

$317,860 |

Certain officers of the Fund are also officers of the Adviser.

OTHER SERVICE PROVIDERS

Ultimus Fund Solutions, LLC (“Ultimus”) provides fund administration, fund accounting, compliance and transfer agency services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including but not limited to postage, supplies and costs of pricing the Fund’s portfolio securities.

DISTRIBUTION AGREEMENT

Under the terms of a Distribution Agreement with the Trust, Ultimus Fund Distributors, LLC (the “Distributor”) serves as principal underwriter to the Fund. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Fund) for acting as principal underwriter.

Certain Trustees and officers of the Trust are also officers of Ultimus and the Distributor.

TRUSTEE COMPENSATION

Each Trustee who is not an “interested person” of the Trust (“Independent Trustee”) receives from the Fund a fee of $500 for each Board meeting attended plus reimbursement of travel and other meeting-related expenses. In addition, effective January 1, 2015, each Independent Trustee also receives a $500 annual retainer from the Fund. Trustees affiliated with the Adviser or Ultimus are not compensated by the Trust for their services.

APEXcm SMALL/MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

PRINICIPAL HOLDERS OF FUND SHARES

As of May 31, 2015, the following shareholders owned of record 5% or more of the outstanding shares of the Fund:

|

Name of Record Owner |

% Ownership |

|

UBS Financial Services, Inc. (for the benefit of its customers) |

31% |

|

Charles Schwab & Company, Inc. (for the benefit of its customers) |

28% |

A beneficial owner of 25% or more of a Fund’s outstanding shares may be considered a controlling person. That shareholder’s vote could have a more significant effect on matters presented at a shareholder’s meeting.

5. Sector Risk

If a Fund has significant investments in the securities of issuers within a particular sector, any development affecting that sector will have a greater impact on the value of the net assets of the Fund than would be the case if the Fund did not have significant investments in that sector. In addition, this may increase the risk of loss in the Fund and increase the volatility of the Fund’s net asset value per share. Occasionally, market conditions, regulatory changes or other developments may negatively impact this sector, and therefore the value of the Fund’s portfolio will be adversely affected. As of May 31, 2015, the Fund had 31.3% of the value of its net assets invested in stocks within the Information Technology sector.

6. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

7. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events.

APEXcm SMALL/MID-CAP GROWTH FUND

REPORT OF INDEPENDENT REGISTERED

PUBLIC ACCOUNTING FIRM

To the Board of Trustees of Ultimus Managers Trust

and the Shareholders of APEXcm Small/Mid Cap Growth Fund

We have audited the accompanying statement of assets and liabilities of APEXcm Small/Mid Cap Growth Fund (the “Fund”), a series of shares of beneficial interest in Ultimus Managers Trust, including the schedule of investments, as of May 31, 2015, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, and the financial highlights for each of the years in the two-year period then ended and for the period June 29, 2012 (commencement of operations) through May 31, 2013. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audits.

We conducted our audits in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of May 31, 2015 by correspondence with the custodian and brokers. An audit also includes assessing the accounting principles used and significant estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audits provide a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of APEXcm Small/Mid Cap Growth Fund as of May 31, 2015, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years in the two-year period then ended and for the period June 29, 2012 through May 31, 2013, in conformity with accounting principles generally accepted in the United States of America.

|

|

|

BBD, LLP |

Philadelphia, Pennsylvania

July 27, 2015

APEXcm SMALL/MID-CAP GROWTH FUND

ABOUT YOUR FUND’S EXPENSES (Unaudited)

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period (December 1, 2014) and held until the end of the period (May 31, 2015).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the third column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (“SEC”) requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

APEXcm SMALL/MID-CAP GROWTH FUND

ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued)

More information about the Fund’s expenses can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

|

|

Beginning |

Ending |

Expenses |

|

Based on Actual Fund Return |

$ 1,000.00 |

$ 1,066.70 |

$ 5.41 |

|

Based on Hypothetical 5% Return (before expenses) |

$ 1,000.00 |

$ 1,019.70 |

$ 5.29 |

|

* |

Expenses are equal to the Fund’s annualized expense ratio of 1.05% for the period, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

OTHER INFORMATION (Unaudited)

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-888-575-4800, or on the SEC’s website at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge upon request by calling toll-free 1-888-575-4800, or on the SEC’s website at http://www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year on Form N-Q. These filings are available upon request by calling 1-888-575-4800. Furthermore, you may obtain a copy of the filings on the SEC’s website at http://www.sec.gov. The Trust’s Forms N-Q may also be reviewed and copied at the SEC’s Public Reference Room in Washington, DC, and information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

APEXcm SMALL/MID-CAP GROWTH FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited)

The Board of Trustees has overall responsibility for management of the Trust’s affairs. The Trustees serve during the lifetime of the Trust and until its termination, or until death, resignation, retirement, or removal. The Trustees, in turn, elect the officers of the Fund to actively supervise its day-to-day operations. The officers have been elected for an annual term. Unless otherwise noted, each Trustee’s and officer’s address is 225 Pictoria Drive, Suite 450, Cincinnati, Ohio 45246. The following are the Trustees and executive officers of the Fund:

|

Name and |

Length of Time Served |

Position(s) Held with Trust |

Principal Occupation(s) During Past 5 Years |

Number of Funds in Trust Overseen by Trustee |

Directorships of Public Companies Held by Trustee During Past 5 Years |

|

Interested Trustees: |

|||||

|

Robert G. Dorsey* Year of Birth: 1957 |

Since February 2012 |

Trustee (February 2012 to present) President (June 2012 to October 2013) |

Managing Director of Ultimus Fund Solutions, LLC and Ultimus Fund Distributors, LLC (1999 to present) |

11 |

n/a |

|

Independent Trustees: |

|||||

|

John C. Davis Year of Birth: 1952 |

Since June 2012 |

Chairman (July 2014 to present) Trustee (June 2012 to present) |

Consultant ( government services) since May 2011; Retired Partner of PricewaterhouseCoopers LLP (1974-2010) |

11 |

n/a |

|

David M. Deptula Year of Birth: 1958 |

Since June 2012 |

Trustee |

Vice President of Tax at The Standard Register Company since November 2011; Tax Partner at Deloitte Tax LLP from 1984 to 2011 |

11 |

n/a |

|

John J. Discepoli Year of Birth: 1963 |

Since June 2012 |

Trustee |

Owner of Discepoli Financial Planning, LLC (personal financial planning company) since November 2004 |

11 |

n/a |

|

* |

Mr. Dorsey is considered an “interested person” of the Trust within the meaning of Section 2(a)(19) of the 1940 Act because of his relationship with the Trust’s administrator, transfer agent and distributor. Mr. Dorsey was President of the Trust from June 2012 to October 2013. |

APEXcm SMALL/MID-CAP GROWTH FUND

BOARD OF TRUSTEES AND EXECUTIVE OFFICERS

(Unaudited) (Continued)

|

Name and |

Length of Time Served |

Position(s) Held with Trust |

Principal Occupation(s) During Past 5 Years |

|

Executive Officers: |

|||

|

Nitin N. Kumbhani 8163 Old Yankee Road, Suite E Dayton, Ohio 45458 Year of Birth: 1948 |

Since June 2012 |

Principal Executive Officer of APEXcm Small/Mid-Cap Growth Fund |

President and Chief Investment Officer of Apex Capital Management, Inc. (1987 to present) |

|

Michael Kalbfleisch 8163 Old Yankee Road, Suite E Dayton, Ohio 45458 Year of Birth: 1959 |

Since June 2012 |

Vice President of APEXcm Small/Mid-Cap Growth Fund |

Vice President and Chief Compliance Officer of Apex Capital Management, Inc. (2001 to present) |

|

David R. Carson Year of Birth: 1958 |

Since April 2013 |

President (October 2013 to present) Vice President (April 2013 to October 2013) |

Vice President and Director of Client Strategies of Ultimus Fund Solutions, LLC (2013 to present); Chief Compliance Officer, The Huntington Funds (2005 to 2013), The Flex-Funds (2006 to 2011), Meeder Financial (2007 to 2011), Huntington Strategy Shares (2012 to 2013), and Huntington Asset Advisors (2013); Vice President, Huntington National Bank (2001 to 2013) |

|

Jennifer L. Leamer Year of Birth: 1976 |

Since April 2014 |

Treasurer (October 2014 - present) Assistant Treasurer (April 2014 - October 2014) |

Mutual Fund Controller of Ultimus Fund Solutions, LLC (2014 to present); Business Analyst of Ultimus Fund Solutions, LLC (2007 to 2014) |

|

Bo J. Howell Year of Birth: 1981 |

Since October 2014 |

Secretary (April 2015 to present) Assistant Secretary (October 2014 to April 2015) |

V.P., Director of Fund Administration for Ultimus Fund Solutions, LLC (2014 to present); Counsel – Securities and Mutual Funds for Western & Southern Financial Group (2012 to 2014); U.S. Securities and Exchange Commission, Senior Counsel (2009 to 2012) |

|

Stephen L. Preston Year of Birth: 1966 |

Since June 2012 |

Chief Compliance Officer |

Vice President and Chief Compliance Officer of Ultimus Fund Distributors, LLC and Vice President of Ultimus Fund Solutions, LLC (2011 to present); Senior Consultant at Mainstay Capital Markets Consultants (2010 to 2011); Chief Compliance Officer at INTL Trading, Inc. (2008 to 2010) |

Additional information about members of the Board and executive officers is available in the Fund’s Statement of Additional Information (“SAI”). To obtain a free copy of the SAI, please call 1-888-575-4800.

APEXcm SMALL/MID-CAP GROWTH FUND

DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited)

The Board of Trustees (the “Board”), including the Independent Trustees voting separately, has reviewed and approved the Fund’s Investment Advisory Agreement with Apex Capital Management, Inc. (the “Adviser”) for an additional annual term. Approval took place at an in-person meeting held on April 20, 2015, at which all of the Trustees were present.

In the course of their deliberations, the Board was advised by legal counsel. The Board received and reviewed information provided by the Adviser in response to requests of the Board and counsel.

In considering the Investment Advisory Agreement and reaching their conclusions with respect thereto, the Board reviewed and analyzed various factors that they determined were relevant, including the factors described below.

The nature, extent, and quality of the services provided by the Adviser. In this regard, the Board reviewed the services being provided by the Adviser to the Fund including, without limitation, its investment advisory services since the Fund’s inception, the Adviser’s compliance procedures and practices, and its efforts to promote the Fund and assist in its distribution. The Board also noted that a principal of the Adviser serves as the Fund’s Principal Executive Officer without additional compensation. After reviewing the foregoing information and further information regarding the Adviser’s business, the Board concluded that the quality, extent, and nature of the services provided by the Adviser were satisfactory and adequate for the Fund.

The investment performance of the Fund. In this regard, the Board compared the performance of the Fund with the performance of its benchmark index and related Morningstar category. The Board also considered the consistency of the Adviser’s management with the Fund’s investment objective and policies. Following discussion of the investment performance of the Fund and its performance relative to its Morningstar category, the Adviser’s experience in managing mutual funds, its historical investment performance, and other factors, the Board concluded that the investment performance of the Fund has been satisfactory.

The costs of the services provided and profits realized by the Adviser and its affiliates from its relationship with the Fund. In this regard, the Board considered the Adviser’s staffing, personnel, and methods of operations; the education and experience of its personnel; compliance program, policies, and procedures; financial condition and the level of commitment to the Fund, and, generally, the Adviser’s advisory business; the asset level of the Fund; the overall expenses of the Fund, including the advisory fee; and the differences in fees and services to the Adviser’s other clients that may be similar to the Fund. The Board considered the Adviser’s Expense Limitation Agreement (the “ELA”) with the Fund, and considered the Adviser’s current and

APEXcm SMALL/MID-CAP GROWTH FUND

DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued)

past fee reductions and expense reimbursements for the Fund. The Board further took into account the Adviser’s commitment to continue the ELA for the Fund until at least October 1, 2016.

The Board also considered potential benefits for the Adviser in managing the Fund, including promotion of the Adviser’s name and the potential for it to receive research, statistical, or other services from the Fund’s trades. The Board compared the Fund’s advisory fee and overall expense ratio to the average advisory fees and average expense ratios for its Morningstar category. The Board noted that the advisory fee for the Fund was above the average and the median for the Morningstar Mid Cap Growth category. The Board further noted that the overall annual expense ratio of 1.05 percent for the Fund with the Adviser’s ELA is lower than the Morningstar category’s average expense ratio (1.33 percent) and median expense ratio (1.23 percent). The Board also noted that the Fund had significantly less assets than the average or median fund in its Morningstar category. The Board also compared the fees paid by the Fund to the fees paid by other clients of the Adviser, and considered the similarities and differences of services received by such other clients as compared to the service provided to the Fund. Following these comparisons and upon further consideration and discussion of the foregoing, the Board concluded that the advisory fee paid to the Adviser by the Fund is fair and reasonable.

The extent to which economies of scale would be realized as the Fund grows and whether advisory fee levels reflect these economies of scale for the benefit of the Fund’s investors. In this regard, the Board considered that the Fund’s fee arrangements with the Adviser involve both the advisory fee and the ELA. The Board determined that while the advisory fee remained the same as asset levels increased, the shareholders of the Fund have experienced benefits from the ELA. Following further discussion of the Fund’s asset level, expectations for growth, and level of fees, the Board determined that the Fund’s fee arrangements with the Adviser would continue to provide benefits. The Board also determined that the fee arrangements were fair and reasonable given the Fund’s projected asset levels for the next year.

Brokerage and portfolio transactions. In this regard, the Board considered the Adviser’s trading policies, procedures, and performance in seeking best execution for the Fund. The Board also considered the historical portfolio turnover rate for the Fund; the process by which evaluations are made of the overall reasonableness of commissions paid; the method and basis for selecting and evaluating the broker-dealers used; any anticipated allocation of portfolio business to persons affiliated with the Adviser; and the extent to which the Fund’s trades are allocated to soft-dollar arrangements. After further review and discussion, the Board determined that the Adviser’s practices regarding brokerage and portfolio transactions were satisfactory.

APEXcm SMALL/MID-CAP GROWTH FUND

DISCLOSURE REGARDING APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued)

Possible conflicts of interest. In evaluating the possibility for conflicts of interest, the Board considered such matters as the experience and abilities of the advisory personnel assigned to the Fund, the Adviser’s process for allocating trades among its different clients, and the substance and administration of the Adviser’s code of ethics. Following further consideration and discussion, the Board found that the Adviser’s standards and practices relating to the identification and mitigation of potential conflicts of interests were satisfactory.

Conclusion

After consideration of the above factors as well as other factors, the Board unanimously concluded that approval of the Investment Advisory Agreement was in the best interests of the Fund and its shareholders.

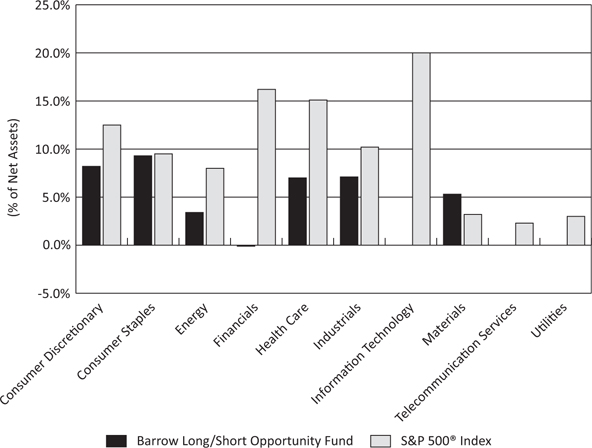

BARROW VALUE OPPORTUNITY FUND

INSTITUTIONAL CLASS (BALIX)

INVESTOR CLASS (BALAX)

BARROW LONG/SHORT OPPORTUNITY FUND

INSTITUTIONAL CLASS (BFSLX)

INVESTOR CLASS (BFLSX)

Annual Report

May 31, 2015

|

BARROW VALUE OPPORTUNITY FUND |

June 26, 2015 |

Dear Shareholder,

We are pleased to report on the status and performance of Barrow Value Opportunity Fund (“the Fund”) for the fiscal year ended May 31, 2015. On May 1, 2015 the Fund changed its name from Barrow All-Cap Core Fund.

We believe that the Fund owns a well-positioned portfolio of equity interests in excellent businesses at attractive valuations. This portfolio is highly diversified by market capitalization segments (large, middle, small), industry sectors, and issuers. The underlying businesses feature high returns on capital, wide operating margins, and low debt loads. Based on our estimates of intrinsic value, our portfolio’s valuation is attractively low on an absolute basis and less expensive than the U.S. stock market as represented by the S&P 500® Index (the “S&P 500”).

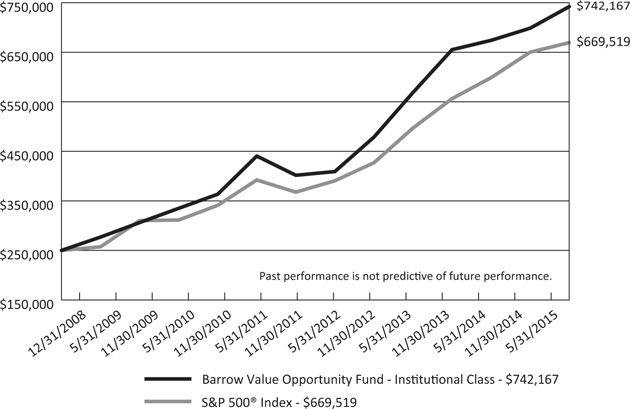

On August 30, 2013, the Fund was reorganized as a mutual fund from a private limited partnership, which had commenced operations on December 31, 2008. Please refer to the Performance Information on pages 4 and 5 for a summary of Fund performance versus the S&P 500 over various periods of time since the Fund’s inception.

The Fund’s long-term performance has been excellent relative to the S&P 500. The Fund has exceeded the total return of the S&P 500 in five of the past six calendar years1. During the fiscal year ended May 31, 2015, the Institutional Class of the Fund returned 10.10% net of all fees and expenses, which lagged the S&P 500 by 1.71%. This lag is attributable to the Fund’s large-cap and small-cap positions, which underperformed the S&P 500, while its mid-cap positions outperformed. We are confident the Fund’s large-cap and small-cap holdings will make meaningful contributions to the Fund’s performance over time, as they have in the past, and the Fund continues to hold substantial positions in each market capitalization segment.

Barrow Street Advisors, LLC (the “Adviser”) continued using its proprietary private-equity approach to uncover companies that exhibit its Quality-meets-Value criteria. Based on extensive research by the Adviser, the Fund seeks to invest in companies with fundamental operating and financial attributes representative of both quality and value. To increase the Fund’s chances for success, we harness these opportunities by investing in a variety of positions diversified across market capitalization and industry sectors.

Over the past fiscal year, we uncovered 114 new investment opportunities, composed of 53 small caps, 28 mid caps, and 33 large caps, and representing six different industry sectors. We believe all of these new additions to the Fund’s portfolio are excellent companies with strong balance sheets. These companies are generally using their ample free cash flow to: a) re-invest in growth opportunities at high rates of return; b) pay dividends; c) repurchase stock at attractive valuations; and/or d) retire outstanding debt.

In keeping with our practice since the beginning of 2009, over the past year the Fund’s investments were sourced by taking account of the opportunity set of all companies in our broad investment universe each time we committed capital to a new position. We think this approach allows us to uncover excellent investment opportunities that arise from temporary market inefficiencies and to gather up the most compelling investments across a wide array of industries and market capitalizations, while avoiding the destructive behavioral biases inherent in concentrated-stock and sector-specialized investing.

Seven of the Fund’s holdings were announced as take-over targets over the past year, which was approximately 1.4x the market average. The Fund has had investments in 67 take-overs since December 31, 2008, or roughly 4x the market average2. The control premiums we have captured by virtue of holding stocks that end up being merger targets have made repeated and meaningful contributions to the Fund’s total returns, and we expect continued benefits from this effect going forward. We sell companies from the Fund’s portfolio soon after they are announced as take-over targets and re-invest that capital.

Over the past fiscal year, the Fund’s portfolio generated a total return, before fees and expenses, of +11.24%, including +8.03% for large caps, +14.98% for mid caps and +9.45% for small caps. This compares to +11.81% for the S&P 500 (for large caps), +12.28% for the S&P 400 Midcap (for mid caps), and +11.32% for the Russell 2000 (for small caps) over the same period. The Fund’s sectors with the best absolute performance were Health Care and Consumer Staples, which generated total returns of +28.80% and +21.15%, respectively. The Fund’s sectors with the worst absolute performance were Energy and Materials, which returned -20.84% and +7.32%, respectively.

You can find additional commentary and reports about the Adviser’s management of the Fund’s portfolio on the Barrow Funds’ website (www.barrowfunds.com), including our unique quarterly “consolidated look-through” report in which we compare the portfolio of the Fund with the S&P 500 as if they were both public holding companies like Berkshire Hathaway. The consolidated look-through analysis is another example of how we look at our portfolio through a private equity lens. We focus on the key characteristics of good business, such as total enterprise value (not just equity market capitalization), unleveraged cash flow, return on capital, leverage, growth, and insider ownership. At the same time, we are buying a diverse group of these high quality companies at attractive valuation levels. This unique approach has served our investors well, and we remain confident in the future.

Sincerely,

|

Nicholas Chermayeff |

Robert F. Greenhill, Jr. |

David R. Bechtel |

|

Co-Portfolio Manager, |

Co-Portfolio Manager, |

Principal, |

|

Investment Committee |