UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM

(Mark One)

For the quarterly period ended

OR

Commission File Number:

(Exact Name of Registrant as Specified in its Charter)

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer |

(Address of principal executive offices) |

(Zip Code) |

(

Registrant’s telephone number, including area code

N/A

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

|

☐ |

|

Accelerated filer |

|

☐ |

|

|

|

|

|||

|

☒ |

|

Smaller reporting company |

|

||

|

|

|

|

|

|

|

|

|

|

|

Emerging growth company |

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

As of May 8, 2024, the registrant had

|

|

Page |

|

PART I - FINANCIAL INFORMATION |

|

Item 1. |

Financial Statements (unaudited) |

|

|

Consolidated Balance Sheets as of March 31, 2024 and December 31, 2023 |

3 |

|

Consolidated Statements of Operations for the three months ended March 31, 2024 and 2023 |

4 |

|

5 |

|

|

Consolidated Statements of Cash Flows for the three months ended March 31, 2024 and 2023 |

6 |

|

7 |

|

Item 2. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

17 |

Item 3. |

25 |

|

Item 4. |

25 |

|

|

PART II - OTHER INFORMATION |

|

Item 1. |

27 |

|

Item 1A |

Risk Factors |

27 |

Item 2. |

27 |

|

Item 5. |

Other Information |

27 |

Item 6. |

28 |

|

29 |

||

PART I – FINANCIAL INFORMATION

Item 1. Financial Statements

CLEARSIDE BIOMEDICAL, INC.

Consolidated Balance Sheets

(in thousands, except share and per share data)

(unaudited)

|

|

March 31, |

|

|

December 31, |

|

||

Assets |

|

|

|

|

|

|

||

Current assets: |

|

|

|

|

|

|

||

Cash and cash equivalents |

|

$ |

|

|

$ |

|

||

Accounts receivable |

|

|

|

|

|

|

||

Prepaid expenses |

|

|

|

|

|

|

||

Other current assets |

|

|

|

|

|

|

||

Total current assets |

|

|

|

|

|

|

||

Property and equipment, net |

|

|

|

|

|

|

||

Operating lease right-of-use asset |

|

|

|

|

|

|

||

Other assets |

|

|

|

|

|

|

||

Total assets |

|

$ |

|

|

$ |

|

||

Liabilities and stockholders’ (deficit) equity |

|

|

|

|

|

|

||

Current liabilities: |

|

|

|

|

|

|

||

Accounts payable (includes $ |

|

$ |

|

|

$ |

|

||

Accrued liabilities (includes $ |

|

|

|

|

|

|

||

Current portion of operating lease liabilities |

|

|

|

|

|

|

||

Deferred revenue |

|

|

|

|

|

|

||

Total current liabilities |

|

|

|

|

|

|

||

Liability related to the sales of future royalties, net |

|

|

|

|

|

|

||

Warrant liabilities |

|

|

|

|

|

|

||

Operating lease liabilities |

|

|

|

|

|

|

||

Other non-current liabilities |

|

|

|

|

|

|

||

Total liabilities |

|

|

|

|

|

|

||

|

|

|

|

|

|

|||

Stockholders’ (deficit) equity: |

|

|

|

|

|

|

||

Preferred stock, $ |

|

|

|

|

|

|

||

Common stock, $ |

|

|

|

|

|

|

||

Additional paid-in capital |

|

|

|

|

|

|

||

Accumulated deficit |

|

|

( |

) |

|

|

( |

) |

Total stockholders’ deficit |

|

|

( |

) |

|

|

( |

) |

Total liabilities and stockholders’ (deficit) equity |

|

$ |

|

|

$ |

|

||

See accompanying notes to the consolidated financial statements.

3

CLEARSIDE BIOMEDICAL, INC.

Consolidated Statements of Operations

(in thousands, except share and per share data)

(unaudited)

|

|

Three Months Ended |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

|

$ |

|

|

$ |

|

|||

Operating expenses: |

|

|

|

|

|

|

||

Research and development (includes $ |

|

|

|

|

|

|

||

General and administrative |

|

|

|

|

|

|

||

Total operating expenses |

|

|

|

|

|

|

||

Loss from operations |

|

|

( |

) |

|

|

( |

) |

Interest income |

|

|

|

|

|

|

||

Other expense |

|

|

( |

) |

|

|

|

|

Non-cash interest expense on liability |

|

|

( |

) |

|

|

( |

) |

Net loss |

|

$ |

( |

) |

|

$ |

( |

) |

Net loss per share of common stock — basic and diluted |

|

$ |

( |

) |

|

$ |

( |

) |

Weighted average shares outstanding — basic and diluted |

|

|

|

|

|

|

||

See accompanying notes to the consolidated financial statements.

4

CLEARSIDE BIOMEDICAL, INC.

Consolidated Statements of Stockholders’ (Deficit) Equity

(in thousands, except share data)

(unaudited)

|

|

Three Months Ended March 31, 2024 |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|||||

|

|

Common Stock |

|

|

Additional |

|

|

Accumulated |

|

|

Stockholders' |

|

||||||||

|

|

Shares |

|

|

Amount |

|

|

Paid-In-Capital |

|

|

Deficit |

|

|

(Deficit) Equity |

|

|||||

Balance at December 31, 2023 |

|

|

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

( |

) |

|||

Issuance of common stock under registered direct |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||

Issuance of common stock under at-the-market |

|

|

|

|

|

— |

|

|

|

|

|

|

— |

|

|

|

|

|||

Exercise of stock options |

|

|

|

|

|

— |

|

|

|

|

|

|

|

|

|

|

||||

Vesting and settlement of restricted stock units |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Issuance of common stock under employee stock |

|

|

|

|

|

— |

|

|

|

|

|

|

— |

|

|

|

|

|||

Share-based compensation expense |

|

|

— |

|

|

|

— |

|

|

|

|

|

|

— |

|

|

|

|

||

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

( |

) |

|

|

( |

) |

Balance at March 31, 2024 |

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

( |

) |

|||

|

|

Three Months Ended March 31, 2023 |

|

|||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total |

|

|||||

|

|

Common Stock |

|

|

Additional |

|

|

Accumulated |

|

|

Stockholders' |

|

||||||||

|

|

Shares |

|

|

Amount |

|

|

Paid-In-Capital |

|

|

Deficit |

|

|

Equity |

|

|||||

Balance at December 31,2022 |

|

|

|

|

$ |

|

|

$ |

|

|

$ |

( |

) |

|

$ |

|

||||

Issuance of common stock under at-the-market |

|

|

|

|

|

— |

|

|

|

|

|

|

— |

|

|

|

|

|||

Vesting and settlement of restricted stock units |

|

|

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Issuance of common stock under employee |

|

|

|

|

|

— |

|

|

|

|

|

|

— |

|

|

|

|

|||

Share-based compensation expense |

|

|

— |

|

|

|

— |

|

|

|

|

|

|

— |

|

|

|

|

||

Net loss |

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

|

( |

) |

|

|

( |

) |

Balance at March 31, 2023 |

|

|

|

|

|

|

|

|

|

|

|

( |

) |

|

|

|

||||

See accompanying notes to the consolidated financial statements.

5

CLEARSIDE BIOMEDICAL, INC.

Consolidated Statements of Cash Flows

(in thousands)

(unaudited)

|

|

Three Months Ended |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Operating activities |

|

|

|

|

|

|

||

Net loss |

|

$ |

( |

) |

|

$ |

( |

) |

Adjustments to reconcile net loss to net cash used in operating activities: |

|

|

|

|

|

|

||

Non-cash interest expense on liability related to the sales of |

|

|

|

|

|

|

||

Depreciation |

|

|

|

|

|

|

||

Share-based compensation expense |

|

|

|

|

|

|

||

Change in fair value of warrant liabilities |

|

|

|

|

|

|

||

Issuance costs allocated to warrant liabilities |

|

|

|

|

|

|

||

Changes in operating assets and liabilities: |

|

|

|

|

|

|

||

Prepaid expenses and other current assets |

|

|

|

|

|

( |

) |

|

Other assets and liabilities |

|

|

( |

) |

|

|

( |

) |

Accounts payable and accrued liabilities (includes $( |

|

|

( |

) |

|

|

( |

) |

Deferred revenue |

|

|

|

|

|

|

||

Net cash used in operating activities |

|

|

( |

) |

|

|

( |

) |

Investing activities |

|

|

|

|

|

|

||

Acquisition of property and equipment |

|

|

( |

) |

|

|

( |

) |

Net cash used in investing activities |

|

|

( |

) |

|

|

( |

) |

Financing activities |

|

|

|

|

|

|

||

Proceeds from issuance of common stock and warrants under |

|

|

|

|

|

|

||

Proceeds from at-the-market sales agreement, net of issuance costs |

|

|

|

|

|

|

||

Proceeds from exercise of stock options |

|

|

|

|

|

|

||

Proceeds from shares issued under employee stock purchase plan |

|

|

|

|

|

|

||

Net cash provided by financing activities |

|

|

|

|

|

|

||

Net increase (decrease) in cash and cash equivalents |

|

|

|

|

|

( |

) |

|

Cash and cash equivalents, beginning of period |

|

|

|

|

|

|

||

Cash and cash equivalent, end of period |

|

$ |

|

|

$ |

|

||

Supplemental disclosure |

|

|

|

|

|

|

||

Purchase of property and equipment included in accrued liabilities |

|

$ |

|

|

$ |

|

||

See accompanying notes to the consolidated financial statements.

6

CLEARSIDE BIOMEDICAL, INC.

Notes to the Consolidated Financial Statements

(unaudited)

1. The Company

Clearside Biomedical, Inc. (the “Company”) is a biopharmaceutical company focused on revolutionizing the delivery of therapies to the back of the eye through the suprachoroidal space (SCS®). Incorporated in the State of Delaware on

The Company’s activities since inception have primarily consisted of developing product and technology rights, raising capital and performing research and development activities. The Company is subject to a number of risks and uncertainties similar to those of other life science companies at a similar stage of development, including, among others, the need to obtain adequate additional financing, successful development efforts including regulatory approval of products, compliance with government regulations, successful commercialization of potential products, protection of proprietary technology and dependence on key individuals.

Liquidity

The Company had cash and cash equivalents of $

Historically, the Company has funded its operations primarily through the sale of common stock and convertible preferred stock, the issuance of long-term debt, and license agreements.

On February 6, 2024, the Company entered into a securities purchase agreement with institutional investors and an existing stockholder, pursuant to which the Company issued and sold, in a registered direct offering (the “Registered Direct Offering”): (i) an aggregate of

On January 31, 2024 (the “Amendment Effective Date”), the Company entered into a fourth amendment to the license agreement (as amended, the “Emory License Agreement”) with Emory University and Georgia Tech Research Corporation (collectively, the “Licensor”) pursuant to which the parties agreed to reduce the Sublicense Percentage (as defined in the Emory License Agreement) from a low double digit percentage to a high single digit percentage that the Company will pay the Licensor applicable to any fees or payments paid to the Company by any Sublicensee (as defined in the Emory License Agreement) of the Licensed Patents and/or Licensed Technology (each as defined in the Emory License Agreement), excluding (i) amounts paid to the Company by a Sublicensee to reimburse the Company for certain research and development costs pursuant to a written agreement between the Company and such Sublicensee, (ii) the value of intellectual property transferred or granted to the Company if necessary or helpful to the development or commercialization of Licensed Products (as defined in the Emory License Agreement) and (iii) amounts paid for shares of the Company’s stock. The payment to Licensor of any such Sublicense Percentage is due within 30 days of receipt by the Company of a qualifying payment from a Sublicensee, provided however, with respect to any qualifying payments received by the Company from a Sublicensee prior to January 1, 2025, the payment to Licensor of any such Sublicensee Percentage is due to Licensor by March 31, 2025. The parties also agreed to a revised annual license maintenance fee due each year (the “Maintenance Fee”) starting in 2023 through 2028, as follows: $

On December 22, 2023, Clearside Biomedical, Inc., through its wholly owned subsidiary Royalty Sub, entered into a letter agreement (the “Letter Agreement”) with HCR (as defined below) and HCR Clearside SPV, LLC (as assignee of HCR Collateral Management, LLC) (“Agent”) amending that certain Purchase and Sale Agreement, dated as of August 8, 2022, by and among Royalty Sub, HCR and Agent ("Purchase and Sale Agreement"). Pursuant to the terms of the Letter Agreement, Royalty Sub and Agent mutually agreed that Royalty Sub waived any and all rights to the $

On November 1, 2023, the Company, entered into a license agreement (the “BioCryst License Agreement”) with BioCryst Pharmaceuticals, Inc. (“BioCryst”) pursuant to which the Company granted BioCryst an exclusive, worldwide and sublicensable license to the Company’s SCS Microinjector for the delivery of BioCryst’s proprietary plasma kallikrein inhibitor known as avoralstat for the treatment and prevention of diabetic macular edema (“DME”). The Company received an upfront license fee payment of $

7

sales, with the highest royalty rate applied to sales over $

In May 2023, the Company terminated its at-the-market sales agreement with Cowen and Company, LLC (the "ATM Agreement"). The Company sold

In May 2023, the Company entered into a Controlled Equity OfferingSM Sales Agreement (the "Sales Agreement") with Cantor Fitzgerald & Co. ("Cantor") under which the Company may offer and sell, from time to time at its sole discretion, shares of its common stock, having an aggregate offering price of up to $

The Company has suffered recurring losses and negative cash flows from operations since inception and anticipates incurring additional losses until such time, if ever, that it can generate significant revenue. The Company has no current source of revenue to sustain present activities. The Company does not expect to generate other meaningful revenue until and unless the Company's licensees successfully commercialize XIPERE and the Company has fulfilled its obligations under the Purchase and Sale Agreement, its other licensees receive regulatory approval and successfully commercialize its product candidates, or the Company commercializes its product candidates either on its own or with a third party. In the absence of product or other revenues, the amount, timing, nature or source of which cannot be predicted, the Company’s losses will continue as it conducts its research and development activities.

The Company will continue to need to obtain additional financing to fund future operations, including completing the development, partnering and potential commercialization of its primary product candidates. The Company will need to obtain financing to complete the development and conduct clinical trials for the regulatory approval of its product candidates if requested by regulatory bodies. If such product candidates were to receive regulatory approval, the Company would need to obtain financing to prepare for the potential commercialization of its product candidates, if the Company decides to commercialize the products on its own.

Based on its current plans and forecasted expenses, the Company expects that its cash and cash equivalents as of the filing date, May 10, 2024 will enable the Company to fund its planned operating expenses and capital expenditure requirements into the third quarter of 2025. The Company has based this estimate on assumptions that may prove to be wrong, and it could exhaust its capital resources sooner than expected. Until the Company can generate sufficient revenue, the Company will need to finance future cash needs through public or private equity offerings, license agreements, debt financings or restructurings, collaborations, strategic alliances and marketing or distribution arrangements.

2. Significant Accounting Policies

Basis of Presentation and Principles of Consolidation

The Company's consolidated financial statements include the results of the financial operations of Clearside Biomedical, Inc. and its wholly-owned subsidiary, Clearside Royalty, LLC. a Delaware limited liability company, which was formed for the purposes of the transactions contemplated by the Purchase and Sale Agreement described in Note 5. All intercompany balances and transactions have been eliminated.

The Company’s consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“U.S. GAAP”). In the opinion of management, the Company has made all necessary adjustments, which include normal recurring adjustments necessary for a fair statement of the Company’s consolidated financial position and results of operations for the interim periods presented. The results for the three months ended March 31, 2024 are not indicative of results to be expected for the year ending December 31, 2024, any other interim periods or any future year or period. These unaudited financial statements should be read in conjunction with the audited financial statements and related footnotes, which are included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2023.

Use of Estimates

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and reported amounts of income and expenses during the reporting periods. Significant items subject to such estimates and assumptions include the estimate of the total amount of future royalty revenue and milestone payments to be generated over the life of the Purchase and Sale Agreement, revenue recognition, the accounting for useful lives to calculate depreciation and amortization, clinical trial expense accruals, share-based compensation expense and income tax valuation allowance. Actual results could differ from these estimates.

Revenue Recognition

8

The Company recognizes revenue from its contracts with customers under Financial Accounting Standards Board Accounting Standards Codification (“ASC”) Topic 606, Revenue from Contracts with Customers. The Company’s primary revenue arrangements are license agreements, which typically include upfront payments, regulatory and commercial milestone payments and royalties based on future product sales. The arrangements may also include payments for the Company’s SCS Microinjector devices as well as payments for assistance and oversight of the customer’s use of the Company’s technology. In determining the amount of revenue to be recognized under these agreements, the Company performs the following steps: (i) identifies the promised goods and services to be transferred in the contract, (ii) identifies the performance obligations, (iii) determines the transaction price, (iv) allocates the transaction price to the performance obligations and (v) recognizes revenue as the performance obligations are satisfied.

The Company receives payments from its customers based on billing schedules established in each contract. Upfront and other payments may require deferral of revenue recognition to a future period until the Company performs its obligations under the arrangement. Amounts are recorded as accounts receivable when the Company’s right to consideration is unconditional. The Company does not assess whether a contract has a significant financing component if the expectation at contract inception is such that the period between payment by the customer and the transfer of the promised goods or services to the customer will be one year or less.

Research and Development Costs

Research and development costs are charged to expense as incurred and include:

Costs for certain development activities, such as clinical trial activities, are recognized based on an evaluation of the estimated total costs for the clinical trial, progress to completion of specific tasks using data such as patient enrollment, pass-through expenses, clinical site activations, data from the clinical sites or information provided to the Company by its vendors on their actual costs incurred. Payments for these activities are based on the terms of the individual contracts and any subsequent amendments, which may differ from the patterns of costs incurred, and are reflected in the financial statements as prepaid or accrued expenses.

Share-Based Compensation

Compensation cost related to share-based awards granted to employees, directors and consultants is measured based on the estimated fair value of the award at the grant date. The Company estimates the fair value of stock options using a Black-Scholes option pricing model. The fair value of restricted stock units granted is measured based on the market value of the Company’s common stock on the date of grant. Share-based compensation costs are expensed on a straight-line basis over the relevant vesting period.

Compensation cost related to shares purchased through the Company’s employee stock purchase plan, which is considered compensatory, is based on the estimated fair value of the shares on the offering date, including consideration of the discount and the look-back period. The Company estimates the fair value of the shares using a Black-Scholes option pricing model. Compensation expense is recognized over the six-month withholding period prior to the purchase date.

All share-based compensation costs are recorded in general and administrative or research and development costs in the statements of operations based upon the recipient's underlying role within the Company.

Cash Equivalents

Cash equivalents consist of short-term, highly liquid investments with an original term of three months or less at the date of purchase.

9

Concentration of Credit Risk Arising From Cash Deposits in Excess of Insured Limits

The Company maintains its cash in bank deposits that at times may exceed federally insured limits. The Company has not experienced any loss in such accounts. The Company believes it is not exposed to any significant risks with respect to its cash balances.

Liability Related to the Sales of Future Royalties and Non-Cash Interest Expense

In connection with the Purchase and Sale Agreement, the Company recognizes a liability related to the sales of future royalties under ASC 470-10 Debt and ASC 835-30 Interest - Imputation of Interest. The initial funds received by the Company pursuant to the terms of the Purchase and Sale Agreement were recorded as a liability and are accreted under the effective interest method up to the estimated amount of future royalties and milestone payments to be made under the Purchase and Sale Agreement. The issuance costs were recorded as a direct deduction to the carrying amount of the liability and are amortized under the effective interest method over the estimated period the liability will be repaid. The Company estimates the total amount of future royalty revenue and milestone payments to be generated over the life of the Purchase and Sale Agreement, and a significant increase or decrease in these estimates could materially impact the liability balance and the related interest expense. If the timing of the receipt of royalty payments or milestones is materially different from the original estimates, the Company will prospectively adjust the effective interest and the related amortization of the liability and related issuance costs.

Warrant Liabilities

The Company accounts for warrants as either equity-classified or liability-classified instruments based on an assessment of the warrant’s specific terms and applicable authoritative guidance in FASB ASC Topic 480, Distinguishing Liabilities from Equity (ASC 480) and FASB ASC Topic 815, Derivatives and Hedging (ASC 815). The assessment considers whether the warrants (i) are freestanding financial instruments pursuant to ASC 480, (ii) meet the definition of a liability pursuant to ASC 480, and (iii) meet all of the requirements for equity classification under ASC 815, including whether the warrants are indexed to the Company's own stock and whether the warrant holders could potentially require “net cash settlement” in a circumstance outside of the Company’s control, among other conditions for equity classification. This assessment, which requires the use of professional judgment, is conducted at the time of warrant issuance and as of each subsequent quarterly period end date while the warrants are outstanding.

For warrants that meet all criteria for equity classification, the warrants are required to be recorded as a component of additional paid-in capital, on the consolidated statement of stockholders’ deficit at the time of issuance. For warrants that do not meet all the criteria for equity classification, the warrants are required to be recorded at their initial fair value on the date of issuance and on each balance sheet date thereafter.

The Company’s warrant liabilities are measured at fair value using a simulation model which takes into account, as of the valuation date, factors including the current exercise price, the expected life of the warrant, the current price of the Company's common stock, the expected volatility, holding cost, the risk-free interest rate for the term of the warrant and the likelihood of achieving certain future milestone events and the related impact to the price of the Company's common stock. The warrant liability is revalued at each reporting period and changes in fair value are recognized in other expense in the consolidated statements of operations. The selection of the appropriate valuation model and the inputs and assumptions that are required to determine the valuation requires significant judgment and requires management to make estimates and assumptions that affect the reported amount of the related liability and reported amounts of the change in fair value. Actual results could differ from those estimates, and changes in these estimates are recorded when known.

3. Property and Equipment, Net

Property and equipment, net consisted of the following (dollar amounts in thousands):

|

|

Estimated |

|

March 31, |

|

|

December 31, |

|

||

Furniture and fixtures |

|

|

$ |

|

|

$ |

|

|||

Machinery and equipment |

|

|

|

|

|

|

|

|||

Computer equipment |

|

|

|

|

|

|

|

|||

Leasehold improvements |

|

|

|

|

|

|

|

|

||

Work in process |

|

|

|

|

|

|

|

|

||

Total property and equipment |

|

|

|

|

|

|

|

|

||

Less: Accumulated depreciation |

|

|

|

|

( |

) |

|

|

( |

) |

Property and equipment, net |

|

|

|

$ |

|

|

$ |

|

||

10

4. Accrued Liabilities

Accrued liabilities consisted of the following (in thousands):

|

|

March 31, |

|

|

December 31, |

|

||

|

|

2024 |

|

|

2023 |

|

||

Accrued research and development |

|

$ |

|

|

$ |

|

||

Accrued employee costs |

|

|

|

|

|

|

||

Accrued professional fees |

|

|

|

|

|

|

||

Accrued expense |

|

|

|

|

|

|

||

|

|

$ |

|

|

$ |

|

||

5. Royalty Purchase and Sale Agreement

On August 8, 2022 (the “Closing Date”), the Company, through its wholly owned subsidiary Clearside Royalty LLC, a Delaware limited liability company ("Royalty Sub"), entered into the Purchase and Sale Agreement with entities managed by HealthCare Royalty Management, LLC ("HCR"), pursuant to which Royalty Sub sold to HCR certain of its rights to receive royalty and milestone payments payable to Royalty Sub under the Arctic Vision License Agreement, the Bausch License Agreement, that certain License Agreement, effective as of July 3, 2019, by and between the Company and Aura Biosciences, Inc. (the “Aura License Agreement”), that certain Option and License Agreement, dated as of August 29, 2019, by and between REGENXBIO Inc. and the Company (the “REGENXBIO License Agreement”) and any and all out-license agreements following the Closing Date for, or related to XIPERE or the SCS Microinjector technology (to be used in connection with compounds or products of any third parties) delivered, in whole or in part, by means of the SCS Microinjector technology), excluding, for the avoidance of doubt, any in-licensed or internally developed therapies following the Closing Date (collectively, the “Royalties”), in exchange for up to $

Under the terms of the Purchase and Sale Agreement, Royalty Sub received an initial payment of $

On December 22, 2023, the Company, through its wholly owned subsidiary Royalty Sub, entered into the Letter Agreement with the Agent amending the Purchase and Sale Agreement. Pursuant to the terms of the Letter Agreement, Royalty Sub and Agent mutually agreed that Royalty Sub waived any and all rights to the First Milestone Payment in connection with the closing of the transactions contemplated by the Purchase and Sale Agreement and agreed to the release of the First Milestone Payment to Agent.

Issuance costs pursuant to the Purchase and Sale Agreement consisting primarily of advisory and legal fees, totaled $

11

The following table summarizes the activity of the Purchase and Sale Agreement for the three months ended March 31, 2024 (in thousands):

Royalty Purchase and Sale Agreement balance at December 31, 2023 |

|

$ |

|

|

Non-cash interest expense |

|

|

|

|

Balance at March 31, 2024 |

|

$ |

|

|

|

|

|

|

|

Effective interest rate |

|

|

% |

|

6. Common Stock

The Company’s amended and restated certificate of incorporation authorizes the Company to issue

7. Common Stock Warrants

In September 2016, in connection with a loan agreement, the Company issued warrants to purchase up to

On February 6, 2024, the Company entered into a securities purchase agreement with institutional investors and an existing stockholder, pursuant to which the Company issued and sold, in a registered direct offering (i) an aggregate of

The following table summarizes the change in fair value of the warrant liabilities during the three months ended March 31, 2024 (in thousands):

Fair value of warrants at issuance February 9, 2024 |

|

$ |

|

|

Change in fair value during the period |

|

|

|

|

Fair value of warrants at March 31, 2024 |

|

$ |

|

The following table summarizes certain key inputs for the valuation of the Warrants at March 31, 2024:

Common stock price |

|

$ |

|

|

|

Exercise price per share |

|

$ |

|

|

|

Expected volatility |

|

|

|

% |

|

Risk-free interest rate |

|

|

|

% |

|

Contractual term (in years) |

|

|

|

|

|

Expected dividend yield |

|

|

|

% |

8. Share-Based Compensation

Share-based compensation is accounted for in accordance with the provisions of ASC 718, Compensation-Stock Compensation.

Stock Options

The Company has granted stock option awards to employees, directors and consultants from its 2011 Stock Incentive Plan (the “2011 Plan”) and its 2016 Equity Incentive Plan (the “2016 Plan”). The estimated fair value of options granted is determined as of the date of grant using the Black-Scholes option pricing model. The resulting fair value is recognized ratably over the requisite service period, which is generally the vesting period of the awards.

12

Share-based compensation expense for options granted under the 2016 Plan is reflected in the statements of operations as follows (in thousands):

|

|

Three Months Ended |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Research and development |

|

$ |

|

|

$ |

|

||

General and administrative |

|

|

|

|

|

|

||

Total |

|

$ |

|

|

$ |

|

||

The following table summarizes the activity related to stock options granted under the 2011 Plan and the 2016 Plan during the three months ended March 31, 2024:

|

|

|

|

|

Weighted |

|

||

|

|

Number of |

|

|

Average |

|

||

|

|

Shares |

|

|

Exercise Price |

|

||

Options outstanding at December 31, 2023 |

|

|

|

|

$ |

|

||

Granted |

|

|

|

|

|

|

||

Exercised |

|

|

( |

) |

|

|

|

|

Forfeited |

|

|

( |

) |

|

|

|

|

Options outstanding at March 31, 2024 |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||

Options exercisable at December 31, 2023 |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||

Options exercisable at March 31, 2024 |

|

|

|

|

|

|

||

As of March 31, 2024, the Company had $

Restricted Stock Units

The Company has granted restricted stock units (“RSUs”) to employees under the 2016 Plan. The shares underlying the RSU awards have vesting terms of four years from the date of grant subject to the employees’ continuous service and subject to accelerated vesting in specified circumstances. The fair value of the RSUs granted is measured based on the market value of the Company’s common stock on the date of grant and is recognized ratably over the requisite service period, which is generally the vesting period of the awards.

The total share-based compensation expense related to RSUs is reflected in the statements of operations as follows (in thousands):

|

|

Three Months Ended |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Research and development |

|

$ |

|

|

$ |

|

||

General and administrative |

|

|

|

|

|

|

||

Total |

|

$ |

|

|

$ |

|

||

The following table summarizes the activity related to RSUs during the three months ended March 31, 2024:

|

|

|

|

|

Weighted Average |

|

||

|

|

Number of |

|

|

Grant Date |

|

||

|

|

Shares |

|

|

Fair Value |

|

||

Non-vested RSUs outstanding at December 31, 2023 |

|

|

|

|

$ |

|

||

Vested |

|

|

( |

) |

|

|

|

|

Non-vested RSUs outstanding at March 31, 2024 |

|

|

|

|

|

|

||

As of March 31, 2024, the Company had $

13

Employee Stock Purchase Plan

The 2016 Employee Stock Purchase Plan (the “2016 ESPP”) became effective on June 1, 2016. The 2016 ESPP is considered a compensatory plan and the fair value of the discount and the look-back period are estimated using the Black-Scholes option pricing model and expense is recognized over the six-month withholding period prior to the purchase date.

The share-based compensation expense recognized for the 2016 ESPP is reflected in the statements of operations as follows (in thousands):

|

|

Three Months Ended |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Research and development |

|

$ |

|

|

$ |

|

||

General and administrative |

|

|

|

|

|

|

||

Total |

|

$ |

|

|

$ |

|

||

During the three months ended March 31, 2024, the Company issued

9. Commitments and Contingencies

Lease Commitment Summary

In November 2022, the Company signed an amended office lease agreement to lease approximately

The Company recognizes a right-of-use asset for the right to use the underlying asset for the lease term, and a lease liability, which represents the present value of the Company’s obligation to make payments over the lease term.

Equipment leases with an initial term of 12 months or less are not recorded with operating lease liabilities. The Company recognizes expense for these leases on a straight-line basis over the lease term. The equipment leases were deemed to be immaterial.

Georgia Tech License Agreement

As described in Note 1, the Company entered into a fourth amendment to the Georgia Tech License Agreement pursuant to which the parties agreed to revised Maintenance Fee payments. The Company paid the Maintenance Fee for 2023 in February 2024.

Year Ending December 31, |

|

Amount |

|

|

2024 |

|

$ |

|

|

2025 |

|

|

|

|

2026 |

|

|

|

|

2027 |

|

|

|

|

2028 |

|

|

|

|

Total |

|

$ |

|

|

Contract Service Providers

In the course of the Company’s normal business operations, it has agreements with contract service providers to assist in the performance of its research and development, clinical research and manufacturing. Substantially all of these contracts are on an as needed basis.

10. License and Other Agreements

Bausch + Lomb

On October 22, 2019, the Company entered into a License Agreement (as amended, the "Bausch License Agreement") with Bausch + Lomb (“Bausch”). Pursuant to the Bausch License Agreement, the Company has granted an exclusive license to Bausch to develop, manufacture, distribute, promote, market and commercialize XIPERE using the Company’s proprietary SCS Microinjector (the “Device”), as well as specified other steroids, corticosteroids and NSAIDs in combination with the Device (together with

14

XIPERE, the “Products”), subject to specified exceptions, in the United States and Canada (the “Territory”) for the treatment of ophthalmology indications, including non-infectious uveitis.

Pursuant to the Bausch License Agreement, Bausch paid the Company an aggregate of $

Arctic Vision (Hong Kong) Limited

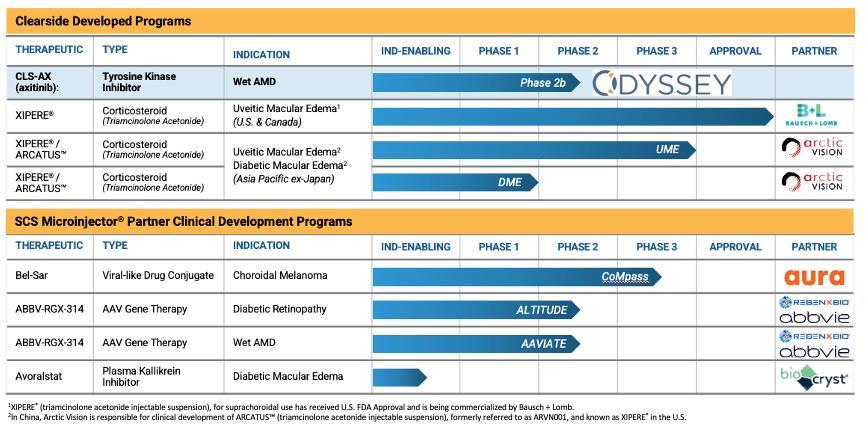

On March 10, 2020, the Company entered into a License Agreement (the “Arctic License Agreement”) with Arctic Vision (Hong Kong) Limited (“Arctic Vision”). Pursuant to the Arctic License Agreement, the Company has granted an exclusive license to Arctic Vision to develop, distribute, promote, market and commercialize XIPERE, subject to specified exceptions, in China, Hong Kong, Macau, Taiwan and South Korea (the “Arctic Territory”). Under the terms of the Arctic License Agreement, neither party may commercialize XIPERE in the other party’s territory. Arctic Vision has agreed to use commercially reasonable efforts to pursue the development and commercialization of XIPERE for indications associated with uveitis in the Arctic Territory. In addition, upon receipt of the Company’s consent, Arctic Vision will have the right, but not the obligation, to develop and commercialize XIPERE for additional indications in the Arctic Territory.

Pursuant to the Arctic License Agreement, Arctic Vision has paid the Company an aggregate of $

In August 2021, the Company entered into an amendment to the Arctic License Agreement to expand the territories covered by the license to include India and the ASEAN Countries (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam). In September 2021, the Company entered into a second amendment to the Arctic Vision License Agreement to expand the Arctic Territory to include Australia and New Zealand. The Company received an aggregate of $

BioCryst Pharmaceuticals, Inc.

On November 1, 2023, the Company entered into the BioCryst License Agreement pursuant to which the Company granted BioCryst an exclusive, worldwide and sublicensable license to the Company’s SCS Microinjector for the delivery of BioCryst’s proprietary plasma kallikrein inhibitor known as avoralstat for the treatment and prevention of DME.

The Company received an upfront license fee payment of $

BioCryst will be responsible for all development, regulatory and commercialization activities for avoralstat. The Company is responsible for supplying SCS Microinjectors to meet BioCryst’s reasonable needs.

15

Other

The Company periodically enters into short-term agreements with other customers to evaluate the potential use of its proprietary SCS Microinjector with third-party product candidates for the treatment of various diseases. Funds received from these agreements are recognized as revenue over the term of the agreement.

11. Fair Value Measurements

The Company’s material financial instruments at March 31, 2024 and December 31, 2023 consisted primarily of cash and cash equivalents. The fair values of cash and cash equivalents, other current assets and accounts payable approximate their respective carrying values due to the short term nature of these instruments and are classified as Level 1 in the fair value hierarchy. The fair value of the liability related to the sales of future royalties (see Note 5) approximates the carrying value and is classified as Level 1 in the fair value hierarchy. The fair value of the warrant liabilities (see Note 7) require significant unobservable inputs and is classified as Level 3 in the fair value hierarchy.

There were

12. Related Party Transactions

A member of the Company's Board of Directors is chief executive officer of a company that is a vendor of the Company. As of March 31, 2024, the Company has recorded $

The chair of the board of directors of BioCryst also serves on the Company’s Board of Directors. For the three months ended March 31, 2024, the Company has recorded $

13. Net Loss Per Share

Basic net loss per share is calculated by dividing the net loss by the weighted average number of shares of common stock outstanding for the period, without consideration of the dilutive effect of potential common stock equivalents. Diluted net loss per share gives effect to all dilutive potential shares of common stock outstanding during this period. For all periods presented, the Company’s potential common stock equivalents, which included stock options, restricted stock units and common stock warrants, have been excluded from the computation of diluted net loss per share as their inclusion would have the effect of reducing the net loss per share. Therefore, the denominator used to calculate both basic and diluted net loss per share is the same in all periods presented.

|

|

Three Months Ended |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

Outstanding stock options |

|

|

|

|

|

|

||

Non-vested restricted stock units |

|

|

|

|

|

|

||

Common stock warrants |

|

|

|

|

|

|

||

|

|

|

|

|

|

|

||

16

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

Certain statements contained in this Quarterly Report on Form 10-Q may constitute forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. The words or phrases “would be,” “will allow,” “intends to,” “will likely result,” “are expected to,” “will continue,” “is anticipated,” “estimate,” “project,” or similar expressions, or the negative of such words or phrases, are intended to identify “forward-looking statements.” We have based these forward-looking statements on our current expectations and projections about future events. Because such statements include risks and uncertainties, actual results may differ materially from those expressed or implied by such forward-looking statements. Factors that could cause or contribute to these differences include those below and elsewhere in this Quarterly Report on Form 10-Q and our other filings with the Securities and Exchange Commission, or SEC, under the heading “Risk Factors”. Statements made herein are as of the date of the filing of this Form 10-Q with the SEC and should not be relied upon as of any subsequent date. Unless otherwise required by applicable law, we do not undertake, and we specifically disclaim, any obligation to update any forward-looking statements to reflect occurrences, developments, unanticipated events or circumstances after the date of such statement.

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited financial statements and related notes that appear in Item 1 of this Quarterly Report on Form 10-Q and with our audited financial statements and related notes for the year ended December 31, 2023 appearing in our Annual Report on Form 10-K filed with the SEC on March 12, 2024.

Overview

We are a biopharmaceutical company focused on revolutionizing the delivery of therapies to the back of the eye through the suprachoroidal space, or SCS®. Our novel SCS injection platform, utilizing our proprietary SCS Microinjector®, enables an in-office, repeatable, non-surgical procedure for the targeted and compartmentalized delivery of a wide variety of therapies to the macula, retina or choroid to potentially preserve and improve vision in patients with sight-threatening eye diseases. Our SCS injection platform can be used in conjunction with existing drugs designed for delivery to the SCS, novel therapies and future therapeutic innovations. We believe our proprietary suprachoroidal administration platform has the potential to become a standard for delivery of therapies intended to treat chorioretinal diseases.

We are leveraging our SCS injection platform by building an internal research and development pipeline targeting retinal diseases and by creating external collaborations with other companies. We are developing our own pipeline of small molecule product candidates for administration via our SCS Microinjector, and we also strategically partner with companies developing other ophthalmic therapeutic innovations to be administered using our SCS injection platform. Our first product, XIPERE® (triamcinolone acetonide injectable suspension) for suprachoroidal use, was approved by the U.S. Food and Drug Administration, or the FDA, in October 2021. Approval of XIPERE was a significant milestone for us as it is the first approved therapeutic delivered into the SCS, the first commercial product developed by us and the first therapy for macular edema associated with uveitis. We believe that we are creating a broad therapeutic platform for developing product candidates to treat serious eye diseases.

17

The current development status of our pipeline of internal product candidates and external collaborations is summarized in the chart below:

Clinical Development Pipeline

CLS-AX (axitinib injectable suspension)

CLS-AX, our most advanced product candidate, is our proprietary suspension of the TKI axitinib for suprachoroidal injection delivered via our SCS Microinjector. We are developing CLS-AX for administration to the SCS as a long-acting therapy for neovascular age-related macular degeneration (wet AMD), a retinal degenerative disease that causes a progressive loss of central vision.

In February 2023, we announced the final, positive results from the OASIS Phase 1/2a clinical trial in wet AMD. CLS-AX was well-tolerated and demonstrated a favorable safety profile across all cohorts. The full extension data for Cohorts 3 and 4 showed promising durability and signs of biological effect.

Based on the results from the OASIS trial, we are conducting a randomized, controlled, double-masked, Phase 2b clinical trial of CLS-AX for the treatment of wet AMD, which we refer to as ODYSSEY. ODYSSEY will compare CLS-AX suprachoroidal injection and aflibercept intravitreal injection over 36 weeks and is expected to have 60 total participants with a 2:1 randomization. The primary outcome measure is a mean change in best-corrected visual acuity from baseline to week 36. The secondary outcome measures are changes in visual function and ocular anatomy, the need for supplemental treatment and treatment burden as measured by total injections over the trial duration. We began enrolling participants in May 2023 and randomized our first participants in July 2023. On October 31, 2023, we completed the recruitment of participants. The final participant was randomized to the CLS-AX treatment of the aflibercept comparator arm in December 2023. We expect to report topline data at the end of the third quarter of 2024.

Preclinical

We have an experienced team of scientists and researchers evaluating small molecules that may be utilized as potential treatment options for back of the eye diseases utilizing our SCS Microinjector for delivery in the suprachoroidal space.

External Collaborations Pipeline

In order to expand the global reach of our suprachoroidal injection platform, we have strategically partnered some of our assets for development and/or commercialization and intend to continue partnering our assets. By entering into these partnerships, we have

18

been able to expand the use of our suprachoroidal injection platform to other indications and geographies globally. We currently have collaborations with Bausch Health, Arctic Vision, REGENXBIO, Inc., Aura Biosciences and BioCryst Pharmaceuticals, Inc.

Commercial Product

XIPERE® (triamcinolone acetonide injectable suspension) for suprachoroidal use, was approved by the FDA in October 2021. XIPERE is the first approved therapeutic delivered into the SCS, the first commercial product developed by us and the first therapy for macular edema associated with uveitis. XIPERE commercialization rights are licensed to Bausch + Lomb in the United States and Canada and Arctic Vision in Asia, not including Japan.

ISO and EC Certifications

We have received the International Organization for Standardization (ISO) Certification EN ISO 13485:2016 for “The design, development, and manufacture of sterile piston syringes, needles, and associated accessories for the area of ophthalmology.” The certificate is available on our website. The information contained on our website is not incorporated by reference into this Quarterly Report on Form 10-Q.

We have received European Community (EC) Certification for the SCS Microinjector from our Notified Body, Intertek Medical Notified Body, AB. The Certificate of Conformance with the Medical Device Regulation 2017/745, Annex IV was issued July 21, 2023, with the Intended Purpose of the SCS Microinjector as "delivery of triamcinolone acetonide injectable suspension, 40 mg/mL to the suprachoroidal space of the eye".

Recent Developments

In February 2024, we entered into a securities purchase agreement, or the Purchase Agreement, with institutional investors and an existing stockholder, pursuant to which we agreed to issue and sell, in a registered direct offering (i) an aggregate of 11,111,111 shares of common stock; and (ii) warrants to purchase up to 11,111,111 shares of common stock, or the Warrants, for net proceeds of $13.9 million.

On March 14, 2024, we appointed Victor Chong, M.D., MBA to serve as our Chief Medical Officer. On April 15, 2024, we appointed Anthony S. Gibney to serve on our board of directors as a Class III director whose term will expire at our 2025 annual meeting of stockholders.

Operating Outlook

We have incurred net losses since our inception. In recent years, our operations have consisted primarily of conducting preclinical studies and clinical trials, raising capital and undertaking other research and development initiatives. To date, we primarily generated revenue through upfront payments and milestone payments related to license agreements and from collaboration agreements, and we have primarily financed our operations through public offerings and private placements of our equity securities, issuances of convertible promissory notes and loan agreements. As of March 31, 2024, we had an accumulated deficit of $332.7 million. We recorded net losses of $11.8 million and $9.3 million for the three months ended March 31, 2024 and 2023, respectively. We anticipate that a substantial portion of our capital resources and efforts in the foreseeable future will be focused on completing the necessary development for and obtaining regulatory approval of our product candidates, as well as discovering compounds and developing proprietary formulations to utilize with our SCS Microinjector.

We expect to continue to incur significant and increasing operating losses at least for the next several years. We do not expect to generate significant product or license and other revenue unless and until XIPERE is successfully commercialized by our licensees or until we successfully complete the development of, obtain regulatory approval for and commercialize additional product candidates, either on our own or together with a third party. Our financial results may fluctuate significantly from quarter to quarter and year to year, depending on the timing of our clinical trials and our expenditures on other research and development activities. We expect clinical trial expenses to increase in the remainder of 2024 as a result of our Phase 2b clinical trial of CLS-AX, as well as continuing our pipeline development. We also will continue our efforts to discover, research and develop additional product candidates and obtain regulatory approvals in additional regions for XIPERE for the treatment of macular edema associated with uveitis.

Macroeconomic Conditions

Unfavorable conditions in the economy in the United States and abroad may negatively affect the growth of our business and our results of operations. For example, macroeconomic events, rising inflation, the U.S. Federal Reserve raising interest rates, and conflicts in Ukraine, Russia and the Middle East have led to economic uncertainty globally. The effect of macroeconomic conditions may not be fully reflected in our results of operations until future periods. If, however, economic uncertainty increases or the global economy worsens, our business, financial condition and results of operations may be harmed. For further discussion of the potential impacts of macroeconomic events on our business, financial condition, and operating results, see “Risk Factors” included in Part I, Item 1A of the Annual Report on Form 10-K filed with the SEC on March 12, 2024.

19

Components of Operating Results

License and Other Revenue

We have not generated any revenue from the sale of XIPERE and we do not expect to generate any other product revenue unless or until we obtain regulatory approval for and commercialize our other product candidates, either on our own or with a third party. The revenue received under the Bausch license agreement, as well as other certain payments from our licensees, will be recorded as non-cash revenue until we have fulfilled our obligations under the Purchase and Sale Agreement. Our revenue in recent years has been generated primarily from our license agreements. We are seeking to enter into additional licenses and other agreements with third parties to evaluate the potential use of our proprietary SCS Microinjector with the third party’s product candidates for the treatment of various eye diseases. These agreements may include payments to us for technology access, upfront license payments, regulatory and commercial milestone payments and royalties.

Research and Development

Research and development expenses consist primarily of costs incurred for the research and development of our preclinical and clinical product candidates, which include:

We expense research and development costs to operations as incurred. These costs include preclinical activities, such as manufacturing and stability and toxicology studies, that are supportive of the product candidate itself. In addition, there are expenses related to clinical trials and similar activities for each program, including costs associated with CROs. Clinical costs are recognized based on the terms of underlying agreements, as well as an evaluation of the progress to completion of specific tasks using data such as patient enrollment, clinical site activations and additional information provided to us by our vendors about their actual costs incurred. Expenses related to activities that support more than one development program or activity, such as salaries, share-based compensation and depreciation, are not classified as direct preclinical costs or clinical costs and are separately classified as unallocated.

The following table shows our research and development expenses by program for the three months ended March 31, 2024 and 2023 (in thousands).

|

|

Three Months Ended |

|

|||||

|

|

2024 |

|

|

2023 |

|

||

XIPERE (uveitis program) |

|

$ |

52 |

|

|

$ |

28 |

|

CLS-AX (wet AMD program) |

|

|

2,258 |

|

|

|

1,359 |

|

Total |

|

|

2,310 |

|

|

|

1,387 |

|

Unallocated |

|

|

3,305 |

|

|

|

3,064 |

|

Total research and development expense |

|

$ |

5,615 |

|

|

$ |

4,451 |

|

Our expenses related to clinical trials are based on estimates of patient enrollment and related expenses at clinical investigator sites as well as estimates for the services received and efforts expended under contracts with research institutions, consultants and CROs that conduct and manage clinical trials on our behalf. We generally accrue expenses related to clinical trials based on contracted amounts applied to the level of patient enrollment and activity according to the protocol. If future timelines or contracts are modified based upon changes in the clinical trial protocol or scope of work to be performed, we would modify our estimates of accrued expenses accordingly on a prospective basis.

Research and development activities are central to our business model. Product candidates in later stages of clinical development generally have higher development costs than those in earlier stages of clinical development, primarily due to the

20

increased size and duration of later-stage clinical trials. However, it is difficult to determine with certainty the duration and completion costs of our current or future preclinical programs and clinical trials of our product candidates, or if, when, or to what extent we will generate revenues from the commercialization and sale of any of our product candidates that obtain regulatory approval. We may never succeed in achieving regulatory approval for any of our current or future product candidates.

The duration, costs and timing of clinical trials and development of our product candidates will depend on a variety of factors that may include, among others:

In addition, the probability of success for each product candidate will depend on numerous factors, including competition, manufacturing capability and commercial viability. We will determine which programs to pursue and how much to fund each program in response to the scientific and clinical success of each product candidate, as well as an assessment of each product candidate’s commercial potential.

General and Administrative

General and administrative expenses consist primarily of salaries and other related costs, including share-based compensation, for personnel in executive, finance and administrative functions. General and administrative costs historically included commercial pre-launch preparations for XIPERE, and also include facility related costs not otherwise included in research and development expenses, as well as professional fees for legal, patent, consulting, and accounting and audit services.

Interest Income

Interest income consists of the accrued interest and interest income earned on our cash and cash equivalents. Interest income is not considered significant to our financial statements.

Other Expense

Other expense consists of expenses allocated to the warrants issued in connection with our registered direct offering in February 2024 and the change in fair value during the period.

Non-cash Interest Expense on Liability Related to the Sales of Future Royalties

Non-cash interest expense on liability related to the sales of future royalties consists of imputed interest on the carrying value of the liability and the amortization of the related issuance costs.

Critical Accounting Policies and Significant Judgments and Estimates

Our management’s discussion and analysis of our financial condition and results of operations is based on our consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States of America, or U.S. GAAP. The preparation of these consolidated financial statements requires us to make estimates, judgments and assumptions that affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities as of the dates of the balance sheets and the reported amounts of expenses during the reporting periods. In accordance with U.S. GAAP, we evaluate our estimates and judgments on an ongoing basis. Significant estimates include assumptions used in the determination of share-based

21

compensation and some of our research and development expenses. We base our estimates on historical experience and on various other factors that we believe are reasonable under the circumstances, the results of which form the basis for making judgments about the carrying value of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates under different assumptions or conditions.

We define our critical accounting policies as those accounting principles generally accepted in the United States of America that require us to make subjective estimates and judgments about matters that are uncertain and are likely to have a material impact on our financial condition and results of operations, as well as the specific manner in which we apply those principles. During the three months ended March 31, 2024, there were no significant changes to our critical accounting policies disclosed in our audited financial statements for the year ended December 31, 2023, which are included in our Annual Report on Form 10-K, as filed with the SEC on March 12, 2024, other than the warrant liabilities discussed in Note 2 to the consolidated financial statements.

Results of Operations for the Three Months Ended March 31, 2024 and 2023

The following table sets forth our results of operations for the three months ended March 31, 2024 and 2023.

|

|

Three Months Ended |

|

|

Period-to-Period |

|

||||||

|

|

2024 |

|

|

2023 |

|

|

Change |

|

|||

|

|

(in thousands) |

|

|||||||||

License and other revenue |

|

$ |

230 |

|

|

$ |

4 |

|

|

$ |

226 |

|

Operating expenses: |

|

|

|

|

|

|

|

|

|

|||

Research and development |

|

|

5,615 |

|

|

|

4,451 |

|

|

|

1,164 |

|

General and administrative |

|

|

2,824 |

|

|

|

3,158 |

|

|

|

(334 |

) |

Total operating expenses |

|

|

8,439 |

|

|

|

7,609 |

|

|

|

830 |

|

Loss from operations |

|

|

(8,209 |

) |

|

|

(7,605 |

) |

|

|

(604 |

) |

Interest income |

|

|

348 |

|

|

|

492 |

|

|

|

(144 |

) |

Other expense |

|

|

(1,499 |

) |

|

|

— |

|

|

|

(1,499 |

) |

Non-cash interest expense on liability |

|

|

(2,403 |

) |

|

|

(2,167 |

) |

|

|

(236 |

) |

Net loss |

|

$ |

(11,763 |

) |

|

$ |

(9,280 |

) |

|

$ |

(2,483 |

) |

License and other revenue. In the three months ended March 31, 2024 and 2023, we recognized $0.2 million and $4,000, respectively, of revenue associated with our license agreements, which includes revenue for services and the sales of our SCS Microinjector kits to our licensees.

Research and development. Research and development expenses increased by $1.2 million from $4.5 million for the three months ended March 31, 2023 to $5.6 million for the three months ended March 31, 2024. This increase was primarily due to a $0.9 million increase in costs related to the CLS-AX program, which includes costs for ODYSSEY, our Phase 2b clinical trial. In addition, there was a $0.4 million research and development tax credit received in the prior year.

General and administrative. General and administrative expenses decreased by $0.3 million, from $3.2 million for the three months ended March 31, 2023 to $2.8 million for the three months ended March 31, 2024. This was primarily attributable to a $0.3 million decrease in professional fees.

Interest income. Interest income for the three months ended March 31, 2024 and 2023 was comprised of interest income from cash and cash equivalents. The decrease is due to the lower balance of our cash and cash equivalents.

Other expense. Other expense for the three months ended March 31, 2024 was due to the increase in fair value of the warrant liabilities from February 9, 2024, the issuance date of the warrants, to March 31, 2024 and the direct registered offering costs that were allocated to the warrants.

Non-cash interest expense on liability related to the sales of future royalties. Non-cash interest expense on liability related to the sales of future royalties for the three months ended March 31, 2024 and 2023 was comprised of imputed interest on the liability related to the sales of future royalties and the amortization of the associated issuance costs.

Liquidity and Capital Resources

Sources of Liquidity

We have funded our operations primarily through the proceeds of public offerings of our common stock, sales of convertible preferred stock and the issuance of long-term debt. As of March 31, 2024, we had cash and cash equivalents of $35.4 million. We

22

invest any cash in excess of our immediate requirements primarily with a view to liquidity and capital preservation. As of March 31, 2024, our funds were held in cash and money market funds.

On February 6, 2024, we entered into the Purchase Agreement, pursuant to which we issued and sold, in a registered direct offering: (i) an aggregate of 11,111,111 shares of our common stock; and (ii) 11,111,111 Warrants. The combined purchase price of each share and accompanying Warrant was $1.35. The exercise price for the Warrants is $1.62 per share. The Warrants will be exercisable from August 9, 2024 and will expire on August 9, 2029. The net proceeds to us from the Registered Direct Offering were $13.9 million.