UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

(Mark One)

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2015

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number: 001-35538

The Carlyle Group L.P.

(Exact name of registrant as specified in its charter)

Delaware | 45-2832612 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

1001 Pennsylvania Avenue, NW Washington, D.C. | 20004-2505 | |

(Address of principal executive offices) | (Zip Code) | |

(202) 729-5626

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common units representing limited partner interests | The NASDAQ Global Select Market | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No ¨

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ý

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act

Large accelerated filer | ý | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ (do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No ý

The aggregate market value of the common units of the Registrant held by non-affiliates as of June 30, 2015 was $2,201,818,205.

The number of the Registrant’s common units representing limited partner interests outstanding as of February 19, 2016 was 81,340,808.

DOCUMENTS INCORPORATED BY REFERENCE

None

1

TABLE OF CONTENTS

Page | ||

ITEM 1. | ||

ITEM 1A. | ||

ITEM 1B. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

ITEM 5. | ||

ITEM 6. | ||

ITEM 7. | ||

ITEM 7A. | ||

ITEM 8. | ||

ITEM 9. | ||

ITEM 9A. | ||

ITEM 9B. | ||

ITEM 10. | ||

ITEM 11. | ||

ITEM 12. | ||

ITEM 13. | ||

ITEM 14. | ||

PART IV. | ||

ITEM 15. | ||

1

Forward-Looking Statements

This report may contain forward-looking statements within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934, which reflect our current views with respect to, among other things, our operations and financial performance. You can identify these forward-looking statements by the use of words such as “outlook,” “believe,” “expect,” “potential,” “continue,” “may,” “will,” “should,” “seek,” “approximately,” “predict,” “intend,” “plan,” “estimate,” “anticipate” or the negative version of these words or other comparable words. Such forward-looking statements are subject to various risks and uncertainties. Accordingly, there are or will be important factors that could cause actual outcomes or results to differ materially from those indicated in these statements. We believe these factors include, but are not limited to, those described under “Risk Factors” in this report, as such factors may be updated from time to time in our periodic filings with the United States Securities and Exchange Commission (the “SEC”), which are accessible on the SEC’s website at www.sec.gov. These factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this report and in our other periodic filings. We undertake no obligation to publicly update or review any forward-looking statement, whether as a result of new information, future developments or otherwise, except as required by law.

Unless the context suggests otherwise, references in this report to “Carlyle,” the “Company,” “we,” “us” and “our” refer to The Carlyle Group L.P. and its consolidated subsidiaries. When we refer to the “partners of The Carlyle Group L.P.,” we are referring specifically to the common unitholders and our general partner and any others who may from time to time be partners of that specific Delaware limited partnership. When we refer to our “senior Carlyle professionals,” we are referring to the partner-level personnel of our firm. References in this report to the ownership of the senior Carlyle professionals and other employees include the ownership of personal planning vehicles of these individuals.

“Carlyle funds,” “our funds” and “our investment funds” refer to the investment funds and vehicles advised by Carlyle. Our “carry funds” refer to (i) those investment funds that we advise, including the buyout funds, growth capital funds, real estate funds, infrastructure funds, certain energy funds and opportunistic credit, distressed debt and mezzanine funds (but excluding our structured credit funds, hedge funds, business development companies, mutual fund, and fund of funds vehicles), where we receive a special residual allocation of income, which we refer to as a carried interest, in the event that specified investment returns are achieved by the fund and (ii) those investment funds advised by NGP Energy Capital Management (together with its affiliates and subsidiaries, “NGP”) from which we are entitled to receive a carried interest. The “NGP management fee funds” refer to those funds advised by NGP from which we only receive an allocation of income based on the funds' management fees. Our “fund of funds vehicles” refers to those funds, accounts and vehicles advised by AlpInvest Partners B.V. (“AlpInvest”), Metropolitan Real Estate Equity Management, LLC (“Metropolitan”), and Diversified Global Asset Management (“DGAM”). For an explanation of the fund acronyms used throughout this Annual Report, refer to “Business—Our Family of Funds.”

“Fee-earning assets under management” or “Fee-earning AUM” refer to the assets we manage or advise from which we derive recurring fund management fees. Our Fee-earning AUM generally equals the sum of:

(a) | for substantially all carry funds and certain co-investment vehicles where the original investment period has not expired, and for Metropolitan fund of funds vehicles during the weighted-average investment period of the underlying funds, the amount of limited partner capital commitments, and for AlpInvest fund of funds vehicles, the amount of external investor capital commitments during the commitment fee period, and for the NGP management fee funds and certain carry funds advised by NGP, the amount of investor capital commitments before the first investment realization; |

(b) | for substantially all carry funds and certain co-investment vehicles where the original investment period has expired and for Metropolitan fund of funds vehicles after the expiration of the weighted-average investment period of the underlying funds, the remaining amount of limited partner invested capital at cost, and for the NGP management fee funds and certain carry funds advised by NGP where the first investment has been realized, the amount of partner commitments less realized and written-off investments; |

(c) | the amount of aggregate fee-earning collateral balance at par of our collateralized loan obligations (“CLOs”), as defined in the fund indentures (typically exclusive of equities and defaulted positions) as of the quarterly cut-off date for each CLO, and the aggregate principal amount of the notes of our other structured products; |

(d) | the net asset value of our mutual fund and the external investor portion of the net asset value (pre-redemptions and subscriptions) of our long/short credit funds, emerging markets, multi-product macroeconomic, fund of hedge funds vehicles and other hedge funds; |

(e) | the gross assets (including assets acquired with leverage), excluding cash and cash equivalents of our business development companies and certain carry funds; and |

(f) | for AlpInvest fund of funds vehicles where the commitment fee period has expired, and certain carry funds where the investment period has expired, the lower of cost or fair value of invested capital. |

“Assets under management” or “AUM” refers to the assets we manage or advise. Our AUM equals the sum of the following:

(a) the fair value of the capital invested in Carlyle carry funds, co-investment vehicles, NGP management fee funds and fund of funds vehicles plus the capital that Carlyle is entitled to call from investors in those funds and vehicles (including Carlyle commitments to those funds and vehicles and those of senior Carlyle professionals and employees) pursuant to the terms of their capital commitments to those funds and vehicles;

(b) | the amount of aggregate collateral balance and principal cash at par or aggregate principal amount of the notes of our CLOs and other structured products (inclusive of all positions); |

(c) | the net asset value (pre-redemptions and subscriptions) of our long/short credit, emerging markets, multi-product macroeconomic, fund of hedge funds vehicles, mutual fund and other hedge funds; and |

(d) | the gross assets (including assets acquired with leverage) of our business development companies. |

We include in our calculation of AUM and Fee-earning AUM certain energy and renewable resources funds that we jointly advise with Riverstone Holdings L.L.C. (“Riverstone”) and certain NGP management fee funds and carry funds that are advised by NGP.

For our carry funds, co-investment vehicles, fund of funds vehicles, and NGP management fee funds, total AUM includes the fair value of the capital invested, whereas Fee-earning AUM includes the amount of capital commitments or the remaining amount of invested capital, depending on whether the original investment period for the fund has expired. As such, Fee-earning AUM may be greater than total AUM when the aggregate fair value of the remaining investments is less than the cost of those investments.

Our calculations of AUM and Fee-earning AUM may differ from the calculations of other alternative asset managers. As a result, these measures may not be comparable to similar measures presented by other alternative asset managers. In addition, our calculation of AUM (but not Fee-earning AUM) includes uncalled commitments to, and the fair value of invested capital in, our investment funds from Carlyle and our personnel, regardless of whether such commitments or invested capital are subject to management or performance fees. Our calculations of AUM or Fee-earning AUM are not based on any definition of AUM or Fee-earning AUM that is set forth in the agreements governing the investment funds that we manage or advise.

With respect to certain of the hedge funds and vehicles that we advise, we are entitled to incentive fees that are paid annually, semi-annually or quarterly, as the case may be, if the net asset value of an investor’s account has increased above the high-water mark. A hedge fund's or vehicle's “high-water mark” refers to the highest period end net asset value of an investor’s account on which incentive fees were previously paid.

2

PART I.

ITEM 1. BUSINESS

Overview

We are one of the world’s largest and most diversified multi-product global alternative asset management firms. We advise an array of specialized investment funds and other investment vehicles that invest across a range of industries, geographies, asset classes and investment strategies and seek to deliver attractive returns for our fund investors. Since our firm was founded in Washington, D.C. in 1987, we have grown to become a leading global alternative asset manager with more than $183 billion in AUM across 126 funds and 160 fund of funds vehicles as of December 31, 2015. We have more than 1,700 employees, including more than 700 investment professionals in 36 offices across six continents, and we serve more than 1,700 active carry fund investors from 78 countries. Across our Corporate Private Equity (“CPE”) and Real Assets segments, we have investments in more than 250 active portfolio companies that employ more than 675,000 people. In general, we have more investment professionals, offices, investment funds, and investments across our platform than many of our peers. We have structured our firm in this manner to provide our fund investors with a more diverse product set tailored to individual investing decisions, and a broader global reach, but such structure increases our costs of doing business.

The growth and development of our firm has been guided by several fundamental tenets:

• | Excellence in Investing. Our primary goal is to invest wisely and create value for our fund investors. We strive to generate superior investment returns by combining deep industry expertise, a global network of local investment teams who can leverage extensive firm-wide resources and a consistent and disciplined investment process. |

• | Commitment to our Fund Investors. Our fund investors come first. This commitment is a core component of our firm culture and informs every aspect of our business. We believe this philosophy is in the long-term best interests of Carlyle and its owners, including our common unitholders. |

• | Investment in the Firm. We have invested, and intend to continue to invest, significant resources in hiring and retaining a deep talent pool of investment professionals and in building the infrastructure of the firm, including our expansive local office network and our comprehensive investor services team, which provides finance, legal and compliance and tax services in addition to other services. |

• | Expansion of our Platform. We innovate continuously to expand our investment capabilities through the creation or acquisition of new asset-, sector- and regional-focused strategies in order to provide our fund investors a variety of investment options. |

• | Unified Culture. We seek to leverage the local market insights and operational capabilities that we have developed across our global platform through a unified culture we call “One Carlyle.” Our culture emphasizes collaboration and sharing of knowledge and expertise across the firm to create value. We believe our collaborative approach enhances our ability to analyze investments, deploy capital and improve the performance of our portfolio companies. |

There are four primary drivers of our business — fundraising or attracting new capital commitments to our funds; investing; working to create value for our investors or to achieve appreciation of our various investments; and harvesting, selling or otherwise disposing of our carry fund investments. Operational and strategic highlights for 2015 include the following:

• | During 2015, we raised approximately $23 billion in gross new commitments, or $16 billion net of redemptions, across our platform; made equity investments through our carry funds of approximately $9 billion in 279 new and follow-on investments; realized proceeds of more than $18 billion through 51 funds; and increased the value of our carry fund portfolio by approximately 7%. |

• | We continued to bolster our senior management team by hiring a new Chief Information Officer and promoting the co-head of our U.S. buyout group to Co-Deputy Chief Investment Officer of CPE. |

• | We further aligned our interests with those of our fund investors with Carlyle, our senior Carlyle professionals, advisors, other professionals and advisors increasing their commitments to our investment funds by over $0.7 billion to a total cumulative commitment of $8.9 billion. |

3

• | Each of our segments continued to leverage the One Carlyle platform to take advantage of economies of scale and offer our fund investors differentiated products. Specifically: |

◦ | In our CPE segment: |

▪ | We closed our fourth Europe buyout fund, our third Japan buyout fund and our third European technology fund. We launched fundraising for our fifth Asia growth fund and continued to see investor demand for our second U.S. mid-market fund and our first longer duration global buyout fund. In total, we closed on $8.0 billion in commitments in our CPE segment. |

• | We invested in, among others, Asia Satellite Telecom Holdings (through CAP IV), The Innovation Group (through CEP IV), JIC Leasing Co., Ltd. (through CAGP IV), Novetta Solutions, LLC (through CP VI), PA Consulting (through CEP IV), PNB Housing Finance Limited (through CAP IV), PrimeSport (through CEOF I), Rede D’or São Luiz S.A. (through CSABF and related coinvestments, and CP VI) and SEACOR Marine Holdings Inc. (through CEOF II). |

• | We sold our stake in, among others, Altice S.A., a CEP II and CEP III portfolio company, kbro Limited, a CAP II portfolio company, Metrologic Group SA, a CETP II portfolio company, The Nielsen Company, a CP IV and CEP II portfolio company, Veyance Technologies, Inc., a CP IV portfolio company, Telecable de Asturias, S.A., a CEP III portfolio company, and a portion of our stake in both Axalta Coating Systems and CommScope, Inc., both CP V and CEP III portfolio companies. We also undertook several successful initial public offerings including Tsubaki Nakashima Co., Ltd., a CJP II portfolio company, Guangxi Nanning Waterworks Co., Ltd., a CAGP IV portfolio company and Focus Media, a CAP III portfolio company. In total, we realized proceeds of $12.8 billion for our CPE carry fund investors. |

◦ | In our Global Market Strategies (“GMS”) segment: |

▪ | We raised $2.4 billion for our second generation energy mezzanine fund, continued fundraising for our first Asian structured credit fund and launched fundraising for our fourth generation distressed fund. We closed five new collateralized loan obligations (“CLOs”) in the U.S. and closed three new CLOs in Europe in 2015 with $4.3 billion of AUM at December 31, 2015. In total, we raised more than $2.9 billion for our GMS funds. |

▪ | CSP III and CEMOF I were particularly active this year, investing in Nationwide Accident Repair Services (CSP III), Trey Resources (CEMOF I), and Clearly Petroleum Holdings (CEMOF I), among others. |

▪ | We established a partnership with Hilcorp Energy Company that will seek to acquire, operate, and develop onshore oil and natural gas properties and related assets in North America. CEMOF I and CEMOF II have entered into an agreement to invest more than $1 billion in the newly formed partnership. |

◦ | In our Real Assets segment: |

▪ | We closed our seventh U.S. real estate fund and our first international energy fund, both reaching their caps; NGP XI also had a final close at its cap. Demand for our second power fund remained strong, and we launched fundraising for a new core-plus real estate fund. Building on our existing expertise in real estate and infrastructure, we intend to launch a global infrastructure fund later this year. In total, we closed on approximately $3.9 billion in commitments to our Real Assets segment. |

• | We invested nearly $1.4 billion to acquire or develop real estate properties, primarily in the U.S. across multiple sectors including multi-family and for-sale residential properties in the U.S. We invested in power generating facilities in the United States, an office property in China and a Romanian oil and gas development platform. |

4

• | We exited a number of investments, including a student housing portfolio in the United Kingdom, a Florida based 250 MW coal-fired power facility, a southern California apartment complex and a Northern Virginia mid-rise apartment complex. In total, we realized proceeds of approximately $4.8 billion for our Real Assets carry fund investors. |

◦ | In our Investment Solutions segment: |

▪ | We launched fundraising for our sixth AlpInvest secondaries fund and closed on more than $400 million for funds that are focused on a real estate secondaries and coinvestments for Metropolitan real Estate, our real estate fund of funds business. In total, we closed on approximately $1.6 billion in commitments to our Investment Solutions segment. |

▪ | We named a new Head of Investment Solutions, promoting the segment's Chief Operating Officer and Chief Financial Officer to the position. |

Business Segments

We operate our business across four segments: (1) Corporate Private Equity, (2) Global Market Strategies, (3) Real Assets and (4) Investment Solutions. Information about our segments should be read together with “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Although we primarily transact business in the United States and a significant amount of our revenues are generated domestically, we have established investment vehicles whose primary focus is making investments in specified geographical locations. Refer to “Information by Geographic Location” in Note 18 to the consolidated financial statements included in this Annual Report on Form 10-K for more information on consolidated revenues and assets based on the geographical focus of the associated investment vehicle.

Corporate Private Equity

Our Corporate Private Equity segment, established in 1990 with our first U.S. buyout fund, advises our buyout and growth capital funds, which pursue a wide variety of corporate investments of different sizes and growth potentials. Our 32 active CPE funds are each carry funds. They are organized and operated by geography or industry and are advised by separate teams of local professionals who live and work in the markets where they invest. In our CPE segment we also have 56 active external co-investment entities. We believe this diversity of funds and entities allows us to deploy more targeted and specialized investment expertise and strategies and offers our fund investors the ability to tailor their investment choices.

Our CPE teams have two primary areas of focus:

• | Buyout Funds. Our buyout teams advise a diverse group of 22 active funds that invest in transactions that focus either on a particular geography (e.g., United States, Europe, Asia, Japan, MENA, Sub-Saharan Africa or South America) or a particular industry. We continually seek to expand and diversify our buyout portfolio into new areas where we see opportunity for future growth. In 2015, we had final closings on our fourth European buyout fund and third Japan buyout fund and continued fundraising for our first longer duration global buyout fund. We invested $4.1 billion in new and follow-on investments through our buyout funds. As of December 31, 2015, our buyout funds had, in the aggregate, approximately $56.2 billion in AUM. |

• | Growth Capital Funds. Our 10 active growth capital funds are advised by four regionally focused teams in the United States, Europe and Asia, with each team generally focused on middle-market and growth companies consistent with specific regional investment considerations. The investment mandate for our growth capital funds is to seek out companies with the potential for growth, strategic redirection and operational improvements. These funds typically do not invest in early stage or venture-type investments. In 2015, launched our fifth Asia growth fund, held a final closing for our third Europe technology fund at its cap and continued fundraising for our second U.S. equity opportunities fund. As of December 31, 2015, our growth capital funds had, in the aggregate, approximately $7.0 billion in AUM. |

From inception through December 31, 2015, our CPE segment has invested approximately $67 billion in 535 investments. Of that total, we have invested 60% in 262 investments in North and South America, 20% in 121 investments in

5

Europe, the Middle East and Africa and 20% in 152 investments in the Asia-Pacific region. We have fully realized 353 of these investments, meaning that our funds have completely exited, and no longer own an interest in, those investments.

The following table presents certain data about our CPE segment as of December 31, 2015 (dollar amounts in billions; amounts invested include co-investments).

AUM | % of Total AUM | Fee-earning AUM | Active Investments | Active Funds | Available Capital | Investment Professionals | Amount Invested Since Inception | Investments Since Inception | ||||||||

$63 | 35% | $41 | 182 | 32 | $24 | 278 | $67 | 535 | ||||||||

Global Market Strategies

Our Global Market Strategies segment, established in 1999 with our first high yield fund, advises a group of 68 active funds that pursue investment strategies including leveraged loans and structured credit, energy mezzanine opportunities, middle market lending, distressed debt, long/short credit, long/short emerging markets equities, macroeconomic strategies, commodities trading and commodity structured transactions. In 2015, the GMS segment ended the year at $35.3 billion of AUM, down from $36.7 billion at December 31, 2014. This decrease was primarily due to redemptions in our hedge funds, offset by eight new issue CLOs, fundraising for our second generation energy mezzanine fund, our second securitized commodity structured transactions vehicle and fundraising for our first carry fund dedicated to Asian structured credit.

Primary areas of focus for our GMS teams include:

• | Structured Credit Funds. Our structured credit funds invest primarily in performing senior secured bank loans through structured vehicles and other investment vehicles. In 2015, we closed five new U.S. CLOs and three CLOs in Europe with a total of $2.8 billion and $1.5 billion, respectively, of AUM at December 31, 2015. As of December 31, 2015, our structured credit team advised 43 structured credit funds and one carry fund in the United States, Europe, and Asia totaling, in the aggregate, approximately $18.4 billion in AUM. |

• | Distressed and Corporate Opportunities. Our distressed and corporate opportunities funds generally invest in liquid and illiquid securities and obligations, including secured debt, senior and subordinated unsecured debt, convertible debt obligations, preferred stock and public and private equity of financially distressed companies in defensive and asset-rich industries. In certain investments, our funds may seek to restructure pre-reorganization debt claims into controlling positions in the equity of reorganized companies. As of December 31, 2015, our distressed and corporate opportunities team advised two funds totaling, in the aggregate, approximately $1.4 billion in AUM. |

• | Middle Market Finance. Our middle market finance business comprises our business development companies (“BDCs”), which invest primarily in first lien loans (which include unitranche, "first out" and "last out" loans) and second lien loans, a CLO consisting of middle market senior, first lien loans, and our corporate mezzanine funds, which invest in the first-lien, second-lien and mezzanine loans of middle-market companies, typically defined as companies with annual EBITDA ranging from $10 million to $100 million that lack access to the broadly syndicated loan and bond markets. As of December 31, 2015, our middle market investment team advised five funds totaling, in the aggregate, approximately $2.2 billion in AUM. |

• | Energy Mezzanine Opportunities. Our energy mezzanine opportunities team invests primarily in privately negotiated mezzanine debt investments in North American energy and power projects and companies. As of December 31, 2015, our energy mezzanine opportunities team advised two funds with approximately $4.3 billion in AUM. |

• | Long/Short Credit. Claren Road Asset Management LLC (“Claren Road”) advises two long/short credit hedge funds focusing on the global high grade and high yield markets totaling, in the aggregate, $3.4 billion in AUM as of December 31, 2015, which includes $2.3 billion of AUM that is subject to outstanding redemption requests as of the beginning of the first quarter of 2016. Claren Road seeks to profit from market mispricing of long and/or short positions in corporate and municipal bonds and loans, and their derivatives, across investment grade, below investment grade (high yield) or distressed companies. |

6

• | Emerging Market Equity and Macroeconomic Strategies. Emerging Sovereign Group LLC (“ESG”) advises six emerging markets equities and macroeconomic hedge funds with $4.3 billion in the aggregate of AUM as of December 31, 2015, which includes $0.7 billion of AUM that is subject to outstanding redemption requests as of the beginning of the first quarter of 2016. ESG’s emerging markets equities funds invest in publicly traded equities across a range of developing countries. ESG’s macroeconomic funds pursue investment strategies in developed and developing countries, and opportunities resulting from changes in the global economic environment. |

• | Commodities. Carlyle Commodity Management ("CCM," a New York-based commodities investment manager formerly known as Vermillion Asset Management) serves as investment manager to five hedge funds and two structured products totaling, in the aggregate, approximately $1.3 billion of AUM as of December 31, 2015, which includes $0.1 billion of AUM that is subject to outstanding redemption requests as of the beginning of the first quarter of 2016. CCM’s investment strategies include relative value, enhanced index and long-biased physical commodities, commodity sector-focused funds, and structured transactions. CCM seeks to produce positive, uncorrelated returns, through a liquid, relative-value, low volatility approach to trading both physical commodities and their derivatives and structuring transactions in physical commodities. |

The following table presents certain data about our GMS segment as of December 31, 2015 (dollar amounts in billions).

AUM | % of Total AUM | Fee-earning AUM | Active Funds | Investment Professionals (1) | ||||

$35 | 19% | $31 | 68 | 208 | ||||

(1) | Includes 67 middle-office and back office professionals. |

Real Assets

Our Real Assets segment, established in 1997 with our first U.S. real estate fund, advises our 26 active carry funds focused on real estate, infrastructure and energy and natural resources (including power) and also includes the six NGP management fee funds and three carry funds that are advised by NGP. This segment pursues investment opportunities across a diverse array of tangible assets, such as office buildings, hotels, retail and residential properties, industrial properties and senior-living facilities, as well as oil and gas exploration and production, midstream, refining and marketing, power generation, pipelines, wind farms, refineries, airports, toll roads, transportation, water utility and agriculture, as well as the companies providing services or otherwise related to them.

Our Real Assets teams have two primary areas of focus:

• | Real Estate. Our eight active real estate funds pursue real estate investment opportunities in Asia, Europe and the United States and generally focus on acquiring single-property assets rather than large-cap companies with real estate portfolios. Our team of 108 real estate investment professionals has made more than 675 investments in 327 cities/metropolitan statistical areas around the world as of December 31, 2015, including office buildings, hotels, retail and residential properties, industrial properties and senior living facilities. As of December 31, 2015, our real estate funds had, in the aggregate, approximately $13.8 billion in AUM. |

• | Energy and Natural Resources. Our energy and natural resources activities focus on buyouts, growth capital investments and strategic joint ventures in the midstream, upstream, power and oilfield services sectors, the renewable and alternative sectors and the energy and power industries around the world. Historically, we conducted our energy activities jointly with Riverstone, advising five funds with approximately $6.3 billion in AUM as of December 31, 2015 (we refer to these energy funds as our “Legacy Energy funds”). Currently, we conduct our North American energy investing through our partnership with NGP Energy Capital Management, an Irving, Texas-based energy investor. NGP advises nine funds with approximately $12.4 billion in AUM as of December 31, 2015. Our power team focuses on investment opportunities in the North American power generation sector. As of December 31, 2015, the power team managed approximately $1.8 billion in AUM through two funds. Our international energy investment team focuses on investments in a full range of energy assets outside of North America. As of December 31, 2015, the international energy team |

7

managed approximately $2.7 billion in AUM through one fund. We also have an infrastructure team that focuses on investments in infrastructure companies and assets. As of December 31, 2015, we advised one infrastructure fund with over $1.0 billion in AUM.

Our Real Assets carry funds, including Carlyle-advised co-investment vehicles, have, from inception through December 31, 2015, invested on a global basis approximately $39 billion in 858 investments (including more than 150 portfolio companies). Of that total, we have invested 77% in 682 investments in North and South America, 17% in 114 investments in Europe, the Middle East and Africa and 6% in 62 investments in the Asia-Pacific region. We have fully realized 510 of these investments, meaning that our funds have completely exited, and no longer own an interest in, those investments.

The following table presents certain data about our Real Assets segment as of December 31, 2015 (dollar amounts in billions; amounts invested include co-investments).

AUM | % of Total AUM | Fee-earning AUM | Active Investments (2) | Active Funds (3) | Available Capital | Investment Professionals (1) | Amount Invested Since Inception(2) | Investments Since Inception(2) | ||||||||

$38 | 21% | $31 | 348 | 26 | $16 | 137 | $39 | 858 | ||||||||

(1) | Excludes NGP and Riverstone employees. |

(2) | Excludes investment activity of the NGP management fee funds. |

(3) | Includes the six NGP management fee funds and three carry funds advised by NGP. |

Investment Solutions

Our Investment Solutions segment provides comprehensive investment opportunities and resources for our investors and clients to build private equity and real estate portfolios through fund of funds, secondary purchases of existing portfolios and managed coinvestment programs. Investment Solutions executes these activities through AlpInvest, one of the world’s largest investors in private equity and, Metropolitan, one of the largest managers of indirect investment in global real estate. In February 2016, we decided to restructure our Investment Solutions segment to focus on private market secondaries, co-investment and managed account activities and, given the challenging market environment, discontinue our fund of hedge funds and liquid alternative initiatives. In connection with the restructuring, we commenced a wind down of the operations of DGAM, a global manager of hedge funds based in Toronto, Canada that we acquired in February 2014. We expect that this action will improve our Investment Solutions results in the future, exclusive of costs incurred in connection with the wind down.

The primary areas of focus for our Investment Solutions teams include:

• | Private Equity Fund Investments. Our fund of funds vehicles advised by AlpInvest make investment commitments directly to buyout, growth capital, venture and other alternative asset funds advised by other general partners (“portfolio funds”). As of December 31, 2015, AlpInvest advised 48 fund of funds vehicles totaling, in the aggregate, approximately $28.2 billion in AUM. |

• | Private Equity Co-investments. AlpInvest invests alongside other private equity and mezzanine funds in which it typically has a fund investment throughout Europe, North America and Asia (for example, when an investment opportunity is too large for a particular fund, the sponsor of the fund may seek to raise additional “co-investment” capital from sources such as AlpInvest). As of December 31, 2015, our co-investment programs were conducted through 35 vehicles totaling, in the aggregate, over $6.4 billion in AUM. |

• | Private Equity Secondary Investments. We manage through AlpInvest funds that acquire limited partnership interests in secondary market transactions. Private equity investors who desire to sell or restructure their pre-existing investment commitments to a fund may negotiate to sell the fund interests to AlpInvest. In this manner, AlpInvest’s secondary investments team provides liquidity and restructuring alternatives for third-party private equity investors. In 2015, we established a secondary team dedicated to finding opportunities in the energy and infrastructure space. As of December 31, 2015, our secondary investments program was conducted through 35 fund of funds vehicles totaling, in the aggregate, more than $7.7 billion in AUM. |

• | Real Estate, Funds of Funds and Co-Secondary Investments. The principal strategic focus in our real estate fund of funds vehicles is on value add/opportunistic real estate investments through direct commitments with 90 highly focused, specialist real estate managers across the globe. As of December 31, 2015, we advised 26 |

8

real estate fund of funds vehicles with approximately $1.9 billion in AUM. We also focus on real estate secondaries and coinvestments.

The following table presents certain data about our Investment Solutions segment as of December 31, 2015 (dollar amounts in billions). See “— Structure and Operation of Our Investment Funds — Incentive Arrangements/Fee Structure” in this Item 1 for a discussion of the arrangements with the historical owners and management of AlpInvest regarding the allocation of carried interest in respect of the historical investments of and the historical and certain future commitments to our fund of funds vehicles.

AUM(1) | % of Total AUM | Fee-earning AUM | Fund of Funds Vehicles | Available Capital | Investment Professionals | Amount Invested Since Inception(2) | ||||||

$46 | 25% | $28 | 160 | $14 | 107 | $54 | ||||||

(1) | Under our arrangements with the historical owners and management team of AlpInvest, we generally do not retain any carried interest in respect of the historical investments and commitments to our fund of funds vehicles that existed as of July 1, 2011 (including any options to increase any such commitments exercised after such date). We are entitled to 15% of the carried interest in respect of commitments from the historical owners of AlpInvest for the period between 2011 and 2020 and 40% of the carried interest in respect of all other commitments (including all future commitments from third parties). |

(2) | AlpInvest only. |

Investment Approach

Corporate Private Equity

The investment approach of our Corporate Private Equity teams is generally characterized as follows:

• | Consistent and Disciplined Investment Process. We believe our successful investment track record is the result in part of a consistent and disciplined application of our investment process. Investment opportunities for our CPE funds are initially sourced and evaluated by one or more of our deal teams. The due diligence and transaction review process places a special emphasis on, among other considerations, the reputation of a target company’s shareholders and management, the company’s size and sensitivity of cash flow generation, the business sector and competitive risks, the portfolio fit, exit risks and other key factors highlighted by the deal team. In evaluating each deal, we consider what expertise or experience (i.e., the “Carlyle Edge”) we can bring to the transaction. An investment opportunity must secure final approval from the investment committee of the applicable investment fund. The investment committee approval process involves a detailed overview of the transaction and investment thesis, business, risk factors and diligence issues, as well as financial models. |

• | Geographic- and Industry-Focused. We have developed a global network of local investment teams with deep local insight into the areas in which they invest and have adopted an industry-focused approach to investing. Our extensive network of global investment professionals has the knowledge, experience and relationships on a local level that allow them to identify and take advantage of opportunities which may be unavailable to firms who do not have our global reach and resources. We also have particular industry expertise in aerospace, defense and government services, consumer and retail, financial services, healthcare, industrial, telecom, media and technology and transportation. As a result, we believe that our in-depth knowledge of specific industries improves our ability to source and create transactions, conduct effective and more informed due diligence, develop strong relationships with management teams and use contacts and relationships within such industries to identify potential buyers as part of a coherent exit strategy. |

• | Variable Deal Sizes and Creative Structures. Our teams are staffed not only to effectively pursue large transactions, but also other transactions of varying sizes. We often invest in smaller companies and this has allowed us to obtain greater diversity across our entire portfolio. Additionally, we may undertake large, strategic minority investments with certain control elements or private investment in public equity (PIPE) transactions in large companies with a clear exit strategy. In certain jurisdictions around the world, we may make investments with little or no debt financing and seek alternative structures to opportunistically pursue transactions. We generally seek to obtain board representation and typically appoint our investment professionals and advisors to represent us on the boards of the companies in which we invest. Where our |

9

funds, either alone or as part of a consortium, are not the controlling investor, we typically, subject to applicable regulatory requirements, acquire significant voting and other control rights with a view to securing influence over the conduct of the business.

• | Driving Value Creation. Our CPE teams seek to make investments in portfolio companies in which our particular strengths and resources may be employed to their best advantage. Typically, as part of a CPE investment, our investment teams will prepare and execute a value creation plan that is developed during a thorough due diligence effort and draws on the deep resources available across our global platform, specifically relying on: |

• | Reach: Our global team and global presence that enables us to support international expansion efforts and global supply chain initiatives. |

• | Expertise: Our investment professionals and our industry specialists, who provide extensive sector-specific knowledge and local market expertise. |

• | Insight: We engage 26 operating executives and advisors as independent consultants to work with our investment teams during due diligence, provide board-level governance and support and advise our portfolio company CEOs. These advisors are former CEOs or other high level executives of some of the world’s most successful corporations and currently sit on the board of directors of a diverse mix of companies. We use this collective group of advisors to provide special expertise to support specific value creation initiatives. |

• | Data: The goal of our research function is to extract as much information from the portfolio as possible about the current state of the economy and its likely evolution over the near-to-medium term. Our CPE investment portfolio includes over 175 active portfolio companies as of December 31, 2015, across a diverse range of industries and geographies that each generate multiple data points (e.g., orders, shipments, production volumes, occupancy rates, bookings). By evaluating these data on a systematic basis, we work to identify the data with the highest correlation with macroeconomic data and map observed movements in the portfolio to anticipated variation in the economy, including changes in growth rates across industries and geographies. |

• | Pursuing Best Exit Alternatives. In determining when to exit an investment, our private equity teams consider whether a portfolio company has achieved its objectives, the financial returns and the appropriate timing in industry cycles and company development to strive for the optimal value. The fund’s investment committee approves all exit decisions. |

Global Market Strategies

The investment approach of our Global Market Strategies credit-focused funds is generally characterized as follows:

• | Source Investment Opportunities. Our GMS teams source investment opportunities from both the primary and secondary markets through our global network and strong relationships with the financial community. We typically target portfolio companies that have a demonstrated track record of profitability, market leadership in their respective niche, predictable cash flow, a definable competitive advantage and products or services that are value added to its customer base. |

• | Conduct Fundamental Due Diligence and Perform Capital Structure Analyses. After an opportunity is identified, our GMS teams conduct fundamental due diligence to determine the relative value of the potential investment and capital structure analyses to determine the credit worthiness. Our due diligence approach typically incorporates meetings with management, company facility visits, discussions with industry analysts and consultants and an in-depth examination of financial results and projections. |

• | Evaluation of Macroeconomic Factors. Our GMS teams evaluate technical factors such as supply and demand, the market’s expectations surrounding a company and the existence of short- and long-term value creation or destruction catalysts. Inherent in all stages of credit evaluation is a determination of the likelihood of potential catalysts emerging, such as corporate reorganizations, recapitalizations, asset sales, changes in a company’s liquidity and mergers and acquisitions. |

10

• | Risk Minimization. Our GMS teams seek to make investments in capital structures to enable companies to both expand and weather downturns and/or below-plan performance. They work to structure investments with strong financial covenants, frequent reporting requirements and board representation, if possible. Through board representation or observation rights, our GMS teams work to provide a consultative, interactive approach to equity sponsors and management partners as part of the overall portfolio management process. |

Real Assets

Our Real Assets business includes investments in real estate assets, infrastructure and energy and natural resources (including power) companies and projects. The investment approach of the teams advising the international energy, power and infrastructure funds is similar to that of our CPE funds.

Generally, the investment approach of our real estate teams is characterized as follows:

• | Pursue Single Asset Transactions. In general, our U.S. real estate funds have focused on single asset transactions. We follow this approach in the U.S. because we believe that pursuing single assets enables us to better understand the factors that contribute to the fundamental value of each property, mitigate concentration risk, establish appropriate asset-by-asset capital structures and maintain governance over major property-level decisions. In addition, direct ownership of assets typically enables us to effectively employ an active asset management approach and reduce financing and operating risk, while increasing the visibility of factors that affect the overall returns of the investment. Historically, we have used an opportunistic real estate investment strategy; however, we have recently expanded our platform to include a core-plus investment strategy. In the U.S., we will continue to focus on single asset transactions in both our opportunistic and core plus investment strategies. Outside the U.S., we continue to opportunistically invest in the Asia and European markets. Currently, we are pursuing a value add strategy in China and focusing on opportunities such as logistics and data center platforms. In Europe, we pursue investment opportunities across asset classes and geographies both for single assets and portfolios, with a focus on opportunistic or value-add strategies. |

• | Seek out Strong Joint Venture Partners or Managers. Where appropriate, we seek out joint venture partners or managers with significant operational expertise. For each joint venture, we design structures and terms that provide situationally appropriate incentives, often including, for example, the subordination of the joint venture partner’s equity and profits interest to that of a fund, clawback provisions and/or profits escrow accounts in favor of a fund and exclusivity. We also typically structure positions with control or veto rights over major decisions. |

• | Source Deals Directly. Our teams endeavor to establish “market presence” in our target geographies where we have a history of operating in local markets and benefit from extensive long-term relationships with developers, corporate real estate owners, institutional investors and private owners. Such relationships have resulted in our ability to source a large number of investments on a direct negotiated basis. |

• | Focus on Sector-Specific Strategies. Our real estate funds focus on specific sectors and markets in areas where we believe the fundamentals are sound and dynamic capital markets allow for identification of assets whose value is not fully recognized. The real estate funds we advise have invested according to strategies established in several main sectors: office, hotel, retail, residential, industrial and senior living. |

• | Actively Manage our Real Estate Investments. Our real estate investments often require active management to uncover and create value. Accordingly, we have put in place experienced local asset management teams. These teams add value through analysis and execution of capital expenditure programs, development projects, lease negotiations, operating cost reduction programs and asset dispositions. The asset management teams work closely with the other real estate professionals to effectively formulate and implement strategic management plans. |

• | Manage the Exit of Investments. We believe that “exit management” is as important as traditional asset management in order to take full advantage of the typically short windows of opportunity created by temporary imbalances in capital market forces that affect real estate. In determining when to exit an investment, our real estate teams consider whether an investment has fulfilled its strategic plan, the depth of the market and generally prevailing industry conditions. |

11

Our energy and natural resources activities primarily focus on three areas: international energy, North American energy and power.

• | International Energy Investing. Our international energy team pursues investment opportunities in oil and gas exploration and production, midstream, oilfield services and refining and marketing in Europe, Africa, Latin America and Asia. Seeking to take advantage of the lack of capital in the international energy market, we pursue transactions where we have a distinctive competitive advantage and can create tangible value for companies in which we invest, through industry specialization, deployment of human capital and access to our global network. In seeking to build a geographically diverse international energy portfolio, we focus on cash generating opportunities, with a particular focus on proven reserves and production, and strategically seek to enhance the efficiency of the portfolio through exploration or infrastructure improvements. |

• | North American Energy Investing. We conduct our current North American energy investing through our partnership with NGP Energy Capital Management, an Irving, Texas-based energy investment firm that focuses on investments across a range of energy and natural resource assets, including oil and gas resources, oilfield services, pipelines and processing, as well as agricultural investments and properties. NGP seeks to align itself with “owner-managers” who are invested in the enterprise, have a top-tier technical team and who have a proprietary edge that differentiates their business plan. NGP strives to establish a portfolio of platform companies to grow through acquisitions and development and provides financial and strategic support and access to additional capital at the lowest cost. We do not control or manage the NGP management fee funds or the existing carry funds that are advised by NGP. NGP is managed by its founders and other senior members of NGP. |

• | Power Investing. Our power team focuses on investment opportunities in the North American power generation sector. Leveraging the expertise of the investment professionals at Cogentrix Energy L.L.C., one of our portfolio companies, the team seeks investments where it can obtain direct or indirect operational control to facilitate the implementation of technical enhancements. We seek to capitalize on secular trends and to identify assets where engineering and technical expertise, in addition to a strong management team, can facilitate performance. |

Investment Solutions

Our Investment Solutions team aims to apply a wide array of capabilities to help clients meet their investment objectives. The investment approach of our Investment Solutions platform is generally characterized as follows:

• | Depth of Investment Expertise. Investment Solutions has dedicated teams for each area of focus, and seeks to attract and retain talent with the required skill-set for each strategy. Investment Solutions professionals have trading, operational, portfolio and risk management expertise. From a top-down perspective, investment professionals seek to position the Investment Solutions business to capitalize on market opportunities through focused research and allocation of resources. From a bottom-up perspective, they seek to build deep relationships with underlying fund managers that are strengthened by the investment professionals’ relevant experience in the broader financial markets. |

• | Discipline. Investment Solutions professionals focus on diversification, risk management and downside protection. Its processes include the analysis and interpretation of macrodevelopments in the global economy and the assessment of a wide variety of issues that can influence the emphasis placed on sectors, geographies, asset classes and strategies when constructing investment portfolios. After making an investment commitment, the investment portfolios are subject to at least semi-annual reviews conducted by the respective investment team responsible for each investment. |

• | Innovation. Investment Solutions professionals seek to leverage the intellectual capital throughout the firm to identify emerging trends, market anomalies and new investment technologies to facilitate the formation of new strategies, as well as to set the direction for exiting strategies. This market intelligence provides them with an additional feedback channel for the development of new investment products. |

Our Family of Funds

The following chart presents the name (acronym), total capital commitments (in the case of our carry funds, structured credit funds, certain fund of funds vehicles, and the NGP management fee funds), assets under management (in the case of our hedge funds, fund of hedge funds vehicles, and other structured products), gross assets (in the case of our business development companies), and vintage year of the active funds in each of our segments, as of December 31, 2015. We present total capital commitments (as opposed to assets under management) for our closed-end investment funds because we believe this metric provides the most useful information regarding the relative size and scale of such funds. In the case of our hedge funds, fund of hedge funds vehicles, and other structured products which are open-ended and accordingly do not have permanent committed capital, we believe the most useful metric regarding relative size and scale is assets under management.

Corporate Private Equity | Global Market Strategies | Real Assets | ||||||||

Buyout Carry Funds | Structured Credit Funds | Real Estate Carry Funds | ||||||||

Carlyle Partners (U.S.) | Cash CLO Funds | Carlyle Realty Partners (U.S.) | ||||||||

CP VI | $13.0 bn | 2013 | U.S. | $14.4 bn | 1999-2015 | CRP VII | $4.2 bn | 2014 | ||

CP V | $13.7 bn | 2007 | Europe | €7.6 bn | 2005-2015 | CRP VI | $2.3 bn | 2011 | ||

CP IV | $7.9 bn | 2005 | Middle Market CLO | CRP V | $3.0 bn | 2006 | ||||

Global Financial Services Partners | U.S. | $1.2 bn | 2011 | CRP IV | $950 mm | 2005 | ||||

CGFSP II | $1.0 bn | 2013 | Global Market Strategies Carry Funds | CRP III | $564 mm | 2001 | ||||

CGFSP I | $1.1 bn | 2008 | Carlyle Mezzanine Partners | Carlyle Europe Real Estate Partners | ||||||

Carlyle Europe Partners | (Corporate Mezzanine) | CEREP III | €2.2 bn | 2007 | ||||||

CEP IV | €3.7 bn | 2014 | CMP II | $553 mm | 2008 | CEREP II | €763 mm | 2005 | ||

CEP III | €5.3 bn | 2007 | CMP I | $436 mm | 2004 | Carlyle Asia Real Estate Partners | ||||

CEP II | €1.8 bn | 2003 | Carlyle Strategic Partners | CAREP II | $486 mm | 2008 | ||||

Carlyle Asia Partners | (Distressed) | Natural Resources Funds | ||||||||

CAP IV | $3.9 bn | 2012 | CSP III | $703 mm | 2011 | Infrastructure Carry Fund | ||||

CBPF | RMB 2.1 bn | 2010 | CSP II | $1.4 bn | 2007 | CIP I | $1.1 bn | 2006 | ||

CAP III | $2.6 bn | 2008 | Carlyle Energy Mezzanine | Power Carry Funds | ||||||

CAP II | $1.8 bn | 2006 | Opportunities Fund | CPP II | $1.1 bn | 2014 | ||||

CAP I | $750 mm | 1998 | CEMOF II | $2.4 bn | 2015 | CPOCP | $433 mm | 2013 | ||

Carlyle Japan Partners | CEMOF I | $1.4 bn | 2010 | International Energy Carry Fund | ||||||

CJP III | ¥119.5 bn | 2013 | Carlyle Asia Structured Credit Opportunities | CIEP | $2.5 bn | 2013 | ||||

CJP II | ¥165.6 bn | 2006 | CASCOF | $238 mm | 2015 | NGP Energy Carry Funds | ||||

CJP I | ¥50.0 bn | 2001 | Hedge Funds and Other Vehicles1 | NGP XI | $5.3 bn | 2014 | ||||

Carlyle Mexico Partners | Long/Short Credit | NGP X | $3.6 bn | 2012 | ||||||

Mexico | $134 mm | 2005 | Claren Road | NGP Agribusiness Carry Fund | ||||||

Carlyle MENA Partners | Opportunities Fund | $1.1 bn | 2008 | NGP GAP | $402 mm | 2014 | ||||

MENA I | $471 mm | 2008 | Claren Road | NGP Management Fee Funds | ||||||

Carlyle South American Buyout Fund | Master Fund | $2.2 bn | 2006 | Various3 | $7.8 bn | 2004-2008 | ||||

CSABF I | $776 mm | 2009 | Emerging Markets Strategies | Legacy Energy Carry Funds | ||||||

Carlyle Sub-Saharan Africa Fund | Cross Border Equity Master Fund | $2.4 bn | 2002 | Carlyle/Riverstone Global Energy | ||||||

CSSAF I | $698 mm | 2012 | Domestic Opportunity Master Fund | $1.3 bn | 2011 | Energy IV | $6.0 bn | 2008 | ||

Carlyle Peru Fund | Emerging Sovereign Group - Various | $622 mm | 2002 | Energy III | $3.8 bn | 2005 | ||||

CPF I | $308 mm | 2012 | Commodities | Energy II | $1.1 bn | 2003 | ||||

Carlyle Global Partners | Carlyle Commodity Management - Various (4) | $1.3 bn | 2005-2015 | Carlyle/Riverstone Renewable Energy | ||||||

CGP | $3.3 bn | 2015 | Business Development Companies2 | Renew II | $3.4 bn | 2008 | ||||

Growth Carry Funds | Carlyle GMS Finance, Inc. | $1.1 bn | 2013 | Renew I | $685 mm | 2006 | ||||

Carlyle U.S. Venture/Growth Partners | NF Investment Corp | $254 mm | 2013 | |||||||

CEOF II | $2.3 bn | 2015 | ||||||||

CEOF I | $1.1 bn | 2011 | Investment Solutions | |||||||

CUSGF III | $605 mm | 2006 | AlpInvest | |||||||

CVP II | $602 mm | 2001 | Fund of Private Equity Funds | |||||||

Carlyle Europe Technology Partners | 48 vehicles | €40.4 bn | 2000-2015 | |||||||

CETP III | €657 mm | 2014 | Secondary Investments | |||||||

CETP II | €522 mm | 2008 | 35 vehicles | €10.7 bn | 2000-2015 | |||||

CETP I | €222 mm | 2005 | Co-Investments | |||||||

Carlyle Asia Venture/Growth Partners | 35 vehicles | €11.9 bn | 2000-2015 | |||||||

CAGP IV | $1.0 bn | 2008 | Metropolitan Real Estate | |||||||

CAGP III | $680 mm | 2005 | Real Estate Fund of Funds | |||||||

Carlyle Cardinal Ireland | 26 vehicles | $3.2 bn | 2003-2015 | |||||||

CCI | €292 mm | 2014 | Diversified Global Asset Management1 | |||||||

Fund of Hedge Funds | ||||||||||

16 vehicles | $2.0 bn | 2004-2015 | ||||||||

Note: All funds are closed-end and amounts shown represent total capital commitments as of December 31, 2015, unless otherwise noted. Certain of our recent vintage funds are currently in fundraising and total capital commitments are subject to change.

(1) | Open-ended hedge funds and other pooled vehicles. Amounts represent AUM across all products as of December 31, 2015. Our GMS hedge fund partnerships had outstanding redemption requests for $3.1 billion in the aggregate as of the beginning of the first quarter of 2016. As disclosed in Note 3 to the consolidated financial statements, the Partnership commenced a wind down of the operations of Diversified Global Asset Management in the first quarter of 2016. |

(2) | Amounts represent gross assets as of December 31, 2015. |

(3) | Includes NGP ETP I, NGP M&R, NGP ETP II, NGP VII, NGP VIII and NGP IX. |

(4) | Carlyle Commodity Management was formerly known as Vermillion Asset Management. |

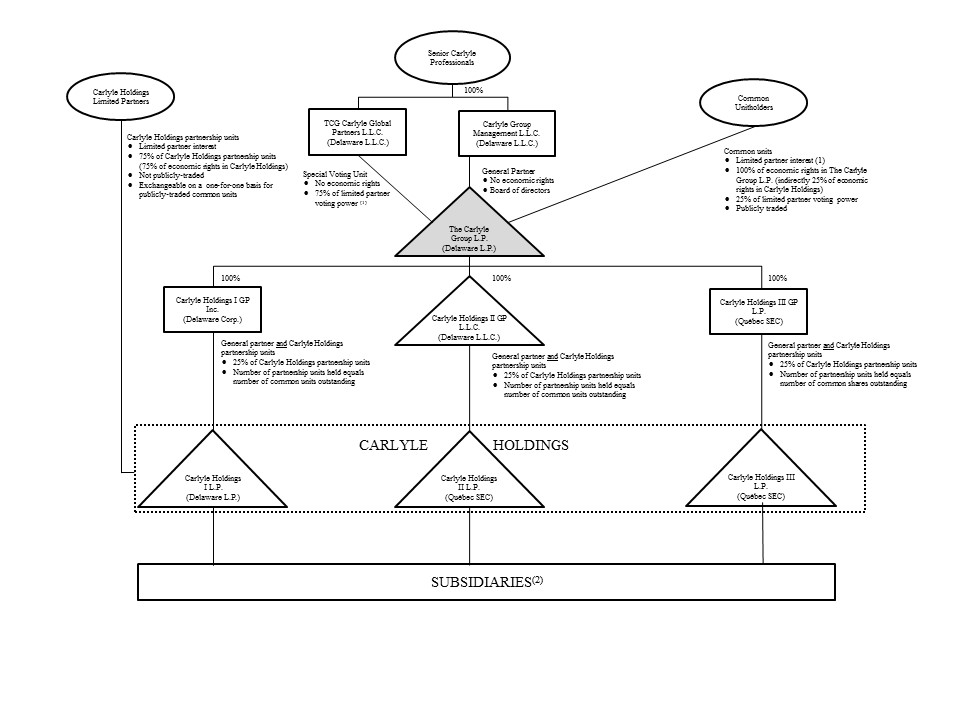

Organizational Structure

The simplified diagram below depicts our organizational structure. Ownership information in the diagram below is presented as of December 31, 2015. The diagram does not depict all of our subsidiaries, including intermediate holding companies through which certain of the subsidiaries depicted are held. As discussed in greater detail below, The Carlyle Group L.P. holds, through wholly owned subsidiaries, a number of Carlyle Holdings partnership units that is equal to the number of common units that The Carlyle Group L.P. has issued and benefits from the income of Carlyle Holdings to the extent of its equity interests in the Carlyle Holdings partnerships. While the holders of common units of The Carlyle Group L.P. are entitled to all of the economic rights in The Carlyle Group L.P., the limited partners of the Carlyle Holdings partnerships, like the wholly owned subsidiaries of The Carlyle Group L.P., hold Carlyle Holdings partnership units that entitle them to economic rights in Carlyle Holdings to the extent of their equity interests in the Carlyle Holdings partnerships. Public investors do not directly hold equity interests in the Carlyle Holdings partnerships.

(1) | The Carlyle Group L.P. common unitholders have only limited voting rights and have no right to remove our general partner or, except in limited circumstances, elect the directors of our general partner. TCG Carlyle Global Partners L.L.C., an entity wholly owned by our senior Carlyle professionals, holds a special voting unit in The Carlyle Group L.P. that entitles it, on those few matters that may be submitted for a vote of The Carlyle Group L.P. common unitholders, to participate in the vote on the same basis as the common unitholders and provides it with a number of votes that is equal to the aggregate number of vested and unvested partnership units in Carlyle Holdings held by the limited partners of Carlyle Holdings on the relevant record date. |

12

(2) | Certain individuals engaged in our business own interests directly in selected subsidiaries, including, in certain instances, entities that receive management fees from funds that we advise. See “— Structure and Operation of Our Investment Funds — Incentive Arrangements/Fee Structure” in this Item 1 for additional information. |

The Carlyle Group L.P. conducts all of its material business activities through Carlyle Holdings. Each of the Carlyle Holdings partnerships was formed to hold our interests in different businesses. Carlyle Holdings I L.P. owns all of our U.S. fee-generating businesses and many of our non-U.S. fee-generating businesses, as well as our carried interests (and other investment interests) that derive income that we believe is not qualifying income for purposes of the U.S. federal income tax publicly-traded partnership rules and certain of our carried interests (and other investment interests) that do not relate to investments in stock of corporations or in debt, such as equity investments in entities that are pass-through for U.S. federal income tax purposes. Carlyle Holdings II L.P. holds a variety of assets, including our carried interests in many of the investments by our carry funds in entities that are treated as domestic corporations for U.S. federal income tax purposes and in certain non-U.S. entities. Certain of our non-U.S. fee-generating businesses, as well as our non-U.S. carried interests (and other investment interests) that derive income that we believe is not qualifying income for purposes of the U.S. federal income tax publicly-traded partnership rules and certain of our non-U.S. carried interests (and other investment interests) that do not relate to investments in stock of corporations or in debt, such as equity investments in entities that are pass-through for U.S. federal income tax purposes are held by Carlyle Holdings III L.P.

The Carlyle Group L.P. has wholly owned subsidiaries that serve as the general partners of the Carlyle Holdings partnerships: Carlyle Holdings I GP Inc. (a Delaware corporation that is a domestic corporation for U.S. federal income tax purposes), Carlyle Holdings II GP L.L.C. (a Delaware limited liability company that is a disregarded entity and not an association taxable as a corporation for U.S. federal income tax purposes) and Carlyle Holdings III GP L.P. (a Québec société en commandite that is a foreign corporation for U.S. federal income tax purposes) serve as the general partners of Carlyle Holdings I L.P., Carlyle Holdings II L.P. and Carlyle Holdings III L.P., respectively. Carlyle Holdings I GP Inc. and Carlyle Holdings III GP L.P. serve as the general partners of Carlyle Holdings I L.P. and Carlyle Holdings III L.P., respectively, through wholly owned subsidiaries that are disregarded for federal income tax purposes. We refer to Carlyle Holdings I GP Inc., Carlyle Holdings II GP L.L.C. and Carlyle Holdings III GP L.P. collectively as the “Carlyle Holdings General Partners.”

Holding Partnership Structure

The Carlyle Group L.P. is treated as a partnership and not as a corporation for U.S. federal income tax purposes, although our partnership agreement does not restrict our ability to take actions that may result in our being treated as an entity taxable as a corporation for U.S. federal (and applicable state) income tax purposes. An entity that is treated as a partnership for U.S. federal income tax purposes is not a taxable entity and incurs no U.S. federal income tax liability. Instead, each partner is required to take into account its allocable share of items of income, gain, loss and deduction of the partnership in computing its U.S. federal income tax liability, whether or not cash distributions are made. Each holder of our common units is a limited partner of The Carlyle Group L.P., and accordingly, is generally required to pay U.S. federal income taxes with respect to the income and gain of The Carlyle Group L.P. that is allocated to such holder, even if The Carlyle Group L.P. does not make cash distributions. We believe that the Carlyle Holdings partnerships should also be treated as partnerships and not as corporations for U.S. federal income tax purposes. Accordingly, the holders of partnership units in Carlyle Holdings, including The Carlyle Group L.P.’s wholly owned subsidiaries, incur U.S. federal, state and local income taxes on their proportionate share of any net taxable income of Carlyle Holdings.

Each of the Carlyle Holdings partnerships has an identical number of partnership units outstanding, and we use the terms “Carlyle Holdings partnership unit” or “partnership unit in/of Carlyle Holdings” to refer collectively to a partnership unit in each of the Carlyle Holdings partnerships. The Carlyle Group L.P. holds, through wholly owned subsidiaries, a number of Carlyle Holdings partnership units equal to the number of common units that The Carlyle Group L.P. has issued. The Carlyle Holdings partnership units that are held by The Carlyle Group L.P.’s wholly owned subsidiaries are economically identical to the Carlyle Holdings partnership units that are held by the limited partners of the Carlyle Holdings partnerships. Accordingly, the income of Carlyle Holdings benefits The Carlyle Group L.P. to the extent of its equity interest in Carlyle Holdings.

The Carlyle Group L.P. is managed and operated by our general partner, Carlyle Group Management L.L.C., to whom we refer as “our general partner,” which is in turn wholly owned by our senior Carlyle professionals. Our general partner does not have any business activities other than managing and operating us. We reimburse our general partner and its affiliates for all costs incurred in managing and operating us, and our partnership agreement provides that our general partner determines the expenses that are allocable to us. Although there are no ceilings on the expenses for which we will reimburse our general partner and its affiliates, the expenses to which they may be entitled to reimbursement from us, such as director fees, historically have not been, and are not expected to be, material.

13

LP Relations

Our diverse and sophisticated investor base includes more than 1,700 active carry fund investors located in 78 countries. Included among our many longstanding fund investors are pension funds, sovereign wealth funds, insurance companies and high net worth individuals in the United States, Asia, Europe, the Middle East and South America.

We strive to maintain a systematic fundraising approach to support growth and serve our investor needs. This approach to fundraising has been critical in raising over $16 billion, net of redemptions, in 2015. We work for our fund investors and continuously seek to strengthen and expand our relationships with them through frequent investor engagement and by cross-selling products across our diverse platform. We have a dedicated in-house LP relations group, which includes 27 geographically focused professionals with extensive investor relations and fundraising experience. In addition, we have 18 product specialists with a focus on specific business segments and 10 professionals focused on high net worth distribution. Our LP relations group is supported by 66 support staff responsible for project management and fulfillment. Our LP relations professionals are in constant dialogue with our fund investors, which enables us to monitor client preferences and tailor future fund offerings to meet investor demand. We strive to secure a first-mover advantage with key investors, often by establishing a local presence and providing a broad and diverse range of investment opportunities.

As of December 31, 2015, approximately 92% of commitments to our active carry funds (by dollar amount) were from investors who are committed to more than one active carry fund, and approximately 62% of commitments to our active carry funds (by dollar amount) were from investors who are committed to more than five active carry funds. We believe the loyalty of our fund investor base, as evidenced by our substantial number of multi-fund relationships, enhances our ability to raise new funds and successor funds in existing strategies.

Investor Services

We have a team of over 700 investor services professionals worldwide. The investor services group performs a range of functions to support our investment teams, LP relations group, and the corporate infrastructure of Carlyle. Our investor services professionals provide an important control function, ensuring that transactions are structured pursuant to the partnership agreements, assisting in global regulatory compliance requirements and investor reporting to enable investors to easily monitor the performance of their investments. We have devoted substantial resources to creating comprehensive and timely investor reports, which are increasingly important to our investor base. The investor services group also works closely with each fund’s lifecycle, from fund formation and investments to portfolio monitoring and fund liquidation. We maintain an internal global legal and compliance team, which includes 22 professionals and a government relations group with a presence around the globe, which includes 15 professionals as of December 31, 2015. We intend to continue to build and invest in our legal, regulatory and compliance functions to enable our investment teams to better serve our investors.

Structure and Operation of Our Investment Funds

We conduct the sponsorship and management of our carry funds and other investment vehicles primarily through limited partnerships, which are organized by us, to accept commitments and/or funds for investment from institutional investors and high net worth individuals. Each investment fund that is a limited partnership, or “partnership” fund, has a general partner that is responsible for the management and operation of the fund’s affairs and makes all policy and investment decisions relating to the conduct of the investment fund’s business. The limited partners of such funds take no part in the conduct or control of the business of such funds, have no right or authority to act for or bind such funds and have no influence over the voting or disposition of the securities or other assets held by such funds, although such limited partners may vote on certain partnership matters including the removal of the general partner or early liquidation of the partnership by simple majority vote, as discussed below. In the case of certain separately managed accounts advised by us, the investor, rather than us, may control the asset or the investment decisions related thereto or certain investment vehicles or entities that hold or have custody of such assets.

Each investment fund and in the case of our separately managed accounts, the client, engages an investment adviser. Carlyle Investment Management L.L.C. (“CIM”) or one of its subsidiaries or affiliates serves as an investment adviser for most of our carry funds and is registered under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). Our investment advisers are generally entitled to a management fee from each investment fund for which they serve as investment advisers. For a discussion of the management fees to which our investment advisers are entitled across our various types of investment funds, see “— Incentive Arrangements / Fee Structure” below.

Our carry funds and hedge funds themselves typically do not register as investment companies under the Investment Company Act of 1940, as amended (the “1940 Act” or the “Investment Company Act”), in reliance on Section 3(c)(7) or Section 7(d) thereof or, typically in the case of funds formed prior to 1997, Section 3(c)(1) thereof. Section 3(c)(7) of the 1940 Act exempts from the 1940 Act’s registration requirements investment funds privately placed in the United States whose

14

securities are owned exclusively by persons who, at the time of acquisition of such securities, are “qualified purchasers” as defined under the 1940 Act and purchase their interests in a private placement. Section 3(c)(1) of the 1940 Act exempts from the 1940 Act’s registration requirements privately placed investment funds whose securities are beneficially owned by not more than 100 persons and purchase their interests in a private placement. In addition, under certain current interpretations of the SEC, Section 7(d) of the 1940 Act exempts from registration any non-U.S. investment fund all of whose outstanding securities are beneficially owned either by non-U.S. residents or by U.S. residents that are qualified purchasers and purchase their interests in a private placement.