SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a)

of the Securities Exchange Act of 1934

Filed by the Registrant o

Filed by a Party other than the Registrant x

Check the appropriate box:

| o | Preliminary Proxy Statement |

| o | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| o | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| o | Soliciting Material Under Rule 14a-12 |

HomeStreet, Inc.

(Name of Registrant as Specified In Its Charter)

Roaring Blue Lion Capital Management, L.P.

Blue Lion Opportunity Master Fund, L.P.

BLOF II LP

Charles W. Griege, Jr.

Ronald K. Tanemura

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (check the appropriate box):

| x | No fee required. |

| o | Fee computed on table below per Exchange Act Rule 14a-6(i)(4) and 0-11. |

| 1) | Title of each class of securities to which transaction applies: | |

| 2) | Aggregate number of securities to which transaction applies: | |

| 3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined): |

| 4) | Proposed maximum aggregate value of transaction: | |

| 5) | Total fee paid: | |

| o | Fee paid previously with preliminary materials. |

| o | Check box if any part of the fee is offset as provided by filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. Exchange Act Rule 0-11(a)(2) and identify the |

| 1) | Amount Previously Paid: | |

| 2) | Form, Schedule or Registration Statement No.: | |

| 3) | Filing Party: | |

| 4) | Date Filed: |

Roaring Blue Lion Capital Management, L.P. has responded to claims made by HomeStreet, Inc. in the form of a presentation to shareholders, which is attached hereto as Exhibit 1.

Exhibit 1

Responding to HomeStreet’s Misleading Claims June 3, 2019 www.FixHMST.com

2 Table of Contents Deconstructing HomeStreet’s Stock Performance Since Its 2012 IPO 3 HomeStreet’s TSR is Poor Regardless of How It Is Measured 4 - 6 Clarifying HomeStreet’s Appropriate Peer Group 7 - 8 HomeStreet’s Future Consolidated Efficiency Ratio Will Still Be Worst Among Peers 9 Blue Lion Capital vs. HomeStreet – Whose Narrative is Focused on Shareholders and Improving the Bank? 10 - 11

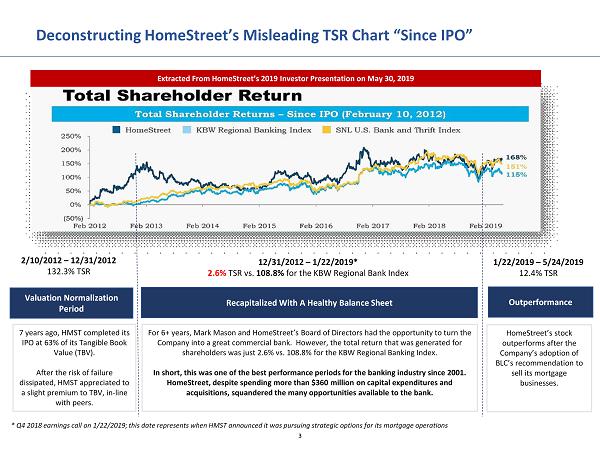

3 Deconstructing HomeStreet’s Misleading TSR Chart “Since IPO” 7 years ago, HMST completed its IPO at 63% of its Tangible Book Value (TBV). After the risk of failure dissipated, HMST appreciated to a slight premium to TBV, in - line with peers. For 6+ years, Mark Mason and HomeStreet’s Board of Directors had the opportunity to turn the Company into a great commercial bank. However, the total return that was generated for shareholders was just 2.6% vs. 108.8% for the KBW Regional Banking Index. In short, this was one of the best performance periods for the banking industry since 2001. HomeStreet, despite spending more than $360 million on capital expenditures and acquisitions, squandered the many opportunities available to the bank. Extracted From HomeStreet’s 2019 Investor Presentation on May 30, 2019 HomeStreet’s stock outperforms after the Company’s adoption of BLC’s recommendation to sell its mortgage businesses. 2/10/2012 – 12/31/2012 132.3% TSR 12/31/2012 – 1/22/2019* 2.6% TSR vs. 108.8% for the KBW Regional Bank Index 1/22/2019 – 5/24/2019 12.4% TSR Valuation Normalization Period Recapitalized With A Healthy Balance Sheet Outperformance * Q4 2018 earnings call on 1/22/2019; this date represents when HMST announced it was pursuing strategic options for its mort gag e operations

4 HomeStreet’s TSR Relative To Peers On a Rolling Basis 1 - , 3 - , and 5 - year Rolling TSRs vs. Peers 1 – HomeStreet significantly underperforms 1 Year Rolling TSR vs. Peers – HMST Underperforms 66% Of The Time 2 3 Year Rolling TSR vs. Peers – HMST Underperforms 94% Of The Time 3 5 Year Rolling TSR vs. Peers – HMST Underperforms 100% Of The Time 4 Source: FactSet. 1 Pacific NW Peers: BANR, GBCI, COLB, HFWA; CA Peers: PPBI, WABC, CVBF and TCBK. Weekly data. 2 first observation date 2/17/13, 3 first observation date 2/17/15, 4 first observation date 2/17/17 • HomeStreet “cherry picks” certain dates to show favorable TSRs and then argues that Blue Lion does the same • A “Rolling” analysis for the entire time period that HMST has been a public company eliminates the ability to pick favorable dates • Whether you use a 1 - , 3 - , or 5 - year time horizon, HomeStreet has underperformed its peers for the vast majority of its life as a public company • There is no way to debate the results of this analysis given the thousands of data points

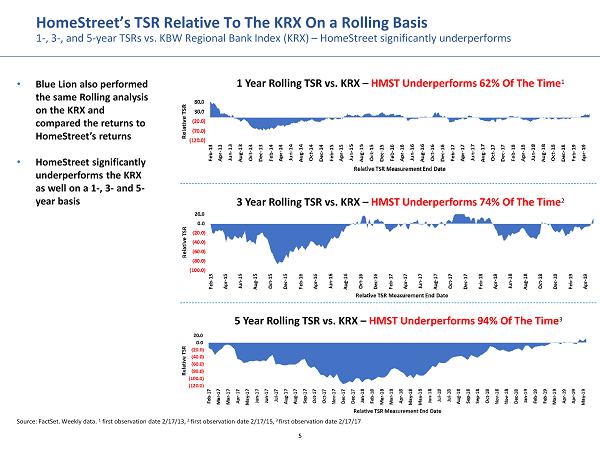

5 HomeStreet’s TSR Relative To The KRX On a Rolling Basis 1 - , 3 - , and 5 - year TSRs vs. KBW Regional Bank Index (KRX) – HomeStreet significantly underperforms 1 Year Rolling TSR vs. KRX – HMST Underperforms 62% Of The Time 1 3 Year Rolling TSR vs. KRX – HMST Underperforms 74% Of The Time 2 5 Year Rolling TSR vs. KRX – HMST Underperforms 94% Of The Time 3 Source: FactSet. Weekly data. 1 first observation date 2/17/13, 2 first observation date 2/17/15, 3 first observation date 2/17/17 • Blue Lion also performed the same Rolling analysis on the KRX and compared the returns to HomeStreet’s returns • HomeStreet significantly underperforms the KRX as well on a 1 - , 3 - and 5 - year basis

6 Since Its IPO Through January 22, 2019 * , HomeStreet Shareholders Would Have Been Better Off Buying the KRX 82% Of The Time The KBW Regional Bank Index Outperformed HomeStreet 1,424 Days HomeStreet Outperformed the KBW Regional Bank Index 322 Days • Out of 1,746 buy and hold periods 1 , HomeStreet’s stock has underperformed the KBW Regional Bank Index 82% of the time Source: Bloomberg. Does not represent TSR as it includes simple price appreciation only. 1 Buy and hold periods represent every day a shareholder could have purchased HMST’s stock and held it though 1/22/2019. * Q4 2018 earnings call on 1/22/2019; this date represents when HMST announced it is pursuing strategic options for its mortg age operations

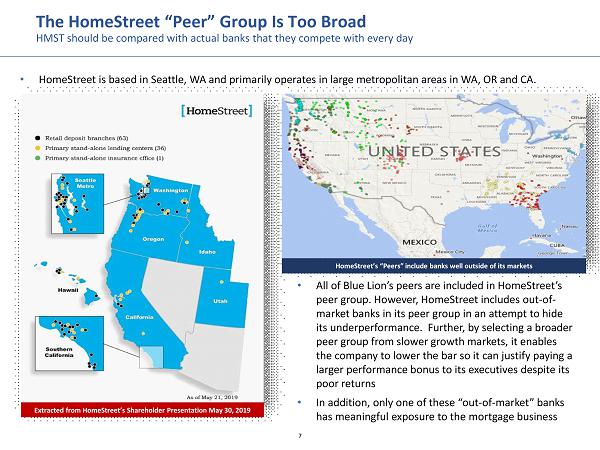

7 The HomeStreet “Peer” Group Is Too Broad HMST should be compared with actual banks that they compete with every day Extracted from HomeStreet’s Shareholder Presentation May 30, 2019 • HomeStreet is based in Seattle, WA and primarily operates in large metropolitan areas in WA, OR and CA. • All of Blue Lion’s peers are included in HomeStreet’s peer group. However, HomeStreet includes out - of - market banks in its peer group in an attempt to hide its underperformance. Further, by selecting a broader peer group from slower growth markets, it enables the company to lower the bar so it can justify paying a larger performance bonus to its executives despite its poor returns • In addition, only one of these “out - of - market” banks has meaningful exposure to the mortgage business HomeStreet’s “Peers” include banks well outside of its markets

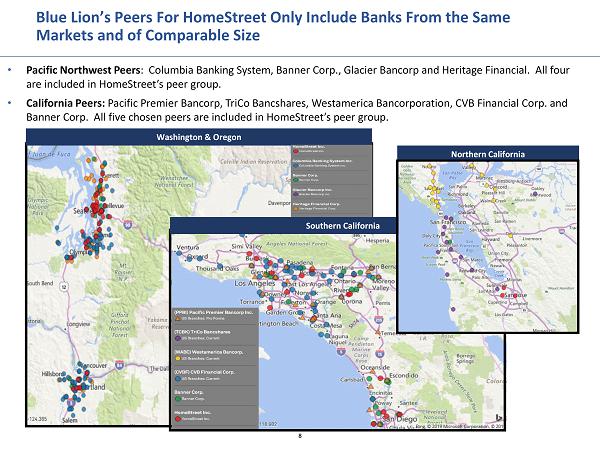

8 Blue Lion’s Peers For HomeStreet Only Include Banks From the Same Markets and of Comparable Size • Pacific Northwest Peers : Columbia Banking System, Banner Corp., Glacier Bancorp and Heritage Financial. All four are included in HomeStreet’s peer group. • California Peers: Pacific Premier Bancorp, TriCo Bancshares, Westamerica Bancorporation, CVB Financial Corp. and Banner Corp. All five chosen peers are included in HomeStreet’s peer group. Washington & Oregon Northern California Southern California

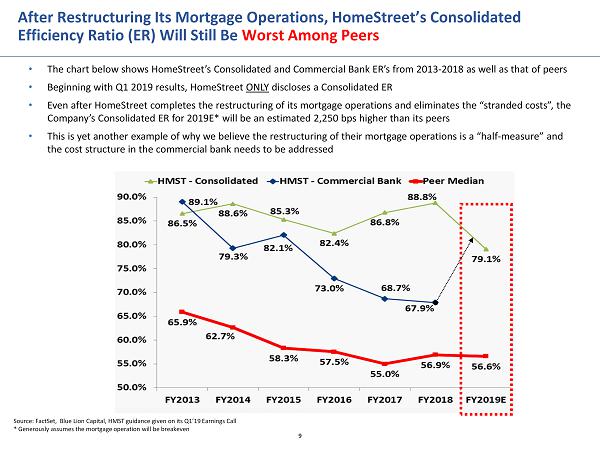

9 After Restructuring Its Mortgage Operations, HomeStreet’s Consolidated Efficiency Ratio (ER) Will Still Be Worst Among Peers Source: FactSet, Blue Lion Capital, HMST guidance given on its Q1’19 Earnings Call * Generously assumes the mortgage operation will be breakeven • The chart below shows HomeStreet’s Consolidated and Commercial Bank ER’s from 2013 - 2018 as well as that of peers • Beginning with Q1 2019 results, HomeStreet ONLY discloses a Consolidated ER • Even after HomeStreet completes the restructuring of its mortgage operations and eliminates the “stranded costs”, the Company’s Consolidated ER for 2019E* will be an estimated 2,250 bps higher than its peers • This is yet another example of why we believe the restructuring of their mortgage operations is a “half - measure” and the cost structure in the commercial bank needs to be addressed

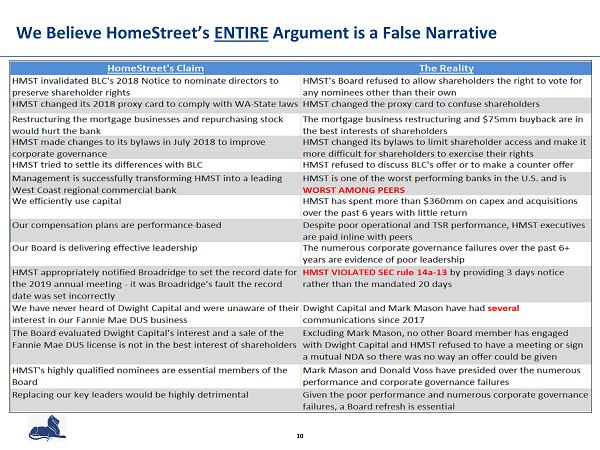

10 We Believe HomeStreet’s ENTIRE Argument is a False Narrative

11 Blue Lion Capital’s Narrative Has Been Consistent and ALWAYS For the Benefit of Shareholders We have consistently stated our belief that: • HomeStreet can be a great bank • But, HomeStreet’s management and Board have failed to craft and execute a sound strategy, resulting in: o Poor operational performance o Poor TSR o Poor capital allocation o Lost confidence in management by shareholders • The Board of HomeStreet has presided over numerous corporate governance failures: o Failure to provide oversight o Failure to act in the best interests of shareholders o Failure to act in good faith and exercise appropriate care o Failure to check the power of a combined Chairman and CEO • As a result, change is needed on the HomeStreet Board Vote the BLUE Proxy Card “FOR” Charles Griege and Ron Tanemura To Refresh HomeStreet’s Board of Directors

Vote The BLUE Proxy Card “ FOR ” Our Shareholder Proposals BLUE CARD Advisory Vote On The Compensation of Named Executive Officers The Company’s compensation practices are not constructed in the best interest of the Company & shareholders COMPANY PROPOSAL #2 VOTE AGAINST Ratification Of Exclusive Forum Selection Bylaw COMPANY PROPOSAL #4 VOTE AGAINST Would limit shareholders’ rights and options with grievances against the Company or its directors Declassify The Board, Eliminate Supermajority Vote To Approve Major Corporate Changes COMPANY PROPOSALS #5 & #6 The Company is finally following our lead by embracing these best practices VOTE FOR SHAREHOLDER PROPOSAL #7 Repeal Certain Bylaw Amendments Will prevent any possible interference with our right to present business at the Annual Meeting VOTE FOR SHAREHOLDER PROPOSAL #8 Vote For An Independent Chair An independent chair is important at an underperforming company like HomeStreet VOTE F OR VOTE FOR Ratification Of The Company’s Public Accounting Firm COMPANY PROPOSAL #3 Ratification is on a non - binding basis 12

Contact Information Blue Lion Capital 8115 Preston Road Suite 550 Dallas, TX 75225 Chuck Griege chuck@bluelioncap.com 214 - 855 - 2430 Brad Berry brad@bluelioncap.com 214 - 855 - 2430 Justin Hughes Justin@bluelioncap.com 214 - 855 - 2430 13

For additional information or assistance voting your shares please contact Blue Lion Capital's proxy solicitor 509 Madison Avenue Suite 1206 New York, NY 10022 Shareholders Call Toll Free: (800) 662 - 5200 Email: BlueLion@morrowsodali.com 14

15 IMPORTANT INFORMATION Roaring Blue Lion Capital Management, L.P., Blue Lion Opportunity Master Fund, L.P., BLOF II LP, Charles W. Griege, Jr. (collectively, "Blue Lion") and Ronald K. Tanemura (together with Blue Lion, the "Participants") have filed with the Securiti es and Exchange Commission (the "SEC") a definitive proxy statement and accompanying form of proxy to be used in connection with the solicitation of proxies from shareholders of HomeStreet, Inc. (the "Company"). All shareholders of the Company are advise d to read the definitive proxy statement and other documents related to the solicitation of proxies by the Participants, as the y contain important information, including additional information related to the Participants. The definitive proxy statement a nd an accompanying proxy card is being furnished to some or all of the Company's shareholders and is, along with other relevant documents, available at no charge on the SEC website at http://www.sec.gov/ or from the Participants' proxy solicitor, Morrow Sodali , LLC. Information about the Participants and a description of their direct or indirect interests by security holdings is contained in the definitive proxy statement on Schedule 14A filed by Blue Lion with the SEC on May 16, 2019. This document is available free o f charge from the sources indicated above.

16 DISCLAIMER This presentation, the materials contained herein, and the views expressed herein (this “Presentation”) are for discussion an d g eneral informational purposes only. This Presentation does not have regard to the specific investment objective, financial situation, suitability, or the particu lar need of any specific person who may receive this presentation, and should not be taken as advice on the merits of any investment decision. In addition, this Pres ent ation should not be deemed or construed to constitute an offer to sell or a solicitation of any offer to buy any security described herein in any jurisdict ion to any person, nor should it be deemed as investment advice or a recommendation to purchase or sell any specific security. Nor should this Presentation be considere d t o be an offer to sell or the solicitation of an offer to buy any interests in any fund managed by Roaring Blue Lion Capital Management, L.P. or any of its af filiates ("Blue Lion”). Such an offer to sell or solicitation of an offer to buy interests may only be made pursuant to definitive subscription documents. The views expressed herein represent the current opinions as of the date hereof of Blue Lion and are based on publicly availa ble information regarding HomeStreet , Inc. (“ Homestreet ” or the “Company”). Certain financial information and data used herein have been derived or obtained from, without independ ent verification, public filings, including filings made by HomeStreet with the Securities and Exchange Commission (“SEC”) and other sources. Blue Lion shall not be responsible for or have any liability for any misinformation contained in any SEC or other regulatory filing, any third party re port, or this Presentation. All amounts, market value information, and estimates included in this Presentation have been obtained from outside sources that Blue Lion bel ieves to be reliable or represent the best judgment of Blue Lion as of the date of this Presentation. Blue Lion is an independent company, and its opinions and pr ojections within this Presentation are not those of HomeStreet and have not been authorized, sponsored, or otherwise approved by HomeStreet . The information contained within the body of this Presentation is supplemented by footnotes which identify Blue Lion’s sources, assumptions, estimates, and calculations. This inf ormation contained herein should be reviewed in conjunction with the footnotes. In addition, the information contained herein reflects projections, market outlooks, assumptions, opinions and estimates made by Blue Lion as of the date hereof that may constitute forward - looking statements. Such forward - looking statements are based on certain assumptions and involve ce rtain risks and uncertainties, including risks and changes affecting industries generally and the Company specifically and are subject to change without not ice at any time. Given the inherent uncertainty of projections and forward - looking statements, you should be aware that actual results may differ materially from th e projections and other forward - looking statements contained herein due to reasons that may or may not be foreseeable. Therefore, Blue Lion does not represent that any opinion or projection will be realized, and Blue Lion offers no assurances a s t o the price of Company securities in the future. While the information presented herein is believed to be reliable, no representation or warranty is made concerni ng the accuracy of any data presented, the information or views contained herein, nor concerning any forward - looking statements. Blue Lion has an economic interest in the price movement of the securities discussed in this presentation, but Blue Lion’s economic interest is subject to change at any time. Blue Lion has not sought or obtained consent from any third party to use any statements or information indicated herein as ha vin g been obtained or derived from statements made or published by third parties, nor has it paid for any such statements. Any such statements or information sh oul d not be viewed as indicating the support of such third party for the views expressed herein. Blue Lion does not endorse third - party estimates or research which a re used in this presentation solely for illustrative purposes. All registered or unregistered service marks, trademarks and trade names referred to in this Pres ent ation are the property of their respective owners, and Blue Lion’s use herein does not imply an affiliation with, or endorsement by, the owners of these serv ice marks, trademarks and trade names or the goods and services sold or offered by such owners.