R OAD S HOW P RESENTATION April 2013 MERGER OF TRIO MERGER CORP. (TRIO & TMRGW) AND SAEXPLORATION HOLDINGS, INC.

1 The attached slide show was filed with the Securities and Exchange Commission on April 3 , 2013 as part of the Form 8 - K filed by Trio Merger Corp . (“Trio”) . Trio is holding presentations for certain of its stockholders, as well as other persons who might be interested in purchasing Trio’s securities, regarding its merger with SAExploration Holdings, Inc . (“SAE” or the “Company”) . The attached slide show will be distributed to attendees of these presentations . EarlyBirdCapital, Inc . (“EBC”), the managing underwriter of Trio’s initial public offering (“IPO”) consummated on June 24 , 2011 , is acting as Trio’s investment banker in these efforts . EBC will receive a fee of $ 2 , 415 , 000 in connection with this engagement . Trio and its directors and executive officers, and EBC may be deemed to be participants in the solicitation of proxies for the special meeting of Trio’s stockholders to be held to approve the merger . STOCKHOLDERS OF TRIO AND OTHER INTERESTED PERSONS ARE ADVISED TO READ TRIO’S DEFINITIVE PROXY STATEMENT (“PROXY STATEMENT”), WHEN AVAILABLE, WHICH WILL CONTAIN IMPORTANT INFORMATION . Until the Proxy Statement is filed, such persons may read Trio’s preliminary Proxy Statement, dated March 22 , 2013 (the “Preliminary Proxy Statement”) and Trio’s final Prospectus, dated January 21 , 2011 (the “Prospectus”), for a description of the security holdings of Trio’s officers and directors and of EBC and their respective interests in the successful consummation of the business combination . The Proxy Statement will replace the Preliminary Proxy Statement in its entirety and will be mailed to stockholders as of a record date to be established for voting on the merger . Stockholders will also be able to obtain a copy of the Proxy Statement, without charge, by directing a request to : Trio Merger Corp . , 777 Third Avenue, 37 th Floor, New York, New York 10017 . The Preliminary Proxy Statement and Prospectus and the Proxy Statement, once available, can also be obtained, without charge, at the Securities and Exchange Commission’s internet site (http : //www . sec . gov) . Important Disclosures

2 This presentation may contain forward - looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 , about Trio, SAE and their combined business after completion of the proposed acquisition . Forward looking statements are statements that are not historical facts . Such forward - looking statements, based upon the current beliefs and expectations of Trio’s and SAE’s management, are subject to risks and uncertainties, which could cause actual results to differ from the forward looking statements . The following factors, among others, could cause actual results to differ from those set forth in the forward - looking statements : business conditions ; weather and natural disasters ; changing interpretations of generally accepted accounting principles ; outcomes of government reviews ; inquiries and investigations and related litigation ; continued compliance with government regulations ; legislation or regulatory environments ; requirements or changes adversely affecting the businesses in which SAE is engaged ; fluctuations in customer demand ; management of rapid growth ; intensity of competition from other providers of seismic services ; general economic conditions ; community relations ; permitting issues ; geopolitical events and regulatory changes, as well as other relevant risks detailed in Trio’s filings with the Securities and Exchange Commission . The information set forth herein should be read in light of such risks . Additionally, SAE’s 2010 financial information is unaudited and does not conform to SEC Regulation S - X . Furthermore, it includes certain financial information (EBITDA) not derived in accordance with generally accepted accounting principles (“GAAP”) . Accordingly, such information may be materially different when presented in Trio’s Definitive Proxy Statement to solicit stockholder approval of the merger . Trio believes that the presentation of this non - GAAP measure provides information that is useful to investors as it indicates more clearly the ability of SAE to meet capital expenditures and working capital requirements and otherwise meet its obligations as they become due . SAE’s EBITDA was derived by taking earnings before interest, taxes, depreciation and amortization excluding certain one - time non - recurring items and exclusions . Neither Trio nor SAE assumes any obligation to update the information contained in this presentation . Safe Harbor

3 Investment Highlights » One of the larger international seismic data acquisition and processing companies in the world » Attractive valuation – significant discount to peers despite higher projected growth profile » High growth company with annual EBITDA growth of over 37% from 2010 through 2012 and projected EBITDA growth of over 32% 1 per year from 2012 through 2014 » International geographic diversification and a blue chip customer base » Experienced management team » Significant ongoing ownership by SAE management team Note: 1 Based on the midpoint of the 2014 EBITDA target of $54 million

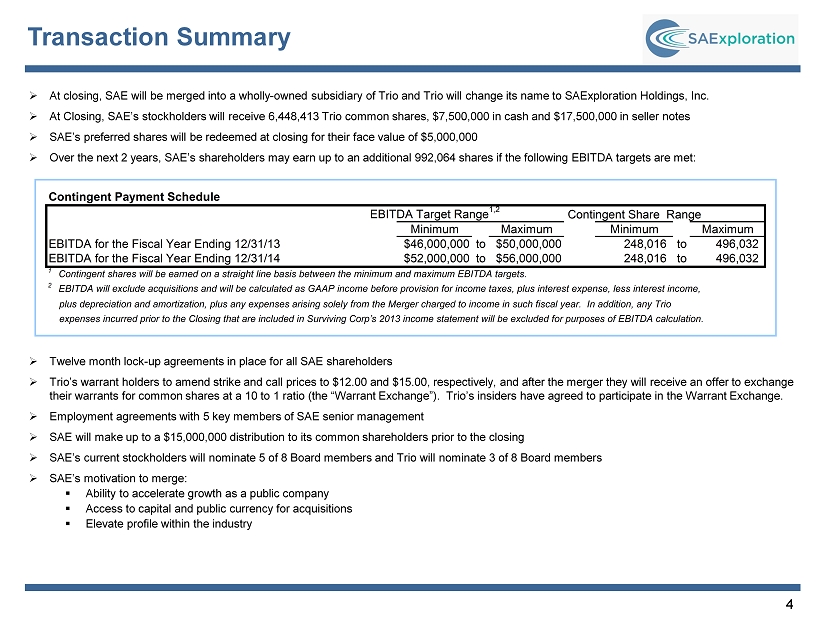

4 Transaction Summary » At closing, SAE will be merged into a wholly - owned subsidiary of Trio and Trio will change its name to SAExploration Holdings, I nc. » At Closing, SAE’s stockholders will receive 6,448,413 Trio common shares, $7,500,000 in cash and $17,500,000 in seller notes » SAE’s preferred shares will be redeemed at closing for their face value of $5,000,000 » Over the next 2 years, SAE’s shareholders may earn up to an additional 992,064 shares if the following EBITDA targets are met : » Twelve month lock - up agreements in place for all SAE shareholders » Trio’s warrant holders to amend strike and call prices to $12.00 and $15.00, respectively, and after the merger they will rec eiv e an offer to exchange their warrants for common shares at a 10 to 1 ratio (the “Warrant Exchange”). Trio’s insiders have agreed to participate in the Warrant Exchange. » Employment agreements with 5 key members of SAE senior management » SAE will make up to a $15,000,000 distribution to its common shareholders prior to the closing » SAE’s current stockholders will nominate 5 of 8 Board members and Trio will nominate 3 of 8 Board members » SAE’s motivation to merge: ▪ Ability to accelerate growth as a public company ▪ Access to capital and public currency for acquisitions ▪ Elevate profile within the industry Contingent Payment Schedule EBITDA Target Range 1,2 Contingent Share Range Minimum Maximum Minimum Maximum EBITDA for the Fiscal Year Ending 12/31/13 $46,000,000 to $50,000,000 248,016 to 496,032 EBITDA for the Fiscal Year Ending 12/31/14 $52,000,000 to $56,000,000 248,016 to 496,032 1 Contingent shares will be earned on a straight line basis between the minimum and maximum EBITDA targets. 2 EBITDA will exclude acquisitions and will be calculated as GAAP income before provision for income taxes, plus interest expense, less interest income, plus depreciation and amortization, plus any expenses arising solely from the Merger charged to income in such fiscal year. In addition, any Trio expenses incurred prior to the Closing that are included in Surviving Corp’s 2013 income statement will be excluded for purposes of EBITDA calculation.

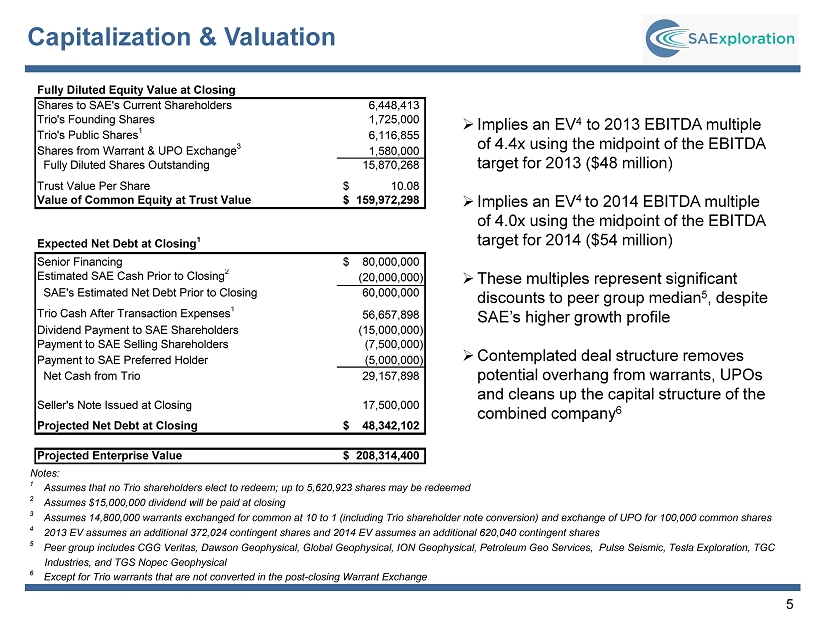

5 Capitalization & Valuation » Implies an EV 4 to 2013 EBITDA multiple of 4.4x using the midpoint of the EBITDA target for 2013 ($48 million) » Implies an EV 4 to 2014 EBITDA multiple of 4.0x using the midpoint of the EBITDA target for 2014 ($54 million) » These multiples represent significant discounts to peer group median 5 , despite SAE’s higher growth profile » Contemplated deal structure removes potential overhang from warrants, UPOs and cleans up the capital structure of the combined company 6 Fully Diluted Equity Value at Closing Shares to SAE's Current Shareholders 6,448,413 Trio's Founding Shares 1,725,000 Trio's Public Shares 1 6,116,855 Shares from Warrant & UPO Exchange 3 1,580,000 Fully Diluted Shares Outstanding 15,870,268 Trust Value Per Share 10.08$ Value of Common Equity at Trust Value 159,972,298$ Expected Net Debt at Closing 1 Senior Financing 80,000,000$ Estimated SAE Cash Prior to Closing 2 (20,000,000) SAE's Estimated Net Debt Prior to Closing 60,000,000 Trio Cash After Transaction Expenses 1 56,657,898 Dividend Payment to SAE Shareholders (15,000,000) Payment to SAE Selling Shareholders (7,500,000) Payment to SAE Preferred Holder (5,000,000) Net Cash from Trio 29,157,898 Seller's Note Issued at Closing 17,500,000 Projected Net Debt at Closing 48,342,102$ Projected Enterprise Value 208,314,400$ Notes: 1 Assumes that no Trio shareholders elect to redeem; up to 5,620,923 shares may be redeemed 2 Assumes $15,000,000 dividend will be paid at closing 3 Assumes 14,800,000 warrants exchanged for common at 10 to 1 (including Trio shareholder note conversion) and exchange of UPO for 100,000 common shares 4 2013 EV assumes an additional 372,024 contingent shares and 2014 EV assumes an additional 620,040 contingent shares 5 Peer group includes CGG Veritas, Dawson Geophysical, Global Geophysical, ION Geophysical, Petroleum Geo Services, Pulse Seismic, Tesla Exploration, TGC Industries, and TGS Nopec Geophysical 6 Except for Trio warrants that are not converted in the post-closing Warrant Exchange

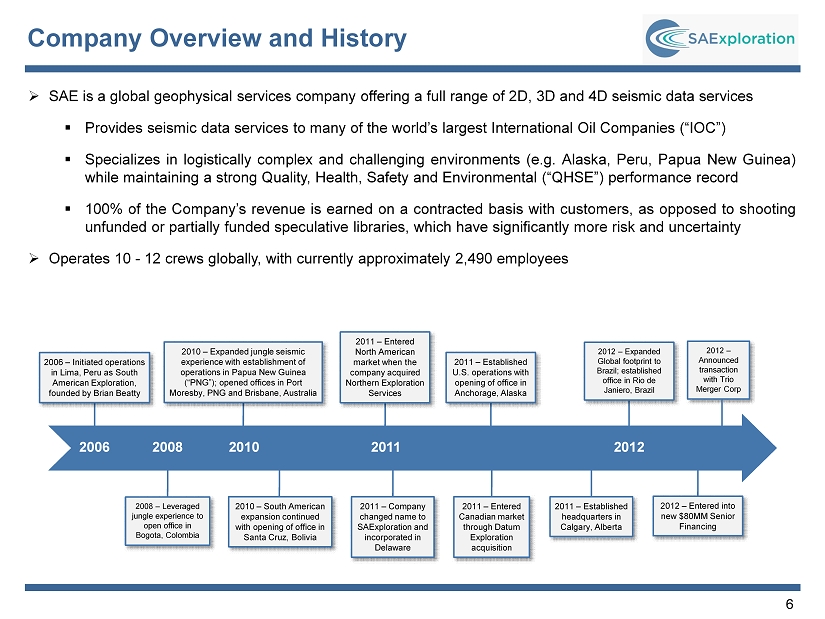

6 » SAE is a global geophysical services company offering a full range of 2 D, 3 D and 4 D seismic data services ▪ Provides seismic data services to many of the world’s largest International Oil Companies (“IOC”) ▪ Specializes in logistically complex and challenging environments (e . g . Alaska, Peru, Papua New Guinea) while maintaining a strong Quality, Health, Safety and Environmental (“QHSE”) performance record ▪ 100 % of the Company’s revenue is earned on a contracted basis with customers, as opposed to shooting unfunded or partially funded speculative libraries, which have significantly more risk and uncertainty » Operates 10 - 12 crews globally, with currently approximately 2 , 490 employees Company Overview and History 2006 2008 2010 2011 2012 2006 – Initiated operations in Lima, Peru as South American Exploration, founded by Brian Beatty 2008 – Leveraged jungle experience to open office in Bogota, Colombia 2010 – Expanded jungle seismic experience with establishment of operations in Papua New Guinea (“PNG”); opened offices in Port Moresby, PNG and Brisbane, Australia 2010 – South American expansion continued with opening of office in Santa Cruz, Bolivia 2011 – Entered North American market when the company acquired Northern Exploration Services 2011 – Established U.S. operations with opening of office in Anchorage, Alaska 2011 – Company changed name to SAExploration and incorporated in Delaware 2011 – Entered Canadian market through Datum Exploration acquisition 2011 – Established headquarters in Calgary, Alberta 2012 – Expanded Global footprint to Brazil; established office in Rio de Janiero, Brazil 2012 – Entered into new $80MM Senior Financing 2012 – Announced transaction with Trio Merger Corp

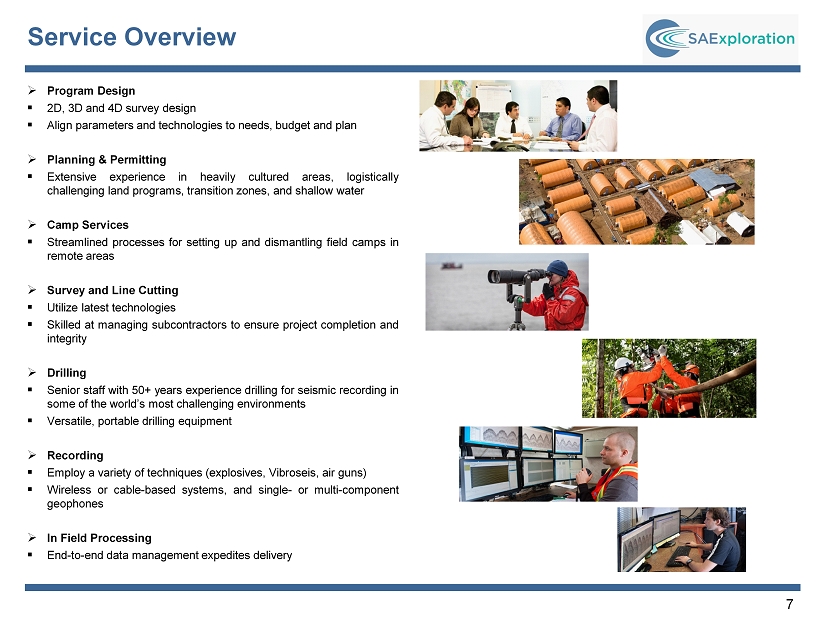

7 Service Overview » Program Design ▪ 2 D, 3 D and 4 D survey design ▪ Align parameters and technologies to needs, budget and plan » Planning & Permitting ▪ Extensive experience in heavily cultured areas, logistically challenging land programs, transition zones, and shallow water » Camp Services ▪ Streamlined processes for setting up and dismantling field camps in remote areas » Survey and Line Cutting ▪ Utilize latest technologies ▪ Skilled at managing subcontractors to ensure project completion and integrity » Drilling ▪ Senior staff with 50 + years experience drilling for seismic recording in some of the world’s most challenging environments ▪ Versatile, portable drilling equipment » Recording ▪ Employ a variety of techniques (explosives, Vibroseis, air guns) ▪ Wireless or cable - based systems, and single - or multi - component geophones » In Field Processing ▪ End - to - end data management expedites delivery

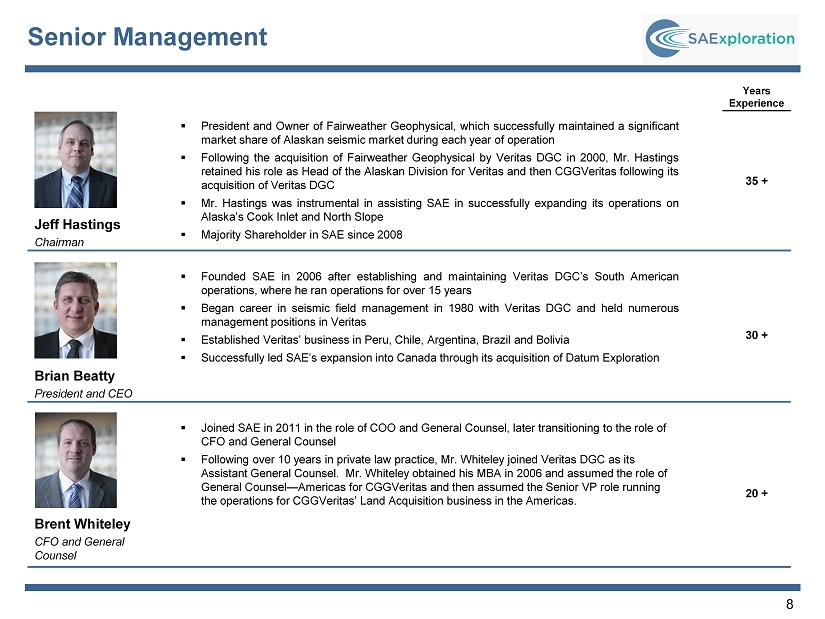

8 Senior Management Years Experience 35 + Jeff Hastings Chairman ▪ President and Owner of Fairweather Geophysical, which successfully maintained a significant market share of Alaskan seismic market during each year of operation ▪ Following the acquisition of Fairweather Geophysical by Veritas DGC in 2000 , Mr . Hastings retained his role as Head of the Alaskan Division for Veritas and then CGGVeritas following its acquisition of Veritas DGC ▪ Mr . Hastings was instrumental in assisting SAE in successfully expanding its operations on Alaska’s Cook Inlet and North Slope ▪ Majority Shareholder in SAE since 2008 Brian Beatty President and CEO ▪ Founded SAE in 2006 after establishing and maintaining Veritas DGC’s South American operations, where he ran operations for over 15 years ▪ Began career in seismic field management in 1980 with Veritas DGC and held numerous management positions in Veritas ▪ Established Veritas’ business in Peru, Chile, Argentina, Brazil and Bolivia ▪ Successfully led SAE’s expansion into Canada through its acquisition of Datum Exploration 30 + Brent Whiteley CFO and General Counsel ▪ Joined SAE in 2011 in the role of COO and General Counsel, later transitioning to the role of CFO and General Counsel ▪ Following over 10 years in private law practice, Mr. Whiteley joined Veritas DGC as its Assistant General Counsel. Mr. Whiteley obtained his MBA in 2006 and assumed the role of General Counsel — Americas for CGGVeritas and then assumed the Senior VP role running the operations for CGGVeritas’ Land Acquisition business in the Americas. 20 +

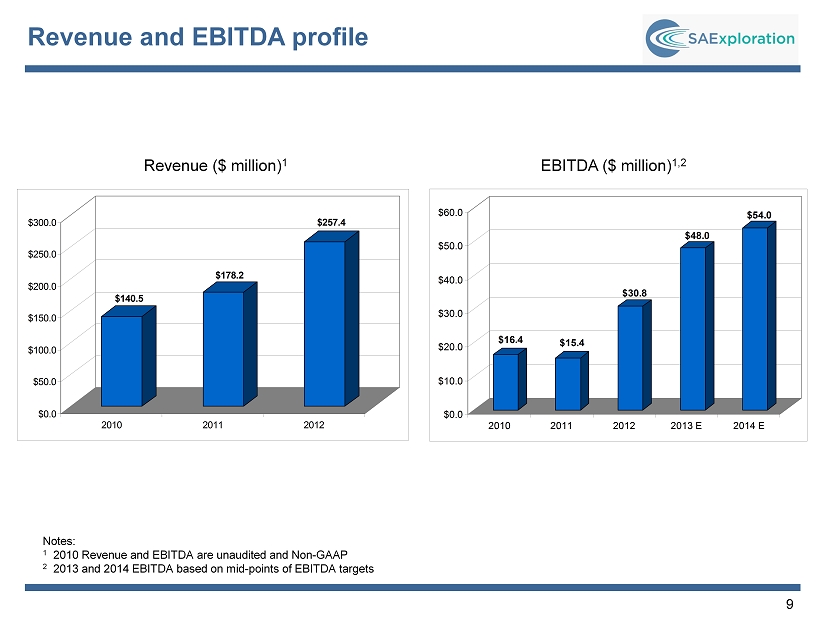

9 Revenue and EBITDA profile Revenue ($ million) 1 EBITDA ($ million) 1,2 Notes: 1 2010 Revenue and EBITDA are unaudited and Non - GAAP 2 2013 and 2014 EBITDA based on mid - points of EBITDA targets $140.5 $178.2 $257.4 $0.0 $50.0 $100.0 $150.0 $200.0 $250.0 $300.0 2010 2011 2012 $16.4 $15.4 $30.8 $48.0 $54.0 $0.0 $10.0 $20.0 $30.0 $40.0 $50.0 $60.0 2010 2011 2012 2013 E 2014 E

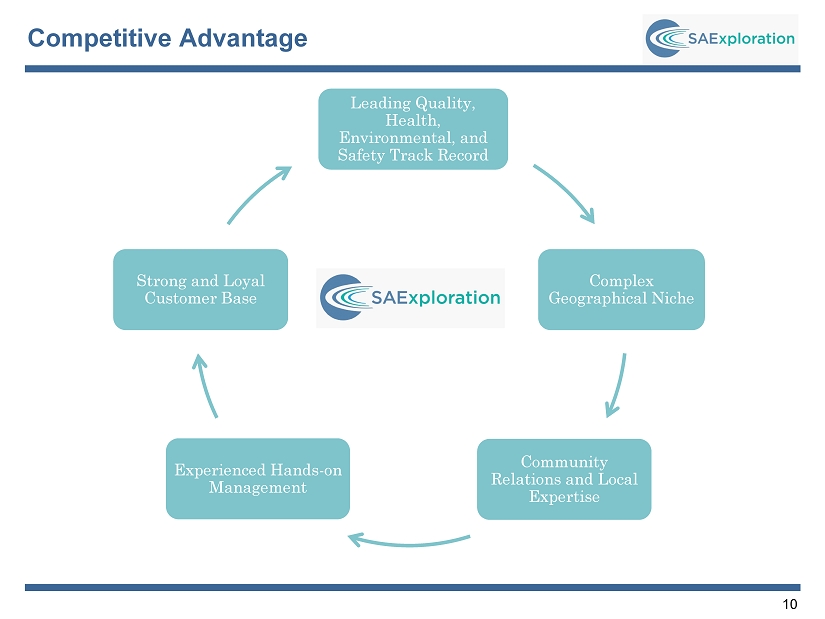

10 Leading Quality, Health, Environmental, and Safety Track Record Complex Geographical Niche Community Relations and Local Expertise Experienced Hands - on Management Strong and Loyal Customer Base Competitive Advantage

11 Select Major Customers Senior management has an average of 10+ years of experience with SAE’s largest customers

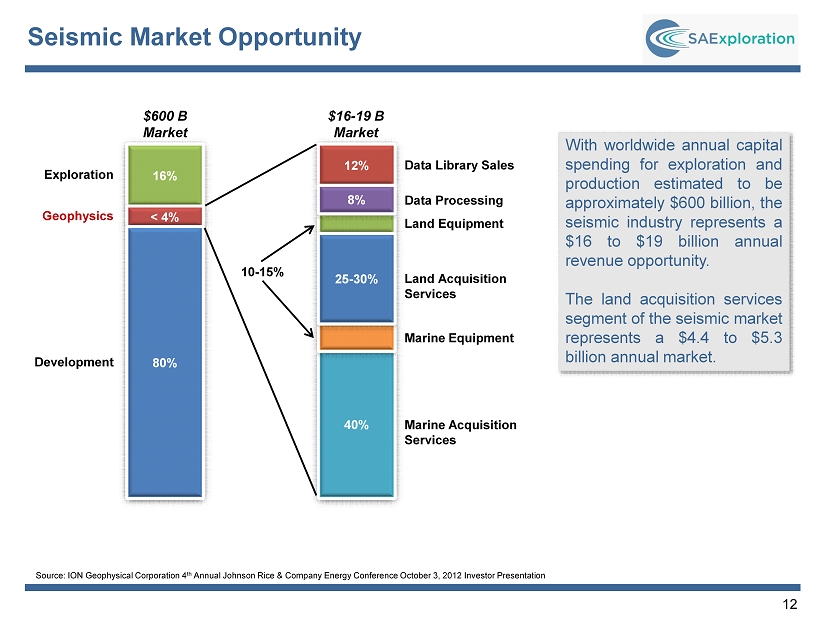

12 Seismic Market Opportunity 16% < 4% 80% 12% 8% 40% 25 - 30% $600 B Market $16 - 19 B Market Exploration Geophysics Development 10 - 15% Data Library Sales Data Processing Land Equipment Land Acquisition Services Marine Equipment Marine Acquisition Services With worldwide annual capital spending for exploration and production estimated to be approximately $ 600 billion, the seismic industry represents a $ 16 to $ 19 billion annual revenue opportunity . The land acquisition services segment of the seismic market represents a $ 4 . 4 to $ 5 . 3 billion annual market . Source: ION Geophysical Corporation 4 th Annual Johnson Rice & Company Energy Conference October 3, 2012 Investor Presentation

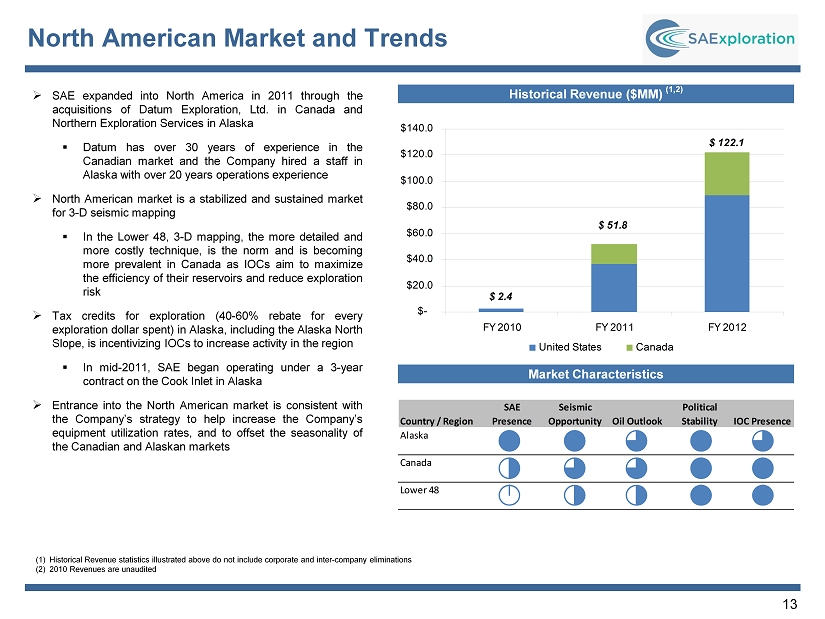

13 North American Market and Trends » SAE expanded into North America in 2011 through the acquisitions of Datum Exploration, Ltd . in Canada and Northern Exploration Services in Alaska ▪ Datum has over 30 years of experience in the Canadian market and the Company hired a staff in Alaska with over 20 years operations experience » North American market is a stabilized and sustained market for 3 - D seismic mapping ▪ In the Lower 48 , 3 - D mapping, the more detailed and more costly technique, is the norm and is becoming more prevalent in Canada as IOCs aim to maximize the efficiency of their reservoirs and reduce exploration risk » Tax credits for exploration ( 40 - 60 % rebate for every exploration dollar spent) in Alaska, including the Alaska North Slope, is incentivizing IOCs to increase activity in the region ▪ In mid - 2011 , SAE began operating under a 3 - year contract on the Cook Inlet in Alaska » Entrance into the North American market is consistent with the Company’s strategy to help increase the Company’s equipment utilization rates, and to offset the seasonality of the Canadian and Alaskan markets Country / Region SAE Presence Seismic Opportunity Oil Outlook Political Stability IOC Presence Alaska Canada Lower 48 Historical Revenue ($MM) (1,2) (1) Historical Revenue statistics illustrated above do not include corporate and inter - company eliminations (2) 2010 Revenues are unaudited Market Characteristics $ 2.4 $ 51.8 $ 122.1 $- $20.0 $40.0 $60.0 $80.0 $100.0 $120.0 $140.0 FY 2010 FY 2011 FY 2012 United States Canada

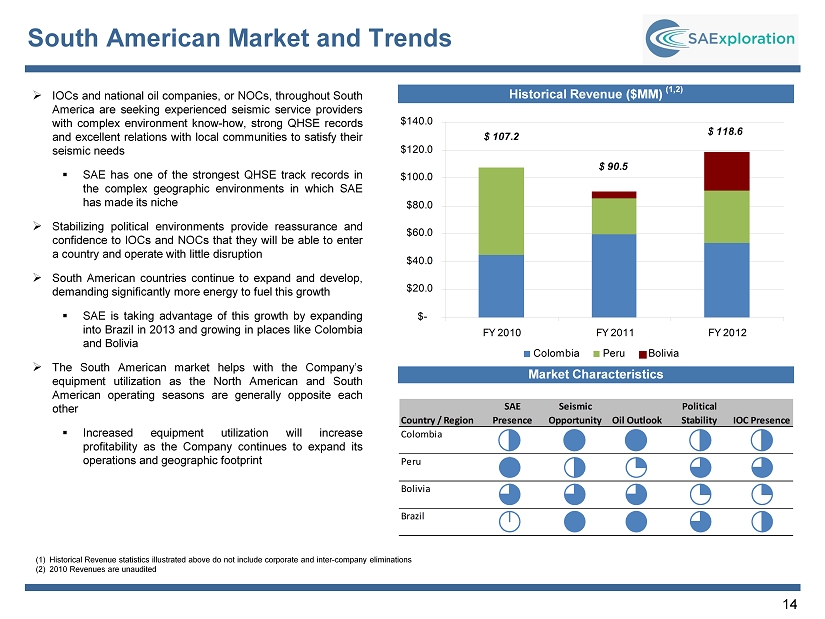

14 South American Market and Trends » IOCs and national oil companies, or NOCs, throughout South America are seeking experienced seismic service providers with complex environment know - how, strong QHSE records and excellent relations with local communities to satisfy their seismic needs ▪ SAE has one of the strongest QHSE track records in the complex geographic environments in which SAE has made its niche » Stabilizing political environments provide reassurance and confidence to IOCs and NOCs that they will be able to enter a country and operate with little disruption » South American countries continue to expand and develop, demanding significantly more energy to fuel this growth ▪ SAE is taking advantage of this growth by expanding into Brazil in 2013 and growing in places like Colombia and Bolivia » The South American market helps with the Company’s equipment utilization as the North American and South American operating seasons are generally opposite each other ▪ Increased equipment utilization will increase profitability as the Company continues to expand its operations and geographic footprint Historical Revenue ($MM) (1,2) Market Characteristics Country / Region SAE Presence Seismic Opportunity Oil Outlook Political Stability IOC Presence Colombia Peru Bolivia Brazil (1) Historical Revenue statistics illustrated above do not include corporate and inter - company eliminations (2) 2010 Revenues are unaudited $ 107.2 $ 90.5 $ 118.6 $- $20.0 $40.0 $60.0 $80.0 $100.0 $120.0 $140.0 FY 2010 FY 2011 FY 2012 Colombia Peru Bolivia

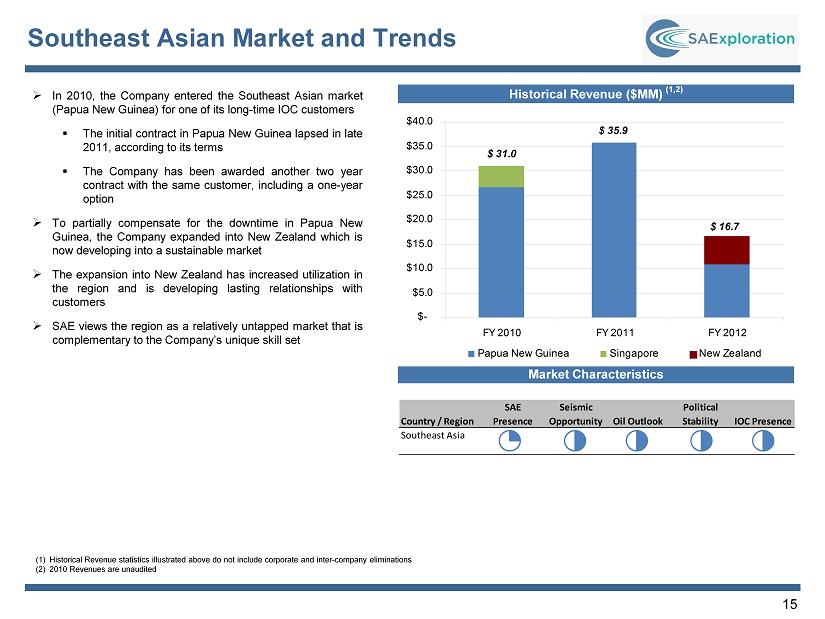

15 Southeast Asian Market and Trends » In 2010 , the Company entered the Southeast Asian market (Papua New Guinea) for one of its long - time IOC customers ▪ The initial contract in Papua New Guinea lapsed in late 2011 , according to its terms ▪ The Company has been awarded another two year contract with the same customer, including a one - year option » To partially compensate for the downtime in Papua New Guinea, the Company expanded into New Zealand which is now developing into a sustainable market » The expansion into New Zealand has increased utilization in the region and is developing lasting relationships with customers » SAE views the region as a relatively untapped market that is complementary to the Company’s unique skill set Historical Revenue ($MM) (1,2) Market Characteristics Country / Region SAE Presence Seismic Opportunity Oil Outlook Political Stability IOC Presence Southeast Asia (1) Historical Revenue statistics illustrated above do not include corporate and inter - company eliminations (2) 2010 Revenues are unaudited $ 31.0 $ 16.7 $ 35.9 $- $5.0 $10.0 $15.0 $20.0 $25.0 $30.0 $35.0 $40.0 FY 2010 FY 2011 FY 2012 Papua New Guinea Singapore New Zealand

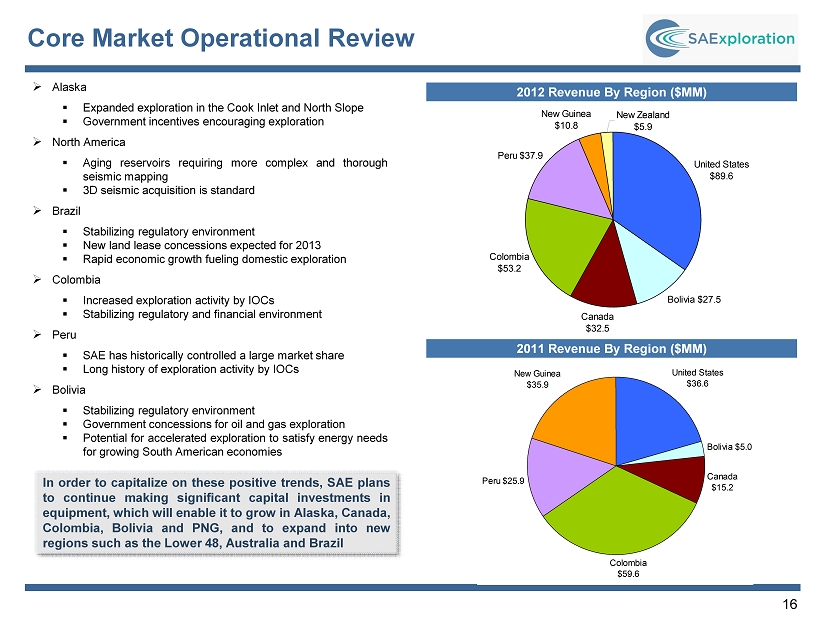

16 Core Market Operational Review » Alaska ▪ Expanded exploration in the Cook Inlet and North Slope ▪ Government incentives encouraging exploration » North America ▪ Aging reservoirs requiring more complex and thorough seismic mapping ▪ 3 D seismic acquisition is standard » Brazil ▪ Stabilizing regulatory environment ▪ New land lease concessions expected for 2013 ▪ Rapid economic growth fueling domestic exploration » Colombia ▪ Increased exploration activity by IOCs ▪ Stabilizing regulatory and financial environment » Peru ▪ SAE has historically controlled a large market share ▪ Long history of exploration activity by IOCs » Bolivia ▪ Stabilizing regulatory environment ▪ Government concessions for oil and gas exploration ▪ Potential for accelerated exploration to satisfy energy needs for growing South American economies 2012 Revenue By Region ($MM) In order to capitalize on these positive trends, SAE plans to continue making significant capital investments in equipment, which will enable it to grow in Alaska, Canada, Colombia, Bolivia and PNG, and to expand into new regions such as the Lower 48 , Australia and Brazil 2011 Revenue By Region ($MM) United States $89.6 Bolivia $27.5 Canada $32.5 Colombia $53.2 Peru $37.9 New Guinea $10.8 New Zealand $5.9 Bolivia $5.0 Canada $15.2 Colombia $59.6 Peru $25.9 New Guinea $35.9 United States $36.6

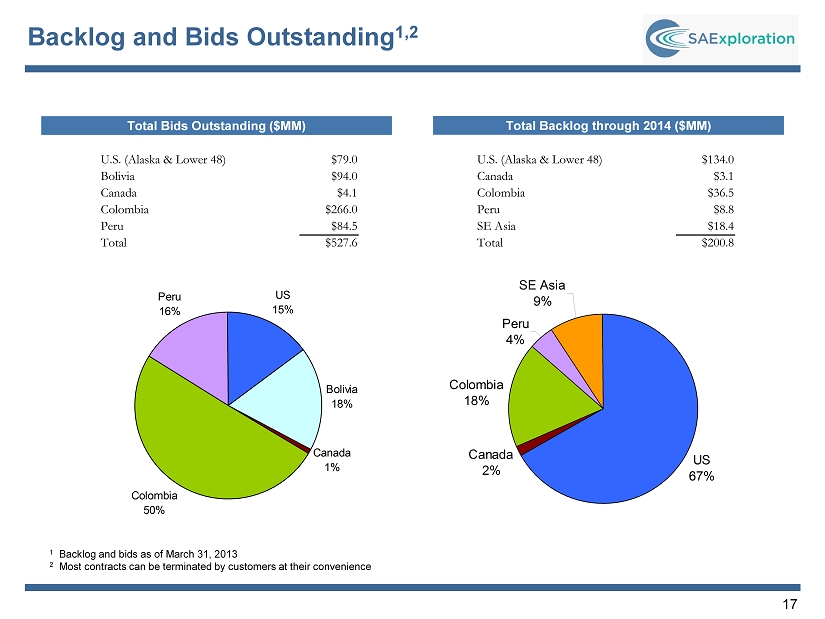

17 Backlog and Bids Outstanding 1,2 Total Bids Outstanding ($MM) Total Backlog through 2014 ($MM) U.S. (Alaska & Lower 48) $79.0 Bolivia $94.0 Canada $4.1 Colombia $266.0 Peru $84.5 Total $527.6 U.S. (Alaska & Lower 48) $134.0 Canada $3.1 Colombia $36.5 Peru $8.8 SE Asia $18.4 Total $200.8 US 15% Bolivia 18% Canada 1% Colombia 50% Peru 16% US 67% Canada 2% Colombia 18% Peru 4% SE Asia 9% 1 Backlog and bids as of March 31, 2013 2 Most contracts can be terminated by customers at their convenience

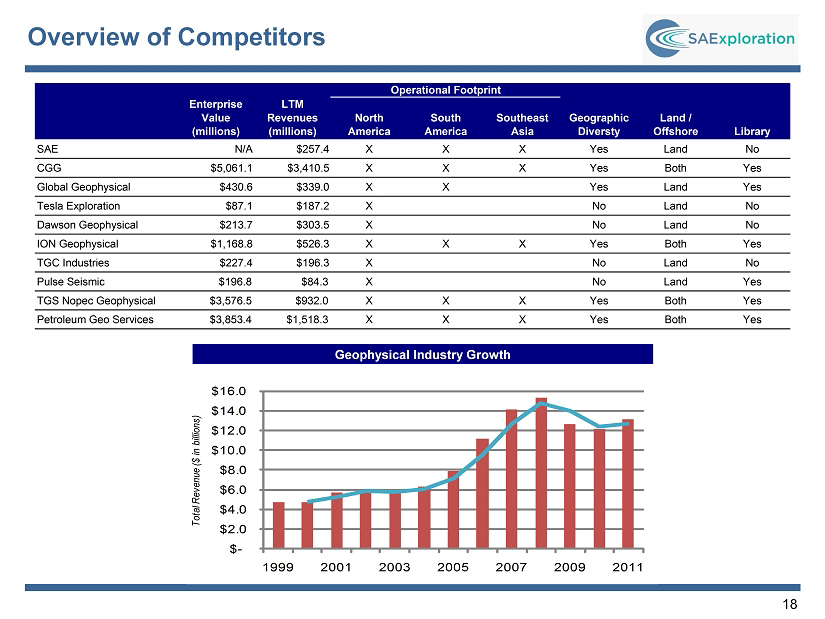

18 Overview of Competitors $ - $2.0 $4.0 $6.0 $8.0 $10.0 $12.0 $14.0 $16.0 1999 2001 2003 2005 2007 2009 2011 Total Revenue ($ in billions) Geophysical Industry Growth Geophysical Industry Growth Enterprise Value (millions) LTM Revenues (millions) North America South America Southeast Asia Geographic Diversty Land / Offshore Library SAE N/A $257.4 X X X Yes Land No CGG $5,061.1 $3,410.5 X X X Yes Both Yes Global Geophysical $430.6 $339.0 X X Yes Land Yes Tesla Exploration $87.1 $187.2 X No Land No Dawson Geophysical $213.7 $303.5 X No Land No ION Geophysical $1,168.8 $526.3 X X X Yes Both Yes TGC Industries $227.4 $196.3 X No Land No Pulse Seismic $196.8 $84.3 X No Land Yes TGS Nopec Geophysical $3,576.5 $932.0 X X X Yes Both Yes Petroleum Geo Services $3,853.4 $1,518.3 X X X Yes Both Yes Operational Footprint

19 Appendix » Historical financial results » Historical balance sheet » Historical cash flows

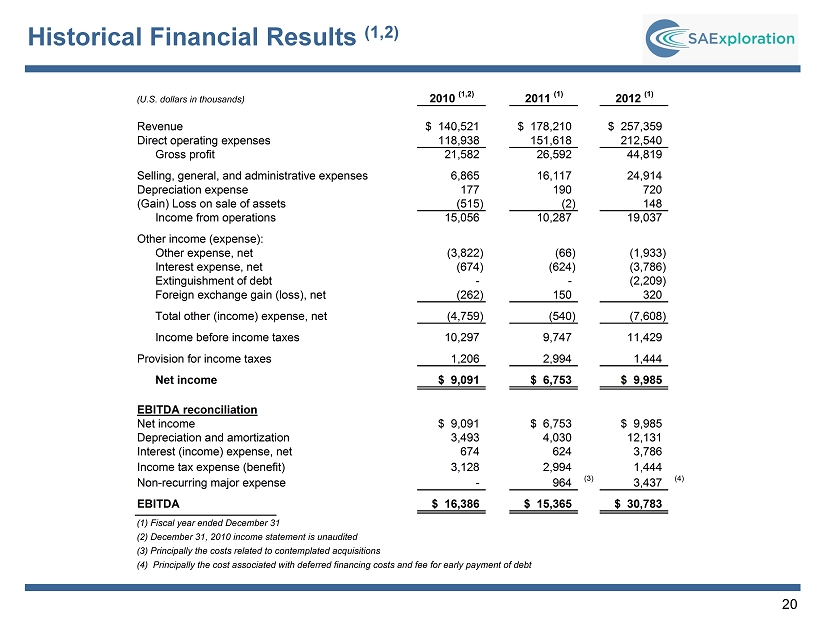

20 Historical Financial Results (1,2) (U.S. dollars in thousands) 2010 (1,2) 2011 (1) 2012 (1)Revenue $ 140,521 $ 178,210 $ 257,359 Direct operating expenses 118,938 151,618 212,540 Gross profit 21,582 26,592 44,819 Selling, general, and administrative expenses 6,865 16,117 24,914 Depreciation expense 177 190 720 (Gain) Loss on sale of assets (515) (2) 148 Income from operations 15,056 10,287 19,037 Other income (expense): Other expense, net (3,822) (66) (1,933) Interest expense, net (674) (624) (3,786) Extinguishment of debt - - (2,209) Foreign exchange gain (loss), net (262) 150 320 Total other (income) expense, net (4,759) (540) (7,608) Income before income taxes 10,297 9,747 11,429 Provision for income taxes 1,206 2,994 1,444 Net income $ 9,091 $ 6,753 $ 9,985 EBITDA reconciliation Net income $ 9,091 $ 6,753 $ 9,985 Depreciation and amortization 3,493 4,030 12,131 Interest (income) expense, net 674 624 3,786 Income tax expense (benefit) 3,128 2,994 1,444 Non-recurring major expense - 964 (3) 3,437 (4) EBITDA $ 16,386 $ 15,365 $ 30,783 (1) Fiscal year ended December 31 (2) December 31, 2010 income statement is unaudited (3) Principally the costs related to contemplated acquisitions (4) Principally the cost associated with deferred financing costs and fee for early payment of debt

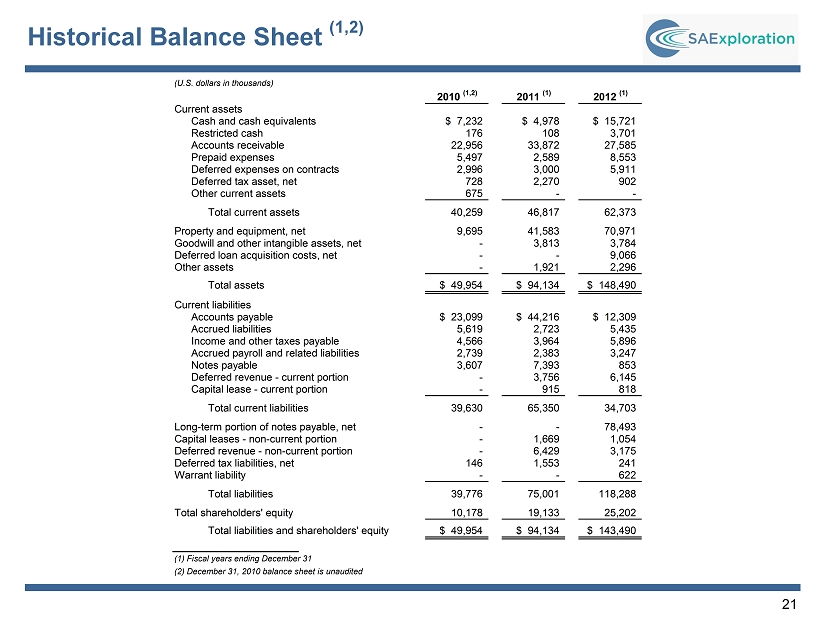

21 Historical Balance Sheet (1,2) (U.S. dollars in thousands) 2010 (1,2) 2011 (1) 2012 (1) Current assets Cash and cash equivalents $ 7,232 $ 4,978 $ 15,721 Restricted cash 176 108 3,701 Accounts receivable 22,956 33,872 27,585 Prepaid expenses 5,497 2,589 8,553 Deferred expenses on contracts 2,996 3,000 5,911 Deferred tax asset, net 728 2,270 902 Other current assets 675 - - Total current assets 40,259 46,817 62,373 Property and equipment, net 9,695 41,583 70,971 Goodwill and other intangible assets, net - 3,813 3,784 Deferred loan acquisition costs, net - - 9,066 Other assets - 1,921 2,296 Total assets $ 49,954 $ 94,134 $ 148,490 Current liabilities Accounts payable $ 23,099 $ 44,216 $ 12,309 Accrued liabilities 5,619 2,723 5,435 Income and other taxes payable 4,566 3,964 5,896 Accrued payroll and related liabilities 2,739 2,383 3,247 Notes payable 3,607 7,393 853 Deferred revenue - current portion - 3,756 6,145 Capital lease - current portion - 915 818 Total current liabilities 39,630 65,350 34,703 Long-term portion of notes payable, net - - 78,493 Capital leases - non-current portion - 1,669 1,054 Deferred revenue - non-current portion - 6,429 3,175 Deferred tax liabilities, net 146 1,553 241 Warrant liability - - 622 Total liabilities 39,776 75,001 118,288 Total shareholders' equity 10,178 19,133 25,202 Total liabilities and shareholders' equity $ 49,954 $ 94,134 $ 143,490 (1) Fiscal years ending December 31 (2) December 31, 2010 balance sheet is unaudited

22 Historical Summary Cash Flow Statements 2010 (1,2) 2011 (1) 2012 (1) Operating activities: Net income $9,091 $6,753 $9,985 Adjustments to reconcile net income to net cash (used in) provided by operating activities: Depreciation and amortization 3,493 4,110 12,470 Write off of loan issuance costs - - 1,229 Deferred income taxes - (477) (1,566) Loss (gain) on sale of property and equipment (1,135) (2) 148 Share-based compensation (515) - 21 Changes in operating assets and liabilities, net of effects of acquisition 2,516 8,277 (23,775) Net cash (used in) provided by operating activities 13,450 18,661 (1,488) Investing activities: Purchase of property and equipment (8,844) (22,231) (49,949) Acquisition of business, net of cash received - (1,322) (760) Proceeds from sale of property and equipment 1,005 23 849 Net cash used in investing activities (7,839) (23,530) (49,860) Financing activities: Principal borrowings on notes payable 2,284 4,139 105,220 Repayments on notes payable, other (4,100) (650) (31,335) Repayments of advances from related parties (928) (895) (1,917) Advances from related parties 1,648 1,192 - Repayments of capital lease obligations (170) (225) (1,122) Dividend payments (154) (359) (168) Payments of loan issuance costs - - (8,657) Net cash provided by financing activities (1,420) 3,202 62,021 Effects of exchange rate changes on cash (171) (587) 70 Net change in cash and cash equivalents 4,020 (2,254) 10,743 Cash at the beginning of period 3,211 7,232 4,978 Cash at the end of period $7,231 $4,978 $15,721 (1) Fiscal years ending December 31 (2) December 31, 2010 cash flow statement is unaudited