Exhibit 99.1

Investors:

Ryan Osterholm: 630-824-1907

Media:

Anna Rozenich: 630-824-1945

SUNCOKE ENERGY, INC. THIRD QUARTER 2011 RESULTS

REFLECT SEQUENTIAL QUARTERLY IMPROVEMENT

| • | Operating income was $30.1 million in third quarter 2011 down from $48.4 million in third quarter 2010 primarily due to contract amendments with ArcelorMittal |

| • | Third quarter 2011 Adjusted EBITDA of $44.8 million reflects sequential improvement over first and second quarter 2011 |

| • | Achieved record domestic cokemaking production of 964 thousand tons in the quarter, driven by strong performance at Indiana Harbor operations |

| • | Increased ownership in Indiana Harbor cokemaking facility partnership |

| • | Recently constructed Middletown, Ohio facility delivered first metallurgical coke production to AK Steel |

| • | Higher metallurgical coal pricing drove improved results at coal mining operations; planned expansion slowed to drive operational improvements |

Lisle, IL. (November 2, 2011) – SunCoke Energy, Inc. (NYSE: SXC) today reported third quarter 2011 net income attributable to shareholders of $18.4 million compared with $37.4 million for the third quarter 2010. On a per share basis, third quarter 2011 earnings were $0.26 per share compared with $0.53 per share for the third quarter 2010.

“SunCoke Energy’s ongoing focus on operational excellence in our coke and coal businesses drove sequential improvement in our quarterly results for the last two quarters. We are encouraged by the early operational momentum we are experiencing in the business, and believe we have the people, systems and plan in place to drive improved and consistent performance across our Company,” said Frederick “Fritz” A. Henderson, Chairman and Chief Executive Officer of SunCoke Energy, Inc. “Our U.S. cokemaking business, which operated at more than 100% capacity, produced a record level of coke in the quarter. The coal mining segment delivered better year-over-year results on stronger metallurgical coal pricing. Nonetheless, our mining operations continue to be challenged by higher cash costs, deteriorating yields and diminished production. As a result, we have decided to slow our planned expansion to focus our efforts on operational improvements in our existing mines and to augment compliance activities. Our results were also impacted by administrative costs related to becoming an independent, standalone public company, nonrecurring headquarters relocation activity and start up costs at our new Middletown, Ohio facility.”

Henderson also noted that, “Early this week, we completed our first delivery of metallurgical coke to our customer AK Steel from the newly constructed Middletown operation. Over the next several months, our plan is to ramp-up production at Middletown with the expectation that we will be operating at full capacity by July 2012.”

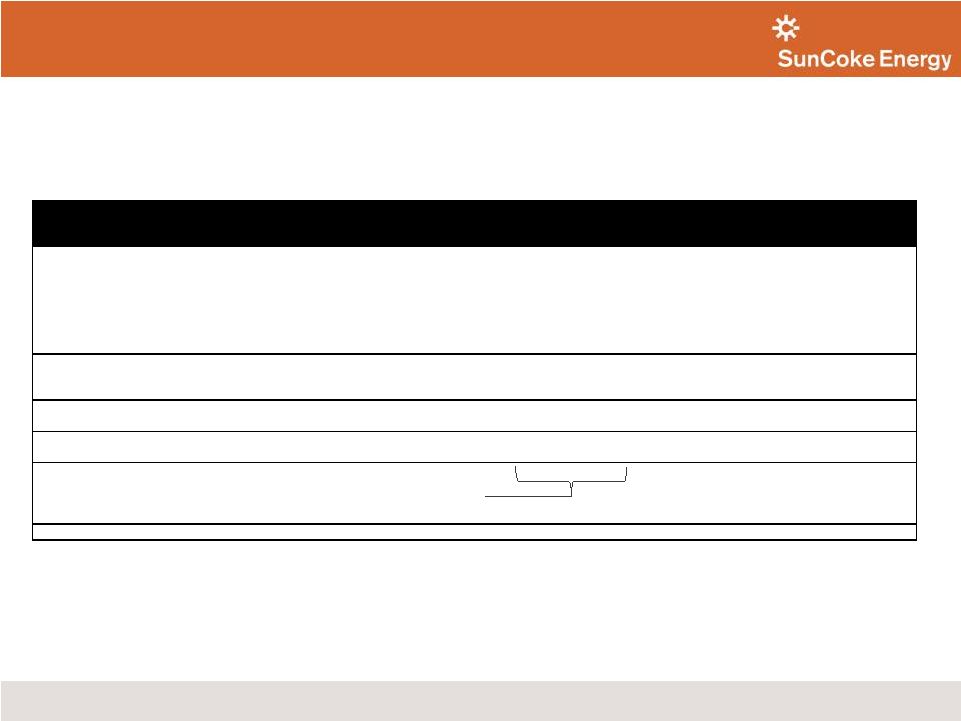

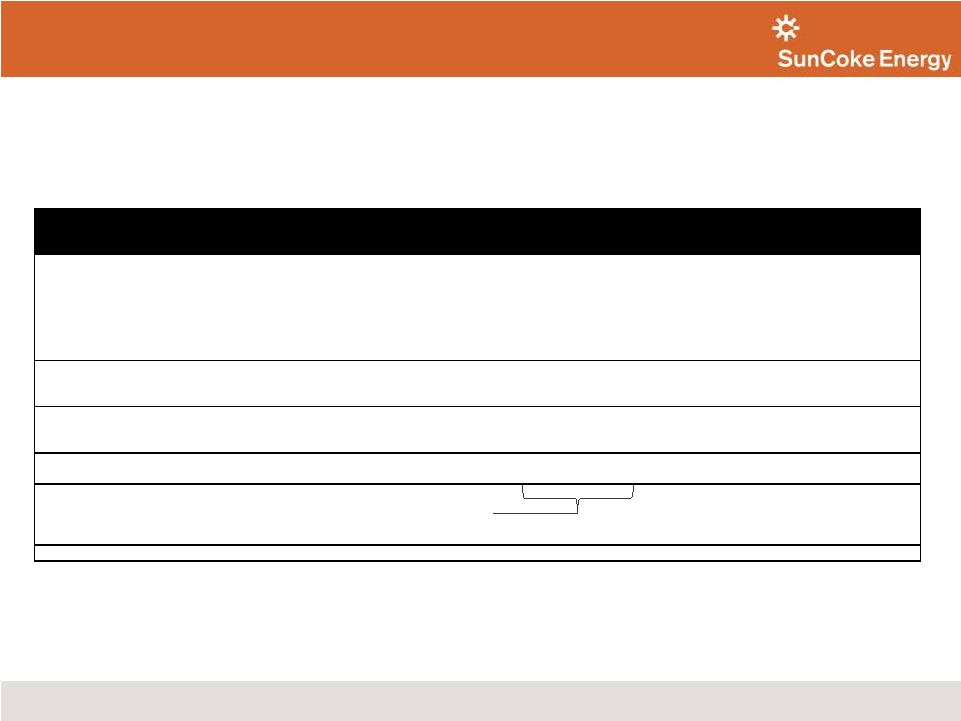

CONSOLIDATED RESULTS

| Three Months Ended September 30, | ||||||||||||

| (In millions) |

2011(2) | 2010 | Increase/ Decrease |

|||||||||

| Revenues |

$ | 403.5 | $ | 331.6 | $ | 71.9 | ||||||

| Operating Income |

$ | 30.1 | $ | 48.4 | ($ | 18.3 | ) | |||||

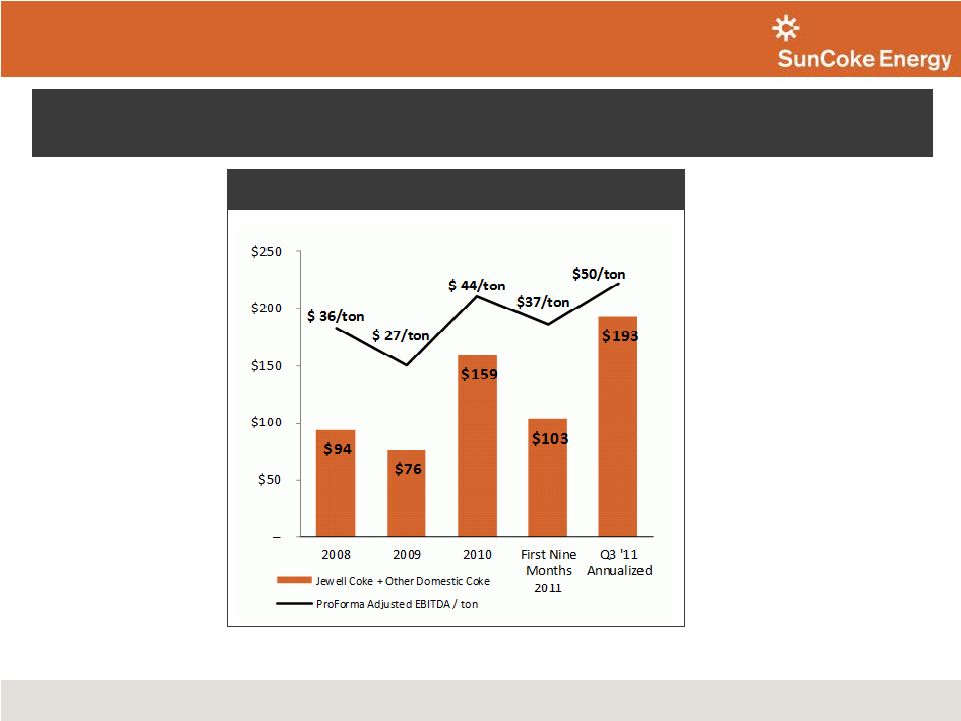

| Adjusted EBITDA(1) |

$ | 44.8 | $ | 62.2 | ($ | 17.4 | ) | |||||

| Net Income Attributable to Shareholders |

$ | 18.4 | $ | 37.4 | ($ | 19.0 | ) | |||||

| (1) | See definitions of Adjusted EBITDA and reconciliations of Adjusted EBITDA elsewhere in this release. |

| (2) | Reflects impact of contract amendments with ArcelorMittal that became effective in first quarter 2011. Had these revised provisions been in place in 2010, revenues, operating income, Adjusted EBITDA and net income attributable to shareholders (assuming a 37 percent tax rate ) would have been $7.9 million, $7.9 million, $7.9 million and $5.0 million lower, respectively, in third quarter 2010. |

Revenues rose 22 percent to $403.5 million in the third quarter 2011 versus third quarter 2010 due to increased sales in our Other Domestic Coke segment driven by higher coal prices and the sales contribution from Harold Keene Coal Company, Inc. (“HKCC”), which was acquired in January 2011. Comparability between years is impacted by a lower coke sales price in the Jewell Coke segment resulting from the January 2011 contract amendments with ArcelorMittal. These contract changes eliminated the fixed adjustment factor in the coke pricing formula and as a result, significantly reduced the impact of higher coal prices on the financial results of the Jewell Coke segment. The amendments also increased the operating cost and fixed fee components the Company receives under its Jewell Coke and Haverhill contracts with ArcelorMittal and extended the take-or-pay terms of these contracts to 2020.

Operating income, Adjusted EBITDA and net income attributable to shareholders declined in the third quarter 2011 due to the impact of the contract amendments discussed above and higher costs and operating expenses. The increased costs were driven by higher coal production costs, increased coal and coke volumes, the impact of HKCC and higher corporate expenses associated with public company readiness and relocation costs.

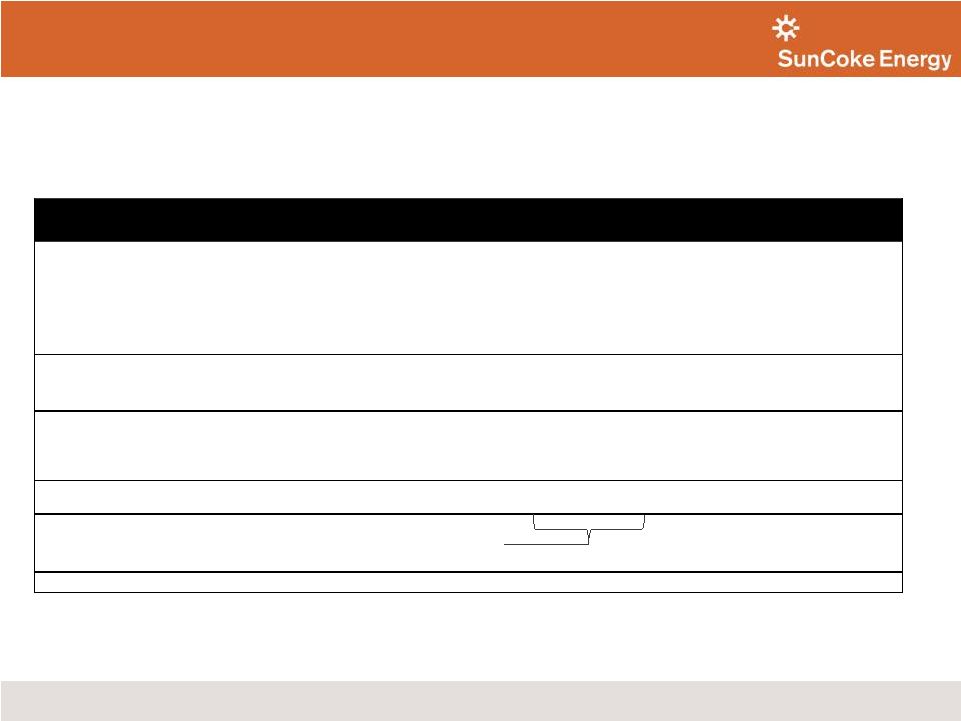

SEGMENT RESULTS

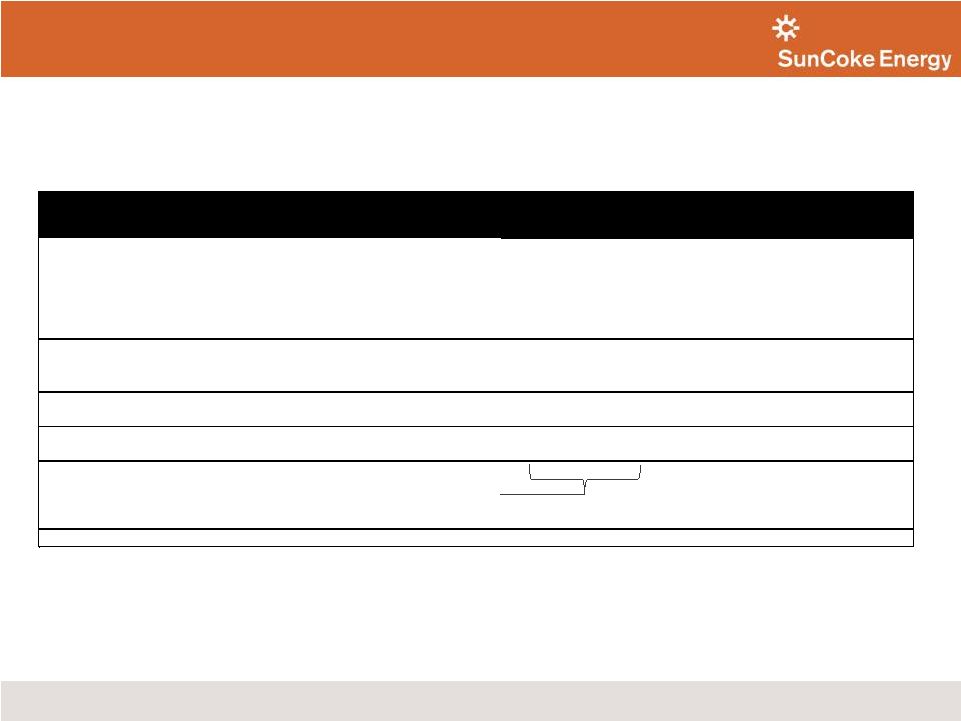

Jewell Coke

The Jewell Coke segment consists of the operations of the Company’s cokemaking facilities in Vansant, VA. Substantially all of the metallurgical coal used at our Jewell cokemaking facility is supplied from our coal mining operations.

| Three Months Ended September 30, | ||||||||||||

| (In millions, except per ton amounts) |

2011(2) | 2010 | Increase/ Decrease |

|||||||||

| Segment Earnings (1) |

$ | 13.1 | $ | 27.0 | ($ | 13.9 | ) | |||||

| Adjusted EBITDA(1) |

$ | 14.3 | $ | 28.1 | ($ | 13.8 | ) | |||||

| Sales Volumes (in thousand tons) |

191 | 196 | (5 | ) | ||||||||

| Adjusted EBITDA/Ton(1) |

$ | 75 | $ | 143 | ($ | 68 | ) | |||||

| (1) | See definitions of Segment Earnings, Adjusted EBITDA and Adjusted EBITDA/Ton and reconciliations of Adjusted EBITDA elsewhere in this release. |

| (2) | Reflects impact of contract amendments with ArcelorMittal that became effective in first quarter 2011. Had these revised provisions been in place in 2010, segment earnings and Adjusted EBITDA would have each been $12.8 million lower in the third quarter 2010. |

2

| • | The decline in segment earnings and Adjusted EBITDA was due to: |

| • | The previously discussed contract amendments with ArcelorMittal, which accounted for $12.8 million of the decline in segment earnings and Adjusted EBITDA. |

| • | Internal coal transfer pricing increased from $103.68 per ton in the third quarter 2010 to $163.53 per ton in the third quarter 2011, negatively impacting segment earnings by $15.7 million, with a corresponding increase in the earnings of the Coal Mining segment. Other items, including the absence of spot coke sales made in the third quarter 2010 and slightly lower sales volumes, reduced segment earnings by approximately $2.4 million. These items were offset by $17.0 million of higher revenues, which resulted from the pass-through of higher coal costs. |

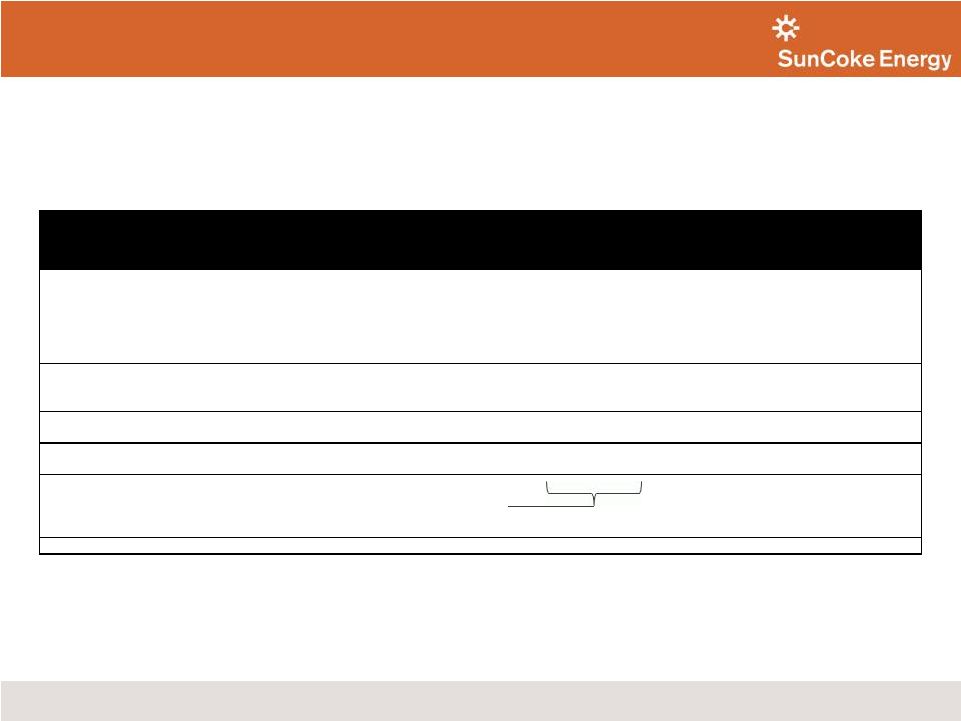

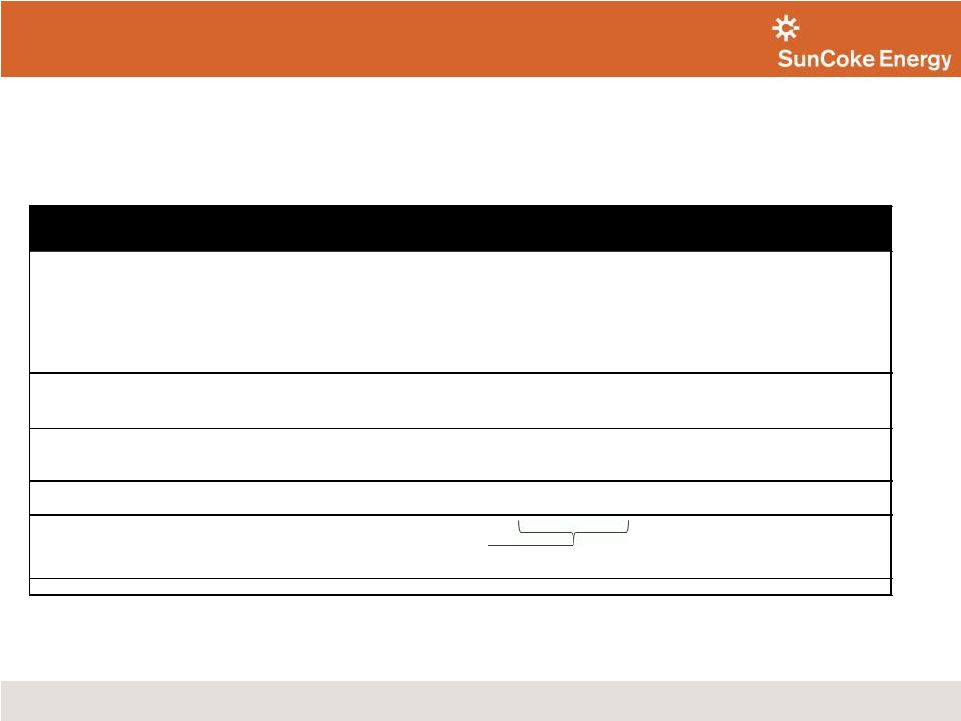

Other Domestic Coke

Other Domestic Coke consists of cokemaking facilities and heat recovery operations at the Indiana Harbor, Haverhill, and Granite City plants in East Chicago, Indiana, Franklin Furnace, Ohio and Granite City, Illinois, respectively. On September 30, 2011, we increased our ownership in the partnership that owns the Indiana Harbor cokemaking facility from 66 percent to 85 percent by acquiring the interest held by one of the third-party partners.

| Three Months Ended September 30, | ||||||||||||

| (In millions, except per ton amounts) |

2011 | 2010 | Increase/ Decrease |

|||||||||

| Segment Earnings(1)(2) |

$ | 22.1 | $ | 24.5 | ($ | 2.4 | ) | |||||

| Adjusted EBITDA(1)(2) |

$ | 34.3 | $ | 37.5 | ($ | 3.2 | ) | |||||

| Sales Volumes (in thousand tons) |

777 | 788 | (11 | ) | ||||||||

| Adjusted EBITDA/Ton(1)(2) |

$ | 44 | $ | 48 | ($ | 4 | ) | |||||

| (1) | See definitions of Segment Earnings, Adjusted EBITDA and Adjusted EBITDA/Ton and reconciliations of Adjusted EBITDA elsewhere in this release. |

| (2) | Excludes income (loss) attributable to noncontrolling investors in Indiana Harbor. |

| • | Segment earnings and Adjusted EBITDA declined due to: |

| • | A decline in coal and operating cost recovery of $3.4 million at Haverhill due to a change in the coke pricing mechanism in our AK Steel-Haverhill contract from fixed pricing in 2010 to pass-through pricing in 2011, which reduced coke margins by $1.4 million as well as the absence of a favorable coal inventory adjustment in the prior year period, which reduced margins by $2.0 million. |

| • | Lower recovery of coal and operating costs at Granite City and Indiana Harbor of $2.9 million. The decrease was primarily driven by the absence of a favorable coal inventory adjustment and strong coal-to-coke yield performance in the third quarter 2010. |

| • | These declines were partly offset by increased fee revenue of $4.9 million at Haverhill due to the previously discussed ArcelorMittal-Haverhill contract amendments. |

| • | Operating income attributable to noncontrolling interests decreased segment earnings by $2.4 million in the third quarter 2011 and $2.5 million in third quarter 2010. |

International Coke

International Coke consists of a cokemaking facility in Vitória, Brazil, which we operate for a Brazilian affiliate of ArcelorMittal. International Coke earns operating and technology licensing fees based on production, and recognizes a dividend on its preferred stock investment, generally in the fourth quarter, assuming certain minimum production levels are achieved at the facility.

3

| • | Segment earnings increased to $1.7 million in the third quarter up from $0.6 million in the prior year. The increase is due primarily to lower selling, general and administrative costs as a result of a change in the corporate allocation methodology. |

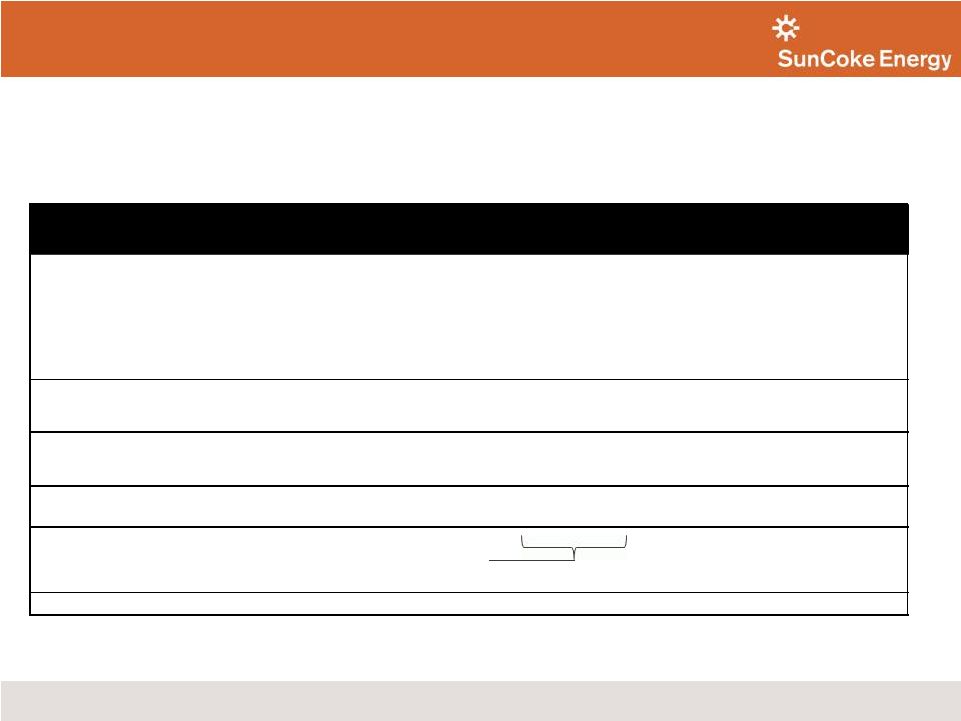

Coal Mining

Coal Mining consists of our metallurgical coal mining activities conducted in Virginia and West Virginia, and includes the results of HKCC, which was acquired in January 2011. A substantial portion of the metallurgical coal produced by our coal mining operations is sold to our Jewell segment for conversion into metallurgical coke.

| Three Months Ended September 30, | ||||||||||||

| (In millions, except per ton amounts) |

2011 | 2010 | Increase/ Decrease |

|||||||||

| Segment Earnings (1) |

$ | 5.5 | ($ | 2.7 | ) | $ | 8.2 | |||||

| Adjusted EBITDA (1) |

$ | 8.8 | ($ | 0.7 | ) | $ | 9.5 | |||||

| Sales Volumes (in thousand tons)(2) |

371 | 314 | 57 | |||||||||

| Sales Price per ton (excludes transportation costs)(3) |

$ | 154 | $ | 104 | $ | 50 | ||||||

| Adjusted EBITDA/Ton (1) |

$ | 24 | (2 | ) | $ | 26 | ||||||

| (1) | See definitions of Segment Earnings, Adjusted EBITDA and Adjusted EBITDA/Ton and reconciliations of Adjusted EBITDA elsewhere in this release. |

| (2) | Includes sales to affiliates and third party sales. |

| (3) | Includes sales to affiliates, including sales to Jewell Coke established via a transfer pricing agreement. |

| • | Segment earnings and Adjusted EBITDA benefited from $11.9 million in higher intersegment sales and $12.7 million in higher third-party sales, $4.3 million of which were attributable to HKCC. |

| • | Partially offsetting these increases was $17.3 million in higher operating costs, of which $13.7 million were from existing operations and $3.6 million were due to HKCC. The cost increase at existing operations were a result of incremental expenses associated with training, higher wage rates, the implementation of a new bonus program to retain skilled mine employees and higher royalty payments. In addition, lower productivity due to labor shortages and the variations in the thickness and quality of the coal seams reduced Jewell production volumes, which negatively impacted coal cash production costs per ton. A favorable fair value adjustment of $1.9 million relating to the HKCC contingent consideration arrangement that requires the payment of royalties to HKCC’s former owners reduced coal production costs. |

| • | Segment earnings were also impacted by higher selling, general and administrative expense of $1.0 million and higher depreciation, depletion and amortization expenses of $1.4 million. |

Corporate and Other

Corporate expenses increased $11.1 million to $14.6 million for the third quarter 2011 compared to the third quarter 2010. This increase was primarily driven by additional headcount and expenses required to operate as a public company, $2.5 million in expenses related to the start up of Middletown and $1.7 million in restructuring costs. On an annualized basis, the incremental costs related to becoming a public company in the quarter approximates the expected annual range of $15 million to $20 million.

Net financing expense was $4.3 million for the third quarter 2011 as compared with $4.0 million of income for the third quarter 2010. This change reflects $8.9 million of interest expense associated with the issuance of debt, a $4.4 million increase in capitalized interest related to capital projects and a $5.1 million decrease in interest income from Claymont, a subsidiary of Sunoco, Inc. (“Sunoco”).

4

COMBINED CASH FLOWS AND FINANCIAL POSITION

Cash Flows

Net cash provided by operating activities decreased by $195.2 million for the nine months ended September 30, 2011 to $58.7 million primarily due to increases in working capital in 2011 largely due to an increase in coal and coke inventories and higher accounts receivable, partly offset by higher accounts payable related to inventory purchases. Lower net income also contributed to the decrease in cash from operations.

Capital expenditures were $184.2 million during the nine months ended September 30, 2011, of which $145.4 million was attributable to the construction of our new Middletown, Ohio facility. With the completion of the Middletown facility, we anticipate capital expenditures will be lower in 2012, which will have positive implications for our free cash flow (defined as cash provided by operations less cash used in investing activities less cash distributions to noncontrolling interests).

Total cash and cash equivalents on September 30, 2011 was $110.9 million, an increase of $80.4 million since June 30, 2011. The increase in cash position during the third quarter 2011 is primarily attributable to the net issuance of $679.6 million of long-term debt and $42.3 million in cash generated from operations offset by a net change in advances from and payables to affiliate of $550.5 million, capital expenditures of $56.2 million and $34.0 million used to purchase the interest of a third-party minority partner in the Indiana Harbor cokemaking operations.

INITIAL PUBLIC OFFERING AND RELATED TRANSACTIONS

The financial results contained in this release that relate to periods that ended prior to the completion of our initial public offering of 13,340,000 shares of common stock (the “IPO”) on July 26, 2011, and prior to the effective dates of the agreements we entered into with Sunoco in connection with the IPO and our separation from Sunoco, pertain to the operations that comprised the cokemaking and coal mining operations of Sunoco prior to their transfer to us.

DEFINITIONS

| • | Adjusted EBITDA represents earnings before interest, taxes, depreciation, depletion and amortization (“EBITDA”) adjusted for sales discounts and the deduction of income attributable to non-controlling interests in our Indiana Harbor cokemaking operations. EBITDA reflects sales discounts included as a reduction in sales and other operating revenue. The sales discounts represent the sharing with customers of a portion of nonconventional fuels tax credits, which reduce our income tax expense. However, we believe our Adjusted EBITDA would be inappropriately penalized if these discounts were treated as a reduction of EBITDA since they represent sharing of a tax benefit which is not included in EBITDA. Accordingly, in computing Adjusted EBITDA, we have added back these sales discounts. Our Adjusted EBITDA also reflects the deduction of income attributable to noncontrolling interests in our Indiana Harbor cokemaking operations. EBITDA and Adjusted EBITDA do not represent and should not be considered alternatives to net income or operating income under GAAP and may not be comparable to other similarly titled measures in other businesses. Management believes Adjusted EBITDA is an important measure of the operating performance of the Company’s net assets and is indicative of the Company’s ability to generate cash from operations. See the tables (unaudited) at the end of this release for reconciliations of net income and operating income to EBITDA and Adjusted EBITDA. |

| • | Adjusted EBITDA/Ton represents Adjusted EBITDA divided by tons sold. |

5

| • | Segment Earnings represents operating income attributable to SunCoke shareholders of our segments: Jewell Coke, Other Domestic Coke, International Coke and Coal Mining. |

RELATED COMMUNICATIONS

SunCoke Energy, Inc. will host an investor conference call today at 10:00 AM ET (9:00 AM CT). This call will be webcast live and archived for replay in the Investor Relations section of the Company’s website at www.suncoke.com. To listen to the live call, dial 800-471-6718 (domestic) or 630-691-2735 (international), confirmation code: 30885786. Please connect at least 10 minutes prior to start time. A recorded replay will be available for seven days by calling 888-843-7419 (domestic) or 630-652-3042, confirmation code: 30885786#.

SUNCOKE ENERGY, INC.

SunCoke Energy, Inc. is the largest independent producer of metallurgical coke in the Americas, with more than 45 years of experience supplying coke to the integrated steel industry. Our advanced, heat recovery cokemaking process produces high-quality coke for use in steelmaking, captures waste heat for derivative energy resale and meets or exceeds environmental standards. Our cokemaking facilities are located in Virginia, Indiana, Ohio, Illinois and Vitoria, Brazil, and our coal mining operations, which have more than 100 million tons of proven and probable reserves, are located in Virginia and West Virginia. To learn more about SunCoke Energy, Inc., visit our website at www.suncoke.com.

FORWARD LOOKING STATEMENTS

Some of the statements included in this press release constitute “forward looking statements” (as defined in Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities Exchange Act of 1934, as amended). Such forward-looking statements are based on management’s beliefs and assumptions and on information currently available. Forward-looking statements include the information concerning SunCoke’s possible or assumed future results of operations, business strategies, financing plans, competitive position, potential growth opportunities, potential operating performance improvements, effects resulting from our separation from Sunoco, the effects of competition and the effects of future legislation or regulations. Forward-looking statements include all statements that are not historical facts and may be identified by the use of forward looking terminology such as the words “believe,” “expect,” “plan,” “intend,” “anticipate,” “estimate,” “predict,” “potential,” “continue,” “may,” “will,” “should” or the negative of these terms or similar expressions. Forward-looking statements involve risks, uncertainties and assumptions. Actual results may differ materially from those expressed in these forward-looking statements. You should not put undue reliance on any forward-looking statements.

In accordance with the safe harbor provisions of the Private Securities Litigation Reform Act of 1995, SunCoke has included in its filings with the Securities and Exchange Commission cautionary language identifying important factors (but not necessarily all the important factors) that could cause actual results to differ materially from those expressed in any forward-looking statement made by SunCoke. For more information concerning these factors, see SunCoke’s Securities and Exchange Commission filings. All forward-looking statements included in this press release are expressly qualified in their entirety by such cautionary statements. SunCoke undertakes no obligation to update publicly any forward-looking statement (or its associated cautionary language) whether as a result of new information, future events or otherwise.

###

6

SunCoke Energy, Inc.

Combined and Consolidated Statements of Income

(Unaudited)

| For the Three Months Ended September 30 |

For the Nine Months Ended September 30 |

|||||||||||||||

| (Dollars and shares in thousands, except per share amounts) | 2011 | 2010 | 2011 | 2010 | ||||||||||||

| Revenues |

||||||||||||||||

| Sales and other operating revenue |

$ | 403,100 | $ | 330,628 | $ | 1,113,724 | $ | 1,009,197 | ||||||||

| Other income, net |

399 | 1,007 | 1,051 | 180 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total revenues |

403,499 | 331,635 | 1,114,775 | 1,009,377 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Costs and operating expenses |

||||||||||||||||

| Cost of products sold and operating expenses |

332,723 | 254,524 | 933,266 | 773,510 | ||||||||||||

| Loss on firm purchase commitments |

— | — | 18,544 | — | ||||||||||||

| Selling, general and administrative expenses |

25,939 | 14,732 | 64,803 | 41,537 | ||||||||||||

| Depreciation, depletion and amortization |

14,752 | 14,013 | 42,377 | 35,832 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total costs and operating expenses |

373,414 | 283,269 | 1,058,990 | 850,879 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Operating income |

30,085 | 48,366 | 55,785 | 158,498 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Interest income—affiliate |

1,123 | 6,186 | 12,485 | 17,965 | ||||||||||||

| Interest income |

166 | 2 | 284 | 33 | ||||||||||||

| Interest cost—affiliate |

(342 | ) | (1,330 | ) | (3,565 | ) | (4,422 | ) | ||||||||

| Interest cost |

(8,860 | ) | — | (8,860 | ) | — | ||||||||||

| Capitalized interest |

4,633 | 206 | 5,344 | 421 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total financing (expense) income |

(3,280 | ) | 5,064 | 5,688 | 13,997 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Income before income tax expense |

26,805 | 53,430 | 61,473 | 172,495 | ||||||||||||

| Income tax expense |

5,073 | 12,490 | 10,093 | 41,266 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income |

21,732 | 40,940 | 51,380 | 131,229 | ||||||||||||

| Less: Net income (loss) income attributable to noncontrolling interests |

3,372 | 3,494 | (1,226 | ) | 10,466 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income attributable to SunCoke Energy, Inc./net parent investment |

$ | 18,360 | $ | 37,446 | $ | 52,606 | $ | 120,763 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings per common share: |

||||||||||||||||

| Basic |

$ | 0.26 | $ | 0.53 | $ | 0.75 | $ | 1.73 | ||||||||

| Diluted |

$ | 0.26 | $ | 0.53 | $ | 0.75 | $ | 1.73 | ||||||||

| Weighted average common shares outstanding: |

||||||||||||||||

| Basic |

70,000 | 70,000 | 70,000 | 70,000 | ||||||||||||

| Diluted |

70,000 | 70,000 | 70,000 | 70,000 | ||||||||||||

7

SunCoke Energy, Inc.

Combined and Consolidated Balance Sheets

| September 30, 2011 |

December 31, 2010 |

|||||||

| (Dollars and shares in thousands, except per share amounts) | (Unaudited) | |||||||

| Assets |

||||||||

| Cash and cash equivalents |

$ | 110,850 | $ | 40,092 | ||||

| Accounts receivable |

52,033 | 44,606 | ||||||

| Inventories |

222,436 | 106,610 | ||||||

| Receivable from affiliate |

672 | — | ||||||

| Deferred income taxes |

552 | 1,140 | ||||||

|

|

|

|

|

|||||

| Total current assets |

386,543 | 192,448 | ||||||

|

|

|

|

|

|||||

| Notes receivable from affiliate |

— | 289,000 | ||||||

| Investment in Brazilian cokemaking operations |

40,976 | 40,976 | ||||||

| Properties, plants and equipment, net |

1,353,499 | 1,173,518 | ||||||

| Lease and mineral rights, net |

53,392 | 6,690 | ||||||

| Goodwill |

9,388 | 3,400 | ||||||

| Deferred charges and other assets |

35,396 | 12,434 | ||||||

|

|

|

|

|

|||||

| Total assets |

$ | 1,879,194 | $ | 1,718,466 | ||||

|

|

|

|

|

|||||

| Liabilities and Equity |

||||||||

| Advances from affiliate |

$ | — | $ | 888,512 | ||||

| Accounts payable |

185,184 | 106,350 | ||||||

| Current portion of long-term debt |

3,000 | — | ||||||

| Accrued liabilities |

51,996 | 53,158 | ||||||

| Taxes payable |

11,593 | 7,704 | ||||||

|

|

|

|

|

|||||

| Total current liabilities |

251,773 | 1,055,724 | ||||||

|

|

|

|

|

|||||

| Long-term debt |

694,784 | — | ||||||

| Payable to affiliate |

— | 55,813 | ||||||

| Accrual for black lung benefits |

27,538 | 26,605 | ||||||

| Retirement benefit liabilities |

45,281 | 42,854 | ||||||

| Deferred income taxes |

223,840 | 85,930 | ||||||

| Asset retirement obligations |

12,236 | 11,014 | ||||||

| Other deferred credits and liabilities |

19,247 | 11,185 | ||||||

| Commitments and contingent liabilities |

||||||||

|

|

|

|

|

|||||

| Total liabilities |

1,274,699 | 1,289,125 | ||||||

|

|

|

|

|

|||||

| Equity |

||||||||

| Preferred stock, $0.01 par value. Authorized 50,000 shares; no issued and outstanding shares at September 30, 2011 and December 31, 2010 |

— | — | ||||||

| Common stock, $0.01 par value. Authorized 300,000 shares; issued and outstanding 70,006 shares at September 30, 2011 and no shares outstanding at December 31, 2010 |

700 | — | ||||||

| Additional paid-in capital |

556,292 | — | ||||||

| Accumulated other comprehensive income |

437 | — | ||||||

| Retained earnings |

12,003 | — | ||||||

| Net parent investment |

— | 369,541 | ||||||

|

|

|

|

|

|||||

| Total SunCoke Energy, Inc. stockholders’ equity / net parent investment |

569,432 | 369,541 | ||||||

| Noncontrolling interests |

35,063 | 59,800 | ||||||

|

|

|

|

|

|||||

| Total equity |

604,495 | 429,341 | ||||||

|

|

|

|

|

|||||

| Total liabilities and equity |

$ | 1,879,194 | $ | 1,718,466 | ||||

|

|

|

|

|

|||||

8

SunCoke Energy, Inc.

Combined and Consolidated Statements of Cash Flows

(Unaudited)

| For the Nine Months Ended September 30 |

||||||||

| (Dollars in thousands) | 2011 | 2010 | ||||||

| Cash Flows from Operating Activities: |

||||||||

| Net income |

$ | 51,380 | $ | 131,229 | ||||

| Adjustments to reconcile net income to net cash provided by operating activities: |

||||||||

| Loss on firm purchase commitment |

18,544 | — | ||||||

| Depreciation, depletion and amortization |

42,377 | 35,832 | ||||||

| Deferred income tax expense |

14,630 | 10,885 | ||||||

| Payments less than (in excess of) expense for retirement plans |

267 | (3,081 | ) | |||||

| Changes in working capital pertaining to operating activities: |

||||||||

| Accounts receivable |

(4,157 | ) | 41,994 | |||||

| Inventories |

(112,822 | ) | (1,353 | ) | ||||

| Accounts payable and accrued liabilities |

53,904 | 42,590 | ||||||

| Taxes payable |

(2,236 | ) | 2,836 | |||||

| Other |

(3,208 | ) | (7,007 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by operating activities |

58,679 | 253,925 | ||||||

|

|

|

|

|

|||||

| Cash Flows from Investing Activities: |

||||||||

| Capital expenditures |

(184,217 | ) | (135,833 | ) | ||||

| Acquisition of business, net of cash received |

(37,575 | ) | — | |||||

| Proceeds from sales of assets |

— | 72 | ||||||

|

|

|

|

|

|||||

| Net cash used in investing activities |

(221,792 | ) | (135,761 | ) | ||||

|

|

|

|

|

|||||

| Cash Flows from Financing Activities: |

||||||||

| Proceeds from issuance of long-term debt |

698,500 | — | ||||||

| Debt issuance costs |

(18,874 | ) | — | |||||

| Repayment of long-term debt |

(750 | ) | — | |||||

| Purchase of noncontrolling interest in Indiana Harbor facility |

(34,000 | ) | — | |||||

| Net decrease in advances from affiliate |

(412,783 | ) | (113,636 | ) | ||||

| Repayments of notes payable assumed in acquisition |

(2,315 | ) | — | |||||

| Increase (decrease) in payable to affiliate |

5,279 | 30,296 | ||||||

| Cash distributions to noncontrolling interests in cokemaking operations |

(1,186 | ) | (19,296 | ) | ||||

|

|

|

|

|

|||||

| Net cash provided by (used in) financing activities |

233,871 | (102,636 | ) | |||||

|

|

|

|

|

|||||

| Net increase in cash and cash equivalents |

70,758 | 15,528 | ||||||

| Cash and cash equivalents at beginning of period |

40,092 | 2,741 | ||||||

|

|

|

|

|

|||||

| Cash and cash equivalents at end of period |

$ | 110,850 | $ | 18,269 | ||||

|

|

|

|

|

|||||

9

SunCoke Energy, Inc.

Segment Data

(Unaudited)

| For the Three Months Ended September 30 |

For the Nine Months Ended September 30 |

|||||||||||||||

| (Dollars in thousands, except per ton data) | 2011 | 2010 | 2011 | 2010 | ||||||||||||

| Sales and other operating revenue: |

||||||||||||||||

| Jewell Coke |

$ | 71,029 | $ | 65,518 | $ | 197,176 | $ | 242,988 | ||||||||

| Jewell Coke intersegment sales |

— | 1,941 | — | 1,941 | ||||||||||||

| Other Domestic Coke |

309,970 | 255,399 | 857,250 | 736,657 | ||||||||||||

| International Coke |

9,412 | 9,598 | 29,085 | 29,113 | ||||||||||||

| Coal Mining |

12,689 | 113 | 30,213 | 439 | ||||||||||||

| Coal Mining intersegment sales |

44,450 | 32,511 | 129,456 | 98,962 | ||||||||||||

| Elimination of intersegment sales |

(44,450 | ) | (34,452 | ) | (129,456 | ) | (100,903 | ) | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

$ | 403,100 | $ | 330,628 | $ | 1,113,724 | $ | 1,009,197 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Earnings: |

||||||||||||||||

| Jewell Coke |

$ | 13,075 | $ | 27,009 | $ | 42,587 | $ | 128,552 | ||||||||

| Other Domestic Coke(1) |

22,093 | 24,458 | 33,236 | 33,309 | ||||||||||||

| International Coke |

1,670 | 555 | 3,394 | 1,095 | ||||||||||||

| Coal Mining |

5,477 | (2,664 | ) | 13,018 | (1,493 | ) | ||||||||||

| Corporate and Other: |

||||||||||||||||

| Corporate expenses |

(14,622 | ) | (3,466 | ) | (32,286 | ) | (10,371 | ) | ||||||||

| Net financing(1) |

(4,260 | ) | 4,044 | 2,750 | 10,937 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Pretax income attributable to SunCoke Energy, Inc./net parent investment |

23,433 | 49,936 | 62,699 | 162,029 | ||||||||||||

| Income tax expense |

5,073 | 12,490 | 10,093 | 41,266 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Net income attributable to SunCoke Energy, Inc./net parent investment |

$ | 18,360 | $ | 37,446 | $ | 52,606 | $ | 120,763 | ||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Coke Operating Data: |

||||||||||||||||

| Capacity Utilization(%) |

||||||||||||||||

| Jewell Coke |

98 | 99 | 98 | 99 | ||||||||||||

| Other Domestic Coke |

105 | 103 | 100 | 96 | ||||||||||||

| Total |

104 | 102 | 100 | 97 | ||||||||||||

| Coke production volumes (thousands of tons): |

||||||||||||||||

| Jewell Coke |

179 | 180 | 530 | 535 | ||||||||||||

| Other Domestic Coke |

785 | 773 | 2,217 | 2,143 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Domestic Coke |

964 | 953 | 2,747 | 2,678 | ||||||||||||

| International Coke—operated facility |

373 | 431 | 1,149 | 1,266 | ||||||||||||

| Coke sales volumes (thousands of tons): |

||||||||||||||||

| Jewell Coke |

191 | 196 | 536 | 559 | ||||||||||||

| Other Domestic Coke |

777 | 788 | 2,231 | 2,167 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

968 | 984 | 2,767 | 2,726 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Coal Operating Data(2): |

||||||||||||||||

| Coal sales volumes (thousands of tons): |

||||||||||||||||

| Internal use |

272 | 314 | 865 | 955 | ||||||||||||

| Third parties |

99 | — | 226 | — | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total |

371 | 314 | 1,091 | 955 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Coal production (thousands of tons)(3) |

340 | 270 | 1,015 | 846 | ||||||||||||

| Purchased coal (thousands of tons) |

22 | 51 | 97 | 92 | ||||||||||||

| Coal sales price per ton (excludes transportation costs)(4) |

$ | 153.81 | $ | 103.70 | $ | 146.08 | $ | 103.72 | ||||||||

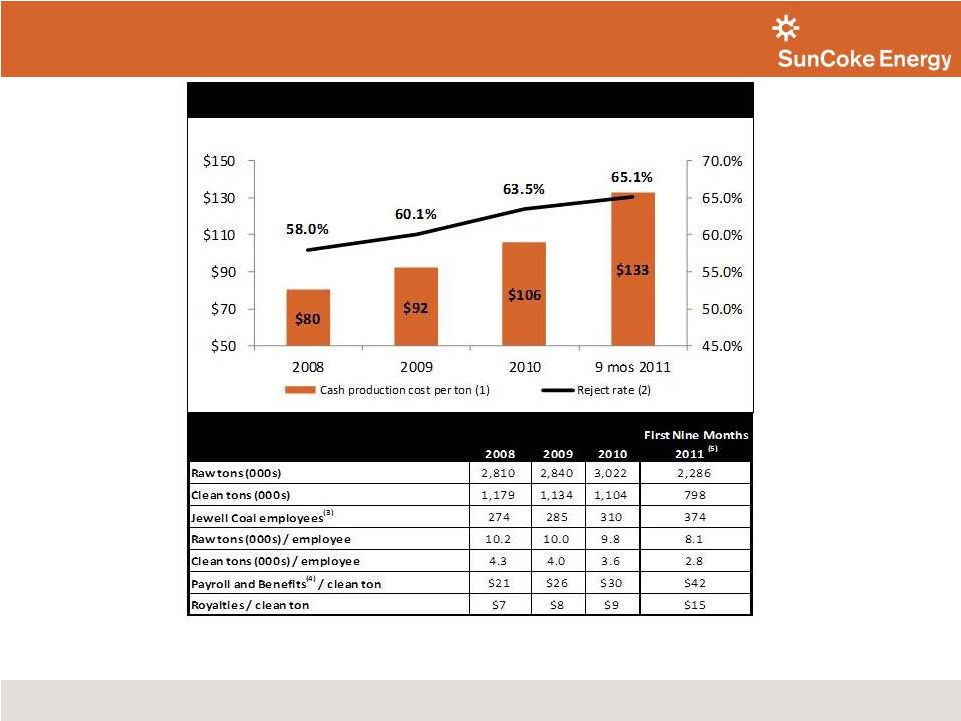

| Coal cash production cost per ton(5) |

$ | 132.08 | $ | 105.84 | $ | 124.77 | $ | 98.52 | ||||||||

| Purchased coal cost per ton(6) |

$ | 78.79 | $ | 100.75 | $ | 108.52 | $ | 76.50 | ||||||||

| Total coal production cost per ton(7) |

$ | 133.73 | $ | 111.49 | $ | 130.22 | $ | 101.96 | ||||||||

| (1) | Excludes income (loss) attributable to noncontrolling investors in our Indiana Harbor cokemaking operations. |

| (2) | Includes production from company and contractor-operated mines. |

10

| (3) | Includes HKCC coal production of 68 thousand tons and 218 thousand tons for the third quarter and first nine months of 2011, respectively. |

| (4) | Includes sales to affiliates, including sales to Jewell Coke established via a transfer pricing agreement. The transfer price per ton to Jewell Coke was $163.53 and $103.68 for the third quarter of 2011 and 2010, respectively, and $151.25 and $103.70 for the first nine months of 2011 and 2010, respectively. |

| (5) | Mining and preparation costs for tons produced, excluding $1.9 million HKCC favorable fair value adjustment for contingent consideration in the third quarter and first nine months of 2011 and depreciation, depletion and amortization, divided by coal production volume. |

| (6) | Costs of purchased raw coal divided by purchased coal volume. |

| (7) | Cost of mining and preparation costs, purchased raw coal costs, and depreciation, depletion and amortization divided by coal sales volume. Depreciation, depletion and amortization per ton were $8.96 and $6.26 for the third quarter of 2011 and 2010, respectively and $8.45 and $5.94 for the first nine months of 2011 and 2010, respectively. |

11

SunCoke Energy, Inc.

Reconciliations of Adjusted EBITDA to

Operating Income and Net Income

| Three Months Ended September 30, 2011 | ||||||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

| Jewell Coke |

Other Domestic Coke |

Internat’l Coke |

Coal Mining |

Corporate and Other |

Combined | |||||||||||||||||||

| Net Income |

$ | 21,732 | ||||||||||||||||||||||

| Add: Depreciation, depletion and amortization |

14,752 | |||||||||||||||||||||||

| Subtract: Interest income |

(1,289 | ) | ||||||||||||||||||||||

| Add: Interest cost |

342 | |||||||||||||||||||||||

| Subtract: Capitalized interest |

(4,633 | ) | ||||||||||||||||||||||

| Add: Interest expense |

8,860 | |||||||||||||||||||||||

| Add: Income tax expense |

5,073 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

$ | 14,286 | $ | 34,328 | $ | 1,727 | $ | 8,797 | $ | (14,301 | ) | $ | 44,837 | |||||||||||

| Add: Sales discounts provided to customers due to sharing of nonconventional fuel tax credits |

— | 3,348 | — | — | — | 3,348 | ||||||||||||||||||

| Add (Subtract): Net (income) loss attributable to noncontrolling interests |

— | (3,372 | ) | — | — | — | (3,372 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 14,286 | $ | 34,304 | $ | 1,727 | $ | 8,797 | $ | (14,301 | ) | $ | 44,813 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income (loss) |

$ | 13,075 | $ | 24,485 | $ | 1,670 | $ | 5,477 | $ | (14,622 | ) | $ | 30,085 | |||||||||||

| Add: Depreciation, depletion and amortization |

1,211 | 9,843 | 57 | 3,320 | 321 | 14,752 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

$ | 14,286 | $ | 34,328 | $ | 1,727 | $ | 8,797 | $ | (14,301 | ) | $ | 44,837 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Three Months Ended September 30, 2010 | ||||||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

| Jewell Coke |

Other Domestic Coke |

Internat’l Coke |

Coal Mining |

Corporate and Other |

Combined | |||||||||||||||||||

| Net Income |

$ | 40,940 | ||||||||||||||||||||||

| Add: Depreciation, depletion and amortization |

14,013 | |||||||||||||||||||||||

| Subtract: Interest income |

(6,188 | ) | ||||||||||||||||||||||

| Add: Interest cost |

1,330 | |||||||||||||||||||||||

| Subtract: Capitalized interest |

(206 | ) | ||||||||||||||||||||||

| Add: Interest expense |

— | |||||||||||||||||||||||

| Add: Income tax expense |

12,490 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

$ | 28,108 | $ | 37,646 | $ | 581 | $ | (699 | ) | $ | (3,257 | ) | $ | 62,379 | ||||||||||

| Add: Sales discounts provided to customers due to sharing of nonconventional fuel tax credits |

— | 3,305 | — | — | — | 3,305 | ||||||||||||||||||

| Add (Subtract): Net (income) loss attributable to noncontrolling interests |

— | (3,494 | ) | — | — | — | (3,494 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 28,108 | $ | 37,457 | $ | 581 | $ | (699 | ) | $ | (3,257 | ) | $ | 62,190 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income (loss) |

$ | 27,009 | $ | 26,932 | $ | 555 | $ | (2,664 | ) | $ | (3,466 | ) | $ | 48,366 | ||||||||||

| Add: Depreciation, depletion and amortization |

1,099 | 10,714 | 26 | 1,965 | 209 | 14,013 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

$ | 28,108 | $ | 37,646 | $ | 581 | $ | (699 | ) | $ | (3,257 | ) | $ | 62,379 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

12

SunCoke Energy, Inc.

Reconciliations of Adjusted EBITDA to

Operating Income and Net Income

| Three Months Ended June 30, 2011 | ||||||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

| Jewell Coke |

Other Domestic Coke |

Internat’l Coke |

Coal Mining |

Corporate and Other |

Combined | |||||||||||||||||||

| Net Income |

$ | 23,993 | ||||||||||||||||||||||

| Add: Depreciation, depletion and amortization |

14,605 | |||||||||||||||||||||||

| Subtract: Interest income (primarily from affiliates) |

(5,763 | ) | ||||||||||||||||||||||

| Add: Interest cost |

1,723 | |||||||||||||||||||||||

| Subtract: Capitalized interest |

(399 | ) | ||||||||||||||||||||||

| Add: Income tax expense |

1,881 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

$ | 12,892 | $ | 23,695 | $ | 843 | $ | 9,144 | $ | (10,534 | ) | $ | 36,040 | |||||||||||

| Add: Sales discounts provided to customers due to sharing of nonconventional fuel tax credits |

— | 3,174 | — | — | — | 3,174 | ||||||||||||||||||

| Add (Subtract): Net (income) loss attributable to noncontrolling interests |

— | (1,573 | ) | — | — | — | (1,573 | ) | ||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 12,892 | $ | 25,296 | $ | 843 | $ | 9,144 | $ | (10,534 | ) | $ | 37,641 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income (loss) |

$ | 11,559 | $ | 14,059 | $ | 788 | $ | 5,964 | $ | (10,935 | ) | $ | 21,435 | |||||||||||

| Add: Depreciation, depletion and amortization |

1,333 | 9,636 | 55 | 3,180 | 401 | 14,605 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

$ | 12,892 | $ | 23,695 | $ | 843 | $ | 9,144 | $ | (10,534 | ) | $ | 36,040 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Three Months Ended March 31, 2011 | ||||||||||||||||||||||||

| (Dollars in thousands) | ||||||||||||||||||||||||

| Jewell Coke |

Other Domestic Coke |

Internat’l Coke |

Coal Mining |

Corporate and Other |

Combined | |||||||||||||||||||

| Net Income |

$ | 5,655 | ||||||||||||||||||||||

| Add: Depreciation, depletion and amortization |

13,020 | |||||||||||||||||||||||

| Subtract: Interest income (primarily from affiliates) |

(5,717 | ) | ||||||||||||||||||||||

| Add: Interest cost |

1,500 | |||||||||||||||||||||||

| Subtract: Capitalized interest |

(312 | ) | ||||||||||||||||||||||

| Add: Income tax expense |

3,139 | |||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

$ | 19,054 | $ | (857 | ) | $ | 988 | $ | 4,296 | $ | (6,196 | ) | $ | 17,285 | ||||||||||

| Add: Sales discounts provided to customers due to sharing of nonconventional fuel tax credits |

— | 3,125 | — | — | — | 3,125 | ||||||||||||||||||

| Add (Subtract): Net (income) loss attributable to noncontrolling interests |

— | 6,171 | — | — | — | 6,171 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Adjusted EBITDA |

$ | 19,054 | $ | 8,439 | $ | 988 | $ | 4,296 | $ | (6,196 | ) | $ | 26,581 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income (loss) |

$ | 17,953 | $ | (9,472 | ) | $ | 935 | $ | 1,577 | $ | (6,728 | ) | $ | 4,265 | ||||||||||

| Add: Depreciation, depletion and amortization |

1,101 | 8,615 | 53 | 2,719 | 532 | 13,020 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| EBITDA |

$ | 19,054 | $ | (857 | ) | $ | 988 | $ | 4,296 | $ | (6,196 | ) | $ | 17,285 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

13