Table of Contents

As filed with the Securities and Exchange Commission on August 17, 2011

Registration No. 333-175353

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

AMENDMENT NO. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

TransUnion Corp.

(Exact name of registrant as specified in its charter)

| Delaware (State or other jurisdiction of incorporation or organization) |

7320 (Primary Standard Industrial Classification Code Number) |

74-3135689 (I.R.S. Employer Identification Number) |

555 West Adams Street

Chicago, Illinois 60661

Telephone: (312) 985-2000

(Address, including zip code, and telephone number, including area code, of registrants’ principal executive offices)

John W. Blenke

Executive Vice President, Corporate General Counsel and Corporate Secretary

TransUnion Corp.

555 West Adams Street

Chicago, Illinois 60661

Telephone: (312) 985-2000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| Michael A. Pucker Cathy A. Birkeland Roderick O. Branch Latham & Watkins LLP 233 South Wacker Drive, Suite 5800 Chicago, Illinois 60606 (312) 876-7700 |

Samuel A. Hamood Executive Vice President and TransUnion Corp. 555 West Adams Street Chicago, Illinois 60661 (312) 985-2000 |

Andrew J. Pitts Craig F. Arcella Cravath, Swaine & Moore LLP Worldwide Plaza 825 Eighth Avenue New York, New York 10019 (212) 474-1000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer ¨ | Accelerated Filer ¨ | Non-Accelerated Filer x | Smaller reporting company ¨ | |||

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1)(2) |

Amount of Registration Fee | ||

| Common Stock, par value $0.01 per share |

$ 325,000,000 | $ 37,732.50(3) | ||

|

| ||||

|

| ||||

| (1) | Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(0) under the Securities Act of 1933, as amended (the “Securities Act”). |

| (2) | Includes additional shares that the Underwriters have the option to purchase to cover over-allotments, if any. See “Underwriting.” |

| (3) | The registration fee has been previously paid. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We and the selling stockholders may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we and the selling stockholders are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus dated August 17, 2011

PROSPECTUS

Shares

TransUnion Corp.

Common Stock

This is TransUnion’s initial public offering. We are selling shares of our common stock.

We expect the public offering price to be between $ and $ per share. Currently, no public market exists for the shares. After pricing of the offering, we expect that the shares will trade on the New York Stock Exchange under the symbol “TRUN.”

Investing in the common stock involves risks that are described in the “Risk Factors” section beginning on page 15 of this prospectus.

| Per Share |

|

Total | ||||

| Public offering price |

$ | $ | ||||

| Underwriting discount |

$ | $ | ||||

| Proceeds, before expenses, to us |

$ | $ |

The underwriters may also exercise their option to purchase up to an additional shares from the selling stockholders at the public offering price, less the underwriting discount, for 30 days after the date of this prospectus to cover overallotments, if any. We will not receive any of the proceeds from the sale of shares sold by the selling stockholders pursuant to the underwriters’ overallotment option.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares will be ready for delivery on or about , 2011.

Joint Book-Running Managers

| BofA Merrill Lynch | J.P. Morgan | Deutsche Bank Securities |

| Credit Suisse | Morgan Stanley |

The date of this prospectus is , 2011.

Table of Contents

Table of Contents

| 1 | ||||

| 15 | ||||

| 30 | ||||

| 32 | ||||

| 32 | ||||

| 33 | ||||

| 35 | ||||

| 37 | ||||

| 38 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

40 | |||

| 65 | ||||

| 83 | ||||

| 92 | ||||

| 113 | ||||

| 116 | ||||

| 120 | ||||

| 124 | ||||

| 129 | ||||

| MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS OF OUR COMMON STOCK |

131 | |||

| 135 | ||||

| 141 | ||||

| 141 | ||||

| 141 | ||||

| F-1 |

You should rely only on the information contained in this prospectus and any free writing prospectus prepared by or on behalf of us that we have referred to you. Neither we, the selling stockholders nor the underwriters have authorized anyone to provide you with additional or different information from that contained in this prospectus or in any free writing prospectus. If anyone provides you with additional, different or inconsistent information, you should not rely on it. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information in this prospectus may only be accurate on the date of this prospectus.

Industry and Market Data

This prospectus includes industry and trade association data, forecasts and information that we have prepared based, in part, upon data, forecasts and information obtained from independent trade associations, industry publications and surveys and other information available to us. Some data is also based on our good faith estimates, which are derived from management’s knowledge of the industry and independent sources.

i

Table of Contents

This summary contains selected information contained elsewhere in this prospectus. This summary does not contain all the information you should consider in making your investment decision. You should carefully read this entire prospectus, including the information set forth under the headings “Risk Factors,” “Selected Historical Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and our financial statements and the related notes thereto appearing elsewhere in this prospectus before deciding to invest in our common stock.

Unless we indicate otherwise or the context otherwise requires, all references to “TransUnion,” the “Company,” “we,” “us” and “our” refer collectively to TransUnion Corp. and its consolidated subsidiaries. References in this prospectus to years are to our fiscal years, which end on December 31.

Overview

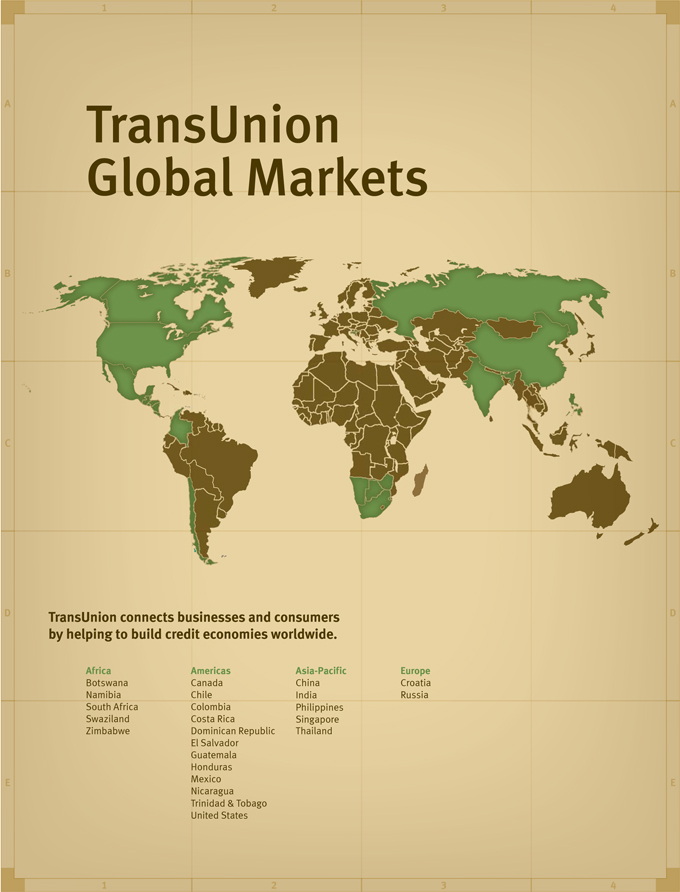

We are a leading global provider of information and risk management solutions. We provide these solutions to businesses across multiple industries and to individual consumers. Our technology and services enable businesses to make more timely and informed credit granting, risk management, underwriting, fraud protection and customer acquisition decisions by delivering high quality data, and by integrating advanced analytics and enhanced decision-making capabilities. Our interactive website provides consumers with real-time access to their personal credit information and analytical tools that help them understand and proactively manage their personal finances. Over a million unique consumers visit our website each month. We have operations in the United States, Africa, Canada, Latin America, East Asia and India and provide services in 23 countries. Since our founding in 1968, we have built a stable and highly diversified customer base of approximately 45,000 businesses in multiple industries, including financial services, insurance, healthcare, automotive, retail and communications.

High quality data is the cornerstone of our business. Businesses depend on our data for their daily risk-management processes. Consumers seek our data to help them understand their credit profile and protect themselves against identity theft. Together with our unconsolidated subsidiaries, we maintain credit files on approximately 500 million consumers and businesses worldwide. We refine and enhance the financial, credit, identity, insurance claims, bankruptcy and other data we obtain from thousands of sources and use our sophisticated matching algorithms to create proprietary databases. We combine our data with our analytics and decisioning technology to deliver additional value to our customers. Our analytics, such as predictive modeling and scoring, customer segmentation, benchmarking and forecasting, enable businesses and consumers to efficiently monitor and manage risk. Our decisioning technology, which is delivered on a software-as-a-service platform, enables businesses to interpret data and scores and apply their specific qualifying criteria to make real-time decisions at the point of interaction with their customers.

We have a diverse and stable global customer base, which includes many of the largest companies in each of the primary industries we serve. For example, in the United States, we contract with nine of the ten largest banks, all of the major credit card issuers and eight of the ten largest property and casualty insurance carriers and we provide services to thousands of healthcare providers. In addition, we provide subscription-based interactive services to a growing base of over a million consumers. Our deep industry knowledge and experience allow us to craft solutions tailored to our customers’ specific needs. We maintain long-standing relationships with the majority of our largest customers, including relationships of over ten years with each of our top ten global financial services customers. We attribute the length of our customer relationships to the critical nature of the services we provide, our consistency and reliability, and our innovative and collaborative approach to meeting our customers’ continually changing needs.

1

Table of Contents

We manage our business through three operating segments. U.S. Information Services, (“USIS”), which represented approximately 65% of our revenue for the six months ended June 30, 2011, provides consumer reports, credit scores, verification services, analytical services and decisioning technology to businesses in the United States. USIS offers these services to customers in the financial services, insurance, healthcare and other industries, and delivers them through both direct and indirect channels. International, which represented approximately 21% of our revenue for the six months ended June 30, 2011, provides services similar to our USIS and Interactive segments in several countries outside the United States. Interactive, which represented approximately 14% of our revenue for the six months ended June 30, 2011, provides services to consumers that help them understand and proactively manage their personal finances and protect them from identity theft.

We had revenues of $956.5 million for the year ended December 31, 2010, and $503.4 million for the six months ended June 30, 2011. We had net income attributable to TransUnion Corp. of $36.6 million for the year ended December 31, 2010 and a net loss attributable to TransUnion Corp. of $2.6 million for the six months ended June 30, 2011. The year-to-date 2011 net loss attributable to TransUnion Corp. was directly attributable to the loss on the early extinguishment of debt incurred in connection with the refinancing of our senior secured credit facility in the first quarter of 2011, including a write-off of unamortized deferred financing fees of $49.8 million and a prepayment premium of $9.5 million. See “Description of Certain Indebtedness—Senior Secured Credit Facility” and Note 9, “Debt,” of our unaudited consolidated financial statements appearing elsewhere in this prospectus for additional information. We had Adjusted EBITDA of $326.6 million for the year ended December 31, 2010, and $170.5 million for the six months ended June 30, 2011. See “—Summary Historical Consolidated Financial Data” for a reconciliation of Adjusted EBITDA to its most comparable GAAP measure, net income (loss) attributable to TransUnion Corp.

Market Opportunity

We believe several important trends in the global macroeconomic environment, as well as within the key industries we serve, are driving market growth for information and risk management solutions.

| • | Large and Growing Market for Data and Analytics. We believe that the business information services market is large and growing. According to the 2010 publication, “Communications Industry Forecast 2010-2014” from Veronis Suhler Stevenson, spending on business information in the United States reached $51.6 billion in 2009 and is projected to grow at a compounded annual growth rate (“CAGR”) of 7.0% from 2009 through 2014. For 2009, $11.0 billion of this amount was attributed to credit and risk information. Spending in this category of information is projected to grow at a CAGR of 6.4% from 2009 through 2014. We believe that the demand for targeted data and sophisticated analytical tools will continue to grow meaningfully as businesses seek real time access to more granular data in order to better understand their customers. |

| • | Substantial Focus on Risk Management. As a result of the recent economic downturn, new regulatory requirements and a heightened focus on reducing fraud and losses, we believe there is a growing demand for risk-based pricing and underwriting strategies as well as ongoing reviews of existing customers’ risk profiles. For example, since 2008 insurance carriers have seen double-digit percentage increases in the number of quotes requested, leading to increased underwriting and administrative costs. In addition, financial institutions are utilizing more robust account and portfolio management strategies in order to manage losses within their existing customer base. Changing regulations in the credit card industry are motivating issuers to use more advanced customer segmentation and scoring tools to match customers to appropriate products. |

| • | Growth Driven by Non-traditional Users of Consumer Data. Non-traditional users of consumer data are recognizing the value of credit information and analytical tools. Healthcare companies use these tools to manage their revenue cycle, capital markets participants use them to develop better |

2

Table of Contents

| valuations of securitized loan portfolios, and for-profit education companies use them to reduce loan defaults. In the healthcare industry, for example, increases in high-deductible health plans and the number of uninsured and under-insured consumers have increased collection risks for healthcare providers. According to a 2011 article published by the Centers for Disease Control and Prevention, entitled “Ambulatory Medical Care Utilization Estimates for 2007,” in 2007 there were 1 billion patient visits annually to physician offices, hospital outpatient and emergency departments. To manage costs associated with these visits, healthcare providers are increasingly seeking information about their patients at the time of registration through modernized healthcare technology and electronic records. We believe companies that can offer real-time, reliable data and technology will be best positioned to benefit from the increasing demand for and use of consumer data by non-traditional users. |

| • | Growth in Emerging International Markets. Economic growth in emerging markets continues to outpace the global average. According to an April 2011 World Economic Outlook Report by the International Monetary Fund, entitled “Tensions from a Two-Speed Recovery—Unemployment, Commodities and Capital Flows,” for 2012, the average GDP of emerging markets is projected to grow over 2.5 times faster than that of developed markets. As economies in emerging markets continue to develop and mature, we believe there will continue to be a rise in favorable socio-economic trends, such as an increase in the size of middle and affluent classes, and a significant increase in the use of financial services. In addition, credit penetration is relatively low in emerging markets compared to developed markets. For example, using our database of information compiled from financial institutions as a benchmark of credit activity, we estimate that less than 20% of the adult population in India is currently credit active. We expect the populations in emerging markets to become more credit active, resulting in increased demand for our services. |

| • | Increased Consumer Focus on Managing Personal Finances and Protecting Against Identity Theft. Consumers are increasingly focused on proactively managing their finances and protecting their identities. According to research published in a September 2010 article, entitled “2010 Annual Identity Protection Services Scorecard,” by Javelin Strategy and Research, a third-party industry source, the annual market for online credit monitoring and identity theft protection services is $2.4 billion. According to a press release by the Federal Trade Commission in March 2011, identity theft was the top consumer complaint received by the agency in 2010. Tighter availability of credit and stricter lending practices are prompting individual consumers to seek a better understanding of their credit profile. As a result of these factors, an increasing number of consumers are accessing their credit reports and purchasing credit monitoring services. |

Our Competitive Strengths

| • | Global Leader in Information Management Solutions. We are one of only three leading global participants in the consumer credit and information management industry. Over the past 40 years, we have established comprehensive proprietary databases and information management solutions and developed the ability to rapidly and reliably deliver high quality consumer information, creating what we believe is a sustainable competitive advantage. We have a diverse and stable global customer base, which includes many of the largest companies in each of our primary industries. We believe that our scale, global footprint, reputation and strong market positions will allow us to capitalize on business opportunities in countries and regions around the world and contribute to our long-term growth. |

| • | Innovative and Differentiated Information Solutions. We have developed innovative and differentiated service offerings to meet the evolving needs of our customers. Our industry-leading triggers platform notifies our business customers of changes to consumer profiles on a daily basis. |

3

Table of Contents

| Our decisioning technology helps businesses interpret both data and predictive model results, and applies customer-specific criteria to facilitate real-time, automated decisions at the point of consumer interaction. We develop industry studies and provide a source of market intelligence that we believe provide a more holistic perspective on macroeconomic and market trends than comparable offerings of our competitors. We believe our specialized data, analytics and decisioning services differentiate us from our competitors. |

| • | Deep and Specialized Industry Expertise. We have developed substantial expertise in a number of industries, including financial services, insurance and healthcare, and have placed industry experts in key leadership positions throughout our organization. Our thought leadership and published studies have enhanced our reputation within these industries. In addition, we have been able to apply our industry knowledge and high-quality data assets to form strategic partnerships with other leading companies in key industries to develop new solutions and revenue opportunities. We believe that our industry knowledge base, coupled with our collaborative customer approach, has made it possible for us to anticipate and address our customers’ needs and enables us to offer additional proprietary value-added services. |

| • | Strong Presence in Attractive International Markets. We currently provide services in 22 countries outside the United States in both developed and emerging markets with significant growth potential. We have a strong presence in our developed markets, where we hold a leading market position. We are also well-positioned as a first mover in several fast-growing emerging markets, such as India, a market we entered in 2003. Since 1993, we have hosted the most extensive credit database in South Africa, which positions us well for expansion into the rest of the African continent. In addition, we have become a significant credit information and analytics provider in Latin America through partnerships and acquisitions, such as our recent acquisition in Chile. We believe that our flexible approach to forming local partnerships has allowed us to establish a foothold in certain markets ahead of our major competitors. |

| • | Attractive Business Model. Data, analytics and technology are the three key components of our business model, which is characterized by diversified, predictable revenue streams, low working capital requirements and operating leverage. We own 100% of our U.S. consumer credit data base and we typically obtain information at little or no cost, which provides us with an efficient cost structure and allows us to benefit from economies of scale. Our significant investments to upgrade and improve our technology provide us with the ability to address our customers’ needs with minimal and predictable capital investment. Additionally, our ongoing Operational Excellence program, which is aimed at creating a long-term competitive and efficient cost structure, has institutionalized our cost-management practices. |

| • | Proven and Experienced Management Team. We have a seasoned senior management team with an average of 15 years of experience in a variety of industries, including the credit and information management, financial services and information technology industries. Our senior management team has a track record of strong performance and depth of expertise in the markets we serve. This team has overseen our expansion into new industries and geographies while managing ongoing cost-saving initiatives. As a result of the sustained focus of our management team, we have maintained stable operating performance despite the recent economic downturn. |

Our Growth Strategy

| • | Develop Innovative Solutions to Meet Market Challenges. We have a culture of innovation. Our industry expertise and collaborative approach allow us to prioritize investments in new data sources and development of additional services to provide integrated solutions to meet our customers’ |

4

Table of Contents

| needs. In addition, we plan to take advantage of strategic partnerships to develop innovative services that differentiate us from our competitors. As the needs of our customers evolve, we plan to continue to provide creative solutions to meet their challenges and further expand our relationships with them. |

| • | Expand Internationally. We believe international markets present a significant opportunity for growth, as these economies continue to develop and their populations become more credit active. Given our incumbent position in many fast-growing emerging markets, we are well positioned to benefit from the ongoing expansion of consumer credit in these regions. We will continue to focus on expanding into new industries in developed international markets with the introduction of new solutions and lines of business. We will continue to expand globally by forming alliances with local partners, pursuing strategic acquisitions and developing operations in new markets. |

| • | Focus on Underpenetrated and Growth Industries. We continue to focus on underpenetrated and growth industries in the United States, such as insurance and healthcare, where we believe that the use of information-based analytics and decisioning technology is low. Insurers have seen an increase in claims dollars paid, reinforcing their need to price risk appropriately. We offer a range of solutions, including new fraud detection tools and predictive scores, that help insurers price risk appropriately in the quoting and underwriting process. Similarly, we expect providers and payers in the growing healthcare market to utilize more of our data and analytics as they manage collection risks and respond to new regulations that require them to measure the quality of their care in order to be eligible for full reimbursement by the government. We expect that these industries will continue to be a source of growing revenue and profitability for us. |

| • | Expand Interactive Business. Consumers are becoming increasingly aware of the need to proactively manage their personal finances and protect their identities. We will continue to invest in consumer-driven product enhancements and utilize our data-driven customer acquisition strategy through advertising and mobile and social media. In addition to our direct-to-consumer offerings, we will continue our low capital intensive strategy of test marketing new product enhancements and configurations through strategic partners who combine our services with their own offerings. We also plan to leverage the success of our U.S. based Interactive business to offer similar services in our international markets. |

| • | Pursue Strategic Acquisitions. We will evaluate and pursue strategic acquisitions in order to accelerate growth within our existing businesses and diversify into new businesses. We are focused on opportunities to expand our geographic footprint and the breadth and depth of our services, including acquiring proprietary datasets and industry expertise, in our key industries. We may also increase our investments in foreign entities where we hold a minority interest, as we recently did in India with the purchase of an additional interest in Credit Information Bureau (India) Limited. We plan to maintain our disciplined fiscal approach to any acquisition. |

Risk Factors

Investing in our common stock involves risks. Important factors that could materially affect our business, financial condition and results of operations are disclosed under “Risk Factors” and elsewhere in this prospectus. Some of the factors that we believe could materially affect our results include:

| • | Our revenues are concentrated in the U.S. consumer credit and financial services industries. When these industries or the broader financial markets experience a downturn, demand for our services, our revenues and the collectability of receivables may be adversely affected. |

5

Table of Contents

| • | Data security and integrity are critically important to our business, and breaches of security, unauthorized disclosure of confidential information or the perception that confidential information is not secure, could result in a material loss of business, substantial legal liability, or significant harm to our reputation. |

| • | If we experience system failures or capacity constraints, the delivery of our services to our customers could be delayed or interrupted, which could harm our business and reputation and result in the loss of revenues of customers. |

| • | We could lose our access to data sources, which could prevent us from providing our services. |

| • | Our business is subject to various governmental regulations and laws, compliance with which may cause us to incur significant expenses, and if we fail to maintain satisfactory compliance with certain regulations, we could be subject to civil or criminal penalties. |

| • | We depend, in part, on strategic alliances, joint ventures and acquisitions to grow our business. If we are unable to make strategic acquisitions and develop and maintain these strategic alliances and joint ventures, our growth may be adversely affected. |

| • | We have a substantial amount of indebtedness, which could adversely affect our financial position. |

Our History

Our business was founded in 1968 as a Delaware corporation and, in 1969, we acquired the Credit Bureau of Cook County, located in Chicago, Illinois, to provide regional credit reporting services. In the early 1970s, we began expanding on a national scale by acquiring and partnering with other regional credit bureaus, and by 1988, we had collected consumer credit information covering the United States. We were acquired by Marmon Holdings, Inc. (“Marmon”) in 1981 and continued to operate within Marmon’s corporate structure until 2005, when we were spun-off to the Pritzker family business interests (the stockholders of Marmon at that time). Since the spin-off, we have operated as a stand-alone corporate group. For purposes of this prospectus, the term “Pritzker family business interests” refers to the following: (1) various lineal descendants of Nicholas J. Pritzker (deceased) and spouses and adopted children of such descendants; (2) various U.S. situs trusts for the benefit of the individuals described in clause (1) and trustees thereof; (3) various non-U.S. situs trusts for the benefit of the individuals described in clause (1) and trustees thereof; and (4) various entities owned and/or controlled, directly and/or indirectly, by the individuals and trusts described in (1), (2) and (3).

On June 15, 2010, an affiliate of Madison Dearborn Partners, LLC (“Madison Dearborn” or the “Sponsor”), on behalf of certain of its investment funds, acquired 51.0% of our outstanding common stock from Pritzker family business interests and certain employee and director stockholders of TransUnion. We refer to this transaction as the “Change in Control Transaction” and describe the transaction in more detail below. Madison Dearborn, based in Chicago, is an experienced and successful private equity investment firm that has raised over $18 billion of capital. Since its formation in 1992, the Sponsor’s investment funds have invested in approximately 120 companies. The Sponsor’s investment funds invest in businesses across a broad spectrum of industries, including basic industries, communications, consumer, financial services and healthcare. Madison Dearborn’s objective is to invest in companies with strong competitive characteristics that it believes have the potential for significant long-term equity appreciation. To achieve this objective, the Sponsor seeks to partner with outstanding management teams that have a solid understanding of their businesses as well as track records of building shareholder value.

The Change in Control Transaction

On June 15, 2010, an affiliate of Madison Dearborn, on behalf of certain of its investment funds, acquired 51.0% of our outstanding common stock from Pritzker family business interests and certain employee and director stockholders of TransUnion.

6

Table of Contents

The Change in Control Transaction consisted of the following principal components:

| • | Debt Financing—The following debt financing, the proceeds of which we used to repay certain of our outstanding debt and to fund the Interim Merger described below among other things: |

| • | borrowings of $965.0 million under a new $1,150.0 million senior secured credit facility entered into on June 15, 2010 (the terms of which were subsequently amended and restated on February 10, 2011), which consisted of $950.0 million of borrowings under a senior secured term loan and $15.0 million of borrowings under a $200.0 million senior secured revolving line of credit; |

| • | the issuance of $645.0 million aggregate principal amount of 11 3/8% Senior Notes due 2018 (the “senior notes”); and |

| • | borrowings of approximately $16.7 million on an unsecured, interest-free basis with a maturity date of December 15, 2018 (the “RFC loan”) from Pritzker family business interests. |

| • | Sale of Shares of Common Stock by Employee and Director Stockholders to Madison Dearborn—Following the debt financing described above, on June 15, 2010, an affiliate of Madison Dearborn purchased shares of TransUnion Corp. common stock from certain employee and director stockholders of TransUnion Corp. representing 2.8% of the then outstanding common stock of TransUnion Corp. |

| • | Interim Merger—Following the transactions described above, on June 15, 2010, certain outstanding shares of TransUnion Corp. common stock were converted into the right to receive cash from us and otherwise cancelled pursuant to a merger (the “Interim Merger”) of a newly-formed Delaware corporation (“MergerCo”) with and into TransUnion Corp., with TransUnion Corp. continuing as the surviving corporation. The Interim Merger was structured as follows: |

| • | immediately prior to the Interim Merger, certain stockholders of TransUnion Corp., including Pritzker family business interests, members of senior management and the affiliate of Madison Dearborn, contributed shares representing 38.2% of the outstanding common stock of TransUnion Corp. to MergerCo in exchange for shares of voting and, in the case of employee stockholders, non-voting common stock of MergerCo (the “MergerCo Contribution”). After giving effect to the MergerCo Contribution, the outstanding shares of TransUnion Corp. common stock were held by Pritzker family business interests, certain other stockholders and MergerCo; |

| • | at the effective time of the Interim Merger on June 15, 2010, |

| • | the outstanding shares of TransUnion Corp. common stock (other than shares of TransUnion common stock owned by MergerCo) were converted into the right to receive an aggregate of approximately $1.18 billion in cash from TransUnion and were otherwise cancelled pursuant to Delaware law. The shares converted into the right to receive cash in the Interim Merger represented 61.8% of the then outstanding shares of common stock of TransUnion Corp. Pritzker family business interests received approximately $1.17 billion for their shares of TransUnion common stock in the Interim Merger; |

| • | the outstanding shares of TransUnion Corp. common stock owned by MergerCo were cancelled without payment of any consideration; |

7

Table of Contents

| • | the outstanding shares of MergerCo voting common stock automatically converted into voting common stock of TransUnion Corp. (the surviving corporation); and |

| • | the outstanding shares of MergerCo non-voting common stock held by employee stockholders automatically converted into non-voting common stock of TransUnion Corp. (the surviving corporation). |

| • | Madison Dearborn Purchase—Following the transactions described above, on June 15, 2010, an affiliate of Madison Dearborn purchased certain shares of voting common stock of TransUnion Corp. from Pritzker family business interests and certain other TransUnion Corp. stockholders, immediately following which such Madison Dearborn affiliate owned 51.0% of our outstanding voting common stock (the “Madison Dearborn Purchase”). Immediately following the Madison Dearborn Purchase, the affiliate of Madison Dearborn owned 51.4% of our outstanding voting common stock and 51.0% of our total outstanding common stock; Pritzker family business interests owned 48.6% of our outstanding voting common stock and 48.15% of our total outstanding common stock; and employee stockholders owned 100% of our outstanding non-voting common stock and 0.85% of our total outstanding common stock. |

For more information about the effect of the Change in Control Transaction on our financial condition and results of operations, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 2, “Change in Control,” of our audited and unaudited consolidated financial statements appearing elsewhere in this prospectus. For more information about our debt, see “Description of Certain Indebtedness” and Note 9, “Debt,” of our unaudited consolidated financial statements and Note 13, “Debt,” of our audited consolidated financial statements appearing elsewhere in this prospectus.

Stock Repurchases from Pritzker Family Business Interests

| • | On November 25, 2008, we purchased $398.1 million of our common stock from Pritzker family business interests at a purchase price of $25.85 per share. |

| • | On December 17, 2009, we purchased $897.3 million of our common stock from Pritzker family business interests at a purchase price of $26.24 per share. |

| • | On June 15, 2010, at the effective time of the Interim Merger and as described above, shares of our outstanding common stock held by Pritzker family business interests converted into the right to receive an aggregate of approximately $1.17 billion in cash from TransUnion and were otherwise cancelled pursuant to Delaware law. |

For additional information regarding these share repurchases, see “Certain Relationships and Related Party Transactions—Stock Repurchases” and “—The Change in Control Transaction.”

Corporate Information

Our principal executive offices are located at 555 West Adams Street, Chicago, Illinois 60661. Our telephone number is (312) 985-2000. Our website address is www.transunion.com. The information on, or that may be accessed through, our website is not a part of this prospectus.

This prospectus includes our trademarks such as “TransUnion,” which are protected under applicable intellectual property laws and are the property of TransUnion Corp. or its subsidiaries. This prospectus also contains trademarks, service marks, trade names and copyrights of other companies, which are the property of their respective owners. Solely for convenience, trademarks and trade names referred to in this prospectus may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensor to these trademarks and trade names.

8

Table of Contents

THE OFFERING

| Common Stock offered by us |

shares |

| Common Stock to be outstanding immediately after this offering |

shares |

| Overallotment option |

The selling stockholders have granted the underwriters an option to purchase up to additional shares of our common stock at the initial public offering price for a period of 30 days after the date of this prospectus. |

| Common stock to be held by the Sponsor and Pritzker family business interests after this offering |

Upon completion of this offering, the Sponsor will beneficially own approximately % of our outstanding common stock (or approximately % of our outstanding common stock if the underwriters fully exercise their overallotment option) and Pritzker family business interests will beneficially own approximately % of our outstanding common stock (or approximately % of our outstanding common stock if the underwriters fully exercise their overallotment option). The Sponsor will, for the foreseeable future, have significant influence over our reporting and corporate management and affairs, and virtually all matters requiring stockholder approval. |

| Use of Proceeds |

We currently intend to use approximately $251.4 million of the net proceeds to us from this offering to redeem 35% of the aggregate principal amount of the senior notes at a redemption price equal to 111.375% of the principal amount of the senior notes to be redeemed plus accrued and unpaid interest, pursuant to the terms of the indenture governing the senior notes. As of June 30, 2011, $645.0 million of the senior notes were outstanding. The senior notes have a stated maturity of June 15, 2018 and accrue interest at a rate equal to 11 3/8% per annum. See “Description of Certain Indebtedness—Senior Notes.” We intend to use any remaining proceeds for working capital and other general corporate purposes. We will not receive any proceeds from the sale of shares by the selling stockholders pursuant to the underwriters’ overallotment option. See “Use of Proceeds.” |

| Risk Factors |

See “Risk Factors” beginning on page 15 of this prospectus for a discussion of factors you should carefully consider before deciding to invest in our common stock. |

9

Table of Contents

| Proposed symbol for trading on the New York Stock Exchange (the “NYSE”) |

“TRUN” |

The total number of shares of common stock to be outstanding immediately after this offering is based on 29,827,867 shares of our common stock outstanding as of June 30, 2011, and excludes:

| • | 3,272,658 shares of common stock issuable upon exercise of options outstanding as of June 30, 2011, at an exercise price of $24.37 per share, of which 296,866 options to purchase shares were exercisable as of that date; |

| • | 9,000 shares of common stock issuable upon exercise of options outstanding as of June 30, 2011, at an exercise price of $44.47 per share, of which no options to purchase shares were exercisable as of that date; and |

| • | 133,287 additional shares of common stock reserved for issuance under our TransUnion Corp. 2010 Management Equity Plan (as amended and restated effective February 9, 2011) (our “2010 Management Equity Plan”) (see “Compensation Discussion and Analysis”). |

Except as otherwise indicated, information in this prospectus:

| • | reflects the automatic conversion of all outstanding shares of our non-voting common stock into 306,351 shares of voting common stock immediately prior to the consummation of this offering; |

| • | assumes (1) no exercise by the underwriters of their option to purchase up to additional shares from the selling stockholders and (2) an initial public offering price of $ per share, the midpoint of the initial public offering price range indicated on the cover of this prospectus; and |

| • | assumes filing of our amended and restated certificate of incorporation and adoption of our amended and restated bylaws, which will occur at or prior to the consummation of the offering. |

10

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following tables set forth our summary historical consolidated financial data for the periods ended and as of the dates indicated below.

We have derived the summary historical consolidated financial data as of December 31, 2010 and 2009, and for each of the years in the three-year period ended December 31, 2010, from our audited consolidated financial statements appearing elsewhere in this prospectus. We have derived the summary historical consolidated financial data for the six months ended June 30, 2011, and June 30, 2010, and the summary historical consolidated balance sheet data as of June 30, 2011, from our unaudited consolidated financial statements appearing elsewhere in this prospectus. The unaudited consolidated financial statements have been prepared on the same basis as our audited consolidated financial statements, and, in our opinion, reflect all adjustments, including normal recurring adjustments, necessary to present fairly in all material respects our financial position and results of operations for the six months ended June 30, 2011. Our results of operations for the six months ended June 30, 2011, are not necessarily indicative of the results that may be expected for the full year. Additionally, our historical results are not necessarily indicative of the results expected for any future period.

The summary historical financial data set forth below is only a summary and should be read in conjunction with “Unaudited Pro Forma Consolidated Financial Data,” “Selected Historical Consolidated Financial Data,” “Risk Factors,” “Use of Proceeds,” “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our historical consolidated financial statements and related notes appearing elsewhere in this prospectus.

| Six Months Ended June 30, | Twelve Months Ended December 31, | |||||||||||||||||||

| (in millions, except per share data) |

2011 | 2010 | 2010 | 2009 | 2008 | |||||||||||||||

| (Unaudited) | ||||||||||||||||||||

| Income Statement Data: |

||||||||||||||||||||

| Revenue |

$ | 503.4 | $ | 464.3 | $ | 956.5 | $ | 924.8 | $ | 1,015.9 | ||||||||||

| Operating expenses: |

||||||||||||||||||||

| Cost of services |

212.1 | 199.2 | 395.8 | 404.2 | 432.2 | |||||||||||||||

| Selling, general and administrative |

132.5 | 138.1 | 263.0 | 234.6 | 305.5 | |||||||||||||||

| Depreciation and amortization |

43.2 | 40.3 | 81.6 | 81.6 | 85.7 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total operating expenses(1) |

387.8 | 377.6 | 740.4 | 720.4 | 823.4 | |||||||||||||||

| Operating income |

115.6 | 86.7 | 216.1 | 204.4 | 192.5 | |||||||||||||||

| Non-operating income and expense(2) |

(120.2 | ) | (61.2 | ) | (133.1 | ) | 1.3 | 17.4 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from continuing operations before income tax |

(4.6 | ) | 25.5 | 83.0 | 205.7 | 209.9 | ||||||||||||||

| Benefit (provision) for income tax |

6.6 | (23.6 | ) | (46.3 | ) | (73.4 | ) | (75.5 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from continuing operations |

2.0 | 1.9 | 36.7 | 132.3 | 134.4 | |||||||||||||||

| Discontinued operations, net of tax |

(0.5 | ) | 8.7 | 8.2 | 1.2 | (15.9 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

1.5 | 10.6 | 44.9 | 133.5 | 118.5 | |||||||||||||||

| Less: net income attributable to noncontrolling interests |

(4.1 | ) | (3.9 | ) | (8.3 | ) | (8.1 | ) | (9.2 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) attributable to TransUnion Corp. |

$ | (2.6 | ) | $ | 6.7 | $ | 36.6 | $ | 125.4 | $ | 109.3 | |||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income (loss) from continuing operations attributable to TransUnion Corp. common stockholders per share, basic |

$ | (0.07 | ) | $ | (0.03 | ) | $ | 0.55 | $ | 1.13 | $ | 1.01 | ||||||||

| Income (loss) from continuing operations attributable to TransUnion Corp. common stockholders per share, diluted |

$ | (0.07 | ) | $ | (0.03 | ) | $ | 0.55 | $ | 1.13 | $ | 1.00 | ||||||||

| Weighted average shares, basic |

29.8 | 72.8 | 51.1 | 109.5 | 124.5 | |||||||||||||||

| Weighted average shares, diluted |

29.8 | 72.8 | 51.3 | 109.8 | 125.0 | |||||||||||||||

11

Table of Contents

| Six Months Ended June 30, | Twelve Months Ended December 31, | |||||||||||||||||||

| (in millions) |

2011 | 2010 | 2010 | 2009 | 2008 | |||||||||||||||

| (Unaudited) | ||||||||||||||||||||

| Other Financial Data: |

||||||||||||||||||||

| Adjusted EBITDA(3) |

$ | 170.5 | $ | 157.7 | $ | 326.6 | $ | 299.8 | $ | 343.7 | ||||||||||

| Cash provided by operating activities of continuing operations |

57.6 | 84.6 | 204.6 | 251.8 | 230.4 | |||||||||||||||

| Capital expenditures of continuing operations(4) |

38.9 | 19.0 | 46.8 | 56.3 | 93.5 | |||||||||||||||

| As of June 30, 2011 | As of December 31, | |||||||||||||||

| (in millions) |

Actual | As Adjusted(5)(6) | 2010 | 2009 | ||||||||||||

| (Unaudited) | ||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||

| Cash and cash equivalents |

$ | 122.8 | $ | $ | 131.2 | $ | 137.5 | |||||||||

| Total assets |

934.3 | 954.2 | 1,010.0 | |||||||||||||

| Total debt |

1,605.6 | 1,606.0 | 591.3 | |||||||||||||

| Total stockholders’ equity(7) |

(862.5 | ) | (862.0 | ) | 249.4 | |||||||||||

| (1) | For the six months ended June 30, 2011, total operating expenses included a $3.6 million outsourcing vendor contract early termination fee and a $2.7 million software impairment and related restructuring charge due to a regulatory change requiring a software platform replacement. For the twelve months ended December 31, 2010, total operating expenses included $21.4 million of accelerated stock-based compensation and related expenses resulting from the Change in Control Transaction and a gain of $3.9 million on the trade in of mainframe computers. See Note 2, “Change in Control,” and Note 16, “Stock-Based Compensation,” of our audited consolidated financial statements appearing elsewhere in this prospectus for further information about the impact of the Change in Control Transaction. |

| (2) | For the six months ended June 30, 2011, non-operating income and expense included $64.3 million of interest expense and, as a result of refinancing our senior secured credit facility in February 2011, a $9.5 million prepayment premium and $49.8 million write-off of unamortized loan costs incurred in connection with financing the Change in Control Transaction in June 2010. For the twelve months ended December 31, 2010, non-operating income and expense included $90.1 million of interest expense, $28.7 million of acquisition fees and $20.5 million of loan fees, primarily related to the Change in Control Transaction. See Note 2, “Change in Control,” of our audited consolidated financial statements appearing elsewhere in this prospectus for further information about the impact of the Change in Control Transaction. See Note 9, “Debt,” of our unaudited consolidated financial statements and Note 13, “Debt,” of our audited consolidated financial statements appearing elsewhere in this prospectus for further information about interest expense and the refinancing. |

| (3) | Adjusted EBITDA is a non-GAAP measure. We present Adjusted EBITDA as a supplemental measure of our operating performance because it eliminates the impact of certain items that we do not consider indicative of our ongoing operating performance. In addition, Adjusted EBITDA does not reflect our capital expenditures, interest, income tax, depreciation, amortization or stock-based compensation. Other companies in our industry may calculate Adjusted EBITDA differently than we do, limiting its usefulness as a comparative measure. Because of these limitations, Adjusted EBITDA should not be considered in isolation or as a substitute for performance measures calculated in accordance with GAAP. |

In addition to its use as a measure of our operating performance, our board of directors and executive management team focus on Adjusted EBITDA as a compensation measure. The annual variable compensation for certain members of our management is based in part on Adjusted EBITDA.

12

Table of Contents

Adjusted EBITDA is not a measure of financial condition or profitability under GAAP and should not be considered an alternative to cash flow from operating activities, as a measure of liquidity or as an alternative to operating income or net income as an indicator of operating performance. We believe that the most directly comparable GAAP measure to Adjusted EBITDA is net income (loss) attributable to TransUnion Corp. The reconciliation of net income (loss) attributable to TransUnion Corp. to Adjusted EBITDA, is as follows:

| Six Months Ended June 30, | Twelve Months Ended December 31, | |||||||||||||||||||

| (in millions) |

2011 | 2010 | 2010 | 2009 | 2008 | |||||||||||||||

| (Unaudited) | ||||||||||||||||||||

| Net income (loss) attributable to TransUnion Corp |

$ | (2.6 | ) | $ | 6.7 | $ | 36.6 | $ | 125.4 | $ | 109.3 | |||||||||

| Discontinued operations |

0.5 | (8.7 | ) | (8.2 | ) | (1.2 | ) | 15.9 | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income (loss) from continuing operations attributable to TransUnion Corp. |

$ | (2.1 | ) | $ | (2.0 | ) | $ | 28.4 | $ | 124.2 | $ | 125.2 | ||||||||

| Net interest expense (income) |

64.0 | 15.5 | 89.1 | — | (20.6 | ) | ||||||||||||||

| Income taxes |

(6.6 | ) | 23.6 | 46.3 | 73.4 | 75.5 | ||||||||||||||

| Depreciation and amortization |

43.2 | 40.3 | 81.6 | 81.6 | 85.7 | |||||||||||||||

| Stock-based compensation |

2.4 | 8.5 | 10.8 | 16.1 | 20.1 | |||||||||||||||

| Other (income) and expense(A) |

63.3 | 50.4 | 52.9 | 4.5 | 10.5 | |||||||||||||||

| Adjustments(B) |

6.3 | 21.4 | 17.5 | — | 47.3 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Adjusted EBITDA |

$ | 170.5 | $ | 157.7 | $ | 326.6 | $ | 299.8 | $ | 343.7 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (A) | For the six months ended June 30, 2011, as a result of refinancing our senior secured credit facility in February 2011, other income and expense included a $59.3 million loss on the early extinguishment of debt as a result of refinancing our senior secured credit facility and $4.0 million of other income and expense. See Note 9, “Debt,” of our unaudited consolidated financial statements appearing elsewhere in this prospectus for further information about the refinancing. For the twelve months ended December 31, 2010, other income and expense included $28.7 million of acquisition fees and $20.5 million of loan fees, primarily related to the Change in Control Transaction, and $3.7 million of other income and expense. See Note 2, “Change in Control,” of our audited consolidated financial statements appearing elsewhere in this prospectus for further information about the impact of the Change in Control Transaction. For the twelve months ended December 31, 2008, other income and expense included a $7.7 million impairment loss on marketable securities and $2.8 million of other income and expense. Other income and expense included in the reconciliation of net income (loss) attributable to TransUnion Corp. to Adjusted EBITDA includes all amounts included in other income and expense, net, on our income statement except for earnings from equity method investments and dividends received from cost method investments. |

| (B) | For the six months ended June 30, 2011, adjustments included a $3.6 million outsourcing vendor contract early termination fee and a $2.7 million software impairment and related restructuring charge due to a regulatory change requiring a software platform replacement. For the twelve months ended December 31, 2010, adjustments included $21.4 million of accelerated stock-based compensation and related expenses resulting from the Change in Control Transaction and a gain of $3.9 million on the trade in of mainframe computers. See Note 2, “Change in Control,” and Note 16, “Stock-Based Compensation,” of our audited consolidated financial statements appearing elsewhere in this prospectus for further information about the impact of the Change in Control Transaction. For the twelve months ended December 31, 2008, adjustments comprised $47.3 million related to the settlement of the Privacy Litigation. See “Business—Legal Proceedings—Privacy Litigation.” |

13

Table of Contents

| (4) | Capital expenditures for the six months ended June 30, 2011, included $18.8 million paid in the first quarter of 2011 for assets purchased and accrued for in the fourth quarter of 2010. |

| (5) | Reflects the issuance and sale of shares of our common stock in this offering at an assumed initial public offering price of $ per share, the midpoint of the range set forth on the front cover of this prospectus, our receipt of the net proceeds from this offering, after deducting the underwriting discount and estimated offering expenses payable by us and our use of the net proceeds from this offering to reduce our outstanding indebtedness as described in this prospectus. |

| (6) | A $1.00 increase or decrease in the assumed initial public offering price of $ per share, the midpoint of the range set forth on the front cover of this prospectus, would result in an approximately $ million increase or decrease in each of cash and cash equivalents, total assets and total stockholders’ equity, assuming that the number of shares offered by us set forth on the front cover of this prospectus, remains the same, and after deducting the underwriting discount and estimated offering expenses payable by us. Each increase or decrease of 1.0 million shares in the number of shares offered by us would increase or decrease in each of cash and cash equivalents, total assets and total stockholders’ equity by approximately $ million, assuming that the assumed initial public offering price of $ per share, the midpoint of the range set forth on the front cover of this prospectus, remains the same, and after deducting the underwriting discount and estimated offering expenses payable by us. The as adjusted information discussed above is illustrative only and will change based on the actual initial public offering price and the other terms of this offering. |

| (7) | The balance of total stockholders’ equity decreased from December 31, 2009, to December 31, 2010, primarily due to the Change in Control Transaction. See Note 2, “Change in Control,” of our audited consolidated financial statements appearing elsewhere in this prospectus. |

14

Table of Contents

You should consider carefully the risks and uncertainties described below and the other information in this prospectus before deciding to invest in our common stock. The following risks and uncertainties could materially affect our business, financial condition or results of operations. As a result, the market price of our common stock could decline, and you could lose part, or all, of your investment.

Risks Related to Our Business

Our revenues are concentrated in the U.S. consumer credit and financial services industries. When these industries or the broader financial markets experience a downturn, demand for our services, our revenues and the collectability of receivables may be adversely affected.

Our largest customers depend on favorable macroeconomic conditions and are impacted by the availability of credit, the level and volatility of interest rates, inflation, employment levels, consumer confidence and housing demand. When financial markets experience volatility, illiquidity and disruption, as they did beginning in 2008, our customer base suffers. These recent market developments and the potential for increased and continuing disruptions going forward present considerable risks to our businesses and operations. Changes in the economy have resulted, and may continue to result, in fluctuations in demand, and the volumes, pricing and operating margins for our services. For example, the banking and financial market downturn that began to affect our business in 2008 caused a greater focus on expense reduction by our customers and led to a decline in their account acquisition mailings, which resulted in reduced revenues from our credit marketing programs. In addition, financial institutions tightened lending standards and granted fewer mortgage loans, student loans, automobile loans and other consumer loans. As a result, we experienced a reduction in our credit report volumes. If businesses in these industries experience economic hardship, we cannot assure you that we will be able to generate future revenue growth or collect our receivables. In addition, if consumer demand for financial services and products and the number of credit applications decrease, the demand for our services could also be materially reduced. These types of disruptions could lead to a decline in the volumes of services we provide our customers and could negatively impact our revenue and results of operations.

Data security and integrity are critically important to our business, and breaches of security, unauthorized disclosure of confidential information or the perception that confidential information is not secure, could result in a material loss of business, substantial legal liability or significant harm to our reputation.

We own a large amount of highly sensitive and confidential consumer financial and personal information. This data is often accessed through secure transmissions over public networks, including the internet. Despite our technical and contractual precautions to prevent the unauthorized access to and disclosure of our data, we cannot assure you that the networks that access our services and databases will not be compromised, whether as a result of criminal conduct, advances in computer hacking or otherwise. Several recent, highly publicized data security breaches have heightened consumer awareness of this issue. Unauthorized disclosure, loss or corruption of our data could disrupt our operations, subject us to substantial legal liability, result in a material loss of business, and significantly harm our reputation.

Due to concerns about data security and integrity, a growing number of legislative and regulatory bodies have adopted consumer notification requirements in the event that consumer information is accessed by unauthorized persons. In the United States, federal and state laws provide for over 40 disparate notification regimes, all of which we are subject to. Complying with such numerous and complex regulations in the event of unauthorized access will be expensive and difficult, and failure to comply with these regulations could subject us to regulatory scrutiny and additional liability.

If we experience system failures or capacity constraints, the delivery of our services to our customers could be delayed or interrupted, which could harm our business and reputation and result in the loss of revenues or customers.

Our ability to provide reliable service largely depends on the efficient and uninterrupted operation of our computer network, systems and data centers, some of which have been outsourced to third-party providers. In

15

Table of Contents

addition, we generate a significant amount of our revenues through channels that are dependent on links to telecommunications providers. Our systems and operations could be exposed to damage or interruption from fire, natural disasters, power loss, war, terrorist acts, telecommunication failures, computer viruses, denial of service attacks or human error. For example, in 2007, a service interruption occurring during a routine maintenance visit by one of our hardware vendors resulted in a disruption in our ability to deliver data and services for almost 24 hours. We may not have sufficient redundant operations to cover a loss or failure of our systems in a timely manner. Any significant interruption could severely harm our business and reputation and result in a loss of revenue and customers.

We could lose our access to data sources which could prevent us from providing our services.

Our services and products depend extensively upon continued access to and receipt of data from external sources, including data received from customers, strategic partners and various government and public records depositories. Our data providers could stop providing data or increase the costs for their data, for a variety of reasons, including a perception that our systems are insecure as a result of a data security breach or a desire to generate additional revenue. We could also become subject to legislative, regulatory or judicial restrictions on the collection or use of such data, in particular if such data is not collected by our providers in a way that allows us to legally use the data. In some cases, we compete with our data providers. If we lost access to this external data or if our access was restricted or became less economical, our ability to provide services could be negatively impacted, which would adversely affect our reputation, business, financial condition and results of operations. We cannot provide assurance that we will be successful in maintaining our relationships with these external data source providers or that we will be able to continue to obtain data from them on acceptable terms or at all. Furthermore, we cannot provide assurance that we will be able to obtain data from alternative sources if our current sources become unavailable.

Our business is subject to various governmental regulations and laws, compliance with which may cause us to incur significant expenses, and if we fail to maintain satisfactory compliance with certain regulations, we could be subject to civil or criminal penalties.

Our business is subject to significant international, federal, state and local laws and regulations, including but not limited to privacy and consumer data protection, financial, tax and labor regulations. See “Business—Regulatory Matters” for a description of select regulatory regimes to which we are subject. These laws and regulations are complex, change frequently and have tended to become more stringent over time. We currently incur significant expenses in our attempt to ensure compliance with these laws. In addition, in the future we may be subject to significant additional expense to remedy violations of these laws and regulations. Any failure by us to comply with applicable laws or regulations could also result in significant liability to us, including liability to private plaintiffs as a result of individual or class-action litigation, or may result in the cessation of our operations or portions of our operations or impositions of fines and restrictions on our ability to carry on or expand our operations. In addition, because many of our services are sold into regulated industries, we must comply with additional regulations in marketing our services into these industries, including, but not limited to, state insurance laws and regulations and the Health Insurance Portability and Accountability Act of 1996.

Certain of the laws and regulations governing our business are opaque and subject to interpretation by judges, juries and administrative bodies, creating substantial uncertainty for our business. In the past, we have incurred liability as a result of selling target marketing lists, a practice that was found by the Federal Trade Commission (the “FTC”) to be unlawful under the Fair Credit Reporting Act, despite a lack of statutory or regulatory guidance. We paid $75 million into a class-action settlement fund in connection with the Privacy Litigation as a result of this finding. See “Business—Legal Proceedings—Privacy Litigation.” We cannot predict what effect the interpretation of existing or new laws or regulations may have on our business.

16

Table of Contents

The Dodd-Frank Act authorizes the newly created Bureau of Consumer Financial Protection (the “CFPB”) to adopt rules that could potentially have a substantial impact on our and our customers’ businesses and it also empowers the CFPB and state officials to bring enforcement actions against companies that violate federal consumer financial laws.

In 2010, the United States Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”). Title X of the Dodd-Frank Act establishes the Bureau of Consumer Financial Protection and significant portions of the Dodd-Frank Act related to the CFPB became effective on July 21, 2011. The CFPB has broad powers to promulgate, administer and enforce consumer financial regulations, including those applicable to us and our customers. Final regulations could place significant restrictions on our business and the businesses of our customers, particularly customers in the lending industry, and could increase the costs of or make the continuance of all or a portion of our current business impractical or unprofitable. Compliance with the Dodd-Frank Act, CFPB regulations, or other new laws, regulations or interpretations could result in substantial compliance costs or otherwise adversely impact our business, financial condition and our results of operations.

In addition to the Dodd-Frank Act’s grant of regulatory and supervisory powers to the CFPB, the Dodd-Frank Act gives the CFPB authority to conduct examinations and pursue administrative proceedings or litigation for violations of federal consumer financial laws, including the CFPB’s own rules. In these proceedings, the CFPB can obtain cease and desist orders, which can include orders for restitution or rescission of contracts, as well as other kinds of affirmative relief, and monetary penalties ranging from $5,000 per day for ordinary violations of federal consumer financial laws to $25,000 per day for reckless violations and $1 million per day for knowing violations. Also, where a company has violated Title X of the Dodd-Frank Act or CFPB regulations under Title X, the Dodd-Frank Act empowers state attorneys general and state regulators to bring civil actions for the kind of cease and desist orders available to the CFPB (but not for civil penalties). Potentially, if the CFPB or one or more state officials believe we have violated the foregoing laws, they could exercise their enforcement powers in ways that would have a material adverse effect on us.

Changes in legislation or regulations governing consumer privacy may affect our ability to collect, manage and use personal information.

There has been an increasing public concern about the use of personal information, particularly Social Security numbers, dates of birth, financial information, medical information and department of motor vehicle data. As a result, there may be legislative or regulatory efforts to further restrict the use of this personal information. In addition, we provide credit reports and scores to consumers for a fee, and this income stream may be reduced or interrupted by legislation. For example, in 2003, the United States Congress passed a law requiring us to provide consumers with one credit report per year free of charge. Recently, legislation was introduced requiring us to provide credit scores to consumers without charge. Changes in applicable legislation or regulations that restrict our ability to collect and disseminate information, or that require us to provide services to customers or a segment of customers without charge, could result in decreased demand for our services, increase our compliance costs, restrict or eliminate our access to consumer data and adversely affect our business, financial position and results of operations.

The outcome of litigation or regulatory proceedings in which we are involved, or in which we may become involved, could subject us to significant monetary damages or restrictions on our ability to do business.

Legal proceedings arise frequently as part of the normal course of our business. These include individual consumer cases, class action lawsuits and actions brought by federal or state regulators. The outcome of these proceedings is difficult to assess or quantify. Plaintiffs in these lawsuits may seek recovery of large amounts and the cost to defend this litigation may be significant. There may also be adverse publicity associated with litigation that could decrease customer acceptance of our services. In addition, a court-ordered injunction or an administrative cease-and-desist order may require us to modify our business practices or may prohibit conduct that would otherwise be legal and in which our competitors may engage. Many of the technical and complex statutes to which we are subject, including state and federal credit reporting, medical privacy, and financial

17

Table of Contents

privacy requirements, may provide for civil and criminal penalties and may permit consumers to maintain individual or class actions against us and obtain statutorily prescribed damages. While we do not believe that the outcome of any pending or threatened litigation or regulatory enforcement action will have a material adverse effect on our financial position, litigation is inherently uncertain and adverse outcomes could result in significant monetary damages, penalties or injunctive relief against us. For example, in 2008, pursuant to the terms of a settlement agreement with respect to certain class action proceedings, which we refer to as the Privacy Litigation (as defined in “Business—Legal Proceedings”), we paid $75.0 million into a fund for the benefit of class members and provided approximately 600,000 individuals with up to 9 months of free credit monitoring services. Moreover, in 2009, pursuant to a settlement agreement we agreed with the other two defendants in a class action proceeding, which we refer to as the Bankruptcy Tradeline Litigation (as defined in “Business—Legal Proceedings”), to deposit $17.0 million, our share of the $51.0 million total settlement, into a settlement fund for the benefit of class members. Final approval of this monetary settlement by the Court occurred on July 15, 2011. Certain objectors to this monetary settlement have appealed the decision of the Court. Our insurance coverage may be insufficient to cover adverse judgments against us. See “Business—Legal Proceedings” for further information regarding the Privacy Litigation, the Bankruptcy Tradeline Litigation and other material pending litigation.

We depend, in part, on strategic alliances, joint ventures and acquisitions to grow our business. If we are unable to make strategic acquisitions and develop and maintain these strategic alliances and joint ventures, our growth may be adversely affected.

An important focus of our business is to identify business partners who can enhance our services and enable us to develop solutions that differentiate us from our competitors. We have entered into several alliance agreements or license agreements with respect to certain of our data sets and services and may enter into similar agreements in the future. These arrangements may require us to restrict our use of certain of our technologies among certain customer industries, or to grant licenses on terms that ultimately may prove to be unfavorable to us, either of which could reduce the value of our common stock. Relationships with our alliance agreement partners may include risks due to incomplete information regarding the marketplace and commercial strategies of our partners, and our alliance agreements or other licensing agreements may be the subject of contractual disputes. If we or our alliance agreements’ partners are not successful in commercializing the alliance agreements’ services, such commercial failure could adversely affect our business.

In addition, a significant strategy for our international expansion is to establish operations through strategic alliances or joint ventures with local financial institutions and other partners. We cannot provide assurance that these arrangements will be successful or that our relationships with our partners will continue to be mutually beneficial. If these relationships cannot be established or maintained it could negatively impact our business, financial condition and results of operations. Moreover, our ownership in and control of our foreign investments may be limited by local law.

We also selectively evaluate and consider acquisitions as a means of expanding our business and entering into new markets. We may not be able to acquire businesses we target due to a variety of factors such as competition from companies that are better positioned to make the acquisition. Our inability to make such strategic acquisitions could restrict our ability to expand our business and enter into new markets which would limit our ability to generate future revenue growth.

When we engage in acquisitions, investments in new businesses or divestitures of existing businesses, we will face risks that may adversely affect our business.