Table of Contents

As filed with the Securities and Exchange Commission on August 10, 2011

Registration No. 333-172411

UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

Form S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Home Loan Servicing Solutions, Ltd.

(Exact Name of Registrant As Specified in Its Charter)

| Cayman Islands | 6162 | 98-0683664 | ||

| (State or Other Jurisdiction of Incorporation or Organization) |

(Primary Standard Industrial Classification Code Number) |

(I.R.S. Employer Identification Number) |

Home Loan Servicing Solutions, Ltd.

c/o Walkers Corporate Services Limited

Walker House, 87 Mary Street

George Town, Grand Cayman KY1-9005

Cayman Islands

Telephone: +(345) 945-3727

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

C T Corporation System

111 Eighth Avenue

New York, New York 10011

(212) 894-8940

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

William C. Erbey

Home Loan Servicing Solutions, Ltd.

2002 Summit Boulevard, Sixth Floor

Atlanta, Georgia 30319

Telephone: (561) 682-7721

| Philip J. Niehoff Jon Van Gorp Mayer Brown LLP 71 S. Wacker Drive Chicago, Illinois 60606 Telephone: (312) 782-0600 |

Russell J. Pinilis Kramer Levin Naftalis & Frankel LLP 1177

Avenue of the Americas |

Danielle Carbone Shearman & Sterling LLP 599 Lexington Avenue New York, New York 10022 Telephone: (212) 848-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller reporting company ¨ |

| (Do not check if a smaller reporting company) | ||

CALCULATION OF REGISTRATION FEE

|

| ||||

| Title of Each Class of Securities to be Registered |

Proposed Maximum Aggregate Offering Price(1) |

Amount of Registration Fee(2)(3) | ||

| Ordinary shares, par value $0.01 per share |

$316,250,000 | $36,717 | ||

|

| ||||

| (1) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Calculated pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (3) | Previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

| SUBJECT TO COMPLETION, DATED AUGUST 10, 2011 |

PROSPECTUS

18,333,333 Ordinary Shares

We are offering ordinary shares. This is Home Loan Servicing Solutions, Ltd.’s initial public offering and no public market currently exists for our ordinary shares. Simultaneously with this offering, William C. Erbey, the founder of our company and the Chairman of our Board of Directors, will purchase $10 million of our ordinary shares at a price per share equal to the initial public offering price in a private placement. We currently expect the initial public offering price of our ordinary shares to be $15.00 per share.

We have applied to list our ordinary shares on The NASDAQ Global Market under the symbol “HLSS.”

Investing in our ordinary shares involves risks that are described under “Risk Factors” beginning on page 14.

| Per Share | Total | |||

| Initial price to public |

$ | $ | ||

| Underwriting discounts and commissions |

$ | $ | ||

| Proceeds, before expenses, to us |

$ | $ |

We have granted the underwriters an option for a period of 30 days from the date of this prospectus to purchase up to an additional 2,750,000 ordinary shares from us, at the initial public offering price, less the underwriting discount, to cover over-allotments, if any. If the underwriters exercise the option in full, the total underwriting discounts and commissions payable by us will be $ and the total proceeds to us, before expenses, will be $ .

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the ordinary shares to purchasers on or about , 2011.

| Wells Fargo Securities | Barclays Capital | |

Prospectus dated , 2011.

Table of Contents

| Page | ||||

| 1 | ||||

| 14 | ||||

| 37 | ||||

| 39 | ||||

| 40 | ||||

| 41 | ||||

| 42 | ||||

| 43 | ||||

| 44 | ||||

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

49 | |||

| 73 | ||||

| 97 | ||||

| 103 | ||||

| 108 | ||||

| 109 | ||||

| 113 | ||||

| 120 | ||||

| MATERIAL CAYMAN ISLANDS AND UNITED STATES FEDERAL INCOME TAX CONSIDERATIONS |

121 | |||

| 126 | ||||

| 127 | ||||

| 131 | ||||

| 131 | ||||

| 131 | ||||

| F-1 | ||||

We are responsible for the information contained in this prospectus and in any related free writing prospectus we prepare or authorize. Neither we nor the underwriters and their affiliates have authorized anyone to give you any other information. We do not, and the underwriters and their affiliates do not, take any responsibility for, and can provide no assurance as to the reliability of, any information that others may give you. We are offering to sell, and seeking offers to buy, our ordinary shares only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date on the front cover of this prospectus, or other earlier date stated in this prospectus, regardless of the time of delivery of this prospectus or of any sale of our ordinary shares.

For investors outside of the United States: neither we nor any of the underwriters has done anything that would permit this offering outside the United States or to permit the possession or distribution of this prospectus outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of our ordinary shares and the distribution of this prospectus outside of the United States.

Table of Contents

This summary highlights information contained elsewhere in this prospectus and does not contain all of the information that you should consider in making your investment decision. Before investing in our ordinary shares, you should carefully read this entire prospectus, including our consolidated financial statements and the related notes included elsewhere in this prospectus. You should also consider, among other things, the matters described under “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “The Proposed Business” appearing elsewhere in this prospectus. Unless otherwise stated, all references to “us,” “our,” “we,” the “Company” and similar designations refer to Home Loan Servicing Solutions, Ltd. and its consolidated subsidiaries.

Our Company

We are a newly incorporated Cayman Islands exempted company formed to acquire mortgage servicing assets consisting of mortgage servicing rights, rights to fees and other income from servicing mortgage loans, and associated servicing advances. We will not originate or purchase mortgage loans, and as a result we will not be subject to the risk of loss related to the origination or ownership of mortgage loans. We will engage one or more high quality residential mortgage loan servicers to service the mortgage loans underlying our mortgage servicing assets and therefore do not intend to develop our own mortgage servicing platform. We believe that our revenue and expense structure will be predictable and generate a stable income stream and that the quality of our assets will be strong. We believe this combination will accomplish our primary objective of delivering attractive and consistent risk-adjusted returns to our shareholders. We intend to distribute at least 90% of our net income to our shareholders in the form of a monthly cash dividend. In addition, unlike many income-oriented investment alternatives, we believe that our income stream and the valuation of our assets are not substantially correlated to movements in interest rates.

We have assembled an executive management team with extensive experience in the mortgage servicing industry. Our executive officers are currently in senior management roles at Ocwen Financial Corporation or “Ocwen.” Upon the completion of this offering, they will resign from their positions at Ocwen and become members of our executive management team. We believe our executive management team’s extensive experience will provide us with the ability to assess the vital characteristics of the mortgage loans underlying the mortgage servicing assets we may seek to acquire and evaluate the quality of potential mortgage servicers. We believe this experience will further enable us to accurately value mortgage servicing assets and better forecast future asset performance and servicing cash flows. In addition, we believe our management team has demonstrated historical success in arranging cost-effective servicing advance financing through a variety of economic cycles.

William C. Erbey, the founder of our company and the Chairman of our Board of Directors and the Chairman of the Board of Directors of Ocwen, has agreed to purchase $10 million of our ordinary shares at a price per share equal to the initial public offering price in a private placement that will close concurrently with this offering, which we refer to as the “Concurrent Private Placement” and together with this offering, the “Offerings.”

Our business strategy is focused on acquiring mortgage servicing rights. In many cases, however, the transfer of legal ownership of mortgage servicing rights requires the prior approval or consent of various third parties, including rating agencies. If the seller from which we have agreed to purchase mortgage servicing rights has not obtained the necessary approvals and consents to transfer legal ownership of the mortgage servicing rights to us, we will instead seek to acquire the rights to receive the servicing fees that the current servicer is entitled to receive. We refer to these rights, along with the right to acquire legal ownership of the related mortgage servicing rights automatically upon obtaining the necessary approvals and consents to transfer the mortgage servicing rights, as “Rights to MSRs.” Upon receipt of the necessary

1

Table of Contents

third party approvals and consents, the seller would be obligated to transfer legal ownership of the mortgage servicing rights to us without any additional payment. Whether we acquire mortgage servicing rights or Rights to MSRs, we would also acquire servicing advances and other associated assets. We do not believe that our business strategy or financial performance will be materially affected by whether we directly own mortgage servicing rights or the related Rights to MSRs.

We will use the proceeds from the Offerings to purchase the right to receive servicing fees and other servicing revenue, associated servicing advances and other related assets from Ocwen Loan Servicing, LLC or “Ocwen Loan Servicing,” a wholly owned subsidiary of Ocwen, simultaneously with the closing of the Offerings. These Rights to MSRs are related to mortgage servicing rights owned by Ocwen Loan Servicing with respect to 116 pooling and servicing agreements with an unpaid principal balance of approximately $17.0 billion as of June 30, 2011, which we refer to as the “Initial Mortgage Servicing Rights.” Ocwen Loan Servicing will not have obtained the necessary third party approvals and consents to transfer legal ownership of the Initial Mortgage Servicing Rights to us prior to the closing of the Offerings, and as result, the transfer of legal ownership of the Initial Mortgage Servicing Rights will occur automatically only if and when such approvals and consents are received.

Throughout this prospectus, when we refer to our “Mortgage Servicing Assets,” we are referring to the Rights to MSRs that we own and the mortgage servicing rights that we may acquire in the future, and when we refer to “Purchased Assets,” we are referring to the Mortgage Servicing Assets, together with the associated servicing advances and any other assets related to such Mortgage Servicing Assets that we have acquired. We refer to the acquisition of the Initial Purchased Assets described in more detail below as the “Initial Acquisition.” The agreements relating to the Initial Acquisition, including the Purchase Agreement and the Subservicing Agreement described in more detail below, have not yet been finalized. See “The Acquisition of the Initial Purchased Assets” below for a description of the Purchased Assets that we intend to acquire in connection with the Initial Acquisition.

We do not intend to develop our own mortgage servicing platform but instead will rely on high quality third-party residential mortgage loan servicers. Ocwen Loan Servicing is a leader in the residential subprime and Alt-A mortgage servicing industry based on its historical servicing performance through a variety of real estate and economic cycles. Prior to the transfer of legal ownership of the Initial Mortgage Servicing Rights to us, Ocwen Loan Servicing will remain obligated to service the underlying mortgage loans and will remit to us the servicing fees and other servicing revenue (excluding any ancillary income that Ocwen Loan Servicing will retain) it recognizes in each month related to the Initial Mortgage Servicing Rights. Following the transfer of legal ownership of any Initial Mortgage Servicing Rights to us, we will engage Ocwen Loan Servicing as subservicer to service the underlying mortgage loans on our behalf, and we will receive the servicing fees and other servicing revenue (excluding any ancillary income) directly. As compensation for its servicing and subservicing activities, Ocwen Loan Servicing will receive from us a monthly base fee initially equal to 12% of such recognized servicing fee revenue. Ocwen Loan Servicing will also have the opportunity to earn a monthly performance based incentive fee that will fluctuate based on collections and servicing advance reduction criteria with respect to the underlying mortgage loans. We believe this arrangement will align the interests of both companies. The method used to calculate the fees that we will pay to Ocwen Loan Servicing under the Purchase Agreement with respect to the Rights to MSRs will be the same as the method used to calculate the fees that we will pay to Ocwen Loan Servicing under the Subservicing Agreement with respect to any Initial Mortgage Servicing Rights that we have acquired.

We anticipate future growth through subsequent acquisitions of Mortgage Servicing Assets. As part of our strategy to acquire additional Mortgage Servicing Assets, we intend to purchase substantially all of the remaining mortgage servicing rights currently owned by Ocwen Loan Servicing or, to the extent that Ocwen Loan Servicing has not received the necessary third party approvals and consents prior to the closing of any subsequent acquisitions of mortgage servicing rights, the related Rights to MSRs. As of June 30, 2011, this related to approximately $25.7 billion of unpaid principal balance of subprime and Alt-A

2

Table of Contents

mortgage loans, which is expected to increase upon the consummation of Ocwen’s proposed acquisition of Litton Loan Servicing LP and its mortgage servicing rights (the “Litton Acquisition”). We have not entered into any agreement to acquire these assets, and our ability to do so will depend on a number of factors, including access to adequate financing. In addition, we believe that competitive and regulatory dynamics in the mortgage servicing industry will present us with opportunities to acquire Mortgage Servicing Assets from banks, other financial institutions and independent mortgage servicers. We believe that our business model and capital structure will enable us to competitively bid for these Mortgage Servicing Assets, particularly as we develop a longer operating history. Although we do not expect to maintain excess cash for potential future acquisitions of Mortgage Servicing Assets, any excess cash flow generated from the amortization of our Mortgage Servicing Assets and the reduction in outstanding servicing advances may be used to acquire additional Mortgage Servicing Assets. We intend to primarily fund any future acquisition of Mortgage Servicing Assets and associated servicing advances with the proceeds of issuances of additional ordinary shares and additional advance financing facilities or other financing arrangements.

We were incorporated as an exempted company in the Cayman Islands, which currently does not levy income taxes on individuals or companies. We expect to be treated as a passive foreign investment company (“PFIC”) under U.S. federal income tax laws and intend to distribute at least 90% of our net income to our shareholders in the form of a monthly dividend that will primarily be based on projected annual earnings, although we are not required by law to do so. Payment of a monthly dividend is not a condition of our tax status, and our decision to pay this dividend is not expected to be impacted by any changes in our status for U.S. tax purposes. Except for our subsidiary that is taxed as a corporation for U.S. federal income tax purposes, we do not expect to be treated as engaged in a trade or business in the United States and thus do not expect to be subject to more than a nominal amount of U.S. federal income taxation.

On , 2011, our Board of Directors declared a contingent interim dividend of $ per ordinary share for each of the three months ended , and , which will be payable, subject to the stated contingencies and all applicable laws, on , and , respectively. These dividends will be contingent upon the consummation of the Offerings and the successful completion of the Initial Acquisition as described below under “The Acquisition of the Initial Purchased Assets.” Our Board of Directors has the right to rescind these dividends at any time prior to the applicable dividend payment date. See “Dividend Policy,” “Description of Share Capital” and “Material Cayman Islands and United States Federal Income Tax Considerations.”

The Acquisition of the Initial Purchased Assets

The Mortgage Servicing Assets that we will purchase in connection with the Initial Acquisition are a portion of the assets acquired by Ocwen Loan Servicing when it acquired the U.S. subprime mortgage servicing business known as “HomEq Servicing” on September 1, 2010. The business acquired by Ocwen Loan Servicing included the mortgage servicing rights and associated servicing advances of HomEq Servicing, as well as the servicing platform based in Sacramento, California and Raleigh, North Carolina. The sellers were Barclays Bank PLC and Barclays Capital Real Estate Inc. (collectively, “Barclays”). The unpaid principal balance of the subprime and Alt-A mortgage loans underlying the Initial Mortgage Servicing Rights is approximately $17.0 billion and the amount of associated servicing advances outstanding is approximately $604 million, in each case as of June 30, 2011.

Pursuant to a master servicing rights purchase agreement with Ocwen Loan Servicing that we refer to as the “Purchase Agreement,” we will use the proceeds from the Offerings to purchase the following:

| • | the contractual right to receive the servicing fees (excluding any ancillary income) related to the Initial Mortgage Servicing Rights; |

| • | the contractual right to receive any investment earnings on the custodial accounts related to the Initial Mortgage Servicing Rights that Ocwen Loan Servicing receives pursuant to the related |

3

Table of Contents

| pooling and servicing agreements, which are the agreements that govern the packaging of mortgage loans into a pool, the servicing of such mortgage loans and the terms of the mortgage-backed securities issued by the securitization trust; |

| • | the right to automatically obtain legal ownership, without any additional payment to Ocwen Loan Servicing, of each Initial Mortgage Servicing Right upon the receipt of the necessary third party approvals and consents (this right, together with rights described in the bullet points above, constitute the “Rights to MSRs” with respect to the Initial Mortgage Servicing Rights); |

| • | the outstanding servicing advances associated with the related pooling and servicing agreements; and |

| • | other assets related to the foregoing (collectively, the foregoing represent the “Initial Purchased Assets”). |

We will also assume a related match funded servicing advance financing facility from Ocwen Loan Servicing.

The estimated purchase price for the Initial Purchased Assets is $ million (including $ million of assumed match funded liabilities), subject to certain closing adjustments. We intend to obtain a third-party opinion relating to the fairness, from a financial point of view, of the purchase price to us.

Ocwen Loan Servicing will retain legal ownership of each Initial Mortgage Servicing Right until such time as the approvals and consents necessary to transfer legal ownership of such Initial Mortgage Servicing Rights to us are obtained. The approvals, consents and other documentation from third parties necessary to transfer legal ownership of the Initial Mortgage Servicing Rights to us include:

| • | statements from the rating agencies that rated the related securitization transactions (which include Moody’s Investors Service, Standard & Poor’s Ratings Service and Fitch Ratings Service) that the transfer of legal ownership of the Initial Mortgage Servicing Rights to us will not cause a downgrade of the related mortgage-backed securities; |

| • | the consent of parties to the related pooling and servicing agreements, which may include the trustees of the related securitization trusts, the sponsors of the securitization transactions, any master servicer for the securitization transactions or any bond insurers or other credit enhancers insuring the mortgage-backed securities issued by the securitization trusts; and |

| • | any amendments to the related pooling and servicing agreements required to effectuate the transfer and sale of the related Initial Mortgage Servicing Rights to us. |

We refer to these requirements collectively as the “Required Third Party Consents” throughout this prospectus. The actual Required Third Party Consents for individual pooling and servicing agreements will vary. At this time, some but not all of the rating agencies have indicated that they would issue a statement that the transfer of legal ownership of the Initial Mortgage Servicing Rights to us would not result in a downgrade of the related mortgage-backed securities. One of the rating agencies from whom a rating confirmation is required prior to the transfer of legal ownership of the mortgage servicing rights to us has indicated that it would not provide such confirmation primarily because we are a newly formed entity with no demonstrated operating history as a mortgage servicer. After our acquisition of the Rights to MSRs pursuant to the Initial Acquisition, we and Ocwen Loan Servicing will continue to pursue the Required Third Party Consents. We will automatically obtain legal ownership of the Initial Mortgage Servicing Rights without any additional payment to Ocwen Loan Servicing if and when we obtain the Required Third Party Consents.

4

Table of Contents

So long as the Required Third Party Consents have not been obtained with respect to any Initial Mortgage Servicing Right:

| • | Ocwen Loan Servicing will remain obligated to perform its obligations as servicer under the related pooling and servicing agreement as long as any servicing advances made by Ocwen Loan Servicing are made in accordance with its advance and stop advance policies; |

| • | we will be contractually required to purchase any servicing advances that Ocwen Loan Servicing is required to make pursuant to such pooling and servicing agreement; and |

| • | Ocwen Loan Servicing will be prohibited from taking actions inconsistent with our right to acquire legal ownership of the related mortgage servicing right upon receipt of the Required Third Party Consents. |

If and when we obtain the Required Third Party Consents and become the legal owner of any Initial Mortgage Servicing Right:

| • | we will be contractually obligated to service the mortgage loans underlying such Initial Mortgage Servicing Right in accordance with the related pooling and servicing agreement; and |

| • | we will engage Ocwen Loan Servicing pursuant to the Subservicing Agreement to perform substantially all of the servicing functions it currently performs relating to such Initial Mortgage Servicing Right on our behalf, other than maintaining custodial accounts, remitting amounts from the custodial accounts and funding servicing advances pursuant to the terms of the related pooling and servicing agreement, which are functions for which we will be responsible. |

We cannot be certain of how long it will take to obtain the Required Third Party Consents or if we will be able to obtain them at all. We do not believe, however, that our business strategy or financial performance will be materially affected by whether we own the Initial Mortgage Servicing Rights or the related Rights to MSRs.

The Market Opportunity

We believe that the current dynamics of the subprime and Alt-A mortgage servicing market have created a unique opportunity where the supply of mortgage servicing rights potentially for sale outweighs the number of potential buyers. These dynamics include:

| • | higher borrower delinquencies and defaults experienced over the last few years and increased regulatory oversight has led to substantially higher costs for mortgage servicers and negatively impacted their profitability; |

| • | regulatory changes resulting from the implementation of Basel III, which will impose increased regulatory capital costs on depository institutions for owning mortgage servicing rights; and |

| • | our belief that subprime and Alt-A mortgage servicing has become less attractive to many mortgage servicers due to increasingly negative publicity and heightened government and regulatory scrutiny. |

We believe that our business model will allow us to be highly competitive in the acquisition of Mortgage Servicing Assets due to our cost structure, ability to access advance financing and our relationship with Ocwen Loan Servicing. We believe that if and when we obtain the Required Third Party Consents for the Initial Mortgage Servicing Rights, it will be easier for us to obtain any consents required for future acquisitions of mortgage servicing rights. We anticipate that most of our acquisitions of Mortgage Servicing Assets from sellers other than Ocwen Loan Servicing would involve engaging a party other than such seller to service the underlying mortgage loans. In addition, we may also pursue

5

Table of Contents

opportunities to purchase mortgage servicing rights relating to loans guaranteed or securitized by the U.S. government or government sponsored entities such as Fannie Mae and Freddie Mac (collectively, the “GSEs”).

Competitive Strengths

We believe we are well positioned to execute our business strategy based on the following competitive strengths:

Experienced Management Team with Extensive Knowledge of the Mortgage Servicing Industry. We have assembled an executive management team with extensive experience in the mortgage servicing industry. This experience includes evaluating and acquiring mortgage servicing rights, performing asset valuation analysis and financing mortgage servicing businesses through a variety of economic cycles. Key members of our executive management team also have experience in managing a public company in the mortgage servicing industry.

Asset Acquisition and Evaluation Expertise. We believe that our asset acquisition evaluation process, which includes using proprietary historical data to project the performance of mortgage loans, and our executive management team’s experience and judgment in identifying, assessing, valuing and acquiring new Mortgage Servicing Assets will enable us to accurately price assets.

Access to Mortgage Servicing Assets. Members of our executive management team have extensive relationships in the mortgage servicing industry, including relationships with mortgage loan originators and potential sellers of mortgage servicing rights. In addition, we intend to acquire substantially all of Ocwen Loan Servicing’s remaining mortgage servicing rights relating to subprime and Alt-A mortgage loans which had an unpaid principal balance of approximately $25.7 billion as of June 30, 2011, which is expected to increase upon the consummation of the proposed Litton Acquisition by Ocwen. Future acquisitions of Ocwen Loan Servicing’s remaining mortgage servicing rights will depend on various factors, including our ability to access financing and obtain the required third party approvals and consents, and may not take place.

Relationship with Ocwen. We intend to capitalize on the servicing capabilities of Ocwen Loan Servicing, which we view as superior relative to other servicers in terms of cost, management experience, technology infrastructure and platform scalability. Ocwen Loan Servicing will continue to service the mortgage loans underlying the Initial Mortgage Servicing Rights during the period of time prior to the transfer of legal ownership of the Initial Mortgage Servicing Rights to us. Thereafter, we will engage Ocwen Loan Servicing to service on our behalf the mortgage loans underlying any additional mortgage servicing rights that we may acquire from them in the future, provided that the performance criteria specified in the Subservicing Agreement are met. We may also engage Ocwen Loan Servicing to service mortgage loans underlying any mortgage servicing rights that we acquire from other third parties in the future.

6

Table of Contents

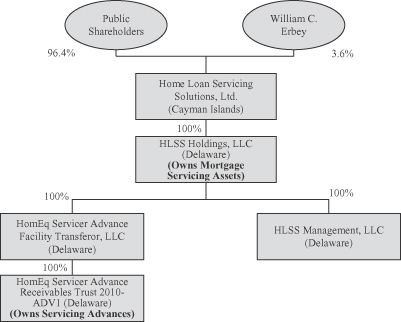

Ownership, Organizational and Operating Structure

On December 1, 2010, we were incorporated as a Cayman Islands exempted company. The following diagram illustrates our corporate structure, the jurisdiction of formation and the ownership interests of our subsidiaries after giving effect to the Offerings and the Initial Acquisition.

Risk Factors

We are a new company and our business model is untested. An investment in our ordinary shares involves significant risks. Below is a summary of some of the key risk factors that you should consider in evaluating an investment in our ordinary shares. This list is not exhaustive and you should carefully read the full discussion of these risks and other risks described under “Risk Factors” beginning on page 14.

| • | We may be unable to implement our business strategy or operate our business as currently expected, including being unable to obtain the Required Third Party Consents. |

| • | The assumptions underlying our business model may prove incorrect. |

| • | We will have increased risk related to our relationship with Ocwen Loan Servicing so long as it retains legal ownership of the Initial Mortgage Servicing Rights. |

| • | We may not be able to pay dividends on our ordinary shares. |

| • | We will rely on Ocwen Loan Servicing to service the mortgage loans underlying the Initial Mortgage Servicing Rights both before legal ownership is transferred to us and after. |

| • | We will need to acquire additional Mortgage Servicing Assets to maintain and grow our business as planned. |

| • | We may not be able to obtain financing to fund our servicing advances and future growth. |

| • | Government regulation may adversely affect our business. |

| • | We may become subject to taxation in the United States. |

7

Table of Contents

Corporate Information

Our principal executive offices are located in the Cayman Islands c/o Walkers Corporate Services Limited, Walker House, 87 Mary Street, George Town, Grand Cayman KYI-9005, Cayman Islands. We also maintain offices in the United States located at 2002 Summit Boulevard, Sixth Floor, Atlanta, Georgia 30319. We can be reached by telephone at (561) 682-7721. We do not incorporate information on, or accessible through, our corporate website into this prospectus, and you should not consider it a part of this prospectus.

8

Table of Contents

| Issuer |

Home Loan Servicing Solutions, Ltd. |

| Ordinary shares offered in this offering |

18,333,333 ordinary shares. |

| Underwriters’ option to purchase additional ordinary shares |

We have granted the underwriters an option to purchase up to an additional 2,750,000 ordinary shares from us at the initial public offering price, less the underwriting discounts, for a period of 30 days from the date of this prospectus to cover over-allotments, if any. |

| Concurrent Private Placement |

On February 23, 2011, we entered into a stock purchase agreement with William C. Erbey, our founder and the Chairman of our Board of Directors and the Chairman of Ocwen’s Board of Directors, pursuant to which he agreed to purchase $10 million of our ordinary shares at the initial public offering price per share in a private placement exempt from the registration requirements of the Securities Act of 1933, as amended (the “Securities Act”), pursuant to Section 4(2) of the Securities Act. No underwriting discounts or commissions will be paid in respect of these shares. Pursuant to a registration rights agreement to be entered into with William C. Erbey (the “Registration Rights Agreement”), we will grant to Mr. Erbey demand registration rights, which he may exercise not more than one time, and unlimited piggyback registrations rights. See “Certain Relationships and Related Party Transactions—Registration Rights.” The closing of the Concurrent Private Placement will take place concurrently with the closing of this offering. Each of the closing of this offering and the Concurrent Private Placement is conditioned on the concurrent closing of the other offering. |

| Number of ordinary shares to be outstanding after the Offerings |

19,020,000 ordinary shares (21,770,000 ordinary shares if the underwriters’ option to purchase additional ordinary shares is exercised in full). |

| Initial Acquisition |

We intend to acquire the Initial Purchased Assets and expect to assume the existing advance financing facility relating to the Initial Mortgage Servicing Rights from Ocwen Loan Servicing simultaneously with the closing of the Offerings. The estimated purchase price for these assets is $ million (including $ million of assumed match funded liabilities with respect to the advance financing facility), subject to certain closing adjustments. See “The Proposed Business—Description of Purchase Agreement.” |

| Use of proceeds |

We estimate that the net proceeds to us from this offering, after deducting underwriting discounts and commissions and our estimated offering expenses, will be approximately |

9

Table of Contents

| $ million, assuming an initial public offering price of $15.00 per share. In addition, we will receive $10 million of proceeds from the sale of our ordinary shares in the Concurrent Private Placement. We intend to use $ million of the net proceeds to acquire the Initial Purchased Assets from Ocwen Loan Servicing simultaneously with the closing of the Offerings. We intend to use the remaining net proceeds, if any, for working capital and general corporate purposes, which may include the repayment of indebtedness or the purchase of additional Mortgage Servicing Assets. Legal ownership of the Initial Mortgage Servicing Rights will be transferred to us upon receipt of the Required Third Party Consents without any additional payment to Ocwen Loan Servicing. See “Use of Proceeds.” |

| Dividend policy |

We intend to distribute at least 90% of our net income to shareholders on a monthly basis through a regular monthly cash dividend, although we are not required by law to do so. On , 2011, our Board of Directors declared a contingent interim dividend of $ per ordinary share for each of the three months ended , and , which will be payable, subject to the stated contingencies and all applicable laws, on each of , and , respectively. These dividends will be contingent upon the consummation of the Offerings and the successful completion of the Initial Acquisition. Our Board of Directors has the right to rescind these dividends at any time prior to the applicable dividend payment date. |

| Proposed NASDAQ Global Market symbol |

“HLSS.” |

| Tax Considerations |

We expect that we will be treated as a PFIC for U.S. federal income tax purposes. In order to avoid possible adverse tax consequences, including deferred tax and interest charges under the U.S. Internal Revenue Code and Treasury regulations thereunder, “U.S. Holders” (as defined below under “Material Cayman Islands and United States Federal Income Tax Considerations—United States Federal Income Taxation”) may make a “qualified electing fund,” or QEF, election or a mark-to-market election with respect to their investments in our ordinary shares. U.S. Holders should consult with their tax advisors as to whether or not to make such elections and the related consequences and should carefully review the information set forth under “Material Cayman Islands and United States Federal Income Tax Considerations—United States Federal Income Taxation—Consequences to U.S. Holders—Passive Foreign Investment Company Status and Related Tax Consequences” for additional information. |

| Risk Factors |

Please read “Risk Factors” beginning on page 14 of this prospectus for a discussion of the factors that you should carefully consider before deciding to invest in our ordinary shares. |

10

Table of Contents

Except as otherwise indicated, all information in this prospectus reflects or assumes no exercise by the underwriters of their option to purchase up to an additional 2,750,000 ordinary shares in this offering at the initial public offering price of $15.00 per share.

11

Table of Contents

Summary Consolidated Financial Data

We were incorporated as a Cayman Islands exempted company on December 1, 2010, and our operations to date have been limited to negotiating the Purchase Agreement and the Subservicing Agreement with Ocwen Loan Servicing, negotiating arrangements with lenders, ratings agencies and other third parties to effect the transfer of Mortgage Servicing Assets, associated servicing advances and the related match funded liabilities to us, negotiating professional and administrative services agreements with Ocwen Loan Servicing and Altisource Portfolio Solutions, S.A. (“Altisource”) and general corporate functions. We have also entered into a stock purchase agreement pursuant to which William C. Erbey, the founder of our company and the Chairman of our Board of Directors, has agreed to purchase $10 million of our ordinary shares at the initial public offering price concurrently with and conditioned upon the closing of this offering. Therefore, we have no historical financial statements reflecting our operations prior to our inception, and our balance sheet as of June 30, 2011 and the results of our operations for the period from December 1, 2010 through June 30, 2011 reflect only the activities described above.

We have derived the balance sheet data as of June 30, 2011 from our unaudited financial statements appearing at the end of this prospectus. You should read the following information together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our financial statements and the related notes, which are included in this prospectus.

The unaudited as adjusted balance sheet data below gives effect to the completion of the Offerings and the Initial Acquisition as if they had been completed at June 30, 2011. The unaudited as adjusted balance sheet data should be read together with our financial statements and the related notes, which are included in this prospectus.

The unaudited as adjusted balance sheet data set forth below give effect to:

| • | the sale of 18,333,333 ordinary shares in this offering at the initial public offering price of $15.00 per share, after deducting underwriting discounts and commissions and estimated offering expenses of approximately $ million payable by us; and |

| • | the concurrent sale of 666,667 ordinary shares in the Concurrent Private Placement at the initial public offering price of $15.00 per share. |

The unaudited as further adjusted balance sheet data set forth below give further effect to:

| • | the completion of the Initial Acquisition at an estimated purchase price of $ million (including $ million of assumed match funded liabilities), subject to certain closing adjustments. |

12

Table of Contents

Consolidated Balance Sheet

As of June 30, 2011

(dollars in thousands)

| Actual | As adjusted for this offering and the Concurrent Private Placement |

As further adjusted for the Initial Acquisition |

||||||||||

| Assets |

||||||||||||

| Cash and cash equivalents |

$ | 296.4 | $ | $ | ||||||||

| Prepaid expenses and other assets |

2,201.9 | |||||||||||

| Match funded advances |

— | |||||||||||

| Rights to MSRs |

— | |||||||||||

|

|

|

|

|

|

|

|||||||

| Total Assets |

$ | 2,498.3 | $ | $ | ||||||||

|

|

|

|

|

|

|

|||||||

| Liabilities and Equity |

||||||||||||

| Liabilities |

||||||||||||

| Match funded liabilities |

$ | — | $ | $ | ||||||||

| Accrued expenses |

1,962.8 | |||||||||||

| Other liabilities |

296.9 | |||||||||||

|

|

|

|

|

|

|

|||||||

| Total Liabilities |

$ | 2,259.7 | $ | $ | ||||||||

|

|

|

|

|

|

|

|||||||

| Equity |

||||||||||||

| Stockholders’ equity — ordinary shares, $0.01 par value; 5,000,000 shares (actual) and 200,000,000 shares (as adjusted) authorized; 20,000 shares (actual) and shares (as adjusted) issued and outstanding at June 30, 2011 |

$ | 0.2 | $ | $ | ||||||||

| Additional paid-in-capital |

299.8 | |||||||||||

| Deficit accumulated during the development stage |

(61.4 | ) | ||||||||||

|

|

|

|

|

|

|

|||||||

| Total Equity |

$ | 238.6 | $ | $ | ||||||||

|

|

|

|

|

|

|

|||||||

| Total Liabilities and Equity |

$ | 2,498.3 | $ | $ | ||||||||

|

|

|

|

|

|

|

|||||||

13

Table of Contents

An investment in our ordinary shares involves significant risks. We describe below the principal risks and uncertainties that we believe affect us or could affect us in the future. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties that we are not aware of or focused on or that we currently deem immaterial may also negatively affect our business operations. You should carefully read and consider the risks and uncertainties described below, together with all of the other information included in this prospectus, before you decide to invest in our ordinary shares. If any of the following risks actually occur, our financial condition and results of operations could be materially and adversely affected. If this were to happen, our ability to pay dividends in the future may be adversely affected, the value of our ordinary shares could significantly decline and you could lose all or part of your investment.

Risks Related to Our Business and Industry

We are a new company. If we are unable to implement our business strategy or operate our business as we currently expect, our operating results may be adversely affected and we may not be able to pay dividends in the future.

Our operations will commence upon the closing of the Offerings and the Initial Acquisition. Our business model is untested and we may not be able to execute our business strategy as planned, which may negatively impact our financial performance and our ability to pay dividends in the future. Businesses such as ours, which are starting up or in their initial stages of development, present substantial business and financial risks and may suffer significant losses. While we are commencing our operations with an executive management team whose members are experienced in the mortgage servicing industry, their prior experience and relationships in the industry may not be successfully transferred to our company. In addition, primarily because we do not have a demonstrated operating history as a mortgage servicer, we are unable to obtain all of the Required Third Party Consents necessary to transfer legal ownership of the Initial Mortgage Servicing Rights to us at this time. Our untested business model and lack of operating history may also make it more difficult for us to acquire additional mortgage servicing rights from Ocwen Loan Servicing or other third parties in the future. As a new company we also must establish operating procedures, implement new systems and complete other tasks necessary to conduct our intended business activities.

Because we are a newly formed company, the historical financial and operating data relating to the Initial Purchased Assets presented in this prospectus may not be representative of our future results.

We are a new company and have no historical operating results. In preparing our business and economic model, we made a number of assumptions about future revenues, expenses, assets and liabilities relating to the Initial Purchased Assets. We based these assumptions, in part, on the historical financial and operating data relating to the Initial Purchased Assets while they were owned by Ocwen Loan Servicing and the prior owners of the Initial Purchased Assets, which may not be indicative of the results we will be able to achieve in the future. In addition, historical financial performance should not be considered a reliable indicator of future performance, and historical trends may not be reliable indicators of anticipated financial performance or trends in future periods. If these assumptions prove incorrect, we may be unable to pay dividends in the future.

We may not be able to obtain the Required Third Party Consents necessary to transfer legal ownership of the Initial Mortgage Servicing Rights to us.

Generally, most pooling and servicing agreements require the consent of various parties, including the rating agencies, the trustees of the related securitization trusts, the sponsors of the securitization transactions, any master servicer or any bond insurers or other credit enhancers insuring the mortgage-backed securities issued by the securitization trusts, prior to the transfer of legal ownership of the related mortgage servicing rights. At this time, some but not all of the rating agencies have indicated that they would issue a statement that the transfer of legal ownership of the Initial Mortgage Servicing Rights to us

14

Table of Contents

would not result in a downgrade to the rating of the related mortgage-backed securities, and we have not received all of the other Required Third Party Consents. Until we obtain the Required Third Party Consents necessary to transfer legal ownership of an Initial Mortgage Servicing Right to us and to engage Ocwen Loan Servicing as a subservicer, Ocwen Loan Servicing will retain legal ownership of such Initial Mortgage Servicing Right. Although we will pursue the Required Third Party Consents together with Ocwen Loan Servicing, we may not be able to obtain all the Required Third Party Consents in a timely manner or at all. Our understanding of one of the primary issues related to obtaining the Required Third Party Consents is that one of the rating agencies would not provide confirmation of its rating of the related mortgage-backed securities, at least until such time as we have developed an operating history as a mortgage servicer. We may not be able to obtain the ratings confirmations or other third party approvals or consents in a timely manner or at all. Until we receive the Required Third Party Consents and transfer legal ownership of the Initial Mortgage Servicing Rights to us, we are subject to increased risks as a result of Ocwen Loan Servicing continuing to own the Initial Mortgage Servicing Rights, including the risks relating to the potential of Ocwen Loan Servicing filing for bankruptcy or being terminated as servicer. See below under “—A bankruptcy of Ocwen Loan Servicing could adversely affect our business, expected dividends on our ordinary shares and the value of your investment in us.”

A bankruptcy of Ocwen Loan Servicing could adversely affect our business, expected dividends on our ordinary shares and the value of your investment in us.

If Ocwen Loan Servicing becomes subject to a bankruptcy proceeding, our business could be materially adversely affected, and you could suffer losses.

The validity or priority of our security interest in the Initial Mortgage Servicing Rights could be challenged in a bankruptcy proceeding of Ocwen Loan Servicing, and the Purchase Agreement could be rejected in such proceeding. Ocwen Loan Servicing’s obligations under the Purchase Agreement with respect to the Rights to MSRs will be secured by a security interest in the Initial Mortgage Servicing Rights and the proceeds of the Initial Mortgage Servicing Rights. We will undertake all requirements under applicable law to properly create and perfect this security interest, including pledging the collateral in the Purchase Agreement and filing financing statements in appropriate jurisdictions to perfect it. Nonetheless, our security interest may be ruled unenforceable or ineffective by a bankruptcy court. If Ocwen Loan Servicing were to file, or to become the subject of, a bankruptcy proceeding under the United States Bankruptcy Code or similar state insolvency laws, during the period of time prior to the transfer of the Initial Mortgage Servicing Rights to us, Ocwen Loan Servicing (as debtor-in-possession in the bankruptcy proceeding) or the bankruptcy trustee could reject the Purchase Agreement and attempt to stop payments to us of the servicing fees or other servicing revenues with respect to the Rights to MSRs and terminate our right to acquire those Initial Mortgage Servicing Rights that we have not already acquired. In the event the security interest is declared unenforceable or ineffective, we would be subject to the risk that our claim for any damages from the rejection of the Purchase Agreement or the failure to pay us the servicing fees or other servicing revenues with respect to the Rights to MSRs would be treated as a general unsecured claim for purposes of distributions from Ocwen Loan Servicing’s bankruptcy estate. In addition, even if the security interest is found to be valid and enforceable, if a bankruptcy court determines that the value of the collateral exceeds the underlying obligation to us, then Ocwen Loan Servicing (as debtor-in-possession in the bankruptcy proceeding) or the bankruptcy trustee would have the power (with the approval of the bankruptcy court) to modify the terms of the payment obligations to us, to substitute collateral securing the security interest or to reduce the collateral securing the security interest to a lesser amount deemed “adequate” to secure payment of our claim.

Payments made by Ocwen Loan Servicing to us could be avoided by a court under federal or state preference laws. If Ocwen Loan Servicing were to file, or to become the subject of, a bankruptcy proceeding under the United States Bankruptcy Code or similar state insolvency laws and our security interest is declared unenforceable or ineffective, payments previously made by Ocwen Loan Servicing to us

15

Table of Contents

pursuant to the Purchase Agreement may be recoverable on behalf of the bankruptcy estate as preferential transfers. A payment could constitute a preferential transfer if a court were to find that the payment was a transfer of an interest of property of Ocwen Loan Servicing that:

| • | was made to or for the benefit of a creditor; |

| • | was for or on account of an antecedent debt owed by Ocwen Loan Servicing before that transfer was made; |

| • | was made while Ocwen Loan Servicing was insolvent (a company is presumed to have been insolvent on and during the 90 days preceding the date the company’s bankruptcy petition was filed); |

| • | was made on or within 90 days (or if we are determined to be a statutory insider, on or within one year) before Ocwen Loan Servicing’s bankruptcy filing; and |

| • | permitted us to receive more than we would have received in a Chapter 7 liquidation case under applicable bankruptcy laws. |

If the court were to determine that any payments were avoidable as preferential transfers, we would be required to return such payments to Ocwen Loan Servicing’s bankruptcy estate.

A sale of Mortgage Servicing Assets or other assets could be re-characterized as a pledge of such assets in a bankruptcy proceeding. If Ocwen Loan Servicing’s transfer to us of Mortgage Servicing Assets or any other asset transferred pursuant to the Purchase Agreement were considered to be a sale of such assets, then such assets would not be part of Ocwen Loan Servicing’s bankruptcy estate. Ocwen Loan Servicing (as debtor-in-possession in the bankruptcy proceeding) or the bankruptcy trustee might assert in a bankruptcy proceeding, however, that mortgage servicing rights or any other asset transferred to us pursuant to the Purchase Agreement were not sold to us but were merely pledged to us as security for Ocwen Loan Servicing’s obligation to repay amounts paid by us to Ocwen Loan Servicing pursuant to the Purchase Agreement. If such assertion were successful, all or part of the Mortgage Servicing Assets or any other asset transferred to us pursuant to the Purchase Agreement would constitute property of the bankruptcy estate of Ocwen Loan Servicing, and our rights against Ocwen Loan Servicing would be those of a secured creditor, and not those of an owner, of such assets. Although we will take steps to properly create and perfect a security interest in the assets we purchase pursuant to the Purchase Agreement in case such purchase is re-characterized as a secured financing, the validity or priority of the security interest could be challenged. See above under “—The validity or priority of our security interest in the Initial Mortgage Servicing Rights could be challenged in a bankruptcy proceeding of Ocwen Loan Servicing, and the Purchase Agreement could be rejected in such proceeding” for a description of the risks associated with such security interest.

Payments made to us by Ocwen Loan Servicing, or obligations incurred by it, could be avoided by a court under federal or state fraudulent conveyance laws. Ocwen Loan Servicing (as debtor-in-possession in the bankruptcy proceeding) or the bankruptcy trustee could also attempt to claim that a sale of Rights to MSRs or sale of mortgage servicing rights or other assets by Ocwen Loan Servicing to us was a fraudulent conveyance. Under the United States Bankruptcy Code and similar state insolvency laws, payments made, or obligations incurred, could be voided if Ocwen Loan Servicing, at the time it made such payment or incurred such obligation: (a) received less than reasonably equivalent value or fair consideration for such transfer or incurrence; and (b) either (i) was insolvent at the time of, or was rendered insolvent by reason of, such transfer or incurrence; (ii) was engaged in, or was about to engage in, a business or transaction for which the assets remaining with Ocwen Loan Servicing were an unreasonably small capital; or (iii) intended to incur, or believed that it would incur, debts beyond its ability to pay such debts as they mature. If any transfer or incurrence is determined to be a fraudulent conveyance, Ocwen Loan Servicing (as debtor-in-possession in the bankruptcy proceeding) or the bankruptcy trustee would be entitled to recover such transfer or to avoid the obligation previously incurred.

The Subservicing Agreement could be rejected in a bankruptcy proceeding. If Ocwen Loan Servicing were to file, or to become the subject of, a bankruptcy proceeding under the United States Bankruptcy Code

16

Table of Contents

or similar state insolvency laws, Ocwen Loan Servicing (as debtor-in-possession in the bankruptcy proceeding) or the bankruptcy trustee could reject the Subservicing Agreement and terminate Ocwen Loan Servicing’s obligation to service the mortgage loans underlying one or more of the mortgage servicing rights that we have acquired and that Ocwen Loan Servicing has agreed to service for us pursuant to the Subservicing Agreement. As we will not have and in the future do not expect to have the employees, servicing platforms or technical resources necessary to service mortgage loans, if the Subservicing Agreement is rejected we will need to either engage an alternate subservicer, which may not be readily available on acceptable terms or at all, or negotiate a new servicing arrangement with Ocwen Loan Servicing, which would presumably be on less favorable terms to us. Any claim we have for damages arising from the rejection of the Subservicing Agreement would be treated as a general unsecured claim for purposes of distributions from Ocwen Loan Servicing’s bankruptcy estate.

Any of the foregoing events might have a material adverse effect on our financial condition or operating results and our ability to pay dividends, which could cause delays or reductions in payments on our ordinary shares or a reduction in the value of our ordinary shares.

We may not be able to pay dividends on our ordinary shares.

We intend to declare and pay regular cash dividends on our ordinary shares. We intend to distribute at least 90% of our net income to shareholders on a monthly basis, although we are not required by law to do so. On , 2011, our Board of Directors declared a contingent interim dividend of $ per ordinary share for each of the three months ended , and , which will be payable, subject to the stated contingencies and all applicable laws, on each of , and , respectively. The payment of these dividends will be contingent upon the consummation of the Offerings and the successful completion of the Initial Acquisition. Our Board of Directors has the right to rescind these dividends at any time prior to the applicable dividend payment date. While we intend to continue to pay monthly dividends at this rate, we may not be able to do so in the future. Our dividend policy is subject to the discretion of our Board of Directors and will depend, among other things, on cash available for distributions, general economic and business conditions, our strategic plans and prospects, our financial results and condition, contractual, legal and regulatory restrictions on the declaration and payment of dividends by us and such other factors as our Board of Directors considers to be relevant.

Our ability to declare and pay dividends is dependent on cash flow generated by our subsidiaries because we are a holding company.

We are a holding company with no operations. Our subsidiaries will own all of the assets that will generate income. Therefore, our ability to declare and pay dividends is dependent on the generation of cash flow by our subsidiaries and their ability to make such cash available to us, by dividend, distribution or otherwise. Our subsidiaries may not be able or permitted to make distributions to enable us to make dividend payments in respect of our ordinary shares. Each of our subsidiaries is a distinct legal entity formed and governed under the laws of the State of Delaware, and, under certain circumstances, legal and contractual restrictions may limit our ability to obtain cash from them. The subsidiary that holds the Rights to MSRs and that will hold any mortgage servicing rights we acquire in the future is a Delaware limited liability company. Delaware law provides that a limited liability company is prohibited from making a distribution of cash or other property to a member to the extent that, at the time of and after giving effect to the distribution, the limited liability company’s liabilities exceed the fair value of its assets, subject to certain exceptions. In addition, while our subsidiaries currently are not subject to any contractual restrictions with respect to the payment of dividends, any future financing or other arrangements that our subsidiaries enter into could limit their ability to make distributions to us. In the event that we do not receive distributions from our subsidiaries, we may be unable to make dividend payments on our ordinary shares.

17

Table of Contents

We are highly dependent upon our senior management team.

Our business model and the execution of our business strategy is highly dependent upon the members of our senior management team who will resign their positions at Ocwen and become our employees simultaneously with the closing of the Offerings and the Initial Acquisition. The loss of the services of any of our senior executives or key employees could delay or prevent us from executing our business strategy and could significantly and negatively affect our business.

Our senior management team will also devote a portion of its time to performing certain functions for Ocwen pursuant to a professional services agreement, which we refer to as the “Ocwen Professional Services Agreement,” that we will enter into with Ocwen Loan Servicing simultaneously with the closing of the Offerings and the Initial Acquisition. This will detract from the amount of time these executives have available to focus on our business.

In the future, we may need to hire additional personnel to meet the demands of our business, including any changes to our business strategy or operations due to a failure to obtain consents needed to transfer mortgage security rights on a timely basis or at all. The number of available, qualified personnel in the mortgage servicing industry may be limited, and the lack of qualified personnel may delay our ability to execute our business model as planned.

The continued economic slowdown and/or continued deterioration of the housing market could increase delinquencies and defaults on the mortgage loans underlying the mortgage servicing rights we acquire, which would negatively affect our operating results.

The residential mortgage market in the United States has experienced and may continue to experience a variety of difficulties and challenging economic conditions. Housing prices in many parts of the United States have declined or stopped appreciating after extended periods of significant appreciation. Any further deterioration of the U.S. housing market and declines in home prices could result in increased delinquencies or defaults on the mortgage loans underlying the mortgage servicing rights we acquire.

During any period in which the borrower is not making payments on a mortgage loan, the servicer under substantially all pooling and servicing agreements is required to advance its funds to meet contractual principal and interest remittance requirements for the securitization trust that owns the mortgage loans, pay property taxes and insurance premiums, process foreclosures and maintain, repair and market foreclosed real estate properties.

If the economy slows and/or the housing market continues to deteriorate, our operating results would be adversely affected in the following ways:

Revenue. Because we recognize fee revenue as principal and interest payments are collected from the borrowers on the mortgage loans underlying our Mortgage Servicing Assets and as delinquent loans are resolved, an increase in delinquencies would reduce the fee revenue that we recognize.

Expenses. An increase in servicing advances outstanding relative to the amount of the unpaid principal balance of the mortgage loans underlying our Mortgage Servicing Assets could result in substantial strain on our financial resources because growth of outstanding servicing advances relative to the unpaid principal balance of mortgage loans would increase financing costs with no offsetting increase in revenue, thus reducing profitability. If servicing advances increase to a level where we are unable to fund additional servicing advances, we may not be able to fulfill our obligations under the Purchase Agreement to purchase the servicing advances that Ocwen Loan Servicing is required to make pursuant to the pooling and servicing agreements related to the Initial Mortgage Servicing Rights, or our obligations to fund servicing advances under those pooling and servicing agreements for which we are the servicer. As a result, the Purchase Agreement could be terminated, and we could lose the revenues associated with our Rights to MSRs or be terminated as servicer under any affected pooling and servicing agreements and lose the revenues associated with the mortgage servicing rights, as applicable.

18

Table of Contents

Valuation of Mortgage Servicing Assets. Defaults on mortgage loans will decrease the value of the associated Mortgage Servicing Assets. In addition, future default rates that exceed current estimates may result in higher amortization and an impairment in the value of our Mortgage Servicing Assets such that revenue may decline and amortization and interest expense may increase.

A significant increase in prepayment speeds would reduce the unpaid principal balance of the mortgage loans underlying our Mortgage Servicing Assets and could adversely affect our operating results.

Prepayment speeds significantly affect our business. Prepayment speed is the measurement of how quickly borrowers pay down the unpaid principal balance of their loans or how quickly loans are otherwise brought current, modified, liquidated or charged off. Prepayment speeds, which are presently driven primarily by involuntary liquidations of subprime and Alt-A mortgage loans, have a significant impact on our revenues, our expenses and the valuation of our Mortgage Servicing Assets as follows:

Revenue. If prepayment speeds increase, our fee revenue will decline more rapidly than estimated because of the greater than expected decrease in the unpaid principal balance of the mortgage loans on which those fees are based.

Expenses. Amortization of Mortgage Servicing Assets will be our largest operating expense. Since we amortize Mortgage Servicing Assets in proportion to total expected income over the life of the Mortgage Servicing Assets, an increase in prepayment speeds will lead to increased amortization expense as we revise downward our estimate of total expected income.

Valuation of Mortgage Servicing Assets. We base the price we pay for Mortgage Servicing Assets and the rate of amortization of those assets on, among other things, our projection of the cash flows from the related pool of mortgage loans. Our expectation of prepayment speeds is a significant assumption underlying those cash flow projections. If prepayment speeds are significantly greater than expected, the carrying value of our Mortgage Servicing Assets could exceed their estimated fair value. If the carrying value of our Mortgage Servicing Assets exceeds their fair value, we will be required to record a non-cash impairment charge, which would have a negative impact on our operating results.

We may not be able to successfully compete for the acquisition of mortgage servicing rights, which could adversely affect our business.

Our success depends, in large part, on our ability to acquire additional mortgage servicing rights on terms consistent with our business and economic model. We expect to compete with independent mortgage loan servicers, private equity firms, hedge funds and other large financial services companies in acquiring additional mortgage servicing rights. Many of our anticipated competitors are significantly larger than we are, have access to greater capital and other resources and may have other advantages over us. In addition, some of our competitors may have higher risk tolerances or different risk assessments, which could lead them to offer higher prices than we would be willing to pay for these assets.

Under most pooling and servicing agreements the approval or consent of third parties will be required to transfer mortgage servicing rights to us. We have not yet been able to obtain all the Required Third Party Consents necessary to transfer legal ownership of the Initial Mortgage Servicing Rights to us, primarily because we do not have a demonstrated operating history as a mortgage servicer. Until such time as we establish an operating history as a mortgage servicer, we may need to continue to structure purchases of mortgage servicing rights as purchases of Rights to MSRs to the extent that the related pooling and servicing agreements require approvals or consents that we are unable to obtain. As a result, other potential purchasers of mortgage servicing rights may be more attractive to sellers if the sellers believe that they can obtain any necessary third party approvals and consents to transfer the mortgage servicing rights to these potential purchasers more easily than if they were transferring them to us. This may negatively effect our ability to acquire additional mortgage servicing rights or limit the available mortgage servicing rights or types of mortgage servicing rights that we are able to offer to acquire.

19

Table of Contents

We also do not intend to build a mortgage servicing platform. Therefore, we may not be an attractive buyer for those sellers of mortgage servicing rights that prefer to sell mortgage servicing rights and their mortgage servicing platform in a single transaction. Since our business model does not currently include acquiring and running servicing platforms, to engage in a bid for such a business we would need to find a partner to acquire and run the platform or we would need to incur additional costs to shut down the acquired servicing platform. The need to work with a partner in these situations increases the complexity of such potential acquisitions, and Ocwen Loan Servicing may be unwilling to act as servicer or subservicer on any mortgage servicing rights acquisition we want to execute. The complexity of these transactions and the additional costs incurred by us if we were to execute future acquisitions of this type could adversely affect our future operating results.

We may be unable to maintain the unpaid principal balance of the mortgage loans underlying our Mortgage Servicing Assets at an adequate level, which may cause administrative expenses to increase relative to our equity base.

The unpaid principal balance of the mortgage loans underlying the Initial Mortgage Servicing Rights will decline naturally over time. In addition, the unpaid principal balance of the mortgage loans underlying the Initial Mortgage Servicing Rights could be reduced in connection with any loan put-backs. A loan put-back is a request by the securitization trustee for the originator of the loan or the party that transferred the loan to the securitization to repurchase the loan at par. These requests generally arise because the originator or transferor is found to have breached representations or warranties made at the time of origination or securitization. We intend to acquire additional Mortgage Servicing Assets to maintain a sufficient level of unpaid principal balance of the mortgage loans underlying our Mortgage Servicing Assets relative to the size of our operations. Given competition in our industry for the acquisition of mortgage servicing rights and the continued decrease in new securitizations, primarily as a result of the lack of new originations of subprime and Alt-A mortgage loans, a sufficient number of subprime and Alt-A mortgage servicing rights may not be available at attractive prices or at all. If we are unable to acquire new Mortgage Servicing Assets, our revenue, which is based on the unpaid principal balance of the loans underlying our Mortgage Servicing Assets, may decline as mortgage loans are repaid or liquidated. As a result, our future expenses may increase disproportionately to the size of our equity base, which will negatively affect our profitability and may limit our ability to pay dividends in the future.

Our assumptions in determining the purchase price for Mortgage Servicing Assets may be inaccurate or the basis for such assumptions may change, which could adversely affect our results of operations.

To the extent that we purchase Mortgage Servicing Assets in the future, our success will be highly dependent upon accurate pricing of such Mortgage Servicing Assets. In determining the purchase price for Mortgage Servicing Assets, we will make assumptions regarding the following:

| • | the rates of prepayment and repayment of the underlying mortgage loans; |

| • | amount of future servicing advances; |

| • | projected rates of delinquencies and defaults; |

| • | future interest rates; and |

| • | the costs associated with engaging subservicers to service the loans. |

If any of our assumptions regarding the Mortgage Servicing Assets that we acquire are inaccurate or the basis for such assumptions change, the price we pay to acquire Mortgage Servicing Assets may prove to be too high. This could result in lower than expected profitability or a loss.

We do not intend to operate a mortgage servicing platform and will need to engage subservicers to service the mortgage loans underlying any mortgage servicing rights we ultimately acquire. We may not be able to engage subservicers on terms that are favorable to us or at all.

We do not intend to operate a mortgage servicing platform. Our success will depend on our ability to enter into subservicing agreements with high-quality mortgage servicers, like Ocwen Loan Servicing, to service the mortgage loans underlying any mortgage servicing rights we ultimately acquire.

20

Table of Contents

The terms of any subservicing agreement will be negotiated with the subservicer prior to the acquisition of the related mortgage servicing rights. It is unlikely that the term of any subservicing agreement we enter into will match the life of any mortgage servicing rights that we ultimately acquire and therefore will need to be renewed. As a result, the terms of any new subservicing agreement or renewal will depend on the economic environment and the costs of providing subservicing at that time. For example, the initial term of the Subservicing Agreement that will take effect immediately upon the closing of the Initial Acquisition will expire in six years from the closing date. Therefore, we will need to renegotiate the terms of this agreement before these assets wind down. In addition, the terms of any future subservicing agreements, including those we enter into with Ocwen Loan Servicing, may not be similar to the terms of the Subservicing Agreement we expect to enter into with Ocwen Loan Servicing for the Initial Mortgage Servicing Rights.

We may be unable to obtain sufficient capital to meet the financing requirements of our business, which could adversely affect our operating results and our ability to pay dividends in the future.

We will need access to capital to finance servicing advances relating to the Mortgage Servicing Assets we may acquire and to fund future acquisitions of additional Mortgage Servicing Assets and associated servicing advances.