UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-22523

Destra Investment Trust II

(Exact name of registrant as specified in charter)

One North Wacker, 48th Floor

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Nicholas Dalmaso

One North Wacker, 48th Floor

Chicago, IL 60606

(Name and address of agent for service)

Registrant's telephone number, including area code: 1-312-843-6161

Date of fiscal year end: September 30

Date of reporting period: September 30, 2014

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 100 F Street, NE, Washington, DC 20549. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

Destra Preferred and Income Securities Fund

Destra Focused Equity Fund

Annual Report

September 30, 2014

|

Table of Contents

|

|

|

Shareholder Letter

|

3

|

|

Destra Preferred and Income Securities Fund Discussion of Fund Performance

|

5

|

|

Destra Preferred and Income Securities Fund Portfolio Manager Letter

|

7

|

|

Destra Preferred and Income Securities Fund – Fund Risk Disclosures

|

10

|

|

Destra Focused Equity Fund Discussion of Fund Performance

|

12

|

|

Destra Focused Equity Fund Portfolio Manager Letter

|

14

|

|

Destra Focused Equity Fund – Fund Risk Disclosures

|

16

|

|

Overview of Fund Expenses

|

18

|

|

Portfolio of Investments

|

|

|

Destra Preferred and Income Securities Fund

|

19

|

|

Destra Focused Equity Fund

|

21

|

|

Statements of Assets and Liabilities

|

22

|

|

Statements of Operations

|

23

|

|

Statements of Changes in Net Assets

|

24

|

|

Financial Highlights

|

26

|

|

Notes to Financial Statements

|

30

|

|

Report of Independent Registered Public Accounting Firm

|

36

|

|

Supplemental Information

|

37

|

|

Board Considerations Regarding the Approval of the Investment Management Agreement

|

|

|

and Investments Sub-Advisory Agreements

|

38

|

|

Shareholder Meeting Results

|

41

|

|

Board of Trustees and Officers

|

42

|

|

General Information

|

47

|

Not FDIC or Government Insured, No Bank Guarantee, May Lose Value

2

Dear Fellow Shareholders,

Thank you for investing in the Destra Funds (the “Funds”). Destra Capital Advisors LLC ("Destra") provides investors and their advisors access to specialty-based asset managers with original investment theories. We strive to give mutual fund investors access to deliberate, conscious and qualitative investment products with a differentiated point of view, through our Destra Family of Mutual Funds. Destra’s investment products are developed with the goal of helping investors realize their long-term investment objectives. For the Funds’ fiscal year ending September 30, 2014, US equity markets, as represented by the S&P 500 Index (“S&P 500”), had a very strong year with a total return of 19.73%. Fixed income markets also had a strong, albeit volatile, year with the Barclays US Aggregate Bond Index (“Barclays Agg”) generating a total return of 3.96% for the year.

The Funds’ fiscal year began on shaky ground as the US Government shutdown for the first half of October 2013. However, a last-minute congressional deal was struck to extend the government’s debt ceiling ahead of the October 17th deadline which translated to a swift upward movement in the US equity markets. In December, the Federal Reserve (“Fed”) noted that it saw improvement in economic activity and labor market conditions. Consequently, the Fed announced that it would reduce its monthly purchases of mortgage-backed securities and US Treasuries to $75 billion per month, down from $85 billion, beginning a tapering of its Quantitative Easing (“QE”) program.

The tapering news was interpreted by investors as a sign the US economy is on more solid footing and added further impetus to the US equity markets, which had continued to rise following its early-October jitters. The S&P 500 hit an all-time high prior to the end of fourth quarter, culminating in the best calendar year for US stocks since 1997. During the fourth quarter of 2013, the S&P 500 generated a total return of 10.51% while the Barclays Agg generated a total return of -0.14%.

During the first quarter of 2014 the S&P 500 continued to hit a series of record closing highs and the Barclays Agg generated a positive total return. The Fed also began tapering its QE program at a pace of $10 billion per month. The new Fed Chair Janet Yellen gave her first testimony before Congress. During her press conference, she signaled that no changes would be made to the schedule of QE tapering and that interest rates are likely to remain low for some time. Her thoughts were positively received by both equity and fixed income investors. During the first quarter of 2014, the S&P 500 Index generated a total return of 1.81% while the Barclays US Aggregate generated a total return of 1.84%.

The second quarter of 2014 was yet another strong quarter for the S&P 500 and the Barclays Agg. Economic data releases generally pointed to an improvement in economic growth which followed a disappointing first quarter where GDP contracted by 2.9%. The Fed cut its 2014 US GDP forecast due to the harsh winter weather (Destra is based outside of Chicago so we can attest to the harsh weather this winter) that affected first quarter growth. Keep in mind that this forecast still implied strong economic progress for the remainder of 2014. During the second quarter of 2014, the S&P 500 Index generated a total return of 5.23% while the Barclays Agg generated a total return of 2.04%.

After two rather placid quarters in the US equity and fixed income markets, volatility reared its head during the third quarter of 2014. While volatile, the S&P 500 Index generated a total return of 1.13% while the Barclays Agg generated a total return of 0.17% during the quarter. Geopolitical concerns, including building conflicts in the Middle East and Ukraine, contributed to additional investor risk aversion but were insufficient in curtailing US economic growth as investors were positively surprised with the strong second quarter GDP growth of 4.6%. In addition to the strong economic data, a series of large mergers and acquisitions were announced during the quarter which helped bolster the US equity markets. As many say “bull markets climb a wall of worry” and the third quarter of 2014 was certainly a testament to this adage.

We believe that experience sets Destra apart. The Destra team of investment professionals have decades of knowledge in their areas of expertise. This allows us to rise above fleeting market statistics and provides perspective to us when designing our portfolio-enhancing investment strategies and products. By confidently taking the long view, we believe that we build investment strategies that forgo what’s currently in favor for what’s right for long-term investors.

We believe our investment managers continue to adhere to their investment strategy and focus on attempting to limit downside risk when markets are down while participating in the upside when markets go up. This report should provide you with information on your Fund’s performance and other insights regarding the Fund’s investment strategy and management.

3

On August 25, 2014, Arrowpoint Asset Management LLC ("Arrowpoint") agreed to acquire additional units in Destra Capital Management LLC, the parent company of Destra Advisors LLC. As a result, Arrowpoint and its affiliates will own in the aggregate approximately 79% of Destra Capital Management LLC following the consummation of this transaction. The closing of the transaction is subject to certain conditions, including among others, approval of the new investment management agreements and new sub-advisory agreements by the Boards and the shareholders of the Funds. Assuming satisfaction of all required closing conditions, the closing is expected to occur by November 20, 2014.

Thank you for the confidence you have placed in us and we can assure you that we will work every day in an effort to earn your confidence.

Sincerely,

Destra Capital Advisors LLC

Index Information

S&P 500 Index –a capitalization weighted index of 500 stocks. Indexes are unmanaged, do not reflect the deduction of fees or expenses and are not available for direct investment.

Barlcays U.S. Aggregate Index – index that provides a measure of performance of the U.S. investment grade bond markets, which includes investment grade U.S. Government bonds, investment grade corporate bonds, mortgage pass-through securities and asset-backed securities. The securities that comprise the index must be denominated in US dollars and must be fixed rate, nonconvertible and taxable.

Unlike the portfolio returns, the index returns do not reflect any fees or expenses and do not include the effect of any cash reserves.

4

| DESTRA PREFERRED AND INCOME SECURITIES FUND | ||||||

| DISCUSSION OF FUND PERFORMANCE | ||||||

|

Destra Preferred and Income Securities Fund Average Annual Total Returns as of September 30, 2014

|

||||||

|

Inception Date: April 12, 2011

|

Inception Date: November 1, 2011 | |||||

|

Life

|

Life

|

|||||

|

Share Class

|

1 year

|

3 year

|

of Fund

|

Share Class

|

1 year

|

of Fund

|

|

A at NAV

|

11.49%

|

9.63%

|

8.32%

|

C at NAV

|

10.68%

|

8.34%

|

|

A with Load

|

6.55%

|

7.98%

|

6.91%

|

C with Load

|

9.68%

|

8.34%

|

|

I at NAV

|

11.93%

|

10.02%

|

8.69%

|

|||

|

Preferred Benchmark

|

13.03%

|

9.59%

|

7.43%

|

Preferred Benchmark

|

13.03%

|

8.73%

|

Performance shown is historical and may not be indicative of future returns. Investment returns and principal value will vary, and shares may be worth more or less at redemption than at original purchase. Performance shown is as of the date indicated, and current performance may be lower or higher than the performance data quoted. To obtain performance as of the most recent month end, please visit www.destracapital.com or call 877.855.3434. Fund performance in the table above does not reflect the deduction of taxes a shareholder would pay on distributions or the redemption of shares. Class A shares have a maximum sales charge of 4.50% and a 12b-1 fee of .25%. Class C shares have a maximum deferred sales charge of 1.00% and a 12b-1 fee of 1.00%.

The Fund’s total returns would have been lower if certain expenses had not been waived or reimbursed by the investment adviser. Fund returns include the reinvestment of dividends.

The Destra Preferred and Income Securities Fund’s estimated total annual operating expense ratios, gross of any fee waiver or expense reimbursement, were anticipated to be 1.99% for Class A, 3.09% for Class C, and 1.55% for Class I shares. There is a voluntary fee waiver currently in place for this Fund through February 1, 2022, to the extent necessary to keep the Fund’s operating expense ratios from exceeding 1.50% for Class A, 2.25% for Class C, and 1.22% for Class I shares of average net assets per year. Some expenses fall outside of this cap and actual expenses may be higher than 1.50% for Class A, 2.25% for Class C, and 1.22% for Class I shares. Without this expense cap, actual returns would be lower.

The Preferred Benchmark is calculated as the sum of 50% of the monthly return on the BofA Merrill Lynch Hybrid Preferred Securities 8% Constrained Index and 50% of the monthly return on the BofA Merrill Lynch US Capital Securities US Issuers 8% Constrained Index. Index returns include investments of any distributions. It is not possible to invest directly in an index.

The BofA Merrill Lynch Hybrid Preferred Securities 8% Constrained Index includes taxable, fixed-rate, US dollar denominated investment-grade, preferred securities listed on a US exchange. The BofA Merrill Lynch US Capital Securities US Issuers 8% Constrained Index includes investment grade fixed rate or fixed-to-floating rate $1,000 par securities that receive some degree of equity credit from the rating agencies or their regulators. Unlike the portfolio returns, the index returns do not reflect any fees or expenses and do not include the effect of any cash reserves.

Growth of $10,000 Investment

Since Inception At Offering Price

The chart above represents historical performance of a hypothetical investment of $10,000 over the life of the Fund. Class A Shares have a maximum sales charge of 4.50% imposed on purchases. Indexes are unmanaged and do not take into account fees, expenses or other costs. Past performance does not guarantee future results. The hypothetical example does not represent the returns of any particular investment.

5

DESTRA PREFERRED AND INCOME SECURITIES FUND

DISCUSSION OF FUND PERFORMANCE, CONTINUED

As of September 30, 2014

|

Credit Quality

|

|||

|

Moody’s

|

Standard & Poor’s

|

||

|

Aa3

|

AA-

|

||

|

A1

|

A+

|

2.2%

|

|

|

A2

|

A

|

||

|

A3

|

1.6%

|

A-

|

|

|

Baa1

|

5.1%

|

BBB+

|

1.5%

|

|

Baa2

|

17.9%

|

BBB

|

21.7%

|

|

Baa3

|

16.8%

|

BBB-

|

26.3%

|

|

Ba1

|

27.7%

|

BB+

|

13.1%

|

|

Ba2

|

9.2%

|

BB

|

21.3%

|

|

Ba3

|

7.7%

|

BB-

|

9.0%

|

|

<Ba

|

5.3%

|

<BB

|

1.1%

|

|

Not Rated

|

5.6%

|

Not Rated

|

0.7%

|

|

Cash

|

3.1%

|

Cash

|

3.1%

|

|

Top 10 Issuers

|

% of Total Investments

|

|

HSBC PLC

|

4.8%

|

|

Goldman Sachs Group

|

4.5%

|

|

Citigroup

|

4.5%

|

|

JPMorgan Chase

|

4.3%

|

|

MetLife

|

3.6%

|

|

ING Groep NV

|

3.5%

|

|

Fifth Third Bancorp

|

3.0%

|

|

XL Group PLC

|

3.0%

|

|

First Republic Bank

|

2.9%

|

|

Barclays Bank PLC

|

2.7%

|

|

Portfolio Characteristics

|

Fund

|

|

Number of Issues

|

79

|

|

QDI Eligibility

|

54.2%

|

|

Geographic Concentration

|

|

|

Domestic/International

|

78%/22%

|

Qualified Dividend Income (QDI) meets specific criteria to be taxed at lower long-term capital gains tax rates rather than at an individual’s ordinary income rate.

Holdings, sectors and security types are subject to change without notice. There is no assurance that the investment process will lead to successful investing.

The credit quality breakdowns are based on actual ratings issued by the relevant NRSRO or the NRSRO’s rating of a similar security of the same issuer. The credit quality of the investments in the portfolio does not apply to the stability or safety of the Fund. Credit quality ratings are subject to change and pertain to the underlying holdings of the Fund and not the Fund itself.

Portfolio Sector Allocation

as of 9/30/14 (% of Total Investments)

Security Types

as of 9/3014 (% of Total Investments)

6

DESTRA PREFERRED AND INCOME SECURITIES FUND

DESTRA PREFERRED AND INCOME SECURITIES FUND PORTFOLIO MANAGER LETTER

Fund Snapshot

The Destra Preferred and Income Securities Fund (the “Fund”) is sub-advised by investment manager Flaherty & Crumrine Incorporated (“Flaherty & Crumrine”). The Fund’s investment objective is to seek total return, with an emphasis on high current income.

Flaherty & Crumrine was founded in 1983 and is one of the oldest preferred securities managers in the industry. Through the years they have built a proprietary database with information on over 1,500 separate issues of preferred securities. Flaherty & Crumrine then leverages their experience and database seeking to unlock hidden value, in what they believe is an inefficient preferred securities market. To accomplish this goal the Fund will, in normal markets, invest at least 80% of its net assets in a portfolio of preferred and income producing securities. The securities in which the Fund may invest include traditional preferred stock, trust preferred securities, hybrid securities, convertible securities, contingent-capital securities, subordinated debt, and senior debt securities of other open-end, closed-end or exchange-traded funds that invest primarily in the same types of securities. The Fund may invest up to 40% of its assets in securities of non-U.S. companies and up to 15% of its assets in common stocks. In addition, under normal market conditions, the Fund invests more than 25% of its total assets in companies principally engaged in financial services.

The Fund principally invests in (i) investment grade quality securities or (ii) below investment grade quality preferred or subordinated securities of companies with investment grade senior debt outstanding, in either case determined at the time of purchase. Securities that are rated below investment grade are commonly referred to as “high yield” or “junk bonds.” However, some of the Fund’s total assets may be invested in securities rated (or issued by companies rated) below investment grade at the time of purchase. Preferred and debt securities of below investment grade quality are regarded as having predominantly speculative characteristics with respect to capacity to pay dividends and interest and repayment of principal. Due to the risks involved in investing in preferred and debt securities of below investment grade quality, an investment in the Fund should be considered speculative. The maturities of preferred and debt securities in which the Fund will invest generally will be longer-term (perpetual, in the case of some preferred securities, and ten years or more for other preferred and debt securities); however, in light of changing market conditions and interest rates, the Fund may also invest in shorter-term securities.

The following report is Flaherty & Crumrine’s review of the Fund’s performance over the twelve months comprising the annual reporting period and outlook for the markets the Fund invests in going forward.

How did the Fund perform during the year-ended September 30, 2014?

During fiscal year-ended September 30, 2014, the Fund’s Class A shares had a total return of 11.49% based on Net Asset Value (“NAV”), the Class I shares had a total return of 11.93% on NAV and the Class C shares had a total return of 10.68% on NAV. During the period surveyed, the Fund’s benchmark (50%/50% blend of the BofA Merrill Lynch 8% Constrained Hybrid Preferred Securities Index and the BofA Merrill Lynch US Capital Securities US Issuers 8% Constrained Index) had a total return of 13.03%.

Two important factors to consider when surveying fund returns – first, the returns include reinvestment of all distributions, and second, it is not possible to invest directly in an index. All of the Fund’s share classes have the same investment objective - total return with an emphasis on high current income.

Preferred Benchmark is a 50/50 blend of the BofA Merrill Lynch 8% Constrained Hybrid Preferred Securities Index, a subset of the BofA Merrill Lynch Fixed Rate Preferred Securities IndexSM that contains all subordinated constituents of the fixed rate index with a payment deferral feature and with issuer concentration capped at a maximum of 8% (the fixed-rate index includes investment grade DRD eligible and non- DRD eligible preferred stock and senior debt); and the BofA Merrill Lynch US Capital Securities US Issuers 8% Constrained Index, a subset of the BofA Merrill Lynch Corporate All Capital Securities IndexSM that contains securities issued by US corporations (the index includes investment grade fixed-rate or fixed-to-floating rate $1,000 par securities that receive some degree of equity credit from the rating agencies or their regulators and with issuer concentration capped at a maximum of 8%). Indexes are unmanaged, do not reflect the deduction of fees or expenses and are not available for direct investment.

7

DESTRA PREFERRED AND INCOME SECURITIES FUND

DESTRA PREFERRED AND INCOME SECURITIES FUND PORTFOLIO MANAGER LETTER, CONTINUED

What were the significant events affecting the economy and market environment during the period surveyed?

After a difficult stretch during the second half of 2013, the preferred securities market seemed ripe for recovery. In fact, it would be difficult to argue that the performance of preferreds over the first six months of the year was less than fantastic. In most cases, market prices rose back to, or above, levels of a year ago—prior to the selloff that began with hints of Fed “taper” and a sharp rise in rates that was compounded by tax-loss selling and other technical factors late in 2013. Much of the recovery may have been expected as year-end selling subsided, but strong fundamental and technical conditions have contributed to a sustained rally.

Among the fundamental reasons for the rally, credit quality continues to improve for most issuers of preferreds. Regulation of financial companies is still evolving, but national regulators generally are adhering to standards established under Basel III as they roll out their specific rules. To meet these new requirements, financial companies are holding much more common equity capital than in the past, which is credit enhancing for preferreds.

Bank stress tests completed earlier this year confirmed that progress has been made. Most large U.S. banks now have excess common equity capital, even under new, stricter guidelines. As a result, banks are beginning to return more capital to shareholders. This is a healthy development that should not harm the position of preferred holders in the near future, as overall capital levels should be maintained at reasonable levels. Broader economic improvement, while not as robust as many hoped, continues to support the outlook for credit improvement for corporations and households alike. Loan losses at banks are well off their highs, and are reverting to more “normal” levels consistent with slow improvement in consumer balance sheets.

The market’s technical backdrop also deserves a good deal of credit for preferreds’ performance this year. Interest rates have retreated from their recent highs, perhaps even more than most would have predicted. Monetary policy remains accommodative, and options for fixed-income investors to find yield are limited. Preferreds are currently the highest-yielding domestic asset class by most measures, and their yields have attracted buyers from many areas of fixed-income markets.

As you may know, the preferred market is dwarfed in size by the corporate bond market – the traditional staple in a fixed-income portfolio. So when investors look outside the corporate bond market for yield and turn their sights to preferreds, the amount of money interested in our market can be overwhelming. This has been the pattern of late, which has created strong demand for preferreds.

U.S. economic growth now appears to be running around 3%, after averaging just 1.3% in 2014’s first half. Job growth is up, unemployment is down and inflation remains low. The Fed is not filling its monetary punch bowl as quickly as before, but, while it’s always hard to predict what the Fed will do, it probably won’t start to raise short-term interest rates until mid-2015 or later. In contrast, economic growth abroad has slowed, with most developed countries trailing the U.S. recovery and monetary policy in many of those countries is easing further.

Supply of new issues remains steady—a key measure of market health. From October 2013 through September 2014, U.S. and foreign companies issued 116 new securities in the United States, raising just under $70 billion. Over the same period, issuers redeemed 92 preferred securities totaling $28 billion.

New issue supply was dominated by banks tailoring their capital to meet new regulatory requirements. Large U.S. banks (those deemed to be a systemically important financial institution, or “SIFI”) have issued traditional non-cumulative perpetual preferred stock. Non-U.S. SIFI banks are utilizing a preferred stock variation termed Contingent Convertible Securities, or CoCos. The Fund currently has no investments in CoCos but we think of them as an extension of the preferred market. As this market develops further, we may determine CoCos are suitable investments for the portfolio. One thing is certain: CoCos will be a growing part of the preferred securities market over coming years as European banks refinance older non-compliant issues and raise additional capital.

How did the aforementioned events affect the Fund?

The Fund’s portfolio benefited from declines in intermediate and long-term interest rates over the past year. Moreover, the portfolio was favorably impacted by on-going demand for higher yields of preferred securities and continued improvement in the capital of banks and other financial company issuers.

8

DESTRA PREFERRED AND INCOME SECURITIES FUND

DESTRA PREFERRED AND INCOME SECURITIES FUND PORTFOLIO MANAGER LETTER, CONTINUED

With foreign economies lagging recovery in the U.S. and foreign banks issuing securities such as CoCos that we have not yet been inclined to buy, the portion of the portfolio invested in foreign securities has drifted lower this fiscal year. Over the past year, this portion declined from 25% of the portfolio to 22%. We anticipate this rate could fall further through more issuer redemptions.

Another portfolio trend is a continued shift to “fixed-to-float” securities. These have coupons that are fixed for an initial period, typically five or ten years. Afterwards, coupons float based on a formula set at issuance. Prices on floating rate issues typically are less sensitive to changes in benchmark interest rates; this effect has spilled over to fixed-to-float preferred securities as well. If long-term interest rates begin to rise, as we expect they will eventually, these securities should tend to outperform issues with fixed-for-life coupons, all other things being equal. As of September 30th, the portion of the portfolio in this structure was 44%. We continue to look for opportunities to add fixed-to-float holdings. Although these issues yield a bit less than many fixed-for-life securities, and thus may reduce portfolio income at the margin, we believe owning fixed-to-float securities is prudent and consistent with our interest-rate outlook.

Which holdings contributed to the Fund’s performance during the period surveyed?

The preferred market hit a low during the last few months of 2013, as fears of rising interest rates along with tax loss selling drove prices down. However, gains in 2014 so far have more than made up for the decline. To some degree a rebound was expected, but strong performance in the preferred market has been driven by fundamentals as credit quality has improved. The strength in the preferred market has been broad based with all industry sectors participating in the rally. However preferreds issued by real estate investment trusts (REITs) have done especially well and the Fund’s REIT exposure was a significant contributor to the Fund’s returns during the period. PS Business Parks (2.30% of Net Assets) is among the largest REIT holdings in the Fund and performed especially well over the period.

Which holdings detracted from the Fund’s performance during the period surveyed?

The Fund’s overweight to banks relative to the benchmark was a drag on performance during the period. Over the past year, banks faced some negative sentiment and lagged the broader preferred market. Even as banks continued to raise capital and reduce risk exposure (they are now much better capitalized than they were before the financial crisis), banks were weighed down by concerns about profit growth in a low interest rate environment as well as negative sentiment surrounding mortgage settlements with the government. Goldman Sachs (4.69% of Net Assets) and JPMorgan Chase (4.54% of Net Assets) were significant holdings in the Fund that lagged the broader preferred market.

What is your outlook for the preferred securities marketplace?

Although long-term interest rates in the U.S. will probably rise modestly over coming quarters, we think any upward movement will be limited by moderate GDP growth and strong investor demand for yield. Credit conditions continue to improve for most issuers of preferred securities, as earnings remain healthy and companies continue to build capital. With this backdrop, we believe prospective returns remain attractive for long-term investors.

9

DESTRA PREFERRED AND INCOME SECURITIES FUND

FUND RISK DISCLOSURES – DESTRA PREFERRED AND INCOME SECURITIES FUND

This document may contain forward-looking statements representing Destra’s, the portfolio managers’ or sub-adviser’s beliefs concerning future operations, strategies, financial results or other developments. Investors are cautioned that such forward-looking statements involve risks and uncertainties. Because these forward-looking statements are based on estimates and assumptions that are subject to significant business, economic and competitive uncertainties, many of which are beyond Destra’s, the portfolio managers’ or sub-adviser’s control or are subject to change, actual results could be materially different. There is no guarantee that such forward-looking statements will come to pass.

Some important risks of the Destra Preferred and Income Securities Fund are:

PRINCIPAL RISKS

Risk is inherent in all investing. The value of your investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly from day to day and over time. You may lose part or all of your investment in the Fund or your investment may not perform as well as other similar investments. The following is a summary description of certain risks of investing in the Fund.

Active Management Risk—The Fund is an actively managed portfolio and its success depends upon the investment skills and analytical abilities of the Fund’s sub-adviser to develop and effectively implement strategies that achieve the Fund’s investment objective. Subjective decisions made by the investment sub-adviser may cause the Fund to incur losses or to miss profit opportunities on which it may otherwise have capitalized.

Concentration Risk—The Fund intends to invest 25% or more of its total assets in securities of financial services companies. This policy makes the Fund more susceptible to adverse economic or regulatory occurrences affecting financial services companies.

Convertible Securities Risk—The market value of a convertible security often performs like that of a regular debt security; that is, if market interest rates rise, the value of a convertible security usually falls. In addition, convertible securities are subject to the risk that the issuer will not be able to pay interest or dividends when due, and their market value may change based on changes in the issuer’s credit rating or the market’s perception of the issuer’s creditworthiness. Since it derives a portion of its value from the common stock into which it may be converted, a convertible security is also subject to the same types of market and issuer risks that apply to the underlying common stock.

Credit Risk—Credit risk is the risk that an issuer of a security will be unable or unwilling to make dividend, interest and principal payments when due and the related risk that the value of a security may decline because of concerns about the issuer’s ability to make such payments. Credit risk may be heightened for the Fund because the Fund may invest in “high yield” or “high risk” securities; such securities, while generally offering higher yields than investment grade securities with similar maturities, involve greater risks, including the possibility of default or bankruptcy, and are regarded as predominantly speculative with respect to the issuer’s capacity to pay dividends and interest and repay principal.

Currency Risk—Since a portion of the Fund’s assets may be invested in securities denominated foreign currencies, changes in currency exchange rates may adversely affect the Fund’s NAV, the value of dividends and income earned, and gains and losses realized on the sale of securities.

Financial Services Companies Risk—Financial services companies are especially subject to the adverse effects of economic recession, currency exchange rates, government regulation, decreases in the availability of capital, volatile interest rates, portfolio concentrations in geographic markets and in commercial and residential real estate loans, and competition from new entrants in their fields of business.

Foreign Investment Risk—Because the Fund can invest its assets in foreign instruments, the value of Fund shares can be adversely affected by changes in currency exchange rates and political and economic developments abroad. Foreign markets may be smaller, less liquid and more volatile than the major markets in the United States, and as a result, Fund share values may be more volatile. Trading in foreign markets typically involves higher expense than trading in the United States. The Fund may have difficulties enforcing its legal or contractual rights in a foreign country. In addition, the European financial markets have recently experienced volatility and adverse trends due to concerns about economic

10

DESTRA PREFERRED AND INCOME SECURITIES FUND

FUND RISK DISCLOSURES – DESTRA PREFERRED AND INCOME SECURITIES FUND, CONTINUED

downturns in, or rising government debt levels of several European countries. These events may spread to other countries in Europe, including countries that do not use the Euro. These events may affect the value and liquidity of certain of the Fund’s investments.

General Fund Investing Risks—The Fund is not a complete investment program and you may lose money by investing in the Fund. All investments carry a certain amount of risk and there is no guarantee that the Fund will be able to achieve its investment objective. In general, the annual fund operating expenses expressed as a percentage of the Fund’s average daily net assets will change as Fund assets increase and decrease, and the Fund’s annual fund operating expenses may differ in the future. Purchase and redemption activities by Fund shareholders may impact the management of the Fund and its ability to achieve its objective. Investors in the Fund should have long-term investment perspective and be able to tolerate potentially sharp declines in value. An investment in the Fund is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency, entity or person.

High Yield Securities Risk—High yield securities generally are less liquid, have more volatile prices, and have greater credit risk than investment grade securities.

Income Risk—The income earned from the Fund’s portfolio may decline because of falling market interest rates. This can result when the Fund invests the proceeds from new share sales, or from matured or called preferred or debt securities, at market interest rates that are below the portfolio’s current earnings rate.

Interest Rate Risk—If interest rates rise, in particular, if long-term interest rates rise, the prices of fixed-rate securities held by the Fund will fall.

Investment Companies Risk—As with other investments, investments in other investment companies are subject to market and selection risk. In addition, if the Fund acquires shares of investment companies, including ones affiliated with the Fund, shareholders bear both their proportionate share of expenses in the Fund (including management and advisory fees) and, indirectly, the expenses of the investment companies. To the extent the Fund is held by an affiliated fund, the ability of the Fund itself to hold other investment companies may be limited.

Liquidity Risk—This Fund, like all open-end funds, is limited to investing up to 15% of its net assets in illiquid securities. From time to time, certain securities held by the Fund may have limited marketability and may be difficult to sell at favorable times or prices. It is possible that certain securities held by the Fund will not be able to be sold in sufficient amounts or in a sufficiently timely manner to raise the cash necessary to meet any potentially large redemption requests by fund shareholders.

Market Risk and Selection Risk—Market risk is the risk that one or more markets in which the Fund invests will go down in value, including the possibility that the markets will go down sharply and unpredictably. Selection risk is the risk that the securities selected by Fund management will underperform the markets, the relevant indices or the securities selected by other funds with similar investment objectives and investment strategies. This means you may lose money.

Non-Diversification/Limited Holding Risk—The Fund is non-diversified, which means that it may invest in the securities of fewer issuers than a diversified fund. As a result, it may be more susceptible to a single adverse economic or regulatory occurrence affecting one or more of these issuers, may experience increased volatility and may be highly concentrated in certain securities. Furthermore, because the Fund has a relatively small number of issuers, the Fund has greater susceptibility to adverse developments in one issuer or group of issuers.

Preferred Security Risk—Preferred and other subordinated securities rank lower than bonds and other debt instruments in a company’s capital structure and therefore will be subject to greater credit risk than those debt instruments. Distributions on some types of these securities may also be skipped or deferred by issuers without causing a default. Finally, some of these securities typically have special redemption rights that allow the issuer to redeem the security at par earlier than scheduled.

Investors should consider the investment objective and policies, risk considerations, charges and ongoing expenses of an investment carefully before investing. The prospectus contains this and other information relevant to an investment in the Fund. Please read the prospectus carefully before investing. To obtain a prospectus, please contact your investment representative or Destra Capital Investments LLC at 877-855-3434 or access our website at destracapital.com.

11

| DESTRA FOCUSED EQUITY FUND | ||||||

|

DISCUSSION OF FUND PERFORMANCE

|

||||||

|

Destra Focused Equity Fund’s Average Annual Total Returns as of September 30, 2014

|

||||||

| Inception Date: April 12, 2011 |

Inception Date: November 1, 2011

|

|||||

|

Life

|

Life

|

|||||

|

Share Class

|

1 year

|

3 year

|

of Fund

|

Share Class |

1 year

|

of Fund

|

|

A at NAV

|

16.25%

|

18.82%

|

13.19%

|

C at NAV

|

15.40%

|

14.56%

|

|

A with Load

|

9.59%

|

16.49%

|

11.26%

|

C with Load

|

14.40%

|

14.56%

|

|

I at NAV

|

16.66%

|

19.24%

|

13.58%

|

|||

|

S&P 500 Index

|

19.73%

|

22.99%

|

14.87%

|

S & P 500 Index

|

19.73%

|

19.40%

|

Performance shown is historical and may not be indicative of future returns. Investment returns and principal value will vary, and shares may be worth more or less at redemption than at original purchase. Performance shown is as of the date indicated, and current performance may be lower or higher than the performance data quoted. To obtain performance as of the most recent month-end, please visit www.destracapital.com or call 877.855.3434. Fund performance in the table above does not reflect the deduction of taxes a shareholder would pay on distributions or the redemption of shares. Class A shares have a maximum sales charge of 5.75% and a 12b-1 fee of .25%. Class C shares have a maximum deferred sales charge of 1.00% and a 12b-1 fee of 1.00%.

The Fund’s total returns would have been lower if certain expenses had not been waived or reimbursed by the investment adviser. Fund returns include the reinvestment of distributions.

The Destra Focused Equity Fund’s estimated total annual operating expense ratios, gross of any fee waiver or expense reimbursement, were anticipated to be 1.90% for Class A, 3.45% for Class C, and 1.54% for Class I shares. There is a voluntary fee waiver currently in place for this Fund through February 1, 2022, to the extent necessary to keep the Fund’s operating expense ratios from exceeding 1.60% for Class A, 2.35% for Class C, and 1.32% for Class I shares of average net assets per year. Some expenses fall outside of this cap and actual expenses may be higher than 1.60% for Class A, 2.35% for Class C, and 1.32% for Class I shares. Without this expense cap, actual returns would be lower.

S&P 500 Index – a capitalization weighted index of approximately 500 stocks. Indexes are unmanaged, do not reflect the deduction of fees or expenses and are not available for direct investment.

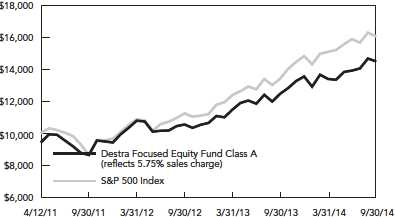

Growth of $10,000 Investment

Since Inception At Offering Price

The chart above represents historical performance of a hypothetical investment of $10,000 over the life of the Fund. Class A shares have a maximum sales charge of 5.75% imposed on purchases. Indexes are unmanaged and do not take into account fees, expenses, or other costs. Past performance does not guarantee future results. The hypothetical example does not represent the returns of any particular investment.

12

DESTRA FOCUSED EQUITY FUND

DISCUSSION OF FUND PERFORMANCE, CONTINUED

As of September 30, 2014

|

Top 10 Holdings

|

|

|

as of 9/30/14

|

% of Total Investments

|

|

Celgene Corp.

|

5.1%

|

|

eBay, Inc.

|

5.1%

|

|

Costco Wholesale Corp.

|

5.1%

|

|

HCA Holdings, Inc.

|

5.1%

|

|

Adobe Systems, Inc.

|

5.0%

|

|

Michael Kors Holdings Ltd.

|

4.9%

|

|

Nike, Inc.

|

4.9%

|

|

Oracle Corp.

|

4.9%

|

|

The Walt Disney Co.

|

4.9%

|

|

Apple, Inc.

|

4.8%

|

|

Portfolio Characteristics

|

Fund |

Index

|

|

Number of Holdings

|

20 |

502

|

|

Average Market Cap

|

$106.4 bil |

$36.9 bil

|

|

Price to Earnings Ratio

|

20.7x |

17.6x

|

|

Price to Book Ratio

|

5.6x |

4.4x

|

Holdings sectors and security types are subject to change without notice. There is no assurance that the investment process will lead to successful investing.

Glossary

Number of Holdings: The total number of individual securities held by the Fund or covered in the index.

Price to Earnings Ratio: A valuation ratio of current share price compared to its per-share operating earnings over the previous four quarters.

Average Market Capitalization: The average of market capitalization (market price multiplied by the number of shares outstanding) of the stocks in the portfolio.

Price to Book: A ratio used to compare a stock’s market value to its book value. It is calculated by dividing the current closing price of the stock by the latest quarter’s book value per share.

Portfolio Sector Allocation

as of 9/30/14 (% of Total Investments)

13

DESTRA FOCUSED EQUITY FUND

DESTRA FOCUSED EQUITY FUND PORTFOLIO MANAGER LETTER

Fund Snapshot

The Destra Focused Equity Fund (the “Fund”) is sub-advised by investment manager WestEnd Advisors (“WestEnd”). The Fund’s investment objective is to seek long-term capital appreciation.

Under normal market conditions, the Fund invests primarily (at least 80% of net assets, plus the amount of any borrowings for investment purposes) in equity securities. The Fund’s investment manager, WestEnd, believes that sector and industry performance is correlated with particular stages of the business cycle. The managers select sectors they believe will experience economic tailwinds, and avoid sectors they see as untimely. Through this process, they target high-quality, market-leading companies within the favored sectors.

The following report is their review of the Fund’s performance over the twelve months comprising the annual reporting period and an outlook for the markets the Fund invests in going forward.

How did the Fund perform during the year-ended September 30, 2014?

During the fiscal year-ended September 30, 2014, the Fund’s Class A shares had a total return of 16.25% based on Net Asset Value (“NAV”), the Class I shares had a total return of 16.66% on NAV and the Class C shares had a total return of 15.40% on NAV. During the period surveyed, the Fund’s benchmark, the S&P 500 Index, returned 19.73%.

Two important factors to consider when surveying fund returns – first, the returns include reinvestment of all distributions, and second, it is not possible to invest directly in an index. All of the Fund’s share classes have the same investment objective - long-term total return and current income.

The S&P 500 Index is a capitalization-weighted index of approximately 500 stocks. Indexes are unmanaged, do not reflect the deduction of fees or expenses and are not available for direct investment.

What were the significant events affecting the economy and market environment during the period surveyed?

For the twelve months ended September 30, 2014, U.S. economic growth remained moderate despite signals at times that growth had picked up and indications at other times that growth had weakened materially. GDP growth, for example, fell 2.1% in the first quarter of 2014 before increasing 4.6% in the second quarter of the year. An examination of the data revealed that the underlying economic trends were steadier. Removing inventory from GDP - the most volatile component of GDP - growth has been consistent near 2% year-over-year for the last four quarters. A variety of other key economic indicators like industrial production, exports and payrolls also pointed to stable, yet modest growth.

The steady economic gains in the U.S. translated into what will likely be 7.5% earnings growth for the S&P 500 Index for the 12 months ended September 30, 2014 compared to the twelve months ended September 2013. Increases in stock valuations, however, led to much stronger stock market performance as the S&P 500 Index returned 19.73% for the twelve months ended September 30, 2014.

How did the aforementioned events affect the Fund?

The Fund was positioned for this moderate growth environment with no allocation to the most economically sensitive sectors of the market, like Energy and Materials, which typically perform well in a dynamic growth environment. The Fund also had no allocation to the defensive Utilities Sector, which typically performs well when economic growth falters.

The Fund benefitted from the broad move up in stock valuations. During the period surveyed, the Fund had allocations to the Health Care and Information Technology Sectors, which were the two best performing sectors of the S&P 500 for the year ended September 30, 2014. However, the Fund also had an allocation to the Consumer Discretionary Sector, which was the worst performing sector of the S&P 500 during the period surveyed, even as consumer spending growth was solid.

Which holdings contributed to the Fund’s performance during the period surveyed?

The largest contributor to the relative performance of the Fund for the twelve months ended September 30, 2014 was its overweight of the Health Care Sector, which was the second best performing sector in the S&P 500 Index. The second largest contributor to relative performance of the Fund over the twelve month period was the avoidance of the Energy

14

DESTRA FOCUSED EQUITY FUND

DESTRA FOCUSED EQUITY FUND PORTFOLIO MANAGER LETTER, CONTINUED

Sector. The Fund had no allocation to Energy, which was the second worst performing sector in the S&P 500 Index over the period surveyed. The stocks that made the largest contribution to the Fund’s performance during the time period were Gilead Sciences, Inc. (4.82% of Net Assets) and CVS Health Corp. (4.84% of Net Assets).

Which holdings detracted from the Fund’s performance during the period surveyed?

The largest negative contributor to the relative performance of the Fund for twelve months ended September 30, 2014, was the overweight to the Consumer Discretionary Sector, which was the worst performing sector of S&P 500 Index over the twelve month period. WestEnd Advisors’ research indicates an overweight of the sector is warranted in a moderate growth environment, which is why the Fund was overweight the sector during the period. WestEnd continues to believe that the Fund’s stocks in the Consumer Discretionary Sector companies will outperform in this economic environment ahead, and the Fund remains overweight this sector.

Coach, Inc., which is no longer a holding in the Fund, was the worst performing stock in the Fund for the twelve months ended September 30, 2014. Michael Kors Holdings, Ltd. (4.90% of Net Assets) was the second worst performing stock in the Fund.

What is your outlook for the United States equity markets?

Moderate U.S. economic growth should continue to look attractive relative to other developed economies, and that will likely attract foreign capital to the U.S., which should help support U.S. equity valuations. A strong dollar will likely weigh on commodity prices, which in turn will hurt commodity-based businesses in the Energy and Materials Sectors.

Moderate economic growth in the U.S. and weaker growth abroad, along with anticipated further gains for the U.S. Dollar, warrant avoiding the most economically sensitive sectors of the market - Energy, Materials, Industrials and Financials. We also see risks in slower-growth sectors like Utilities and Telecom that have higher valuations and would be hurt by the eventual normalization of long-term interest rates. At the same time, we believe there are areas of economic strength that can be capitalized on by investors. Solid fundamentals behind health care spending should benefit Health Care companies’ sales and earnings. Similarly, Consumer Discretionary and Information Technology companies should perform well with healthy consumer and business spending.

15

DESTRA FOCUSED EQUITY FUND

FUND RISK DISCLOSURES – DESTRA FOCUSED EQUITY FUND

This document may contain forward-looking statements representing Destra’s, the portfolio managers’ or sub-adviser’s beliefs concerning future operations, strategies, financial results or other developments. Investors are cautioned that such forward-looking statements involve risks and uncertainties. Because these forward-looking statements are based on estimates and assumptions that are subject to significant business, economic and competitive uncertainties, many of which are beyond Destra’s, the portfolio managers’ or sub-adviser’s control or are subject to change, actual results could be materially different. There is no guarantee that such forward-looking statements will come to pass.

Some important risks of the Destra Focused Equity Fund are:

PRINCIPAL RISKS

Risk is inherent in all investing. The value of your investment in the Fund, as well as the amount of return you receive on your investment, may fluctuate significantly from day to day and over time. You may lose part or all of your investment in the Fund or your investment may not perform as well as other similar investments. The following is a summary description of certain risks of investing in the Fund.

Active Management Risk—The Fund is an actively managed portfolio and its success depends upon the investment skills and analytical abilities of the Fund’s sub-adviser to develop and effectively implement strategies that achieve the Fund’s investment objective. Subjective decisions made by the investment sub-adviser may cause the Fund to incur losses or to miss profit opportunities on which it may otherwise have capitalized.

Consumer Discretionary Companies Risk—Consumer discretionary companies manufacture products and provide discretionary services directly to the consumer, and the success of these companies is tied closely to the performance of the overall domestic and international economy, interest rates, competition and consumer confidence. The success of this sector depends heavily on disposable household income and consumer spending. Changes in demographics and consumer tastes can also affect the demand for, and success of, consumer discretionary products in the marketplace.

Consumer Staples Companies Risk—Consumer staples companies may be affected by the permissibility of using various product components and production methods, marketing campaigns and other factors affecting consumer demand. Tobacco companies, in particular, may be adversely affected by new laws, regulations and litigation. Consumer staples companies may also be adversely affected by changes or trends in commodity prices, which may be influenced or characterized by unpredictable factors.

Equity Securities Risk—Stock markets are volatile. The price of equity securities fluctuates based on changes in a company’s financial condition and overall market and economic conditions.

General Fund Investing Risks—The Fund is not a complete investment program and you may lose money by investing in the Fund. All investments carry a certain amount of risk and there is no guarantee that the Fund will be able to achieve its investment objective. In general, the annual fund operating expenses expressed as a percentage of the Fund’s average daily net assets will change as Fund assets increase and decrease, and the Fund’s annual fund operating expenses may differ in the future. Purchase and redemption activities by Fund shareholders may impact the management of the Fund and its ability to achieve its objective. Investors in the Fund should have long-term investment perspective and be able to tolerate potentially sharp declines in value. An investment in the Fund is not a deposit in a bank and is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency, entity or person.

Health Care Companies Risk—The Fund invests in health care companies, including those that are involved in medical services or health care, including biotechnology research and production, drugs and pharmaceuticals and health care facilities and services, and are subject to extensive competition, generic drug sales or the loss of patent protection, product liability litigation and increased government regulation. Research and development costs of bringing new drugs to market are substantial, and there is no guarantee that the product will ever come to market. Health care facility operators may be affected by the demand for services, efforts by government or insurer to limit rates, restriction of government financial assistance and competition from other providers.

Information Technology Companies Risk—Information technology companies are generally subject to the risks of rapidly changing technologies, short product life cycles, fierce competition, aggressive pricing and reduced profit margins, loss of patent, copyright and trademark protections, cyclical market patterns, evolving industry standards and frequent new product introductions. Information technology companies may be smaller and less experienced companies, with limited product lines, markets or financial resources and fewer experienced management or marketing personnel. Information technology company stocks, particularly those involved with the Internet, have experienced extreme price and volume fluctuations that often have been unrelated to their operating performance.

16

DESTRA FOCUSED EQUITY FUND

FUND RISK DISCLOSURES – DESTRA FOCUSED EQUITY FUND, CONTINUED

Investment Strategy Risk—The Fund invests in common stocks of companies that the sub-adviser believes will perform well in certain phases of the business cycle. The sub-adviser’s investment approach may be out of favor at times, causing the Fund to underperform funds that also seek capital appreciation but use different approaches to the stock selection and portfolio construction process.

Market Risk and Selection Risk—Market risk is the risk that one or more markets in which the Fund invests will go down in value, including the possibility that the markets will go down sharply and unpredictably. Selection risk is the risk that the securities selected by Fund management will underperform the markets, the relevant indices or the securities selected by other funds with similar investment objectives and investment strategies. This means you may lose money.

Non-Diversification/Limited Holdings Risk—The Fund is non-diversified, which means that it may invest in the securities of fewer issuers than a diversified fund. As a result, it may be more susceptible to a single adverse economic or regulatory occurrence affecting one or more of these issuers, may experience increased volatility and may be highly concentrated in certain issues. Furthermore, because the Fund has a relatively small number of issuers, the Fund has greater susceptibility to adverse developments in one issuer or group of issuers.

Sector Focus Risk—The Fund will typically focus its investments on companies within particular economic sectors. To the extent that it does so, developments affecting companies in those sectors will have a magnified effect on the Fund’s NAV and total return.

Investors should consider the investment objective and policies, risk considerations, charges and ongoing expenses of an investment carefully before investing. The prospectus contains this and other information relevant to an investment in the Fund. Please read the prospectus carefully before investing. To obtain a prospectus, please contact your investment representative or Destra Capital Investments LLC at 877-855-3434 or access our website at destracapital.com.

17

OVERVIEW OF FUND EXPENSES

As of September 30, 2014 (unaudited)

As a shareholder of the Destra Investment Trust II, you incur advisory fees and other Fund expenses. The expense examples below are intended to help you understand your ongoing costs (in dollars) of investing in the Funds and to compare these costs with the ongoing costs of investing in other funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period as indicated below.

Actual Expenses

The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period 3/31/14 to 9/30/14” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed annual rate of return of 5% before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid during the period. You may use this information to compare the ongoing cost of investing in a Fund and other funds by comparing this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads) or contingent deferred sales charges. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

|

Annualized

|

||||

|

Expense

|

||||

|

Ratios

|

Expenses

|

|||

|

Beginning

|

Ending

|

During the

|

Paid During

|

|

|

Account

|

Account

|

Period

|

the Period

|

|

|

Value

|

Value

|

3/31/14

|

3/31/14 to

|

|

|

3/31/14

|

9/30/14

|

to 9/30/14

|

9/30/14†

|

|

|

Destra Preferred and Income Securities Fund Class A

|

||||

|

Actual

|

$1,000.00

|

$1,038.72

|

1.50%

|

$7.67

|

|

Hypothetical (5% return before expenses)

|

1,000.00

|

1,017.55

|

1.50%

|

7.59

|

|

Destra Preferred and Income Securities Fund Class C

|

||||

|

Actual

|

1,000.00

|

1,035.32

|

2.25%

|

11.48

|

|

Hypothetical (5% return before expenses)

|

1,000.00

|

1,013.79

|

2.25%

|

11.36

|

|

Destra Preferred and Income Securities Fund Class I

|

||||

|

Actual

|

1,000.00

|

1,041.64

|

1.22%

|

6.24

|

|

Hypothetical (5% return before expenses)

|

1,000.00

|

1,018.95

|

1.22%

|

6.17

|

|

Destra Focused Equity Fund Class A

|

||||

|

Actual

|

1,000.00

|

1,082.41

|

1.60%

|

8.35

|

|

Hypothetical (5% return before expenses)

|

1,000.00

|

1,017.05

|

1.60%

|

8.09

|

|

Destra Focused Equity Fund Class C

|

||||

|

Actual

|

1,000.00

|

1,078.67

|

2.35%

|

12.25

|

|

Hypothetical (5% return before expenses)

|

1,000.00

|

1,013.29

|

2.35%

|

11.86

|

|

Destra Focused Equity Fund Class I

|

||||

|

Actual

|

1,000.00

|

1,084.41

|

1.32%

|

6.90

|

|

Hypothetical (5% return before expenses)

|

1,000.00

|

1,018.45

|

1.32%

|

6.68

|

† Expenses are calculated using the Fund’s annualized expense ratio, which includes waived fees or reimbursed expenses, multiplied by the average account value for the period, multiplied by 183/365 (to reflect the six-month period).

18

DESTRA PREFERRED AND INCOME SECURITIES FUND

PORTFOLIO OF INVESTMENTS

September 30, 2014

|

Number

|

||||

|

of

|

Moody’s

|

|||

|

Shares

|

Ratings

|

Fair Value

|

||

|

Long-Term Investments - 101.2%

|

||||

|

Preferred Stocks - 80.2%

|

||||

|

Banks - 44.8%

|

||||

|

33,810

|

Astoria Financial Corp., PFD

|

|||

|

6.500%, Series C (a)

|

Ba2

|

$ 822,935

|

||

|

Barclays Bank PLC, PFD

|

||||

|

23,500

|

7.100%, Series 3 (a)

|

Ba2

|

604,890

|

|

|

4,169

|

7.750%, Series 4 (a)

|

Ba2

|

107,810

|

|

|

16,550

|

8.125%, Series 5 (a)

|

Ba2

|

429,804

|

|

|

24,050

|

BB&T Corp., PFD

|

|||

|

5.625%, Series E (a)

|

Baa2

|

556,517

|

||

|

5,000

|

Capital One Financial Corp., PFD

|

|||

|

6.000%, Series B (a)

|

Ba1

|

116,950

|

||

|

Citigroup, Inc., PFD

|

||||

|

59,049

|

6.875%, Series K (a)

|

Ba3

|

1,555,351

|

|

|

12,150

|

7.125%, Series J (a)

|

Ba3

|

324,769

|

|

|

5,000

|

City National Corp., PFD

|

|||

|

5.500%, Series C (a)

|

Baa3

|

110,650

|

||

|

47,931

|

Fifth Third Bancorp, PFD

|

|||

|

6.625%, Series I (a)

|

Ba1

|

1,267,775

|

||

|

5,000

|

First Horizon National Corp., PFD

|

|||

|

6.200%, Series A (a)

|

Ba3

|

118,650

|

||

|

30,000

|

First Niagara Financial Group, Inc.,

|

|||

|

PFD 8.625%, Series B (a)

|

B1

|

849,000

|

||

|

49,425

|

First Republic Bank, PFD

|

|||

|

6.200%, Series B (a)

|

Baa3

|

1,224,752

|

||

|

Goldman Sachs Group, Inc., PFD

|

||||

|

8,896

|

5.950%, Series I (a)

|

Ba2

|

214,394

|

|

|

65,833

|

6.375%, Series K (a)

|

Ba2

|

1,667,550

|

|

|

21,364

|

HSBC Holdings PLC, PFD

|

|||

|

8.000%, Series 2 (a)

|

Baa2

|

569,137

|

||

|

ING Groep NV,

|

||||

|

300

|

PFD 6.375% (a)

|

Ba1

|

7,584

|

|

|

8,202

|

PFD 7.050% (a)

|

Ba1

|

208,823

|

|

|

5,000

|

PFD 7.200% (a)

|

Ba1

|

128,550

|

|

|

43,754

|

PFD 7.375% (a)

|

Ba1

|

1,117,915

|

|

|

5,000

|

JPMorgan Chase & Co., PFD

|

|||

|

6.700%, Series T (a)

|

Ba1

|

127,800

|

||

|

35,000

|

Morgan Stanley, PFD

|

|||

|

6.875%, Series F (a)

|

Ba3

|

914,550

|

||

|

39,300

|

Regions Financial Corp., PFD

|

|||

|

6.375%, Series B (a)

|

B1

|

997,434

|

||

|

14,000

|

Royal Bank of Scotland Group PLC,

|

|||

|

PFD 7.250%, Series T (a)

|

B2

|

353,500

|

||

|

15,500

|

SunTrust Banks, Inc., PFD

|

|||

|

5.875%, Series E (a)

|

Ba1

|

357,275

|

||

|

33,219

|

Texas Capital Bancshares, Inc., PFD

|

|||

|

6.500% 09/21/42

|

Ba1

|

798,585

|

||

|

20,000

|

US Bancorp, PFD

|

|||

|

6.500%, Series F (a)

|

Baa1

|

573,600

|

||

|

24,342

|

Webster Financial Corp., PFD

|

|||

|

6.400%, Series E (a)

|

Ba1

|

594,675

|

||

|

20,000

|

Wells Fargo & Co., PFD

|

|||

|

8.000%, Series J (a)

|

Baa3

|

580,400

|

||

|

Zions Bancorporation, PFD

|

||||

|

4,000

|

6.300%, Series G (a)

|

BB- (b)

|

101,360

|

|

|

8,000

|

6.950% 09/15/28

|

BB+ (b)

|

213,920

|

|

|

12,803

|

7.900%, Series F (a)

|

BB- (b)

|

358,484

|

|

|

17,975,389

|

||||

|

Diversified Financials - 6.4%

|

||||

|

32,277

|

Affiliated Managers Group, Inc., PFD

|

|||

|

6.375% 08/15/42

|

BBB (b) $

|

822,418

|

||

|

11,477

|

Deutsche Bank Contingent Capital

|

|||

|

Trust V, PFD 8.050% (a)

|

Ba3

|

326,750

|

||

|

57,211

|

HSBC Finance Corp., PFD

|

|||

|

6.360%, Series B (a)

|

Baa3

|

1,434,852

|

||

|

2,584,020

|

||||

|

Insurance - 13.5%

|

||||

|

16,050

|

Arch Capital Group Ltd., PFD

|

|||

|

6.750%, Series C (a)

|

Baa2

|

430,782

|

||

|

Aspen Insurance Holdings Ltd.,

|

||||

|

12,286

|

PFD 5.950% (a)

|

Ba1

|

306,782

|

|

|

2,714

|

PFD 7.250% (a)

|

Ba1

|

70,808

|

|

|

44,000

|

Axis Capital Holdings Ltd., PFD

|

|||

|

6.875%, Series C (a)

|

Baa3

|

1,140,040

|

||

|

34,501

|

Delphi Financial Group, Inc., PFD

|

|||

|

7.376% 05/15/37

|

BBB- (b)

|

867,918

|

||

|

Endurance Specialty Holdings Ltd.,

|

||||

|

18,807

|

PFD 7.500%, Series B (a)

|

Ba1

|

486,537

|

|

|

3,681

|

PFD 7.750%, Series A (a)

|

Ba1

|

96,111

|

|

|

10,000

|

Hartford Financial Services Group,

|

|||

|

Inc. (The), PFD

|

||||

|

7.875% 04/15/42

|

Ba1

|

295,900

|

||

|

PartnerRe Ltd., PFD

|

||||

|

11,922

|

5.875%, Series F (a)

|

Baa2

|

286,128

|

|

|

15,500

|

7.250%, Series E (a)

|

Baa2

|

416,485

|

|

|

24,887

|

Principal Financial Group, Inc., PFD

|

|||

|

6.518%, Series B (a)

|

Ba1

|

633,623

|

||

|

8,897

|

RenaissanceRe Holdings Ltd., PFD

|

|||

|

5.375%, Series E (a)

|

Baa2

|

194,488

|

||

|

8,223

|

WR Berkley Corp., PFD

|

|||

|

5.625% 04/30/53

|

Baa3

|

191,760

|

||

|

5,417,362

|

||||

|

Real Estate - 9.2%

|

||||

|

10,430

|

CubeSmart, PFD

|

|||

|

7.750%, Series A (a)

|

Baa3

|

275,352

|

||

|

16,667

|

Duke Realty Corp., PFD

|

|||

|

6.600%, Series L (a)

|

Baa3

|

418,675

|

||

|

35,000

|

Equity Commonwealth, PFD

|

|||

|

7.250%, Series E (a)

|

Ba1

|

900,550

|

||

|

Kimco Realty Corp., PFD

|

||||

|

1,500

|

5.500%, Series J (a)

|

Baa2

|

34,665

|

|

|

13,012

|

6.900%, Series H (a)

|

Baa2

|

342,866

|

|

|

National Retail Properties, Inc., PFD

|

||||

|

4,100

|

5.700%, Series E (a)

|

Baa2

|

97,785

|

|

|

4,230

|

6.625%, Series D (a)

|

Baa2

|

109,472

|

|

|

PS Business Parks, Inc., PFD

|

||||

|

26,100

|

5.750%, Series U (a)

|

Baa2

|

596,385

|

|

|

8,839

|

6.000%, Series T (a)

|

Baa2

|

212,578

|

|

|

4,448

|

6.875%, Series R (a)

|

Baa2

|

114,180

|

|

|

17,063

|

Realty Income Corp., PFD

|

|||

|

6.625%, Series F (a)

|

Baa2

|

446,197

|

||

|

5,560

|

Weingarten Realty Investors, PFD

|

|||

|

6.500%, Series F (a)

|

Baa3

|

140,168

|

||

|

3,688,873

|

||||

|

Utilities - 6.3%

|

||||

|

4,000

|

Dominion Resources, Inc., PFD

|

|||

|

8.375% 06/15/64, Series A

|

Baa3

|

100,760

|

||

|

9,648

|

Entergy Louisiana LLC,

|

|||

|

PFD 6.950% (a)

|

Baa3

|

972,639

|

The accompanying notes are an integral part of these financial statements.

19

DESTRA PREFERRED AND INCOME SECURITIES FUND

PORTFOLIO OF INVESTMENTS, CONTINUED

September 30, 2014

|

Number

|

||||

|

of Shares/

|

Moody’s

|

|||

|

Par Value

|

Ratings

|

Fair Value

|

||

|

Utilities (continued)

|

||||

|

8,000

|

Integrys Energy Group, Inc., PFD

|

|||

|

6.000% 08/01/73

|

Baa1

|

$ 205,120

|

||

|

10,000

|

PPL Capital Funding, Inc., PFD

|

|||

|

5.900% 04/30/73, Series B

|

Ba1

|

243,800

|

||

|

21,825

|

SCANA Corp., PFD

|

|||

|

7.700% 01/30/65, Series A

|