UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

(Mark One)

| ☐ | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☒ | ANNUAL REPORT PURSUANT TO

SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the fiscal year ended December 31, 2016 |

OR

| ☐ | TRANSITION REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ☐ | SHELL COMPANY REPORT PURSUANT

TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 Date of event requiring this shell company report |

For the transition period from ________________ to ________________

Commission file number: 001-35129

ARCOS DORADOS HOLDINGS INC.

(Exact name of Registrant as specified in its charter)

British Virgin Islands

(Jurisdiction of incorporation or organization)

Dr. Luis Bonavita 1294, Office 501

Montevideo, Uruguay, 11300 WTC Free Zone

(Address of principal executive offices)

Juan David Bastidas

Chief Legal Officer

Arcos Dorados Holdings Inc.

Dr. Luis Bonavita 1294, 5th floor, Office 501, WTC Free Zone

Montevideo, Uruguay 11300

Telephone: +598 2626-3000

Fax: +598 2626-3018

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

Name of each exchange on which registered |

| Class A shares, no par value | New York Stock Exchange |

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital stock or common stock as of the close of the period covered by the annual report.

Class A shares: 130,711,224

Class B shares: 80,000,000

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

☒ Yes ☐ No

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

☐ Yes ☒ No

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

☒ Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

☒ Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or an emerging growth company. See definition of “large accelerated filer, ” accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ☐ | Accelerated filer ☒ | Non-accelerated filer ☐ | Emerging growth company ☐ |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act.

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

| U.S. GAAP ☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board ☐ | Other ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow.

☐ Item 17 ☐ Item 18

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

☐ Yes ☒ No

ARCOS DORADOS HOLDINGS INC.

____________________

Page

i

| ITEM 10. ADDITIONAL INFORMATION | 101 |

ii

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

All references to “U.S. dollars,” “dollars,” “U.S.$” or “$” are to the U.S. dollar. All references to “Argentine pesos” or “ARS$” are to the Argentine peso. All references to “Brazilian reais” or “R$” are to the Brazilian real. All references to “Mexican pesos” or “Ps.” are to the Mexican peso. All references to “Venezuelan bolívares” or “Bs.” are to the Venezuelan bolívar, the legal currency of Venezuela. See “Item 3. Key Information—A. Selected Financial Data—Exchange Rates and Exchange Controls” for information regarding exchange rates for the Argentine, Brazilian and Mexican currencies since January 1, 2012.

Definitions

In this annual report, unless the context otherwise requires, all references to “Arcos Dorados,” the “Company,” “we,” “our,” “ours,” “us” or similar terms refer to Arcos Dorados Holdings Inc., together with its subsidiaries. All references to “systemwide” refer only to the system of McDonald’s-branded restaurants operated by us or our franchisees in 20 countries and territories in Latin America and the Caribbean, including Argentina, Aruba, Brazil, Chile, Colombia, Costa Rica, Curaçao, Ecuador, French Guiana, Guadeloupe, Martinique, Mexico, Panama, Peru, Puerto Rico, Trinidad and Tobago, Uruguay, the U.S. Virgin Islands of St. Croix and St. Thomas, and Venezuela, which we refer to as the “Territories,” and do not refer to the system of McDonald’s-branded restaurants operated by McDonald’s Corporation, its affiliates or its franchisees (other than us).

We own our McDonald’s franchise rights pursuant to a Master Franchise Agreement for all of the Territories, except Brazil, which we refer to as the MFA, and a separate, but substantially identical, Master Franchise Agreement for Brazil, which we refer to as the Brazilian MFA. We refer to the MFA and the Brazilian MFA, as amended or otherwise modified to date, collectively as the MFAs. We commenced operations on August 3, 2007, as a result of our purchase of McDonald’s operations and real estate in the Territories (except for Trinidad and Tobago), which we refer to collectively as the “McDonald’s LatAm” business, and the acquisition of McDonald’s franchise rights pursuant to the MFAs, which together with the purchase of the McDonald’s LatAm business, we refer to as the “Acquisition.”

Financial Statements

We maintain our books and records in U.S. dollars and prepare our financial statements in accordance with accounting principles and standards generally accepted in the United States, or “U.S. GAAP.”

The financial information contained in this annual report includes our consolidated financial statements at December 31, 2016 and 2015 and for the years ended December 31, 2016, 2015 and 2014, which have been audited by Pistrelli, Henry Martin y Asociados S.R.L., member firm of Ernst & Young Global, as stated in their report included elsewhere in this annual report.

We were incorporated on December 9, 2010 as a direct, wholly owned subsidiary of Arcos Dorados Limited, the prior holding company for the Arcos Dorados business. On December 13, 2010, Arcos Dorados Limited effected a downstream merger into and with us, with us as the surviving entity. The merger was accounted for as a reorganization of entities under common control in a manner similar to a pooling of interest and the consolidated financial statements reflect the historical consolidated operations of Arcos Dorados Limited as if the reorganization structure had existed since Arcos Dorados Limited was incorporated in July 2006.

Our fiscal year ends December 31. References in this annual report to a fiscal year, such as “fiscal year 2016,” relate to our fiscal year ended on December 31 of that calendar year.

Operating Data

In January 2013, we made certain organizational changes in the structure of our geographical divisions in order to balance their relative weight in terms of number of restaurants and revenues. As a result of the reorganization effective January 1, 2013, Colombia and Venezuela, which were part of the South Latin America division, or “SLAD,” became part of the Caribbean division with headquarters located in Colombia. Therefore, from the beginning of 2013, SLAD is comprised of Argentina, Chile, Ecuador, Peru and Uruguay, and the Caribbean division is comprised of Aruba, Colombia, Curaçao, French Guiana, Guadeloupe, Martinique, Puerto Rico, Trinidad and Tobago, the U.S. Virgin Islands of St. Croix and St. Thomas, and Venezuela. Our other geographical divisions are

iii

Brazil and the North Latin America division, or “NOLAD,” consisting of Costa Rica, Mexico and Panama. In accordance with ASC 280, Segment Reporting, we began reporting the results of the revised structure of our geographical divisions on our segment financial reporting in the first quarter of fiscal year 2013. In accordance with ASC 280, Segment Reporting, we have restated our comparative segment information as of and for the year ended December 31, 2012 based on the structure prevailing since January 1, 2013.

As of January 1, 2016, senior management made changes in the allocation of certain expenses across operating segments. We made corresponding changes in the allocation of these expenses in order to align our segment financial reporting with the new allocation used by senior management as of that date. In accordance with ASC 280, Segment Reporting, we have restated our comparative segment information as of and for the years ended December 31, 2015 and 2014 based on the new allocation of expenses prevailing since January 1, 2016.

We operate McDonald’s-branded restaurants under two different operating formats: those directly operated by us, or “Company-operated” restaurants, and those operated by franchisees, or “franchised” restaurants. All references to “restaurants” are to our freestanding, food court, in-store and mall store restaurants and do not refer to our McCafé locations or Dessert Centers. Systemwide data represents measures for both our Company-operated restaurants and our franchised restaurants.

We are the majority stakeholder in three joint ventures with third parties that collectively own 18 restaurants. We consider these restaurants to be Company-operated restaurants. We also have granted developmental licenses to 11 restaurants. Developmental licensees own or lease the land and buildings on which their restaurants are located and pay a franchise fee to us in addition to the continuing franchise fee due to McDonald’s. We consider these restaurants to be franchised restaurants.

Market Share and Other Information

Market data and certain industry forecast data used in this annual report were obtained from internal reports and studies, where appropriate, as well as estimates, market research, publicly available information (including information available from the United States Securities and Exchange Commission, or the SEC, website) and industry publications, including Millward Brown Optimor, the United Nations Economic Commission for Latin America and the Caribbean and the CIA World Factbook. Industry publications generally state that the information they include has been obtained from sources believed to be reliable, but that the accuracy and completeness of such information is not guaranteed. Similarly, internal reports and studies, estimates and market research, which we believe to be reliable and accurately extracted by us for use in this annual report, have not been independently verified. However, we believe such data is accurate and agree that we are responsible for the accurate extraction of such information from such sources and its correct reproduction in this annual report.

Basis of Consolidation

The accompanying consolidated financial statements have been prepared on the accrual basis of accounting and include the accounts of the Company and its subsidiaries. All significant intercompany balances and transactions have been eliminated in consolidation.

Rounding

We have made rounding adjustments to some of the figures included in this annual report. Accordingly, numerical figures shown as totals in some tables may not be an arithmetic aggregation of the figures that preceded them.

This annual report contains statements that constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Many of the forward-looking statements contained in this annual report can be identified by the use of forward-looking words such as “anticipate,” “believe,” “could,” “expect,” “should,” “plan,” “intend,” “estimate” and “potential,” among others.

Forward-looking statements appear in a number of places in this annual report and include, but are not limited to, statements regarding our intent, belief or current expectations. Forward-looking statements are based on our

iv

management’s beliefs and assumptions and on information currently available to our management. Such statements are subject to risks and uncertainties, and actual results may differ materially from those expressed or implied in the forward-looking statements due to of various factors, including, but not limited to, those identified in “Item 3. Key Information—D. Risk Factors” in this annual report. These risks and uncertainties include factors relating to:

| · | general economic, political, demographic and business conditions in Latin America and the Caribbean; |

| · | fluctuations in inflation and exchange rates in Latin America and the Caribbean; |

| · | our ability to implement our growth strategy; |

| · | the success of operating initiatives, including advertising and promotional efforts and new product and concept development by us and our competitors; |

| · | our ability to compete and conduct our business in the future; |

| · | changes in consumer tastes and preferences, including changes resulting from concerns over nutritional or safety aspects of beef, poultry, french fries or other foods or the effects of health pandemics and food-borne illnesses such as “mad cow” disease and avian influenza or “bird flu,” and changes in spending patterns and demographic trends, such as the extent to which consumers eat meals away from home; |

| · | the availability, location and lease terms for restaurant development; |

| · | our intention to focus on our restaurant reimaging plan; |

| · | our franchisees, including their business and financial viability and the timely payment of our franchisees’ obligations due to us and to McDonald’s; |

| · | our ability to comply with the requirements of the MFAs, including McDonald’s standards; |

| · | our decision to own and operate restaurants or to operate under franchise agreements; |

| · | the availability of qualified restaurant personnel for us and for our franchisees, and the ability to retain such personnel; |

| · | changes in commodity costs, labor, supply, fuel, utilities, distribution and other operating costs; |

| · | changes in labor laws; |

| · | our ability, if necessary, to secure alternative distribution of supplies of food, equipment and other products to our restaurants at competitive rates and in adequate amounts, and the potential financial impact of any interruptions in such distribution; |

| · | changes in government regulation; |

| · | material changes in tax legislation; |

| · | other factors that may affect our financial condition, liquidity and results of operations; and |

| · | other risk factors discussed under “Item 3. Key Information—D. Risk Factors.” |

Forward-looking statements speak only as of the date they are made, and we do not undertake any obligation to update them in light of new information or future developments or to release publicly any revisions to these statements in order to reflect later events or circumstances or to reflect the occurrence of unanticipated events.

v

We are incorporated under the laws of the British Virgin Islands with limited liability. We are incorporated in the British Virgin Islands because of certain benefits associated with being a British Virgin Islands company, such as political and economic stability, an effective judicial system, a favorable tax system, the absence of exchange control or currency restrictions, and the availability of professional and support services. However, the British Virgin Islands has a less developed body of securities laws as compared to the United States and provides protections for investors to a significantly lesser extent. In addition, British Virgin Islands companies may not have standing to sue before the federal courts of the United States.

A majority of our directors and officers, as well as certain of the experts named herein, reside outside of the United States. A substantial portion of our assets and several of such directors, officers and experts are located principally in Argentina, Brazil and Uruguay. As a result, it may not be possible for investors to effect service of process outside Argentina, Brazil and Uruguay upon such directors or officers, or to enforce against us or such parties in courts outside Argentina, Brazil and Uruguay judgments predicated solely upon the civil liability provisions of the federal securities laws of the United States or other non-Argentine, Brazilian or Uruguayan regulations, as applicable. In addition, local counsel to the Company have advised that there is doubt as to whether the courts of Argentina, Brazil or Uruguay would enforce in all respects, to the same extent and in as timely a manner as a U.S. court or non-Argentine, Brazilian or Uruguayan court, an original action predicated solely upon the civil liability provisions of the U.S. federal securities laws or other non-Argentine, Brazilian or Uruguayan regulations, as applicable; and that the enforceability in Argentine, Brazilian or Uruguayan courts of judgments of U.S. courts or non-Argentine, Brazilian or Uruguayan courts predicated upon the civil liability provisions of the U.S. federal securities laws or other non-Argentine, Brazilian or Uruguayan regulations, as applicable, will be subject to compliance with certain requirements under Argentine, Brazilian or Uruguayan law, including the condition that any such judgment does not violate Argentine, Brazilian or Uruguayan public policy.

We have been advised by Maples and Calder, our counsel as to British Virgin Islands law, that the United States and the British Virgin Islands do not have a treaty providing for reciprocal recognition and enforcement of judgments of courts of the United States in civil and commercial matters and that a final judgment for the payment of money rendered by any general or state court in the United States based on civil liability, whether or not predicated solely upon the U.S. federal securities laws, would not be automatically enforceable in the British Virgin Islands. We have been advised by Maples and Calder that a final and conclusive judgment obtained in U.S. federal or state courts under which a sum of money is payable (i.e., not being a sum claimed by a revenue authority for taxes or other charges of a similar nature by a governmental authority, or in respect of a fine or penalty or multiple or punitive damages) may be the subject of an action on a debt in the court of the British Virgin Islands under British Virgin Islands common law.

vi

ITEM 1. IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

| A. | Directors and Senior Management |

Not applicable.

| B. | Advisers |

Not applicable.

| C. | Auditors |

Not applicable.

ITEM 2. OFFER STATISTICS AND EXPECTED TIMETABLE

| A. | Offer Statistics |

Not applicable.

| B. | Method and Expected Timetable |

Not applicable.

| A. | Selected Financial Data |

The selected balance sheet data as of December 31, 2016 and 2015 and the income statement data for the years ended December 31, 2016, 2015 and 2014 of Arcos Dorados Holdings Inc. are derived from the consolidated financial statements included elsewhere in this annual report, which have been audited by Pistrelli, Henry Martin y Asociados S.R.L., member firm of Ernst & Young Global. The selected balance sheet data as of December 31, 2014, 2013 and 2012 and the income statement data for the years ended December 31, 2013 and 2012 of Arcos Dorados Holdings Inc. are derived from consolidated financial statements audited by Pistrelli, Henry Martin y Asociados S.R.L., which are not included herein.

In January 2013, we made certain organizational changes in the structure of our geographical divisions in order to balance their relative weight in terms of number of restaurants and revenues. As a result of the reorganization effective January 1, 2013, Colombia and Venezuela, which were part of SLAD, became part of the Caribbean division with headquarters located in Colombia. Therefore, from the beginning of 2013, SLAD is comprised of Argentina, Chile, Ecuador, Peru and Uruguay, and the Caribbean division is comprised of Aruba, Colombia, Curaçao, French Guiana, Guadeloupe, Martinique, Puerto Rico, Trinidad and Tobago, the U.S. Virgin Islands of St. Croix and St. Thomas, and Venezuela. Our other geographical divisions are Brazil and NOLAD, consisting of Costa Rica, Mexico and Panama. In accordance with ASC 280 Segment Reporting, we began reporting the results of the revised structure of our geographical divisions on our segment financial reporting in the first quarter of fiscal year 2013. In accordance with ASC 280, Segment Reporting, we have restated our comparative segment information as of and for the year ended December 31, 2012 based on the structure prevailing since January 1, 2013.

As of January 1, 2016, senior management made changes in the allocation of certain expenses across operating segments. We made corresponding changes in the allocation of these expenses in order to align our segment financial reporting with the new allocation used by senior management as of that date. In accordance with ASC 280, Segment Reporting, we have restated our comparative segment information as of and for the years ended December 31, 2015 and 2014 based on the new allocation of expenses prevailing since January 1, 2016.

We were incorporated on December 9, 2010 as a direct, wholly owned subsidiary of Arcos Dorados Limited, the prior holding company for the Arcos Dorados business. On December 13, 2010, Arcos Dorados Limited effected a downstream merger into and with us, with us as the surviving entity. The merger was accounted for as a reorganization of entities under common control in a manner similar to a pooling of interest and the consolidated financial statements reflect the historical consolidated operations of Arcos Dorados Limited as if the reorganization structure had existed since Arcos Dorados Limited was incorporated in July 2006. We did not commence operations until the Acquisition on August 3, 2007.

1

We maintain our books and records in U.S. dollars and prepare our consolidated financial statements in accordance with U.S. GAAP. This financial information should be read in conjunction with “Presentation of Financial and Other Information,” “Item 5. Operating and Financial Review and Prospects” and our consolidated financial statements, including the notes thereto, included elsewhere in this annual report.

| For the Years Ended December 31, | ||||||||||||||||||||

| 2016 | 2015 (1) | 2014 (1) | 2013 (1) | 2012 (1) | ||||||||||||||||

| (in thousands of U.S. dollars, except for per share data) | ||||||||||||||||||||

| Income Statement Data: | ||||||||||||||||||||

| Sales by Company-operated restaurants | $ | 2,803,334 | $ | 2,930,379 | $ | 3,504,302 | $ | 3,859,883 | $ | 3,634,371 | ||||||||||

| Revenues from franchised restaurants | 125,296 | 122,361 | 146,763 | 173,427 | 163,023 | |||||||||||||||

| Total revenues | 2,928,630 | 3,052,740 | 3,651,065 | 4,033,310 | 3,797,394 | |||||||||||||||

| Company-operated restaurant expenses: | ||||||||||||||||||||

| Food and paper | (1,012,976 | ) | (1,037,487 | ) | (1,243,907 | ) | (1,350,515 | ) | (1,269,146 | ) | ||||||||||

| Payroll and employee benefits | (607,082 | ) | (660,773 | ) | (791,677 | ) | (814,112 | ) | (753,120 | ) | ||||||||||

| Occupancy and other operating | (752,428 | ) | (793,622 | ) | (939,481 | ) | (1,055,188 | ) | (984,004 | ) | ||||||||||

| Royalty fees | (142,777 | ) | (149,089 | ) | (173,663 | ) | (188,885 | ) | (180,547 | ) | ||||||||||

| Franchised restaurants—occupancy | (55,098 | ) | (54,242 | ) | (63,939 | ) | (63,273 | ) | (56,057 | ) | ||||||||||

| General and administrative expenses | (221,075 | ) | (270,680 | ) | (272,065 | ) | (317,745 | ) | (314,619 | ) | ||||||||||

| Other operating income (expenses), net | 41,386 | 6,560 | (95,476 | ) | (15,070 | ) | (3,261 | ) | ||||||||||||

| Total operating costs and expenses | (2,750,050 | ) | (2,959,333 | ) | (3,580,208 | ) | (3,804,788 | ) | (3,560,754 | ) | ||||||||||

| Operating income | 178,580 | 93,407 | 70,857 | 228,522 | 236,640 | |||||||||||||||

| Net interest expense | (66,880 | ) | (64,407 | ) | (72,750 | ) | (88,156 | ) | (54,247 | ) | ||||||||||

| Loss from derivative instruments | (3,065 | ) | (2,894 | ) | (685 | ) | (4,141 | ) | (891 | ) | ||||||||||

| Foreign currency exchange results | 32,354 | (54,032 | ) | (74,117 | ) | (38,783 | ) | (18,420 | ) | |||||||||||

| Other non-operating (expenses) income | (2,360 | ) | (627 | ) | 146 | (848 | ) | (2,119 | ) | |||||||||||

| Income (loss) before income taxes | 138,629 | (28,553 | ) | (76,549 | ) | 96,594 | 160,963 | |||||||||||||

| Income tax expense | (59,641 | ) | (22,816 | ) | (32,479 | ) | (42,722 | ) | (46,375 | ) | ||||||||||

| Net income (loss) | 78,988 | (51,369 | ) | (109,028 | ) | 53,872 | 114,588 | |||||||||||||

| Less: Net income attributable to non-controlling interests | (178 | ) | (264 | ) | (305 | ) | (18 | ) | (256 | ) | ||||||||||

| Net income (loss) attributable to Arcos Dorados Holdings Inc. | 78,810 | (51,633 | ) | (109,333 | ) | 53,854 | 114,332 | |||||||||||||

| Earnings (Loss) per share: | ||||||||||||||||||||

| Basic net income (loss) per common share attributable to Arcos Dorados | $ | 0.37 | $ | (0.25 | ) | $ | (0.52 | ) | $ | 0.26 | $ | 0.55 | ||||||||

| Diluted net income (loss) per common share attributable to Arcos Dorados | $ | 0.37 | $ | (0.25 | ) | $ | (0.52 | ) | $ | 0.26 | $ | 0.55 | ||||||||

2

| As of December 31, | ||||||||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||||

| (in thousands of U.S. dollars, except for share data) | ||||||||||||||||||||

| Balance Sheet Data(2): | ||||||||||||||||||||

| Cash and cash equivalent | $ | 194,803 | $ | 112,519 | $ | 139,030 | $ | 175,648 | $ | 184,851 | ||||||||||

| Total current assets | 445,190 | 378,996 | 447,196 | 666,451 | 601,498 | |||||||||||||||

| Property and equipment, net | 847,966 | 833,357 | 1,092,994 | 1,244,311 | 1,176,350 | |||||||||||||||

| Total non-current assets | 1,059,863 | 1,024,206 | 1,347,584 | 1,513,808 | 1,447,665 | |||||||||||||||

| Total assets | 1,505,053 | 1,403,202 | 1,794,780 | 2,180,259 | 2,049,163 | |||||||||||||||

| Accounts payable | 217,914 | 187,685 | 220,337 | 311,060 | 244,365 | |||||||||||||||

| Short-term debt and current portion of long-term debt | 28,099 | 163,740 | 38,684 | 12,276 | 2,202 | |||||||||||||||

| Total current liabilities | 548,308 | 577,314 | 542,066 | 659,156 | 578,274 | |||||||||||||||

| Long-term debt, excluding current portion | 551,580 | 491,327 | 761,080 | 771,171 | 649,968 | |||||||||||||||

| Total non-current liabilities | 605,169 | 538,998 | 795,127 | 825,804 | 724,579 | |||||||||||||||

| Total liabilities | 1,153,477 | 1,116,312 | 1,337,193 | 1,484,960 | 1,302,853 | |||||||||||||||

| Total common stock | 506,884 | 504,772 | 498,616 | 491,735 | 484,569 | |||||||||||||||

| Total equity | 351,576 | 286,890 | 457,587 | 695,299 | 746,310 | |||||||||||||||

| Total liabilities and equity | 1,505,053 | 1,403,202 | 1,794,780 | 2,180,259 | 2,049,163 | |||||||||||||||

| Shares outstanding | 210,711,224 | 210,538,896 | 210,216,043 | 209,867,426 | 209,529,412 | |||||||||||||||

| For the Years Ended December 31, | ||||||||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012(3) | ||||||||||||||||

| (in thousands of U.S. dollars, except percentages) | ||||||||||||||||||||

| Other Data: | ||||||||||||||||||||

| Total Revenues | ||||||||||||||||||||

| Brazil | $ | 1,333,237 | $ | 1,361,989 | $ | 1,816,046 | $ | 1,842,324 | $ | 1,797,556 | ||||||||||

| Caribbean division(4) | 409,671 | 398,144 | 594,220 | 830,447 | 754,730 | |||||||||||||||

| NOLAD | 363,965 | 367,364 | 385,114 | 407,772 | 384,041 | |||||||||||||||

| SLAD | 821,757 | 925,243 | 855,685 | 952,767 | 861,067 | |||||||||||||||

| Total | 2,928,630 | 3,052,740 | 3,651,065 | 4,033,310 | 3,797,394 | |||||||||||||||

| Operating Income(5) | ||||||||||||||||||||

| Brazil | $ | 122,636 | $ | 116,820 | $ | 155,799 | $ | 188,445 | $ | 193,339 | ||||||||||

| Caribbean division(4) | (12,392 | ) | (40,102 | ) | (91,859 | ) | 37,837 | 40,692 | ||||||||||||

| NOLAD | 45,145 | 8,710 | (9,150 | ) | (5,314 | ) | (5,557 | ) | ||||||||||||

| SLAD | 66,359 | 78,022 | 62,768 | 84,324 | 74,824 | |||||||||||||||

| Corporate and others and purchase price allocation | (43,168 | ) | (70,043 | ) | (46,701 | ) | (76,770 | ) | (66,658 | ) | ||||||||||

| Total | 178,580 | 93,407 | 70,857 | 228,522 | 236,640 | |||||||||||||||

| Operating Margin(5)(6) | ||||||||||||||||||||

| Brazil | 9.2 | % | 8.6 | % | 8.6 | % | 10.2 | % | 10.8 | % | ||||||||||

| Caribbean division(4) | (3.0 | ) | (10.1 | ) | (15.5 | ) | 4.6 | 5.4 | ||||||||||||

| NOLAD | 12.4 | 2.4 | (2.4 | ) | (1.3 | ) | (1.4 | ) | ||||||||||||

| SLAD | 8.1 | 8.4 | 7.3 | 8.9 | 8.7 | |||||||||||||||

| Total | 6.1 | 3.1 | 1.9 | 5.7 | 6.2 | |||||||||||||||

3

| Adjusted EBITDA(5)(7) | ||||||||||||||||||||

| Brazil | $ | 168,076 | $ | 174,102 | $ | 220,711 | $ | 245,957 | $ | 240,954 | ||||||||||

| Caribbean division(4) | 18,049 | 2,059 | (11,284 | ) | 67,180 | 69,109 | ||||||||||||||

| NOLAD | 36,288 | 31,424 | 25,035 | 27,397 | 26,738 | |||||||||||||||

| SLAD | 76,327 | 100,718 | 82,859 | 105,495 | 93,756 | |||||||||||||||

| Corporate and others | (60,295 | ) | (78,132 | ) | (65,647 | ) | (101,562 | ) | (89,996 | ) | ||||||||||

| Total | 238,445 | 230,171 | 251,674 | 344,467 | 340,561 | |||||||||||||||

| Adjusted EBITDA Margin(5)(8) | ||||||||||||||||||||

| Brazil | 12.6 | % | 12.8 | % | 12.2 | % | 13.4 | % | 13.4 | % | ||||||||||

| Caribbean division(4) | 4.4 | 0.5 | (1.9) | 8.1 | 9.2 | |||||||||||||||

| NOLAD | 10.0 | 8.6 | 6.5 | 6.7 | 7.0 | |||||||||||||||

| SLAD | 9.3 | 10.9 | 9.7 | 11.1 | 10.9 | |||||||||||||||

| Total | 8.1 | 7.5 | 6.9 | 8.5 | 9.0 | |||||||||||||||

| Other Financial Data: | ||||||||||||||||||||

| Working capital(9) | $ | (103,118 | ) | $ | (198,318 | ) | $ | (94,870 | ) | $ | 7,295 | $ | 23,224 | |||||||

| Capital expenditures(10) | 92,282 | 92,055 | 170,638 | 313,786 | 300,482 | |||||||||||||||

| Dividends declared per common share | — | — | 0.24 | 0.24 | 0.24 | |||||||||||||||

| As of December 31, | |||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||

| Number of systemwide restaurants | 2,156 | 2,141 | 2,121 | 2,062 | 1,948 | ||||||||||

| Brazil | 902 | 883 | 866 | 812 | 731 | ||||||||||

| Caribbean division | 353 | 356 | 359 | 365 | 353 | ||||||||||

| NOLAD | 517 | 518 | 513 | 507 | 503 | ||||||||||

| SLAD | 384 | 384 | 383 | 378 | 361 | ||||||||||

| Number of Company-operated restaurants | 1,553 | 1,588 | 1,577 | 1,538 | 1,453 | ||||||||||

| Brazil | 584 | 615 | 614 | 583 | 533 | ||||||||||

| Caribbean division | 266 | 267 | 270 | 270 | 259 | ||||||||||

| NOLAD | 365 | 364 | 352 | 344 | 335 | ||||||||||

| SLAD | 338 | 342 | 341 | 341 | 326 | ||||||||||

| Number of franchised restaurants | 603 | 553 | 544 | 524 | 495 | ||||||||||

| Brazil | 318 | 268 | 252 | 229 | 198 | ||||||||||

| Caribbean division | 87 | 89 | 89 | 95 | 94 | ||||||||||

| NOLAD | 152 | 154 | 161 | 163 | 168 | ||||||||||

| SLAD | 46 | 42 | 42 | 37 | 35 | ||||||||||

____________________

| (1) | Due to certain changes in accounting for expenses in 2016, certain reclassifications have been made from “Occupancy and other operating expenses” to “Payroll and employee benefits” in the Income Statement Data for the fiscal years ended December 31, 2015 and 2014 in order to ensure comparability with our results for the fiscal year ended December 31, 2016. Income Statement Data for the fiscal years ended December 31, 2013 and 2012 has not been restated and is therefore not comparable to 2016, 2015 and 2014. See Note 2 to our consolidated financial statements for additional information. |

| (2) | Due to changes in accounting standards, certain reclassifications have been made from “Non-current assets” to “Short-term debt and current portion of long-term debt” and to “Long-term debt, excluding current portion” in the Balance Sheet Data as of December 31, 2015. Balance Sheet Data as of December 31, 2014, 2013 and 2012 has not been restated and is therefore not comparable to the Balance Sheet Data as of December 31, 2016 and 2015. See Note 2 to our consolidated financial statements for additional information. |

4

| (3) | Segment information as of and for the year ended December 31, 2012 is presented based on the segment structure prevailing as of and from January 1, 2013. See “Presentation of Financial and Other Information—Operating Data.” |

| (4) | Currency devaluations in Venezuela have had a significant effect on our income statements and have impacted the comparability of our income statements in 2016 and 2015 as compared to 2014, 2013 and 2012. See “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Foreign Currency Translation—Venezuela.” |

| (5) | Segment information for the years ended December 31, 2016, 2015 and 2014 is presented based on the allocation of expenses prevailing as of January 1, 2016. See “Presentation of Financial and Other Information—Operating Data.” Segment information for the years ended December 31, 2013 and 2012 has not been restated and is therefore not comparable to the segment information for the years ended December 31, 2016, 2015 and 2014. |

| (6) | Operating margin is operating income divided by total revenues, expressed as a percentage. |

| (7) | Adjusted EBITDA is a measure of our performance that is reviewed by our management. Adjusted EBITDA does not have a standardized meaning and, accordingly, our definition of Adjusted EBITDA may not be comparable to Adjusted EBITDA as used by other companies. Total Adjusted EBITDA is a non-GAAP measure. For our definition of Adjusted EBITDA, see “Item 5. Operating and Financial Review and Prospects—A. Operating Results—Key Business Measures” |

| (8) | Adjusted EBITDA margin is Adjusted EBITDA divided by total revenues, expressed as a percentage. |

| (9) | Working capital equals current assets minus current liabilities. |

| (10) | Includes property and equipment expenditures and purchase of restaurant businesses paid at the acquisition date. |

Presented below is the reconciliation between net income and Adjusted EBITDA on a consolidated basis:

| For the Years Ended December 31, | ||||||||||||||||||||

|

Consolidated Adjusted EBITDA Reconciliation |

2016 | 2015 | 2014 | 2013 | 2012 | |||||||||||||||

| (in thousands of U.S. dollars) | ||||||||||||||||||||

| Net income (loss) attributable to Arcos Dorados Holdings Inc. | $ | 78,810 | $ | (51,633 | ) | $ | (109,333 | ) | $ | 53,854 | $ | 114,332 | ||||||||

| Plus (Less): | ||||||||||||||||||||

| Net interest expense | 66,880 | 64,407 | 72,750 | 88,156 | 54,247 | |||||||||||||||

| Loss from derivative instruments | 3,065 | 2,894 | 685 | 4,141 | 891 | |||||||||||||||

| Foreign currency exchange results | (32,354 | ) | 54,032 | 74,117 | 38,783 | 18,420 | ||||||||||||||

| Other non-operating expenses (income), net | 2,360 | 627 | (146 | ) | 848 | 2,119 | ||||||||||||||

| Income tax expense | 59,641 | 22,816 | 32,479 | 42,722 | 46,375 | |||||||||||||||

| Net income attributable to non-controlling interests | 178 | 264 | 305 | 18 | 256 | |||||||||||||||

| Operating income | 178,580 | 93,407 | 70,857 | 228,522 | 236,640 | |||||||||||||||

| Plus (Less): | ||||||||||||||||||||

| Items excluded from computation that affect operating income: | ||||||||||||||||||||

| Depreciation and amortization | 92,969 | 110,715 | 116,811 | 114,860 | 92,328 | |||||||||||||||

|

Gains from sale or insurance recovery of property and equipment

|

(57,244 | ) | (12,308 | ) | (3,379 | ) | (10,326 | ) | (3,328 | ) | ||||||||||

| Write-offs and related contingencies of property and equipment | 5,776 | 6,038 | 7,111 | 6,489 | 4,259 | |||||||||||||||

| Impairment of long-lived assets | 7,697 | 12,343 | 50,886 | 2,958 | 1,982 | |||||||||||||||

| Impairment of goodwill | 5,045 | 679 | 2,029 | — | 683 | |||||||||||||||

| Stock-based compensation related to the special awards in connection with the initial public offering under the 2011 Plan | — | 210 | 2,503 | 1,964 | 7,997 | |||||||||||||||

| Reorganization and optimization plan | 5,341 | 18,346 | 4,707 | — | — | |||||||||||||||

| 2008 Long-Term Incentive Plan incremental compensation from modification |

281 | 741 | 149 | — | — | |||||||||||||||

| Adjusted EBITDA | 238,445 | 230,171 | 251,674 | 344,467 | 340,561 | |||||||||||||||

5

Exchange Rates and Exchange Controls

In 2016, 73.9% of our total revenues were derived from our restaurants in Argentina, Brazil, Mexico and Puerto Rico. While we maintain our books and records in U.S. dollars, our revenues are conducted in the local currency of the territories in which we operate, and as such may be affected by changes in the local exchange rate to the U.S. dollar. The exchange rates discussed in this section have been obtained from each country’s central bank. However, in most cases, for consolidation purposes, we use a foreign currency to U.S. dollar exchange rate provided by Bloomberg that differs slightly from that reported by the aforementioned central banks.

Argentina

During 2001 and 2002, Argentina went through a period of severe political, economic and social crisis. Among other consequences, the crisis resulted in Argentina defaulting on its foreign debt obligations and the introduction of numerous changes in economic policies, including currency controls that tightened restrictions on capital flows, exchange controls, an official U.S. dollar exchange and transfer restrictions that substantially limited the ability of companies to retain foreign currency or make payments abroad. In addition, since 2007, Argentina has faced significant inflationary pressures and experienced several economic recessions, from which the Argentine economy has yet not fully recovered.

Since President Mauricio Macri assumed office on December 10, 2015, the Macri administration has adopted several significant economic and policy reforms. For instance, the Macri administration eased currency controls in place since 2001 and reached agreements with a large majority of holdout creditors (in terms of claims) in connection with its 2001-2002 default on foreign indebtedness, which allowed Argentina to regain access to international financial markets.

In addition, on January 8, 2016, President Macri declared a state of administrative emergency on the national statistics system in response to the divergence between official and private inflation statistics that began in 2007 and resulted in censure by the International Monetary Fund (the “IMF”) in 2013. The declaration temporarily suspended publication of statistical data by the INDEC, the national institute for statistics. Since then, the Macri administration’s appointee to the INDEC implemented a series of methodological reforms, which have reduced the divergence between official and private inflation statistics and led the IMF to lift its censure on November 10, 2016.

While exchange control restrictions have been eased, exchange control restrictions impacted our ability to transfer funds abroad and prevented or delayed payments that our Argentine subsidiaries were required to make outside Argentina in the past.

The Argentine peso depreciated 14.3% against the U.S. Dollar in 2012, 32.4% in 2013, 30.7% in 2014, 51.7% in 2015, 21.9% in 2016, and appreciated 2.9% in the first quarter of 2017.

The following table sets forth, for the periods indicated, the high, low, average and period-end exchange rates for the purchase of U.S. dollars expressed in Argentine pesos per U.S. dollar. The average rate is calculated by using the average of the Central Bank of Argentina’s reported exchange rates on each day during a monthly period and on the last day of each month during an annual or interim period. As of April 25, 2017, the exchange rate for the purchase of U.S. dollars as reported by the Central Bank of Argentina was ARS$15.414 per U.S. dollar.

|

Period- |

Average |

Low |

High | |

| (Argentine pesos per U.S. dollar) | ||||

| ARS$ | ARS$ | ARS$ | ARS$ | |

| Year Ended December 31: | ||||

| 2012 | 4.917 | 4.224 | 4.305 | 4.917 |

| 2013 | 6.518 | 5.543 | 4.923 | 6.518 |

| 2014 | 8.552 | 8.231 | 6.543 | 8.556 |

| 2015 | 13.005 | 9.442 | 8.554 | 13.763 |

| 2016 | 15.850 | 14.945 | 13.069 | 16.039 |

6

| Quarter Ended: | ||||

| March 31, 2017 | 15.382 | 15.681 | 15.368 | 16.053 |

| Month Ended: | ||||

| October 31, 2016 | 15.175 | 15.181 | 15.115 | 15.225 |

| November 30, 2016 | 15.844 | 15.340 | 15.018 | 15.844 |

| December 31, 2016 | 15.850 | 15.830 | 15.523 | 16.039 |

| January 31, 2017 | 15.912 | 15.907 | 15.808 | 16.053 |

| February 24, 2017 | 15.455 | 15.599 | 15.368 | 15.835 |

| March 31, 2017 | 15.382 | 15.524 | 15.382 | 15.669 |

| April 30, 2017 (through April 25, 2017) | 15.414 | 15.451 | 15.174 | 15.669 |

____________________

Note: For consolidation purposes, we use an Argentine peso / U.S. dollar exchange rate provided by Bloomberg that differs slightly from that reported by the Central Bank of Argentina.

Exchange Controls

In June 2005, the Argentine government issued Decree 616/2005, which established additional restrictions over all capital flows that could result in future payment obligations of foreign currency by residents to non-residents. Pursuant to the decree, all private sector indebtedness of physical persons or corporations in Argentina were required to be agreed upon and repaid not prior to 365 days from the date of entry of the funds into Argentina, regardless of the form of repayment. The decree outlined several types of transactions that were exempted from its requirements, including foreign trade financings and primary offerings of debt securities issued pursuant to a public offering and listed on an authorized market.

In addition, the decree stipulated that all capital inflows within the private sector to the local exchange market due to foreign indebtedness of physical persons or corporations within Argentina (excluding foreign trade financings and primary offerings of debt securities issued pursuant to a public offering and listed on an authorized market), as well as all capital inflows of non-residents received by the local exchange market destined for local money holdings, all kinds of financial assets or liabilities of the financial and non-financial private sector (excluding foreign direct investment and primary offerings of debt securities issued pursuant to a public offering and listed on an authorized market) and investments in securities issued by the public sector that are acquired in secondary markets, had to meet certain requirements described in section 4 of the decree, including the following:

| · | the funds could only be transferred outside the local exchange market after a 365-day period from the date of entry of the funds into Argentina (the “Minimum Stay Period”) of 365 calendar days; |

| · | any amounts resulting from the exchange of the funds had to be credited to an account within the Argentine banking system; |

| · | a non-transferable, non-interest-bearing deposit had to be maintained for a term of 365 calendar days, in an amount equal to 30% of any inflow of funds to the Argentine foreign exchange market (the “Deposit”); and |

| · | the Deposit had to be in U.S. dollars, in any of the financial entities of Argentina, and could not be used as collateral or guaranty for any credit transaction. Any breach of the provisions of Argentine foreign exchange regulations is subject to criminal penalties. |

The requirements of Decree No. 616/2005 were subsequently eased by the Macri administration as detailed below.

On December 18, 2015, through Resolution No. 3/2015, the Ministry of Treasury and Public Finance amended Executive Decree No. 616/2005, stating that for new inflows of funds into Argentina through the Argentine foreign exchange market, (i) the Minimum Stay Period was reduced from 365 calendar days to 120 calendar days from the date of entry of the funds into Argentina and (ii) the rate of the Deposit was reduced to 0% of the funds, effectively eliminating it as a requirement. Subsequently, on January 5, 2017, the Ministry of Treasury published Resolution No. 1-E/2017, which further reduced the Minimum Stay Period from 120 to 0 days, effectively eliminating it as a requirement.

7

On August 8, 2016, the Central Bank of Argentina also introduced material changes to the foreign exchange regime by means of Communication “A” 6037 (“Communication 6037”) that significantly eased foreign exchange controls. The current foreign exchange regime is detailed below.

Inflow and settlement through the local foreign exchange market. The proceeds from foreign financial indebtedness incurred by institutions in the private non-financial sector and the financial sector and by Argentine local governments are not required to be transferred and settled through the local foreign exchange market, which would otherwise require conversion into Argentine pesos.

Whether funds are settled through the local foreign exchange market or not, resident debtors with foreign debt from the private non-financial sector and the financial sector are required to register such debt in the “Report of Issuances of Securities and Other Foreign Indebtedness of the Private Financial and Non-Financial Sector” pursuant to Central Bank of Argentina’s Communication “A” 3602, as amended, supplemented and restated (“Communication 3602”).

Payment of Services and Profits (Interest, Earnings and Dividends). Local residents are entitled to access the local foreign exchange market to transfer outside of Argentina amounts for payment of any services, interests, earnings, dividends and the acquisition of non-financial, non-produced assets (activos no financieros no producidos).

Access to the local foreign exchange market for any of these purposes requires the presentation of documentation evidencing compliance with the reporting regimes established by Communication 3602 and, in the case of direct investments (such as an ownership interest of at least 10% of a local company’s capital stock or voting rights), the requirements of Communication “A” 4237 (as amended, supplemented and restated) shall also apply.

Payment of Principal on Foreign Financial Debts. In the case of access to the local foreign exchange market for payment of principal on foreign financial indebtedness, including cancellation of financial standby arrangements granted by Argentine banking entities, applicable regulations require a sworn affidavit by the debtor confirming the filing, if applicable, in the “Report of Issuances of Securities and Other Foreign Indebtedness of the Private Financial and Non-Financial Sector” pursuant to Communication 3602.

Foreclosure of Local Guarantees. Only an Argentine financial entity that provides a guarantee for an Argentine import operation shall have access to the local foreign exchange market in order to make payments under such guarantee. Consequently, an Argentine resident that is not a financial entity and that is a guarantor of any cross-border financing shall not have access to the local foreign exchange market in order to make payments or transfer funds abroad pursuant to the guarantee.

However, as of the date hereof, subject to the satisfaction of certain conditions, resident individuals, legal entities from the private sector organized in Argentina and not authorized to deal in foreign exchange, certain trusts and other estates domiciled in Argentina, as well as Argentine local governments will be allowed access to the local foreign exchange market without the prior authorization of the Central Bank of Argentina to purchase foreign currency without specific allocation (atesoramiento). Previously, acquisitions of foreign currency for a non-specific purpose were subject to monthly caps. The Central Bank of Argentina eliminated these caps on August 9, 2016 through Communication 6037.

In addition, non-residents have access to the local foreign exchange market to transfer outside of Argentina payments for services, income and current transfers payable in Argentina, pursuant to the specific legal framework that regulates the access to this market by non-residents.

Notwithstanding the measures recently adopted by the Macri administration, the Central Bank of Argentina and the federal government in the future may impose additional exchange controls that may impact our ability to transfer funds abroad and may prevent or delay payments that our Argentine subsidiaries are required to make outside Argentina.

Brazil

Brazilian Resolution 3,568 establishes that, without prejudice to the duty of identifying customers, operations of foreign currency purchase or sale up to $3,000 or its equivalent in other currencies are not required to submit documentation relating to legal transactions underlying these foreign exchange operations. According to Resolution 3,568, the Central Bank of Brazil may define simplified forms to record operations of foreign currency purchases and sales of up to $3,000 or its equivalent in other currencies.

8

The Brazilian Monetary Council may issue further regulations in relation to foreign exchange transactions, as well as on payments and transfers of Brazilian currency between Brazilian residents and non-residents (such transfers being commonly known as the international transfer of reais), including those made through so-called non-resident accounts.

Brazilian law also imposes a tax on foreign exchange transactions, or “IOF/Exchange,” on the conversion of reais into foreign currency and on the conversion of foreign currency into reais. As of October 7, 2014, the general IOF/Exchange rate applicable to almost all foreign currency exchange transactions was increased from zero to 0.38%, although other rates may apply in particular operations, such as the below transactions which are currently not taxed:

| · | inflow related to transactions carried out in the Brazilian financial and capital markets, including investments in our common shares by investors which register their investment under Resolution No. 4,373; |

| · | outflow related to the return of the investment mentioned under the first bulleted item above; and |

| · | outflow related to the payment of dividends and interest on shareholders’ equity in connection with the investment mentioned under the first bulleted item above. |

Notwithstanding these rates of the IOF/Exchange, in force as of the date hereof, the Minister of Finance is legally entitled to increase the rate of the IOF/Exchange to a maximum of 25% of the amount of the currency exchange transaction, but only on a prospective basis.

Although the Central Bank of Brazil has intervened occasionally to control movements in the foreign exchange rates, the exchange market may continue to be volatile as a result of capital movements or other factors, and, therefore, the Brazilian real may substantially decline or appreciate in value in relation to the U.S. dollar in the future.

Brazilian law further provides that whenever there is a significant imbalance in Brazil’s balance of payments or reasons to foresee such a significant imbalance, the Brazilian government may, and has done so in the past, impose temporary restrictions on the remittance of funds to foreign investors of the proceeds of their investments in Brazil. The likelihood that the Brazilian government would impose such restricting measures may be affected by the extent of Brazil’s foreign currency reserves, the availability of foreign currency in the foreign exchange markets on the date a payment is due, the size of Brazil’s debt service burden relative to the economy as a whole and other factors. We cannot assure you that the Central Bank will not modify its policies or that the Brazilian government will not institute restrictions or delays on cross-border remittances in respect of securities issued in the international capital markets.

The Brazilian real depreciated 9.6% against the U.S. dollar in 2012, 15.5% in 2013, 11.3% in 2014, 47.0% in 2015, and appreciated 19.4% in 2016 and 5.9% in the first quarter of 2017.

The following table sets forth, for the periods indicated, the high, low, average and period-end exchange rates for the purchase of U.S. dollars expressed in Brazilian reais per U.S. dollar as reported by the Central Bank of Brazil. As of April 25, 2017, the exchange rate for the purchase of U.S. dollars as reported by the Central Bank of Brazil was R$3.158 per U.S. dollar.

|

Period- |

Average |

Low |

High | |

| (Brazilian reais per U.S. dollar) | ||||

| R$ | R$ | R$ | R$ | |

| Year Ended December 31: | ||||

| 2012 | 2.112 | 1.955 | 1.702 | 2.112 |

| 2013 | 2.343 | 2.158 | 1.953 | 2.446 |

| 2014 | 2.656 | 2.356 | 2.197 | 2.740 |

| 2015 | 3.905 | 3.388 | 2.569 | 4.195 |

| 2016 | 3.259 | 3.450 | 3.119 | 4.156 |

9

|

Period- |

Average |

Low |

High | |

| (Brazilian reais per U.S. dollar) | ||||

| R$ | R$ | R$ | R$ | |

| Quarter Ended: | ||||

| March 31, 2017 | 3.168 | 3.146 | 3.064 | 3.273 |

| Month Ended: | ||||

| October 31, 2016 | 3.181 | 3.187 | 3.119 | 3.236 |

| November 30, 2016 | 3.397 | 3.342 | 3.202 | 3.445 |

| December 31, 2016 | 3.259 | 3.352 | 3.259 | 3.465 |

| January 31, 2017 | 3.127 | 3.200 | 3.127 | 3.273 |

| February 28, 2017 | 3.099 | 3.104 | 3.051 | 3.148 |

| March 31, 2017 | 3.168 | 3.128 | 3.077 | 3.174 |

| April 30, 2017 (through April 25, 2017) | 3.158 | 3.125 | 3.092 | 3.158 |

| ____________________ |

Note: For consolidation purposes, we use a Brazilian reais / U.S. dollar exchange rate provided by Bloomberg that differs slightly from that reported by the Central Bank of Brazil.

Mexico

For the last few years, the Mexican government has maintained a policy of non-intervention in the foreign exchange markets, other than conducting periodic auctions for the purchase of U.S. dollars, and has not had in effect any exchange controls (although these controls have existed and have been in effect in the past). We cannot assure you that the Mexican government will maintain its current policies with regard to the Mexican peso or that the Mexican peso will not further depreciate or appreciate significantly in the future.

The Mexican peso depreciated 19.8% against the U.S. dollar in 2016 and appreciated 9.0% in the first quarter of 2017.

The following table sets forth, for the periods indicated, the high, low, average and period-end free-market exchange rate for the purchase of U.S. dollars, expressed in nominal Mexican pesos per U.S. dollar, as reported by the Central Bank of Mexico in the Federal Official Gazette. All amounts are stated in Mexican pesos per U.S. dollar. The annual and interim average rates reflect the average of month-end rates, and monthly average rates reflect the average of daily rates. As of April 25, 2017, the free-market exchange rate for the purchase of U.S. dollars as reported by the Central Bank of Mexico in the Federal Official Gazette as the rate of payment of obligations denominated in non-Mexican currency payable in Mexico was Ps.18.923 per U.S. dollar.

|

Period |

Average |

Low |

High | |

| (Mexican pesos per U.S. dollar) | ||||

| Ps. | Ps. | Ps. | Ps. | |

| Year Ended December 31: | ||||

| 2012 | 13.010 | 13.167 | 12.630 | 14.395 |

| 2013 | 13.077 | 12.821 | 11.981 | 13.439 |

| 2014 | 14.718 | 13.358 | 12.846 | 14.785 |

| 2015 | 17.207 | 15.967 | 14.556 | 17.378 |

| 2016 | 20.664 | 18.789 | 17.177 | 21.051 |

| Quarter Ended: | ||||

| March 31, 2017 | 18.796 | 20.321 | 18.708 | 21.908 |

| Month Ended: | ||||

| October 31, 2016 | 18.844 | 18.973 | 18.515 | 19.409 |

| November 30, 2016 | 20.552 | 19.969 | 18.509 | 21.051 |

| December 31, 2016 | 20.664 | 20.543 | 20.223 | 20.749 |

| January 31, 2017 | 21.021 | 21.396 | 20.619 | 21.908 |

| February 28, 2017 | 19.834 | 20.353 | 19.701 | 20.791 |

| March 31, 2017 | 18.796 | 19.301 | 18.708 | 19.937 |

| April 30, 2017 (through April 25, 2017) | 18.923 | 18.736 | 18.486 | 18.923 |

____________________

Note: For consolidation purposes, we use a Mexican peso/U.S. dollar exchange rate provided by Bloomberg that differs slightly from that reported by the Central Bank of Mexico.

10

| B. | Capitalization and Indebtedness |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds |

Not applicable.

| D. | Risk Factors |

Our business, financial condition and results of operations could be materially and adversely affected if any of the risks described below occur. As a result, the market price of our class A shares could decline, and you could lose all or part of your investment. This annual report also contains forward-looking statements that involve risks and uncertainties. See “Forward-Looking Statements.” Our actual results could differ materially and adversely from those anticipated in these forward-looking statements as a result of certain factors, including the risks facing our company or investments in Latin America and the Caribbean described below and elsewhere in this annual report.

Certain Factors Relating to Our Business

Our rights to operate and franchise McDonald’s-branded restaurants are dependent on the MFAs, the expiration of which would adversely affect our business, results of operations, financial condition and prospects.

Our rights to operate and franchise McDonald’s-branded restaurants in the Territories, and therefore our ability to conduct our business, derive exclusively from the rights granted to us by McDonald’s in two MFAs through 2027. The initial term of the franchise for French Guiana, Guadeloupe and Martinique expires on August 2, 2017 and includes an option to extend the agreement for these territories for an additional period of 10 years through August 2, 2027. On July 20, 2016, we exercised our option to extend our rights to operate and franchise McDonald’s-branded restaurants in these three territories. As a result, our ability to continue operating in our current capacity following the extended term of the MFAs is dependent on the renewal of our contractual relationship with McDonald’s.

McDonald’s has the right, in its reasonable business judgment based on our satisfaction of certain criteria set forth in the MFAs, to grant us an option to extend the term of the MFAs with respect to all Territories for an additional period of 10 years after the expiration in 2027 of the initial term of the MFAs upon such terms as McDonald’s may determine. Pursuant to the MFAs, McDonald’s will determine whether to grant us the option to renew between August 2020 and August 2024. If McDonald’s grants us the option to renew and we elect to exercise the option, then we and McDonald’s will amend the MFAs to reflect the terms of such renewal option, as appropriate. We cannot assure you that McDonald’s will grant us an option to extend the term of the MFAs or that the terms of any renewal option will be acceptable to us, will be similar to those contained in the MFAs or will not be less favorable to us than those contained in the MFAs.

If McDonald’s elects not to grant us the renewal option or we elect not to exercise the renewal option, we will have a three-year period in which to solicit offers for our business, which offers would be subject to McDonald’s approval. Upon the expiration of the MFAs, McDonald’s has the option to acquire all of our non-public shares and all of the equity interests of our wholly owned subsidiary Arcos Dourados Comercio de Alimentos Ltda., the master franchisee of McDonald’s for Brazil, at their fair market value.

In the event McDonald’s does not exercise its option to acquire LatAm, LLC and Arcos Dourados Comercio de Alimentos Ltda., the MFAs would expire and we would be required to cease operating McDonald’s-branded restaurants, identifying our business with McDonald’s and using any of McDonald’s intellectual property. Although we would retain our real estate and infrastructure, the MFAs prohibit us from engaging in certain competitive businesses, including Burger King, Subway, KFC or any other quick-service restaurant, or QSR, business, or duplicating the McDonald’s system at another restaurant or business during the two-year period following the expiration of the MFAs. As the McDonald’s brand and our relationship with McDonald’s are among our primary competitive strengths, the expiration of the MFAs for any of the reasons described above would materially and adversely affect our business, results of operations, financial condition and prospects.

11

Our business depends on our relationship with McDonald’s and changes in this relationship may adversely affect our business, results of operations and financial condition.

Our rights to operate and franchise McDonald’s-branded restaurants in the Territories, and therefore our ability to conduct our business, derive exclusively from the rights granted to us by McDonald’s in the MFAs. As a result, our revenues are dependent on the continued existence of our contractual relationship with McDonald’s.

Pursuant to the MFAs, McDonald’s has the ability to exercise substantial influence over the conduct of our business. For example, under the MFAs, we are not permitted to operate any other QSR chains, we must comply with McDonald’s high quality standards, we must own and operate at least 50% of all McDonald’s-branded restaurants in each of the Territories, we must maintain certain guarantees in favor of McDonald’s, including a standby letter of credit (or other similar financial guarantee acceptable to McDonald’s) in an amount of $80.0 million, to secure our payment obligations under the MFAs and related credit documents, we cannot incur debt above certain financial ratios, we cannot transfer the equity interests of our subsidiaries, any significant portion of their assets or any of the real estate properties we own without McDonald’s consent, and McDonald’s has the right to approve the appointment of our chief executive officer and chief operating officer. In addition, the MFAs require us to reinvest a significant amount of money, including through reimaging our existing restaurants, opening new restaurants and advertising, which plans McDonald’s has the right to approve. Under the 2017-2019 restaurant opening and reinvestment plan, we are required to open 180 restaurants and to reinvest $292 million in existing restaurants from 2017 through 2019. We cannot assure you that we will have available the funds necessary to finance these commitments, and their satisfaction may require us to incur additional indebtedness, which could adversely affect our financial condition. Moreover, we may not be able to obtain additional indebtedness on favorable terms, or at all. Failure to comply with these commitments could constitute a material breach of the MFAs and may lead to a termination by McDonald’s of the MFAs. In addition, on January 25, 2017, McDonald’s Corporation agreed to provide growth support for the same period. We project that the impact of this support could result in an effective royalty rate of 5.3% in 2017, 5.7% in 2018 and 5.9% in 2019.

Notwithstanding the foregoing, McDonald’s has no obligation to fund our operations. In addition, McDonald’s does not guarantee any of our financial obligations, including trade payables or outstanding indebtedness, and has no obligation to do so.

If the terms of the MFAs excessively restrict our ability to operate our business or if we are unable to satisfy our restaurant opening and reinvestment commitments under the MFAs, our business, results of operations and financial condition would be materially and adversely affected.

For certain periods of 2014, 2015 and 2016, McDonald’s Corporation granted us limited waivers for our non-compliance with certain quarterly financial ratios specified in the MFA; a failure to extend such waiver or comply with our original commitments could result in a material breach of the MFA.

During certain periods of 2014, 2015 and 2016, we were not in compliance with certain quarterly financial ratios specified in the MFA. We obtained a limited waiver from McDonald’s Corporation through and including June 30, 2016. During the waiver period we were not required to maintain these quarterly financial ratios. We have been in compliance with these quarterly ratios since the expiration of the waiver. However, if we are unable to comply with our original commitments under the MFA or to obtain a waiver for any non-compliance in the future, we could be in material breach. If we breach the MFA, McDonald’s will have certain rights, including the ability to acquire all or portions of our business. See “Item 10. Additional Information—C. Material Contracts—The MFAs.”

McDonald’s has the right to acquire all or portions of our business upon the occurrence of certain events and, in the case of a material breach of the MFAs, may acquire our non-public shares or our interests in one or more Territories at 80% of their fair market value.

Pursuant to the MFAs, McDonald’s has the right to acquire our non-public shares or our interests in one or more Territories upon the occurrence of certain events, including the death or permanent incapacity of our controlling shareholder or a material breach of the MFAs. In the event McDonald’s were to exercise its right to acquire all of our non-public shares, McDonald’s would become our controlling shareholder.

12

McDonald’s has the option to acquire all, but not less than all, of our non-public shares at 100% of their fair market value during the twelve-month period following the eighteen-month anniversary of the death or permanent incapacity of Mr. Staton, our Executive Chairman and controlling shareholder. In addition, if there is a material breach that relates to one or more Territories in which there are at least 100 restaurants in operation, McDonald’s has the right either to acquire all of our non-public shares or our interests in our subsidiaries in such Territory or Territories. By contrast, if the initial material breach of the MFAs affects or is attributable to any of the Territories in which there are less than 100 restaurants in operation, McDonald’s only has the right to acquire the equity interests of any of our subsidiaries in the relevant Territory. For example, since we have more than 100 restaurants in Mexico, if a Mexican subsidiary were to materially breach the MFA, McDonald’s would have the right either to acquire our entire business throughout Latin America and the Caribbean or just our Mexican operations, whereas upon a similar breach by our Ecuadorean subsidiary, McDonald’s would only have the right to acquire our interests in our operations in Ecuador.

McDonald’s was granted a perfected security interest in the equity interests of LatAm, LLC, Arcos Dourados Comercio de Alimentos Ltda. and certain of their subsidiaries to protect this right. In the event this right is exercised as a result of a material breach of the MFAs, the amount to be paid by McDonald’s would be equal to 80% of the fair market value of the acquired equity interests. If McDonald’s exercises its right to acquire our interests in one or more Territories as a result of a material breach, our business, results of operations and financial condition would be materially and adversely affected. See “Item 10. Additional Information—C. Material Contracts—The MFAs—Termination” for more details about fair market value calculation.

The failure to successfully manage our future growth may adversely affect our results of operations.

Our business has grown significantly since the Acquisition, largely due to the opening of new restaurants in existing and new markets within the Territories, and also from an increase in comparable store sales. Our total number of restaurant locations has increased from 1,569 at the date of the Acquisition to 2,156 as of December 31, 2016. However, during 2014, 2015 and 2016, our rate of restaurant openings slowed. This was mainly due to a shift in capital allocation strategy to increase our focus on existing restaurants over continued expansion.

Our growth is, to a certain extent, dependent on new restaurant openings and therefore may not be constant from period to period; it may accelerate or decelerate in response to certain factors. There are many obstacles to opening new restaurants, including determining the availability of desirable locations, securing reliable suppliers, hiring and training new personnel and negotiating acceptable lease terms, and, in times of adverse economic conditions, franchisees may be more reluctant to provide the investment required to open new restaurants. In addition, our growth in comparable store sales is dependent on continued economic growth in the countries in which we operate as well as our ability to continue to predict and satisfy changing consumer preferences.

We plan our capital expenditures on an annual basis, taking into account historical information, regional economic trends, restaurant opening and reimaging plans, site availability and the investment requirements of the MFAs in order to maximize our returns on invested capital. The success of our investment plan may, however, be harmed by factors outside our control, such as changes in macroeconomic conditions, changes in demand and construction difficulties that could jeopardize our investment returns and our future results and financial condition.

We depend on oral agreements with third-party suppliers and distributors for the provision of products that are necessary for our operations.

Supply chain management is an important element of our success and a crucial factor in optimizing our profitability. We use McDonald’s centralized supply chain management model, which relies on approved third-party suppliers and distributors for goods, and we generally use several suppliers to satisfy our needs for goods. This system encompasses selecting and developing suppliers of core products—beef, chicken, buns, produce, cheese, dairy mixes, beverages and toppings—who are able to comply with McDonald’s high quality standards, and establishing sustainable relationships with these suppliers. McDonald’s standards include cleanliness, product consistency, timeliness, following internationally recognized manufacturing practices, meeting or exceeding all local food regulations and compliance with our Hazard Analysis Critical Control Plan, a systematic approach to food safety that emphasizes protection within the processing facility, rather than detection, through analysis, inspection and follow-up.

13

Our 16 largest suppliers account for approximately 55.0% of our purchases. Very few of our suppliers have entered into written contracts with us as we only have oral agreements with a vast majority of them. Our supplier approval process is thorough and lengthy in order to ensure compliance with McDonald’s high quality standards. We therefore tend to develop strong relationships with approved suppliers and, given our importance to them, have found that oral agreements with them are generally sufficient to ensure a reliable supply of quality products. While we source our supplies from many approved suppliers in Latin America and the Caribbean, thereby reducing our dependence on any one supplier, the informal nature of the majority of our relationships with suppliers means that we may not be assured of long-term or reliable supplies of products from those suppliers.

In addition, certain supplies, such as beef, must often be locally sourced due to restrictions on their importation. In light of these restrictions, as well as the MFAs’ requirement to purchase certain core supplies from approved suppliers, we may not be able to quickly find alternate or additional supplies in the event a supplier is unable to meet our orders.

If our suppliers fail to provide us with products in a timely manner due to unanticipated demand, production or distribution problems, financial distress or shortages, if our suppliers decide to terminate their relationship with us or if McDonald’s determines that any product or service offered by an approved supplier is not in compliance with its standards and we are obligated to terminate our relationship with such supplier, we may have difficulty finding appropriate or compliant replacement suppliers. As a result, we may face inventory shortages that could negatively affect our operations.

Our financial condition and results of operations depend, to a certain extent, on the financial condition of our franchisees and their ability to fulfill their obligations under their franchise agreements.

As of December 31, 2016, 28.0% of our restaurants were franchised. Under our franchise agreements, we receive monthly payments which are, in most cases, the greater of a fixed rent or a certain percentage of the franchisee’s gross sales. Franchisees are independent operators with whom we have franchise agreements. We typically own or lease the real estate upon which franchisees’ restaurants are located and franchisees are required to follow our operating manual that specifies items such as menu choices, permitted advertising, equipment, food handling procedures, product quality and approved suppliers. Our operating results depend to a certain extent on the restaurant profitability and financial viability of our franchisees. The concurrent failure by a significant number of franchisees to meet their financial obligations to us could jeopardize our ability to meet our obligations.

In addition, we are liable for our franchisees’ monthly payment of a continuing franchise fee to McDonald’s, which represents a percentage of those franchised restaurants’ gross sales. To the extent that our franchisees fail to pay this fee in full, we are responsible for any shortfall. As such, the concurrent failure by a significant number of franchisees to pay their continuing franchise fees could have a material adverse effect on our results of operations and financial condition.

We do not have full operational control over the businesses of our franchisees.

We are dependent on franchisees to maintain McDonald’s quality, service and cleanliness standards, and their failure to do so could materially affect the McDonald’s brand and harm our future growth. Although we exercise significant influence over franchisees through the franchise agreements, franchisees have some flexibility in their operations, including the ability to set prices for our products in their restaurants, hire employees and select certain service providers. In addition, it is possible that some franchisees may not operate their restaurants in accordance with our quality, service, cleanliness, health or product standards. Although we take corrective measures if franchisees fail to maintain McDonald’s quality, service and cleanliness standards, we may not be able to identify and rectify problems with sufficient speed and, as a result, our image and operating results may be negatively affected.

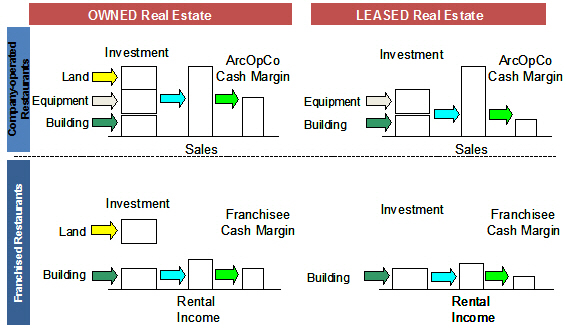

Ownership and leasing of a broad portfolio of real estate exposes us to potential losses and liabilities.

As of December 31, 2016, we owned the land for 496 of our 2,156 restaurants and the buildings for all but 11 of our restaurants. The value of these assets could decrease or rental costs could increase due to changes in local demographics, the investment climate and increases in taxes.