As filed with the Securities and Exchange Commission on December 17, 2019

File Nos. 333-[ ] and 811-22509

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

|

FORM N-14

|

|

|

THE SECURITIES ACT OF 1933

Pre-Effective Amendment No.

Post-Effective Amendment No.

|

*

*

|

|

LoCorr Investment Trust

(Exact Name of Registrant as Specified in Charter)

|

|

|

687 Excelsior Boulevard

Excelsior, MN 55331

(Address of Principal Executive Offices) (Zip Code)

|

|

|

Registrant’s Telephone Number, including Area Code: 952.767.2920

|

|

|

CT Corporation System

1300 East Ninth Street

Cleveland, OH 44114

(Name and Address of Agent for Service)

|

|

|

With copy to:

|

|

|

JoAnn Strasser

Thompson Hine LLP 41 South High Street, Suite 1700 Columbus, Ohio 43215-6101 |

|

Title of securities being registered: Class A, Class C and Class I shares of LoCorr Macro Strategies Fund, a series of the Registrant

No filing fee is required because the Registrant is relying on Section 24(f) of the Investment Company Act of 1940, as amended, pursuant to which it has previously registered an

indefinite number of shares.

Approximate date of proposed public offering: As soon as practicable after this Registration Statement becomes effective under the Securities Act of 1933, as amended.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically

states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant

to said Section 8(a), may determine.

CONTENTS OF REGISTRATION STATEMENT

This Registration Statement contains the following papers and documents:

Cover Sheet

Contents of Registration Statement

Letter to Shareholders

Notice of Special Meeting

Questions and Answers

Part A - Combined Proxy Statement/ Prospectus

Part B - Statement of Additional Information

Part C - Other Information

Signature Page

Exhibit Index

Steben Managed Futures Strategy Fund

A Series of Steben Alternative Investment Funds

9711 Washingtonian Boulevard, Suite 400

Gaithersburg, MD 20878

Gaithersburg, MD 20878

Dear Shareholder:

We wish to provide you with some important information concerning your investment. You are receiving the enclosed Proxy Statement/Prospectus because you own shares of the

Steben Managed Futures Strategy Fund (the “Target Fund”), a series of Steben Alternative Investment Funds (the “Trust”). The Board of Trustees of the Trust (the “Board”), after careful consideration and upon the recommendation of Steben &

Company, Inc. (“Steben”), the investment adviser to the Target Fund has approved an Agreement and Plan of Reorganization (the “Plan”), which provides for the reorganization (the “Reorganization”) of the Target Fund into the LoCorr Macro

Strategies Fund (the “Acquiring Fund” and together with the Target Fund, the “Funds”), a series of LoCorr Investment Trust. While the Funds’ investment objectives, principal investment strategies and investment policies are similar, there are

differences between the two, as further described in the enclosed Proxy Statement/Prospectus.

On October 31, 2019, Steben was acquired by Octavus Group, LLC, the parent company of LoCorr Fund Management LLC, the Acquiring Fund’s investment adviser (the “Acquisition”).

The Acquisition resulted in a change of control of Steben, and the assignment and termination of the investment advisory, subadvisory and trading advisory agreements with respect to the Target Fund and Steben Managed Futures Cayman Fund, Ltd.

(the “Cayman Fund”), the Target Fund’s wholly-owned subsidiary. In order for Steben and the Target Fund’s subadvisor and trading advisors to continue to provide services to the Target Fund and the Cayman Fund after the closing of the

Acquisition, on September 23, 2019, the Board of Trustees of the Trust and the Board of Directors of the Cayman Fund approved interim investment advisory, subadvisory and trading advisory agreements with respect to the Target Fund and the

Cayman Fund, as applicable (the “Interim Agreements”). The Interim Agreements became effective upon the closing of the Acquisition and will remain in effect for a period of up to 150 days, or March 29, 2020, as permitted by Rule 15a-4 under

the Investment Company Act of 1940, as amended.

Steben’s recommendation to reorganize the two Funds was based largely on the Target Fund’s inability to attract assets and reach scale and its history of net redemption activity. The Plan is

subject to approval by shareholders of the Target Fund. If the Plan is approved and other closing conditions are satisfied or waived, you will receive the same class of shares of the Acquiring Fund equal in value to the shares that you hold in

the Target Fund as of the closing date of the Reorganization, except that holders of Class N shares of the Target Fund will receive Class A shares of the Acquiring Fund because (i) the Acquiring Fund does not offer Class N shares and (ii) Class

A shares of the Acquiring Fund have an ongoing expense structure similar to that of Class N shares of the Target Fund. The transfer effectively would be an exchange of your shares of the Target Fund for shares

of the Acquiring Fund, which would be distributed pro rata by the Target Fund to holders of its shares as follows:

|

Steben Managed Futures Strategy Fund

|

|

LoCorr Macro Strategies Fund

|

|

Class A Shares Target Fund (SKLAX)

|

Class A Shares Acquiring Fund (LFMAX)

|

|

|

Class C Shares Target Fund (SKLCX)

|

Class C Shares Acquiring Fund (LFMCX)

|

|

|

Class I Shares Target Fund (SKLIX)

|

Class I Shares Acquiring Fund (LFMIX)

|

|

|

Class N Shares Target Fund (SKLNX)

|

Class A Shares Acquiring Fund (LFMAX)

|

Steben believes the Reorganization offers a number of benefits to shareholders of the Target Fund, including being shareholders of a Fund with greater asset size that creates

greater opportunity to benefit from long-term economies of scale. Following the Reorganization, based on current expenses and determined on a pro forma basis, the total annual operating expense ratios for the Acquiring Fund’s Class A, Class C

and Class I shares are anticipated to be lower than the total annual operating expense ratios for the Target Fund’s Class A, Class C and Class I shares, respectively, and Class N shares (as compared to the Acquiring Fund’s Class A shares).

Steben also believes that Target Fund shareholders will benefit from the expertise and experience of the Acquiring Fund’s adviser, LoCorr Fund Management, LLC.

No sales loads, commissions or other transactional fees will be imposed on shareholders in connection with the exchange of their shares. The Reorganization is designed to

qualify as a tax-free reorganization, so you should not realize a tax gain or loss for federal income tax purposes as a direct result of the Reorganization, although prior to the closing date, you may receive an additional taxable distribution

of ordinary income and/or capital gains that the Target Fund has accumulated prior to the date of the distribution.

If the Plan is not approved by shareholders by March 29, 2020, the Interim Agreements will expire and Steben intends to recommend that the Board vote to liquidate the Target

Fund. Shareholders would receive a liquidating distribution on the liquidation date equal to the value of the shares owned. The liquidating distribution would result in a taxable transaction.

The Plan will be presented to shareholders at a special meeting of shareholders to be held on January 17, 2020 (the “Meeting”). Additional details about the Reorganization are

described in the enclosed Q&A and Proxy Statement/Prospectus, which you should read carefully.

The Board unanimously recommends that shareholders vote FOR the Plan.

Please read the enclosed Proxy Statement/Prospectus carefully and submit your vote. If you have any questions about the Proposal or how to vote your shares, please call (877)

536-1561.

Thank you for your consideration of the Proposal, which is important and warrants your consideration.

|

Sincerely,

|

|

|

Kenneth Steben

|

|

|

President

|

|

|

Steben Alternative Investment Funds

|

Steben Managed Futures Strategy Fund

A Series of Steben Alternative Investment Funds

9711 Washingtonian Boulevard, Suite 400

Gaithersburg, MD 20878

Gaithersburg, MD 20878

NOTICE OF SPECIAL MEETING OF SHAREHOLDERS

To Be Held January 17, 2020

To Be Held January 17, 2020

Notice is hereby given that the Board of Trustees of Steben Alternative Investment Funds (the “Trust”) has called a Special Meeting of Shareholders of Steben Managed Futures Strategy Fund (the

“Target Fund”), a series of the Trust, to be held at the offices of Steben & Company, Inc., 9711 Washingtonian Boulevard, Gaithersburg, MD 20878, on January 17, 2020, at 9 a.m. Central Standard Time (together with any adjournments or

postponements thereof, the “Meeting”). At the Meeting, shareholders of the Target Fund will be asked to vote on the Proposal set forth below, and to transact such other business, if any, as may properly come before the Meeting.

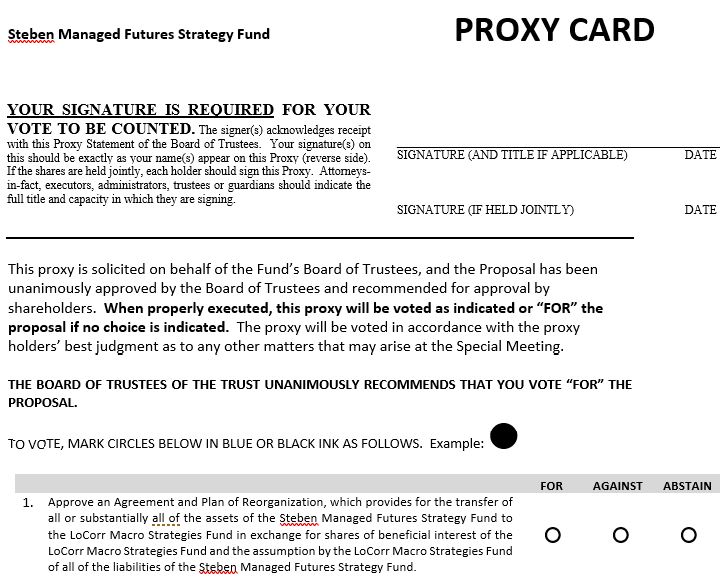

| Proposal: |

Approve an Agreement and Plan of Reorganization, which provides for the transfer of all or substantially all of the assets of the Steben Managed Futures Strategy Fund to the LoCorr Macro Strategies Fund in

exchange for shares of beneficial interest of the LoCorr Macro Strategies Fund and the assumption by the LoCorr Macro Strategies Fund of all of the liabilities of the Steben Managed Futures Strategy Fund.

|

Only shareholders of record of the Target Fund as of the close of business on December 6, 2019 (the “Record Date”) are entitled to notice of, and to vote at, the Meeting and any adjournments or

postponements thereof. The Notice of Meeting, Proxy Statement/Prospectus and accompanying form of proxy will first be mailed to shareholders on or about December 20, 2019.

If the necessary quorum to transact business or the vote required to approve the Proposal is not obtained at the Meeting or if a quorum is obtained but sufficient votes required to approve the

Proposal are not obtained, the Trust expects the Meeting to be adjourned in order to solicit additional proxies.

The Board of Trustees of the Trust unanimously recommends that shareholders of the Target Fund vote FOR the

Proposal.

Proposal.

By Order of the Board of Trustees,

December 18, 2019

Important Notice Regarding the Availability of Proxy Materials for the Special Meeting of Shareholders to be Held on January 17, 2020 or any adjournment or

postponement thereof. This Notice and enclosed Proxy Statement/Prospectus are available on the internet at vote.proxyonline.com/Steben/docs/Steben2019.pdf. On this website, you will be able to access this Notice, the Proxy

Statement/Prospectus, any accompanying materials and any amendments or supplements to the foregoing material that are required to be furnished to shareholders. We encourage you to access and review all of the important information contained in

the proxy materials before voting.

YOUR VOTE IS IMPORTANT

To assure your representation at the Meeting, please complete, date and sign the enclosed proxy card and return it promptly in the accompanying envelope. You also may vote by

telephone or via the Internet by following the instructions on the enclosed proxy card. Whether or not you plan to attend the Meeting in person, please vote your shares; if you attend the Meeting, you may revoke your proxy and vote your shares

in person. For more information or assistance with voting, please call (877) 536-1561.

STEBEN MANAGED FUTURES STRATEGY FUND

PROXY STATEMENT/PROSPECTUS DATED DECEMBER 18, 2019

Relating to the acquisition of the assets of

STEBEN MANAGED FUTURES STRATEGY FUND,

a series of Steben Alternative Investment Funds

9711 Washingtonian Boulevard, Suite 400

Gaithersburg, MD 20878

Gaithersburg, MD 20878

(240) 631-7600

by and in exchange for shares of beneficial interest of

LOCORR MACRO STRATEGIES FUND,

a series of LoCorr Investment Trust

a series of LoCorr Investment Trust

687 Excelsior Boulevard

Excelsior, MN 55331

(952) 767-2920

INTRODUCTION

This proxy statement/prospectus (the “Proxy Statement/Prospectus”) is being furnished to shareholders of the Steben Managed Futures Strategy Fund (the “Target Fund”), a series

of Steben Alternative Investment Funds (the “Trust”), in connection with a special meeting of the shareholders of the Target Fund to be held at the offices of Steben & Company, Inc., 9711 Washingtonian Boulevard, Gaithersburg, MD 20878 at

10 a.m. Eastern Standard Time (together with any adjournments or postponements thereof, the “Meeting”). The Board of Trustees of the Trust (the “Board of Trustees,” the “Board” or the “Trustees”) is soliciting proxies from shareholders of the

Target Fund for the Meeting.

At the Meeting, shareholders will be asked to vote on the Proposal set forth below, and to transact such other business, if any, as may properly come before the Meeting.

| Proposal: |

Approve an Agreement and Plan of Reorganization, which provides for the transfer of all or substantially all of the assets of the Steben Managed Futures Strategy Fund to the LoCorr Macro Strategies Fund in

exchange for shares of beneficial interest of the LoCorr Macro Strategies Fund and the assumption by the LoCorr Macro Strategies Fund of all of the liabilities of the Steben Managed Futures Strategy Fund.

|

We refer to LoCorr Macro Strategies Fund as the “Acquiring Fund.” We refer to the Target Fund and the Acquiring Fund collectively as the “Funds.” The Agreement and Plan of

Reorganization for this proposed transaction is referred to herein as the “Plan,” and the transaction contemplated by the Plan is referred to herein as the “Reorganization.”

As a result of the Reorganization, each shareholder of the Target Fund will receive a number of full and fractional shares of the Acquiring Fund equal in value to their shares

of the Target Fund as of the close of regular trading on the New York Stock Exchange (“NYSE”) on the closing date of the Reorganization, as follows:

|

Steben Managed Futures Strategy Fund

|

LoCorr Macro Strategies Fund t

|

|

|

Class A Shares Target Fund (SKLAX)

|

à

|

Class A Shares Acquiring Fund (LFMAX)

|

|

Class C Shares Target Fund (SKLCX)

|

à

|

Class C Shares Acquiring Fund (LFMCX)

|

|

Class I Shares Target Fund (SKLIX)

|

à

|

Class I Shares Acquiring Fund (LFMIX)

|

|

Class N Shares Target Fund (SKLNX)

|

à

|

Class A Shares Acquiring Fund (LFMAX)

|

The number of Acquiring Fund shares of each class that a shareholder of the Target Fund receives will depend on the relative net asset values per share of the applicable class of each Fund

immediately prior to the Reorganization. Thus, although the aggregate net asset value in a shareholder’s account will be the same, a Target Fund shareholder may receive a greater or lesser number of shares of the Acquiring Fund than the number

of shares of the Target Fund held by the shareholder. The Reorganization will not affect the value of your investment at the time of Reorganization and your interest in the Target Fund will not be diluted.

Steben & Company, Inc. (“Steben” or the “Adviser”) is the investment adviser for the Target Fund. LoCorr Fund Management, LLC (“LoCorr”) is the investment adviser of the

Acquiring Fund. On October 31, 2019, Steben was acquired by Octavus Group, LLC, the parent company of LoCorr (the “Acquisition”). The Acquisition resulted in a change of control of Steben, and the assignment and termination of the investment

advisory, subadvisory and trading advisory agreements with respect to the Target Fund and Steben Managed Futures Cayman Fund, Ltd. (the “Cayman Fund”), the Target Fund’s wholly-owned subsidiary. In order for Steben and the Target Fund’s

subadvisor and trading advisors to continue to provide services to the Target Fund and the Cayman Fund after the closing of the Acquisition, on September 23, 2019, the Board of Trustees of the Trust and the Board of Directors of the Cayman Fund

(“Directors”) approved interim investment advisory, subadvisory and trading advisory agreements with respect to the Target Fund and the Cayman Fund, as applicable (the “Interim Agreements”). The Interim Agreements became effective upon the

closing of the Acquisition and will remain in effect for a period of up to 150 days, or March 29, 2020, as permitted by Rule 15a-4 under the Investment Company Act of 1940, as amended.

LoCorr will remain the investment adviser for the Acquiring Fund following the completion of the Reorganization. After the Reorganization is completed, the Target Fund will be

dissolved. The closing of the Reorganization is contingent upon approval of the Plan by shareholders of the Target Fund and the satisfaction or waiver of other closing conditions. A form of the Plan is attached as Appendix A. If shareholders

approve the Plan, the Reorganization is expected to occur on or about January 31, 2020, or as soon as practicable thereafter (the “Closing Date”).

This Proxy Statement/Prospectus, Notice of Special Meeting, and the proxy card(s) are first being mailed to shareholders of the Target Fund on or about December 20, 2019.

Shareholders of record of the Target Fund as of the close of business on December 6, 2019 (the “Record Date”) are entitled to notice of and to vote at the Meeting.

The Board of Trustees unanimously recommends that shareholders of the Target Fund vote FOR the Proposal.

This Proxy Statement/Prospectus, which you should read carefully and retain for future reference, sets forth the information that you should know about the Target Fund, the

Acquiring Fund and the proposed Reorganization, before voting on the Proposal. While the Funds’ investment objectives, principal investment strategies and investment policies are similar, there are differences between the two, as further

described herein.

The Board has approved the Proposal. Steben believes that shareholders of the Target Fund may benefit by being shareholders of a Fund with greater asset size that creates

greater opportunity to benefit from long-term economies of scale. Following the Reorganization, based on current expenses and determined on a pro forma basis, the total annual operating expense ratios for the Acquiring Fund’s Class A, Class C

and Class I shares are anticipated to be lower than the total annual operating expense ratios for the Target Fund’s Class A, Class C and Class I shares, respectively, and Class N shares (as compared to the Acquiring Fund’s Class A shares). .

Steben also believes that Target Fund shareholders will benefit from the expertise and experience of the Acquiring Fund’s adviser, LoCorr Fund Management, LLC. The Proxy Statement/Prospectus serves as a prospectus of the Acquiring Fund in

connection with the issuance of the Acquiring Fund shares in the Reorganization.

No person has been authorized to give any information or make any representation not contained in this Proxy Statement/Prospectus and, if so given or made,

such information or representation must not be relied upon as having been authorized. This Proxy Statement/Prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities in any jurisdiction in which, or to

any person to whom, it is unlawful to make such offer or solicitation.

Shares of the Acquiring Fund have not been approved or disapproved by the U.S. Securities and Exchange Commission (“SEC”) nor has the SEC passed upon the

accuracy or adequacy of this Proxy Statement/Prospectus. Any representation to the contrary is a criminal offense. The shares of the Funds are not deposits or obligations of, or guaranteed or endorsed by, any financial institution or the U.S.

Government, are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board or any other government agency, and involve risk, including the possible loss of the principal amount invested.

Incorporation by Reference

For more information about the investment objective, strategies, restrictions, and risks of the Funds, see:

| • |

The Target Fund’s Prospectus and Statement of Additional Information filed in Post-Effective Amendment No. 16 to Steben Alternative Investment Funds’ registration statement on Form N-1A (File Nos.

811-22880 and 333-190813), dated July 29, 2019, filed on July 26, 2019, as supplemented;

|

| • |

The Acquiring Fund’s Prospectus and Statement of Additional Information filed in Post-Effective Amendment No. 45 to LoCorr Investment Trust’s registration statement on Form N-1A (File Nos. 811-22509 and

333-171360), dated March 1, 2019, filed on March 1, 2019, as supplemented;

|

| • |

The Target Fund’s Annual Report, filed on Form N-CSR (File No. 811-22880), for the fiscal year ended March 31, 2019, filed on June 3, 2019;

|

| • |

The Target Fund’s Semi-Annual Report, filed on Form N-CSRS (File No. 81122880), for the six-month period ended September 30, 2019, filed on November 25, 2019;

|

| • |

The Acquiring Fund’s Annual Report, filed on Form N-CSR (File No. 811-22509), for the fiscal year ended December 31, 2018, filed on March 6, 2019; and

|

| • |

The Acquiring Fund’s Semi-Annual Report, filed on Form N-CSRS (File No. 811-22509), for the six-month period ended June 30, 2019, filed on September 5, 2019.

|

The above documents (the “Disclosure Documents”) have been filed with the SEC and are incorporated by reference herein. The Prospectus of each class of the Target Fund and its

most recent shareholder report have previously been delivered to such Fund’s shareholders.

A Statement of Additional Information dated December 18, 2019 relating to the Reorganization has been filed with the SEC and is incorporated by reference into this Proxy

Statement/Prospectus. You can obtain a free copy of that document by contacting your plan sponsor, broker-dealer, or financial intermediary or by calling (877) 536-1561.

Each Fund is subject to the informational requirements of the Securities Exchange Act of 1934, as amended, and the Investment Company Act of 1940, as amended (the “1940 Act”),

and, in accordance therewith, files reports, proxy materials, and other information with the SEC. Copies of these materials and other information about the Funds may be obtained without charge by writing or calling the Funds at the addresses

and telephone numbers shown on the previous pages. You may also obtain reports and other information about the Funds from the Electronic Data Gathering Analysis and Retrieval (EDGAR) Database on the SEC’s website at http://www.sec.gov. In

addition, such information may be inspected and copied from the Public Reference Branch, Office of Consumer Affairs and Information Services, Securities and Exchange Commission, Washington, DC, 20549 at prescribed rates.

PROXY STATEMENT/PROSPECTUS

DECEMBER 18, 2019

DECEMBER 18, 2019

|

Table of Contents

|

|

QUESTIONS AND ANSWERS

|

1

|

|

PROPOSAL – THE REORGANIZATION OF STEBEN MANAGED FUTURES STRATEGY FUND \INTO LOCORR MACRO STRATEGIES FUND

|

|

|

SUMMARY

|

9

|

|

Comparison of Management Fees

|

9

|

|

Current Fees and Expenses

|

9

|

|

Shareholder Fees

|

9

|

|

Annual Fund Operating Expenses

|

10

|

|

Fund Turnover

|

12

|

|

Investment Objectives

|

13

|

|

Principal Investment Strategies

|

13

|

|

Principal Investment Risks

|

17

|

|

Comparison of Fund Performance

|

27

|

|

Management of the Funds

|

29

|

|

Buying and Selling Fund Shares

|

30

|

|

Tax Information

|

30

|

|

Payments to Broker-Dealers, Insurers, and Other Financial Intermediaries

|

31

|

|

THE REORGANIZATION

|

32

|

|

The Plan

|

32

|

|

Reasons for the Reorganization

|

33

|

|

U.S. Federal Income Tax Consequences

|

35

|

|

Securities to Be Issued, Shareholder Rights

|

36

|

|

Capitalization

|

37

|

|

ADDITIONAL INFORMATION ABOUT THE FUNDS

|

37

|

|

Additional Investment Strategies and General Fund Policies

|

37

|

|

Acquiring Fund – Additional Information about the Fund’s Subadvisers’ Processes

|

40

|

|

Fundamental Investment Policies and Restrictions

|

42

|

|

Target Fund

|

42

|

|

Acquiring Fund

|

44

|

|

Other Comparative Information about the Funds

|

45

|

|

Fund Policies on Pricing of Fund Shares, Purchases and Redemptions, Dividends and Distributions,

|

|

|

Frequent Purchases and Redemptions, Tax Consequences and Distribution Arrangements

|

53

|

|

Financial Highlights

|

53

|

|

ADDITIONAL INFORMATION

|

58

|

|

Quorum and Voting

|

58

|

i

|

Share Ownership

|

58

|

|

Solicitation of Proxies

|

59

|

|

Shareholder Proposals for Subsequent Meetings

|

59

|

|

Shareholder Communications

|

60

|

|

Reports to Shareholders and Financial Statements

|

60

|

|

“Householding”

|

60

|

|

APPENDIX A: FORM OF AGREEMENT AND PLAN OF REORGANIZATION

|

A-1

|

|

APPENDIX B: ACQUIRING FUND POLICIES ON PRICING OF FUND SHARES, PURCHASES AND REDEMPTIONS, DIVIDENDS AND DISTRIBUTIONS, FREQUENT PURCHASES AND REDEMPTIONS, TAX CONSEQUENCES AND DISTRIBUTION ARRANGEMENTS

|

B-1 |

ii

The following is a brief overview of the Proposal to be voted on at the Meeting relating to the proposed Reorganization. The Proxy Statement/Prospectus contains more

detailed information about the Proposal and proposed Reorganization, and we encourage you to read it in its entirety before voting. This synopsis is qualified in its entirety by the remainder of this Proxy Statement/Prospectus. The

description of the Plan is qualified by reference to the full text of the form of the Plan, which is attached as Appendix A to this Proxy Statement/Prospectus.

| Q. |

What is being proposed?

|

| A. |

The Board of Trustees recommends that shareholders of the Target Fund approve the Plan that authorizes the reorganization of the Target Fund into the Acquiring Fund. You are receiving this Proxy

Statement/Prospectus because, as a shareholder of the Target Fund on the Record Date (defined below), you have the right to vote on the Plan.

|

If the Plan is approved by shareholders of the Target Fund, as of the close of regular trading on the NYSE on the Closing Date of the Reorganization, Target Fund

shareholders will receive a number of full and fractional shares of the Acquiring Fund equal in value to their shares of the Target Fund immediately prior to the Reorganization. Specifically, all or substantially all of the assets of the

Target Fund will be transferred to the Acquiring Fund in exchange for shares of beneficial interest of the Acquiring Fund and the assumption by the Acquiring Fund of all of the liabilities of the Target Fund. The shares of the Acquiring

Fund received by the Target Fund will be distributed pro rata to Target Fund shareholders of record, determined as of the close of business on the Closing Date. After the Reorganization is

completed, the Target Fund will be dissolved. The Reorganization is designed to qualify as a tax-free reorganization, so you should not realize a tax gain or loss for federal income tax purposes as a

direct result of the Reorganization.

| Q. |

Why am I being asked to approve the Plan to reorganize my Fund into the LoCorr Macro Strategies Fund?

|

| A. |

Steben believes the proposed Reorganization offers a number of benefits to shareholders of the Target Fund, including being shareholders of a Fund with greater asset size that creates greater

opportunity to benefit from long‑term economies of scale. Steben also believes that the Target Fund shareholders will benefit from the expertise and experience of the Acquiring Fund’s adviser, LoCorr Fund Management, LLC.

|

| Q. |

If the Reorganization occurs, how will the Acquiring Fund be managed?

|

| A. |

If the Reorganization is consummated, (i) the Target Fund will be reorganized into the Acquiring Fund; (ii) the Acquiring Fund will be managed by its current investment team at LoCorr; (iii) the

investment objective of the Acquiring Fund, which is similar to that of the Target Fund, will not change; and (iv) the investment policies, principal strategy and risks of the Acquiring Fund will not change.

|

| Q. |

What is the recommendation of the Board of Trustees on the Reorganization?

|

| A. |

At a meeting held on November 1, 2019, the Board of Trustees of the Target Fund considered the Reorganization and determined that the Reorganization would be in the best interests of the Target Fund

and its shareholders and that the Reorganization would not dilute the interests of the Target Fund’s shareholders. In reaching these determinations, the Trustees reviewed and analyzed various factors it deemed relevant,

including the following factors, among others:

|

| • |

The terms of the Reorganization, including that no sales loads, commissions or other transactional fees would be imposed on Target Fund shareholders in connection with the Reorganization and that

Target Fund shareholders would receive a number of full and fractional shares of the Acquiring Fund equal in value to their holdings in the Target Fund as of the Closing Date;

|

| • |

The Funds’ investment objectives, policies and strategies are similar from an investment perspective in that both Funds pursue a managed futures investment strategy through a wholly-owned subsidiary,

as well as a fixed income investment strategy;

|

| • |

Following the Reorganization, based on current expenses and determined on a pro forma basis, the total annual operating expense ratios for the Acquiring Fund’s Class A, Class C and Class I shares are

anticipated to be lower than the total annual operating expense ratios for the Target Fund’s Class A, Class C and Class I shares, respectively, and Class N shares (as compared to the Acquiring Fund’s Class A shares).

|

1

| • |

The larger asset base of the Acquiring Fund creates the opportunity for shareholders of the Target Fund to benefit from long-term economies of scale;

|

| • |

The Acquiring Fund has generally outperformed the Target Fund since the Target Fund’s inception date of April 1, 2014. Below are the average annual returns for both Funds’ Class I shares as of

9/30/19 for the periods shown:

|

|

Performance as of 9/30/19

|

1 yr

|

3 yr

|

5yr

|

Since inception

of the Target

Fund (4/1/14)

|

|

Steben Managed Futures Strategy Fund

|

5.12%

|

1.37%

|

2.05%

|

2.89%

|

|

LoCorr Macro Strategies Fund

|

9.20%

|

1.92%

|

4.50%

|

5.94%

|

| • |

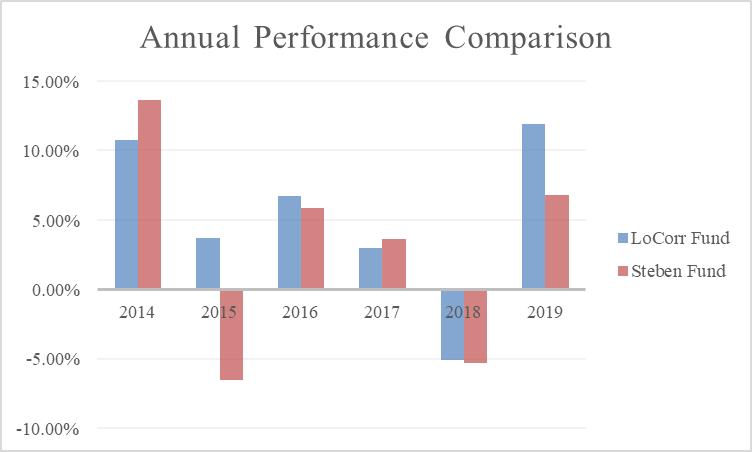

The calendar year performance of the two Funds’ Class I shares, since the Target Fund’s inception date of 4/1/14, through 9/30/19, are as follows:

|

| • |

As of September 30, 2019, the Acquiring Fund has outperformed its benchmark for the 1-year and 5-year periods and since inception of the Acquiring Fund (March 24, 2011);

|

| • |

Information provided by LoCorr demonstrating it is an experienced provider of investment advisory services to mutual funds. The nature and quality of services that the shareholders of the Target

Fund are expected to receive as shareholders of the Acquiring Fund will generally be comparable to the nature and quality of services that such shareholders currently receive;

|

| • |

The background and experience of the Acquiring Fund’s portfolio managers and subadvisers, including that two of the Target Fund’s trading advisors, Milburn and Revolution, also serve as subadvisers to

the Acquiring Fund;

|

| • |

Prior to the Reorganization, the futures and currency forwards positions held by the Target Fund will be converted to cash, but the Target Fund’s fixed income investments will be transferred to the

Acquiring Fund. For more information about the conversion of the Target Fund’s futures and currency forwards positions, please refer to the section entitled “The Plan” below.

|

| • |

The Reorganization is expected to be tax-free for federal income tax purposes for each Fund and its shareholders, although prior to the Closing Date, Target Fund shareholders may receive an additional

taxable distribution of ordinary income and/or capital gains that the Target Fund has accumulated prior to the date of the distribution;

|

2

| • |

That the Acquiring Fund may not be able to utilize certain tax loss carry forwards, if any, that would otherwise be available;

|

| • |

There will be no change in the rights of the Target Fund’s shareholders as a result of the Reorganization;

|

| • |

The Reorganization will be submitted to the shareholders of the Target Fund for their approval and that shareholders who do not wish to become shareholders of the Acquiring Fund may redeem their

Target Fund shares before the closing of the Reorganization, although redemption may be a taxable transaction for them;

|

| • |

The costs of the Reorganization, other than costs incurred to reposition the Target Fund in connection with the Reorganization, will be borne by LoCorr or its affiliates;

|

| • |

The Board noted that the Acquisition had resulted in a change of control of Steben, and the assignment and termination of the investment advisory, subadvisory and trading advisory agreements with

respect to the Target Fund and its subsidiary. The Board considered that since the closing of the Acquisition, Steben, the subadvisor and the trading advisors were providing services to the Target Fund and its subsidiary

pursuant to the interim agreements. The Board considered that, if the proposed Reorganization is not approved by shareholders by March 29, 2020, the interim agreements will expire and Steben intends to recommend that the Board

vote to liquidate the Target Fund; and

|

| • |

In light of the Target Fund’s inability to attract assets and reach scale and its history of redemption activity, the most likely alternative to the Reorganization would be the liquidation of the

Target Fund and the subsidiary, which would be less desirable than the Reorganization, as a liquidating distribution would result in a taxable transaction for the Target Fund’s shareholders.

|

The Board of Trustees unanimously recommends that shareholders of the Target Fund vote FOR the approval of the Plan.

| Q. |

Will I own the same number of shares of the Acquiring Fund as I currently own of the Target Fund?

|

| A. |

No. You will receive shares of the class of the Acquiring Fund outlined below with equivalent dollar value as the shares of the Target Fund you own as of the time the Reorganization closes. However,

the number of shares you receive will depend on the relative net asset values (“NAVs”) of the shares of the Target Fund and the corresponding class of shares of the Acquiring Fund as of the close of trading on the New York Stock

Exchange (“NYSE”) on the day of the closing of the Reorganization.

|

|

Steben Managed Futures Strategy Fund

|

LoCorr Macro Strategies Fund

|

|

|

Class A Shares Target Fund

|

à

|

Class A Shares Acquiring Fund

|

|

Class C Shares Target Fund

|

à

|

Class C Shares Acquiring Fund

|

|

Class I Shares Target Fund

|

à

|

Class I Shares Acquiring Fund

|

|

Class N Shares Target Fund

|

à

|

Class A Shares Acquiring Fund

|

| Q. |

How do the Funds’ investment objectives and principal investment strategies compare?

|

| A. |

The following summarizes the primary similarities and differences in the Funds’ investment objectives and principal investment strategies.

|

Similarities:

Investment Objectives: The Funds have similar investment objectives.

3

| • |

Target Fund. The Fund seeks to achieve positive long term absolute returns with low correlation to broad equity and fixed income market returns.

|

| • |

Acquiring Fund. The Fund's primary investment objective is capital appreciation in rising and falling equity markets with managing volatility as a

secondary objective.

|

Principal Investment Strategies:

| • |

Both Funds utilize a managed futures strategy.

|

| • |

Both Funds pursue a fixed income strategy. The Target Fund invests generally between 60% and 80% of its assets directly in fixed income investments to generate returns and interest income. The

Acquiring Fund allocates approximately 75% of its assets to its fixed income strategy.

|

Diversification: Each Fund is classified as “diversified” under the 1940 Act, meaning that each Fund may not,

with respect to 75% of its total assets, invest more than 5% of its total assets in any issuer and may not own more than 10% of the outstanding voting securities of an issuer.

Differences:

Principal Investment Strategies:

While each Fund utilizes managed futures and fixed income strategies, the Funds’ implementation of these strategies differs. The Target Fund pursues a managed futures strategy designed to

capture absolute returns and a fixed income strategy designed to generate returns and investment income. By contrast, the Acquiring Fund’s managed futures strategy is designed to produce capital appreciation, and its fixed income strategy

is designed to generate interest income and preserve principal. While the Funds’ managed futures strategies are similar in the types of futures contracts bought and sold, the Target Fund has had more exposure to futures on agricultural

products than the Acquiring Fund has. More detail about each Fund’s implementation of its strategies is provided below:

| • |

Target Fund. The Target Fund seeks to achieve its investment objective by pursuing a managed futures strategy which intends to capture absolute returns in the commodity and financial futures

markets (equity, interest rate and currency) by investing in (i) futures contracts (such as currency futures, futures on broad-based security indices and futures on commodities), (ii) foreign currency transactions (such as U.S.

and foreign spot currencies and currency forward contracts); and options on futures and swaps. The Target Fund invests generally between 60% to 80% of its assets directly in fixed income investments to generate returns and

interest income, diversifying the returns of the Fund’s investments in managed futures. Steben allocates fixed income assets to the Fund’s subadviser, who invests primarily in investment grade securities.

|

| • |

Acquiring Fund. The Acquiring Fund seeks to achieve its investment objective by allocating its assets using two principal strategies, a managed futures strategy and a fixed income strategy.

The managed futures strategy is designed to produce capital appreciation by capturing returns related to the commodity and financial markets by investing long or short in: (i) futures,

(ii) forwards, (iii) options, (iv) spot contracts, or (v) swaps, each of which may be tied to (a) currencies, (b) interest rates, (c) stock market indices, (d) energy resources, (e) metals or (f) agricultural products. The

Acquiring Fund’s fixed income strategy is designed to generate interest income and preserve principal by investing primarily in investment grade securities.

|

Further information comparing the Funds’ investment objectives, strategies, restrictions, and risks is included below under “Summary of the Funds”. In addition, the Acquiring Fund’s

Prospectus, as supplemented, is enclosed for your reference.

| Q. |

How do the Funds compare in size?

|

| A. |

As of October 31, 2019, the Target Fund’s net assets were approximately $66 million, and the Acquiring Fund’s net assets were approximately $697 million. If the Reorganization were completed as of

October 31, 2019, the combined net assets of the Acquiring Fund would be approximately $763 million. The asset size of each Fund fluctuates on a daily basis, and the asset size of the Acquiring Fund after the Reorganization may

be larger or smaller than the combined assets of the Funds as of October 31, 2019.

|

4

| Q. |

How do the fee and expense structures of the Funds compare?

|

| A. |

Advisory Fees. The Target Fund pays an advisory fee at an annual rate of 1.75% of average daily net assets, while the Acquiring Fund pays an advisory fee at an

annual rate of 1.65% of average daily net assets.

|

Expense Structures.

Target Fund. Pursuant to an Operating Services Agreement with the Fund, the Fund pays Steben 0.24% of the Fund’s average daily net assets, and

Steben has contractually agreed to pay all of the Fund’s ordinary expenses including the Fund’s acquired fund fees and expenses, but excluding management fees, distribution and/or service fees, shareholder servicing fees and certain other

expenses. As a result, the Fund’s net expense ratio for each share class (excluding distribution and/or service (12b-1) fees) is 1.99%.

Acquiring Fund. Following the Reorganization, based on current expenses and determined on a pro forma basis, the total annual operating expense

ratios for the Acquiring Fund’s Class A, Class C and Class I shares are anticipated to be lower than the total annual operating expense ratios for the Target Fund’s Class A, Class C and Class I shares, respectively, and Class N shares (as

compared to the Acquiring Fund’s Class A shares). Additionally, LoCorr has contractually agreed to reduce its fees and/or absorb expenses of the Fund, until at least April 30, 2021, to ensure that the total annual operating expenses after

fee waiver and/or reimbursement (exclusive of distribution and/or service (12b-1) fees, acquired fund fees and expenses and certain other expenses) will not exceed 1.99% of the Fund’s daily average net assets attributable to each class of

the Fund. Unlike the Target Fund, the Acquiring Fund’s adviser does not absorb acquired fund fees and expenses.

| Q. |

Will the Reorganization result in higher investment advisory fees for Target Fund shareholders?

|

| A. |

No. The Reorganization will result in lower investment advisory fees for Target Fund shareholders. The Acquiring Fund will retain the same investment advisory fee schedule after the Reorganization,

which is an annual rate of 1.65% of average daily net assets. The Target Fund pays an investment advisory fee at the annual rate of 1.75% of average daily net assets.

|

| Q. |

Will the Reorganization result in higher total net operating expenses?

|

| A. |

No. The Target Fund’s Class A, Class C, Class I and Class N shares have a net operating expense of 2.24%, 2.99%, 1.99% and 2.24%, respectively. The Acquiring Fund’s Class A, Class C, Class I and

Class A (as compared to the Target Fund’s Class N) shares currently have a net operating expense ratio of 2.25%, 3.00%, 2.00% and 2.25%, respectively, which includes approximately 0.07% of recoupment of fee waivers previously

waived by the Acquiring Fund’s adviser. The recoupment of previously waived fees is expected to be completed by January 31, 2020, resulting in a pro forma net operating expense ratio of approximately 2.17%, 2.92%, 1.92% and

2.17% after that date for Class A, Class C, Class I and Class A (as compared to Target Fund’s Class N) shares, respectively.

|

| Q. |

What are the U.S. federal income tax consequences of the Reorganization?

|

| A. |

The Reorganization is expected to qualify as a tax-free reorganization for U.S. federal income tax purposes (under section 368(a) of the Internal Revenue Code of 1986, as amended) (the “Code”) and will

not take place unless counsel provides an opinion to that effect. Assuming the Reorganization so qualifies, shareholders should not recognize any capital gain or loss for federal income tax purposes as a direct result of the

Reorganization. Prior to the Closing Date, the futures positions held by the Target Fund’s Cayman Fund will be converted to cash. As a result, you may receive an additional taxable distribution of ordinary income and/or capital

gains that the Target Fund has accumulated prior to the date of the distribution.

|

As always, if you choose to redeem or exchange your shares (whether before or after the Reorganization), you may realize a taxable gain or loss depending on the performance

of such shares since you acquired them. Shareholders should consult a tax adviser with respect to the tax consequences of the Reorganization and any exchange or redemption.

| Q. |

Will my cost basis for U.S. federal income tax purposes change as a result of the Reorganization?

|

| A. |

Your total cost basis for U.S. federal income tax purposes is not expected to change as a result of the Reorganization. However, since the number of shares you hold after the Reorganization is expected

to be different than the number of shares you held prior to the Reorganization, your average cost basis per share may change.

|

5

| Q. |

Will the service providers to my Fund change?

|

| A. |

Yes. Steben serves as the investment adviser to the Target Fund. LoCorr serves as the investment adviser to the Acquiring Fund and will continue to serve in that capacity following the Reorganization.

|

Steben allocates the Target Fund’s assets among five trading advisors for the Fund’s futures portfolio, Crabel Capital Management, LLC, Millburn Ridgefield Corporation

(“Millburn”), PGR Capital LLP, Revolution Capital Management, LLC (“Revolution”) and Welton Investment Partners, LLC. Additionally, Principal Global Investors, LLC provides subadvisory services to the Target Fund with respect to the Target

Fund’s fixed income strategy. The Acquiring Fund has retained Milburn, Revolution and Graham Capital Management, L.P. to provide subadvisory services with respect to the Acquiring Fund’s futures portfolio and Nuveen Asset Management, LLC

to provide subadvisory services to the Acquiring Fund with respect to its fixed income strategy.

U.S. Bank, N.A., the Target Fund’s custodian, and U.S. Bancorp Global Fund Services, LLC, the Target Fund’s transfer agent and administrator, serve in similar capacities for

the Acquiring Fund and will continue to serve in such capacities following the Reorganization.

Foreside Fund Services, LLC, the Target Fund’s distributor, and KPMG LLP, the Target Fund’s auditor, will not serve in such capacities for the Acquiring Fund following the

Reorganization. Instead, Quasar Distributors, LLC and Cohen & Company, Ltd, the Acquiring Fund’s distributor and auditor, respectively, will continue to serve in such capacities following the Reorganization.

| Q. |

Will there be any sales load, commission or other transactional fee in connection with the Reorganization?

|

| A. |

No. There will be no sales load, commission or other transactional fee in connection with the Reorganization. The full and fractional value of shares of the Target Fund will be exchanged for full and

fractional corresponding shares of the Acquiring Fund having equal value, without any sales load, commission or other transactional fee being imposed. Target Fund Class C shareholders that receive Class C shares of the

Acquiring Fund will be subject to a 1.00% contingent deferred sales charge for any Acquiring Fund Class C shares sold less than one year after the Reorganization. For the purposes of the application of the contingent deferred

sales charge, a Target Fund Class C shareholder’s holding period prior to the close of the Reorganization will count towards the one-year period. Class N shareholders of the Target Fund that receive Class A shares of the

Acquiring Fund pursuant to the Reorganization will be able to purchase additional Class A shares of the Acquiring following the Reorganization on a load-waived basis provided that they qualify to do so. It is expected, based on

the terms of the Acquiring Fund’s currently effective prospectus, that such Class N shareholders will be able to qualify for subsequent load-waived purchases of Acquiring Fund Class A shares after the Reorganization.

|

| Q. |

Can I still add to my existing Target Fund account until the Reorganization?

|

| A. |

Yes. Current Target Fund shareholders may continue to make additional investments until the Closing Date (anticipated to be on or about January 31, 2020), unless the Board of Trustees determines to

limit future investments to ensure a smooth transition of shareholder accounts or for any other reason.

|

| Q. |

Will either Fund pay fees or expenses associated with the Reorganization?

|

| A. |

No. The costs of the Reorganization will be borne by LoCorr. Such costs, including preparation and filing of the Proxy Statement/Prospectus, printing and mailing costs, solicitation costs, board

meeting costs, and legal, accounting and auditor fees, are estimated to be approximately $60,000. However, the Funds will bear any brokerage commissions, transaction costs and similar expenses in connection with any purchases

or sales of securities related to Fund repositioning in connection with the Reorganization, which are expected to be minimal.

|

| Q. |

If shareholders approve the Reorganization, when will the Reorganization take place?

|

| A. |

If Target Fund shareholders approve the Reorganization and other conditions are satisfied or waived, the Reorganization is expected to occur on or about January 31, 2020, or as soon as reasonably

practicable after shareholder approval is obtained. An account in the Acquiring Fund will be set up in your name, and you will receive shares of the corresponding class of shares of the Acquiring Fund. You will receive

confirmation of this transaction following the completion of the Reorganization.

|

6

| Q. |

What happens if the Reorganization is not completed?

|

| A. |

If the proposed Reorganization is not approved by shareholders, the Adviser intends to recommend that the Board of Trustees vote to liquidate the Target Fund. Shareholders would receive a liquidating

distribution on the liquidation date equal to the value of the shares owned. The liquidating distribution would result in a taxable transaction.

|

| Q. |

How many votes am I entitled to cast?

|

| A. |

Each shareholder is entitled to one (1) vote per share held, and fractional votes for fractional shares held, on any matter submitted to a vote at the Meeting.

|

Miscellaneous Matters

| Q. |

Who is eligible to vote?

|

| A. |

Shareholders who owned shares of the Target Fund at the close of business on December 6, 2019 (the “Record Date”) will receive notice of the Meeting and be entitled to be present and vote at the

Meeting.

|

| Q. |

What is the required vote to approve the Proposal?

|

| A. |

Approval of the Plan requires the affirmative vote of a “majority of the outstanding voting securities” as defined under the 1940 Act (such a majority referred to herein as a “1940 Act Majority”) of

the Target Fund. A 1940 Act Majority means the lesser of the vote of (i) 67% or more of the shares of the Target Fund entitled to vote thereon present at the Meeting, if the holders of more than 50% of such outstanding shares

are present in person or represented by proxy; or (ii) more than 50% of such outstanding shares of the Target Fund entitled to vote thereon.

|

A quorum of the Target Fund’s shareholders is required to take action at the Meeting. The presence in person or by proxy of the holders of record of one-third of the Target

Fund’s shares outstanding and entitled to vote at the Meeting constitutes a quorum.

If the necessary quorum to transact business is not obtained at the Meeting or if a quorum is obtained but sufficient votes required to approve the Proposal are not

obtained, the Meeting may be adjourned to a later date in order to solicit additional proxies.

| Q. |

How can I vote my shares?

|

| A. |

You can vote or provide instructions in any one of four ways:

|

| • |

By Internet through the website listed in the proxy voting instructions;

|

| • |

By telephone by calling the toll-free number listed on your proxy card(s) and following the recorded instructions;

|

| • |

By mail, by sending the enclosed proxy card(s) (signed and dated) in the enclosed envelope; or

|

| • |

In person at the Meeting on January 17, 2020.

|

Whichever method you choose, please take the time to read the full text of this Proxy Statement/Prospectus before you vote.

It is important that Target Fund shareholders respond to ensure that there is a quorum for the Meeting. If a quorum is not present or sufficient votes to approve the Proposal are not received

by the date of the Meeting, the Meeting may be adjourned to a later date so that we can continue to seek additional votes.

7

| Q. |

If I vote my proxy now as requested, can I change my vote later?

|

| A. |

Yes. You may revoke your proxy vote at any time before it is voted at the Meeting by (1) delivering a written revocation to the Secretary of the Target Fund; (2) submitting a subsequently executed

proxy vote; or (3) attending the Meeting and voting in person. Even if you plan to attend the Meeting, we ask that you return the enclosed proxy card or vote by telephone or the internet. This will help us to ensure that an

adequate number of shares are present at the Meeting for consideration of the Proposal. Target Fund shareholders should send notices of revocation to Steben Alternative Investment Funds at Steben & Company, 9711

Washingtonian Blvd, Suite 400, Gaithersburg, MD, 20878.

|

8

INTO LOCORR MACRO STRATEGIES FUND

This section provides a summary of certain information with respect to the Reorganization, the Target Fund, and the Acquiring Fund, including but not limited to

comparative information regarding each Fund’s investment objectives, fees and expenses, principal investment strategies and risks, historical performance, and other information. Please note that this is only a brief discussion and is

qualified in its entirety by reference to the complete information contained herein, including the Funds’ prospectuses which are incorporated by reference.

There is no assurance that a Fund will achieve its stated objective. Each Fund is designed for investors seeking long term capital appreciation.

The Target Fund pays Steben an investment advisory fee at an annual rate of 1.75% of the Fund’s average daily net assets, calculated daily and paid monthly.

The Acquiring Fund pays LoCorr an investment advisory fee at an annual rate of 1.65% of the Fund’s average daily net assets, calculated daily and paid monthly. After the

Reorganization, the Acquiring Fund will continue to pay this same fee rate to LoCorr.

The following tables compare the fees and expenses you may bear as an investor in the Target Fund or Acquiring Fund as well as pro forma fees and expenses of the Acquiring

Fund upon the close of the Reorganization. Fees and expenses shown for the Target Fund were determined based on the Fund’s average daily net assets for the annual period ended March 31, 2019 as included in the Target Fund’s prospectus

dated July 29, 2019. Fees and expenses shown for the Acquiring Fund were determined based on the Fund’s average daily net assets for the six months ended June 30, 2019, as included in the Acquiring Fund’s semi-annual shareholder report

dated June 30, 2019.

|

Target Fund Class A

|

Acquiring Fund Class A

|

Acquiring Fund Class A (Pro Forma)

|

|

|

Maximum Sales Charge (Load) Imposed on Purchases

(as a % of offering price)

|

5.75%

|

5.75%

|

5.75%

|

|

Maximum Deferred Sales Charge (Load)

(as a % of original purchase price)

|

1.00%*

|

1.00%**

|

1.00%**

|

|

Maximum Sales Charge (Load) Imposed on

Reinvested Dividends and other Distributions |

None

|

None

|

None

|

|

Redemption Fee

|

None

|

None

|

None

|

|

Management fee

|

Target Fund Class C

|

Acquiring Fund Class C

|

Acquiring Fund Class C (Pro Forma)

|

|

Maximum Sales Charge (Load) Imposed on Purchases

(as a % of offering price)

|

None

|

None

|

None

|

|

Maximum Deferred Sales Charge (Load)

(as a % of original purchase price)

|

1.00%***

|

1.00%***

|

1.00%***

|

|

Maximum Sales Charge (Load) Imposed on

Reinvested Dividends and other Distributions |

None

|

None

|

None

|

|

Redemption Fee

|

None

|

None

|

None

|

9

|

Target Fund Class I

|

Acquiring Fund Class I

|

Acquiring Fund Class I (Pro Forma)

|

|

|

Maximum Sales Charge (Load) Imposed on Purchases

(as a % of offering price)

|

None

|

None

|

None

|

|

Maximum Deferred Sales Charge (Load)

(as a % of original purchase price)

|

None

|

None

|

None

|

|

Maximum Sales Charge (Load) Imposed on

Reinvested Dividends and other Distributions |

None

|

None

|

None

|

|

Redemption Fee

|

1.00%****

|

None

|

None

|

|

Target Fund Class N

|

Acquiring Fund Class A

|

Acquiring Fund Class A (Pro Forma)

|

|

|

Maximum Sales Charge (Load) Imposed on Purchases

(as a % of offering price)

|

None

|

5.75%

|

5.75%

|

|

Maximum Deferred Sales Charge (Load)

(as a % of original purchase price)

|

None

|

1.00%**

|

1.00%**

|

|

Maximum Sales Charge (Load) Imposed on

Reinvested Dividends and other Distributions |

None

|

None

|

None

|

|

Redemption Fee

|

1.00%****

|

None

|

None

|

* If purchase is $1 million or more and shareholder redeems within 18 months.

** Applied to purchases of $1 million or more that are redeemed within 12 months of their purchase.

*** Applied to shares redeemed within 12 months of their purchase.

**** As a percentage of the amount redeemed, if sold within 30 days of the purchase of shares.

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of

your investment)

|

Target Fund Class A

|

Acquiring Fund Class A

|

Acquiring Fund Class A (Pro Forma)

|

|

|

Management Fees

|

1.75%

|

1.65%

|

1.65%

|

|

Distribution and/or Service (12b-1) Fees

|

0.25%

|

0.25%

|

0.25%

|

|

Other Expenses

|

0.24%(1)

|

0.34%

|

0.26%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%(2)

|

0.01%(2)

|

|

Total Annual Fund Operating Expenses

|

2.24%

|

2.25%

|

2.17%

|

|

Target Fund Class C

|

Acquiring Fund Class C

|

Acquiring Fund Class C (Pro Forma)

|

|

|

Management Fees

|

1.75%

|

1.65%

|

1.65%

|

|

Distribution and/or Service (12b-1) Fees

|

1.00%

|

1.00%

|

1.00%

|

|

Other Expenses

|

0.24%(1)

|

0.34%

|

0.26%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%(2)

|

0.01%(2)

|

|

Total Annual Fund Operating Expenses

|

2.99%

|

3.00%

|

2.92%

|

|

Target Fund Class I

|

Acquiring Fund Class I

|

Acquiring Fund Class I (Pro Forma)

|

|

|

Management Fees

|

1.75%

|

1.65%

|

1.65%

|

|

Distribution and/or Service (12b-1) Fees

|

0.00%

|

0.00%

|

0.00%

|

|

Other Expenses

|

0.24%(1)

|

0.34%

|

0.26%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%(2)

|

0.01%(2)

|

|

Total Annual Fund Operating Expenses

|

1.99%

|

2.00%

|

1.92%

|

10

|

Target Fund Class N

|

Acquiring Fund Class A

|

Acquiring Fund Class A (Pro Forma)

|

|

|

Management Fees

|

1.75%

|

1.65%

|

1.65%

|

|

Distribution and/or Service (12b-1) Fees

|

0.25%

|

0.25%

|

0.25%

|

|

Other Expenses

|

0.24%(1)

|

0.34%

|

0.26%

|

|

Acquired Fund Fees and Expenses

|

0.00%

|

0.01%(2)

|

0.01(2)

|

|

Total Annual Fund Operating Expenses

|

2.24%

|

2.25%

|

2.17%

|

(1) “Other Expenses” include the expenses of the Cayman Fund, the Target Fund’s consolidated wholly owned subsidiary. Pursuant to an Operating Services Agreement with the Target Fund, the

Target Fund pays Steben 0.24% of the Target Fund’s average daily net assets and Steben has contractually agreed to pay all of the Target Fund’s ordinary expenses including the Target Fund’s acquired fund fees and expenses (which are

indirect fees and expenses that the Target Fund incurs from investing in the shares of other mutual funds, including money market funds and exchange traded funds) and the organizational and offering expenses but not the following Target

Fund expenses: the Management Fee, the Distribution/Servicing Fee, borrowing costs, interest expenses, brokerage commissions and other transaction and investment-related costs, taxes, litigation and indemnification expenses, judgments and

other extraordinary expenses not incurred in the ordinary course of the Target Fund’s business. The fees paid to Steben under the Operating Services Agreement may exceed the Target Fund’s actual ordinary operating expenses. This Operating

Services Agreement may be terminated at any time by the Target Fund’s Board of Trustees.

(2) Acquired Fund Fees and Expenses are the indirect costs of investing in other investment companies. The operating expenses in this fee table will not correlate to the expense ratio in the

Acquiring Fund’s financial highlights because the financial statements include only the direct operating expenses incurred by the Acquiring Fund.

LoCorr has contractually agreed to reduce its fees and/or absorb expenses of the Acquiring Fund, until at least April 30, 2021 to ensure that Total Annual Fund Operating Expenses After Fee

Waiver and/or Reimbursement (exclusive of any Rule 12b-1 distribution and/or servicing fees, taxes, interest, brokerage commissions, expenses incurred in connection with any merger or reorganization, dividend expenses on short sales, swap

fees, indirect expenses, expenses of other investment companies in which the Fund may invest, or extraordinary expenses such as litigation expenses and inclusive of offering and organizational costs incurred prior to the commencement of

operations) will not exceed 1.99% of the Acquiring Fund’s daily average net assets attributable to each class of the Acquiring Fund. These fee waivers and expense reimbursements are subject to possible recoupment from the Acquiring Fund

within three years following the date on which the fee waiver or expense reimbursement occurred, if the Acquiring Fund is able to make the repayment without exceeding the expense limitation in place at the time of waiver or its current

expense limitations and the repayment is approved by the Acquiring Fund’s Board of Trustees. This agreement may be terminated only by the Acquiring Fund’s Board of Trustees, on 60 days’ written notice to LoCorr.

Annual Fund Operating Expenses are paid out of a Fund’s assets and include fees for Fund management, administration and administrative services, including recordkeeping,

accounting or sub-accounting, and other shareholder services, as well as acquired fund fees and expenses. You do not pay these fees directly, but as the examples in the tables below show, these costs are borne indirectly by all

shareholders.

Examples

The Examples are intended to help you compare the cost of investing in the Funds with the cost of investing in other mutual funds. The Examples assume that you invest

$10,000 in the Funds for the time periods indicated and then redeem all of your shares at the end of those periods. The Examples also assume that your investment has a 5% return each year and that the Funds’ operating expenses remain the

same. The Examples also disregard the effect of any recapture of previously waived fees or reimbursed expenses after Year 1 for the Acquiring Fund. Although your actual costs may be higher or lower, based on these assumptions your costs

would be:

|

1 year

|

3 years

|

5 years

|

10 years

|

|

|

Target Fund

(Class A) |

$789

|

$1,235

|

$1,706

|

$3,002

|

|

Acquiring Fund (Class A)

|

$790

|

$1,224

|

$1,683

|

$2,949

|

|

Pro Forma Fund (Class A)

|

$782

|

$1,215

|

$1,672

|

$2,934

|

11

|

Target Fund

(Class C) |

$402*

|

$924

|

$1,572

|

$3,308

|

|

Acquiring

Fund (Class C) |

$403**

|

$913

|

$1,549

|

$3,257

|

|

Pro Forma Fund (Class C)

|

$395***

|

$904

|

$1,538

|

$3,242

|

|

Target Fund

(Class I)

|

$202

|

$624

|

$1,073

|

$2,317

|

|

Acquiring

Fund (Class I) |

$203

|

$613

|

$1,048

|

$2,259

|

|

Pro Forma Fund (Class I)

|

$195

|

$603

|

$1,037

|

$2,243

|

|

Target Fund (Class N)

|

$227

|

$700

|

$1,200

|

$2,575

|

|

Acquiring Fund (Class A)

|

$790

|

$1,224

|

$1,683

|

$2,949

|

|

Pro Forma Fund (Class A)

|

$782

|

$1,215

|

$1,672

|

$2,934

|

* If you held your shares instead of redeeming at the end of the period, your expenses would be $302.

** If you held your shares instead of redeeming at the end of the period, your expenses would be $303.

***If you held your shares instead of redeeming at the end of the period, your expenses would be $295.

Each Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate

higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the Examples, affect each Fund’s performance. During

each Fund’s most recent fiscal year, the Target Fund’s Fund turnover rate was 19.02% of the average value of its portfolio and the Acquiring Fund’s Fund turnover rate was 105% of the average value of its portfolio.

12

|

Target Fund

|

Acquiring Fund

|

|

Investment Objectives

|

|

|

The Fund seeks to achieve positive long term absolute returns with low correlation to broad equity and fixed

income market returns.

|

The Fund's primary investment objective is capital appreciation in rising

and falling equity markets with managing volatility as a secondary objective.

|

The following is intended to show the primary similarities and differences between the Funds’ principal investment strategies. The Funds’ investment objectives, policies

and strategies are similar from an investment perspective in that both Funds pursue a managed futures investment strategy through a wholly-owned subsidiary, as well as a fixed income investment strategy. The Acquiring Fund will continue

to have the same investment strategies shown below following the Reorganization. This information is qualified in its entirety by the prospectuses of each Fund.

|

Target Fund

|

Acquiring Fund

|

|

Principal Investment Strategy – Managed Futures

|

|

|

The Fund seeks to achieve its investment objective by pursuing a managed futures strategy which intends to capture

absolute returns in the commodity and financial futures markets (equity, interest rate and currency) by investing in:

• futures

contracts (such as currency futures, futures on broad-based security indices and futures on commodities);

• foreign

currency transactions (such as U.S. and foreign spot currencies and currency forward contracts); and

• options

on futures and swaps (collectively, Derivative Instruments).

The Fund may invest directly in Derivative Instruments or it may invest up to 25% of its total assets at the time

of purchase in a wholly owned and controlled subsidiary (Subsidiary) to pursue its managed futures strategy through investments in Derivative Investments. The principal investment strategies of the Subsidiary are the same as the

principal investment strategies of the Fund.

The Fund’s adviser generally expects that the Fund’s performance will have a low correlation to the long-term

performance of the general global equity, fixed income, currency and commodity markets; however, the Fund’s performance may correlate to the performance of any one or more of those markets over short-term periods.

The Fund invests in the Subsidiary to gain exposure to the commodities markets within the limitations of the

federal tax laws, rules and regulations that apply to regulated investment companies. The Subsidiary invests exclusively in any of the investments named above or may use a combination of such investments. Such investment exposure

could far exceed the value of the Subsidiary’s portfolio and its investment performance could be primarily dependent upon investments it does not own. The Subsidiary complies with the same asset coverage requirements under the

Investment Company Act of 1940, as amended (1940 Act) with respect to its investments in Derivative Instruments that are applicable to the Fund’s transactions in derivatives. The Subsidiary is organized under the laws of the

Cayman Islands.

|

The Managed Futures strategy is designed to produce capital appreciation by capturing returns related to the

commodity and financial markets by investing long or short in: (i) futures, (ii) forwards, (iii) options, (iv) spot contracts, or (v) swaps, each of which may be tied to (a) currencies, (b) interest rates, (c) stock market

indices, (d) energy resources, (e) metals or (f) agricultural products. These derivative instruments are used as substitutes for securities, interest rates, currencies and commodities and for hedging. To the extent the Fund

uses swaps or structured notes under the Managed Futures strategy, the investments will generally have payments linked to commodity or financial derivatives. The Fund does not invest more than 25% of its assets in contracts with

any one counterparty. Managed futures sub-strategies may include investment styles that rely upon buy and sell signals generated from technical analysis systems such as trend-pattern recognition, as well as from fundamental

economic analysis and relative value comparisons. Managed Futures strategy investments will be made without restriction as to country.

The Fund will execute its Managed Futures strategy primarily by investing up to 25% of its total assets

(measured at the time of purchase) in a wholly-owned and controlled subsidiary (the “Subsidiary”). The Subsidiary will invest primarily in futures, forwards, options, spot contracts, swaps, and other assets intended to serve as

margin or collateral for derivative positions. The Subsidiary is subject to the same investment restrictions as the Fund.

|

13

|

Target Fund

|

Acquiring Fund

|

|

Use of Outside Managers

|

|

|

The Fund utilizes managers who employ a variety of managed futures trading strategies (Trading Advisors). The

managed futures strategies to which the Fund seeks exposure typically include the following investment styles:

• trend

following - quantitative and other strategies are used to identify underlying market trends over various time frames in prices to seek to exploit the market’s tendency to exhibit consecutive periods of price advances and/or

declines

• short-term

systematic and discretionary trading - quantitative strategies are used in an attempt to exploit short-term price patterns in financial and commodity markets

• counter-trend

or mean reversion strategies - quantitative and other methods are used in an attempt to forecast price reversals over various time frames

The managed futures programs employed by the Trading Advisors have a wide variety of trading styles across a broad

range of financial markets and asset classes. Managed futures strategies typically invest either long or short in one or a combination of Derivative Instruments for both speculative and hedging purposes, each of which may be tied

to (a) agricultural products, (b) currencies, (c) equity (stock market) indices, (d) energy, (e) fixed income and interest rates, (f) metals or (g) other commodities.