United States

Securities and Exchange Commission

Washington, D.C. 20549

FORM 10-K

(Mark One)

| [X] | ANNUAL REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2016

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number 0-54402

BIORESTORATIVE THERAPIES, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 91-1835664 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S.

Employer Identification No.) |

| 40 Marcus Drive, Melville, New York | 11747 | |

| (Address of principal executive offices) | (Zip Code) |

(631) 760-8100

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |

| None | Not applicable |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value $0.001 per share

(Title of Class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer”” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] |

| Non-accelerated [ ] (Do not check if a smaller reporting company) | Smaller reporting company [X] |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X]

As of June 30, 2016, the aggregate market value of the registrant’s common stock held by non-affiliates of the registrant was $9,795,332 based on the closing sale price as reported on the OTCQB market. As of March 15, 2017, there were 5,276,027 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

None

INDEX

| 2 |

This Annual Report contains forward-looking statements as that term is defined in the federal securities laws. The events described in forward-looking statements contained in this Annual Report may not occur. Generally these statements relate to business plans or strategies, projected or anticipated benefits or other consequences of our plans or strategies, projected or anticipated benefits from acquisitions to be made by us, or projections involving anticipated revenues, earnings or other aspects of our operating results. The words “may,” “will,” “expect,” “believe,” “anticipate,” “project,” “plan,” “intend,” “estimate,” and “continue,” and their opposites and similar expressions are intended to identify forward-looking statements. We caution you that these statements are not guarantees of future performance or events and are subject to a number of uncertainties, risks and other influences, many of which are beyond our control, that may influence the accuracy of the statements and the projections upon which the statements are based. Factors which may affect our results include, but are not limited to, the risks and uncertainties discussed in Item 7 of this Annual Report under “Factors That May Affect Future Results and Financial Condition”.

Any one or more of these uncertainties, risks and other influences could materially affect our results of operations and whether forward-looking statements made by us ultimately prove to be accurate. Our actual results, performance and achievements could differ materially from those expressed or implied in these forward-looking statements. We undertake no obligation to publicly update or revise any forward-looking statements, whether from new information, future events or otherwise.

Intellectual Property

This Annual Report includes references to our federally registered trademarks, BioRestorative Therapies, the Dragonfly Logo, brtxDISC, ThermoStem, Stem Cellutrition, Stem Pearls and Stem the Tides of Time. The Dragonfly Logo is also registered with the U.S. Copyright Office. This Annual Report also includes references to trademarks, trade names and service marks that are the property of other organizations. Solely for convenience, trademarks and trade names referred to in this Annual Report appear without the ®, SM or ™ symbols, and copyrighted content appears without the use of the symbol ©, but the absence of use of these symbols does not reflect upon the validity or enforceability of the intellectual property owned by us or third parties.

| 3 |

| ITEM 1. | BUSINESS. |

(a) Business Development

As used in this Annual Report on Form 10-K (the “Annual Report”), references to the “Company”, “we”, “us”, or “our” refer to BioRestorative Therapies, Inc. and its subsidiaries.

We were incorporated in Nevada on June 13, 1997. On August 15, 2011, we changed our name from “Stem Cell Assurance, Inc.” to “BioRestorative Therapies, Inc.” Effective January 1, 2015, we reincorporated in Delaware.

During the year ended December 31, 2016, we raised an aggregate of $3,711,236 in connection with sales of common stock and warrants and from the exercise of warrants, and an aggregate of $1,345,470 in net debt financing. As of December 31, 2016, our outstanding debt of $2,336,565, together with interest at rates ranging between 0% and 15% per annum, was due through October 2017. Subsequent to December 31, 2016 and through March 15, 2017, we have received aggregate equity proceeds (including proceeds received from the exercise of common stock purchase warrants) and debt proceeds of $945,000 and $200,000, respectively, debt and accrued interest of $325,000 and $9,679, respectively, has been converted into or exchanged for common stock, $89,000 of debt and net short-term advances have been repaid and the due date for the repayment of $322,000 of debt has been extended through April 2017. Giving effect to the above actions, we currently have notes payable aggregating $427,500 which are past due.

In February 2016, Robert B. Catell joined our Board of Directors. See Item 10 (“Directors, Executive Officers and Corporate Governance”).

Between March 2016 and September 2016, we sold to John M. Desmarais, one of our directors and principal stockholders, an aggregate of 330,000 shares of our common stock at an aggregate purchase price of $1,240,000. In June 2016, we borrowed $500,000 from a trust for which Mr. Desmarais serves as a trustee and which was established for the benefit of his immediate family. See Item 10 (“Directors, Executive Officers and Corporate Governance”) and Item 13 (“Certain Relationship and Related Transactions, and Director Independence”).

In January 2017, we announced that we had submitted an investigational new drug, or an IND, application to the U.S. Food and Drug Administration, or the FDA, to obtain clearance to commence a Phase 2 clinical trial using our lead cell therapy candidate, BRTX-100, to treat chronic lower back pain due to degenerative disc disease related to protruding/bulging discs. In February 2017, we received such clearance from the FDA.

| 4 |

(b) Business

General

We develop therapeutic products and medical therapies using cell and tissue protocols, primarily involving adult (non-embryonic) stem cells. Our two core programs, as described below, relate to the treatment of disc/spine disease and metabolic disorders:

| ● | Disc/Spine Program (brtxDisc). Our lead cell therapy candidate, BRTX-100, is a product formulated from autologous (or a person’s own) cultured mesenchymal stem cells, or MSCs, collected from the patient’s bone marrow. We intend that the product will be used for the non-surgical treatment of protruding and bulging lumbar discs in patients suffering from chronic lumbar disc disease. The BRTX-100 production process involves collecting bone marrow from a patient, isolating and culturing stem cells from the bone marrow and cryopreserving the cells. In an outpatient procedure, BRTX-100 is to be injected by a physician into the patient’s damaged disc. The treatment is intended for patients whose pain has not been alleviated by non-surgical procedures or conservative therapies and who potentially face the prospect of surgery. In January 2017, we submitted an IND application to the FDA to obtain clearance to commence a Phase 2 clinical trial using our lead cell therapy candidate, BRTX-100, to treat chronic lower back pain due to degenerative disc disease related to protruding/bulging discs. In February 2017, we received such clearance from the FDA. We intend to commence such clinical trial during the fourth quarter of 2017. See “Disc/Spine Program” below. | |

| ● | Metabolic Program (ThermoStem). We are developing a cell-based therapy to target obesity and metabolic disorders using brown adipose (fat) derived stem cells, or BADSC, to generate brown adipose tissue, or BAT. We refer to this as our ThermoStem Program. BAT is intended to mimic naturally occurring brown adipose depots that regulate metabolic homeostasis in humans. Initial preclinical research indicates that increased amounts of brown fat in the body may be responsible for additional caloric burning, as well as reduced glucose and lipid levels. Researchers have found that people with higher levels of brown fat may have a reduced risk for obesity and diabetes. In March 2014, we entered into a Research Agreement with Pfizer, Inc., a global pharmaceutical company, pursuant to which we were engaged to provide research and development services with regard to a joint study of the development and validation of a human brown adipose (fat) cell model. A United States patent related to the ThermoStem Program issued in September 2015. See “Metabolic Brown Adipose (Fat) Program” below. |

We have also licensed a curved needle device designed to deliver cells and/or other therapeutic products or material to the spine and discs. In August 2015, a United States patent for this device was issued to the licensor, Regenerative Sciences, LLC. See “Curved Needle Device” below.

In addition, we have developed a human cellular extract that has been demonstrated in in vitro skin studies to increase the production of collagen and fibronectin, which are proteins that are essential to combating the aging of skin. We also offer plant stem cell-based facial creams and beauty products under the Stem Pearls brand. See “Cosmetic Products” below.

Overview

Every human being has stem cells in his or her body. These cells exist from the early stages of human development until the end of a person’s life. Throughout our lives, our body continues to produce stem cells that regenerate to produce differentiated cells that make up various aspects of the body such as skin, blood, muscle and nerves. These are generally referred to as adult (non-embryonic) stem cells. These cells are important for the purpose of medical therapies aiming to replace lost or damaged cells or tissues or to otherwise treat disorders.

| 5 |

Regenerative cell therapy relies on replacing diseased, damaged or dysfunctional cells with healthy, functioning ones or repairing damaged or diseased tissue. A great range of cells can serve in cell therapy, including cells found in peripheral and umbilical cord blood, bone marrow and adipose (fat) tissue. Physicians have been using adult stem cells from bone marrow to treat various blood cancers for 60 years (the first successful bone marrow transplant was performed in 1956). Recently, physicians have begun to use stem cells to treat various other diseases. We intend to develop cell and tissue products and regenerative therapy protocols, primarily involving adult stem cells, to allow patients to undergo cellular-based treatments.

We intend to concentrate initially on therapeutic areas in which risk to the patient is low, recovery is relatively easy, results can be demonstrated through sufficient clinical data, and patients and physicians will be comfortable with the procedure. We believe that there will be readily identifiable groups of patients who will benefit from these procedures.

Accordingly, we have focused our initial efforts in offering cellular-based therapeutic products and treatment programs in selective areas of medicine for which the treatment protocol is minimally invasive. Such areas include the treatment of the disc and spine and metabolic-related disorders. We will seek to obtain third party reimbursement for our products and procedures; however; patients may be required to pay for our products and procedures out of pocket in full and without the ability to be reimbursed by any governmental and other third party payers.

We have obtained a patent, as well as licenses, for the exclusive use of a patent and a patent pending and have undertaken research and development efforts in connection with the development of therapeutic products and medical therapies using cell and tissue protocols, primarily involving adult stem cells. See “Disc/Spine Program”, “Metabolic Brown Adipose (Fat) Program” and “Curved Needle Device” below.

We have developed a human adult stem cell-derived extract that, when applied to human skin cells, significantly increases the production of collagen and fibronectin, which are proteins that are essential to combating the aging of skin. We also offer plant stem cell derived facial creams and beauty products under the Stem Pearls brand. See “Cosmetic Products” below.

We have established a laboratory facility and will seek to further develop cellular-based treatments, products and protocols, stem cell-related intellectual property, or IP, and translational research applications. See “Laboratory” below.

We have not generated any significant revenues from our operations. The implementation of our business plan, as discussed below, will require the receipt of sufficient equity and/or debt financing to purchase necessary equipment, technology and materials, fund our research and development efforts, retire our outstanding debt (see Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations - Liquidity and Capital Resources – Availability of Additional Funds”) and otherwise fund our operations. We intend to seek such financing from current shareholders and debtholders as well as from other accredited investors. We also intend to seek to raise capital through investment bankers and from biotech funds, strategic partners and other financial institutions. We anticipate that we will require between $8,000,000 and $10,000,000 in financing to commence and complete a Phase 2 clinical trial and we will require between $20,000,000 and $30,000,000 in further additional funding to complete our clinical trials using BRTX-100, as further discussed in this Item 1 (assuming the receipt of no revenues from operations), repay our outstanding debt ($2,336,565 as of December 31, 2016) (assuming that no debt is converted into equity) and fund general operations. We will also require a substantial amount of additional funding to implement our other programs discussed in this Item 1. No assurance can be given that the anticipated amounts of required funding are correct or that we will be able to accomplish our goals within the timeframes projected. In addition, no assurance can be given that we will be able to obtain any required financing on commercially reasonable terms or otherwise. We may also seek to have our debtholders convert all or a portion of their debt into equity. No assurance can be given that we will be able to convert such debt into equity on commercially reasonable terms or otherwise. If we are unable to obtain adequate funding, we may be required to significantly curtail or discontinue our proposed operations. See Item 7 (“Management’s Discussion and Analysis of Financial Condition and Results of Operations – Factors That May Affect Future Results and Financial Condition - We will need to obtain additional financing to satisfy debt obligations and continue our operations.”).

| 6 |

Disc/Spine Program

General

Among the initiatives that we are currently pursuing is our Disc/Spine Program, with our initial product being called BRTX-100. We have obtained a license (see “License” below) that permits us to use technology for adult stem cell treatment of disc and spine conditions, including protruding and bulging discs. The technology is an advanced stem cell culture and injection procedure into the intervertebral disc, or IVD, that may offer relief from lower back pain, buttock and leg pain, and numbness and tingling in the legs and feet.

Lower back pain is the most common, most disabling, and most costly musculoskeletal ailment faced worldwide. According to a recent market report, there are nearly 25 million people in the United States with chronic lower back pain of which approximately 5 million have pain caused by a protruding or bulging disc. We believe that between 500,000 and 1 million of these back pain sufferers will have an invasive surgical procedure to try to alleviate the pain associated with these lower back conditions. Clinical studies have documented that the source of the pain is most frequently damage to the IVD. This can occur when forces, whether a single load or repetitive microtrauma, exceed the IVD’s inherent capacity to resist those loads. Aging, obesity, smoking, lifestyle, and certain genetic factors may predispose one to an IVD injury.

While once thought to be benign, the natural history of lower back pain is often one of chronic recurrent episodes of pain leading to progressive disability. This is believed to be a direct result of the IVD’s poor healing capacity after injury. The IVD is the largest avascular (having few or no blood vessels) structure in the body and is low in cellularity. Therefore, its inherent capacity to heal after injury is poor. The clinical rationale of BRTX-100 is to deliver a high concentration of the patient’s own MSCs into the site of pathology to promote healing and relieve pain.

We have developed a mesenchymal stem cell product, BRTX-100, derived from autologous (or a person’s own) human bone marrow, cultured and formulated to be delivered into a protruding or bulging disc.

In January 2017, we announced that we had submitted an IND application to the FDA to obtain clearance to commence a Phase 2 clinical trial using our lead cell therapy candidate, BRTX-100, to treat chronic lower back pain due to degenerative disc disease related to protruding/bulging discs. In February 2017, we received such clearance from the FDA. We intend to commence such clinical trial during the fourth quarter of 2017.

| 7 |

In addition to developing BRTX-100, we may also seek to sublicense the technology to third parties for use in connection with cellular-based treatment programs with regard to disc and spine related conditions.

We have established a laboratory, which includes a clean room facility, to perform the production of cell products (including BRTX-100) for use in our clinical trials. We intend to certify the operation of the cleanroom by the third quarter of 2017. This capability may also enable us to develop our pipeline of future products and expand our stem cell-related IP. See “Laboratory” and “Technology; Research and Development” below.

BRTX-100

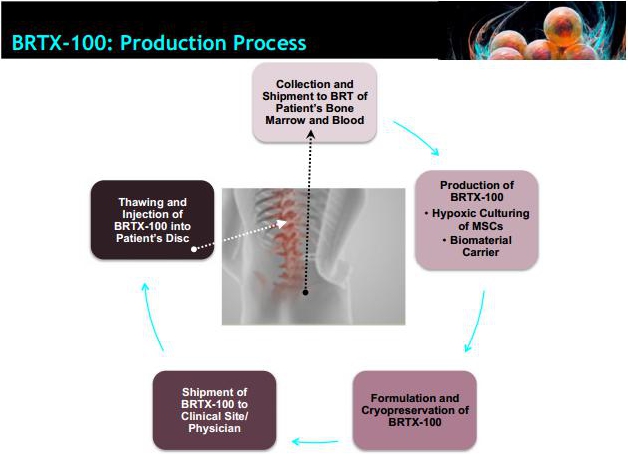

Our lead therapeutic product, BRTX-100, is an autologous hypoxic (low oxygen) cultured mesenchymal stem cell product derived from a patient’s bone marrow and formulated with a proprietary carrier. The cryopreserved sterile cellular product will be provided to the clinician in vials for injection into damaged lumbar discs. The therapeutic delivery of BRTX-100, in treatment of chronic lumbar disc disease, is performed using a standard 20 gauge 3.5 inch introducer needle and a 25 gauge 6 inch needle that extends into the disc region where the product is delivered. Specific medical practitioners will be provided training using the product with regard to the injection procedure. It is anticipated that the treatment and delivery of the product will be a 30 minute outpatient procedure.

MSCs used in BRTX-100 are similar to other MSCs under development by others; however, in order to enhance the survivability of our bone marrow-derived MSCs in the avascular environment of the damaged disc, BRTX-100 is expanded under hypoxic conditions for a period of approximately three weeks. This process results in a cell population with enhanced viability and therapeutic potential following injection locally into injured spinal discs. Publications and scientific literature have indicated that MSCs preconditioned in hypoxic environment show enhanced skeletal muscle regeneration, improved blood flow and vascular formation compared to MSCs cultured under normoxic (normal oxygen) conditions.

Production and Delivery

The production of BRTX-100 begins with the physician collecting bone marrow from the patient under a local anesthesia. Peripheral blood is also collected from the patient. The physician will then send the patient’s bone marrow and blood samples to our laboratory (or a contract laboratory) for culturing and formulation. The hypoxic culturing process applied is intended to result in the selection of a cell population that is suitable for an improved possibility of survival in the internal disc environment. The cell culturing process and product formulation will take approximately three weeks, with an additional two weeks required for quality control testing required to meet product release criteria. We will then send the therapeutic cryopreserved stem cells (BRTX-100) in a sterile vial back to the physician’s offices where it will be thawed prior to the procedure. The price structure for the procedure and our services has not been determined and no assurances can be given in this regard. The following illustrates the process.

| 8 |

License

Pursuant to our license agreement with Regenerative Sciences, LLC, or Regenerative, that became effective in April 2012, we have obtained, among other things, a worldwide (excluding Asia and Argentina), exclusive, royalty-bearing license from Regenerative to utilize or sublicense a certain method for culturing cells for use in treating, among other things, disc and spine conditions, including protruding and bulging discs. The technology that has been licensed is an advanced stem cell culture and injection procedure that may offer relief from lower back pain, buttock and leg pain, and numbness and tingling in the legs and feet. Pursuant to the license agreement, we have also obtained a worldwide, exclusive, royalty-bearing license from Regenerative to utilize or sublicense a certain curved needle device for the administration of specific cells and/or cell products to the disc and/or spine (and other parts of the body). It will be necessary to advance the design of this medical device to facilitate the delivery of substances, including living cells, to specific locations within the body and minimize the potential for damage to nearby structures.

The license agreement provides for the requirement that we achieve certain milestones or pay certain minimum royalty amounts in order to maintain the exclusive nature of the licenses. The license agreement also provides for a royalty-bearing sublicense of certain of the technology to Regenerative for use for certain purposes, including in the United States and the Cayman Islands. Further, the license agreement requires that Regenerative furnish certain training, assistance and consultation services with regard to the licensed technology.

| 9 |

Animal Study

The efficacy and safety of BRTX-100 has been tested in a degenerative intervertebral rabbit disc model. In this study, 80 rabbits underwent surgery to create a puncture in the discs. Four weeks post surgery, each rabbit had either contrast, a biomaterial carrier or BRTX-100 injected into the discs. In order to study the biodistribution and efficacy of BRTX-100, the rabbits were evaluated at day 56 and day 120.

The key safety findings of the animal study are as follows:

| ● | There was no evidence or observation of gross toxicity related to the administration of BRTX-100 at either time point. The clinical pathology across both groups and time points were within expected normal historical ranges and under the conditions of the test. No abnormalities (including fractures or overt signs of lumbar disc disease) were identified after review of the radiographic images taken at both endpoints for both groups. No toxicity or adverse finding was evident in the systemic tissues or the discs of animals receiving BRTX-100. | |

| ● | There was no detectable presence of human cells (BRTX-100) observed at the day 56 interim time point. This is consistent with the proposed mechanism of action that BRTX-100 acts through a paracrine effect of secreted growth and immunomodulation factors. |

The key efficacy findings of the animal study are as follows:

| ● | BRTX-100 showed a statistically significant DHI (disc height increase) over the control group at day 120. | |

| ● | BRTX-100 showed a statistically significant improvement in disc histology over the control group at day 120 as graded by a validated histology scale. BRTX-100 showed a significant improvement in the cellularity and matrix of the disc when compared to the control at day 120. |

Clinical Trial

In December 2014, we held a pre-IND meeting with the FDA’s Office of Cellular Tissue and Gene Therapies within the FDA’s Center for Biologics, Evaluation and Research. At the meeting, representatives of the FDA commented on our plans for an IND submission and a clinical trial with regard to the disc program. The FDA representatives identified certain necessary pre-clinical research and data as well as various suggestions to modify the clinical trial design. We believe that these comments and suggestions will not materially impact our plans for a clinical trial. In January 2017, we announced that we had submitted an IND application to the FDA to obtain clearance to commence a Phase 2 clinical trial using our lead cell therapy candidate, BRTX-100, to treat chronic lower back pain due to degenerative disc disease related to protruding/bulging discs. In February 2017, we received such clearance from the FDA. We intend to commence such clinical trial during the fourth quarter of 2017. One of the principal investigators for our clinical trial is intended to be Dr. Gregory E. Lutz, our Chief Medical Advisor for Spine Medicine. See Item 10 (“Directors, Executive Officers and Corporate Governance-Scientific Advisors”).

| 10 |

The following describes the Phase 2 clinical trial cleared by the FDA:

A Phase 2 Prospective, Double-Blinded, Placebo Controlled, Randomized Study

| ● | General |

| ● | 72 patients; randomized 2:1, BRTX-100 to control | |

| ● | 10-20 clinical trial sites | |

| ● | Primary efficacy endpoint at 6 months | |

| ● | Patient follow up at 12 and 24 months |

| ● | Primary Efficacy Endpoint |

| ● | Responder endpoint - % of patients that meet the improvement in function and reduction in pain threshold | |

| ● | Improvement in function defined as at least a 30% increase in function based on the Oswestry questionnaires (ODI) | |

| ● | Reduction of pain defined as at least a 30% decrease in pain as measured using the Visual Analogue Scale (VAS) |

| ● | Additional or Secondary Endpoints |

| ● | Quality of life assessment | |

| ● | Evolution of affected disc(s) by magnetic resonance imaging (MRI) |

The FDA approval process can be lengthy, expensive and uncertain and there is no guarantee that the clinical trial(s) will be commenced or completed or that the product will ultimately receive approval or clearance. See “Government Regulation” below and Item 7 (“Management’s Discussion and Analysis of Financial Condition and Results of Operations – Factors That May Affect Future Results and Financial Condition – Risks Related to Our Cell Therapy Product Development Efforts; and – Risks Related to Government Regulation”).

Metabolic Brown Adipose (Fat) Program

Since June 2011, we have been engaging in pre-clinical research efforts with respect to a platform technology utilizing brown adipose (fat) derived stem cells for therapeutic purposes. We have labeled this initiative our ThermoStem Program.

Brown fat is a specialized adipose (fat) tissue found in the human body that plays a key role in the evolutionarily conserved mechanisms underlying thermogenesis (generation of non-shivering body heat) and energy homeostasis in mammals - long known to be present at high levels in hibernating mammals and human newborns. Recent studies have demonstrated that brown fat is present in the adult human body and may be correlated with the maintenance and regulation of healthy metabolism, thus potentially being involved in caloric regulation. The pre-clinical ThermoStem Program involves the use of a cell-based (brown adipose tissue) treatment for metabolic disease, such as type 2 diabetes, obesity, hypertension and other metabolic disorders and cardiac deficiencies. We have had initial success in transplanting the tissue in animals, and we are currently exploring ways to deliver the brown fat tissue into humans. Even though present, BAT mass is very low in healthy adults and even lower in obese populations. Therefore, it may not be sufficient to either naturally impact whole body metabolism, or to be targeted by drugs intended to increase its activity in the majority of the population. Increasing BAT mass is crucial in order to benefit from its metabolic activity and this is what our ThermoStem Program seeks to accomplish. We may also identify other naturally occurring and chemically engineered molecules that may enhance brown adipose tissue performance.

| 11 |

Obesity, the abnormal accumulation of white fat tissue, leads to a number of metabolic disorders and is the driving force behind the rise of type 2 diabetes and cardiovascular diseases worldwide. Pharmacological efforts to alter metabolic homeostasis through modulating central control of appetite and satiety have had limited market penetration due to significant psychological and physiological safety concerns directly attributed to modulating these brain centers. Adipose tissue is one of the largest organs in the human body and plays a key role in central energy balance and lipid homeostasis. Two types of adipose tissues are found in mammals, white and brown adipose tissues. White adipose tissue function is to store energy, whereas BAT specializes in energy expenditure. Recent advancements in unraveling the mechanisms that control the induction, differentiation, proliferation, and thermogenic activity of BAT, along with the application of imaging technologies for human BAT visualization, have generated optimism that these advances may provide novel strategies for targeting BAT activation/thermogenesis, leading to efficacious and safe obesity targeted therapies.

We are developing a cell-based therapy to target obesity and metabolic disorders using BADSC. Our goal is to develop a bioengineered implantable brown adipose tissue intended to mimic ones naturally occurring in the human body. We have isolated and characterized a human multipotent stem cell population that resides within BAT depots. We have expanded these stem cells to clinically relevant numbers and successfully differentiated them into functional brown adipocytes. We intend to use adult stem cells that may be differentiated into progenitor or fully differentiated brown adipocytes, or a related cell type, which can be used therapeutically in patients. We are focusing on the development of treatment protocols that utilize allogeneic cells (i.e., stem cells from a genetically similar but not identical donor).

In order to deliver these differentiated cells into target locations in vivo, we seeded BADSC onto 3-dimensional biological scaffolds. Pre-clinical animal models of diet-induced obesity, that were transplanted with differentiated BADSC supported by a biological scaffold, presented significant reductions in weight and blood glucose levels compared to saline injected controls. We are identifying technology for in vivo delivery in small animal models. Having completed our proof of concept using our BAT in small animals, we are currently developing our next generation BAT. It is anticipated that this next version will contain a higher purity of BADSC, which is expected to increase the therapeutic effect compared to our first generation product. In addition, we are exploring the delivery of the therapeutic using encapsulation technology, which will only allow for reciprocal exchange of small molecules between the host circulation and the BAT implant. We expect that encapsulation may present several advantages over our current biological scaffolds, including prevention of any immune response or implant rejection that might occur in an immunocompetent host and an increase in safety by preventing the implanted cells from invading the host tissues and forming tumors. We have developed promising data on the transplantation of human stem cell-derived tissue engineered brown fat into an encapsulation device to be used as a cell delivery system for our metabolic platform program for the treatment of type 2 diabetes, obesity, hyperlipidemia and hypertension. This advancement may lead to successful transplantation of brown fat in humans. By successfully seeding human BADSC into an encapsulation device, we are advancing the development of our cell therapy program to treat metabolic disorders. This data is expected to progress our program to enable transplanted brown adipose cells to effectively maintain or regulate normal metabolism in humans. We are evaluating the next generation of BAT constructs that will first be tested in small animal models. No assurance can be given that this delivery system will be effective in vivo in animals or humans. Our allogeneic brown adipose derived stem cell platform potentially provides a therapeutic and commercial model for the cell-based treatment of obesity and related metabolic disorders.

| 12 |

In June 2012, we entered into an Assignment Agreement with the University of Utah Research Foundation, or the Foundation, and a Research Agreement with the University of Utah, or the Utah Research Agreement. Pursuant to the Assignment Agreement, which provides for royalty payments, we acquired the rights to two provisional patent applications that relate to human brown fat cell lines. No royalty amounts are payable to date. The applications have been converted to a utility application in the United States and several foreign jurisdictions. Pursuant to the Utah Research Agreement, the University of Utah, or the University, provided research services relating to the identification of brown fat tissue and the development and characterization of brown fat cell lines. The Utah Research Agreement provides that all inventions, discoveries, patent rights, information, data, methods and techniques, including all cell lines, cell culture media and derivatives thereof, are owned by us.

In February 2014, our research with regard to the identification of a population of brown adipose derived stem cells was published in Stem Cells, a respected stem cell journal.

In March 2014, we entered into a Research Agreement with Pfizer Inc, or the Pfizer Research Agreement, a global pharmaceutical company. Pursuant to the Pfizer Research Agreement, we were engaged to provide research and development services with regard to a joint study of the development and validation of a human brown adipose (fat) cell model. The Pfizer Research Agreement provided for an initial payment to us of $250,000 and the payment of up to an additional $525,000 during the two-year term of the Agreement, all of which has been received.

In August 2015, we entered into a one year research collaboration agreement with the University of Pennsylvania with regard to the understanding of brown adipose (fat) biology and its role in metabolic disorders. No amounts are payable by or to us pursuant to this agreement.

In September 2015, a United States patent related to the ThermoStem Program was issued to us.

Following our research activities, we intend to undertake preclinical studies in order to determine whether our proposed treatment protocol is safe. Such studies are planned to begin by the third quarter of 2017. Following the completion of such studies, if required, we intend to file an IND with the FDA and initiate a clinical trial. See “Government Regulation” below and Item 7 (“Management’s Discussion and Analysis of Financial Condition and Results of Operations – Factors That May Affect Future Results and Financial Condition – Risks Related to Our Cell Therapy Product Development Efforts; and – Risks Related to Government Regulation”). The FDA approval process can be lengthy, expensive and uncertain and there is no guarantee of ultimate approval or clearance.

| 13 |

We anticipate that much of our development work in this area will take place at our laboratory facility, outside core facilities at academic, research or medical institutions, or contractors. See “Laboratory” below.

Curved Needle Device

Pursuant to the Regenerative license agreement discussed under “Disc/Spine Program-License” above, we have licensed and further developed a curved needle device, or CND, that is a needle system with a curved inner cannula to allow access to difficult-to-locate regions for the delivery or removal of fluids and other substances. The CND is intended to deliver stem cells and/or other therapeutic products or material to the interior of a human intervertebral disc, the spine region, or potentially other areas of the body. The device relies on the use of pre-curved nested cannulae that allow the cells or material to be deposited in the posterior and lateral aspects of the disc to which direct access is not possible due to outlying structures such as vertebra, spinal cord and spinal nerves. We anticipate that the use of the CND will facilitate the delivery of substances, including living cells, to specific locations within the body and minimize the potential for damage to nearby structures. The device may also have more general use applications. In August 2015, a United States patent for the CND was issued to the licensor, Regenerative Sciences, LLC. We anticipate that FDA approval or clearance will be necessary for the CND prior to commercialization. See “Government Regulation” below and Item 7 (“Management’s Discussion and Analysis of Financial Condition and Results of Operations – Factors That May Affect Future Results and Financial Condition – Risks Related to Our Cell Therapy Product Development Efforts; and – Risks Related to Government Regulation”). The FDA review and approval process can be lengthy, expensive and uncertain and there is no guarantee of ultimate approval or clearance.

Laboratory

We have established a laboratory in Melville, New York for research purposes and have built a cleanroom within the laboratory for the possible production of cell-based therapies, such as BRTX-100, for use in a clinical trial. We intend to certify the operation of the cleanroom by the third quarter of 2017.

As operations grow, our plans include the expansion of our laboratory to perform cellular characterization and culturing, product, protocol and stem cell-related IP development, translational research and therapeutic outcome analysis. As we develop our business and additional stem cell treatments are approved, we will seek to establish ourselves as a key provider of adult stem cells for therapies and expand to provide cells in other market areas for stem cell therapy. We may also use outside laboratories specializing in cell therapy services and manufacturing of cell products.

Technology; Research and Development

We intend to utilize our laboratory or a third party laboratory in connection with cellular research activities. We also intend to seek to obtain cellular-based therapeutic technology licenses and increase our IP portfolio. We intend to seek to develop potential stem cell delivery systems or devices. The goal of these specialized delivery systems or devices is to deliver cells into specific areas of the body, control the rate, amount and types of cells used in a treatment, and populate these areas of the body with sufficient stem cells so that there is a successful therapeutic result.

| 14 |

We also intend to perform research to develop certain stem cell optimization compounds, media or “recipes” to enhance cellular growth and regeneration for the purpose of improving pre-treatment and post-treatment outcomes.

We have two pending United States patent applications with regard to two patent families. We have been issued a United States patent with regard to one of the two patent families. Patent applications with regard to one patent family have been filed in five foreign jurisdictions (of which one application has become inactive). In addition, a Patent Cooperation Treaty, or PCT, application has been filed with regard to a second patent family and such PCT application has been filed in four foreign jurisdictions. Regenerative has filed two patent applications with regard to the technology that is the subject of the license agreement between us (see “Disc/Spine Program-License” above). Regenerative has been issued a patent with regard to its curved needle therapeutic delivery device. Our patent applications and those of Regenerative are currently in prosecution (i.e., we and Regenerative are seeking issued patents). A description of the patent applications and issued patents is set forth below:

| Program | I.D. | Jurisdiction | Title | |||

| Disc/Spine | 13/132,840* | US | Methods and compositions to facilitate repair of avascular tissue | |||

| U.S. Patent No. 9,113,950 B2** | US | Therapeutic delivery device | ||||

| Metabolic | U.S. Patent No. 9,133,438 | US | Brown fat cell compositions and methods

| |||

| 13/932,468 | US | |||||

| 2012275335 | Australia | |||||

| 12743811.7 | Europe | |||||

| 230237 | Israel | |||||

| 2014-519026 | Japan | |||||

| 14/255,595 | US | Human brown adipose derived stem cells and uses | ||||

| PCT/US2014/034540 | Patent Cooperation Treaty | |||||

| 2014253920 | Australia | |||||

| 14729769.1 | Europe | |||||

| 242150 | Israel | |||||

| 2016-509105 | Japan |

| *Patent application filed by licensor, Regenerative Sciences, LLC |

| **Patent issued to licensor, Regenerative Sciences, LLC |

In March 2014, we entered into a Research and Development Agreement with Rohto Pharmaceutical Co., Ltd., a Japanese pharmaceutical company. Pursuant to the Rohto Research and Development Agreement, we were engaged to provide research and development services with regard to stem cells. The Rohto Research and Development Agreement provided for an initial payment to us of $150,000 and the payment of up to an additional $100,000 subject to the satisfaction of certain milestones (all of which has been earned and received). The Rohto Research and Development Agreement expired in June 2015.

In March 2014, we entered into the Pfizer Research Agreement, as discussed above under “Metabolic Brown Adipose (Fat) Program”.

| 15 |

We have secured registrations in the U.S. Patent and Trademark Office for the following trademarks:

| ● |  | |

| ● |  | |

| ● |  | |

| ● | THERMOSTEM | |

| ● | STEM CELLUTRITION | |

| ● | STEM PEARLS, and | |

| ● | STEM THE TIDES OF TIME. |

We also have federal common law rights in the trademarks, BioRestorative Therapies, BRTX-100, and other trademarks used in the conduct of our business that are not registered.

Our success will depend in large part on our ability to develop and protect our proprietary technology. We intend to rely on a combination of patent, trade secret and know-how, copyright and trademark laws, as well as confidentiality agreements, licensing agreements, non-compete agreements and other agreements, to establish and protect our proprietary rights. Our success will also depend upon our ability to avoid infringing upon the proprietary rights of others, for if we are judicially determined to have infringed such rights, we may be required to pay damages, alter our services, products or processes, obtain licenses or cease certain activities. We conduct prior rights searches before launching any new product or service to put us in the best position to avoid claims of infringement.

During the years ended December 31, 2016 and 2015, we incurred $2,883,563 and $2,105,059, respectively, in research and development expenses.

Cosmetic Products

We have developed a human adult stem cell-derived extract that, when applied to human skin cells, significantly increases the production of collagen and fibronectin, which are proteins that are essential to combating the aging of skin. No arrangements with regard to the commercial distribution of products that utilize our extract as a cosmetic ingredient are currently in place or are under consideration.

We offer plant derived stem cell cosmetic products under the Stem Pearls brand. We have not commenced marketing efforts or generated any significant revenue with regard to Stem Pearls products.

| 16 |

Scientific Advisors

We have established a Scientific Advisory Board whose purpose is to provide advice and guidance in connection with scientific matters relating to our business. Our four Scientific Advisory Board members are Dr. Wayne Marasco, Chairman, Dr. Naiyer Imam, Dr. Wayne Olan and Dr. Joy Cavagnaro. In addition, Dr. Gregory Lutz has been retained as our Chief Medical Advisor for Spine Medicine. See Item 10 (“Directors, Executive Officers and Corporate Governance – Scientific Advisors”) for a listing of the principal positions for Drs. Marasco, Imam, Olan, Cavagnaro and Lutz.

Competition

We will compete with many pharmaceutical, biotechnology, and medical device companies, as well as other private and public stem cell companies involved in the development and commercialization of cell-based medical technologies and therapies.

Regenerative medicine is rapidly progressing, in large part through the development of cell-based therapies or devices designed to isolate cells from human tissues. Most efforts involve cell sources, such as bone marrow, adipose tissue, embryonic and fetal tissue, umbilical cord and peripheral blood and skeletal muscle.

Companies working in the area of regenerative medicine with regard to the disc and spine include, among others, Isto Biologics, Harvest Technologies (acquired by Terumo), Celling Biosciences, Mesoblast, Tissue Genesis, Discgenics and Arthrex. Companies that are developing products and therapies to combat obesity, diabetes and other metabolic disorders including through the use of brown fat, include, among others, Pfizer, AstraZeneca, Genentech (acquired by Roche), Eli Lilly, Amgen, Energesis Pharmaceuticals, Sanofi, Novo Nordisk, Johnson & Johnson, Novartis, GlaxoSmithKline, Bristol-Myers Squibb, Mitsubishi Tanabe Pharma, Takeda Pharmaceutical, Vivus, Arena Pharmaceuticals, Teva Pharmaceuticals, Merck, Blu Pharmaceuticals (acquired by PuraCap Pharmaceutical), BioTime, Merz Pharmaceuticals, ViaCyte and Regeneron. Many of our competitors and potential competitors have substantially greater financial, technological, research and development, marketing and personnel resources than we do. We cannot, with any accuracy, forecast when or if these companies are likely to bring their products and therapies to market in competition with those that we are pursuing.

With the enactment of the Biologics Price Competition and Innovation Act of 2009, or BPCIA, an abbreviated pathway for the approval of biosimilar and interchangeable biological products was created. The abbreviated regulatory pathway establishes legal authority for the FDA to review and approve biosimilar biologics, including the possible designation of a biosimilar as “interchangeable” based on its similarity to an existing reference product. Under the BPCIA, an application for a biosimilar product cannot be approved by the FDA until 12 years after the original branded product is approved under a biologics license application, or BLA. Although the FDA has approved several biosimilar products, complex provisions of the law are still being implemented by the FDA and interpreted by the federal courts. As a result, the ultimate impact, implementation, and meaning of the BPCIA are still subject to some uncertainty and FDA actions and court decisions concerning the law could have a material adverse effect on the future commercial prospects for our biological products.

| 17 |

We believe that, if any of our product candidates are approved as a biological product under a BLA, it should qualify for the 12-year period of exclusivity. However, there is a risk that the FDA could permit biosimilar applicants to reference approved biologics other than our therapeutic candidates, thus circumventing our exclusivity and potentially creating the opportunity for competition sooner than anticipated. Additionally, this period of regulatory exclusivity does not apply to companies pursuing regulatory approval via their own traditional BLA, rather than via the abbreviated pathway. Moreover, the extent to which a biosimilar, once approved, will be substituted for any one of our reference products in a way that is similar to traditional generic substitution for non-biological products is not yet clear, and will depend on a number of marketplace and regulatory factors that are still developing.

Customers

Our cell and tissue therapeutic products are intended to be marketed to physicians, other health care professionals, hospitals, research institutions, pharmaceutical companies and the military. It is anticipated that physicians who are trained and skilled in performing spinal injections will be the physicians most likely to treat discs with injections of BRTX-100. These physicians would include interventional physiatrists (physical medicine physicians), pain management-anesthesiologists, interventional radiologists and neurosurgeons.

Governmental Regulation

U.S. Government Regulation

The health care industry is highly regulated in the United States. The federal government, through various departments and agencies, state and local governments, and private third-party accreditation organizations regulate and monitor the health care industry, associated products, and operations. The following is a general overview of the laws and regulations pertaining to our business.

FDA Regulation of Stem Cell Treatment and Products

The FDA regulates the manufacture of human stem cell treatments and associated products under the authority of the Public Health Service Act, or PHSA, and the Federal Food, Drug, and Cosmetic Act, or FDCA. Stem cells can be regulated under FDA’s Human Cells, Tissues, and Cellular and Tissue-Based Products Regulations, or HCT/Ps, or may also be subject to FDA’s drug, biological product, or medical device regulations, each as discussed below.

Human Cells, Tissues, and Cellular and Tissue-Based Products Regulation

Under Section 361 of the PHSA, the FDA issued specific regulations governing the use of HCT/Ps in humans. Pursuant to Part 1271 of Title 21 of the Code of Federal Regulations, or CFR, the FDA established a unified registration and listing system for establishments that manufacture and process HCT/Ps. The regulations also include provisions pertaining to donor eligibility determinations; current good tissue practices covering all stages of production, including harvesting, processing, manufacture, storage, labeling, packaging, and distribution; and other procedures to prevent the introduction, transmission, and spread of communicable diseases.

| 18 |

The HCT/P regulations strictly constrain the types of products that may be regulated solely under these regulations. Factors considered include the degree of manipulation, whether the product is intended for a homologous function, whether the product has been combined with noncellular or non-tissue components, and the product’s effect or dependence on the body’s metabolic function. In those instances where cells, tissues, and cellular and tissue-based products have been only minimally manipulated, are intended strictly for homologous use, have not been combined with noncellular or nontissue substances, and do not depend on or have any effect on the body’s metabolism, the manufacturer is only required to register with the FDA, submit a list of manufactured products, and adopt and implement procedures for the control of communicable diseases. If one or more of the above factors has been exceeded, the product would be regulated as a drug, biological product, or medical device rather than an HCT/P.

Because we are an enterprise in the early stages of operations and have not generated significant revenues from operations, it is difficult to anticipate the likely regulatory status of the array of products and services that we may offer. We believe that some of the adult autologous (self-derived) stem cells that will be used in our cellular therapy and biobanking products and services, including the brown adipose (fat) tissue that we intend to use in our ThermoStem Program, may be regulated by the FDA as HCT/Ps under 21 C.F.R. Part 1271. This regulation defines HCT/Ps as articles “containing or consisting of human cells or tissues that are intended for implantation, transplantation, infusion or transfer into a human recipient.” However, the FDA may disagree with this position or conclude that some or all of our stem cell therapy products or services do not meet the applicable definitions and exemptions to the regulation. If we are not regulated solely under the HCT/P provisions, we would need to expend significant resources to comply with the FDA’s broad regulatory authority under the FDCA. Third party litigation concerning the autologous use of a stem cell mixture to treat musculoskeletal and spinal injuries has increased the likelihood that some of our products and services are likely to be regulated as a drug or biological product and require FDA approval. In the litigation, the FDA asserted that the defendants’ use of cultured stem cells without FDA approval is in violation of the FDCA, claiming that the defendants’ product is a drug. The defendants asserted that their procedure is part of the practice of medicine and therefore beyond the FDA’s regulatory authority. The District Court ruled in favor of the FDA, and in February 2014 the Circuit Court affirmed the District Court’s holding.

If regulated solely under the FDA’s HCT/P statutory and regulatory provisions, once our laboratory in the United States becomes operational, it will need to satisfy the following requirements, among others, to process and store stem cells:

| ● | registration and listing of HCT/Ps with the FDA; | |

| ● | donor eligibility determinations, including donor screening and donor testing requirements; | |

| ● | current good tissue practices, specifically including requirements for the facilities, environmental controls, equipment, supplies and reagents, recovery of HCT/Ps from the patient, processing, storage, labeling and document controls, and distribution and shipment of the HCT/Ps to the laboratory, storage, or other facility; | |

| ● | tracking and traceability of HCT/Ps and equipment, supplies, and reagents used in the manufacture of HCT/Ps; | |

| ● | adverse event reporting; | |

| ● | FDA inspection; and | |

| ● | abiding by any FDA order of retention, recall, destruction, and cessation of manufacturing of HCT/Ps. |

| 19 |

Non-reproductive HCT/Ps and non-peripheral blood stem/progenitor cells that are offered for import into the United States and regulated solely under Section 361 of the PHSA must also satisfy the requirements under 21 C.F.R. § 1271.420. Section 1271.420 requires that the importer of record of HCT/Ps notify the FDA prior to, or at the time of, importation and provide sufficient information for the FDA to make an admissibility decision. In addition, the importer must hold the HCT/P intact and under conditions necessary to prevent transmission of communicable disease until an admissibility decision is made by the FDA.

If the FDA determines that we have failed to comply with applicable regulatory requirements, it can impose a variety of enforcement actions including public warning letters, fines, consent decrees, orders of retention, recall or destruction of product, orders to cease manufacturing, and criminal prosecution. If any of these events were to occur, it could materially adversely affect us.

To the extent that our cellular therapy activities are limited to developing products and services outside the United States, as described in detail below, the products and services would not be subject to FDA regulation, but will be subject to the applicable requirements of the foreign jurisdiction. We intend to comply with all applicable foreign governmental requirements.

Drug and Biological Product Regulation

An HCT/P product that does not meet the criteria for being solely regulated under Section 361 of the PHSA will be regulated as a drug, device or biological product under the FDCA and/or Section 351 of the PHSA, and applicable FDA regulations. The FDA has broad regulatory authority over drugs and biologics marketed for sale in the United States. The FDA regulates the research, clinical testing, manufacturing, safety, effectiveness, labeling, storage, recordkeeping, promotion, distribution, and production of drugs and biological products. The FDA also regulates the export of drugs and biological products manufactured in the United States to international markets.

For products that are regulated as drugs, an investigational new drug, or IND, application and an approved new drug application, or NDA, are required before marketing and sale in the United States pursuant to the requirements of 21 C.F.R. Parts 312 and 314, respectively. An IND application notifies the FDA of prospective clinical testing and allows the test product to be shipped in interstate commerce. Approval of a NDA requires a showing that the drug is safe and effective for its intended use and that the methods, facilities, and controls used for the manufacturing, processing, and packaging of the drug are adequate to preserve its identity, strength, quality, and purity. If regulated as a biologic, the product must be subject to an IND to conduct clinical trials and a manufacturer must obtain an approved biologics license application, or BLA, before introducing a product into interstate commerce. To obtain a BLA, a manufacturer must show that the proposed product is safe, pure, and potent and that the facility in which the product is manufactured, processed, packed, or held meets established quality control standards.

| 20 |

Drug and biological products must also comply with applicable registration, product listing, and adverse event reporting requirements as well as FDA’s general prohibition against misbranding and adulteration. Additionally, the FDA actively enforces regulations prohibiting marketing and promotion of drugs and biologics for indications or uses that have not been approved by the FDA (i.e., “off label” promotion).

In the event that the FDA does not regulate our services in the United States solely under the HCT/P regulation, our products and activities could be regulated as drug or biological products under the FDCA. If regulated as drug or biological products, we will need to expend significant resources to ensure regulatory compliance. If an IND and NDA or BLA are required for any of our products, there is no assurance as to whether or when we will receive FDA approval of the product. The process of designing, conducting, compiling and submitting the non-clinical and clinical studies required for NDA or BLA approval is time-consuming, expensive and unpredictable. The process can take many years, depending on the product and the FDA’s requirements.

If the FDA determines that we have failed to comply with applicable regulatory requirements, it can impose a variety of enforcement actions from public warning letters, fines, injunctions, consent decrees and civil penalties to suspension or delayed issuance of approvals, seizure of our products, total or partial shutdown of our production, withdrawal of approvals, and criminal prosecutions. If any of these events were to occur, it could materially adversely affect us.

Medical Device Regulation

The FDA also has broad authority over the regulation of medical devices marketed for sale in the United States. The FDA regulates the research, clinical testing, manufacturing, safety, labeling, storage, recordkeeping, premarket clearance or approval, promotion, distribution, and production of medical devices. The FDA also regulates the export of medical devices manufactured in the United States to international markets.

Under the FDCA, medical devices are classified into one of three classes- Class I, Class II, or Class III, depending upon the degree of risk associated with the medical device and the extent of control needed to ensure safety and effectiveness. Class I devices are subject to the lowest degree of regulatory scrutiny because they are considered low risk devices and need only comply with the FDA’s General Controls. The General Controls include compliance with the registration, listing, adverse event reporting requirements, and applicable portions of the Quality System Regulation as well as the general misbranding and adulteration prohibitions.

Class II devices are subject to the General Controls as well as certain Special Controls such as 510(k) premarket notification. Class III devices are subject to the highest degree of regulatory scrutiny and typically include life supporting and life sustaining devices and implants. They are subject to the General Controls and Special Controls that include a premarket approval application, or PMA. “New” devices are automatically regulated as Class III devices unless they are shown to be low risk, in which case they may be subject to de novo review to be moved to Class I or Class II. Clinical research of an investigational device is regulated under the investigational device exemption, or IDE, regulations of 21 C.F.R. Part 812. Nonsignificant risk devices are subject to abbreviated requirements that do not require a submission to the FDA but must have Institutional Review Board (IRB) approval and comply with other requirements pertaining to informed consent, labeling, recordkeeping, reporting, and monitoring. Significant risk devices require the submission of an IDE application to the FDA and the FDA’s approval of the IDE application.

| 21 |

The FDA premarket clearance and approval process can be lengthy, expensive and uncertain. It generally takes three to twelve months from submission to obtain 510(k) premarket clearance, although it may take longer. Approval of a PMA could take one to four years, or more, from the time the application is submitted and there is no guarantee of ultimate clearance or approval. Securing FDA clearances and approvals may require the submission of extensive clinical data and supporting information to the FDA. Additionally, the FDA actively enforces regulations prohibiting marketing and promotion of devices for indications or uses that have not been cleared or approved by the FDA. In addition, modifications or enhancements of products that could affect the safety or effectiveness or effect a major change in the intended use of a device that was either cleared through the 510(k) process or approved through the PMA process may require further FDA review through new 510(k) or PMA submissions.

In the event we develop processes, products or services which qualify as medical devices subject to FDA regulation, we intend to comply with such regulations. If the FDA determines that our products are regulated as medical devices and we have failed to comply with applicable regulatory requirements, it can impose a variety of enforcement actions from public warning letters, application integrity proceedings, fines, injunctions, consent decrees and civil penalties to suspension or delayed issuance of approvals, seizure of our products, total or partial shutdown of our production, withdrawal of approvals, and criminal prosecutions. If any of these events were to occur, it could materially adversely affect us.

Current Good Manufacturing Practices and other FDA Regulations of Cellular Therapy Products

Products that fall outside of the HCT/P regulations and are regulated as drugs, biological products, or devices must comply with applicable good manufacturing practice regulations. The current Good Manufacturing Practices, or cGMPs regulations for drug products are found in 21 C.F.R. Parts 210 and 211; the General Biological Product Standards for biological products are found in 21 C.F.R. Part 610; and the Quality System Regulation for medical devices are found in 21 C.F.R. Part 820. These cGMPs and quality standards are designed to ensure the products that are processed at a facility meet the FDA’s applicable requirements for identity, strength, quality, sterility, purity, and safety. In the event that our domestic United States operations are subject to the FDA’s drug, biological product, or device regulations, we intend to comply with the applicable cGMPs and quality regulations.

If the FDA determines that we have failed to comply with applicable regulatory requirements, it can impose a variety of enforcement actions from public warning letters, fines, injunctions, consent decrees and civil penalties to suspension or delayed issuance of approvals, seizure of our products, total or partial shutdown of our production, withdrawal of approvals, and criminal prosecutions. If any of these events were to occur, it could materially adversely affect us.

| 22 |

Good Laboratory Practices

The FDA prescribes good laboratory practices, or GLPs, for conducting nonclinical laboratory studies that support applications for research or marketing permits for products regulated by the FDA. These regulations are published in Part 58 of Title 21 of the CFR. GLPs are intended to assure the quality and integrity of the safety data filed in research and marketing permits. GLPs provide requirements for organization, personnel, facilities, equipment, testing facilities operation, test and control articles, protocol for nonclinical laboratory study, records, reports, and disqualification by the FDA. To the extent that we are required to, or the above regulation applies, we intend that our nonclinical studies that are intended to support FDA submissions will comply with GLPs.

Promotion of Foreign-Based Cellular Therapy Treatment—“Medical Tourism”

We may establish, or license technology to third parties in connection with their establishment of, adult stem cell therapy facilities outside the United States. We also intend to work with hospitals and physicians to make the stem cell-based therapies available for patients who travel outside the United States for treatment. “Medical tourism” is defined as the practice of traveling across international borders to obtain health care.

The Federal Trade Commission, or the FTC, has the authority to regulate and police advertising of medical treatments, procedures, and regimens in the United States under the Federal Trade Commission Act, or the FTCA. Under Sections 5(a) and 12 of the FTCA (15 U.S.C. §§45(a) and 52), the FTC has regulatory authority to prevent unfair and deceptive practices and false advertising. Specifically, the FTC requires advertisers and promoters to have a reasonable basis to substantiate and support claims. The FTC has many enforcement powers, one of which is the power to order disgorgement by promoters deemed in violation of the FTCA of any profits made from the promoted business and can order injunctions from further violative promotion. Advertising that we may utilize in connection with our medical tourism operations will be subject to FTC regulatory authority, and we intend to comply with such regulatory régime. Similar laws and requirements are likely to exist in other countries and we intend to comply with such requirements.

| 23 |

Federal Regulation of Clinical Laboratories

Congress passed the Clinical Laboratory Improvement Amendments, or CLIA, in 1988, which provided the Centers for Medicare and Medicaid Services, or CMS, authority over all laboratory testing, except research, that is performed on humans in the United States. The Division of Laboratory Services, within the Survey and Certification Group, under the Center for Medicaid and State Operations, or CMSO, has the responsibility for implementing the CLIA program.

The CLIA program is designed to establish quality laboratory testing by ensuring the accuracy, reliability, and timeliness of patient test results. Under CLIA, a laboratory is a facility that does laboratory testing on specimens derived from humans and used to provide information for the diagnosis, prevention, treatment of disease, or impairment of, or assessment of health. Laboratories that handle stem cells and other biologic matter are, therefore, included under the CLIA program. Under the CLIA program, laboratories must be certified by the government, satisfy governmental quality and personnel standards, undergo proficiency testing, be subject to inspections, and pay fees. The failure to comply with CLIA standards could result in suspension, revocation, or limitation of a laboratory’s CLIA certificate. In addition, fines or criminal penalties could also be levied. To the extent that our business activities require CLIA certification, we intend to obtain and maintain such certification.

Health Insurance Portability and Accountability Act—Protection of Patient Health Information

The Health Insurance Portability and Accountability Act of 1996, or HIPAA, included the Administrative Simplification provisions that required the Secretary of the Department of Health and Human Services, or HHS, to adopt regulations for the electronic exchange, privacy, and security of individually identifiable health information that HIPAA protects (called “protected health information”). HHS published the Standards for Privacy of Individually Identifiable Health Information, or the Privacy Rule, and the Security Standards for the Protection of Electronic Protected Health Information, or the Security Rule, to protect the privacy and security of protected health information. The Privacy Rule specifies the required, permitted and prohibited uses and disclosures of an individual’s protected health information by health plans, health care clearinghouses, and any health care provider that transmits health information in electronic format (referred to as “covered entities”). The Security Rule establishes a national security standard for safeguarding protected health information that is held or transferred in electronic form (referred to as “electronic protected health information”). The Security Rule addresses the technical and non-technical safeguards that covered entities must implement to secure individuals’ electronic protected health information.

In addition to covered entities, the Health Information Technology for Economic and Clinical Health Act, or the HITECH Act, made certain provisions of the Security Rule, as well as the additional requirements the HITECH Act imposed that relate to security or privacy and that are imposed on covered entities, directly applicable as a matter of law to individuals and entities that perform permitted functions on behalf of covered entities when those functions involve the use or disclosure of protected health information. These individuals and entities are called “business associates.” Covered entities are required to enter into a contract with business associates, called a “business associate agreement,” that also imposes many of the Privacy Rule requirements on business associates as a matter of contract.

| 24 |

Regulations implementing the majority of the requirements created by the HITECH Act were issued in January 2013 (we refer to these regulations as the Final Rule). Among other things, the Final Rule broadened the definition of “business associate” to include subcontractors. As a result, a subcontractor who performs tasks involving the use or disclosure of protected health information on behalf of a business associate must likewise comply with the same obligations as the business associate.

The HITECH Act also established notification requirements in the event that a breach of the protected health information occurs at a covered entity or business associate. These notification obligations mandate that each affected individual whose protected health information was impermissibly accessed receive written notification mailed to his residence of record and that the Secretary of HHS and potentially the media also be notified. HHS, through its Office for Civil Rights, investigates breach reports and determines whether administrative or technical modifications are required and whether civil or criminal sanctions should be imposed. Companies failing to comply with HIPAA and the implementing regulations may also be subject to civil money penalties or in the case of knowing violations, potential criminal penalties, including monetary fines, imprisonment, or both. In some cases, the State Attorneys General may seek enforcement and appropriate sanctions in federal court.

To the extent that we are a covered entity or a business associate of a covered entity, we must comply with HIPAA and the implementing regulations. We must also comply with other additional federal or state privacy laws and regulations that may apply to certain diagnoses, such as HIV/AIDS, to the extent that they apply to us.

Other Applicable U.S. Laws

In addition to the above-described regulation by United States federal and state government, the following are other federal and state laws and regulations that could directly or indirectly affect our ability to operate the business:

| ● | state and local licensure, registration, and regulation of the development of pharmaceuticals and biologics; | |

| ● | state and local licensure of medical professionals; | |

| ● | state statutes and regulations related to the corporate practice of medicine; | |

| ● | laws and regulations administered by U.S. Customs and Border Protection related to the importation of biological material into the United States; | |

| ● | other laws and regulations administered by the FDA; |

| 25 |

| ● | other laws and regulations administered by HHS; | |

| ● | state and local laws and regulations governing human subject research and clinical trials; | |

| ● | the federal physician self-referral prohibition, also known as Stark Law, and any state equivalents to Stark Law; | |

| ● | the federal Anti-Kickback Statute and any state equivalent statutes and regulations’ | |

| ● | federal and state coverage and reimbursement laws and regulations; | |

| ● | state and local laws and regulations for the disposal and handling of medical waste and biohazardous material; | |

| ● | Occupational Safety and Health Administration, or OSHA, regulations and requirements; | |

| ● | the Intermediate Sanctions rules of the IRS providing for potential financial sanctions with respect to “excess benefit transactions” with tax-exempt organizations; | |

| ● | the Physician Payments Sunshine Act (in the event that our products are classified as drugs, biologics, devices or medical supplies and are reimbursed by Medicare, Medicaid or the Children’s Health Insurance Program); and | |

| ● | state and other federal laws addressing the privacy of health information. |

Foreign Government Regulation

In general, we will need to comply with the government regulations of each individual country in which our therapy centers are located and products are to be distributed and sold. These regulations vary in complexity and can be as stringent, and on occasion even more stringent, than FDA regulations in the United States. Due to the fact that there are new and emerging cell therapy and cell banking regulations that have recently been drafted and/or implemented in various countries around the world, the application and subsequent implementation of these new and emerging regulations have little to no precedence. Therefore, the level of complexity and stringency is not always precisely understood today for each country, creating greater uncertainty for the international regulatory process. Furthermore, government regulations can change with little to no notice and may result in up-regulation of our product(s), thereby creating a greater regulatory burden for our cell processing and cell banking technology products. We have not yet thoroughly explored the applicable laws and regulations that we will need to comply with in foreign jurisdictions. It is possible that we may not be permitted to expand our business into one or more foreign jurisdictions.

| 26 |