UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended March 31, 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from __________ to __________

Commission File Number: 001-35172

(Exact Name of Registrant as Specified in Its Charter)

| (State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) | ||||||||||

| (Address of Principal Executive Offices) | (Zip Code) | ||||||||||

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol(s) | Name of Each Exchange on Which Registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | x | ||||||||||||

| Non-accelerated filer | o | Smaller reporting company | ||||||||||||

| Emerging growth company | ||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value at September 30, 2022 of the Common Units held by non-affiliates of the registrant, based on the reported closing price of the Common Units on the New York Stock Exchange on such date ($1.30 per Common Unit) was $133.9 million. For purposes of this computation, all executive officers, directors and 10% beneficial owners of the registrant are deemed to be affiliates. Such a determination should not be deemed an admission that such executive officers, directors and 10% beneficial owners are affiliates.

At May 26, 2023, there were 131,927,343 common units issued and outstanding.

TABLE OF CONTENTS

i

Forward-Looking Statements

This Annual Report on Form 10-K (“Annual Report”) contains various forward-looking statements and information that are based on our beliefs and those of our general partner, as well as assumptions made by and information currently available to us. These forward-looking statements are identified as any statement that does not relate strictly to historical or current facts. Certain words in this Annual Report such as “anticipate,” “believe,” “could,” “estimate,” “expect,” “forecast,” “goal,” “intend,” “may,” “plan,” “project,” “will,” and similar expressions and statements regarding our plans and objectives for future operations, identify forward-looking statements. Although we and our general partner believe such forward-looking statements are reasonable, neither we nor our general partner can assure they will prove to be correct. Forward-looking statements are subject to a variety of risks, uncertainties and assumptions. If one or more of these risks or uncertainties materialize, or if underlying assumptions prove incorrect, our actual results may vary materially from those expected. Among the key risk factors that may affect our consolidated financial position and results of operations are:

•the prices of crude oil, natural gas liquids, gasoline, diesel, biodiesel and energy prices generally;

•the general level of demand, and the availability of supply, for crude oil, natural gas liquids, gasoline, diesel, and biodiesel;

•the level of crude oil and natural gas drilling and production in areas where we have operations and facilities;

•the ability to obtain adequate supplies of products if an interruption in supply or transportation occurs and the availability of capacity to transport products to market areas;

•the effect of weather conditions on supply and demand for crude oil, natural gas liquids, gasoline, diesel, and biodiesel;

•the effect of natural disasters, earthquakes, hurricanes, tornados, lightning strikes, or other significant weather events;

•the availability of local, intrastate, and interstate transportation infrastructure with respect to our transportation services;

•the availability, price, and marketing of competing fuels;

•the effect of energy conservation efforts on product demand;

•energy efficiencies and technological trends;

•issuance of executive orders, changes in applicable laws, regulations and policies, including tax, environmental, transportation, and employment regulations, or new interpretations by regulatory agencies concerning such laws and regulations and the effect of such laws, regulations and policies (now existing or in the future) on our business operations;

•the effect of executive orders and legislative and regulatory actions on hydraulic fracturing, water disposal and transportation, and the treatment of flowback and produced water;

•hazards or operating risks related to transporting and distributing petroleum products that may not be fully covered by insurance;

•the maturity of the crude oil, natural gas liquids, and refined products industries and competition from other markets;

•loss of key personnel;

•the ability to renew contracts with key customers;

•the ability to maintain or increase the margins we realize for our services;

•the ability to renew leases for our leased equipment and storage facilities;

•inflation, interest rates, and general economic conditions (including recessions and other future disruptions and volatility in the global credit markets, as well as the impact of these events on customers and suppliers);

•the nonpayment, nonperformance or bankruptcy by our counterparties;

•the availability and cost of capital and our ability to access certain capital sources;

•a deterioration of the credit and capital markets;

1

•the ability to successfully identify and complete accretive acquisitions and organic growth projects, and integrate acquired assets and businesses;

•the costs and effects of legal and administrative proceedings;

•changes in general economic conditions, including market and macroeconomic disruptions resulting from global pandemics and related governmental responses;

•political pressure and influence of environmental groups upon policies and decisions related to the production, gathering, refining, processing, fractionation, transportation and sale of crude oil, refined products, natural gas, natural gas liquids, gasoline, diesel or biodiesel; and

•other risks and uncertainties, including those discussed under Part I, Item 1A–“Risk Factors.”

You should not put undue reliance on any forward-looking statements. All forward-looking statements speak only as of the date of this Annual Report. Except as may be required by state and federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements as a result of new information, future events, or otherwise. When considering forward-looking statements, please review the risks discussed under Part I, Item 1A–“Risk Factors.”

2

PART I

References in this Annual Report to (i) “NGL Energy Partners LP,” “we,” “us,” “our,” or the “Partnership” or similar terms refer to NGL Energy Partners LP and its operating subsidiaries, (ii) “NGL Energy Holdings LLC” or “general partner” refers to NGL Energy Holdings LLC, our general partner (“GP”), (iii) “NGL Energy Operating LLC” refers to NGL Energy Operating LLC, the direct operating subsidiary of NGL Energy Partners LP, and (iv) the “NGL Energy GP Investor Group” refers to, collectively, the 45 individuals and entities that own all of the outstanding membership interests in our GP.

We have presented operational data in Part I, Item 1–“Business” for the year ended March 31, 2023. Unless otherwise indicated, this data is as of March 31, 2023.

Item 1. Business

Overview

We are a diversified midstream energy partnership that transports, treats, recycles and disposes of produced water generated as part of the energy production process as well as transports, stores, markets and provides other logistics services for crude oil and liquid hydrocarbons. Originally formed in September 2010, we are a Delaware master limited partnership and our business is currently organized into the following three segments:

•Our Water Solutions segment transports, treats, recycles and disposes of produced and flowback water generated from crude oil and natural gas production. We also sell produced water for reuse and recycle and brackish non-potable water to our producer customers to be used in their crude oil exploration and production activities. As part of processing water, we aggregate and sell recovered crude oil, also known as skim oil. We also dispose of solids such as tank bottoms, drilling fluids and drilling muds and perform other ancillary services such as truck and frac tank washouts. Our activities in this segment are underpinned by long-term, fixed fee contracts and acreage dedications, some of which contain minimum volume commitments with leading oil and gas companies including large, investment grade producer customers.

•Our Crude Oil Logistics segment purchases crude oil from producers and marketers and transports it to refineries or for resale at pipeline injection stations, storage terminals, barge loading facilities, rail facilities, refineries, and other trade hubs, and provides storage, terminaling and transportation services through its owned assets. Our activities in this segment are supported by certain long-term, fixed rate contracts which include minimum volume commitments on our owned and leased pipelines.

•Our Liquids Logistics segment conducts supply operations for natural gas liquids, refined petroleum products and biodiesel to a broad range of commercial, retail and industrial customers across the United States and Canada. These operations are conducted through our 25 owned terminals, third-party storage and terminal facilities, nine common carrier pipelines and a fleet of leased railcars. We also provide services for marine exports of butane through our facility located in Chesapeake, Virginia, and we own a propane pipeline system in Michigan.

Business Repositioning

Over the past several years, we have undertaken a number of important strategic actions in an effort to leverage the Partnership’s core areas of competitive strength and focus on generating stable, growing and predictable cash flows, while improving our credit profile. We believe these collective actions have substantially simplified our business mix and has allowed us to focus on what we believe are the core areas of our business and improved our overall financial position. These transactions are expected to position us for sustained growth in the future.

For more information regarding our results of operations and reportable segments, see Part II, Item 7–“Management’s Discussion and Analysis of Financial Condition and Results of Operations” and Note 11 to our consolidated financial statements included in this Annual Report. For more information regarding our dispositions and acquisitions transactions and the impact to our operations, see Note 17 and Note 18 to our consolidated financial statements included in this current Annual Report and our Annual Reports on Form 10-K for the years ended March 31, 2022 and 2021.

Debt Refinancing

As previously disclosed, on February 4, 2021, we closed on a private offering of $2.05 billion of our 7.5% senior secured notes due 2026 (“2026 Senior Secured Notes”) and a new credit agreement which consisted of a $500.0 million asset-based revolving credit facility (“ABL Facility”). We used the net proceeds from the issuance to repay all outstanding

3

borrowings under and terminate our former revolving credit facility and our term credit agreement, as well as to pay fees and expenses. As part of this refinancing, we also agreed to certain restricted payment provisions under the 2026 Senior Secured Notes and ABL Facility, one of which was the suspension of the quarterly common unit distributions, which began with the quarter ended December 31, 2020, and all preferred unit distributions, which began with the quarter ended March 31, 2021.

On April 13, 2022, we amended the ABL Facility to increase the commitments to $600.0 million under the accordion feature within the ABL Facility. As part of the amendment, we agreed to reduce the commitments back to $500.0 million on or before March 31, 2023. On February 16, 2023, we amended the ABL Facility to extend the maturity date of the additional $100.0 million of commitments through the remaining term of the ABL Facility.

For additional information related to the ABL Facility and 2026 Senior Secured Notes, see Note 7 to our consolidated financial statements included in this Annual Report.

4

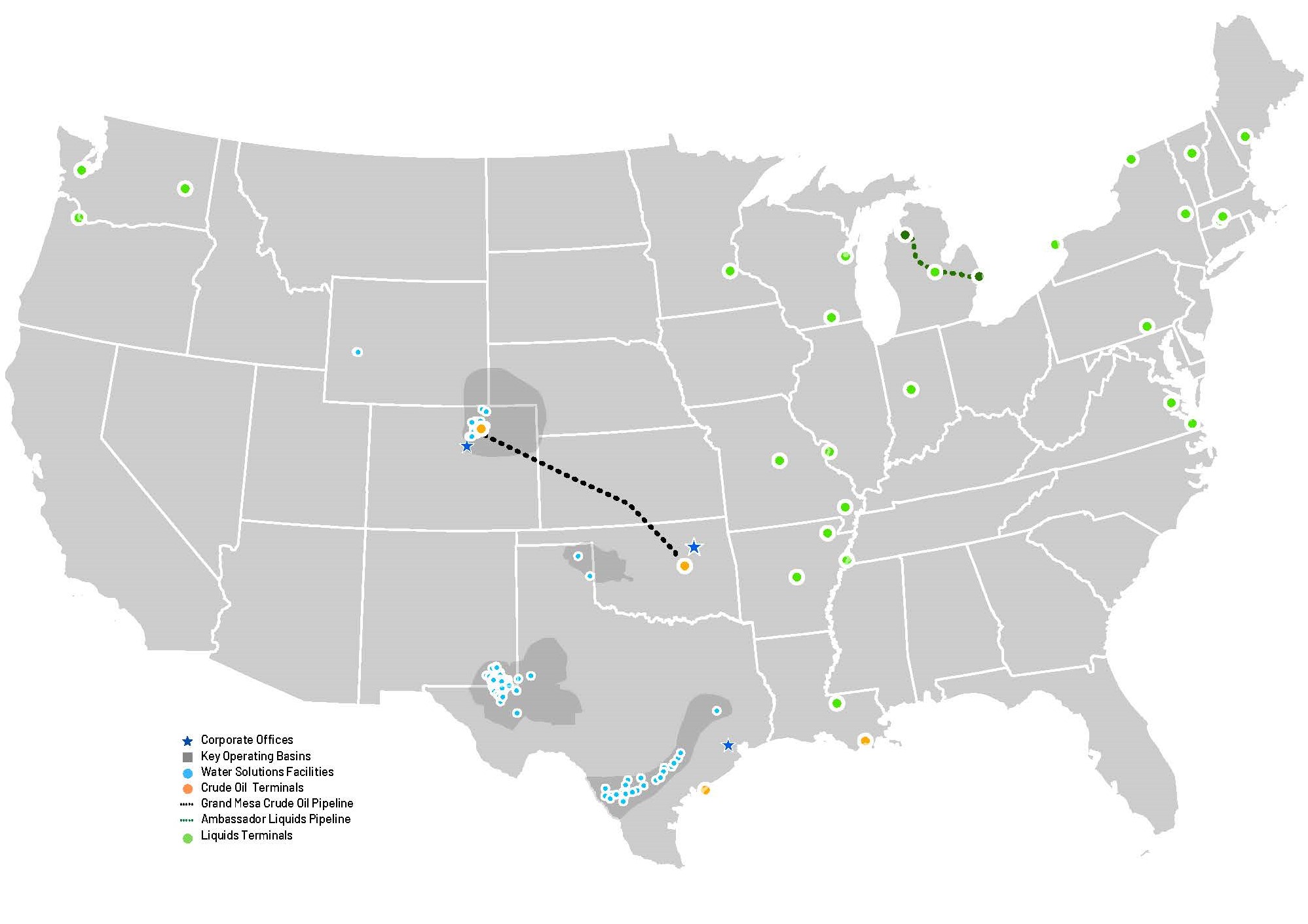

Primary Service Areas

The following map shows the primary service areas of our businesses at March 31, 2023:

5

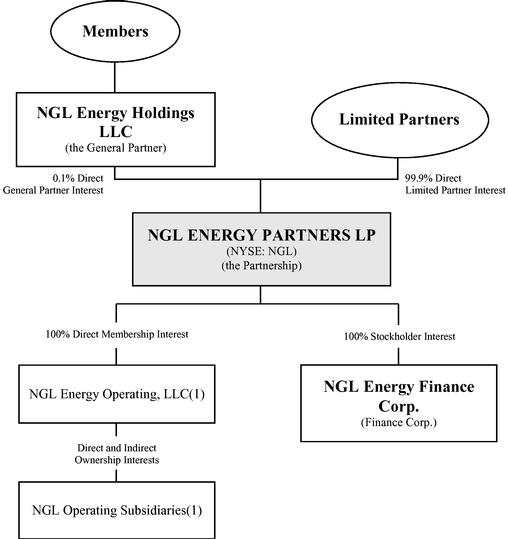

Organizational Chart

The following chart provides a summarized overview of our legal entity structure at March 31, 2023:

(1) Includes (i) NGL Water Solutions, LLC, which includes the operations of our Water Solutions segment, (ii) NGL Crude Logistics, LLC, which includes the operations of our Crude Oil Logistics segment and certain of our businesses within our Liquids Logistics segment and (iii) NGL Liquids, LLC, which includes the operations of certain of our businesses within our Liquids Logistics segment.

6

Our Business Strategies

Our principal business objectives are to maximize the profitability and stability of our businesses, grow our businesses in an accretive and prudent manner, and maintain a strong balance sheet. We intend to accomplish these business objectives by executing the following strategies:

•Prudently manage our balance sheet to provide us with maximum financial flexibility for funding our operations, capital projects and strategic acquisitions. Our primary focus is to reduce our absolute debt and leverage and maintain sufficient liquidity to continue to reduce our overall leverage and reinstate the payment of distributions. We are also focused on maintaining credit metrics to manage existing and future capital requirements as well as to take advantage of market opportunities. We expect to continue to evaluate the capital markets and may opportunistically pursue financing transactions to optimize our capital structure.

•Focus on building a diversified midstream master limited partnership providing multiple services to customers. We continue to enhance our ability to transport produced water from the wellhead to treatment for disposal, recycle, or discharge, crude oil from the wellhead to refineries, and natural gas liquids from processing plants and supply hubs to end users.

•Operate in a safe and environmentally responsible manner. We seek to operate our business in a safe and environmentally responsible manner by working with our employees, customers, vendors and local communities to minimize our environmental impact and comply with local, state and federal environmental laws and regulations.

•Focus on consistent annual cash flows from operations under multi-year contracts that minimize commodity price risk and generate fee-based revenues. We intend to focus on generating revenues under long-term fixed fee contracts in addition to back-to-back contracts which minimize commodity price exposure. We seek to continue to increase cash flows that are supported by certain fixed fee, multi-year contracts, some of which include acreage dedications from producers or minimum volume commitments.

•Achieve growth by utilizing our existing footprint of assets, investing in new assets, customers and ventures that increase volume and enhance our operations, and generate attractive rates of return. We have available capacity in many of the assets that we own and operate that can be utilized to increase cash flows with minimal incremental capital investment. We have invested and expect to continue to invest within our existing businesses to capitalize on accretive, organic growth opportunities. We also continue to pursue strategic transactions and ventures that complement and enhance our existing footprint.

Our Competitive Strengths

We believe that we are well positioned to successfully execute our business strategies and achieve our principal business objectives because of the following competitive strengths:

•Our water processing facilities, which are strategically located near areas of high crude oil and natural gas production. Our water processing facilities are located among the most prolific crude oil and natural gas producing areas in the United States, including the Delaware Basin, the Denver-Julesburg (“DJ”) Basin and the Eagle Ford Basin. These assets are underpinned by long-term, fixed fee contracts and acreage dedications, some of which contain minimum volume commitments. Additionally, we believe that the technological capabilities of our Water Solutions business can be quickly implemented at new facilities and locations as needed. Our system located in the Northern Delaware Basin is an integrated network of large diameter produced water pipelines, recycling facilities and disposal wells that collectively provides reliable service to producer customers and would be difficult for competitors to replicate at this time.

•Our network of crude oil transportation and storage assets, which allows us to serve customers over a wide geographic area and optimize sales. Our strategically deployed terminals, as well as our owned and contracted pipeline capacity, provide access to a wide range of customers and markets. We use this expansive network of transportation assets to deliver crude oil to optimal markets. These operations are supported by certain long-term, fixed rate contracts with producers, refiners and marketers and include minimum volume commitments on our owned and leased pipelines.

•Our network of natural gas liquids transportation, terminal, and storage assets, which allows us to provide multiple services across the United States and Canada. Our strategically located terminals, propane pipeline system in Michigan, large leased railcar fleet, shipper status on common carrier pipelines, and substantial leased

7

storage enable us to be a preferred purchaser and seller of natural gas liquids. We have a diverse base of long-standing customers and believe that our performance metrics allow us to reliably supply, store and transport products throughout the United States and Canada.

•Our diversified operations allow us to generate more predictable and stable cash flows on a year-to-year basis. Our ability to provide multiple services to customers in numerous geographic areas enhances our competitive position. Our three business segments are diversified by geography, customer base and commodity sensitivities, which we believe provides us with more stable cash flows through the typical commodity cycles.

•Our seasoned management team with extensive midstream industry experience and a track record of acquiring, integrating, operating and growing successful businesses. Our management team has significant experience managing companies in the energy industry, including master limited partnerships. In addition, through decades of experience, our management team has developed strong business relationships with key industry participants throughout the United States. We believe that our management’s knowledge of the industry, relationships within the industry, and experience provide us with the opportunities to optimize our existing assets. Our management team also has experience in identifying, evaluating and completing acquisitions and other ventures that provide us with additional opportunities to complement, grow and expand our existing operations.

Our Businesses

Water Solutions

Overview. Our Water Solutions segment transports, treats, recycles and disposes of produced and flowback water generated from crude oil and natural gas production. We also sell produced water for reuse and recycle and brackish non-potable water to our producer customers to be used in their crude oil exploration and production activities. As part of processing water, we aggregate and sell recovered crude oil, also known as skim oil. We also dispose of solids such as tank bottoms, drilling fluids and drilling muds and perform other ancillary services such as truck and frac tank washouts. Our activities in this segment are underpinned by long-term, fixed fee contracts and acreage dedications, some of which contain minimum volume commitments with leading oil and gas companies including large, investment grade producer customers.

We operate in a number of the most prolific crude oil and natural gas producing areas in the United States including the Delaware Basin in New Mexico and Texas, the DJ Basin in Colorado and the Eagle Ford Basin in Texas. With a system that handled approximately 849.5 million barrels of produced water across its areas of operation during the year ended March 31, 2023, we believe that we are the largest independent produced water transportation and disposal company in the United States. We currently have approximately 670,000 acres dedicated to our system under long-term agreements in the Northern Delaware Basin. In addition, we have several minimum volume commitments and other commercial agreements covering the Delaware, DJ, Eagle Ford and Pinedale Anticline Basins. Our focus in building our Water Solutions business has been to secure long-term, fixed fee contracts that contain minimum volume commitments, acreage dedications or similarly strong contractual relationships with large, well-capitalized producer customers.

Our core asset in the Water Solutions segment is our system located in the Northern Delaware Basin, where we own and operate the largest integrated network of large diameter produced water pipelines, recycling facilities and disposal wells. This system spans six counties in New Mexico and Texas that represent one of the most prolific crude oil producing regions in the United States with some of the most economic hydrocarbon resources and lowest break-even economics for producers. Our system has approximately 730 miles of newly-built, in-service large diameter produced water pipelines connected to 57 active saltwater disposal facilities and 125 active disposal wells. We currently have approximately 670,000 acres dedicated to the Northern Delaware system providing a multi-decade drilling inventory and significant growth opportunity.

We own or have a possessory interest in over 120,000 acres of real estate on two ranches located in Eddy and Lea Counties, New Mexico. Our two ranches include 16 commercial water permits and four strategically located brackish non-potable water facilities (including 45 brackish non-potable water wells). Additionally, on both ranches we are organically developing surface mineral mining operations, solid waste facilities, and are exploring other uses for our real estate holdings.

In February 2022, our Water Solutions segment announced a collaboration with XRI Holdings, LLC (“XRI”) to advance full cycle produced water management across operations in the Northern Delaware Basin. This collaboration will benefit from each of our unique characteristics by leveraging existing infrastructure assets, technology, and experience, as we own and operate the largest integrated produced water pipeline system in the Northern Delaware Basin and XRI is the largest produced water recycling company in the Permian Basin, allowing us the opportunity to address the greatly increasing demand for sustainable use of produced water in our customers’ completions activities. The flexible, non-exclusive nature of this joint effort allows each of us to continue to operate produced water reuse and recycling activities independent of one another. During

8

the year ended March 31, 2023, we sold approximately 43.4 million barrels of recycled water, which includes the sale of produced water and recycled water for use in our customers’ completion activities.

Operations. We own 93 water treatment and disposal facilities, including 197 injection wells. The location and permitted processing capacities of these facilities are summarized below.

| Number of | Number of | Permitted Processing Capacity (barrels per day) | ||||||||||||||||||||||||||||||

| Location | Facilities | Wells | Own (1) | Lease (2) | Total | |||||||||||||||||||||||||||

| Permian Basin | ||||||||||||||||||||||||||||||||

| Delaware Basin (3) - Texas and New Mexico | 57 | 125 | 1,489,000 | 3,462,300 | 4,951,300 | |||||||||||||||||||||||||||

| Eagle Ford Basin (3)(4) - Texas | 19 | 33 | 474,000 | 362,000 | 836,000 | |||||||||||||||||||||||||||

| DJ Basin - Colorado | 13 | 31 | 373,000 | 162,500 | 535,500 | |||||||||||||||||||||||||||

| Granite Wash (3) - Texas | 2 | 3 | 60,000 | — | 60,000 | |||||||||||||||||||||||||||

| Pinedale Anticline Basin - Wyoming | 1 | 4 | — | 90,240 | 90,240 | |||||||||||||||||||||||||||

| Eaglebine - Texas | 1 | 1 | 20,000 | — | 20,000 | |||||||||||||||||||||||||||

| Total - All Facilities | 93 | 197 | 2,416,000 | 4,077,040 | 6,493,040 | |||||||||||||||||||||||||||

(1) These facilities are located on lands we own.

(2) These facilities are located on lands we lease.

(3) Certain facilities can dispose of both produced water and solids such as tank bottoms, drilling fluids and drilling muds.

(4) Includes one facility with a permitted processing capacity of 40,000 barrels per day in which we own a 75% interest.

On March 31, 2023, we sold certain saltwater disposal assets in the Midland Basin (see Note 17 to our consolidated financial statements included in this Annual Report).

Our customers bring produced and flowback water generated by crude oil and natural gas exploration and production operations to our facilities for treatment through pipeline gathering systems and by truck. During the year ended March 31, 2023, in the Delaware Basin, we received approximately 98% of produced and flowback water via pipelines. Once we take delivery of the water, the level of processing is determined by the ultimate disposition of the water.

Our facilities in Colorado, New Mexico and Texas dispose of produced water primarily into deep underground formations via injection wells. At our disposal facilities, we use proprietary well maintenance programs to enhance injection rates and extend the service lives of the wells.

Customers. The primary customers of our operations consist mainly of large publicly traded, oil and gas companies with diversified acreage positions across multiple leading oil and gas plays. During the year ended March 31, 2023, 70% of the revenues of our Water Solutions segment were generated from our ten largest customers of the segment.

Competition. The principal elements of competition are system reliability, project execution capability and reputation, system capacity and flexibility, rates for services and system location relative to the producer’s operations. Our competitors include independent produced water transportation and disposal companies and the water transportation and disposal operations owned by oil and gas production companies themselves. Location can be an important consideration for our customers, who seek to minimize the cost of transporting the produced water to disposal facilities. Many of our facilities are strategically located near areas of high crude oil and natural gas production which provides us with a distinct advantage over a competitor that must build a system that can compete with our assets.

Pricing Policy. We charge customers a fee per barrel of produced water received. Our contractual agreements can consist of: (a) minimum volume commitments requiring the customer to deliver a specified minimum volume of produced water over a specified period of time; (b) acreage dedications requiring the customer to deliver all volumes produced from the dedicated acreage with us; and (c) produced water pipeline and trucked disposal agreements providing interruptible service in exchange for a fee per barrel of produced water received. We also generate revenue from the sale of crude oil we recover in processing the produced water. In addition, we may charge fees for the sale of produced water for reuse by our customers, pipeline transportation fees, pipeline interconnection fees and solids disposal fees.

Trade Names. Our Water Solutions segment operates primarily under the NGL Water Solutions and Anticline Disposal trade names.

9

Technology. We hold multiple patents for processing technologies. We believe that the technological capabilities of our Water Solutions business can be quickly implemented at new facilities and locations.

Crude Oil Logistics

Overview. Our Crude Oil Logistics segment purchases crude oil from producers and marketers and transports it to refineries or for resale at pipeline injection stations, storage terminals, barge loading facilities, rail facilities, refineries, and other trade hubs, and provides storage, terminaling and transportation services through its owned assets. Our activities in this segment are supported by certain long-term, fixed rate contracts which include minimum volume commitments on our owned and leased pipelines. Our operations are concentrated in and around four prolific crude oil producing regions in the United States, including the DJ Basin in Colorado, the Permian Basin in Texas and New Mexico, the Eagle Ford Basin in Texas and the United States Gulf Coast.

Our foundational asset in this segment is the Grand Mesa Pipeline, a 550-mile pipeline that transports crude oil from its origin in Weld County, Colorado to our terminal in Cushing, Oklahoma. The Grand Mesa Pipeline commenced operations on November 1, 2016 and has operated continuously since then. The main line portion of this pipeline is comprised of an undivided interest with Saddlehorn Pipeline Company, LLC (“Saddlehorn”) in which we have ownership of 150,000 barrels per day of capacity of the pipeline. During the year ended March 31, 2023, approximately 27.7 million barrels of crude oil were transported on the Grand Mesa Pipeline. Operating costs associated with the Grand Mesa Pipeline are allocated to us based on our proportionate ownership interest and throughput. We also own and operate origin terminals at Lucerne and Riverside, Colorado, where we aggregate crude oil volumes of different types and grades and store them until they are ready for transfer to the Grand Mesa Pipeline. The Lucerne terminal has 950,000 barrels of storage and a 12 bay truck loading facility. The Riverside terminal has 20,000 barrels of storage and a four bay truck loading facility.

Through our ownership in the Grand Mesa Pipeline, we have sufficient capacity to service our customer contracts at the same origin and termination points with the ability to accept additional volume commitments. We retained ownership of our previously acquired easements for the potential future development of transportation projects involving petroleum commodities other than crude oil and condensate. With the consent and participation of Saddlehorn, we and Saddlehorn may consider future opportunities using these easements, to the extent such easements remain in effect, for projects involving the transportation of crude oil and condensate.

We own and operate a large scale crude oil terminal located in Cushing, Oklahoma with 3,626,000 barrels of storage capacity, seven off-loading lease automatic custody transfer units (“LACTs”), a full control room, on-site quality management building, and three 24-inch bi-directional pipelines each capable of moving 360,000 barrels per day. The terminal features advantaged connectivity to other terminals and pipelines including important connections to the Grand Mesa Pipeline and to TC Energy’s terminal with access to the United States Gulf Coast via Marketlink. Our terminal is situated on 200 acres and is designed to be expanded based on customer demand. Cushing is one of the most liquid crude oil trading hubs in the world and is the delivery point for West Texas Intermediate futures contracts.

We own and operate a crude oil marine terminal in Point Comfort, Texas with 355,000 barrels of storage capacity, six off-loading LACTs and three docks (two for ocean-going barges and ships and one for inland barges).

We own and operate a crude oil pipeline and marine terminal in Houma, Louisiana with 288,000 barrels of storage capacity, two off-loading LACTs, a brown water barge dock and two 12-inch bi-directional pipelines each capable of moving 120,000 barrels per day with connectivity to Shell’s Zydeco System.

Operations. We purchase crude oil from producers and marketers and transport it to refineries or for resale. Our strategically deployed terminals, as well as our owned and contracted pipeline capacity, provide access to a wide range of customers and markets. We use this expansive network of transportation assets to deliver crude oil to optimal markets.

We currently transport crude oil using the following assets:

•The Grand Mesa Pipeline, which is described above, and 19 other common carrier pipelines owned by third parties; and

•396 owned railcars (all of which are leased or subleased to third parties).

All of our 396 owned railcars are compliant with the standards for railcars built subsequent to 2011 for the commodities they are transporting. (See Part I, Item 1 “Government Regulation”).

10

We also own 27 strategically located pipeline injection stations, the locations of which are summarized below.

| State | Number of Pipeline Injection Stations | |||||||

| Texas | 13 | |||||||

| New Mexico | 6 | |||||||

| Oklahoma | 5 | |||||||

| Kansas | 3 | |||||||

| Total | 27 | |||||||

On March 30, 2023, we sold our marine assets (see Note 17 to our consolidated financial statements included in this Annual Report).

Customers. Our customers include crude oil refiners, producers, and marketers. During the year ended March 31, 2023, 85% of the revenues of our Crude Oil Logistics segment were generated from our ten largest customers of the segment. Additionally, certain key customers of the Crude Oil Logistics segment contribute significantly to the cash flows and profitability of the organization. Any loss of those customers or their contracts could have an adverse impact on our financial results.

Competition. Our Crude Oil Logistics segment faces significant competition, as many entities are engaged in the crude oil logistics business, some of which are larger and have greater financial resources than we do. The primary factors on which we compete are:

•price;

•availability of supply and refinery demand;

•reliability of service;

•open credit;

•logistics capabilities, including the availability of railcars, proprietary terminals, and owned pipeline and railcars; and

•long-term customer relationships.

Supply. We obtain crude oil from a large base of suppliers, which consists primarily of crude oil producers. We currently purchase crude oil from approximately 276 producers at approximately 2,875 leases.

Pricing Policy. Most of our contracts to purchase or sell crude oil are at floating prices that are indexed to published rates in active markets such as Cushing, Oklahoma, St. James, Louisiana, and Magellan East Houston. We seek to manage price risk by entering into purchase and sale contracts of similar volumes based on similar indexes and by hedging exposure due to fluctuations in actual volumes and scheduled volumes.

Our profitability is impacted by forward crude oil prices. Crude oil markets can either be in contango (a condition in which forward crude oil prices are greater than spot prices) or can be in backwardation (a condition in which forward crude oil prices are lower than spot prices). Our Crude Oil Logistics segment benefits when the market is in contango, as increasing prices result in inventory value gains during the time between when we purchase the inventory and when we sell it. In addition, we are able to better utilize our storage assets when contango markets justify storing barrels. When markets are in backwardation, our inventory values decrease during the time period between when we purchase inventory and when we sell it and the declining prices also typically have an unfavorable impact on our storage tank lease rates. To help mitigate the impact of changing prices, we enter into derivative instruments to hedge our inventory.

Trade Names. Our Crude Oil Logistics segment operates primarily under the NGL Crude Logistics, NGL Crude Transportation, NGL Crude Terminals and NGL Crude Cushing trade names.

Liquids Logistics

Overview. Our Liquids Logistics segment conducts supply operations for natural gas liquids, refined petroleum products and biodiesel to a broad range of commercial, retail and industrial customers across the United States and Canada. These operations are conducted through our 25 owned terminals, third-party storage and terminal facilities, nine common

11

carrier pipelines and a fleet of leased railcars. We also provide services for marine exports of butane through our facility located in Chesapeake, Virginia, and we own a propane pipeline system in Michigan. We employ a number of contractual and hedging strategies to minimize commodity exposure and maximize earnings stability of this segment. During the year ended March 31, 2023, we sold approximately 2.7 billion gallons of natural gas liquids, refined products and renewables products, or 7.45 million gallons (approximately 177,000 barrels) per day.

Operations. We procure natural gas liquids from refiners, natural gas processing plants, producers and other resellers for delivery to leased or owned storage space, common carrier pipelines, railcar terminals, and direct to certain customers. Our customers take delivery by loading natural gas liquids into transport vehicles from common carrier pipeline terminals, private terminals, our terminals, directly from refineries and rail terminals, and by railcar.

A portion of our wholesale propane gallons are presold to third-party retailers and wholesalers at a fixed price under back-to-back contracts. Back-to-back contracts, in which we balance our contractual portfolio by buying physical propane supply or derivatives when we have a matching purchase commitment from our wholesale customers, protect our margins and mitigate commodity price risk. Presales also reduce the impact of warm weather because the customer is required to take delivery of the propane regardless of the weather or any other factors. We generally require cash deposits from these customers. In addition, on a daily basis we have the ability to balance our inventory by buying or selling propane, butanes, and natural gasoline to refiners, resellers, and propane producers through pipeline inventory transfers at major storage hubs.

In order to secure consistent supply during the heating season, we are often required to purchase volumes of propane during the entire fiscal year. In order to mitigate storage costs and price risk, we may sell those volumes at a lesser margin in lower demand months than we earn in our other wholesale operations.

We purchase butane from refiners during the summer months, when refiners have a greater butane supply than they need, and sell butane to refiners during the winter blending season, when demand for butane is higher. We utilize a portion of our railcar fleet and a portion of our leased underground storage to store butane for this purpose. We also transport customer-owned natural gas liquids on our leased railcars and charge the customers a transportation service fee as well as sublease railcars to certain customers. Our owned and leased terminals and railcar fleet give us the opportunity to access markets throughout the United States, and to move product to locations where demand is highest. We provide transportation, storage, and throughput services to third parties at our facilities at Port Hudson, Louisiana and Chesapeake, Virginia.

We purchase refined petroleum and renewable products primarily in the Gulf Coast, West Coast and Midwest regions of the United States and schedule them for delivery at various locations throughout the country. We conduct just-in-time sales at a nationwide network of terminals owned by third parties via rack spot sales or delivered sales that do not involve continuing contractual obligations to purchase or deliver product. Rack spot sales are priced and delivered on a daily basis through truck loading racks. At the end of each day for each of the terminals that we market from, we establish the next day selling price for each product for each of our delivery locations. We announce or “post” to customers via website, e-mail, and telephone communications the rack spot sale price of various products for the following morning. When customers decide to purchase product from us, we purchase the same volume of product from a supplier at a previously agreed-upon price. For these just-in-time transactions, our purchase from the supplier occurs at the same time as our sale to our customer. Typical rack spot sale purchasers include commercial and industrial end users, independent retailers and small, independent marketers who resell product to retail gasoline stations or other end users. Our selling price of a particular product on a particular day is a function of our supply at that delivery location or terminal, our estimate of the costs to replenish the product at that delivery location, and our desire to reduce product volume at that particular location that day. A significant percentage of our business is priced on a back-to-back basis which minimizes our commodity price exposure.

12

The following table summarizes the location of our facilities and respective storage capacity and interconnects to those facilities.

| Storage Capacity (in gallons) | ||||||||||||||||||||||||||||||||

| Location | Number of Facilities | Own (1) | Lease (2) | Total | Terminal Interconnects | |||||||||||||||||||||||||||

| Virginia | 2 | 20,888,000 | — | 20,888,000 | Rail Facility; Marine Facility | |||||||||||||||||||||||||||

| Arkansas | 3 | 3,765,000 | 90,000 | 3,855,000 | Connected to Enterprise Texas Eastern Products Pipeline; Rail Facility | |||||||||||||||||||||||||||

| Minnesota | 1 | 1,829,000 | — | 1,829,000 | Connected to Enterprise Mid-America Pipeline; Rail Facility | |||||||||||||||||||||||||||

| Missouri | 2 | 1,770,000 | — | 1,770,000 | Connected to Phillips66 Blue Line Pipeline | |||||||||||||||||||||||||||

| Indiana | 1 | 1,530,000 | — | 1,530,000 | Connected to Enterprise Texas Eastern Products Pipeline; Rail Facility | |||||||||||||||||||||||||||

| Wisconsin | 2 | 696,000 | 390,000 | 1,086,000 | Connected to Enterprise Mid-America Pipeline; Rail Facility | |||||||||||||||||||||||||||

| Massachusetts | 2 | 668,400 | 120,000 | 788,400 | Rail Facility | |||||||||||||||||||||||||||

| Louisiana | 1 | 720,000 | — | 720,000 | Truck Facility | |||||||||||||||||||||||||||

| Washington | 3 | 300,000 | 355,000 | 655,000 | Rail Facility | |||||||||||||||||||||||||||

| Illinois | 1 | 480,000 | — | 480,000 | Connected to Phillips66 Blue Line Pipeline | |||||||||||||||||||||||||||

| Michigan | 1 | 480,000 | 480,000 | Connected to Ambassador Pipeline | ||||||||||||||||||||||||||||

| New York | 2 | — | 450,000 | 450,000 | Rail Facility | |||||||||||||||||||||||||||

| Pennsylvania | 1 | 180,000 | — | 180,000 | Rail Facility | |||||||||||||||||||||||||||

| Maine | 1 | — | 120,000 | 120,000 | Rail Facility | |||||||||||||||||||||||||||

| Vermont | 1 | — | 120,000 | 120,000 | Rail Facility | |||||||||||||||||||||||||||

| United States Total | 24 | 33,306,400 | 1,645,000 | 34,951,400 | ||||||||||||||||||||||||||||

| Ontario, Canada | 1 | — | 120,000 | 120,000 | Truck Facility | |||||||||||||||||||||||||||

| Canada Total | 1 | — | 120,000 | 120,000 | ||||||||||||||||||||||||||||

| Total | 25 | 33,306,400 | 1,765,000 | 35,071,400 | ||||||||||||||||||||||||||||

(1) These facilities are located on lands we own.

(2) These facilities are located on lands we lease.

We have operating agreements with third parties for certain of our terminals. The terminals in East St. Louis, Illinois and Jefferson City, Missouri were operated for us by a third party for a monthly fee under an operating and maintenance agreement that we terminated as of March 31, 2023. The terminal in St. Catharines, Ontario, Canada is operated by a third party under a year-to-year agreement.

We own the land on which 15 of the 25 natural gas liquids terminals are located and we either have easements or lease the land on which the remaining terminals are located.

We own a natural gas liquids terminal that supports refined products blending in Port Hudson, Louisiana, and a marine export/import terminal in Chesapeake, Virginia. The Port Hudson terminal is located near Baton Rouge, Louisiana, and is in proximity to other refined products infrastructure along the Colonial pipeline. This truck unloading and storage facility allows for the aggregation and supply of butane and naphtha for motor fuel blending and consists of storage tanks with a total capacity of 720,000 gallons. The Chesapeake facility is a marine export/import terminal situated upstream of Norfolk, Virginia on the Elizabeth River. The site includes a proprietary dock with the capacity to berth handy-sized vessels (a dry bulk carrier of an oil tanker with a capacity between 15,000 and 35,000 dead weight tonnage) to very large gas carriers (a carrier capable of loading anywhere between 100,000 cubic meters to 200,000 cubic meters of natural gas), truck loading and off-road racks along with 22 railcar spots, with service provided by Norfolk Southern Railroad. The facility has an aggregate storage capacity of 20,378,000 gallons.

We own 28 transloading units, which enable customers to transfer product from railcars to trucks. These transloading units can be moved to locations along a railroad where it is most convenient for customers to transfer their product.

13

We own the Ambassador Pipeline, an approximately 225-mile propane pipeline, which runs from the Kalkaska gas plant in Kalkaska County, Michigan to a termination point near Marysville in St. Clair County, Michigan. The Marysville, Michigan connection was completed in August 2022 and this allowed the Ambassador Pipeline to be fully operational. The Wheeler propane terminal, in central Michigan, is located at the mid-point of the pipeline. These assets complement our existing assets in the upper Midwest and will expand our presence in Michigan, one of the top propane markets in the United States.

We utilize a fleet of approximately 4,400 high-pressure and general purpose leased railcars of which 145 railcars are subleased by third parties.

We lease storage space to accommodate the supply requirements and contractual needs of our retail and wholesale customers.

The following table summarizes our significant leased storage space at natural gas liquids and refined products storage facilities and interconnects to those facilities:

| Leased Storage Space (in gallons) | ||||||||||||||||||||

| Storage Facility Location | Beginning April 1, 2023 | At March 31, 2023 | Storage Interconnects | |||||||||||||||||

| Kansas | 56,700,000 | 56,700,000 | Connected to Enterprise Mid-America Pipeline, NuStar Pipelines and ONEOK North System Pipeline; Rail Facility; Truck Facility | |||||||||||||||||

| Michigan | 23,520,000 | 24,780,000 | Rail Facility; Truck Facility | |||||||||||||||||

| Utah | 15,750,000 | 16,800,000 | Rail Facility | |||||||||||||||||

| Arizona | 7,056,000 | 7,056,000 | Rail Facility; Truck Facility | |||||||||||||||||

| Texas | 4,830,000 | 3,150,000 | Connected to Enterprise Texas Eastern Products Pipeline; Truck Facility | |||||||||||||||||

| Mississippi | 3,780,000 | 3,780,000 | Connected to Enterprise Dixie Pipeline; Rail Facility | |||||||||||||||||

| Oregon | 2,100,000 | 554,400 | Connected to Kinder Morgan Pipeline and Olympic Pipeline | |||||||||||||||||

| United States Total | 113,736,000 | 112,820,400 | ||||||||||||||||||

| Ontario, Canada | 8,467,200 | 8,467,200 | Rail Facility | |||||||||||||||||

| Alberta, Canada | 3,970,092 | 3,970,092 | Connected to Cochin Pipeline; Rail Facility | |||||||||||||||||

| Canada Total | 12,437,292 | 12,437,292 | ||||||||||||||||||

| Total | 126,173,292 | 125,257,692 | ||||||||||||||||||

Customers. Our Liquids Logistics segment serves approximately 1,300 customers in 48 states, Mexico and Canada, including national, regional and independent retail, industrial, wholesale, petrochemical, refiner and natural gas liquids production customers. During the year ended March 31, 2023, 23% of the revenues of our Liquids Logistics segment were generated from our ten largest customers of the segment.

Seasonality. Our wholesale liquids business is largely seasonal as the primary users of propane as heating fuel generally purchase propane during the typical fall and winter heating season. However, we are able to partially mitigate the effects of seasonality by preselling a portion of our wholesale volumes to retailers and wholesalers and requiring the customer to take delivery of the product regardless of the weather.

The demand for gasoline typically peaks during the summer driving season, which extends from April to September, and declines during the fall and winter months. However, the demand for diesel typically peaks during the fall and winter months due to colder temperatures, and peaks in the Midwest during spring planting and fall harvest.

Competition. Our Liquids Logistics segment faces significant competition from other natural gas liquids wholesalers, trading companies and companies involved in the natural gas liquids midstream industry (such as terminal and refinery operations), some of which have greater financial resources than we do. The primary factors on which we compete are:

•price;

•availability of supply;

14

•reliability of service;

•available space on common carrier pipelines;

•storage availability;

•logistics capabilities, including the availability of railcars, and proprietary terminals; and

•long-term customer relationships.

Market Price Risk. Our philosophy is to maintain minimum commodity price exposure through a combination of purchase contracts, sales contracts and financial derivatives. A significant percentage of our refined products and biodiesel businesses is priced on a back-to-back basis which minimizes our commodity price exposure. For discretionary inventory, and for those instances where physical transactions cannot be appropriately matched, we utilize financial derivatives to mitigate commodity price exposure. Specific exposure limits are mandated in our credit agreement and in our market risk policy.

The value of refined products in any local delivery market is the sum of the commodity price as reflected on the New York Mercantile Exchange (“NYMEX”) and the basis differential for that local delivery market. The basis differential for any local delivery market is the spread between the cash price in the physical market and the quoted price in the futures markets for the prompt month. We typically utilize NYMEX futures contracts to mitigate commodity price exposure. We generally do not manage the financial impact on us from changes in basis differentials affected by local market supply and demand disruptions.

Pricing Policy. In our Liquids Logistics segment, we offer our customers the following categories of contracts:

•customer pre-buys, which typically require deposits based on market pricing conditions;

•market based, which can either be a posted price or an index to spot price at time of delivery; and

•load package, a firm price agreement for customers seeking to purchase specific volumes delivered during a specific time period.

We use back-to-back contracts for many of our liquids business sales to limit exposure to commodity price risk and protect our margins. We are able to match our supply and sales commitments by offering our customers purchase contracts with flexible price, location, storage, and ratable delivery. However, certain common carrier pipelines require us to keep minimum in-line inventory balances year round to conduct our daily business, and these volumes are not matched with a sales commitment.

We generally require deposits from our customers for fixed price future delivery if the delivery date is more than 30 days after the time of contractual agreement.

Legal and Regulatory Considerations. Demand for ethanol and biodiesel is driven in large part by government mandates and incentives. Refiners and producers are required to blend a certain percentage of renewables into their refined products, although the percentage can vary from year to year based on the United States Environmental Protection Agency (“EPA”) mandates. In addition, the federal government has in recent years granted certain tax credits for the use of biodiesel, although on several occasions these tax credits have expired. In August 2022, the federal government extended the tax credit, with the tax credit now expiring on December 31, 2024. Changes in future mandates and incentives, or decisions by the federal government related to future reinstatement of the biodiesel tax credit, could result in changes in demand for ethanol and biodiesel.

Trade Names. Our Liquids Logistics segment operates primarily under the NGL Supply Wholesale, NGL Supply Terminal Company, Centennial Energy, Centennial Gas Liquids and NGL Crude Logistics trade names.

Human Capital

At March 31, 2023, we had 638 employees in 29 states and Canada. Of those employees, 229 provide work primarily for our Water Solutions segment, 67 provide work primarily for our Crude Oil Logistics segment, 167 provide work primarily for our Liquids Logistics segment, and 175 provide administrative services to the various business segments. NGL is an equal-opportunity employer, and our employee handbook underscores that commitment, with policies prohibiting discrimination, harassment, and retaliation.

We understand the importance of competitive benefits packages for the health and welfare of our employees and for our ability to recruit and retain the best talent. In that regard, at the end of fiscal year 2021, we implemented $20 per hour

15

minimum wage for all regular, full-time employees. More than 95% of our eligible employees participated in the NGL 401(k) Plan in fiscal year 2023. As of January 1, 2023, we shortened the NGL 401(k) eligibility period from the first day after six months of employment to the first day of the month after three months of employment. In addition, we provide access to a traditional PPO or a high-deductible medical plan including a health savings account with employer contributions; a flexible spending account option for those not enrolled in the high-deductible medical plan; a dental plan; a vision plan; an Employee Assistance Plan including free counseling for employees and members of their household; company-paid short-term disability coverage; voluntary long-term disability coverage; company-paid life and AD&D coverage; and voluntary life and AD&D coverage options for employees and their family members.

Our operations are guided by specific health and safety protocols. We endeavor to conduct our business in a manner that meets or exceeds applicable health and safety regulations and minimizes risk, both to our employees and the communities where we operate. Our environmental, health and safety team:

• Advises on safety and industrial hygiene regulatory requirements and best practices;

• Develops safety procedures and guidelines;

• Conducts safety inspections;

• Advises on strategies to improve safety and health performance; and

• Designs and conducts safety and industrial hygiene training courses.

As part of this effort, we have implemented an enterprise management information system designed to help us achieve a better understanding of our performance, identify root causes of incidents, and where appropriate, implement necessary mitigations.

Government Regulation

Regulation of the Oil and Natural Gas Industries

Regulation of Oil and Natural Gas Exploration, Production and Sales. Sales of crude oil and natural gas liquids are not currently regulated and are transacted at market prices. In 1989, the United States Congress enacted the Natural Gas Wellhead Decontrol Act, which removed all remaining price and non-price controls affecting wellhead sales of natural gas. The Federal Energy Regulatory Commission (“FERC”), which has authority under the Natural Gas Act to regulate the prices and other terms and conditions of the sale of natural gas for resale in interstate commerce, has issued blanket authorizations for all natural gas resellers subject to its regulation, except interstate pipelines, to resell natural gas at market prices. Either Congress or the FERC (with respect to the resale of natural gas in interstate commerce), however, could re-impose price controls in the future.

Exploration and production operations and water disposal facilities are subject to various types of federal, state and local regulation, including, but not limited to, permitting, well location, methods of drilling, well operations, and conservation of resources. These regulations may affect our businesses and the businesses of certain of our customers and suppliers. It is not possible to predict how or when regulations affecting our operations or our customers’ or suppliers’ operations might change.

Regulation of the Transportation and Storage of Natural Gas and Oil and Related Facilities. The FERC regulates oil pipelines under the Interstate Commerce Act and natural gas pipeline and storage companies under the Natural Gas Act, and Natural Gas Policy Act of 1978 (the “NGPA”), as amended by the Energy Policy Act of 2005. The Grand Mesa Pipeline became operational on November 1, 2016 and has several points of origin in Colorado, runs from those origin points through Kansas and terminates in Cushing, Oklahoma. The transportation services on the Grand Mesa Pipeline are subject to FERC regulation. In February 2018, the FERC issued a revised policy to disallow income tax allowance cost recovery in rates charged by pipeline companies organized as master limited partnerships. The FERC’s revised policy impacts cost-of-service rates on oil pipelines. Currently, the volumes of crude oil that are transported on the Grand Mesa Pipeline are subject to contractual agreements. Therefore, the FERC’s revised policy has not impacted the Grand Mesa Pipeline at the present time. Additionally, contracts we enter into for the interstate transportation or storage of crude oil or natural gas may be subject to FERC regulation including reporting or other requirements. In addition, the intrastate transportation and storage of crude oil and natural gas is subject to regulation by the state in which such facilities are located, and such regulation can affect the availability and price of our supply, and have both a direct and indirect effect on our business.

Anti-Market Manipulation. We are subject to the anti-market manipulation provisions in the Natural Gas Act and the NGPA, which authorizes the FERC to impose fines of up to $1 million per day per violation of the Natural Gas Act, the NGPA,

16

or their implementing regulations. In addition, the Federal Trade Commission (“FTC”) holds statutory authority under the Energy Independence and Security Act of 2007 to prevent market manipulation in petroleum markets, including the authority to request that a court impose fines of up to $1 million per violation. These agencies have promulgated broad rules and regulations prohibiting fraud and manipulation in oil and gas markets. The Commodity Futures Trading Commission (“CFTC”) is directed under the Commodity Exchange Act to prevent price manipulations in the commodity and futures markets, including the energy futures markets. Pursuant to statutory authority, the CFTC has adopted anti-market manipulation regulations that prohibit fraud and price manipulation in the commodity and futures markets. The CFTC also has statutory authority to seek civil penalties of up to the greater of $1 million per day per violation or triple the monetary gain to the violator for violations of the anti-market manipulation sections of the Commodity Exchange Act. We are also subject to various reporting requirements that are designed to facilitate transparency and prevent market manipulation.

Environmental Regulation

General. Our operations are subject to federal, state and local laws and regulations relating to the protection of the environment. Existing regulatory structure shapes our decision-making and business activities in many ways, such as:

•shaping decisions regarding what types of pollution-control equipment to deploy and how a facility should be designed;

•informing decision-making regarding construction activities, such as where to locate and where not to locate a facility; e.g., locating construction activities away from sensitive environmental, cultural or historic areas, including wetlands, coastal regions or areas inhabited by endangered or threatened species, and limiting or prohibiting construction activities during certain sensitive periods, such as when threatened or endangered species are breeding/nesting;

•informing decision-making regarding the timing of activities, for example, we will delay construction or system modification or upgrades during the issuance or renewal periods of certain permits;

•informing decision-making pertaining to our approach to investigating, mitigating and remediating unplanned releases from our facilities and operations or attributable to former facilities or operations, as necessary and appropriate; and

•shaping our decision-making about whether a facility or operation should be temporarily halted to address potential non-compliance with relevant permit requirements.

Consideration of and compliance with relevant environmental regulatory requirements has led our business activities to be more sustainable while simultaneously mitigating exposure to long and short-term environmental risk. Conversely, failure to comply with these laws and regulations may trigger a variety of administrative, civil, and criminal enforcement measures, including the assessment of monetary penalties. Certain environmental statutes impose strict and/or joint and several liability for costs required to clean up and restore sites where substances such as crude oil or wastes have been disposed or otherwise unlawfully released. The trend in environmental regulation is to place more restrictions and limitations on activities that may adversely affect the environment. Thus, there can be no assurance as to the amount or timing of future expenditures for environmental compliance or remediation, and actual future expenditures may be different from the amounts we currently anticipate.

The following is a discussion of the material environmental laws and regulations that relate to our businesses.

Hazardous Substances and Waste. We are subject to various federal, state, and local environmental laws and regulations governing the storage, distribution, and transportation of natural gas liquids and the operation of bulk storage liquefied petroleum gas (LPG) terminals, as well as laws and regulations governing environmental protection, including those addressing the discharge of materials into the environment or otherwise relating to protection of the environment. Generally, these laws (i) regulate air and water quality, impose limitations on the discharge of pollutants and establish standards for the handling of solid and hazardous wastes; (ii) subject our operations to certain permitting and registration requirements; (iii) may result in the suspension or revocation of necessary permits, licenses and authorizations; (iv) impose substantial liabilities on us for pollution resulting from our operations; (v) require remedial measures to mitigate pollution from former or ongoing operations; and (vi) may result in the assessment of administrative, civil and criminal penalties for failure to comply with such laws. These laws include, among others, the Resource Conservation and Recovery Act (“RCRA”), the Comprehensive Environmental Response, Compensation and Liability Act (“CERCLA”), the federal Clean Air Act (“CAA”), the Homeland Security Act of 2002, the Emergency Planning and Community Right to Know Act, the Clean Water Act (“CWA”), the Safe Drinking Water Act, the Oil Spills Prevention and Preparedness Regulations, and comparable state statutes.

17

CERCLA, also known as the “Superfund” law, and similar state laws, impose liability on certain classes of potentially responsible persons that are considered to have contributed to the release of a “hazardous substance” into the environment. These persons include the current and past owner or operator of the site where the release occurred and anyone who disposed or arranged for the disposal of a hazardous substance released at the site. While natural gas liquids are not a hazardous substance within the meaning of CERCLA, other chemicals used in or generated by our operations may be classified as a hazardous substance. Persons who are or were responsible for releases of hazardous substances under CERCLA may be subject to strict and/or joint and several liability for the costs of investigating and cleaning up the hazardous substances that have been released into the environment and for damages to natural resources and for the costs of certain health studies. It is not uncommon for neighboring landowners and other third parties to file claims for personal injury and property damage allegedly caused by the release of hazardous substances into the environment.

RCRA, and comparable state statutes and their implementing regulations, regulate the generation, transportation, treatment, storage, disposal and cleanup of solid and hazardous wastes. Under a delegation of authority from the EPA, most states administer some or all of the provisions of RCRA, sometimes in conjunction with their own, more stringent requirements. Federal and state regulatory agencies can seek to impose administrative, civil and criminal penalties for alleged non-compliance with RCRA and analogous state requirements. Certain wastes associated with the production of oil and natural gas, as well as certain types of petroleum-contaminated media and debris, are excluded from regulation as hazardous waste under Subtitle C of RCRA. These wastes, instead, are regulated as solid waste under RCRA’s less stringent Subtitle D, state laws or other federal laws. It is possible, however, that certain wastes now classified as non-hazardous solid waste could be classified as hazardous wastes in the future and thereby be subject to more rigorous and costly disposal requirements. Legislation has been proposed from time to time in Congress to regulate certain oil and natural gas wastes as “hazardous wastes under RCRA.” Any such change could result in an increase in our costs to manage and dispose of wastes, which could have a material adverse effect on our consolidated results of operations and financial position.

We currently own or lease properties where crude oil is being or has been handled for many years. Although previous operators have utilized operating and disposal practices that were standard in the industry at the time, crude oil or other wastes may have been disposed of or released on or under the properties owned or leased by us or on or under the other locations where the crude oil and wastes have been transported for treatment or disposal. These properties and the wastes disposed thereon may be subject to CERCLA, RCRA and analogous state laws. Under these laws, we could be required to remove or remediate previously disposed wastes (including wastes disposed of or released by prior owners or operators), to clean up contaminated property (including contaminated groundwater) or to implement remedial measures to prevent or mitigate future contamination. We are not currently aware of any facts, events or conditions relating to such requirements that could materially impact our consolidated results of operations or financial position.

Oil Pollution Prevention. In 1973, the EPA adopted oil pollution prevention regulations under the CWA. These oil pollution prevention regulations, as amended several times since their original adoption, require the preparation of a Spill Prevention Control and Countermeasure (“SPCC”) plan for facilities engaged in drilling, producing, gathering, storing, processing, refining, transferring, distributing, using, or consuming crude oil and oil products, and which due to their location, could reasonably be expected to discharge oil in harmful quantities into or upon the navigable waters of the United States. SPCC requirements under the CWA require appropriate containment berms and similar structures to help prevent the discharge of pollutants into regulated waters in the event of a crude oil or other constituent tank spill, rupture or leak. The owner or operator of an SPCC-regulated facility is required to prepare a written, site-specific spill prevention plan, which details how a facility’s operations comply with the requirements. To be in compliance, the facility’s SPCC plan must satisfy all of the applicable requirements for drainage, bulk storage tanks, tank car and truck loading and unloading, transfer operations (intra-facility piping), inspections and records, security, and training. Most importantly, the facility must fully implement the SPCC plan and train personnel in its execution. Where applicable, we strive to maintain and implement SPCC plans for our facilities.

Air Emissions. Our operations are subject to the CAA and comparable state and local laws and regulations, which regulate emissions of air pollutants from various industrial sources and mandate certain permitting, monitoring, recordkeeping and reporting requirements. The CAA and its implementing regulations may require that we obtain permits prior to the construction, modification or operation of certain projects or facilities expected to produce or increase air emissions above certain threshold levels, that we obtain and strictly comply with air permits containing emissions and operational limitations, or utilize specific emission control technologies to limit emissions, any of which could impose significant costs on our business. Violation of CAA requirements could subject us to monetary penalties, injunctions, conditions or restrictions on operations and, potentially, criminal enforcement actions. Furthermore, we may make certain future capital expenditures for air pollution control equipment in connection with obtaining and maintaining operating permits and approvals for air emissions.

Water Discharges. The CWA and analogous state laws impose restrictions and strict controls regarding the discharge of pollutants into state waters as well as navigable waters, defined as waters of the United States (“WOTUS”), and impose

18

requirements affecting our ability to conduct construction activities in waters and wetlands. Certain state regulations and the general permits issued under the CWA’s National Pollutant Discharge Elimination System program prohibit the discharge of pollutants and chemicals. The federal SPCC program requires appropriate containment berms and similar structures to help prevent the contamination of regulated waters in the event of a crude oil or other constituent tank spill, rupture or leak. The CWA prohibits the placement of dredge or fill material in wetlands or other WOTUS unless authorized by a permit issued by the U.S. Army Corps of Engineers or a delegated state agency pursuant to Section 404. In addition, the CWA and analogous state laws require individual permits or coverage under general permits for discharges of storm water runoff from certain types of facilities. We maintain a number of discharge permits, some of which may require us to monitor and sample storm water runoff from such facilities. Some states also maintain groundwater protection programs that require permits for discharges or operations that may impact groundwater conditions. Federal and state regulatory agencies can impose administrative, civil and criminal penalties for non-compliance with discharge permits or other requirements of the CWA and analogous state laws and regulations.

Underground Injection Control. The underground injection of crude oil and natural gas wastes is regulated by the Underground Injection Control Program, as authorized by the Safe Drinking Water Act, as well as by state programs focused on the conservation of hydrocarbon resources. The primary objective of injection well operating requirements is to ensure the mechanical integrity of the injection apparatus and to prevent migration of fluid from the injection zone into underground sources of drinking water, as well as to prevent communication between injected fluids and zones capable of producing hydrocarbons. The Safe Drinking Water Act establishes requirements for permitting, testing, monitoring, record keeping, and reporting of injection well activities, as well as a prohibition against the migration of fluid containing any contaminant into underground sources of drinking water. Any leakage from the subsurface portions of the injection wells could cause degradation of fresh groundwater resources, potentially resulting in suspension of our underground injection control (“UIC”) permits, issuance of fines and penalties from governmental agencies, incurrence of expenditures for remediation of the affected resource and imposition of liability by third parties for property damages and personal injuries.

Under the auspices of the federal UIC program as implemented by states with UIC primacy, regulators, particularly at the state level, are becoming increasingly sensitive to possible correlations between underground injection and seismic activity. Consequently, state regulators implementing both the federal UIC program and state corollaries are heavily scrutinizing the location of injection facilities relative to faulting and are limiting both the density or injection facilities as well as the rate and volume of injection.

Hydraulic Fracturing. Hydraulic fracturing involves the injection of water, sand, and chemicals under pressure into the formation to stimulate oil and gas production. We do not conduct any hydraulic fracturing activities. However, a portion of our customers’ crude oil and natural gas production is developed from unconventional sources that require hydraulic fracturing as part of the completion process, and our Water Solutions business treats and disposes of produced water generated from crude oil and natural gas production, including production employing hydraulic fracturing. Legislation to amend the Safe Drinking Water Act to repeal the exemption for hydraulic fracturing from the definition of underground injection and require federal permitting and regulatory control of hydraulic fracturing, as well as legislative proposals to require disclosure of the chemical constituents of the fluids used in the fracturing process, have been proposed in recent sessions of Congress. Congress will likely continue to consider legislation to amend the Safe Drinking Water Act to subject hydraulic fracturing operations to regulation under the Act’s UIC program and/or require disclosure of chemicals used in the hydraulic fracturing process. Federal agencies, including the EPA and the United States Department of the Interior, have asserted their regulatory authority to, for example, study the potential impacts of hydraulic fracturing on the environment, and initiate rulemakings to compel disclosure of the chemicals used in hydraulic fracturing operations, and establish pretreatment standards and effluent limitation guidelines for produced water from hydraulic fracturing operations. In addition, some states and local governments have also proposed or adopted legislative or regulatory restrictions on hydraulic fracturing, which include additional permit requirements, public disclosure of fracturing fluid contents, operational restrictions, and/or temporary or permanent bans on hydraulic fracturing. We expect that scrutiny of hydraulic fracturing activities will continue in the future.

Greenhouse Gas Regulation