UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

For the fiscal year ended December 31 , 2022

or

For the transition period from to

Commission File Number: 000-55190

(Exact Name of Registrant as Specified in its Charter)

| (State or Other Jurisdiction of | (IRS Employer | ||||

| Incorporation or Organization) | Identification No.) | ||||

(Address of Principal Executive Offices, Including Zip Code)

(929 ) 777-3125

(Registrant’s Telephone Number, Including Area Code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| None | None | |||||||||||||

Securities registered pursuant to Section 12(g) of the Act : Common Stock, $0.01 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ¨ | Accelerated filer | ¨ | ☒ | Smaller reporting company | ||||||||||||||||||

| Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ý

There is no established trading market for the registrant’s common stock and therefore the aggregate market value of the registrant’s common stock held by non-affiliates cannot be determined.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date:

The Company has one class of common stock, $0.01 par value per share, 195,421,665 shares outstanding as of March 27, 2023.

NORTHSTAR HEALTHCARE INCOME, INC.

FORM 10-K

TABLE OF CONTENTS

| Index | Page | |||||||

Item 9A. | Control and Procedures | |||||||

Item 9B. | ||||||||

2

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains certain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933, as amended, or Securities Act, and Section 21E of the Securities Exchange Act of 1934, as amended, or Exchange Act. Forward-looking statements are generally identifiable by use of forward-looking terminology such as “may,” “will,” “should,” “potential,” “intend,” “expect,” “seek,” “anticipate,” “estimate,” “believe,” “could,” “project,” “predict,” “continue,” “future” or other similar words or expressions. Forward-looking statements are not guarantees of performance and are based on certain assumptions, discuss future expectations, describe plans and strategies, contain projections of results of operations or of financial condition or state other forward-looking information. Such statements include, but are not limited to, those relating to our ability to make distributions to our stockholders; our ability to retain our senior executives and other sufficient personnel to manage our business; our ability to realize substantial efficiencies as well as anticipated strategic and financial benefits of the internalization of our management function as operating costs and business disruption may be greater than expected; the operating performance of our investments, our financing needs, the effects of our current strategies and investment activities and our ability to effectively deploy capital. Our ability to predict results or the actual effect of plans or strategies is inherently uncertain. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements and you should not unduly rely on these statements. These forward-looking statements involve risks, uncertainties and other factors that may cause our actual results in future periods to differ materially from those forward-looking statements.

All forward-looking statements included in this Annual Report on Form 10-K are based on information available to us on the date hereof and we are under no duty to update any of the forward-looking statements after the date of this report to conform these statements to actual results.

Factors that could have a material adverse effect on our operations and future prospects are set forth in our filings with the U.S. Securities and Exchange Commission, or the SEC, including in this Annual Report on Form 10-K under the heading “Risk Factor Summary” and Item 1A. “Risk Factors” below. The risk factors set forth in our filings with the SEC could cause our actual results to differ significantly from those contained in any forward-looking statement contained in this report.

3

RISK FACTOR SUMMARY

Investing in our securities involves a high degree of risk. Below is a summary of principal factors that make an investment in our securities speculative or risky. This summary does not address all of the risks that we face. Additional discussion of the risks summarized in this risk factor summary, as well as other risks that we face, can be found under the heading Item 1A. “Risk Factors” below.

Risks Related to Our Business

•The continuing effects of the COVID-19 pandemic may have a material adverse effect on our business, results of operations, cash flows and financial condition.

•There is a high degree of uncertainty regarding oversight of funds provided through the CARES Act and other statutory relief efforts related to the COVID-19 pandemic.

•Macroeconomic trends, including rising labor costs and historically low unemployment, increases in inflation and rising interest rates may adversely affect our business and financial results.

•We are directly exposed to operational risks at substantially all of our owned properties and are dependent on the operators or managers of these properties to manage these risks.

•Our Winterfell, Rochester and Arbors portfolios do not currently generate sufficient cash flow from operations to satisfy all debt service obligations and capital expenditure needs.

•Events that adversely affect the ability of seniors and their families to afford resident fees at our seniors housing facilities could cause our occupancy rates, resident fee revenues and results of operations to decline.

•Increased competition could adversely affect future occupancy rates, operating margins and profitability at our properties.

•We are subject to risks associated with capital expenditures, and our failure to adequately manage such risks could have a material adverse effect on our business, financial condition and results of operations.

•We depend on two operators/managers, Watermark Retirement Communities, or Watermark, and Solstice Senior Living, or Solstice, for a significant majority of our revenues and net operating income. Adverse developments in Watermark’s or Solstice’s business and affairs or financial condition could have a material adverse effect on us.

•If we must replace any of our operators or managers, we might be unable to reposition the properties on as favorable terms, or at all, and we could be subject to delays, limitations and expenses, which could have a material adverse effect on us.

•Our strategy depends upon identifying and executing on disposition opportunities that achieve a desired return.

•Our joint venture partners could take actions that decrease the value of an investment to us and lower our overall return.

•We may have limited rights to information or ability to influence material decisions for our unconsolidated investments.

•Our unconsolidated investments involve different asset classes, structures and jurisdictions, which may expose us to different risks.

Risks Related to Our Capital Structure

•Market conditions and the actual and perceived state of the capital markets generally could negatively impact our business, financial condition and results of operations.

•We may be forced to dispose of assets at suboptimal times due to debt maturities.

•We require capital in order to operate our business, and the failure to obtain such capital would have a material adverse effect on our business, financial condition and results of operations.

•We use significant leverage in connection with our investments, which increases the risk of loss associated with our investments and restricts our ability to engage in certain activities.

•Our distribution policy is subject to change. We may not be able to make distributions in the future.

•Stockholders are not currently able to sell any of their shares of our common stock back to us pursuant to our share repurchase program, or the Share Repurchase Program, and if they do sell their shares on any limited market that may develop, they may not receive the price they paid upon subscription.

4

•Our board of directors determined an estimated value per share of $2.93 for our common stock as of June 30, 2022, which may not reflect the current value of shares of our common stock.

•No public trading market for our shares currently exists, and as a result, it will be difficult for stockholders to sell their shares and, if stockholders are able to sell their shares, stockholders will likely sell them at a substantial discount to the price paid for those shares.

•If we do not successfully implement a liquidity transaction, stockholders may have to hold their investments for an indefinite period.

Risks Related to Our Company and Corporate Structure

•As a result of the Internalization, we are newly self-managed.

•We may not realize some or all of the targeted benefits of the Internalization.

•We are reliant on certain transition services provided by our Former Advisor under the TSA, and may not find a suitable provider for these transition services if our Former Advisor no longer provides the transition services to which we are entitled under the TSA.

•Our ability to operate our business successfully would be harmed if key personnel terminate their employment with us.

•We are subject to substantial litigation risks and may face significant liabilities and damage to our professional reputation as a result of litigation allegations and negative publicity.

•We are subject to substantial regulation, numerous contractual obligations and extensive internal policies and failure to comply with these matters could have a material adverse effect on our business, financial condition and results of operations.

Risks Related to Regulatory Matters and Our REIT Tax Status

•Our failure to continue to qualify as a real estate investment trust, or REIT, would subject us to federal income tax.

5

PART I

Item 1. Business

References to “we,” “us” or “our” refer to NorthStar Healthcare Income, Inc. and its subsidiaries, unless context specifically requires otherwise.

Overview

We own a diversified portfolio of seniors housing properties, including independent living facilities, or ILFs, assisted living facilities, or ALFs, and memory care facilities, or MCFs, located throughout the United States. In addition, we have made investments through non-controlling interests in joint ventures in a broader spectrum of healthcare real estate, including seniors housing properties, as well as continuing care retirement communities, or CCRCs, skilled nursing facilities, or SNFs, medical office buildings, or MOBs, specialty hospitals and ancillary services businesses, across the United States and United Kingdom.

We were formed in October 2010 as a Maryland corporation and commenced operations in February 2013. We elected to be taxed as a REIT under the Internal Revenue Code of 1986, as amended, or the Internal Revenue Code, commencing with the taxable year ended December 31, 2013. We conduct our operations so as to continue to qualify as a REIT for U.S. federal income tax purposes.

From inception through December 31, 2022, we raised $2.0 billion in total gross proceeds from the sale of shares of our common stock in our continuous, public offerings, including $232.6 million pursuant to our distribution reinvestment plan, or our DRP, collectively referred to as our Offering.

The Internalization

From inception through October 21, 2022, we were externally managed by CNI NSHC Advisors, LLC or its predecessor, or the Former Advisor, an affiliate of NRF Holdco, LLC, or the Former Sponsor. The Former Advisor was responsible for managing our operations, subject to the supervision of our board of directors, pursuant to an advisory agreement. On October 21, 2022, we completed the internalization of our management function, or the Internalization. In connection with the Internalization, we agreed with the Former Advisor to terminate the advisory agreement and arranged for the Former Advisor to continue to provide certain services for a transition period. Going forward, we will be self-managed under the leadership of Kendall Young, who was appointed by the board of directors as Chief Executive Officer and President concurrent with the Internalization.

Our Strategy

Our primary objective is to maximize value and generate liquidity for shareholders. The key elements of our strategy include:

•Grow the Operating Income Generated by Our Portfolio. Through active portfolio management, we will continue to review and implement operating strategies and initiatives that address factors impacting the industry, including inflation and other economic conditions, to enhance the performance of our existing investment portfolio.

•Deploy Strategic Capital Expenditures. We will continue to invest capital into our investments in order to maintain market position, functional and operating standards, and improve occupancy and resident rates, in an effort to enhance the overall value of our assets.

•Pursue Dispositions and Opportunities for Asset Repositioning to Maximize Value. We will actively pursue dispositions of assets and portfolios where we believe the disposition will achieve a desired return and generate value for shareholders. Additionally, we will continue to assess the need for strategic repositioning of assets, joint ventures, operators and markets to position our portfolio for optimal performance.

Our Investments

Our investments are categorized as follows:

•Direct Investments - Operating - Properties operated pursuant to management agreements with managers, in which we own a controlling interest.

•Direct Investments - Net Lease - Properties operated under net leases with an operator, in which we own a controlling interest.

•Unconsolidated Investments - Joint ventures, which include properties operated under net leases with an operator or pursuant to management agreements with managers, in which we own a minority, non-controlling interest.

6

Our direct investments are in seniors housing facilities, which includes ILFs, ALFs, and MCFs, as described in further detail below. Revenues generated by seniors housing facilities typically come from private pay sources, including private insurance, and to a much lesser extent government reimbursement programs, such as Medicaid.

•Independent living facilities. ILFs are properties with central dining facilities that provide services that include security, housekeeping, nutrition and limited laundry services. ILFs are designed specifically for independent seniors who are able to live on their own, but desire the security and conveniences of community living. ILFs typically offer several services covered under a regular monthly fee.

•Assisted living facilities. ALFs provide services that include minimal assistance for activities in daily living and permit residents to maintain some of their privacy and independence as they do not require constant supervision and assistance. Services may be bundled within one monthly fee or based on the care needs of the resident and usually include three meals per day in a central dining room, daily housekeeping, laundry, medical reminders and 24-hour availability of assistance with the activities of daily living, such as eating, dressing and bathing. ALFs typically are comprised of studios, one and two bedroom suites equipped with private bathrooms and efficiency kitchens.

•Memory care facilities. MCFs offer specialized options for seniors with Alzheimer’s disease and other forms of dementia. These facilities offer dedicated care and specialized programming for various conditions relating to memory loss in a secured environment. Residents require a higher level of care and more assistance with activities of daily living than in ALFs. Therefore, these facilities have staff available 24 hours a day to respond to the unique needs of their residents.

Through our unconsolidated investments, we have additional investments in seniors housing facilities, as well as in additional types of healthcare real estate, including the following:

•Continuing care retirement communities. CCRCs provide, as a continuum of care, the services described for ILFs, ALFs and SNFs in an integrated campus.

•Skilled Nursing Facilities. SNFs provide services that include daily nursing, therapeutic rehabilitation, social services, housekeeping, nutrition and administrative services for individuals requiring certain assistance for activities in daily living. A typical SNF includes mostly one and two bed units, each equipped with a private or shared bathroom and community dining facilities. Revenues generated from SNFs typically come from government reimbursement programs, including Medicare and Medicaid, as well as private pay sources, including private insurance.

•Care Homes. Care homes are daily rate or rental properties in the United Kingdom that may provide residential, nursing and/or dementia care. Revenues generated from care homes typically come from private pay sources, as well as government reimbursement.

•Medical Office Buildings. MOBs are typically either single-tenant properties associated with a specialty group or multi-tenant properties leased to several unrelated medical practices. Tenants include physicians, dentists, psychologists, therapists and other healthcare providers, who require space devoted to patient examination and treatment, diagnostic imaging, outpatient surgery and other outpatient services. MOBs are similar to commercial office buildings, although they require greater plumbing, electrical and mechanical systems to accommodate physicians’ requirements such as sinks in every room, brighter lights and specialized medical equipment.

•Specialty Hospitals. Services provided by operators and tenants in hospitals are paid for by private sources, third-party payers (e.g., insurance and Health Maintenance Organizations), or through the Medicare and Medicaid programs. Our hospital properties typically will include long-term acute care, specialty and rehabilitation hospitals and generally are leased to operators under triple-net lease structures.

For financial information regarding our reportable segments, refer to Note 11, “Segment Reporting” in our accompanying consolidated financial statements included in Part II, Item 8. “Financial Statements and Supplementary Data.”

7

The following table presents a summary of investments as of December 31, 2022 (dollars in thousands):

Properties(1) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Investment Type / Portfolio | Amount(2) | Seniors Housing | MOB | SNF | Hospitals | Total | Primary Locations | Ownership Interest | ||||||||||||||||||||||||||||||||||||||||||

| Direct Investments - Operating | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Winterfell | $ | 711,505 | 32 | — | — | — | 32 | 12 U.S. States | 100.0% | |||||||||||||||||||||||||||||||||||||||||

| Rochester | 186,277 | 10 | — | — | — | 10 | New York | 97.0% | ||||||||||||||||||||||||||||||||||||||||||

| Avamere | 93,474 | 5 | — | — | — | 5 | Washington/Oregon | 100.0% | ||||||||||||||||||||||||||||||||||||||||||

| Aqua | 82,769 | 4 | — | — | — | 4 | Texas/Ohio | 97.0% | ||||||||||||||||||||||||||||||||||||||||||

| Oak Cottage | 18,613 | 1 | — | — | — | 1 | California | 100.0% | ||||||||||||||||||||||||||||||||||||||||||

| Subtotal | $ | 1,092,638 | 52 | — | — | — | 52 | |||||||||||||||||||||||||||||||||||||||||||

| Direct Investments - Net Lease | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Arbors | $ | 103,915 | 4 | — | — | — | 4 | New York | 100.0% | |||||||||||||||||||||||||||||||||||||||||

| Total Direct Investments | $ | 1,196,553 | 56 | — | — | — | 56 | |||||||||||||||||||||||||||||||||||||||||||

| Unconsolidated Investments | ||||||||||||||||||||||||||||||||||||||||||||||||||

Trilogy(3) | $ | 128,884 | 23 | — | 75 | — | 98 | 4 U.S. States | 23.2% | |||||||||||||||||||||||||||||||||||||||||

Diversified US/UK(4) | 28,442 | 95 | 106 | 39 | 9 | 249 | 17 U.S. States & U.K. | 14.3% | ||||||||||||||||||||||||||||||||||||||||||

| Eclipse | 834 | 35 | — | 9 | — | 44 | 10 U.S. States | 5.6% | ||||||||||||||||||||||||||||||||||||||||||

| Espresso | 18,019 | 1 | — | 32 | — | 33 | Ohio/Michigan | 36.7% | ||||||||||||||||||||||||||||||||||||||||||

| Subtotal | $ | 176,179 | 154 | 106 | 155 | 9 | 424 | |||||||||||||||||||||||||||||||||||||||||||

Solstice(5) | 323 | — | — | — | — | — | 20.0% | |||||||||||||||||||||||||||||||||||||||||||

| Total Unconsolidated Investments | $ | 176,502 | 154 | 106 | 155 | 9 | 424 | |||||||||||||||||||||||||||||||||||||||||||

| Total Investments | $ | 1,373,055 | 210 | 106 | 155 | 9 | 480 | |||||||||||||||||||||||||||||||||||||||||||

_______________________________________

(1)Classification based on predominant services provided, but may include other services.

(2)For direct investments, amount represents operating real estate, before accumulated depreciation as presented in our consolidated financial statements as of December 31, 2022. For unconsolidated investments, amount represents the carrying value of our investments in unconsolidated ventures as presented in our consolidated financial statements as of December 31, 2022. For additional information, refer to “Note 3, Operating Real Estate” and “Note 4, Investments in Unconsolidated Ventures” of Part II, Item 8. “Financial Statements and Supplementary Data.”

(3)Includes institutional pharmacy, therapy businesses and lease purchase buy-out options, which are not subject to property count.

(4)Refer to “—Business Update” for additional information on recent transactions.

(5)Represents our investment in Solstice Senior Living, LLC, or Solstice, the manager of the Winterfell portfolio. Solstice is a joint venture between affiliates of Integral Senior Living, LLC, or ISL, a management company of ILF, ALF and MCF founded in 2000, which owns 80.0%, and us, who owns 20.0%.

8

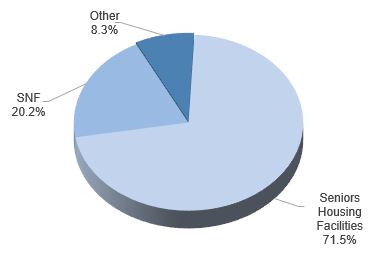

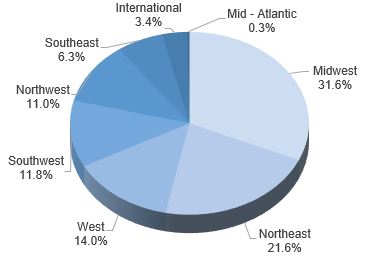

The following presents the properties of our direct and unconsolidated investments by property type and geographic location based on our proportionate share of cost as of December 31, 2022:

Real Estate Equity by Property Type(1) | Real Estate Equity by Geographic Location | |||||||

|  | |||||||

_______________________________________

(1)Classification based on predominant services provided, but may include other services.

The following table presents the operators and managers of our direct investments (dollars in thousands):

| As of December 31, 2022 | Year Ended December 31, 2022 | |||||||||||||||||||||||||

| Operator / Manager | Properties Under Management | Units Under Management(1) | Property and Other Revenues(2) | % of Total Property and Other Revenues | ||||||||||||||||||||||

Solstice Senior Living(3) | 32 | 3,993 | $ | 112,553 | 60.8 | % | ||||||||||||||||||||

| Watermark Retirement Communities | 14 | 1,782 | 45,276 | 24.3 | % | |||||||||||||||||||||

| Avamere Health Services | 5 | 453 | 19,778 | 10.7 | % | |||||||||||||||||||||

| Integral Senior Living | 1 | 40 | 4,913 | 2.7 | % | |||||||||||||||||||||

Arcadia Management(4) | 4 | 572 | 1,597 | 0.9 | % | |||||||||||||||||||||

Other(5) | — | — | 1,019 | 0.6 | % | |||||||||||||||||||||

| Total | 56 | 6,840 | $ | 185,136 | 100.0 | % | ||||||||||||||||||||

_______________________________________

(1)Represents rooms for ALFs, ILFs and MCFs, based on predominant type.

(2)Includes rental income received from our net lease properties as well as rental income, ancillary service fees and other related revenue earned from ILF residents and resident fee income derived from our ALFs and MCFs, which includes resident room and care charges, ancillary fees and other resident service charges.

(3)Solstice is a joint venture of which affiliates of ISL own 80%.

(4)During the year ended December 31, 2022, we recorded rental income to the extent rental payments were received.

(5)Consists primarily of interest income earned on corporate-level cash accounts.

Direct Investments - Operating

We generate revenues from resident fees and rental income through our operating properties. Resident fee income is recorded by our ALFs and MCFs when services are rendered and includes resident room and care charges and other resident charges and rental income is generated from our ILFs.

Our operating properties allow us to participate in the risks and rewards of the operations of the facilities, as compared to receiving only contractual rent under a net lease. We engage independent managers to operate these facilities pursuant to management agreements, including procuring supplies, hiring and training all employees, entering into all third-party contracts for the benefit of the property, including resident/patient agreements, complying with laws and regulations, including but not limited to healthcare laws, and providing resident care and services, in exchange for a management fee. As a result, we must rely on our managers’ personnel, expertise, technical resources and information systems, risk management processes, proprietary information, good faith and judgment to manage our operating properties efficiently and effectively. We also rely on our managers to set appropriate resident fees, to provide accurate property-level financial results in a timely manner and otherwise

9

operate our seniors housing facilities in compliance with the terms of our management agreements and all applicable laws and regulations.

Our management agreements generally provide for monthly management fees which are calculated based on various performance measures, including revenue, net operating income and other objective financial metrics. We are also required to reimburse our managers for expenses incurred in the operation of the properties, as well as to indemnify our managers in connection with potential claims and liabilities arising out of the operation of the properties. Our management agreements are terminable after a stated term with certain renewal rights, though we have the ability to terminate earlier upon certain events with or without the payment of a fee.

Watermark Retirement Communities and Solstice, together with their affiliates, manage substantially all of our operating properties. As of December 31, 2022, Watermark and Solstice or their respective affiliates collectively managed 46 of our seniors housing facilities pursuant to management agreements. For the year ended December 31, 2022, properties managed by Watermark and Solstice represented 24.6% and 61.1% of our total property and other revenues, respectively, and 22.4% and 59.5% of our operating real estate, respectively. Through our 20.0% ownership of Solstice, we are entitled to certain rights and minority protections. The following table presents a summary of the terms of the Watermark and Solstice management agreements:

| Manager | Portfolio | Properties | Expiration Date | Management Fees | ||||||||||||||||||||||

| Solstice Senior Living | Winterfell | 32 | October 2025 | •5% of monthly gross revenues, subject to certain exclusions •7% of actual costs of certain capital projects •Additional fees if net operating income exceeds annual target •Additional fees if net operating income long-term growth is achieved | ||||||||||||||||||||||

Watermark Retirement Communities(1) | Aqua | 2 | December 2023 | •5% of monthly gross revenues, subject to certain exclusions •Eligible for promote in connection with disposition | ||||||||||||||||||||||

| Aqua | 2 | February 2024 | ||||||||||||||||||||||||

| Rochester | 10 | August 2023 | ||||||||||||||||||||||||

_______________________________________

(1)Affiliates of Watermark also own a 3% non-controlling interest in the Rochester and Aqua portfolios, which may impact various rights and economics under the management agreements.

Direct Investments - Net Lease

We generate revenues from rental income from net leases to operators through our net lease properties. A net lease will typically provide for fixed rental payments, subject to periodic increases based on certain percentages or the consumer price index, and obligate the operator to pay all property-related expenses, including maintenance, utilities, repairs, taxes, insurance and capital expenditures.

As of December 31, 2022, we had four ALF properties operated by Arcadia Management under net leases. These leases obligate Arcadia to pay a fixed rental amount and pay all property-level expenses, with a lease term that expires in August 2029. However, Arcadia has been unable to satisfy its obligations under its leases since February 2021, and instead remits rent and pays property-level expenses based on its available cash. We are in discussions with Arcadia regarding the rent shortfalls and resulting defaults under the leases. However, we expect the rent shortfalls to continue in the near-term, in varying amounts based on the property’s performance, and may also directly incur operating expenses to the extent Arcadia is unable to generate sufficient cash flow.

10

Unconsolidated Investments

The following table presents our unconsolidated investments (dollars in thousands):

Properties as of December 31, 2022 | ||||||||||||||||||||||||||||||||||||||||||||||||||||||||

| Portfolio | Partner | Acquisition Date | Ownership | Amount(1) | Seniors Housing Facilities | MOB | SNF | Hospitals | Total | |||||||||||||||||||||||||||||||||||||||||||||||

| Trilogy | American Healthcare REIT / Management Team of Trilogy Investors, LLC | Dec-2015 | 23.2 | % | $ | 128,884 | 23 | — | 75 | — | 98 | |||||||||||||||||||||||||||||||||||||||||||||

Diversified US/UK (2) | NRF and Partner | Dec-2014 | 14.3 | % | 28,442 | 95 | 106 | 39 | 9 | 249 | ||||||||||||||||||||||||||||||||||||||||||||||

| Eclipse | NRF and Partner/ Formation Capital, LLC | May-2014 | 5.6 | % | 834 | 35 | — | 9 | — | 44 | ||||||||||||||||||||||||||||||||||||||||||||||

| Espresso | Formation Capital, LLC/Safanad Management Limited | Jul-2015 | 36.7 | % | 18,019 | 1 | — | 32 | — | 33 | ||||||||||||||||||||||||||||||||||||||||||||||

| Subtotal | $ | 176,179 | 154 | 106 | 155 | 9 | 424 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Solstice | Jul-2017 | 20.0 | % | 323 | — | — | — | — | — | |||||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | 176,502 | 154 | 106 | 155 | 9 | 424 | |||||||||||||||||||||||||||||||||||||||||||||||||

_______________________________________

(1)Represents the carrying value of our investments in unconsolidated ventures as presented in our consolidated financial statements as of December 31, 2022. For additional information, refer to “Note 4, Investments in Unconsolidated Ventures” of Part II, Item 8. “Financial Statements and Supplementary Data.”

(2)Refer to “—Business Update” for additional information on recent transactions.

We report our proportionate interest of revenues and expenses from unconsolidated joint ventures through equity in earnings (losses) of unconsolidated ventures on our consolidated statements of operations. Our unconsolidated investment portfolios are as follows:

•Diversified US/UK. Consists of three sub-portfolios: a portfolio of 15 MOBs, or the MOB Sub-Portfolio, a diversified portfolio of 91 MOBs, 47 seniors housing facilities, including ALFs, MCFs and CCRCs, 39 SNFs and nine specialty hospitals, or the Mixed U.S. Sub-Portfolio, and 48 care homes located in the United Kingdom operated under a net lease, or the U.K. Sub-Portfolio. The Former Sponsor and other minority partners own the remaining 85.7% of this portfolio.

•Trilogy. Portfolio of predominantly SNFs, as well as ALFs, ILFs, MCFs, and CCRCs located in the Midwest and operated pursuant to management agreements with Trilogy Health Services. The portfolio includes ancillary services businesses, including a therapy business and a pharmacy business. American Healthcare REIT, Inc., or AHR, and management of Trilogy own the remaining 76.8% of this portfolio.

•Eclipse. Portfolio of SNFs, ALFs, MCFs, and ILFs located in 10 U.S. States, and leased to, or managed by, five different operators/managers. The Former Sponsor and other minority partners and Formation Capital, LLC, or Formation, own 86.4% and 8.0% of this portfolio, respectively.

•Espresso. The joint venture is actively conducting the sales process for its remaining net lease portfolio of 32 SNFs and one ALF located in Ohio and Michigan. An affiliate of Formation acts as the general partner and manager of this investment. Formation and Safanad Management Limited own the remaining 63.3% of this portfolio.

•Solstice. Operator platform joint venture established to manage the operations of the Winterfell portfolio. An affiliate of ISL owns the remaining 80.0%.

11

Human Capital

On October 21, 2022, as a result of completing the Internalization, we became a self-managed REIT. Prior to the Internalization, we had no employees and were externally managed by the Former Advisor or its affiliates, who provided management, acquisition, advisory, marketing, investor relations and certain administrative services for us. As of December 31, 2022, we had eight full-time employees.

The decision to internalize, and to be able to employ directly the personnel that advance the Company’s strategic objectives, was a turning point for the Company. We believe our employees are critical to our success. All of our employees are provided with a comprehensive benefits and wellness package, which may include medical, dental and vision insurance, life insurance, 401(k) matching, long-term incentive plans, among other things. In connection with the Internalization, we worked with a compensation consultant to evaluate and benchmark the competitiveness of our compensation programs focused on pay practices that reward performance and support the needs of the Company. Our executive management team oversees our human capital resources and employment practices to ensure that an asset as important as our employees is strategically integrated with our goals and business plan as a healthcare REIT.

We are also committed to providing a safe and healthy workplace. We continuously strive to meet or exceed compliance with all laws, regulations and accepted practices pertaining to workplace safety.

We utilize a professional employer organization, or PEO, who is the employer of record of our employees and administers our benefits, payroll, and other human resource management services.

Portfolio Management

The portfolio management process for our investments includes oversight by our executive and asset management teams, regular management meetings and an operating results review process. These processes are designed to evaluate and proactively identify asset-specific issues and trends on a portfolio-wide, sub-portfolio or asset type basis. The teams work in conjunction with our managers and operators to create tailored action plans to address issues identified.

Our executive and asset management teams are experienced and use many methods to actively manage our investments to enhance or preserve our income, value and capital and mitigate risk. Our teams seek to identify opportunities for our investments that may involve replacing or renovating facilities in our portfolio which, in turn, would allow us to improve occupancy and resident rates and enhance the overall value of our assets. To manage risk, our teams engage in frequent review and dialogue with operators/managers/third party advisors and periodic inspections of our owned properties. In addition, our teams consider the impact of regulatory changes on the performance of our portfolio.

Our teams will continue to monitor the performance of, and actively manage, all of our investments. However, there can be no assurance that our investments will continue to perform in accordance with our expectations.

Profitability and Performance Metrics

We calculate Funds from Operations, or FFO, and Modified Funds from Operations, or MFFO (see “Non-GAAP Financial Measures—Funds from Operations and Modified Funds from Operations” for a description of these metrics) to evaluate the profitability and performance of our business.

Seasonality

Our revenues, and our operators’ revenues, are dependent on occupancy and may fluctuate based on seasonal trends. It is difficult to predict the magnitude of seasonal trends and the related potential impact of the cold and flu season, occurrence of epidemics or any other widespread illnesses on the occupancy of our facilities. A decrease in occupancy could affect our operating income.

Competition

Our investments will experience local and regional market competition for residents, operators and staff. Competition will be based on quality of care, reputation, physical appearance of properties, services offered, family preference, physicians, staff and price. Competition will come from independent operators as well as companies managing multiple properties, some of which may be larger and have greater resources than our operators. Some of these properties are operated for profit while others are owned by governmental agencies or tax-exempt, non-profit organizations. Competitive disadvantages may result in vacancies at facilities, reductions in net operating income and ultimately a reduction in shareholder value.

12

Inflation

Macroeconomic trends such as increases in inflation and rising interest rates can have a substantial impact on our business and financial results. Many of our costs are subject to inflationary pressures. These include labor, repairs and maintenance, food costs, utilities, insurance and other operating costs. Our managers’ ability to offset increased costs by increasing the rates charged to residents may be limited and cost inflation may therefore substantially affect the net operating income of our operating properties as well as the ability of our net lease operator to make payments to us.

Refer to Item 7A. “Quantitative and Qualitative Disclosures About Market Risk” for additional details.

Regulation

We are subject, in certain circumstances, to supervision and regulation by state and federal governmental authorities and are subject to various laws and judicial and administrative decisions imposing various requirements and restrictions, which, among other things:

•require compliance with applicable REIT rules;

•regulate healthcare operators with respect to licensure, certification for participation in government programs and relationships with patients, physicians, tenants and other referral sources;

•regulate occupational health and safety;

•regulate removal or remediation of hazardous or toxic substances;

•regulate land use and zoning;

•regulate removal of barriers to access by persons with disabilities and other public accommodations;

•regulate tax treatment and accounting standards; and

•regulate use of derivative instruments and our ability to hedge our risks related to fluctuations in interest rates and exchange rates.

Tax Regulation

We elected to be taxed as a REIT under the Internal Revenue Code, commencing with our taxable year ended December 31, 2013. If we maintain our qualification as a REIT for federal income tax purposes, we will generally not be subject to federal income tax on our taxable income that we distribute as dividends to our stockholders. If we fail to maintain our qualification as a REIT in any taxable year after electing REIT status, we will be subject to federal income tax on our taxable income at regular corporate income tax rates and will generally not be permitted to qualify for treatment as a REIT for federal income tax purposes for four years following the year in which our qualification is denied. Such an event could materially and adversely affect our net income. However, we believe that we are organized and operate in a manner that enables us to qualify for treatment as a REIT for federal income tax purposes and we intend to continue to operate so as to remain qualified as a REIT for federal income tax purposes. In addition, we operate certain healthcare properties through structures permitted under the REIT Investment Diversification and Empowerment Act of 2007, which permit the Company, through taxable REIT subsidiaries, or TRSs, to have direct exposure to resident fee income and incur related operating expenses.

U.S. Healthcare Regulation

Overview

ALFs, ILFs, MCFs, hospitals, SNFs and other healthcare providers that operate properties in our portfolio are subject to extensive and complex federal, state and local laws, regulations and industry standards governing their operations. Although the properties within our portfolio may be subject to varying levels of governmental scrutiny, we expect that the healthcare industry, in general, will continue to face increased regulation and pressure. Changes in laws, regulations, reimbursement and enforcement activity can all have a significant effect on our operations and financial condition, as set forth below and under Item 1A. “Risk Factors.”

Fraud and Abuse Enforcement

Healthcare providers are subject to federal and state laws and regulations that govern their operations, including those that require providers to furnish only medically necessary services and submit to third-party payors valid and accurate statements for each service, as well as kickback laws, self-referral laws and false claims laws. In particular, enforcement of the federal False Claims Act has resulted in increased enforcement activity for healthcare providers and can involve significant monetary damages

13

and awards to private plaintiffs who successfully bring “whistleblower” lawsuits. Sanctions for violations of these laws, regulations and other applicable guidance may include, but are not limited to, loss of licensure, loss of certification or accreditation, denial of reimbursement, imposition of civil and criminal penalties and fines, suspension or exclusion from federal and state healthcare programs or closure of the facility.

Reimbursements

Sources of revenues for our seniors housing properties are primarily private payors, including private insurers and self-pay patients, and payments from state Medicaid programs. By contrast, the skilled nursing facilities and hospitals within our unconsolidated investments receive the majority of their revenues from the Medicare and Medicaid programs, with the balance representing payments from private payors. Medicare is a federal health insurance program for persons aged 65 and over, some disabled persons and persons with end-stage renal disease. Medicaid is a medical assistance program for eligible needy persons that is funded jointly by federal and state governments and administered by the states. Medicaid eligibility requirements and benefits vary by state. The Medicare and Medicaid programs are highly regulated and subject to frequent and substantial changes resulting from legislation, regulations and administrative and judicial interpretations of existing law.

Federal, state and private payor reimbursement methodologies applied to healthcare providers are continuously evolving. Congress as well as federal and state healthcare financing authorities are continuing to implement new or modified reimbursement methodologies that shift risk to healthcare providers and generally reduce payments for services, which may negatively impact healthcare property operations. With significant budgetary pressures, federal and state governments continue to seek ways to reduce Medicare and Medicaid spending through reductions in reimbursement rates and increased enrollment in managed care programs, among other things. Private payors, such as insurance companies, are also continuously seeking opportunities to control healthcare costs. Legislation introduced in the U.S. Congress and certain state legislatures include changes that directly or indirectly affect reimbursement and promote shifts from traditional fee-for-service reimbursement models to alternative payment models that tie reimbursement to quality and cost of care, such as accountable care organizations and bundled payments. It is difficult to predict the nature and success of future financial or delivery system reforms, but changes to reimbursement rates and related policies could adversely impact our and our unconsolidated investments’ results of operations.

Licensure, CON, Certification and Accreditation

Hospitals, SNFs, seniors housing facilities and other healthcare providers that operate healthcare properties in our portfolio may be subject to extensive state licensing and certificate of need, or CON, laws and regulations, which may restrict the ability of our operators to add new properties, expand an existing facility’s size or services, or transfer responsibility for operating a particular facility to a new operator. The failure of our operators or managers to obtain, maintain or comply with any required license, CON or other certification, accreditation or regulatory approval (which could be required as a condition of licensure or third-party payor reimbursement) could result in loss of licensure, loss of certification or accreditation, denial of reimbursement, imposition of civil and/or criminal penalties and fines, suspension or exclusion from federal and state healthcare programs or closure of the facility, any of which could have an adverse effect on our operations and financial condition.

Enrollment

The federal government has taken steps to require nursing facilities to disclose detailed information regarding owners, operators, and managers of nursing homes, including both direct and indirect owning or managing entities, with a particular focus on ownership by private equity companies or REITs. Disclosure would also extend to individuals or entities that lease or sublease real property to the facilities or that own in the value of such real property. The government intends that such disclosed data would also be made publicly available. We do not know how this increased transparency will impact government scrutiny into the operations and standard of care provided at our facilities.

Health Information Privacy and Security

Healthcare providers, including those in our portfolio, are subject to numerous state and federal laws that protect the privacy and security of patient health information. The federal government, in particular, has significantly increased its enforcement of these laws. The failure of our operators and managers to maintain compliance with privacy and security laws could result in the imposition of penalties and fines, which in turn may adversely impact us.

CARES ACT and Similar Governmental Funding Programs

A variety of federal, state and local government efforts were initiated in response to the COVID-19 pandemic. At the federal level, Congress enacted a series of emergency stimulus packages, including the Coronavirus Aid, Relief and Economic Security Act, or the CARES Act, the Paycheck Protection Program and Health Care Enhancement Act, or the PPPHCE Act, and the Consolidated Appropriations Act, 2021, or CAA, to provide economic stimulus to individuals and businesses impacted by the

14

COVID-19 pandemic. The CARES Act includes provisions reimbursing eligible health care providers for certain health care-related expenses or lost revenues not otherwise reimbursed that are directly attributable to COVID-19 through the U.S. Department of Health and Human Services, or HHS, Provider Relief Fund. Recipients must satisfy reporting obligations and attest to terms and conditions. The HHS has significant anti-fraud monitoring of the funds distributed and made available a public list of providers and their payments.

We applied for and received grants from the Provider Relief Fund for our seniors housing properties. Many of our operators, including within our unconsolidated investments, also received grants from the Provider Relief Fund. As a recipient of funds from the Provider Relief Fund, we are required to comply with detailed reporting requirements specified by HHS, including in some instances by providing a third-party audit of the use of the funds received. In addition, the HHS Office of Inspector General and the Pandemic Response Accountability Committee each have the right to conduct their own audits of our use of funds from the Provider Relief Fund and HHS has the right to recoup some or all of the payments if it determines those payments were not made or the funds were not used in compliance with its rules, regulations and interpretive guidance.

The CARES Act and other relief legislation also made other forms of financial assistance available to healthcare providers in response to the COVID-19 pandemic, which benefited our seniors housing properties and our unconsolidated investments to varying degrees. This assistance included Medicare and Medicaid payment adjustments and an expansion of the Medicare Accelerated and Advance Payment Program, which made accelerated payments of Medicare funds available in 2020 in order to increase cash flow to providers. These accelerated payments are repaid by recoupment from future Medicare payments owed to providers beginning one year from the date the payment was issued. The CARES Act and related legislation also temporarily suspended Medicare sequestration payment adjustments, expanded coverage of COVID-19 testing and preventive services, addressed healthcare workforce needs and eased other legal and regulatory burdens on healthcare providers.

Federal law enforcement authorities are expected to scrutinize COVID-19 pandemic-related payments to providers as well as compliance with various reporting and transparency disclosures arising under the CARES Act, the PPPHCE Act and the CAA. Similarly, Congress is conducting its own oversight to ensure that federal dollars were properly allocated. We and our operators could become subject to this type of scrutiny, which could result in requests to repay funds, negative publicity and other adverse consequences.

Investment Company Act

We believe that we are not, and intend to conduct our operations so as not to become, regulated as an investment company under the Investment Company Act of 1940, as amended, or the Investment Company Act. We have relied, and intend to continue to rely, on current interpretations of the staff of the SEC in an effort to continue to qualify for an exemption from registration under the Investment Company Act. For more information on the exemptions that we use, refer to Item 1A. “Risk Factors—Risks Related to Regulatory Matters and Our REIT Tax Status—Maintenance of our Investment Company Act exemption imposes limits on our operations.”

For additional information regarding regulations applicable to us, refer to below and Item 1A. “Risk Factors.”

Independent Directors’ Review of Our Policies

As required by our charter, our independent directors have reviewed our policies, including but not limited to our policies regarding investments, leverage and conflicts of interest and determined that they are in the best interests of our stockholders.

Corporate Governance and Internet Address

We emphasize the importance of professional business conduct and ethics through our corporate governance initiatives. Our board of directors consists of a majority of independent directors. The audit committee and compensation committee of our board of directors are composed exclusively of independent directors. We have adopted corporate governance guidelines and a code of ethics, which delineate our standards for our officers and directors.

Our internet address is www.northstarhealthcarereit.com. The information on our website is not incorporated by reference in this Annual Report on Form 10-K. We make available, free of charge through a link on our website, our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to such reports, if any, as filed or furnished with the SEC, as soon as reasonably practicable after such filing or furnishing. Our site also contains our code of ethics, corporate governance guidelines, our audit committee charter and our compensation committee charter. Within the time period required by the rules of the SEC, we will post on our website any amendment to our code of ethics or any waiver applicable to any of our directors, executive officers or senior financial officers.

15

Item 1A. Risk Factors

The following risk factors and other information included in this Annual Report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us, or that we currently deem immaterial or that generally apply to all businesses also may adversely impact our business. If any of the following risks occur, our business, financial condition, operating results, cash flow and liquidity could be materially adversely affected.

Risks Related to Our Business and Strategy

The continuing effects of the COVID-19 pandemic may have a material adverse effect on our business, results of operations, cash flows and financial condition.

The COVID-19 pandemic has, and may continue to, materially and adversely impact our business. Our financial results have been adversely impacted as result of the pandemic and its continuing effects, including increased operating costs at our seniors housing communities as a result of labor pressures, public health measures and other operational and regulatory dynamics attributable or related to the pandemic, rising interest rates and decreased revenues.

Our industry has in particular been disproportionately impacted by COVID-19. Our revenue depends significantly on occupancy levels at our properties. COVID-19 has, to varying degrees during the course of the pandemic, prevented prospective residents and their families from visiting seniors housing and skilled nursing facilities and limited the ability of new occupants to move into these facilities. The continued impact of the pandemic on occupancy remains uncertain at this stage.

At the same time, our properties have also incurred increased operational costs as a result of the COVID-19 pandemic. Lower labor force participation rates and inflationary pressures affecting wages have driven increased labor expenses across our industry, with our managers and operators implementing higher wage rates, more costly overtime and usage of contract labor to address these challenges. Our managers and operators have also experienced significant cost increases as a result of increased health and safety measures, increased governmental regulation and compliance, vaccine mandates and other operational changes necessitated either directly or indirectly by the COVID-19 pandemic. Many of these expenses may remain at these higher levels even as the pandemic continues to subside.

The extent of the continuing effect of the pandemic, policy and other actions taken in response to the pandemic and their respective consequences on our operational and financial performance will depend on a variety of factors, including the rise of new variants of the COVID-19 virus and the effectiveness of available vaccines and therapeutics against those variants; the availability and accuracy of testing; the rate of acceptance of available vaccines, vaccine boosters and therapeutics; the speed at which available vaccines, including boosters and updated versions of vaccines, and therapeutics can be successfully deployed; the rise and spread of other health conditions, such as flu and respiratory syncytial virus (RSV); ongoing clinical experience, which may differ considerably across regions and fluctuate over time; the ongoing impact on the macroeconomic environment and global financial markets, including on inflation, interest rates and the labor market; and on other future developments, including the ultimate duration, spread and intensity of new outbreaks of COVID-19 and other conditions, such as flu and RSV, the extent to which governments impose, rollback or re-impose preventative restrictions, the availability of ongoing government financial support to our business and whether any regulatory waivers or other flexibilities continue to be extended by HHS and state governments to ease providers out of the pandemic.

There is a high degree of uncertainty regarding oversight of funds provided through the CARES Act and other statutory relief efforts related to the COVID-19 pandemic.

In response to the COVID-19 pandemic, the CARES Act, the Consolidated Appropriations Act of 2021 and the American Rescue Plan Act of 2021 authorized funds to be distributed to healthcare providers through the Provider Relief Fund, which is administered by HHS. Congress intended these grants to reimburse eligible providers for healthcare-related expenses or lost revenues incurred to prevent, prepare for, and respond to COVID-19. Recipients are not required to repay distributions from the Provider Relief Fund, provided that they attest to and comply with certain terms and conditions, including reporting, record maintenance and audit requirements and not using grants received from the Provider Relief Fund to reimburse expenses or losses that other sources are obligated to reimburse. Federal, state and local governments and agencies implemented or announced other programs to provide financial and other support to businesses affected by the COVID-19 pandemic, some of which benefited us or our operators, but that impose significant regulatory and compliance obligations.

We and our operators applied for and received grants under the Provider Relief Fund. As a recipient of these funds, we are required to comply with detailed reporting requirements specified by HHS, including in some instances by providing a third-party audit of the use of the funds. In addition, the HHS Office of Inspector General and the Pandemic Response Accountability Committee each have the right to conduct their own audits of our use of funds from the Provider Relief Fund and HHS has the

16

right to recoup some or all of the payments if it determines those payments were not made or the funds not used in compliance with its rules, regulations and interpretive guidance.

There remains a high degree of uncertainty surrounding the implementation, interpretation and application of the CARES Act and other federal, state and local government pandemic relief programs, and the rules, regulations and guidance thereunder. There can be no assurance that we or our operators are or will remain in compliance with all requirements related to the payments received under the Provider Relief Fund or other government relief programs, that the terms and conditions of the Provider Relief Fund grants or other government relief programs will not change or be interpreted in ways that affect our ability or the ability of our operators to comply with such terms and conditions (which could affect the ability to retain any grants or other funds), the amount of total financial grants or other funds that we or our operators may ultimately receive or our or their eligibility to participate in any future funding. We continue to assess the potential impact of the COVID-19 pandemic and government responses to the pandemic on our business, financial condition and results of operations.

Macroeconomic trends, including rising labor costs and historically low unemployment, increases in inflation and rising interest rates may adversely affect our business and financial results.

Macroeconomic trends, including rising labor costs and historically low unemployment, increases in inflation and rising interest rates, may adversely impact our business, financial condition and results of operations. Increased labor costs and a shortage of available skilled and unskilled workers has and may continue to increase the cost of staffing at our seniors housing communities. To the extent our managers cannot hire sufficient workers, they may be required to enhance pay and benefits packages to compete effectively for such personnel or use more costly contract or overtime labor. We may not be able to offset this increased labor cost by increasing the rates charged to residents, which will result in a decrease in our net operating income.

The COVID-19 pandemic, policy and other actions taken in response to the pandemic and other recent events, such the conflict between Russia and Ukraine and supply chain disruptions, have exacerbated, and may continue to exacerbate, increases in the consumer price index. Many of our costs, including operating and administrative expenses, interest expense and capital project costs, are subject to inflation. These include expenses for property-related contracted services, utilities, repairs and maintenance and insurance and general and administrative costs. If there is an increase in these costs, our business, cash flows and operating results could be adversely affected.

Additionally, U.S. government policies implemented to address inflation, including actions by the Board of Governors of the Federal Reserve System, or the U.S. Federal Reserve, to increase interest rates could negatively impact consumer spending and future demand for our properties. In particular, primarily in response to concerns about inflation, the U.S. Federal Reserve significantly raised its benchmark federal funds rate, which has led to increases in interest rates in the credit markets and other impacts on the macroeconomic environment. The U.S. Federal Reserve may continue to raise the federal funds rate, which will likely lead to higher interest rates in the credit markets and the possibility of lower asset values, slowing economic growth and a recession.

We are directly exposed to operational risks at substantially all of our owned properties and are dependent on the operators or managers of these properties to manage these risks.

Substantially all of our owned properties, excluding unconsolidated joint ventures, are operated pursuant to management agreements, where we are directly exposed to various operational risks. These risks include: (i) fluctuations in occupancy; (ii) fluctuations in private pay rates and, to a lesser extent, government reimbursement; (iii) increases in the cost of food, materials, energy, labor (as a result of unionization, COVID-19 related workforce challenges or otherwise) or other services; (iv) rent control regulations; (v) national and regional economic conditions; (vi) the imposition of new or increased taxes; (vii) capital expenditure requirements; (viii) federal, state, local licensure, certification and inspection, fraud and abuse, and privacy and security laws, regulations and standards; (ix) professional and general liability claims; (x) the availability and increases in cost of general and professional liability insurance coverage; and (xi) the impact of actual and anticipated outbreaks of disease and epidemics, such as COVID-19. Any one or a combination of these factors may adversely affect our revenue and operations.

The pandemic resulted in significant declines in revenue at the same time that operating costs increased. Even as the pandemic has subsided, significant uncertainty continues to exist regarding the continued impact of the pandemic and macroeconomic trends on revenue and expenses at our properties, including with respect to labor and employment, inflation, rising interest rates and potential changes or disruptions in government reimbursement. For substantially all of our directly owned properties, we are responsible for operating shortfalls if the properties do not generate sufficient revenues to cover expenses. For the year ended December 31, 2022, four of our direct operating investment properties generated operating losses.

Although we are directly exposed to operational risks, our managers are ultimately in control of the day-to-day business of our seniors housing facilities. We rely on our managers’ personnel, expertise, technical resources and information systems, proprietary information, good faith and judgment to manage our seniors housing facilities efficiently and effectively. We also

17

rely on our managers to set appropriate resident fees, to provide accurate property-level financial results for our properties in a timely manner and to otherwise operate our seniors housing facilities in compliance with all applicable laws and regulations. While we have various rights as the property owner under our management agreements, we may have limited recourse under our management agreements if we believe that the managers are not performing adequately. The failure by our managers to effectively manage these properties could have a material adverse effect on our business, results of operations and financial condition.

Our Winterfell, Rochester and Arbors portfolios do not currently generate sufficient cash flow from operations to satisfy all debt service obligations and capital expenditure needs.

As of December 31, 2022, our Winterfell, Rochester and Arbors portfolios, which represent 59.5%, 15.6% and 8.7% of our operating real estate, respectively, and 64.7%, 14.1% and 9.0% of our borrowings outstanding, respectively, do not currently generate sufficient cash flow from operations to satisfy all debt service obligations on the borrowings for these portfolios, as well as the capital expenditures we deem necessary in order to maintain the value of the portfolios. We are currently using other sources of capital to satisfy these obligations, including cash flow generated by other portfolios and dispositions. These operating shortfalls are adversely impacting our liquidity and results of operations. If performance of these portfolios does not improve, it will have a material adverse impact on the overall value of our investments.

Events that adversely affect the ability of seniors and their families to afford resident fees at our seniors housing facilities could cause our occupancy rates, resident fee revenues and results of operations to decline.

Costs to seniors associated with independent and assisted living services are generally not reimbursable under government reimbursement programs such as Medicare and Medicaid. Only seniors with income or assets meeting or exceeding the comparable median in the regions where our facilities are located typically will be able to afford to pay the monthly resident fees, and a weak economy, depressed housing market or changes in demographics could adversely affect their continued ability to do so. If our operators and managers are unable to retain and attract seniors with sufficient income, assets or other resources required to pay the fees associated with independent and assisted living services, our occupancy rates and resident fee revenues could decline, which could, in turn, materially adversely affect our business, results of operations and financial condition.

Increased competition could adversely affect future occupancy rates, operating margins and profitability at our properties.

The healthcare and seniors housing industries are highly competitive, and our operators and managers may encounter increased competition for residents and patients, including with respect to the scope and quality of care and services provided, reputation and financial condition, physical appearance of the properties, price and location. If development outpaces demand in the markets in which our properties are located, those markets may become saturated and our operators and managers could experience decreased occupancy, reduced operating margins and lower profitability, which could have a material adverse effect on us.

We are subject to risks associated with capital expenditures, and our failure to adequately manage such risks could have a material adverse effect on our business, financial condition and results of operations.

Our properties require significant investment in capital expenditures. If we fail to adequately invest in capital expenditures, occupancy rates and the amount of rental and reimbursement income generated by our facilities may decline, which would negatively impact the overall value of the affected facilities. At the same time, capital expenditures subject us to risks, including cost overruns, the inability of the operator to generate sufficient cash flow to achieve the projected return and potential declines in the value of the property. There can be no assurance that any investment in capital expenditures increases the overall return on our investments. If we fail to adequately manage such risks, it could have a material adverse effect on our business, financial condition and results of operations. These risks may be further heightened due to our limited sources of liquidity, and we could find ourselves in a position with insufficient liquidity to fund future obligations.

We depend on two operators/managers, Watermark Retirement Communities, or Watermark, and Solstice Senior Living, or Solstice, for a significant majority of our revenues and net operating income. Adverse developments in Watermark’s or Solstice’s business and affairs or financial condition could have a material adverse effect on us.

As of December 31, 2022, Watermark and Solstice or their respective affiliates collectively managed 46 of our seniors housing facilities pursuant to management agreements. For the year ended December 31, 2022, properties managed by Watermark and Solstice represented 24.6% and 61.1% of our total property and other revenues, respectively, and 22.4% and 59.5% of our operating real estate, respectively.

Watermark and Solstice, either directly or through affiliates, operate other properties or have other business initiatives that may be in conflict with our interests or cause them to fail to prioritize our properties. In addition, if either Watermark or Solstice are unable to attract, retain and incentivize qualified personnel, it could impair their respective ability to manage our properties

18

efficiently and effectively. Further, any significant changes in senior management or equity ownership, or adverse developments in their businesses and affairs or financial condition, could also impair their respective ability to manage our properties and could have a materially adverse effect on us.

If we must replace any of our operators or managers, we might be unable to reposition the properties on as favorable terms, or at all, and we could be subject to delays, limitations and expenses, which could have a material adverse effect on us.

If our operators or managers experience performance challenges, or at the expiration of a lease term, we may need to negotiate new leases or management agreements with our operators or managers or reposition our properties with new operators or managers. In these circumstances, rental payments or operating cash flow on the related properties could decline or cease altogether while we reposition the properties. We also may not be successful in identifying suitable replacements or enter into new leases or management agreements on a timely basis or on terms as favorable to us as our current leases and management agreements, if at all, and we may be required to fund certain expenses and obligations (e.g., real estate taxes, insurance, debt costs and maintenance expenses) to preserve the value of, and avoid the imposition of liens on, our properties while they are being repositioned. In addition, we may incur certain obligations and liabilities, including obligations to indemnify the replacement operator or manager. Replacement of operators or managers may also be subject to regulatory approvals. Once a suitable replacement operator/manager has taken over operation of the properties, it may still take an extended period of time before the properties are fully repositioned and value restored, if at all. If we are unable to find a suitable replacement operator or manager, we may determine to dispose of a property, which may result in a loss. Any of these results could have a material adverse effect on our business, financial condition and results of operations.

Our strategy depends upon identifying and executing on disposition opportunities that achieve a desired return.

An important part of our business strategy is to identify and execute on disposition opportunities that achieve a desired return. Our ability to execute this strategy is affected by many factors outside of our control, including general economic conditions and disruptions in capital markets. If the performance of our properties does not improve, due to labor markets, inflation, concerns regarding pandemics or otherwise, or rising interest rates or disruptions in the capital markets result in lower asset values, we may be unable to achieve desired returns. In addition, a significant amount of our borrowings mature in 2025, which may force us to sell assets at a suboptimal time, further limiting our ability to achieve a desired return.

Because real estate investments are relatively illiquid, we may not be able to sell or exchange our properties in response to changes in economic and other conditions, which may result in losses to us.

Real estate investments are relatively illiquid, and our ability to quickly sell or exchange our properties in response to changes in economic or other conditions is limited. In the event we market any of our properties for sale, the value of those properties and our ability to sell at prices or on terms acceptable to us could be adversely affected by a downturn in the real estate industry or any economic weakness in the healthcare and seniors housing industries. In addition, transfers of healthcare and seniors housing properties may be subject to regulatory approvals that are not required for transfers of other types of commercial properties. We cannot assure you that we will recognize the full value of any property that we sell for liquidity or other reasons, and the inability to respond quickly to changes in the performance of our investments could adversely affect our business, results of operations and financial condition.

Our joint venture partners could take actions that decrease the value of an investment to us and lower our overall return.

We have made significant investments through joint ventures with third parties, both in circumstances where we have a controlling, majority interest, such as our joint ventures with Watermark for the Aqua and Rochester portfolios, and a minority, non-controlling interest, such as our unconsolidated investments in the Diversified US/UK, Eclipse, Espresso and Trilogy portfolios.

These investments generally involve risks not otherwise present with other methods of investment, including, for example, the following risks:

•fraud or other misconduct by our joint venture partners;

•we may share decision-making authority with our joint venture partner regarding certain major decisions affecting the ownership of the joint venture and the joint venture property, such as the sale of the property or the making of additional capital contributions for the benefit of the property, which may prevent us from taking actions that are opposed by our joint venture partner;