0001501697False2023FYDelaware61 North Beacon Street4th FloorMassachusettsBoston0213410-Khttp://fasb.org/us-gaap/2023#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2023#OtherAssetsNoncurrent1falsehttp://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2023#OtherLiabilitiesNoncurrentP5YP3YON SALE OF NONFINANCIAL ASSETSDuring the year ended December 31, 2022, a third party, who had previously acquired rights to certain intellectual

property from the Company, terminated the arrangement and transferred these rights back to the Company. Also during the year ended December 31, 2022, the Company transferred these rights to another third party in return for $0.5 million. The Company has no continuing involvement in any ongoing research and development activities associated with the intellectual

property. The Company concluded that these third parties are "non-customers" as the underlying intellectual property

transferred to and from these third parties supports potential drug candidates that are not aligned with the Company's strategic

focus and, therefore, are not an output of the Company's ordinary activities. Accordingly, the Company accounted for the sale

of the intellectual property as the sale of a non-financial asset under ASC Topic 610-20, Gains and Losses from the

Derecognition of Nonfinancial Assets ("ASC 610-20"), and included the gain in gain on sale of non-financial asset for the year ended December 31, 2022.

00015016972023-01-012023-12-3100015016972023-06-30iso4217:USD00015016972024-03-18xbrli:shares00015016972023-12-3100015016972022-12-31iso4217:USDxbrli:shares00015016972022-01-012022-12-3100015016972021-01-012021-12-310001501697xfor:RedeemableCommonStockMember2020-12-310001501697us-gaap:CommonStockMember2020-12-310001501697us-gaap:AdditionalPaidInCapitalMember2020-12-310001501697us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001501697us-gaap:RetainedEarningsMember2020-12-3100015016972020-12-310001501697xfor:RedeemableCommonStockMember2021-01-012021-12-310001501697us-gaap:CommonStockMember2021-01-012021-12-310001501697us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001501697us-gaap:RetainedEarningsMember2021-01-012021-12-310001501697xfor:RedeemableCommonStockMember2021-12-310001501697us-gaap:CommonStockMember2021-12-310001501697us-gaap:AdditionalPaidInCapitalMember2021-12-310001501697us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-310001501697us-gaap:RetainedEarningsMember2021-12-3100015016972021-12-310001501697us-gaap:CommonStockMember2022-01-012022-12-310001501697us-gaap:AdditionalPaidInCapitalMember2022-01-012022-12-310001501697us-gaap:RetainedEarningsMember2022-01-012022-12-310001501697xfor:RedeemableCommonStockMember2022-12-310001501697us-gaap:CommonStockMember2022-12-310001501697us-gaap:AdditionalPaidInCapitalMember2022-12-310001501697us-gaap:AccumulatedOtherComprehensiveIncomeMember2022-12-310001501697us-gaap:RetainedEarningsMember2022-12-310001501697us-gaap:CommonStockMember2023-01-012023-12-310001501697us-gaap:AdditionalPaidInCapitalMember2023-01-012023-12-310001501697us-gaap:RetainedEarningsMember2023-01-012023-12-310001501697xfor:RedeemableCommonStockMember2023-12-310001501697us-gaap:CommonStockMember2023-12-310001501697us-gaap:AdditionalPaidInCapitalMember2023-12-310001501697us-gaap:AccumulatedOtherComprehensiveIncomeMember2023-12-310001501697us-gaap:RetainedEarningsMember2023-12-310001501697xfor:MinCashTestDate1Memberxfor:HerculesSecondAmendedLoanAgreementMember2023-12-310001501697xfor:WalthamLeaseMemberus-gaap:LetterOfCreditMember2023-12-310001501697xfor:WalthamLeaseMemberus-gaap:LetterOfCreditMember2022-12-310001501697us-gaap:LetterOfCreditMemberxfor:ViennaLeaseArrangementMember2023-12-310001501697us-gaap:LetterOfCreditMemberxfor:ViennaLeaseArrangementMember2022-12-310001501697us-gaap:LetterOfCreditMemberxfor:AllstonLeaseMember2023-12-310001501697us-gaap:LetterOfCreditMemberxfor:AllstonLeaseMember2022-12-310001501697xfor:HerculesFirstAmendedLoanAgreementMember2023-01-012023-12-310001501697srt:MinimumMemberus-gaap:FurnitureAndFixturesMember2023-12-310001501697srt:MaximumMemberus-gaap:FurnitureAndFixturesMember2023-12-310001501697us-gaap:ComputerEquipmentMember2023-12-310001501697us-gaap:EquipmentMembersrt:MinimumMember2023-12-310001501697us-gaap:EquipmentMembersrt:MaximumMember2023-12-310001501697us-gaap:LeaseholdImprovementsMembersrt:MaximumMember2023-12-31xfor:reporting_unit0001501697xfor:GenzymeAgreementMember2023-01-012023-12-310001501697xfor:GenzymeAgreementMember2023-12-310001501697xfor:A6NetSalesMemberxfor:GenzymeAgreementMember2023-12-31xbrli:pure0001501697xfor:A6NetSalesMemberxfor:GenzymeAgreementMember2023-01-012023-12-310001501697xfor:A10NetSalesMemberxfor:GenzymeAgreementMember2023-12-310001501697xfor:A10NetSalesMemberxfor:GenzymeAgreementMembersrt:MinimumMember2023-01-012023-12-310001501697xfor:A10NetSalesMembersrt:MaximumMemberxfor:GenzymeAgreementMember2023-01-012023-12-310001501697xfor:GenzymeAgreementMemberxfor:A12NetSalesMember2023-12-310001501697xfor:GenzymeAgreementMemberxfor:A12NetSalesMember2023-01-012023-12-310001501697xfor:GenzymeAgreementMember2021-01-012021-12-310001501697xfor:GeorgetownMember2016-12-012016-12-310001501697xfor:GeorgetownMember2023-01-012023-12-310001501697xfor:GeorgetownMember2021-01-012021-12-310001501697xfor:GeorgetownMember2022-01-012022-12-310001501697xfor:GeorgetownMember2022-12-310001501697xfor:GeorgetownMember2023-12-310001501697xfor:GeorgetownMember2021-12-310001501697xfor:BidmcAgreementMember2016-12-012016-12-310001501697xfor:BidmcAgreementMember2022-01-012022-12-310001501697xfor:BidmcAgreementMember2021-01-012021-12-310001501697xfor:BidmcAgreementMember2023-01-012023-12-310001501697xfor:DFCIMember2020-11-012020-11-300001501697xfor:DFCIMember2023-01-012023-12-310001501697xfor:MTSAustriaMember2023-01-012023-12-310001501697xfor:ResearchAndDevelopmentIncentiveProgramMember2023-12-310001501697xfor:ResearchAndDevelopmentIncentiveProgramMember2022-12-310001501697xfor:ResearchAndDevelopmentIncentiveProgramMember2023-01-012023-12-310001501697xfor:ResearchAndDevelopmentIncentiveProgramMember2022-01-012022-12-310001501697xfor:ResearchAndDevelopmentIncentiveProgramMember2021-01-012021-12-310001501697xfor:AbbiskoAgreementMember2023-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMember2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMemberus-gaap:FairValueInputsLevel2Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMemberus-gaap:FairValueInputsLevel3Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMember2023-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:USTreasuryBillSecuritiesMember2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USTreasuryBillSecuritiesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USTreasuryBillSecuritiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:USTreasuryBillSecuritiesMember2023-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMember2023-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel2Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2023-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMember2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel2Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2023-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMember2023-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMember2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMemberus-gaap:FairValueInputsLevel2Member2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMemberus-gaap:FairValueInputsLevel3Member2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:MoneyMarketFundsMember2022-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMember2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMember2022-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel2Member2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:DerivativeFinancialInstrumentsLiabilitiesMember2022-12-310001501697us-gaap:FairValueInputsLevel1Memberus-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMember2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel2Member2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2022-12-310001501697us-gaap:FairValueMeasurementsRecurringMemberus-gaap:WarrantMember2022-12-310001501697us-gaap:USTreasurySecuritiesMember2023-12-310001501697us-gaap:USGovernmentCorporationsAndAgenciesSecuritiesMember2023-12-310001501697us-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2020-12-310001501697xfor:PIPEWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2020-12-310001501697xfor:ClassCWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2020-12-310001501697us-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2021-01-012021-12-310001501697xfor:PIPEWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2021-01-012021-12-310001501697xfor:ClassCWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2021-01-012021-12-310001501697us-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2021-12-310001501697xfor:PIPEWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2021-12-310001501697xfor:ClassCWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2021-12-310001501697us-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2022-01-012022-12-310001501697xfor:PIPEWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2022-01-012022-12-310001501697xfor:ClassCWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2022-01-012022-12-310001501697us-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2022-12-310001501697xfor:PIPEWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2022-12-310001501697xfor:ClassCWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2022-12-310001501697us-gaap:WarrantMember2023-01-012023-12-310001501697us-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2023-01-012023-12-310001501697xfor:PIPEWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2023-01-012023-12-310001501697xfor:ClassCWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2023-01-012023-12-310001501697us-gaap:DerivativeFinancialInstrumentsLiabilitiesMemberus-gaap:FairValueInputsLevel3Member2023-12-310001501697xfor:PIPEWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2023-12-310001501697xfor:ClassCWarrantsMemberus-gaap:WarrantMemberus-gaap:FairValueInputsLevel3Member2023-12-310001501697xfor:PIPEWarrantsMember2022-07-060001501697xfor:PIPEWarrantsMember2022-09-010001501697us-gaap:WarrantMember2022-12-070001501697us-gaap:WarrantMember2022-12-310001501697us-gaap:WarrantMember2023-12-310001501697xfor:PIPEWarrantsMember2022-07-062022-07-060001501697xfor:PIPEWarrantsMember2022-09-012022-09-010001501697us-gaap:WarrantMember2022-12-072022-12-070001501697us-gaap:WarrantMember2022-01-012022-12-310001501697us-gaap:WarrantMember2023-01-012023-12-310001501697us-gaap:LeaseholdImprovementsMember2023-12-310001501697us-gaap:LeaseholdImprovementsMember2022-12-310001501697us-gaap:FurnitureAndFixturesMember2023-12-310001501697us-gaap:FurnitureAndFixturesMember2022-12-310001501697us-gaap:ComputerEquipmentMember2022-12-310001501697xfor:SoftwareMember2023-12-310001501697xfor:SoftwareMember2022-12-310001501697xfor:LabEquipmentMember2023-12-310001501697xfor:LabEquipmentMember2022-12-310001501697xfor:HerculesLoanAgreementMember2023-12-310001501697xfor:HerculesLoanAgreementMember2018-10-012021-03-310001501697xfor:HerculesLoanAgreementMember2023-01-012023-12-310001501697xfor:HerculesLoanAgreementMemberus-gaap:PrimeRateMember2023-01-012023-12-310001501697xfor:HerculesLoanAgreementMember2023-10-012023-12-310001501697srt:ScenarioForecastMemberxfor:HerculesLoanAgreementMember2024-07-012024-07-010001501697xfor:HerculesLoanAgreementMember2022-01-012022-12-310001501697xfor:HerculesLoanAgreementMember2021-01-012021-12-310001501697xfor:HerculesSecondAmendedLoanAgreementMember2023-12-310001501697xfor:HerculesSecondAmendedLoanAgreementMember2023-01-012023-12-310001501697xfor:AllstonLeaseMember2019-11-112019-11-11utr:sqft0001501697xfor:AllstonLeaseMember2019-11-110001501697xfor:WalthamLeaseMember2019-03-132019-03-1300015016972019-03-132019-03-130001501697xfor:NewViennaLeaseMember2020-09-012020-09-010001501697xfor:NewViennaLeaseMember2020-09-010001501697xfor:SalesAgentsMemberus-gaap:CommonStockMember2020-08-072020-08-070001501697xfor:SalesAgentsMemberus-gaap:CommonStockMember2023-12-310001501697xfor:IssuanceOnMarch232021Member2021-03-182021-03-180001501697xfor:IssuanceOnMarch232021Memberus-gaap:RedeemablePreferredStockMember2021-03-182021-03-180001501697xfor:PreFundedWarrantMemberxfor:IssuanceOnMarch232021Member2023-12-310001501697xfor:IssuanceOnMarch232021Member2023-12-310001501697xfor:FundedMember2021-03-2300015016972021-03-182021-03-180001501697xfor:RedeemableCommonStockMember2021-03-182021-03-180001501697xfor:LincolnParkCapitalFundLLCMember2022-01-142022-01-140001501697us-gaap:EquityUnitPurchaseAgreementsMember2020-10-142020-10-1400015016972022-01-1400015016972022-01-142022-01-140001501697xfor:Q12022PIPEMember2022-03-032022-03-030001501697xfor:Q12022PIPEMember2022-03-030001501697xfor:PreFundedWarrantMember2022-03-0300015016972022-03-030001501697xfor:Q22022PrivatePlacementMember2023-01-012023-12-310001501697xfor:Q22022PrivatePlacementMemberxfor:PreFundedWarrantMember2023-12-310001501697xfor:Q22022PrivatePlacementMember2021-03-230001501697xfor:Q22022PrivatePlacementMemberxfor:PreFundedWarrantMember2019-11-260001501697xfor:Q22022PrivatePlacementMember2023-12-310001501697xfor:Q22022PrivatePlacementMember2021-03-232021-03-2300015016972022-09-010001501697us-gaap:WarrantMember2022-07-060001501697xfor:PreFundedWarrantMember2022-07-0600015016972023-04-012023-06-300001501697xfor:Q42022PublicOfferingMember2022-12-072022-12-070001501697xfor:Q42022PublicOfferingMemberxfor:PreFundedWarrantMember2022-12-070001501697xfor:Q42022PublicOfferingMember2022-12-070001501697xfor:ClassCWarrantsMemberxfor:Q42022PublicOfferingMember2022-12-0700015016972022-12-070001501697xfor:Q22023PIPEMember2023-05-152023-05-150001501697xfor:Q22023PIPEMember2023-05-150001501697xfor:PreFundedWarrantMemberxfor:Q22023PIPEMember2023-05-150001501697xfor:ClassAWarrantMember2019-04-162019-04-160001501697xfor:ClassAWarrantMember2019-04-160001501697xfor:ClassBWarrantsMember2019-11-260001501697xfor:ClassBWarrantsMember2019-11-2900015016972019-11-262019-11-260001501697xfor:ClassCWarrantsMember2022-12-090001501697srt:MinimumMember2021-03-230001501697srt:MaximumMember2021-03-2300015016972020-01-012020-12-310001501697xfor:IssuanceOnOctoberTwentyFiveTwoThousandSixteenMember2023-12-310001501697xfor:IssuanceOnDecemberTwentyEightTwoThousandSeventeenOneMember2023-12-310001501697xfor:IssuanceOnSeptemberTwelveTwoThousandEighteenOneMember2023-12-310001501697xfor:IssuanceOnOctoberNineteenTwoThousandEighteenMember2023-12-310001501697xfor:IssuanceOnMarchThirteenTwoThousandNineteenMember2023-12-310001501697xfor:IssuanceOnAprilSixteenTwoThousandNineteenMember2023-12-310001501697xfor:IssuanceOnNovemberTwentyNineTwoThousandNineteenOneMember2023-12-310001501697xfor:IssuanceOnNovemberNineTwoThousandTwentyOneMember2023-12-310001501697xfor:IssuanceOnMarch32022Member2023-12-310001501697xfor:IssuanceOnJuly20221Member2023-12-310001501697xfor:IssuanceOnJuly620222Member2023-12-310001501697xfor:IssuanceOnDecember92022Member2022-12-090001501697xfor:IssuanceOnDecember92022Member2023-12-310001501697xfor:IssuanceOnDecember920222Member2022-12-090001501697xfor:IssuanceOnDecember920222Member2023-12-310001501697xfor:IssuanceOnMay182023Member2023-05-180001501697xfor:IssuanceOnMay182023Member2023-12-310001501697xfor:PreFundedWarrantMember2019-11-2900015016972019-11-2900015016972021-03-230001501697xfor:FundedMember2021-11-0900015016972021-11-3000015016972021-11-090001501697xfor:FundedMember2022-03-030001501697xfor:FundedMember2022-07-0600015016972022-07-060001501697xfor:FundedMember2022-12-0900015016972022-12-090001501697srt:MaximumMemberus-gaap:EmployeeStockOptionMember2023-01-012023-12-310001501697xfor:IncentiveStockOptionsAndRestrictedStockAwardsMember2023-01-012023-12-310001501697srt:MinimumMemberxfor:NonStatutoryOptionsMember2023-01-012023-12-310001501697srt:MaximumMemberxfor:NonStatutoryOptionsMember2023-01-012023-12-310001501697xfor:A2015EquityIncentivePlanMember2023-12-310001501697xfor:TwoThousandSeventeenEquityIncentivePlanMember2023-01-012023-12-310001501697xfor:TwoThousandSeventeenEquityIncentivePlanMember2023-12-310001501697xfor:TwoThousandSeventeenEquityIncentivePlanMember2021-01-010001501697xfor:EmployeeStockPurchasePlansMemberxfor:TwoThousandSeventeenEquityIncentivePlanMember2023-01-012023-12-310001501697xfor:EmployeeStockPurchasePlansMemberxfor:TwoThousandSeventeenEquityIncentivePlanMember2023-12-310001501697xfor:TwoThousandNineteenEquityIncentivePlanMember2023-12-310001501697us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001501697us-gaap:RestrictedStockUnitsRSUMember2022-12-310001501697us-gaap:RestrictedStockUnitsRSUMember2023-12-310001501697us-gaap:ResearchAndDevelopmentExpenseMember2023-01-012023-12-310001501697us-gaap:ResearchAndDevelopmentExpenseMember2022-01-012022-12-310001501697us-gaap:ResearchAndDevelopmentExpenseMember2021-01-012021-12-310001501697us-gaap:GeneralAndAdministrativeExpenseMember2023-01-012023-12-310001501697us-gaap:GeneralAndAdministrativeExpenseMember2022-01-012022-12-310001501697us-gaap:GeneralAndAdministrativeExpenseMember2021-01-012021-12-310001501697us-gaap:WarrantMember2023-07-012023-07-010001501697us-gaap:WarrantMember2022-07-062022-07-060001501697us-gaap:StockAppreciationRightsSARSMember2023-01-012023-12-310001501697us-gaap:StockAppreciationRightsSARSMember2022-01-012022-12-310001501697us-gaap:DomesticCountryMember2023-12-310001501697us-gaap:StateAndLocalJurisdictionMember2023-12-310001501697us-gaap:ForeignCountryMember2023-12-310001501697us-gaap:DomesticCountryMemberus-gaap:ResearchMember2023-12-310001501697us-gaap:StateAndLocalJurisdictionMemberus-gaap:ResearchMember2023-12-310001501697us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-12-310001501697us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-12-310001501697us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-12-310001501697us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-01-012023-12-310001501697us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2022-01-012022-12-310001501697us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-01-012021-12-310001501697us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2023-12-310001501697xfor:PreFundedWarrantMembersrt:MinimumMember2023-12-310001501697us-gaap:StockOptionMember2023-01-012023-12-310001501697us-gaap:StockOptionMember2022-01-012022-12-310001501697us-gaap:StockOptionMember2021-01-012021-12-310001501697us-gaap:RestrictedStockUnitsRSUMember2023-01-012023-12-310001501697us-gaap:RestrictedStockUnitsRSUMember2022-01-012022-12-310001501697us-gaap:RestrictedStockUnitsRSUMember2021-01-012021-12-310001501697us-gaap:WarrantMember2023-01-012023-12-310001501697us-gaap:WarrantMember2022-01-012022-12-310001501697us-gaap:WarrantMember2021-01-012021-12-31 UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One) | | | | | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023

or

| | | | | |

| o | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number: 001-38295

_________________________________________________________________________________________________________

X4 PHARMACEUTICALS, INC.

(Exact name of registrant as specified in its charter)

________________________________________________________________________________________________________ | | | | | |

Delaware (State or other jurisdiction of incorporation or organization) | 27-3181608 (I.R.S. Employer Identification No.) |

|

|

61 North Beacon Street, 4th Floor Boston, Massachusetts (Address of principal executive offices) | 02134 (Zip Code) |

(857) 529-8300

(Registrant’s telephone number, including area code)

_____________________________________________________________________________________

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | | | | | | | |

| Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

| Common Stock |

| XFOR |

| The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: none

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (of this chapter) during the preceding 12 months (of for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. | | | | | | | | | | | | | | |

| Large Accelerated Filer | ☐ |

| Accelerated Filer | ☐ |

| Non-accelerated filer | ☒ |

| Smaller reporting company | ☒ |

|

|

| Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐ Indicate by check mark whether the registrant has filed a report on an attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. Yes ☐ No ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to § 240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐

On June 30, 2023, the aggregate market value of the registrant’s voting common stock held by non-affiliates of the registrant was approximately $318 million based upon the closing sale price on the Nasdaq Capital Market reported on June 30, 2023. In determining the market value of non-affiliate common stock, shares of the registrant’s common stock beneficially owned by officers, directors and affiliates have been excluded. This determination of affiliate status is not necessarily a conclusive determination for other purposes. | | | | | | | | | | | | | | |

| Independent Registered Public Accounting Firm | PricewaterhouseCoopers LLP | Boston, Massachusetts, US | Firm ID | 238 |

As of March 18, 2024, there were 167,937,781 shares of the registrant’s common stock, $0.001 par value per share outstanding. DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive proxy statement, (the “2024 Proxy Statement”) for its 2024 Annual Meeting of Stockholders, which the registrant intends to file pursuant to Regulation 14A with the Securities and Exchange Commission not later than 120 days after the registrant's fiscal year ended December 31, 2023, are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS | | | | | | | | |

| | |

| | 5 |

| | |

| | |

| Item 1C. | | 66 |

| | |

| | |

| | |

| | |

| | |

| | |

| | 70 |

| | |

| | |

| | |

| | |

| | |

| Item 9C. | | 80 |

| | |

| | 81 |

| | 81 |

| | 81 |

| | 81 |

| | 81 |

| | |

| | 82 |

| Item 16. | | 86 |

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), that relate to future events or to our future operations or financial performance. These statements may be identified by such forward-looking terminology as “may,” “should,” “expects,” “intends,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “continue” or the negative of these terms or other comparable terminology. Our forward-looking statements are based on a series of expectations, assumptions, estimates and projections about our company, are not guarantees of future results or performance and involve substantial risks and uncertainty. We may not actually achieve the plans, intentions or expectations disclosed in these forward-looking statements. Actual results or events could differ materially from the plans, intentions and expectations disclosed in these forward-looking statements. These forward-looking statements are subject to a number of known and unknown risks, uncertainties and assumptions, including risks described in the section titled “Risk Factors” and elsewhere in this report, regarding, among other things:

•the timing of and our ability to obtain and maintain regulatory approval of our existing product candidates or any product candidates that we may develop in the future, and any related restrictions, limitations, or warnings in the label of any approved product candidates;

•the initiation, timing, progress and results of our current and future preclinical studies and clinical trials and related preparatory work and the period during which the results of the trials will become available, as well as our research and development programs;

•the potential benefits, including clinical utility, that may be derived from any of our product candidates;

•our plans to research, develop, manufacture and commercialize our product candidates;

•the timing of our regulatory filings for our product candidates, along with regulatory developments in the United States and other foreign countries;

•the size and growth potential of the markets for our product candidates, if approved, and the rate and degree of market acceptance of our product candidates, including reimbursement that may be received from payors;

•the benefits of U.S. Food and Drug Administration and European Commission designations, including, without limitation, Fast Track, orphan designation and Breakthrough Therapy;

•our commercialization, marketing and manufacturing capabilities and strategy;

•our ability to attract and retain qualified employees and key personnel;

•our competitive position and the development of and projections relating to our competitors or our industry;

•our expectations regarding our ability to obtain and maintain intellectual property protection;

•the success of competing therapies that are or may become available;

•our estimates and expectations regarding future operations, financial position, revenues, costs, expenses, uses of cash, capital requirements or our need for additional financing;

•our ability to continue as a going concern;

•our plans to in-license, acquire, develop and commercialize additional product candidates;

•the impact of laws and regulations;

•our plans to identify additional product candidates with significant commercial potential that are consistent with our commercial objectives;

•our ability to raise additional capital;

•our strategies, prospects, plans, expectations or objectives; and

•other risks and uncertainties, including those listed under the section titled “Risk Factors” in this Annual Report.

You should refer to the section titled “Risk Factors” in this Annual Report for a discussion of important factors that may cause our actual results to differ materially from those expressed or implied by our forward-looking statements. As a result of these factors, we cannot assure you that the forward-looking statements in this Annual Report will prove to be accurate. Furthermore, if our forward-looking statements prove to be inaccurate, the inaccuracy may be material. In light of the significant uncertainties in these forward-looking statements, you should not regard these statements as a representation or warranty by us or any other person that we will achieve our objectives and plans in any specified time frame, or at all. We undertake no obligation to publicly update any forward-looking statements, whether as a result of new information, future events or otherwise, except as required by law. You should, therefore, not rely on these forward-looking statements as representing our views as of any date subsequent to the date of this Annual Report.

Unless the context requires otherwise, references in this Annual Report to “X4”, “we”, “us” and “our” refer to X4 Pharmaceuticals, Inc. and its subsidiaries.

PART I

ITEM 1. BUSINESS

Overview

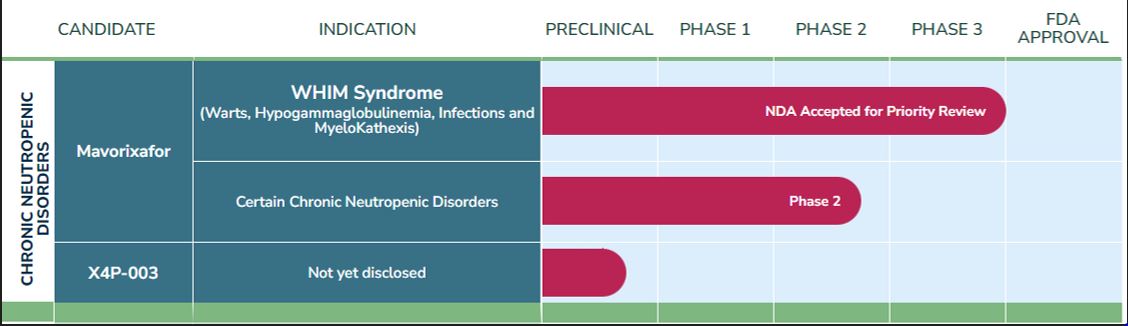

We are a late clinical-stage biopharmaceutical company discovering and developing novel therapeutics for the treatment of rare diseases and those with limited treatment options, with a focus on conditions resulting from dysfunction of the immune system.

Our lead clinical candidate is mavorixafor, a small-molecule selective antagonist of chemokine receptor CXCR4, that is being developed as an oral, once-daily therapy. Due to its ability to increase the mobilization of mature, functional white blood cells into the bloodstream, we believe that mavorixafor has the potential to provide therapeutic benefit across a variety of chronic neutropenic disorders, including WHIM (Warts, Hypogammaglobulinemia, Infections, and Myelokathexis) syndrome, a rare, primary immunodeficiency.

We are currently seeking approval from the U.S. Food and Drug Administration (“FDA”) for the use of oral, once-daily mavorixafor in the treatment of people aged 12 years and older with WHIM syndrome following the October 2023 acceptance of our New Drug Application (“NDA”) by the FDA. The FDA has granted the NDA Priority Review, establishing a goal of six months review from the date of acceptance and assigning a Prescription Drug User Fee Act (“PDUFA”) target action date of April 30, 2024. At this time, the FDA has notified us that they are not planning to hold an advisory committee meeting to review the filing. Due to mavorixafor’s Rare Pediatric Disease designation in the U.S. for WHIM syndrome, should mavorixafor be approved, we are eligible to receive a Priority Review Voucher (“PRV”), which may be used to obtain Priority Review for a subsequent application or sold to another drug sponsor.

The NDA is supported by our successfully completed global, pivotal, Phase 3 clinical trial (“4WHIM”) that evaluated the safety and efficacy of mavorixafor in 31 people with WHIM syndrome. The 4WHIM trial met its primary endpoint and a key secondary endpoint, demonstrating statistically significant increases in time above threshold for absolute neutrophil counts (“TAT-ANC”) in patients treated with mavorixafor and time above threshold for absolute lymphocyte counts (“TAT-ALC”) versus placebo. Additional data showed that mavorixafor treatment resulted in statistically significant reductions in annualized infection rates versus placebo and clinically meaningful reductions in both the severity and duration of infections versus placebo. Mavorixafor was generally well tolerated throughout the 52-week trial.

In anticipation of a potential second quarter 2024 U.S. launch of mavorixafor in WHIM syndrome, we have continued to build our go-to-market organization, with key hires across commercial and medical functions, increased interactions with key stakeholders and rare disease patient advocacy organizations, and launched a disease awareness campaign aiming to further the understanding of WHIM syndrome and educate patients and physicians on the importance and benefits of early diagnosis.

We are also advancing mavorixafor for the treatment of people with certain chronic neutropenic disorders following positive results from a Phase 1b clinical trial of a single dose of mavorixafor in people with idiopathic, cyclic, and congenital chronic neutropenia. We are conducting a Phase 2 clinical trial, evaluating the durability, safety, and tolerability of chronic dosing of once-daily oral mavorixafor with or without concurrent treatment with injectable granulocyte colony-stimulating factor (“G-CSF”) in the same patient population. Preliminary results from the trial showed that the first three participants experienced clinically meaningful increases in absolute neutrophil counts (“ANC”). We expect to share further data from the Phase 2 trial in the second quarter of 2024. Concurrent with conducting this Phase 2 trial, we are advancing our plans for a Phase 3 trial of mavorixafor in people with certain chronic neutropenic disorders. This Phase 3 trial will be a global, randomized, placebo-controlled trial assessing the safety and efficacy of mavorixafor, with or without concomitant G-CSF, in people with idiopathic or congenital neutropenia. We expect that this Phase 3 trial will initiate in the second quarter of 2024.

We believe that successfully developing mavorixafor and providing new therapeutic options to individuals in the United States diagnosed with certain chronic neutropenic disorders has the potential to revolutionize the treatment landscape, which is principally served by injectable therapies that are frequently associated with treatment-limiting adverse events.

Our Focus

We have developed a pipeline of small-molecule, oral antagonists of the chemokine receptor CXCR4, or C-X-C receptor type 4. CXCR4 is a cell receptor that helps regulate the movement of immune cells within the body. CXCR4 receptor stimulation by its cognate ligand, CXCL12, has been shown to play a key role in the maturation and mobilization of white blood cells such as neutrophils, lymphocytes (including both B cells and T cells), and monocytes, into the bloodstream. Because antagonism of the CXCR4 receptor has been shown to increase the trafficking of white blood cells, we believe that therapeutic inhibition of the

CXCR4/CXCL12 axis holds the potential to benefit people with a wide variety of diseases where there remain significant unmet needs, including chronic neutropenic disorders and certain types of cancer.

Chronic neutropenic disorders are rare blood conditions where people of all ages experience low levels of neutrophils and tend to be at greater risk of developing infections and certain types of cancer. Depending on the levels of circulating neutrophils in the blood, neutropenia can be categorized as mild, moderate, or severe.

We are currently focused on advancing our lead clinical candidate, mavorixafor, for the treatment of a number of chronic neutropenia indications, including WHIM syndrome, while also pursuing partnership opportunities to further advance our previous work in oncology indications.

Our Pipeline

Our deep understanding of the biology of the CXCR4 pathway has enabled us to discover and develop multiple small-molecule CXCR4 antagonists. To date, we have advanced our lead candidate, mavorixafor, into late-stage clinical development. Mavorixafor is an orally available, small-molecule CXCR4 antagonist designed to facilitate the mobilization of white blood cells from the bone marrow into the blood, to increase levels of circulating neutrophils, lymphocytes, and monocytes, and to improve immune system function.

To date, more than 350 subjects in clinical trials have been dosed with mavorixafor, with a favorable tolerability profile observed. In these trials, we have observed drug exposure levels, a 22-hour half-life, and bioavailability of mavorixafor to support once-daily oral dosing, which we believe would provide convenient dosing and facilitate patient compliance for chronic or life-long use, if approved. The manufacturing process for mavorixafor utilizes well established, small-molecule chemistry. The commercial product, if approved, can be supported by specialty pharmacy distribution.

We have successfully advanced mavorixafor through a pivotal, Phase 3 clinical trial, referred to as the 4WHIM trial, in people with WHIM (Warts, Hypogammaglobulinemia, Infections, and Myelokathexis) syndrome, a rare, combined primary immunodeficiency. We have also completed a Phase 1b clinical trial of a single dose of mavorixafor in people with congenital, idiopathic, or cyclic neutropenia and we are now conducting a Phase 2 clinical trial evaluating the durability, safety, and tolerability of chronic dosing of once-daily oral mavorixafor with or without concurrent treatment with injectable G-CSF in the same patient population.

We have two pre-clinical candidates: X4P-003, a second-generation CXCR4 antagonist designed to have enhanced properties relative to mavorixafor, potentially enabling broader opportunities in CXCR4-dependent disorders and primary immunodeficiencies; and X4P-002, a CXCR4 antagonist with a unique distribution profile and a demonstrated ability to cross the blood-brain barrier.

About WHIM Syndrome

WHIM syndrome is both a rare, combined immunodeficiency and a congenital neutropenic disorder in which the body’s immune system does not function properly and has trouble fighting infections. In many patients, WHIM is caused by “gain of function” variations in the single gene that encodes for the CXCR4 receptor. In healthy individuals, the CXCR4 receptor is typically internalized into the cell after CXCL12 binds to it, enabling the receptor to be appropriately “recycled” and the signaling to be diminished. In most WHIM patients, however, a genetic variation in the receptor gene prevents the post-binding internalization (“normal recycling”) of the receptor. As a result, the CXCR4 receptor is maintained on the surface of the cell and is exposed to the ligand, which creates a perpetual “on” signal and retention of white blood cells in the bone marrow where they are produced, leading to the chronic peripheral neutropenia, lymphopenia, and monocytopenia that are the clinical hallmarks of WHIM syndrome.

Genetic testing is typically used to diagnose WHIM syndrome to confirm the presence of a genetic variation in the CXCR4 receptor. The diagnosis of WHIM syndrome may occur at any age: about one-half of reported patients are diagnosed as children, primarily before of at the age of 18 years, with the other half diagnosed as adults, mostly between 18 and 40 years of age.

WHIM syndrome is named for its four common manifestations, although not all patients experience all symptoms, and not all symptoms are required for a diagnosis: Warts, related to infection with the Human Papilloma Virus (HPV), Hypogammaglobulinemia, a condition of low immunoglobulin (“IG”) levels, Infections, including both bacterial and fungal infections, and Myelokathexis, a hyper-dense population of immune cells in the bone marrow. These conditions reduce the body’s ability to achieve a healthy immune response. Left untreated, those with WHIM syndrome may experience debilitating and life-threatening complications, including an increased cancer risk, irreversible end-organ damage, and/or sepsis.

The incidence and prevalence of WHIM syndrome are not well established. We believe that this is due to the relatively recent elucidation of the genetics underlying WHIM syndrome, lack of universal or accessible genetic testing, and limited medical education and awareness of the disease, which is in part driven by the lack of available disease-modifying treatments. Based on a preliminary U.S. market research study sponsored by us and conducted by a third-party research firm, we believe that the prevalence of WHIM syndrome worldwide is significantly higher than previous registries suggest.

•The study solicited input from community-based physicians of different specialties, including physicians focused on non-malignant hematology, immunology, dermatology, pulmonology, and infectious diseases, who are known to manage and/or treat patients with WHIM syndrome.

•The 212 physicians across these specialties identified to participate in this study reported more than 1,700 patients in the United States with genetically confirmed or highly probable WHIM syndrome.

In addition, we have also completed a study using artificial intelligence, interrogating a database of approximately 300 million American lives that included up to 10 years of insurance claims on diagnoses, drug treatments, procedures, and treatment pathways. This study suggests that there may be as many as 3,700 WHIM patients in the United States based on the WHIM-like phenotypes described.

The first CXCR4 genetic variation determined to cause WHIM syndrome was identified in 2003. Since then, several CXCR4 variations have been identified as “gain of function” variations causing WHIM syndrome. Our research has subsequently identified a number of new genetic variations, among them a new missense variation, called D84H, that is relatively frequent in the general population. The D84H mutation is the first mutation to be identified outside of the C-terminus of the CXCR4 receptor showing gain-of-function signaling and WHIM disease phenotype. We believe that the frequency of the D84H variation, as derived from broad population genomic databases, further supports our current WHIM prevalence estimate. Our research into additional WHIM-causing genetic variations is ongoing and we are continuing to identify novel pathogenic variants, further expanding our understanding of the clinical phenotype of people with WHIM syndrome.

In partnership with Invitae, a genetic information company, we sponsor a no-charge genetic testing and counseling program called PATH4WARD for individuals who may carry a genetic variation known to be associated with chronic neutropenia or primary immunodeficiency disorders (“PIDs”), including WHIM syndrome. The genetic panel looks at more than 550 genes known to be associated with PIDs; to date, the program has proven helpful not only in diagnosing WHIM, but also providing a better understanding of novel genetic variants causing PIDs and assisting participant enrollment in X4-sponsored clinical trials.

We continue to increase awareness of WHIM syndrome among patients, physicians, and their support systems through our partnerships with key patient foundations, including the Jeffrey Modell Foundation, International Patient Organisation for Primary Immunodeficiencies, and Immune Deficiency Foundation.

We have also deployed of a field force of Medical Science Liaisons (“MSLs”) and Patient Diagnostic Liaisons (“PDLs”) in the United States to further drive education and awareness of WHIM syndrome and its diagnosis. Upon obtaining approval of our NDA by the FDA, we plan to deploy a field sales force who will provide information about our approved drug product to health care providers who are known to or potentially could have WHIM patients under their care.

Limited Current Treatment Landscape for WHIM Syndrome

Currently, there are no approved therapies for the treatment of WHIM syndrome and care is limited to the treatment of the syndrome’s different symptoms, mainly the prevention and management of infections. None of these symptomatic treatments, however, address the underlying cause of this multi-faceted disease. Current symptoms and their treatment limitations are as follows:

•Warts: The presence of warts in WHIM syndrome is driven by an underlying HPV infection. Standard treatments, such as topical therapies (for example, imiquimod and salicylic acid), cryotherapy and laser therapy, as well as more aggressive approaches, such as cauterization or surgical removal, have been ineffective in providing durable treatment of warts associated with chronic HPV infections. As WHIM patients generally have limited response to vaccines, the HPV vaccine appears to have limited effectiveness. The number, size, and severity of visible warts in WHIM patients can have a significant negative impact on the patient’s quality of life and result in social anxiety issues. Left untreated, chronic HPV-infections are also known to increase the risk of cancer.

•Hypogammaglobulinemia: Intravenous or subcutaneous IG administration, referred to as IVIG (“IVIG”) or SCIG (“SCIG”), respectively, can be administered to patients with low IG levels. In WHIM patients, the administration of IG therapies raises IG levels, but has shown no impact on circulating white blood cells and limited or no impact on immune responses. IG treatment of patients with WHIM syndrome is based on empirical and anecdotal evidence, and there are no clinical data demonstrating the efficacy of IG treatment for WHIM syndrome. IG treatment also does not treat or protect against HPV-associated symptoms and diseases, such as warts and certain cancers. Furthermore, IG administration is costly and time consuming.

•Infections: Bacterial infections are managed with antibiotics. Acute infections usually resolve, although we are aware of reports from clinicians citing death due to pneumonia or sepsis in young WHIM patients. Importantly, even with antibiotic use, infections are known to recur more frequently and persist longer in patients with WHIM syndrome. Further, the toll of multiple, chronic infections in WHIM patients has been known to lead to devastating irreversible pathologies such as hearing loss, due to chronic ear infections and bronchiectasis (damaged lung airways). Patients are sometimes given granulocyte-colony stimulating factor (“G-CSF”) to increase neutrophil counts, but G-CSF has demonstrated little, if any, impact on lymphopenia or the incidence of infections in WHIM patients. Side effects of G-CSF have been reported to include disabling bone pain, which can be more severe in certain age groups. Additional, less common, treatment-limiting complications of chronic G-CSF administration include myelofibrosis and leukemia.

•Myelokathexis: G-CSF is also sometimes used to treat the myelokathexis characteristic of WHIM syndrome to try to increase the number of neutrophils in the peripheral blood, but G-CSF has no effect on lymphocytes and other types of white blood cells.

While the costs of managing the chronic impact of WHIM syndrome are unknown, the per-patient cost of treating primary immunodeficiencies that are similar to WHIM syndrome, based on drug costs alone, exceeds $100,000 per year in the United States for therapies such as antibiotics, IVIG, SCIG and/or G-CSF, despite the limited effectiveness of these treatments. Beyond these estimated direct costs, other costs associated with direct and indirect management of the disease, such as repeated immunization, physician visits, or hospitalizations, have not been quantified but are likely to be significant. We believe that there is a significant need for a treatment targeting the underlying excessive signaling caused by genetic variations to the CXCR4 receptor, which is the established cause of WHIM syndrome.

Our approach to treating WHIM syndrome involves addressing the underlying cause of the disease by blocking CXCR4 signaling using mavorixafor, which has been shown to bind to the CXCR4 receptor in a manner that inhibits the receptor from being stimulated by CXCL12, enabling white blood cells to properly mature and release into the bloodstream and improving immune cell numbers and function.

Clinical Development of Mavorixafor in WHIM Syndrome

In January 2017, we initiated a Phase 2 clinical trial of mavorixafor for the treatment of people with WHIM syndrome. This trial was an open-label, dose-escalation trial in eight WHIM patients conducted at two sites in the United States and Australia pursuant to an Investigational New Drug (“IND”) application that we submitted to the U.S. Food and Drug Administration (“FDA”) in June 2016.

The primary objective of the Phase 2 clinical trial was to determine the safety and tolerability of mavorixafor and to determine the dose of mavorixafor for exploration in a pivotal Phase 3 clinical trial. The secondary objective of the Phase 2 trial was to evaluate the potential efficacy of mavorixafor in people with WHIM syndrome by measuring biomarkers, specifically absolute neutrophil (“ANC”) and lymphocyte (“ALC”) counts, over 24-hour dosing cycles. The frequency of infections, antibiotic use, hospitalizations, severity of warts lesions, and vaccine titer levels, among other metrics, were also examined. To be included in the trial, participants must have had a confirmed genetic diagnosis of WHIM syndrome, be at least 18 years of age, and have a neutrophil count equal to or less than 400 cells per microliter or a lymphocyte count equal to or less than 650 cells per microliter.

In the trial, participants received escalating doses of mavorixafor starting at 50 mg once daily to up to 400 mg once daily. Participants were dose-escalated from their starting dose based on an in-hospital 24-hour measurement of ANC and ALC above or below the pre-defined target thresholds of 600 cells per microliter and 1,000 cells per microliter, respectively.

We completed the dose-titration portion of the Phase 2 clinical trial in March 2018 and, based on the reported results, the Data Review Committee recommended the Phase 3 dose of 400 mg administered orally once daily. The choice of time above threshold for absolute neutrophil count (“TAT-ANC”), defined as the number of hours during which the absolute neutrophil count is raised above a 500 cells per microliter threshold, was selected as the primary endpoint of the Phase 3 clinical trial.

Following completion of the dose-titration portion of the Phase 2 clinical trial, participants were allowed to continue on study drug in a Phase 2 open-label extension trial. In June 2020, we announced the following positive data from the open-label extension portion of the Phase 2 clinical trial:

•Sustained, dose-dependent increases in white blood cells, ANC, and ALC were achieved; higher doses of mavorixafor were shown to increase the TAT-ANC at least 4.5-fold versus the TAT-ANC at lower doses.

•These long-term hematological improvements correlated with fewer infections and reduced numbers of cutaneous warts.

•A decreased yearly infection rate from 4.63 [95%CI 3.3,6.3] events in the 12 months prior to the trial, to 2.27 [95%CI 1.4, 3.5] events when treated with mavorixafor at higher doses once daily; notably, deeper reductions in yearly infection rates correlated with increased time on treatment.

•The participants with cutaneous warts on hands and/or feet at baseline achieved an average 75% reduction in the number of warts.

•Mavorixafor was well tolerated for the extended duration of up to more than two years without any attributable serious adverse effects.

In December 2021, we announced the following additional data from the Phase 2 open-label extension trial of mavorixafor in people with WHIM syndrome:

•Mavorixafor continued to show durable increases in neutrophils, lymphocytes, and monocytes, sustained improvements in infections and warts, and was well tolerated (median treatment duration = 148.4 weeks).

•Decreases in mean annualized infection rates correlated well with TAT-ANC.

•Standardized participant interviews revealed that long-term treatment with mavorixafor was well tolerated and continued to demonstrate beneficial treatment effects, including decreased frequency, severity, and duration of infections and fewer hospital/doctor visits.

In June 2019, we initiated 4WHIM, a pivotal, global, randomized, double-blind, placebo-controlled, multicenter Phase 3 clinical trial designed to evaluate the efficacy and safety of mavorixafor in people with genetically confirmed WHIM syndrome. Originally designed to enroll 18-28 patients, the trial achieved full enrollment in September 2021, with 31 participants aged 12 and older receiving either 200-400 mg mavorixafor or placebo orally once daily for 52 weeks; all participants then became eligible to receive treatment with mavorixafor in an open-label trial extension.

The primary endpoint of the 4WHIM trial was a clinically relevant reduction of duration of severe neutropenia as measured by the increase in TAT-ANC (500 cells per microliter) in peripheral blood. Secondary endpoints include time above threshold-absolute lymphocyte count (TAT-ALC) of ≥ 1,000 cells per microliter over a 24-hour period, a composite clinical efficacy endpoint for mavorixafor based on total infection score and total wart change score, total wart change score for mavorixafor based on central

blinded, independent review of 3 target skin regions, total infection score for mavorixafor based on number and severity of infections adjudicated by a blinded, independent adjudication committee; and a number of quality-of-life measurements and other exploratory endpoints.

In November 2022, we reported positive top-line results from the Phase 3 4WHIM trial:

•4WHIM met its primary endpoint, with mavorixafor achieving clinical and statistical superiority over placebo (P<0.0001) when measuring the length of time that participants’ ANC remained above a clinically meaningful threshold of 500 cells per microliter (severe neutropenia), over 24-hour periods at 4 time points throughout the 52-week trial.

•4WHIM also met a key secondary endpoint, with mavorixafor achieving clinical and statistical superiority over placebo (P<0.0001) when measuring the length of time that participants’ ALC remained above a clinically meaningful threshold of 1,000 cells per microliter (lymphopenia), over 24-hour periods at 4 time points throughout the 52-week trial.

•Mavorixafor was generally well tolerated in the trial, with no treatment-related serious adverse events reported and no discontinuations for safety events.

In the second quarter of 2023, we presented additional data and analysis of the secondary and exploratory endpoints of the 4WHIM trial. Additional data presented revealed that mavorixafor treatment also resulted in statistically significant reductions in annualized infection rates versus placebo and effected clinically meaningful reductions in the both the severity and duration of infections versus placebo in trial participants. More specifically, the additional data showed the following:

•Rate of Infections: In the trial, mavorixafor treatment resulted in a statistically significant reduction (~60%) in annualized infection rate versus placebo (p<0.01). In addition, the data showed that the reduction was greater with time on treatment, with participants on mavorixafor experiencing less than one infection per year versus 4.5 for those on placebo; during the second 6 months of the trial, the difference also achieved statistical significance (p<0.005).

•Severity of Infections: During the trial, 29% (5 of 17) of those on placebo experienced Grade 3 or higher infections, whereas only 7% (1 of 14) of those on mavorixafor experienced a Grade 3 or higher infection, equating to a 75% reduction in the number of individuals experiencing severe infections. Importantly, the single Grade 3 infection in the mavorixafor treatment arm occurred during the first 3 months of the trial; after 3 months of treatment, there were no serious infections in the mavorixafor-arm, whereas the frequency of severe infections in those on placebo remained unchanged over the 52-week trial period.

•Duration of Infections: In the trial, mavorixafor treatment reduced the total duration (in days) of infections by more than 70% as compared to placebo, with those on placebo experiencing a mean of 7 weeks (49.1 days) with infections over the 52-week trial period versus a mean of only 2 weeks (14.1 days) with infections for those treated with mavorixafor.

•Other Infection Metrics: Mavorixafor treatment resulted in a 40% lower total infection score, a metric that combines infection number and severity (LS mean [95% CI]: mavorixafor, 7.41 [1.64–13.19]; placebo, 12.27 [7.24–17.30]). Treatment with mavorixafor also resulted in reductions in upper and lower respiratory tract and skin infections compared with those on placebo; participants on placebo required greater medical intervention, with 10 of the 17 participants on placebo requiring treatment with antibiotics over the course of the study, versus 3 of the 14 receiving mavorixafor; and slight improvements in warts were demonstrated both in the mavorixafor and placebo arms (no difference between arms).

•Safety and Tolerability: As reported previously, mavorixafor was generally well tolerated in the 4WHIM trial, with no drug-related serious adverse events, no treatment limiting toxicities, and no discontinuations due to safety. Approximately 90% of participants in the trial continued on to receive mavorixafor treatment at the start of the ongoing open-label extension study.

In August 2023, we submitted to the FDA an NDA with the goal of obtaining approval for mavorixafor for the treatment of people in the United States, aged 12 and older, with WHIM syndrome. The FDA accepted the NDA in late October 2023 for priority review and established a PDUFA target action date of April 30, 2024.

Mavorixafor has received multiple special designations from global regulatory authorities in WHIM syndrome, including Breakthrough Therapy Designation, Fast Track Designation, and Rare Pediatric Designation in the United States, and orphan designation in both the United States and European Union. In addition, upon approval of an NDA, we are eligible to receive a Priority Review Voucher (“PRV”) as a result of mavorixafor’s Rare Pediatric Designation in the United States. If obtained, such PRV could potentially be sold to a third party.

About Chronic Neutropenic Disorders

Due to its demonstrated ability to durably elevate levels of circulating white blood cells across multiple clinical trials, we believe that mavorixafor may be useful in the treatment of people with a variety of chronic neutropenic disorders.

Chronic neutropenia is defined as periods lasting more than three months persistently or intermittently where there are abnormally low levels of neutrophils circulating in the blood, and may be idiopathic (of unknown origin), cyclic (episodes typically occurring every three weeks), or congenital (of genetic causation). Similar to WHIM syndrome, chronic neutropenia disorders are rare blood conditions similarly characterized by increased risks of infections and cancer due to abnormally low levels of neutrophils in the body. In all cases, the CXCL12/CXCR4 pathway is the key regulator of neutrophil release from the bone marrow.

The incidence and prevalence of chronic neutropenic disorders are not well established. In December 2022, we presented results from what we believe was the first study examining the prevalence of chronic neutropenia disorders (including idiopathic, cyclic, and congenital neutropenia) in the United States; we believe that determining the estimated projected prevalence of chronic neutropenic disorders is a key step to understanding the extent of existing unmet medical needs in this patient population.

•Using a retrospective analysis of a large U.S. claims database, the analysis included people with a diagnosis code for neutropenia during the calendar years 2018, 2019, and 2021 (the year 2020 was excluded from this analysis owing to anticipated reduced claims during the COVID-19 pandemic).

•People with a diagnostic, procedural, or product code for neutropenia resulting from secondary causes including chemotherapy, drug exposure, infection, solid organ transplantation, myelodysplastic syndrome, and end-stage renal disease within 24-month period prior to selection were excluded.

•A 13- to 24-month look back period prior to index date was used to confirm chronic status.

•The analysis used longitudinal prescription data and office-based claims data from an IQVIA claims database that included 93% of retail prescription claims, 77% of mail-in prescription claims, and had more than 1.5 billion office-based claims per year.

•This retrospective analysis projected that in 2021, up to 48,000 people in the United States were living with a diagnosis of chronic neutropenia, with the most common type of chronic neutropenic disorder being idiopathic (~40,000), followed by cyclic (~5,000), and congenital (~3,000), and with the majority of affected people being female adults. Our research into the estimated individuals in the U.S. diagnosed with chronic neutropenia confirms significant unmet medical needs exist despite the availability and use of G-CSF and, if our analysis is correct, this suggests a potential minimal addressable market for mavorixafor of approximately one third of this population, or approximately 15,000 individuals in the U.S., plus meaningful potential market expansion opportunities.

In 2022, we also completed an electronic medical records study to better understand the risk of serious or severe infection in people with chronic neutropenia in the United States, analyzing the medical records of 44 healthcare organizations treating approximately 66 million patients. The analysis examined patients who had experienced at least two Serious Infections Events (“SIEs”) following documentation of chronic neutropenia in each calendar year compared with those who did not have neutropenia. SIEs are defined as infections requiring hospitalization or intravenous antibiotics or that result in disability or death.

•The results of this analysis indicated that the incidence rate of SIEs per 100,000 person days was increased for all levels of chronic neutropenia: it was two times greater for patients with any chronic neutropenia (ANC less than 1,500 cells per microliter) and four times greater for patients with severe congenital neutropenia (ANC less than 500 cells per microliter).

•The risk of serious infection increased with the worsening of neutropenia.

•Approximately 25% of patients with chronic neutropenia had at least 2 SIEs in the latest calendar year examined, which was 2019.

People living with chronic neutropenia have few treatment options and may be treated with G-CSF, an injectable therapy approved in the United States for the treatment of severe, chronic neutropenia. G-CSF is used to stimulate the bone marrow to produce neutrophils. Side effects of G-CSF include disabling bone pain, which can be more severe in certain age groups. Additional, less common, treatment-limiting complications of chronic G-CSF administration include myelofibrosis and leukemia. In chronic neutropenia cases that are unresponsive to G-CSF, or if leukemia has developed, bone marrow transplants have been made with varying degrees of success. Bone marrow transplantation is often applied to severe neutropenia from bone marrow failure. Bone marrow transplants bring additional risks into the management of the disorders.

Clinical Development of Mavorixafor in Chronic Neutropenic Disorders

In 2022, we conducted a proof-of-concept Phase 1b open-label, multicenter study designed to assess the safety and tolerability of oral mavorixafor, with or without injectable G-CSF, in participants with chronic neutropenic disorders, including idiopathic, cyclic, and congenital neutropenia. Participants received a single dose of 400 mg oral mavorixafor to assess the magnitude of treatment response.

In September 2022, we announced positive results from the Phase 1b clinical trial:

•A total of 25 participants were enrolled in the study.

•100% of study participants responded to treatment with a single dose of 400 mg of mavorixafor, alone or dosed concurrently with G-CSF:

◦Participants achieved a mean ANC increase at peak of >3,000 cells per microliter.

◦Consistent responses were seen across all of the chronic neutropenic disorders studied – idiopathic, cyclic, and congenital neutropenia.

•All neutropenic participants (n=14) reached normalized ANC levels (>1,500 cells per microliter):

◦When assessed as a monotherapy in participants with severe chronic neutropenia who were not being treated with G-CSF (n=6), a single dose of mavorixafor led to normalized ANC levels in all participants within 2 hours, with a mean ANC increase at peak of ~2,500 cells per microliter.

◦When assessed in participants with moderate or severe neutropenia, despite being treated with G-CSF (n=8), 100% reached normalized ANC levels, suggesting the potential of mavorixafor to both normalize the neutrophil counts in patients with partial response to G-CSF and also to potentially enable the reduction or elimination of G-CSF dosing.

•When assessed in participants with chronic neutropenia with normalized ANC counts on chronic G-CSF (n=11), all participants experienced a consistent and sustained increase in ANC, suggesting mavorixafor’s potential to reduce or possibly eliminate G-CSF treatment in these patients.

•Mavorixafor was well tolerated in the study; all treatment-related adverse events were deemed to be low grade, consistent with previous clinical studies in WHIM syndrome, and no treatment-related serious adverse events were reported.

Following these positive results, an amendment to the Phase 1b clinical trial was initiated aiming to evaluate the use of daily oral mavorixafor with or without injectable G-CSF for up to 6 months in participants with chronic neutropenic disorders as a Phase 2 clinical trial. The ongoing Phase 2 trial is assessing the durability of ANC responses, the potential of mavorixafor to enable patients to taper down dosing with G-CSF, and to evaluate the tolerability of mavorixafor in combination with G-CSF in chronic use. The trial is now fully enrolled and we expect to report additional data in the second quarter of 2024.

Concurrent with this Phase 2 trial execution, we are advancing our plans to conduct a Phase 3 program of mavorixafor in people with certain chronic neutropenic disorders. The planned Phase 3 trial will be a global, randomized, double-blinded, placebo-controlled trial assessing the safety and efficacy of once-daily oral mavorixafor, with or without concomitant G-CSF, in people with idiopathic or congenital neutropenia. The 52-week trial is expected to enroll 150 participants aged 12 years and older with both an ANC less than 1,500 cells per microliter and 2 or more infections requiring intervention during the 12 months preceding the trial. The primary endpoint of the trial is a two-component endpoint that includes the annualized infection rate and ANC response in the mavorixafor-treated group versus the placebo group. Secondary endpoints are expected to include analysis of the severity and duration of infections, antibiotic use, fatigue, and quality of life parameters. The dosing of mavorixafor will be the same as in the 4WHIM Phase 3 clinical trial. The Company anticipates enrolling the first participants in this Phase 3 clinical trial in the second quarter of 2024.

Competition

The pharmaceutical and biotechnology industries are characterized by rapidly advancing technologies, intense competition, and a strong emphasis on proprietary products. We face potential competition from many different sources, including major pharmaceutical, specialty pharmaceutical and biotechnology companies, academic institutions, governmental agencies, and public and private research institutions. Any product candidates that we successfully develop and commercialize will compete with existing therapies and new therapies that may become available in the future.

Many of our competitors may have significantly greater financial resources and expertise in research and development, manufacturing, preclinical testing, conducting clinical trials, obtaining regulatory approvals, and marketing approved products than we do. Other firms also compete with us in recruiting and retaining qualified scientific and management personnel and establishing clinical trial sites and patient enrollment for clinical trials, as well as in acquiring technologies complementary to, or

necessary for, our programs. Mergers and acquisitions in the pharmaceutical, biotechnology, and diagnostic industries may result in even more resources being concentrated among a smaller number of our competitors. Smaller or early stage companies may also prove to be significant competitors to us, particularly through collaborative arrangements with large and established companies.

Our commercial opportunities could be reduced or eliminated if our competitors develop and commercialize therapeutics that are safer, more effective, have fewer or less severe side effects, are more convenient or are less expensive than any products that we may develop. Our competitors also may obtain marketing approvals for their products more rapidly than we may obtain approval for our products, which could result in our competitors establishing a strong market position before we are able to enter the market. In addition, our ability to compete may be affected because in some cases insurers or other third-party payors, including government programs, seek to encourage the use of generic products. This may have the effect of making branded products less attractive to buyers from a cost perspective.

We are aware of other companies that are developing injectable CXCR4 inhibitors. However, we are not aware of any companies with CXCR4 antagonist programs in development for the indications of WHIM syndrome or chronic neutropenia. With regard to chronic neutropenia, we are not aware of any companies who are developing an oral therapy to elevate neutrophils in the blood. Filgrastim injections (human G-CSF) and two biosimilars (Zarxio and Nivestym) are FDA approved to reduce the incidence and duration of after-effects of severe neutropenia (e.g. fever, infections, oropharyngeal ulcers) in symptomatic patients with severe neutropenia.

Manufacturing

We do not own or operate, and currently have no plans to establish, manufacturing facilities for the production of clinical or commercial quantities of mavorixafor or any of our other product candidates. We currently rely, and expect to continue to rely, on third parties for the manufacture of any of our product or product candidates.

We currently have a master services agreement, as amended from time to time, with Evotec A.G. (“Evotec”, previously known as Aptuit, Oxford), pursuant to which Evotec develops and manufactures the active pharmaceutical ingredient (“API”), mavorixafor. The term of the Evotec Agreement expires in February 2027 unless terminated by us and/or Evotec. Evotec is currently our sole supplier for mavorixafor drug substance. We are in the process of transitioning the Evotec Agreement to a commercial supply agreement to support our potential WHIM launch and subsequent commercial supply.

We also have a master services agreement in place with Catalent Inc. (“Catalent”), which is our sole manufacturer for the final capsule drug product formulation of mavorixafor. The term of the master services agreement with Catalent expires on September 10, 2024, and may be terminated by (1) us upon 30 days-notice to Catalent or (2) by either party following a material breach by the other party that remains uncured for 30 days. We are in the process of transitioning the master services agreement with Catalent to a commercial supply agreement to support our potential WHIM launch and subsequent commercial supply.

We obtain clinical, and potentially commercial, supplies from Evotec and Catalent pursuant to typical industry standard commercial and clinical supply agreements. We believe that both manufacturers have the capability and capacity to manufacture currently projected clinical trial supply and commercial volumes of mavorixafor.

Sales and Marketing

We are currently building a commercial infrastructure to support sales of mavorixafor should the FDA provide marketing approval for mavorixafor in the United States. We expect to manage sales, marketing and distribution through internal resources and third-party relationships. Upon obtaining approval of our NDA by the FDA, we plan to have a field sales force who will provide information about our approved drug product to health care providers who are known to or potentially could have WHIM patients under their care.

We have entered into agreements with a third-party logistics company (“3PL”) for the warehousing and distribution of our drug product. We have also entered into an agreement with a specialty pharmacy, who will purchase our labelled drug product and dispense such drug product to patients pursuant to prescriptions provided by health care providers. The specialty pharmacy will also serve as our point of contact for inbound health care provider and patient inquiries, prescription processing, insurance investigation and patient on-boarding.

We currently intend to file a marketing authorization application (“MAA”) with the European Medicines Agency (“EMA”) for the marketing of mavorixafor in the European Union. Prior to filing the MAA, we must complete a Pediatric Investigational Plan (“PIP”). We anticipate submitting an MAA with the EMA in the fourth quarter of 2024 or in early 2025.

License Agreement

License Agreement with Genzyme

In July 2014, we entered into a license agreement with Genzyme Corporation (“Genzyme”), a wholly owned subsidiary of Sanofi, pursuant to which we were granted an exclusive license to certain patent applications and other intellectual property owned or controlled by Genzyme related to the CXCR4 receptor to develop and commercialize products containing licensed compounds, including but not limited to, mavorixafor. Genzyme has retained the non-exclusive right to conduct preclinical research involving compounds in any field, including any fields licensed to us, but has not retained rights to conduct any clinical development or commercialization of those compounds identified in the agreement in any of the fields licensed to us. We are primarily responsible for the preparation, filing, prosecution and maintenance of all patent applications and patents covering the intellectual property licensed to us under the agreement at our sole expense.

We are obligated to use commercially reasonable efforts to develop and commercialize licensed products for use in the field in the United States and at least one other major market country. We have the right to grant sublicenses of the licensed rights that cover mavorixafor to third parties. If we wish to grant a sublicense to any licensed product other than mavorixafor, we are obligated to first offer the sublicense to Genzyme. If Genzyme expresses written interest for the sublicense, then we will negotiate exclusively with Genzyme for a certain stated period to obtain a license to such rights, after which Genzyme shall have no further rights with respect to such licensed product and we will be free to negotiate a sublicense with respect to such licensed product with any third party.