UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

☒ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE QUARTERLY PERIOD ENDED DECEMBER 31, 2019

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Commission File Number 000-54761

NOBLE VICI GROUP, INC.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware | 42-1772663 | |

| (State or Other Jurisdiction | (I.R.S. Employer | |

| of Incorporation or Organization) | Identification No.) |

1 Raffles Place, #33-02

One Raffles Place Tower One

Singapore 048616

+65 6491 7998

(Address of Principal Executive Offices and Issuer’s

Telephone Number, including Area Code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Stock, $0.0001 par value | NVGI | N/A |

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 229.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ | |

| Non-accelerated filer ☐ | Smaller reporting company ☒ | |

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of February 7, 2020, the issuer had outstanding 210,804,160 shares of common stock.

| 2 |

NOBLE VICI GROUP, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

AS OF DECEMBER 31, 2019 AND MARCH 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

| December 31, 2019 | March 31, 2019 | |||||||

| (Unaudited) | (Audited) | |||||||

| ASSETS | ||||||||

| Current assets: | ||||||||

| Cash and cash equivalents | $ | 682,382 | $ | 691,331 | ||||

| Accounts receivable | 1,208,689 | 6,145,460 | ||||||

| Purchase deposits | 4,834,731 | 2,600,732 | ||||||

| Amount due from a third party | 221,373 | 221,327 | ||||||

| Deposits, prepayment and other receivables | 223,137 | 361,884 | ||||||

| Tax recoverable | 48,330 | – | ||||||

| Inventories | 16,640 | 16,636 | ||||||

| Total current assets | 7,235,282 | 10,037,370 | ||||||

| Non-current assets: | ||||||||

| Intangible assets, net | 358,214 | 566,262 | ||||||

| Property, plant and equipment, net | 3,658,279 | 3,754,685 | ||||||

| Total non-current assets | 4,016,493 | 4,320,947 | ||||||

| TOTAL ASSETS | $ | 11,251,775 | $ | 14,358,317 | ||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current liabilities: | ||||||||

| Accounts payable | $ | 375,929 | $ | – | ||||

| Accrued liabilities and other payables | 1,806,747 | 964,001 | ||||||

| Commission liabilities | 1,210,431 | 1,617,855 | ||||||

| Deferred revenue | 2,928,582 | 8,979,352 | ||||||

| Amount due to a director | 17,784 | 91,483 | ||||||

| Amounts due to a related party | 280,317 | 280,317 | ||||||

| Tax payable | – | 84,672 | ||||||

| Current portion of obligations under finance leases | 252,490 | 246,957 | ||||||

| Total current liabilities | 6,872,280 | 12,264,637 | ||||||

| Long-term liabilities: | ||||||||

| Obligations under finance leases | 1,840,727 | 2,008,708 | ||||||

| TOTAL LIABILITIES | 8,713,007 | 14,273,345 | ||||||

| Commitments and contingencies | – | – | ||||||

| STOCKHOLDERS’ EQUITY | ||||||||

| Common stock, 3,000,000,000 authorized common shares of $0.0001 par value, 210,804,160 and 210,704,160 shares issued and outstanding as of December 31, 2019 and March 31, 2019, respectively | 21,080 | 21,070 | ||||||

| Additional paid up capital | 136,427,910 | 136,227,920 | ||||||

| Deferred compensation | – | (10,936,760 | ) | |||||

| Accumulated other comprehensive (loss) income | (136,423 | ) | 20,089 | |||||

| Accumulated losses | (133,609,887 | ) | (125,141,278 | ) | ||||

| Total NVGI stockholders’ equity | 2,702,680 | 191,041 | ||||||

| Non-controlling interest | (163,912 | ) | (106,069 | ) | ||||

| 2,538,768 | 84,972 | |||||||

| TOTAL LIABILITIES AND STOCKHOLDERS’ EQUITY | $ | 11,251,775 | $ | 14,358,317 | ||||

See accompanying notes to unaudited condensed consolidated financial statements.

| 3 |

NOBLE VICI GROUP, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

FOR THE THREE AND NINE MONTHS ENDED DECEMBER 31, 2019 AND 2018

(Currency expressed in United States Dollars (“US$”))

(UNAUDITED)

| Three months ended December 31, | Nine months ended December 31, | |||||||||||||||

| 2019 | 2018 | 2019 | 2018 | |||||||||||||

| REVENUE, NET | $ | 2,063,937 | $ | 1,207,151 | $ | 14,674,821 | $ | 2,170,648 | ||||||||

| Cost of revenue | (2,250,717 | ) | (1,396,126 | ) | (8,311,170 | ) | (1,813,928 | ) | ||||||||

| Gross (loss) profit | (186,780 | ) | (188,975 | ) | 6,363,651 | 356,720 | ||||||||||

| Operating expenses: | ||||||||||||||||

| Sales and marketing | 83,651 | 200,505 | 421,972 | 442,651 | ||||||||||||

| General and administrative | 1,116,808 | 916,444 | 3,372,306 | 2,033,487 | ||||||||||||

| Stock-based compensation | 200,000 | 41,081,998 | 11,136,760 | 41,081,998 | ||||||||||||

| Total operating expenses | 1,400,459 | 42,198,947 | 14,931,038 | 43,558,136 | ||||||||||||

| LOSS FROM OPERATIONS | (1,587,239 | ) | (42,387,922 | ) | (8,567,387 | ) | (43,201,416 | ) | ||||||||

| Other (expense) income: | ||||||||||||||||

| Interest expense | (22,545 | ) | (23,076 | ) | (67,110 | ) | (24,775 | ) | ||||||||

| Government subsidy income | 14,632 | – | 14,632 | 1,047 | ||||||||||||

| Management fee income | 11,024 | 34,957 | 43,897 | 34,957 | ||||||||||||

| Sundry income | 1,346 | 4,807 | 27,392 | 17,193 | ||||||||||||

| Total other income | 4,457 | 16,688 | 18,811 | 28,422 | ||||||||||||

| LOSS BEFORE INCOME TAXES | (1,582,782 | ) | (42,371,234 | ) | (8,548,576 | ) | (43,172,994 | ) | ||||||||

| Income tax credit (expense) | 29,779 | (174,110 | ) | 18,555 | (174,110 | ) | ||||||||||

| NET LOSS | $ | (1,553,003 | ) | $ | (42,545,344 | ) | $ | (8,530,021 | ) | $ | (43,347,104 | ) | ||||

| Less: Net loss attributable to non-controlling interest | (126,020 | ) | – | (61,412 | ) | – | ||||||||||

| Net loss attributable to NVGI | (1,426,983 | ) | (42,545,344 | ) | (8,468,609 | ) | (43,347,104 | ) | ||||||||

| NET LOSS | $ | (1,553,003 | ) | $ | (42,545,344 | ) | $ | (8,530,021 | ) | $ | (43,347,104 | ) | ||||

| Other comprehensive income: | ||||||||||||||||

| – Foreign currency translation gain (loss) | 4,957 | 58,894 | (156,512 | ) | 118,780 | |||||||||||

| COMPREHENSIVE LOSS | $ | (1,548,046 | ) | $ | (42,486,450 | ) | $ | (8,686,533 | ) | $ | (43,228,324 | ) | ||||

| Net loss per share: | ||||||||||||||||

| – Basic and diluted | $ | (0.01 | ) | $ | (0.30 | ) | $ | (0.04 | ) | $ | (0.30 | ) | ||||

| Weighted average common shares outstanding: | ||||||||||||||||

| – Basic and diluted | 210,773,725 | 142,818,378 | 210,727,433 | 146,217,422 | ||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

| 4 |

NOBLE VICI GROUP, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY (DEFICIT)

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019 AND 2018

(Currency expressed in United States Dollars (“US$”))

(UNAUDITED)

| Nine months ended December 31, 2019 | ||||||||||||||||||||||||||||||||||||

| Accumulated | ||||||||||||||||||||||||||||||||||||

| other | ||||||||||||||||||||||||||||||||||||

| Additional | comprehensive | Total | Non- | |||||||||||||||||||||||||||||||||

| Common stock | paid up | Deferred | income | Accumulated | stockholders’ | controlling | Total | |||||||||||||||||||||||||||||

| No. of shares | Amount | capital | compensation | (loss) | losses | equity | interest | equity | ||||||||||||||||||||||||||||

| Balance as of April 1, 2019 | 210,704,160 | $ | 21,070 | $ | 136,227,920 | $ | (10,936,760 | ) | $ | 20,089 | $ | (125,141,278 | ) | $ | 191,041 | $ | (106,069 | ) | $ | 84,972 | ||||||||||||||||

| Shares issued for legal service | 100,000 | 10 | 199,990 | – | – | – | 200,000 | – | 200,000 | |||||||||||||||||||||||||||

| Non-controlling interest | – | – | – | – | – | – | – | 3,569 | 3,569 | |||||||||||||||||||||||||||

| Amortization of stock-based compensation | – | – | – | 10,936,760 | – | – | 10,936,760 | – | 10,936,760 | |||||||||||||||||||||||||||

| Foreign currency translation adjustment | – | – | – | – | (156,512 | ) | – | (156,512 | ) | – | (156,512 | ) | ||||||||||||||||||||||||

| Net loss for the period | – | – | – | – | – | (8,468,609 | ) | (8,468,609 | ) | (61,412 | ) | (8,530,021 | ) | |||||||||||||||||||||||

| Balance as of December 31, 2019 | 210,804,160 | $ | 21,080 | $ | 136,427,910 | $ | – | $ | (136,423 | ) | $ | (133,609,887 | ) | $ | 2,702,680 | $ | (163,912 | ) | $ | 2,538,768 | ||||||||||||||||

| 5 |

NOBLE VICI GROUP, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY (DEFICIT)

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019 AND 2018

(Currency expressed in United States Dollars (“US$”))

(continued)

(UNAUDITED)

| Nine months ended December 31, 2018 | ||||||||||||||||||||||||||||||||

| Accumulated | |||||||||||||||||||||||||||||||

| other | ||||||||||||||||||||||||||||||||

| Additional | comprehensive | Total | Non- | |||||||||||||||||||||||||||||

| Common stock | paid up | (loss) | Accumulated | stockholders’ | controlling | Total | ||||||||||||||||||||||||||

| No. of shares | Amount | capital | income | losses | deficit | interest | deficit | |||||||||||||||||||||||||

| Balance as of April 1, 2018 | 140,000,000 | $ | 14,000 | $ | – | $ | (46,440 | ) | $ | (1,131,214 | ) | $ | (1,163,654 | ) | $ | – | $ | (1,163,654 | ) | |||||||||||||

| Shares issued for acquisition of legal acquirer | 2,663,135 | 266 | – | – | (319,234 | ) | (318,968 | ) | – | (318,968 | ) | |||||||||||||||||||||

| Fractional shares from reverse splits | 26 | – | – | – | – | – | – | – | ||||||||||||||||||||||||

| Capital injection from shareholder | – | – | 152,726 | – | – | 152,726 | – | 152,726 | ||||||||||||||||||||||||

| Share issued for acquisition of subsidiaries | 1,020,000 | 102 | 2,039,898 | – | – | 2,040,000 | – | 2,040,000 | ||||||||||||||||||||||||

| Shares issued to sales agents for services | 20,540,999 | 2,054 | 41,079,944 | – | – | 41,081,998 | – | 41,081,998 | ||||||||||||||||||||||||

| Non-controlling interest from acquisition | – | – | – | – | – | – | (50,612 | ) | (50,612 | ) | ||||||||||||||||||||||

| Foreign currency translation adjustment | – | – | – | 118,780 | – | 118,780 | – | 118,780 | ||||||||||||||||||||||||

| Net loss for the period | – | – | – | – | (43,347,104 | ) | (43,347,104 | ) | – | (43,347,104 | ) | |||||||||||||||||||||

| Balance as of December 31, 2018 | 164,224,160 | $ | 16,422 | $ | 43,272,568 | $ | 72,340 | $ | (44,797,552 | ) | $ | (1,436,222 | ) | $ | (50,612 | ) | $ | (1,486,834 | ) | |||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

| 6 |

NOBLE VICI GROUP, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY (DEFICIT)

FOR THREE MONTHS ENDED DECEMBER 31, 2019 AND 2018

(Currency expressed in United States Dollars (“US$”))

(UNAUDITED)

| Three months ended December 31, 2019 | ||||||||||||||||||||||||||||||||

| Accumulated | ||||||||||||||||||||||||||||||||

| Additional | other | Total | Non- | |||||||||||||||||||||||||||||

| Common stock | paid up | comprehensive | Accumulated | stockholders’ | controlling | Total | ||||||||||||||||||||||||||

| No. of shares | Amount | capital | loss | losses | equity | interest | equity | |||||||||||||||||||||||||

| Balance as of October 1, 2019 | 210,704,160 | $ | 21,070 | $ | 136,227,920 | $ | (141,380 | ) | $ | (132,182,904 | ) | $ | 3,924,706 | $ | (37,892 | ) | $ | 3,886,814 | ||||||||||||||

| Shares issued for legal service | 100,000 | 10 | 199,990 | – | – | 200,000 | – | 200,000 | ||||||||||||||||||||||||

| Foreign currency translation adjustment | – | – | – | 4,957 | – | 4,957 | – | 4,957 | ||||||||||||||||||||||||

| Net loss for the period | – | – | – | – | (1,426,983 | ) | (1,426,983 | ) | (126,020 | ) | (1,553,003 | ) | ||||||||||||||||||||

| Balance as of December 31, 2019 | 210,804,160 | $ | 21,080 | $ | 136,427,910 | $ | (136,423 | ) | $ | (133,609,887 | ) | $ | 2,702,680 | $ | (163,912 | ) | $ | 2,538,768 | ||||||||||||||

| Three months ended December 31, 2018 | ||||||||||||||||||||||||||||||||

| Accumulated | ||||||||||||||||||||||||||||||||

| Additional | other | Total | Non- | |||||||||||||||||||||||||||||

| Common stock | paid up | comprehensive | Accumulated | stockholders’ | controlling | Total | ||||||||||||||||||||||||||

| No. of shares | Amount | capital | income | losses | deficit | interest | deficit | |||||||||||||||||||||||||

| Balance as of October 1, 2018 (restated) | 143,683,161 | $ | 14,368 | $ | 2,192,624 | $ | 13,446 | $ | (2,252,208 | ) | $ | (31,770 | ) | $ | 10,872 | $ | (20,898 | ) | ||||||||||||||

| Shares issued to sales agents for services | 20,540,999 | 2,054 | 41,079,944 | – | – | 41,081,998 | – | 41,081,998 | ||||||||||||||||||||||||

| Non-controlling interest from acquisition | – | – | – | – | – | – | (61,484 | ) | (61,484 | ) | ||||||||||||||||||||||

| Foreign currency translation adjustment | – | – | – | 58,894 | – | 58,894 | – | 58,894 | ||||||||||||||||||||||||

| Net loss for the period | – | – | – | – | (42,545,344 | ) | (42,545,344 | ) | – | (42,545,344 | ) | |||||||||||||||||||||

| Balance as of December 31, 2018 | 164,224,160 | $ | 16,422 | $ | 43,272,568 | $ | 72,340 | $ | (44,797,552 | ) | $ | (1,436,222 | ) | $ | (50,612 | ) | $ | (1,486,834 | ) | |||||||||||||

See accompanying notes to unaudited condensed consolidated financial statements.

| 7 |

NOBLE VICI GROUP, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019 AND 2018

(Currency expressed in United States Dollars (“US$”))

(UNAUDITED)

| Nine months ended December 31, | ||||||||

| 2019 | 2018 | |||||||

| Cash flow from operating activities: | ||||||||

| Net loss | $ | (8,530,021 | ) | $ | (43,347,104 | ) | ||

| Adjustments for: | ||||||||

| Amortization of intangible assets | 206,390 | 44,279 | ||||||

| Depreciation of property, plant and equipment | 147,031 | 183,289 | ||||||

| Stock based compensation | 11,136,760 | 41,081,998 | ||||||

| Gain on disposal of property, plant and equipment | (3,604 | ) | – | |||||

| Change in operating assets and liabilities: | ||||||||

| Accounts receivable | 4,895,929 | – | ||||||

| Deposits, prepayment and other receivables | 137,637 | (3,385,254 | ) | |||||

| Amounts due from related companies | – | (316,409 | ) | |||||

| Accounts payable | 372,722 | (382,356 | ) | |||||

| Accrued liabilities and other payables | 835,358 | 856,593 | ||||||

| Commission liabilities | (404,283 | ) | 1,489,999 | |||||

| Deferred revenue | (6,001,010 | ) | 4,038,460 | |||||

| Purchase deposits | (2,214,407 | ) | – | |||||

| Tax payable | (131,886 | ) | (254,100 | ) | ||||

| Net cash generated from operating activities | 446,616 | 9,395 | ||||||

| Cash flow from investing activities: | ||||||||

| Proceeds from disposal of property, plant and equipment | 52,676 | – | ||||||

| Purchase of property, plant and equipment | (99,741 | ) | (3,487,021 | ) | ||||

| Purchase of intangible assets | – | (183,986 | ) | |||||

| Cash from acquisition of subsidiaries | – | 37,576 | ||||||

| Net cash used in investing activities | (47,065 | ) | (3,633,431 | ) | ||||

| Cash flow from financing activities: | ||||||||

| Capital injection | – | 160,362 | ||||||

| (Repayment to) proceeds from a director | (73,089 | ) | 21,292 | |||||

| Proceeds from finance lease | – | 2,349,421 | ||||||

| Repayment of finance lease | (161,528 | ) | (130,912 | ) | ||||

| Net cash (used in) generated from financing activities | (234,617 | ) | 2,400,163 | |||||

| Foreign currency translation adjustment | (173,883 | ) | (95,821 | ) | ||||

| Net change in cash and cash equivalents | (8,949 | ) | (1,319,694 | ) | ||||

| BEGINNING OF PERIOD | 691,331 | 1,536,980 | ||||||

| END OF PERIOD | $ | 682,382 | $ | 217,286 | ||||

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION | ||||||||

| Cash paid for taxes | $ | 126,312 | $ | – | ||||

| Cash paid for interest | $ | 67,110 | $ | 33,665 | ||||

See accompanying notes to unaudited condensed consolidated financial statements.

| 8 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

NOTE —1 BASIS OF PRESENTATION

The accompanying unaudited condensed consolidated financial statements have been prepared by management in accordance with both accounting principles generally accepted in the United States (“GAAP”), and the instructions to Form 10-Q and Rule 10-01 of Regulation S-X. Certain information and note disclosures normally included in audited financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted pursuant to those rules and regulations, although the Company believes that the disclosures made are adequate to make the information not misleading.

In the opinion of management, the consolidated balance sheet as of March 31, 2019 which has been derived from audited financial statements and these unaudited condensed consolidated financial statements reflect all normal and recurring adjustments considered necessary to state fairly the results for the periods presented. The results for the period ended December 31, 2019 are not necessarily indicative of the results to be expected for the entire fiscal year ending March 31, 2020 or for any future period.

These unaudited condensed consolidated financial statements and notes thereto should be read in conjunction with the Management’s Discussion and the audited financial statements and notes thereto included in the Annual Report on Form 10-K for the year ended March 31, 2019.

NOTE—2 DESCRIPTION OF BUSINESS AND ORGANIZATION

Noble Vici Group, Inc. (the “Company”), formerly known as Gold Union Inc., was incorporated under the laws of the State of Delaware on July 6, 2010 under the name of Advanced Ventures Corp. Effective January 6, 2014, the Company changes its name to “Gold Union Inc.” Effective March 26, 2019, the Company changes its current name to Noble Vici Group, Inc (“NVGI”).

The Company is currently engaged in the IoT, Big Data, Blockchain and E-commerce business.

| 9 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

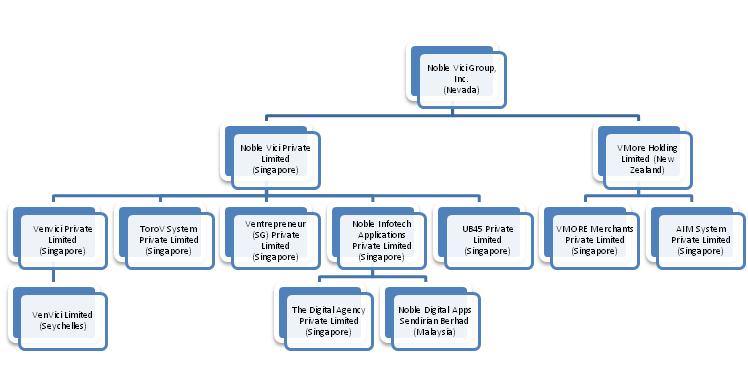

Description of subsidiaries

| Name |

Place of incorporation and kind of legal entity |

Principal activities and place of operation |

Particulars of issued/ registered share capital |

Effective interest held | ||||

| Noble Vici Pte Ltd | Republic of Singapore | Holding company | S$200,001 | 100% | ||||

| Noble Infotech Applications Pte Ltd | Republic of Singapore | Development of software for interactive digital media and software consultancy | S$ 1 | 100% | ||||

| Noble Digital Apps Sendirian Berhad | Federation of Malaysia | Digital apps and big data business | MYR1,000 | 51% | ||||

| The Digital Agency Pte. Ltd. | Republic of Singapore | Business and management consultancy services | $1 | 51% | ||||

|

Venvici Pte Ltd

|

Republic of Singapore | Business and management consultancy services on e-commerce service | S$100,000 | 100% | ||||

|

Venvici Ltd

|

Republic of Seychelles | Business and management consultancy services on e-commerce service | US$50,000 | 100% | ||||

| Ventrepreneur (SG) Pte Ltd | Republic of Singapore | Online retailing | S$10,000 | 100% | ||||

| UB45 Pte Limited | Republic of Singapore | Investment holding | S$10,000 | 100% | ||||

| ToroV System Private Limited | Republic of Singapore | IoT Retailing | S$10,000 | 51% | ||||

| VMore Holding Limited | New Zealand | New Zealand holding company | NZ$10,000 | 100% | ||||

| VMore Merchants Pte Ltd | Republic of Singapore | Merchants onboarding | S$1,000 | 100% | ||||

| AIM System Pte Ltd | Republic of Singapore | Affiliate System Provider | S$1,000 | 100% |

The Company and its subsidiaries are hereinafter referred to as (the “Company”).

| 10 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

NOTE—3 SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

The accompanying condensed consolidated financial statements reflect the application of certain significant accounting policies as described in this note and elsewhere in the accompanying condensed consolidated financial statements and notes.

| ☐ | Basis of presentation |

These accompanying condensed consolidated financial statements have been prepared in accordance with generally accepted accounting principles in the United States of America (“US GAAP”).

| ☐ | Basis of consolidation |

The condensed consolidated financial statements include the accounts of the Company and its subsidiaries. All significant inter-company balances and transactions within the Company have been eliminated upon consolidation.

| ☐ | Use of estimates and assumptions |

In preparing these condensed consolidated financial statements, management makes estimates and assumptions that affect the reported amounts of assets and liabilities in the balance sheet and revenues and expenses during the periods reported. Actual results may differ from these estimates. Significant estimates in the nine months ended December 31, 2019 and 2018 include the useful life of property and equipment and intangible assets, assumptions used in assessing impairment of goodwill and the value of stock-based compensation.

| ☐ | Cash and cash equivalents |

Cash and cash equivalents are carried at cost and represent cash on hand, demand deposits placed with banks or other financial institutions and all highly liquid investments with an original maturity of three months or less as of the purchase date of such investments.

| ☐ | Accounts receivable |

Accounts receivable consist of amounts due from customers in connection with our normal business activities and are carried at sales value less allowance for doubtful accounts. The allowance for doubtful accounts is established to reflect the expected losses of accounts receivable based on past collection history, age, account payment status compared to invoice payment terms and specific individual risks identified. The delinquency of a receivable account is determined based on these factors. The Company does not accrue interest on aged accounts receivable. As of December 31, 2019, there were no allowances for doubtful accounts.

| ☐ | Intangible assets |

Intangible assets represented the acquired game right from a related party, which are stated at acquisition cost, less accumulated amortization. The Company amortizes its intangible assets with definite lives over their estimated useful lives and reviews these assets for impairment when an indicator for potential impairment exists. The Company is currently amortizing its intangible assets with definite lives over periods of 3 years.

| 11 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

| ☐ | Property, plant and equipment |

Property, plant and equipment are stated at cost less accumulated depreciation and accumulated impairment losses, if any. Depreciation is calculated on the straight-line basis over the following expected useful lives from the date on which they become fully operational and after taking into account their estimated residual values:

| Expected useful lives | |||

| Building | 38 years or lesser than term of lease | ||

| Leasehold improvements | 3-10 years or lesser than term of lease | ||

| Furniture and fittings | 3 years | ||

| Office equipment and computers | 1- 3 years | ||

| Motor vehicle | 2 years |

Expenditures for repairs and maintenance are expensed as incurred. When assets have been retired or sold, the cost and related accumulated depreciation are removed from the accounts and any resulting gain or loss is recognized in the results of operations.

Depreciation expense for the three months ended December 31, 2019 and 2018 were $49,011 and $120,356, as part of operating expenses, respectively.

Depreciation expense for the nine months ended December 31, 2019 and 2018 were $147,031 and $183,289, as part of operating expenses, respectively.

| ☐ | Impairment of long-lived assets |

In accordance with Accounting Standards Codification ("ASC") Topic 360-10-5, “ Impairment or Disposal of Long-Lived Assets ”, the Company reviews its long-lived assets, including property, plant and equipment, as well as intangible assets for impairment whenever events or changes in circumstances indicate that the carrying amount of the assets may not be fully recoverable or that useful lives are no longer appropriate. If the total of the expected undiscounted future net cash flows is less than the carrying amount of the asset, a loss is recognized for the difference between the fair value and carrying amount of the asset. There has been no impairment charge as of December 31, 2019.

| ☐ | Revenue recognition |

Revenue is recognized when it is realized or realizable and earned, in accordance with ASC 605 Revenue Recognition (“ASC 605”). Revenue from the sale of products is recognised when all of the following criteria are met: (1) persuasive evidence of an arrangement exists; (2) delivery has occurred or services have been performed; (3) the seller’s price to the buyer is fixed or determinable; and (4) collectability is reasonably assured. Product sales are recorded net of good and service taxes and product returns.

The Company records revenues from the sales of third-party products on a “gross” basis pursuant to ASC 605-45 Revenue Recognition - Principal Agent Considerations, when we are the primary obligor in the arrangement with the end customer and have the risks and rewards as principal in the transaction, such as responsibility for fulfillment, retaining the risk for collection, and establishing the price of the products. If these indicators have not been met, or if indicators of net revenue reporting specified in ASC 605-45 are present in the arrangement, revenue is recognized net of related direct costs.

| 12 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

| ☐ | Commission credits |

The Company maintains a membership program, whereby certain members earn commission credits, based on the sales volume of certain other members who are sponsored directly or indirectly by the member. Commission credits are redeemable on future spending of the products purchased or playing online games. Commission credits are recorded and classified as operating expense when the products are delivered and revenue is recognized. The estimated liability for unredeemed commission credit is included in commission liability on the accompanying balance sheets. Management reviews the adequacy for the accrual for unredeemed commission credits by periodically evaluating the historical redemption and projected trends.

| ☐ | Income taxes |

The Company adopted the ASC 740 Income tax provisions of paragraph 740-10-25-13, which addresses the determination of whether tax benefits claimed or expected to be claimed on a tax return should be recorded in the consolidated financial statements. Under paragraph 740-10-25-13, the Company may recognize the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the taxing authorities, based on the technical merits of the position. The tax benefits recognized in the consolidated financial statements from such a position should be measured based on the largest benefit that has a greater than fifty percent (50%) likelihood of being realized upon ultimate settlement. Paragraph 740-10-25-13 also provides guidance on de-recognition, classification, interest and penalties on income taxes, accounting in interim periods and requires increased disclosures. The Company had no material adjustments to its liabilities for unrecognized income tax benefits according to the provisions of paragraph 740-10-25-13.

The estimated future tax effects of temporary differences between the tax basis of assets and liabilities are reported in the accompanying balance sheets, as well as tax credit carry-backs and carry-forwards. The Company periodically reviews the recoverability of deferred tax assets recorded on its balance sheets and provides valuation allowances as management deems necessary.

| ☐ | Uncertain tax positions |

The Company did not take any uncertain tax positions and had no adjustments to its income tax liabilities or benefits pursuant to the ASC 740 provisions of Section 740-10-25 for the three and nine months ended December 31, 2019 and 2018.

| ☐ | Finance leases |

Leases that transfer substantially all the rewards and risks of ownership to the lessee, other than legal title, are accounted for as finance leases. Substantially all of the risks or benefits of ownership are deemed to have been transferred if any one of the four criteria is met: (i) transfer of ownership to the lessee at the end of the lease term, (ii) the lease containing a bargain purchase option, (iii) the lease term exceeding 75% of the estimated economic life of the leased asset, (iv) the present value of the minimum lease payments exceeding 90% of the fair value. At the inception of a finance lease, the Company as the lessee records an asset and an obligation at an amount equal to the present value of the minimum lease payments. The leased asset is amortized over the shorter of the lease term or its estimated useful life if title does not transfer to the Company, while the leased asset is depreciated in accordance with the Company’s depreciation policy if the title is to eventually transfer to the Company. The periodic rent payments made during the lease term are allocated between a reduction in the obligation and interest element using the effective interest method in accordance with the provisions of ASC Topic 835-30, “Imputation of Interest”.

| ☐ | Foreign currencies translation |

Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchange rates prevailing at the dates of the transaction. Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency using the applicable exchange rates at the balance sheet dates. The resulting exchange differences are recorded in the consolidated statement of operations.

| 13 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

The reporting currency of the Company is United States Dollar ("US$") and the accompanying consolidated financial statements have been expressed in US$. In addition, the Company’s operating subsidiaries in Singapore and Seychelles maintain their books and record in its local currency, Singapore Dollars (“S$”), which is a functional currency as being the primary currency of the economic environment in which their operations are conducted. In general, for consolidation purposes, assets and liabilities of its subsidiaries whose functional currency is not US$ are translated into US$, in accordance with ASC Topic 830-30, “ Translation of Financial Statement”, using the exchange rate on the balance sheet date. Revenues and expenses are translated at average rates prevailing during the year. The gains and losses resulting from translation of financial statements of foreign subsidiaries are recorded as a separate component of accumulated other comprehensive income within the statements of changes in stockholder’s equity.

Translation of amounts from S$ into US$1 has been made at the following exchange rates for the period ended December 31, 2019 and 2018:

| December 31, 2019 | December 31, 2018 | |||||||

| Period-end S$:US$1 exchange rate | 1.3552 | 1.3632 | ||||||

| Period average S$:US$1 exchange rate | 1.3668 | 1.3588 | ||||||

| ☐ | Comprehensive income |

ASC Topic 220, “Comprehensive Income”, establishes standards for reporting and display of comprehensive income, its components and accumulated balances. Comprehensive income as defined includes all changes in equity during a period from non-owner sources. Accumulated other comprehensive income, as presented in the accompanying consolidated statements of changes in stockholders’ equity, consists of changes in unrealized gains and losses on foreign currency translation. This comprehensive income is not included in the computation of income tax expense or benefit.

| ☐ | Segment reporting |

ASC Topic 280, “Segment Reporting” establishes standards for reporting information about operating segments on a basis consistent with the Company’s internal organization structure as well as information about geographical areas, business segments and major customers in consolidated financial statements. For the three and nine months ended December 31, 2019 and 2018, the Company operates in one reportable operating segment in Singapore and Asian Region.

| ☐ | Related parties |

The Company follows the ASC 850-10, Related Party for the identification of related parties and disclosure of related party transactions.

Pursuant to section 850-10-20 the related parties include a) affiliates of the Company; b) entities for which investments in their equity securities would be required, absent the election of the fair value option under the Fair Value Option Subsection of section 825–10–15, to be accounted for by the equity method by the investing entity; c) trusts for the benefit of employees, such as pension and Income-sharing trusts that are managed by or under the trusteeship of management; d) principal owners of the Company; e) management of the Company; f) other parties with which the Company may deal if one party controls or can significantly influence the management or operating policies of the other to an extent that one of the transacting parties might be prevented from fully pursuing its own separate interests; and g) other parties that can significantly influence the management or operating policies of the transacting parties or that have an ownership interest in one of the transacting parties and can significantly influence the other to an extent that one or more of the transacting parties might be prevented from fully pursuing its own separate interests.

| 14 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

The consolidated financial statements shall include disclosures of material related party transactions, other than compensation arrangements, expense allowances, and other similar items in the ordinary course of business. However, disclosure of transactions that are eliminated in the preparation of consolidated or combined financial statements is not required in those statements. The disclosures shall include: a) the nature of the relationship(s) involved; b) a description of the transactions, including transactions to which no amounts or nominal amounts were ascribed, for each of the periods for which income statements are presented, and such other information deemed necessary to an understanding of the effects of the transactions on the consolidated financial statements; c) the dollar amounts of transactions for each of the periods for which income statements are presented and the effects of any change in the method of establishing the terms from that used in the preceding period; and d) amount due from or to related parties as of the date of each balance sheet presented and, if not otherwise apparent, the terms and manner of settlement.

| ☐ | Commitments and contingencies |

The Company follows the ASC 450-20, Commitments to report accounting for contingencies. Certain conditions may exist as of the date the financial statements are issued, which may result in a loss to the Company but which will only be resolved when one or more future events occur or fail to occur. The Company assesses such contingent liabilities, and such assessment inherently involves an exercise of judgment. In assessing loss contingencies related to legal proceedings that are pending against the Company or un-asserted claims that may result in such proceedings, the Company evaluates the perceived merits of any legal proceedings or un-asserted claims as well as the perceived merits of the amount of relief sought or expected to be sought therein.

If the assessment of a contingency indicates that it is probable that a material loss has been incurred and the amount of the liability can be estimated, then the estimated liability would be accrued in the Company’s financial statements. If the assessment indicates that a potentially material loss contingency is not probable but is reasonably possible, or is probable but cannot be estimated, then the nature of the contingent liability, and an estimate of the range of possible losses, if determinable and material, would be disclosed.

Loss contingencies considered remote are generally not disclosed unless they involve guarantees, in which case the guarantees would be disclosed. Management does not believe, based upon information available at this time that these matters will have a material adverse effect on the Company’s financial position, results of operations or cash flows. However, there is no assurance that such matters will not materially and adversely affect the Company’s business, financial position, and results of operations or cash flows.

| ☐ | Fair value of financial instruments |

The Company follows paragraph 825-10-50-10 of the FASB ASC for disclosures about fair value of its financial instruments and has adopted paragraph 820-10-35-37 of the FASB ASC (“Paragraph 820-10-35-37”) to measure the fair value of its financial instruments. Paragraph 820-10-35-37 of the FASB ASC establishes a framework for measuring fair value in generally accepted accounting principles (GAAP), and expands disclosures about fair value measurements. To increase consistency and comparability in fair value measurements and related disclosures, paragraph 820-10-35-37 of the FASB ASC establishes a fair value hierarchy which prioritizes the inputs to valuation techniques used to measure fair value into three (3) broad levels. The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities and the lowest priority to unobservable inputs. The three (3) levels of fair value hierarchy defined by paragraph 820-10-35-37 of the FASB ASC are described below:

| Level 1 | Quoted market prices available in active markets for identical assets or liabilities as of the reporting date. | |

| Level 2 | Pricing inputs other than quoted prices in active markets included in Level 1, which are either directly or indirectly observable as of the reporting date. | |

| Level 3 | Pricing inputs that are generally observable inputs and not corroborated by market data. |

| 15 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

Financial assets are considered Level 3 when their fair values are determined using pricing models, discounted cash flow methodologies or similar techniques and at least one significant model assumption or input is unobservable.

The fair value hierarchy gives the highest priority to quoted prices (unadjusted) in active markets for identical assets or liabilities and the lowest priority to unobservable inputs. If the inputs used to measure the financial assets and liabilities fall within more than one level described above, the categorization is based on the lowest level input that is significant to the fair value measurement of the instrument.

The carrying amounts of the Company’s financial assets and liabilities, such as cash and cash equivalents, approximate their fair values because of the short maturity of these instruments.

| ☐ | Recent accounting pronouncements |

In February 2016, the FASB issued ASU 2016-02, “Leases (Topic 842)”. Under ASU 2016-02, lessees will be required to recognize all leases (with the exception of short-term leases) at the commencement date including a lease liability, which is a lessee’s obligation to make lease payments arising from a lease, measured on a discounted basis; and a right-of-use (ROU) asset, which is an asset that represents the lessee’s right to use, or control the use of, a specified asset for the lease term. Leases with a term of twelve months or less will be accounted for similar to existing guidance for operating leases. In December 2017, January 2018, July 2018, December 2018 and March 2019, the FASB issued ASU 2017-13, ASU 2018-01, ASU 2018-10 & 11, ASU 2018-20 and ASU 2019-01, respectively, which contain modifications and improvements to ASU 2016-02. The amendments provide entities with an additional (and optional) transition method to adopt the new leases standard. Under the Optional Transition Method, an entity initially applies the new leases standard at the adoption date and recognizes a cumulative-effect adjustment to the opening balance of retained earnings in the period of adoption. On January 1, 2019, the Company adopted ASC Topic 842 using the modified retrospective approach and elected to utilize the Optional Transition Method. In addition, the Company elected the land easement transition practical expedient and did not reassess whether an existing or expired land easement is a lease or contains a lease if it has not historically been accounted for as a lease. The adoption did not impact the Company’s previously reported consolidated financial statements nor did it result in a cumulative effect adjustment to retained earnings as of January 1, 2019.

In June 2018, the FASB issued ASU 2018-07, Compensation—Stock Compensation (Topic 718): Improvements to Nonemployee Share-Based Payment. ASU 2018-07 aligns the accounting for share based payments granted to non-employees with that of share based payments granted to employees. The Company early adopted ASU No. 2018-07 in the fourth quarter of 2018 and there was no cumulative effect of adoption. The adoption of this ASU did not have a material impact on our financial position, results of operations, cash flows, or presentation thereof.

NOTE—4 REVENUE

| Nine months ended December 31, | ||||||||

| 2019 | 2018 | |||||||

| Products sales, as principal | $ | 11,266,471 | $ | 44,735 | ||||

| Products sales, as agent (net basis) | – | 1,721,612 | ||||||

| Sales programming | 947,171 | – | ||||||

| Other operating revenue | 2,461,179 | 404,301 | ||||||

| $ | 14,674,821 | $ | 2,170,648 | |||||

| 16 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

NOTE—5 INTANGIBLE ASSETS

| December 31, 2019 | March 31, 2019 | |||||||

| (Audited) | ||||||||

| Gaming right and software | ||||||||

| Gross carrying value | $ | 1,238,510 | $ | 1,238,254 | ||||

| Less: accumulated amortization | (880,296 | ) | (671,992 | ) | ||||

| Net carrying value | 358,214 | 566,262 | ||||||

| Non-amortising portion | – | – | ||||||

| Intangible assets, net | $ | 358,214 | $ | 566,262 | ||||

Amortization expense for the three months ended December 31, 2019 and 2018 were $69,007 and $18,353, as part of operating expenses, respectively.

Amortization expense for the nine months ended December 31, 2019 and 2018 were $206,390 and $44,279, as part of operating expenses, respectively.

The following table outlines the annual amortization expense for the next two years:

| Years ending December 31: | ||||

| 2020 | $ | 277,553 | ||

| 2021 | 80,661 | |||

| Total | $ | 358,214 | ||

NOTE—6 AMOUNT DUE FROM A THIRD PARTY

As of December 31, 2019, the Company made temporary advance of $221,373 to a third party, which is secured by the stocks held and becomes mature on or before February 17, 2020. Interest is charged at the rate of 5% per annum.

NOTE—7 AMOUNT DUE TO A DIRECTOR

As of December 31, 2019, amount due to a director of the Company, Mr. TANG Wai Chong Eldee, which was unsecured, interest-free and had no fixed terms of repayment. Imputed interest from related party loan is not significant.

NOTE—8 AMOUNT DUE TO A RELATED PARTY

As of December 31, 2019, the Company owed the amount of $280,317 due to the former shareholder of the Company, Miss Kao. The balance is unsecured, interest-free and has no fixed terms of repayment. Imputed interest from related party loan is not significant.

| 17 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

NOTE—9 OBLIGATIONS UNDER FINANCE LEASES

The Company purchased several motor vehicles and properties under finance lease agreements with the effective interest rate ranging from 3.75% to 22.8% per annum, due through March 10, 2026, with principal and interest payable monthly. The obligations under the finance leases are as follows:

| December 31, 2019 | March 31, 2019 | |||||||

| (Audited) | ||||||||

| Finance lease | $ | 2,865,439 | $ | 3,089,747 | ||||

| Less: interest expense | (772,222 | ) | (834,082 | ) | ||||

| Net present value of finance lease | $ | 2,093,217 | $ | 2,255,665 | ||||

| Current portion | $ | 252,490 | $ | 246,957 | ||||

| Non-current portion | 1,840,727 | 2,008,708 | ||||||

| Total | $ | 2,093,217 | $ | 2,255,665 | ||||

As of December 31, 2019, the maturities of the finance leases for each of the five years and thereafter are as follows:

| Years ending December 31: | ||||

| 2020 | $ | 252,490 | ||

| 2021 | 252,490 | |||

| 2022 | 238,977 | |||

| 2023 | 238,977 | |||

| 2024 | 235,782 | |||

| Thereafter | 874,501 | |||

| Total | $ | 2,093,217 | ||

Included in the consolidated balance sheet as of December 31, 2019 under property, plant and equipment are cost and accumulated depreciation related to capitalized leases of $3,527,314 and $149,807, respectively. Included in the consolidated balance sheet as of March 31, 2019 under property, plant and equipment are cost and accumulated depreciation related to capitalized leases of $3,422,556 and $45,482, respectively.

The building under finance lease is personally guaranteed by the director of the Company, Eldee Tang.

| 18 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

NOTE—10 INCOME TAX

The Company generated an operating loss for the nine months ended December 31, 2019 and 2018, recorded tax credit of $18,555 for the nine months ended December 31, 2019. The Company has operations in various countries and is subject to tax in the jurisdictions in which they operate, as follows:

United States of America

NVGI is registered in the State of Delaware and is subject to United States of America tax law. No provision for income taxes have been made as NVGI has generated no taxable income for the periods presented. The Company’s policy is to recognize accrued interest and penalties related to unrecognized tax benefits in its income tax provision. The Company has not accrued or paid interest or penalties which were not material to its results of operations for the period presented.

As of December 31, 2019, the Company incurred $909,352 of cumulative net operating losses which can be carried forward to offset future taxable income. The net operating loss carryforwards begin to expire in 2039, if unutilized. The Company has provided for a full valuation allowance against the deferred tax assets of $190,964 on the expected future tax benefits from the net operating loss carryforwards as the management believes it is more likely than not that these assets will not be realized in the future.

Republic of Singapore

The Company’s operating subsidiaries are registered in Republic of Singapore and are subject to the Singapore corporate income tax at a standard income tax rate of 17% on the assessable income arising in Singapore during its tax year.

The Company’s subsidiary in Republic of Seychelles is also subject to the Singapore corporate income tax regime.

The reconciliation of income tax rate to the effective income tax rate based on income (loss) before income taxes for the nine months ended December 31, 2019 and 2018 are as follows:

| Nine months ended December 31, | ||||||||

| 2019 | 2018 | |||||||

| Income (loss) before income taxes | $ | 2,620,467 | $ | (43,172,994 | ) | |||

| Statutory income tax rate | 17% | 17% | ||||||

| Income tax expense at statutory rate | 445,479 | (7,339,409 | ) | |||||

| Tax effect of (non-taxable income) non-deductible expenses | (464,034 | ) | 7,513,519 | |||||

| Income tax (credit) expense | $ | (18,555 | ) | $ | 174,110 | |||

NOTE - 11 STOCKHOLDERS’ EQUITY

In October 2019, the Company issued 100,000 shares of its common stock to its legal counsel for legal services provided to the Company at the fair value of $200,000, equal to $2 per share.

As of December 31, 2019 and March 31, 2019, the Company had a total of 210,804,160 and 210,704,160 shares of its common stock issued and outstanding, respectively.

| 19 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

NOTE—12 RELATED PARTY TRANSACTIONS

From time to time, the stockholder and director of the Company advanced funds to the Company for working capital purpose. Those advances are unsecured, non-interest bearing and due on demand. The imputed interest on the loan from a related party was not significant.

Royalty charges and marketing expenses paid to a related company totaled $83,651 and $200,505 for the three months ended December 31, 2019 and 2018.

Royalty charges and marketing expenses paid to a related company totaled $421,972 and $442,651 for the nine months ended December

31, 2019 and 2018.

Apart from the transactions and balances detailed elsewhere in these accompanying consolidated financial statements, the Company has no other significant or material related party transactions during the periods presented.

NOTE—13 CONCENTRATIONS OF RISK

The Company is exposed to the following concentrations of risk:

(a) Major customers

For the three and nine months ended December 31, 2019 and 2018, there is no single customer representing more than 10% of the Company’s revenue.

(b) Major vendors

For the three months ended December 31, 2019, this is one single vendor representing more than 10% of the Company’s purchase. This vendor (Vendor A) accounted for 24% of the Company’s purchase amounting to $544,751 with $355,913 of accounts payable.

Eldee Tang, our Chief Executive Officer and Director, owns 31% of Vendor A.

For the three months ended December 31, 2018, there were no vendors representing more than 10% of the Company’s purchase.

For the nine months ended December 31, 2019, this is one single vendor representing more than 10% of the Company’s purchase. This vendor (Vendor A) accounted for 19% of the Company’s purchase amounting to $1,580,300 with $355,913 of accounts payable.

Eldee Tang, our Chief Executive Officer and Director, owns 31% of Vendor A.

For the nine months ended December 31, 2018, there were no vendors representing more than 10% of the Company’s purchase.

| 20 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

The Company considers its business activities to constitute one single reportable segment. The Company’s chief operating decision makers use consolidated results to make operating and strategic decisions. The geographic distribution analysis of the Company’s revenues by region is as follows:

| Three months ended December 31, | ||||||||

| 2019 | 2018 | |||||||

| China | $ | 9,011 | $ | 1,100,799 | ||||

| Singapore | 1,928,059 | 8,784 | ||||||

| Malaysia | 22,171 | – | ||||||

| Philippines | 131 | – | ||||||

| Thailand | 5,039 | – | ||||||

| Indonesia | 14,986 | – | ||||||

| Other countries in Asia Pacific | 84,540 | 97,568 | ||||||

| $ | 2,063,937 | $ | 1,207,151 | |||||

| Nine months ended December 31, | ||||||||

| 2019 | 2018 | |||||||

| China | $ | 225,641 | $ | 1,801,612 | ||||

| Singapore | 7,399,810 | 269,685 | ||||||

| Malaysia | 3,669,216 | – | ||||||

| Philippines | 1,646,733 | – | ||||||

| Thailand | 802,893 | – | ||||||

| Indonesia | 412,002 | – | ||||||

| Other countries in Asia Pacific | 518,526 | 99,351 | ||||||

| $ | 14,674,821 | $ | 2,170,648 | |||||

All of the Company’s long-lived assets are located in Singapore.

(c) Interest rate risk

As the Company has no significant interest-bearing assets, the Company’s income and operating cash flows are substantially independent of changes in market interest rates.

The Company’s interest-rate risk arises from borrowings under finance leases. The Company manages interest rate risk by varying the issuance and maturity dates variable rate debt, limiting the amount of variable rate debt, and continually monitoring the effects of market changes in interest rates. As of December 31, 2019, borrowing under finance lease was at fixed rates.

| 21 |

NOBLE VICI GROUP, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

FOR THE NINE MONTHS ENDED DECEMBER 31, 2019

(Currency expressed in United States Dollars (“US$”), except for number of shares)

(UNAUDITED)

(d) Economic and political risk

The Company’s major operations are conducted in Republic of Singapore. Accordingly, the political, economic, and legal environments in Singapore, as well as the general state of Singapore’s economy may influence the Company’s business, financial condition, and results of operations.

(e) Exchange rate risk

The Company cannot guarantee that the current exchange rate will remain steady; therefore there is a possibility that the Company could post the same amount of profit for two comparable periods and because of the fluctuating exchange rate actually post higher or lower profit depending on exchange rate of S$ converted to US$ on that date. The exchange rate could fluctuate depending on changes in political and economic environments without notice.

NOTE—14 COMMITMENTS AND CONTINGENCIES

(a) Operating lease commitments

During the three and nine months ended December 31, 2019 and 2018, the Company leased its properties under operating leases. The leases typically commence for a period ranging for 1 to 3 years. None of the leases includes contingent rentals.

As of December 31, 2019, the Company has future rental payables under non-cancellable operating leases of $37,473 in the next twelve months.

(b) Capital commitment

On April 1, 2019, the Company entered into a binding Memorandum of Understanding (the “MOU”) with Eldee Wai Chong Tang, our Chief Executive Officer and Director, whereby we agreed to reorganize Elusyf Global Private Limited, a Singapore corporation (“EGPL”), into the Company in accordance with the terms of the MOU. Upon the consummation of such reorganization, EGPL will become a 51% owned subsidiary of the Company. EGPL is engaged in the business of marketing and distribution of health and beauty products, such as Elusyf Mitos Activa and Cell Activa Phytomask, among other offerings, through its wide network of channels. The consummation of the acquisition is subject to the satisfactory completion of financial, tax and legal due diligence of EGPL by the Company, among other conditions. The Company is in the process of completing its due diligence review of EGPL and has not yet consummated the acquisition.

The Company’s director, Mr. Tang owns Fifty-Nine Thousand Nine Hundred Eighty (59,980) ordinary shares of EGPL, representing 51% of the issued and outstanding securities of EGPL. It is considered as related party transaction.

NOTE—15 SUBSEQUENT EVENTS

In accordance with ASC Topic 855, “Subsequent Events”, which establishes general standards of accounting for and disclosure of events that occur after the balance sheet date but before consolidated financial statements are issued, the Company has evaluated all events or transactions that occurred after December 31, 2019, up through February 14, 2020, the Company issued the unaudited condensed consolidated financial statements. During the period, the Company has no material recognizable subsequent events.

| 22 |

ITEM 2 Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-looking statements

The following discussion of our financial condition and results of operations should be read in conjunction with the financial statements and the related notes thereto included elsewhere in this quarterly report on Form 10-Q. This quarterly report on Form 10-Q contains certain forward-looking statements and our future operating results could differ materially from those discussed herein. Certain statements contained in this discussion, including, without limitation, statements containing the words "believes," "anticipates," "expects" and the like, constitute "forward-looking statements" within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). However, as we issue “penny stock,” as such term is defined in Rule 3a51-1 promulgated under the Exchange Act, we are ineligible to rely on these safe harbor provisions. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Given these uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements. We disclaim any obligation to update any such factors or to announce publicly the results of any revisions of the forward-looking statements contained herein to reflect future events or developments.

Currency and exchange rate

Unless otherwise noted, all currency figures quoted as “U.S. dollars”, “dollars” or “$” refer to the legal currency of the United States. Throughout this report, assets and liabilities of the Company’s subsidiaries are translated into U.S. dollars using the exchange rate on the balance sheet date. Revenue and expenses are translated at average rates prevailing during the period. The gains and losses resulting from translation of financial statements of foreign subsidiaries are recorded as a separate component of accumulated other comprehensive income within the statement of stockholders’ equity.

Overview

We were incorporated under the laws of the State of Delaware on July 6, 2010 under the name “Advanced Ventures Corp.” Effective January 6, 2014, we changed our name to “Gold Union Inc.” Effective March 26, 2018, we changed our name to Noble Vici Group, Inc. and our trading symbol was changed to NVGI. On August 8, 2018, we consummated the acquisition of Noble Vici Private Limited, a corporation organized under the laws of Singapore (“NVPL”), which was wholly owned by Eldee Tang, our sole director and Chief Executive Officer. NVPL is engaged in the IoT, Big Data, Blockchain and E-commerce business. As a result of our acquisition of NVPL, we entered into the IoT, Big Data, Blockchain and E-commerce business. We are headquartered in Singapore and operate a branch office in Taiwan. Certain of our resellers are operating “V-More” branded satellite offices in Shenzhen, China.

History

On July 27, 2010, we entered into an exclusive worldwide patent sale agreement (the “Patent Transfer and Sales Agreement”) with Ilanit Appelfeld (the “Seller”), in relation to a patented technology, U.S. Patent Number: 6,743,209 (the “Patent”), for a catheter with an integral anchoring mechanism. The patent and technology were transferred to us in exchange of payment to Ilanit Appelfeld of $17,500 (seventeen thousand five hundred United States Dollars), according to the terms and conditions specified in the Patent Transfer and Sales Agreement related to U.S. Patent Number: 6,743,209.

During the second quarter of 2011 the Company raised gross proceeds of $75,000 pursuant to an effective Form S-1 Registration Statement and issued 37,500,000 post forward stock split shares of common stock that were registered pursuant to the Form S-1 Registration Statement.

| 23 |

Effective March 7, 2012, we increased the number of our authorized shares of common stock to three billion shares (3,000,000,000) and engaged in a forward stock split of its common shares whereby each one share of our common stock was split into fifteen shares of our common stock.

During the second fiscal quarter of 2014, we elected to discontinue our business of exploiting the Patent and began to consider other business opportunities that may bring quicker and greater value to our stockholders. We initially considered entering into the business of trading precious metal bullion primarily in the Asia Pacific region. Therefore, effective January 6, 2014, we changed our name to “Gold Union Inc.” to more adequately reflect our initial intended business operations.

On December 31, 2015, we consummated a Share Exchange Agreement with G.U. International Limited, a limited company incorporated under the laws of the Republic of Seychelles and our wholly owned subsidiary (“GUI”), and Kao Wei-Chen, an individual representing herself and 8 other individuals (collectively, the “Golden Corridor Shareholders”), which agreement was amended several times to extend the closing date of the acquisition (collectively, the “Share Exchange Agreement”). Pursuant to the Share Exchange Agreement, we, through GUI, purchased 480 shares of Phnom Penh Golden Corridor Trading Co. Limited (the “GC Shares”), from 9 private Golden Corridor Shareholders, representing 48% of the issued and outstanding shares of common stock of Golden Corridor. As consideration, we issued to the Golden Corridor Shareholders 2,500,000,000 shares of our common stock, at a value of US $0.002 per share, for an aggregate value of US $5,000,000.

As a result of our acquisition of the GC Shares, we ceased our metal bullion trading business and entered into the real estate development and rental business located in the Kingdom of Cambodia. Golden Corridor owns three parcels of land located at National Road 44, Phum Phkung, Chbarmorn Commune, Chbarmorn District, Kampong Speu Province, Kingdom of Cambodia, measuring an aggregate of 172,510 square meters (collectively, the “Properties”). We intended to develop the Properties into an industrial park for rental income.

Due to difficulties in entering the real estate development and rental business, on February 2, 2018, we engaged in a corporate reorganization and distributed the GC Shares to our shareholders. On March 18, 2018, our subsidiary, G.U. Asia Limited was dissolved.

Change in Control

On March 27, 2018, Lim Yew Chuan, the director, Chief Executive Officer, Chief Financial Officer and Secretary of Noble Vici Group, Inc. (the “Company”), resigned from all of his positions as director, Chief Executive Officer, Chief Financial Officer and Secretary of the Company. Mr. Lim’s decision to leave the Board and his executive officer positions with the Company is due to personal reasons and not due to any dispute or disagreement with the Company on any matter relating to the Company's operations, policies or practices.

Effective March 27, 2018, the following individuals were appointed to serve in the capacities set forth next to their names until his successor(s) shall be duly elected or appointed, unless he resigns, is removed from office or is otherwise disqualified from serving as an executive officer or director of the Company:

| Name | Office(s) |

| Eldee Tang | Chief Executive Officer and Director |

| Sin Chi Yip | Chief Financial Officer |

| Jon Yee Chuan Lim | Chief Operating Officer and Secretary |

On January 29, 2018, Eldee Tang entered into Share Sale Agreements with four shareholders and former affiliates of the Company to purchase up to 1,675,000,000 shares of the Company’s common stock at a per share purchase price of US$0.00008, for an aggregate price of US$134,000. On June 15, 2018, the Company effectuated a 1 for 1,000 reverse stock split whereby every 1,000 shares of the Company’s common stock were reduced to one share. The parties effectuated Mr. Tang’s purchase of 750,000 shares such securities (expressed on a post reverse split basis) effective June 15, 2018. Mr. Tang hopes to purchase the balance of the 925,000 shares from Kao Wei-Chen, a former affiliate of the Company, in the near future. The foregoing description of the Share Sale Agreement with Kao Wei-Chen is qualified in its entirety by reference to such agreement which is filed as Exhibit 10.2 to this Quarterly Report and is incorporated herein by reference.

| 24 |

Effective June 15, 2018, we:

| 1. | Increased the Company’s authorized capital from 3,000,000,000 shares of common stock, par value $0.0001 (the “Common Stock”), to 3,050,000,000 shares, consisting of 3,000,000,000 shares of Common Stock and 50,000,000 shares of undesignated preferred stock, par value $0.0001 (the “Preferred Stock”); | |

| 2. | Effected a 1-for-1000 reverse stock split of our issued and outstanding Common Stock (the “Reverse Stock Split”); | |

| 3. | Elected not to be governed by Section 203 of the Delaware General Corporation Law; | |

| 4. | Changed the Company’s fiscal year end from December 31st to March 31st, for all purposes (including tax and financial accounting); | |

| 5. | Adopted Amended and Restated Certificate of Incorporation for the purpose of consolidating the amendments to the Company’s Certificate of Incorporation; and | |

| 6. | Adopted the Amended and Restated Bylaws of the Company. |

Acquisition of NVPL

On August 8, 2018, we consummated the acquisition of Noble Vici Private Limited, a corporation organized under the laws of Singapore (“NVPL”), in accordance with the terms of a Share Exchange Agreement. NVPL is wholly owned by Eldee Tang, our Chief Executive Officer and Director. Pursuant to the Share Exchange Agreement, we purchased One Million and One (1,000,001) shares of NVPL (the “NVPL Shares”), representing all of the issued and outstanding shares of common stock of NVPL, in consideration of One Hundred Forty Million (140,000,000) shares of our common stock, at a value of US $1.70 per share, for an aggregate value of US $238,000,000. It is our understanding that Mr. Tang is not a U.S. Person within the meaning of Regulations S. Accordingly, the Shares are being sold pursuant to the exemption provided by Section 4(a)(2) of the Securities Act of 1933, as amended, Regulation D and Regulation S promulgated thereunder.

Acquisition of TDA and NDA

On September 17, 2018, we consummated the acquisition of a 51% controlling interest in The Digital Agency Private Limited, a private limited company organized under the laws of Singapore (“TDA”), and a start-up digital marketing company, in accordance with the terms of that certain Share Exchange Agreement by and among the Company, Noble Infotech Applications Private Limited, a private limited company organized under the laws of Singapore and our wholly owned subsidiary (“NIA”), TDA and Mok Jo Han (“the “TDA Share Exchange Agreement”). Pursuant to the terms of the TDA Share Exchange Agreement, we acquired 51 ordinary shares of TDA, representing approximately fifty-one percent (51%) of the issued and outstanding ordinary shares of TDA, in exchange for 510,000 shares of common stock of the Company, par value $0.0001 (the “TDA Shares”), representing an exchange ratio of ONE (1) ordinary share of TDA for Ten Thousand (10,000) shares of common stock of the Company, at a valuation of $2.00 per share of the Company, for an aggregate value of $1,020,000. It is our understanding that Mr. Mok is not a U.S. Person within the meaning of Regulations S. The TDA Shares were sold pursuant to the exemption provided by Section 4(a)(2) of the Securities Act of 1933, as amended, and Regulation S promulgated thereunder.

On September 17, 2018, we consummated the acquisition of a 51% controlling interest in Noble Digital Apps Sendirian Berhad, a private limited company organized under the laws of Malaysia (“NDA”), and a start-up digital apps and big data company in accordance with the terms of that certain Share Exchange Agreement by and among the Company, NIA, NDA, Cheng Bok Woon, Tan Yew Fui, and Yong Swee Sun (“the “NDA Share Exchange Agreement”). Pursuant to the terms of the NDA Share Exchange Agreement, we acquired 510 ordinary shares of NDA, representing approximately fifty-one percent (51%) of the issued and outstanding ordinary shares of NDA, in exchange for 510,000 shares of common stock of the Company, par value $0.0001 (the “NDA Shares”), representing an exchange ratio of ONE (1) ordinary share of NDA for One Thousand (1,000) shares of common stock of the Company, at a valuation of $2.00 per share of the Company, for an aggregate value of $1,020,000. It is our understanding that Mr. Cheng, Mr. Tan and Mr. Yong are not U.S. Person within the meaning of Regulations S. The NDA Shares were sold pursuant to the exemption provided by Section 4(a)(2) of the Securities Act of 1933, as amended, and Regulation S promulgated thereunder.

| 25 |

Issuance of shares to sales affiliates

On September 17, 2018, and September 25, 2018, we approved the issuance of Nine Million One Hundred Thirty Five Thousand Seven Hundred Ninety Four (9,135,794) shares and Five Hundred Sixty Seven Thousand Sixty-Four (567,064) shares of our common stock, par value $0.0001, respectively, representing a total of approximately 6.3% of our issued and outstanding common stock, at a per share price of One Dollars and Ninety Nine Cents (US $1.99), to approximately 460 sales associates for prior sales and marketing services provided to us and our subsidiaries and affiliates. As a condition of receipt of such securities, each recipient executed a Stockholder Representation Letters, which contained, among other things, restrictions prohibiting the transfer of such securities for a minimum period of 18 months up to a maximum period of 66 months after the execution of such letter. For ease of administration, the recipients appointed Noble Infotech Limited (“NIL”) as nominee to hold, manage, administer and effectuate the distribution of such securities upon the expiration of the applicable restricted periods. The shares were issued on October 18, 2018 to NIL. The securities were issued pursuant to the exemption provided by Regulation S promulgated under the Securities Act of 1933, as amended. The foregoing description of the Stockholder Representation Letters are qualified in its entirety by reference to such agreements which are filed as Exhibit 10.3 to this Quarterly Report and are incorporated herein by reference.

On December 3, 2018, we approved the issuance of up to an aggregate of Ten Million Eight Hundred Thirty Eight Thousand One Hundred Forty One (10,838,141) shares of our common stock, par value $0.0001, representing approximately 7.1% of our issued and outstanding common stock, at a per share price of Two Dollars (US $2.00), to about 690 sales associates for prior sales and marketing services provided to us and our subsidiaries and affiliates. As a condition of receipt of such securities, each recipient was required to execute one of two standard forms of Stockholder Representation Letters, which contained, among other things, restrictions prohibiting the transfer of such securities for a minimum period of 18 or 24 months up to a maximum period of 72 months after the execution of such letter. For ease of administration, the recipients appointed Venvici Partners Limited (“VVP”) as nominee to hold, manage, administer and effectuate the distribution of such securities upon the expiration of the applicable restricted periods. The shares were issued on January 4, 2019 to VVP. The securities were issued pursuant to the exemption provided Regulation S promulgated under the Securities Act of 1933, as amended. The foregoing description of the Stockholder Representation Letters and the appointment of VVP as trustee are qualified in its entirety by reference to such agreements which are filed as Exhibits 10.4 and 10.5 to this Quarterly Report and are incorporated herein by reference.