As filed with the Securities and Exchange Commission on January 17, 2014.

Registration No. 333-168971

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

POST-EFFECTIVE AMENDMENT NO. 12

TO FORM S-11

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

APPLE REIT TEN, INC.

(Exact name of Registrant as specified in its charter)

|

|

|

|

|

Virginia |

814 East Main Street |

27-3218228 |

||

(State or other jurisdiction |

(Address. Including zip code, and |

(I.R.S. Employer |

Glade M. Knight

Chairman and Chief Executive Officer

Apple REIT Ten, Inc.

814 East Main Street

Richmond, Virginia 23219

(804) 344-8121

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Martin B. Richards, Esq.

David F. Kurzawa, Esq.

McGuireWoods LLP

901 East Cary Street, One James Center

Richmond, Virginia 23219

(804) 775-1029

(804) 775-7471

Approximate date of commencement of proposed sale to the public: As soon as possible after effectiveness of the Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933 check the following box. S

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. £

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. £

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. £

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. £

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

|

|

|

|

|

|

|

Large accelerated filer £ |

Accelerated filer £ |

Non-accelerated filer S |

Smaller reporting company £ |

Post-Effective Amendment No. 12 to Registration Statement on Form S-11 Contents

(1)

Part I of Registration Statement

Sticker Supplement for Supplement No. 6 (b) Supplement No. 6 dated January 17, 2014 (cumulative, replacing all prior supplements) (c) Prospectus dated July 31, 2013

(2)

Part II of Registration Statement (3) Signature Page (4) Exhibits (see Part II, Item 36, for Exhibit Index)

(Registration No. 333-168971)

(a)

APPLE REIT TEN, INC. STICKER SUPPLEMENT TO Supplement No. 6 to be used with Summary of Supplement to Prospectus Supplement No. 6 (cumulative, replacing all prior supplements) dated January 17, 2014 reports on (a) the status of our best-efforts offering of Units; (b) our recent purchase of 12 hotels containing a total of 1,446 guest rooms for an aggregate gross purchase price of approximately $192.2 million; (c)

our execution of certain purchase contracts that relate to 3 hotels containing a total of 411 guest rooms and that provide for an aggregate gross purchase price of approximately $68.1 million; (d) our execution of a credit agreement, as amended, that provides for a $100 million unsecured revolving credit

facility that may be increased to $150 million; (e) Apple Ten Advisors, Inc.’s subcontracting of its obligations under the advisory agreement with us to Apple REIT Nine, Inc.; (f) an update regarding our legal proceedings; (g) an update regarding our Unit Redemption program; (h) financial and operating

information for our recently purchased hotels; and (i) our recent financial information and certain additional information about us. As of January 27, 2011, we completed our minimum offering of 9,523,810 Units at $10.50 per Unit and raised gross proceeds of $100 million and proceeds net of selling commissions and marketing expenses of $90 million. Each Unit consists of one common share and one Series A Preferred Share.

We are continuing the offering at $11 per Unit in accordance with the prospectus. As of December 31, 2013, we had closed on the sale of 72,866,168 additional Units at $11 per Unit and from such sale we raised gross proceeds of approximately $801.5 million and proceeds net of selling commissions and marketing expenses of approximately $721.4 million. Sales of all Units at

$10.50 per Unit and $11.00 per Unit, when combined, represent gross proceeds of approximately $901.5 million and proceeds net of selling commissions and marketing expenses of approximately $811.4 million. In connection with our hotel purchases to date, we paid a total of approximately $15.7 million, representing 2% of the aggregate gross purchase price, as a commission to Apple Suites Realty Group, Inc. This entity is owned by Glade M. Knight, who is our Chairman and Chief Executive Officer.

SUPPLEMENT NO. 6 DATED JANUARY 17, 2014

PROSPECTUS DATED JULY 31, 2013

(See Supplement for Additional Information)

SUPPLEMENT NO. 6 DATED JANUARY 17, 2014 TO PROSPECTUS DATED JULY 31, 2013 APPLE REIT TEN, INC. The following information supplements the prospectus of Apple REIT Ten, Inc. dated July 31, 2013 and is part of the prospectus. This Supplement updates the information presented in the prospectus. Prospective investors should carefully review the prospectus and this Supplement No. 6 (which is

cumulative and replaces all prior Supplements). TABLE OF CONTENTS

S-3

S-6

S-6

S-7

S-9

S-13 Financial and Operating Information for Our Recently Purchased Properties

S-15

S-18 Management’s Discussion and Analysis of Financial Condition and Results of Operations

S-20

S-20

F-1 Certain forward-looking statements are included in the prospectus and this supplement. These forward-looking statements may involve our plans and objectives for future operations, including future growth and availability of funds. These forward-looking statements are based on current expectations,

which are subject to numerous risks and uncertainties. Assumptions relating to these statements involve judgments with respect to, among other things, the continuation of our offering of Units, the outcome of current and future litigation, regulatory proceedings or inquiries, changes in laws or regulations

or interpretations of current laws and regulations that impact our business, assets or classification as a real estate investment trust, our ability to realize our anticipated return on our energy investment, future economic, competitive and market conditions and future business decisions, together with local,

national and international events (including, without limitation, acts of terrorism or war, and their direct and indirect effects on travel and the economy). All of these matters are difficult or impossible to predict accurately and many of them are beyond our control. Although we believe the assumptions

relating to the forward-looking statements, and the statements themselves, are reasonable, any of the assumptions could be inaccurate and, therefore, there can be no assurance that these forward-looking statements will prove to be accurate. In light of the significant uncertainties inherent in these forward-

looking statements, the inclusion of this information should not be regarded as a representation by us or any other person that our objectives and plans, which we consider to be reasonable, will be achieved.

“Courtyard by Marriott,” “Fairfield Inn,” “Fairfield Inn & Suites,” “TownePlace Suites,” “Marriott,” “SpringHill Suites” and “Residence Inn” are each a registered trademark of Marriott International, Inc. or one of its affiliates. All references below to “Marriott” mean Marriott International, Inc. and all of

its affiliates and subsidiaries, and their respective officers, directors, agents, employees, accountants and attorneys. Marriott is not responsible for the content of this prospectus supplement, whether relating to hotel information, operating information, financial information, Marriott’s relationship with Apple REIT

Ten, Inc., or otherwise. Marriott is not involved in any way, whether as an “issuer” or “underwriter” or otherwise, in the offering by Apple REIT Ten, Inc. and receives no proceeds from the offering. Marriott has not expressed any approval or disapproval regarding this prospectus supplement or the offering

related to this prospectus supplement, and the grant by Marriott of any franchise or other rights to Apple REIT Ten, Inc. shall not be construed as any expression of approval or disapproval. Marriott has not assumed, and shall not have, any liability in connection with this prospectus supplement or the offering

related to this prospectus supplement. “Hampton Inn,” “Hampton Inn & Suites,” “Homewood Suites,” “Embassy Suites,” “Hilton Garden Inn” and “Home2 Suites by Hilton” are each a registered trademark of Hilton Worldwide or one of its affiliates. All references below to “Hilton” mean Hilton Worldwide and all of its affiliates and

subsidiaries, and their respective officers, directors, agents, employees, accountants and attorneys. Hilton is not responsible for the content of this prospectus supplement, whether relating to hotel information, operating information, financial information, Hilton’s relationship with Apple REIT Ten, Inc., or

otherwise. Hilton is not involved in any way, whether as an “issuer” or “underwriter” or otherwise, in the offering by Apple REIT Ten, Inc. and receives no proceeds from the offering. Hilton has not expressed any approval or disapproval regarding this prospectus supplement or the offering related to this

prospectus supplement, and the grant by Hilton of any franchise or other rights to Apple REIT Ten, Inc. shall not be construed as any expression of approval or disapproval. Hilton has not assumed, and shall not have, any liability in connection with this prospectus supplement or the offering related to this

prospectus supplement. S-2

As of January 27, 2011, we completed our minimum offering of 9,523,810 Units at $10.50 per Unit and raised gross proceeds of $100,000,000 and proceeds net of selling commissions and marketing expenses of $90,000,000. Each Unit consists of one common share and one Series A preferred share. We

are continuing the offering at $11.00 per Unit in accordance with the prospectus. We registered to sell a total of 182,251,082 Units. As of December 31, 2013, 99,861,104 Units remain unsold. Our offering of Units expires on January 19, 2014. Pursuant to Rule 415(a)(6) of the Securities Act, we have filed

a new registration statement with the Securities and Exchange Commission (“SEC”) to sell the remaining 99,861,104 Units. While our new registration statement is under review by the SEC, Rule 415(a)(5) of the Securities Act permits us to continue to offer and sell Units, under our original registration

statement, until the earlier of the effective date of our new registration statement or 180 days after the third anniversary of the initial effectiveness date of our original registration statement. As of December 31, 2013, we had closed on the following sales of Units in the offering:

Price Per

Number of

Gross

Proceeds Net $10.50

9,523,810

$

100,000,000

$

90,000,000 $11.00

72,866,168

801,527,853

721,375,067 Total

82,389,978

$

901,527,853

$

811,375,067 Distributions Our distributions since initial capitalization through September 30, 2013 totaled approximately $112.0 million and were paid at a monthly rate of $0.06875 per common share beginning in February 2011. For the same period, our net cash generated from operations was approximately $66.4 million. Due

to the inherent delay between raising capital and investing that same capital in income producing real estate, we have had significant amounts of cash earning interest at short term money market rates. As a result, a portion of distributions paid through September 30, 2013 have been funded from

proceeds from our on-going best-efforts offering of Units and borrowings under our credit facility, and are expected to be treated as a return of capital for federal income tax purposes. The following is a summary of the distributions and net cash from (used in) operations. S-3

Unit

Units Sold

Proceeds

of Selling

Commissions

and Marketing

Expense

Allowance

Period

Total

Total

Net Cash From/

Net Income/

Percentage of For the period Aug. 13, 2010 (initial capitalization through Dec. 31, 2010

$

—

$

—

$

(6,000

)

$

(31,000

)

— 1st Quarter 2011

0.13750

1,855,000

(2,488,000

)

(2,390,000

)

-134

% 2nd Quarter 2011

0.20625

5,753,000

(1,059,000

)

(1,179,000

)

-18

% 3rd Quarter 2011

0.20625

7,596,000

846,000

(473,000

)

11

% 4th Quarter 2011

0.20625

8,390,000

3,522,000

(1,092,000

)

42

% 1st Quarter 2012

0.20625

9,336,000

1,905,000

1,974,000

20

% 2nd Quarter 2012

0.20625

10,596,000

9,616,000

5,900,000

91

% 3rd Quarter 2012

0.20625

12,079,000

11,515,000

5,519,000

95

% 4th Quarter 2012

0.20625

13,023,000

10,097,000

3,686,000

78

% 1st Quarter 2013

0.20625

13,622,000

3,830,000

2,888,000

28

% 2nd Quarter 2013

0.20625

14,339,000

12,994,000

9,186,000

91

% 3rd Quarter 2013

0.20625

15,428,000

15,664,000

8,182,000

102

% Total

$

2.20000

$

112,017,000

$

66,436,000

$

32,170,000

59

% Note for Table:

(a)

See complete consolidated statements of cash flows and consolidated statements of operations for the 12 months ending December 31, 2012 and 2011 included in our most recent Form 10-K for the year ended December 31, 2012 and nine months ending September 30, 2013 included in our most recent

Form 10-Q for the quarter ended September 30, 2013.

In February 2011, our Board of Directors established a policy for an annualized distribution rate of $0.825 per common share, payable in monthly distributions. We intend to continue paying distributions on a monthly basis, consistent with the annualized distribution rate established by our Board of

Directors. Our objective in setting a distribution rate is to project a rate that will provide consistency over our existence taking into account acquisitions and capital improvements, ramp up of new properties and varying economic cycles. To meet this objective, we may require the use of debt or offering

proceeds in addition to cash from operations. Since a portion of distributions to date have been funded with proceeds from our offering of Units and borrowings under our credit facility, our ability to maintain our current intended rate of distribution will be based on our ability to generate cash from

operations at this level, as well as our ability to utilize currently available financing, or our ability to obtain additional financing. Since there can be no assurance that the properties already acquired or that will be acquired will provide income at this level, or that we will be able to obtain additional

financing, there can be no assurance as to the classification or duration of distributions at the current rate. Proceeds of the offering which are distributed are not available for investment in properties. See “Risk Factors—We may be unable to make distributions to our shareholders,” on page 27 of our

prospectus. Net Book Value Per Share In connection with this on-going offering of Units, we are providing information about our net book value per share. Net book value per share is calculated as total book value of assets minus total liabilities. It assumes that the value of real estate assets diminishes predictably over time as shown

through the depreciation and amortization of real estate investments. Real estate values have historically risen or fallen with market conditions. Net book value does not reflect value per share upon an orderly sale or liquidation of the Company in accordance with our investment objectives. Our net book

value reflects dilution in the value of our Units from the issue price as a result of (i) operating losses, which reflect accumulated depreciation and amortization of real estate investments S-4

Distributions

Declared and

Paid per Share

Distributions

Declared and Paid

(Used in)

Operations(a)

(Loss)(a)

Net Cash

From/ (Used in)

Operations To

Total

Distributions

as well as the fees and expenses paid to acquire real estate including commissions to Apple Suites Realty Group, Inc. (“ASRG”), (ii) the funding of distributions from sources other than cash flow from operations, and (iii) fees paid in connection with our on-going best-efforts offering, including selling

commissions and marketing fees. As of September 30, 2013, our net book value per share was $8.75. We calculated our net book value by subtracting total liabilities from total assets and dividing by the total number of Units outstanding at September 30, 2013. The offering price of shares under our on-going best-efforts offering at December 31, 2013 was $11.00. Our offering price was not established on an independent basis and bears no relationship to the net book value of our assets. There is currently no established public market in which our common

shares or Units are traded, however as discussed above in the Status of the Offering section of this supplement, 72.9 million Units have been purchased at $11 per Unit. As discussed in the prospectus the Units will be illiquid for an indefinite period of time. We will continue to use the $11 per Unit price

as the offering price until such time as buyers are not available, or until we have an orderly sale or liquidation in accordance with our investment objectives outlined in the prospectus. Unit Redemption Program In April 2012, we instituted a Unit Redemption Program to provide limited interim liquidity to our shareholders who have held their Units for at least one year. Shareholders may request redemption of Units for a purchase price equal to 92.5% of the price paid per Unit if the Units have been

owned for five years or less, or 100% of the price paid per Unit if the Units have been owned more than five years. The maximum number of Units that may be redeemed in any given year is three percent (3%) of the weighted average number of Units outstanding during the 12-month period

immediately prior to the date of redemption. In the case of redemption of Units following the death of all shareholders in one account, the purchase price will equal 100% of the price paid by the deceased shareholders for the Units. We reserve the right to change the purchase price of redemptions,

reject any request for redemption, or otherwise amend the terms of, suspend, or terminate the Unit Redemption Program. Under the terms of the Unit Redemption Program, the funding for the redemption of Units comes exclusively from the net proceeds we receive from the sale of Units under our best-efforts offering or our dividend reinvestment plan which we plan to implement following the conclusion of our

offering. However, until we implement our dividend reinvestment plan, we funded Unit redemptions for the periods noted below from the net proceeds we received from the sale of our Units under our best-efforts offering. Since inception of the program through December 31, 2013, we have redeemed approximately 3.5 million Units representing $35.9 million. As contemplated in the program, beginning with the October 2012 redemption, the scheduled redemption date for the fourth quarter of 2012, through the April

2013 redemption, the scheduled redemption date for the second quarter of 2013, we redeemed Units on a pro rata basis due to the 3% limitation discussed above. Prior to October 2012 and since July 2013, the scheduled redemption date for the third quarter of 2013, we redeemed 100% of redemption

requests. The following is a summary of the Unit redemptions:

Redemption Date

Total

Units

Total

Average April 2012

474,466

474,466

—

$

10.22 July 2012

961,236

961,236

—

10.09 October 2012

617,811

46,889

570,922

10.58 January 2013

938,026

114,200

823,826

10.73 April 2013

1,063,625

637,779

425,846

10.19 July 2013

677,855

677,855

—

10.16 October 2013

609,079

609,079

—

10.18 S-5

Requested Unit

Redemptions at

Redemption Date

Redeemed

Redemption

Requests Not

Redeemed at

Redemption Date

Price Paid on

Redemptions for

Quarter

The term the “Apple REIT Entities” means Apple REIT Ten, Inc. (the “Company”), Apple REIT Six, Inc., Apple REIT Seven, Inc., Apple REIT Eight, Inc. and Apple REIT Nine, Inc. On December 13, 2011, the United States District Court for the Eastern District of New York ordered that three putative class actions, Kronberg, et al. v. David Lerner Associates, Inc., et al., Kowalski v. Apple REIT Ten, Inc., et al., and Leff v. Apple REIT Ten, Inc., et al., be consolidated and

amended the caption of the consolidated matter to be In re Apple REITs Litigation. The District Court also appointed lead plaintiffs and lead counsel for the consolidated action and ordered lead plaintiffs to file and serve a consolidated complaint by February 17, 2012. The Company was previously

named as a party in all three of the above mentioned class action lawsuits. On February 17, 2012, lead plaintiffs and lead counsel in the In re Apple REITs Litigation, Civil Action No. 1:11-cv-02919-KAM-JO, filed an amended consolidated complaint in the United States District Court for the Eastern District of New York against the Company, Apple Suites Realty Group,

Inc., Apple Eight Advisors, Inc., Apple Nine Advisors, Inc., Apple Ten Advisors, Inc., Apple Fund Management, LLC, Apple REIT Six, Inc., Apple REIT Seven, Inc., Apple REIT Eight, Inc. and Apple REIT Nine, Inc., their directors and certain officers, and David Lerner Associates, Inc. and David

Lerner. The consolidated complaint, which was dismissed in April 2013, was purportedly brought on behalf of all purchasers of Units in the Company and the other Apple REIT Entities, or those who otherwise acquired these Units that were offered and sold to them by David Lerner Associates, Inc., or

its affiliates and on behalf of subclasses of shareholders in New Jersey, New York, Connecticut and Florida, and alleges that the Apple REIT Entities “misrepresented the investment objectives of the Apple REITs, the dividend payment policy of the Apple REITs, and the value of their Apple REIT

investments.” The consolidated complaint asserts claims under Sections 11, 12 and 15 of the Securities Act of 1933, as well as claims for breach of fiduciary duty, aiding and abetting breach of fiduciary duty, negligence, and unjust enrichment, and claims for violation of the securities laws of Connecticut

and Florida. The complaint seeks, among other things, certification of a putative nationwide class and the state subclasses, damages, rescission of share purchases and other costs and expenses. On April 18, 2012, the Company, and the other defendants moved to dismiss the consolidated complaint in the In re Apple REITs Litigation. By Order entered on March 31, 2013 and opinion issued on April 3, 2013, the Court dismissed the consolidated complaint in its entirety with prejudice and

without leave to amend. Plaintiffs filed a Notice of Appeal to the Second Circuit Court of Appeals on April 12, 2013, and filed their Brief for Plaintiffs-Appellants on July 26, 2013. Defendants-Appellees filed their Briefs on October 25, 2013. In response to the Defendants-Appellees Briefs, the Plaintiffs-

Appellants filed a Reply Brief with the court on November 15, 2013. The Company believes that Plaintiffs’ claims against it, its officers and directors and other Apple REIT Entities were properly dismissed by the lower court, and intends to vigorously defend the judgment as entered. In the event some

or all of Plaintiffs’ claims are revived as a result of Plaintiffs’ appeal, the Company will, once again, defend against them vigorously. At this time, the Company cannot reasonably predict the outcome of these proceedings or provide a reasonable estimate of the possible loss or range of loss due to these

proceedings, if any. Credit Facility On July 26, 2013, through one of our wholly-owned subsidiaries, we entered into an unsecured revolving credit facility with a commercial bank in an initial amount of $75 million. On October 3, 2013, the credit agreement was amended to increase the amount of the facility to $100 million and to

allow for future increases in the amount of the facility to $150 million, subject to certain conditions. The credit facility will be utilized for acquisitions, hotel renovations, working capital and other general corporate funding purposes, including the payment of redemptions and distributions. Under the terms

of the credit facility, we may make voluntary prepayments in whole or in part, at any time. The credit facility matures in July 2015; however, we have the right, upon satisfaction of S-6

certain conditions, including covenant compliance and payment of an extension fee, to extend the maturity date to July 2016. Interest payments are due monthly and the interest rate, subject to certain exceptions, is equal to the one-month LIBOR (the London Inter-Bank Offered Rate for a one-month

term) plus a margin ranging from 2.25% to 2.75%, depending upon our leverage ratio, as calculated under the terms of the credit facility. We are also required to pay an unused facility fee of 0.25% or 0.35% on the unused portion of the revolving credit facility, based on the amount of borrowings

outstanding during the quarter. On the day of closing of the credit facility, we borrowed $54.0 million under the credit facility, of which $53.6 million was used to fund a portion of the aggregate purchase price of eight hotels that closed on July 26, 2013 as described below and $0.4 million was used to pay loan origination costs. The credit facility contains mandatory prepayment requirements, customary affirmative covenants, negative covenants and events of default. The financial covenants include, among others, a minimum net worth, maximum debt limits, maximum distributions, minimum debt service and fixed charge

coverage ratios and restrictions on investments. Subcontract Agreement On August 8, 2013, Apple REIT Seven, Inc. (“Apple Seven”), Apple REIT Eight, Inc. (“Apple Eight”) and Apple REIT Nine, Inc. (“Apple Nine”) announced that they have entered into an Agreement and Plan of Merger, as amended (the “Merger Agreement”) pursuant to which Apple Seven and

Apple Eight will merge into Apple Nine in two merger transactions (the “Mergers”), and that as a result of this transaction, Apple Nine will become self-advised and each of Apple Seven, Apple Eight and Apple Nine will terminate its advisory arrangements with its advisors. Concurrently with the execution of the Merger Agreement, on August 7, 2013, Apple Nine entered into a subcontract agreement, as amended (the “Subcontract Agreement”) with Apple Ten Advisors, Inc. (“A10A”). Pursuant to the Subcontract Agreement, A10A will subcontract its obligations under

the advisory agreement between A10A and us (the “Advisory Agreement”) to Apple Nine. The Subcontract Agreement provides that, from and after the effective time of the Mergers, Apple Nine will provide to us the advisory services contemplated under the Advisory Agreement and Apple Nine will

receive fees and expenses payable under the Advisory Agreement from us. We also signed the Subcontract Agreement to acknowledge the terms of the Subcontract Agreement. The Subcontract Agreement has no effect on our contract with A10A. Advisory Agreement Upon a determination by our independent members of our Board of Directors, the Advisory Agreement between us and A10A was renewed for an additional one (1) year term expiring on December 20, 2014. We have elected to “incorporate by reference” certain information into this prospectus supplement. By incorporating by reference, we are disclosing important information to you by referring you to documents we have filed separately with the SEC. The following documents filed with the SEC are

incorporated by reference in this prospectus supplement (Commission File No. 333-168971), except for any document or portion thereof deemed to be “furnished” and not filed in accordance with SEC rules:

•

Quarterly Reports on Form 10-Q for the quarters ended September 30, 2013, June 30, 2013 and March 31, 2013 filed with the SEC on November 6, 2013, August 8, 2013 and May 7, 2013, respectively; • Definitive Proxy Statement filed on Schedule 14A filed with the SEC on April 9, 2013; • Annual Report on Form 10-K for the fiscal year ended December 31, 2012 filed with the SEC on March 6, 2013; S-7

• Current Report on Form 8-K/A filed with the SEC on August 30, 2013; includes the financial statements for Maple Grove Lodging Investors, LLC, Phoenix Southwest Lodging Investors I, LLC, Deer Valley Lodging Investors, LLC, Deer Valley Hotel Investors II, LLC, Omaha Downtown Lodging

Investors III, LLC and Omaha Downtown Lodging Investors IV, LLC (Maple Grove, Minnesota Hilton Garden Inn; Phoenix, Arizona Courtyard; Phoenix North/Happy Valley, Arizona Hampton Inn & Suites; Phoenix North/Happy Valley, Arizona Homewood Suites; Omaha, Nebraska Homewood

Suites and Omaha, Nebraska Hampton Inn & Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on April 30, 2013; includes the financial statements for the Fair Oaks Hotel, LLC (Fairfax, Virginia Marriott) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on November 9, 2011; includes the financial statements for the KRG/White LS Hotel, LLC and Kite Realty/White LS Hotel Operators, LLC (South Bend, Indiana Fairfield Inn & Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on November 9, 2011; includes the financial statements for the Ascent Hospitality, Inc. (Merrillville, Indiana Hilton Garden Inn), Omaha Downtown Lodging Investors II, LLC and Scottsdale Lodging Investors, LLC (Omaha, Nebraska Hilton

Garden Inn and Scottsdale, Arizona Hilton Garden Inn) and VHRMR Round Rock, LTD (Austin/Round Rock, Texas Homewood Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on November 9, 2011; includes the financial statements for the Chicago Hotel Portfolio (Des Plaines, Illinois Hilton Garden Inn and Skokie, Illinois Hampton Inn & Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on November 9, 2011; includes the financial statements for the SASI, LLC (Mason, Ohio Hilton Garden Inn), Omaha Downtown Lodging Investors II, LLC and Scottsdale Lodging Investors, LLC (Omaha, Nebraska Hilton Garden Inn and

Scottsdale, Arizona Hilton Garden Inn), and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on July 20, 2011; includes the financial statements for the Hawkeye Hotel Portfolio (Cedar Rapids, Iowa Homewood Suites; Cedar Rapids, Iowa Hampton Inn & Suites and Davenport, Iowa Hampton Inn & Suites) and the required pro forma

financial information; • Current Report on Form 8-K/A filed with the SEC on July 20, 2011; includes the financial statements for the McKibbon Hotel Portfolio (Knoxville, Tennessee SpringHill Suites; Gainesville, Florida Hilton Garden Inn; Richmond, Virginia SpringHill Suites; Pensacola, Florida TownePlace Suites;

Mobile, Alabama Hampton Inn & Suites; Knoxville, Tennessee TownePlace Suites; Knoxville, Tennessee Homewood Suites and Gainesville, Florida Homewood Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on May 17, 2011; includes the financial statements for the CN Hotel Portfolio (Winston-Salem, North Carolina Hampton Inn & Suites; Matthews, North Carolina Fairfield Inn & Suites; Columbia, South Carolina TownePlace Suites and Jacksonville,

North Carolina Home2 Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on May 17, 2011; includes the financial statements for the CN Hotel Portfolio (Winston-Salem, North Carolina Hampton Inn & Suites; Matthews, North Carolina Fairfield Inn & Suites; Columbia, South Carolina TownePlace Suites and Jacksonville,

North Carolina Home2 Suites) and the required pro forma financial information; • Current Report on Form 8-K/A filed with the SEC on May 17, 2011; includes the financial statements for the Denver, Colorado—Hilton Garden Inn and the required pro forma financial information; S-8

• The description of our Units contained in our Registration Statement filed on Form 8-A (File No. 000-54651), filed with the SEC on April 12, 2012; • Current Reports on Form 8-K filed with the SEC on December 3, 2013, November 13, 2013, August 28, 2013, August 9, 2013, July 31, 2013, June 10, 2013, May 28, 2013, May 23, 2013, May 20, 2013, May 17, 2013, April 19, 2013, April 10, 2013, March 19, 2013, February 5, 2013, January 8, 2013,

November 27, 2012, October 25, 2012, October 17, 2012, August 23, 2012, July 11, 2012, May 23, 2012, May 23, 2012, May 9, 2012, March 5, 2012, February 3, 2012, February 2, 2012, January 13, 2012, January 4, 2012, December 21, 2011, December 13, 2011, December 1, 2011, November 30, 2011,

November 14, 2011, November 7, 2011, November 4, 2011, November 2, 2011, October 19, 2011, October 11, 2011, October 5, 2011, September 23, 2011, September 7, 2011, August 25, 2011, August 11, 2011, July 22, 2011, July 18, 2011, July 13, 2011, July 6, 2011, June 27, 2011, June 14, 2011, June

13, 2011, June 7, 2011, June 7, 2011, June 2, 2011, May 13, 2011, May 6, 2011, May 5, 2011, April 15, 2011, April 7, 2011, March 29, 2011, March 18, 2011, March 8, 2011, March 4, 2011, March 1, 2011, February 14, 2011, February 9, 2011, February 3, 2011, and January 27, 2011. All of the documents that we have incorporated by reference into this prospectus supplement are available on the SEC’s website, www.sec.gov. In addition, these documents can be inspected and copied at the Public Reference Room maintained by the SEC at 100 F Street, NE, Washington, D.C.

20549. Copies also can be obtained by mail from the Public Reference Room at prescribed rates. Please call the SEC at (800) SEC-0330 for further information on the operation of the Public Reference Room. In addition, we will provide to each person, including any beneficial owner of our common shares, to whom this prospectus supplement is delivered, a copy of any or all of the information that we have incorporated by reference into this prospectus supplement but not delivered with this prospectus

supplement. To receive a free copy of any of the documents incorporated by reference in this prospectus supplement, other than exhibits, unless they are specifically incorporated by reference in those documents, call or write us at 814 East Main Street, Richmond, Virginia 23219, Attention: Kelly Clarke,

(804) 344-8121. The documents also may be accessed through our website at www.applereitten.com. The information relating to us contained in this prospectus supplement does not purport to be comprehensive and should be read together with the information contained in the documents incorporated or

deemed to be incorporated by reference in this prospectus supplement. Summary of Real Estate Investments Since our prospectus dated July 31, 2013, we have purchased 12 additional hotels. Currently, through our subsidiaries, we own a total of 47 hotels. These hotels contain a total of 5,933 guest rooms. They were purchased for an aggregate gross purchase price of $784.8 million. Financial and operating

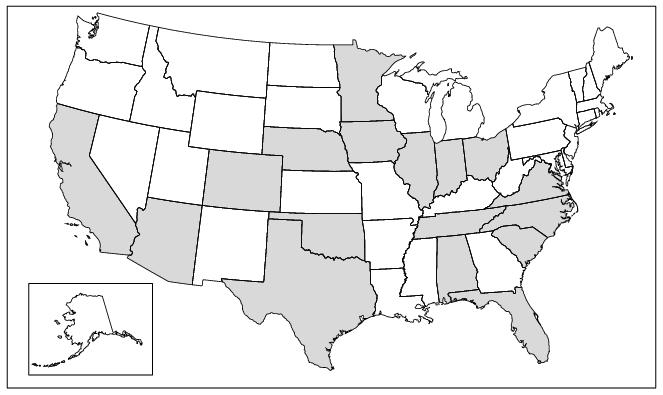

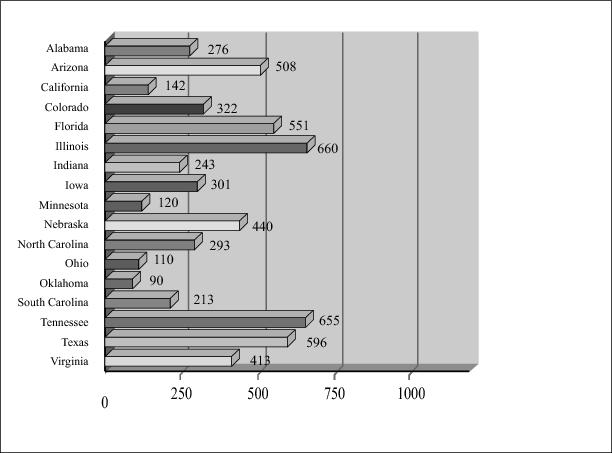

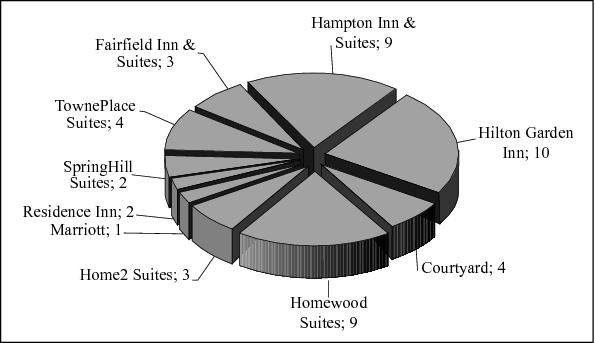

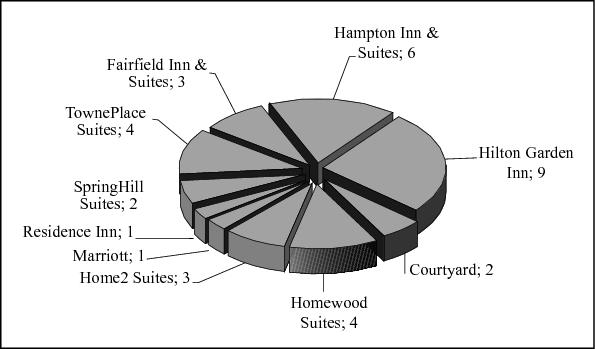

information about our recently purchased hotels is provided in another section below. Description of Real Estate Owned The map below shows the states in which our hotels are located, and the following charts summarize our room and franchise information. S-9

States in which Our Hotels are Located Number of Guest Rooms by State: S-10

Type and Number of Hotel Franchises: Summary of Potential Acquisitions We have entered into, or caused one of our indirect wholly-owned subsidiaries to enter into, purchase contracts for three other hotels. These contracts are for direct hotel purchases or, in certain cases, a purchase of the entity that currently owns the property. The following table summarizes hotel and

contract information:

Hotel Location Franchise

Date of

Number of

Gross

1. Oklahoma City, Oklahoma(a) Hilton Garden Inn

January 11, 2013

155

$

(b)

2. Oklahoma City, Oklahoma(a) Homewood Suites

January 11, 2013

100

(b)

3. Fort Lauderdale, Florida(a)/(c) Residence Inn

February 28, 2013

156

23,088,000

Total

411

$

68,088,000 Notes for Table:

(a)

The indicated hotels are currently under construction. The table shows the expected number of rooms upon hotel completion and the expected franchise. (b) The Hilton Garden Inn and Homewood Suites hotels in Oklahoma City, Oklahoma are part of an adjoining two-hotel complex that will be located on the same site. The two hotels are covered by the same purchase contract with a total gross purchase price of $45 million. The amount is reflected in

the total gross purchase price indicated above. (c) If the seller meets all of the conditions to closing, the Company is obligated to specifically perform under the contract. As the property is under construction, at this time, the seller has not met all of the conditions to closing. We have no material relationship or affiliation with the prospective sellers of the hotels described above, except through the pending purchase contracts and any related documents. In general, each purchase contract listed above required a deposit upon (or shortly after) execution. An additional deposit is typically due upon the expiration of the contract review period. If a closing occurs under a purchase contract, the initial and additional deposits are credited toward the

purchase price. If a closing does not occur because the seller fails to satisfy a condition to closing or breaches the purchase contract, the applicable deposits would be refunded to us. The total S-11

Purchase

Contract

Rooms

Purchase

Price

of both the initial and additional deposits for the purchase contracts listed above is approximately $0.3 million. For each purchase contract listed above, there are material conditions to closing that presently remain unsatisfied. Accordingly, there can be no assurance at this time that a closing will occur under any of these purchase contracts. Source of Funds and Related Party Payments Our recent purchases, which resulted in our ownership of 12 additional hotels, were funded by the proceeds from our ongoing offering of Units and borrowings under our credit facility. Our offering proceeds and borrowings under our credit facility also have been used to fund the deposits required

by the hotel purchase contracts. We have entered into a property acquisition and disposition agreement with ASRG to acquire and dispose of our real estate assets. A fee of 2% of the gross purchase price or gross sale price in addition to certain reimbursable expenses will be payable for these services. The entity is owned by Glade

M. Knight, who is our Chairman and Chief Executive Officer. We used borrowings under our credit facility to pay $3.8 million to ASRG, representing 2% of the gross purchase price for our recent purchases. David Lerner Associates, Inc., ASRG and A10A earned the compensation and expense reimbursements shown below in connection with their services from inception through the period ending September 30, 2013 relating to our offering phase, acquisition phase and operations phase. David Lerner Associates, Inc. is not related to ASRG or A10A. ASRG and A10A are owned by Glade M. Knight, our Chairman and Chief Executive Officer. As described on page 12 of our prospectus under the heading “Compensation” and as shown below, we pay certain fees and expenses as they are incurred, while others accrue and will be paid in future periods, subject in some cases to the achievement of performance criteria. We did not incur any

amounts in connection with our disposition phase through September 30, 2013. Cumulative through September 30, 2013

Incurred

Paid

Accrued Offering Phase Selling commissions paid to David Lerner Associates, Inc. in connection with the offering

$

65,221,500

$

65,221,500

$

— Marketing expense allowance paid to David Lerner Associates, Inc. in connection with the offering

21,740,500

21,740,500

—

86,962,000

86,962,000

— Acquisition Phase Acquisition commission paid to Apple Suites Realty Group, Inc.

13,939,000

13,939,000

— Reimbursement of costs paid to Apple Suites Realty Group, Inc.

1,700,000

1,700,000

— Reimbursement of certain deposits to Apple Suites Realty Group, Inc.

105,000

105,000

— Operations Phase Asset management fee paid to Apple Ten Advisors, Inc.

1,495,000

1,495,000

— Reimbursement of costs paid to Apple Ten Advisors, Inc.

2,700,000

2,700,000

— Fees for Account Maintenance Services to Shareholders paid to David Lerner Associates, Inc.

547,000

490,000

57,000 S-12

SUMMARY OF CONTRACTS FOR OUR RECENTLY PURCHASED PROPERTIES The following information updates the contract information included in our prospectus dated July 31, 2013 for our recently purchased hotels. Ownership, Leasing and Management Summary Each of our recently purchased hotels has been leased to one of our indirect wholly-owned subsidiaries, as the lessee, under a separate hotel lease agreement. For simplicity, the applicable lessee will be referred to below as the “lessee.” Each hotel is managed under a separate management agreement between the applicable lessee and the manager. For simplicity, the applicable manager will be referred to below as the “manager.” We have no material relationship or affiliation with the sellers or managers, except for the relationship resulting from our purchases, our management agreements for the hotels we own, and any related documents. The hotel lease agreements and the management agreements are among the contracts described in another section below. The table below specifies the franchise, hotel owner, lessee and manager for our recently purchased hotels:

Hotel Location

Franchise(a)

Hotel

Lessee

Manager

1.

Oklahoma City, Oklahoma

2.

Denton, Texas

Homewood Suites

Apple Ten Hospitality Ownership, Inc.

Apple Ten Hospitality Texas Services IV, Inc.

Chartwell Hospitality, LLC(b)

3.

Maple Grove, Minnesota

4.

Phoenix North/Happy Valley, Arizona

5.

Phoenix North/Happy Valley, Arizona

6.

Phoenix, Arizona

Courtyard

Apple Ten Hospitality Ownership, Inc.

Apple Ten Hospitality Management, Inc.

North Central Hospitality, LLC(b)

7.

Omaha, Nebraska

Hampton Inn & Suites

Apple Ten Nebraska, LLC

Apple Ten Hospitality Management, Inc.

North Central Hospitality, LLC(b)

8.

Omaha, Nebraska

Homewood Suites

Apple Ten Nebraska, LLC

Apple Ten Hospitality Management, Inc.

North Central Hospitality, LLC(b)

9.

Colorado Springs, Colorado

Apple Ten SPE Colorado Springs, Inc.

Apple Ten Services Colorado Springs, Inc.

Chartwell Hospitality, LLC(b)

10.

Franklin Cool Springs, Tennessee

Apple Ten SPE Franklin I, Inc.

Apple Ten Services Franklin I, Inc.

Chartwell Hospitality, LLC(b)

11.

Franklin Cool Springs, Tennessee

Apple Ten SPE Franklin II, Inc.

Apple Ten Services Franklin II, Inc.

Chartwell Hospitality, LLC(b)

12.

Dallas, Texas

Homewood Suites

Apple Ten Hospitality Ownership, Inc.

Apple Ten Hospitality Texas Services III, Inc.

Texas Western Management Partners, L.P. Notes:

(a)

All brand and trade names, logos or trademarks contained, or referred to, in this prospectus supplement are the properties of their respective owners. These references shall not in any way be construed as participation by, or endorsement of, our offering by any of our franchisors or managers. (b) The hotel specified was purchased from an affiliate of the indicated manager. S-13

Owner/Lessor

Homewood Suites

Apple Ten Oklahoma, LLC

Apple Ten Hospitality Management, Inc.

Chartwell Hospitality, LLC(b)

Hilton Garden Inn

Apple Ten Hospitality Ownership, Inc.

Apple Ten Hospitality Management, Inc.

North Central Hospitality, LLC(b)

Hampton Inn & Suites

Apple Ten Hospitality Ownership, Inc.

Apple Ten Hospitality Management, Inc.

North Central Hospitality, LLC(b)

Homewood Suites

Apple Ten Hospitality Ownership, Inc.

Apple Ten Hospitality Management, Inc.

North Central Hospitality, LLC(b)

Hampton Inn & Suites

Courtyard

Residence Inn

Hotel Lease Agreements Each of our recently purchased hotels is covered by a separate hotel lease agreement between the owner (one of our indirect wholly-owned subsidiaries) and the applicable lessee (another one of our indirect wholly-owned subsidiaries, as specified in the previous section). Each lease provides for an

initial term of 5 years. The applicable lessee has the option to extend its lease term for one additional three-year period, provided it is not in default at the end of the initial term. Each lease provides for annual base rent and percentage rent. Shown below are the annual base rents and the lease commencement dates for our recently purchased hotels:

Hotel Location

Franchise

Annual

Date of Lease

1. Oklahoma City, Oklahoma

Homewood Suites

$

766,000

July 26, 2013

2. Denton, Texas

Homewood Suites

787,000

July 26, 2013

3. Maple Grove, Minnesota

Hilton Garden Inn

1,081,000

July 26, 2013

4. Phoenix North/Happy Valley, Arizona

Hampton Inn & Suites

612,000

July 26, 2013

5. Phoenix North/Happy Valley, Arizona

Homewood Suites

809,000

July 26, 2013

6. Phoenix, Arizona

Courtyard

853,000

July 26, 2013

7. Omaha, Nebraska

Hampton Inn & Suites

1,452,000

July 26, 2013

8. Omaha, Nebraska

Homewood Suites

1,227,000

July 26, 2013

9. Colorado Springs, Colorado

Hampton Inn & Suites

855,000

November 8, 2013

10. Franklin Cool Springs, Tennessee

Courtyard

2,024,000

November 8, 2013

11. Franklin Cool Springs, Tennessee

Residence Inn

1,978,000

November 8, 2013

12. Dallas, Texas

Homewood Suites

1,161,000

December 5, 2013 The annual percentage rent depends on a formula that compares fixed “suite revenue breakpoints” with “suite revenue,” which is equal to gross revenue from guest rentals less sales and room taxes and credit card fees. Management Agreements Each of our recently purchased hotels is being managed by the manager under a separate management agreement between the manager and the applicable lessee (which is one of our indirect wholly-owned subsidiaries, as specified in the previous section). The manager is responsible for managing and

supervising the daily operations of the hotel and for collecting revenues for the benefit of the applicable lessee. The fees and other terms of these agreements are the result of commercial negotiations between otherwise unrelated parties. We believe that such fees and terms are appropriate for the hotels

and the markets in which they operate. Our leasing subsidiary may terminate the management agreements if the managers fail to achieve certain performance levels. Franchise Agreements In general, for our hotels franchised by Hilton Worldwide or one of its affiliates, there is a franchise license agreement between the applicable lessee (as specified in the previous section) and Hilton Worldwide or an affiliate. Each franchise license agreement provides for the payment of royalty fees

and program fees to the franchisor. A percentage of gross room revenues is used to determine these payments. Apple Ten Hospitality, Inc. or another one of our subsidiaries has guaranteed the payment and performance of the lessee under the applicable franchise license agreement. For the hotels franchised by Marriott International, Inc. or one of its affiliates, there is a relicensing franchise agreement between the applicable lessee (as specified in the previous section) and Marriott International, Inc. or an affiliate. Each relicensing franchise agreement provides for the payment of

royalty fees and marketing contributions to the franchisor. A percentage of gross room revenues is used to determine these payments. Apple Ten Hospitality, Inc. or another one of our subsidiaries has guaranteed the payment and performance of the lessee under the applicable relicensing franchise

agreement. S-14

Base Rent

Commencement

The fees and other terms of these agreements are the result of commercial negotiations between otherwise unrelated parties, and we believe that such fees and terms are appropriate for the hotels and the markets in which they operate. FINANCIAL AND OPERATING INFORMATION FOR OUR Our recently purchased hotels offer guest rooms and suites, together with related amenities, that are consistent with their operations. The hotels are located in developed or developing areas and in competitive markets. We believe the hotels are well-positioned to compete in their markets based on

location, amenities, rate structure and franchise affiliation. In the opinion of management, each hotel is adequately covered by insurance. The following tables present further information about our recently purchased hotels: Table 1. General Information

Hotel Location

Franchise

Number of

Gross

Average

Federal

Purchase

1.

Oklahoma City, Oklahoma

Homewood Suites

90

$

11,500,000

$

149-169

$

10,621,510

July 26, 2013

2.

Denton, Texas

Homewood Suites

107

11,300,000

119-159

10,208,840

July 26, 2013

3.

Maple Grove, Minnesota

Hilton Garden Inn

120

12,675,000

139-219

10,980,000

July 26, 2013

4.

Phoenix North/Happy Valley, Arizona

Hampton Inn & Suites

125

8,600,000

99-109

8,600,000

July 26, 2013

5.

Phoenix North/Happy Valley, Arizona

Homewood Suites

134

12,025,000

109-129

12,025,000

July 26, 2013

6.

Phoenix, Arizona

Courtyard

127

10,800,000

124-164

9,416,900

July 26, 2013

7.

Omaha, Nebraska

Hampton Inn & Suites

139

19,775,000

119-159

16,692,720

July 26, 2013

8.

Omaha, Nebraska

Homewood Suites

123

17,625,000

139-199

14,229,080

July 26, 2013

9.

Colorado Springs, Colorado

Hampton Inn & Suites

101

11,500,000

99-144

10,484,000

November 8, 2013

10.

Franklin Cool Springs, Tennessee

Courtyard

126

25,500,000

189-219

24,251,088

November 8, 2013

11.

Franklin Cool Springs, Tennessee

Residence Inn

124

25,500,000

169-259

24,270,912

November 8, 2013

12.

Dallas, Texas

Homewood Suites

130

25,350,000

209-229

23,364,900

December 5, 2013 Total

1,446

$

192,150,000 Notes for Table 1:

(a)

The amounts shown are subject to change, and exclude discounts that may be offered to corporate, frequent and other select customers. Rates reflected were in effect at acquisition. (b) The depreciable life is 39 years (or less, as may be permitted by federal tax laws) using the straight-line method. The modified accelerated cost recovery system will be used for the hotel’s personal property component. S-15

RECENTLY PURCHASED PROPERTIES

Rooms/

Suites

Purchase

Price

Daily Rate

(Price) per

Room/Suite(a)

Income Tax

Basis for

Depreciable

Real Property

Component of

Hotel(b)

Date

Table 2. Loan Information(a)

Hotel Location

Franchise

Assumed Principal

Annual

Maturity Date

1. Colorado Springs, Colorado

Hampton Inn & Suites

$

8,231,000

6.25

%

July 2021

2. Franklin Cool Springs, Tennessee

Courtyard and Residence Inn

30,492,000

6.25

%

August 2021

$

38,723,000 Note for Table 2:

(a)

This table summarizes loans that (i) pre-dated our purchase, (ii) are secured by our hotels, as indicated and (iii) were assumed by our purchasing subsidiary. Each loan provides for monthly payments of principal and interest on an amortized basis.

Table 3. Operating Information(a) PART A

Hotel Location

Franchise

Avg. Daily Occupancy Rates (%)

2008

2009

2010

2011

2012

1. Oklahoma City, Oklahoma

Homewood Suites

67

%

75

%

80

%

80

%

84

%

2. Denton, Texas

Homewood Suites

n/a

25

%

63

%

81

%

81

%

3. Maple Grove, Minnesota

Hilton Garden Inn

60

%

56

%

62

%

61

%

70

%

4. Phoenix North/Happy Valley, Arizona

Hampton Inn & Suites

15

%

26

%

45

%

53

%

58

%

5. Phoenix North/Happy Valley, Arizona

Homewood Suites

2

%

28

%

63

%

64

%

72

%

6. Phoenix, Arizona

Courtyard

34

%

51

%

59

%

58

%

56

%

7. Omaha, Nebraska

Hampton Inn & Suites

59

%

66

%

72

%

74

%

79

%

8. Omaha, Nebraska

Homewood Suites

53

%

60

%

67

%

71

%

77

%

9. Colorado Springs, Colorado

Hampton Inn & Suites

65

%

64

%

73

%

75

%

72

%

10. Franklin Cool Springs, Tennessee

Courtyard

n/a

66

%

77

%

81

%

81

%

11. Franklin Cool Springs, Tennessee

Residence Inn

n/a

51

%

80

%

86

%

88

%

12. Dallas, Texas(b)

Homewood Suites

n/a

n/a

n/a

n/a

n/a PART B

Hotel Location

Franchise

Revenue per Available Room/Suite ($)

2008

2009

2010

2011

2012

1. Oklahoma City, Oklahoma

Homewood Suites

$

64

$

70

$

74

$

75

$

81

2. Denton, Texas

Homewood Suites

n/a

$

21

$

55

$

71

$

75

3. Maple Grove, Minnesota

Hilton Garden Inn

$

75

$

61

$

65

$

67

$

82

4. Phoenix North/Happy Valley, Arizona

Hampton Inn & Suites

$

12

$

21

$

36

$

45

$

52

5. Phoenix North/Happy Valley, Arizona

Homewood Suites

$

2

$

22

$

47

$

53

$

58

6. Phoenix, Arizona

Courtyard

$

36

$

52

$

58

$

60

$

62

7. Omaha, Nebraska

Hampton Inn & Suites

$

74

$

70

$

79

$

84

$

92

8. Omaha, Nebraska

Homewood Suites

$

62

$

66

$

73

$

83

$

93

9. Colorado Springs, Colorado

Hampton Inn & Suites

$

66

$

63

$

72

$

77

$

76

10. Franklin Cool Springs, Tennessee

Courtyard

n/a

$

76

$

87

$

98

$

105

11. Franklin Cool Springs, Tennessee

Residence Inn

n/a

$

55

$

88

$

99

$

108

12. Dallas, Texas(b)

Homewood Suites

n/a

n/a

n/a

n/a

n/a Notes for Table 3:

(a)

Operating data is presented for the last five years (or since the beginning of hotel operations). See Table 1. General Information above for the date the hotel was acquired. (b) There is no data prior to 2013 because the hotel was under construction and did not open until October 2013. S-16

Balance of Loan

Interest Rate

Table 4. Tax and Related Information

Hotel Location

Franchise

Tax Year(b)

Real

Real

1. Oklahoma City, Oklahoma

Homewood Suites

2012

1.3

%

$

89,112

2. Denton, Texas

Homewood Suites

2012

2.5

%

138,584

3. Maple Grove, Minnesota

Hilton Garden Inn

2013

4.1

%

222,698

4. Phoenix North/Happy Valley, Arizona

Hampton Inn & Suites

2012

2.4

%

96,279

(c)

5. Phoenix North/Happy Valley, Arizona

Homewood Suites

2012

2.4

%

103,212

(c)

6. Phoenix, Arizona

Courtyard

2012

2.9

%

211,993

7. Omaha, Nebraska

Hampton Inn & Suites

2012

2.1

%

276,433

8. Omaha, Nebraska

Homewood Suites

2012

2.1

%

250,635

9. Colorado Springs, Colorado

Hampton Inn & Suites

2012

1.7

%

105,428

10. Franklin Cool Springs, Tennessee

Courtyard

2013

2.6

%

111,701

(d)

11. Franklin Cool Springs, Tennessee

Residence Inn

2013

2.6

%

109,927

(d)

12. Dallas, Texas

Homewood Suites

2013

2.9

%

82,933

(e) Notes for Table 4:

(a)

Property tax rate is an aggregate figure for county, city and other local taxing authorities (to the extent applicable). (b) Represents a calendar year. (c) Phoenix North/Happy Valley Hampton Inn & Suites and Homewood Suites are located on the same parcel. (d) Franklin Cool Springs Courtyard and Residence Inn are located on the same parcel. (e) The hotel property consisted of undeveloped land for a portion of the tax year, and the real property tax is not necessarily indicative of property taxes expected for the hotel in the future. S-17

Property

Tax Rate(a)

Property

Tax

(in thousands except per share and statistical data)

Nine Months Ended

Year Ended

Year Ended

For the period Revenues: Room revenue

$

104,647

$

106,759

$

37,911

$

— Other revenue

10,922

10,907

4,180

— Total revenue

115,569

117,666

42,091

— Expenses: Hotel operating expenses

64,621

65,948

23,737

— Property taxes, insurance and other

7,822

8,067

2,420

— General and administrative

3,305

4,408

3,062

28 Acquisition related costs

4,904

1,582

11,265

— Depreciation

15,082

15,795

6,009

— Investment income

(4,467

)

(247

)

(395

)

— Interest expense

3,802

4,729

1,002

3 Income tax expense

244

305

125

— Total expenses

95,313

100,587

47,225

31 Net income (loss)

$

20,256

$

17,079

$

(5,134

)

$

(31

) Per Share: Net income (loss) per common share

$

0.29

$

0.31

$

(0.18

)

$

(3,083.50

) Distributions paid per common share

$

0.61875

$

0.825

$

0.756

$

— Weighted-average common shares outstanding — basic and diluted

70,308

54,888

29,333

— Balance Sheet Data (at end of period): Cash and cash equivalents

$

—

$

146,530

$

7,079

$

124 Investment in real estate, net

$

675,130

$

506,689

$

452,205

$

— Energy investment

$

100,329

$

—

$

—

$

— Total assets

$

794,448

$

667,785

$

471,222

$

992 Notes payable

$

115,075

$

81,186

$

69,636

$

400 Shareholders’ equity

$

670,250

$

579,525

$

395,915

$

17 Net book value per share

$

8.75

$

8.92

$

9.10

$

— Other Data: Cash Flow From (Used In): Operating activities

$

32,488

$

33,133

$

821

$

(6

) Investing activities

$

(282,856

)

$

(58,606

)

$

(393,640

)

$

— Financing activities

$

103,838

$

164,924

$

399,774

$

82 Number of hotels owned at end of period

43

31

26

— Average Daily Rate (ADR)(a)

$

116

$

114

$

110

$

— Occupancy

73

%

70

%

69

%

— Revenue Per Available Room (RevPAR)(b)

$

85

$

79

$

76

$

— Total rooms sold(c)

905,011

937,392

344,152

— Total rooms available(d)

1,236,348

1,347,740

499,089

— S-18

September 30,

2013

December 31,

2012

December 31,

2011

August 13, 2010

(initial capitalization)

through December 31,

2010

(in thousands except per share and statistical data)

Nine Months Ended

Year Ended

Year Ended

For the period Modified Funds From Operations Calculation(e): Net income (loss)

$

20,256

$

17,079

$

(5,134

)

$

(31

) Depreciation of real estate owned

15,082

15,795

6,009

— Funds from operations

35,338

32,874

875

(31

) Acquisition related costs

4,904

1,582

11,265

— Modified funds from operations

$

40,242

$

34,456

$

12,140

$

(31

)

(a)

Total room revenue divided by number of rooms sold. (b) ADR multiplied by occupancy percentage. (c) Represents the number of room nights sold during the period. (d) Represents the number of rooms owned by the Company multiplied by the number of nights in the period. (e) Funds from operations (FFO) is defined as net income (loss) (computed in accordance with generally accepted accounting principles—GAAP) excluding gains and losses from sales of depreciable property, plus depreciation and amortization. Modified FFO (MFFO) excludes costs associated with the

acquisition of real estate. The Company considers FFO and MFFO in evaluating property acquisitions and its operating performance and believes that FFO and MFFO should be considered along with, but not as an alternative to, net income and cash flows as a measure of the Company’s activities in

accordance with GAAP. The Company considers FFO and MFFO as supplemental measures of operating performance in the real estate industry, and along with the other financial measures included in this Supplement, including net income, cash flow from operating activities, financing activities and

investing activities, they provide investors with an indication of the performance of the Company. The Company’s definition of FFO and MFFO are not necessarily the same as such terms that are used by other companies. FFO and MFFO are not necessarily indicative of cash available to fund cash

needs. S-19

September 30,

2013

December 31,

2012

December 31,

2011

August 13, 2010

(initial capitalization)

through December 31,

2010

MANAGEMENT’S DISCUSSION AND ANALYSIS Our Management’s Discussion and Analysis of Financial Condition and Results of Operations from our most recent Form 10-Q for the quarter ended September 30, 2013 has been incorporated by reference herein. See “Incorporation by Reference” on page S-7 of this prospectus supplement. The consolidated financial statements of Apple REIT Ten, Inc. appearing in Apple REIT Ten, Inc.’s Annual Report (Form 10-K) for the year ended December 31, 2012 (including the financial statement schedule appearing therein), and the effectiveness of Apple REIT Ten, Inc.’s internal control

over financial reporting as of December 31, 2012, have been audited by Ernst & Young, LLP, independent registered public accounting firm, as set forth in their reports thereon, included therein, and incorporated herein by reference. Such consolidated financial statements and schedule and Apple REIT

Ten, Inc. management’s assessment of the effectiveness of internal control over financial reporting as of December 31, 2012 are incorporated herein by reference in reliance upon such reports given on the authority of such firm as experts in accounting and auditing. The financial statements of the Denver, Colorado-Hilton Garden Inn appearing on Form 8-K/A dated May 17, 2011 for the years ended December 31, 2010 and 2009, have been audited by Ernst & Young LLP, independent registered public accounting firm, as set forth in their report thereon, included

therein, and are incorporated herein by reference. Such financial statements are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The financial statements of the CN Hotel Portfolio (Winston-Salem, North Carolina Hampton Inn & Suites; Matthews, North Carolina Fairfield Inn & Suites; Columbia, South Carolina TownePlace Suites; and Jacksonville, North Carolina Home2 Suites) at December 31, 2010 and 2009 and for the years

then ended, incorporated by reference herein, have been audited by Gerald O. Dry, PA, independent registered public accounting firm, as set forth in their report thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting

and auditing. The financial statements of the McKibbon Hotel Portfolio (Knoxville, Tennessee SpringHill Suites; Gainesville, Florida Hilton Garden Inn; Richmond, Virginia SpringHill Suites; Pensacola, Florida TownePlace Suites; Mobile, Alabama Hampton Inn & Suites; Knoxville, Tennessee TownePlace Suites;

Knoxville, Tennessee Homewood Suites and Gainesville, Florida Homewood Suites) at December 31, 2010 and 2009 and for the years then ended, incorporated by reference herein, have been audited by Mauldin & Jenkins, LLC, independent registered public accounting firm, as set forth in their report

thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The financial statements of the Hawkeye Hotel Portfolio (Cedar Rapids, Iowa Homewood Suites; Cedar Rapids, Iowa Hampton Inn & Suites and Davenport, Iowa Hampton Inn & Suites) at December 31, 2010 and 2009 and for the years then ended, incorporated by reference herein, have been audited

by Wade Stables P.C., independent registered public accounting firm, as set forth in their report thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The financial statements of SASI, LLC (Mason, Ohio Hilton Garden Inn) at December 31, 2010 and for the year then ended, incorporated by reference herein, have been audited by Warren Averett, LLC (formerly Wilson, Price, Barranco, Blankenship & Billingsley, P.C.), independent registered public

accounting firm, as set forth in their report thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The financial statements of Omaha Downtown Lodging Investors II, LLC and Scottsdale Lodging Investors, LLC (Omaha, Nebraska Hilton Garden Inn and Scottsdale, Arizona Hilton S-20

OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

(for the nine months ended September 30, 2013)

Garden Inn) at December 31, 2010 and for the year then ended, incorporated by reference herein, have been audited by Baker Tilly Virchow Krause, LLP, independent registered public accounting firm, as set forth in their report thereon, and are incorporated herein by reference in reliance upon such

report given on the authority of such firm as experts in accounting and auditing. The financial statements of the Chicago Hotel Portfolio (Des Plaines, Illinois Hilton Garden Inn and Skokie, Illinois Hampton Inn & Suites) at December 31, 2010 and 2009 and for the years then ended, incorporated by reference herein, have been audited by Warren Averett, LLC (formerly Wilson,

Price, Barranco, Blankenship & Billingsley, P.C.), independent registered public accounting firm, as set forth in their report thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The financial statements of Ascent Hospitality, Inc. (Merrillville, Indiana Hilton Garden Inn) at December 31, 2010 and for the year then ended, incorporated by reference herein, have been audited by Warren Averett, LLC (formerly Wilson, Price, Barranco, Blankenship & Billingsley, P.C.),

independent registered public accounting firm, as set forth in their report thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The financial statements of VHRMR Round Rock, LTD (Austin/Round Rock, Texas Homewood Suites) at December 26, 2010 and for the year then ended, incorporated by reference herein, have been audited by Pannell Kerr Forster of Texas, P.C., independent registered public accounting firm, as

set forth in their report thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The combined financial statements of KRG/White LS Hotel, LLC and Kite Realty/White LS Hotel Operators, LLC (South Bend, Indiana Fairfield Inn & Suites) at December 31, 2010 and for the year then ended, incorporated by reference herein, have been audited by Crowe Horwath LLP,

independent auditor, as set forth in their report thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The financial statements of Fair Oaks Hotel, LLC (Fairfax, Virginia Marriott) at December 31, 2012 and for the year then ended, incorporated by reference herein, have been audited by Dixon Hughes Goodman LLP, independent auditor, as set forth in their report thereon, and are incorporated

herein by reference in reliance upon such report given on the authority of such firm as experts in accounting and auditing. The financial statements of Maple Grove Lodging Investors, LLC, Phoenix Southwest Lodging Investors I, LLC, Deer Valley Lodging Investors, LLC, Deer Valley Hotel Investors II, LLC, Omaha Downtown Lodging Investors III, LLC and Omaha Downtown Lodging Investors IV, LLC (Maple

Grove, Minnesota Hilton Garden Inn; Phoenix, Arizona Courtyard; Phoenix North/Happy Valley, Arizona Hampton Inn & Suites; Phoenix North/Happy Valley, Arizona Homewood Suites; Omaha, Nebraska Homewood Suites and Omaha, Nebraska Hampton Inn & Suites) at December 31, 2012 and for the

year then ended, incorporated by reference herein, have been audited by Baker Tilly Virchow Krause, LLP, independent registered public accounting firm, as set forth in their report thereon, and are incorporated herein by reference in reliance upon such report given on the authority of such firm as

experts in accounting and auditing. S-21

APPLE REIT TEN, INC. INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

Page Financial Statements of Company Apple REIT Ten, Inc. (Audited) Report of Independent Registered Public Accounting Firm

* Consolidated Balance Sheets—December 31, 2012 and 2011

* Consolidated Statements of Operations—Years Ended December 31, 2012 and December 31, 2011 and For the Period August 13, 2010 (initial capitalization) through December 31, 2010

* Consolidated Statements of Shareholders’ Equity—Years Ended December 31, 2012 and December 31, 2011 and For the Period August 13, 2010 (initial capitalization) through December 31, 2010

* Consolidated Statements of Cash Flows—Years Ended December 31, 2012 and December 31, 2011 and For the Period August 13, 2010 (initial capitalization) through December 31, 2010

* Notes to Consolidated Financial Statements

* Financial Statement Schedule

* (Unaudited) Consolidated Balance Sheets—September 30, 2013 and December 31, 2012

* Consolidated Statements of Operations—Three and nine months ended September 30, 2013 and 2012

* Consolidated Statements of Cash Flows—Nine months ended September 30, 2013 and 2012

* Notes to Consolidated Financial Statements

* Financial Statements of Businesses Acquired Denver, Colorado—Hilton Garden Inn (Audited) Report of Independent Auditors

* Balance Sheets—As of December 31, 2010 and 2009

* Statements of Operations—Years Ended December 31, 2010 and 2009

* Statements of Owners’ Equity—Years Ended December 31, 2010 and 2009

* Statements of Cash Flows—Years Ended December 31, 2010 and 2009

* Notes to Financial Statements

* CN Hotel Portfolio (Winston-Salem, North Carolina Hampton Inn & Suites; Matthews, North Carolina Fairfield Inn & Suites; Columbia, South Carolina TownePlace Suites; and Jacksonville, North Carolina Home2 Suites) (Audited) Independent Auditors’ Report

* Combined Balance Sheets—December 31, 2010 and 2009

* Combined Statements of Operations—For the Years Ended December 31, 2010 and 2009

* Combined Statements of Cash Flows—For the Years Ended December 31, 2010 and 2009

* Notes to Combined Financial Statements

* F-1

Page McKibbon Hotel Portfolio (Knoxville, Tennessee SpringHill Suites; Gainesville, Florida Hilton Garden Inn; Richmond, Virginia SpringHill Suites; Pensacola, Florida TownePlace Suites; Mobile, Alabama Hampton Inn & Suites; Knoxville, Tennessee TownePlace Suites; Knoxville, Tennessee Homewood Suites and Gainesville,

Florida Homewood Suites) (Audited) Independent Auditor’s Report

* Combined Balance Sheets—As of December 31, 2010 and 2009

* Combined Statements of Income—For the Years Ended December 31, 2010 and 2009

* Combined Statements of Owner’s (Deficit)—For the Years Ended December 31, 2010 and 2009

* Combined Statements of Cash Flows—For the Years Ended December 31, 2010 and 2009

* Notes to Combined Financial Statements

* (Unaudited) Combined Balance Sheets—As of March 31, 2011 and 2010

* Combined Statements of Income—For the Three Months Ended March 31, 2011 and 2010

* Combined Statements of Owner’s (Deficit)—For the Three Months Ended March 31, 2011 and 2010

* Combined Statements of Cash Flows—For the Three Months Ended March 31, 2011 and 2010

* Hawkeye Hotel Portfolio (Cedar Rapids, Iowa Homewood Suites; Cedar Rapids, Iowa Hampton Inn & Suites and Davenport, Iowa Hampton Inn & Suites) (Audited) Independent Auditors Report

* Combined Balance Sheets—As of December 31, 2010 and 2009

* Combined Statements of Operations—Years Ended December 31, 2010 and 2009

* Combined Statements of Members’ Equity and Accumulated Comprehensive Loss—Years Ended December 31, 2010 and 2009

* Combined Statements of Cash Flows—Years Ended December 31, 2010 and 2009

* Notes to Combined Financial Statements