UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark One)

For the Fiscal Year Ended

OR

For the Transition Period from to

Commission File No.

(Exact name of registrant as specified in its charter)

|

||

(State or other jurisdiction of incorporation or organization) |

|

(IRS Employer Identification No.) |

|

|

|

|

||

(Address of principal executive offices) |

|

(Zip code) |

Registrant’s telephone number, including area code:

Securities registered pursuant to Section 12(b) of the Act:

Title of each class |

Trading Symbol |

Name of each exchange on which registered |

The |

Securities registered pursuant to section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “accelerated filer”, “large accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer |

☐ |

|

Accelerated filer |

☐ |

☒ |

|

Smaller reporting company |

||

|

|

|

Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or

issued its audit report. ☐

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements.

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No

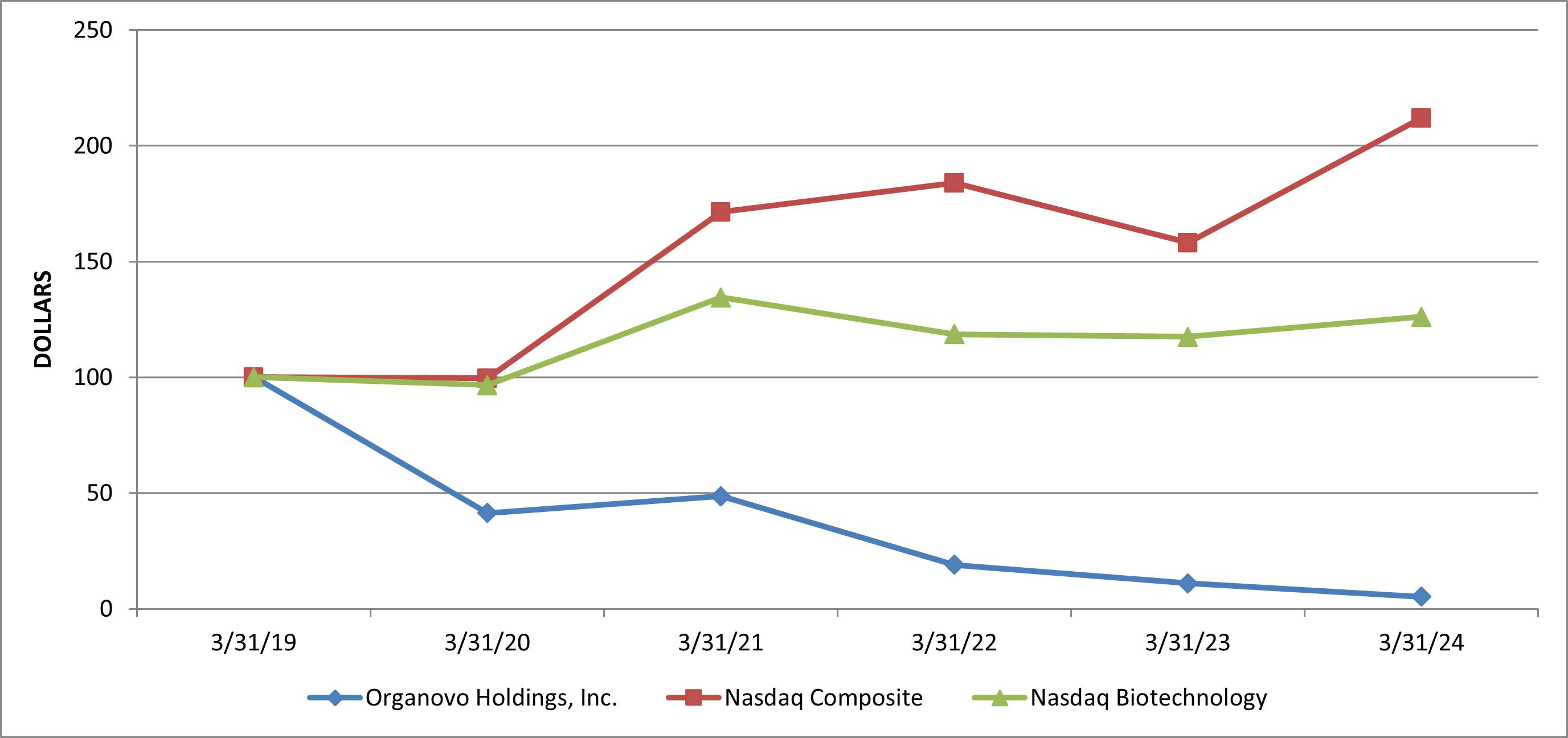

The aggregate market value of the voting and non-voting common equity held by non-affiliates based on the closing stock price as reported on the Nasdaq Capital Market on September 30, 2023, the last trading day of the registrant’s second fiscal quarter, was $

The number of outstanding shares of the registrant’s common stock, as of May 25, 2024 was

DOCUMENTS INCORPORATED BY REFERENCE

Certain information required for Part III of this report is incorporated herein by reference to the definitive proxy statement for the 2024 annual meeting of the registrant’s stockholders, expected to be filed within 120 days of the end of the registrant’s fiscal year.

Auditor Firm Id: |

Auditor Name: |

Auditor Location: |

Organovo Holdings, Inc.

Annual Report on Form 10-K

For the Year Ended March 31, 2024

Table of Contents

|

|

|

|

Page |

|

1 |

|||

|

|

|

|

|

|

|

|

2 |

|

|

|

|

|

|

Item 1. |

|

|

2 |

|

Item 1A. |

|

|

7 |

|

Item 1B. |

|

|

27 |

|

Item 1C. |

|

|

27 |

|

Item 2. |

|

|

27 |

|

Item 3. |

|

|

27 |

|

Item 4. |

|

|

28 |

|

|

|

|

|

|

|

|

|

29 |

|

|

|

|

|

|

Item 5. |

|

|

29 |

|

Item 6. |

|

|

30 |

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

31 |

Item 7A. |

|

|

36 |

|

Item 8. |

|

|

F-1 |

|

Item 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

37 |

Item 9A. |

|

|

37 |

|

Item 9B. |

|

|

37 |

|

Item 9C. |

|

Disclosure Regarding Foreign Jurisdictions that Prevent Inspections |

|

38 |

|

|

|

|

|

|

|

|

39 |

|

|

|

|

|

|

Item 10. |

|

|

39 |

|

Item 11. |

|

|

39 |

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

|

39 |

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

39 |

Item 14. |

|

|

39 |

|

|

|

|

|

|

|

|

|

40 |

|

|

|

|

|

|

Item 15. |

|

|

40 |

|

Important Information Regarding Forward-Looking Statements

Portions of this Annual Report on Form 10-K (including information incorporated by reference) (“Annual Report”) include “forward-looking statements” within the meaning of the safe harbor provisions of the United States Private Securities Litigation Reform Act of 1995, based on our current beliefs, expectations and projections regarding any strategic transaction process; the ability to advance our research and development activities and pursue development of any of our pipeline products; our technology; our product and service development opportunities and timelines; our business strategies; customer acceptance and the market potential of our technology; products and services; our future capital requirements; our future financial performance; and other matters. This includes, in particular, Item 1. “Business” and Item 7. “Management’s Discussion and Analysis of Financial Condition and Results of Operations” of this Annual Report, as well as other portions of this Annual Report. The words “believe,” “expect,” “anticipate,” “project,” “could,” “would,” and similar expressions, among others, generally identify “forward-looking statements,” which speak only as of the date the statements were made. The matters discussed in these forward-looking statements are subject to risks, uncertainties and other factors that could cause our actual results to differ materially from those projected, anticipated or implied in the forward-looking statements. As a result, you should not place undue reliance on any forward-looking statements. The most significant of these risks, uncertainties and other factors are described in Item 1A. “Risk Factors” of this Annual Report. Except to the limited extent required by applicable law, we undertake no obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

1

PART I

Item 1. Business.

Overview

Organovo Holdings, Inc. (“Organovo,” “we,” “us,” “our,” the “Company” and “our Company”) is a clinical stage biotechnology company that is focused on developing FXR314 in inflammatory bowel disease (“IBD”), including ulcerative colitis (“UC”), based on demonstration of clinical promise in three-dimensional (“3D”) human tissues as well as strong preclinical data. FXR is a mediator of gastrointestinal and liver diseases. FXR agonism has been tested in a variety of preclinical models of IBD. FXR314 is the lead compound in our established FXR program containing two clinically tested compounds (including FXR314) and over 2,000 discovery or preclinical compounds. FXR314 is a drug with safety and tolerability after daily oral dosing in Phase 1 and Phase 2 trials. Further, FXR314 has FDA clinical trial authorization for a Phase 2 trial in UC.

Our current clinical focus is in advancing FXR314 in IBD, including UC and Crohn’s disease (“CD”). We plan to start a Phase 2a clinical trial in UC in the calendar year 2024. We released Phase 2 data for FXR314 for the treatment of metabolic function-associated steatohepatitis ("MASH") in April 2024 that are supportive of ongoing development, and we believe FXR314 has a commercial opportunity in MASH, most likely in combination therapy. We are exploring the potential for combination therapies using FXR314 and currently approved mechanisms in preclinical animal studies and our IBD disease models.

Our second focus is building high fidelity, 3D tissues that recapitulate key aspects of human disease. We use our proprietary technology to build functional 3D human tissues that mimic key aspects of native human tissue composition, architecture, function, and disease. We believe these attributes can enable critical complex, multicellular disease models that can be used to develop clinically effective drugs across multiple therapeutic areas.

As with the clinical development program, we are initially focusing on the intestine and have ongoing 3D tissue development efforts in human tissue models of UC and CD. We use these models to identify new molecular targets responsible for driving the disease and to explore the mechanism of action of known drugs including FXR314 and related molecules. We intend to initiate drug discovery programs around these new validated targets to identify drug candidates for partnering and/or internal clinical development.

Our current understanding of intestinal tissue models and IBD disease models leads us to believe that we can create models that provide greater insight into the biology of these diseases than are generally currently available. We are creating high fidelity disease models, leveraging our prior work including the work found in our peer-reviewed publication on bioprinted intestinal tissues (Madden et al. Bioprinted 3D Primary Human Intestinal Tissues Model Aspects of Native Physiology and ADME/Tox Functions. iScience. 2018 Apr 27;2:156-167. doi: 10.1016/j.isci.2018.03.015.) Our advances include cell type-specific compartments, prevalent intercellular tight junctions, and the formation of microvascular structures.

Using these disease models, we intend to identify and validate novel therapeutic targets. After finding therapeutic drug targets, we intend to focus on developing novel small molecule, antibody, or other therapeutic drug candidates to treat the disease, and advance these novel drug candidates towards an Investigational New Drug filing and potential future clinical trials.

We expect to broaden our work into additional therapeutic areas over time and are currently exploring specific tissues for development. In our work to identify the areas of interest, we evaluate areas that might be better served with 3D disease models than currently available models as well as the potential commercial opportunity. In line with these plans, we are building upon both our external and in house scientific expertise, which will be essential to our drug development effort.

Recent Developments

Mosaic Cell Sciences Division

In February 2024, we formed our Mosaic Cell Sciences division (“Mosaic”) to serve as a key source of certain primary human cells we utilize in our research and development efforts. We believe Mosaic can help us optimize our supply chain, reduce operating expenses related to cell sourcing and procurement and ensure that the cellular raw materials we use are of the highest quality and are derived from tissues that are ethically sourced in full compliance with state and federal guidelines. We intend for Mosaic to provide us with qualified human cells for use in our clinical research and development programs. In addition to supplying us with primary human cells, we intend for Mosaic to offer human cells for sale to life science customers, both directly and through distribution partners, which we expect to offset costs and over time become a profit center that offsets overall research and development ("R&D") spending by Organovo.

Best Efforts Public Offering

2

On May 8, 2024, we priced a best efforts public offering (the “Offering”) of: (i) 1,562,500 shares of our common stock and accompanying common warrants (“Common Warrants”) to purchase up to 1,562,500 shares of common stock at a combined public offering price of $0.80 per share and accompanying Common Warrant to purchase one share of common stock and (ii) pre-funded warrants (“Pre-Funded Warrants”) to purchase 5,000,000 shares of common stock and accompanying Common Warrants to purchase up to 5,000,000 shares of common stock at a combined public offering price of $0.799 per Pre-Funded Warrant and accompanying Common Warrant to purchase one share of common stock. In connection with the Offering, we entered into Securities Purchase Agreements with the purchasers of the securities in the Offering on May 8, 2024.

The per share exercise price for the Pre-Funded Warrants is $0.001, subject to adjustment as provided therein. The Pre-Funded Warrants were immediately exercisable, subject to certain beneficial ownership limitations, and will expire when exercised in full. The holders may exercise the Pre-Funded Warrants by means of a “cashless exercise.”

The per share exercise price for the Common Warrants is $0.80, subject to adjustment as provided therein. The Common Warrants were immediately exercisable, subject to certain beneficial ownership limitations, and will expire on the date that is five years following the original issuance date. If a registration statement covering the issuance of the shares of common stock issuable upon exercise of the Common Warrants is not available for the issuance, then the holders may exercise the Common Warrants by means of a “cashless exercise.”

In connection with the Offering, we paid JonesTrading Institutional Services LLC, which acted as the placement agent in connection with the Offering, a cash fee of 5.0% of the aggregate gross proceeds raised in the Offering.

The closing of the Offering occurred on May 13, 2024. We received net proceeds of approximately $4.7 million from the Offering, after deducting the estimated offering expenses payable by us, including the Placement Agent fees.

Our Platform Technology

Our 3D human tissue platform is multifaceted. We approach each tissue agnostic to specific technologies, and intend to apply the best 3D technology to a given disease. We are developing novel disease models using high throughput systems, bioprinted and flow/stretch capable 3D systems as appropriate. Our proprietary NovoGen Bioprinters® and related technologies for preparing bio-inks and bioprinting multicellular tissues with complex architecture are grounded in over a decade of peer-reviewed scientific publications, deriving originally from research led by Dr. Gabor Forgacs, one of our founders and a former George H. Vineyard Professor of Biological Physics at the University of Missouri-Columbia (“MU”). We have a broad portfolio of intellectual property rights covering the principles, enabling instrumentation, applications, tissue constructs and methods of cell-based printing, including exclusive licenses to certain patented and patent pending technologies from MU and Clemson University. We own or exclusively license more than 160 patents and pending applications worldwide covering specific tissue designs, uses, and methods of manufacture.

The NovoGen Bioprinter® Platform

Our NovoGen Bioprinters® are automated devices that enable the fabrication of 3D living tissues comprised of mammalian cells. A custom graphic user interface (“GUI”) facilitates the 3D design and execution of scripts that direct precision movement of multiple dispensing heads to deposit defined cellular building blocks called bio-ink. Bio-ink can be formulated as a 100% cellular composition or as a mixture of cells and other matter (hydrogels, particles). Our NovoGen Bioprinters® can also dispense pure hydrogel formulations, provided the physical properties of the hydrogel are compatible with the dispensing parameters. Most typically, hydrogels are deployed to create void spaces within specific locations in a 3D tissue or to aid in the deposition of specific cell types. We are able to employ a wide variety of proprietary cell- and hydrogel-based bio-inks in the fabrication of tissues. Our NovoGen Bioprinters® also serve as important components of our tissue prototyping and manufacturing platform, as they are able to rapidly and precisely fabricate intricate small-scale tissue models for in vitro use as well as larger-scale tissues suitable for in vivo use.

Generation of bio-ink comprising human cells is the first step in our standard bioprinting. A wide variety of cells and cell-laden hydrogels can be formulated into bio-ink and bioprinted tissues, including cell lines, primary cells, and stem/progenitor cells. The majority of tissue designs employ two or more distinct varieties of bio-ink, usually comprised of cells that represent distinct compartments within a target tissue. For example, a 3D liver tissue might consist of two to three distinct bio-inks that are each made from a single cell type, a combination of cell types, and/or a combination of primary cells and one or more bio-inert hydrogels that serve as physical supports for the bioprinted tissue during its maturation period, or to transiently occupy negative spaces in a tissue design.

Research Collaborations

We continue to collaborate with several academic institutions by providing them with access to our NovoGen Bioprinters® for research purposes, including: Yale School of Medicine, Knight Cancer Institute at Oregon Health & Science University, and the

3

University of Virginia. We believe that the use of our bioprinting platform by major research institutions may help to advance the capabilities of the platform and generate new applications for bioprinted tissues. In prior instances, an academic institution or other third party provided funding to support the academic collaborator’s access to our technology platform. This funding was typically reflected as collaboration revenues in our financial statements. Our academic research collaborations typically involve both parties contributing resources directly to projects. We are not currently generating any revenues from these collaborations.

Intellectual Property

We rely on a combination of patents, trademarks, trade secrets, confidential know-how, copyrights, and a variety of contractual mechanisms such as confidentiality, material transfer, licenses, research collaboration, limited technology access, and invention assignment agreements, to protect our intellectual property. Our intellectual property portfolio for our core technology was initially built through licenses from MU and the Medical University of South Carolina. We subsequently expanded our intellectual property portfolio by filing our own patent and trademark applications worldwide and negotiating additional licenses and purchases.

On an ongoing basis we review and analyze our full intellectual property portfolio to align it with our current business needs, strategies and objectives. Based on that ongoing review, selected patents and patent applications in various countries are or will be abandoned or allowed to lapse. The numbers provided herein are reflective of those changes.

We solely own or hold exclusive licenses to 34 issued U.S. patents and more than 45 issued international patents in foreign jurisdictions including Australia, Canada, China, Denmark, France, Great Britain, Germany, Ireland, Japan, South Korea, Sweden, the Netherlands and Switzerland. We solely or jointly own or hold exclusive licenses to 17 pending U.S. patent applications and more than 5 pending international applications in foreign jurisdictions including Australia, Canada, China, the European Patent Office, Japan and South Korea. These patent families relate to our bioprinting technology and our engineered tissue products and services, including our various uses in areas of tissue creation, in vitro testing, utilization in drug discovery, and in vivo therapeutics.

In connection with the recent acquisition of the FXR program from Metacrine, we acquired the related patent portfolio by way of assignment. This includes filings on the lead candidate, FXR314, and selected filings on the prior candidate (no longer in development), FXR125. With respect to this FXR portfolio, we solely own 7 issued patents and 15 international patents in jurisdictions, including Australia, China, Eurasia, India, Israel, Mexico, Japan and South Africa. We solely own 8 pending U.S. patent applications and more than 50 pending international applications in foreign jurisdictions, including Argentina, Australia, Brazil, Chile, Canada, Eurasia, Europe, Israel, India, Japan, South Korea, Mexico, Philippines, Singapore, South Africa, Hong Kong and Taiwan. These patent families relate to FXR125 and FXR314, including generic coverage, species coverage, methods of use, formulations and polymorph crystals.

In-Licensed Intellectual Property

In 2009 and 2010, we obtained world-wide exclusive licenses to intellectual property owned by MU and the Medical University of South Carolina, which now includes 7 issued U.S. patents, 2 pending U.S. applications and 16 issued international patents. Dr. Gabor Forgacs, one of our founders and a former George H. Vineyard Professor of Biophysics at MU, was one of the co-inventors of all of these works (collectively, the “Forgacs Intellectual Property”). The Forgacs Intellectual Property provides us with intellectual property rights relating to cellular aggregates, the use of cellular aggregates to create engineered tissues, and the use of cellular aggregates to create engineered tissue with no scaffold present. The intellectual property rights derived from the Forgacs Intellectual Property also enables us to utilize our NovoGen Bioprinter® to create engineered tissues.

In 2011, we obtained an exclusive license to a U.S. patent (U.S. Patent No. 7,051,654) owned by the Clemson University Research Foundation that provides us with intellectual property rights relating to methods of using ink-jet printer technology to dispense cells and relating to the creation of matrices of bioprinted cells on gel materials.

In connection with the acquisition of the FXR program from Metacrine in 2023, we were assigned and assumed a license agreement with the Salk Institute for Biological Studies requiring milestone and royalty payments based on the development and commercialization of FXR314.

The patent rights we obtained through these exclusive licenses are not only foundational within the field of 3D bioprinting and FXR agonist therapies but provide us with favorable priority dates. We are required to make ongoing royalty payments under these exclusive licenses based on net sales of products and services that rely on the intellectual property we in-licensed. For additional information regarding our royalty obligations see “Note 6. Collaborative Research, Development, and License Agreements” in the Notes to the Consolidated Financial Statements included in this Annual Report.

4

Company Owned Intellectual Property

In addition to the intellectual property we have in-licensed, we have historically innovated and grown our intellectual property portfolio.

With respect to our bioprinting platform, we have 11 issued U.S. patents and 13 issued foreign patents directed to our NovoGen Bioprinter® and methods of bioprinting: U.S. Patent Nos. 8,931,880; 9,149,952; 9,227,339; 9,315,043; 9,499,779; 9,855,369; 10,174,276, 10,967,560, 11,577,450, 11,577,451 and 11,413,805 ; Australia Patent Nos. 2015202836, and 2014296246; Canada Patent No. 2,812,766; China Patent Nos. ZL201180050831.4 and ZL201480054148.1; European Patent Nos. 2838985, 2629975, and 3028042; Japan Patent Nos. 6333231, 6566426 and 6842918, and Russian Patent No. 2560393. These issued patents and pending patent applications carry remaining patent terms ranging from over 20 years to just over 7 years. We have additional U.S. continuation applications pending in these families as well foreign counterpart applications in multiple countries.

Our ExVive™ Human Liver Tissue is protected by U.S. Patent Nos. 9,222,932, 9,442,105, 10,400,219 and 11,127,774; Australia Patent Nos. 2014236780 and 2017200691; and Canada Patent No. 2,903,844. Our ExVive™ Human Kidney Tissue is protected by U.S. Patent Nos. 9,481,868, 10,094,821 and 10,962,526; Australian Patent No. 2015328173, Canadian Patent No. 2,962,778, European Patent No. 3204488 and Japan Patent No. 7021177. These issued patents and pending patent applications carry remaining patent terms ranging from over 11 years to just over 9 years. We have additional U.S. patent applications pending in these families, as well as foreign counterpart applications in multiple countries. We currently have pending numerous patent applications in the U.S. and globally that are directed to additional features on bioprinters, additional tissue types, their methods of fabrication, and specific applications.

Our U.S. Patent Nos. 9,855,369 and 9,149,952, which relate to our bioprinter technology, were the subject of IPR proceedings filed by Cellink AB and its subsidiaries (collectively, “BICO Group AB”), one of our competitors. Likewise, U.S. Patent Nos. 9,149,952, 9,855,369, 8,931,880, 9,227,339, 9,315,043 and 10,967,560 (all assigned to Organovo, Inc.) and U.S. Patent Nos. 7,051,654, 8,241,905, 8,852,932 and 9,752,116 (assigned to Clemson University and the University of Missouri, respectively) were implicated in a declaratory judgment complaint filed against Organovo, Inc., our wholly owned subsidiary, by BICO Group AB and certain of its subsidiaries in the United States District Court for the District of Delaware. All of these matters have since been settled in a favorable manner for the Company. Specifically, on February 23, 2022, we announced an agreement of a non-exclusive license for BICO Group AB and its affiliate companies to Organovo’s foundational patent portfolio in 3D bioprinting. For more information regarding these proceedings, see the section titled Part I, Item 3 of this Annual Report on Form 10-K.

With respect to our FXR agonist program covering FXR314 and FXR125, we have 7 issued U.S. patents and 15 issued foreign patents directed to composition of matter protection (generic and specific) for FXR314 and FXR125, as well claims directed to methods of treatment of GI diseases, formulations of FXR314 and polymorphs of the FXR314 molecule including United States Patent Nos.11,214,538, 10,703,712, 10,927,082, 10,961,198, 11,236,071 and 11,084,817, granted Australian Patent Nos. 2016323992 and 2018236275, Chinese Patent Nos. 201680066917 and 269065, Eurasian Patent Nos. 040003 and 040704, Israeli Patent Nos. 258011, 296068 and 296065, Indian Patent No. 380510, Japanese Patent Nos. 6905530 and 717709, Mexican Patent Nos. 386,752 and 397265 and South African Patent No. 2018/01750. In addition, we have 8 pending U.S. patent applications and over 50 pending foreign patent applications, including U.S. Patent Application Nos. 18/156,069, 18/174,393, 17/349,757, 17/906,580, 17/906,582 and 17/906,585 and over 50 pending international patent applications in a number of countries including, Australia, Brazil, Canada, Chile, China, the Eurasian Patent Office, the European Patent Office, Israel, India, Japan, South Korea, Mexico, Singapore, Philippines and Hong Kong. These issued patents and pending patent applications carry remaining patent terms ranging from over 18 years to just over 15 years.

Employees and Human Capital

As of May 1, 2024, we had 20 employees, of which 12 are full-time. We have also retained some of our former employees as consultants, in addition to a number of expert consultants in specific scientific and operational areas. Our employees are not represented by labor unions or covered under any collective bargaining agreements. We consider our relationship with our employees to be good.

Our human capital resources objectives include, as applicable, identifying, recruiting, retaining, incentivizing and integrating our existing and additional employees. The principal purposes of our equity incentive plans are to attract, retain and motivate selected employees, consultants, and directors through the granting of equity-based compensation awards.

5

Corporate Information

We are operating the business of our subsidiaries, including Organovo, Inc., our wholly-owned subsidiary, which we acquired in February 2012. Organovo, Inc. was incorporated in Delaware in April 2007. Our common stock has traded on The Nasdaq Stock Market LLC under the symbol “ONVO” since August 8, 2016 and our common stock currently trades on the Nasdaq Capital Market. Prior to that time, it traded on the NYSE MKT under the symbol “ONVO” and prior to that was quoted on the OTC Market.

Our principal executive offices are located at 11555 Sorrento Valley Rd, Suite 100, San Diego CA 92121 and our phone number is (858) 224-1000. Our Internet website can be found at http://www.organovo.com. The content of our website is not intended to be incorporated by reference into this Annual Report or in any other report or document that we file.

Available Information

Our investor relations website is located at http://ir.organovo.com. We are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Reports filed with the Securities and Exchange Commission (the “SEC”) pursuant to the Exchange Act, including annual and quarterly reports, and other reports we file, are available free of charge, through our website. The content of our website is not intended to be incorporated by reference into this Annual Report or in any other report or document that we file. We make them available on our website as soon as reasonably possible after we file them with the SEC. The reports we file with the SEC are also available on the SEC’s website (http://www.sec.gov).

6

Item 1A. Risk Factors.

Investment in our common stock involves a substantial degree of risk and should be regarded as speculative. As a result, the purchase of our common stock should be considered only by persons who can reasonably afford to lose their entire investment. Before you elect to purchase our common stock, you should carefully consider the risk and uncertainties described below in addition to the other information incorporated herein by reference. Additional risks and uncertainties of which we are unaware or which we currently believe are immaterial could also materially adversely affect our business, financial condition or results of operations. If any of the risks or uncertainties discussed in this Annual Report occur, our business, prospects, liquidity, financial condition and results of operations could be materially and adversely affected, in which case the trading price of our common stock could decline, and you could lose all or part of your investment.

Risk Factor Summary

Below is a summary of the principal factors that make an investment in our common stock speculative or risky. This summary does not address all of the risks that we face. Additional discussion of the risks summarized in this risk factor summary, and other risks that we face, can be found below and should be carefully considered, together with other information in this Annual Report on Form 10-K and our other filings with the Securities and Exchange Commission before making investment decisions regarding our common stock.

7

Risks Related to our Business

We are a clinical stage biotechnology company focusing on clinical drug development of the farnesoid X receptor (“FXR”) agonist FXR314, which involves a substantial degree of uncertainty, and on 3D bioprinting technology to develop human tissues and disease models for drug discovery and development, which is an unproven business strategy that may never achieve profitability.

We are a clinical stage biotechnology company that is focused on developing FXR314 in inflammatory bowel disease ("IBD"), including ulcerative colitis ("UC"), based on demonstration of clinical promise in three-dimensional ("3D") human tissues as well as strong preclinical data. Our current clinical focus is in advancing FXR314 in IBD, including UC and Crohn's disease. Our secondary focus is building high fidelity, 3D tissues that recapitulate key aspects of human disease. Our success will depend upon our ability to advance the development of FXR314, our ability to determine the appropriate clinical focus for FXR314, our ability to identify additional drug candidates to pursue and the viability of our platform technology and any disease models we develop. Our success will also depend on our ability to select an appropriate development strategy for FXR314 and any other drug candidates we may identify, including internal development or partnering or licensing arrangements with pharmaceutical companies. We may not be able to partner or license our drug candidates. We may never achieve profitability, or even if we achieve profitability, we may not be able to maintain or increase our profitability.

We will incur substantial additional operating losses over the next several years as our research and development activities increase.

We will incur substantial additional operating losses over the next several years as our research and development activities increase. The amount of future losses and when, if ever, we will achieve profitability are uncertain. Our ability to generate revenue and achieve profitability will depend on, among other things:

We might not succeed at any of these undertakings. If we are unsuccessful at one or more of these undertakings, our business, prospects, and results of operations will be materially adversely affected.

Using our platform technology to develop human tissues and disease models for drug discovery and development is new and unproven.

Utilizing our 3D bioprinting platform technology to develop human tissues and disease models for drug discovery and development will involve new and unproven technologies, disease models and approaches, each of which is subject to the risk associated with new and evolving technologies. To date, we have not identified or developed any drug candidates utilizing our new business model. Our future success will depend on our ability to utilize our 3D bioprinting platform to develop human tissues and disease models that will enable us to identify and develop viable drug candidates. We may experience unforeseen technical complications, unrecognized defects and limitations in our technology or our ability to develop disease models or identify viable drug candidates. These complications could materially delay or substantially increase the anticipated costs and time to identify and develop viable drug candidates, which would have a material adverse effect on our business and financial condition and our ability to continue operations.

8

We will face intense competition in our drug discovery efforts.

The biotechnology and pharmaceutical industry is subject to intense competition and rapid and significant technological change. There are many potential competitors for the disease indications we may pursue, including major drug companies, specialized biotechnology firms, academic institutions, government agencies and private and public research institutions. Many of these competitors have significantly greater financial and technical resources, experience and expertise in the following areas than we have, including:

Principal competitive factors in our industry include: the quality, scientific and technical support, management and the execution of drug development and regulatory approval strategies; skill and experience of employees, including the ability to recruit and retain skilled, experienced employees; intellectual property portfolio; range of capabilities, including drug identification, development and regulatory approval; and the availability of substantial capital resources to fund these activities.

In order to effectively compete, we may need to make substantial investments in our research and technology development, drug candidate identification and development, testing and regulatory approval and licensing and business development activities. There is no assurance that we will be successful in discovering effective drug candidates using our 3D bioprinted tissues or disease models. Our technologies and drug development plans also may be rendered obsolete or noncompetitive as a result of drugs, intellectual property, technologies, products and services introduced by competitors. Any of these risks may prevent us from building a successful drug discovery business or entering into a strategic partnership or collaboration related to, any drug candidates we identify on favorable terms, or at all.

As we pursue drug development through 3D tissues and disease models, we will require access to a constant, steady, reliable supply of human cells to support our development activities.

As we pursue drug development through 3D tissues and disease models, we will require access to a constant, steady, reliable supply of human cells to support our 3D tissue development activities. We purchase human cells from selected third-party suppliers based on quality assurance, cost effectiveness, and regulatory requirements. We need to continue to identify additional sources of qualified human cells and there can be no guarantee that we will be able to access the quantity and quality of raw materials needed at a cost-effective price. Any failure to obtain a reliable supply of sufficient human cells or a supply at cost effective prices would harm our business and our results of operations and could cause us to be unable to support our drug development efforts.

We may not be successful in establishing our Mosaic Cell Sciences division (“Mosaic”) as a profitable commercial business.

We formed Mosaic to serve as a key source of certain of the primary human cells we utilize in our research and development efforts. In addition to supplying human cells for our business requirements, we believe there is an opportunity for Mosaic to operate as a commercial business by selling human cells to other pharmaceutical, biotech and research organizations. We intend for Mosaic to begin selling its human cell offerings to end users both directly and through distribution partners during fiscal 2025. Operating and developing Mosaic’s business is subject to a number of risks and uncertainties, including:

9

If any of these or any other risks and uncertainties occur, our efforts to establish Mosaic as a commercial business may be unsuccessful, which would harm our business and results of operations.

Our business will be adversely impacted if we are unable to successfully attract, hire and integrate key additional employees or contractors.

Our future success depends in part on our ability to successfully attract and then retain key additional executive officers and other key employees and contractors to support our drug discovery plans. Recruiting and retaining qualified scientific and clinical personnel is critical to our success. Competition to hire qualified personnel in our industry is intense, and we may be unable to hire, train, retain or motivate these key personnel on acceptable terms given the competition among numerous pharmaceutical and biotechnology companies for similar personnel. If we are unable to attract and retain high quality personnel, our ability to pursue our drug discovery business will be limited, and our business, prospects, financial condition, and results of operations may be adversely affected.

We may require substantial additional funding. Raising additional capital would cause dilution to our existing stockholders and may restrict our operations or require us to relinquish rights to our technologies or to a product candidate.

We currently do not have any committed external source of funds and do not expect to generate any meaningful revenue in the foreseeable future. If our board of directors decides that we should pursue further research and development activities than already proposed, we will require substantial additional funding to operate our proposed business, including expanding our facilities and hiring additional qualified personnel, and we would expect to finance these cash needs through a combination of equity offerings, debt financings, government or other third-party funding and licensing or collaboration arrangements.

To the extent that we raise additional capital through the sale of equity or convertible debt, the ownership interests of our stockholders will be diluted. In addition, the terms of any equity or convertible debt we agree to issue may include liquidation or other preferences that adversely affect the rights of our stockholders. Convertible debt financing, if available, may involve agreements that include covenants limiting or restricting our ability to take specific actions, such as incurring additional debt, making capital expenditures, and declaring dividends, and may impose limitations on our ability to acquire, sell or license intellectual property rights and other operating restrictions that could adversely impact our ability to conduct our business. Moreover, we have the ability to sell up to $0.8 million of additional shares of our common stock to the public through an “at the market offering” pursuant to a Sales Agreement that we entered into with H.C. Wainwright & Co., LLC and JonesTrading Institutional Services LLC on March 16, 2018 (the “Sales Agreement”). Any shares of common stock issued in the “at the market offering” (“ATM offering”) will result in dilution to our existing stockholders.

We currently have an effective shelf registration statement on Form S-3 filed with the Securities and Exchange Commission (the “SEC”), which we may use to offer from time to time any combination of debt securities, common and preferred stock and warrants. On March 16, 2018, we entered into the Sales Agreement pursuant to which we have the ability to sell shares of our common stock to the public through an ATM offering. As of March 31, 2024, we have issued and sold pursuant to the Sales Agreement an aggregate of 5,371,418 shares of our common stock for gross proceeds of approximately $46.9 million. However, in the event that the aggregate market value of our common stock held by non-affiliates (“public float”) is less than $75.0 million, the amount we can raise through primary public offerings of securities, including sales under the Sales Agreement, in any twelve-month period using shelf registration statements is limited to an aggregate of one-third of our public float. As of May 15, 2024, our public float was less than $75.0 million, and therefore we are limited to an aggregate of one-third of our public float in the amount we could raise through primary public offerings of securities in any twelve-month period using shelf registration statements, or $2,474,091. Although we would still maintain the ability to raise funds through other means, such as through the filing of a registration statement on Form S-1 or in private placements, the rules and regulations of the SEC or any other regulatory agencies may restrict our ability to conduct certain types of financing activities, or may affect the timing of and amounts we can raise by undertaking such activities.

Further, additional funds may not be available when we need them on terms that are acceptable to us, or at all. If adequate funds are not available to us on a timely basis, we may be required to curtail or cease our operations. Raising additional funding through debt or equity financing is likely to be difficult or unavailable altogether given the early stage of our technology and any drug candidates we identify. Furthermore, the issuance of additional securities, whether equity or debt, by us, or the possibility of such issuance, may cause the market price of our common stock to decline further and existing stockholders may not agree with our financing plans or the terms of such financings.

10

Clinical drug development involves a lengthy and expensive process with uncertain timelines and uncertain outcomes, and results of earlier studies and trials may not be predictive of future results.

Before obtaining marketing approval from regulatory authorities for the sale of any drug candidates we identify, any such drug candidates must undergo extensive clinical trials to demonstrate the safety and efficacy of the drug candidates in humans. Human clinical testing is expensive and can take many years to complete, and we cannot be certain that any clinical trials will be conducted as planned or completed on schedule, if at all. We may elect to complete this testing, or some portion thereof, internally or enter into a partnering or development agreement with a pharmaceutical company to complete these trials. Our inability, or the inability of any third party with whom we enter into a partnering or development agreement, to successfully complete preclinical and clinical development could result in additional costs to us and negatively impact our ability to generate revenues or receive development or milestone payments. Our future success is dependent on our ability, or the ability of any pharmaceutical company with whom we enter into a partnering or development agreement, to successfully develop, obtain regulatory approval for, and then successfully commercialize any drug candidates we identify.

Any drug candidates we identify will require additional clinical development, management of clinical, preclinical and manufacturing activities, regulatory approval in applicable jurisdictions, achieving and maintaining commercial-scale supply, building of a commercial organization, substantial investment and significant marketing efforts. We are not permitted to market or promote any of our drug candidates before we receive regulatory approval from the U.S. Food and Drug Administration (“FDA”) or comparable foreign regulatory authorities, and we may never receive such regulatory approval for any of our drug candidates.

We, or any third party with whom we enter into a partnering or development agreement, may experience numerous unforeseen events during, or as a result of, clinical trials that could delay or prevent our ability to earn development or milestone payments or for any drug candidates to obtain regulatory approval, including:

If we, or any third party with whom we enter into a partnering or development agreement, experience delays in the completion of, or termination of, any clinical trial of any drug candidates that we develop, or are unable to achieve clinical endpoints due to unforeseen events, the commercial prospects of our drug candidates will be harmed, and our ability to develop milestones, development fees or product revenues from any of these drug candidates will be delayed.

We may expend our limited resources to pursue a particular product candidate or indication and fail to capitalize on product candidates or indications that may be more profitable or for which there is a greater likelihood of success.

Because we have limited financial and managerial resources, we focus on research programs and product candidates that we identify for specific indications among many potential options. As a result, we may forego or delay pursuit of opportunities with other product candidates or for other indications that later prove to have greater commercial potential. Currently, we are focused on developing FXR314 in IBD, including UC, based on demonstration of clinical promise in 3D human tissues as well as strong preclinical data. Our resource allocation decisions may cause us to fail to capitalize on viable commercial medicines or profitable market opportunities. Our

11

projections of both the number of people who have these diseases, as well as the subset of people with these diseases who have the potential to benefit from treatment with our product candidates, are based on estimates. If any of our estimates are inaccurate, the market opportunities for any of our product candidates could be significantly diminished and have an adverse material impact on our business. Additionally, the potentially addressable patient population for our product candidates may be limited, or may not be amenable to treatment with our product candidates. Our spending on current and future research and development programs and product candidates for specific indications may not yield any commercially viable product candidates. If we do not accurately evaluate the commercial potential or target market for a particular product candidate, we may relinquish valuable rights to that product candidate through collaboration, licensing, or other royalty arrangements in cases in which it would have been more advantageous for us to retain sole development and commercialization rights to such product candidate. Any such event could have a material adverse effect on our business, financial condition, results of operations and prospects.

We will rely upon third-party contractors and service providers for the execution of critical aspects of any future development programs. Failure of these collaborators to provide services of a suitable quality and within acceptable timeframes may cause the delay or failure of any future development programs.

We plan to outsource certain functions, tests and services to CROs, medical institutions and collaborators as well as outsource manufacturing to collaborators and/or contract manufacturers, and we will rely on third parties for quality assurance, clinical monitoring, clinical data management and regulatory expertise. We may elect, in the future, to engage a CRO to run all aspects of a clinical trial on our behalf. There is no assurance that such individuals or organizations will be able to provide the functions, tests, biologic supply or services as agreed upon or in a quality fashion and we could suffer significant delays in the development of our drug candidates or development programs.

In some cases, there may be only one or few providers of such services, including clinical data management or manufacturing services. In addition, the cost of such services could be significantly increased over time. We may rely on third parties and collaborators to enroll qualified patients and conduct, supervise and monitor our clinical trials. Our reliance on these third parties and collaborators for clinical development activities reduces our control over these activities. Our reliance on these parties, however, does not relieve us of our regulatory responsibilities, including ensuring that our clinical trials are conducted in accordance with Good Clinical Practice (“GCP”) regulations and the investigational plan and protocols contained in the regulatory agency applications. In addition, these third parties may not complete activities on schedule or may not manufacture under Current Good Manufacturing Practice (“cGMP”) conditions. Preclinical or clinical studies may not be performed or completed in accordance with Good Laboratory Practices (“GLP”) regulatory requirements or our trial design. If these third parties or collaborators do not successfully carry out their contractual duties or meet expected deadlines, obtaining regulatory approval for manufacturing and commercialization of our drug candidates may be delayed or prevented. We may rely substantially on third-party data managers for our clinical trial data. There is no assurance that these third parties will not make errors in the design, management or retention of our data or data systems. There is no assurance these third parties will pass FDA or regulatory audits, which could delay or prohibit regulatory approval.

In addition, we will exercise limited control over our third-party partners and vendors, which makes us vulnerable to any errors, interruptions or delays in their operations. If these third parties experience any service disruptions, financial distress or other business disruption, or difficulties meeting our requirements or standards, it could make it difficult for us to operate some aspects of our business.

The near and long-term viability of our drug discovery and development efforts will depend on our ability to successfully establish strategic relationships.

The near and long-term viability of our drug discovery and development efforts depend in part on our ability to successfully establish new strategic partnering, collaboration and licensing arrangements with biotechnology companies, pharmaceutical companies, universities, hospitals, insurance companies and or government agencies. Establishing strategic relationships is difficult and time-consuming. Potential partners and collaborators may not enter into relationships with us based upon their assessment of our technology or drug candidates or our financial, regulatory or intellectual property position. If we fail to establish a sufficient number of strategic relationships on acceptable terms, we may not be able to develop and obtain regulatory approval for our drug candidates or generate sufficient revenue to fund further research and development efforts. Even if we establish new strategic relationships, these relationships may never result in the successful development or regulatory approval for any drug candidates we identify for a number of reasons both within and outside of our control.

Investors’ expectations of our performance relating to environmental, social and governance factors may impose additional costs and expose us to new risks.

There is an increasing focus from certain investors, employees, regulators and other stakeholders concerning corporate responsibility, specifically related to environmental, social and governance (“ESG”) factors. Some investors and investor advocacy groups may use

12

these factors to guide investment strategies and, in some cases, investors may choose not to invest in our company if they believe our policies relating to corporate responsibility are inadequate. Third-party providers of corporate responsibility ratings and reports on companies have increased to meet growing investor demand for measurement of corporate responsibility performance, and a variety of organizations currently measure the performance of companies on such ESG topics, and the results of these assessments are widely publicized. Investors, particularly institutional investors, use these ratings to benchmark companies against their peers and if we are perceived as lagging with respect to ESG initiatives, certain investors may engage with us to improve ESG disclosures or performance and may also make voting decisions, or take other actions, to hold us and our board of directors accountable. In addition, the criteria by which our corporate responsibility practices are assessed may change, which could result in greater expectations of us and cause us to undertake costly initiatives to satisfy such new criteria. If we elect not to or are unable to satisfy such new criteria, investors may conclude that our policies with respect to corporate responsibility are inadequate. We may face reputational damage in the event that our corporate responsibility procedures or standards do not meet the standards set by various constituencies.

We may face reputational damage in the event our corporate responsibility initiatives or objectives do not meet the standards set by our investors, stockholders, lawmakers, listing exchanges or other constituencies, or if we are unable to achieve an acceptable ESG or sustainability rating from third-party rating services. A low ESG or sustainability rating by a third-party rating service could also result in the exclusion of our common stock from consideration by certain investors who may elect to invest with our competition instead. Ongoing focus on corporate responsibility matters by investors and other parties as described above may impose additional costs or expose us to new risks. Any failure or perceived failure by us in this regard could have a material adverse effect on our reputation and on our business, share price, financial condition, or results of operations, including the sustainability of our business over time.

Unstable market and economic conditions may have serious adverse consequences on our business, financial condition and share price.

Our business, financial condition and share price could be adversely affected by general conditions in the global economy and in the global financial markets. As widely reported, in the past several years, global credit and financial markets have experienced volatility and disruptions, and especially in 2020, 2021 and 2022 due to the impacts of the COVID-19 pandemic, and, more recently, the ongoing conflict between Ukraine and Russia and the global impact of restrictions and sanctions imposed on Russia, including, for example, severely diminished liquidity and credit availability, declines in consumer confidence, declines in economic growth, increases in unemployment rates and uncertainty about economic stability. Moreover, the global impacts of the Israel-Hamas war are still unknown. There can be no assurances that further deterioration in credit and financial markets and confidence in economic conditions will not occur. For example, U.S. debt ceiling and budget deficit concerns have increased the possibility of additional credit-rating downgrades and economic slowdowns, or a recession in the United States. Although U.S. lawmakers passed legislation to raise the federal debt ceiling on multiple occasions, including a suspension of the federal debt ceiling in June 2023, ratings agencies have lowered or threatened to lower the long-term sovereign credit rating on the United States. The impact of this or any further downgrades to the U.S. government’s sovereign credit rating or its perceived creditworthiness could adversely affect the U.S. and global financial markets and economic conditions. Absent further quantitative easing by the Federal Reserve, these developments could cause interest rates and borrowing costs to rise, which may negatively impact our results of operations or financial condition.

Our general business strategy may be adversely affected by any such economic downturn, volatile business environment or continued unpredictable and unstable market conditions. If the current equity and credit markets deteriorate, it may make any necessary debt or equity financing more difficult, more costly and more dilutive. Failure to secure any necessary financing in a timely manner and on favorable terms could have a material adverse effect on our growth strategy, financial performance and share price and could require us to delay or abandon clinical development plans. Any of the foregoing could harm our business and we cannot anticipate all of the ways in which the current economic climate and financial market conditions could adversely impact our business.

The impact of the Russian invasion of Ukraine and the Israel-Hamas war on the global economy, energy supplies and raw materials is uncertain, but may prove to negatively impact our business and operations.

The short and long-term implications of Russia’s invasion of Ukraine and the Israel-Hamas war are difficult to predict at this time. We continue to monitor any adverse impact that the outbreak of war in Ukraine and the subsequent institution of sanctions against Russia by the United States and several European and Asian countries, and the Israel-Hamas war may have on the global economy in general, on our business and operations and on the businesses and operations of our suppliers and other third parties with which we conduct business. For example, a prolonged conflict in Ukraine or Israel may result in increased inflation, escalating energy prices and constrained availability, and thus increasing costs, of raw materials. We will continue to monitor this fluid situation and develop contingency plans as necessary to address any disruptions to our business operations as they develop. To the extent the wars in Ukraine or Israel may adversely affect our business as discussed above, they may also have the effect of heightening many of the other risks described herein. Such risks include, but are not limited to, adverse effects on macroeconomic conditions, including inflation; disruptions to our technology infrastructure, including through cyberattack, ransom attack, or cyber-intrusion; adverse changes in

13

international trade policies and relations; disruptions in global supply chains; and constraints, volatility, or disruption in the capital markets, any of which could negatively affect our business and financial condition.

Risks Related to Government Regulation

In the past, we have used hazardous chemicals, biological materials and infectious agents in our business. Any claims relating to improper handling, storage or disposal of these materials could be time consuming and costly.

Our product manufacturing, research and development, and testing activities have involved the controlled use of hazardous materials, including chemicals, biological materials and infectious disease agents. We cannot eliminate the risks of accidental contamination or the accidental spread or discharge of these materials, or any resulting injury from such an event. We may be sued for any injury or contamination that results from our use or the use by third parties of these materials, and our liability may exceed our insurance coverage and our total assets. Federal, state and local laws and regulations govern the use, manufacture, storage, handling and disposal of these hazardous materials and specified waste products, as well as the discharge of pollutants into the environment and human health and safety matters. We were also subject to various laws and regulations relating to safe working conditions, laboratory and manufacturing practices, and the experimental use of animals. Our operations may have required that environmental permits and approvals be issued by applicable government agencies. If we failed to comply with these requirements, we could incur substantial costs, including civil or criminal fines and penalties, clean-up costs or capital expenditures for control equipment or operational changes necessary to achieve and maintain compliance.

If we fail to obtain and sustain an adequate level of reimbursement for our potential products by third-party payors, potential future sales would be materially adversely affected.

There will be no viable commercial market for our drug candidates, if approved, without reimbursement from third-party payors. Reimbursement policies may be affected by future healthcare reform measures. We cannot be certain that reimbursement will be available for our current drug candidates or any other drug candidate we may develop. Additionally, even if there is a viable commercial market, if the level of reimbursement is below our expectations, our anticipated revenue and gross margins will be adversely affected.

Third-party payors, such as government or private healthcare insurers, carefully review and increasingly question and challenge the coverage of and the prices charged for drugs. Reimbursement rates from private health insurance companies vary depending on the Company, the insurance plan and other factors. Reimbursement rates may be based on reimbursement levels already set for lower cost drugs and may be incorporated into existing payments for other services. There is a current trend in the U.S. healthcare industry toward cost containment.

Large public and private payors, managed care organizations, group purchasing organizations and similar organizations are exerting increasing influence on decisions regarding the use of, and reimbursement levels for, particular treatments. Such third-party payors, including Medicare, may question the coverage of, and challenge the prices charged for, medical products and services, and many third-party payors limit coverage of or reimbursement for newly approved healthcare products. In particular, third-party payors may limit the covered indications. Cost-control initiatives could decrease the price we might establish for products, which could result in product revenues being lower than anticipated. We believe our drugs will be priced significantly higher than existing generic drugs and consistent with current branded drugs. If we are unable to show a significant benefit relative to existing generic drugs, Medicare, Medicaid and private payors may not be willing to provide reimbursement for our drugs, which would significantly reduce the likelihood of our products gaining market acceptance.

We expect that private insurers will consider the efficacy, cost-effectiveness, safety and tolerability of our potential products in determining whether to approve reimbursement for such products and at what level. Obtaining these approvals can be a time consuming and expensive process. Our business, financial condition and results of operations would be materially adversely affected if we do not receive approval for reimbursement of our potential products from private insurers on a timely or satisfactory basis. Limitations on coverage could also be imposed at the local Medicare carrier level or by fiscal intermediaries. Medicare Part D, which provides a pharmacy benefit to Medicare patients as discussed below, does not require participating prescription drug plans to cover all drugs within a class of products. Our business, financial condition and results of operations could be materially adversely affected if Part D prescription drug plans were to limit access to, or deny or limit reimbursement of, our drug candidates or other potential products.

Reimbursement systems in international markets vary significantly by country and by region, and reimbursement approvals must be obtained on a country-by-country basis. In many countries, the product cannot be commercially launched until reimbursement is approved. In some foreign markets, prescription pharmaceutical pricing remains subject to continuing governmental control even after initial approval is granted. The negotiation process in some countries can exceed 12 months. To obtain reimbursement or pricing

14

approval in some countries, we may be required to conduct a clinical trial that compares the cost-effectiveness of our products to other available therapies.

If the prices for our potential products are reduced or if governmental and other third-party payors do not provide adequate coverage and reimbursement of our drugs, our future revenue, cash flows and prospects for profitability will suffer.

Current and future legislation may increase the difficulty and cost of commercializing our drug candidates and may affect the prices we may obtain if our drug candidates are approved for commercialization.

In the U.S. and some foreign jurisdictions, there have been a number of adopted and proposed legislative and regulatory changes regarding the healthcare system that could prevent or delay regulatory approval of our drug candidates, restrict or regulate post-marketing activities and affect our ability to profitably sell any of our drug candidates for which we obtain regulatory approval.

In the U.S., the Medicare Prescription Drug, Improvement, and Modernization Act of 2003 (“MMA”) changed the way Medicare covers and pays for pharmaceutical products. Cost reduction initiatives and other provisions of this legislation could limit the coverage and reimbursement rate that we receive for any of our approved products. While the MMA only applies to drug benefits for Medicare beneficiaries, private payors often follow Medicare coverage policy and payment limitations in setting their own reimbursement rates. Therefore, any reduction in reimbursement that results from the MMA may result in a similar reduction in payments from private payors.

In addition, on August 16, 2022, President Biden signed into law the Inflation Reduction Act of 2022, which, among other things, includes policies that are designed to have a direct impact on drug prices and reduce drug spending by the federal government, which shall take effect in 2023. Under the Inflation Reduction Act of 2022, Congress authorized Medicare beginning in 2026 to negotiate lower prices for certain costly single-source drug and biologic products that do not have competing generics or biosimilars. This provision is limited in terms of the number of pharmaceuticals whose prices can be negotiated in any given year and it only applies to drug products that have been approved for at least 9 years and biologics that have been licensed for 13 years. Drugs and biologics that have been approved for a single rare disease or condition are categorically excluded from price negotiation. Further, the new legislation provides that if pharmaceutical companies raise prices in Medicare faster than the rate of inflation, they must pay rebates back to the government for the difference. The new law also caps Medicare out-of-pocket drug costs at an estimated $4,000 a year in 2024 and, thereafter beginning in 2025, at $2,000 a year.

In March 2010, the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act of 2010 (collectively the “PPACA”), was enacted. The PPACA was intended to broaden access to health insurance, reduce or constrain the growth of healthcare spending, enhance remedies against healthcare fraud and abuse, add new transparency requirements for healthcare and health insurance industries, impose new taxes and fees on the health industry and impose additional health policy reforms. The PPACA increased manufacturers’ rebate liability under the Medicaid Drug Rebate Program by increasing the minimum rebate amount for both branded and generic drugs and revised the definition of “average manufacturer price”, which may also increase the amount of Medicaid drug rebates manufacturers are required to pay to states. The legislation also expanded Medicaid drug rebates and created an alternative rebate formula for certain new formulations of certain existing products that is intended to increase the rebates due on those drugs. The Centers for Medicare & Medicaid Services (“CMS”), which administers the Medicaid Drug Rebate Program, also has proposed to expand Medicaid rebates to the utilization that occurs in the territories of the U.S., such as Puerto Rico and the Virgin Islands. Further, beginning in 2011, the PPACA imposed a significant annual fee on companies that manufacture or import branded prescription drug products and required manufacturers to provide a 50% discount off the negotiated price of prescriptions filled by beneficiaries in the Medicare Part D coverage gap, referred to as the “donut hole.” Legislative and regulatory proposals have been introduced at both the state and federal level to expand post-approval requirements and restrict sales and promotional activities for pharmaceutical products.

There have been public announcements by members of the U.S. Congress, regarding plans to repeal and replace the PPACA and Medicare. For example, on December 22, 2017, President Trump signed into law the Tax Cuts and Jobs Act of 2017, which, among other things, eliminated the individual mandate requiring most Americans (other than those who qualify for a hardship exemption) to carry a minimum level of health coverage, effective January 1, 2019. On December 14, 2018, a U.S. District Court Judge in the Northern District of Texas, or the Texas District Court Judge, ruled that the individual mandate is a critical and inseverable feature of the PPACA, and therefore, because it was repealed as part of the Tax Cuts and Jobs Act of 2017, the remaining provisions of the PPACA are invalid as well. On December 18, 2019, the U.S. Court of Appeals for the Fifth Circuit upheld the District Court’s ruling with respect to the individual mandate but remanded the case to the District Court to consider whether other parts of the law can remain in effect. While the Texas District Court Judge has stated that the ruling will have no immediate effect, it is unclear how this decision, subsequent appeals, and other efforts to repeal and replace the PPACA will impact the law and our business. We are not sure whether additional legislative changes will be enacted, or whether the FDA regulations, guidance or interpretations will be changed, or what the impact of such changes on the marketing approvals of our drug candidates, if any, may be. In addition, increased scrutiny by

15

the U.S. Congress of the FDA’s approval process may significantly delay or prevent marketing approval, as well as subject us to more stringent product labeling and post-marketing approval testing and other requirements.

Moreover, payment methodologies may be subject to changes in healthcare legislation and regulatory initiatives. For example, CMS may develop new payment and delivery models, such as bundled payment models. In addition, there has been heightened governmental scrutiny over the manner in which manufacturers set prices for their marketed products, which has resulted in several U.S. Congressional inquiries and proposed and enacted federal and state legislation designed to, among other things, bring more transparency to drug pricing, reduce the cost of prescription drugs under government payor programs, and review the relationship between pricing and manufacturer patient programs. The U.S. Department of Health and Human Services has started soliciting feedback on some of these measures and, at the same time, is implementing others under its existing authority. For example, in May 2019, CMS issued a final rule to allow Medicare Advantage Plans the option of using step therapy for Part B drugs beginning January 1, 2020. This final rule codified CMS’s policy change that was effective January 1, 2019. While any proposed measures will require authorization through additional legislation to become effective, Congress has indicated that it will continue to seek new legislative and/or administrative measures to control drug costs. We expect that additional U.S. federal healthcare reform measures will be adopted in the future, any of which could limit the amounts that the U.S. federal government will pay for healthcare products and services, which could result in reduced demand for our drug candidates, if approved for commercialization.

In Europe, the United Kingdom formally withdrew from the European Union on January 31, 2020, and entered into a transition period that ended on December 31, 2020. A significant portion of the regulatory framework in the United Kingdom is derived from the regulations of the European Union. We cannot predict what consequences the recent withdrawal of the United Kingdom from the European Union will have on the regulatory frameworks of the United Kingdom or the European Union, or on our future operations, if any, in these jurisdictions, and the United Kingdom is in the process of negotiating trade deals with other countries. Additionally, the United Kingdom’s withdrawal from the European Union may increase the possibility that other countries may decide to leave the European Union again.

Actions that we have taken to restructure our business to align our cost structure with our strategic priorities may not have the anticipated effects.

In August 2023, we announced a plan to reduce our workforce by six employees, which represented approximately 24% of our employees as of August 18, 2023. The decision to reduce our workforce was made in order to focus spending on our clinical program for FXR314, reduce ongoing operating expenses not related to clinical expenses, and extend our cash runway. As a result of the reduction in force, we incurred approximately $0.4 million of cash expenditures in connection with the reduction in force, which relate to severance pay, in the year ended March 31, 2024. We may incur additional expenses not currently contemplated due to events associated with the reduction in force; for example, the reduction in force may have a future impact on other areas of our liabilities and obligations, which could result in losses in future periods. Moreover, we may not realize, in full or in part, the anticipated benefits and savings from this restructuring due to unforeseen difficulties, delays or unexpected costs. If we are unable to realize the expected operational efficiencies and cost savings from the restructuring, our operating results and financial condition would be adversely affected. In addition, we may need to undertake additional workforce reductions or restructuring activities in the future.

Risks Related to Our Capital Requirements, Finances and Operations

Management has performed an analysis and concluded that substantial doubt exists about our ability to continue as a going concern. Separately, our independent registered public accounting firm has included in its opinion for the year ended March 31, 2024 an explanatory paragraph expressing substantial doubt in our ability to continue as a going concern, which may hinder our ability to obtain future financing.