Exhibit 99.1

|

|

Sprott |

|

|

|

|

|

|

|

|

|

|

|

Interim Report to Unitholders |

|

|

|

|

|

SEPTEMBER 30, |

|

|

2017 |

|

|

|

|

|

|

|

|

|

The management report of fund performance is an analysis and explanation that is designed to complement and supplement an investment fund’s financial statements. This report contains financial highlights but does not contain the complete financial statements of the investment fund. A copy of the financial statements has been included separately within the Report to Unitholders. You can also get a copy of the financial statements at your request, and at no cost, by calling 1-866-299-9906, by visiting our website at www.sprottphysicalsilvertrust.com or SEDAR at www.sedar.com or by writing to us at: Sprott Asset Management LP, Royal Bank Plaza, South Tower, 200 Bay Street, Suite 2600, P.O. Box 26, Toronto, Ontario M5J 2J1.

2

Management Report of Fund Performance (in U.S. dollars)

Investment Objective and Strategies

Sprott Physical Silver Trust (the “Trust”) is a closed-end mutual fund trust organized under the laws of the Province of Ontario, Canada, created to invest and hold substantially all of its assets in physical silver bullion. The Trust seeks to provide a secure, convenient and exchange-traded investment alternative for investors interested in holding physical silver bullion without the inconvenience that is typical of a direct investment in physical silver bullion. The Trust intends to achieve its objective by investing primarily in long-term holdings of unencumbered, fully allocated, physical silver bullion and does not speculate with regard to short-term changes in silver prices.

The units of the Trust are listed on the New York Stock Exchange (“NYSE”) Arca and the Toronto Stock Exchange (“TSX”) under the symbols “PSLV” and “PSLV.U”, respectively.

Risks

The risks of investing in the Trust are detailed in the Trust’s annual information form dated March 23, 2017. There have been no material changes to the Trust since inception that have affected the overall level of risk. The principal risks associated with investing in the Trust are the price of silver, the net asset value and/or the market price of the units, the purchase, transport, insurance and storage of physical silver bullion, liabilities of the Trust, and redemption of units.

Results of Operations

For the period from July 1, 2017 to September 30, 2017, the total change in unrealized gains on physical silver bullion amounted to $1.9 million compared to the change in unrealized gains of $25.0 million during the same period in 2016. For the period from January 1, 2017 to September 30, 2017, the total change in unrealized gains on physical silver bullion amounted to $41.7 million compared to the change in unrealized gains of $279.3 million during the same period in 2016.

During the period from January 1, 2017 to September 30, 2017, the Trust issued 1,711,798 units for gross proceeds of $11,140,135 and net proceeds of $10,982,012 after fees and expenses. During that period, the Trust redeemed 2,000 units for cash at a total cost of of $11,974.56.

The value of the net assets of the Trust as of September 30, 2017 was $935.3 million or $6.30 per unit, compared $888.5 million or $6.06 per unit as at December 31, 2016, the Trust’s most recent fiscal year end. The Trust held 55,911,090 ounces of physical silver bullion as of September 30, 2017 compared to 55,659,095 ounces at December 31, 2016. As at September 30, 2017, the spot price of silver was $16.65 an ounce compared to a price of $15.92 an ounce as at December 31, 2016. The Trust returned 4.0% compared to the return on spot silver of 4.6% for the period from January 1, 2017 to September 30, 2017.

The Trust’s net asset value per unit on September 30, 2017 was $6.30 compared to $6.06 per unit as at December 31, 2016. The units closed at $6.28 on the NYSE Arca and $6.31 on the TSX on September 29, 2017 compared to closing prices of $6.08 on the NYSE Arca and $6.10 on the TSX on December 31, 2016. The units are denominated in U.S. dollars on both exchanges. During the period from January 1, 2017 to September 30, 2017, the Trust’s units traded on the NYSE Arca at an average discount to net asset value of approximately 0.0%.

Recent Developments

On June 24, 2016, the Trust entered into a sales agreement with Cantor Fitzgerald & Co. whereby the Trust may, in its sole discretion and subject to its operating and investment restrictions, offer and sell trust units through an “at the market offering” program (the “ATM Program”) in transactions on the NYSE Arca or any other existing trading market for the trust units in the United States or to or through a market maker in the United States pursuant to a registration statement filed with the U.S. Securities and Exchange Commission and a prospectus supplement to a short form base shelf prospectus filed with the Ontario Securities Commission, as principal regulator, and with each of the securities commissions or similar regulatory authorities in each of the provinces and territories of Canada. During the period from January 1, 2017 to September 30, 2017, the Trust sold 1,711,798 units through the ATM Program.

3

OPERATING EXPENSES

The Trust pays its own operating expenses, which include, but are not limited to, audit, legal, trustee fees, unitholder reporting expenses, general and administrative fees, filing and listing fees payable to applicable securities regulatory authorities and stock exchanges, storage fees for the physical silver bullion, costs incurred in connection with the Trust’s continuous disclosure public filing requirements and investor relations and any expenses associated with the implementation and on-going operation of the Independent Review Committee of the Trust. Operating expenses for the period from July 1, 2017 to September 30, 2017 amounted to $455,576 (not including applicable Canadian taxes) compared to $347,771 for the same period in 2016. Operating expenses for the period from January 1, 2017 to September 30, 2017 amounted to $1,452,466 (not including applicable Canadian taxes) compared to $1,278,346 for the same period in 2016. Operating expenses for the period from July 1, 2017 to September 30, 2017 amounted to 0.19% of the average net assets during the period on an annualized basis, compared to 0.13% for the same period in 2016. Operating expenses for the period from January 1, 2017 to September 30, 2017 amounted to 0.20% of the average net assets during the period on an annualized basis, compared to 0.19% for the same period in 2016.

Related Party Transactions

MANAGEMENT FEES

The Trust pays the Manager, Sprott Asset Management LP, a monthly management fee equal to 1/12 of 0.45% of the value of the net assets of the Trust (determined in accordance with the Trust’s trust agreement), plus any applicable Canadian taxes. The management fee is calculated and accrued daily and payable monthly in arrears on the last day of each month. For the period from July 1, 2017 to September 30, 2017, the Trust incurred management fees of $1,057,481 (not including applicable Canadian taxes) compared to $1,203,567 for the same period in 2016. For the period from January 1, 2017 to September 30, 2017, the Trust incurred management fees of $3,225,252 (not including applicable Canadian taxes) compared to $3,021,180 for the same period in 2016.

4

Financial Highlights

The following tables show selected key financial information about the Trust and are intended to help you understand the Trust’s financial performance for the three and nine-month periods ended September 30, 2017 and the years shown.

Net assets per unit1

|

|

|

For the three |

|

For the nine |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

months ended |

|

months ended |

|

December 31, |

|

December 31, |

|

December 31, |

|

December 31, |

|

December 31, |

|

|

|

|

September 30, 2017 |

|

September 30, 2017 |

|

2016 |

|

2015 |

|

2014 |

|

2013 |

|

2012 |

|

|

|

|

$ |

|

$ |

|

$ |

|

$ |

|

$ |

|

$ |

|

$ |

|

|

Net assets per Unit, beginning of period |

|

6.30 |

|

6.06 |

|

5.33 |

|

6.09 |

|

7.60 |

|

11.86 |

|

10.81 |

|

|

Increase (decrease) from operations2: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Total revenue |

|

– |

|

– |

|

– |

|

– |

|

– |

|

– |

|

– |

|

|

Total expenses |

|

(0.01) |

|

(0.03) |

|

(0.04) |

|

(0.05) |

|

(0.05) |

|

(0.06) |

|

(0.08) |

|

|

Realized losses for the period |

|

(0.00) |

|

(0.01) |

|

(0.02) |

|

(0.03) |

|

– |

|

– |

|

– |

|

|

Unrealized gains (losses) for the period |

|

0.01 |

|

0.28 |

|

0.67 |

|

(0.68) |

|

(1.46) |

|

(4.21) |

|

0.57 |

|

|

Total increase (decrease) from operations |

|

(0.00) |

|

0.24 |

|

0.62 |

|

(0.76) |

|

(1.51) |

|

(4.27) |

|

0.49 |

|

|

Net assets per Unit, end of period |

|

6.30 |

|

6.30 |

|

6.06 |

|

5.33 |

|

6.09 |

|

7.60 |

|

11.86 |

|

|

1. |

This information is derived from the Trust’s financial statements. |

|

2. |

Net assets per unit is calculated based on the actual number of units outstanding at the relevant time. The increase/decrease from operations is based on the weighted average number of units outstanding over the period shown. This table is not intended to be a reconciliation of the beginning to ending net assets per unit. |

Ratios and Supplemental Data

|

|

|

September 30, |

|

December 31, |

|

December 31, |

|

December 31, |

|

December 31, |

|

December 31, |

|

|

|

|

2017 |

|

2016 |

|

2015 |

|

2014 |

|

2013 |

|

2012 |

|

|

Total net asset value (000’s)1 |

|

$935,267 |

|

$888,534 |

|

$678,584 |

|

$775,016 |

|

$967,551 |

|

$1,510,942 |

|

|

Number of Units outstanding1 |

|

148,433,821 |

|

146,724,023 |

|

127,331,218 |

|

127,360,215 |

|

127,365,280 |

|

127,367,197 |

|

|

Management expense ratio2 |

|

0.69% |

|

0.70% |

|

0.75% |

|

0.76% |

|

0.65% |

|

0.65% |

|

|

Trading expense ratio3 |

|

nil |

|

nil |

|

nil |

|

nil |

|

nil |

|

nil |

|

|

Portfolio turnover rate4 |

|

nil |

|

0.29% |

|

nil |

|

nil |

|

nil |

|

nil |

|

|

Net asset value per Unit |

|

$6.30 |

|

$6.06 |

|

$5.33 |

|

$6.09 |

|

$7.60 |

|

$11.86 |

|

|

Closing market price – NYSE Arca |

|

$6.28 |

|

$6.08 |

|

$5.27 |

|

$6.15 |

|

$7.57 |

|

$12.04 |

|

|

Closing market price – TSX |

|

$6.31 |

|

$6.10 |

|

$5.29 |

|

$6.16 |

|

$7.58 |

|

$12.07 |

|

|

1. |

This information is provided as at the date shown, as applicable. |

|

2. |

Management expense ratio (“MER”) is based on total expenses (including applicable Canadian taxes and excluding commissions and other portfolio transaction costs) for the stated period and is expressed as an annualized percentage of daily average net asset value during the period. |

|

3. |

The trading expense ratio represents total commissions and other portfolio transaction costs expressed as an annualized percentage of daily average net asset value during the period shown. Since there are no direct trading costs associated with physical bullion trades, the trading expense ratio is nil. |

|

4. |

The Trust’s portfolio turnover rate indicates how actively the Trust’s portfolio adviser trades its portfolio investments. A portfolio turnover rate of 100% is equivalent to the Trust buying and selling all of the securities in its portfolio once in the course of the year. The higher the Trust’s portfolio turnover rate in a year, the greater the chance of an investor receiving taxable capital gains in the year. There is not necessarily a relationship between a high turnover rate and the performance of the Trust. |

5

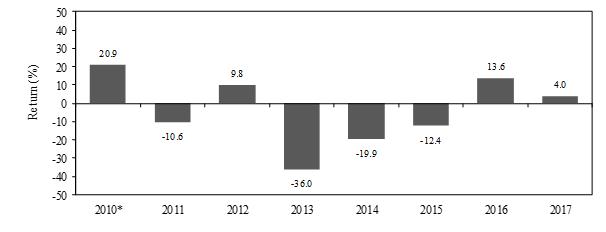

Past Performance

The indicated rates of return are the historical total returns including changes in unit values and assume reinvestment of all distributions in additional units of the Trust. These returns do not take into account sales, redemption, distribution or optional charges or income taxes payable by any unitholder that may reduce returns. Please note that past performance is not indicative of future performance. All rates of returns are calculated based on the Net Asset Value of the units of the Trust.

Year-by-Year Returns

The bar chart below indicates the performance of the Trust units for the nine months ended September 30, 2017 and the years shown. The chart shows, in percentage terms, how much an investment made on the first day of each period would have grown or decreased by the last day of each period.

*Return for the period from October 28, 2010 to December 31, 2010 (not annualized)

Summary of Investment Portfolio

As of September 30, 2017

|

|

|

|

|

|

|

|

|

|

|

% of |

|

|

|

|

|

|

Fair Value |

|

|

|

Fair |

|

Net Asset |

|

|

|

|

|

|

per ounce |

|

Cost |

|

Value |

|

Value |

|

|

|

|

Ounces |

|

$ |

|

$ |

|

$ |

|

% |

|

|

Physical silver bullion |

|

55,911,090 |

|

16.65 |

|

1,463,398,352 |

|

931,059,428 |

|

99.6 |

|

|

Cash |

|

|

|

|

|

|

|

4,675,925 |

|

0.5 |

|

|

Other Net Liabilities |

|

|

|

|

|

|

|

(467,862) |

|

(0.1) |

|

|

Total Net Asset Value |

|

|

|

|

|

|

|

935,267,492 |

|

100.0 |

|

This summary of investment portfolio may change due to the ongoing portfolio transactions of the Trust.

6

7

Unaudited statements of comprehensive income (loss)

(in U.S. dollars, except unit amounts)

|

|

|

For the |

|

For the |

|

For the |

|

For the |

|

|

|

|

three months ended |

|

three months ended |

|

nine months ended |

|

nine months ended |

|

|

|

|

September 30, 2017 |

|

September 30, 2016 |

|

September 30, 2017 |

|

September 30, 2016 |

|

|

|

|

$ |

|

$ |

|

$ |

|

$ |

|

|

Income |

|

|

|

|

|

|

|

|

|

|

Net realized losses on redemptions and sales of silver bullion |

|

(723,187) |

|

– |

|

(966,565) |

|

(2,391,049) |

|

|

Change in unrealized gains on silver bullion |

|

1,908,161 |

|

24,952,669 |

|

41,667,221 |

|

279,276,613 |

|

|

Other income |

|

– |

|

– |

|

– |

|

1,505 |

|

|

|

|

1,184,974 |

|

24,952,669 |

|

40,700,656 |

|

276,887,069 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Expenses |

|

|

|

|

|

|

|

|

|

|

Management fees (note 8) |

|

1,057,481 |

|

1,203,567 |

|

3,225,252 |

|

3,021,180 |

|

|

Bullion storage fees |

|

304,712 |

|

267,359 |

|

991,600 |

|

946,009 |

|

|

Sales tax |

|

89,125 |

|

96,976 |

|

259,656 |

|

254,046 |

|

|

Unitholder reporting costs |

|

82,947 |

|

19,867 |

|

188,974 |

|

73,069 |

|

|

Administrative fees |

|

27,336 |

|

5,340 |

|

80,534 |

|

71,632 |

|

|

Listing and regulatory filing fees |

|

21,113 |

|

24,324 |

|

80,730 |

|

76,972 |

|

|

Audit fees |

|

11,404 |

|

9,063 |

|

36,920 |

|

38,249 |

|

|

Legal fees |

|

9,639 |

|

18,115 |

|

73,636 |

|

64,346 |

|

|

Trustee fees |

|

1,038 |

|

1,250 |

|

3,378 |

|

3,750 |

|

|

Independent Review Committee fees |

|

976 |

|

1,039 |

|

3,271 |

|

3,113 |

|

|

Custodial fees |

|

(4) |

|

165 |

|

205 |

|

388 |

|

|

Net foreign exchange (gains) losses |

|

(3,585) |

|

1,249 |

|

(6,782) |

|

818 |

|

|

|

|

1,602,182 |

|

1,648,314 |

|

4,937,374 |

|

4,553,572 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Net income (loss) and comprehensive income (loss) |

|

(417,208) |

|

23,304,355 |

|

35,763,282 |

|

272,333,497 |

|

|

Weighted average number of Units |

|

147,622,999 |

|

142,419,470 |

|

147,063,898 |

|

136,700,102 |

|

|

|

|

|

|

|

|

|

|

|

|

|

Increase (decrease) in total equity from operations per Unit |

|

(0.00) |

|

0.16 |

|

0.24 |

|

1.99 |

|

The accompanying notes are an integral part of these financial statements.

On behalf of the Manager, Sprott Asset Management LP,

by its General Partner, Sprott Asset Management GP Inc.:

|

Kevin Hibbert |

Ahsan Ahmed |

|

|

Director |

Director |

8

Unaudited statements of financial position

(in U.S. dollars)

|

|

|

As at |

|

As at |

|

|

|

|

September 30, 2017 |

|

December 31, 2016 |

|

|

|

|

$ |

|

$ |

|

|

Assets |

|

|

|

|

|

|

Current assets |

|

|

|

|

|

|

Cash |

|

4,675,925 |

|

2,739,135 |

|

|

Silver bullion |

|

931,059,428 |

|

885,981,474 |

|

|

Prepaid assets |

|

221,641 |

|

175,305 |

|

|

Total assets |

|

935,956,994 |

|

888,895,914 |

|

|

|

|

|

|

|

|

|

Liabilities |

|

|

|

|

|

|

Current liabilities |

|

|

|

|

|

|

Accounts payable |

|

689,502 |

|

361,742 |

|

|

Total liabilities |

|

689,502 |

|

361,742 |

|

|

|

|

|

|

|

|

|

Equity |

|

|

|

|

|

|

Unitholders’ capital |

|

1,586,460,088 |

|

1,575,339,953 |

|

|

Unit premiums and reserves |

|

59,713 |

|

59,083 |

|

|

Retained earnings (deficit) |

|

(584,729,635) |

|

(620,500,312) |

|

|

Underwriting commissions and issue expenses |

|

(66,522,674) |

|

(66,364,552) |

|

|

Total equity (note 7) |

|

935,267,492 |

|

888,534,172 |

|

|

|

|

|

|

|

|

|

Total liabilities and equity |

|

935,956,994 |

|

888,895,914 |

|

|

|

|

|

|

|

|

|

Total equity per Unit |

|

6.30 |

|

6.06 |

|

The accompanying notes are an integral part of these financial statements.

9

Unaudited statements of changes in equity

(in U.S. dollars, except unit amounts)

For the nine months ended September 30, 2017 and 2016

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Underwriting |

|

Unit |

|

|

|

|

|

|

Number of |

|

|

|

|

|

Commissions |

|

Premiums |

|

|

|

|

|

|

Units |

|

Unitholders’ |

|

Retained |

|

and Issue |

|

and |

|

|

|

|

|

|

outstanding |

|

Capital |

|

Earnings |

|

Expenses |

|

Reserves |

|

Total Equity |

|

|

|

|

|

|

$ |

|

$ |

|

$ |

|

$ |

|

$ |

|

|

Balance as at January 1, 2016 |

|

127,331,218 |

|

1,453,136,520 |

|

(712,142,865) |

|

(62,467,856) |

|

58,617 |

|

678,584,416 |

|

|

Proceeds from issuance of Units (note 7) |

|

15,614,048 |

|

97,500,366 |

|

– |

|

– |

|

– |

|

97,500,366 |

|

|

Cost of Redemption of Units (note 7) |

|

– |

|

– |

|

– |

|

– |

|

– |

|

– |

|

|

Net income for the period |

|

– |

|

– |

|

272,333,497 |

|

– |

|

– |

|

272,333,497 |

|

|

Underwriting commissions and issue expenses |

|

– |

|

– |

|

– |

|

(3,751,304) |

|

– |

|

(3,751,304) |

|

|

Balance as at September 30, 2016 |

|

142,945,266 |

|

1,550,636,886 |

|

(439,809,368) |

|

(66,219,160) |

|

58,617 |

|

1,044,666,975 |

|

|

Balance as at January 1, 2017 |

|

146,724,023 |

|

1,575,339,953 |

|

(620,500,312) |

|

(66,364,552) |

|

59,083 |

|

888,534,172 |

|

|

Proceeds from issuance of Units (note 7) |

|

1,711,798 |

|

11,140,135 |

|

– |

|

– |

|

– |

|

11,140,135 |

|

|

Cost of Redemption of Units (note 7) |

|

(2,000) |

|

(20,000) |

|

7,395 |

|

– |

|

630 |

|

(11,975) |

|

|

Net income for the period |

|

– |

|

– |

|

35,763,282 |

|

– |

|

– |

|

35,763,282 |

|

|

Underwriting commissions and issue expenses |

|

– |

|

– |

|

– |

|

(158,122) |

|

– |

|

(158,122) |

|

|

Balance as at September 30, 2017 |

|

148,433,821 |

|

1,586,460,088 |

|

(584,729,635) |

|

(66,522,674) |

|

59,713 |

|

935,267,492 |

|

The accompanying notes are an integral part of these financial statements.

10

Unaudited statements of cash flows

(in U.S. dollars)

|

|

|

For the nine months ended |

|

For the nine months ended |

|

|

|

|

September 30, 2017 |

|

September 30, 2016 |

|

|

|

|

$ |

|

$ |

|

|

Cash flows from operating activities |

|

|

|

|

|

|

Net income for the period |

|

35,763,282 |

|

272,333,497 |

|

|

Adjustments to reconcile net income for the period to net cash from operating activities |

|

|

|

|

|

|

Net realized losses on redemptions and sales of bullion |

|

966,565 |

|

2,391,049 |

|

|

Change in unrealized gains on silver bullion |

|

(41,667,221) |

|

(279,276,613) |

|

|

Net changes in operating assets and liabilities |

|

|

|

|

|

|

Increase in prepaid assets |

|

(46,336) |

|

(117,570) |

|

|

Increase in subscriptions receivable |

|

– |

|

(920,375) |

|

|

Increase (decrease) in accounts payable |

|

327,760 |

|

77,501 |

|

|

Net cash used in operating activities |

|

(4,655,950) |

|

(5,512,511) |

|

|

|

|

|

|

|

|

|

Cash flows from investing activities |

|

|

|

|

|

|

Purchases of bullion |

|

(5,981,523) |

|

(88,788,468) |

|

|

Sales of bullion |

|

1,604,225 |

|

2,610,022 |

|

|

Net cash provided by (used in) investing activities |

|

(4,377,298) |

|

(86,178,446) |

|

|

|

|

|

|

|

|

|

Cash flows from financing activities |

|

|

|

|

|

|

Proceeds from issuance of Units (note 7) |

|

11,140,135 |

|

97,500,366 |

|

|

Payments on redemption of Units (note 7) |

|

(11,975) |

|

– |

|

|

Underwriting commissions and issue expenses |

|

(158,122) |

|

(3,751,304) |

|

|

Net cash provided by (used in) financing activities |

|

10,970,038 |

|

93,749,062 |

|

|

Net increase (decrease) in cash during the period |

|

1,936,790 |

|

2,058,105 |

|

|

Cash at beginning of period |

|

2,739,135 |

|

357,197 |

|

|

Cash at end of period |

|

4,675,925 |

|

2,415,302 |

|

The accompanying notes are an integral part of these financial statements.

11

|

Sprott Physical Silver Trust |

|

(in-U.S. dollars)

Financial Risk Management (note 6)

Investment Objective

The investment objective of the Trust is to seek to provide a secure, convenient and exchange-traded investment alternative for investors interested in holding physical silver bullion without the inconvenience that is typical of a direct investment in physical silver bullion. The Trust invests and intends to continue to invest primarily in long-term holdings of unencumbered, fully allocated, physical silver bullion and does not speculate with regard to short-term changes in silver prices. The Trust has only purchased and expects only to own “Good Delivery Bars” as defined by the London Bullion Market Association (“LBMA”), with each bar purchased being verified against the LBMA source.

Significant risks that are relevant to the Trust are discussed here. General information on risks and risk management is described in Note 6 of the Generic Notes.

Fair Value Measurements

The reconciliation of bullion holdings for the nine months ended September 30, 2017 and the year ended December 31, 2016 is presented as follows:

|

|

|

|

September 30, 2017 |

|

December 31, 2016 |

|

|

|

|

|

$ |

|

$ |

|

|

Balance at beginning of year |

|

|

885,981,474 |

|

678,629,331 |

|

|

Purchases |

|

|

5,981,523 |

|

111,950,640 |

|

|

Sales |

|

|

(1,604,225) |

|

(2,610,022) |

|

|

Redemptions for physical bullion |

|

|

- |

|

- |

|

|

Realized losses on sales and redemptions for physical bullion |

|

|

(966,565) |

|

(2,391,049) |

|

|

Change in unrealized gains (losses) |

|

|

41,667,221 |

|

100,402,574 |

|

|

Balance at end of period |

|

|

931,059,428 |

|

885,981,474 |

|

Realized gains (losses) on physical bullion include both realized gains (losses) on sales of physical bullion, and realized gains (losses) occurring upon unitholder redemptions for physical bullion.

Market Risk

a) Other Price Risk

If the market value of silver increased by 1%, with all other variables held constant, this would have increased total equity and comprehensive income by approximately $9.3 million (December 31, 2016: $8.9 million); conversely, if the value of silver bullion decreased by 1%, this would have decreased total equity and comprehensive income by the same amount.

b) Currency Risk

As at September 30, 2017, approximately $24,000 (December 31, 2016: $305,000) of the Trust’s liabilities were denominated in Canadian dollars. As a result, a 1% change in the exchange rate between the Canadian and U.S. Dollars would have no material impact to the Trust.

Concentration Risk

The Trust’s risk is concentrated in physical silver bullion, whose value constitutes 99.6% of total equity as at September 30, 2017 (99.7% as at December 31, 2016).

12

|

Sprott Physical Silver Trust |

|||

Management Fees (note 8)

The Trust pays the Manager a monthly management fee equal to 1/12 of 0.45% of the value of net assets of the Trust (determined in accordance with the Trust’s trust agreement) plus any applicable Canadian taxes, calculated and accrued daily and payable monthly in arrears on the last day of each month.

Tax Loss Carryforwards

As of the taxation year ended December 31, 2016, the Trust had capital losses available for tax purposes of $3,174,901 (2015: $2,044,356).

Related Party Disclosures (note 8)

There have been no transactions between the Trust and its related parties during the reporting period, other than management fees as discussed above.

13

|

Sprott Physical Bullion Trusts |

|

1. Organization of the Trusts

Sprott Physical Gold Trust, Sprott Physical Silver Trust and Sprott Physical Platinum and Palladium Trust (collectively, the “Trusts” and each a “Trust”) are closed-end mutual fund trusts created under the laws of the Province of Ontario, Canada, pursuant to trust agreements. Sprott Asset Management LP (the “Manager”) acts as the manager of the Trusts. RBC Investor Services Trust, a trust company organized under the laws of Canada, acts as the trustee of the Trusts. RBC Investor Services Trust also acts as custodian on behalf of the Trusts for the Trusts’ assets other than physical bullion. The Royal Canadian Mint acts as custodian on behalf of the Trusts for the physical bullion owned by the Trusts. The Trusts’ registered office is located at Suite 2600, South Tower, Royal Bank Plaza, 200 Bay Street, Toronto, Ontario, Canada, M5J 2J1. The Trusts are authorized to issue an unlimited number of redeemable, transferable trust units (the “Units”). All issued Units have no par value, are fully paid for, and are listed and traded on the New York Stock Exchange Arca (the “NYSE Arca”) and the Toronto Stock Exchange (the “TSX”). The date of inception and trading symbols of each of the Trusts is as follows:

|

|

|

Trust Agreement date |

|

Initial Public Offering date |

|

NYSE Arca and TSX symbols, respectively |

|

Sprott Physical Gold Trust |

August 28, 2009, as amended and restated as of December 7, 2009 and as further amended and restated as of February 1, 2010 |

March 3, 2010 |

PHYS, PHYS.U |

|||

|

Sprott Physical Silver Trust |

June 30, 2010, as amended and restated as of October 1, 2010 |

October 28, 2010 |

PSLV, PSLV.U |

|||

|

Sprott Physical Platinum and Palladium Trust |

December 23, 2011, as amended and restated as of June 6, 2012 |

December 19, 2012 |

SPPP, SPPP.U |

The Statements of Financial Position for the Trusts are as at September 30, 2017 and December 31, 2016. The Statements of Comprehensive Income, the Statements of Changes in Equity and Statements of Cash Flows for the Trusts are for the three and nine month periods ended September 30, 2017 and 2016. These financial statements were authorized for issue by the Manager on November 10, 2017.

2. Basis of Preparation

These financial statements have been prepared in compliance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”) and include estimates and assumptions made by the Manager that may affect the reported amounts of assets, liabilities, income, expenses and the reported amounts of changes in Net Assets during the reporting period. Actual results could differ from those estimates.

The financial statements have been prepared on a going concern basis using the historical cost convention, except for physical bullion and financial assets and financial liabilities held at fair value through profit or loss, which have been measured at fair value.

The financial statements are presented in U.S. dollars and all values are rounded to the nearest dollar unless otherwise indicated.

3. Summary of Significant Accounting Policies

The following is a summary of significant accounting policies followed by the Trusts:

Physical bullion

Investments in physical bullion are measured at fair value determined by reference to published price quotations, with unrealized and realized gains and losses recorded in income based on the International Accounting Standards 40 Investment Property fair value model as IAS 40 is the most relevant standard to apply. Investment transactions in physical bullion are accounted for on the business day following the date the order to buy or sell is executed. Realized and unrealized gains and losses of holdings are calculated on an average cost basis.

Other assets and liabilities

Other assets and liabilities are recognized at fair value upon initial recognition. Other assets such as due from broker and other receivables are classified as loans and receivables and measured at amortized cost. Other financial liabilities are measured at amortized cost.

14

|

Sprott Physical Bullion Trusts |

|

Income taxes

In each taxation year, the Trusts will be subject to income tax on taxable income earned during the year, including net realized taxable capital gains. However, the Trusts intend to distribute their taxable income to unitholders at the end of every fiscal year and therefore the Trusts themselves would not have any income tax liability.

Functional and presentation currency

Each Trust’s functional and presentation currency is the U.S. Dollar. Each Trusts’ performance is evaluated and its liquidity is managed in U.S. Dollars. Therefore, the U.S. Dollar is considered as the currency that most faithfully represents the economic effects of the underlying transactions, events and conditions.

Standards issued but not yet effective

Standards issued but not yet effective up to the date of issuance of the Trusts’ financial statements are listed below. The Trusts intend to adopt applicable standards when they become effective.

IFRS 9, Financial Instruments - Classification and Measurement (“IFRS 9”): In July 2014, the IASB issued the final version of IFRS 9, bringing together the classification and measurement, impairment and hedge accounting phases of the IASB’s project to replace IAS 39 and all previous versions of IFRS 9. IFRS 9 introduces a logical, single classification and measurement approach for financial assets that reflects the business model in which they are managed and their cash flow characteristics. Built upon this is a forward-looking expected credit loss model that will result in more timely recognition of loan losses and is a single model that is applicable to all financial instruments subject to impairment accounting. In addition, IFRS 9 also removes the volatility in profit or loss that was caused by changes in the credit risk of liabilities elected to be measured at fair value, such that gains caused by the deterioration of an entity’s own credit risk on such liabilities are no longer recognized in profit or loss. IFRS 9 also includes an improved hedge accounting model to better link the economics of risk management with its accounting treatment. IFRS 9 is effective for annual periods beginning on or after January 1, 2018, with early adoption permitted. In addition, the credit changes can be early applied in isolation without otherwise changing the accounting for financial instruments. Management has established a working group and plan to ensure compliance with IFRS 9 by January 1, 2018, which includes identifying differences between existing policies and this new standard and disclosing the prior years’ quantitative impact within the notes of the annual 2017 financial statements. Management is currently executing its adoption plan of this new standard and continues to assess the impact on the Trust’s financial statements.

4. Critical Accounting Estimates and Judgments

The preparation of financial statements requires management to use judgment in applying its accounting policies and to make estimates and assumptions about the future. The following discusses the most significant accounting judgments and estimates that the Trusts have made in preparing the financial statements:

Estimation uncertainty

For tax purposes, the Trusts generally treat gains from the disposition of bullion as capital gains, rather than income, as the Trusts intend to be long-term passive holders of bullion, and generally dispose of their holdings in bullion only for the purposes of meeting redemptions and to pay expenses. The Canada Revenue Agency has, however, expressed its opinion that gains (or losses) of mutual fund trusts resulting from transactions in commodities should generally be treated for tax purposes as ordinary income rather than as capital gains, although the treatment in each particular case remains a question of fact to be determined having regard to all the circumstances.

The Trusts based their assumptions and estimates on parameters available when the financial statements were prepared. However, existing circumstances and assumptions about future developments may change due to market changes or circumstances arising beyond the control of the Trusts. Such changes are reflected in the assumptions when they occur.

15

|

Sprott Physical Bullion Trusts |

|

5. Fair Value Measurements

The Trusts use a three-tier hierarchy as a framework for disclosing fair value based on inputs used to value their investments. The fair value hierarchy has the following levels:

Level 1Unadjusted quoted prices in active markets for identical, unrestricted assets or liabilities that the Trusts have the ability to access at the measurement date;

Level 2Quoted prices which are not active, or inputs that are observable (either directly or indirectly) for substantially the full term of the asset or liability; and

Level 3Prices, inputs or complex modeling techniques which are both significant to the fair value measurement and unobservable (supported by little or no market activity).

Physical bullion is measured at fair value. The fair value measurement of all bullion falls within Level 1 of the hierarchy, and is based on published price quotations. All fair value measurements are recurring. The carrying values of cash, accounts receivable and accounts payable approximate their fair values due to their short-term nature.

6. Financial Risk, Management and Objectives

The Trusts’ objective in managing risk is the creation and protection of unitholder value. Risk is inherent in the Trusts’ activities, but it is managed through a process of ongoing identification, measurement and monitoring, subject to risk limits and other controls. The Trusts have investment guidelines that set out their overall business strategies, their tolerance for risk and their general risk management philosophy, as set out in each Trust’s offering documents. The Trusts’ Manager is responsible for identifying and controlling risks. The Trusts are exposed to market risk (which includes price risk, interest rate risk and currency risk), credit risk, liquidity risk and concentration risk arising from the bullion that they hold. Only certain risks of the Trusts are actively managed by the Manager, as the Trusts are passive investment vehicles. Significant risks that are relevant to the Trusts are discussed below. Refer to the Notes to financial statements — Trust specific information of each Trust for specific risk disclosures.

Price risk

Price risk arises from the possibility that changes in the market price of each Trust’s investments, which consist almost entirely of bullion, will result in changes in fair value of such investments.

Interest rate risk

Interest rate risk arises from the possibility that changes in interest rates will affect the value of financial instruments. The Trusts do not hedge their exposure to interest rate risk as that risk is minimal.

Currency risk

Currency risk arises from the possibility that changes in the price of foreign currencies will result in changes in carrying value. Each Trust’s assets, substantially all of which consist of an investment in bullion, are priced in U.S. dollars. Some of the Trusts’ expenses are payable in Canadian dollars. Therefore, the Trusts are exposed to currency risk, as the value of their liabilities denominated in Canadian dollars will fluctuate due to changes in exchange rates. Most of such liabilities, however, are short term in nature and are not significant in relation to the net assets of the Trusts, and, as such, exposure to foreign exchange risk is limited. The Trusts do not enter into currency hedging transactions.

Credit risk

Credit risk arises from the potential that counterparties will fail to satisfy their obligations as they come due. The Trusts primarily incur credit risk when entering into and settling bullion transactions. It is each Trust’s policy to only transact with reputable counterparties. The Manager closely monitors the creditworthiness of the Trusts’ counterparties, such as bullion dealers, by reviewing their financial statements when available, regulatory notices and press releases. The Trusts seek to minimize credit risk relating to unsettled transactions in bullion by only engaging in transactions with bullion dealers with high creditworthiness. The risk of default is considered minimal, as payment for bullion is only made against the receipt of the bullion by the custodian.

16

|

Sprott Physical Bullion Trusts |

|

Liquidity risk

Liquidity risk is defined as the risk that the Trusts will encounter difficulty in meeting obligations associated with financial liabilities and redemptions. Liquidity risk arises because of the possibility that the Trusts could be required to pay their liabilities earlier than expected. The Trusts are also subject to redemptions for both cash and bullion on a regular basis. The Trusts manage their obligation to redeem units when required to do so and their overall liquidity risk by only allowing for redemptions monthly, which require 15-day advance notice to the Trusts. Each Trust’s liquidity risk is minimal, since it’s primary investment is physical bullion, which trades in a highly liquid market. All of the Trusts’ financial liabilities, including due to brokers, accounts payable and management fees payable have maturities of less than three months.

Concentration risk

Each Trust’s risk is concentrated in the physical bullion of precious metals.

7. Unitholders’ Capital

The Trusts are authorized to issue an unlimited number of redeemable, transferrable Trust Units in one or more classes and series of Units. The Trusts’ capital is represented by the issued, redeemable, transferable Trust Units. Quantitative information about the Trusts’ capital is provided in their statements of changes in equity. Under the trust agreements of each Trust, Units may be redeemed at the option of the unitholder on a monthly basis for physical bullion or cash. Units redeemed for physical bullion will be entitled to a redemption price equal to 100% of the Net Asset Value (“NAV”) of the redeemed Units on the last business day of the month in which the redemption request is processed. A unitholder redeeming Units for physical bullion will be responsible for expenses in connection with effecting the redemption and applicable delivery expenses, including the handling of the notice of redemption, the delivery of the physical bullion for Units that are being redeemed and the applicable bullion storage in-and-out fees. Units redeemed for cash will be entitled to a redemption price equal to 95% of the lesser of (i) the volume-weighted average trading price of the Units traded on the NYSE Arca, or, if trading has been suspended on the NYSE Arca, on the TSX for the last five business days of the month in which the redemption request is processed and (ii) the NAV of the redeemed Units as of 4:00 p.m., Eastern Standard time, on the last business day of the month in which the redemption request is processed.

When Units are redeemed and cancelled and the cost of such Units is either above or below their stated or assigned value, the unitholders’ capital is reduced by an amount equal to the stated or assigned value of the Units. The difference between the redemption price and the stated or assigned values of the Units is allocated to the Unit premiums and reserves account (equal to the 5% reduction to the redemption price for Units redeemed for cash as described above) and the retained earnings account based on the allocated portion attributable to the redemption.

The Trusts’ units are classified as equity on the Statements of Financial Position, since the Trusts’ units meet the criteria in IAS 32, Financial Instruments: Presentation (“IAS 32”) for classification as equity.

Net Asset Value

NAV is defined as a Trust’s net assets (fair value of total assets less fair value of total liabilities, excluding all liabilities represented by outstanding Units, if any) calculated using the value of physical silver bullion based on the end-of-day price provided by a widely recognized pricing service.

Capital management

As a result of the ability to issue, repurchase and resell Units of the Trusts, the capital of the Trusts as represented by the Unitholders’ capital in the statements of financial position can vary depending on the demand for redemptions and subscriptions to the Trusts. The Trusts are not subject to externally imposed capital requirements and have no legal restrictions on the issue, repurchase or resale of redeemable Units beyond those included in their trust agreements. The Trusts may not issue additional Units except (i) if the net proceeds per Unit to be received by the Trusts are not less than 100% of the most recently calculated NAV immediately prior to, or upon, the determination of the pricing of such issuance or (ii) by way of Unit distribution in connection with an income distribution.

Each Trusts’ objectives for managing capital are:

17

|

Sprott Physical Bullion Trusts |

|

|

· |

To invest and hold substantially all of the Trust’s assets in physical bullion; and |

|

· |

To maintain sufficient liquidity to meet the expenses of each Trust, and to meet redemption requests as they arise. |

Refer to “Financial risk, management and objectives” (Note 6) for the policies and procedures applied by the Trusts in managing their capital.

8. Related Party Disclosures

Management Fees

The Trusts pay the Manager a monthly management fee, calculated and accrued daily and payable monthly in arrears on the last day of each month. Management fees are unique to each Trust and are subject to applicable taxes.

9. Independent Review Committee (“IRC”)

In accordance with National Instrument 81-107, Independent Review Committee for Investment Funds (“NI 81-107”), the Manager has established an IRC for a number of funds managed by it, including the Trusts. The mandate of the IRC is to consider and provide recommendations to the Manager on conflicts of interest to which the Manager is subject when managing certain funds, including the Trusts. The IRC is composed of three individuals, each of whom is independent of the Manager and all funds managed by the Manager, including the Trusts. Each fund subject to IRC oversight pays a share of the IRC member fees, costs and other fees in connection with operation of the IRC. The IRC reports annually to unitholders of the funds subject to its oversight on its activities, as required by NI 81-107.

10. Personnel

The Trusts did not employ any personnel during the period, as their affairs were administered by the personnel of the Manager and/or the Trustee, as applicable.

18

Corporate Information

Head Office

Sprott Physical Silver Trust

Royal Bank Plaza, South Tower

200 Bay Street

Suite 2600, PO Box 26

Toronto, Ontario M5J 2J1

Telephone: (416) 203-2310

Toll Free: (877) 403-2310

Email: ir@sprott.com

Auditors

KPMG LLP

Bay Adelaide Centre

333 Bay Street

Suite 4600

Toronto, Ontario M5H 2S5

Legal Counsel

Baker & McKenzie LLP

Brookfield Place

Bay Wellington Tower

181 Bay Street, Suite 2100

Toronto, Ontario Canada M5J 2T3

Seward & Kissel LLP

901 K Street NW, 8th Floor

Washington, DC 20001