Use these links to rapidly review the document

Table of Contents

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on February 18, 2014

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Nord Anglia Education, Inc.

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant's name into English)

| Cayman Islands (State or other jurisdiction of incorporation or organization) |

8200 (Primary Standard Industrial Classification Code Number) |

Not Applicable (I.R.S. Employer Identification Number) |

Level 27, World-Wide House

19 Des Voeux Road

Central, Hong Kong

+852-3977-0765

(Address, including zip code, and telephone number, including area code, of Registrant's principal executive offices)

Law Debenture Corporate Services Inc.

400 Madison Avenue, 4th Floor

New York, New York 10017

+1 (212) 750-6474

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||||||

Marc D. Jaffe, Esq. Ian D. Schuman, Esq. Latham & Watkins LLP 885 Third Avenue New York, New York 10022 +1 (212) 906-1281 |

Eugene Y. Lee, Esq. Latham & Watkins 18/F One Exchange Square 8 Connaught Place Central, Hong Kong +852-2912-2515 |

Rod Miller, Esq. Milbank, Tweed, Hadley & McCloy LLP 1 Chase Manhattan Plaza New York, New York 10005 +1 (212) 530-5022 |

Joshua M. Zimmerman, Esq. Milbank, Tweed, Hadley & McCloy 30/F Alexandra House 18 Chater Road Central, Hong Kong +852-2971-4811 |

|||

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earliest effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

|

||||

| Title of each class of securities to be registered |

Proposed maximum aggregate offering price(1) |

Amount of registration fee |

||

|---|---|---|---|---|

Ordinary shares, par value $0.01 per share(2) |

$300,000,000 | $38,640 | ||

|

||||

- (1)

- Estimated

solely for the purpose of determining the amount of registration fee in accordance with Rule 457(o) under the Securities Act.

- (2)

- Includes (i) ordinary shares initially offered and sold outside the United States that may be resold from time to time in the United States either as part of their distribution or within 40 days after the later of the effective date of this registration statement and the date the shares are first bona fide offered to the public and (ii) ordinary shares that may be purchased by the underwriters pursuant to an option to purchase additional ordinary shares. The ordinary shares are not being registered for the purposes of sales outside of the United States.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, or until the registration statement shall become effective on such date as the Commission, acting pursuant to such Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED , 2014

Ordinary Shares

Nord Anglia Education, Inc.

This is the initial public offering of our ordinary shares. We are offering ordinary shares. We expect the initial public offering price to be between $ and $ per share.

We have applied to list our ordinary shares on the New York Stock Exchange under the symbol "NORD".

The underwriters have an option to purchase up to an additional shares from us to cover over-allotments, at the initial public offering price less underwriting discounts and commissions, within 30 days from the date of this prospectus.

We are an "emerging growth company" under the U.S. federal securities laws and will be subject to reduced public reporting requirements. Investing in our ordinary shares involves risks. See "Risk Factors" beginning on page 20 of this prospectus.

|

||||||

| |

Initial public offering price |

Underwriting discounts and commissions(1) |

Proceeds, before expenses, to us |

|||

|---|---|---|---|---|---|---|

Per share |

$ | $ | $ | |||

Total |

$ | $ | $ | |||

|

||||||

- (1)

- See "Underwriting" for details of compensation to be received by the underwriters.

The underwriters expect to deliver the ordinary shares to purchasers on or about , 2014.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse | Goldman, Sachs & Co. | J.P. Morgan |

| Barclays | Deutsche Bank Securities | RBC Capital Markets | BMO Capital Markets | |||

HSBC |

William Blair |

|||||

The date of this prospectus is , 2014

You should rely only on the information contained in this prospectus or in any related free writing prospectus that we have filed with the SEC. Neither we nor the underwriters have authorized anyone to provide you with information that is different. If anyone provides you with different or inconsistent information, you should not rely on it. This prospectus may only be used where it is legal to offer and sell these securities. Unless otherwise indicated, the information in this document may only be accurate as of the date of this document.

We have not taken any action to permit a public offering of our ordinary shares outside the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about and observe any restrictions on the offering of our ordinary shares and the distribution of this prospectus outside the United States.

Until , 2014 (25 days after commencement of this offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers' obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

i

The following summary highlights selected information appearing elsewhere in this prospectus and should be read in conjunction with the more detailed information and financial statements appearing elsewhere in this prospectus. You should read the entire prospectus carefully, including our financial statements and the related notes and the sections entitled "Risk Factors" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" before deciding whether to buy our ordinary shares. Unless otherwise specified or the context requires otherwise, the terms "we," "us," and "our" refer to Nord Anglia Education, Inc., its predecessor, and their respective consolidated subsidiaries; "China" and "PRC" refer to the People's Republic of China, excluding Taiwan, Hong Kong and Macau; and "$" and "dollars" refer to the legal currency of the United States. Operating data concerning students and "FTEs" relate to full-time equivalent students. Our fiscal year ends August 31 for all periods presented. This prospectus contains information from reports we commissioned from The Parthenon Group LLC, a global consulting firm and one of our shareholders, in 2013 and 2012; unless otherwise indicated, references to Parthenon are to the 2013 report.

Our Business

We believe we are the world's leading international operator of premium schools. As of February 16, 2014, we had over 17,000 students, and in fiscal 2013 our average revenue per student was approximately $26,600. We teach children from kindergarten through the end of secondary school ("K-12") at our 27 premium schools in China, Europe, the Middle East and Southeast Asia ("ME/SEA") and North America. Parthenon estimates that globally K-12 premium schools teaching primarily in English generated revenue of approximately $58 billion in the 2012/2013 academic year. We define premium schools as schools charging at least $10,000 per year in tuition fees. We primarily operate in geographic markets with high foreign direct investment ("FDI"), large expatriate populations and rising disposable incomes. We believe that these factors contribute to high demand for premium schools and strong growth in our business. Our student enrollment increased at a compound annual growth rate ("CAGR") of 29% from the end of fiscal 2008 to the end of fiscal 2013.

Our commitment to quality drives our strong operating performance. Almost all of our schools teach the English National Curriculum, and our principals, teachers and support staff strive to maximize every student's academic performance. Although our admissions policy is not based on academic ability, and English is not the first language of many of our students, our students' standardized examination results exceed global averages. In 2013, nearly one out of five of our graduates matriculated to one of the world's top 30 universities, as ranked by QS World University Rankings. Our academic quality helps us maintain our market-leading position, supports our premium pricing and drives consistent enrollment growth.

Our schools derive all of their revenue from private sources and therefore are not exposed to government funding risk. As of November 30, 2013, 73% of our students were expatriates and 27% were from local families. Employers of expatriates fund most of our tuition fees as part of expatriate compensation packages, through allowances or direct payments to our schools. Education benefits are often key recruitment incentives for expatriate employees.

Our attractive business model leads to good visibility, price inelasticity, low capital requirements and strong cash generation. Our average student tenure of 3.5 years provides good visibility on future enrollments and revenues. Our private-pay model and the importance of education to parents make us resilient to changing economic conditions and government policies. We have been able to increase tuition fees at an average of approximately 4-6% per annum over the last three years. Our capital-light approach to growth enables us to generate high returns on capital. We focus on securing high-quality, purpose-built schools through long-term leases, with the construction costs of many of our schools funded by real estate developers desiring premium schools within their residential and commercial

1

developments. Our strong margins make our business highly cash generative. We received approximately 55% of our fiscal 2013 schools' revenue before August 31, 2012.

We have grown our business significantly since the 2008 financial crisis, despite a challenging global economic climate. We increased our student capacity and enrollments from 5,393 places and 4,010 students as of August 31, 2008 to 21,737 places and 17,109 students as of February 16, 2014. During that period, we expanded capacity at our existing schools by 1,980 places, developed two greenfield schools with a total of 3,000 places and acquired 19 schools with a total of 11,364 places.

On May 22, 2013, we purchased 100% of the share capital of WCL Group Limited and acquired its 11 schools in North America, the Middle East and Europe. This acquisition enabled us to enter the North American market and strengthened our position in the Middle East and Europe. Giving pro forma effect to our acquisition of WCL Group as though it had been completed on September 1, 2012, in fiscal 2013 we generated $415.0 million of pro forma revenue, $103.4 million of pro forma Adjusted EBITDA and $16.0 million of pro forma loss for the year. See "Unaudited Pro Forma Condensed Consolidated Financial Information."

For the three months ended November 30, 2013, we had revenue of $135.1 million, profit for the period of $3.5 million and Adjusted EBITDA of $38.7 million.

In fiscal 2013, our schools in China, Europe, ME/SEA and North America contributed 36.0%, 33.4%, 14.4% and 16.3% of our schools' pro forma revenue, respectively.

The following table shows our regional enrollments as of February 16, 2014:

| |

February 16, 2014 | % of Total | |||||

|---|---|---|---|---|---|---|---|

Full-time equivalent students: |

|||||||

China |

4,826 | 28% | |||||

Europe |

4,494 | 26% | |||||

Middle East/South East Asia |

5,045 | 30% | |||||

North America |

2,744 | 16% | |||||

Total |

17,109 | 100% | |||||

Our Market Opportunity

We compete in the large, growing and highly fragmented market for premium schools that teach primarily in English. Parthenon estimates that in the 2012/2013 academic year, there were approximately 9,000 schools globally teaching primarily in English that charged tuition fees of $10,000 or more per year. According to Parthenon, these schools generated revenue of approximately $58 billion. Parthenon estimates that of the 150 largest premium school markets, more than 40 grew enrollments at over 10% annually between 2009 and 2013. Despite the large number of premium schools, operators with two or more campuses constitute only approximately 11% of the global market, according to Parthenon.

We primarily target geographic markets with high FDI, large expatriate populations and rising disposable incomes, all of which increase demand for premium schools. Employers of expatriates fund most of our tuition fees. Companies that rely on expatriate employees view the availability of high-quality schools as vital to recruiting and retaining key employees. According to a 2013 survey by Brookfield Global Relocation Services, 89% of corporate respondents viewed education as either very critical or highly important to prospective employees considering international assignments. In addition, many governments and business and trade associations actively promote premium international schools in their jurisdictions, recognizing that the availability of premium quality education for the children of expatriate employees is critical to attracting FDI from corporations.

2

A majority of premium schools are family-owned and operated or managed by foundations. Family operators and foundations typically focus on academic performance, exclusivity and prestige. These operators have historically been reluctant to add capacity even when demand in their markets exceeds supply, leaving significant opportunities for companies that operate schools with high academic standards while also focusing on financial performance and growth.

Competitors seeking to enter the premium school market face significant barriers to entry, including:

- •

- the lead time required to build brand recognition and reputation, both locally and globally;

- •

- the challenges unproven operators face in securing government licenses and regulatory approval in many jurisdictions;

- •

- in many markets, the scarcity of real estate in desirable areas that can accommodate a sizeable campus with the

comprehensive and high-quality facilities expected of premium schools;

- •

- the tendency of property developers and landlords to require school operators with significant financial resources and a

reputation for quality in order to enhance the value of their adjacent residential or retail real estate; and

- •

- the tendency of students to stay enrolled in the same school until they graduate or their parents relocate.

We believe increasing globalization and a growing emphasis by parents on high-quality education for their children will drive strong growth in many markets. There are few premium-quality operators with the global scale required to benefit from this attractive opportunity.

Our Strengths

Global Market Leadership

We believe we are the world's leading international operator of premium schools, with a network of 27 premium schools in 23 locations in 11 countries. We are a trusted partner of key stakeholders, including governments, sellers of premium schools and real estate developers, and enjoy significant benefits of scale.

Our strong reputation among governmental authorities, which recognize the importance of premium schools in attracting FDI, helps us secure schools in prime education markets. For example, in April 2013, following an extensive tender process, the Hong Kong Education Bureau awarded us a vacant school site in Kowloon, Hong Kong. This school was one of three allocated by the Hong Kong Education Bureau in 2013, and we were the only school operator without an established school in Hong Kong to be granted a campus. We expect to open the school in September 2014 with a capacity of approximately 720 places.

Sellers of premium schools often focus on the operating record, financial stability and reputation of potential buyers. Our acquisitions in China, Switzerland and Thailand resulted from exclusive discussions with sellers who were primarily concerned with the success and reputation of their schools under their new owners. In addition, real estate developers and landlords seek school operators with a reputation for quality in order to enhance the value of their adjacent residential or retail real estate. For example, in Shanghai-Puxi we collaborated with a developer and the local government, who were eager to develop Puxi into an attractive location for expatriates. We started the school in 2005 with a capacity of 668 places and have increased capacity to 2,000 places, with all of the building expansion costs funded by the developer.

3

Our market leadership and scale also enable us to:

- •

- recruit, develop and retain top-quality principals and teachers;

- •

- set tuition fees at the high end of each market;

- •

- apply best practices throughout our network, including cost management and control through benchmarking;

- •

- stay at the forefront of educational theory through our centralized education team and achieve educational synergies from

a British-style education based upon the English National Curriculum at almost all of our schools; and

- •

- offer initiatives, such as the Global Classroom, which develop our students into world-ready, global citizens.

Premium Quality Education with Strong Brand Recognition

Our schools have excellent reputations and are among the most respected premium K-12 school brands in their markets. We focus on the needs of individual students and track each student's performance against personalized targets to help maximize every student's academic achievement.

Our approach to education and the benefits of belonging to a global network of premium schools help to distinguish our schools from our competitors. For example, we have developed a supplementary online learning environment, the Global Classroom, which is accessible to all of our students. The Global Classroom is an Internet-based system that complements our curricula and allows our students to interact online with experts in various fields and collaborate with students at any of our schools around the world. This innovative learning environment creates independent learners, prepares students for future university study and helps them to become global citizens.

Although our admissions policy is not based on academic ability, and English is not the first language of many of our students, our students' standardized examination results exceed global averages. In 2013, our International Baccalaureate Diploma Program ("IBDP") pass rate equaled 91.0% compared to the IB World Average of 78.5%, and 11.5% of our IBDP students scored over 40 points out of 45, compared with the IB World Average of 6.6%. In 2013, nearly one out of five of our graduates matriculated to one of the world's top 30 universities, as ranked by QS World University Rankings.

Our reputation for quality and distinctive approach to education result in high referral rates: 90% of parents of children at our schools whom we surveyed in the academic year 2012/2013 reported that they would recommend our schools. Our reputation and attention to individual students are key to parents who choose our schools over competing schools.

Our principals and teaching staff are highly qualified and experienced, and we recruit them through a rigorous hiring process. We are able to attract highly qualified staff through our international scale, reputation for quality and competitive compensation packages. We emphasize on-going professional development and a policy to promote from within to attract and retain teachers. Initiatives such as Nord Anglia University, which provides comprehensive professional training programs for teachers and principals, underscore our commitment to professional development. We believe the quality and motivation of our teachers form the foundation for the outstanding education we provide.

Superior Business Model

Our business model emphasizes operational efficiency and uses a data-driven approach to drive student achievement, growth and profitability. Our global, regional and school teams track and analyze key performance indicators and we refine our operating strategy accordingly.

4

We focus on the following key areas of our operations:

- •

- Academic quality assurance: We monitor the academic

quality of our schools and assess the quality of schools we acquire through a structured quality review framework that includes an annual review by our central Schools' Academic Performance Board. In

addition, we perform ad hoc assessments of schools as required. We evaluate the achievement of students, the quality of teaching, the behaviour and safety of students, the quality of school

leadership and management and overall effectiveness.

- •

- Student recruitment: We have a systematic approach to

student recruitment. Our comprehensive recruitment strategies are adapted to each school's local market and executed by each school's principal, admissions team and marketing manager. We use a

relationship management system to monitor an applicant's file from initial inquiry through enrollment.

- •

- Pricing: We monitor local market trends, including

economic developments and supply and demand dynamics, to set tuition fees.

- •

- Cost management: We use metrics-based management

throughout our school operations to enhance efficiencies. We achieve operational efficiencies through various means, including efficient class scheduling and optimizing our teaching resources. We

accomplish this by minimizing teachers' administrative responsibilities, allowing them to spend more time focused on teaching.

- •

- Capacity planning: Our expertise in planning and adding capacity to meet demand enables us to manage growth by efficiently utilizing capacity at existing schools and expanding as necessary. We also work with architectural consultants who specialize in optimizing school configurations. Our approach to growing our network of schools is highly analytical, includes the use of demographic and economic models and we often commission third-party market research to identify opportunities for expansion.

We use a balanced scorecard of key performance indicators that measures each school's performance from the perspective of all stakeholders, including parents, students, teachers and investors. Our balanced scorecard evaluates each school based on student safety, student performance, financial performance, staff performance and marketing and admissions. By regularly monitoring key performance indicators at each school, we can ensure that its operations meet our expectations. We learn of potential problems at any school in real time and intervene as required. This helps us maintain consistency across our schools and allows us to quickly integrate newly acquired or greenfield schools, which makes our business highly scalable.

Capital-Light, Returns-Focused Approach to Growth

We have significantly grown our business while driving high returns on capital. Our capital-light expansion strategy focuses on securing high-quality, purpose-built schools through long-term leases, with the construction cost of many of our schools funded by real estate developers. When we acquire existing schools, we often acquire the operating businesses and enter into long-term leases with the sellers who retain ownership of the real estate. In fiscal 2013, our pro forma return on capital ("ROC"), calculated as adjusted operating profit divided by adjusted invested capital, was 28.0%. ROC is a non-IFRS measure. For additional information, including a calculation of ROC, see "—Summary Historical and Pro Forma Consolidated Financial and Operating Data."

Highly Attractive Financial Profile

- •

- High Visibility and Predictability: We operate a highly visible and predictable business. Average student tenure across our network in the last three years was 3.5 years. In our latest academic year we lost only 3% of our students for reasons related to academic quality, student needs or tuition levels, based on parent responses to our exit surveys. At a majority of our schools, our

5

terms and conditions require a full term's notice of withdrawal for a refund of prepaid tuition. The final academic term at most of our schools starts in April of each year and historically we have had few requests for refunds. We track inquiries and visits to estimate new enrollments. In fiscal 2013, we converted 62% of prospective student visits to our schools into enrollments (excluding schools acquired in 2013). As a result, we can estimate in-year and year-to-year student re-enrollment, new enrollment and revenue.

- •

- Favorable Working Capital Dynamics: We received

approximately 55% of our fiscal 2013 schools' revenue before August 31, 2012. We collected an additional 24% of our schools' revenue prior to January 2013, and an additional 13% prior to

April 2013. The timing of our schools' revenue collection allows us to finance our operating expenses principally with pre-paid tuition fees.

- •

- Price Inelasticity Supported by Private-Pay Model: We

have been able to increase our tuition fees at an average of approximately 4-6% per annum over the last three years (which exceeds the median rate of inflation in the markets where our schools are

located), while continuing to grow enrollment organically. Our private-pay model insulates our schools from volatility in government funding resulting from changing economic conditions or policies.

The high quality of our schools supports our premium pricing. Most of our tuition fees are directly or indirectly paid by employers, who we believe accept price increases because education allowances

typically represent only a small percentage of an expatriate's total compensation. We believe self-funding expatriates and affluent local families also accept our price increases because of the

importance they place on a quality education for their children.

- •

- Strong Margins: Our premium pricing and operating efficiencies result in strong margins. For the three months ended November 30, 2013, our Adjusted EBITDA margin was 28.6%. In fiscal 2013 our pro forma Adjusted EBITDA margin was 24.9%. With capacity utilization of 79% as of February 16, 2014, we have significant scope to expand our margins by growing enrollments without increasing capacity.

Experienced Management Team with Local and Global Expertise

Our management team combines seasoned executives with experience in running publicly listed companies and leading education specialists. Andrew Fitzmaurice has been our CEO for more than ten years and was CEO when Nord Anglia Education plc was listed on the main board of the London Stock Exchange. Over the last several years, we have bolstered our senior management team with a number of significant appointments, including our corporate development director, education director, human resources director and director of student recruitment. Our senior management team is supported by experienced regional managers and local school administrators who implement our operating philosophy in each of our markets.

Our Strategies

Continue to Deliver High-Quality Education and Strong Outcomes for Students

Our commitment to quality will remain the foundation of our operating performance and growth. We will continue to offer our students an excellent education, recruit and retain experienced and highly qualified principals and teachers and strive to help each student achieve high academic performance. We believe that building upon our reputation for quality and ensuring that our schools live up to the expectations of students and parents are key to strengthening our position as the world's leading international operator of premium schools.

Increase Student Enrollments at Our Existing Schools

We aim to continue to increase enrollments by applying our systematic processes for generating inquiries, converting inquiries to enrollments and retaining existing students. Our school principals lead

6

the recruitment effort with dedicated admissions and marketing teams. We generate inquiries and visits through referrals and digital and other marketing activities. In fiscal 2013, we converted 62% of prospective student visits to our schools into enrollments (excluding schools acquired in fiscal 2013).

Continue Price Leadership

We will continue to invest in our teachers and campuses to enable us to consistently provide high-quality premium education. Improving our schools supports our strong reputation in the markets where we operate, which we expect will allow us to continue increasing prices in excess of inflation.

Increase Capacity

Using our capital-light, returns-focused approach, we plan to continue expanding capacity at existing schools, opening new campuses on greenfield sites and pursuing acquisitions.

- •

- Capacity Expansion at Our Existing Schools. We intend to

expand capacity at our existing schools where market demand supports additional places. We will continue to develop our relationships with real estate developers and landlords, who we expect will

continue to fund the vast majority of our capacity expansion. Our systematic approach to capacity expansion has enabled us to add 1,980 places to existing schools since August 31, 2008,

including expansions at our schools in Shanghai-Pudong, Shanghai-Puxi and Beijing-Shunyi, which were funded by real estate developers.

- •

- Greenfield Expansion in Existing and

New Markets. We will continue to strategically open new schools in markets where we currently operate and in attractive new

markets. We have successfully completed seven greenfield projects since 1992 and have three greenfield projects under development. For example, we plan to take advantage of market demand in

Chicago by building a second campus with approximately 1,000 places, more than doubling our capacity. On December 13, 2013, we entered into agreements with a real estate developer who will

build the new campus to our specifications, and we expect to open the new campus in September 2015.

In many new markets, our global market leadership and premium quality attract inquiries from governments, real estate developers and landlords. Governments and business and trade associations recognize that the availability of premium quality education for the children of expatriate employees is critical to attracting FDI from corporations. For example, in 2007, the China Britain Business Council approached us to partner with a local developer in order to develop our school in Beijing-Shunyi. More recently, in April 2013, following an extensive tender process, the Hong Kong Education Bureau awarded us a vacant school in Kowloon, Hong Kong. In Dubai, a landholder who obtained a site specifically for the development of an international school chose us from among several candidates to operate the new school. The landholder is now developing a state-of-the-art school to our specifications and will become our landlord upon its completion. We expect to open the school in September 2014 with a capacity of approximately 1,500 places.

- •

- Pursue Acquisitions. According to Parthenon, single-site

operators comprise approximately 89% of the premium schools market. The abundance of single-site operators provides a continuous supply of incremental acquisition opportunities. Potential sellers

often engage with us in exclusive negotiations because of our reputation, success at integrating schools, capital resources and interest in keeping sellers involved as landlords and consultants

without the ongoing responsibility of operating the school.

We evaluate each potential acquisition using a returns-based approach focused upon the school's quality, reputation, curriculum, local market dynamics, tuition levels, financial position and opportunities for growth. Once we acquire a school, our proven operating model drives educational improvements, enrollment growth and operational efficiencies. We have a highly

7

successful record of acquiring and integrating schools, having purchased and integrated 19 schools since the end of fiscal 2008. Since we acquired these schools, their Adjusted EBITDA has grown at an average CAGR of approximately 26% (excluding schools we have owned for less than 12 months).

Risks Related to Our Business

Our ability to achieve our goals and execute our strategies is subject to risks and uncertainties. We believe the following are the major risks and uncertainties that may materially affect us:

- •

- changes in our key industry drivers, globalization and FDI, may materially adversely affect our business;

- •

- increased competition in the premium school market could reduce our enrollments;

- •

- our inability to increase or maintain our tuition fees may materially adversely affect our financial

performance; and

- •

- damage to our reputation, including as a result of our staff failing to appropriately supervise children under their care, could reduce our enrollments.

See "Risk Factors" and "Special Note Regarding Forward-Looking Statements" for detailed discussions of these and other risks and uncertainties associated with our business and investing in our ordinary shares.

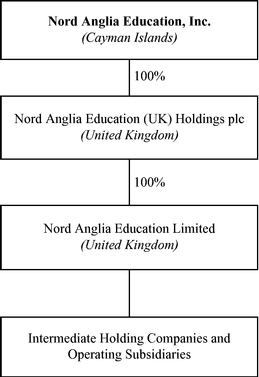

Corporate History

Our controlling shareholder is Premier Education Holdings, which is controlled by The Baring Asia Private Equity Fund IV ("Baring Private Equity Asia").

Our business was founded in 1972. From 1997 through August 2008, we conducted business as Nord Anglia Education plc, whose shares were listed on the main board of the London Stock Exchange. In August 2008, Nord Anglia Education plc was acquired in a going-private transaction led by Baring Private Equity Asia. Premier Education (UK) Holdco Limited, renamed "Nord Anglia Education (UK) Holdings plc" in 2012, was the buying consortium's ultimate holding vehicle that owned the acquiring entity that purchased all the shares in Nord Anglia Education plc. After the acquisition, Nord Anglia Education plc was delisted and renamed "Nord Anglia Education Limited." We, Nord Anglia Education, Inc., were incorporated in 2011, and in 2012 shareholders of Nord Anglia Education (UK) Holdings plc swapped their shares for shares in our company.

Corporate Information

Our principal executive offices are located at Level 27, World-Wide House, 19 Des Voeux Road, Central, Hong Kong. Our telephone number at this address is +852-3977-0765. Our registered office is located at Maples Corporate Services Limited, P.O. Box 309, Ugland House, Grand Cayman, KY1-1104, Cayman Islands.

Investor inquiries should be directed to us at the address and telephone number of our principal executive offices. Our website is www.nordanglia.com. The information contained on or accessible through our website does not constitute part of this prospectus. Our agent for service of process in the United States is Law Debenture Corporate Services Inc., 400 Madison Avenue, 4th Floor, New York, New York 10017.

Implications of Being an Emerging Growth Company

As a company with less than $1 billion in revenue during our last fiscal year, we qualify as an "emerging growth company" as defined in the Jumpstart Our Business Startups Act of 2012 (the "JOBS Act"). For so long as we remain an emerging growth company, we are permitted to rely on

8

exemptions from some of the reporting requirements that are applicable to public companies that are not emerging growth companies. These exemptions include:

- •

- being permitted to provide only two years of selected financial data (rather than five years) and only two years of

audited financial statements (rather than three years), in addition to any required unaudited interim financial statements, with correspondingly reduced "Management's Discussion and Analysis of

Financial Condition and Results of Operations" disclosure; and

- •

- not being required to comply with the auditor attestation requirements of the Sarbanes-Oxley Act of 2002 in the assessment of our internal control over financial reporting.

We may take advantage of these reporting exemptions until we are no longer an emerging growth company. We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following the fifth anniversary of the completion of this offering, (b) in which we have total annual gross revenue of at least $1 billion or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common stock that is held by non-affiliates exceeds $700 million as of the prior June 30, and (2) the date on which we have issued more than $1 billion in non-convertible debt during the prior three-year period. We may choose to take advantage of some, but not all, of the available exemptions. We have included three years of selected financial data in this prospectus in reliance on the first exemption described above. Accordingly, the information contained herein may be different than the information you receive from other public companies in which you hold stock.

In addition, under the JOBS Act, emerging growth companies can delay adopting new or revised accounting standards issued by the Financial Accounting Standards Board until those standards apply to private companies. We have irrevocably elected not to avail ourselves of this exemption from new or revised accounting standards. Because we prepare our financial statements in accordance with International Financial Reporting Standards as issued by the International Accounting Standards Board ("IFRS"), accounting standards issued by the Financial Accounting Stands Board will not apply to us unless we adopt U.S. generally accepted accounting principles in place of IFRS or present a reconciliation of our financial statements to U.S. generally accepted accounting principles.

9

The Offering

Ordinary shares we are offering |

shares |

|

Ordinary shares outstanding immediately after this offering |

shares |

|

Use of Proceeds |

We estimate that the net proceeds from this offering will be approximately $ million, or $ million if the underwriters exercise their over-allotment option in full. We intend to use the net proceeds from this offering, together with borrowings under a new secured term loan facility that we intend to enter into at the close of this offering, to redeem in full our 10.25% senior secured notes due 2017 and our 8.50%/9.50% senior PIK toggle notes due 2018, and the remainder, if any, to partially redeem our preference shares held by Premier Education Holdings and members of our management. We refer to the refinancing of the notes as the "Refinancing" in this prospectus. See "Use of Proceeds" and "Management's Discussion and Analysis of Financial Condition and Results of Operations—Debt—Refinancing of Notes." |

|

Proposed New York Stock Exchange symbol |

NORD |

The number of ordinary shares outstanding immediately after this offering assumes:

- •

- in accordance with our articles of association currently in effect, the redemption at par value of deferred shares and

redeemable A ordinary shares from Premier Education Holdings Limited and other classes of redeemable ordinary shares from other shareholders to give effect to a ratchet mechanism that increases the

percentage shareholding of certain shareholders, primarily our management and employees, upon the closing of this offering;

- •

- the conversion of all classes of preference shares, including one preference share to be issued to Premier Education

Holdings immediately prior to the completion of this offering in exchange for $31.1 million of debt, into redeemable A ordinary shares upon the closing of this offering (see "Related Party

Transactions—Relationship with Baring Private Equity Asia—Debt"); and

- •

- the conversion of all classes of redeemable ordinary shares into ordinary shares, par value $0.01 per share, upon the closing of this offering.

The partial redemption, if any, of our preference shares with the proceeds of this offering will occur prior to the conversion of our redeemable ordinary shares into ordinary shares, par value $0.01 per share, upon the closing of this offering and will not affect the number of ordinary shares offered hereby or the number of ordinary shares outstanding following the completion of this offering.

Following the completion of this offering, we will have one class of shares outstanding.

The number of ordinary shares outstanding immediately after this offering excludes additional ordinary shares reserved for future grants under our stock option plan.

Unless otherwise indicated, all information in this prospectus assumes no exercise by the underwriters of their option to purchase up to an additional ordinary shares.

10

Summary Historical and Pro Forma Consolidated Financial and Operating Data

The following historical summary consolidated income statement data for the years ended August 31, 2011, 2012 and 2013 and consolidated balance sheet data as of August 31, 2012 and 2013 have been derived from our audited consolidated financial statements included elsewhere in this prospectus. Our historical summary consolidated income statement data for the three months ended November 30, 2012 and 2013 and consolidated balance sheet data as of November 30, 2013 have been derived from our unaudited interim consolidated financial statements included elsewhere in this prospectus. Our consolidated financial statements have been prepared in accordance with IFRS. The historical financial information presented below for periods prior to May 22, 2013, the date on which we acquired WCL Group, does not reflect the acquisition or WCL Group's results of operations.

We have adopted IAS 19 Employee Benefits (revised) ("IAS 19") prospectively effective September 1, 2013 in our unaudited interim consolidated financial statements as of November 30, 2013 and for the period ended November 30, 2013. We have not restated our audited consolidated financial statements for the years ended August 31, 2011, 2012 and 2013 and our unaudited interim consolidated financial statements for the quarter ended November 30, 2012 as the impact of this revised standard is not material to our results of operations and financial position.

The following unaudited pro forma summary consolidated income statement data for the year ended August 31, 2013 and the three months ended November 30, 2012 give effect to our acquisition of WCL Group as though it had occurred on September 1, 2012. The historical and pro forma financial and operating results presented below are not necessarily indicative of our results for any future fiscal period. You should read the summary consolidated financial data set forth below in conjunction with "Unaudited Pro Forma Condensed Consolidated Financial Information," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and our and WCL Group's consolidated financial statements and related notes included elsewhere in this prospectus.

11

| |

For the year ended August 31, | For the three months ended November 30, |

||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2013 | 2012 | 2012 | 2013 | |||||||||||||||

| |

Actual | Actual | Actual | Pro forma | Actual | Pro forma | Actual | |||||||||||||||

| |

|

|

|

(unaudited) |

(unaudited) |

(unaudited) |

(unaudited) |

|||||||||||||||

| |

(in millions of dollars, except per share data) |

|||||||||||||||||||||

Consolidated Income Statement Data: |

||||||||||||||||||||||

Revenue |

225.2 | 274.4 | 323.7 | 415.0 | 89.1 | 117.9 | 135.1 | |||||||||||||||

Cost of sales |

(105.0 | ) | (126.5 | ) | (147.6 | ) | (189.8 | ) | (40.7 | ) | (54.4 | ) | (61.9 | ) | ||||||||

Gross Profit |

120.2 | 147.9 | 176.1 | 225.2 | 48.4 | 63.5 | 73.2 | |||||||||||||||

Selling, general and administrative expenses(1) |

(78.1 | ) | (84.6 | ) | (96.0 | ) | (131.3 | ) | (22.1 | ) | (29.9 | ) | (38.2 | ) | ||||||||

Depreciation |

(7.2 | ) | (9.9 | ) | (11.7 | ) | (16.0 | ) | (2.6 | ) | (4.1 | ) | (5.3 | ) | ||||||||

Amortization |

(2.8 | ) | (3.5 | ) | (5.7 | ) | (8.8 | ) | (0.9 | ) | (1.9 | ) | (2.4 | ) | ||||||||

Impairment of goodwill |

(16.7 | ) | (10.7 | ) | — | — | — | — | — | |||||||||||||

Exceptional items |

(9.4 | ) | (12.5 | ) | (17.7 | ) | (9.1 | ) | (1.0 | ) | (1.0 | ) | (1.6 | ) | ||||||||

Total selling, general and administrative expenses |

(114.2 | ) | (121.2 | ) | (131.1 | ) | (165.2 | ) | (26.6 | ) | (36.9 | ) | (47.5 | ) | ||||||||

Operating profit |

6.0 | 26.7 | 45.0 | 60.0 | 21.8 | 26.6 | 25.7 | |||||||||||||||

Finance income |

10.1 | 2.0 | 2.3 | 2.3 | 0.6 | 0.6 | 0.6 | |||||||||||||||

Finance expense |

||||||||||||||||||||||

- Shareholder loan notes accrued interest |

(36.8 | ) | (25.4 | ) | — | — | — | — | — | |||||||||||||

- Bank loans, notes and overdrafts |

(12.9 | ) | (22.9 | ) | (50.9 | ) | (59.3 | ) | (9.5 | ) | (12.3 | ) | (16.5 | ) | ||||||||

- Other finance expenses |

(2.0 | ) | (1.4 | ) | (0.4 | ) | (0.4 | ) | (0.1 | ) | (0.1 | ) | (0.2 | ) | ||||||||

Total finance expense(2) |

(51.7 | ) | (49.7 | ) | (51.3 | ) | (59.7 | ) | (9.6 | ) | (12.4 | ) | (16.7 | ) | ||||||||

Net financing expense |

(41.6 | ) | (47.7 | ) | (49.0 | ) | (57.4 | ) | (9.0 | ) | (11.8 | ) | (16.1 | ) | ||||||||

(Loss)/profit before tax |

(35.6 | ) | (21.0 | ) | (4.0 | ) | 2.6 | 12.8 | 14.8 | 9.6 | ||||||||||||

Income tax expense |

(12.5 | ) | (16.4 | ) | (19.3 | ) | (18.6 | ) | (5.5 | ) | (5.0 | ) | (6.1 | ) | ||||||||

(Loss)/profit for the period |

(48.1 | ) | (37.4 | ) | (23.3 | ) | (16.0 | ) | 7.3 | 9.8 | 3.5 | |||||||||||

(Loss)/profit per share attributable to equity holders (in dollars) |

||||||||||||||||||||||

Basic (loss)/profit per share |

(0.38 | ) | (0.27 | ) | (0.27 | ) | (0.22 | ) | 0.05 | 0.07 | 0.02 | |||||||||||

Diluted loss per share |

(1.26 | ) | (1.17 | ) | (1.24 | ) | (1.00 | ) | 0.05 | 0.07 | 0.02 | |||||||||||

12

| |

As of August 31, | |

||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| |

As of November 30, 2013 | |||||||||

| |

2012 | 2013 | ||||||||

| |

|

|

(unaudited) |

|||||||

| |

(in millions of dollars) |

|||||||||

Consolidated Balance Sheet Data: |

||||||||||

Cash and cash equivalents |

108.5 | 171.1 | 131.4 | |||||||

Other current assets |

49.6 | 84.2 | 85.5 | |||||||

Total non-current assets |

508.7 | 870.7 | 877.7 | |||||||

Total assets |

666.8 | 1,126.0 | 1,094.6 | |||||||

Current liabilities |

254.3 | 398.7 | 366.5 | |||||||

Total non-current liabilities |

368.7 | 707.3 | 700.3 | |||||||

Total equity |

43.8 | 20.0 | 27.8 | |||||||

Total equity and liabilities |

666.8 | 1,126.0 | 1,094.6 | |||||||

- (1)

- Excludes

depreciation, amortization, impairment of goodwill and exceptional items.

- (2)

- As described under "Management's Discussion and Analysis of Financial Condition and Results of Operations—Debt—Refinancing of Notes," we intend to refinance our notes with the proceeds of this offering and a new secured term loan facility. We expect that the new term loan facility will bear interest based on applicable margin percentages of % per annum for base rate loans and % per annum for LIBOR rate loans, provided that LIBOR may not be lower than %. Based on these anticipated interest rates, and assuming we use $ million of the net proceeds of this offering to redeem 35% of the notes and borrowings under the term loan facility to redeem the remainder of the notes, we estimate that (i) net finance expense attributable to the portion of the notes redeemed using offering proceeds, before taxes, would have decreased by approximately $ million, $ million and $ million for the year ended August 31, 2013, the three months ended November 30, 2013 and the three months ended November 30, 2012, respectively, and (ii) net finance expense attributable to the portion of the notes redeemed using borrowings under the new term loan facility would have decreased by approximately, $ million, $ million and $ million for the year ended August 31, 2013, the three months ended November 30, 2013 and the three months ended November 30, 2012, respectively. An increase (decrease) in the anticipated interest rates under the new term loan facility by 0.125% would decrease (increase) the net interest expense savings with respect to the portion of the notes redeemed with borrowings under the new term loan facility, before taxes, by $ million, $ million and $ million for the year ended August 31, 2013, the three months ended November 30, 2013 and the three months ended November 30, 2012, respectively. We expect to incur an exceptional charge of approximately $ million related to the redemption of our notes. The charge will be included in finance expense in the quarter in which we redeem the notes.

Based on the anticipated interest rates set forth above, assuming our new term loan facility had been fully drawn during the three months ended November 30, 2013, and that none of our notes were outstanding during the three months ended November 30, 2013, our net interest expense, before tax, for the period would have decreased by $ million. An increase (decrease) in the anticipated interest rates under the new term loan facility by 0.125% would decrease (increase) the net interest expense savings by $ million for the period.

13

| |

For the year ended August 31, | For the three months ended November 30, |

||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2012 | 2013 | |||||||||||

Key Operating Data:(1) |

||||||||||||||||

Full-time equivalent students (average for the period)(2) |

||||||||||||||||

China |

3,070 | 3,622 | 4,075 | 4,029 | 4,819 | |||||||||||

Europe |

3,412 | 3,775 | 4,448 | 4,448 | 4,502 | |||||||||||

Middle East/South East Asia |

572 | 783 | 3,364 | 3,261 | 4,902 | |||||||||||

North America |

— | — | 2,491 | 2,429 | 2,713 | |||||||||||

Total |

7,054 | 8,180 | 14,377 | 14,167 | 16,936 | |||||||||||

Capacity (average for the period)(3) |

||||||||||||||||

China |

4,860 | 5,360 | 5,375 | 5,360 | 6,964 | |||||||||||

Europe |

4,052 | 4,342 | 5,160 | 5,147 | 5,322 | |||||||||||

Middle East/South East Asia |

1,500 | 1,500 | 4,791 | 4,791 | 5,691 | |||||||||||

North America |

— | — | 3,660 | 3,660 | 3,760 | |||||||||||

Total |

10,412 | 11,202 | 18,986 | 18,958 | 21,737 | |||||||||||

Utilization (average for the period)(4) |

||||||||||||||||

China |

63 | % | 68 | % | 76 | % | 75 | % | 69 | % | ||||||

Europe |

84 | % | 87 | % | 86 | % | 86 | % | 85 | % | ||||||

Middle East/South East Asia |

38 | % | 52 | % | 70 | % | 68 | % | 86 | % | ||||||

North America |

— | — | 68 | % | 66 | % | 72 | % | ||||||||

Average |

68 | % | 73 | % | 76 | % | 75 | % | 78 | % | ||||||

Revenue per full-time equivalent student (in thousands of dollars)(5) |

||||||||||||||||

China |

27.9 | 30.8 | 33.8 | 9.6 | 9.8 | |||||||||||

Europe |

29.6 | 29.5 | 28.7 | 8.5 | 8.9 | |||||||||||

Middle East/South East Asia |

10.3 | 12.5 | 16.4 | 4.7 | 4.7 | |||||||||||

North America |

— | — | 25.0 | 7.2 | 7.4 | |||||||||||

- (1)

- For

fiscal 2013 and the three months ended November 30, 2012, the key performance indicators are presented as if our acquisition of WCL Group had

completed on September 1, 2012. For fiscal 2011, the key performance indicators are presented as if our acquisition of Collège Alpin Beau Soleil, Collège

Champittet-Lausanne and Collège Champittet-Nyon had completed on September 1, 2010.

- (2)

- We

calculate average FTEs for a period by dividing the total number of FTEs at each calendar month end in the period by the number of calendar months in

the period.

- (3)

- We

calculate average capacity for a period by dividing the total number of FTEs that can be accommodated in our schools based on their existing classrooms

at each calendar month end in the period by the number of months in the period.

- (4)

- We

calculate utilization for a period as a percentage equal to the ratio of average FTEs for the period divided by average capacity for the period.

- (5)

- We calculate revenue per FTE for a period by dividing revenue from our schools for the period by the average FTEs for the period.

14

| |

For the year ended August 31, | For the three months ended November 30, | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2013 | 2012 | 2012 | 2013 | |||||||||||||||

| |

Actual | Actual | Actual | Pro forma | Actual | Pro forma | Actual | |||||||||||||||

| |

|

|

|

(unaudited) |

(unaudited) |

(unaudited) |

(unaudited) |

|||||||||||||||

| |

(in millions of dollars, except percentages) |

|||||||||||||||||||||

Supplementary Financial Data: |

||||||||||||||||||||||

Adjusted EBITDA(1) |

||||||||||||||||||||||

Schools |

||||||||||||||||||||||

China |

40.8 | 53.8 | 66.8 | 66.8 | 18.9 | 18.9 | 21.7 | |||||||||||||||

Europe |

16.3 | 25.6 | 22.7 | 25.5 | 8.0 | 9.2 | 9.5 | |||||||||||||||

Middle East/South East Asia |

(5.6 | ) | (3.8 | ) | 5.9 | 11.8 | 1.2 | 2.5 | 6.1 | |||||||||||||

North America |

— | — | 0.3 | 18.3 | — | 5.7 | 7.1 | |||||||||||||||

Discontinuing(2) |

(0.4 | ) | (0.0 | ) | — | — | — | — | — | |||||||||||||

Total |

51.1 | 75.6 | 95.7 | 122.4 | 28.1 | 36.3 | 44.4 | |||||||||||||||

Other(3) |

13.7 |

10.3 |

6.6 |

7.6 |

2.2 |

2.2 |

0.5 |

|||||||||||||||

Central and regional expenses |

(16.9 | ) | (15.7 | ) | (22.8 | ) | (26.6 | ) | (4.6 | ) | (5.9 | ) | (6.2 | ) | ||||||||

Adjusted EBITDA |

47.9 | 70.2 | 79.5 | 103.4 | 25.7 | 32.6 | 38.7 | |||||||||||||||

Adjusted EBITDA Margin(4) |

21.3 | % | 25.6 | % | 24.6 | % | 24.9 | % | 28.8 | % | 27.7 | % | 28.6 | % | ||||||||

Adjusted Net Income(1) |

(14.0 |

) |

(4.4 |

) |

(1.3 |

) |

9.8 |

8.4 |

11.3 |

10.7 |

||||||||||||

Return on Capital(5) |

33.1 |

% |

25.0 |

% |

28.0 |

% |

||||||||||||||||

- (1)

- We use EBITDA, Adjusted EBITDA and Adjusted Net Income as supplemental financial measures of our operating performance. We define EBITDA as (loss)/profit for the year plus income tax expense, net financing (expense)/income, exceptional items, impairment of goodwill, amortization and depreciation, and we define Adjusted EBITDA as EBITDA adjusted for the items set forth in the table below. We define Adjusted Net Income as Adjusted EBITDA adjusted for the items in the table below. EBITDA, Adjusted EBITDA and Adjusted Net Income are not standard measures under IFRS. EBITDA, Adjusted EBITDA and Adjusted Net Income should not be considered in isolation or construed as alternatives to cash flows, net income or any other measure of financial performance or as indicators of our operating performance, liquidity, profitability or cash flows generated by operating, investing or financing activities. We may incur expenses similar to the adjustments in this presentation in the future and certain of these items could be recurring. EBITDA, Adjusted EBITDA and Adjusted Net Income presented herein may not be comparable to similarly titled measures presented by other companies. Set forth below is a reconciliation of EBITDA, Adjusted EBITDA and Adjusted Net Income to the most directly comparable IFRS measure, loss for the year.

15

| |

For the year ended August 31, | For the three months ended November 30, | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2011 | 2012 | 2013 | 2013 | 2012 | 2012 | 2013 | |||||||||||||||

| |

Actual | Actual | Actual | Pro forma | Actual | Pro forma | Actual | |||||||||||||||

| |

|

|

|

(unaudited) |

(unaudited) |

(unaudited) |

(unaudited) |

|||||||||||||||

| |

(in millions of dollars) |

|||||||||||||||||||||

(Loss)/profit for the period |

(48.1 | ) | (37.4 | ) | (23.3 | ) | (16.0 | ) | 7.3 | 9.8 | 3.5 | |||||||||||

Income tax expense |

12.5 | 16.4 | 19.3 | 18.6 | 5.5 | 5.0 | 6.1 | |||||||||||||||

Net financing expense(a) |

41.6 | 47.7 | 49.0 | 57.4 | 9.0 | 11.8 | 16.1 | |||||||||||||||

Exceptional items(b) |

9.4 | 12.5 | 17.7 | 9.1 | 1.0 | 1.0 | 1.6 | |||||||||||||||

Impairment of goodwill(c) |

16.7 | 10.7 | — | — | — | — | — | |||||||||||||||

Amortization |

2.8 | 3.5 | 5.7 | 8.8 | 0.9 | 1.9 | 2.4 | |||||||||||||||

Depreciation |

7.2 | 9.9 | 11.7 | 16.0 | 2.6 | 4.1 | 5.3 | |||||||||||||||

EBITDA |

42.1 | 63.3 | 80.1 | 93.9 | 26.3 | 33.6 | 35.0 | |||||||||||||||

Loss on disposal of property, plant and equipment(d) |

1.0 | 0.3 | 0.1 | 0.1 | — | — | — | |||||||||||||||

Exchange (gain)/loss(e) |

(3.5 | ) | 4.6 | (4.0 | ) | (1.8 | ) | (0.5 | ) | (1.1 | ) | 2.1 | ||||||||||

Restructuring(f) |

— | — | — | 0.8 | — | — | — | |||||||||||||||

Pre-acquisition and corporate structuring costs(g) |

3.2 | 0.6 | — | 0.8 | — | 0.2 | — | |||||||||||||||

Write-off of management charges to a related party(h) |

1.8 | — | — | — | — | — | — | |||||||||||||||

School and contract closure costs(i) |

1.8 | — | — | — | — | — | — | |||||||||||||||

Share based payments(j) |

0.3 | 0.6 | 0.1 | 6.4 | — | — | 1.1 | |||||||||||||||

Management fees(k) |

— | — | 3.3 | 3.3 | — | — | 0.5 | |||||||||||||||

Others(l) |

1.2 | 0.8 | (0.1 | ) | (0.1 | ) | (0.1 | ) | (0.1 | ) | 0.0 | |||||||||||

Adjusted EBITDA(m) |

47.9 | 70.2 | 79.5 | 103.4 | 25.7 | 32.6 | 38.7 | |||||||||||||||

Depreciation |

(7.2 |

) |

(9.9 |

) |

(11.7 |

) |

(16.0 |

) |

(2.6 |

) |

(4.1 |

) |

(5.3 |

) |

||||||||

Net financing expense(a) |

(41.6 | ) | (47.7 | ) | (49.0 | ) | (57.4 | ) | (9.0 | ) | (11.8 | ) | (16.1 | ) | ||||||||

Income tax expense |

(12.5 | ) | (16.4 | ) | (19.3 | ) | (18.6 | ) | (5.5 | ) | (5.0 | ) | (6.1 | ) | ||||||||

Tax adjustments(n) |

(0.6 | ) | (0.6 | ) | (0.8 | ) | (1.6 | ) | (0.2 | ) | (0.4 | ) | (0.5 | ) | ||||||||

Adjusted Net Income |

(14.0 | ) | (4.4 | ) | (1.3 | ) | 9.8 | 8.4 | 11.3 | 10.7 | ||||||||||||

- (a)

- As described under "Management's Discussion and Analysis of Financial Condition and Results of Operations—Debt—Refinancing of Notes," we intend to refinance our notes with the proceeds of this offering and a new secured term loan facility. We expect that the new term loan facility will bear interest based on applicable margin percentages of % per annum for base rate loans and % per annum for LIBOR rate loans, provided that LIBOR may not be lower than %. Based on these anticipated interest rates, and assuming we use $ million of the net proceeds of this offering to redeem 35% of the notes and borrowings under the term loan facility to redeem the remainder of the notes, we estimate that (i) net finance expense attributable to the portion of the notes redeemed using offering proceeds, before taxes, would have decreased by approximately $ million, $ million and $ million for the year ended August 31, 2013, the three months ended November 30, 2013 and the three months ended November 30, 2012, respectively, and (ii) net finance expense attributable to the portion of the notes redeemed using borrowings under the new term loan facility would have decreased by approximately, $ million, $ million and $ million for the year ended August 31, 2013, the three months ended November 30, 2013 and the three months ended November 30, 2012, respectively. An increase (decrease) in the anticipated interest rates under the new term loan facility by 0.125% would decrease (increase) the net interest expense savings with respect to the portion of the notes redeemed with borrowings under the new term loan facility, before taxes, by $ million, $ million and $ million for the year ended August 31, 2013, the three months ended November 30, 2013 and the three months ended November 30, 2012, respectively. We expect to incur an exceptional charge of approximately $ million related to the redemption of our notes. The charges will be included in finance expense in the quarter in which we redeem the notes.

16

- (b)

- In

fiscal 2011, exceptional items included expenses related to the relocation of our central services function to Hong Kong. In fiscal 2012, 2013 and 2013

pro forma, exceptional expenses primarily related to the acquisition of schools, including associated transaction and integration costs, and transaction management fees paid to Baring Private

Equity Asia associated with our notes issuances. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations."

- (c)

- In

fiscal 2011, impairment of goodwill included the non-cash impairment charge on the goodwill associated with the UK learning services business. In fiscal

2012, impairment of goodwill included the non-cash impairment charge on the remaining balance of the goodwill relating to learning services in the Middle East. See "Management's Discussion and

Analysis of Financial Condition and Results of Operations—Results of Operations."

- (d)

- In

fiscal 2011, represents loss on disposal of property, plant and equipment associated with the closure of our school in Nanxiang, Shanghai. In fiscal

2012, 2013 and 2013 pro forma, includes loss on disposal of assets associated with the termination of learning services contracts in the UK.

- (e)

- Represents

foreign currency translational gains/losses primarily associated with our inter-company loan balances.

- (f)

- Represents

the full-year benefit of headcount reductions that have already been implemented.

- (g)

- In

fiscal 2011 and 2012, represents costs associated with legal, tax and accounting advice in relation to the conversion of our U.S. dollar

shareholder loans from pound sterling, as well as costs associated with changes to our corporate structure and lending arrangements to enable us to acquire our schools in Switzerland. In fiscal

2012 and 2013 pro forma, represents costs incurred by WCL Group in connection with the acquisition.

- (h)

- For

fiscal 2010, we earned a management fee for operating Collège Champittet-Lausanne and Collège Champittet-Nyon on behalf of

a related party. These fees were subsequently written off in fiscal 2011.

- (i)

- Represents

school and contract closure costs associated with the closure of our school in Nanxiang.

- (j)

- In

fiscal 2011, 2012, 2013 and the first quarter of fiscal 2014, represents non-cash charges associated with the equity investments in our company by

members of our management. In 2013 pro forma, includes non-cash charges associated with share-based compensation of WCL Group.

- (k)

- Represents

management fees paid to Premier Education Holdings.

- (l)

- In

fiscal 2011 and 2012, represents various fees, expenses and redundancy costs relating to the change in the mix of our business from learning services to

premium schools.

- (m)

- Includes

Adjusted EBITDA losses attributable to BISAD of $5.6 million, $3.8 million, $1.1 million and $0.5 million in fiscal

2011, 2012 and 2013 and the first quarter of fiscal 2013, respectively. In the foregoing periods, BISAD contributed revenue of $5.9 million, $9.8 million, $14.5 million and

$4.5 million, respectively. Also includes pro forma Adjusted EBITDA losses attributable to our school in New York of $0.9 million and $0.2 million in fiscal 2013 and the

first quarter of fiscal 2013, respectively, and Adjusted EBITDA losses attributable to our school in New York of $0.1 million in the first quarter of fiscal 2014. Our school in New York

contributed pro forma revenue of $2.3 million and $0.6 million in fiscal 2013 and the first quarter of fiscal 2013, respectively, and contributed revenue of $0.9 million in

the first quarter of fiscal 2014.

- (n)

- Represents

the tax impact associated with the exclusion of exceptional items and amortization from the calculation of Adjusted

Net Income.

Based on the anticipated interest rates set forth above, assuming our new term loan facility had been fully drawn during the three months ended November 30, 2013, and that none of our notes were outstanding during the three months ended November 30, 2013, our net interest expense, before tax, for the period would have decreased by $ million. An increase (decrease) in the anticipated interest rates under the new term loan facility by 0.125% would decrease (increase) the net interest expense savings by $ million for the period.

- (2)

- Discontinuing

Adjusted EBITDA relates to the results of our school in Nanxiang that we closed in 2011.

- (3)

- Includes

Adjusted EBITDA from our learning services. See "Management's Discussion and Analysis of Financial Condition and Results of

Operations—Overview."

- (4)

- Adjusted

EBITDA divided by revenue.

- (5)

- ROC is not a recognized measure under IFRS. We believe ROC is a meaningful metric for investors because it measures how effectively we use capital to generate operating profit. We

17

define ROC as adjusted operating profit divided by adjusted invested capital. Although ROC is a common financial metric, numerous methods exist for calculating ROC. Accordingly, our method of calculating ROC may differ from the methods other companies use to calculate their ROC. We encourage you to understand the methods other companies use to calculate ROC before comparing their ROC to ours. The following table presents the calculation of ROC for the periods presented:

| |

As of and for the year ended August 31, | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| |

2012 | 2013 | 2013 | ||||||||

| |

Actual | Actual | Pro forma | ||||||||

| |

|

|

(unaudited) |

||||||||

| |

(in millions of dollars, except percentages) |

||||||||||

Operating Profit |

26.7 | 45.0 | 60.0 | ||||||||

Adjustments: |

|||||||||||

Exceptional items(a) |

12.5 | 17.7 | 9.1 | ||||||||

Impairment of goodwill(b) |

10.7 | — | — | ||||||||

Depreciation |

9.9 | 11.7 | 16.0 | ||||||||

Loss on disposal of property, plant and equipment(c) |

0.3 | 0.1 | 0.1 | ||||||||

Exchange (gain)/loss(d) |

4.6 | (4.0 | ) | (1.8 | ) | ||||||

Restructuring(e) |

— | — | 0.8 | ||||||||

Pre-acquisition and corporate structuring costs(f) |

0.6 | — | 0.8 | ||||||||

Share-based payments(g) |

0.6 | 0.1 | 6.4 | ||||||||

Management fees(h) |

— | 3.3 | 3.3 | ||||||||

Others(i) |

0.8 | (0.1 | ) | (0.1 | ) | ||||||

Rental expense(j) |

27.6 | 31.9 | 38.9 | ||||||||

Cash taxes paid |

(15.9 | ) | (25.5 | ) | (26.0 | ) | |||||

Cash tax effect of rental expense adjustment(k) |

(5.5 | ) | (7.4 | ) | (8.8 | ) | |||||

Adjusted Operating Profit |

72.9 | 72.8 | 98.7 | ||||||||

Total assets |

666.8 | 1,126.0 | 1,126.0 | ||||||||

Plus: accumulated depreciation of property, plant and equipment |

20.1 | 32.5 | 36.8 | ||||||||

Plus: capitalized leases(l) |

220.8 | 255.2 | 311.4 | ||||||||

Minus: non-interest bearing current liabilities(m) |

(232.5 | ) | (368.1 | ) | (368.1 | ) | |||||

Minus: goodwill and intangibles |

(455.1 | ) | (753.7 | ) | (753.7 | ) | |||||

Adjusted invested capital |

220.1 | 291.9 | 352.4 | ||||||||

Return on capital |

33.1% | 25.0% | 28.0% | ||||||||

- (a)

- In

fiscal 2012, 2013 and 2013 pro forma, exceptional expenses primarily related to the acquisition of schools, including associated transaction and

integration costs, and transaction management fees paid to Baring Private Equity Asia associated with our notes issuances. See "Management's Discussion and Analysis of Financial Condition and Results

of Operations—Results of Operations."

- (b)

- In

fiscal 2012, impairment of goodwill included the non-cash impairment charge on the remaining balance of the goodwill relating to learning services in the

Middle East. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations."

- (c)

- In fiscal 2012, 2013 and 2013 pro forma, includes loss on disposal of assets associated with the termination of learning services contracts in the U.K.

18

- (d)

- Represents

foreign currency translational gains/losses primarily associated with our inter-company loan balances.

- (e)

- Represents

the full-year benefit of headcount reductions that have already been implemented.

- (f)

- In

fiscal 2012, represents costs associated with legal, tax and accounting advice in relation to the conversion of our U.S. dollar shareholder loans

from pound sterling, as well as costs associated with changes to our corporate structure and lending arrangements to enable us to acquire our schools in Switzerland. In 2013 pro forma,

represents costs incurred by WCL Group in connection with the acquisition.

- (g)

- Represents

non-cash charges associated with the equity investments in our company by members of our management and in 2013 pro forma, includes

non-cash charges associated with share-based compensation of WCL Group.

- (h)

- Represents

management fees paid to Premier Education Holdings.

- (i)

- In

fiscal 2012, various fees, expenses and redundancy costs relating to the change in the mix of our business from learning services to

premium schools.

- (j)

- Represents

actual rental payments for leased schools and offices.

- (k)

- Increase

in cash tax that would have resulted if we had not incurred the rental expenses described in note (j).

- (l)

- Capitalized

lease obligations calculated as rental expense as presented in note (j) multiplied by eight.

- (m)

- Represents total current liabilities minus interest-bearing current liabilities.

19

An investment in our ordinary shares involves significant risks. You should carefully consider the risks described below as well as other information in this prospectus, including our consolidated financial statements and related notes, before you decide to buy our ordinary shares. If any of the following risks materializes, our business, prospects, financial condition and results of operations could be materially harmed, the trading price of our ordinary shares could decline and you could lose all or part of your investment.

Risks Related to Our Business

Adverse changes in key industry drivers may reduce demand for our schools.

We believe that the key industry drivers for our schools include:

- •

- globalization and increasing FDI; and

- •

- a growing emphasis by parents on high-quality education for their children.

Changes in our key industry drivers may materially adversely affect our business, prospects, results of operations and financial condition. For example, if FDI stock declines in one of the countries in which we operate, the number of expatriate families in that country may decrease, which could reduce demand for our schools. During the 2009/2010 academic year, attracting new students was more difficult than in previous and subsequent academic years, which we believe was due in part to the 2008 global financial crisis. Furthermore, as some of the emerging markets in which we operate reach a higher level of economic development and develop a more skilled local workforce, companies could increasingly rely on the local workforce and employ fewer expatriates, which could reduce our business if we are unable to adapt or attract local students.

In addition, we believe that growth of GDP and individual disposable income in emerging markets tends to increase demand from local families, as they increase their focus and spending on premium quality education. Accordingly, decreases or limited growth in GDP or disposable income may reduce demand for our schools from local families and limit our ability to recruit and retain local students.

Competition in the premium school market could reduce enrollments, increase our cost of recruiting and retaining students and teachers and put downward pressure on our tuition fees and profitability.

We face competition from other schools in the locations in which we operate that target the children of expatriate and affluent local families. Some of our existing and potential competitors may be able to devote greater resources than we can to the development and construction of schools offering premium quality education and respond more quickly to changes in parents' demands, admissions standards, market needs or new technologies. Moreover, our competitors may increase capacity in any of our markets to an extent that leads to an over-supply.

If we are unable to differentiate our schools from those of our competitors and successfully market our schools to parents and students, we could face competitive pressures that reduce enrollment. If our enrollment falls, we may be required to reduce our tuition fees or increase spending in order to attract and retain students, which could materially adversely affect our business, prospects, results of operations and financial condition. See "Business—Competition."

If we fail to increase or maintain our tuition fees, our financial performance may suffer.

Tuition fees at our schools are among the highest in their markets. Factors that could affect our ability to increase or maintain our premium tuition fees include:

- •

- a decline in our reputation for quality;

- •

- resistance to tuition fee increases from parents and expatriates' employers as a result of difficult economic conditions or fee increases in recent academic years;

20

- •

- pricing pressure from other premium schools in our markets; and

- •