UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended March 31, 2019

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to __________

Commission file number: 001-38249

LIVEXLIVE MEDIA, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 98-0657263 | |

| (State

or other jurisdiction of incorporation or organization) |

(I.R.S.

Employer Identification No.) | |

| 269 South Beverly Drive, Suite #1450 Beverly Hills, California |

90212 | |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s telephone number, including area code (310) 601-2500

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| Common stock, $0.001 par value per share | LIVX | The NASDAQ Capital Market |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§223.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☒ | ||

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ | ||

| Emerging Growth Company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The aggregate market value of the voting stock held by non-affiliates of the registrant, computed by reference to the closing price as of the last business day of the registrant’s most recently completed second fiscal quarter ended September 30, 2018, was approximately $128,230,000. For the sole purpose of making this calculation, the term “non-affiliate” has been interpreted to exclude directors, executive officers, holders of 10% or more of the registrant’s common stock and their affiliates.

As of June 9, 2019, the registrant had 52,496,095 shares of common stock outstanding.

TABLE OF CONTENTS

i

Use of Market and Industry Data

This Annual Report on Form 10-K (this “Annual Report”) includes market and industry data that we have obtained from third party sources, including industry publications, as well as industry data prepared by our management on the basis of its knowledge of and experience in the industries in which we operate (including our management’s estimates and assumptions relating to such industries based on that knowledge). Management has developed its knowledge of such industries through its experience and participation in these industries. While our management believes the third-party sources referred to in this Annual Report are reliable, neither we nor our management have independently verified any of the data from such sources referred to in this Annual Report or ascertained the underlying economic assumptions relied upon by such sources. Furthermore, references in this Annual Report to any publications, reports, surveys or articles prepared by third parties should not be construed as depicting the complete findings of the entire publication, report, survey or article. The information in any such publication, report, survey or article is not incorporated by reference in this Annual Report.

Forecasts and other forward-looking information obtained from these sources involve risks and uncertainties and are subject to change based on various factors, including those discussed in sections entitled “Forward-Looking Statements,” “Item 1A. Risk Factors” and “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Annual Report.

Trademarks, Service Marks and Trade Names

This Annual Report contains references to our trademarks, service marks and trade names and to trademarks, service marks and trade names belonging to other entities. Solely for convenience, trademarks, service marks and trade names referred to in this Annual Report, including logos, artwork and other visual displays, may appear without the ® or TM symbols, but such references are not intended to indicate, in any way, that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend our use or display of other companies’ trade names, service marks or trademarks or any artists’ or other individuals’ names to imply a relationship with, or endorsement or sponsorship of us by, any other companies or persons.

ii

PART I

| Item 1. | Business |

Overview

LiveXLive Media, Inc. (the “Company,” “LXL,” “we,” “us,” or “our”) is a pioneer in the acquisition, distribution and monetization of live music, Internet radio and music-related streaming and video content. Through our comprehensive service offerings and innovative content platform, we provide music fans the ability to watch, listen, experience, discuss, deliberate and enjoy live music and entertainment 24/7/365. Serving a global music audience, our mission is to bring the experience of live music and entertainment to music consumers wherever music is watched, listened to, discussed, deliberated or performed around the world. Through March 31, 2019, we operated two core integrated services - LiveXLive (“LiveXLive”), one of the industry’s leading live music streaming platforms, and Slacker Radio, a streaming music service that we obtained through our acquisition of Slacker, Inc. (or “Slacker”) on December 29, 2017; and also produced original music-related content. LiveXLive is the first ‘live social music network’, delivering premium live-streamed, digital audio and on-demand music experiences from the world’s top music festivals and concerts, including Rock in Rio, EDC Las Vegas, Hangout Music Festival and many more. LiveXLive also gives audiences access to premium original content, artist exclusives and industry interviews. During the fiscal year ended March 31, 2019, we livestreamed 24 major music festivals and live music events to over 50 million fans across the world, and our subscription services eclipsed 680,000 paid subscribers and 1.3 million monthly active users across our audio services. Through our music audio services, our users have access to millions of songs and hundreds of expert-curated radio platforms and stations. In May 2019, we combined Slacker’s pioneering personalization and LiveXLive’s industry-leading livestreaming expertise into a new application offering access to live events, audio streams, original episodic content, podcasts, video on demand, real-time livestreams, and social sharing of content. Today, our business is comprised of a single operating segment (hereon referred to as our “music services”).

We generate revenue primarily through the sale of subscription-based services and advertising from our music offerings, and secondarily from the licensing of our live music content rights and services.

Music Services

Our music services provide our music fans the ability to experience, engage in and listen to live music, digital Internet radio and music streaming services on any connected device and screen 24/7/365, including desk-top, tablets, mobile applications (iOS and Android) and automobile music play interfaces. Today, we provide our music services through a dedicated over-the-top application (“Apps”) called LiveXLive. Our music services are delivered through digital streaming transmissions over the Internet and or through satellite transmissions. Our users can also access our music platform from our websites, including www.livexlive.com and www.slacker.com, and through our digital App.

We acquire the rights to stream our live and recorded music and broadcasts from a combination of festival owners, such as Anschutz Entertainment Group (“AEG”) and Live Nation Entertainment, Inc. (“Live Nation”), music labels, including Universal Music, Warner Music and Sony Music, and through individual music publishers and rights holders. Today, the majority of our content acquisition agreements provide us the exclusive rights to produce, license, broadcast and distribute live broadcast streams of these festivals and events throughout the world and across any digital platform, including cable, Internet, video, audio, video-on-demand (“VOD”) and virtual reality (“VR”). Our license rights to provide recorded music licenses and broadcasts principally cover North America today. Through March 31, 2019, we held the streaming rights to over 40 festivals and live music events under long-term contracts that range from two to seven years in duration. Today, we have increased these live streaming festival rights to over 50 festivals and live music events, and are working to expand our VOD, content catalog and content capabilities.

Our music services commenced operations through LiveXLive in the fiscal year ended March 31, 2015, when we streamed our first music festival. During the fiscal year ended March 31, 2018, we acquired Slacker and deployed our subscription-based music services. After the Slacker acquisition, we launched our LXL App across Apple, Roku and Amazon Fire platforms. In February 2018, we entered into a multi-year agreement with Insomniac Holdings LLC (“Insomniac”), a partner with Live Nation and the owner of EDC (“Electronic Daisy Carnival”) festival and other dance music festivals and events, to produce and stream up to 20 major festivals around the world and over 100 events annually across our music platform. In December 2018, we launched LiveZone, a traveling studio originating from live music events and festivals all over the world. LiveZone will mix music news, commentary, festival updates and artist interviews, and provide context to premiere events by showcasing exotic locales, unique venues, and artist backstories, adding “pre-show” and “post-show” segments to livestreamed artist performances and original festival-based content. In March 2019, we entered into a multi-year agreement with iHeartMedia that combines content, production, distribution and promotion. The agreement gives us exclusive global livestreaming rights for 17 events this year. Today, we have over 50 live festivals and music events, 700,000 paid subscribers and 1.4 million monthly active users (“MAUs”), making us online one of the largest music platforms capable of streaming live and recorded music and broadcasts globally. We use MAUs, which is a non-GAAP financial measure, as a measure of our performance and define a MAU as a user of one of our platforms who has logged in and visited our music subscription platform, as a unique user, on the day of measurement.

1

As of March 31, 2019, we livestreamed the following major festivals and live music events, which included over 400 live artist performances since April 1, 2018 alone (including streaming dates and major artists):

| ● | Rock in Rio – Rio de Janeiro, Brazil and Lisbon, Portugal (September 2015, May 2016, September 2017 and May 2018; Katy Perry, The Killers, Muse, Demi Lovato, Metallica, Maroon 5, Justin Timberlake, Bon Jovi, Guns N’ Roses) |

| ● | Outside Lands – San Francisco, California (August 2016 and 2017; Radiohead, Lorde, Metallica, The Who) |

| ● | Hangout Festival – Gulf Shores, Alabama (May 2017/2018; The Killers, The Chainsmokers, Kendrick Lamar, Mumford & Sons, Weezer, Chance The Rapper, Twenty One Pilots, DJ Snake) |

| ● | Summerfest – Milwaukee, Wisconsin (June/July 2017; Red Hot Chili Peppers, Paul Simon, Tom Petty, Willie Nelson, Bob Dylan) |

| ● | EDC Las Vegas – Las Vegas, Nevada (May 2018; Above & Beyond, Marshmello, Martin Garrix, Diplo) |

| ● | Rock On The Range - Columbus, Ohio (May 2018; Avenged Sevenfold, Alice In Chains) |

| ● | Country 500 Music Festival - Daytona, Florida (May 2018; Dierks Bentley) |

| ● | Montreux Jazz Festival – Lake Geneva, Switzerland (June/July 2018; Queens of the Stone Age, Odesza, Nine Inch Nails Tyler The Creator, Jack White, Billy Idol, Alice in Chains) |

| ● | Paleo Festival Nyon – Nyon, Switzerland (July 2018; Red Hot Chile Peppers, Arcade Fire, Macklemore) |

| ● | Global Dance Festival – Denver, Colorado (July 2018; Kevin Gates, Juicy J, Machine Gun Kelly, Rich The Kid, Adventure Club) |

| ● | HARD Summer Fest 2018 – Fontana, California (August 2018; Jaden Smith, Travis Scott, Rick Ross, Diplo, Dillon Frances, Marshmello) |

| ● | Sziget Festival – Budapest, Hungary (August 2018; Artic Monkeys, Kendrick Lamar, Mumford & Sons) |

| ● | Bumbershoot Festival – Seattle, Washington (August/September 2018; Ludacris, J. Cole, T-Pain, Young Thug, SZA Blondie) |

| ● | Rolling Loud Festival / Bay Area – Oakland, California (September 2018; Travis Scott, Wiz Khalifa, Gucci Mane) |

| ● | Life Is Beautiful Music and Arts Festival – Las Vegas, Nevada (September 2018; The Weekend, Arcade Fire, Florence + The Machine, DJ Snake) |

| ● | Escape – San Bernardino, California (October 2018; Martin Garrix, Kaskade, Galantis, Alan Walker, Excision) |

| ● | EDC Orlando – Orlando, Florida (November 2018; Tiesto, Alesso, Pendulum, Martin Garrix) |

| ● | Mac Miller: A Celebration of Life – Los Angeles, California (November 2018; Chance The Rapper, Ty Dolla $ign, John Mayer, Miguel, SZA, Travis Scott) |

| ● | Rolling Loud Festival / Los Angeles – Los Angeles, California (December 2018; Post Malone, Lil Uzi Vert, Lil Wayne, Wiz Khalifa, Playboi Carti) |

| ● | LiveXLive Presents – Los Angeles, California (December 2018; February 2019) and Las Vegas, Nevada (CES January 2019) – Nas, Chromeo, Charli XCX, Rick Ross, Tierra Whack, DJ MettyBeats, G. Perico, Jay Hype, London On Da Track, Shaboozey, Sheck Wes, O.T. Genasis, Cousin Stizz, and Tabi. |

2

| ● | ALTer Ego – Los Angeles, California (January 2019) – The Killers, Weezer, Muse, Twenty One Pilots, Rise Against |

| ● | EDC Mexico – Mexico City, Mexico (February 2019) - Skrillex, Dimitri Vegas & Like Mike, Kygo, RL Grime, and Gryffin |

| ● | Weezer iHeartRadio Theater – New York, New York (February 2019 record release party) |

As of March 31, 2019, our users could listen to our Internet digital radio services through our website, across most major mobile telephone carriers, Apple iTunes and Google android operating systems and in automobiles, such as Tesla, Honda, Acura, Fiat, Chrysler, Dodge, Ram, Jeep, Ford, Lexus, Scion, Subaru and Toyota.

Live Music Events

We produce, edit, curate and stream live music events through broadband transmission over the Internet and or satellite networks to our users throughout the world, where permitted. This service allows our users to access live music content over the Internet through their personal cellular phones, desktops, computers, tablets, and televisions, including the ability to chat and communicate over our platform. Today, LiveXLive provides these live music events for free to our users. During the year ended March 31, 2019, we began monetizing these live events through third party advertising and sponsorship, including with brands such as Kia, Samsung and Dos Equis, and selling territorial licensing rights to Tencent in China and Ocesa in Mexico. Our cost structure varies by festival, and is customarily in the form of a set upfront fee, the amount of which is often dependent on the festival’s existing production infrastructure or lack thereof, and, in turn, our production/financial commitment to the live stream, against a revenue share. The fees generated from any advertising, sponsored content, VOD and other services are generally subject to the aforementioned revenue sharing arrangements with our festival owners and music right holders, when applicable.

Digital Internet Radio and Music Services

Today, our digital Internet radio and music services are available to users online and through original equipment manufacturers (“OEMs”) on a white label basis, which allow certain OEMs to customize the radio and music services with their own logos, branding and systems. Our users are able to listen to a variety of music, radio personalities, news, sports and the audio of live music events. Our fee structure for our digital Internet radio and music services varies, and may be in the form of (i) a free service to the listener supported by paid advertising, (ii) paid premium subscription services, and or (iii) a fixed fee per user. The fees generated from ad-supported and subscription services are generally subject to revenue sharing arrangements with music right holders and labels, and fees to festivals, clubs, events, concerts, artists, promoters, venues, music labels and publishers (“Content Providers”).

Ancillary Products and Services

We also provide our customers the following:

| ● | Regulatory Support – streaming of music is generally subject to copyright protection. Whenever possible, we use our best efforts to clear music copyright licenses, artist streaming preferences and music publishing rights in advance of usage. |

| ● | Post-Implementation Support - once our App is live, we provide technical and network support, which includes 24/7 operational assistance and monitoring of our services and performance. |

Our Industry

Globally, recorded music revenues increased to $19.1 billion in 2018, up 9.7% from $17.4 billion in 2017 (IFPI Global Music Report 2019). In the U.S. alone, live music events were projected to surpass $8.0 billion in 2019 (source: Statista). Our addressable market includes streaming of live music and entertainment, Internet radio, audio and downloadable music and online VOD services. These three markets are experiencing significant growth and now represent the majority of the music industry’s overall revenue, as physical and digital record sales have steadily declined. We both capitalize on these trends and provide additional earnings opportunities to industry stakeholders, including agents, managers, distributors, producers, labels, publishers, advertisers and social influencers (collectively, “Industry Stakeholders”).

3

Live Music Industry

The live music industry is a large, growing market that creates, manages and promotes live performances and events, ranging from festivals to concerts and events in stadiums, arenas, and other smaller venues. In the U.S. alone, the live music industry is expected to have generated over $29.0 billion of revenue annually by 2020, representing a +1% growth rate over 2016 (IBIS World) and over $5.0 billion in live music sponsorship for the same periods. Live events and festivals have become an increasingly important cultural phenomenon as seen by more than 2,000 music festivals worldwide. Each festival can attract hundreds of thousands of people with attendance at the largest festival in the United States estimated at over 140,000 people per day. Rock in Rio, for instance, attracted a combined attendance of over 1,000,000 people in 2015 and 2016 in Lisbon and Rio. The most popular festivals based on attendance include Coachella, EDC, Glastonbury, Outside Lands Music and Arts Festival, Rock Werchter, Rock in Rio, Roskilde, Tomorrowland and Ultra Music Festival. The live event industry is a global market with only a fraction of the leading live music events located in the U.S. In addition to festivals, there are thousands of live music events and performances that occur nightly in large and small venues such as arenas, theatres, clubs, bars and lounges.

As a result of the popularity of live music performances, there has been a growing interest in experiencing live events and performances via online streaming distribution. For example, in 2019, over 14 million people viewed our weekend livestream of three major festivals (EDC Las Vegas, Hangout Music Festival and Rock on the Range). Moreover, with the introduction of LiveZone in December 2018, we experienced an over 75% increase in livestream views of Rolling Loud - Los Angeles festival (December 2018) versus Rolling Loud – Bay Area festival (September 2018).

Additionally, the growth of the live music industry benefits ancillary verticals, such as merchandise and primary/secondary ticket marketplaces. Merchandise includes the retail sales of licensed music-related goods and is estimated to be larger than $2 billion since 2014.

Digital Music Streaming Industry

The addressable market for paid digital music streaming is large and growing, representing almost half of global music revenue. In 2018, streaming revenue grew 33% from 2017 to approximately $9.1 billion (IFPI Global Music Report 2019), and is expected to surpass $11.0 billion by 2020 (IBISWorld; PwC Global Entertainment and Media Outlook). The 2018 growth in streaming revenue has more than surpassed the year-over-year declines in physical and download revenues of 10.1% and 21.2%, respectively (IFPI Global Music Report 2019). At the end of 2018, there was approximately 255 million users of paid streaming services. According to Goldman Sachs, paid streaming users are expected to surpass 800 million by 2030.

These same fans are increasingly engaging digitally on their mobile devices. With over 2.5 billion smartphone users globally in 2018, we expect that mobile will continue to represent a significant opportunity for streaming live music and music-related content. More than 60% of Internet users globally listened to music through direct download or live stream from services such as Apple Music and iTunes, Pandora, iHeartRadio, Deezer and Spotify (eMarketer, August 2016).

We believe that the demand for live music and music-related content that is optimized for Internet-connected devices will continue to grow with the further development of mobile devices and increases in mobile carrier bandwidth. We intend to continue to extend our global reach by executing deals with new partners and strengthening our business model to enable us to further monetize the content offered on our network across these devices.

Online Video Streaming Industry

The addressable market for online video streaming is large and growing. The online video streaming industry is expected to generate $24.8 billing in revenue by 2019, up 8% from 2018 with expected growth to $28.2 billion by 2023 (Statista).

Additionally, an important subset of the growing online video streaming market is live video streaming. According to Facebook Live, users watch live video three times longer and comment ten times more than recorded footage (Eventbrite Blog, August 22, 2016). Moreover, YouTube claims that over 35% of all videos watched are music related. We aim to capitalize on what we believe is an increasing trend in user engagement with live video content.

4

Technology

We own over 10 registered or pending patents on our streaming Internet radio services, including patents over playback of digital media content, method for providing user personalized content, systems for portable personalized radio, method for interactive distribution of digital content and systems for scoring and raking digital content based on activity of network users. Key components of this technology include:

| ● | User authorization system |

| ● | Data Warehouse/Data Management Platform, including user preferences and behavior |

| ● | Enterprise Content Management and Delivery Platform for Music |

| ● | Relevancy and Personalization Technology |

| ● | Patented off-line mode |

| ● | Mobile and over-the-top (“OTT”) Development |

| ● | Development around the balance between curated and programmatically generated content |

| ● | Integrated carrier billing with most major carriers |

| ● | Service-based technology systems which allows for easier development of new products |

While we do not currently have a trademark on the LiveXLive name, on September 23, 2017, we entered into a Co-Existence Agreement with Monday Sessions Media, Inc. D/B/A Live X (“Live X”), in which we consented to Live X’s use and registration of the name and mark Live X and agreed to not challenge, dispute or contest Live X’s rights in such mark. Pursuant to this agreement, we agreed to not offer certain production services to third party businesses in connection with our mark LIVEXLIVE and use commercially reasonable efforts to afford Live X opportunities to bid on production or streaming service opportunities. We intend to protect our trademarks, brands, copyrights, patents and other original and acquired works, ancillary goods and services. In connection with the Slacker acquisition, we acquired a trademark for the Slacker name. We believe that certain trademarks and other proprietary rights that we may apply for or otherwise obtain will have significant value and will be important to our brand-building efforts and the marketing of our services. We cannot predict, however, whether steps taken by us to protect our proprietary rights will be successful or adequate to prevent misappropriation, infringement or other violation of these rights. Upon the consummation of any future acquisitions, we may acquire additional registered trademarks, as well as applied-for trademarks potentially for worldwide use.

Streaming Internet Radio

We continuously obtain high-quality digital content and associated data from the record labels. These master files are stored in a secure database and transcoded into various audio formats that are then pushed to our production environment. The production system supports numerous streaming formats as required to serve the numerous end-user consumption devices that our service supports, including mobile handsets, connected car audio systems, smart TVs, HTML web players, etc. The production infrastructure consists of servers housed in our data center and caching servers, managed by our partners, distributed across the Internet. The caching servers temporarily store the content and related formats that are in high demand, thereby placing the most popular content closest to user endpoints, reducing latency and the number of content requests sent to our data center. When a given user makes a play request from their mobile device, the web, connected car, etc., the system sets up a secure connection to that user’s device, automatically detects the proper format and the highest quality bitrate that can be streamed, and delivers the stream to our users.

Live Music

Technology is a key component of the LiveXLive network that brings our ecosystem to life for our users and Content Providers. We currently deliver our viewer experience through an HTML-based website compatible with most major web browsers (e.g., Chrome, Safari, Internet Explorer) and operating systems (e.g., Windows, MacOS, iOS, Android). Our developers bring extensive experience building technology solutions for the leading media companies of the world, including the design of live and VOD workflows, the video content management system and delivery of content on mobile, OTT and desktop clients.

More recently, we built and launched a pioneering technology stack for delivering our content to users on nearly any Internet-connected device. As of May 2018, our updated version of the LXL App was available on the iOS and Android operating systems and through Apple TV, Roku and Amazon Fire platforms. We are also continuing to finalize our OTT strategy, which to date has resulted in the release of our custom OTT application the aforementioned platforms and will be ultimately be available on most OTT platforms and consoles. We believe our full-service, delivery-to-distribution back-end will allow us to capitalize on monetization opportunities and is the first step in creating a digital supply chain for live music and music-related video content.

In April 2018, we entered into an agreement with a third-party to create interactive streaming experiences around live music events which will be streamed on the LiveXLive website and our LXL App. The interactive streaming develops engagement and analytics software and offers a platform that enables a new category of live experiences that facilitates two-way interactions between streamers and their audiences. The overall platform also enables enterprise live streamers to engage their audiences and gather data insights which will help us analyze how we can increase user retention and develop and increase our monetization opportunities.

5

Users

We currently stream our music services for live events globally to music fans worldwide, and with users located in North America for our digital music streaming services. We are currently developing plans to expand our digital Internet radio presence internationally. Our music streaming customers include individual users and OEMs such as Tesla, Verizon, T-Mobile, and, to a lesser extent, advertisers and third-party licensees. For the fiscal year ended March 31, 2019 and 2018, we had one single customer that represented approximately 41% and 24% of our total consolidated revenue in the period, respectively.

We provide live production and content curating and processing services to our festival and event partners on an exclusive basis, globally. These agreements are generally for three to seven years in duration. Our customers also include major cable networks such as MTV, where we have historically agreed to share production costs for certain festivals. As of March 31, 2019, we were the exclusive representative to over 40 festivals around the world.

Competitive Advantage

We are producers, acquirers and distributors of live and digital music and Internet radio entertainment services, and work closely with major and independent labels, music festival owners and other content producers to provide unique and compelling music content across our platform for our listeners. Accordingly, our significant operating and deal-making experience and relationships with Content Providers, OEMs such as Tesla, cable networks such as MTV, major advertisers and music publishers and distribution companies in our industry gives us a number of competitive advantages and may present us with a substantial number of additional business targets and relationships to facilitate growth going forward. We believe that we have sustainable competitive advantages due to our growing market position in live events, technology and relationships with important music labels, content suppliers and festival owners.

Our leadership team, consisting of our senior and executive management and our board of directors, collectively brings a wealth of industry relationships and expertise in the fields of programming, promotion, marketing, sales, distribution, web, digital, linear, mobile, legal and finance. The members of our advisory board are renowned in their respective fields, are considered thought leaders in the entertainment industry by their peers, further enhance our credibility and provide strategic guidance to our management team.

Many of the members of our leadership team have built businesses as entrepreneurs and/or have been executives at Fortune 500 companies. The team includes seasoned Wall Street executives that have collectively been extensively involved in mergers and acquisitions in the live event, recorded music, music publishing, fashion, technology and other media and entertainment businesses. Our leadership team provides the knowledge to source, analyze, negotiate and complete acquisition transactions, partnerships and other business combinations.

Strategy

Content

During the year ended March 31, 2019, we livestreamed 24 major music festivals and events. As of today, we are contracted to stream over 50 live performance festivals and events. The majority of our agreements provide us multi-year, exclusive rights to produce and digitally stream these live festivals across any screen in most major territories around the world for periods between two to seven years. Moreover, and in most cases, we also have the exclusive rights to VOD, AR, VR, broadcast TV and audio rights from these festivals (subject to music copyright clearances). We believe there is substantial value in producing and streaming live music events.

Our near-term strategy is to continue aggressively acquiring and aggregating live and on-demand performances (e.g., on stage sets) and non-performance (e.g., behind the scenes, interviews) music-related video content from festivals, clubs, events, concerts, artists, promoters, venues, music labels and publishers (collectively, the “Content Providers”); acquiring and producing original music-related video and audio content; and curating existing online and digital radio premium content. In addition to acquiring and/or partnering with third party Content Providers, our digital studio, LXL Studios, plans to develop and produce original music-related video content, including digital magazine-style news programming and original-concept digital pilots and documentaries.

With approximately 2,000 festival-like live events in the world today, we also believe there is enough live music content to acquire and fill our programming 24/7/365.

Over the long term, our strategy is to combine our live events with our audio music and radio services (collectively, the “Music Services”). We believe that the combination of these Music Services will serve as our user engagement platform, differentiate our Music Services from our competitors and provide us more opportunities to expand and grow our current user base and revenues from subscription fees, advertising, sponsorship and licensing. Moreover, we plan to drive more audience to our Music Services platform of as we grow our streamed live events, helping us leverage and lower our overall marketing spending and drive more user growth.

6

Advertising and Long-Term Revenue Opportunities

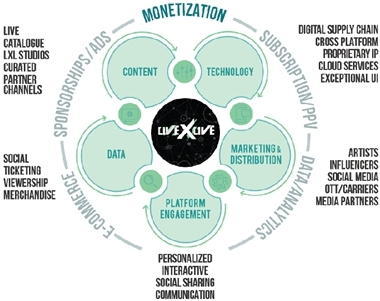

During the years ended March 31, 2019 and 2018, approximately 10% of our revenue was from advertising and licensing, respectively, and the remainder was from subscription revenue from our audio music services platform. Our near-term strategy is to increase the overall percentage mix of advertising and licensing versus subscription revenue. Beginning in the second half of our year ended March 31, 2019, we launched advertising services across our LiveXLive streaming services. Over the long-term, our plan is to continue to grow our advertising and licensing capabilities across our entire Music Services platform. Part of our long-term strategy also includes immersing our fans into the live music experience digitally. As a result, we also plan to introduce other revenue lines of services customarily available at live events including event ticket sales and music merchandise sales. We also believe the data we generate from our platform will be valuable to Industry Stakeholders.

Platform Innovation

Our platform engagement strategy is to build a compelling online and digital experience for our users, anchored by a pioneering website and our custom LXL App. The LiveXLive platform offers access to some of the world’s leading music festivals and live events with multi-day and simultaneous multi-stage coverage, unique concerts, intimate performances and premium original programming. It is fueled by our LXL App, which we believe will drive 24/7/365 user engagement and data that we will be able to convert to earnings and cash flow through multiple potential revenue streams.

We have designed and developed our new custom App with interactive features that enhance the live music experience and, when combined with our platform’s functionality, unique features and underlying music service, create an immersive digital experience in and of itself. We believe the combination of the intuitive, modern LiveXLive user interface and cross-platform capabilities will be instrumental in creating a deeply engaging, personally-tailored central hub for live music, music-related video content and streaming music content, particularly for those users who are otherwise unable to attend live events in person. Our aim is to also include features for personalization, social interaction services, multiple live channels, vertical video, merchandise and other offerings to further solidify users’ affinity toward our platform and their interests.

LiveXLive currently runs on a responsive HTML-based website that has been developed to work across browsers on any Internet-connected screen. The website’s home page includes featured content portals used for programming the most relevant content. The remainder of the page features video content and music stations that are updated regularly and covers a full spectrum of music genres. As our content library and user data grows, the featured content portals and other aspects of the user experience will be individually personalized and tailored to a user’s preferences and interests. We have added video, display and other advertising to the website to generate additional revenue. We will work with our developers to continue to iterate, add and tweak features based on internal and external feedback.

Launched in May 2019, the new unified LXL App ecosystem includes live streaming video, VOD, streaming music stations, push notifications, festival-specific functionality, original content video, locally sold and programmatic ads capability, the capability to display time-shifted content and enhanced functionality that will support social media sharing and user community engagement. The main Live page of the LXL App includes a top hero carousel depicting featured performances and options for viewing concurrent programming located below the top carousel. The LXL App also include a Live Video experience tab dedicated to ongoing and past festivals. For this section, we allow users to view multiple stages of a single festival broadcasting live simultaneously when applicable. We believe this fun and simple interface layout, together with LiveZone, will highlight key content and encourage users to also discover our other content offerings.

7

The new unified LXL App will showcase several features that we believe will encourage and facilitate user engagement and interactivity, including:

Artist Picker - Personalization — This feature is foundational for personalization and recommendations of content with user profile integration; artists that are picked will track to user profiles for personalization. Through our acquisition of Slacker, we are able to add their highly developed enterprise content and user management systems to the LiveXLive platform. Once they have been upgraded to work with video as well as audio, they will form the core of LiveXLive’s data management platform and personalization system.

Personalized & Programmed Content Carousels — Content carousels are a key feature of the new unified App with the ability to feature multiple programmed and personalized content of Live events, VOD featured content and audio streams.

Slacker-Powered Music Service — With the unification convergence of two content services, this integration includes the Slacker music service for streaming radio stations with data informed human curation. Slacker’s expertise and toolset for generating both human curated and programmatically generated media channels allow LiveXLive to quickly bring both audio and video channels to market for a fraction of the expense typically associated with those activities.

Live Video Experience — The centerpiece foundation of our digital live experience to engage music fans is the Live Video experience section in which livestream video feeds, video on-demand, set-time schedules, real-time user interface elements and community interaction come together in a single unique digital environment.

Dynamic Video Player — Our player supports both Live streams and VOD playback, and also supports Vertical Video, which displays video with an edge-to-edge format in portrait view. This is how younger generations consume video and is a commonly familiar format catering to Millennials and Gen Zers.

Multiple Live Channels — For Live video broadcasts, this video player feature allows for easily switching between multi-channel perspectives covering different performances and stages of the live event being watched.

Social Sharing — With this social sharing functionality, app users are able to share content to Facebook, Twitter, Gmail, by SMS text and more.

Chat — In our endeavor to enhance the live event experience digitally, we will feature an integrated user chat system so users can connect, share and comment regarding the live content. The integrated chat will allow users to connect, comment and share, all without leaving the LXL App.

Community Features — Central to the consumption of live music online is the ability for the audience to interact with each other, our hosts and influencers, and the artists themselves. We are building out the social features for our social community based around highly engaging, exclusive live music festival broadcasts that will enable us to innovate our social engagement tools beyond the competition.

By executing the above strategies, we are creating a platform that is dedicated to live music and has the breadth and depth of content to reach and be relevant to a global audience of all ages.

8

Market Leader – Live Music Events and Content

We believe there is significant unmet demand for experiencing live music, musical performance video on demand and related content online. To become a centralized hub for live music and music-related video content, we plan to execute the following interconnected components of our business: Content Aggregation, Technology Development, Marketing and Distribution, Platform Engagement and Data Collection:

Competition

While the broader market for live entertainment remains highly competitive, the digital distribution of live and music-related video content is still a nascent market. We believe live streamed music video content is the only remaining media genre without a dominant brand. We believe there is a tremendous amount of high-quality live music content available to be captured and produced but without a singular home for distribution and access by the public at large.

We expect to compete for the time and attention of our users with other Content Providers based on a number of factors, including: quality of experience, relevance, acceptance and diversity of content, ease of use, price, accessibility, perceptions of advertisement load, brand awareness and reputation. We also expect to compete for the time and attention of users based on the presence and/or visibility of the LiveXLive platform as compared with other platforms and Content Providers that deliver content through Internet-connected screens.

Our competitors includes (i) broadcast radio providers, including terrestrial radio providers such as CBS and satellite radio providers such as Sirius XM, (ii) interactive on-demand audio content and pre-recorded entertainment, such as Apple’s iTunes Music Store and Apple Music, Rhapsody, Spotify, Pandora, Tidal and Amazon Music that allow listeners to stream music or select the audio content that they stream or purchase, (iii) other forms of entertainment, including Facebook, Twitch, Instagram, Google / YouTube, Twitter (including Periscope), and Yahoo, which offer a variety of Internet and mobile device-based products, services and content, and (iv) promoters and producers of content on mobile, online and AR/VR platforms such as Red Bull TV, Live Nation TV and independent content owners. To the extent that existing or potential users choose to watch satellite or cable television, streaming video from on demand services such as Hulu, VEVO or YouTube, or play interactive video games on their home-entertainment system, computer or mobile phone rather than use the LiveXLive service, these content services pose a competitive threat. Conversely, these content platforms can also become valuable distribution partners. For example, in 2019 we livestreamed our music festivals and events across Facebook, YouTube and Twitch, and partnered with iHeartMedia to livestream multiple iHeart-sponsored events across our music platform.

We may also face direct competition from other large live music event competitors with regards to online distribution of live music and music-related video content, ticketing and sponsorship opportunities, including from Live Nation, AEG, and LiveStyle (formerly SFX). Furthermore, there are many smaller, regional companies that compete in the market as well.

Music Copyright and Rights Regulation

As a participant in the global music and radio industries, we are subject to a variety of copyright and regulatory obligations.

| ● | Broadcast Music, Inc. (“BMI”) – BMI is a bridge between songwriters and the business and organizations that want to play their music publicly. BMI supports businesses and organizations that play music publicly by offering blanket music licenses that permit them to play nearly 13 million musical works. |

| ● | The American Society of Composers, Authors and Publishers (“ASCAP”) – ASCAP is a membership association of more than 670,000 songwriters, composers and music publishers. ASCAP licenses over 11.5 million songs and scores to the businesses that play them publicly. |

| ● | SoundExchange – SoundExchange collects and distributes digital performance royalties on behalf of more than 155,000 recording artists and master rights owners and licensees. |

9

Government Regulation

Our operations are subject to various federal, state and local laws statutes, rules, regulations, policies and procedures, both domestically and internationally, governing matters such as:

| ● | labor and employment laws; |

| ● | the United States Foreign Corrupt Practice Act (the “FCPA”) and similar regulations and laws in other countries; |

| ● | sales and other taxes and withholding of taxes; |

| ● | United States Securities and Exchange Commission (the “SEC”) requirements; |

| ● | privacy laws and protection of personally identifiable information; |

| ● | marketing activities online; and |

| ● | United States copyright laws. |

We believe that we are in material compliance with these laws. We are also required to comply with the laws of the countries we operate in and anti-bribery regulations under the FCPA. Such regulations make it illegal for us to pay, promise to pay, or receive money or anything of value to, or from, any government or foreign public official for the purpose of directly or indirectly obtaining or retaining business. This ban on illegal payments and bribes also applies to agents or intermediaries who use funds for purposes prohibited by the statute.

From time to time, governmental bodies have proposed legislation that could have an effect on our business. For example, some legislatures have proposed laws in the past that would impose potential liability on promoters and producers of live music events for entertainment taxes and for incidents that occur at such events, particularly incidents relating to drugs and alcohol. More recently, some jurisdictions have proposed legislation that would restrict ticketing methods and mandate ticket inventory disclosure.

Privacy Policy

As a company conducting business on the Internet, we are subject to a number of foreign and domestic laws and regulations relating to information security, data protection and privacy, among others. Many of these laws and regulations are still evolving and could be interpreted in ways that could hurt our business. In the area of information security and data protection, the laws in several states require companies to implement specific information security controls to protect certain types of personally identifiable information. Likewise, all but a few states have laws in place requiring companies to notify users if there is a security breach that compromises certain categories of their personally identifiable information. Any failure on our part to comply with these laws may subject us to significant liabilities.

We are also subject to federal and state laws regarding privacy of listener data. Our privacy policy and terms of use describe our practices concerning the use, transmission and disclosure of listener information and are posted on our website. Any failure to comply with our posted privacy policy or privacy-related laws and regulations could result in proceedings against us by governmental authorities or others, which could harm our business. Further, any failure by us to adequately protect the privacy or security of our users’ information could result in a loss of confidence in our brand among existing and potential users, and ultimately, in a loss of users and advertising users, which could adversely affect our business.

We will also collect and use certain types of information from our users in accordance with the privacy policies posted on our websites. We will collect personally identifiable information directly from our platform’s users when they register to use our service, fill out their listener profiles, post comments, use our service’s social networking features, participate in polls and contests and sign up to receive email newsletters. We may also obtain information about our platform’s users from other platform users and third parties. We also collect information from users using our other websites in order to provide ticketing services and other user support. Our policy is to use the collected information to customize and personalize our offerings for platform users and other users and to enhance the listeners’ experience when using our service.

The sharing, use, disclosure and protection of personally identifiable information and other user data are governed by existing and evolving federal, state and international laws. We could be adversely affected if legislation or regulations are expanded to require changes in business practices or privacy policies, or if governing jurisdictions interpret or implement their legislation or regulations in ways that negatively affect our business, financial condition and results of operations. We intend to attract users from all over the world, and as we expand into new jurisdictions, the costs associated with compliance with these regulations increases. It is possible that government or industry regulation in these markets will require us to deviate from our standard processes, which will increase operational cost and risk. We intend to commit capital resources to ensure our compliance with any such regulations.

10

Intellectual Property

While we do not currently have a trademark on the LiveXLive name, on September 23, 2017, we entered into a Co-Existence Agreement with Monday Sessions Media, Inc. D/B/A Live X (“Live X”), in which we consented to Live X’s use and registration of the name and mark Live X and agreed to not challenge, dispute or contest Live X’s rights in such mark. Pursuant to this agreement, we agreed to not offer certain production services to third party businesses in connection with our mark LIVEXLIVE and use commercially reasonable efforts to afford Live X opportunities to bid on production or streaming service opportunities. We intend to protect our trademarks, brands, copyrights, patents and other original and acquired works, ancillary goods and services. In connection with the Slacker acquisition, we acquired a trademark for the Slacker name. We believe that certain trademarks and other proprietary rights that we may apply for or otherwise obtain will have significant value and will be important to our brand-building efforts and the marketing of our services. We cannot predict, however, whether steps taken by us to protect our proprietary rights will be successful or adequate to prevent misappropriation, infringement or other violation of these rights. Upon the consummation of any future acquisitions, we may acquire additional registered trademarks, as well as applied-for trademarks potentially for worldwide use. See section below entitled “Item 1A. Risk Factors — We may be unable to adequately protect our intellectual property rights.”

Employees

As of March 31, 2019, we had 76 full-time employees, including through our subsidiaries. All of our employees are located in the United States. We are not party to any collective bargaining agreements and have not experienced any strikes or work stoppages. We believe our relationship with all of our employees is very good. In addition to our employees, we engage key consultants and utilize the services of independent contractors to perform various services on our behalf. Some of our executive officers and directors are engaged in outside business activities that we do not believe conflict with our business.

Going Concern

We are dependent upon the receipt of capital investment and other financing to fund our ongoing operations and to execute our business plan. If continued funding and capital resources are unavailable at reasonable terms, we may not be able to implement our plan of operations. We may be required to obtain alternative or additional financing, from financial institutions or otherwise, in order to maintain and expand our existing operations. The failure by us to obtain such financing would have a material adverse effect upon our business, financial condition and results of operations.

Our consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. Our independent registered public accounting firm has included an explanatory paragraph in their report in our audited consolidated financial statements for the fiscal year ended March 31, 2019 to the effect that our losses from operations and our negative cash flows from operations raise substantial doubt about our ability to continue as a going concern. Our consolidated financial statements do not include any adjustments that might be necessary should we be unable to continue as a going concern within one year after the date that the financial statements are issued. We may be required to cease operations which could result in our stockholders losing all or almost all of their investment.

Segment Reporting and Geographic Information

For additional information regarding our segments, including information about our financial results by geography, see Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations and Note 1 – Organization and Basis of Presentation to our consolidated financial statements included elsewhere in this Annual Report.

Corporate History

On August 2, 2017, our name changed from “Loton, Corp” to “LiveXLive Media, Inc.”, and we reincorporated from the State of Nevada to the State of Delaware, pursuant to the reincorporation merger of Loton, Corp (“Loton”), a Nevada corporation, with and into LiveXLive Media, Inc., a Delaware corporation and Loton’s wholly owned subsidiary, effected on the same date. As a result of such reincorporation merger, Loton ceased to exist as a separate entity, with LiveXLive Media, Inc. being the surviving entity. Our principal executive offices are located at 269 South Beverly Drive, Suite #1450, Beverly Hills, CA 90212.

Available Information

Our main corporate website address is www.livexlive.com. Copies of our Quarterly Reports on Form 10-Q, Annual Reports on Form 10-K, Current Reports on Form 8-K and our other reports and documents filed with or furnished to the SEC, and any amendments to the foregoing, will be provided without charge to any shareholder submitting a written request to the Secretary at our principal executive offices or by calling (310) 601-2500. All of our SEC filings are also available on our website at http://ir.livexlive.com/ir-home as soon as reasonably practicable after having been electronically filed or furnished to the SEC. All of our SEC filings are also available at the SEC’s website at www.sec.gov.

We began formal investor earnings calls during the fiscal year ended March 31, 2019, and certain events we participate in or host with members of the investment community on the investor relations section of our corporate website. Additionally, we provide notifications of news or announcements regarding our financial performance, including SEC filings, investor events, and press and earnings releases on the investor relations section of our corporate website. Investors can receive notifications of new press releases and SEC filings by signing up for email alerts on our website. Further corporate governance information, including our board committee charters and code of ethics, is also available on our website at http://ir.livexlive.com/ir-home. The information included on our website or social media accounts, or any of the websites of entities that we are affiliated with, is not incorporated by reference into this Annual Report or in any other report or document we file with the SEC, and any references to our website or social media accounts are intended to be inactive textual references only.

11

| Item 1A. | Risk Factors |

You should carefully consider the risks described below, together with all of the other information included in this Annual Report, before deciding whether to invest in our common stock. The occurrence of any of the risks described below could have a material adverse effect on our business, financial condition, results of operations and future growth prospects. In these circumstances, the market price of our common stock could decline, and you may lose all or part of your investment.

Risks Related to Our Business and Industry

We rely on one key customer for a substantial percentage of our music services revenue.

Our business is dependent on our customer relationship with Tesla, which accounted for 41% and 24% of our consolidated revenue for the years ended March 31, 2019 and 2018. Our existing agreement with Tesla governs our music services to its car user base in North America, including our audio music streaming services. If we fail to maintain certain minimum service level requirements related to our service with Tesla, Tesla may terminate our agreement to provide them with such service. Similarly, if we fail to meet other obligations related to our technology or services, Tesla may have the right to terminate our agreement to provide them with such services. Tesla may also terminate their agreement with us for convenience Our business would be materially adversely affected if Tesla terminates our services or our agreement to provide them with our services.

Our limited operating history makes it difficult to evaluate our current business and future prospects, and we may be unsuccessful in executing our business model.

We began our current business operations in February 2015 and have a limited operating history related to our current business. We are now a global digital media company focused on live entertainment. As of March 31, 2019, we generated minimal revenue from the operations of our live music streaming platform. In December 2017, we acquired Slacker Radio (“Slacker”) and substantially all of our revenues as of March 31, 2019 were generated by Slacker. To date, we have devoted most of our financial resources to developing our current business model, growing Slacker’s user base and product offerings and making key acquisitions. We expect to continue to incur substantial and increased expenses as we continue to execute our business approach, including expanding and developing our content and platform and potentially making other accretive acquisitions.

The likelihood of our success must be considered in light of the problems, expenses, difficulties, complications and delays frequently encountered by a developing company starting a new business enterprise, the difficulties that may be encountered with integrating acquired companies and the highly competitive environment in which we operate. For example, while several companies have been successful in the digital music streaming industry and the online video streaming industry, companies have had no or limited success in operating a premium Internet network devoted to live music and music-related video content. Because we have a limited operating history, we cannot assure you that our business will be profitable or that we will ever generate sufficient revenue to fully meet our expenses and support our anticipated activities.

We have incurred significant operating and net losses since our inception and anticipate that we will continue to incur significant losses for the foreseeable future; our auditors have included in their audit report for the fiscal year ended March 31, 2019 an explanatory paragraph as to substantial doubt as to our ability to continue as a going concern.

As reflected in our consolidated financial statements included elsewhere herein, we have incurred significant operating and net losses in each year since our inception, including net losses of $37.8 million and $23.3 million for the fiscal years ended March 31, 2019 and 2018, respectively. As of March 31, 2019, we had an accumulated deficit of $89.2 million and a working capital deficiency of $14.6 million. We anticipate incurring additional losses until such time that we can generate significant increases to our revenues, and/or reduce our operating costs and loses. To date, we have financed our operations exclusively through the sale of equity and/or debt securities (including convertible securities). The size of our future net losses will depend, in part, on the rate of future expenditures and our ability to significantly grow our business and increase our revenues. We expect to continue to incur substantial and increased expenses as we grow our business. We also expect a continued increase in our expenses associated with our operations as a publicly-traded company. We may incur significant losses in the future for a number of other reasons, including unsuccessful acquisitions, costs of integrating new businesses, expenses, difficulties, complications, delays and other unknown events. As a result of the foregoing, we expect to continue to incur significant losses for the foreseeable future and we may not be able to achieve or sustain profitability.

Our auditors have included in their audit report for the fiscal year ended March 31, 2019 a “going concern” explanatory paragraph raising substantial doubt as to our ability to continue as a going concern. Our ability to meet our total liabilities of $49.4 million as of March 31, 2019, and to continue as a going concern, is dependent on our ability to increase revenue, reduce costs, achieve a satisfactory level of profitable operations, obtain additional sources of suitable and adequate financing and further develop and execute on our business plan. We may never achieve profitability, and even if we do, we may not be able to sustain being profitable. As a result of the going concern uncertainty, there is an increased risk that you could lose the entire amount of your investment in our company, which assumes the realization of our assets and the satisfaction of our liabilities and commitments in the normal course of business.

12

We may require additional capital, including to fund our current debt obligations and to fund potential acquisitions and capital expenditures, which may not be available on terms acceptable to us or at all and which depends on many factors beyond our control.

Historically, we have funded our business operations and capital expenditures primarily through equity and/or debt issuances (including convertible securities). To support our growing business, we must have sufficient capital to continue to make significant investments in our platform and product offerings. If we raise additional funds through the issuance of equity, equity-linked or debt securities, those securities may have rights, preferences or privileges senior to those of our common stock, and our existing stockholders may experience dilution. Any debt financing secured by us in the future could involve restrictive covenants relating to our capital-raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital and to pursue business opportunities. Any refinancing of our indebtedness could be at significantly higher interest rates, require additional restrictive financial and operational covenants, or require us to incur significant transaction fees, issue warrants or other equity securities, or issue convertible securities. These restrictions and covenants may restrict our ability to finance our operations and engage in, expand, or otherwise pursue our business activities and strategies. Our ability to comply with these covenants and restrictions may be affected by events beyond our control, and breaches of these covenants and restrictions could result in a default and an acceleration of our obligations under a debt agreement. If we raise additional funds through collaborations and licensing arrangements, we might be required to relinquish significant rights to our technologies or our solutions under development, or grant licenses on terms that are not favorable to us, which could lower the economic value of those programs to us.

We evaluate financing opportunities from time to time, and our ability to obtain financing will depend, among other things, on our development efforts, business plans and operating performance and the condition of the capital markets at the time we seek financing and to an extent, subject to general economic, financial, competitive, legislative, regulatory and other factors that are beyond our control. We cannot be certain that additional financing will be available to us on favorable terms, or at all. If we are unable to obtain adequate financing or financing on terms satisfactory to us, when we require it, our ability to continue to support our business growth and to respond to business challenges could be significantly limited, and our business, financial condition and results of operations could be adversely affected.

We depend on a limited number of customers for a substantial portion of our revenues. The loss of a key customer or the significant reduction of business or growth of business from our largest customer could significantly adversely affect our business, financial condition and results of operations.

We have derived, and we believe that we will continue to derive, a substantial portion of our revenues from a limited number of customers. For example, for the year ended March 31, 2019 and 2018, our largest customer by revenue accounted for 41% and 24% of our revenues, respectively. If we were to lose one or more of our key customers or experience a significant reduction of business from our largest customer, there is no assurance that we would be able to replace such customers or lost business with new customers that generate comparable revenue, which would significantly adversely affect our business, financial condition and results of operations. In addition, there could be no assurance that our revenues from our largest customer continues to grow at same rate or at all. Any revenue growth will depend on our success in growing our customers’ revenues on our platform and expanding our customer base to include additional customers.

Our business is partially dependent on our ability to secure music streaming rights from Content Providers and to stream their live music and music-related video content on our platform, and we may not be able to secure such content on commercially reasonable terms or at all.

Our business is dependent on our ability to secure rights to stream on our platform a variety of popular content from Content Providers. Our licensing, distribution and/or production arrangements with Content Providers may be short-term and do not guarantee the continuation or renewal of these arrangements on commercially reasonable terms, if at all. For example, our agreement with Rock in Rio expires in 2020 and there is no guarantee that we will be able to renew this agreement on commercially reasonable terms or at all. Additionally, while our agreements with music festivals and other live music events and venues allow us to stream content from such events and venues, we typically require additional permission from the artists performing at such events, other rights holders and venues. While the majority of artists at music festivals and other live music events and venues that we have contracts with have in the past agreed to allow us to stream their performances, there is no guarantee that artists at an event will agree to allow us to stream their performances. Any unwillingness of such partners to supply content to us or lack of availability of popular artists to perform at such venues and events could limit our ability to enhance user experience and deepen user engagement with our platform and therefore reduce our revenue opportunities. If we are unable to secure rights to steam our content, then our business, financial condition and results of operations would be adversely affected. Additionally, to the extent any music festival or other live music event that we have rights to stream is cancelled or delayed, whether as a result of cancellation by artists, weather, terrorism or otherwise, we may receive little or no content from such live event.

In the 2019 fiscal year, we also began livestreaming our own live events under “LiveXLive Presents”. As we continue to livestream and grow our own live events, we may directly compete with our current and prospective Content Providers. This direct competition with our current and prospective Content Providers could harm our existing and future relationships with our Content Providers, and may result in a decline in the number of live events partnership, license, distribution and/or production opportunities available to us, which could adversely affect our business, financial condition and results of operations.

Some Content Providers and distributors, currently or in the future, may also take action to make it more difficult or impossible for us to partner with, license, distribute and/or produce their content, including as a result of them offering a competing product. Other content owners, providers or distributors may seek to limit our access to, increase the cost of, or otherwise restrict or prohibit our use of such content. As a result, we may be unable to offer a wide variety of content at reasonable prices with acceptable usage rules or expand our geographic reach.

13

Additionally, some content on our platform is currently provided free of digital rights management to prevent the unauthorized redistribution of digital media. If our business model changes, we may have to develop or license digital rights management technology. There is no assurance that we will be able to develop or license such technology at a reasonable cost and in a timely manner. In addition, certain countries have passed or may propose and adopt legislation that would require us to license our digital rights management, if any, which could weaken the protection of content, subject us to piracy and also negatively affect arrangements with our Content Providers.

We may be unable to fund any significant up-front and/or guaranteed payment cash requirements associated with our live music streaming rights, which could result in the inability to secure and retain such streaming rights and may limit our operating flexibility, which may adversely affect our business, operating results and financial condition.

In order to secure event and festival live music streaming rights, we may be required to fund significant up-front and/or guaranteed payment cash requirements to artists or festival or event promoters prior to the event or festival taking place. For example, our agreement with Insomniac requires us to pay Insomniac $1 million per year during the 5-year term, in addition to other payments and upfront expenses required to be paid by us under the agreement, and there is no guarantee that we will be able to make such payments on time. As of March 31, 2019, we have estimated future up-front and minimum guarantee (“MGs”) commitments of $5.8 million. While some MGs are recoupable by us as a direct cost before we share any revenue with the underlying partners, such future MGs are not tied to a number of users, active users, premium subscribers or the number of times we stream such content on our platform. Accordingly, our ability to achieve and sustain profitability and operating leverage on our services in part depends on our ability to increase our revenues through increased sales of premium services and advertising sales on terms that maintain an adequate gross margin. The duration of our content acquisition agreements that contain MGs is typically between three to seven years, but our premium subscribers may cancel their subscriptions at any time. If our forecasts for premium subscribers do not meet our expectations or the number of our premium subscribers or advertising sales do not materialize and or decline significantly during the term of our content acquisition agreements, our margins may be materially and adversely impacted. To the extent our premium service revenue growth or advertising sales do not meet our or our partners’ collective expectations, our business, operating results and financial condition also could be adversely impacted as a result of such MGs. In addition, the fixed cost nature of these MGs may limit our flexibility in planning for, or reacting to, changes in our business and the market segments in which we operate.

We rely on estimates of the market share of licensable content controlled by each content provider, as well as our own user growth and forecasted advertising revenue, to forecast whether such MGs could be recouped against our actual content acquisition costs incurred over the duration of each content acquisition agreement. To the extent that these revenue and/or market share estimates underperform relative to our expectations, leading to content acquisition costs that do not exceed such up-front and minimum guarantees, our margins may be materially and adversely impacted. If we do not have sufficient cash on hand or available capacity to advance the necessary cash for any given artist, event or festival, we would not be able to retain the rights for that artist, festival or event, such counter parties may be able to terminate their content acquisition agreements with us, and as a result our business, financial condition and results of operations may be adversely affected.

If we fail to increase the number of users consuming our live music and music-related video content on our platform, and/or the number of subscribers to Slacker, our business, financial condition and results of operations may be adversely affected.

The size of our user base is critical to our success, and we will need to develop and grow our user base to be successful. We currently generate revenue from Slacker’s operations and expect to generate additional revenue based upon subscription, VOD, and PPV, advertising and sponsorship, licensing, e-commerce and data, which is dependent on the number of users we retain and attract. For example, if we are unable to retain and attract users, we may be unable to attract users to our network and/or increase the frequency of users’ engagement with our platform. In addition, if users do not perceive our content as original, entertaining or engaging, we may not be able to attract sponsorship opportunities and/or increase the resulting frequency of users’ engagement with our platform and content. If we are unable to retain and attract users, our network and services could also be less attractive to potential new users, as well as to Content Providers and other Industry Stakeholders, which could have a material and adverse impact on our business, financial condition and results of operations.

14

Our ability to attract and retain users is highly sensitive to rapidly changing public tastes in music and technology.