Registration No. 333-167277

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C.

20549

FORM F-1/A 4

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Pan American Lithium

Corp.

(Exact name of Registrant as specified in its

charter)

Not Applicable

(Translation of Registrant’s

name into English)

| British Columbia | 1099 | 98-0643065 |

| (State or other jurisdiction of | (Primary standard industrial | (IRS Employer |

| incorporation or organization) | Classification Code Number) | Identification No.) |

Suite 110, 3040 N. Campbell Avenue

Tucson, Arizona USA

85719

(520) 989-0031

(Address, including zip code, and

telephone number, including area code, of Registrant’s principal executive

offices)

Pan American Lithium Corp.

Suite 110, 3040 N. Campbell Avenue

Tucson, Arizona USA 85719

(520) 989-0031

(Name, address, including zip code, and

telephone number, including area code, of agent for service)

Approximate date of commencement of proposed sale to the public: From time to time after this Registration Statement is declared effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to

Rule 462(d) under the Securities Act, check the following box and list the

Securities Act registration statement number of the earlier effective

registration statement for the same offering. [ ]

CALCULATION OF REGISTRATION FEE

| Proposed | ||||||||||||

| Maximum | Proposed | |||||||||||

| Amount | Offering | Maximum | Amount of | |||||||||

| Title of Each Class of | to be | Price Per | Offering | Registration | ||||||||

| Securities to be Registered | Registered | Share(1) | Price | Fee | ||||||||

| Common Stock to be offered for resale by selling stockholders | 2,913,400 | $ | 0.15 | $ | 437,010.00 | $ | 42.83 | |||||

| Common Stock to be offered for resale by selling stockholders upon exercise of options | 425,000 | $ | 0.15 | $ | 63,750 | $ | 11.82 |

(1) Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(o) under the Securities Act.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The selling shareholders will sell the common stock being registered in this offering at a fixed price of $0.15 per share, until the securities are quoted on the OTC Bulletin Board and thereafter at prevailing market prices or privately negotiated prices. Our shares may never be quoted on the OTC Bulletin Board.

2

SUBJECT TO COMPLETION, DATED ______________, 2010.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS

PAN AMERICAN LITHIUM CORP.

3,338,400 Shares of Common stock

This prospectus relates to the resale by the selling security holders named in this prospectus of up to 3,338,400 shares of our common stock consisting of:

- up to 2,913,400 shares of our common stock that we issued to 18 investors; and

- up to 425,000 shares of our common stock that may be issued upon the exercise of up to 425,000 outstanding options that were issued to 5 investors.

We will not receive any proceeds from the sale of the shares of common stock by the selling security holders, though we may receive up to $163,750 in proceeds upon the exercise of all of the options to purchase shares of common stock.

The securities being registered in this offering may be illiquid because they are not listed on any U.S. exchange or quoted on the OTC Bulletin Board and no market for these securities may develop. Further, while our common shares are traded on the TSX Venture Exchange, our common shares have historically been sporadically or thinly traded on the TSX Venture Exchange. The selling shareholders will sell the common stock being registered in this offering at a fixed price of $0.15 per share, until the securities are quoted on the OTC Bulletin Board or listed on an exchange and thereafter at prevailing market prices or privately negotiated prices. Our shares may never be quoted on the OTC Bulletin Board or listed on an exchange.

Our Auditor has raised substantial doubts about our ability to continue as a going concern.

The securities offered in this prospectus involve a high degree of risk. You should consider the risk factors beginning on page 6 before purchasing our common stock.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is _______________, 2010.

Table of Contents

Unless otherwise specified, the information in this prospectus is set forth as of November 19, 2010, and we anticipate that changes in our affairs will occur after such date. We have not authorized any person to give any information or to make any representations, other than as contained in this prospectus, in connection with the offer contained in this prospectus. If any person gives you any information or makes representations in connection with this offer, do not rely on it as information we have authorized. This prospectus is not an offer to sell our common stock in any state or other jurisdiction to any person to whom it is unlawful to make such offer.

4

PROSPECTUS SUMMARY

In this prospectus, unless otherwise specified, all references to “common shares” refer to the shares of our common stock and the terms “we”, “us”, “our”, and “the Company” mean Pan American Lithium Corp.

The following summary highlights selected information from this prospectus and may not contain all the information that is important to you. To understand our business and this offering fully, you should read this entire prospectus carefully, including the financial statements and the related notes beginning on page F-1. This prospectus contains forward-looking statements and information relating to us. See “Cautionary Note Regarding Forward Looking Statements” on page 32.

Our Company

We were incorporated under the laws of the Province of British Columbia on September 18, 2006. We are a mineral exploration company traded on the TSX Venture Exchange engaged in the business of acquiring, exploring, and evaluating natural resource properties, and recently focused on the acquisition of interests in, and exploring for, lithium properties in Latin America. We are currently listed for trading on the TSX Venture Exchange under the symbol “PL.”

We currently have one set of lithium exploration properties consisting of interests in nine lithium brine salars in Atacama Region III, Chile and an option to acquire an indirect interest in the Cerro Prieto lithium geothermal brine project in Baja California Norte, Mexico, described below under “Proposed Transactions.” We formerly owned the Aspen Grove copper property in the Nicola Mining District, British Columbia, Canada, the details of which are set out below. We have not yet determined whether our property interests contain reserves that are economically recoverable. The recoverability of amounts shown for resource properties and related deferred exploration expenditures are dependent upon the discovery of economically recoverable reserves, confirmation of the our interest in the underlying mineral claims, our ability to obtain necessary financing to complete the development of the resource at such property and upon future profitable production or proceeds from the disposition thereof.

Our principal executive office is located at Suite 110, 3040 N. Campbell Avenue, Tucson, Arizona USA 85719. Our telephone number is ( 520 ) 623-3090.

ABOUT THIS OFFERING

Securities Being Offered

This prospectus relates to the resale by the selling security holders named in this prospectus of up to 3,338,400 shares of our common stock consisting of:

- up to 2,913,400 shares of our common stock that we issued to 18 investors; and

- up to 425,000 shares of our common stock that may be issued upon the exercise of up to 425,000 outstanding options that were issued to 5 investors.

Offering Price

The selling shareholders will sell the common stock being registered in this offering at a fixed price of $0.15 per share, until the securities are quoted on the OTC Bulletin Board or listed on an exchange and thereafter at prevailing market prices or privately negotiated prices. Our shares may never be quoted on the OTC Bulletin Board.

Use of Proceeds

We will not receive any proceeds from the sale of the shares of common stock by the selling security holders, though we may receive up to $163,750 in proceeds upon the exercise of all of the options to purchase shares of common stock. We will pay all the expenses of the offering.

Risk Factors

An investment in our common stock is highly speculative and involves a high degree of risk. See Risk Factors beginning on page 6.

5

RISK FACTORS

An investment in our common stock is highly speculative, involves a high degree of risk, and should be made only by investors who can afford a complete loss. You should carefully consider the following risk factors, together with the other information in this prospectus, including our financial statements and the related notes, before you decide to buy our common stock. If any of the following risks actually occur, our business, financial condition, or results of operations could be materially adversely affected, the trading of our common stock could decline, and you may lose all or part of your investment therein.

Risks Relating to the Early Stage of our Company and Ability to Raise Capital

We are at a very early stage and our success is subject to the substantial risks inherent in the establishment of a new business venture.

The implementation of our business strategy is in a very early stage and subject to all of the risks inherent in the establishment of a new business venture. Accordingly, our intended business and prospective operations may not prove to be successful in the near future, if at all. Any future success that we might enjoy will depend upon many factors, many of which are beyond our control, or which cannot be predicted at this time, and which could have a material adverse effect upon our financial condition, business prospects and operations and the value of an investment in our company.

We have no operating history and our business plan is unproven and may not be successful.

Although our business formed in September 2006, we have no commercial operations. None of our projects have proven or provable reserves, are built, or are in production. We have not licensed or sold any mineral products commercially and do not have any definitive agreements to do so. We have not proven that our business model will allow us to generate a profit.

We have suffered operating losses since inception and we may not be able to achieve profitability.

We had an accumulated deficit of $ 2,844,909 as of August 31, 2010 and we expect to continue to incur significant discovery and development expenses in the foreseeable future related to the completion of feasibility, development and commercialization of our projects. As a result, we will be sustaining substantial operating and net losses, and it is possible that we will never be able to sustain or develop the revenue levels necessary to attain profitability.

We may have difficulty raising additional capital, which could deprive us of necessary resources.

We expect to continue to devote significant capital resources to fund exploration and development of our properties. In order to support the initiatives envisioned in our business plan, we will need to raise additional funds through public or private debt or equity financing, collaborative relationships or other arrangements. Our ability to raise additional financing depends on many factors beyond our control, including the state of capital markets, the market price of our common stock and the development or prospects for development of competitive technology or competitive projects by others. Because our common stock is not listed on a major stock market, many investors may not be willing or allowed to purchase our common shares or may demand steep discounts. Sufficient additional financing may not be available to us or may be available only on terms that would result in further dilution to the current owners of our common stock.

We expect to raise additional capital during 2010-2011 and have, as of November 19 , 2010, closed a private placement financing in the gross amount of CDN$814,931, but we do not have any firm commitments for funding beyond this recent placement. If we are unsuccessful in raising additional capital, or the terms of raising such capital are unacceptable, we may have to modify our business plan and/or significantly curtail our planned activities. If we are successful raising additional capital through the issuance of additional equity, our investor’s interest will be diluted.

There are substantial doubts about our ability to continue as a going concern and if we are unable to continue our business, our shares may have little or no value.

Our ability to become a profitable operating company is dependent upon our ability to generate revenues and/or obtain financing adequate to explore and develop our properties. Achieving a level of revenues adequate to support our cost structure has raised substantial doubts about our ability to continue as a going concern. We plan to attempt to raise additional equity capital by issuing shares covered by this offering and, if necessary through one or more private placement or public offerings. However, the doubts raised relating to our ability to continue as a going concern may make our shares an unattractive investment for potential investors. These factors, among others, may make it difficult to raise any additional capital.

6

Failure to effectively manage our growth could place additional strains on our managerial, operational and financial resources and could adversely affect our business and prospective operating results.

Our growth has placed, and is expected to continue to place, a strain on our managerial, operational and financial resources. Further, as our subsidiary’s business grows, and if and as we acquire interests in more subsidiaries and other entities, we will be required to manage multiple relationships. Any further growth by us or our subsidiary, or an increase in the number of our strategic relationships will increase this strain on our managerial, operational and financial resources. This strain may inhibit our ability to achieve the rapid execution necessary to implement our business plan, and could have a material adverse effect upon our financial condition, business prospects and prospective operations and the value of an investment in our company.

Risks Relating to Our Business

Because of the unique difficulties and the speculative nature of exploration and uncertainties inherent in mineral exploration companies, we may not be able to develop any proven and probable reserves and faces a high risk of business failure.

Potential investors should be aware of the difficulties normally encountered by mineral exploration companies and the high rate of failure of such enterprises. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration program that we intend to undertake on our properties and any additional properties that we may acquire. These potential problems include unanticipated problems relating to exploration, and additional costs and expenses that may exceed current estimates. The expenditures to be made by us in the exploration of properties we own or may acquire may not result in the discovery of proven and probable mineral reserves. Problems such as unusual or unexpected geological formations and other conditions are involved in all mineral exploration and often result in unsuccessful exploration efforts. If the results of our exploration do not reveal viable commercial mineralization, we may decide to abandon some or all of our property interests.

The potential profitability of mineral ventures depends in part upon factors beyond our control and even if we discover and exploit proven and probable reserves, we may never become commercially viable and/or we may be forced to cease operations.

The commercial feasibility of an exploration program on a mineral property is dependent upon many factors beyond our control, including the existence and size of mineral deposits in the properties we explore, the proximity and capacity of processing equipment, market fluctuations of prices, taxes, royalties, country fiscal regime, land tenure, allowable production, availability of financing and environmental regulation. These factors cannot be accurately predicted and any one or a combination of these factors may result in us not receiving an adequate return on invested capital. These factors may have material and negative effects on our financial performance and our ability to initiate or continue operations.

Exploration development and exploitation activities are subject to comprehensive regulation and permitting which may cause substantial delays or require capital outlays in excess of those anticipated causing a material adverse effect on us.

Exploration, development and exploitation activities are subject to federal, provincial, state and local laws, regulations and policies, including laws regulating permitting and the removal of natural resources from the ground and the discharge of materials into the environment. Exploration, development and exploitation activities are also subject to federal, provincial, state and local laws and regulations which seek to maintain health and safety standards by regulating the design and use of drilling methods and equipment and other operational activities.

Environmental and other legal standards imposed by federal, provincial, state or local authorities may be changed and any such changes may prevent us from conducting planned activities or may increase our costs of doing so, which could have material adverse effects on our business. Moreover, compliance with such laws may cause substantial delays or require capital outlays in excess of those anticipated, thus causing a material adverse effect on us. Additionally, we may be subject to liability for pollution or other environmental damages that we may not be able to or elect not to insure against due to prohibitive premium costs and other reasons. Any laws, regulations or policies of any government body or regulatory agency may be changed, applied or interpreted in a manner which could materially alter and negatively affect our ability to carry on our business.

Title to mineral properties and water rights is a complex issue and we may suffer a material adverse effect in the event one or more of our property interests are determined to have title deficiencies.

Acquisition of title to mineral properties and related water rights can be a very detailed and time-consuming process. Title to, and the area of, mineral properties and water rights may be disputed. Although we have obtained a title opinion in respect to our Chilean salar property interests, we cannot give an assurance that title to such property will not be challenged or impugned. Mineral properties sometimes contain claims or transfer histories that examiners cannot verify. A successful claim that we do not have title to one or more of our properties or lack appropriate water rights could cause us to lose any rights to explore, develop and mine any minerals on that property, without compensation for our prior expenditures relating to such property.

7

One set of our properties is located in Chile, and any material change to the laws of Chile affecting mineral properties may have a material adverse effect on us.

Chile is a developing country. We will be subject to certain risks which may result from changes in Chilean law and politics, including expropriation, currency fluctuation and possible political instability which may result in the impairment or loss of mineral concessions or other mineral or water rights. Changes in regulations or shifts in political conditions are beyond our control and may materially adversely affect our business. Obtaining legal and accounting services in under-developed countries may be difficult and may make implementation of proper controls difficult and assessment of our legal entitlements less certain. Operations may be affected in varying degrees by government regulations with respect to restrictions on production, price controls, export controls, capital repatriation, income taxes, expropriation of property, environmental legislation and mine safety. Chile’s status as a developing country may make it more difficult for us to obtain any required exploration, development and production financing for our projects.

Mineral concessions under Chilean law do not automatically vest title to lithium.

Under Chilean mining law, lithium and certain other metals are technically reserved to the state of Chile for the Chilean National Nuclear Commission. As a consequence, we must apply through the Ministry of Mines for a special operating permit that allows us to process and export lithium products. This permit is authorized and must be signed by the President of Chile. Although we are not aware of any current lithium project in Chile which upon application has not received this permit, the risk still remains that the application which may be submitted by us for this purpose could be rejected. In this event the failure to secure a lithium operating permit could materially and adversely affect our ability to carry on our business.

Because our property interests may not contain proven and probable mineral reserves and because we have never made a profit from our operations, our securities are highly speculative and investors may lose all of their investment in us.

Our securities must be considered highly speculative, generally because of the nature of our business and our stage of operations. We currently have exploration stage property interests which may not contain proven and probable reserves and mineral deposits. We may or may not acquire additional interests in other mineral properties and, except as stated herein, we do not have plans to acquire rights in any specific mineral properties as of the date of this report. Accordingly, we have not generated revenues nor have we realized a profit from our operations to date and there is little likelihood that we will generate any revenues or realize any profits in the short term. Any profitability in the future from our business will be dependent upon locating and exploiting mineral deposits on the our current properties or mineral deposits on any additional properties that we may acquire. The likelihood that any mineral properties that we may acquire or have an interest in will contain commercially exploitable mineral deposits is extremely remote. We may never discover proven and probable reserves on mineral deposits in respect to our current properties or any other area, or we may do so and still not be commercially successful if we are unable to exploit those mineral deposits profitably. We may not be able to operate profitably and may have to cease operations, the price of our securities may decline and investors may lose all of their investment in us.

As we face intense competition in the mineral exploration and exploitation industry, we will have to compete with our competitors for financing and for qualified managerial and technical employees.

Our competition includes large established mining companies with substantial capabilities and with greater financial and technical resources than us. As a result of this competition, we may have to compete for financing and may be unable to acquire financing on terms we consider acceptable. We may also have to compete with the other mining companies for the recruitment and retention of qualified managerial and technical employees. If we are unable to successfully compete for financing or for qualified employees, our exploration programs may be slowed down or suspended, which may cause us to cease operations as a company.

Our future is dependent upon our ability to obtain financing and if we do not obtain such financing, we may have to cease our exploration activities and investors could lose their entire investment.

There is no assurance that we will operate profitably or will generate positive cash flow in the future. We require additional financing in order to proceed with the exploration and development of our properties. We will also require additional financing for the fees we must pay to maintain our rights to our properties and to pay the fees and expenses necessary to operate as a public company. We will also need more funds if the costs of the exploration of our mineral claims are greater than we have anticipated. We will require additional financing to sustain our business operations if we are not successful in earning revenues. We will also need further financing if we decide to obtain additional mineral properties. Although, as of November 19 , 2010, we closed a private placement financing in the gross amount of CDN$814,931, we currently do not have any arrangements for further financing and we may not be able to obtain financing when required. Our future is dependent upon our ability to obtain financing. If we do not obtain such financing, our business could fail and investors could lose their entire investment.

8

Our directors and officers are engaged in other business activities and accordingly may not devote sufficient time to our business affairs, which may affect our ability to conduct operations and generate revenues.

Our directors and officers are involved in other business activities and serve as officers and directors of other mineral exploration companies. As a result of their other business endeavors, the directors and officers may not be able to devote sufficient time to our business affairs, which may negatively affect our ability to conduct our ongoing operations and our ability to generate revenues. In addition, our management may be periodically interrupted or delayed as a result of our officers’ other business interests.

Risks Relating to our Stock

There are a large number of unexercised share purchase warrants and stock options outstanding. If these are exercised, your interest in our company will be diluted.

As of November 19, 2010, there were 38,100,943 shares of our common stock issued and outstanding. If all of the share purchase warrants and options that were issued and outstanding as of that date were to be exercised, including warrants and options that are not yet exercisable, we would be required to issue up to an additional 14,728,740 shares of our common stock, or approximately 38.7% of our issued and outstanding shares of common stock on November 19, 2010. This would substantially decrease the proportionate ownership and voting power of all other stockholders. This dilution could cause the price of our shares to decline and it could result in the creation of new control persons. In addition, our stockholders could suffer dilution in the net book value per share.

Because we can issue additional shares of common stock, purchasers of our common stock may incur immediate dilution and may experience further dilution.

We are authorized to issue an unlimited number of shares of common stock, of which 38,100,943 shares were issued and outstanding as of November 19, 2010. Our board of directors has the authority to cause us to issue additional shares of common stock without consent of any of our stockholders. Consequently, the stockholders may experience more dilution in their ownership of our stock in the future.

The sale of the shares of common stock acquired in private placements could cause the price of our common stock to decline.

The selling stockholders under this registration statement may sell none, some or all of the shares of common stock acquired from us. We have no way of knowing whether or when the selling stockholders will sell the shares covered by this registration statement. Depending upon market liquidity at the time, a sale of shares covered by this registration statement at any given time could cause the trading price of our common stock to decline. The sale of a substantial number of shares of our common stock under this registration statement, or anticipation of such sales, could make it more difficult for us to sell equity or equity-related securities in the future at a time and at a price that we might otherwise wish to effect sales.

Both the registration of shares hereunder and the running of the tacking period under Rule 144 may have the effect of reducing the market price available for shares. Such shares will not be available for sale in the open market without the registration except in reliance upon Rule 144 under the Act. In general, under Rule 144 a person (or persons whose shares are aggregated) who has beneficially owned shares acquired in a non-public transaction for at least one year, including persons who may be deemed Affiliates of our company (as that term is defined under the Act) would be entitled to sell such shares. If a substantial number of the shares owned by management became eligible for sale in the future and were sold pursuant to Rule 144 or a registered offering, the market price of the common stock could be adversely affected.

We will apply to have our common stock traded over the counter, which may deprive stockholders of the full value of their shares.

We currently plan to have our common stock quoted on the OTC Bulletin Board upon the effectiveness of the registration statement of which this prospectus forms a part. In order to do this, a market maker must file a Form 15c-211 to allow the market maker to make a market in shares of our common stock and we are not aware that any market maker has any such intention. We cannot provide our investors with any assurance that our common stock will be traded on the OTC Bulletin Board or, if traded, that a public market will materialize.

Further, the OTC Bulletin Board is not a listing service or exchange, but is instead a dealer quotation service for subscribing members. Therefore, our common stock is expected to have fewer market makers, lower trading volumes and larger spreads between bid and asked prices than securities listed on an exchange such as the New York Stock Exchange or the NASDAQ Stock Market. These factors may result in higher price volatility and less market liquidity for the common stock. Our shares may never be quoted on the OTC Bulletin Board

9

Our stock is a penny stock. Trading of our stock may be restricted by the Securities and Exchange Commission’s penny stock regulations which may limit a stockholder’s ability to buy and sell our stock.

Our common stock is expected to trade at a price substantially below $5.00 per share, which will make it a penny stock. The Securities and Exchange Commission has adopted Rule 15g-9 which generally defines “penny stock” to be any equity security that has a market price (as defined) less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our securities are covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and “accredited investors”. The term “accredited investor” refers generally to institutions with assets in excess of $5,000,000 or individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 jointly with their spouse. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form prepared by the SEC which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction and monthly account statements showing the market value of each penny stock held in the customer’s account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the customer in writing before or with the customer’s confirmation. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules; the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules. Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules discourage investor interest in and limit the marketability of our common stock.

FINRA sales practice requirements may also limit a stockholder's ability to buy and sell our stock.

In addition to the “penny stock” rules promulgated by the Securities and Exchange Commission, the Financial Industry Regulatory Authority (FINRA) has adopted rules that require that in recommending an investment to a customer, a broker-dealer must have reasonable grounds for believing that the investment is suitable for that customer. Prior to recommending speculative low priced securities to their non-institutional customers, broker-dealers must make reasonable efforts to obtain information about the customer’s financial status, tax status, investment objectives and other information. Under interpretations of these rules, the FINRA believes that there is a high probability that speculative low priced securities will not be suitable for at least some customers. The FINRA requirements make it more difficult for broker-dealers to recommend that their customers buy our common stock, which may limit your ability to buy and sell our stock.

An investor’s ability to trade our common stock may be limited by trading volume.

A consistently active trading market for our common stock may not occur on the OTC Bulletin Board. A limited trading volume may prevent our shareholders from selling shares at such times or in such amounts as they may otherwise desire. Our shares may never be quoted on the OTC Bulletin Board or listed on an exchange. Further, while our common shares are traded on the TSX Venture Exchange, our common shares have historically been sporadically or thinly traded on the TSX Venture Exchange.

We have not voluntarily implemented various corporate governance measures, in the absence of which, shareholders may have more limited protections against interested director transactions, conflicts of interest and similar matters.

Recent federal legislation, including the Sarbanes-Oxley Act of 2002, has resulted in the adoption of various corporate governance measures designed to promote the integrity of the corporate management and the securities markets. Some of these measures have been adopted in response to legal requirements. Others have been adopted by companies in response to the requirements of national securities exchanges, such as the NYSE or The NASDAQ Stock Market, on which their securities are listed. Among the corporate governance measures that are required under the rules of national securities exchanges and NASDAQ are those that address board of directors independence, audit committee oversight and the adoption of a code of ethics. While our board of directors has formed an audit committee of which the majority are independent directors, and has adopted a set of corporate governance guidelines, we have not adopted a Code of Ethics and Business Conduct, and other relevant corporate governance measures and, since our securities are not listed on a national securities exchange or NASDAQ, we are not required to do so. It is possible that if we were to adopt some or all of these corporate governance measures, shareholders would benefit from somewhat greater assurances that internal corporate decisions were being made by disinterested directors and that policies had been implemented to define responsible conduct. For example, in the absence of nominating and compensation committees comprised of at least a majority of independent directors, decisions concerning matters such as compensation packages to our senior officers and recommendations for director nominees may be made by a majority of directors who have an interest in the outcome of the matters being decided. Prospective investors should bear in mind our current lack of corporate governance measures in formulating their investment decisions.

10

Because we will not pay dividends in the foreseeable future, stockholders will only benefit from owning common stock if it appreciates.

We have never paid dividends on our common stock and we do not intend to do so in the foreseeable future. We intend to retain any future earnings to finance our growth. Accordingly, any potential investor who anticipates the need for current dividends from his investment should not purchase our common stock.

USE OF PROCEEDS

We will not receive any proceeds from the sale of the shares of common stock by the selling security holders, though we may receive up to $163,750 in proceeds upon the exercise of all of the options to purchase shares of common stock. We will pay all the expenses of the offering.

We are registering the resale of 425,000 shares of common stock to be issued upon the exercise of certain options. The options were granted as follows:

| Date of Grant |

Number of Options |

Exercise Price per Share |

Gross Proceeds upon Exercise |

| Jan. 15, 2010 (1) | 150,000 | $0.50 | $75,000 |

| April 21 , 2010 (2) | 25,000 | $0.55 | $13,750 |

| May 26, 2010 (3) | 250,000 | $0.30 | $75,000 |

(1) One-half of these options became exercisable upon their

grant. The remaining one-half will become exercisable on Jan 15, 2011. The

option agreements are filed as Exhibits 10.22 and 10.25 to this Registration

Statement.

(2) One-half of these options became exercisable upon their grant.

The remaining one-half will become exercisable on April 21, 2011. The option

agreement is filed as Exhibit 10.33 to this Registration Statement.

(3)

One-half of these options became exercisable upon their grant. The remaining

one-half will become exercisable on May 26, 2011. The option agreements are

filed as Exhibits 10.31 and 10.34 to this Registration Statement.

Assuming all the options are exercised, we would receive $163,750.

Our management will have broad discretion in the allocation of the net proceeds of the exercise of the options; however, the following table outlines management’s current anticipated allocation of the net proceeds from the exercise of options. As all the options may not be exercised, management has outlined how they anticipate allocating the net proceeds based on a certain percentage of options being exercised. The scenarios are presented for illustrative purposes only and the actual amount of proceeds, if any, may differ. Pending such uses, we intend to invest the net proceeds in short-term, investment grade, interest-bearing securities. We anticipate that the proceeds from the exercise of any options will not be a significant source of financing. As set out in “Liquidity — Anticipated Cash Requirements”, we anticipate our expenses for the next twelve months will be $1,643,000. Our plans to finance our anticipate expenses are set out in the section entitled “Liquidity” below.

| Use of Proceeds | |||||

| Assuming 25% | Assuming 50% | Assuming 75% | Assuming 100% | Anticipated Total | |

| of options | of options | of options | of options | expense for the next | |

| are exercised | are exercised | are exercised | are exercised | 12 months | |

| Professional fees | $26,000.00 | $26,000.00 | $26,000.00 | $58,750.00 | $181,000.00 |

| Office and Miscellaneous and Rent | $14,937.50 | $14,937.00 | $41,000.00 | $41,000.00 | $41,000.00 |

| Transfer Agent and Filing Fees | nil | $29,000.00 | $29,000.00 | $29,000.00 | $29,000.00 |

| Travel | nil | $11,938.00 | $26,812.00 | $35,000.00 | $35,000.00 |

| Total | $40,937.50 | $81,875.00 | $122,812.00 | $163,750.00 | $286,000.00 |

CAPITALIZATION

The following table sets forth our capitalization as at August 31, 2010, February 28, 2010 and February 28, 2009.

| August 31, | February 28, | February 28, | |||||||

| 2010 | 2010 | 2009 | |||||||

| Long-term liabilities | $ | - | $ | - | $ | - | |||

| Stockholder’s deficit: | |||||||||

| Preferred stock | - | - | - | ||||||

| Common stock net of share issue costs | 6,395,755 | 6,288,322 | 368,088 | ||||||

| Contributed Surplus | 1,352,402 | 992,715 | - | ||||||

| Accumulated deficit | (2,844,909 | ) | (1,631,147 | ) | (242,781 | ) | |||

| Total stockholders’ (deficit) equity | 4,903,248 | 5,649,890 | 125,307 | ||||||

| Total capitalization | $ | 4,903,248 | $ | 5,649,890 | $ | 125,307 |

11

DILUTION

The net tangible book value of our company as of February 28, 2010 was $5,649,890 or $(0.18) per share of common stock. Net tangible book value per share is determined by dividing the tangible book value of our company (total tangible assets less total liabilities) by the number of outstanding shares of our common stock on February 28, 2010.

As of November 19, 2010, there were 38,100,943 shares of our common stock issued and outstanding. If all of the share purchase warrants and options that were issued and outstanding as of that date were to be exercised, including warrants and options that are not yet exercisable, we would be required to issue up to an additional 14,728,740 shares of our common stock, or approximately 38.7% of our issued and outstanding shares of common stock on November 19, 2010. If these are exercised, your interest in our company will be diluted. Further, our board of directors is authorized to issue an unlimited number of our common stock. If our board of directors issues additional stock, your interest in our company will be diluted.

In connection with our initial public offering in Canada in June of 2009, we issued 5,600,000 shares of common stock, which represented an increase of 106% of our issued and outstanding stares at that time and resulted in the substantial dilution of our existing stockholders. We are dependent upon the sale of our equity securities in order to fund our operations for the foreseeable future. Additionally, we largely rely on the issuance of equity securities to acquire additional property interests and consummate acquisitions. Any such issuance of equity securities will substantially decrease the proportionate ownership and voting power of all other stockholders. This dilution could cause the price of our shares to decline and it could result in the creation of new control persons. In addition, our stockholders could suffer dilution in the net book value per share.

Since our initial public offering in Canada, our company issued a significant number of shares of our common stock which has substantially diluted our existing shareholders. As we are a development stage mineral exploration company, we are dependent upon the sale of our equity securities which will further result in the dilution of our existing shareholders.

MARKET FOR COMMON EQUITY AND RELATED STOCKHOLDER MATTERS

Our common shares commenced trading on the TSX Venture Exchange on January 21, 2010. We cannot assure that the market for the shares will develop or be sustained. We currently plan to have our common stock quoted on the OTC Bulletin Board upon the effectiveness of the registration statement of which this prospectus forms a part. Our shares may never be quoted on the OTC Bulletin Board. The following table sets forth, for the periods indicated, the high and low sales prices for our common stock on the TSX Venture Exchange:

| Quarter Ended | High | Low |

| August 31, 2010 | 0.285 | 0.15 |

| May 31, 2010 | 0.44 | 0.19 |

| February 28, 2010(1) | 0.82 | 0.52 |

(1) Our common shares began trading on the TSX Venture Exchange on January 21, 2010.

The following table sets forth, for the most recent six months, the high and low market price for each month:

| Month Ended | High | Low |

| September 30, 2010 | 0.26 | 0.165 |

| August 31, 2010 | 0.185 | 0.15 |

| July 31, 2010 | 0.215 | 0.135 |

| June 30, 2010 | 0.285 | 0.20 |

| May 31, 2010 | 0.385 | 0.19 |

| April 30, 2010 | 0.49 | 0.35 |

12

We have not paid any dividends on our common stock and do not anticipate paying cash dividends in the foreseeable future. We intend to retain any earnings to finance the growth of our business. We cannot assure you that we will ever pay cash dividends. Whether we pay cash dividends in the future will be at the discretion of our Board of Directors and will depend upon our financial condition, results of operations, capital requirements and any other factors that the Board of Directors decides are relevant. See Management’s Discussion and Analysis of Financial Condition and Results of Operations.

As of November 19, 2010, we have approximately one hundred five (105) shareholders who hold 100% of our issued and outstanding common stock.

DESCRIPTION OF BUSINESS AND PROPERTY

General

We were incorporated as Etna Resources, Inc. under the laws of the Province of British Columbia on September 18, 2006. On January 20, 2010, we effected a name change to Pan American Lithium Corp. We are a mineral exploration company engaged in the business of acquiring, exploring and evaluating natural resource properties, and recently focused on the acquisition of interests in, and exploring for, lithium properties in Latin America. We are currently listed for trading on the TSX Venture Exchange under the symbol “PL” and are filing this Registration Statement on Form F-1 with the United States Securities and Exchange Commission with the goal to register our common shares under the United States Securities Exchange Act of 1934.

We currently have one set of lithium exploration properties consisting of interests in nine lithium brine salars in Atacama Region III, Chile, and an option to acquire an indirect interest in the Cerro Prieto geothermal brine project in Baja California Norte, Mexico. We formerly owned the Aspen Grove copper property in the Nicola Mining District, British Columbia, Canada, the details of which are set out below. We have not yet determined whether our property interests contain reserves that are technically or economically recoverable. The recoverability of amounts shown for resource properties and related deferred exploration expenditures are dependent upon the discovery of economically recoverable reserves, confirmation of our interest in the underlying mineral claims, our ability to obtain necessary financing to complete the development of the resource at such property and upon future profitable production or proceeds from the disposition thereof.

CHILEAN SALARS – ATACAMA REGION III,

General

On December 4, 2009, and subsequent to the three months ended November 30, 2009, we acquired 99% of South American Lithium Company S.A. Cerrada (“Salico”) which, in turn, holds interests in a total of nine lithium properties in Chile as depicted in the table below. Salico obtained its rights in the concessions at these properties from Sociedad Gareste Ltda. (“Gareste”), a Chilean limited liability company. We acquired our 99% interest in Salico in connection with the closing of an Amended and Restated Securities Exchange Agreement dated October 18, 2009. Pursuant to the terms of the Amended and Restated Securities Exchange Agreement, and at the closing thereof, we purchased 99% of the interests of Salico from the owners in consideration for us issuing 10,494,000 common shares to such holders at a fair value of $3,148,200. Acquisition costs also included $184,000 which is the fair value of 613,333 finders shares issued. We also agreed to pay US$50,000 to the former holder of the property interests on signing to cover costs incurred in connection with the formation and organization of Salico and a monthly fee of US$25,000 to compensate general and administrative costs of the former holder from the execution date to the closing date. The closing of the agreement occurred on December 4, 2009.

13

The existing portfolio of rights in the nine properties includes surface brine lakes or surface flow at Laguna Verde, Laguna Brava and Rio de la Sal /Pedernales, and six additional lithium brine salar projects, all located in the mineral-rich Atacama Region III. The rights in these nine lithium projects cover a cumulative area in excess of 13,000 hectares. Seven of these properties are accessible by passenger car and are adjacent to serviceable roads, while two of the salars (Salar de Wheelwright and Lagunas Jilgueros) are primarily accessible by passenger car, but require a short (under 5 km) traverse, using four wheel drive vehicles, from serviceable roads. It is believed that the salars collectively carry the potential to host lithium in three distinct brine types: surface water, shallow and deep brines. None of these projects is past the exploration stage, and we have not yet identified reserves at any of these properties.

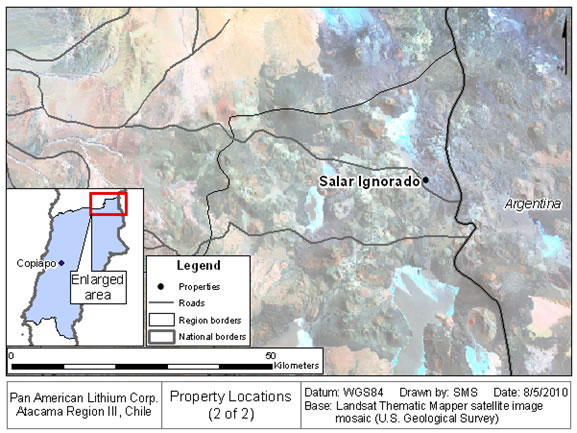

The following two maps depict the locations of and access to each of the nine properties in Chile Atacama Region III in which Salico owns or has rights in mineral concessions.

14

We consider only the Laguna Verde property to be material as of the date of this filing.

Mineral Title in Chile

Chile’s current mining policy is based on legal provisions founded in Spanish law with modifications via a series of prior Mining Codes leading to the revised Mining Code of 1982. These were established to stimulate the development of mining and to guarantee the property rights of both local and foreign investors. According to the law, the state owns all mineral resources, but exploration and exploitation of these resources by private parties is permitted through mining concessions, which are granted, to any claimant to mineral rights who follows the required procedures. An exploration claim can be placed on any area, whereas the survey to establish a permanent exploitation claim (“mensura”) can only be effected on “free” areas which have no valid claims in place or in process of constitution.

The concessions have both rights and obligations as defined by a Constitutional Organic Law as enacted in 1982. Concessions can be mortgaged or transferred and the holder has full ownership rights and is entitled to obtain the rights of way for exploration and exploitation. The concession holder has the right to use, for mining purposes, any water flows which infiltrate any mining workings. In addition, the concession holder has the right to defend his ownership against state and third parties. An exploration concession is obtained by a claims filing and includes all minerals that may exist within its area. Exploration and exploitation mining rights in Chile are acquired in the following stages:

Pedimento: A pedimento is an initial exploration claim whose position is well defined by UTM coordinates which define north-south and east-west boundaries. The minimum size of a pedimento is 100 hectares and the maximum is 5,000 hectares with a maximum length-to-width ratio of 5:1. The duration of validity is for a maximum period of 2 years from the date of constitution, however at the end of this period it may a) be reduced in size by at least 50% and renewed for an additional 2 years or b) entered in the process to establish a permanent claim by converting to a “manifestation”. New pedimentos are allowed to overlap with pre-existing ones; however the pedimento with the earliest filing date always takes precedence, providing the claim holder continues the process of constitution in accordance with the Mining Code and the applicable regulations. Pedimentos are maintained by yearly payments of approximately U.S. $3.00 per hectare.

Manifestacion: Before a pedimento expires, or at any stage during its two year life, it may be converted to a manifestacion which lasts for 220 days.

15

Mensura: Prior to the expiration of a manifestacion, the owner of a manifestacion must request a survey (“mensura”). After acceptance of the “Survey Request” (solicitud de Mensura), the owner has approximately 12 months to have the claim surveyed by a government licensed surveyor. The surrounding claim owners may witness the survey, which is subsequently described in a legal format and presented to the National Mining Service (“SERNAGEOMIN”) for technical review which includes field inspection and verification. Following the technical approval by SERNAGEOMIN, the file returns to the judge of the appropriate jurisdiction who must dictate the constitution of the claim as a “mensura” (equivalent of a patented claim in the United States). Once constituted, an abstract describing the claim is published in Chile’s official mining bulletin, which is published weekly, and 30 days later the claim can be inscribed in the appropriate Mining Registry (referred to as “Conservador de Minas”).

Once constituted, a “mensura” is a permanent property right, with no expiration date. So long as the annual fees (referred to as “patentes”) are paid in a timely manner, (from March to May of each year) clear title and ownership of the mineral rights is assured in perpetuity. Currently, the patentes are the equivalent of US$7.33 per hectare per year. Failure to pay the annual patentes for an extended period can result in the claim being listed for “remate”, which is an Auction Sale, wherein a third party may acquire a claim for the payment of back taxes owed plus a penalty payment. In such a case, the claim is included in a list published 30 days prior to the Auction and the owner has the possibility of paying the back taxes plus penalty and thus removing the claim from the Auction List.

Mineral concessions under Chilean mining law provide for direct exploitation of mineral salts like potassium, magnesium, calcium, and sodium. Under Article 7 of the Chilean Mining Code, lithium, uranium, and thorium are technically reserved to the state of Chile for the Chilean National Nuclear Commission. As a consequence, under Articles 8 through 10 of the Chilean Mining Code, there are three alternative approaches, under each of which Salico could produce and market lithium minerals:

| 1. |

Salico can secure through the Ministry of Mines a special operating permit that allows it to process and export lithium products. This permit is authorized and signed by the President of Chile. This procedure has been used for all contracts under which existing lithium production companies operate in Chile. We are not aware of any lithium exploitation project wherein the special operating permit was not granted. Salico expects to apply for and receive such special permits on its projects that are subsequently shown to be economically feasible. We consider this special operating permit scenario to be a reasonable expectation, given prior precedents set by Soquem Inc., Chemetall Foote Corp, and other lithium operations in Chile, all of which operate under the special permit process. | |

| 2. |

Alternatively, Salico may process lithium as a by-product in a conventional salt recovery circuit. The lithium products must then offered to the Chilean National Nuclear Commission, which then must elect whether or not to take delivery. If the Commission decides not to take delivery, then by default Salico will be at liberty to commercialize the lithium products with third parties. | |

| 3. |

If the Commission elects to take delivery of the lithium products under scenario 2, Salico is obligated to deliver the lithium at its cost. Before taking delivery, however, the Commission is required to pay, in advance, for all infrastructure and operational costs related to the separation and delivery of the lithium product. In a typical lithium recovery system, where evaporation ponds are used to sequentially separate out various non-lithium salts, and where lithium is the last salt processed, the Commission would have to pay a large portion of the infrastructure and operational costs, resulting in recovery of all non- lithium by-products at a drastically reduced capital and operational cost to Salico. |

We are not aware of any instance whereby the Commission has required delivery of lithium or of any research or development by the government of Chile that would require the acquisition and use of lithium. We do not know of any special appropriation or line-item in the national Chilean budget that would allow for the Commission to purchase lithium and pay for corresponding infrastructure and operational costs.

Permitting, Environmental and Water Issues in Chile

The following summary is based upon Chile’s Environmental Law 19.300 and the Regulations regarding environmental impact studies, as posted on the web site of Chile’s Regional Commission for the Environment (“CONAMA”) (http://www.conama.cl/portal/1255/channel.html).

Chile’s environmental law (referred to as “Law Nº 19.300”), which regulates all environmental activities in the country, was first published on March 9th, 1994. An exploration project or field activity cannot be initiated until its potential impact to the environment is carefully evaluated. This is documented in Article 8 of the environmental law and is referred to as the Sistema de Evaluación de Impacto Ambiental (“SEIA”).

16

The SEIA is administered and coordinated on both regional and national levels by the Comisión Regional del Medio Ambiente (“COREMA”) and the Comisión Nacional del Medio Ambiente (“CONAMA”), respectively. The initial application is generally made to COREMA, in the corresponding region where the property is located, however in cases where the property might affect various regions the application is made directly to the CONAMA. Various other Chilean government organizations are also involved with the review process, however most documentation is ultimately forwarded to CONAMA, which is the final authority on the environment and is the organization that issues the final environmental permits.

There are two types of environmental review; an Environmental Impact Statement (Declaración de Impacto Ambiental, or “DIA”), and an Environmental Impact Assessment (Evaluación de Impacto Ambiental, or “EIA”). As defined in the SEIA, a Declaration (DIA) must be prepared prior to starting detailed drilling for a mining project (defined as the stage of reducing “uncertainty” in the quantification of mineral resources and for purposes of defining a mining plan). The regulations provide an exemption from the need to prepare a DIA during the “exploratory stage” when the extent of the orebody is being determined. A DIA is prepared in cases when the applicant believes that there will be no significant environmental impact or social controversy as a result of the proposed drilling and advanced exploration activities. The potential impacts include areas such as health risks, contamination of soils, air and/or water, relocation of communities or alteration of their ways of life, proximity to “endangered” areas or archaeological sites, alteration of the natural landscape, and/or alteration of cultural heritage sites. The DIA will include a statement from the applicant declaring that the project will comply with the current environmental legislation, and a detailed description of the type of planned activities, including any voluntary environmental commitments that might be completed during the project.

For any detailed drilling phase, a DIA will be required. A full Environmental Impact Study (“EIA”) will only be required in connection with permitting process when the project moves forward to approval for construction. The EIA report is much more detailed and includes a table of contents, an executive summary, a detailed description of the design of the project facilities and operating parameters, a program for compliance with the environmental legislation, a detailed description of the possible impacts and an assessment of how they would be dealt with and repaired, a baseline study, a plan for compensation (if required), details of a follow-up program, a description of the EIA presentation made to COREMA or CONAMA, and an appendix with all of the backup documentation. Once an application is made, the review process by COREMA or CONAMA will take a maximum of 120 days. Question and answer cycles typically delay this process. After the basic environmental approval is given a number of construction/operating permits may be granted by the appropriate authorities allowing the mine development and facilities construction to commence. If, however, COREMA or CONAMA comes back with additional questions or deficiencies, an equal period of time is granted to the applicant to make the appropriate corrections or additions. Once re-submitted and a 60 day period has elapsed, if no further notification from COREMA or CONAMA is received, the application is assumed to be approved.

Presentation of a pre-feasibility or scoping study to the General Direction of Waters (“DGA”) that indicates the scope of the project and related criteria are a requirement in order to obtain final water usage permits for a project. These studies also determine which of the projects require consumptive water usage permits, versus non-consumptive water usage permits.

Under the Chilean mining law, mineral concessions carry the right to exploit all potential surface and subsurface mineral assemblages including rock, salt crusts, muds, clays, unconsolidated and consolidated erosional material and sediments, and other salt depositional complexes. Processing of brines and other waters contained within the Pan American mineral concessions will require additional permits as granted by the Chilean General Direction of Waters, which has a Regional office in Copiapo.

Laguna Verde property

Location and Access

The Laguna Verde property is depicted on Property Location Map 1 above and the property map below, and at this time is the only property considered to be material by us.

17

The Laguna Verde property is accessible via paved International Highway (“Camino Internacional”) C31 from Copiapo (the capital of Atacama Region III) leading northeasterly and easterly 161 kilometres to the border station at Maricunga, then south and east 80 kilometres to Laguna Verde. The roads are all well maintained by the local provincial authorities and accessible via 2 wheel drive vehicles. Travel time from Copiapo to Laguna Verde is about 4 hours. Although lithium has been identified in both the brines and the sediments in the Laguna Verde salar, there has been no known production. There is no record or visible sign of production of any salts from either the brines or the salar sediments at this property. There are no physical improvements at the site other than a small stone structure adjacent to a geothermal bathing spring on the periphery of the surface lake.

Titles and Nature of Concessions; Royalties

Pertinent data relating to the nature of the mineral concessions comprising Laguna Verde is contained in the following table:

18

MINERAL CONCESSION DATA—LAGUNA VERDE (UTM coordinates—WGS84 Datum)

The Laguna Verde Project comprises 13 mineral exploration claims, which are pedimentos, totalling 3,400 hectares. The pedimentos were staked in April 2009, constituted earliest in November of 2009, and are valid for two years. The pedimentos are maintained by yearly payments of approximately U.S. $3.00 per hectare, which in the aggregate total US$10,166 per year, the responsibility for which belongs to Salico and ultimately our company. At the end of two years, the claims must be converted to exploitation claims. Our intent is to pay all annual fees and hold the concessions in exploration status for the complete period allowed under Chilean law. The claims protect the claimant as to all mineral rights, and a right of surface access upon agreement with the surface owner. As the surface owner at Laguna Verde is the state of Chile, we, through Salico, will solicit a surface rights agreement with the government of Chile at the time of and in connection with a feasibility study.

In connection with the closing of the December, 2009 acquisition of Laguna Verde and the other 8 properties, Salico granted a 2% net smelter return royalty to the vendor on future production from Laguna Verde, payable following commencement of commercial production, to a maximum of US$6 million. Prior to commencement of commercial production at Laguna Verde, Salico may repurchase one-half of this net smelter return royalty (1%) for US$2 million.

Geology and Mineralization

Laguna Verde has the following physical characteristics:

| 1. | Altitude | 4350 m | |

| 2. | Catchment basin size | 1075 km2 | |

| 3. | Lake surface area | 15 km2 | |

| 4. | Annual Precipitation | 170 mm/yr | |

| 5. | Evaporation potential | 2000 mm/yr | |

| 6. | Water temperature (surface) | 1o C |

The catchment basin draining into Laguna Verde is dominated entirely by young andesitic and dacitic volcanic rocks. Young volcanic cones and vents surround the entire basin, and in most instances constitute the divides separating the basin from other valleys and nearby salars. Elevations surrounding Laguna Verde reach 6,800 meters and more. The lake is fed by active hot springs, and is thought to be of geothermal origin. The volcano Ojo del Salado forms a significant and commanding divide to the south. The high elevations around the basin are all volcanic cones and vents. Figure 1 is illustrative of the young volcanism at Laguna Verde.

19

Figure 1. View of Volcanic Cones at Laguna Verde

Lithium and associated elements (potassium, magnesium, boron, sodium) occur in salar brines as complex salts, fluorides, and sulfates. Lithium also occurs as lithium dioxide. The high solubility of lithium allows for dispersion in water of the ion Li+.

Work completed at Laguna Verde

Laguna Verde was examined in detail by the French Institut de Recherche pour le Development (IRD) in 1995 as part of a program to evaluate the high Andes salars for potable water. Their sample results and chemistry (in Mg/liter) are presented below:

| Smpl | PH | Cl | SO4 | B | Si | Na | K | Li | Ca | Mg |

| Lav 1 | 7.56 | 92500 | 13800 | 513 | 13.3 | 57700 | 5400 | 204 | 533 | 2380 |

| (8+2+3)E | 7.89 | 90800 | 14700 | 494 | 13.7 | 56400 | 7660 | 318 | 441 | 1960 |

| Lav-8E | 7.79 | 83400 | 21600 | 674 | 16.2 | 58400 | 6400 | 229 | 674 | 532 |

| Lav-3E | 7.63 | 100000 | 6500 | 594 | 14.1 | 50200 | 7260 | 453 | 2210 | 5140 |

| Lav-6E | 8.98 | 84800 | 20200 | 358 | 18.3 | 61000 | 6360 | 186 | 9.23 | 32.3 |

| Lav-7E | 9.77 | 75500 | 21200 | 562 | 31.5 | 60000 | 7200 | 185 | 0.526 | 1.80 |

| Lav-2E | 10.1 | 41200 | 23300 | 396 | 54.7 | 62100 | 5950 | 155 | 0.372 | 1.33 |

In March of 2010, we undertook a work program at Laguna Verde to determine the depth and volume of the surface lake. Based on bathymetric measurements taken from a Zodiac boat, water depths vary from 0.5m to in excess of 60m, and the mean lake depth is 33m. The lake is perennial and water levels vary seasonally by only a half meter or so, judging by stone wall construction and thermal spring usage by travelers through the area.

We initiated a comprehensive lake brine sampling program on our Laguna Verde Project in April 2010. This sampling program, conducted under the supervision of John Hiner, L.P. Geo, an independent professional geologist, entailed the collection of brine lake water samples from surface and at various depths on a pre-established grid at 500 m or less designed in consultation with Mr. Hiner. Access to sample points was achieved using a 4m Zodiac boat. Grid sampling across the lake was undertaken for the purpose of determining lateral and vertical distribution of lithium and other elements in the lake waters. The sample points were located by GPS and samples were then taken at surface and at depth.

Samples taken at depth were collected using a Van Dorn Vertical Water Sampling Bottle – Type Beta Plus. This device is a weighted elongated cylinder with valves at the top and bottom that allow the device to pass through water to the desired depth. On reaching the targeted depth a weighted control is sent down the line and on reaching the device triggers the closure of the valves, thereby collecting an “undisturbed water sample” at depth. Due to high winds and rough water collection at depths greater than 15m were not possible due to the angle on the sampler control lines caused by wind drifting which made closing the sampler valves difficult.

Sample Preparation, Analyses and Security

For the grid sample program, water samples were collected in sterilized plastic bottles. The bottles were labeled with felt marker pen, double-rinsed and submerged to collect a sample with as little entrained oxygen as possible. None of the samples were acidized, as all of the waters had pH levels above 7.0, and because the high solubility of lithium in water renders such buffering unnecessary. Sample locations were noted by GPS and noted in field notebook. Where possible, photographs of sample sites were taken.

20

No employee, officer, director, or associate of our company or Salico was involved in the selection of samples to be taken, the collection of the samples, or the preparation of the samples. For the grid sampling program, independent contractors were interviewed, selected, and trained by Mr. Hiner, who was on site during sample collection. The samples remained in the possession of Mr. Hiner until delivered to a common carrier overnight shipping facility in Copiapo, Chile

Brine samples were collected in sterilized plastic bottles under the supervision of Mr. Hiner, sealed on site, and shipped by common carrier to an independent certified laboratory--ALS Chemex Environmental laboratories in Burnaby, British Columbia, Canada, for analysis. The samples were analyzed directly as submitted by inductively coupled plasma-mass spectrometry (“ICP”). Any over limit results were subsequently reanalyzed by ICP methods using higher limit standards. Two control samples consisting of distilled water were inserted into the sample stream. No geochemical lithium standard is yet available commercially in either liquid or solid form.

A total of 78 brine samples were collected at Laguna Verde, two of which were control samples of distilled water. All samples were tested using ICP for total dissolved solids and a suite of 30 metals. Sulphates were analyzed via a turbidimetric method.

The average chemical composition (in mg/l) of elements of interest at Laguna Verde is shown in the following table.

Element/Metal |

Detection Limits (mg/l) |

Laguna Verde | |

| Average Grade |

Standard Deviation | ||

| Boron mg/l | 10 | 522 | 15 |

| Calcium mg/l | 5 | 899 | 24 |

| Lithium mg/l | 1 | 213 | 14 |

| Magnesium mg/l | 10 | 2545 | 76 |

| Potassium mg/l | 200 | 4881 | 299 |

| Sodium mg/l | 200 | 64887 | 3742 |

| Total Dissolved Solids | 200 | 194052 | 8042 |

| Sulfates (SO4) | 50 | 15985 | 569 |

| Density | 1.14 | 0 | |

An analysis of the values for lithium, magnesium and potassium throughout the lake and at depth indicated that the standard deviation of no more than 6% of the average grade at Laguna Verde. The density of the lake waters was found to be constant from surface to a depth of 15m at 1.14 and consequently there did not appear to be any notable increase amount of dissolved solids or grades of metals with depth.

The results of this sampling program compare favorably with water chemistry results taken by IRD in the 1990s, supporting the proposition that water chemistry is consistent over time.

Laguna Verde has no known reserves reportable under US securities laws, and the programs carried out on the property to date have been simply exploratory in nature. However, on June 14, 2010, we filed on SEDAR a National Instrument 43-101 technical report, compliant with Canadian law, for an inferred resource estimates for our Laguna Verde property. The inferred resource estimate was determined using a volumetric calculation for water volume in the lake, and calculations of contained metals and elements based on average grades. The following criteria were utilized:

- The surface area of the lake was established by both polygonal method, and confirmed by planimetric measurement to be 15.2 square kilometers.

- The mean average depth of the lake was determined by a bathymetric survey using a weighted rope line to be 33 meters with a maximum measured depth of 60 meters.

- Based on the results of 78 samples, lithium and potassium values are consistent throughout the lake. Average grades have a standard deviation of 14 mg/l for lithium and 299 mg/l for potassium, a difference of +/- 7%. The brines are uniformly consistent based on available data. Therefore the average grades for Li of 213 mg/l and K of 4881 mg/l were used over the total volume.

- Spacing of sample points were on a grid at an interval of 500 m between points. At each sample point vertical samples were taken.

The formula used for calculating lithium carbonate equivalent is 1 tonne of lithium metal equals 5.285 tons of lithium carbonate. The formula used for calculating potash equivalent is 1 tonne of potassium metal equals 1.910 tonnes of potassium chloride. Industrial markets ordinarily trade lithium and construct offtake agreements as lithium carbonate equivalent. Likewise, potassium chloride is generally the stated media for both spot sales and offtake agreements. It is therefore common in initial resource evaluations by industrial mineral companies to utilize these terms as part of the measurement of tonnages of product under evaluation.

21

The inferred resource estimate at the Laguna Verde surface lake was computed at an average grade of 212.40 mg/litre to be 512,960 tons of lithium carbonate equivalent, and at an average potassium grade of 4,881 mg/litre computed to be 4,223,134 tons of potassium chloride equivalent. For more information, see the technical report filed on SEDAR on June 14, 2010. Cautionary Note to U.S. Investors-The United States Securities and Exchange Commission permits U.S. mining companies, in their filings with the SEC, to disclose only those mineral deposits that a company can economically and legally extract or produce. We use certain terms in our press releases, on its website, and herein such as “measured,” “indicated,” or “inferred” “resources, which the SEC guidelines strictly prohibit U.S. registered companies from including in their filings with the SEC. U.S. investors are urged to consider closely the disclosure in this Form F-1.

Exploration Status, Costs and Budget

We have completed our initial exploration efforts, described above, which have resulted in the calculation of a Canadian law-compliant inferred resource estimate at Laguna Verde for contained tonnes of both lithium carbonate equivalent and potassium chloride equivalent. Costs incurred in connection with this exploration and calculation totaled approximately US$185,000.

The sequential phases of investigation for Laguna Verde are (1) a scoping study to select the optimal processes through which to recover lithium and other metals from the lake brines, followed by (2) a pre-feasibility study to evaluate preliminary economics for the selected process methodology, and (3) a full, bankable feasibility study accompanied by final exploration and reserve calculations, initial process engineering and permitting. Estimated costs for each of these phases are as follows:

- Scoping Study—US$300,000

- Pre-Feasibility Study—US$1,700,000

- Full Feasibility, Permitting, etc.—US$8 million

Upon successful permitting and production of a bankable feasibility study, we anticipate that, subject to available financing, we would engineer and construct the facilities and improvements reflected by the feasibility study.