Prospectus

J.P. Morgan Exchange-Traded Funds

March 1, 2023

| JPMorgan International Research Enhanced Equity ETF |

Ticker: JIRE |

Listing Exchange: NYSE Arca |

The Securities and Exchange Commission and the Commodity Futures Trading Commission have not approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

JPMorgan International Research Enhanced Equity ETF

| | |

| Management Fees |

|

| Other Expenses |

|

| Total Annual Fund Operating Expenses |

|

| Fee Waivers and/or Expense Reimbursements1 |

- |

| Total Annual Fund Operating Expenses after Fee Waiv- ers and/or Expense Reimbursements1 |

|

1

| | ||||

| |

1 Year |

3 Years |

5 Years |

10 Years |

| SHARES ($) |

|

|

|

|

1MSCI EAFE Index is a registered service mark of MSCI, Inc., which does not sponsor and is in no way affiliated with the Fund.

March 1, 2023 | 1

JPMorgan International Research Enhanced Equity ETF (continued)

2 | J.P. Morgan Exchange-Traded Funds

March 1, 2023 | 3

JPMorgan International Research Enhanced Equity ETF (continued)

4 | J.P. Morgan Exchange-Traded Funds

| |

| |

|

|

| |

|

|

| | |||

| |

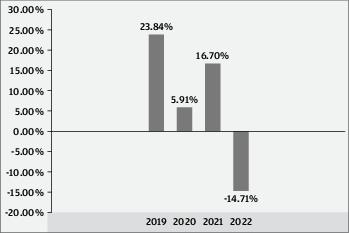

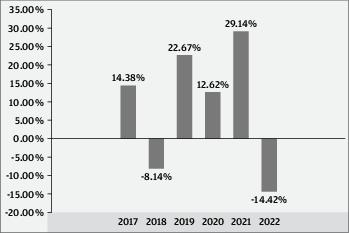

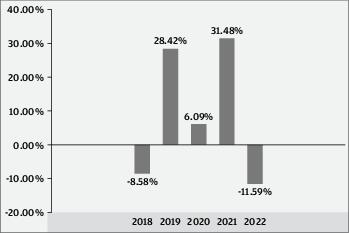

Past 1 Year |

Past 5 Years |

Past 10 Years |

| SHARES |

|

|

|

| Return Before Taxes |

- |

|

|

| Return After Taxes on Distributions |

- |

|

|

| Return After Taxes on Distributions and Sale of Fund Shares |

- |

|

|

| MSCI EAFE INDEX (Net Total Return) (Reflects No Deduction for Fees, Expenses, or Taxes, Except Foreign Withholding Taxes) |

- |

|

|

Management

J.P. Morgan Investment Management Inc. (the adviser)

| Portfolio Manager |

Managed the Fund Since |

Primary Title with Investment Adviser |

| Piera Elisa Grassi |

2022 |

Managing Director |

| Nicholas Farserotu |

2022 |

Vice President |

| Winnie Cheung |

2022 |

Vice President |

Ms. Grassi, Mr. Farserotu and Ms. Cheung also were the predecessor fund's portfolio managers since 2016, 2020 and 2020, respectively.

Purchase and Sale of Shares

Individual Shares of the Fund may only be purchased and sold in secondary market transactions through brokers or financial intermediaries. Shares of the Fund are listed for trading on the Exchange, and because Shares trade at market prices rather than NAV, Shares of the Fund may trade at a price greater than NAV (premium) or less than NAV (discount). Certain affiliates of the Fund and the adviser may purchase and resell Shares pursuant to this prospectus.

An investor may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase Shares of the Fund (bid) and the lowest price a seller is willing to accept for Shares (ask) when buying or selling Shares in the secondary market (the bid-ask spread).

Recent information, including information about the Fund’s NAV, market price, premiums and discounts, and bid-ask spreads, is included on the Fund’s website at jpmorganfunds.com.

Tax Information

To the extent the Fund makes distributions, those distributions will be taxed as ordinary income or capital gains, except when your investment is in an IRA, 401(k) plan or other tax-advantaged investment plan, in which case you may be subject to federal income tax upon withdrawal from the tax-advantaged investment plan.

March 1, 2023 | 5

JPMorgan International Research Enhanced Equity ETF (continued)

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase Shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the adviser and its related companies may pay the financial intermediary for the sale of Shares and related services. These payments may

create a conflict of interest by influencing the broker-dealer or financial intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

6 | J.P. Morgan Exchange-Traded Funds

More About the Fund

Additional Information About the Fund’s Investment Strategies

The Fund is an ETF, which is a fund that trades like other publicly-traded securities. The Fund is not an index fund. The Fund is actively managed and does not seek to replicate the performance of a specified index.

The name, investment objective and policies of the Fund are similar to other funds advised by the adviser or its affiliates. However, the investment results of the Fund may be higher or lower than, and there is no guarantee that the investment results of the Fund will be comparable to, any other of these funds. A new fund or a fund with fewer assets under management may be more significantly affected by purchases and redemptions of its Creation Units (as defined below) than a fund with relatively greater assets under management would be affected by purchases and redemptions of its shares. As compared to a larger fund, a new or smaller fund is more likely to sell a comparatively large portion of its portfolio to meet significant Creation Unit redemptions, or invest a comparatively large amount of cash to facilitate Creation Unit purchases, in each case when the fund otherwise would not seek to do so. Such transactions may cause funds to make investment decisions at inopportune times or prices or miss attractive investment opportunities. Such transactions may also accelerate the realization of taxable income if sales of securities resulted in gains and the fund redeems Creation Units for cash, or otherwise cause a fund to perform differently than intended. While such risks may apply to funds of any size, such risks are heightened in funds with fewer assets under management. In addition, new funds may not be able to fully implement their investment strategy immediately upon commencing investment operations, which could reduce investment performance.

Investment Strategies

Under normal circumstances, the Fund invests at least 80% of its Assets in equity securities. “Assets” means net assets, plus the amount of borrowings for investment purposes. The Fund primarily invests in foreign companies of various market capitalizations, including foreign subsidiaries of U.S. companies. The equity securities in which the Fund may invest include, but are not limited to, common stock, preferred stock, depositary receipts, privately placed securities and real estate investment trusts (REITs).

The Fund seeks to outperform the MSCI Europe, Australasia, Far East (EAFE) Index1 (net of foreign withholding taxes) (the Index) over time while maintaining similar risk characteristics, including sector and geographic risks. In implementing its strategy, the Fund primarily invests in securities included within the universe of the Index. In addition, the Fund may also invest in securities not included within the Index. The Fund only invests in the securities of companies located in developed markets.

Within each sector, the Fund may modestly overweight equity securities that it considers undervalued while modestly underweighting or not holding equity securities that appear over-valued. By emphasizing investment in equity securities that appear undervalued or fairly valued, the Fund seeks returns that modestly exceed those of the Index over the long term with a modest level of volatility.

The Fund may use exchange-traded futures to gain exposure to particular foreign securities or markets and for the efficient management of cash flows. The Fund may invest in securities denominated in any currency and may from time to time hedge a portion of its foreign currency exposure using currency forwards.

An issuer of a security will be deemed to be located in a particular country if: (i) the principal trading market for the security is in such country, (ii) the issuer is organized under the laws of such country or (iii) the issuer derives at least 50% of its revenues or profits from such country or has at least 50% of its total assets situated in such country.

Investment Process: In managing the Fund, the adviser combines fundamental research with a disciplined portfolio construction process. The adviser utilizes proprietary research, risk management techniques and individual security selection in constructing the Fund’s portfolio. In-depth, fundamental research into individual securities is conducted by research analysts who emphasize each issuer’s long-term prospects. This research allows the adviser to rank issuers within each sector group according to what it believes to be their relative value. The adviser also integrates financially material ESG factors as part of the Fund's investment process (ESG Integration). ESG Integration is the systematic inclusion of ESG issues in investment analysis and investment decisions. As a part of this analysis, the adviser seeks to assess the risks presented by certain environmental, social and governance factors. While these particular risks are considered, securities of issuers presenting such risks may be purchased and retained by the Fund.

The adviser will ordinarily overweight securities which it deems to be attractive and underweight or not hold those securities which it believes are unattractive. The adviser may sell a security as its valuations or rankings change or if more attractive investments become available.

In managing the Fund, the adviser will seek to help manage risk in the Fund’s portfolio by investing in issuers in at least three foreign countries. However, the Fund may invest a substantial part of its assets in just one country.

The main investment strategies for the Fund are summarized above. The Fund will invest primarily in equity and equity-related securities as described above. These equity securities may include:

1MSCI EAFE Index is a registered service mark of MSCI, Inc., which does not sponsor and is in no way affiliated with the Fund.

March 1, 2023 | 7

More About the Fund (continued)

•

common stock

•

preferred stock

•

convertible securities

•

trust or partnership interests

•

warrants and rights to buy common stock

•

privately placed securities

The main investment strategies for the Fund may also include the following, some of which may be equity securities:

•

real estate investment trusts (REITs), which are pooled vehicles that invest primarily in income-producing real estate or loans related to real estate

•

foreign securities, which may be in the form of depositary receipts

•

securities denominated in U.S. dollars, other major reserve currencies, such as the euro, yen and pound sterling and currencies of other countries in which the Fund may invest

•

derivatives, including participation notes and certain forwards and futures

Although not main strategies, the Fund may also utilize the following which may be equity securities:

•

high yield securities which are below investment grade (junk bonds) and securities in the lowest investment grade category.

•

sovereign debt

•

corporate debt

•

securities lending

•

derivatives, including certain futures, forwards, options and swaps

•

other investment companies

•

exchange-traded funds (ETFs)

•

affiliated money market funds

•

closed-end investment companies

Derivatives, which are instruments that have a value based on another instrument, exchange rate or index, may also be used as substitutes for securities in which the Fund can invest.

The Fund may use futures contracts, options, swaps, participation notes, forwards and other instruments to more effectively gain targeted equity exposure from its cash positions, to hedge various investments, for risk management and to increase the Fund’s gain. The Fund may use exchange-traded futures to manage cash flows.

ETFs, which are pooled investment vehicles whose ownership interests are purchased and sold on a securities exchange, may be passively or actively managed. Passively managed ETFs generally seek to track the performance of a particular market index, including broad-based market indexes, as well as indexes relating to particular sectors, markets, regions or industries. Actively managed ETFs do not seek to track the performance of a particular market index. Ordinarily, the Fund must limit its investments in a single non-affiliated ETF to 5% of its total assets and in all non-affiliated ETFs to 10% of its total assets. The Securities and Exchange Commission has issued exemptive orders to many ETFs that currently allow any fund investing in such ETFs to disregard these 5% and 10% limitations, subject to certain conditions. If the Fund invests in ETFs that have received such exemptive orders, it may invest any amount of its total assets in a single ETF or in multiple ETFs. ETFs that are not structured as investment companies as defined in the Investment Company Act of 1940 are not subject to these percentage limitations. The price movement of an index-based ETF may not track the underlying index and may result in a loss. In addition, ETFs may trade at a price above (premium) or below (discount) their NAV, especially during periods of significant market volatility or stress, causing investors to pay or receive significantly more or less than the value of the ETF’s underlying portfolio when they purchase or sell their ETF shares, respectively.

The Fund may utilize the investment strategies listed herein, including the use of derivatives, to a greater or lesser degree.

The Fund will provide shareholders with at least 60 days’ prior notice of any change in its 80% investment policy above.

The frequency with which the Fund buys and sells securities will vary from year to year, depending on market conditions.

| FUNDAMENTAL INVESTMENT OBJECTIVE |

| An investment objective is fundamental if it cannot be changed without the consent of a majority of the outstanding Shares of the Fund. The Fund’s investment objective is fundamental. |

8 | J.P. Morgan Exchange-Traded Funds

Securities Lending. The Fund may engage in securities lending to increase its income. Securities lending involves the lending of securities owned by the Fund to financial institutions such as certain broker-dealers in exchange for cash collateral. The Fund will invest cash collateral in one or more money market funds advised by the adviser or its affiliates. The adviser or its affiliates will receive additional compensation from the affiliated money market funds on the Fund’s investment in such money market funds. During the term of the loan, the Fund is entitled to receive amounts equivalent to distributions paid on the loaned securities as well as the return on the cash collateral investments. Upon termination of the loan, the Fund is required to return the cash collateral to the borrower plus any agreed upon rebate. Cash collateral investments will be subject to market depreciation or appreciation, and the Fund will be responsible for any loss that might result from its investment of cash collateral. If the adviser determines to make securities loans, the value of the securities loaned may not exceed 33 1∕3% of the value of total assets of the Fund. Loan collateral (including any investment of that collateral) is not subject to the percentage limitations regarding the Fund’s investments described elsewhere in this prospectus. Securities lending is not a principal strategy of the Fund.

The Fund also may use other non-principal strategies that are not described herein, but which are described in the Statement of Additional Information.

Investment Risks

There can be no assurance that the Fund will achieve its investment objective.

The main risks associated with investing in the Fund are summarized in the “Risk/Return Summary” at the front of this prospectus. In addition to the Fund’s main risks, the Fund may be subject to additional risks in connection with investments and strategies used by the Fund from time to time. The table below identifies main risks and some of the additional risks for the Fund.

The Fund is subject to management risk and may not achieve its objective if the adviser’s expectations regarding particular instruments or markets are not met.

An investment in the Fund or any other fund may not provide a complete investment program. The suitability of an investment in the Fund should be considered based on the investment objective, strategies and risks described in this prospectus, considered in light of all of the other investments in your portfolio, as well as your risk tolerance, financial goals and time horizons. You may want to consult with a financial advisor to determine if the Fund is suitable for you.

The Fund is subject to the main risks designated as such in the table below, any of which may adversely affect the Fund’s net asset value (NAV), market price, performance and ability to meet its investment objective. The Fund may also be subject to additional risks that are noted in the table below, as well as those that are not described herein but which are described in the Statement of Additional Information.

| |

International Research Enhanced Equity ETF |

| Authorized Participant Concentration Risk |

• |

| Convertible Securities Risk |

○ |

| Currency Risk |

• |

| Cyber Security Risk |

○ |

| Depositary Receipts Risk |

○ |

| Derivatives Risk |

• |

| Developed Asia Pacific (ex-Japan) Market Risk |

○ |

| Equity Market Risk |

• |

| European Market Risk |

• |

| Exchange-Traded Fund (ETF) and Other Investment Company Risk |

○ |

| Foreign Securities Risk |

• |

| General Market Risk |

• |

| Geographic Focus Risk |

• |

| Industry and Sector Focus Risk |

• |

•

Main Risks

○

Additional Risks

March 1, 2023 | 9

More About the Fund (continued)

| |

International Research Enhanced Equity ETF |

| Initial Public Offerings (IPO) Risk |

○ |

| Interest Rate Risk |

○ |

| Japan Risk |

• |

| Market Trading Risk |

• |

| Preferred Securities Risk |

○ |

| Privately Placed Securities Risk |

○ |

| Real Estate Securities Risk |

○ |

| Regulatory and Legal Risk |

○ |

| Securities Lending Risk |

○ |

| Smaller Company Risk |

○ |

| Structured Instrument Risk |

○ |

| Transactions and Liquidity Risk |

○ |

| Volcker Rule Risk |

○ |

•

Main Risks

○

Additional Risks

Foreign Securities Risk. Investments in foreign securities (including depositary receipts) are subject to special risks in addition to those of U.S. investments. These risks include political and economic risks, unstable governments, civil conflicts and war, greater volatility, decreased market liquidity, expropriation and nationalization risks, sanctions or other measures by the United States or other governments, currency fluctuations, higher transaction costs, delayed settlement, possible foreign controls on investment, and less stringent investor protection and disclosure standards of foreign markets. The securities markets of many foreign countries are relatively small, with a limited number of companies representing a small number of industries. If foreign securities are denominated and traded in a foreign currency, the value of the Fund’s foreign holdings can be affected by currency exchange rates and exchange control regulations. In certain markets where securities and other instruments are not traded “delivery versus payment,” the Fund may not receive timely payment for securities or other instruments it has delivered or receive delivery of securities paid for and may be subject to increased risk that the counterparty will fail to make payments or delivery when due or default completely. Events and evolving conditions in certain economies or markets may alter the risks associated with investments tied to countries or regions that historically were perceived as comparatively stable becoming riskier and more volatile.

Foreign market trading hours, clearance and settlement procedures, and holiday schedules may limit the Fund’s ability to buy and sell securities. Investments in foreign markets may also be adversely affected by governmental actions such as the imposition of capital controls, nationalization of companies or industries, expropriation of assets or the imposition of punitive taxes. The governments of certain countries may prohibit or impose substantial restrictions on foreign investing in their capital markets or in certain sectors or industries. In addition, a foreign government may limit or cause delay in the convertibility or repatriation of its currency which would adversely affect the U.S. dollar value and/or liquidity of investments denominated in that currency. Certain foreign investments may become less liquid in response to market developments or adverse investor perceptions, or become illiquid after purchase by the Fund, particularly during periods of market turmoil. Moreover, the growing interconnectivity of global economies and financial markets has increased the probability that adverse developments and conditions in one country or region will affect the stability of economies and financial markets in other countries or regions. A reduction in trading in securities of issuers located in countries whose economies are heavily dependent upon trading with key partners may have an adverse impact on the Fund’s investments.

Securities registration, custody, and settlement may in some instances be subject to delays and legal and administrative uncertainties. Foreign investment in the securities markets of certain foreign countries is restricted or controlled to varying degrees. These restrictions or controls may at times limit or preclude investment in certain securities and may increase the costs and expenses of the Fund. In addition, the repatriation of investment income, capital or the proceeds of sales of securities from certain of the countries is controlled under regulations, including in some cases the need for certain advance government notification or authority, and if a deterioration occurs in a country’s balance of payments, the country could impose temporary restrictions on foreign capital remittances. The Fund also could be adversely affected by delays in, or a refusal to grant, any required governmental approval for repatriation, as well as by the application to it of other restrictions on investment.

10 | J.P. Morgan Exchange-Traded Funds

Geographic Focus Risk. In addition to the more general Foreign Securities Risk above, the Fund may focus its investments in one or more foreign regions or small groups of countries. As a result, the Fund’s performance may be subject to greater volatility than a more geographically diversified fund and may be subject to the risks facing certain regions.

Equity Market Risk. The price of equity securities may rise or fall because of changes in the broad market or changes in a company’s financial condition, sometimes rapidly or unpredictably. These price movements may result from factors affecting individual companies, sectors or industries selected for the Fund’s portfolio or the securities market as a whole, such as changes in economic or political conditions. Equity securities are subject to “stock market risk” meaning that stock prices in general (or in particular, the prices of the types of securities in which the Fund invests) may decline over short or extended periods of time. When the value of the Fund’s securities goes down, your investment in the Fund decreases in value.

General Market Risk. Economies and financial markets throughout the world are becoming increasingly interconnected, which increases the likelihood that events or conditions in one country or region will adversely impact markets or issuers in other countries or regions. Securities in the Fund’s portfolio may underperform in comparison to securities in general financial markets, a particular financial market or other asset classes due to a number of factors, including inflation (or expectations for inflation), deflation (or expectations for deflation), interest rates, global demand for particular products or resources, market instability, debt crises and downgrades, embargoes, tariffs, sanctions and other trade barriers, regulatory events, other governmental trade or market control programs and related geopolitical events. In addition, the value of the Fund’s investments may be negatively affected by the occurrence of global events such as war, terrorism, environmental disasters, natural disasters or events, country instability, and infectious disease epidemics or pandemics.

For example, the outbreak of COVID-19 has negatively affected economies, markets and individual companies throughout the world, including those in which the Fund invests. The effects of this pandemic to public health and business and market conditions, including, among other things, reduced consumer demand and economic output, supply chain disruptions and increased government spending, may continue to have a significant negative impact on the performance of the Fund’s investments, increase the Fund’s volatility, negatively impact the Fund’s arbitrage and pricing mechanisms, exacerbate pre-existing political, social and economic risks to the Fund, and negatively impact broad segments of businesses and populations. In addition, governments, their regulatory agencies, or self-regulatory organizations have taken or may take actions in response to the pandemic that affect the instruments in which the Fund invests, or the issuers of such instruments, in ways that could have a significant negative impact on the Fund’s investment performance. The duration and extent of COVID-19 and associated economic and market conditions and uncertainty over the long-term cannot be reasonably estimated at this time. The ultimate impact of COVID-19 and the extent to which the associated conditions impact the Fund will also depend on future developments, which are highly uncertain, difficult to accurately predict and subject to frequent changes.

European Market Risk. The Fund’s performance will be affected by political, social and economic conditions in Europe, such as growth of the economic output (the gross national product), the rate of inflation, the rate at which capital is reinvested into European economies, the success of governmental actions to reduce budget deficits, the resource self-sufficiency of European countries and interest and monetary exchange rates between European countries. European financial markets may experience volatility due to concerns about high government debt levels, credit rating downgrades, rising unemployment, the future of the euro as a common currency, possible restructuring of government debt and other government measures responding to those concerns, and fiscal and monetary controls imposed on member countries of the European Union. The risk of investing in Europe may be heightened due to steps taken by the United Kingdom to exit the European Union. On January 31, 2020, the United Kingdom officially withdrew from the European Union. On December 30, 2020, the European Union and the United Kingdom signed the EU-UK Trade and Cooperation Agreement (TCA), an agreement on the terms governing certain aspects of the European Union’s and the United Kingdom’s relationship, many of which are still to be determined, including those related to financial services. Notwithstanding the TCA, significant uncertainty remains in the market regarding the ramifications of the United Kingdom’s withdrawal from the European Union. The impact on the United Kingdom and European economies and the broader global economy could be significant, resulting in increased volatility and illiquidity, currency fluctuations, impacts on arrangements for trading and on other existing cross-border cooperation arrangements (whether economic, tax, fiscal, legal, regulatory or otherwise), and in potentially lower growth for companies in the United Kingdom, Europe and globally, which could have an adverse effect on the value of the Fund’s investments. In addition, if one or more other countries were to exit the European Union or abandon the use of the euro as a currency, the value of investments tied to those countries or the euro could decline significantly and unpredictably.

Japan Risk. The Japanese economy may be subject to economic, political and social instability, which could have a negative impact on Japanese securities. In the past, Japan’s economic growth rate has remained relatively low, and it may remain low in the future. Furthermore, the Japanese economic growth rate could be impacted by Bank of Japan’s monetary policies, rising interest rates, tax increases, budget deficits, consumer confidence and volatility in the Japanese yen. At times, the Japanese economy has been adversely impacted by government intervention and protectionism, changes in its labor market, and an unstable financial services sector. International trade, government support of the financial services sector and other troubled sectors, government policy,

March 1, 2023 | 11

More About the Fund (continued)

natural disasters, an aging demographic and declining population and/or geopolitical developments associated with actual or potential conflicts with one or more countries in Asia could significantly affect the Japanese economy. Strained foreign relations with neighboring countries (China, South Korea, North Korea and Russia) may not only negatively impact the Japanese economy, but also the geographic region as well as globally. A significant portion of Japan’s trade is conducted with developing nations and can be affected by conditions in these nations or by currency fluctuations. Japan is an island state with few natural resources and limited land area and is reliant on imports for its commodity needs. Any fluctuations or shortages in the commodity markets could have a negative impact on the Japanese economy. In addition, Japan's economy has in the past and could in the future be significantly impacted by natural disasters.

Derivatives Risk. The Fund may use derivatives in connection with its investment strategies. Derivatives may be riskier than other types of investments because they may be more sensitive to changes in economic or market conditions than other types of investments and could result in losses that significantly exceed the Fund’s original investment. Derivatives are subject to the risk that changes in the value of a derivative may not correlate perfectly with the underlying asset, rate or index. The use of derivatives may not be successful, resulting in losses to the Fund, and the cost of such strategies may reduce the Fund’s returns. Certain derivatives also expose the Fund to counterparty risk (the risk that the derivative counterparty will not fulfill its contractual obligations), including credit risk of the derivative counterparty. In addition, the Fund may use derivatives for non-hedging purposes, which increases the Fund’s potential for loss. Certain derivatives are synthetic instruments that attempt to replicate the performance of certain reference assets. With regard to such derivatives, the Fund does not have a claim on the reference assets and is subject to enhanced counterparty risk.

Investing in derivatives will result in a form of leverage. Leverage involves special risks. The Fund may be more volatile than if the Fund had not been leveraged because the leverage tends to exaggerate any effect on the value of the Fund’s portfolio securities. Registered investment companies are limited in their ability to engage in derivative transactions and required to identify and earmark assets to provide asset coverage for derivative transactions.

The possible lack of a liquid secondary market for derivatives and the resulting inability of the Fund to sell or otherwise close a derivatives position could expose the Fund to losses and could make derivatives more difficult for the Fund to value accurately.

The Fund’s transactions in futures contracts, swaps and other derivatives could also affect the amount, timing and character of distributions to shareholders which may result in the Fund realizing more short-term capital gain and ordinary income subject to tax at ordinary income tax rates than it would if it did not engage in such transactions, which may adversely impact the Fund’s after-tax return.

| WHAT IS A DERIVATIVE? |

| Derivatives are securities or contracts (for example, futures and options) that derive their value from the performance of underlying assets or securities. |

Currency Risk. Changes in foreign currency exchange rates will affect the value of the Fund’s securities and may affect the price of the Fund’s Shares. Generally, when the value of the U.S. dollar rises in value relative to a foreign currency, an investment in that country loses value because that currency is worth less in U.S. dollars. Currency exchange rates may fluctuate significantly over short periods of time for a number of reasons, including changes in interest rates. Devaluation of a currency by a country’s government or banking authority also will have a significant impact on the value of any investments denominated in that currency. Currency markets generally are not as regulated as securities markets, may be riskier than other types of investments and may increase the volatility of the Fund. The Fund may engage in various strategies to hedge against currency risk. These strategies may consist of use of forward currency contracts including non-deliverable forward contracts and foreign currency futures contracts. To the extent the Fund enters into such transactions in markets other than in the United States, the Fund may be subject to certain currency, settlement, liquidity, trading and other risks similar to those described in this prospectus with respect to the Fund’s investments in foreign securities. There can be no assurance that the Fund’s hedging activities will be effective, and the Fund will incur costs in connection with the hedging. Currency hedging may limit the Fund’s return if the relative values of currencies change. Furthermore, the Fund may only engage in hedging activities from time to time and may not necessarily be engaging in hedging activities when movements in currency exchange rates occur.

Industry and Sector Focus Risk. At times, the Fund may increase the relative emphasis of its investments in a particular industry or sector. The prices of securities of issuers in a particular industry or sector may be more susceptible to fluctuations due to changes in economic or business conditions, government regulations, availability of basic resources or supplies, or other events that affect that industry or sector more than securities of issuers in other industries and sectors. To the extent that the Fund increases the relative emphasis of its investments in a particular industry or sector, the value of the Fund’s Shares may fluctuate in response to events affecting that industry or sector.

12 | J.P. Morgan Exchange-Traded Funds

Market Trading Risk

Risk that Shares of the Fund May Trade at Prices Other Than NAV. Shares of the Fund may trade on the Exchange at prices above, below or at their most recent NAV. The NAV of the Fund’s Shares, which is calculated at the end of each business day, will generally fluctuate with changes in the market value of the Fund’s holdings. The market prices of the Shares will also fluctuate, in some cases materially, in accordance with changes in NAV and the intraday value of the Fund’s holdings, as well as the relative supply of and demand for the Shares on the Exchange. Differences between secondary market prices of Shares and the intraday value of the Fund’s holdings may be due largely to supply and demand forces in the secondary market, which may not be the same forces as those influencing prices for securities held by the Fund at a particular time.

Given the fact that Shares can be created and redeemed by authorized participants in Creation Units, the adviser believes that large discounts or premiums to the NAV of Shares should not be sustained in the long-term. While the creation/redemption feature is designed to make it likely that Shares normally will trade close to the value of the Fund’s holdings, market prices are not expected to correlate exactly to the Fund’s NAV due to timing reasons, supply and demand imbalances and other factors. In addition, disruptions to creations and redemptions, adverse developments impacting market makers, authorized participants or other market participants, or high market volatility may result in market prices for Shares of the Fund that differ significantly from its NAV or to the intraday value of the Fund’s holdings. As a result of these factors, among others, the Fund’s Shares may trade at a premium or discount to NAV, especially during periods of significant market volatility.

Given the nature of the relevant markets for certain of the securities for the Fund, Shares may trade at a larger premium or discount to NAV than shares of other kinds of ETFs. In addition, the securities held by the Fund may be traded in markets that close at a different time than the Exchange. Liquidity in those securities may be reduced after the applicable closing times. Accordingly, during the time when the Exchange is open but after the applicable market closing, fixing or settlement times, bid/ask spreads and the resulting premium or discount to the Shares’ NAV may widen.

Cost of Buying or Selling Shares. When you buy or sell Shares of the Fund through a broker, you will likely incur a brokerage commission or other charges imposed by brokers. In addition, the market price of Shares, like the price of any exchange-traded security, includes a “bid-ask spread” charged by the market makers or other participants that trade the particular security. The spread of the Fund’s Shares varies over time based on the Fund’s trading volume and market liquidity and may increase if the Fund’s trading volume, the spread of the Fund’s underlying securities, or market liquidity decrease. In times of severe market disruption, including when trading of the Fund’s holdings may be halted, the bid-ask spread may increase significantly. This means that Shares may trade at a discount to the Fund’s NAV, and the discount is likely to be greatest during significant market volatility.

Short Selling Risk. Shares of the Fund, similar to shares of other issuers listed on a stock exchange, may be sold short and are therefore subject to the risk of increased volatility and price decreases associated with being sold short.

No Guarantee of Active Trading Market Risk. While Shares are listed on the Exchange, there can be no assurance that active trading markets for the Shares will be maintained by market makers or by authorized participants. JPMorgan Distribution Services, Inc., the distributor of the Fund’s Shares (the Distributor), does not maintain a secondary market in the Shares.

Trading Issues Risk. Trading in Shares on the Exchange may be halted due to market conditions or for reasons that, in the view of the Exchange, make trading in Shares inadvisable. In addition, trading in Shares on the Exchange is subject to trading halts caused by extraordinary market volatility pursuant to the Exchange “circuit breaker” rules. If a trading halt or unanticipated early closing of the Exchange occurs, a shareholder may be unable to purchase or sell Shares of the Fund.

There can be no assurance that the requirements of the Exchange necessary to maintain the listing of the Fund will continue to be met or will remain unchanged.

Authorized Participant Concentration Risk. Only an authorized participant may engage in creation or redemption transactions directly with the Fund. The Fund has a limited number of intermediaries that act as authorized participants and none of these authorized participants is or will be obligated to engage in creation or redemption transactions. To the extent that these intermediaries exit the business or are unable to or choose not to proceed with creation and/or redemption orders with respect to the Fund and no other authorized participant creates or redeems, Shares may trade at a discount to NAV and possibly face trading halts and/or delisting.

Smaller Company Risk. Investments in smaller, newer companies may be riskier, less liquid, more volatile and more vulnerable to economic, market and industry changes than investments in larger, more established companies. The securities of smaller companies may trade less frequently and in smaller volumes than securities of larger companies. As a result, changes in the price of debt or equity issued by such companies may be more sudden or erratic than the prices of large capitalization companies, especially over the short term. Because smaller companies may have limited product lines, markets or financial resources or may depend on a few key employees, they may be more susceptible to particular economic events or competitive factors than large capitalization companies. This may cause unexpected and frequent decreases in the value of the Fund’s investments.

March 1, 2023 | 13

More About the Fund (continued)

Developed Asia Pacific (ex-Japan) Market Risk. Investments in securities of issuers in developed Asia Pacific countries (ex-Japan) involve risks that are specific to the Asia Pacific region, including certain legal, regulatory, political and economic risks. Certain Asia Pacific countries have experienced expropriation and/or nationalization of assets, political and social instability and armed conflict. Some economies in this region are dependent on a range of commodities and are strongly affected by international commodity prices. The market for securities in this region may also be directly influenced by the flow of international capital, and by the economic and market conditions of neighboring countries. Some developed Asia Pacific economies are highly dependent on trade and economic conditions in other countries. Although the Fund only intends to invest in developed countries in the Asia Pacific region, the Fund may be impacted by risks associated with investing in developing and emerging market countries in the Asia Pacific region because the economies of countries (including developed countries) in the Asia Pacific region may be heavily dependent on one another.

Depositary Receipts Risk. The Fund’s investments may take the form of depositary receipts, including unsponsored depositary receipts. Unsponsored depositary receipts may not provide as much information about the underlying issuer and may not carry the same voting privileges as sponsored depositary receipts. Unsponsored depositary receipts are issued by one or more depositaries in response to market demand, but without a formal agreement with the company that issues the underlying securities.

Exchange-Traded Fund (ETF) and Other Investment Company Risk. The Fund may invest in shares of other investment companies and ETFs. Shareholders bear both their proportionate share of the Fund’s expenses and similar expenses of the underlying investment company or ETF when the Fund invests in shares of another investment company or ETF. The Fund is subject to the risks associated with the ETF or investment company’s investments. The price and movement of an ETF or closed-end fund designed to track an index may not track the index and may result in a loss. In addition, ETFs and closed-end investment companies may trade at a price above (premium) or below (discount) their net asset value, especially during periods of significant market volatility or stress, causing investors to pay significantly more or less than the value of the ETF’s underlying portfolio. Certain ETFs or closed-end funds traded on exchanges may be thinly traded and experience large spreads between the “ask” price quoted by a seller and the “bid” price offered by a buyer.

Preferred Securities Risk. Preferred securities generally have a preference as to dividends and liquidation over an issuer’s common stock but ranks junior to debt securities in an issuer’s capital structure. Unlike interest payments on debt securities, dividends on preferred securities are payable only if declared by the issuer’s board of directors. As a consequence, if the board of directors of an issuer does not declare dividends or distributions for the relevant dividend or distribution periods, the issuer will not be obligated to pay dividends or distributions on the relevant payment date, and such dividends and distributions may be forfeited. Holders of preferred securities typically do not have voting rights except in certain circumstances where they may be given only limited voting rights. Preferred securities also may be subject to optional or mandatory redemption provisions. Preferred shares may carry different rights or obligations in jurisdictions outside of the United States.

Privately Placed Securities Risk. Privately placed securities generally are less liquid than publicly traded securities and the Fund may not always be able to sell such securities without experiencing delays in finding buyers or reducing the sale price for such securities. The disposition of some of the securities held by the Fund may be restricted under federal securities laws or by the relevant exchange by a governmental or supervisory authority. As a result, the Fund may not be able to dispose of such investments at a time when, or at a price at which, it desires to do so and may have to bear expenses of registering these securities, if necessary. These securities may also be difficult to value.

Structured Instrument Risk. The Fund may invest in instruments that have similar economic characteristics to equity securities, such as participation notes or other structured instruments that may be developed from time to time (structured instruments). Structured instruments are notes that are issued by banks, broker-dealers or their affiliates and are designed to offer a return linked to a particular underlying equity or market.

If the structured instrument were held to maturity, the issuer would pay to the purchaser the underlying instrument’s value at maturity with any necessary adjustments. The holder of a structured instrument that is linked to a particular underlying security or instrument may be entitled to receive dividends paid in connection with that underlying security or instrument, but typically does not receive voting rights as it would if it directly owned the underlying security or instrument. Structured instruments have transaction costs. In addition, there can be no assurance that there will be a trading market for a structured instrument or that the trading price of a structured instrument will equal the underlying value of the security, instrument or market that it seeks to replicate. Unlike a direct investment in equity securities, structured instruments typically involve a term or expiration date, potentially increasing the Fund’s turnover rate, transaction costs and tax liability.

Due to transfer restrictions, the secondary markets on which a structured instrument is traded may be less liquid than the market for other securities, or may be completely illiquid, which may expose the Fund to risks of mispricing or improper valuation. Structured instruments typically constitute general unsecured contractual obligations of the banks, broker-dealers or their relevant affiliates

14 | J.P. Morgan Exchange-Traded Funds

that issue them, which subjects the Fund to counterparty risk (and this risk may be amplified if the Fund purchases structured instruments from only a small number of issuers). Structured instruments also have the same risks associated with a direct investment in the underlying securities, instruments or markets that they seek to replicate.

Real Estate Securities Risk. The value of real estate securities in general, and REITs in particular, are subject to the same risks as direct investments in real estate and mortgages which include, but are not limited to, sensitivity to changes in real estate values and property taxes, interest rate risk, tax and regulatory risk, fluctuations in rent schedules and operating expenses, adverse changes in local, regional or general economic conditions, deterioration of the real estate market and the financial circumstances of tenants and sellers, unfavorable changes in zoning, building, environmental and other laws, the need for unanticipated renovations, unexpected increases in the cost of energy and environmental factors. Furthermore, a REIT could fail to qualify for tax free pass-through of its income under the Internal Revenue Code or fail to maintain its exemption from registration under the 1940 Act, which could produce adverse economic consequences for the REIT and its investors, including the Fund.

The underlying mortgage loans may be subject to the risks of default or of prepayments that occur earlier or later than expected, and such loans may also include so-called “sub-prime” mortgages. The value of REITs will also rise and fall in response to the management skill and creditworthiness of the issuer. In particular, the value of these securities may decline when interest rates rise and will also be affected by the real estate market and by the management of the underlying properties. REITs may be more volatile and/or more illiquid than other types of equity securities. The Fund will indirectly bear its proportionate share of expenses, including management fees, paid by each REIT in which it invests in addition to the expenses of the Fund.

In addition, certain of the companies in which the Fund intends to invest may have developed or commenced development on properties and may develop additional properties in the future. Real estate development involves significant risks in addition to those involved in the ownership and operation of established properties, including the risks that financing, if needed, may not be available on favorable terms for development projects, that construction may not be completed on schedule (resulting in increased debt service expense and construction costs), that estimates of the costs of construction may prove to be inaccurate and that properties may not be leased, rented or operated on profitable terms and therefore will fail to perform in accordance with expectations. As a result, the value of the Fund’s investment may decrease in value. Real estate securities have limited diversification and are, therefore, subject to risks inherent in operating and financing a limited number of projects. Real estate securities are also subject to heavy cash flow dependency and defaults by borrowers or tenants.

Convertible Securities Risk. A convertible security generally entitles the holder to receive interest paid or accrued on debt securities or the dividend paid on preferred stock until the convertible security matures or is redeemed, converted or exchanged. Before conversion, convertible securities generally have characteristics similar to both debt and equity securities. The value of convertible securities tends to decline as interest rates rise and, because of the conversion feature, tends to vary with fluctuations in the market value of the underlying securities. Convertible securities ordinarily provide a stream of income with generally higher yields than those of common stock of the same or similar issuers. Convertible securities generally rank senior to common stock in a corporation’s capital structure but are usually subordinated to comparable non-convertible securities. Convertible securities generally do not participate directly in any dividend increases or decreases of the underlying securities, although the market prices of convertible securities may be affected by any dividend changes or other changes in the underlying securities. Contingent convertible securities are subject to additional risk factors. A contingent convertible security is a hybrid debt security typically issued by a non-U.S. bank that may be convertible into equity or may be written down if a pre-specified trigger event such as a decline in capital ratio below a prescribed threshold occurs. If such a trigger event occurs, the Fund may lose the principal amount invested on a permanent or temporary basis or the contingent convertible security may be converted to equity. In addition to being subject to a possible write-down upon the occurrence of a trigger event, contingent convertible securities may also be subject to a permanent write-down or conversion into equity (in whole or in part), if the applicable bank regulator or other public administrative authority having responsibility for managing the orderly dissolution of an institution (the “resolution authority”) has determined that the issuer is not viable. Coupon payments on contingent convertible securities may be discretionary and may be cancelled by the issuer. Holders of contingent convertible securities may suffer a loss of capital when comparable equity holders do not. As contingent convertible securities may be perpetual or have long-dated maturities, they may face greater interest rate sensitivity and may be subject to greater fluctuations in value than securities with shorter maturity dates. Such securities also may be subject to prepayment risk due to optional or mandatory redemption provisions.

Initial Public Offerings (IPO) Risk. IPO securities have no trading history, and information about the companies may be available for very limited periods. The prices of securities sold in IPOs may be highly volatile and their purchase may involve high transaction costs. At any particular time or from time to time, the Fund may not be able to invest in securities issued in IPOs, or invest to the extent desired, because, for example, only a small portion (if any) of the securities being offered in an IPO may be made available to the Fund. In addition, under certain market conditions, a relatively small number of companies may issue securities in IPOs. Similarly, as the number of purchasers to which IPO securities are allocated increases, the number of securities issued to the Fund may

March 1, 2023 | 15

More About the Fund (continued)

decrease. The performance of the Fund during periods when it is unable to invest significantly or at all in IPOs may be lower than during periods when the Fund is able to do so. In addition, as the Fund increases in size, the impact of IPOs on the Fund’s performance will generally decrease.

Interest Rate Risk. The Fund’s debt securities will increase or decrease in value based on changes in interest rates. If rates increase, the value of the Fund’s investments generally declines. On the other hand, if rates fall, the value of investments generally increases. Securities with greater interest rate sensitivity and longer maturities tend to produce higher yields, but generally are subject to greater fluctuations in value. The Fund may invest in variable and floating rate securities. Although these instruments are generally less sensitive to interest rate changes than fixed rate instruments, the value of variable and floating rate securities may decline if their interest rates do not rise as quickly or as much as general interest rates. Many factors can cause interest rates to rise. Some examples include central bank monetary policy, rising inflation rates and general economic conditions. The Fund may face a heightened level of interest rate risk due to certain changes or uncertainty in monetary policy, such as an interest rate increase by the Federal Reserve.

Debt market conditions are highly unpredictable and some parts of the market are subject to dislocations. Beginning in March 2022, the Federal Reserve Board began increasing interest rates and has signaled the possibility of further increases. It is difficult to accurately predict the pace at which the Federal Reserve Board will increase interest rates any further, or the timing, frequency or magnitude of any such increases, and the evaluation of macro-economic and other conditions could cause a change in approach in the future. Any such changes could be sudden and could expose debt markets to significant volatility and reduced liquidity for Fund investments.

Securities Lending Risk. The Fund may engage in securities lending. Securities lending involves counterparty risk, including the risk that the loaned securities may not be returned or returned in a timely manner and/or a loss of rights in the collateral if the borrower or the lending agent defaults. This risk is increased when the Fund’s loans are concentrated with a single or limited number of borrowers. In addition, the Fund bears the risk of loss in connection with its investments of the cash collateral it receives from the borrower. To the extent that the value or return of the Fund’s investments of the cash collateral declines below the amount owed to a borrower, the Fund may incur losses that exceed the amount it earned on lending the security. In situations where the adviser does not believe that it is prudent to sell the cash collateral investments in the market, the Fund may borrow money to repay the borrower the amount of cash collateral owed to the borrower upon return of the loaned securities. This will result in financial leverage, which may cause the Fund to be more volatile because financial leverage tends to exaggerate the effect of any increase or decrease in the value of the Fund’s portfolio securities.

Transactions and Liquidity Risk. The Fund could experience a loss when selling securities to meet redemption requests and its liquidity may be negatively impacted. The risk of loss increases if the redemption requests are large or frequent, occur in times of overall market turmoil or declining prices for the securities sold, or when the securities the Fund wishes to or is required to sell are illiquid. To the extent a large proportion of Shares are held by a small number of shareholders (or a single shareholder), including funds or accounts over which the adviser or its affiliates have investment discretion, the Fund is subject to the risk that these shareholders will purchase or redeem Shares in large amounts rapidly or unexpectedly, including as a result of an asset allocation decision made by the adviser or its affiliates. To the extent these larger shareholders transact in the secondary market, such transactions may account for a large percentage of the Fund’s trading volume on the Exchange, which may have a material effect (upward or downward) on the market price of Shares. In addition to the other risks described in this section, these transactions could adversely affect the ability of the Fund to conduct its investment program. The Fund may be unable to sell illiquid securities at its desired time or price or the price at which the securities have been valued for purposes of the Fund’s NAV. Illiquidity can be caused by a drop in overall market trading volume, an inability to find a ready buyer, or legal restrictions on the securities’ resale. Certain securities that were liquid when purchased may later become illiquid, particularly in times of overall economic distress.

Similarly, large purchases of Shares may adversely affect the Fund’s performance to the extent that the Fund is delayed in investing new cash and is required to maintain a larger cash position than it ordinarily would. Large redemptions also could accelerate the realization of capital gains, increase the Fund’s transaction costs and impact the Fund’s performance. To the extent redemptions are effected in cash, an investment in the Fund may be less tax-efficient than an investment in an ETF that distributes portfolio securities entirely in-kind.

Cyber Security Risk. As the use of technology has become more prevalent in the course of business, the Fund has become more susceptible to operational and financial risks associated with cyber security, including: theft, loss, misuse, improper release, corruption and destruction of, or unauthorized access to, confidential or highly restricted data relating to the Fund and its shareholders; and compromises or failures to systems, networks, devices and applications relating to the operations of the Fund and its service providers. Cyber security risks may result in financial losses to the Fund and its shareholders; the inability of the Fund to transact business with its shareholders; delays or mistakes in the calculation of the Fund’s NAV or other materials provided to shareholders; the inability to process transactions with shareholders or other parties; violations of privacy and other laws; regulatory fines, penalties and reputational damage; and compliance and remediation costs, legal fees and other expenses. The Fund’s service providers

16 | J.P. Morgan Exchange-Traded Funds

(including, but not limited to, the adviser, any sub-advisers, administrator, transfer agent, and custodian or their agents), financial intermediaries, companies in which the Fund invests and parties with which the Fund engages in portfolio or other transactions also may be adversely impacted by cyber security risks in their own businesses, which could result in losses to the Fund or its shareholders. While measures have been developed which are designed to reduce the risks associated with cyber security, there is no guarantee that those measures will be effective, particularly since the Fund does not directly control the cyber security defenses or plans of its service providers, financial intermediaries and companies in which it invests or with which it does business.

Regulatory and Legal Risk. U.S. and non-U.S. governmental agencies and other regulators regularly implement additional regulations and legislators pass new laws that affect the investments held by the Fund, the strategies used by the Fund or the level of regulation or taxation applying to the Fund (such as regulations related to investments in derivatives and other transactions). These regulations and laws may adversely impact the investment strategies, performance, costs and operations of the Fund or taxation of shareholders.

Volcker Rule Risk. Pursuant to Section 619 of the Dodd-Frank Wall Street Reform and Consumer Protection Act and certain rules promulgated thereunder known as the Volcker Rule, if the adviser and/or its affiliates own 25% or more of the outstanding ownership interests of the Fund after the permitted seeding period from the implementation of the Fund’s investment strategy, the Fund could be subject to restrictions on trading that would adversely impact the Fund’s ability to execute its investment strategy. Generally, the permitted seeding period is three years from the implementation of the Fund’s investment strategy. As a result, the adviser and/or its affiliates may be required to reduce their ownership interests in the Fund at a time that is sooner than would otherwise be desirable, which may result in the Fund’s liquidation or, if the Fund is able to continue operating, may result in losses, increased transaction costs and adverse tax consequences as a result of the sale of portfolio securities.

For more information about risks associated with the types of investments that the Fund purchases, please read the “Risk/Return Summary” at the front of this prospectus and the Statement of Additional Information.

Conflicts of Interest

An investment in a Fund is subject to a number of actual or potential conflicts of interest. For example, the Adviser and/or its affiliates provide a variety of different services to a Fund, for which the Fund compensates them. As a result, the Adviser and/or its affiliates have an incentive to enter into arrangements with a Fund, and face conflicts of interest when balancing that incentive against the best interests of a Fund. The Adviser and/or its affiliates also face conflicts of interest in their service as investment adviser to other clients, and, from time to time, make investment decisions that differ from and/or negatively impact those made by the Adviser on behalf of a Fund. In addition, affiliates of the Adviser provide a broad range of services and products to their clients and are major participants in the global currency, equity, commodity, fixed income and other markets in which a Fund invests or will invest. In certain circumstances by providing services and products to their clients, these affiliates’ activities will disadvantage or restrict the Funds and/or benefit these affiliates. The Adviser may also acquire material non-public information which would negatively affect the Adviser’s ability to transact in securities for a Fund. JPMorgan and the Funds have adopted policies and procedures reasonably designed to appropriately prevent, limit or mitigate conflicts of interest. In addition, many of the activities that create these conflicts of interest are limited and/or prohibited by law, unless an exception is available. For more information about conflicts of interest, see the Potential Conflicts of Interest section in the Statement of Additional Information.

Temporary Defensive and Cash Positions

For liquidity and to respond to unusual market conditions, the Fund may invest all or most of its total assets in cash and cash equivalents for temporary defensive purposes. These investments may result in a lower yield than lower-quality or longer-term investments.

| WHAT IS A CASH EQUIVALENT? |

| Cash equivalents are highly liquid, high-quality instruments with maturities of three months or less on the date they are purchased. They include securities issued by the U.S. government, its agencies and instrumentalities, repurchase agreements, certificates of deposit, bankers’ acceptances, commercial paper, money market mutual funds, and bank deposit accounts. |

While the Fund is engaged in a temporary defensive position, it may not meet its investment objective. These investments may also be inconsistent with the Fund’s main investment strategies. Therefore, the Fund will pursue a temporary defensive position only when market conditions warrant.

Whether engaging in temporary defensive purposes or otherwise, the Fund may not hold more than 10% of its total assets in cash and cash equivalents. These amounts are in addition to assets held for derivative margin deposits or other segregated accounts.

March 1, 2023 | 17

More About the Fund (continued)

MSCI Disclaimer

Source: MSCI. The MSCI information may only be used for your internal use, may not be reproduced or redisseminated in any form and may not be used as a basis for or a component of any financial instruments or products or indices. None of the MSCI information is intended to constitute investment advice or a recommendation to make (or refrain from making) any kind of investment decision and may not be relied on as such. Historical data and analysis should not be taken as an indication or guarantee of any future performance analysis, forecast, or prediction. The MSCI information is provided on an “as is” basis and the user of this information assumes the entire risk of any use made of this information. MSCI, each of its affiliates and each other person involved in or related to compiling, computing or creating any MSCI information (collectively, the “MSCI Parties”) expressly disclaims all warranties (including, without limitation, any warranties of originality, accuracy, completeness, timeliness, non-infringement, merchantability and fitness for a particular purpose) with respect to this information. Without limiting any of the foregoing, in no event shall any MSCI Party have any liability for any direct, indirect, special, incidental, punitive, consequential (including, without limitation, lost profits) or any other damages. (www.msci.com)

Disclosure of Portfolio Holdings

A description of the policies and procedures with respect to the disclosure of the Fund’s portfolio securities is available in the Fund’s Statement of Additional Information.

Additional Fee Waiver and/or Expense Reimbursement

Service providers to the Fund (as was the case for the predecessor fund) may, from time to time, voluntarily waive all or a portion of any fees to which they are entitled and/or reimburse certain expenses as they may determine from time to time. The Fund’s service providers may discontinue or modify these voluntary actions at any time without notice. Performance for the Fund will reflect (and performance for the predecessor fund reflects) the voluntary waiver of fees and/or the reimbursement of expenses, if any. Without these voluntary waivers and/or expense reimbursements, performance would be less favorable.

18 | J.P. Morgan Exchange-Traded Funds

The Fund’s Management and Administration

The Fund’s Management and Administration

The Fund is a series of J.P. Morgan Exchange-Traded Fund Trust, a Delaware statutory trust (the Trust). The Trust is governed by the Board of Trustees, which is responsible for overseeing all business activities of the Fund.

The Fund’s Investment Adviser

J.P. Morgan Investment Management Inc. (JPMIM or the adviser) is the investment adviser to the Fund. JPMIM is located at 383 Madison Avenue, New York, NY 10179. JPMIM also served as the investment adviser to the predecessor fund.

JPMIM is a wholly-owned subsidiary of JPMorgan Asset Management Holdings Inc., which is a wholly-owned subsidiary of JPMorgan Chase & Co. (JPMorgan Chase), a bank holding company.

In rendering investment advisory services to the Fund, JPMIM uses the portfolio management, research and other resources of a foreign (non-U.S.) affiliate of JPMIM and may provide services to the Fund through a “participating affiliate” arrangement, as that term is used in relief granted by the staff of the SEC. Under this relief, U.S. registered investment advisers are allowed to use portfolio management or research resources of advisory affiliates subject to the regulatory supervision of the registered investment adviser.

During the fiscal year ended 10/31/22, JPMIM was paid management fees (net of waivers) of 0.18% as a percentage of average daily net assets of the Fund.1

A discussion of the basis the Board of Trustees of the Trust used in approving the investment advisory agreement for the Fund will be available in the first shareholder report for the Fund.

The Portfolio Managers

The portfolio management team is led by Piera Elisa Grassi, a Managing Director, Nicholas Farserotu, a Vice President, and Winnie Cheung, a Vice President, work with Ms. Grassi in managing the Fund. Ms. Grassi is the lead portfolio manager for the International Research Enhanced strategies within the International Equity Group, based in London. An employee since 2004, Ms. Grassi was previously a portfolio manager and quantitative analyst. Prior to joining JPMIM or its affiliates (or one of their predecessors), Ms. Grassi was a bond quantitative analyst and risk analyst at Foreign and Colonial Asset Management. Before this, she worked for BARRA in London, focusing on equity risk management and portfolio construction. Ms. Grassi obtained a Laurea from Bocconi University in Milan. Nicholas Farserotu, a Vice President, is a portfolio manager within the International Equity Group focusing on the International Research Enhanced strategies. An employee since 2015, Mr. Farserotu was previously an investment analyst at SphereInvest Group in Geneva. Mr. Farserotu obtained an MSc. in Financial Engineering from Imperial College London (with Distinction) and also holds an MSc. and a BSc. in Economics from the University of Geneva. He is a CFA charterholder. Winnie Cheung, a Vice President, is a portfolio manager in the International Equity Group focusing on the International Research Enhanced strategies. An employee since 2012, Ms. Cheung was previously a performance analyst. Ms. Cheung obtained a MSc in Finance from CassBusiness School in London. Ms. Grassi, Mr. Farserotu and Ms. Cheung have been portfolio managers of the Fund since its inception. Ms. Grassi, Mr. Farserotu and Ms. Cheung also were the predecessor fund's portfolio managers since 2016, 2020 and 2020, respectively.

The Statement of Additional Information provides additional information about the portfolio managers’ compensation, other accounts managed by the portfolio managers and the portfolio managers’ ownership of securities in the Fund.

The Fund’s Administrator

JPMIM provides administration services for and oversees the other service providers of the Fund. JPMIM receives the following annual fee on behalf of the Fund for administration services: 0.075% of the first $10 billion of average daily net assets of the Fund, plus 0.050% of average daily net assets of the Fund between $10 billion and $20 billion, plus 0.025% of average daily net assets of the Fund between $20 billion and $25 billion, plus 0.010% of the average daily net assets of the Fund over $25 billion.

The Fund’s Distributor

JPMorgan Distribution Services, Inc. (the Distributor) is the distributor of the Fund’s Shares. The Distributor or its agent distributes Creation Units for the Fund on an agency basis. The Distributor does not maintain a secondary market in Shares of the Fund. The Distributor has no role in determining the investment policies of the Fund or the securities that are purchased or sold by the Fund. The Distributor’s principal address is 1111 Polaris Parkway, Columbus, OH 43240.

1For the period prior to the close of business on June 10, 2022, this information includes fees paid by the predecessor fund.

March 1, 2023 | 19

The Fund’s Management and Administration (continued)

Payments to Financial Intermediaries

JPMIM and, from time to time, other affiliates of JPMorgan Chase may, at their own expense and out of their own legitimate profits, provide cash payments to Financial Intermediaries whose customers invest in Shares of the Fund. For this purpose, Financial Intermediaries include financial advisors, investment advisers, brokers, financial planners, banks, insurance companies, retirement or 401(k) plan administrators and others, including various affiliates of JPMorgan Chase, that may enter into agreements with JPMIM and/or its affiliates. These cash payments may relate to marketing activities and presentations, educational training programs, the support of technology platforms and/or reporting systems, or the Financial Intermediaries’ making Shares of the Fund available to their customers. Such compensation may provide such Financial Intermediaries with an incentive to favor sales of Shares of the Fund over other investment options they make available to their customers. See the Statement of Additional Information for more information.

20 | J.P. Morgan Exchange-Traded Funds

Purchase and Redemption of Shares

Buying and Selling Shares

In the Secondary Market. Most investors will buy and sell Shares of the Fund in secondary market transactions through brokers. Shares of the Fund are listed and traded on the secondary market on the Exchange. Shares can be bought and sold throughout the trading day like other publicly traded shares. There is no minimum investment. Although Shares are generally purchased and sold in “round lots” of 100 Shares, brokerage firms typically permit investors to purchase or sell Shares in smaller “odd lots,” at no per-Share price differential. When buying or selling Shares through a broker, you will incur customary brokerage commissions and charges, and you may pay some or all of the spread between the bid and the offered price in the secondary market on each leg of a round trip (purchase and sale) transaction. The spread varies over time for Shares of the Fund based on the Fund’s trading volume and market liquidity, and is generally lower if the Fund has a lot of trading volume and market liquidity.

Shares of the Fund trade on the Exchange at prices that may differ to varying degrees from the daily NAV of the Shares.

Directly with the Fund. The Fund’s Shares are issued or redeemed by the Fund at NAV per Share only in a large specified number of Shares called a “Creation Unit” or multiples thereof. Investors such as market makers, large investors and institutions who wish to deal in Creation Units directly with the Fund must have entered into an authorized participant agreement with the Distributor, or purchase through a dealer that has entered into such an agreement. Set forth below is a brief description of the procedures applicable to purchases and redemptions of Creation Units. For more detailed information, see “Creation and Redemption of Creation Unit Aggregations” in the Fund’s Statement of Additional Information.