UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

(Mark One)

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended December 31 , 2023

or

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from ________ to ________

Commission file number 001-39590

fuboTV Inc.

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code (212 ) 672-0055

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes o No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes o No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | o | x | |||||||||

| Non-accelerated filer | o | Smaller reporting company | |||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. x

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. o

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.) Yes o No x

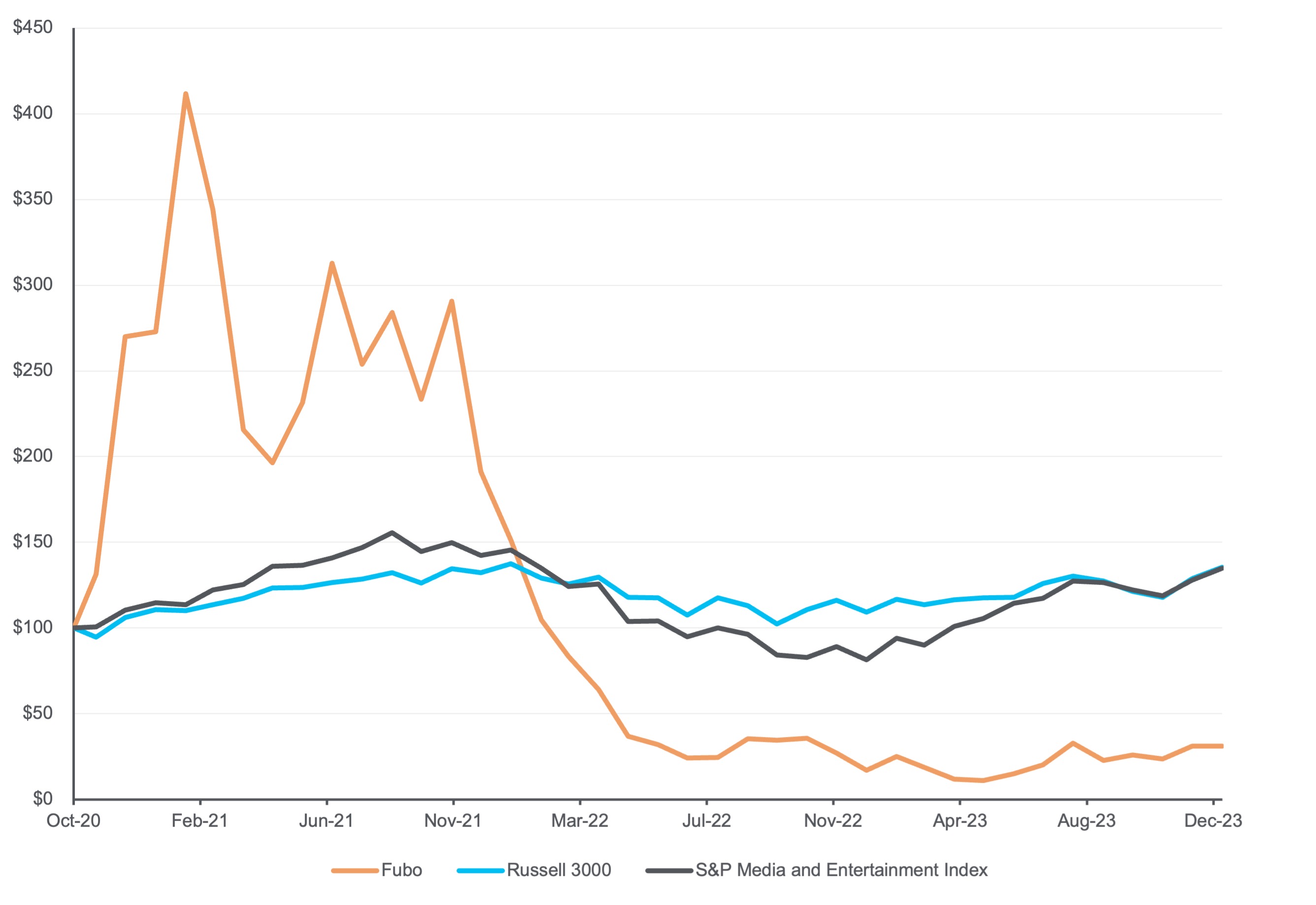

The aggregate market value of the registrant’s voting and non-voting common stock held by non-affiliates of the registrant, based on the closing sale price of the registrant’s common stock on June 30, 2023 (the last business day of the registrant’s most recently completed second fiscal quarter) was $577,302,821 .

The number of shares outstanding of the registrant’s common stock as of February 29, 2024 was 299,502,862 shares.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement relating to its 2024 Annual Meeting of Shareholders, to be filed with the SEC within 120 days after the end of the fiscal year ended December 31 , 2023

TABLE OF CONTENTS

| Page | ||||||||

Item 1C. | ||||||||

2

BASIS OF PRESENTATION

As used in this Annual Report on Form 10-K (“Annual Report”), unless expressly indicated or the context otherwise requires, references to “fuboTV Inc.,” “Fubo,” “we,” “us,” “our,” “the Company,” and similar references refer to fuboTV Inc., a Florida corporation and its consolidated subsidiaries.

FORWARD-LOOKING STATEMENTS

This Annual Report includes forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements, which are subject to a number of risks, uncertainties, and assumptions, generally relate to future events or our future financial or operating performance. In some cases, you can identify these statements by forward-looking words such as “believe,” “may,” “will,” “estimate,” “continue,” “anticipate,” “design,” “intend,” “expect,” “could,” “plan,” “potential,” “predict,” “seek,” “should,” “would,” “target,” “project,” “contemplate,” or the negative version of these words and other comparable terminology that concern our expectations, strategy, plans, intentions, or projections. Forward-looking statements contained in this Annual Report include, but are not limited to, statements regarding our future results of operations and financial position, anticipated cash requirements, industry and business trends, stock-based compensation, revenue recognition, business strategy, plans and market growth, legal proceedings, and our objectives for future operations, including related to investment in our technologies and data capabilities, subscriber acquisition strategies, impacts of the dissolution of our gaming business, and our international operations.

We have based the forward-looking statements contained in this Annual Report primarily on our current expectations and projections about future events and trends that we believe may affect our business, financial condition, results of operations, prospects, business strategy and financial needs. These forward-looking statements are subject to a number of risks, uncertainties, and assumptions, including those described in Part I, Item 1A, “Risk Factors” of this Annual Report. These risks are not exhaustive. Other sections of this Annual Report include additional factors that could adversely impact our business and financial performance. Moreover, we operate in a very competitive and rapidly changing environment, and new risks emerge from time to time. It is not possible for our management to predict all risks, nor can we assess the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements we may make. In light of these risks, uncertainties, and assumptions, the forward-looking events and circumstances discussed in this Annual Report may not occur and actual results could differ materially and adversely from those anticipated or implied in the forward-looking statements and you should not place undue reliance on our forward-looking statements.

In addition, forward-looking statements are based upon information available to us as of the date of this Annual Report, and while we believe such information forms a reasonable basis for such statements, such information may be limited or incomplete, and our statements should not be read to indicate that we have conducted an exhaustive inquiry into, or review of, all potentially available relevant information. These statements are inherently uncertain, and investors are cautioned not to unduly rely upon these statements.

The forward-looking statements made in this Annual Report relate only to events as of the date on which the statements are made. We undertake no obligation to update any forward-looking statements made in this Annual Report to reflect events or circumstances after the date of this Annual Report or to reflect new information or the occurrence of unanticipated events, except as required by law.

3

RISK FACTORS SUMMARY

Our business is subject to numerous risks and uncertainties, including those described in Part I, Item 1A. “Risk Factors” in this Annual Report. Material risks that may affect our business, operating results and financial condition include, but are not limited to, the following:

•We have incurred operating losses in the past, expect to incur operating losses in the future and may never achieve or maintain profitability.

•We may require additional capital to meet our financial obligations and support planned business growth, and this capital might not be available on acceptable terms or at all.

•Our revenue is subject to seasonality, and if subscriber behavior during certain seasons falls below our expectations, our business may be harmed.

•Our operating results may fluctuate, which makes our results difficult to predict.

•If we fail to effectively manage our growth, our business, operating results, and financial condition may suffer.

•The long-term nature of certain of our content commitments may limit our operating flexibility and could adversely affect our liquidity and results of operations.

•Our results may be adversely affected if long-term content contracts are not renewed on sufficiently favorable terms.

•If our efforts to attract and retain subscribers are not successful, our business will be adversely affected.

•Our agreements with certain distribution partners may contain parity obligations which limit our ability to pursue unique partnerships.

•If content providers refuse to license streaming content or other rights upon terms acceptable to us, our business could be adversely affected.

•Our content providers impose a number of restrictions on how we distribute and market our products and services, which can adversely affect our business.

•We rely upon Google Cloud Platform and Amazon Web Services to operate certain aspects of our service, and any disruption of or interference with our use of Google Cloud Platform and/or Amazon Web Services would impact our operations and our business would be adversely impacted.

•Our key metrics and other estimates are subject to inherent challenges in measurement, and real or perceived inaccuracies in those metrics may seriously harm and negatively affect our reputation and our business.

•Preparing and forecasting our financial results requires us to make judgments and estimates which may differ materially from actual results, and if our operating and financial performance does not meet the guidance that we provide to the public, the market price of our common stock may decline.

•TV streaming is highly competitive and many companies, including large technology and entertainment companies, TV brands, and service operators, are actively focusing on this industry. If we fail to differentiate ourselves and compete successfully with these companies, it will be difficult for us to attract or retain subscribers and our business will be harmed.

•If the technology we use in operating our business fails, is unavailable, or does not operate to expectations, our business and results of operation could be adversely impacted.

•If government regulations relating to the Internet or other areas of our business change, we may need to alter the manner in which we conduct our business and we may incur greater operating expenses.

4

•We are subject to taxation-related risks in multiple jurisdictions.

•We could be subject to claims or have liability based on defects with respect to certain historical corporate transactions that were not properly authorized or documented.

•Legal proceedings could cause us to incur unforeseen expenses and could occupy a significant amount of our management’s time and attention.

•We may be unable to successfully expand our international operations and our international expansion plans, if implemented, will subject us to a variety of economic, political, regulatory and other risks.

•The impact of worldwide economic conditions may adversely affect our business, operating results, and financial condition.

•We are subject to a number of legal requirements and other obligations regarding data privacy and security, consumer protection and data protection, and any actual or perceived failure to comply with these requirements or obligations could have an adverse effect on our reputation, business, financial condition and operating results.

•Any significant interruptions, delays or discontinuations in service or disruptions in or unauthorized access to our information technology systems or those of third parties that we utilize in our operations, including those relating to cybersecurity or arising from cyber-attacks, could result in a loss or degradation of service, unauthorized disclosure of data, including subscriber and corporate information, or theft of intellectual property, including digital content assets, which could adversely impact our business.

•The impact of worldwide economic conditions may adversely affect our business, operating results, and financial condition.

5

PART I

Item 1. Business.

Our Mission

With a global mission to aggregate the best in TV, including premium sports, news and entertainment content, through a single app, Fubo aims to transcend the industry’s current TV model.

Overview

We are a sports-first, Pay TV replacement product offering subscribers access to tens of thousands of live sporting events annually, alongside leading news and entertainment content, both live and on demand. Fubo’s platform is designed to empower customers to seamlessly access content through streaming devices and on Smart TVs, mobile phones, tablets, and computers.

Live TV streaming has disrupted the traditional Pay TV model (linear video delivered via cable or satellite providers for a paid subscription), which we refer to as “Pay TV.” This disruption has shifted billions of dollars in subscription and advertising revenue to over-the-top (“OTT”) streaming platforms, as evidenced by the accelerating rate of Pay TV cord-cutting in the United States. Consumers increasingly favor the streaming experience, leading us to believe that advertisers will follow, further shifting dollars away from traditional linear TV advertising towards streaming services. Yet, despite being a growing share of overall consumption, live TV streaming is still a fraction of the size of traditional Pay TV. We believe this creates a significant opportunity for us to capitalize on the cord-cutting movement.

We offer subscribers a live TV streaming service with the option to purchase incremental features, including additional content or enhanced functionality (“Attachments”) best suited to their preferences. Our base plan, Fubo Pro, boasts a broad mix of top Nielsen-ranked channels across sports, news, and entertainment. Our core offering sits on a proprietary technology platform built specifically for live TV and sports viewership, leveraging our first-party data. This enables us to consistently introduce new features and functionalities. Unlike video on demand (VOD)-only services, live TV streaming demands sophisticated infrastructure due to the nuances of regularly refreshing live programming. Notably, our video delivery platform caters to all major sports leagues and entertainment content owners. For example, Apple TV users can enjoy MultiView, allowing them to watch up to four live streams simultaneously. Moreover, we leverage data across the organization to acquire subscriber-preferred content, influence product design and strategy, boost subscriber engagement, and enhance the capabilities and performance of our advertising platform for partners.

Our direct-to-consumer model grants us further insight by capturing billions of data points monthly. This data set drives our continuous innovation, shaping our enhanced user experience, product & content strategy, and differentiated advertising approach. By analyzing this data, we can personalize live and on-demand content discovery in real-time, creating relevant suggestions for each subscriber.

Our growth strategy includes acquiring subscribers who are attracted to our sports offering and can find with us a compelling sports, news, and entertainment viewing alternative to a traditional Pay TV service. We actively engage those subscribers by providing a seamless Pay TV replacement through a personalized easy-to-use streaming product at competitive prices with greater convenience and flexibility than traditional Pay TV providers. We then monetize our audience through subscription fees and our digital advertising offering. In 2022 and 2023, the majority of our revenue was generated from the sale of subscription services and the sale of advertisements in the United States, though the Company also has operations in Canada, Spain and France.

Consistent with our focus on interactivity, we completed the acquisition of Edisn Inc. (“Edisn”), an AI-powered computer vision platform with patent-pending video recognition technologies based in Bangalore, India, in December 2021. With Edisn, we have expanded, and continue to expand, our data science and engineering organization globally, while strengthening our technology capabilities and accelerating innovation. We also acquired Molotov SAS (“Molotov”), a video streaming platform based in Paris, France, in December 2021. With Molotov, we have augmented our technology capabilities, which we believe will enable us to launch our interactive sports and entertainment streaming platform more efficiently on a global scale.

6

Industry Overview

Streaming services have experienced rapid growth in adoption as consumers engage with streaming video and audio through a variety of devices, including connected TVs, mobile phones, and tablets. While traditional Pay TV still accounts for a meaningful share of TV viewing hours for U.S. households, the proportion is declining as customers continue cutting the cord. We believe consumers are increasingly favoring the superior customer experience, competitive pricing, and better value of streaming services.

Sports and news content have been a key driver for Pay TV operators to retain and grow audiences. Historically most streaming subscription services primarily focused on entertainment content offerings, requiring sports fans to, until recently, remain tethered to the Pay TV ecosystem. This positions our offering well to provide a Pay TV replacement service via streaming that also features an enhanced live sports and news viewing experience.

Our Business Model

Our business motto is “come for the sports, stay for the entertainment.” This consists of leveraging sporting events to acquire subscribers at efficient acquisition costs, given the built-in demand for sports. We then leverage our technology and data to drive higher engagement and induce retentive behaviors such as watching content, favoriting channels, recording shows, and increasing discovery through our proprietary machine learning recommendations engine. We monetize our growing base of highly engaged subscribers by driving higher average revenue per user (“ARPU”).

We drive our business model with three core strategies:

•Grow our paid subscriber base

•Optimize our content portfolio, engagement and retention

•Increase monetization through subscription and advertising

Our Offerings

Subscribers

Our live TV streaming platform caters to sports, news, and entertainment fans. With flexible plans and optional "Attachments," users can customize their experience. The base plan, Fubo Pro, boasts over 100+ channels, including top Nielsen-rated networks, and dozens of sports, news, and entertainment options. It also features numerous Regional Sports Networks (RSNs) for in-market games unavailable on national channels. Subscribers can further tailor their experience by adding premium channels and channel packages, or upgrading "Attachments" like Cloud DVR Plus for more storage and Family Share for additional simultaneous streams.

Advertisers

As cord cutting continues and traditional Pay TV viewers decline, advertisers are increasingly allocating their ad budgets to OTT streaming platforms to reach these audiences. We believe our sports-first, live TV streaming platform offers advertisers a growing and valuable live audience, deeply engaged with premium content and unreachable through traditional channels. Moreover, Fubo provides unskippable ad inventory within this high-quality engagement, maximizing exposure. Advertisers further benefit from our innovative ad formats, bridging the gap between traditional Pay TV and the advantages of digital advertising, including measurability, relevancy, and interactivity. We believe this combination delivers a differentiated advertising experience for brands and viewers alike.

Content Providers

Our platform allows content providers to monetize and distribute their content to our highly engaged audience, counteracting the shrinking viewership market share of Pay TV due to cord-cutting. By aggregating a diverse mix of content, we believe Fubo delivers a more compelling and engaging experience for subscribers than providers could offer alone. Furthermore, our data-powered platform generates valuable insights into consumer behavior and preferences, which are increasingly valuable to our content partners.

7

Seasonality

We generate significantly higher levels of revenue and subscriber additions in the third and fourth quarters of the year. This seasonality is driven primarily by an influx of new subscribers at the start of the National Football League and college football. Our operating results may also be affected by the scheduling of major sporting events that do not occur annually, such as the World Cup or Olympic Games, or the cancellation or postponement of sporting events. In addition, we typically see the total number of subscribers on our platform decline from the fourth quarter of the previous year through the first and second quarter of the following year.

Our Growth Strategies

We believe that we are at the early stages of our growth and that we are at an inflection point in the TV industry where streaming has begun to surpass traditional linear Pay TV in several key areas, including content choice, ease of access and use across devices, and cost savings to consumers. We remain committed to our goal of driving sustainable and profitable growth, and we believe we are well-positioned to do this by executing on the following strategies:

•Continue to efficiently grow our subscriber base: As of December 31, 2023, Fubo had approximately 1.618 million paid subscribers in the United States and Canada (“North America” or “NA”) and approximately 406,000 paid subscribers in Spain and France (“Rest of World” or “ROW”), compared to approximately 1.445 million in NA and approximately 420,000 in ROW as of December 31, 2022. We utilize a broad range of subscriber acquisition channels and tactics designed to optimize marketing spend and efficiently acquire and retain subscribers. Our Sales and Marketing expenses relative to total revenues was approximately 15.1% for the year ended December 31, 2023, compared to 18.2% for the year ended December 31, 2022. We will continue to utilize and analyze the data we have collected to help us become more efficient with our marketing campaigns relative to spend.

•Enactment of ARPU expansion efforts: Our NA ARPU was $82.25 and $72.74 for the year ended December 31, 2023 and 2022, respectively. Our ROW ARPU was $6.82 and $6.14 for the year ended December 31, 2023 and 2022, respectively. We drive ARPU expansion through price-increases, attachment sales, and advertising revenue growth. By pricing against content portfolio adjustments, we aim to deliver value through our offerings. Attachments, including channel package add-ons and interactive features, increase our margins by piggybacking on to our base offerings and not meaningfully increasing our cost basis while increasing revenues.

•Further investment in advertising sales team, technology and infrastructure: For the year ended December 31, 2023, Fubo’s advertising revenue was approximately $115.4 million, up from approximately $101.7 million in December 31, 2022. Improvements to our content portfolio, user interface, navigational elements, content merchandising and targeting capabilities, combined with evolutions in customer behavior and growth in our subscriber base, have driven growth of our viewership over time. We are increasingly monetizing this engagement through advertising on the Fubo platform. We intend to continue leveraging our data and analytics to deliver relevant advertising while improving the ability of our advertisers to optimize and measure the results of their campaigns. We have also expanded our direct sales teams to increase the number of advertisers who leverage our platform and continue improving our fill-rates and Cost Per Thousands (“CPMs”).

•Continue to enhance our content portfolio with cost vigilance: Because we have a direct-to-consumer relationship with the ability to analyze all the content that our subscribers consume, we believe we can continue to drive better subscriber experiences. We plan to continue to optimize our content mix to best suit our subscribers’ interests by leveraging our deep understanding of our subscribers through the data captured on the platform, with the goal of expanding unit economics by balancing the aggregation of the best sports and entertainment programming with vigilance around content costs.

•Continue to invest in our technology and data capabilities: We believe our unique combination of technology and content sets us apart. We continue to invest in building a scalable, automated infrastructure specifically designed to fuel subscriber acquisition, strategic content selection, and informed product decisions. We emphasize interactive features that empower users to transform from passive viewers to active participants. Moreover, we believe our integration of the Fubo and Molotov platforms into a single Unified Platform will yield significant cost savings, and increased product development velocity and innovation.

8

•Expand Internationally: Outside of the United States, we currently operate in Canada, Spain and, through our acquisition of Molotov in 2021, France. We believe there remains a significant opportunity to expand internationally.

Intellectual Property

Our intellectual property is an essential element of our business. We rely on a combination of patent, trademark, copyright and other intellectual property laws, confidentiality agreements and license agreements to protect our intellectual property rights. We also license certain third-party technology for use in conjunction with our products.

We believe that our continued success depends on hiring and retaining highly capable and innovative employees, especially as it relates to our engineering base. It is our policy that our employees and independent contractors involved in development are required to sign agreements acknowledging that all inventions, trade secrets, works of authorship, developments and other processes generated by them on our behalf are our property and assigning to us any ownership that they may claim in those works. Despite our precautions, it may be possible for third parties to obtain and use without consent intellectual property that we own or license. Unauthorized use of our intellectual property by third parties, and the expenses incurred in protecting our intellectual property rights, may adversely affect our business.

Patents and Registered Designs

As of December 31, 2023, we had four issued U.S. utility patents, one U.S. utility patent application, five granted foreign utility patents, seventeen foreign utility patent applications, and eighteen granted foreign design registrations in three jurisdictions. The issued U.S. utility patents expire in 2038, the U.S. utility patent application, if granted, will expire in 2041, the granted foreign utility patents will expire on dates ranging from 2033 to 2038, the foreign utility patent applications, if granted, will expire on dates ranging from 2033 to 2041, and the foreign design registrations will expire on dates ranging from 2035 to 2045. Although we actively attempt to utilize patents to protect our technologies, we believe that none of our patents, individually or in the aggregate, are material to our business. We will continue to file and prosecute patent applications when appropriate to attempt to protect our rights in our proprietary technologies. However, there can be no assurance that our patent applications will be approved, that any patents issued will adequately protect our intellectual property, or that such patents will not be challenged by third parties or held to be invalid or unenforceable.

Trademarks

We also rely on several registered and unregistered trademarks to protect our brand. As of December 31, 2023, we had 37 trademarks registered globally. “fuboTV” is a registered trademark in the United States and the European Union ("EU").

Competition

The TV streaming market continues to grow and evolve as more viewers shift from traditional Pay TV to OTT streaming. There is significant competition in the live TV market for users, advertisers, and broadcasters. We principally compete with Pay TV operators, such as Comcast, Cox and Altice, along with other virtual multichannel video programming distributors (“vMVPDs”), such as YouTube TV, Hulu Live and Sling TV. We also compete to a lesser extent with network-operated direct-to-consumer streaming services, such as Peacock, Paramount+, ESPN+, and would expect to compete with the proposed joint venture between The Walt Disney Company ("Disney"), Fox Corporation ("Fox") and Warner Brothers Discovery, Inc. ("WBD") (the “Network JV”), which, if it becomes operational, would operate a new sports streaming service.

We are actively taking steps in response to actions by certain competitors that we believe are harmful to competition within the industry and to consumers. As announced on February 20, 2024, we have filed an antitrust lawsuit against the parties to the Network JV and certain of their affiliates, challenging the formation of the Network JV and their past business practices on antitrust grounds, and seeking injunctive relief to stop the proposed Network JV and other practices, as well as damages. There can be no assurance, however, that we will be successful in this lawsuit. For additional information, please see Part I, Item 1A. “Risk Factors—Risks Related to Our Relationships with Content Providers, Customers and Other Third Parties—If our efforts to attract and retain subscribers are not successful, our business will be adversely affected.” and Part I, Item 3. “Legal Proceedings” in this Annual Report.

9

We compete on various factors to acquire and retain subscribers. These factors include quality and breadth of content offerings, especially within live sports; features of our TV streaming platform; user experience and engagement; brand awareness in the market; and a competitive value proposition. Many users have multiple subscriptions to various Pay TV and streaming services and allocate time and money between them. Thus, while the presence of these competitors in the market has helped to boost consumer awareness of TV streaming, contributing to the growth of the overall market, their resources and brand recognition present substantial competitive challenges.

We also face competition for advertisers, which in part depends on our ability to scale our subscriber base. Providing a large and engaged audience is crucial for advertisers on our live TV streaming platform. In the TV streaming market, the effectiveness of advertisements and return on investments play a pivotal role. As such, we are also competing for advertisers based on the return of ads compared to various other digital advertising platforms, including mobile and web. Additionally, advertisers continue to allocate a large portion of spend to advertise offline. Therefore, we also compete with traditional media platforms such as traditional linear Pay TV and radio. We are increasingly leveraging our data and analytics capabilities to optimize advertisements for both users and advertisers. We need to continue to maintain an appropriate advertising inventory for the growing demand for ads on our platform.

Furthermore, we compete to attract and retain broadcasters. Our ability to license content from broadcasters is dependent on the scale of our user base as well as license terms.

Our People and Human Capital Management

Who We Are

We are a diverse group of individuals, creatives, technologists, analysts and more. Some of us love sports, some binge the news, others prefer rom-coms. But we are united by a common mission — building the world’s leading global live TV streaming platform with the greatest breadth of premium content and interactivity.

As of December 31, 2023, we had approximately 530 employees globally, of which approximately 370 were located in North America and approximately 160 were located in Europe and India. Additionally, we rely on independent contractors and temporary personnel to supplement our workforce from time to time. We have not experienced any work stoppages, and we consider our relationship with our employees to be good. None of our U.S. or Indian employees is represented by a labor union or covered by a collective bargaining agreement. Our French employees are covered by the national collective bargaining agreement for the consulting and engineering activities in France.

Our Values and Talent Development

We view our employees as central to the success of our business and achieving our mission. We onboard new employees with training programs on our values, certain aspects of our business, and important policies, including our Code of Business Conduct. We also value ongoing development and continuous learning, and strive to support and provide enriching opportunities to our employees. Throughout the year we monitor employee engagement and provide periodic training and informational sessions on our business and policies, including security awareness, through a variety of forums, including all-hands meetings, “ask me anything” sessions, and company-wide newsletters. Management uses input collected during these sessions to ensure ongoing awareness of employees’ needs and improve activities aimed to serve our customers. Collectively through these initiatives we aim to keep our employees well-informed and to increase transparency.

Diversity, Equity and Inclusion

We prioritize building a diverse, inclusive, equitable, and empowered team representing a mix of gender, racial and ethnic backgrounds, industries, and levels of experience. We believe the different backgrounds, traditions, views and talents each of our employees brings to Fubo enrich the company as a whole and will help us achieve executional excellence. In 2020, we formed a Diversity, Engagement and Belonging Council, comprised of different team members throughout various levels of the organization, who recommend and help organize diversity and inclusion initiatives within the company. We are committed to creating and maintaining a workplace free from discrimination or harassment on the basis of race, religion, religious creed, color, ethnic or national origin, ancestry, gender, sexual orientation, age, marital status, military service or veteran status, disability, medical condition, or any other status protected by applicable law. Our policies and compliance trainings prohibit such discrimination and harassment, and all our employees are expected to exhibit and promote honest, ethical, and respectful conduct in the workplace.

10

Compensation and Benefits

Our compensation programs and benefits packages are designed to attract, retain and motivate exceptional talent who possess the skills necessary to drive our business objectives, assist in the achievement of our strategic goals and create long-term value for our shareholders. We offer employees compensation packages designed to be competitive that include base salary, and, depending on the role, business function and geographic market, performance-based cash bonuses, commissions, long-term incentive equity, and performance-based equity. We are proud that we have granted equity to the majority of our employees across all levels of the organization as part of their total compensation package. We believe this fosters a stronger sense of ownership and further aligns our employees’ interests with the interest of our shareholders. In addition to our compensation programs, we offer a variety of benefits to our employees, which can include 401(k) plan with matching, health (medical, dental and vision) insurance, life insurance, paid time off, paid parental leave, a referral bonus program and company-sponsored short term and long term disability. We believe that a competitive compensation and benefits program with both short-term and long-term award opportunities, including awards tied to the achievement of meaningful performance metrics, allows us to align employees with shareholder interests.

Health and Safety

We are committed to the health and safety of our employees, and continue to adapt to ever-changing workplace and workforce dynamics. The majority of our employees have adopted a hybrid work schedule (consisting of both in-person work and working from home); however some of our employees continue to work remotely full-time, and, in the long term, we expect some personnel to continue to do so on a regular basis. We are focused on building capabilities to support a variety of work styles where individuals, teams, and our business can be successful. We have invested in programs that help support our employees’ day-to-day wellness needs and goals including access to professional counselors, health coaching and advocacy services. We also maintain a whistleblower hotline through which employees can report health and safety risks.

Government Regulation

Our business and our devices and platform are subject to numerous domestic and foreign laws and regulations covering a wide variety of subject matters. These include general business regulations and laws, as well as regulations and laws specific to providers of Internet-delivered streaming services and Internet-connected devices. New or modified laws and regulations in these areas may have an adverse effect on our business. The costs of compliance with these laws and regulations are high and are likely to increase in the future. We anticipate that several jurisdictions may, over time, impose greater financial and regulatory obligations on us. If we fail to comply with these laws and regulations, we may be subject to significant liabilities and other penalties. Additionally, compliance with these laws and regulations could, individually or in the aggregate, increase our cost of doing business, impact our competitive position relative to our peers, and otherwise have an adverse impact on our operating results. For additional information about the impact of government regulations on our business, see “Risk Factors—Risks Related to Regulation” and “Risk Factors—Risks Related to Privacy, Consumer Protection and Cybersecurity” in Part I, Item 1A in this Annual Report.

Data Protection and Privacy

We are subject to various laws and regulations covering the privacy and protection of users’ data. Because we handle, collect, store, receive, transmit, transfer, and otherwise process certain information, which may include personal information, regarding our users and employees in the ordinary course of business, we are subject to federal, state and foreign laws related to the privacy and protection of such data. These laws and regulations, and their application to our business, are increasingly shifting and expanding. Compliance with these laws and regulations, such as the California Consumer Privacy Act ("CCPA"), as amended by the California Privacy Rights Act ("CPRA"), and the EU General Data Protection Regulation 2016/679 (the “GDPR”) could affect our business, and their potential impact is unknown. Any actual or perceived failure to comply with these laws and regulations may result in investigations, claims and proceedings, regulatory fines or penalties, damages for breach of contract, or orders that require us to change our business practices, including the way we process data.

11

We are also subject to breach notification laws, including the GDPR, in the jurisdictions in which we operate, and we may be subject to litigation and regulatory enforcement actions as a result of any data breach or other unauthorized access to or acquisition or loss of personal information. Any significant change to applicable laws, regulations, interpretations of laws or regulations, or market practices, regarding the processing of personal data, or regarding the manner in which we seek to comply with applicable laws and regulations, could require us to make modifications to our products, services, policies, procedures, notices, and business practices, including potentially material changes. Such changes could potentially have an adverse impact on our business. For additional information about the impact of data protection and privacy regulations on our business, see “Risk Factors—Risks Related to Privacy, Consumer Protection and Cybersecurity” in Part I, Item 1A in this Annual Report.

Corporate Information

We were incorporated in 2009 as a Florida corporation under the name York Entertainment, Inc., and on August 10, 2020, our name was changed to fuboTV Inc. FuboTV Media Inc. (f/k/a fuboTV Inc.) was incorporated in 2014 as a Delaware corporation. Our principal executive offices are located at 1290 Avenue of the Americas, 9th Floor, New York, New York 10104, and our telephone number is (212) 672-0055. Our website address is at https://fubo.tv. Information contained on, or that can be accessed through, our website is not incorporated by reference into this Annual Report, and you should not consider information on our website to be part of this Annual Report.

Available Information

Our internet website address is www.fubo.tv. At our Investor Relations website, ir.fubo.tv, we make available free of charge a variety of information for investors, including our annual report, quarterly reports on Form 10-Q, current reports on Form 8-K and any amendments to those reports, as soon as reasonably practicable after we electronically file that material with or furnish it to the Securities and Exchange Commission (“SEC”). The information found on our website is not part of this or any other report we file with, or furnish to, the SEC.

We announce material information to the public through filings with the SEC, the investor relations page on our website, press releases, our Twitter account (@fuboTV), our Instagram account (@fubotv), our Facebook page (www.facebook.com/fuboTV), our LinkedIn page (www.linkedin.com/company/fubotv/), public conference calls, and webcasts in order to achieve broad, non-exclusionary distribution of information to the public and for complying with our disclosure obligations under Regulation FD. We encourage investors, the media, and others to follow the channels listed above and to review the information disclosed through such channels. Any updates to the list of disclosure channels through which we will announce information will be posted on the investor relations page on our website.

12

Item 1A. Risk Factors.

You should carefully consider the risks and uncertainties described below, together with all of the other information in this Annual Report, including our consolidated financial statements and related notes and the section titled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” If any of the risks actually occur, our business, financial condition, results of operations, and prospects could be adversely affected. In that event, the market price of our common stock could decline, and you could lose part or all of your investment.

This Annual Report also contains forward-looking statements that involve risks and uncertainties. See “Forward-Looking Statements.” Our actual results could differ materially and adversely from those anticipated in these forward-looking statements as a result of certain factors, including those set forth below.

Risks Related to Our Financial Position and Capital Needs

We have incurred operating losses in the past, expect to incur operating losses in the future and may never achieve or maintain profitability.

We have incurred losses since inception. Our net loss on continuing operations for the year ended December 31, 2023 was $293.1 million. We expect that expanding our operations will cause our future operating expenses to increase. If our revenue does not grow at a greater rate than our operating expenses, we will not be able to achieve and maintain profitability. A number of our operating expenses, including expenses related to streaming content obligations, are fixed. If we are not able to either reduce these fixed obligations or other expenses or maintain or grow our revenue, our near-term operating losses may increase. Additionally, we may encounter unforeseen operating or legal expenses, difficulties, complications, delays and other factors that may result in losses in future periods. If our expenses exceed our revenue, we may never achieve or maintain profitability and our business may be harmed.

We may require additional capital to meet our financial obligations and support planned business growth, and this capital might not be available on acceptable terms or at all.

We have made, and intend in the future to make, significant investments to support planned business growth and may require additional funds to respond to business challenges, including the need to develop new features or enhance our existing platform, products and services, expand into additional markets around the world, improve our operating infrastructure or acquire complementary businesses, personnel and technologies. Accordingly, we may need to secure additional funds. If we raise additional funds through future issuances of equity or convertible debt securities, including pursuant to our shelf registration statements on Form S-3, our then existing shareholders could suffer significant dilution, and any new equity securities we issue could have rights, preferences and privileges superior to those of holders of our common stock. Any debt financing we secure could involve restrictive covenants relating to our capital raising activities and other financial and operational matters, which may make it more difficult for us to obtain additional capital and to pursue business opportunities, including potential acquisitions. If we were to violate the restrictive covenants contained in the indenture governing our 2029 Secured Convertible Notes (the “2029 notes indenture”) or in any future document governing our indebtedness, we could incur penalties, increased expenses and an acceleration of the payment terms of our outstanding debt, which could in turn harm our business.

We may not be able to obtain additional financing on terms favorable to us, if at all, due to unfavorable market conditions, including rising interest rates, or otherwise. In addition, the 2029 notes indenture, and the exchange agreement entered into in connection with the issuance of the 2029 Secured Convertible Notes (the “Exchange Agreement), restrict our ability to incur certain indebtedness and issue certain equity securities. If we are unable to obtain adequate financing or financing on terms satisfactory to us when we require it, our ability to support our business growth and to respond to business challenges could be significantly impaired, and our business may be harmed.

In addition, our cash, cash equivalents and restricted cash are maintained at financial institutions in amounts that exceed federally insured limits. In the event of failure of any of the financial institutions where we maintain our cash, cash equivalents and restricted cash, there can be no assurance that we will be able to access uninsured funds in a timely manner or at all, and we may be obligated to seek alternative sources of liquidity.

13

Our revenue is subject to seasonality, and if subscriber behavior during certain seasons falls below our expectations, our business may be harmed.

Seasonal variations in subscriber and marketing behavior significantly affect our business. We have previously experienced, and expect to continue to experience, effects of seasonal trends in subscriber behavior due to the seasonal nature of sports. We generate significantly higher levels of revenue and subscriber additions in the third and fourth quarters of the year, driven primarily by sports leagues, especially the National Football League and college football. Our operating results may also be affected by the scheduling of major sporting events that do not occur annually, such as the World Cup or Olympic Games, or the cancellation or postponement of sporting events. We also typically experience higher advertising sales during the fourth quarter of each calendar year due to greater advertiser demand during the holiday season, but, on the other hand, also typically incur greater marketing expenses as we attempt to attract new subscribers to our platform. In addition, expenditures by advertisers tend to be cyclical and are often discretionary in nature, reflecting overall economic conditions, the economic prospects of specific advertisers or industries, budgeting constraints and buying patterns, and a variety of other factors, many of which are outside our control.

Accordingly, given the seasonal nature of our business, accurate forecasting is critical to our operations. We anticipate that this seasonal impact on revenue is likely to continue, and any shortfall in expected revenue due to macroeconomic conditions, a decline in the effectiveness of our promotional activities, actions by our competitors, or for any other reason, would cause our results of operations to suffer significantly. For example, the COVID-19 pandemic created significant volatility, uncertainty, and economic disruption and, in addition, mounting inflationary cost pressures and potential recession indicators have negatively impacted the global economy. If these factors continue, or worsen, our revenue may be materially impacted. A substantial portion of our expenses are personnel-related and include salaries, stock-based compensation and benefits that are not seasonal in nature. Accordingly, in the event of a revenue shortfall, we would be unable to mitigate the negative impact on margins, at least in the short term, and our business would be harmed.

We might not be able to utilize a significant portion of our net operating loss carryforwards.

As of December 31, 2023, we had federal net operating loss carryforwards of approximately $1,381.0 million, a portion of which will expire at various dates if not used prior to such dates. Under legislation enacted in 2017, informally titled the Tax Cuts and Jobs Act, as modified by the Coronavirus Aid, Relief, and Economic Security (“CARES”) Act, federal net operating losses incurred in 2018 and in future years may be carried forward indefinitely, but the deductibility of such federal net operating losses in tax years beginning after December 31, 2020 is limited. Other limitations may apply for state tax purposes.

In addition, under Section 382 of the Internal Revenue Code of 1986, as amended (the “Code”), and corresponding provisions of state law, if a corporation undergoes an “ownership change,” which is generally defined as a greater than 50% change, by value, in its equity ownership over a three-year period, the corporation’s ability to use its pre-change net operating loss carryforwards to offset its post-change income may be limited. We have experienced ownership changes in the past, and therefore a portion of our net operating loss carryforwards are subject to an annual limitation under Section 382 of the Code. In addition, we may experience ownership changes in the future as a result of subsequent changes in our stock ownership, including as a result of conversions of the 2026 Convertible Notes and 2029 Secured Convertible Notes, some of which may be outside of our control. A past or future ownership change that materially limits our ability to use our historical net operating loss and tax credit carryforwards may harm our future operating results by effectively increasing our future tax obligations.

14

Our financial condition and results of operations could be adversely affected if we do not effectively manage our current or future debt.

As of December 31, 2023, we had $405.4 million of outstanding indebtedness on a consolidated basis which included $397.5 million of 2026 Convertible Notes and other notes outstanding with an aggregate principal of approximately $7.9 million. In January 2024, the Company exchanged 2026 Convertible Notes with an aggregate principal of $205.8 million for 2029 Secured Convertible Notes with an aggregate principal of $177.5 million. Additionally, the terms of the 2029 notes indenture allow for interest payments on the 2029 Secured Convertible Notes to be paid-in-kind. If we choose to pay interest on the 2029 Secured Convertible Notes in kind, the aggregate principal amount of 2029 Secured Convertible Notes outstanding will increase.

Our obligations related to our outstanding or any future indebtedness could adversely affect our ability to take advantage of corporate opportunities, which could adversely affect our business, financial condition, and results of operations, including, but not limited to, the following:

•our ability to obtain any necessary financing in the future for working capital, capital expenditures, debt service requirements, or other purposes may be limited, or financing may be unavailable;

•a substantial portion of our cash flows must be dedicated to the payment of principal and interest on our indebtedness and other obligations and will not be available for use in our business;

•lack of liquidity could limit our flexibility in planning for, or reacting to, changes in our business and the markets in which we operate;

•our debt obligations will make us more vulnerable to changes in general economic conditions and/or a downturn in our business, thereby making it more difficult for us to satisfy our obligations; and

•if we fail to make required debt payments or to comply with other covenants in our debt agreements, we would be in default under the terms of these agreements, which could permit our creditors to accelerate repayment of the debt and could cause cross-defaults under other debt agreements. For example, our failure to repay or refinance our 2026 Convertible Notes upon or prior to maturity may trigger an event of default under our 2029 Secured Convertible Notes.

We may also incur additional indebtedness to meet future financing needs. If we incur any additional debt, the related risks that we and our subsidiaries face could intensify.

Finally, we may in the future be in non-compliance with the terms of certain of our other debt instruments. To the extent we are in non-compliance with the terms of such debt instruments, we may be required to make payments to the holders of such instruments, those holders may be entitled to the issuance of stock by us, and the holders of such stock may be entitled to registration or other investor rights.

15

Servicing our indebtedness will require a significant amount of cash, and we may not have sufficient cash flow from our business to pay our substantial indebtedness.

Our ability to make scheduled payments of the principal and interest when due, or to refinance our borrowings under our debt agreements, will depend on our future performance and our ability to raise further equity financing, which is subject to economic, financial, competitive and other factors beyond our control. Our business may not generate cash flow from operations in the future sufficient to both (i) satisfy our existing and future obligations to our creditors and (ii) allow us to make necessary capital expenditures. If we are unable to generate such cash flow or raise further equity financing, we may be required to adopt one or more alternatives, such as reducing or delaying investments or capital expenditures, selling assets, refinancing or obtaining additional equity capital on terms that may be onerous or highly dilutive. Additionally, the terms of the 2029 notes indenture allow for interest payments on the 2029 Secured Convertible Notes to be paid-in-kind. If we choose to pay interest on the 2029 Secured Convertible Notes in kind, the aggregate principal amount of 2029 Secured Convertible Notes outstanding will increase. We may need or desire to repay, refinance, restructure or defease our existing indebtedness, including prior to its maturity, in one or more transactions, which may involve the payment of cash or the issuance of additional debt or equity securities. There can be no assurance that we will be able to refinance any of our indebtedness on commercially reasonable terms, if at all. Our ability to refinance existing or future indebtedness will depend on the capital markets and our financial condition at such time. In addition, the terms of the 2029 notes indenture and the Exchange Agreement restrict our ability to incur certain indebtedness and issue certain equity securities.

We may not be able to engage in any of these activities or engage in these activities on desirable terms, which could result in a default on our current or future debt agreements.

Our operating results may fluctuate, which makes our results difficult to predict.

Our revenue and operating results could vary significantly from quarter-to-quarter and year-to-year because of a variety of factors, many of which are outside of our control and may not fully reflect the underlying performance of our business. As a result, comparing our operating results on a period-to-period basis may not be meaningful. In addition to other risk factors discussed herein, factors that may contribute to the variability of our quarterly and annual results include:

•our ability to retain and grow our subscriber base, as well as increase engagement among new and existing subscribers;

•our ability to maintain effective pricing practices, in response to the competitive markets in which we operate or other macroeconomic factors, such as inflation or increased taxes;

•the addition or loss of popular content or channels, including our ability to enter into new content deals or negotiate renewals with our content providers on terms that are favorable to us, or at all;

•our ability to effectively manage our growth;

•our ability to attract and retain existing advertisers;

•seasonal, cyclical or other shifts in revenue and expenses;

•our revenue mix;

•the entrance of new competitors or competitive products or services, whether by established or new companies;

•our ability to keep pace with changes in technology and our competitors, and the timing of the launch of new or updated products, content or features;

•interruptions in service, whether or not we are responsible for such interruptions, and any related impact on our reputation;

•our ability to pursue and appropriately time our entry into new geographic or content markets and, if pursued, our management of this expansion;

16

•costs associated with defending any litigation, including intellectual property infringement litigation;

•the impact of general economic conditions on our revenue and expenses; and

•changes in regulations affecting our business.

This variability makes it difficult to forecast our future results with precision and to assess accurately whether increases or decreases are likely to cause quarterly or annual results to exceed or fall short of previously issued guidance. While we assess our quarterly and annual guidance and update such guidance when we think it is appropriate, unanticipated future volatility can cause actual results to vary significantly from our guidance, even where that guidance reflects a range of possible results.

If we fail to effectively manage our growth, our business, operating results, and financial condition may suffer.

We have experienced significant growth rates in both the number of subscribers on our platform and revenue over the last few years. As we grow larger and increase our subscriber base and usage, we expect it will become increasingly difficult to maintain the rate of growth we have experienced.

In addition, our growth to date has placed significant demands on our management and on our operational and financial infrastructure, and we expect these trends to continue in connection with further growth. In order to attain and maintain profitability, we will need to recruit, integrate, and retain skilled and experienced personnel who can demonstrate our value proposition to subscribers, advertisers, and business partners and who can increase the monetization of our platform. Continued growth could also strain our ability to maintain reliable service levels for our customers, effectively monetize the content streamed, develop and improve our operational and financial controls, and recruit, train, and retain highly skilled personnel. If our systems do not evolve to meet the increased demands placed on us by an increasing number of advertisers, we also may be unable to meet our obligations under advertising agreements with respect to the delivery of advertising or other performance obligations. As our operations grow in size, scope, and complexity, we will need to improve and upgrade our systems and infrastructure, which will require significant expenditures and allocation of valuable technical and management resources. If we fail to maintain efficiency and allocate limited resources effectively in our organization as it grows, our business, operating results, and financial condition may suffer.

We have been expanding our operations internationally, and as our international offering evolves, we are managing and adjusting our business to address varied content offerings, consumer customs and practices, in particular those dealing with e-commerce and streaming video, as well as differing legal and regulatory environments.

Risks Related to Our Relationships with Content Providers, Customers and Other Third Parties

The long-term nature of certain of our content commitments may limit our operating flexibility and could adversely affect our liquidity and results of operations.

In connection with licensing streaming content, we typically enter into multi-year agreements with content providers. Given the multiple-year duration, if subscriber acquisition and retention do not meet our expectations, our margins may be adversely impacted. In the past, we had long term programming deals that required minimum license guarantee payments and we failed to make certain of those minimum guarantee payments to certain key programmers. We currently do not have any material programming deals that require minimum license fees in the United States, however, to the extent we fail to make any minimum guarantee payments in the future, if applicable, we may lose access to such content.

We also enter into multi-year commitments for content that we produce, either directly or through third parties, including elements associated with these productions such as non-cancelable commitments under talent agreements. Payment terms for certain content commitments, such as content we directly produce, will typically require more up-front cash payments than other content licenses or arrangements whereby we do not fund the production of such content.

17

To the extent subscriber and/or revenue growth do not meet our expectations, our liquidity and results of operations could be adversely affected as a result of content commitments and payment requirements of certain agreements. In addition, the long-term nature of certain of our commitments may limit our flexibility in planning for or reacting to changes in our business and the market segments in which we operate. If we license and/or produce content that is not favorably received by consumers in a territory, or is unable to be shown in a territory, acquisition and retention may be adversely impacted and given the long-term and fixed cost nature of certain of our content commitments, as well as operational/technical costs tied to those commitments, we may not be able to adjust our content offering quickly and our results of operations may be adversely impacted.

Our results may be adversely affected if long-term content contracts are not renewed on sufficiently favorable terms.

We typically enter into long-term contracts for both the acquisition and the distribution of media content, including contracts for the acquisition of content rights for sporting events and other programs. As these contracts expire, we must renew or renegotiate the contracts, and if we are unable to renew them on acceptable terms, we may lose content rights or distribution rights. Even if these contracts are renewed, the cost of obtaining content rights may increase (or increase at faster rates than our historical experience). Moreover, our ability to renew these contracts on favorable terms may be affected by consolidation in the market for content distribution, the entrance of new participants in the market for distribution of content, the scale of our subscriber base and other factors. With respect to the acquisition of content rights, particularly sports content rights, the impact of these long-term contracts on our results over the term of the contracts depends on a number of factors, including the strength of advertising markets, subscription levels and rates for content, effectiveness of marketing efforts and the size of viewer audiences. There can be no assurance that revenues from content based on these rights will exceed the cost of the rights plus the other costs of producing and distributing the content.

If we fail to obtain or maintain popular content, we may fail to retain existing subscribers and attract new subscribers.

We have invested a significant amount of time to cultivate relationships with our content providers; however, such relationships may not continue to grow or yield further financial results. We must continuously maintain existing relationships and identify and establish new relationships with content providers to provide popular content. In order to remain competitive, we must consistently meet customer demand for popular streaming channels and content, particularly as we enter new markets, including international markets. If we are not successful in maintaining channels on our platform that attract and retain a significant number of subscribers, or if we are not able to do so in a cost-effective manner, our business will be harmed.

We enter into agreements with our content providers, which have varying terms and conditions, including expiration dates. Upon expiration of these agreements, we are required to re-negotiate and renew them in order to continue providing content from these providers on our streaming platform. We have in the past been unable, and in the future may not be able, to reach a satisfactory agreement with certain content providers before our existing agreements have expired. If we are unable to renew such agreements on a timely basis on mutually agreeable terms, we may be required to temporarily or permanently remove certain channels from our streaming platform. The loss of such channels from our streaming platform for any period of time may harm our business, including as a result of customer confusion and/or dissatisfaction regarding the change in programming available on our platform. If we fail to maintain our relationships with the content providers on terms favorable to us, or at all, or if these content providers face problems in delivering their content across our platform, we may lose channel partners or subscribers and our business may be harmed.

If our efforts to attract and retain subscribers are not successful, our business will be adversely affected.

We have experienced significant subscriber growth over the past several years. Our ability to continue to attract subscribers will depend in part on our ability to consistently provide our subscribers with compelling content choices at competitive prices and effectively market our platform. Furthermore, the relative service levels, content offerings, pricing and related features of our competitors may adversely impact our ability to attract and retain subscribers. In addition, many of our subscribers re-join our platform or originate from word-of-mouth referrals from existing subscribers. If our efforts to satisfy our existing subscribers are not successful, we may not be able to attract subscribers, and as a result, our ability to maintain and/or grow our business will be adversely affected.

18

If consumers perceive a reduction in the value of our platform because, for example, we introduce new or adjust existing features, adjust pricing or platform offerings, or change the mix of content in a manner that is not favorably received by them, we may not be able to attract and retain subscribers. Subscribers cancel their subscription for many reasons, including due to a perception that they do not use the platform sufficiently, the need to cut household expenses, the availability of content is unsatisfactory, competitive services provide a better value or experience and customer service issues are not satisfactorily resolved. We must continually add new subscriptions both to replace canceled or expired subscriptions and to grow our business beyond our current subscription base. While we permit multiple subscribers within the same household to share a single account for non-commercial purposes, if account sharing is abused, our ability to add new subscribers may be hindered and our results of operations may be adversely impacted. If we do not grow as expected, given, in particular, that our content costs are largely contracted over several years, we may not be able to adjust our expenditures or increase our (per subscriber) revenues commensurate with the lowered growth rate such that our margins, liquidity and results of operations may be adversely impacted.

Our business, financial condition, and results of operations are also impacted by changes in the distribution strategy by the various content providers on our platform. This also impacts our ability to accurately forecast subscriber growth and revenue. Some of these changes may include the simulcasting and/or exclusive streaming of content, including sporting events that traditionally were only broadcasted on linear Pay TV, on direct-to-consumer (“DTC”) “plus services” at generally lower prices. If current or future content partners refuse to grant our subscribers access to stream certain channels or sporting events, or make their content available on their own DTC platform or our competitors’ platforms, whether exclusively or at more attractive pricing, this could adversely affect our ability to acquire and retain subscribers, which could materially and adversely affect our business, financial condition and results of operation. In addition, if popular local sports programming, which has historically had limited carriage and distribution via regional sports networks, continues to shift to national broadcast networks and as a result continues to become more widely available on competitor platforms, including those that have not previously carried regionalized sports programming, it could adversely impact our ability to acquire this content, or to do so in cost-effective manner, or our ability to compete with current and new competitors.

If we are unable to successfully compete with current and new competitors in both retaining our existing subscribers and attracting new subscribers, our business could be adversely affected. Further, if excessive numbers of subscribers cancel our service, we may be required to incur significantly higher marketing expenditures than we currently anticipate replacing these subscribers with new subscribers.

We are actively taking steps in response to actions by competitors that we believe are harmful to competition within the industry and to consumers. For example, in February 2024, Disney, Fox and WBD announced the proposed formation of the Network JV, a forthcoming sports streaming service. As announced on February 20, 2024, we have filed an antitrust lawsuit against the parties to the Network JV and certain of their affiliates, challenging the formation of the Network JV and their past business practices on antitrust grounds, and seeking injunctive relief to stop the proposed Network JV and other practices, and damages. There can be no assurance, however, that we will be successful in this lawsuit. If we are not successful in obtaining an injunction and defendants are permitted to operate the Network JV, and/or maintain certain business practices, our business, financial condition and results of operations could be materially and adversely affected.

Our agreements with certain distribution partners may contain parity obligations which limit our ability to pursue unique partnerships.

Our agreements with certain distribution partners contain obligations which require us to offer them the same technical features, content, pricing and packages that we make available to our other distribution partners and also require us to provide parity in the marketing of the availability of our application across our distribution partners. These parity obligations may limit our ability to pursue technological innovation or partnerships with individual distribution partners and may limit our capacity to negotiate favorable transactions with different partners or otherwise provide improved products and services. As our technical feature developments progress at varying speeds and at different times with different distribution partners, we currently offer some enhanced technical features on distribution platforms that we do not make available on other distribution platforms, which limits the quality and uniformity of our offering to all consumers across our distribution platforms. In addition, delays in technical developments across our distribution partners puts us at risk of breaching our parity obligations with such distribution platforms, which threatens the certainty of our agreements with distribution partners.

19

If we are unable to maintain an adequate supply of ad inventory on our platform, our business may be harmed.

We may fail to attract content providers that generate sufficient ad content hours on our platform and continue to grow our video ad inventory. Our business model depends on our ability to grow video ad inventory on our platform and sell it to advertisers. We grow ad inventory by adding and retaining content providers on our platform with ad-supported channels that we can monetize. If we are unable to grow and maintain a sufficient supply of quality video advertising inventory at reasonable costs to keep up with demand, our business may be harmed.

We operate in a highly competitive industry, and we compete for advertising revenue with other internet streaming platforms and services, as well as traditional media, such as radio, broadcast, cable and satellite TV and satellite and Internet radio. We may not be successful in maintaining or improving our fill-rates or CPMs.

Our competitors offer content and other advertising mediums that may be more attractive to advertisers than our TV streaming platform. These competitors are often very large and have more advertising experience and financial resources than we do, which may adversely affect our ability to compete for advertisers and may result in lower revenue from advertising. If we are unable to increase our advertising revenue by, among other things, continuing to improve our platform’s data capabilities to further optimize and measure advertisers’ campaigns, increase our advertising inventory and expand our advertising sales team and programmatic capabilities, our business and our growth prospects may be harmed. We may not be able to compete effectively or adapt to any such changes or trends, which would harm our ability to grow our advertising revenue and harm our business.

If content providers refuse to license streaming content or other rights upon terms acceptable to us, our business could be adversely affected.

Our ability to provide our subscribers with content they can watch depends on content providers and other rights holders licensing rights, including distribution rights, to such content and certain related elements thereof, such as the public performance of music contained within the content we distribute. The license periods and the terms and conditions of such licenses vary, and we may be operating outside the terms of some of our current licenses. As content providers develop their own streaming services, they may be unwilling to provide us with access to certain content, including popular series or movies. If the content providers and other rights holders are not or are no longer willing or able to license us content upon terms acceptable to us, our ability to stream content to our subscribers may be adversely affected and/or our costs could increase. Because of these provisions as well as other actions we may take, content available through our service can be withdrawn on short notice. As competition increases, we see the cost of certain programming increase.

Further, if we do not maintain a compelling mix of content, our subscriber acquisition and retention may be adversely affected.

Our content providers impose a number of restrictions on how we distribute and market our products and services, which can adversely affect our business.