UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the Quarterly Period Ended April 29, 2017

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM ______ TO ______

Commission File Number 001-34742

EXPRESS, INC.

(Exact name of registrant as specified in its charter)

Delaware | 26-2828128 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

1 Express Drive Columbus, Ohio | 43230 | |

(Address of principal executive offices) | (Zip Code) | |

Telephone: (614) 474-4001

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | o |

Non-accelerated filer | o (Do not check if a smaller reporting company) | Smaller reporting company | o |

Emerging growth company | o | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The number of outstanding shares of the registrant’s common stock was 78,795,186 as of May 27, 2017.

1

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q ("Quarterly Report") contains forward-looking statements that are subject to risks and uncertainties. All statements other than statements of historical fact included in this Quarterly Report are forward-looking statements. Forward-looking statements give our current expectations and projections relating to our financial condition, results of operations, plans, objectives, future performance, and business. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as "anticipate," "estimate," "expect," "project," "plan," "intend," "believe," 'may," "will," "should," "can have," "likely," and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating or financial performance or other events. For example, all statements we make relating to our estimated and projected costs, expenditures, cash flows, and financial results, our plans and objectives for future operations, growth, initiatives, or strategies, or the expected outcome or impact of pending or threatened litigation are forward-looking statements. All forward-looking statements are subject to risks and uncertainties that may cause actual results to differ materially from those that we expected, including:

External Risks such as:

• | changes in consumer spending and general economic conditions; |

• | customer traffic at malls, shopping centers, and at our stores and online; |

• | competition from other retailers; |

• | our dependence upon independent third parties to manufacture all of our merchandise; |

• | changes in the cost of raw materials, labor, and freight; |

• | supply chain disruption; |

• | difficulties associated with our distribution facilities; |

• | natural disasters, fire and other events that cause business interruption; |

• | our reliance on third parties to provide us with certain key services for our business; |

Strategic Risks such as:

• | our ability to identify and respond to new and changing fashion trends, customer preferences, and other related factors; |

• | fluctuations in our sales, results of operations, and cash levels on a seasonal basis and due to a variety of other factors, including our product offerings relative to customer demand, the mix of merchandise we sell, promotions, and inventory levels; |

• | our dependence on a strong brand image; |

• | our ability to develop and maintain a relevant and reliable omni-channel experience for our customers; |

• | our dependence upon key executive management; |

• | our ability to achieve our strategic objectives, including improving profitability, increasing brand awareness and elevating customer experience, transforming and leveraging information technology systems, and investing in the growth and development of our associates; |

Information Technology Risks such as:

• | the failure or breach of information systems upon which we rely; |

• | our ability to protect our customer data from fraud and theft; |

Financial Risks such as:

• | our substantial lease obligations; |

• | restrictions imposed on us under the terms of our asset-based loan facility |

• | impairment charges on long-lived assets; |

• | claims made against us resulting in litigation or changes in laws and regulations applicable to our business; |

• | our inability to protect our trademarks or other intellectual property rights that may preclude the use of our trademarks or other intellectual property around the world; |

• | changes in tax requirements, results of tax audits, and other factors that may cause fluctuations in our effective tax rate; |

• | our failure to maintain adequate internal controls. |

We derive many of our forward-looking statements from our operating budgets and forecasts, which are based upon many detailed assumptions. While we believe that our assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors, and it is impossible for us to anticipate all factors that could affect our actual results. For a discussion of these risks and other risks and uncertainties that could cause actual results to differ materially from those contained in our forward-looking statements, please refer to "Item 1A. Risk Factors" in our Annual Report on Form 10-K for the year ended January 28, 2017 ("Annual Report"), filed with the Securities and Exchange Commission ("SEC") on March 24, 2017. The forward-looking statements included in this Quarterly Report are made only as of the date hereof. We undertake no obligation to publicly update or revise any forward-looking statement as a result of new information, future events, or otherwise, except as required by law.

2

INDEX

PART I | ||

ITEM 1. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

PART II | ||

ITEM 1. | ||

ITEM 1A. | ||

ITEM 2. | ||

ITEM 3. | ||

ITEM 4. | ||

ITEM 5. | ||

ITEM 6. | ||

3

PART I – FINANCIAL INFORMATION

ITEM 1. | FINANCIAL STATEMENTS. |

EXPRESS, INC.

CONSOLIDATED BALANCE SHEETS

(Amounts in Thousands, Except Per Share Amounts)

(Unaudited)

April 29, 2017 | January 28, 2017 | ||||||

ASSETS | |||||||

CURRENT ASSETS: | |||||||

Cash and cash equivalents | $ | 190,992 | $ | 207,373 | |||

Receivables, net | 16,218 | 15,787 | |||||

Inventories | 287,496 | 241,424 | |||||

Prepaid minimum rent | 31,109 | 31,626 | |||||

Other | 21,785 | 17,923 | |||||

Total current assets | 547,600 | 514,133 | |||||

PROPERTY AND EQUIPMENT | 1,039,467 | 1,029,176 | |||||

Less: accumulated depreciation | (599,126 | ) | (577,890 | ) | |||

Property and equipment, net | 440,341 | 451,286 | |||||

TRADENAME/DOMAIN NAMES/TRADEMARKS | 197,618 | 197,618 | |||||

DEFERRED TAX ASSETS | 7,797 | 7,926 | |||||

OTHER ASSETS | 13,413 | 14,226 | |||||

Total assets | $ | 1,206,769 | $ | 1,185,189 | |||

LIABILITIES AND STOCKHOLDERS’ EQUITY | |||||||

CURRENT LIABILITIES: | |||||||

Accounts payable | $ | 197,751 | $ | 172,668 | |||

Deferred revenue | 25,179 | 29,428 | |||||

Accrued expenses | 112,344 | 80,301 | |||||

Total current liabilities | 335,274 | 282,397 | |||||

DEFERRED LEASE CREDITS | 147,313 | 146,328 | |||||

OTHER LONG-TERM LIABILITIES | 90,910 | 120,777 | |||||

Total liabilities | 573,497 | 549,502 | |||||

COMMITMENTS AND CONTINGENCIES (Note 10) | |||||||

STOCKHOLDERS’ EQUITY: | |||||||

Preferred stock – $0.01 par value; 10,000 shares authorized; no shares issued or outstanding | — | — | |||||

Common stock – $0.01 par value; 500,000 shares authorized; 92,563 shares and 92,063 shares issued at April 29, 2017 and January 28, 2017, respectively, and 78,737 shares and 78,422 shares outstanding at April 29, 2017 and January 28, 2017, respectively | 926 | 921 | |||||

Additional paid-in capital | 189,111 | 185,097 | |||||

Accumulated other comprehensive loss | (4,172 | ) | (3,803 | ) | |||

Retained earnings | 686,184 | 690,715 | |||||

Treasury stock – at average cost; 13,826 shares and 13,641 shares at April 29, 2017 and January 28, 2017, respectively | (238,777 | ) | (237,243 | ) | |||

Total stockholders’ equity | 633,272 | 635,687 | |||||

Total liabilities and stockholders’ equity | $ | 1,206,769 | $ | 1,185,189 | |||

See Notes to Unaudited Consolidated Financial Statements.

4

EXPRESS, INC.

CONSOLIDATED STATEMENTS OF INCOME AND COMPREHENSIVE INCOME

(Amounts in Thousands, Except Per Share Amounts)

(Unaudited)

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

NET SALES | $ | 467,029 | $ | 502,909 | |||

COST OF GOODS SOLD, BUYING AND OCCUPANCY COSTS | 340,031 | 335,161 | |||||

Gross profit | 126,998 | 167,748 | |||||

OPERATING EXPENSES: | |||||||

Selling, general, and administrative expenses | 130,072 | 135,762 | |||||

Restructuring costs | 6,271 | — | |||||

Other operating (income) expense, net | 401 | 165 | |||||

Total operating expenses | 136,744 | 135,927 | |||||

OPERATING (LOSS)/INCOME | (9,746 | ) | 31,821 | ||||

INTEREST EXPENSE, NET | 797 | 11,731 | |||||

OTHER INCOME, NET | (12 | ) | (690 | ) | |||

(LOSS)/INCOME BEFORE INCOME TAXES | (10,531 | ) | 20,780 | ||||

INCOME TAX (BENEFIT)/EXPENSE | (6,000 | ) | 7,898 | ||||

NET (LOSS)/INCOME | $ | (4,531 | ) | $ | 12,882 | ||

OTHER COMPREHENSIVE INCOME: | |||||||

Foreign currency translation (loss) gain | (369 | ) | 1,531 | ||||

COMPREHENSIVE (LOSS)/INCOME | $ | (4,900 | ) | $ | 14,413 | ||

EARNINGS PER SHARE: | |||||||

Basic | $ | (0.06 | ) | $ | 0.16 | ||

Diluted | $ | (0.06 | ) | $ | 0.16 | ||

WEIGHTED AVERAGE SHARES OUTSTANDING: | |||||||

Basic | 78,446 | 79,063 | |||||

Diluted | 78,446 | 79,914 | |||||

See Notes to Unaudited Consolidated Financial Statements.

5

EXPRESS, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(Amounts in Thousands)

(Unaudited)

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

CASH FLOWS FROM OPERATING ACTIVITIES: | |||||||

Net (loss)/income | $ | (4,531 | ) | $ | 12,882 | ||

Adjustments to reconcile net (loss)/income to net cash provided by operating activities: | |||||||

Depreciation and amortization | 22,893 | 16,783 | |||||

Loss on disposal of property and equipment | 403 | 290 | |||||

Impairment charge | 5,512 | — | |||||

Amortization of lease financing obligation discount | — | 11,354 | |||||

Share-based compensation | 4,018 | 4,368 | |||||

Deferred taxes | 1,133 | (235 | ) | ||||

Landlord allowance amortization | (3,126 | ) | (2,138 | ) | |||

Changes in operating assets and liabilities: | |||||||

Receivables, net | (442 | ) | 5,633 | ||||

Inventories | (46,220 | ) | (25,600 | ) | |||

Accounts payable, deferred revenue, and accrued expenses | 20,635 | (42,534 | ) | ||||

Other assets and liabilities | 676 | 3,536 | |||||

Net cash provided by/(used in) operating activities | 951 | (15,661 | ) | ||||

CASH FLOWS FROM INVESTING ACTIVITIES: | |||||||

Capital expenditures | (14,623 | ) | (18,247 | ) | |||

Net cash used in investing activities | (14,623 | ) | (18,247 | ) | |||

CASH FLOWS FROM FINANCING ACTIVITIES: | |||||||

Payments on lease financing obligations | (414 | ) | (389 | ) | |||

Repayments of financing arrangements | (303 | ) | — | ||||

Proceeds from exercise of stock options | — | 2,703 | |||||

Repurchase of common stock under share repurchase program | — | (41,527 | ) | ||||

Repurchase of common stock for tax withholding obligations | (1,534 | ) | (4,340 | ) | |||

Net cash used in financing activities | (2,251 | ) | (43,553 | ) | |||

EFFECT OF EXCHANGE RATE ON CASH | (458 | ) | 1,591 | ||||

NET DECREASE IN CASH AND CASH EQUIVALENTS | (16,381 | ) | (75,870 | ) | |||

CASH AND CASH EQUIVALENTS, Beginning of period | 207,373 | 186,903 | |||||

CASH AND CASH EQUIVALENTS, End of period | $ | 190,992 | $ | 111,033 | |||

See Notes to Unaudited Consolidated Financial Statements.

6

Notes to Unaudited Consolidated Financial Statements

1. Description of Business and Basis of Presentation

Business Description

Express, Inc., together with its subsidiaries ("Express" or the "Company"), is a specialty apparel and accessories retailer of women's and men's merchandise, targeting the 20 to 30 year old customer. Express merchandise is sold through retail and factory outlet stores and the Company's e-commerce website, www.express.com, as well as its mobile app. As of April 29, 2017, Express operated 543 primarily mall-based retail stores in the United States, Canada, and Puerto Rico as well as 109 factory outlet stores. Additionally, as of April 29, 2017, the Company earned revenue from 18 franchise stores in Latin America. These franchise stores are operated by franchisees pursuant to franchise agreements. Under the franchise agreements, the franchisees operate stand-alone Express stores that sell Express-branded apparel and accessories purchased directly from the Company.

On May 4, 2017, Express announced its intention to exit the Canadian market and Express Fashion Apparel Canada Inc. and one of its wholly owned subsidiaries filed for protection (the "Filing") in Canada under the Companies' Creditors Arrangement Act (CCAA) with the Ontario Superior Court of Justice in Toronto. As of the Filing date, Canada retail operations will be deconsolidated from the Company's financial statements. Canadian financial results prior to the Filing will continue to be included in the Company's consolidated financial statements. See Note 12 for additional information.

Fiscal Year

The Company's fiscal year ends on the Saturday closest to January 31. Fiscal years are referred to by the calendar year in which the fiscal year commences. References herein to "2017" and "2016" represent the 53-week period ended February 3, 2018 and the 52-week period ended January 28, 2017. All references herein to "the first quarter of 2017" and "the first quarter of 2016" represent the thirteen weeks ended April 29, 2017 and April 30, 2016, respectively.

Basis of Presentation

The accompanying unaudited Consolidated Financial Statements have been prepared in accordance with generally accepted accounting principles in the United States of America ("GAAP") for interim financial information and therefore do not include all of the information or footnotes required by GAAP for complete financial statements. In the opinion of management, the accompanying unaudited Consolidated Financial Statements reflect all adjustments (which are of a normal recurring nature) necessary to state fairly the financial position, results of operations, and cash flows for the interim periods, but are not necessarily indicative of the results of operations to be anticipated for 2017. Therefore, these statements should be read in conjunction with the Consolidated Financial Statements and Notes thereto for the year ended January 28, 2017, included in the Company's Annual Report on Form 10-K, filed with the SEC on March 24, 2017.

Principles of Consolidation

The unaudited Consolidated Financial Statements include the accounts of Express, Inc. and its wholly-owned subsidiaries. All intercompany transactions and balances have been eliminated in consolidation.

Use of Estimates in the Preparation of Financial Statements

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the unaudited Consolidated Financial Statements and the reported amounts of revenue and expense during the reporting period, as well as the related disclosure of contingent assets and liabilities as of the date of the unaudited Consolidated Financial Statements. Actual results may differ from those estimates. The Company revises its estimates and assumptions as new information becomes available.

Recently Issued Accounting Pronouncements

In May 2014, the Financial Accounting Standards Board ("FASB") issued Accounting Standards Update ("ASU") No. 2014-09, "Revenue from Contracts with Customers (Topic 606)." ASU 2014-09 supersedes the revenue recognition requirements in "Revenue Recognition (Topic 605)," and requires entities to recognize revenue in a way that depicts the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled to in exchange for those goods or services. In August 2015, the FASB issued ASU 2015-14, which defers the effective date of ASU 2014-09 to annual and interim reporting periods beginning after December 15, 2017 with early application permitted for annual and interim reporting periods beginning after December 15, 2016. The Company continues to evaluate the impact that adopting

7

this standard will have on its consolidated financial statements, but currently expects that the adoption will primarily impact the accounting for points earned under the Company's loyalty program and the timing of revenue recognition for e-commerce sales. Neither of these changes is expected to have a material effect on the Company's financial position.

In February 2016, the FASB issued ASU No. 2016-02, "Leases (Topic 842)." ASU 2016-02 requires entities to recognize lease assets and lease liabilities on the balance sheet and to disclose key information about leasing arrangements. Under ASU 2016-02, a lessee should recognize a liability to make lease payments and a right-of-use asset representing its right to use the underlying asset for the lease term on its balance sheet. The new standard is effective for annual and interim periods beginning after December 15, 2018. ASU 2016-02 mandates a modified retrospective transition method with early adoption permitted. The Company continues to evaluate the impact that adopting ASU 2016-02 will have on its consolidated financial statements, but the most significant impact will be to increase assets and liabilities on the consolidated balance sheet by the present value of the Company's leasing obligations, which are primarily related to store leases.

2. Segment Reporting

The Company defines an operating segment on the same basis that it uses to evaluate performance internally. The Company has determined that, together, its President and Chief Executive Officer and its Chief Operating Officer are the Chief Operating Decision Maker, and that there is one operating segment. Therefore, the Company reports results as a single segment, which includes the operation of its Express brick-and-mortar retail and outlet stores, e-commerce operations, and franchise operations.

The following is information regarding the Company's major product categories and sales channels:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands) | |||||||

Apparel | $ | 408,578 | $ | 441,243 | |||

Accessories and other | 46,773 | 52,652 | |||||

Other revenue | 11,678 | 9,014 | |||||

Total net sales | $ | 467,029 | $ | 502,909 | |||

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands) | |||||||

Stores | $ | 357,779 | $ | 416,902 | |||

E-commerce | 97,572 | 76,993 | |||||

Other revenue | 11,678 | 9,014 | |||||

Total net sales | $ | 467,029 | $ | 502,909 | |||

Other revenue consists primarily of sell-off revenue related to mark-out-of-stock inventory sales to third parties, shipping and handling revenue related to e-commerce activity, and revenue from franchise agreements.

Revenue and long-lived assets relating to the Company's international operations for the thirteen weeks ended and as of April 29, 2017 and April 30, 2016, respectively, were not material for any period presented and, therefore, are not reported separately from domestic revenue or long-lived assets.

3. Earnings Per Share

The following table provides a reconciliation between basic and diluted weighted-average shares used to calculate basic and diluted earnings per share:

8

Thirteen Weeks Ended | |||||

April 29, 2017 | April 30, 2016 | ||||

(in thousands) | |||||

Weighted-average shares - basic | 78,446 | 79,063 | |||

Dilutive effect of stock options and restricted stock units | — | 851 | |||

Weighted-average shares - diluted | 78,446 | 79,914 | |||

Equity awards representing 4.4 million shares of common stock were excluded from the computation of diluted earnings per share for the thirteen weeks ended April 29, 2017, as the inclusion of these awards would have been anti-dilutive. Equity awards representing 1.2 million shares of common stock were excluded from the computation of diluted earnings per share for the thirteen weeks ended April 30, 2016, as the inclusion of these awards would have been anti-dilutive.

Additionally, for the thirteen weeks ended April 29, 2017, 1.5 million shares were excluded from the computation of diluted weighted average shares because the number of shares that will ultimately be issued is contingent on the Company's performance compared to pre-established performance goals which have not been achieved as of April 29, 2017.

4. Fair Value Measurements

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. Assets and liabilities measured at fair value are classified using the following hierarchy, which is based upon the transparency of inputs to the valuation as of the measurement date.

Level 1-Valuation is based upon quoted prices (unadjusted) for identical assets or liabilities in active markets.

Level 2-Valuation is based upon quoted prices for similar assets and liabilities in active markets or other inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument.

Level 3-Valuation is based upon other unobservable inputs that are significant to the fair value measurement.

Financial Assets

The following table presents the Company's financial assets measured at fair value on a recurring basis as of April 29, 2017 and January 28, 2017, aggregated by the level in the fair value hierarchy within which those measurements fall.

April 29, 2017 | |||||||||

Level 1 | Level 2 | Level 3 | |||||||

(in thousands) | |||||||||

Money market funds | $ | 155,232 | $ | — | $ | — | |||

January 28, 2017 | |||||||||

Level 1 | Level 2 | Level 3 | |||||||

(in thousands) | |||||||||

Money market funds | $ | 177,551 | $ | — | $ | — | |||

The carrying amounts reflected on the unaudited Consolidated Balance Sheets for cash, cash equivalents, receivables, prepaid expenses, and payables as of April 29, 2017 and January 28, 2017 approximated their fair values.

Non-Financial Assets

The Company's non-financial assets, which include fixtures, equipment, improvements, and intangible assets, are not required to be measured at fair value on a recurring basis. However, if certain triggering events occur indicating the carrying value of these assets may not be recoverable, or annually in the case of indefinite lived intangibles, an impairment test is required. The impairment test requires the Company to estimate the fair value of the assets and compare this to the carrying value of the assets. If the fair value of the asset is less than the carrying value, then an impairment charge is recognized and the non-financial assets are recorded at fair value. The Company estimates the fair value using a discounted cash flow model. Factors used in the evaluation include, but are not limited to, management's plans for future operations, recent operating results, and projected cash flows. During the thirteen weeks ended April 29, 2017, the Company recognized impairment charges of

9

approximately $5.5 million related to its 17 Canadian stores, all of which are now fully impaired. These charges are included in restructuring costs on the unaudited Consolidated Statement of Income. See Note 12 for additional discussion surrounding the exit of Canada. During the thirteen weeks ended April 30, 2016, the Company did not recognize any impairment charges.

5. Intangible Assets

The following table provides the significant components of intangible assets:

April 29, 2017 | |||||||||||

Cost | Accumulated Amortization | Ending Net Balance | |||||||||

(in thousands) | |||||||||||

Tradename/domain names/trademarks | $ | 197,618 | $ | — | $ | 197,618 | |||||

Licensing arrangements | 425 | 233 | 192 | ||||||||

$ | 198,043 | $ | 233 | $ | 197,810 | ||||||

January 28, 2017 | |||||||||||

Cost | Accumulated Amortization | Ending Net Balance | |||||||||

(in thousands) | |||||||||||

Tradename/domain names/trademarks | $ | 197,618 | $ | — | $ | 197,618 | |||||

Licensing arrangements | 425 | 221 | 204 | ||||||||

$ | 198,043 | $ | 221 | $ | 197,822 | ||||||

The Company's tradename, Internet domain names, and trademarks have indefinite lives. Licensing arrangements are amortized over a period of ten years and are included in other assets on the unaudited Consolidated Balance Sheets.

6. Income Taxes

The provision for income taxes is based on a current estimate of the annual effective tax rate adjusted to reflect the impact of discrete items. The Company's effective income tax rate may fluctuate from quarter to quarter as a result of a variety of factors, including changes in the Company's assessment of certain tax contingencies, valuation allowances, changes in tax law, outcomes of administrative audits, the impact of discrete items, and the mix of earnings.

The Company's effective tax rate was 57.0% and 38.0% for the thirteen weeks ended April 29, 2017 and April 30, 2016, respectively. The effective tax rate for the thirteen weeks ended April 29, 2017 reflects $5.0 million of discrete tax benefit related to our exit from Canada as more fully described in Note 12. This consists of a $7.3 million tax benefit related to the write-off of Express’ excess tax basis in its investment in Canada and a $2.3 million tax expense primarily related to an increase in the valuation allowance as a result of asset impairment. This benefit was partially offset by discrete charges of $2.0 million related to a tax shortfall for share-based compensation and $1.2 million for a valuation allowance that was recorded against the deferred tax asset for deferred compensation. The total deferred tax asset for deferred compensation of $11.4 million, less the estimated valuation allowance of $1.2 million, will be realized upon payout to the Non-Qualified Retirement Plan participants as more fully described in Note 13.

7. Lease Financing Obligations

In certain lease arrangements, the Company is involved in the construction of the building. To the extent the Company is involved in the construction of structural improvements or takes construction risk prior to commencement of a lease, it is deemed the owner of the project for accounting purposes. Therefore, the Company records an asset in property and equipment on the unaudited Consolidated Balance Sheets, including any capitalized interest costs, and related liabilities in accrued interest and lease financing obligations in other long-term liabilities on the unaudited Consolidated Balance Sheets, for the replacement cost of the Company's portion of the pre-existing building plus the amount of construction costs incurred by the landlord as of the balance sheet date.

The initial terms of the lease arrangements for which the Company is considered the owner are expected to expire in 2023 and 2030. The net book value of landlord funded construction, replacement cost of pre-existing property, and capitalized interest in property and equipment on the unaudited Consolidated Balance Sheets was $62.9 million and $63.8 million, as of April 29, 2017 and January 28, 2017, respectively. There was also $67.8 million and $68.2 million of lease financing obligations as

10

of April 29, 2017 and January 28, 2017, respectively, in other long-term liabilities on the unaudited Consolidated Balance Sheets.

Rent expense relating to the land is recognized on a straight-line basis over the lease term. The Company does not report rent expense for the portion of the rent payment determined to be related to the buildings which are owned for accounting purposes. Rather, this portion of the rent payment under the lease is recognized as interest expense and a reduction of the lease financing obligations.

In February 2016, the Company amended its lease arrangement with the landlord of the Times Square Flagship store. The amendment provided the landlord with the option to cancel the lease upon sufficient notice through December 31, 2016. The option was never exercised and therefore expired on December 31, 2016. In conjunction with amending the lease, the Company recognized an $11.4 million put option liability and a related offset as a discount on the lease financing obligation. The discount was amortized over the shortest period under which the landlord was able to exercise this option (60 days). This resulted in the full amortization of the $11.4 million discount during the first quarter of 2016. The amortization of the discount was recorded as interest expense. As of April 29, 2017, the fair value of the put option was $8.8 million of which $8.1 million is included within other long-term liabilities on the Consolidated Balance Sheets. This amount will be amortized through interest expense over the remaining lease term.

8. Debt

A summary of the Company's financing activities are as follows:

Revolving Credit Facility

On May 20, 2015, Express Holding, LLC, a wholly-owned subsidiary of the Company ("Express Holding"), and its subsidiaries entered into an Amended and Restated $250.0 million secured Asset-Based Credit Facility ("Revolving Credit Facility"). The expiration date of the facility is May 20, 2020. As of April 29, 2017, there were no borrowings outstanding and approximately $246.8 million available under the Revolving Credit Facility.

The Revolving Credit Facility requires Express Holding and its subsidiaries to maintain a fixed charge coverage ratio of at least 1.0:1.0 if excess availability plus eligible cash collateral is less than 10% of the borrowing base. In addition, the Revolving Credit Facility contains customary covenants and restrictions on Express Holding's and its subsidiaries' activities, including, but not limited to, limitations on the incurrence of additional indebtedness, liens, negative pledges, guarantees, investments, loans, asset sales, mergers, acquisitions, prepayment of other debt, distributions, dividends, the repurchase of capital stock, transactions with affiliates, the ability to change the nature of its business or fiscal year, and permitted business activities. All obligations under the Revolving Credit Facility are guaranteed by Express Holding and its domestic subsidiaries (that are not borrowers) and secured by a lien on, among other assets, substantially all working capital assets including cash, accounts receivable, and inventory, of Express Holding and its domestic subsidiaries.

Letters of Credit

The Company may enter into stand-by letters of credit ("stand-by LCs") on an as-needed basis to secure payment obligations for merchandise purchases and other general and administrative expenses. As of April 29, 2017 and January 28, 2017, outstanding stand-by LCs totaled $3.2 million.

9. Share-Based Compensation

The Company records the fair value of share-based payments to employees in the unaudited Consolidated Statements of Income and Comprehensive Income as compensation expense, net of forfeitures, over the requisite service period.

11

Share-Based Compensation Plans

The following summarizes share-based compensation expense:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands) | |||||||

Restricted stock units | $ | 3,155 | $ | 3,305 | |||

Stock options | 863 | 1,063 | |||||

Total share-based compensation | $ | 4,018 | $ | 4,368 | |||

The stock compensation related income tax benefit recognized by the Company during the thirteen weeks ended April 29, 2017 and April 30, 2016 was $1.9 million and $5.5 million, respectively.

Stock Options

During the thirteen weeks ended April 29, 2017, the Company granted stock options under the Company's Amended and Restated 2010 Incentive Compensation Plan (the "2010 Plan"). Stock options granted in 2017 under the 2010 Plan vest 25% per year over four years or upon reaching retirement eligibility, defined as providing ten years of service and being at least 55 years old. These options have a ten year contractual life. The expense for stock options is recognized using the straight-line attribution method.

The Company's activity with respect to stock options during the thirteen weeks ended April 29, 2017 was as follows:

Number of Shares | Grant Date Weighted Average Exercise Price Per Share | Weighted-Average Remaining Contractual Life (in years) | Aggregate Intrinsic Value | |||||||||

(in thousands, except per share amounts and years) | ||||||||||||

Outstanding, January 28, 2017 | 2,329 | $ | 18.18 | |||||||||

Granted | 493 | $ | 9.42 | |||||||||

Exercised | — | $ | — | |||||||||

Forfeited or expired | (132 | ) | $ | 18.63 | ||||||||

Outstanding, April 29, 2017 | 2,690 | $ | 16.55 | 6.3 | $ | — | ||||||

Expected to vest at April 29, 2017 | 751 | $ | 13.26 | 9.2 | $ | — | ||||||

Exercisable at April 29, 2017 | 1,869 | $ | 18.07 | 5.0 | $ | — | ||||||

The following table provides additional information regarding the Company's stock options:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands, except per share amounts) | |||||||

Weighted average grant date fair value of options granted (per share) | $ | 4.39 | $ | 9.50 | |||

Total intrinsic value of options exercised | $ | — | $ | 536 | |||

As of April 29, 2017, there was approximately $3.6 million of total unrecognized compensation expense related to stock options, which is expected to be recognized over a weighted average period of approximately 2.0 years.

The Company uses the Black-Scholes-Merton option-pricing model to value stock options granted to employees. The Company's determination of the fair value of stock options is affected by the Company's stock price as well as a number of subjective and complex assumptions. These assumptions include the risk-free interest rate, the Company's expected stock price volatility over the term of the award, expected term of the award, and dividend yield.

12

The fair value of stock options was estimated at the grant date using the Black-Scholes-Merton option pricing model with the following weighted-average assumptions:

Thirteen Weeks Ended | |||||

April 29, 2017 | April 30, 2016 | ||||

Risk-free interest rate (1) | 2.27 | % | 1.60 | % | |

Price volatility (2) | 45.53 | % | 43.15 | % | |

Expected term (years) (3) | 6.10 | 6.54 | |||

Dividend yield (4) | — | — | |||

(1) | Represents the yield on U.S. Treasury securities with a term consistent with the expected term of the stock options. |

(2) | Primarily based on the historical volatility of the Company's common stock over a period consistent with the expected term of the stock options. |

(3) | Calculated using the midpoint scenario, which combines historical exercise data with hypothetical exercise data for outstanding options. The Company believes this data currently represents the best estimate of the expected term of granted employee stock options. |

(4) | The Company does not currently plan on paying regular dividends. |

Restricted Stock Units

During the thirteen weeks ended April 29, 2017, the Company granted restricted stock units ("RSUs") under the 2010 Plan, including 0.8 million RSUs with performance conditions. The fair value of RSUs is determined based on the Company's closing stock price on the day prior to the grant date in accordance with the 2010 Plan. The expense for RSUs without performance conditions is recognized using the straight-line attribution method. The expense for RSUs with performance conditions is recognized using the graded vesting method based on the expected achievement of the performance conditions. The RSUs with performance conditions are also subject to time-based vesting. All of the RSUs granted during the thirteen weeks ended April 29, 2017 that are earned based on the achievement of performance criteria will vest on April 15, 2020. RSUs without performance conditions vest ratably over four years.

The Company's activity with respect to RSUs, including awards with performance conditions, for the thirteen weeks ended April 29, 2017 was as follows:

Number of Shares | Grant Date Weighted Average Fair Value Per Share | ||||

(in thousands, except per share amounts) | |||||

Unvested, January 28, 2017 | 1,683 | $ | 17.64 | ||

Granted (1) | 1,970 | $ | 9.42 | ||

Performance Shares Adjustment (2) | (25 | ) | $ | — | |

Vested | (500 | ) | $ | 17.49 | |

Forfeited | (5 | ) | $ | 13.13 | |

Unvested, April 29, 2017 | 3,123 | $ | 12.50 | ||

(1) | Approximately 0.8 million RSUs with three-year performance conditions were granted in the first quarter of 2017. One hundred percent of these RSUs are currently included as granted in the table above. The number of performance-based RSUs that are ultimately earned may vary from 0% to 200% of target depending on the achievement of predefined financial performance targets. |

(2) | Relates to a change in estimate of RSUs with performance conditions granted in 2015. Currently, 80% of the number of shares granted in 2015 are expected to vest based on estimates against predefined financial performance targets. |

The total fair value of RSUs that vested during the thirteen weeks ended April 29, 2017 was $8.7 million. As of April 29, 2017, there was approximately $30.5 million of total unrecognized compensation expense related to unvested RSUs, which is expected to be recognized over a weighted-average period of approximately 2.2 years.

10. Commitments and Contingencies

In a complaint filed on January 31, 2017 in the Superior Court for the State of California for the County of Orange, certain subsidiaries of the Company were named as defendants in a representative action alleging violations of California state wage and hour statutes and other labor standards. The lawsuit seeks unspecified monetary damages and attorneys' fees. Express is

13

vigorously defending these claims. At this time, Express is not able to predict the outcome of this lawsuit or the amount of any loss that may arise from it.

The Company is subject to various other claims and contingencies arising out of the normal course of business. Management believes that the ultimate liability arising from such claims and contingencies, if any, is not likely to have a material adverse effect on the Company's results of operations, financial condition, or cash flows.

11. Investment in Equity Interests

In the second quarter of 2016, the Company made a $10.1 million investment in Homage, LLC, a privately held retail company based in Columbus, Ohio. The non-controlling investment in the entity is being accounted for under the equity method. The investment is included in other assets on the unaudited Consolidated Balance Sheets.

12. Restructuring Costs

In April of 2017, Express made the decision to close all 17 of its retail stores in Canada and discontinue all operations through its Canadian subsidiary, Express Fashion Apparel Canada Inc. (“Express Canada”). In connection with the plan to close all of its Canadian stores, on May 4, 2017, certain of Express, Inc.’s Canadian subsidiaries filed an application with the Ontario Superior Court of Justice (Commercial List) in Toronto (the “Court”) seeking protection for Express, Inc.’s Canadian subsidiaries under the Companies’ Creditors Arrangement Act in Canada (the "Filing") and the appointment of a monitor to oversee the liquidation and wind-down process. Express Canada began conducting store closing liquidation sales in the middle of May with store closures planned to take effect on or around June 15, 2017.

Asset Impairment

As a result of the decision to close the Canadian stores, Express determined that it was more likely than not that the fixed assets associated with the Canadian stores would be sold or otherwise disposed of prior to the end of their useful lives and therefore evaluated these assets for impairment in the first quarter of 2017. As a result of this evaluation, the Company recognized an impairment charge of $5.5 million on the fixed assets in the first quarter of 2017.

Exit Costs

In the first quarter of 2017, in addition to the impairment charges noted above, the Company also incurred professional fees in the amount of $0.8 million. As of May 4, 2017, the date of the Filing, the Company no longer has a controlling interest in the Canadian subsidiaries and therefore it has deconsolidated the Canadian operations from the Company's consolidated financial statements as of such date. The Company expects to record an additional pretax impairment loss as a result of the deconsolidation and other charges, totaling $22 to $28 million. The pre-tax loss on deconsolidation will include the derecognition of the carrying amounts of the Canadian subsidiaries' assets, liabilities and accumulated other comprehensive loss and the recording of the Company's remaining interests at fair value, which is expected to be zero. In regards to other charges, the Company also expects to incur expenses related to claims that may be asserted against it, primarily under guarantees of certain leases. See Note 6 for the income tax impact of the discontinuation of Canadian operations.

13. Retirement Benefits

Certain eligible employees participate in a non-qualified supplemental retirement plan (the “Non-Qualified Plan”) sponsored by the Company. In the first quarter of 2017, the Company elected to terminate the Non-Qualified Plan effective March 31, 2017. Outstanding participant balances are expected to be distributed via lump sum after a 12-month waiting period per IRS regulations regarding distributions from supplemental nonqualified plans. Interest will continue to accrue on outstanding balances until such distributions are made. As a result of this decision, the liability associated with this plan of $29.5 million was reclassified from other long-term liabilities to accrued expenses on the unaudited Consolidated Balance Sheet as of April 29, 2017. The Company continues to sponsor a qualified defined contribution retirement plan for eligible employees.

14

ITEM 2. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS.

The following discussion summarizes the significant factors affecting the consolidated operating results, financial condition, liquidity, and cash flows of the Company as of the dates and for the periods presented below. The following discussion and analysis should be read in conjunction with our Annual Report on Form 10-K for the year ended January 28, 2017 and our unaudited Consolidated Financial Statements and the related notes included in Item 1 of this Quarterly Report. This discussion contains forward-looking statements that are based on the beliefs of our management, as well as assumptions made by, and information currently available to, our management. Actual results could differ materially from those discussed in or implied by forward-looking statements as a result of various factors. See "Forward-Looking Statements."

Overview

Express is a specialty apparel and accessories retailer offering both women's and men's merchandise. We have over 35 years of experience offering a distinct combination of style and quality at an attractive value, targeting women and men between 20 and 30 years old. We offer our customers an assortment of fashionable apparel and accessories to address fashion needs across multiple wearing occasions, including work, casual, jeanswear, and going-out occasions.

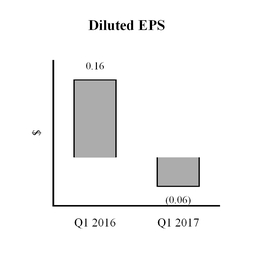

Q1 2017 vs. Q1 2016 |

• Net sales decreased 7% to $467.0 million• Comparable sales decreased 10%• Comparable sales (excluding e-commerce sales) decreased 17%• E-commerce sales increased 27% to $97.6 million• Gross margin percentage decreased 620 basis points• Operating loss decreased $41.5 million to a loss of $9.7 million• Net loss of $4.5 million, a $17.4 million decrease • Diluted earnings per share (EPS) was a loss of $0.06 |

15

The following charts show key performance metrics for the first quarter of 2017 compared to the first quarter of 2016:

Strategic Objectives

We recognize that consumer shopping patterns continue to shift rapidly, with reductions in mall traffic and more purchases being made online, and that the retail environment continues to be highly competitive. We are aggressively adapting our business to capitalize on this shift and remain focused on generating long-term value for our stockholders by improving profitability over time through the following strategic objectives:

Improving Profitability Through A Balanced Approach To Growth. We believe that we can improve profitability over time through a combination of net sales growth and operating margin expansion. We are focused on accomplishing this through (1) increasing the productivity of our existing stores, (2) optimizing our retail store footprint and opening new outlet stores, (3) growing our e-commerce business, and (4) significant cost savings initiatives across our business.

Increasing Brand Awareness And Elevating Our Customer Experience. We are focused on improving the effectiveness of our marketing spend to increase brand awareness and familiarity, customer traffic in-store and online, and purchase intent. In 2017, we will continue to focus on improving our customer experience and improving conversion rates through a relaunch of the Express NEXT loyalty program and the launch of ship-from-store and buy online, pick-up in store capabilities.

Transforming And Leveraging Information Technology Systems. In 2016, we completed several new systems implementations and have now modernized 95% of our portfolio of information technology systems and expect to realize initial benefits from these systems in 2017. By leveraging these new systems, we expect to be able to increase speed to market, conduct planning and allocation with more precision, and introduce new omni-channel capabilities, all of which we believe will allow us to maximize inventory productivity, reduce markdowns, and improve customer experience over time.

16

Investing In The Growth And Development Of Our People. We are committed to ensuring that we continue to attract and retain the talent necessary to achieve our strategic objectives. In 2017, we will remain focused on cultivating a strong corporate culture, based on corporate values, and providing professional development opportunities.

First quarter 2017 update | |

Store Productivity In the first quarter of 2017, comparable sales (excluding e-commerce sales) decreased 17%. We believe this decrease was primarily driven by the following: • Decreased traffic at our stores as a result of shifting consumer shopping patterns which are leading to continued traffic challenges in malls; and• Increased promotional activity at the stores. | Real Estate Optimization As of April 29, 2017, we operated 652 stores, including 109 factory outlet stores. First quarter of 2017 store openings and closures: • Opened five new factory outlet stores in the U.S.• Closed nine retail stores in the U.S.Expectations for the remainder of 2017: • Open 34 factory outlet stores, 20 of which will be converted from existing retail locations.• Close 31 U.S. retail stores, 20 of which will be converted to outlet locations.• Close all 17 Canadian retail stores in the second quarter of 2017 as previously announced. |

E-Commerce In the first quarter of 2017, our e-commerce sales increased 27% compared to the first quarter of 2016. The increase was primarily driven by: • The shift in customer shopping patterns towards e-commerce and mobile; and• Expanded assortment online. E-commerce sales represented 21% of our total net sales in the first quarter of 2017 compared to 15% in the first quarter of 2016. | Progress Against Other Key Initiatives • Cost Savings Initiatives. In 2016, we announced that we believe we have cost savings opportunities of $44 to $54 million that we expect to realize through 2019. We realized $9 million of these savings in 2016 and continue to expect to achieve $20 million in cost savings in 2017. • Increasing Brand Awareness. In the first quarter of 2017 we launched our Spring brand campaign, 'Your Life, Your Dress Code', to elevate and sharpen our brand awareness and positioning by showcasing our multiple wearing occasions for men and women.• Elevating our Customer Experience. We continued the relaunch of our loyalty program by making it easier for customers to enroll and earn rewards with a one-step sign-up process. In addition, we improved the value proposition for private label credit card holders and better aligned the program with our recently upgraded mobile app. |

How We Assess the Performance of Our Business

In assessing the performance of our business, we consider a variety of performance and financial measures. These key measures include net sales, comparable sales, cost of goods sold, buying and occupancy costs, gross profit/gross margin, and selling, general, and administrative expenses. The following table describes and discusses these measures.

Financial Measures | Description | Discussion |

Net Sales | Revenue from the sale of merchandise, less returns and discounts, as well as shipping and handling revenue related to e-commerce, revenue from the rental of our LED sign in Times Square, gift card breakage, and revenue earned from our franchise agreements. | Our business is seasonal, and we have historically realized a higher portion of our net sales in the third and fourth quarters due primarily to the impact of the holiday season. Generally, approximately 45% of our annual net sales occur in the Spring season (first and second quarters) and 55% occur in the Fall season (third and fourth quarters). |

17

Financial Measures | Description | Discussion |

Comparable Sales | Comparable sales is a measure of the amount of sales generated in a period relative to the amount of sales generated in the comparable prior year period. Comparable sales includes: • Sales from stores that were open 12 months or more as of the end of the reporting period, including conversions• E-commerce salesComparable sales excludes: • Sales from stores where the square footage has changed by more than 20% due to remodel or relocation activity• Sales from stores in a phased remodel where a portion of the store is under construction and therefore not productive selling space | Our business and our comparable sales are subject, at certain times, to calendar shifts, which may occur during key selling periods close to holidays such as Easter, Thanksgiving, and Christmas, and regional fluctuations for events such as sales tax holidays. |

Cost of goods sold, buying and occupancy costs | Includes the following: • Direct cost of purchased merchandise• Inventory shrink and other adjustments• Inbound and outbound freight• Merchandising, design, planning and allocation, and manufacturing/production costs• Occupancy costs related to store operations (such as rent and common area maintenance, utilities, and depreciation on assets)• Logistics costs associated with our e-commerce business | Our cost of goods sold typically increases in higher volume quarters because the direct cost of purchased merchandise is tied to sales. The primary drivers of the costs of individual goods are raw materials, labor in the countries where our merchandise is sourced, and logistics costs associated with transporting our merchandise. Buying and occupancy costs related to stores are largely fixed and do not necessarily increase as volume increases. Changes in the mix of products sold may also impact our overall cost of goods sold, buying and occupancy costs. |

Gross Profit/Gross Margin | Gross profit is net sales minus cost of goods sold, buying and occupancy costs. Gross margin measures gross profit as a percentage of net sales. | Gross profit/gross margin is impacted by the price at which we are able to sell our merchandise and the cost of our product. We review our inventory levels on an on-going basis in order to identify slow-moving merchandise and generally use markdowns to clear such merchandise. The timing and level of markdowns are driven primarily by seasonality and customer acceptance of our merchandise and have a direct effect on our gross margin. Any marked down merchandise that is not sold is marked-out-of-stock. We use third-party vendors to dispose of this marked-out-of-stock merchandise. |

Selling, General, and Administrative Expenses | Includes operating costs not included in cost of goods sold, buying and occupancy costs such as: • Payroll and other expenses related to operations at our corporate offices• Store expenses other than occupancy costs• Marketing expenses, including production, mailing, print, and digital advertising costs, among other things | With the exception of store payroll, certain marketing expenses, and incentive compensation, selling, general, and administrative expenses generally do not vary proportionally with net sales. As a result, selling, general, and administrative expenses as a percentage of net sales are usually higher in lower volume quarters and lower in higher volume quarters. |

18

Results of Operations

The First Quarter of 2017 Compared to the First Quarter of 2016

Net Sales

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

Net sales (in thousands) | $ | 467,029 | $ | 502,909 | |||

Comparable sales percentage change | (10 | )% | (3 | )% | |||

Comparable sales percentage change (excluding e-commerce sales) | (17 | )% | (4 | )% | |||

Gross square footage at end of period (in thousands) | 5,612 | 5,557 | |||||

Number of: | |||||||

Stores open at beginning of period | 656 | 653 | |||||

New retail stores | — | — | |||||

New outlet stores | 5 | 4 | |||||

Retail stores converted to outlets | — | — | |||||

Closed stores | (9 | ) | (14 | ) | |||

Stores open at end of period | 652 | 643 | |||||

Net sales decreased approximately $35.9 million compared to the first quarter of 2016. Comparable sales decreased 10% in the first quarter of 2017 compared to the first quarter of 2016. The decrease in comparable sales resulted primarily from a decrease in transactions and in-store average dollar sales per transaction. We attribute these decreases to decreased traffic at our stores due in part to decreases in mall traffic overall. This was partially offset by an increase in e-commerce sales which resulted from the aforementioned shift in consumer shopping patterns and a more expanded assortment online. Non-comparable sales increased $8.1 million, driven primarily by new outlet store openings partially offset by retail store closings.

19

Gross Profit

The following table shows cost of goods sold, buying and occupancy costs, gross profit in dollars, and gross margin percentage for the stated periods:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands, except percentages) | |||||||

Cost of goods sold, buying and occupancy costs | $ | 340,031 | $ | 335,161 | |||

Gross profit | $ | 126,998 | $ | 167,748 | |||

Gross margin percentage | 27.2 | % | 33.4 | % | |||

The 620 basis point decrease in gross margin percentage, or gross profit as a percentage of net sales, in the first quarter of 2017 compared to the first quarter of 2016 was comprised of a 380 basis point decrease in merchandise margin and a 240 basis point increase in buying and occupancy costs as a percentage of net sales. The decrease in merchandise margin was driven by increased promotional activity. The increase in buying and occupancy costs as a percentage of sales was primarily the result of the deleveraging effect of the decrease in sales.

Restructuring Costs

The following table shows restructuring costs for the stated periods:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands, except percentages) | |||||||

Restructuring costs | $ | 6,271 | $ | — | |||

Restructuring costs represent the costs incurred related to the exit of our Canadian business. These costs include $5.5 million in impairment charges and $0.8 million in professional fees during the thirteen weeks ended April 29, 2017.

Selling, General, and Administrative Expenses

The following table shows selling, general, and administrative expenses in dollars and as a percentage of net sales for the stated periods:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands, except percentages) | |||||||

Selling, general, and administrative expenses | $ | 130,072 | $ | 135,762 | |||

Selling, general, and administrative expenses, as a percentage of net sales | 27.9 | % | 27.0 | % | |||

The $5.7 million decrease in selling, general, and administrative expenses in the first quarter of 2017 as compared to the first quarter of 2016 was primarily the result of decreased payroll related expenses of approximately $4.5 million. The reduction in payroll expenses was primarily related to decreases in incentive compensation, store payroll, and performance-based RSU estimates resulting from decreased performance.

Interest Expense, Net

The following table shows interest expense, net in dollars for the stated periods:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands) | |||||||

Interest expense, net | $ | 797 | $ | 11,731 | |||

The $10.9 million decrease in interest expense, net was the result of the amortization of the debt discount related to the lease financing obligation associated with the amendment to our Times Square store lease agreement in the first quarter of 2016.

20

Income Tax Expense

The following table shows income tax expense in dollars for the stated periods:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands) | |||||||

Income tax expense | $ | (6,000 | ) | $ | 7,898 | ||

The effective tax rate was 57.0% for the thirteen weeks ended April 29, 2017 compared to 38.0% for the thirteen weeks ended April 30, 2016. The effective tax rate for the thirteen weeks ended April 29, 2017 includes a tax benefit of approximately $7.3 million related to the write-off of Express’ excess tax basis in its investment in Canada and a $2.3 million tax expense primarily related to an increase in the valuation allowance as a result of asset impairment. Refer to Note 12 of the unaudited Consolidated Financial Statements for additional information. This was partially offset by additional tax expense of $3.2 million related to certain discrete items recognized in the first quarter of 2017. The effective tax rate, excluding discrete items, was 39.2% and 38.6% for the thirteen weeks ended April 29, 2017 and April 30, 2016, respectively.

We anticipate that our effective tax rate, excluding discrete items, will be approximately 40% in 2017.

Non-GAAP Financial Measures

The following table presents adjusted operating (loss)/income, adjusted net (loss)/income and adjusted diluted earnings per share, each non-GAAP financial measures, and operating (loss)/income, net (loss)/income, and diluted earnings per share, the most closely related GAAP measures, for the stated periods. Adjusted operating (loss)/income, adjusted net (loss)/income, and adjusted diluted earnings per share eliminate the impact of the exit of our Canadian business recognized in the first quarter of 2017 and the non-core operating costs incurred in connection with the amendment to the Times Square Flagship store lease in the first quarter of 2016:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands, except per share amounts) | |||||||

Operating (Loss)/Income | $ | (9,746 | ) | $ | 31,821 | ||

Adjusted Operating (Loss)/Income | $ | (3,475 | ) | $ | 31,821 | ||

Net (Loss)/Income | $ | (4,531 | ) | $ | 12,882 | ||

Adjusted Net (Loss)/Income | $ | (5,557 | ) | $ | 19,808 | ||

Diluted Earnings Per Share | $ | (0.06 | ) | $ | 0.16 | ||

Adjusted Diluted Earnings Per Share | $ | (0.07 | ) | $ | 0.25 | ||

We supplement the reporting of our financial information determined under GAAP with certain non-GAAP financial measures: adjusted operating (loss)/income, adjusted net (loss)/income, and adjusted diluted earnings per share. We believe that these non-GAAP measures provide additional useful information to assist stockholders in understanding our financial results and assessing our prospects for future performance. Management believes adjusted operating (loss)/income, adjusted net (loss)/income, and adjusted diluted earnings per share are important indicators of our business performance because they exclude items that may not be indicative of, or are unrelated to, our underlying operating results, and provide a better baseline for analyzing trends in our business. In addition, adjusted diluted earnings per share is used as a performance measure in our executive compensation program for purposes of determining the number of equity awards that are ultimately earned. Because non-GAAP financial measures are not standardized, it may not be possible to compare these financial measures with other companies' non-GAAP financial measures having the same or similar names. These adjusted financial measures should not be considered in isolation or as a substitute for reported operating (loss)/income, reported net (loss)/income, or reported diluted earnings per share. These non-GAAP financial measures reflect an additional way of viewing our operations that, when viewed with our GAAP results and the below reconciliations to the corresponding GAAP financial measures, provide a more complete understanding of our business. We strongly encourage investors and stockholders to review our financial statements and publicly-filed reports in their entirety and not to rely on any single financial measure.

21

The table below reconciles the non-GAAP financial measures, adjusted operating loss, adjusted net loss, and adjusted diluted earnings per share, with the most directly comparable GAAP financial measures, operating loss, net loss, and diluted earnings per share for the first quarter of 2017.

Thirteen Weeks Ended April 29, 2017 | ||||||||||||||

(in thousands, except per share amounts) | Operating Loss | Net Loss | Diluted Earnings per Share | Weighted Average Diluted Shares Outstanding | ||||||||||

Reported GAAP Measure | $ | (9,746 | ) | $ | (4,531 | ) | $ | (0.06 | ) | 78,446 | ||||

Impact of Canadian Exit | 6,271 | 6,271 | 0.08 | |||||||||||

Income Tax Benefit - Canadian Exit | — | (7,297 | ) | (0.09 | ) | |||||||||

Adjusted Non-GAAP Measure | $ | (3,475 | ) | $ | (5,557 | ) | $ | (0.07 | ) | (a) | ||||

(a) Adjusted net loss of $0.07 per diluted share includes $0.04 per diluted share of income tax expense associated with certain discrete tax items.

The table below reconciles the non-GAAP financial measures, adjusted net income and adjusted diluted earnings per share, with the most directly comparable GAAP financial measures, net income and diluted earnings per share for the first quarter of 2016.

Thirteen Weeks Ended April 30, 2016 | ||||||||||

(in thousands, except per share amounts) | Net Income | Diluted Earnings per Share | Weighted Average Diluted Shares Outstanding | |||||||

Reported GAAP Measure | $ | 12,882 | $ | 0.16 | 79,914 | |||||

Interest Expense (a) | 11,354 | 0.14 | ||||||||

Income Tax Benefit (b) | (4,428 | ) | (0.06 | ) | ||||||

Adjusted Non-GAAP Measure | $ | 19,808 | $ | 0.25 | ||||||

(a) | Represents non-core items related to the amendment of the Times Square Flagship store lease discussed in Note 7 of our unaudited Consolidated Financial Statements. |

(b) | Represents the tax impact of the interest expense adjustment at our statutory rate of approximately 39% for the thirteen weeks ended April 30, 2016. |

Liquidity and Capital Resources

A summary of cash provided by or used in operating, investing, and financing activities is shown in the following table:

Thirteen Weeks Ended | |||||||

April 29, 2017 | April 30, 2016 | ||||||

(in thousands) | |||||||

Provided by (used in) operating activities | $ | 951 | $ | (15,661 | ) | ||

Used in investing activities | (14,623 | ) | (18,247 | ) | |||

Used in financing activities | (2,251 | ) | (43,553 | ) | |||

Decrease in cash and cash equivalents | (16,381 | ) | (75,870 | ) | |||

Cash and cash equivalents at end of period | $ | 190,992 | $ | 111,033 | |||

Our business relies on cash flows from operations as our primary source of liquidity, with the majority of those cash flows being generated in the fourth quarter of the year. Our primary operating cash needs are for merchandise inventories, payroll, store rent, and marketing. For the thirteen weeks ended April 29, 2017, our cash flows provided by operating activities were $1.0 million compared to $15.7 million in cash flows used in operating activities for the thirteen weeks ended April 30, 2016. The increase in cash flows from operating activities for the thirteen weeks ended April 29, 2017 was primarily driven by the fact that there was no cash incentive compensation paid in 2017 for the Fall 2016 performance period while the payout of the Fall 2015 incentive compensation accrual occurred during the first quarter of 2016. In addition, lower tax payments were made

22

in the first quarter of 2017 due to a decrease in pretax income in 2016 compared to 2015. These were partially offset by the decreased performance of the business in 2017 and the resulting decline in net income.

In addition to cash flows from operations, we have access to additional liquidity, if needed, through borrowings under our Revolving Credit Facility. As of April 29, 2017, we had $246.8 million available for borrowing under our Revolving Credit Facility. Refer to Note 8 of our unaudited Consolidated Financial Statements for additional information on our Revolving Credit Facility.

We also use cash for capital expenditures and financing transactions. For the thirteen weeks ended April 29, 2017, we had capital expenditures of approximately $14.6 million. These relate primarily to store remodels, new outlet stores, and information technology projects to support our strategic business initiatives. We expect capital expenditures for the remainder of 2017 to be approximately $47 million to $52 million, primarily driven by investments in information technology, new store construction, and store remodels. These capital expenditures do not include the impact of landlord allowances, which are expected to be approximately $5 million to $10 million for the remainder of 2017.

In addition to the cash uses noted previously, we repurchased 2.5 million shares of our common stock under a previously existing stock repurchase program for an aggregate amount equal to $41.5 million, including commissions, during the thirteen weeks ended April 30, 2016.

Our liquidity position benefits from the fact that we generally collect cash from sales to customers the same day or, in the case of credit or debit card transactions, within three to five days of the related sale, and have up to 75 days to pay certain merchandise vendors and 45 days to pay the majority of our non-merchandise vendors.

We believe that cash generated from future operations and the availability of borrowings under our Revolving Credit Facility will be sufficient to meet working capital requirements and anticipated capital expenditures for at least the next 12 months.

Contractual Obligations

Our contractual obligations and other commercial commitments did not change materially between January 28, 2017 and April 29, 2017. For additional information regarding our contractual obligations as of January 28, 2017, see "Management's Discussion and Analysis of Financial Condition and Results of Operations" in our Annual Report on Form 10-K for the year ended January 28, 2017.

Critical Accounting Policies

Management has determined that our most critical accounting policies are those related to revenue recognition, merchandise inventory valuation, long-lived asset valuation, claims and contingencies, and income taxes. We continue to monitor our accounting policies to ensure proper application of current rules and regulations. There have been no significant changes to the policies discussed in our Annual Report on Form 10-K for the year ended January 28, 2017.

ITEM 3. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK.

Quantitative and Qualitative Disclosures About Market Risk

Interest Rate Risk

Our Revolving Credit Facility bears interest at variable rates, however, we did not borrow any amounts under the Revolving Credit Facility during the thirteen weeks ended April 29, 2017. Changes in interest rates are not expected to have a material impact on our future earnings or cash flows given our limited exposure to such changes.

Foreign Currency Exchange Risk

All of our merchandise purchases are denominated in U.S. dollars, therefore we are not exposed to foreign currency exchange risk on these purchases. However, we currently operate 17 stores in Canada, with the functional currency of our Canadian operations being the Canadian dollar. Our Canadian operations have intercompany accounts with our U.S. subsidiaries that eliminate upon consolidation, but the transactions resulting in such accounts do expose us to foreign currency exchange risk. Currently, we do not utilize hedging instruments to mitigate foreign currency exchange risks. As of April 29, 2017, a hypothetical 10% change in the Canadian dollar foreign exchange rate would not have had a material impact on our results of operations.

23

ITEM 4. CONTROLS AND PROCEDURES.

Evaluation of Disclosure Controls and Procedures

We maintain disclosure controls and procedures (as defined in Rule 13a-15(e) and Rule 15d-15(e) promulgated under the Securities Exchange Act of 1934) that are designed to provide reasonable assurance that information required to be disclosed in our Securities Exchange Act of 1934 reports is recorded, processed, summarized, and reported within the time periods specified in the SEC's rules and forms and that such information is accumulated and communicated to our management, including our principal executive officer and principal financial officer, as appropriate, to allow timely decisions regarding required disclosure. In designing and evaluating the disclosure controls and procedures, management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable, and not absolute, assurance of achieving the desired control objectives. In reaching a reasonable level of assurance, management necessarily was required to apply its judgment in evaluating the cost benefit relationship of possible controls and procedures.

Under the supervision and with the participation of our management, including our principal executive officer and principal financial officer, we conducted an evaluation prior to filing this report of our disclosure controls and procedures. Based on this evaluation, our principal executive officer and our principal financial officer concluded that our disclosure controls and procedures were effective at the reasonable assurance level as of April 29, 2017.

Changes in Internal Control Over Financial Reporting

There were no changes in our internal control over financial reporting (as defined in Rules 13a-15(f) and 15d-15(f) under the Securities Exchange Act of 1934) that occurred during the first quarter of 2017 that materially affected, or are reasonably likely to materially affect, our internal control over financial reporting.

PART II - OTHER INFORMATION

ITEM 1. LEGAL PROCEEDINGS.

Information relating to legal proceedings is set forth in Note 10 to our unaudited Consolidated Financial Statements included in Part I of this Quarterly Report and is incorporated herein by reference.

ITEM 1A. | RISK FACTORS. |

In addition to the other information set forth in this Quarterly Report, careful consideration should be given to the risk factors set forth in Part I, Item 1A, Risk Factors, of our Annual Report on Form 10-K for the year ended January 28, 2017, any of which could materially affect our business, operations, financial position, stock price, or future results. The risks described herein and in our Annual Report on Form 10-K for the year ended January 28, 2017, are important to an understanding of the statements made in this Quarterly Report, in our other filings with the SEC, and in any other discussion of our business. These risk factors, which contain forward-looking information, should be read in conjunction with Part I, Item 2, Management’s Discussion and Analysis of Financial Condition and Results of Operations, and the unaudited Consolidated Financial Statements and related notes included in this Quarterly Report.

24

ITEM 2.UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS.

The following table provides information regarding the purchase of shares of our common stock made by or on behalf of the Company or any "affiliated purchaser" as defined in Rule 10b-18(a)(3) under the Securities Exchange Act of 1934, during each month of the quarterly period ended April 29, 2017:

Month | Total Number of Shares Purchased (1) | Average Price Paid per Share | Total Number of Shares Purchased as Part of Publicly Announced Plans or Programs | Approximate Dollar Value of Shares that May Yet be Purchased under the Plans or Programs | ||||||||||

(in thousands, except per share amounts) | ||||||||||||||

January 29, 2017 - February 25, 2017 | — | $ | — | — | $ | — | ||||||||

February 26, 2017 - April 1, 2017 | 2 | $ | 9.49 | — | $ | — | ||||||||

April 2, 2017 - April 29, 2017 | 183 | $ | 8.30 | — | $ | — | ||||||||

Total | 185 | — | ||||||||||||

(1) Includes shares purchased in connection with employee tax withholding obligations under the 2010 Plan.

ITEM 3. | DEFAULTS UPON SENIOR SECURITIES. |

Not applicable.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

ITEM 5. OTHER INFORMATION.

None.

25

ITEM 6. EXHIBITS.

Exhibits. The following exhibits are filed or furnished with this Quarterly Report:

Exhibit Number | Exhibit Description |

10.1+ | Second Amended and Restated Express, Inc. 2010 Incentive Compensation Plan (incorporated by reference to Appendix B to Express, Inc.'s definitive proxy statement on Schedule 14A, filed with the SEC on April 28, 2017). |

31.1* | Certification pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. |

31.2* | Certification pursuant to Section 302 of the Sarbanes-Oxley Act of 2002. |

32.1* | Certification pursuant to Section 906 of the Sarbanes-Oxley Act of 2002. |

101.INS* | XBRL Instance Document. |

101.SCH* | XBRL Taxonomy Extension Schema Document. |

101.CAL* | XBRL Taxonomy Extension Calculation Linkbase Document. |

101.LAB* | XBRL Taxonomy Extension Label Linkbase Document. |

101.PRE* | XBRL Taxonomy Extension Presentation Linkbase Document. |

101.DEF* | XBRL Taxonomy Extension Definition Linkbase Document. |

+ Indicates a management contract or compensatory plan or arrangement. | |

* Filed herewith. | |

26

SIGNATURES