UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

[X] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2018

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

FOR THE TRANSITION PERIOD FROM ____ TO _______

Commission File Number: 000-54286

SURNA INC.

(Exact name of registrant as specified in its charter)

| Nevada | 27-3911608 | |

(State or other jurisdiction of incorporation or organization) |

(I.R.S. Employer Identification No.) |

| 1780 55th Street, Suite C, Boulder, Colorado | 80301 | |

| (Address of principal executive offices) | (Zip code) |

(303) 993-5271

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act:

Title of Each Class Registered

Common stock, par value $0.00001 per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes [ ] No [X].

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes [ ] No [X].

Indicate by check mark whether the issuer (1) has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the last 90 days. Yes [X] No [ ].

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [X] No [ ].

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer, “accelerated filer,” “non-accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | [ ] | Accelerated Filer | [ ] |

| Non-accelerated Filer | [ ] | Smaller Reporting Company | [X] |

| Emerging Growth Company | [ ] | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes [ ] No [X].

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of the last business day of the registrant’s most recently completed second fiscal quarter was approximately $27,700,000 based upon a closing price of $0.17 reported for such date on the OTCMarkets. Common shares held by each executive officer and director and by each person who owns 5% or more of the outstanding common shares have been excluded in that such persons may be deemed to be affiliates.

As of March 19, 2019, the number of outstanding shares of common stock of the registrant was 227,536,638.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s definitive Proxy Statement relating to the 2019 Annual Meeting of Stockholders, to be filed within 120 days after the close of the registrant’s year end, are incorporated by reference into Part III of this Annual Report on Form 10-K.

Surna Inc.

Annual Report on Form 10-K

For Fiscal Year Ended December 31, 2018

Table of Contents

| 2 |

In this Annual Report on Form 10-K, unless otherwise indicated, the “Company”, “we”, “us” or “our” refer to Surna Inc. and, where appropriate, its wholly-owned subsidiary.

CAUTIONARY STATEMENT

This Annual Report on Form 10-K, including “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7, contains forward-looking statements that involve substantial risks and uncertainties. These forward-looking statements are not historical facts, but are based on current management expectations that involve substantial risks, uncertainties, and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed in, or implied by, these forward-looking statements. Forward-looking statements relate to future events or our future financial performance. We generally identify forward-looking statements by terminology such as “may,” “will,” “should,” “expects,” “plans,” “anticipates,” “could,” “intends,” “target,” “projects,” “contemplates,” “believes,” “estimates,” “predicts,” “potential” or “continue” or the negative of these terms or other similar words. All statements, other than statements of historical fact, are statements that could be deemed forward-looking statements including, but not limited to, any projections of revenue, gross profit, earnings or loss, tax provisions, cash flows or other financial items; any statements of the plans, strategies or objectives of management for future operations; any statements regarding current or future macroeconomic or industry-specific trends or events and the impact of those trends and events on us or our financial performance; any statements regarding pending investigations, legal claims or tax disputes; any statements of expectation or belief; and any statements of assumptions underlying any of the foregoing.

These forward-looking statements are subject to known and unknown risks, uncertainties, assumptions and other factors that could cause our actual results of operations, financial condition, liquidity, performance, prospects, opportunities, achievements or industry results, as well as those of the markets we serve or intend to serve, to differ materially from those expressed in, or suggested by, these forward-looking statements. These forward-looking statements are based on assumptions regarding our present and future business strategies and the environment in which we operate. Important factors that could cause those differences include, but are not limited to:

| ● | our business prospects and the prospects of our existing and prospective customers; | |

| ● | the inherent uncertainty of product development; | |

| ● | regulatory, legislative and judicial developments, especially those related to changes in, and the enforcement of, cannabis laws; | |

| ● | increasing competitive pressures in our industry; | |

| ● | our relationships with our customers and suppliers; | |

| ● | general economic conditions or conditions affecting demand for the products offered by us in the markets in which we operate, being less favorable than expected; | |

| ● | changes in our business strategy or development plans, including our expected level of capital expenses and working capital; | |

| ● | our ability to attract and retain qualified personnel; | |

| ● | our ability to raise equity and debt capital to fund our operations and growth strategy, including possible acquisitions; | |

| ● | future revenue being lower than expected; and | |

| ● | our ability to convert our backlog into revenue in a timely manner, or at all; and | |

| ● | our intention not to pay dividends. |

Although we believe that the assumptions on which these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions also could be inaccurate. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this annual report on Form 10-K should not be regarded as a representation by us that our plans and objectives will be achieved. These risks and uncertainties include those described or identified in “Risk Factors” in this Annual Report on Form 10-K. You should not place undue reliance on these forward-looking statements, which apply only as of the date of this Annual Report on Form 10-K. Except as required by the federal securities laws, we undertake no obligation to revise or update any forward-looking statements, whether as a result of new information, future events or otherwise, to reflect events or circumstances occurring after the date of this Annual Report on Form 10-K. The forward-looking statements and projections contained in this Annual Report on Form 10-K are excluded from the safe harbor protection provided by Section 27A of the Securities Act.

| 3 |

Overview

We were incorporated in the State of Nevada on October 15, 2009. On July 25, 2014, we acquired 100% of the membership interests of Hydro Innovations, LLC, a Colorado limited liability company (“Hydro Innovations”), from Stephen and Brandy Keen (the “Keens”). Hydro Innovations was founded by the Keens in Austin, Texas in 2006 to provide agricultural and other growers with the means to maintain a properly controlled indoor cultivation environment with customized, purpose-built cooling equipment, rather than repurposing conventional equipment made for comfort cooling. In 2011, Hydro Innovations delivered its environmental control system to one of the first commercial, state-regulated cannabis cultivation facilities licensed to grow medical cannabis in Arizona.

As state laws regarding the use of cannabis have evolved, we have focused on designing, engineering and manufacturing application-specific environmental control and air sanitation systems for commercial, state- and provincial-regulated indoor cannabis cultivation facilities in the U.S. and Canada. Our engineering and technical team provides energy and water efficient solutions that allow growers to meet the unique demands of a cannabis cultivation environment through precise temperature, humidity, light, and process controls and to satisfy the evolving code and regulatory requirements being imposed at the state, provincial and local levels.

Our objective is to leverage our experience in this sector of the overall cannabis cultivation industry in order to bring value-added climate control solutions to our customers that help improve their overall crop quality and yield as well as optimize the resource efficiency of their controlled environment (i.e., indoor and sealed greenhouses) cultivation facilities. We have been involved in consulting, equipment sales and/or full-scale design for over 800 grow facilities since 2006, making us a trusted resource for indoor environmental design and control management for the cannabis industry.

Our customers include businesses from small cultivation operations to licensed commercial facilities ranging from several thousand to more than 100,000 square feet. We have sold our equipment and systems throughout the U.S. and Canada. Our revenue stream is derived primarily from supplying mechanical engineering services and climate and environmental control equipment to commercial indoor cannabis grow facilities. Although our customers do, we neither produce nor sell cannabis.

We are headquartered in Boulder, Colorado.

Shares of our common stock are traded on the OTCMarkets under the ticker symbol “SRNA.”

Our New Business Model and Strategy

Introduction

Indoor cannabis cultivators are facing the multiple headwinds of high energy costs, increasingly rigorous quality standards and declining cannabis prices. To be competitive, among other things, our customers must develop innovative ways to meet the demands of their business and reduce energy costs, 90% of which is related to their HVAC and lighting systems. That is our focus. We deliver products and services for our customers’ entire facility lifecycles, not just a “one-and-done” environmental control engineering/design and equipment package as part of a facility’s initial construction. We have the advantage of early engagement with our customers at the pre-build and construction phases and the opportunity for building longer-term relationships with our existing customers and their facilities. Going forward, our plan is to capitalize on our existing customer relationships and attempt to become “stickier” to our customers, seeking to generate incremental and recurring revenue.

We have three core assets that we intend to leverage as part of our going forward business strategy. First, we have multi-year relationships with customers and others in the industry. Second, we have specialized engineering know-how and experience gathered from designing environmental control systems for over 200 licensed, commercial cannabis cultivators. Third, we have a line of proprietary environmental control products.

We believe we are well positioned in the industry and, to our knowledge, are the only integrated provider of proprietary environmental control equipment and engineering serving the cannabis space. Further, we believe our employees have more experience than any other mechanical engineering firm serving this industry. Our customers engage us for their environmental and climate control systems because they want experts to design their facilities, and they come to us because of our reputation. We leverage our reputation and know-how against the local contractors and mechanical engineers who collectively constitute our largest competitors.

| 4 |

Our new business plan and strategy is to expand our business with our customers in two ways: (i) by offering a broader range of products and services, and (ii) by addressing a wider range of our customer needs. We believe this plan will take over two years to fully implement. The fiscal objectives of this new strategy are three-fold: (i) diversify our sales by adding recurring, and more consistent and predictable, revenue streams, (ii) achieve revenue growth at a faster rate than operating expenses, and (iii) seek to increase our gross margin by shifting our focus to value-added technology services and proprietary, customized equipment.

If successful, our new product and service initiatives could be “game-changers” for us by providing a more predictable, steady and recurring revenue stream as compared to our traditional one-time engineering/design/equipment projects that, while large in dollar value, were inconsistent and unpredictable and subject to licensing, permitting, funding uncertainties and other factors outside of our control. We believe our new product, service and technology offerings will be attractive to our customers and potentially represent a more consistent revenue stream to the Company.

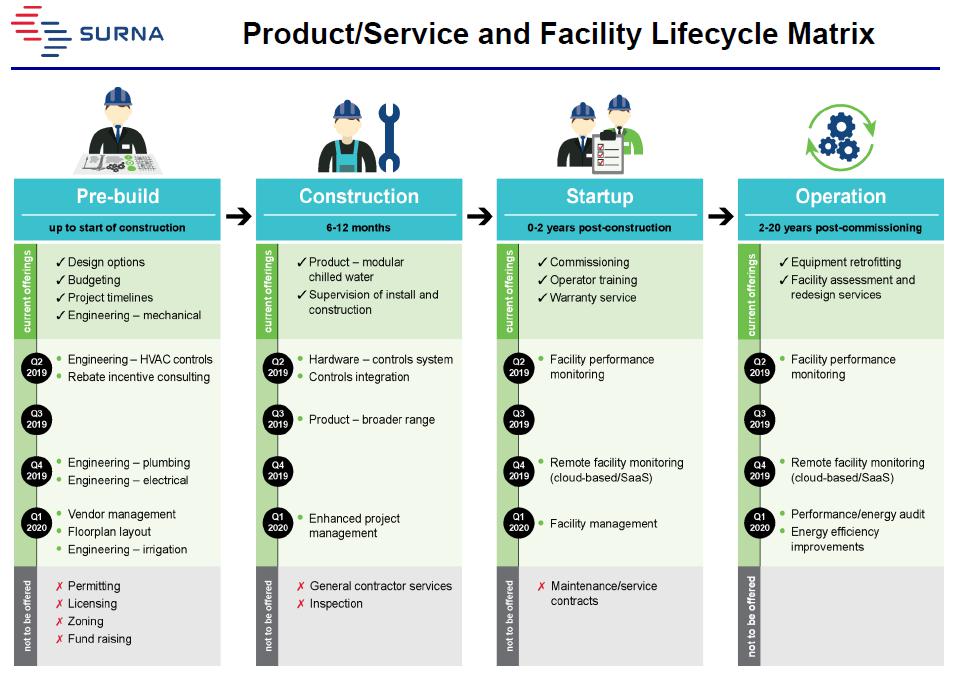

Our strategy to offer more products and services to address the wider range of our customers’ needs is illustrated by the following matrix of product/service depth and facility lifecycle participation.

Cultivation Facility Lifecyle

We previously provided a one-time engineering/design and equipment package primarily in only two of the four principal phases: Pre-build and Construction. As a result, we relinquished opportunities for building longer-term relationships with existing customers and their facilities in the latter two phases: Startup and Operation. Going forward, we will attempt to become “stickier” to our customers by providing products and services across the entire 4-phase facility lifecycle. Each phase of the facility lifecycle has many activities that are opportunities for us, some of which we will pursue. We do not intend to offer products and services in all activities in each phase, but rather we will focus on those that provide value-add to our customers.

Pre-build. This phase includes budgeting, design options, project timelines, floorplan layout, engineering (mechanical, electrical, plumbing, irrigation), vendor management, permitting, licensing, zoning and fund raising. We intend to focus on budgeting, design, floor planning and engineering services.

Construction. This phase includes general contractor services, installation and construction, project management, environmental and climate control products, controls systems, controls integration, contractor management, and inspection. We intend to focus on environmental and climate control products, and control systems.

| 5 |

Startup. This phase includes commissioning, operator training, warranty service, facility management, facility performance monitoring, and maintenance/service contracts. Over time, we expect to be involved to some degree in all of these activities, except maintenance/service contracts.

Operation. This phase includes upgrades and replacements, retrofit/design, energy audit, energy efficiency improvements, and performance audits. Again, over time, we expect to be involved to some degree in all of these activities. We are currently evaluating various strategic partnerships with software, consulting and engineering firms that specialize in utility data collection, rate analysis and rebate programs and provide facility energy auditing and modeling.

Products and Services

We will also offer a deeper range of products and services than the mechanical engineering and modular chilled water systems we historically offered. This includes products and services targeting smaller indoor grow facilities that typically purchase from retailers as well as sealed greenhouse, or hybrid, facilities.

Services: Engineering and Design. Previously, we provided basic engineering and design work, which has steadily improved over the years as we transitioned to larger and more sophisticated commercial projects, and our reputation today reflects this reality. Going forward, we will: (i) expand and emphasize a strong internal mechanical engineering team, with our own professional engineers who have PE (licensed professional engineer) and LEED (leadership in energy and environmental design) credentials, (ii) offer energy modeling to help our customers and enhance our sales closing rate, (iii) produce engineering and design work at industry standards that general contractors expect and need, (iv) develop an engineering, design and audit services program for the expanding retrofit market, which remediates existing grow facilities that suffer from sub-optimal performance, and (v) offer a comprehensive facility management program consisting of facility/performance monitoring, upgrades, warranty, retrofits, energy and efficiency audits, data collection and analytics.

Our technical experience and know-how in designing indoor cannabis cultivation facilities allow us to deliver to our customers practical solutions to complicated problems in three primary areas: (i) precision climate and environmental controls, (ii) energy and water efficiency, and (iii) building code and permitting. Our engineering design typically includes all mechanical components of a climate control system: cooling and heating, dehumidification, ventilation, air sanitation and odor control. We provide load calculations, equipment specifications, and engineered systems drawings for both the cultivation and comfort cooling portions of our customers’ facilities. We also have experience in, or knowledge of, state and local permitting and code compliance for cannabis facilities in states and provinces where cannabis has been legalized for either recreational or medical use or is expected to be legalized, and we provide stamped, engineered drawings in all states and provinces where we operate.

Our competitive advantages are our experience and reputation. Since 2006, we have been continuously improving our facility designs which we believe distinguishes us from our competition, including local heating, ventilation and air conditioning (“HVAC”) contractors, traditional HVAC design consultants, and others who may lack our cannabis-specific expertise. Indoor sealed grow facilities present a very difficult mechanical engineering challenge, and traditional mechanical engineers, without our cannabis experience, are typically unfamiliar with the precise climate and air control requirements needed for such facilities. As important, they may be unable to effectively navigate the local code and permitting rules which did not contemplate cannabis cultivation facilities when enacted. With our engineering design resources and experience, we are able to provide a code-compliant mechanical plan set in any state or province by collaborating with local regulators and our customers to come up with creative solutions that not only meet the intent of the local codes but also address concerns about the growing energy and resource usage of these facilities.

Energy use is, and will continue to be, a primary concern for indoor cultivators and regulators. According to industry sources, legal cannabis cultivation in the U.S. consumed an estimated 1.1 million megawatt hours (MWh) of electricity-based energy in 2017, enough to power 92,500 homes for a year. This consumption is expected to increase 162% from 2017 to 2022. The biggest components are HVAC and lighting which comprise approximately 50% and 40%, respectively, of a facility’s energy use. Unsurprisingly, after labor, energy costs represent the second highest operating cost for indoor cultivators.

As a result, licensed producers are adopting practices to maximize energy efficiency and thereby reduce operating costs, which will become even more important as the industry matures and wholesale prices decline. These practices include water efficiency, LED lighting, and renewable energy alternatives. Sealed greenhouses, or hybrid facilities—which are insulated for energy efficiency and combine natural light with the use of artificial lights—also provide a more economical way to grow cannabis compared to indoor production. But regardless of whether indoor or a hybrid facility is the grow medium, precise environmental controls are required to deliver consistent product quality and yield. We are currently evaluating possible strategic partnerships with greenhouse facility providers that are seeking an environmental controls partner for this specific facility application.

| 6 |

We believe the right solution for our cultivation customers must provide tight temperature/humidity control, reduced fungus, pollen, pesticide and insect contamination risk (“bio-security”), minimized regulatory compliance risk, and lower maintenance complexity, costs and downtime. Our bio-security program uses a combination of a sealed facility and our customized approaches to air sterilization to maintain facility standards while destroying harmful airborne microbes without the production of byproducts. Additionally, our ductless modular chilled water systems using fan coil units within each grow room, isolate the air and potential contaminants within each room, while taking advantage of the energy efficiencies and redundancies offered by such systems. Our experience has shown that our precision environmental controls can reduce the reliance on the use of harmful pesticides and fungicides. We also believe our experience in the tightly regulated Canadian market where pharmaceutical-like standards (including Good Manufacturing Practice standards) exist for filtration, air quality and post-harvest plant quality also gives us an advantage over our competitors, especially as product quality testing regulations continue to be enacted by state, provincial and local agencies.

These are perspectives that help conceptualize the complexity of the environmental controls systems that need to be deployed by indoor cultivators:

| ● | Lighting. Lighting demand is 70 times more energy intensive than commercial office buildings. This lighting intensity creates heat, which when combined with plant transpiration to create humidity, creates the need for dehumidification and corresponding additional energy demand. Further complicating matters, lighting schedules and density must be adjusted for the clone, vegetative and flowering stages of cannabis cultivation, and associated variances in watering rates and temperature and humidity targets, which are usually adjusted based on photoperiod. | |

| ● | HVAC. HVAC energy use is driven by the need to remove the heat emitted from lighting and the moisture released during the plant’s evapotranspiration process, coupled with air circulation and odor and contaminant filtration requirements. | |

| ● | Legacy Systems. Mechanical systems are often designed and/or installed poorly, which can increase energy consumption by up to 50%. Reasons include: (i) unlicensed cultivators deploying HVAC systems without an understanding of how HVAC control the growing environment, (ii) cultivators failing to understand the criticality of proper installation, commissioning and servicing of the equipment, even if properly designed, (iii) HVAC systems selected without understanding the interrelationship between sensible (cooling) and latent (moisture) factors, and (iv) most HVAC systems are designed for buildings for humans, not plants. | |

| ● | High Value Crop. For an indoor 10,000-square foot plant canopy facility, and assuming a wholesale price of $1,500 per pound, a single complete cannabis crop loss (out of a typical five harvests annually) could mean lost revenue of between $600,000 to $1,800,000, with the variance depending on the cultivator’s yield efficiency, which we estimate ranges from one to three pounds per 25 square feet of plant canopy. |

New technologies and applications, coupled with emerging cultivation techniques, are providing opportunities for increased efficiency, which we are positioned to deliver to our customers. Our engineering and technical sales team, which currently consists of 11 people, is fully qualified and committed to delivering energy and resource efficient solutions to commercial cultivators. Leveraging their technical competence, and our customers’ increasing focus on energy efficiency, quality and yield, we intend to offer retrofit/design, energy audit, energy efficiency improvement, and performance audit services.

Products: Environmental Control Systems. Previously, we primarily sold modular chilled water systems. In the future, we will: (i) expand our product offering to include other HVAC solutions, such as custom air handling units, split systems, packaged roof-top units, self-contained and complex water chilled systems, (ii) complete the development of a branded, proprietary controls and monitoring offering (consisting of sensors, controllers, software, monitoring and a user interface) with the goal of eventually generating a recurring revenue stream, (iii) upgrade our proprietary equipment lines of fan coils, dehumidifiers, and chillers, and (iv) source customized, application-specific odor control and air sanitation products.

We believe we are a leading company in North America supplying a complete product line for environmental control and air sanitation systems for the indoor cannabis cultivation market. Since 2006, we have made it our mission to continuously expand our product line and improve the functionality of our equipment. Because of our market experience, we have gained valuable feedback and design insights from our customers, and we continue to innovate and respond as cultivation facilities have increased in both size and complexity. This experience positions us well to offer other HVAC solutions, beyond our traditional modular chilled water systems, to meet the diverse needs of our expanding customer base.

| 7 |

Specific Initiatives in Progress

Our execution plan consists of a series of inter-related initiatives, including: (i) leveraging our strong brand name, (ii) positioning and messaging “Surna as the expert” in environmental controls management; (iii) evaluating first-generation grow facilities as prospects for broader service and product offerings or retrofit work; and (iv) developing a corresponding marketing/service/product plan to address facility lifecycle revenue opportunities. The following are examples of specific product and service initiatives that we are already pursuing or assessing:

New Products and Services. With our engineering know-how, we have the internal resources to develop and offer more environmental control solutions, help more customers and expand our market reach without incurring significant incremental costs. We also completed a full review of our major equipment and hardware lines and have developed a line-up of new, more efficient and proprietary products that we will be rolling out over the next 18 months. We designed these products to meet the increasing demands of our customers.

We recently shipped various configurations of our new fan coil units to two projects with three more under contract. These Surna-branded models offer greater efficiency, design flexibility and control for growers using modular chilled water systems. Our proprietary products, such as our new fan coils, cannot be sourced elsewhere and this gives us greater pricing leverage, which we expect will result in increased margins.

During the second quarter of 2019, we are also planning to roll-out two standard-sized and custom air handler products, which will allow us to meet our customer needs in situations where a ducted air handler is the preferred solution as opposed to the ductless systems that we sell today.

We expect to be able to offer a utility rebate consulting service, beginning the second quarter of 2019, to help our new build customers obtain utility rebates. While this service is not expected to generate significant revenue, it should help us sell our environmental controls systems because our customers will be able to use these rebates to offset some of their capital costs.

We are also offering our new proprietary controls systems product to all new prospects.

Retrofit Market. While hundreds of new indoor cannabis cultivation facilities continue to be built every year, the installed base of first-generation cultivation facilities in the U.S. and Canada has grown into the thousands. Currently, we estimate there are over 3,000 existing cultivation facilities with approximately 8,000 legal cultivation licenses issued throughout the U.S. alone. As discussed above, many of these facilities have environmental control systems that control temperature, humidity, vapor pressure deficit, and CO2, but were designed by mechanical engineers who lacked cannabis application-specific expertise, which is precisely what we have. Some of these facilities are now facing serious operational challenges maintaining the required indoor growing conditions, which may lead to large dollar crop loss, uneven product consistency and quality, and reduced yields. The industry is beginning to recognize the need for our specialized know-how and experience, and we plan to initiate a targeted outreach strategy to the operators of these first-generation facilities. Our facility retrofit projects present an expanded market opportunity for us beyond our typical new facility projects, which carry uncertainties associated with prospect identification, licensing, permitting and funding.

We recently completed a retrofit consulting project—the first of its kind for us—for a large, multi-facility cultivator, and thereafter received a $1,000,000+ order to supply equipment to several of their cultivation facilities that have been operating ineffectively. This order is expected to be fulfilled, and the revenue recognized, in the second or third quarter of 2019.

By the third quarter of 2019, we expect to further refine our retrofit offering for first-generation grow facilities. We are internally developing a facility assessment, analysis and consulting service to assist existing facilities in solving their environmental controls challenges.

Sensors, Controls and Automation Business. In late 2018, we decided to focus our next major product initiative in the sensors, controls and automation (“SCA”) market. This is an important initiative for us for several reasons, from tactical to strategic. Cultivation facilities must have SCA to operate their HVAC equipment. In simple form, SCA is the thermostat in the room, with the occupant selecting the desired temperature set point, the wall thermostat (Sensor) detecting the actual temperature, and when the space temperature deviates from the desired set point the thermostat (Control) commands the furnace or air-conditioner to supply heated or cooled air to bring the room temperature back to the set point. In the case of the cultivation facilities that we serve, there are more environmental conditions to monitor and control (such as temperature, relative humidity, CO2, lighting, system status, and more) than in a typical residential home.

Indoor cannabis growers also need to vary the environmental conditions depending on stage of plant growth (i.e., clone, vegetative and flowering stages of cannabis cultivation), time of day, and plant maturity. In a cultivation facility the desired conditions change many times during the plant’s growth cycle and even within a day, and this is most easily accomplished with a programmable environmental control system (Automation), not unlike a simple programmable thermostat in a home.

| 8 |

We have entered this business to satisfy our customer’s needs that we did not previously address and that historically was provided by third-party controls contractors. Our entry into the SCA market helps both our customer’s and our business. We are also advantageously positioned to offer SCA products because we will be one of the few mechanical systems providers in the market to offer both a branded, proprietary HVAC equipment package as well as a branded SCA product line. Our customers benefit because they are saved the extra work of finding and engaging a controls contractor, allowing them to get their facility up and running more quickly by taking one decision off the table and thereby establishing a single point of responsibility for controls implementation. We are also in a strong position to provide SCA because we know our proprietary equipment better than anyone, thereby ensuring smooth integration with our equipment products with no work scope shortcomings. Longer term, our customers will benefit by having us remotely monitor the status of the HVAC equipment in the facility, thereby avoiding potential catastrophic problems, up to and including total crop loss, as well as using artificial intelligence (AI) to aggregate environment and growing data for our customers to optimize energy use, operating efficiency, and product quality and yield.

From a tactical perspective, with limited incremental selling costs, our current sales team is positioned to offer our SCA package to nearly every prospect since every cultivation facility must have SCA technology. We believe this technology value-added solution gives us an opportunity to achieve incremental project revenue at margins above those of our traditional equipment product lines. Strategically, through our SCA package, we are also able to deepen our ongoing relationship with the customer which positions us for a long-term customer relationship by tethering us to the customer through a controls interface (dashboard) to their facility. Additionally, it positions us as a broad range provider of environmental control products and facility management services for the total lifecycle of the cultivation facility. While there are several other total controls systems providers, we believe that our industry know-how, experience and reputation will give us a compelling and competitive SCA offering.

We will sell Surna-branded precision sensors to measure temperature, humidity, and CO2 levels, which are more accurate than typical HVAC sensors and are able to report within tighter tolerance levels. Our controllers will be purpose-built computers programmed by us to ensure our industrial environmental control equipment follows the engineered sequences of operation to obtain desired setpoints. Our sensors connect to our branded controllers through wires installed in the facility, and similarly they are wired to our HVAC equipment (e.g., chillers, fan coils and dehumidifiers) to direct these pieces of equipment. The controllers also provide a user interface on a screen so that they can be programmed and controlled to achieve the customer’s environmental objectives, and the cultivator may also assess this data and react to alerts remotely.

We will be launching our SCA offering on April 2, 2019 at the Technology Pavilion of the Cannabis Conference in Las Vegas. Similar to the timing of our equipment offering, completion of the SCA portion of our sales contract will be subject to factors beyond our control and may take between six months to two years to be fully deployed following contract execution. While we have no project contracts that include our SCA offerings at this time, we have begun budgeting and quoting SCA systems with existing prospects and have recently presented quotes to about 10 potential customers. We also have a beta-site customer that has agreed to install our SCA products at one of their cultivation facilities.

Beginning in the second half of 2019, we believe that we will be able to sell our SCA package in at least 25% of our engineering/design/equipment projects, with that percentage increasing over time. More specifically, we hope to complete the installation of our branded SCA product in at least four projects in 2019. Additionally, our SCA package can be sold to most existing facilities on a retrofit basis.

One-off Strategic Alliances. We are also in the process of identifying and assessing one-off strategic alliances (e.g., joint ventures, co-marketing, distribution) that are low cost/low risk, easy to implement and execute, can leverage our brand recognition in the cannabis space, expand the offerings that our sales team can present to our past, present and future commercial cannabis cultivators and, most importantly, generate additional revenues and margins, with little incremental costs. We are currently in preliminary discussion with several potential strategic partners that offer a wide range of complimentary products and services, such as energy-efficient lighting, processing equipment, and cloud-based data aggregation and Artificial Intelligence platforms, which we can refer our customers because we are engaged at the early Pre-build phase.

There can be no assurance that we will be able to successfully execute any of these initiatives, or identify, test and develop new and improved products or services, or that such new products or services will generate revenue or profitability at the levels we expect. At this time, our efforts will be primarily focused on working with current and new strategic partners to jointly develop new and improved products and services with cannabis-specific applications, as opposed to seeking acquisitions.

| 9 |

Marketing

New Construction Market Opportunities Follow Legislation

The demand for our environmental control systems currently is primarily driven by the construction of new cannabis cultivation facilities in the U.S. and Canada. New construction activity is, in turn, driven by state legislation approving either medical or recreational cannabis use. Recent regulatory changes involving medical and/or recreational cannabis use in various jurisdictions, such as California, Michigan, Oklahoma, Utah, Missouri and Canada, tend to be a leading indicator for the granting of licenses for new facility construction. As more new cultivation facilities become licensed, we in turn have an expanded set of potential customers that might buy our environmental control systems. However, since both medical and recreational cannabis use remains prohibited under U.S. federal law, uncertainty continues and tends to unfavorably impact the development and financing of new cannabis cultivation facilities in the U.S.

| ● | In the U.S., a total of 33 states (and the District of Columbia) have legalized the medical use of cannabis for over 60 qualifying conditions. Following last year’s mid-term elections, 10 states (and D.C.), with more than 50% of the U.S. population, have legalized access to cannabis for recreational use. With increasing consumer acceptance of cannabis and the growth of the industry as a whole, we believe the number of states that allow cannabis use is set to jump even higher in 2019. Consider the following data gathered from various industry sources and publications: In the U.S., over 24 million persons, or 9.9% of adults age 18 and over consume cannabis regularly, and 115 million persons (or 48%) report having consumed it at some point in their lifetimes. | |

| ● | In states where cannabis is currently legal, sales of medical and recreational cannabis are forecast to grow from $12.9 billion in 2019 to $26.3 billion in 2025. | |

| ● | There were 2.4 million registered U.S. medical cannabis patients in 2018, up 71% since 2014. |

During the year ended December 31, 2018, we booked sales orders for 32 new build projects, each with a contract value over $100,000, which we refer to as commercial-scale projects. This compares to 20 and 18 commercial-scale projects booked for the years ended December 31, 2017 and 2016, respectively. The California and Canadian markets continued to be strong in 2018. Despite our increased bookings for new commercial-scale projects in 2018, the timing for completion of these projects is largely dependent on customer-centric factors—outside of our control—such as industry uncertainty, project financing concerns, and the licensing and qualification of our prospective customers. Further, the increased complexity and size of our new projects also impacts the timing of completion, with larger projects typically taking more time to complete.

In 2018, the average contract value for our commercial-scale project bookings was $408,000 compared to $332,000 for 2017. During 2018, we also booked sales orders with a large, multi-state customer that has put on hold two projects in states where the current market conditions, including wholesale cannabis prices, are not favorable. We estimate that these two projects will not be completed within the next 24 months, and it is possible that they may be abandoned by our customer.

The following table sets forth our commercial-scale project bookings, based on the year the contract was executed and we received an initial deposit, by country/state.

| Number of New Commercial-Scale Project Bookings | ||||||||||||

| 2018 | 2017 | 2016 | ||||||||||

| Canada | 13 | 7 | 1 | |||||||||

| California | 6 | 1 | 3 | |||||||||

| Colorado | - | 2 | 3 | |||||||||

| Arizona | - | 3 | 1 | |||||||||

| Oregon | - | 2 | 2 | |||||||||

| Washington | 3 | 1 | 3 | |||||||||

| Massachusetts | 1 | - | - | |||||||||

| Ohio | 1 | - | - | |||||||||

| Alaska | - | 1 | 2 | |||||||||

| Rhode Island | 1 | 1 | - | |||||||||

| Nevada | - | 1 | 1 | |||||||||

| Texas | - | 1 | - | |||||||||

| Michigan | 4 | - | - | |||||||||

| New Mexico | 1 | - | - | |||||||||

| Hawaii | - | - | 1 | |||||||||

| Wisconsin | - | - | 1 | |||||||||

| Maryland | 1 | - | - | |||||||||

| Arkansas | 1 | - | - | |||||||||

| Total | 32 | 20 | 18 | |||||||||

Our marketing efforts during 2019 will be targeted at owner/operators, investors and companies that are actively seeking licenses to produce cannabis in California, Michigan, Missouri, Oklahoma, Utah and Pennsylvania. These represent the largest markets, based on the state and local regulatory framework, for our products and services. In particular, Pennsylvania and Oklahoma require indoor growing, and Missouri is expected to issue cultivation licenses in 2019. However, as and when new states pass legislation, we will shift our priorities and/or add new salespeople to pursue new facility construction at the early stage.

| 10 |

Marketing and Selling Our Expanded Product and Service Offering

Our marketing and sales efforts in 2019 and beyond will be diversified into three vectors: (i) new commercial build projects, (ii) existing commercial retrofit projects, and (iii) retail sales.

New commercial build projects are our traditional market, where we provide engineering and/or environmental control products for new cannabis grow facilities. We will continue to pursue such projects with an expanded product and service offering, which we expect will increase our average project size and target margins. While we intend to reduce our trade show presence and expenditures, we are enhancing our outreach with a new marketing methodology which will consist of a new customer-aligned messaging and positioning platform that we believe will increase our lead generation for new projects, and in turn allow our sales force to more effectively convert these leads to new contract bookings.

Our direct salespeople are primarily focused on new (and soon, existing) commercial project sales (typically in excess of 4,000 square feet of plant canopy, although some may be smaller) with each covering a specific geographical territory:

| ● | the Northeast region (which includes eastern Canada, and the U.S. East Coast); | |

| ● | the Pacific Northwest region (which includes Washington, Oregon, Alaska and western Canada); | |

| ● | the West Coast region (which currently includes all of California); and | |

| ● | the Midwest region (which includes Michigan). |

We currently do not have a salesperson in our Pacific Northwest sales territory, but we intend to fill this position in the second quarter of 2019. We also intend to expand our sales force as our resources allow.

Existing commercial retrofit projects represent a new opportunity that we have just begun to address. The estimated 3,000+ existing commercial grow facilities in North America are easier to identify than new build projects. We believe, based on evidence and our market knowledge, that some of these exiting facilities have environmental control problems that we can help remediate. We also believe that the energy consumption of these facilities can be reduced, and we are developing services and products to help them realize savings. We have a full product and service offering in mind, but we expect that the roll-out will take up to two years. However, to expedite this roll-out, we are evaluating possible strategic partners that could add products and services that are an immediate value-add to our customers.

Over the last several years, we deemphasized our wholesale efforts to the hydroponic retail stores network while we focused on building our commercial business. However, over time, as we add new products that can be sold at retail, such as fans, dehumidifiers, and nutrient cooling systems, we intend to make a more focused effort on marketing to the major retail chains that serve the cannabis cultivator market. By the third quarter of 2019, we except to develop a retail store sales and marketing strategy to leverage our growing product line, which we expect to fully implement by 2020.

Industry Presence

Our marketing outreach is conducted through three primary channels: magazine advertisement, our website, and industry trade shows.

Magazine Advertisement. We regularly advertise in major industry trade publications such as Cannabis Business Times, Cannabis Tech, Grow Opportunity (Canada), Grow Magazine (Canada), Marijuana Venture, and MJBiz Daily. Over time, we believe such advertisements have proven to be an effective business development tool.

Website. Our website is a consistent source of productive leads. We are currently revamping our website consistent with our new marketing methodology and expect that an update will be deployed in the second quarter of 2019.

Trade Shows. We regularly display at industry trade shows and conventions and conduct speaking engagements to achieve industry visibility and presence cost-effectively. In the past, we have attended most major trade and industry conventions including Lift Expo (Vancouver), CannaCon (Seattle), Cannabis Cultivation (Oakland), Lift Expo (Toronto), NCIA Cannabis Business Summit (San Jose), Cannabis World Congress & Business Expo (Los Angeles), CCIA/NCIA California Cannabis Business Conference (Anaheim) and the Marijuana Business Conference & Expo (Las Vegas), plus some smaller regional shows.

Several of our senior technical advisors and sales people also speak on climate control and energy efficiency at events sponsored by organizations such as National Cannabis Industry Association, Cannabis World Congress and Business Exposition and CannaCon and LIFT Vancouver and Toronto. These advisors and sales people are also frequently cited in industry-related publications. Our co-founder, Brandy Keen is also a member of Denver’s Department of Public Health and Environment Cannabis Sustainability Work Group, whose mission is to promote sustainability in the cannabis industry through education, the development and dissemination of best practices, and the facilitation of dialogue between the cannabis industry, the community, and technical experts. Ms. Keen was also acknowledged as a contributor to the 2018 Cannabis Energy Report published by New Frontier Data, a leading cannabis industry publisher.

| 11 |

We are a part of the Founder’s Circle of Resource Innovations Institute (“RII”), with Ms. Keen being a member of their technical advisory committee. RII promotes and quantifies energy and water conservation in the cannabis industry. As a result of our Founder’s Circle status, we have access to RII’s data as well as speaking position opportunities at their seminars.

These programs give us industry exposure and allow us to showcase our experience in environment management for cannabis cultivation. With many new participants in the cannabis cultivation industry, we will also be able to provide existing and prospective customers with access to a Colorado-licensed indoor cultivation facility managed by Stephen Keen, one of our co-founders, for demonstration tours in a working indoor grow environment, which we believe may assist us in the sale of our products and services in the future. We also have a technical test and demonstration facility in our building where we are developing and refining our controls products.

New Facility Sales Cycle and Risks

The sales cycles for our new build commercial projects can vary significantly. From pre-sales and technical advisory meetings to sales contract execution, to engineering and design services and equipment delivery, and all the way through installation and commissioning of the installed system, the full cycle can range from six months to two years. Since we do not install the climate control systems, our customers are required to use third-party installation contractors, which adds to the variability of the sales cycle.

The length of our sales cycle for new facilities is driven by numerous factors including:

| ● | the large number of first-time participants interested in the indoor cannabis cultivation business; | |

| ● | the complexities and uncertainties involved in obtaining state and local licensure and permitting; | |

| ● | local and state government delays in approving licenses and permits due to lack of staff or the large number of pending applications, especially in states where there is no cap on the number of cultivators; | |

| ● | the customer’s need to obtain cultivation facility financing; | |

| ● | the time needed, and coordination required, for our customers to acquire real estate and properly design and build the facility (to the stage when climate control systems can be installed); | |

| ● | the large price tag and technical complexities of the climate control and air sanitation system; | |

| ● | availability of power; and | |

| ● | delays that are typical in completing any commercial construction project. |

Based on the foregoing factors, there are risks that we may not realize the full contract value of our backlog in a timely manner, or at all. The performance of our obligations under a sales contract, and the timing of our revenue recognition, is dependent upon our customers’ ability to secure funding and real estate, obtain a license and then build their cultivation facility so they can take possession of the equipment. Our sales contracts currently are not time specific as to when our customers are required to take delivery of our services and equipment. More recently, we determined that some of our new construction facility projects are becoming larger and more complex and, as a result, delays were more likely due to licensing and permitting, lack of or delay in funding, staged facility construction, and/or the shifting priorities of certain customers with multiple facility projects in progress at one time. In order to address these risks, the obligations under these sales contracts are generally allocated into the following types of deliverables, and we typically require non-refundable payments from our customers in advance of our performance of services or delivery of equipment. However, in certain situations, especially as we expand our products and services offering for a customer’s entire facility lifecycle (i.e., beyond Pre-build and Construction phases), we may extend credit to our customers in which case we are at risk for the collection of account receivables.

Engineering Services. First, we provide our customer with engineering and design services and drawings. In many cases, the engineering phase is done as part of the license application or building permit process and takes approximately six to eight weeks to complete. Our strategy is to secure the sales contract and commence the engineering and design portion of the project early in the customer’s planning phase of the project. This is important for a number of reasons: (i) we can assist our customers with their engineering and design plans as part of their licensing application process as well as better assure the customer has the right-sized equipment for their application, leading to a higher probability of a successful grow, (ii) we are better positioned to utilize our proprietary equipment for the project at an earlier stage, and (iii) we are able to help reduce a customer’s time to market. Before we commence the engineering phase of the project, we will generally require an advanced payment intended to cover the engineering value of the contract.

Surna Manufactured Equipment. Upon completion of the engineering and design phase, it may take our customer on average six to 12 months to complete the facility build-out, with possible delays due to financing or other aspects which are beyond our control as discussed above. Customer delays in obtaining financing and completing facility build-out make the completion timing of our sales contract unpredictable. For this reason, we require an additional advance payment before we begin manufacturing our proprietary equipment items.

| 12 |

Third-Party Manufactured Equipment. The final phase of our contract typically involves the delivery of third-party manufactured equipment items and other equipment to complete the project. We typically will not deliver until we receive a final advance payment for the remaining contract value. After the project is completed and the environmental control system has been fully installed by third-party installation contractors, we will deploy our technicians to the customer’s cultivation facility to “commission” the system. Commissioning involves testing that the equipment has been properly assembled and installed by the installation contractor and assuring the equipment is operating within the agreed specifications.

Given the timing of the deliverables of our sales contracts, we often have experienced large variances in quarterly revenue. Our revenue recognition is dependent upon shipment of the equipment portions of our sales contracts, which, in many cases, may be delayed while our customers complete permitting, prepare their facilities for equipment installation or obtain project financing.

Competition

Our environmental control systems and our related engineering and design services compete with various national and local HVAC contractors and traditional HVAC equipment suppliers who traditionally resell, design, and implement climate control systems for commercial and industrial facilities, most of whom do not have the specific knowledge that we have about the complexities and challenges of cannabis cultivation. We have positioned ourselves to differ from these competitors by providing engineering and design services and environmental control systems, across all HVAC solutions, including modular chilled water systems, custom air handling units, split systems, packaged roof-top units, and self-contained and complex chilled-water systems, each tailored specifically for managing the distinct challenges involved in indoor cannabis cultivation. We believe our cannabis-specific applications and experience in this market allow us to deliver the right solution to our cultivation customers. Unlike many of our competitors, our solutions are designed specifically for cultivators to provide tight temperature/humidity control, reduce bio-security risk, reduce energy requirements, and minimize maintenance complexity, costs and downtime. However, as the legal cannabis market continues to grow, we expect increased competition in both the climate control systems and engineering services with some of these competitors attempting to emulate our cannabis specific-application model.

Intellectual Property

We rely on a combination of patent and trademark rights, trade secrets, laws that protect intellectual property, confidentiality procedures, and contractual restrictions with our employees and others to establish and protect our intellectual property rights. We have several pending patent applications, which include a combination of Patent Cooperation Treaty, utility and design patent applications that are directed to certain of our technologies. We have registered trademark registrations around our core Surna brand (“Surna”) in the United States and select foreign jurisdictions, as well as the Surna logo and the combined Surna logo and name in the United States. Our wordmark is also registered in the European Union and Canada. Subject to ongoing use and renewal, trademark protection is potentially perpetual.

Employees

We currently have 25 full-time employees. However, we may engage, and have in the past utilized, the services of a number of consultants, independent contractors, and other non-employee professionals. Additional employees may be hired in the future depending on need, available resources, and our achieved growth.

Government Regulation

The use, possession, cultivation, and distribution of marijuana is prohibited by U.S. federal law for medical and recreational purposes. Although certain states have legalized medical and recreational cannabis, companies and individuals involved in the sector are still at risk of being prosecuted by federal authorities. Further, the landscape in the cannabis industry changes rapidly. This means that at any time the city, county, or state where cannabis is permitted can change the current laws and/or the federal government can supersede those laws and take prosecutorial action. Given the uncertain legal nature of the cannabis industry, it is imperative that investors understand that investments in the cannabis industry should be considered very high risk. A change in the current laws or enforcement policy can negatively affect the status and operation of our business, require additional fees, stricter operational guidelines and unanticipated shut-downs.

See the “Risks Related to the Cannabis Industry” set forth in Item 1A of this Annual Report which addresses various risks related to U.S. and foreign regulation and enforcement of cannabis laws and regulations and their potential impact on our business.

| 13 |

Available Information

Our website address is www.surna.com. Our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to reports filed pursuant to Sections 13(a) and 15(d) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), are filed with the U.S. Securities and Exchange Commission (the “SEC”). Such reports and other information filed by us with the SEC are available free of charge through our website when such reports are available on the SEC’s website.

The SEC maintains an Internet site that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC at www.sec.gov.

The contents of the websites referred to above are not incorporated into this filing. Further, references to the URLs for these websites are intended to be inactive textual references only.

Investing in our common stock involves a number of significant risks. Certain factors may have a material adverse effect on our business, financial condition, and results of operations. You should consider carefully the risks and uncertainties described below, in addition to other information contained in this Annual Report on Form 10-K, including our consolidated financial statements and related notes. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that adversely affect our business. If any of the following risks actually occurs, our business, financial condition, results of operations, and future prospects could be materially and adversely affected. In that event, the trading price of our common stock could decline, and you could lose part or all of your investment.

Risks Relating to Our Business

We are solely dependent upon the funds we have raised so far to continue our operations, which may be insufficient to achieve significant revenue, and we may need to obtain additional financing, which may not be available to us and could dilute the ownership of current shareholders.

Historically, we have raised equity and debt capital to support our operations. We anticipate we will require additional cash resources to finance our growth or other future developments, including the launch of our new product and service initiatives and any investments or acquisitions we may decide to pursue. As of December 31, 2018, we had a working capital deficit of approximately $923,000 and our cash balance was $253,000. We are likely to need additional funds to complete further development of our business plan to achieve a sustainable sales level where ongoing operations can be funded from operations. We currently have no debt obligations. During 2017 and 2018, we completed private placement unit offerings, consisting of common stock and warrants, to accredited investors raising aggregate proceeds of $5,663,000. We will likely need to raise debt or equity financing in the future in order to continue our operations and achieve our growth targets. However, there can be no assurance that such financing will be available in sufficient amounts and on acceptable terms, when and if needed, or at all. The precise amount and timing of our funding needs cannot be determined accurately at this time, and will depend on a number of factors, including market demand for our products and services, the success of our product development efforts, the timing of receipts for customer payments, the management of working capital, and the continuation of normal payment terms and conditions for our purchase of goods and services. We believe our cash balances and cash flow from operations will be insufficient to fund our operations and growth for the next 12 months. If we are unable to substantially increase revenues, reduce expenditures, or otherwise generate cash flows from operations, then we will likely need to raise additional funding to continue our operations. Our failure to obtain sufficient financing on acceptable terms and conditions could have a material adverse effect on our growth prospects and our business, financial condition and results of operations.

To the extent that we raise additional equity capital, existing shareholders will experience a dilution in the voting power and ownership of their common stock, and earnings per share, if any, would be negatively impacted. Our inability to use our equity securities to finance our operations could materially limit our growth. Any borrowings made to finance operations could make us more vulnerable to a downturn in our operating results, a downturn in economic conditions, or increases in interest rates on borrowings that are subject to interest rate fluctuations. The amount and timing of such additional financing needs will vary principally depending on the timing of new product launches, investments and/or acquisitions, and the amount of cash flow from our operations. If our resources are insufficient to satisfy our cash requirements, we may seek to issue additional equity or debt securities or obtain a credit facility.

Our independent registered public accounting firm has expressed substantial doubt about our ability to continue as a going concern.

We have determined that our ability to continue as a going concern is dependent on raising additional capital to fund our operations and ultimately on generating future profits. Our independent registered public accounting firm has also included a “going concern” explanatory paragraph in its opinion on our financial statements, expressing substantial doubt that we can continue as an ongoing business for the next 12 months. Our financial statements do not include any adjustments that may result from the outcome of this uncertainty. If we are unable to successfully raise the capital we need, we may need to and believe we can reduce the scope of our business to fully satisfy our future short-term liquidity requirements. If we cannot raise additional capital or reduce the scope of our business, we may be otherwise unable to achieve our goals or continue our operations. While we believe that we will be able to raise the capital we need to continue our operations, there can be no assurances that we will be successful in these efforts or will be able to resolve our liquidity issues or eliminate our operating losses.

| 14 |

Even if we obtain more customers, there is no assurance that we will be able to convert our backlog into revenue or make a profit.

We may be unable to convert the full contract value of our backlog in a timely manner, or at all. The performance of our obligations under a sales contract, and the timing of our revenue recognition, is dependent upon our customers’ ability to secure funding and real estate, obtain a license and then build their cultivation facility so they can take possession of the equipment. Our sales contracts currently are not time specific as to when our customers are required to take delivery of our services and equipment. More recently, we determined that some of our new construction facility projects are becoming larger and more complex and, as a result, delays were more likely due to licensing and permitting, lack of or delay in funding, staged facility construction, and/or the shifting priorities of certain customers with multiple facility projects in progress at one time. Even if we obtain more customers, or increase the average size of our projects, there is no guarantee that we will be able to generate a profit. Because we are a small company with limited capital, limited products and services, and limited marketing activities, we may not be able to generate sufficient revenue to operate profitably. If we cannot operate profitably, we may have to suspend or cease operations.

We may extend credit to our customers in the future and, if we are unable to collect these accounts receivable, our future profitability could be adversely impacted.

Historically, we had little exposure to the collection risk on accounts receivable since we typically received payments from our customers in advance of our performance of services or delivery of equipment. However, in certain situations, especially as we expand our products and services offering for a customer’s entire facility lifecycle (i.e., beyond Pre-build and Construction phases), we may extend credit to our customers in which case we are at risk for the collection of account receivables. Accordingly, we will be at greater risk for the collection of account receivables. Our credit arrangements are negotiated and may not protect us if a customer develops operational difficulty or incurs operating losses which could lead to a bankruptcy. In these cases, we may lose most of the outstanding balance due. In addition, we are typically not able to insure our accounts receivables. The risk is that we derive our revenue and profits from selling products and services to the emerging cannabis industry. The failure of our customers to pay in full amounts due to us could negatively affect future profitability.

Because we currently do not maintain effective internal controls over financial reporting, we may be unable to accurately report our financial results or prevent fraud, and investor confidence and the market price of our common stock may, therefore, be adversely impacted.

Our reporting obligations as a public company place a significant strain on our management, operational and financial resources, and systems, and will continue to do so for the foreseeable future. Annually, we are required to prepare a management report on our management’s assessment of the effectiveness of our internal control over financial reporting. Management has concluded that our internal control over financial reporting is currently not effective and shall report such in management’s report in this annual report on Form 10-K. In the event that our status with the SEC changes to that of an accelerated filer from a smaller reporting company, our independent registered public accounting firm will be required to attest to and report on our management’s assessment of the effectiveness of our internal control over financial reporting. Under such circumstances, even if our management concludes that our internal control over financial reporting is effective, our independent registered public accounting firm may still decline to attest to our management’s assessment, or may issue a report that is qualified, if it is not satisfied with our controls, or the level at which our controls are documented, designed, operated or reviewed, or if it interprets the relevant requirements differently from us.

We have identified a material weakness in our internal control over financial reporting and, if we do not remediate the material weakness or are unable to implement and maintain effective internal control over financial reporting in the future, the accuracy and timeliness of our financial reporting may be adversely affected.

We currently do not maintain effective controls over certain aspects of the financial reporting process because: (i) we lack a sufficient complement of personnel with a level of accounting expertise and an adequate supervisory review structure that is commensurate with our financial reporting requirements, (ii) there is inadequate segregation of duties due to the limitation on the number of our accounting personnel, and (iii) we have insufficient controls and processes in place to adequately verify the accuracy and completeness of spreadsheets that we use for a variety of purposes including revenue, taxes, stock-based compensation and other areas, and place significant reliance on, for our financial reporting. A material weakness is a deficiency or a combination of deficiencies in internal control over financial reporting such that there is a reasonable possibility that a material misstatement of the annual or interim consolidated financial statements will not be prevented or detected on a timely basis. If we are unable to achieve effective internal control over financial reporting, or if our independent registered public accounting firm determines we continue to have a material weakness in our internal control over financial reporting, we could lose investor confidence in the accuracy and completeness of our financial reports, the market price of our shares could decline, and our reputation may be damaged.

| 15 |

Our inability to effectively manage our growth could harm our business and materially and adversely affect our operating results and financial condition.

Our strategy envisions growing our business. We plan to expand our product, sales, administrative and marketing operations. Any growth in or expansion of our business is likely to continue to place a strain on our management and administrative resources, infrastructure and systems. As with other growing businesses, we expect that we will need to further refine and expand our business development capabilities, our systems and processes and our access to financing sources. We also will need to hire, train, supervise, and manage new employees. These processes are time consuming and expensive, will increase management responsibilities and will divert management attention. We cannot assure that we will be able to:

| ● | execute on our new business plan and strategy; | |

| ● | expand our products effectively or efficiently or in a timely manner; | |

| ● | allocate our human resources optimally; | |

| ● | meet our capital needs; | |

| ● | identify and hire qualified employees or retain valued employees; or | |

| ● | effectively incorporate the components of any business or product line that we may acquire in our effort to achieve growth. |

Our inability or failure to manage our growth and expansion effectively could harm our business and materially and adversely affect our operating results and financial condition.

Our operating results may fluctuate significantly based on customer acceptance of our products, industry uncertainty, project financing concerns, and the licensing and qualification of our prospective customers. As a result, period-to-period comparisons of our results of operations are unlikely to provide a good indication of our future performance.

Management expects that we will experience substantial variations in our revenues and operating results from quarter to quarter. Our revenue recognition is dependent upon shipment of the equipment portions of our sales contracts, which, in many cases, may be delayed while our customers complete permitting, prepare their facilities for equipment installation or obtain project financing. Industry uncertainty, project financing concerns, and the licensing and qualification of our prospective customers, which are out of our control, make it difficult for us to predict when we will recognize revenue. If customers are unable to obtain licensing, permitting or financing, our sales and revenue will decline, resulting in a reduction in our operating income or possible increase in losses.

If we do not successfully develop additional products and services, or if such products and services are developed but not successfully commercialized, we could lose revenue opportunities.

Our future success depends, in part, on our ability to expand our product and service offerings. We are currently investigating a number of new and improved product opportunities, and we intend to collaborate with manufacturing partners to optimize these products for the cannabis market. The processes of identifying and commercializing new products is complex and uncertain, and if we fail to accurately predict customers’ changing needs and emerging technological trends our business could be harmed. We have already and may have to continue to commit significant resources to commercializing new products before knowing whether our investments will result in products the market will accept. We may be unable to differentiate our new products from those of our competitors, and our new products may not be accepted by the market. There can be no assurance that we will successfully identify additional new product opportunities, develop and bring new products to market in a timely manner, or achieve market acceptance of our products or that products and technologies developed by others will not render our products or technologies obsolete or noncompetitive. Furthermore, we may not execute successfully on commercializing those products because of errors in product planning or timing, technical hurdles that we fail to overcome in a timely fashion, or a lack of appropriate resources. This could result in competitors providing those solutions before we do and a reduction in revenue and earnings.

| 16 |

Our future success depends on our ability to grow and expand our customer base. Our failure to achieve such growth or expansion could materially harm our business.

Our success and the planned growth and expansion of our business depend on us achieving greater and broader acceptance of our products and services and expanding our commercial customer base. There can be no assurance that customers will purchase our services or products or that we will continue to expand our customer base. If we are unable to effectively market or expand our product and service offerings, we will be unable to grow and expand our business or implement our business strategy. This could materially impair our ability to increase sales and revenue, and materially and adversely affect our margins, which could harm our business and cause our stock price to decline.

Our suppliers could fail to fulfill our orders for parts used to assemble our products, which would disrupt our business, increase our costs, harm our reputation, and potentially cause us to lose our market.