PIMCO Equity Series VIT

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT

COMPANIES

Investment Company Act file number:

811-22376

PIMCO Equity Series VIT

(Exact name of registrant as specified in charter)

840 Newport Center Drive, Newport Beach, CA 92660

(Address of principal

executive offices)

John P. Hardaway

Treasurer and Principal Financial Officer

PIMCO Equity Series VIT

840 Newport Center Drive

Newport Beach, CA 92660

(Name and address of agent for service)

Copies to:

Brendan C. Fox

Dechert LLP

1775 I Street, N.W.

Washington, D.C. 20006

Registrant’s telephone number, including area code: (800) 927-4648

Date of fiscal year end: December 31

Date of reporting period: December 31, 2011

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be

transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information

public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning

the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of

information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30e-1).

| |

• |

|

PIMCO Equity Series VIT—Institutional Class |

| |

• |

|

PIMCO Equity Series VIT—Advisor Class |

Your Global Investment Authority

PIMCO Equity Series VIT

Annual Report

December 31, 2011

PIMCO EqS Pathfinder Portfolio™

Share Class

Table of Contents

This material is authorized for use only when preceded

or accompanied by the current PIMCO Equity Series VIT (the “Trust”) prospectus for the Portfolio. The variable product prospectus may be obtained by contacting your Investment Consultant.

Chairman’s Letter

Dear Shareholder,

Please find enclosed the Annual Report for the PIMCO Equity Series VIT covering the

twelve-month reporting period ended December 31, 2011.

On the

following pages are specific details about the investment performance of the PIMCO EqS Pathfinder Portfolio™ and a discussion of the factors that affected performance during the reporting period. In addition, the letter from the portfolio

managers provides a further review of such factors as well as an overview of their investment strategy, philosophy, and process.

General highlights of the financial markets during our twelve-month reporting period include:

| |

n |

|

Equity markets worldwide remained volatile throughout the reporting period as investors responded to muted global economic growth prospects, rising concerns over

the European sovereign debt crisis, and political gridlock in Washington. U.S. equities, as measured by the S&P 500 Index, returned 2.11%, while global equities, as represented by the MSCI World Index, declined 5.54%. Emerging market (EM)

equities, as represented by the MSCI Emerging Markets Index, declined 18.42% and underperformed developed market equities. |

| |

n |

|

Yields on U.S. Treasury securities ended the period significantly lower (with prices on these securities therefore higher) due to a flight-to-quality brought on

by the European sovereign debt crisis. This combined with a weaker global growth outlook, resulting in increased demand for bonds of nations with perceived stronger balance sheets, top credit ratings, and independent currency and monetary policy.

The Federal Reserve kept the Federal Funds Rate anchored within a range of zero to 0.25%; the Bank of England held its key lending rate at 0.50%; and the European Central Bank reduced its main policy rate to 1.00%. The benchmark ten-year U.S.

Treasury note yielded 1.95% at the end of the reporting period, as compared to 3.29% on December 31, 2010. |

Thank you again for the trust you have placed in us. We value your commitment and will continue to work diligently to meet your broad investment needs.

|

|

|

|

|

|

|

Sincerely,

Brent R. Harris Chairman of the

Board, PIMCO Equity Series VIT January 25, 2012 |

|

|

|

|

|

|

|

|

|

DECEMBER 31, 2011 |

|

ANNUAL REPORT |

|

1 |

Important Information About the Portfolio

PIMCO Equity Series VIT (the “Trust”) is an open-end management investment company

currently consisting of one investment portfolio, the PIMCO EqS Pathfinder PortfolioTM (the “Portfolio”). The Portfolio is only available as a funding vehicle under variable life insurance policies or variable annuity contracts issued by insurance companies (“Variable

Contracts”). Individuals may not purchase shares of the Portfolio directly. Shares of the Portfolio also may be sold to qualified pension and retirement plans outside of the separate account context.

The Portfolio seeks capital appreciation by investing under normal circumstances in

equity securities, including common and preferred stock (and securities convertible into, or that PIMCO expects to be exchanged for, common or preferred stock), of issuers that PIMCO believes are undervalued. The Portfolio’s bottom-up value

investment style attempts to identify securities that are undervalued by the market in comparison to PIMCO’s own determination of the company’s value, taking into account criteria such as asset value, book value and cash flow and earnings

estimates.

The Portfolio may be subject to various risks as described in

the Portfolio’s prospectus. Some of these risks may include, but are not limited to, the following: equity risk, value investing risk, foreign (non-U.S.) investment risk, emerging markets risk, market risk, issuer risk, interest rate risk,

credit risk, high yield and distressed company risk, currency risk, liquidity risk, leveraging risk, management risk, small-cap and mid-cap company risk, arbitrage risk, derivatives risk, short sale risk, commodity risk, tax risk and subsidiary

risk. A complete description of these risks and other risks is contained in the Portfolio’s prospectus. The Portfolio may use derivative instruments for hedging purposes or as part of an investment strategy. Use of these instruments may involve

certain costs and risks such as liquidity risk, interest rate risk, market risk, credit risk, management risk, leverage risk, mispricing or improper valuation risk and the risk that the Portfolio could not close out a position when it would be most

advantageous to do so. The Portfolio could lose more than the principal amount invested in these derivative instruments.

On the Performance Summary page in this Annual Report (“Shareholder Report”), the Average Annual Total Return table and Cumulative Returns chart measure

performance assuming that any dividend and capital gain distributions were reinvested. The Portfolio measures its performance against a broad-based securities market index (benchmark index). The Portfolio’s past performance, before and after

taxes, is not necessarily an indication of how the Portfolio will perform in the future.

An investment in the Portfolio is not a deposit of a bank and is not guaranteed or insured by the Federal Deposit

Insurance Corporation or any other government agency. It is possible to lose money on investments in the Portfolio.

PIMCO has adopted written proxy voting policies and procedures (“Proxy Policy”) as required by Rule 206(4)-6 under the Investment Advisers Act of 1940, as amended. The Proxy Policy has been adopted by the

Trust as the policies and procedures that PIMCO will use when voting proxies on behalf of the Portfolio. A description of the policies and procedures that PIMCO uses to vote proxies relating to portfolio securities of the Portfolio, and information

about how the Portfolio voted proxies relating to portfolio securities held during the most recent twelve-month period ended June 30th, are available without charge, upon request, by calling the Trust at 1-800-927-4648, on the Portfolio’s

website at http://pvit.pimco-funds.com, and on the Securities and Exchange Commission’s (“SEC”) website at http://www.sec.gov.

The Portfolio files a complete schedule of the Portfolio’s holdings with the SEC for the first and third quarters of each fiscal year on Form N-Q. A copy of

the Portfolio’s Form N-Q is available on the SEC’s website at http://www.sec.gov and may be reviewed and copied at the SEC’s Public Reference Room in Washington, D.C. The Portfolio’s Form N-Q will also be available without

charge, upon request, by calling the Trust at 1-800-927-4648 and on the Portfolio’s website at http://pvit.pimco-funds.com. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330.

|

|

|

|

|

|

|

| 2 |

|

PIMCO EQUITY SERIES VIT |

|

|

|

|

The following disclosure provides important information regarding the Portfolio’s Expense Example

(“Example” or “Expense Example”), which appears in this Shareholder Report. Please refer to this information when reviewing the Expense Example for the Portfolio.

Expense Example

As a shareholder of the Portfolio, you incur two types of costs: (1) transaction costs and (2) ongoing costs, including management fees, distribution and/or service

(12b-1) fees (Advisor Class only), and other Portfolio expenses. The Example is intended to help you understand your ongoing costs (in dollars) of investing in the Portfolio and to compare these costs with the ongoing costs of investing in other

mutual funds. The Expense Example does not reflect any fees or other expenses imposed by the Variable Contracts. If it did, the expenses reflected in the Expense Example would be higher. The Example is based on an investment of $1,000 invested at

the beginning of the period and held for the entire period, from July 1, 2011 to December 31, 2011.

Actual Expenses

The information

in the table under the heading “Actual Performance” provides information about actual account values and actual expenses. You may use the information in these columns, together with the amount you invested, to estimate the expenses that

you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = $8.60), then multiply the result by the number in the appropriate column for your share class, in the row entitled

“Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes

The information in the table under the heading “Hypothetical Performance (5% return before expenses)” provides information

about hypothetical account values and hypothetical expenses based on the Portfolio’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Portfolio’s actual return. The hypothetical account

values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Portfolio and other portfolios. To do so, compare

this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other portfolios.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs. Therefore, the

information under the heading “Hypothetical Performance (5% return before expenses)” is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different portfolios. In addition, if these

transactional costs were included, your costs would have been higher.

Expense ratios may vary from period to period because of various factors such as an increase in expenses that are not covered by the management fees, such as fees

and expenses of the independent trustees and their counsel, extraordinary expenses and interest expense.

|

|

|

|

|

|

|

|

|

DECEMBER 31, 2011 |

|

ANNUAL REPORT |

|

3 |

Insights from the Portfolio Managers PIMCO EqS Pathfinder Portfolio™

Dear Shareholder,

Thank you to all who have invested in the PIMCO EqS Pathfinder Portfolio™ (the “Portfolio”) since its launch in April of

2010. For all those who are reading and have an interest in the Portfolio, we have organized our thoughts to update you on the current state of the investment world, on the Portfolio itself and on our outlook.

Review of the Last Period

Over the year, your investment in the Portfolio outperformed its benchmark, the MSCI

World Index, despite posting negative returns. The Portfolio’s outperformance relative to its benchmark occurred during a period marked by extremely high correlation across securities, distinct “risk on” and “risk off” modes

within the market and many professional money managers in both the long only and hedge fund world underperforming their benchmarks by wide margins due to this environment.

While the high correlation and resulting volatility in markets had an impact on the

Portfolio, our historical track record of offering reduced downside exposure stayed intact and was a critical part of outperforming the benchmark over the reporting period. In the following remarks, we’ll relate what we saw in a market that is

multifaceted to the extent that on the one hand, the earnings produced by companies are growing at an attractive rate but on the other hand, some of the macro risks we’re seeing are looming large in the background.

First, we’ll cover the positive developments we saw. Despite a global economy

that can’t be described as strong, companies in the U.S., Asia and even Europe significantly grew their earnings over the reporting period. Growth has been so persistent that many are calling for operating margin declines because it just

doesn’t seem possible that profitability can continue to expand so predictably. For example, revenues and earnings for the MSCI World Index (which includes a healthy number of areas that are perceived to be challenged in Europe and the banking

sector) grew by 6.6% and 2.6% over the year, respectively. In the U.S., as measured by the S&P 500 Index, growth was even stronger with revenues and earnings growth of 8.0% and 6.1%, respectively. Return of capital to shareholders in 2011 was up

over 40% year over year with authorized share repurchases set to be over $550 billion and dividends were up 13.5% in the same period (according to industry reports). In our opinion, this is leaving behind some very attractively valued stocks in all

economies as earnings multiples are stagnant to contracting in many cases.

Second, let’s address what we see in the broader economy, which isn’t as positive and is somewhat in contrast with what we’re seeing with many

individual companies. Over the review period, a number of negative developments came out of Europe and Asia despite a

surprising pick up in the U.S. economy. In Europe, a litany of events revolving around a lack of consensus on how to deal with the overleveraged sovereign balance sheets of peripheral countries

caused volatility in equity markets and has many evaluating the consequences of a Eurozone breakup—once an unimaginable outcome. In Asia, China’s enormous engine of global growth has been sputtering as property values have dropped by as

much as 50% in some areas and the country’s GDP is anticipated to have only expanded at a 9.2% rate in 2011, the lowest since 2009 (according to industry reports). As for the U.S., after a weak report by the Institute for Supply Management

(ISM) at the end of July 2011 and the downgrade of U.S. long-term sovereign debt from AAA to AA+ by independent credit rating agency Standard & Poor’s in early August, the S&P 500 Index experienced a steep decline and the

bears warned us of further downside. However, in a remarkable turnaround, the U.S. economy responded with report after report of better job creation and economic growth than many expected throughout the second half of the reporting period and U.S.

equity markets responded in kind, putting in a 15% advance from the bottom of the market on October 3 (as measured by the S&P 500 Index). Unfortunately, the risks in other parts of the world are likely to inevitably put pressure on the U.S.

if things continue to sour in Europe and Asia.

With these concepts

painting a picture of a tug-of-war between the good and the bad, let’s talk about some of the investment ideas in the Portfolio, including both positive and negative contributors to performance, that we find interesting and how they performed

over the reporting period.

Among the securities that contributed to

performance were the Portfolio’s investments in Phillip Morris and White Mountains Insurance.

Philip Morris

There are often negative headlines on the tobacco sector that deter many investors, but we find

intriguing for the Portfolio, including: declining volumes, litigation risk, increased taxation, plain packaging, and smoking bans. However, the tobacco industry has some characteristics that we consider unique; relatively inelastic pricing power,

growth from emerging markets, highly cash generative business models and generally shareholder friendly managements.

Our security selection process has identified significant value amongst various tobacco companies, and one of them, Philip Morris International, was our top

performer for the period under review.

Philip Morris International is the world’s largest

tobacco manufacturer (excluding China), and owns the market leading brand, Marlboro. It was spun out of the Altria Group in March 2008 (Altria retained its US operations) and owns approximately a 15.6% cigarette market share outside the U.S.

(according to industry reports). The international

|

|

|

|

|

|

|

| 4 |

|

PIMCO EQUITY SERIES VIT |

|

|

|

|

company benefits from its non-U.S. footprint, which to some extent limits its litigation risk compared to its U.S. peers, however, its acquisition of Rothmans in Canada does not make it

completely immune. We believe Philip Morris International benefits from its brand portfolio and size, its international diversification, and its strong cash flow generation. The company is also managed in a very shareholder friendly manner. After

the completion of its first $13 billion share repurchase program, management initiated another share buyback of $12 billion for 2010-2012 and then followed that with an announcement in February 2011 that it would add an additional $5 billion to the

three year repurchase plan.

Although this name had performed well through

the first seven months of the reporting period, the stock began to pull back in early August 2011 as the equity markets began to weaken on heightened fears of contagion from the European debt crisis. We seized upon the opportunity to increase our

exposure to this company and also added selectively to other positions in the portfolio.

White Mountains Insurance

Another area where we have been finding value is in the financial sector. While we

do hold what we believe to be a few select well-managed U.S. thrifts in the Portfolio, our focus has been primarily drawn to the attractive valuations we have uncovered in the property & casualty re-insurance industry. One such company that

we have owned for some time which was a particularly strong performer in the Portfolio over the reporting period was White Mountain Insurance, a Bermuda-domiciled property & casualty insurance and re-insurance business that at the beginning

of the year had a price to book value of 0.75, a 43% discount to its ten-year price-to-book average. Our analysis appears to have been confirmed by other marketplace participants as the company announced in May 2011 that it had signed a definitive

agreement to sell its Esurance and Answer Financial businesses to Allstate for $700 million in cash plus the tangible book value at the time of closing. In addition, management offered a self-tender to purchase up to 300,000 of its own shares in

September 2011. The stock of White Mountain Insurance returned 35% over the year and we continue to find the company an attractive opportunity within the Portfolio.

Among the securities that detracted from performance were the Portfolio’s

investments in Nintendo and Marine Harvest.

Nintendo

Nintendo is a company for which investors appear to have lost faith, however, as somewhat contrarian investors, it intrigues us. While we fully recognize that

Nintendo has made missteps, has wounds that are self-inflicted and faces increased competition, we believe the stock is being priced by investors at a level which anticipates a worst case scenario. The company ended the year with its stock valued at

1.3

times its book value with approximately 73% of the company’s market capitalization held in cash and cash equivalents on its balance sheet. Expectations appear to have been reset to

unreasonably low levels and investors appear to believe the company will never correct its ills, or that there will be a 3DS failure followed by a large amount of wasted money on the second generation Wii console. We, however, believe the company is

worth more than its current price implies, given the quality of its business and its intellectual property rights. Nintendo is also working hard to develop new software and hardware, which we expect to see in early 2012. We believe there is still

room for three major players in the gaming business, and that Nintendo will not only survive, but will do well.

Marine Harvest

Salmon farming is the primary business of Oslo, Norway based Marine Harvest, and to its

detriment salmon pricing has recently come under pressure due to optimistic salmon production forecasts. We see many investors believing there is going to be significant production growth coming out of Norway and Chile, two of the major

commercial salmon growing areas of the world. However, we believe the forecasts for salmon production growth coming out of Chile, in particular, might be difficult to achieve due to challenging biological conditions and prevalent

disease.

Salmon farming enjoys the lowest feed to protein conversion ratio

of any of the major sources of protein. Over the long-term, we believe the emerging markets are going to consume greater and greater quantities of protein as their per capita incomes and standards of living increase. Hence, we continue to

believe there will be increased demand for salmon in the foreseeable future.

Looking Ahead

After a tumultuous 2011 in which global equity markets on a consolidated basis either eked out a small gain or were down, we believe 2012 promises to be just as interesting, but our sense is that a flattish outcome

from equity markets for two years in a row is unlikely. This is the bi-modal world that we discuss at PIMCO where on one hand, a sizeable risk to the global economy and asset markets exists due to imbalances and stretched balance sheets, but on the

other hand, many central banks are drowning their banking systems in fiat currency (paper money declared legal tender) which could lead to a bout of reflation.

To align our portfolio with that view, we expect that high quality stocks trading at steep discounts to their intrinsic value will continue to be added to the

portfolio in addition to the ones we already own. Not only do stocks like these tend to have high margins, little financial leverage and strong cash flow generation, but they also haven’t been offered at such attractive prices in decades, in

our opinion. We’d like

|

|

|

|

|

|

|

|

|

DECEMBER 31, 2011 |

|

ANNUAL REPORT |

|

5 |

Insights from the Portfolio Managers PIMCO EqS Pathfinder

Portfolio™ (Cont.)

to think that “you can have your cake and eat it too” and stocks like these should be well positioned to benefit: if the equity market rallies strongly, we will seek to participate and

deliver a positive return. But if the equity market drops precipitously due to the external environment, we expect companies like these may be less impacted than other stocks and could ultimately have the potential to return to a normal valuation,

in our opinion. Also, we expect stocks with the ability to return capital to shareholders in the form of dividends and share buybacks will be a focus. In a world that has such a divergence in outcomes, companies that are returning cold hard cash

should be favored and if they’re buying back their stock at cheap valuations, so much the better.

To close this letter, we repeat our thanks for staying the course with the PIMCO EqS Pathfinder Portfolio™, just as we’re staying the course and sticking with our discipline of seeking capital

appreciation while also looking to help mitigate downside risk. We’re privileged to have the opportunity to steward your capital and our intent is to use all of the tools at our disposal to continue to serve in that role.

Sincerely,

|

|

|

|

|

|

|

|

|

|

|

Charles Lahr, CFA Co-Portfolio

Manager |

|

Anne Gudefin, CFA Co-Portfolio

Manager |

Top Holdings1

|

|

|

|

|

|

|

| SPDR Gold Trust |

|

|

|

|

3.60% |

|

| Imperial Tobacco Group PLC |

|

|

|

|

3.40% |

|

| British American Tobacco PLC |

|

|

|

|

3.00% |

|

| Danone |

|

|

|

|

2.50% |

|

| Microsoft Corp. |

|

|

|

|

2.40% |

|

| Intel Corp. |

|

|

|

|

2.20% |

|

| Lorillard, Inc. |

|

|

|

|

2.10% |

|

| Lancashire Holdings Ltd. |

|

|

|

|

2.10% |

|

| BP PLC |

|

|

|

|

1.90% |

|

| Koninklijke KPN NV |

|

|

|

|

1.90% |

|

Geographic Breakdown1

|

|

|

|

|

|

|

| United States |

|

|

|

|

35.5% |

|

| United Kingdom |

|

|

|

|

12.1% |

|

| France |

|

|

|

|

11.1% |

|

| Bermuda |

|

|

|

|

6.1% |

|

| Netherlands |

|

|

|

|

5.8% |

|

| Switzerland |

|

|

|

|

4.2% |

|

| Hong Kong |

|

|

|

|

3.1% |

|

| Denmark |

|

|

|

|

2.0% |

|

| Canada |

|

|

|

|

1.5% |

|

| Japan |

|

|

|

|

1.5% |

|

| Norway |

|

|

|

|

1.5% |

|

| Other |

|

|

|

|

7.7% |

|

Sector Breakdown1

|

|

|

|

|

|

|

| Consumer Staples |

|

|

|

|

27.2% |

|

| Financials |

|

|

|

|

21.6% |

|

| Information Technology |

|

|

|

|

8.5% |

|

| Industrials |

|

|

|

|

6.8% |

|

| Energy |

|

|

|

|

6.7% |

|

| Health Care |

|

|

|

|

6.7% |

|

| Consumer Discretionary |

|

|

|

|

5.3% |

|

| Exchange-Traded Funds |

|

|

|

|

3.6% |

|

| Materials |

|

|

|

|

2.9% |

|

| Telecommunication Services |

|

|

|

|

1.8% |

|

| Utilities |

|

|

|

|

0.6% |

|

| 1 |

% of Total Investments as of 12/31/2011. Top Holdings, Geographic and Sector Breakdown solely reflect long positions. Securities sold short, derivatives, and

short-term instruments are not taken into consideration. |

|

|

|

|

|

|

|

| 6 |

|

PIMCO EQUITY SERIES VIT |

|

|

|

|

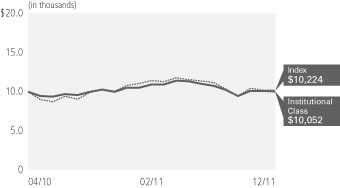

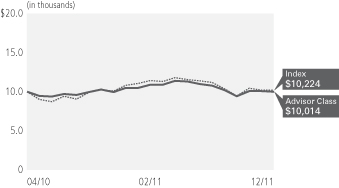

PIMCO EqS Pathfinder

Portfolio™

Cumulative Returns Through

December 31, 2011

$10,000 invested at the end of the month when the Portfolio’s Institutional Class commenced operations.

|

|

|

|

|

|

|

|

|

|

|

| Average Annual Total Return for the period ended December 31, 2011 |

|

|

|

|

| |

|

|

|

1 Year |

|

|

Class Inception

(04/14/2010) |

|

|

|

PIMCO EqS Pathfinder PortfolioTM Institutional Class |

|

|

-4.54% |

|

|

|

-0.81% |

|

|

|

MSCI World

Index± |

|

|

-5.54% |

|

|

|

-0.58% |

|

All Portfolio returns are net of fees and expenses.

Performance quoted represents past performance. Past performance is not

a guarantee or a reliable indicator of future results. Investment return and the principal value of an investment will fluctuate. Shares may be worth more or less than original cost when redeemed. The Portfolio’s performance does not reflect

the deduction of additional charges and expenses imposed in connection with investing in Variable Contracts, which will reduce returns. Current performance may be lower or higher than performance shown. For performance current to the most recent

month-end, visit http://pvit.pimco-funds.com. The Portfolio’s total annual operating expense ratio as stated in the Portfolio’s current prospectus, as supplemented to date, is 1.16% for Institutional Class shares.

± The MSCI World Index is a free float-adjusted market capitalization weighted

index that is designed to measure the equity market performance of developed markets. As of May 27, 2010 the MSCI World Index consisted of the following 24 developed market country indices: Australia, Austria, Belgium, Canada, Denmark, Finland,

France, Germany, Greece, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States. The index represents the unhedged performance of the

constituent stocks, in US dollars. It is not possible to invest directly in an unmanaged index.

|

|

|

|

|

|

|

|

|

| Expense Example |

|

Actual Performance |

|

|

Hypothetical Performance |

|

| |

|

|

|

|

(5% return before expenses) |

|

| |

|

Institutional Class |

|

|

Institutional Class |

|

| Beginning Account Value (07/01/11) |

|

$ |

1,000.00 |

|

|

$ |

1,000.00 |

|

| Ending Account Value (12/31/11) |

|

$ |

910.50 |

|

|

$ |

1,020.27 |

|

| Expenses Paid During Period* |

|

$ |

4.72 |

|

|

$ |

4.99 |

|

| Net Annualized Expense Ratio** |

|

|

0.98 |

% |

|

|

0.98 |

% |

* Expenses are equal to the net annualized expense

ratio for the class, multiplied by the average account value over the period, multiplied by 184/365 (to reflect the one-half year period). Overall fees and expenses of investing in the Portfolio will be higher because the example does not reflect

variable contract fees and expenses.

** The net annualized expense

ratio is reflective of any applicable waivers related to contractual agreements for voluntary fee waivers and special purpose vehicles. Details regarding fee waivers can be found in note 8 in the Notes to Financial Statements.

Please refer to the Important Information section for an explanation of the

information presented in the above Expense Example.

Portfolio Insights

| » |

|

The PIMCO EqS Pathfinder Portfolio™ seeks capital appreciation by investing under normal circumstances in equity securities, including common and preferred

stock (and securities convertible into, or that PIMCO expects to be exchanged for, common or preferred stock), of issuers that PIMCO believes are undervalued. The Portfolio’s bottom-up value investment style attempts to identify securities that

are undervalued by the market in comparison to PIMCO’s own determination of the company’s value, taking into account criteria such as asset value, book value, cash flow and earnings estimates. |

| » |

|

During the reporting period, the Portfolio’s Institutional class shares declined 4.54% after fees, and the Portfolio’s benchmark index,

the MSCI World Index, declined 5.54%. The Portfolio’s performance, although negative, outperformed its benchmark by 1.00% after fees. |

| » |

|

Holdings in Lloyds Banking, Nintendo, and Marine Harvest were notable detractors from returns as prices on these securities declined during the reporting period.

|

| » |

|

In a challenging period for equities, stock selection in the consumer staples sector helped make some notable contributions to the Portfolio’s return.

|

| » |

|

Holdings in Lorillard, Philip Morris International, and White Mountains Insurance were notable performers as prices on these securities appreciated during

the reporting period. |

| » |

|

Given the decline in the equity markets over the reporting period, the Portfolio’s market risk and currency hedging strategies, including its position in a

gold exchange-traded fund (ETF), contributed to performance as these hedging strategies appreciated in value. |

| » |

|

At the end of the reporting period, the Portfolio held approximately 83% in equities we believe are undervalued, approximately 3% (on the long side only) in

merger arbitrage investments, approximately 10% in cash equivalents, and held the balance of the portfolio in currency and market risk hedges, including approximately 4% in gold. |

|

|

|

|

|

|

|

|

|

DECEMBER 31, 2011 |

|

ANNUAL REPORT |

|

7 |

Financial Highlights PIMCO EqS

Pathfinder Portfolio™

|

|

|

|

|

|

|

|

|

| Selected Per Share Data for the Year

or Period Ended: |

|

12/31/2011 |

|

|

04/14/2010-12/31/2010 |

|

|

|

|

| Institutional Class |

|

|

|

|

|

|

|

|

| Net asset value beginning of year or period |

|

$ |

10.33 |

|

|

$ |

10.00 |

|

| Net investment income

(a) |

|

|

0.11 |

|

|

|

0.12 |

|

| Net realized/unrealized gain (loss) |

|

|

(0.58 |

) |

|

|

0.21 |

|

| Total income (loss) from investment operations |

|

|

(0.47 |

) |

|

|

0.33 |

|

| Dividends from net investment income |

|

|

(0.01 |

) |

|

|

0.00 |

|

| Total distributions |

|

|

(0.01 |

) |

|

|

0.00 |

|

| Net asset value end of year or period |

|

$ |

9.85 |

|

|

$ |

10.33 |

|

| Total return |

|

|

(4.54 |

)% |

|

|

3.30 |

% |

| Net assets end of year or period (000s) |

|

$ |

66,439 |

|

|

$ |

3,276 |

|

| Ratio of expenses to average net assets |

|

|

0.98 |

% |

|

|

1.01 |

%* |

| Ratio of expenses to average net assets excluding waivers |

|

|

1.18 |

% |

|

|

3.72 |

%* |

| Ratio of expenses to average net assets excluding interest expense and dividends on securities sold

short |

|

|

0.97 |

% |

|

|

0.97 |

%* |

| Ratio of expenses to average net assets excluding interest expense, dividends on securities sold

short and waivers |

|

|

1.17 |

% |

|

|

3.68 |

%* |

| Ratio of net investment income to average net assets |

|

|

1.14 |

% |

|

|

1.69 |

%* |

| Portfolio turnover rate |

|

|

238 |

%** |

|

|

25 |

%** |

| ** |

The ratio excludes PIMCO Short-Term Floating NAV Portfolio. |

| (a) |

Per share amounts based on average number of shares outstanding during the year or period.

|

|

|

|

|

|

|

|

|

|

| 8 |

|

PIMCO EQUITY SERIES VIT |

|

|

|

|

See Accompanying Notes |

|

Consolidated Statement of Assets and Liabilities PIMCO EqS Pathfinder Portfolio™

|

|

|

|

|

| (Amounts in thousands, except per share amounts) |

|

December 31, 2011 |

|

|

|

| Assets: |

|

|

|

|

| Investments, at value |

|

$ |

416,247 |

|

| Investments in Affiliates, at value |

|

|

34,238 |

|

| Repurchase agreements, at value |

|

|

663 |

|

| Cash |

|

|

1 |

|

| Deposits with counterparty |

|

|

11,409 |

|

| Foreign currency, at value |

|

|

649 |

|

| Receivable for investments sold |

|

|

11 |

|

| Receivable for Portfolio shares sold |

|

|

94 |

|

| Interest and dividends receivable |

|

|

348 |

|

| Dividends receivable from Affiliates |

|

|

8 |

|

| Reimbursement receivable from PIMCO |

|

|

4 |

|

| Unrealized appreciation on foreign currency contracts |

|

|

4,863 |

|

| Unrealized appreciation on OTC swap agreements |

|

|

20 |

|

| |

|

|

468,555 |

|

|

|

| Liabilities: |

|

|

|

|

| Payable for investments purchased |

|

$ |

1 |

|

| Payable for investments in Affiliates purchased |

|

|

8 |

|

| Payable for short sales |

|

|

7,815 |

|

| Deposits from counterparty |

|

|

3,540 |

|

| Payable for Portfolio shares redeemed |

|

|

86 |

|

| Dividends payable |

|

|

10 |

|

| Written options outstanding |

|

|

233 |

|

| Accrued investment advisory fees |

|

|

261 |

|

| Accrued supervisory and administrative fees |

|

|

146 |

|

| Accrued distribution fees |

|

|

87 |

|

| Unrealized depreciation on foreign currency contracts |

|

|

2,259 |

|

| Unrealized depreciation on OTC swap agreements |

|

|

15 |

|

| Other liabilities |

|

|

4 |

|

| |

|

|

14,465 |

|

|

|

| Net Assets |

|

$ |

454,090 |

|

|

|

| Net Assets Consist of: |

|

|

|

|

| Paid in capital |

|

$ |

454,433 |

|

| Undistributed net investment income |

|

|

259 |

|

| Accumulated undistributed net realized (loss) |

|

|

(12,191 |

) |

| Net unrealized appreciation |

|

|

11,589 |

|

| |

|

$ |

454,090 |

|

|

|

| Net Assets: |

|

|

|

|

| Institutional Class |

|

$ |

66,439 |

|

| Advisor Class |

|

|

387,651 |

|

|

|

| Shares Issued and Outstanding: |

|

|

|

|

| Institutional Class |

|

|

6,743 |

|

| Advisor Class |

|

|

39,458 |

|

|

|

| Net Asset Value and Redemption Price Per Share (Net Asset Value Per Share Outstanding): |

|

|

|

|

| Institutional Class |

|

$ |

9.85 |

|

| Advisor Class |

|

|

9.82 |

|

|

|

| Cost of Investments |

|

$ |

407,210 |

|

| Cost of Investments in Affiliates |

|

$ |

34,237 |

|

| Cost of Repurchase Agreements |

|

$ |

663 |

|

| Cost of Foreign Currency Held |

|

$ |

650 |

|

| Proceeds Received on Short Sales |

|

$ |

7,710 |

|

| Premiums Received on Written Options |

|

$ |

372 |

|

|

|

|

|

|

|

|

| See Accompanying Notes |

|

DECEMBER 31, 2011 |

|

ANNUAL REPORT |

|

9 |

Consolidated Statement of Operations PIMCO EqS Pathfinder Portfolio™

|

|

|

|

|

| (Amounts in thousands) |

|

Year Ended

December 31, 2011 |

|

|

|

| Investment Income: |

|

|

|

|

| Interest |

|

$ |

14 |

|

| Dividends, net of foreign taxes* |

|

|

2,778 |

|

| Dividends from Affiliate investments |

|

|

33 |

|

| Total Income |

|

|

2,825 |

|

|

|

| Expenses: |

|

|

|

|

| Investment advisory fees |

|

|

1,050 |

|

| Supervisory and administrative fees |

|

|

489 |

|

| Distribution and/or servicing fees – Advisor Class |

|

|

287 |

|

| Dividends on short sales |

|

|

11 |

|

| Trustees’ fees |

|

|

60 |

|

| Interest expense |

|

|

3 |

|

| Total Expenses |

|

|

1,900 |

|

| Waiver by PIMCO |

|

|

(267 |

) |

| Net Expenses |

|

|

1,633 |

|

|

|

| Net Investment Income |

|

|

1,192 |

|

|

|

| Net Realized and Unrealized Gain (Loss): |

|

|

|

|

| Net realized (loss) on investments |

|

|

(12,410 |

) |

| Net realized gain on Affiliate investments |

|

|

3 |

|

| Net realized gain on futures contracts, written options and swaps |

|

|

255 |

|

| Net realized (loss) on short sales |

|

|

(4 |

) |

| Net realized (loss) on foreign currency transactions |

|

|

(796 |

) |

| Net change in unrealized appreciation on investments |

|

|

8,588 |

|

| Net change in unrealized appreciation on Affiliate investments |

|

|

1 |

|

| Net change in unrealized appreciation on futures contracts, written options and

swaps |

|

|

144 |

|

| Net change in unrealized appreciation on short sales |

|

|

104 |

|

| Net change in unrealized appreciation on translation of assets and liabilities denominated in

foreign currencies |

|

|

2,504 |

|

| Net (Loss) |

|

|

(1,611 |

) |

|

|

| Net (Decrease) in Net Assets Resulting from Operations |

|

$ |

(419 |

) |

|

|

| *Foreign tax withholdings – Dividends |

|

$ |

140 |

|

|

|

|

|

|

|

|

|

|

| 10 |

|

PIMCO EQUITY SERIES VIT |

|

|

|

|

See Accompanying Notes |

|

Consolidated Statements of Changes in Net Assets PIMCO EqS Pathfinder Portfolio™

|

|

|

|

|

|

|

|

|

| (Amounts In thousands) |

|

Year Ended

December 31, 2011 |

|

|

Period From

April 14, 2011-December 31, 2010 |

|

|

|

|

| Increase in Net Assets from: |

|

|

|

|

|

|

|

|

|

|

|

| Operations: |

|

|

|

|

|

|

|

|

| Net investment income |

|

$ |

1,192 |

|

|

$ |

45 |

|

| Net realized (loss) |

|

|

(12,955 |

) |

|

|

(71 |

) |

| Net realized gain on Affiliate investments |

|

|

3 |

|

|

|

0 |

|

| Net change in unrealized appreciation |

|

|

11,340 |

|

|

|

248 |

|

| Net change in unrealized appreciation on Affiliate investments |

|

|

1 |

|

|

|

0 |

|

| Net increase (decrease) resulting from operations |

|

|

(419 |

) |

|

|

222 |

|

|

|

|

| Distributions to Shareholders: |

|

|

|

|

|

|

|

|

| From net investment income |

|

|

|

|

|

|

|

|

| Institutional Class |

|

|

(75 |

) |

|

|

0 |

|

| Advisor Class |

|

|

(138 |

) |

|

|

0 |

|

|

|

|

| Total Distributions |

|

|

(213 |

) |

|

|

0 |

|

|

|

|

| Portfolio Share Transactions: |

|

|

|

|

|

|

|

|

| Net increase resulting from Portfolio share transactions** |

|

|

448,948 |

|

|

|

5,552 |

|

|

|

|

| Total Increase in Net Assets |

|

|

448,316 |

|

|

|

5,774 |

|

|

|

|

| Net Assets: |

|

|

|

|

|

|

|

|

| Beginning of year or period |

|

|

5,774 |

|

|

|

0 |

|

| End of year* |

|

$ |

454,090 |

|

|

$ |

5,774 |

|

|

|

|

| *Including undistributed net investment income of: |

|

$ |

259 |

|

|

$ |

22 |

|

| ** |

See note 11 in the Notes to Financial Statements. |

|

|

|

|

|

|

|

| See Accompanying Notes |

|

DECEMBER 31, 2011 |

|

ANNUAL REPORT |

|

11 |

Consolidated Schedule of Investments PIMCO EqS Pathfinder Portfolio™

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

SHARES |

|

|

|

|

MARKET VALUE (000S) |

|

| COMMON STOCKS 86.6% |

|

|

|

| BERMUDA 6.1% |

|

|

|

| ENERGY 2.7% |

|

| North

Atlantic Drilling Ltd. |

|

|

|

|

3,077,543 |

|

|

$ |

|

|

4,760 |

|

| Seadrill

Ltd. |

|

|

|

|

223,835 |

|

|

|

|

|

7,464 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

12,224 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FINANCIALS 3.4% |

|

| Hiscox

Ltd. |

|

|

|

|

1,011,892 |

|

|

|

|

|

5,860 |

|

| Lancashire

Holdings Ltd. |

|

|

|

|

834,820 |

|

|

|

|

|

9,397 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

15,257 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Bermuda |

|

|

|

|

|

|

|

|

|

|

27,481 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| BRAZIL 1.0% |

|

|

|

| FINANCIALS 1.0% |

|

| Itau

Unibanco Holding S.A. SP - ADR |

|

|

|

|

256,175 |

|

|

|

|

|

4,755 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Brazil |

|

|

|

|

|

|

|

|

|

|

4,755 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| CANADA 1.5% |

|

|

|

| MATERIALS 1.5% |

|

| Cameco

Corp. |

|

|

|

|

154,112 |

|

|

|

|

|

2,782 |

|

| Kinross Gold

Corp. |

|

|

|

|

168,579 |

|

|

|

|

|

1,922 |

|

| Silver

Wheaton Corp. |

|

|

|

|

75,557 |

|

|

|

|

|

2,188 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

6,892 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Canada |

|

|

|

|

|

|

|

|

|

|

6,892 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| DENMARK 2.0% |

|

|

|

| CONSUMER STAPLES 1.5% |

|

| Carlsberg

A/S |

|

|

|

|

99,326 |

|

|

|

|

|

6,994 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FINANCIALS 0.5% |

|

| Jyske Bank

A/S (a) |

|

|

|

|

83,722 |

|

|

|

|

|

2,052 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Denmark |

|

|

|

|

|

|

|

|

|

|

9,046 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FAEROE ISLANDS 0.4% |

|

|

|

| CONSUMER STAPLES 0.3% |

|

| Bakkafrost

P/F |

|

|

|

|

199,159 |

|

|

|

|

|

1,219 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FINANCIALS 0.1% |

|

| BankNordik

P/F |

|

|

|

|

52,480 |

|

|

|

|

|

731 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Faeroe Islands |

|

|

|

|

|

|

|

|

|

|

1,950 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FRANCE 10.0% |

|

|

|

| CONSUMER DISCRETIONARY 3.0% |

|

| Eutelsat

Communications S.A. |

|

|

|

|

156,431 |

|

|

|

|

|

6,093 |

|

| JCDecaux

S.A. (a) |

|

|

|

|

109,825 |

|

|

|

|

|

2,521 |

|

|

Teleperformance

S.A. |

|

|

|

|

216,278 |

|

|

|

|

|

4,805 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

13,419 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| CONSUMER STAPLES 6.5% |

|

| Carrefour

S.A. |

|

|

|

|

341,156 |

|

|

|

|

|

7,762 |

|

|

Danone |

|

|

|

|

182,633 |

|

|

|

|

|

11,461 |

|

| L’Oreal

S.A. |

|

|

|

|

21,550 |

|

|

|

|

|

2,244 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

SHARES |

|

|

|

|

MARKET VALUE (000S) |

|

|

Pernod-Ricard

S.A. |

|

|

|

|

86,614 |

|

|

$ |

|

|

8,017 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

29,484 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ENERGY 0.5% |

|

| Bourbon

S.A. |

|

|

|

|

83,881 |

|

|

|

|

|

2,297 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total France |

|

|

|

|

|

|

|

|

|

|

45,200 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| GERMANY 1.4% |

|

|

|

| HEALTH CARE 0.5% |

|

| Rhoen

Klinikum AG |

|

|

|

|

110,904 |

|

|

|

|

|

2,111 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INDUSTRIALS 0.3% |

|

|

Kloeckner & Co.

SE |

|

|

|

|

93,597 |

|

|

|

|

|

1,198 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| UTILITIES 0.6% |

|

| E.ON

AG |

|

|

|

|

130,509 |

|

|

|

|

|

2,812 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Germany |

|

|

|

|

|

|

|

|

|

|

6,121 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| GUERNSEY, CHANNEL ISLANDS 0.9% |

|

|

|

| FINANCIALS 0.9% |

|

| Resolution

Ltd. |

|

|

|

|

1,085,376 |

|

|

|

|

|

4,231 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Guernsey, Channel Islands |

|

|

|

|

|

|

|

|

|

|

4,231 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| HONG KONG 3.0% |

|

|

|

| CONSUMER DISCRETIONARY 0.4% |

|

| Television

Broadcasts Ltd. |

|

|

|

|

286,000 |

|

|

|

|

|

1,732 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FINANCIALS 2.3% |

|

| AIA Group

Ltd. |

|

|

|

|

2,518,400 |

|

|

|

|

|

7,840 |

|

| First

Pacific Co. Ltd. |

|

|

|

|

2,526,000 |

|

|

|

|

|

2,627 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

10,467 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INDUSTRIALS 0.3% |

|

| Jardine

Matheson Holdings Ltd. |

|

|

|

|

20,300 |

|

|

|

|

|

954 |

|

| Jardine

Strategic Holdings Ltd. |

|

|

|

|

23,700 |

|

|

|

|

|

655 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

1,609 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Hong Kong |

|

|

|

|

|

|

|

|

|

|

13,808 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ISRAEL 0.6% |

|

|

|

| HEALTH CARE 0.6% |

|

| Teva

Pharmaceutical Industries Ltd. SP - ADR |

|

|

|

|

68,846 |

|

|

|

|

|

2,779 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Israel |

|

|

|

|

|

|

|

|

|

|

2,779 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| JAPAN 1.5% |

|

|

|

| INFORMATION TECHNOLOGY 1.5% |

|

| Nintendo Co.

Ltd. |

|

|

|

|

48,717 |

|

|

|

|

|

6,688 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Japan |

|

|

|

|

|

|

|

|

|

|

6,688 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| NETHERLANDS 5.8% |

|

|

|

| CONSUMER STAPLES 1.2% |

|

|

CSM |

|

|

|

|

359,506 |

|

|

|

|

|

5,588 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

SHARES |

|

|

|

|

MARKET VALUE (000S) |

|

| ENERGY 0.9% |

|

| Royal Dutch

Shell PLC ‘A’ |

|

|

|

|

105,104 |

|

|

$ |

|

|

3,856 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FINANCIALS 1.3% |

|

| ING Groep NV

- Dutch Certificate (a) |

|

|

|

|

827,071 |

|

|

|

|

|

5,915 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INFORMATION TECHNOLOGY 0.5% |

|

| Gemalto

NV |

|

|

|

|

49,524 |

|

|

|

|

|

2,400 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| TELECOMMUNICATION SERVICES 1.9% |

|

| Koninklijke

KPN NV |

|

|

|

|

698,996 |

|

|

|

|

|

8,344 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Netherlands |

|

|

|

|

|

|

|

|

|

|

26,103 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| NORWAY 1.5% |

|

|

|

| CONSUMER STAPLES 0.9% |

|

| Marine

Harvest ASA |

|

|

|

|

9,741,864 |

|

|

|

|

|

4,201 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INDUSTRIALS 0.6% |

|

| Orkla

ASA |

|

|

|

|

322,316 |

|

|

|

|

|

2,400 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Norway |

|

|

|

|

|

|

|

|

|

|

6,601 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| SINGAPORE 0.7% |

|

|

|

| FINANCIALS 0.0% |

|

| Great

Eastern Holdings Ltd. |

|

|

|

|

1,160 |

|

|

|

|

|

11 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INDUSTRIALS 0.7% |

|

| Keppel Corp.

Ltd. |

|

|

|

|

452,700 |

|

|

|

|

|

3,241 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Singapore |

|

|

|

|

|

|

|

|

|

|

3,252 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| SOUTH AFRICA 0.9% |

|

|

|

| MATERIALS 0.9% |

|

| AngloGold

Ashanti Ltd. SP - ADR |

|

|

|

|

99,032 |

|

|

|

|

|

4,204 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total South Africa |

|

|

|

|

|

|

|

|

|

|

4,204 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| SOUTH KOREA 0.5% |

|

|

|

| CONSUMER DISCRETIONARY 0.5% |

|

| GS Home

Shopping, Inc. |

|

|

|

|

21,083 |

|

|

|

|

|

2,126 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total South Korea |

|

|

|

|

|

|

|

|

|

|

2,126 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| SPAIN 0.3% |

|

|

|

| CONSUMER STAPLES 0.3% |

|

|

Distribuidora Internacional de

Alimentacion S.A. (a) |

|

|

|

|

270,409 |

|

|

|

|

|

1,217 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Spain |

|

|

|

|

|

|

|

|

|

|

1,217 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| SWEDEN 1.0% |

|

|

|

| CONSUMER DISCRETIONARY 1.0% |

|

| Loomis

AB |

|

|

|

|

315,094 |

|

|

|

|

|

4,527 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Sweden |

|

|

|

|

|

|

|

|

|

|

4,527 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| SWITZERLAND 4.1% |

|

|

|

| CONSUMER STAPLES 1.3% |

|

| Nestle

S.A. |

|

|

|

|

105,866 |

|

|

|

|

|

6,079 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| 12 |

|

PIMCO EQUITY SERIES VIT |

|

|

|

|

See Accompanying Notes |

|

December 31, 2011

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

SHARES |

|

|

|

|

MARKET VALUE (000S) |

|

| HEALTH CARE 1.7% |

|

| Novartis

AG |

|

|

|

|

18,590 |

|

|

$ |

|

|

1,061 |

|

| Roche

Holding AG |

|

|

|

|

39,184 |

|

|

|

|

|

6,627 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7,688 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| INDUSTRIALS 0.7% |

|

| Schindler

Holding AG |

|

|

|

|

25,635 |

|

|

|

|

|

2,971 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| MATERIALS 0.4% |

|

| Sika

AG |

|

|

|

|

1,086 |

|

|

|

|

|

2,042 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total Switzerland |

|

|

|

|

|

|

|

|

|

|

18,780 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| UNITED KINGDOM 11.9% |

|

|

|

| CONSUMER DISCRETIONARY 0.5% |

|

| British Sky

Broadcasting Group PLC |

|

|

|

|

187,957 |

|

|

|

|

|

2,138 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| CONSUMER STAPLES 7.3% |

|

| British

American Tobacco PLC |

|

|

|

|

281,362 |

|

|

|

|

|

13,348 |

|

| Imperial

Tobacco Group PLC |

|

|

|

|

409,244 |

|

|

|

|

|

15,486 |

|

| Reckitt

Benckiser Group PLC |

|

|

|

|

87,011 |

|

|

|

|

|

4,291 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

33,125 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| ENERGY 2.6% |

|

| BP

PLC |

|

|

|

|

1,205,905 |

|

|

|

|

|

8,590 |

|

| Ensco PLC SP

- ADR |

|

|

|

|

70,876 |

|

|

|

|

|

3,326 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

11,916 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FINANCIALS 1.5% |

|

| Barclays

PLC |

|

|

|

|

960,761 |

|

|

|

|

|

2,631 |

|

| Lloyds

Banking Group PLC (a) |

|

|

|

|

10,987,550 |

|

|

|

|

|

4,414 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

7,045 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total United Kingdom |

|

|

|

|

|

54,224 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| UNITED STATES 31.5% |

|

|

|

| CONSUMER STAPLES 7.7% |

|

| Altria

Group, Inc. |

|

|

|

|

202,101 |

|

|

|

|

|

5,992 |

|

| CVS Caremark

Corp. |

|

|

|

|

198,833 |

|

|

|

|

|

8,109 |

|

| Lorillard,

Inc. |

|

|

|

|

82,773 |

|

|

|

|

|

9,436 |

|

| Philip

Morris International, Inc. |

|

|

|

|

60,515 |

|

|

|

|

|

4,749 |

|

| Reynolds

American, Inc. |

|

|

|

|

100,007 |

|

|

|

|

|

4,142 |

|

| Wal-Mart

Stores, Inc. |

|

|

|

|

40,407 |

|

|

|

|

|

2,415 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

34,843 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| FINANCIALS 9.4% |

|

| Alleghany

Corp. (a) |

|

|

|

|

11,995 |

|

|

|

|

|

3,422 |

|

| BankUnited,

Inc. |

|

|

|

|

253,745 |

|

|

|

|

|

5,580 |

|

| Berkshire

Hathaway, Inc. ‘B’ (a) |

|

|

|

|

107,753 |

|

|

|

|

|

8,221 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

SHARES |

|

|

|

|

MARKET VALUE (000S) |

|

| Capitol

Federal Financial, Inc. |

|

|

|

|

81,325 |

|

|

$ |

|

|

938 |

|

| CBOE

Holdings, Inc. |

|

|

|

|

183,408 |

|

|

|

|

|

4,743 |

|

| Northwest

Bancshares, Inc. |

|

|

|

|

241,285 |

|

|

|

|

|