UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934. For the fiscal year ended |

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Date of event requiring this shell company report

For the transition period from ________ to ________

Commission File No.

|

(Exact name of registrant as specified in its charter) |

(Jurisdiction of incorporation or organization)

(Address of principal executive offices)

Intellipharmaceutics International Inc.,

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

Title of each class |

| Trading Symbol(s) |

| Name of each exchange on which registered |

None |

|

|

|

|

Securities registered or to be registered pursuant to Section 12(g) of the Act:

None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

Common shares, no par value

As of November 30, 2021, the registrant had

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ☐

If this report is an annual report or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934.

Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or an emerging growth company. See definition of “large accelerated filer”, “accelerated filer” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer | ☐ | Accelerated filer | ☐ |

| ☒ | Emerging growth company |

If an emerging growth company that prepares its financial statements in accordance with U.S. GAAP, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards† provided pursuant to Section 13(a) of the Exchange Act. ☐

† The term “new or revised financial accounting standard” refers to any update issued by the Financial Accounting Standards Board to its Accounting Standards Codification after April 5, 2012.

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting over Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

☒ | International Financial Reporting Standards as issued by the International Accounting Standards Board | ☐ | Other | ☐ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow:

Item 17 ☐ Item 18 ☐

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

TABLE OF CONTENTS

|

|

| Page |

|

|

| 3 |

| |

| 3 |

| ||

| 3 |

| ||

| 3 |

| ||

| 3 |

| ||

| 3 |

| ||

| 3 |

| ||

| 3 |

| ||

| 3 |

| ||

| 3 |

| ||

| 4 |

| ||

| 4 |

| ||

| 4 |

| ||

| 31 |

| ||

| 31 |

| ||

| 32 |

| ||

| 56 |

| ||

| 57 |

| ||

| 57 |

| ||

| 57 |

| ||

| 58 |

| ||

| 62 |

| ||

| 64 |

| ||

| 64 |

| ||

| 65 |

| ||

| 65 |

| ||

| 66 |

| ||

| 66 |

| ||

| 66 |

| ||

| 68 |

| ||

| 77 |

| ||

| 81 |

| ||

| 81 |

| ||

| 90 |

| ||

| 90 |

| ||

| 91 |

| ||

| 92 |

| ||

| 92 |

| ||

| 95 |

| ||

| 95 |

| ||

| 95 |

| ||

| 95 |

|

i |

| Table of Contents |

| 99 |

| ||

| 100 |

| ||

| 102 |

| ||

| 103 |

| ||

| 112 |

| ||

| 112 |

| ||

| 112 |

| ||

| 112 |

| ||

| 112 |

| ||

| 114 |

| ||

| 114 |

| ||

| 114 |

| ||

| 114 |

| ||

| 114 |

| ||

|

| 115 |

| |

| 115 |

| ||

Material Modifications to the Rights of Security Holders and Use of Proceeds |

| 115 |

| |

| 115 |

| ||

| 116 |

| ||

| 116 |

| ||

| 116 |

| ||

| 116 |

| ||

| 117 |

| ||

Purchases of Equity Securities by the Issuer and Affiliated Purchasers. |

| 117 |

| |

| 117 |

| ||

| 117 |

| ||

| 117 |

| ||

|

| 118 |

| |

| 118 |

| ||

| 118 |

| ||

| 119 |

|

ii |

| Table of Contents |

DISCLOSURE REGARDING FORWARD-LOOKING INFORMATION

Certain statements in this annual report constitute “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and/or “forward-looking information” under the Securities Act (Ontario). These statements include, without limitation, statements expressed or implied regarding our expectations, plans, goals and milestones, status of developments or expenditures relating to our business, plans to fund our current activities, and statements concerning our partnering activities, health regulatory submissions, strategy, future operations, future financial position, future sales, revenues and profitability, projected costs and market penetration and risks or uncertainties arising from the delisting of our shares from Nasdaq and our ability to comply with OTCQB Venture Market (“OTCQB”) and Toronto Stock Exchange (“TSX”) requirements. In some cases, you can identify forward-looking statements by terminology such as “appear”, “unlikely”, “target”, “may”, “will”, “should”, “expects”, “plans”, “plans to”, “anticipates”, “believes”, “estimates”, “predicts”, “confident”, “prospects”, “potential”, “continue”, “intends”, “look forward”, “could”, “would”, “projected”, “goals”, “set to”, “seeking” or the negative of such terms or other comparable terminology. We made a number of assumptions in the preparation of our forward-looking statements. You should not place undue reliance on our forward-looking statements, which are subject to a multitude of known and unknown risks and uncertainties that could cause actual results, future circumstances or events to differ materially from those stated in or implied by the forward-looking statements. Risks, uncertainties and other factors that could affect our actual results include, but are not limited to, the effects of general economic conditions, securing and maintaining corporate alliances, our estimates regarding our capital requirements, and the effect of capital market conditions and other factors, including the current status of our product development programs, capital availability, the estimated proceeds (and the expected use of any proceeds) we may receive from any offering of our securities, the potential dilutive effects of any financing, potential liability from and costs of defending pending or future litigation, risks associated with the novel coronavirus (COVID-19), including its impact on our business and operations, our programs regarding research, development and commercialization of our product candidates, the timing of such programs, the timing, costs and uncertainties regarding obtaining regulatory approvals to market our product candidates and the difficulty in predicting the timing and results of any product launches, the timing and amount of profit-share payments from our commercial partners, and the timing and amount of any available investment tax credits, the actual or perceived benefits to users of our drug delivery technologies, products and product candidates as compared to others, our ability to establish and maintain valid and enforceable intellectual property rights in our drug delivery technologies, products and product candidates, the scope of protection provided by intellectual property rights for our drug delivery technologies, products and product candidates, recent and future legal developments in the United States and elsewhere that could make it more difficult and costly for us to obtain regulatory approvals for our product candidates and negatively affect the prices we may charge, increased public awareness and government scrutiny of the problems associated with the potential for abuse of opioid-based medications, pursuing growth through international operations could strain our resources, our limited manufacturing, sales, marketing and distribution capability and our reliance on third parties for such, the actual size of the potential markets for any of our products and product candidates compared to our market estimates, our selection and licensing of products and product candidates, our ability to attract distributors and/or commercial partners with the ability to fund patent litigation and with acceptable product development, regulatory and commercialization expertise and the benefits to be derived from such collaborative efforts, sources of revenues and anticipated revenues, including contributions from distributors and commercial partners, product sales, license agreements and other collaborative efforts for the development and commercialization of product candidates, our ability to create an effective direct sales and marketing infrastructure for products we elect to market and sell directly, the rate and degree of market acceptance of our products, delays in product approvals that may be caused by changing regulatory requirements, the difficulty in predicting the timing of regulatory approval and launch of competitive products, the difficulty in predicting the impact of competitive products on sales volume, pricing, rebates and other allowances, the number of competitive product entries, and the nature and extent of any aggressive pricing and rebate activities that may follow, the inability to forecast wholesaler demand and/or wholesaler buying patterns, seasonal fluctuations in the number of prescriptions written for our generic Focalin XR® capsules, which may produce substantial fluctuations in revenue, the timing and amount of insurance reimbursement regarding our products, changes in laws and regulations affecting the conditions required by the United States Food and Drug Administration (“FDA”) for approval, testing and labeling of drugs including abuse or overdose deterrent properties, and changes affecting how opioids are regulated and prescribed by physicians, changes in laws and regulations, including Medicare and Medicaid, affecting among other things, pricing and reimbursement of pharmaceutical products, the effect of changes in U.S. federal income tax laws, including but not limited to, limitations on the deductibility of business interest, limitations on the use of net operating losses and application of the base erosion minimum tax, on our U.S. corporate income tax burden, the success and pricing of other competing therapies that may become available, our ability to retain and hire qualified employees, the availability and pricing of third-party sourced products and materials, challenges related to the development, commercialization, technology transfer, scale-up, and/or process validation of manufacturing processes for our products or product candidates, the manufacturing capacity of third-party manufacturers that we may use for our products, potential product liability risks, the recoverability of the cost of any pre-launch inventory, should a planned product launch encounter a denial or delay of approval by regulatory bodies, a delay in commercialization, or other potential issues, the successful compliance with FDA, Health Canada and other governmental regulations applicable to us and our third party manufacturers’ facilities, products and/or businesses, our reliance on commercial partners, and any future commercial partners, to market and commercialize our products and, if approved, our product candidates, difficulties, delays, or changes in the FDA approval process or test criteria for Abbreviated New Drug Applications (“ANDAs”) and New Drug Applications (“NDAs”), challenges in securing final FDA approval for our product candidates, including our oxycodone hydrochloride extended release tablets (“Aximris XRTM”) product candidate, in particular, if a patent infringement suit is filed against us with respect to any particular product candidates (such as in the case of Oxycodone ER), which could delay the FDA’s final approval of such product candidates, healthcare reform measures that could hinder or prevent the commercial success of our products and product candidates, the risk that the FDA may not approve requested product labeling for our product candidate(s) having abuse-deterrent properties and targeting common forms of abuse (oral, intra-nasal and intravenous), risks associated with cyber-security and the potential vulnerability of our digital information or the digital information of a current and/or future drug development or commercialization partner of ours, and risks arising from the ability and willingness of our third-party commercialization partners to provide documentation that may be required to support information on revenues earned by us from those commercialization partners.

| 1 |

| Table of Contents |

Additional risks and uncertainties relating to us and our business can be found in the “Risk Factors” section in Item 3.D below, the “Risk Factors” sections of our latest annual information form and our latest registration statements on Form F-1 and F-3 (including any documents forming a part thereof or incorporated by reference therein), as amended, as well as in our reports, public disclosure documents and other filings with the securities commissions and other regulatory bodies in Canada and the U.S., which are available on www.sedar.com and www.sec.gov. The forward-looking statements reflect our current views with respect to future events, and are based on what we believe are reasonable assumptions as of the date of this document and we disclaim any intention and have no obligation or responsibility, except as required by law, to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Nothing contained in this document should be construed to imply that the results discussed herein will necessarily continue into the future, or that any conclusion reached herein will necessarily be indicative of our actual operating results.

In this annual report, unless the context otherwise requires, the terms “we”, “us”, “our”, “Intellipharmaceutics,” and the “Company” refer to Intellipharmaceutics International Inc. and its subsidiaries. Any reference in this annual report to our “products” includes a reference to our product candidates and future products we may develop. Whenever we refer to any of our current product candidates (including additional product strengths of products we are currently marketing) and future products we may develop, no assurances can be given that we, or any of our strategic partners, will successfully commercialize or complete the development of any of such product candidates or future products under development or proposed for development, that regulatory approvals will be granted for any such product candidate or future product, or that any approved product will be produced in commercial quantities or sold profitably.

Unless stated otherwise, all references to “$”, “U.S.$”, or “U.S. Dollars” are to the lawful currency of the United States and all references to “C$” are to the lawful currency of Canada. In this annual report, we refer to information regarding potential markets for our products, product candidates and other industry data. We believe that all such information has been obtained from reliable sources that are customarily relied upon by companies in our industry. However, we have not independently verified any such information.

Intellipharmaceutics™, Hypermatrix™, Drug Delivery Engine™, IntelliFoam™, IntelliGITransporter™, IntelliMatrix™, IntelliOsmotics™, IntelliPaste™, IntelliPellets™, IntelliShuttle™, nPODDDS™, PODRAS™.Regabatin™ XR and Aximris XR™ are our trademarks. These trademarks are important to our business. Although we may have omitted the “TM” trademark designation for such trademarks in this annual report, all rights to such trademarks are nevertheless reserved. Unless otherwise noted, other trademarks used in this annual report are the property of their respective holders.

We initially named our oxycodone hydrochloride extended-release tablets “Rexista™,” but later changed the name of our product candidate to “Aximris XR™”as the FDA did not approve the proposed name “Rexista”. References in this annual report, and/or the documents incorporated by reference herein or therein to Oxycodone ER,Rexista™ or Aximris XR™ are intended to refer to our oxycodone hydrochloride extended release tablets product candidate.

Unless the context otherwise requires, references in this document to (i) share amounts, per share data, share prices, exercise prices and conversion rates have been adjusted to reflect the effect of the 1-for-10 reverse split (the “reverse split”) which became effective on each of Nasdaq and TSX at the open of market on September 14, 2018, and (ii) ”consolidation” or “share consolidation” are intended to refer to such reverse split. The common shares of the Company are currently traded on the OTCQB and the TSX.

2 |

| Table of Contents |

PART I

Item 1. Identity of Directors, Senior Management and Advisers

A. Directors and Senior Management

Not applicable.

B. Advisers

Not applicable.

C. Auditors

Not applicable.

Item 2 Offer Statistics and Expected Timetable

A. Offer statistics

Not applicable.

B. Method and expected timetable

Not applicable.

Item 3. Key Information

A. Selected Financial Data

The following selected financial data of the Company has been derived from the audited consolidated financial statements of the Company as at and for the years ended November 30, 2021, 2020, 2019, 2018, and 2017.As a result of the IPC Arrangement Transaction (as defined and described in Item 4.A below) completed on October 22, 2009, we selected a November 30 year end. The comparative number of shares issued and outstanding, basic and diluted loss per share have been amended to give effect to this arrangement transaction. These statements were prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). All dollar amounts in this annual report are expressed in U.S. dollars, unless otherwise indicated.

| 3 |

| Table of Contents |

(In thousands of U.S. dollars, except for per share data)

|

| As at and for the year ended November 30, 2021 |

|

| As at and for the year ended November 30, 2020 |

|

| As at and for the year ended November 30, 2019 |

|

| As at and for the year ended November 30, 2018 |

|

| As at and for the year ended November 30, 2017 |

| |||||

Revenue |

| Nil |

|

|

| 1,402 |

|

|

| 3,481 |

|

|

| 1,713 |

|

|

| 5,504 |

| |

Loss for the year |

|

| (5,145 | ) |

|

| (3,391 | ) |

|

| (8,085 | ) |

|

| (13,747 | ) |

|

| (8,857 | ) |

Total assets |

|

| 2,096 |

|

|

| 3,387 |

|

|

| 3,797 |

|

|

| 11,474 |

|

|

| 7,397 |

|

Total liabilities |

|

| 10,252 |

|

|

| 9,701 |

|

|

| 7,489 |

|

|

| 7,372 |

|

|

| 7,010 |

|

Net assets |

|

| (8,155 | ) |

|

| (6,314 | ) |

|

| (3,692 | ) |

|

| 4,102 |

|

|

| 386 |

|

Capital stock |

|

| 49,176 |

|

|

| 46,144 |

|

|

| 45,561 |

|

|

| 44,328 |

|

|

| 35,290 |

|

Loss per share - basic and diluted |

|

| (0.17 | ) |

|

| (0.14 | ) |

|

| (0.37 | ) |

|

| (2.89 | ) |

|

| (2.86 | ) |

Dividends |

| Nil |

|

| Nil |

|

| Nil |

|

| Nil |

|

| Nil |

| |||||

Weighted average common shares |

|

| 29,430 |

|

|

| 23,562 |

|

|

| 21,580 |

|

|

| 4,762 |

|

|

| 3,101 |

|

B. Capitalization and Indebtedness

Not applicable.

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

Prospects for companies in the pharmaceutical industry generally may be regarded as uncertain given the research and development (“R&D”) nature of the industry and uncertainty regarding the prospects of successfully commercializing product candidates and, accordingly, investments in companies such as ours should be regarded as very speculative. An investor should carefully consider the risks and uncertainties described below, as well as other information contained in this annual report. The list of risks and uncertainties described below is not an exhaustive list. Additional risks and uncertainties not presently known to us or that we believe to be immaterial may also adversely affect our business. If any one or more of the following risks occur, our business, financial condition and results of operations could be seriously harmed. Further, if we fail to meet the expectations of the public market in any given period, the market price of our common shares could decline. If any of the following risks actually occurs, our business, operating results, or financial condition could be materially adversely affected.

Our activities entail significant risks. In addition to the usual risks associated with a business, the following is a general description of certain significant risk factors which may be applicable to us.

Risks related to our Company

We have a history of operating losses, which may continue for the foreseeable future and our auditors have indicated that there is a substantial doubt about our ability to continue as a going concern.

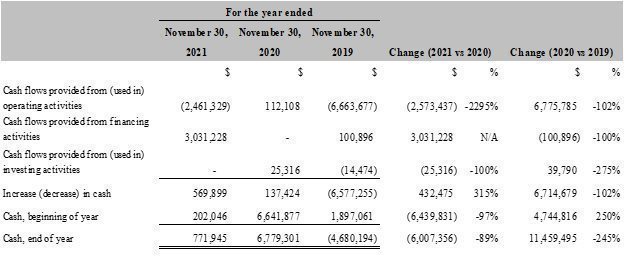

To date, we have not been profitable and have incurred significant losses and cash flow deficits. For fiscal year ended November 30, 2021, we reported net losses of $5,145,155, and negative cash flow from operating activities of $2,461,329. As of November 30, 2021, we had an aggregate accumulated deficit of $102,241,705. We anticipate that we will continue to report losses as well as negative operating cash flow. As a result of these net losses and other factors our independent auditors issued an audit opinion with respect to our financial statements for the three years ended November 30, 2021that indicated that there is a substantial doubt about our ability to continue as a going concern.

| 4 |

| Table of Contents |

There can be no assurance that we will ever be able to achieve or sustain profitability or positive cash flow. In addition to the other factors described in this annual report, our ultimate success will depend on how many of our product candidates receive approval by the FDA or Health Canada and the regulatory authorities of the other countries in which our products are proposed to be sold and whether we are able to successfully market approved products. We cannot be certain that we will be able to receive FDA, Health Canada or such other regulatory approval for any of our current or future product candidates, or that we will reach the level of sales and revenues necessary to achieve and sustain profitability. If we are unsuccessful in commercializing our products and/or securing sufficient financing, we may need to cease or curtail our operations.

Our financial statements do not include any adjustments that might result from the outcome of this uncertainty. These adjustments would likely include substantial impairment of the carrying amount of our assets and potential contingent liabilities that may arise if we are unable to fulfill various operational commitments. In addition, the value of our securities would be greatly impaired. Our ability to continue as a going concern is dependent upon generating sufficient cash flow from operations and obtaining additional capital and financing. If our ability to generate cash flow from operations is delayed or reduced and we are unable to raise additional funding from other sources, we may be unable to continue in business.

Our business is capital intensive and requires significant investment to conduct the research and development, clinical and regulatory activities necessary to bring our products to market, which capital may not be available in amounts or on terms acceptable to us, if at all.

Our business requires substantial capital investment to conduct our R&D, clinical and regulatory activities, to defend against patent litigation claims, and to establish commercial manufacturing, marketing and sales capabilities. As of November 30, 2021, our cash balance was $771,945. We currently expect to meet our short-term cash requirements from quarterly profit share payments from Par and by cost savings resulting from reduced R&D activities and staffing levels, as well as from potential revenues for approved generic products or other collaborations, and other available financing. Effective May 5, 2021 our exclusive license agreements with Tris Pharma, Inc. for generic Seroquel XR®, generic Pristiq® and generic Effexor XR® were mutually terminated. Products were never supplied nor distributed under the licenses. Termination of the exclusive agreements may provide opportunity for the Company to explore options of supplying the products to multiple sources on non-exclusive bases. However, there can be no assurance that the products previously licensed to Tris Pharma will be successfully commercialized and produce significant revenues for us. We will still need to obtain additional funding to, among other things, further product commercialization activities and development of our product candidates. Potential sources of capital may include, if conditions permit, equity and/or debt financing, payments from licensing and/or development agreements and/or new strategic partnership agreements. The Company has funded its business activities principally through the issuance of securities, loans from related parties (see “Related Party Transactions” for more information related to the terms of such loans and applicable maturities) and funds from development agreements. There is no certainty that such funding will be available going forward or, if it is, whether it will be sufficient to meet our needs. Our future operations are highly dependent upon our ability to source additional funding to support advancing our product candidate pipeline through continued R&D activities and to expand our operations. Our ultimate success will depend on whether our product candidates are approved by the FDA, Health Canada, or the regulatory authorities of other countries in which our products are proposed to be sold and whether we are able to successfully market our approved products. We cannot be certain that we will receive such regulatory approval for any of our current or future product candidates, that we will reach the level of revenues necessary to achieve and sustain profitability, or that we will secure other capital sources on terms or in amounts sufficient to meet our needs, or at all. Our cash requirements for R&D during any period depend on the number and extent of the R&D activities we focus on. At present, we are focused principally on the development of 505(b)(2) product candidates, such as our Regabatin™ XR and Oxycodone ER 505(b)(2) product candidates, as well as selected generic product candidates as resources permit. Our development of Oxycodone ER required significant expenditures, including costs to defend against the Purdue (as defined below) litigation (as described in the “Legal Proceedings and Regulatory Actions” section). Some of these costs remain to be paid by the Company. For our Regabatin™ XR product candidate, Phase III clinical trials can be capital intensive, and will only be undertaken consistent with the availability of funds and a prudent cash management strategy.

| 5 |

| Table of Contents |

The availability of equity or other financing will be affected by, among other things, the results of our R&D, our ability to obtain regulatory approvals, our success in commercializing approved products with our commercial partners, the market acceptance of our products, the state of the capital markets generally, the availability of strategic alliance agreements and other relevant commercial considerations. If we raise additional funds by issuing equity securities, our then-existing security holders will likely experience dilution. Any additional indebtedness would create increased debt service obligations and could require us to agree to operating and financial covenants that would restrict our operations. In the event that we do not obtain sufficient additional capital, it will raise substantial doubt about our ability to continue as a going concern, realize our assets, and pay our liabilities as they become due. Our cash outflows are expected to consist primarily of internal and external R&D, legal and consulting expenditures to advance our product pipeline and selling, general and administrative expenses to support our commercialization efforts. Depending upon the results of our R&D programs, the impact of any litigation to which we are a party and the availability of financial resources, we could decide to accelerate, terminate, or reduce certain projects, or commence new ones. Any failure on our part, at any time, to successfully commercialize approved products or raise additional funds on terms favorable to us, or at all, may require us to significantly change or curtail our current or planned operations in order to conserve cash until such time, if ever, that sufficient proceeds from operations are generated, and could result in us not taking advantage of business opportunities, in the termination or delay of clinical trials or us not taking any necessary actions required by the FDA or Health Canada or other regulatory authorities for one or more of our product candidates, in curtailment of our product development programs designed to identify new product candidates, in the sale or assignment of rights to our technologies, products or product candidates, and/or our inability to file ANDAs, Abbreviated New Drug Submissions (“ANDSs”) or NDAs, at all or in time to competitively market our products or product candidates.

Delays, suspensions and terminations in our preclinical studies and clinical trials could result in increased costs to us and delay our ability to generate product revenues.

The commencement of clinical trials can be delayed for a variety of reasons, including delays in:

| · | demonstrating sufficient safety and efficacy to obtain regulatory approval to commence a clinical trial; |

|

|

|

| · | reaching agreement on acceptable terms with prospective contract research organizations and clinical trial sites; |

|

|

|

| · | manufacturing sufficient quantities of a drug candidate; |

|

|

|

| · | obtaining institutional review board approval to conduct a clinical trial at a prospective clinical trial site; |

|

|

|

| · | patient enrollment; and |

|

|

|

| · | for controlled substances, obtaining specific permission to conduct a study, and obtaining import and export permits to ship study samples. |

Once a clinical trial has begun, it may be delayed, suspended or terminated due to a number of factors, including:

| · | the number of patients that participate in the trial; |

|

|

|

| · | the length of time required to enroll suitable subjects; |

|

|

|

| · | the duration of patient follow-up; |

|

|

|

| · | the number of clinical sites included in the trial; |

|

|

|

| · | changes in regulatory requirements or regulatory delays or clinical holds requiring suspension or termination of the trials; |

|

|

|

| · | delays, suspensions or termination of clinical trials due to the institutional review board overseeing the study at a particular site; |

|

|

|

| · | failure to conduct clinical trials in accordance with regulatory requirements; |

|

|

|

| · | unforeseen safety issues, including serious adverse events or side effects experienced by participants; and |

|

|

|

| · | inability to manufacture, through third party manufacturers, adequate supplies of the product candidate being tested. |

Based on results at any stage of product development, we may decide to repeat or redesign preclinical studies or clinical trials, conduct entirely new studies or discontinue development of products for one or all indications. In addition, our product candidates may not demonstrate sufficient safety and efficacy in pending or any future preclinical testing or clinical trials to obtain the requisite regulatory approvals. Even if such approvals are obtained for our products, they may not be accepted in the market as a viable alternative to other products already approved or pending approvals.

| 6 |

| Table of Contents |

If we experience delays, suspensions or terminations in a preclinical study or clinical trial, the commercial prospects for our products will be harmed, and our ability to generate product revenues will be delayed or we may never be able to generate such revenues.

Loss of key scientists and/or failure to attract qualified personnel could limit our growth and negatively impact our operations.

We are dependent upon the scientific expertise of Dr. Isa Odidi, our Chairman, Chief Executive Officer and Co-Chief Scientific Officer, and Dr. Amina Odidi, our President, Chief Operating Officer and Co-Chief Scientific Officer. Although we employ other qualified scientists, Drs. Isa and Amina Odidi are our only employees with the knowledge and experience necessary for us to continue the development of controlled-release products. We do not maintain key-person life insurance on any of our officers or employees. Although we have employment agreements with key members of our management team, each of our employees may terminate his or her employment at any time. The success of our business depends, in large part, on our continued ability to attract and retain highly qualified management, scientific, manufacturing and sales and marketing personnel, on our ability to successfully integrate new employees, and on our ability to develop and maintain important relationships with leading research and medical institutions and key distributors. If we lose the services of our executive officers or other qualified personnel or are unable to attract and retain qualified individuals to fill these roles or develop key relationships, our business, financial condition and results of operations could be materially adversely affected.

Our intellectual property may not provide meaningful protection for our products and product candidates.

We hold certain U.S., Canadian and foreign patents and have pending applications for additional patents outstanding. We intend to continue to seek patent protection for, or maintain as trade secrets, all of our commercially promising drug delivery platforms and technologies. Our success depends, in part, on our and our collaborative partners’ ability to obtain and maintain patent protection for products and product candidates, maintain trade secret protection and operate without infringing the proprietary rights of third parties. Without patent and other similar protection, other companies could offer substantially identical products without incurring sizeable development costs which could diminish our ability to recover expenses of and realize profits on our developed products. If our pending patent applications are not approved, or if we are unable to obtain patents for additional developed technologies, the future protection for our technologies will remain uncertain. Furthermore, third parties may independently develop similar or alternative technologies, duplicate some or all of our technologies, design around our patented technologies or challenge our issued patents. Such third parties may have filed patent applications, or hold issued patents, relating to products or processes competitive with those we are developing or otherwise restricting our ability to do business in a particular area. If we are unable to obtain patents or otherwise protect our trade secrets or other intellectual property and operate without infringing on the proprietary rights of others, our business, financial condition and results of operations could be materially adversely affected.

We may be subject to intellectual property claims that could be costly and could disrupt our business.

Third parties may claim we have infringed their patents, trademarks, copyrights or other rights. We may be unsuccessful in defending against such claims, which could result in the inability to protect our intellectual property rights or liability in the form of substantial damages, fines or other penalties such as injunctions precluding our manufacture, importation or sales of products. The resolution of a claim could also require us to change how we do business or enter into burdensome royalty or license agreements; provided, however, we may not be able to obtain the necessary licenses on acceptable terms, or at all. Insurance coverage may be denied or may not be adequate to cover every claim that third parties could assert against us. Even unsuccessful claims could result in significant legal fees and other expenses, diversion of management’s time and disruptions in our business. Any of these claims could also harm our reputation. Any of the foregoing may have a material adverse effect upon our business and financial condition.

We are a defendant in litigation and are at risk of additional similar litigation in the future that could divert management’s attention and adversely affect our business and could subject us to significant liabilities.

We are a defendant in the litigation matters described in this annual report. The defense of such litigation may increase our expenses and divert our management’s attention and resources, and any unfavorable outcome could have a material adverse effect on our business and results of operations. Any adverse determination in such litigation, or any settlement of such litigation matters could require that we make significant payments. In addition, we may be the target of other litigation in the future. Any negative outcome in any ongoing or future litigation may have a material adverse effect on our business and financial condition.

| 7 |

| Table of Contents |

Recent and future legal developments could make it more difficult and costly for us to obtain regulatory approvals for our product candidates and negatively affect the prices we may charge.

In the United States and elsewhere, recent and proposed legal and regulatory changes to healthcare systems could prevent or delay our receipt of regulatory approval for our product candidates, restrict or regulate our post-approval marketing activities, and adversely affect our ability to profitably sell our products. We do not know whether additional legislative changes will be enacted, or whether the FDA’s regulations, guidance or interpretations will be changed, or what impact any such changes will have, if any, on our ability to obtain regulatory approvals for our product candidates. Further, the U.S. Centers for Medicare and Medicaid Services, or CMS, frequently changes product descriptors, coverage policies, product and service codes, payment methodologies and reimbursement values. Also, increased scrutiny by the U.S. Congress of the FDA’s approval process could significantly delay or prevent our receipt of regulatory approval for our product candidates and subject us to more stringent product labeling and post-marketing testing and other requirements.

We operate in a highly litigious environment.

From time to time, we may be exposed to claims and legal actions in the normal course of business. There has been substantial litigation in the pharmaceutical industry concerning the manufacture, use and sale of new products that are the subject of conflicting patent rights. When we file an ANDA or 505(b)(2) NDA for a bioequivalent version of a drug, we may, in some circumstances, be required to certify to the FDA that any patent which has been listed with the FDA as covering the branded product has expired, the date any such patent will expire, or that any such patent is invalid or will not be infringed by the manufacture, sale or use of the new drug for which the application is submitted. Approval of an ANDA is not effective until each listed patent expires, unless the applicant certifies that the patents at issue are not infringed or are invalid and so notifies the patent holder and the holder of the branded product. A patent holder may challenge a notice of non-infringement or invalidity by suing for patent infringement within 45 days of receiving notice. Such a challenge prevents FDA approval for a period which ends 30 months after the receipt of notice, or sooner if an appropriate court rules that the patent is invalid or not infringed. From time to time, in the ordinary course of business, we face and have faced such challenges and may continue to do so in the future.

As of the date of this annual report, we are not aware of any pending or threatened material litigation claims against us, other than as described in this annual report under the caption “Legal Proceedings and Regulatory Actions”. Litigation to which we are, or may be, subject could relate to, among other things, our patent and other intellectual property rights or such rights of others, business or licensing arrangements with other persons, product liability or financing activities. Such litigation could include an injunction against the manufacture or sale of one or more of our products or potential products or a significant monetary judgment, including a possible punitive damages award, or a judgment that certain of our patent or other intellectual property rights are invalid or unenforceable or infringe the intellectual property rights of others. If such litigation is commenced, our business, results of operations, financial condition and cash flows could be materially adversely affected.

We rely on maintaining as trade secrets our competitively sensitive know-how and other information, the intentional or unintentional disclosure of which could impair our competitive position.

As to many technical aspects of our business, we have concluded that competitively sensitive information is either not patentable or that for competitive reasons it is not commercially advantageous to seek patent protection. In these circumstances, we seek to protect this know-how and other proprietary information by maintaining it in confidence as a trade secret. To maintain the confidentiality of our trade secrets, we generally enter into agreements that contain confidentiality provisions with our employees, consultants, collaborators, contract manufacturers and advisors upon commencement of their relationships with us. These provisions generally require that all confidential information developed by the individual or made known to the individual by us during the course of the individual’s relationship with us be kept confidential and not disclosed to third parties. We may not have these arrangements in place in all circumstances, and the confidentiality provisions in our favor may be breached. We may not become aware of, or have adequate remedies in the event of, any such breach. In addition, in some situations, the confidentiality provisions in our favor may conflict with, or be subject to, the rights of third parties with whom our employees, consultants, collaborators, contract manufacturers or advisors have previous employment or consulting relationships. To the extent that our employees, consultants, collaborators, contract manufacturers or advisors use trade secrets or know-how owned by others in their work for us, disputes may arise as to the ownership of relative inventions. Also, others may independently develop substantially equivalent trade secrets, processes and know-how, and competitors may be able to use this information to develop products that compete with our products, which could adversely impact our business. The disclosure of our trade secrets could impair our competitive position. Adequate remedies may not exist in the event of unauthorized use or disclosure of our confidential information.

| 8 |

| Table of Contents |

Our founders potentially may be able to exercise influence over certain corporate actions.

Our founders, Drs. Amina and Isa Odidi, our President, Chief Operating Officer and Co-Chief Scientific Officer and our Chairman, Chief Executive Officer and Co-Chief Scientific Officer, respectively, and shareholders of our Company, and Odidi Holdings Inc., a privately-held company controlled by Drs. Amina and Isa Odidi, own in the aggregate approximately 1.75% of our issued and outstanding common shares as of March 31, 2022 (and collectively beneficially owned in the aggregate approximately 15.31% of our common shares, including common shares issuable upon the exercise of outstanding options and the conversion of the 2018 Debenture (as defined below), May 2019 Debenture(as defined below) and the November 2019 Debenture (as defined below and collectively with the 2018 Debenture and the May 2019 Debenture, the “Debentures”). As a result, these shareholders potentially may be able to exercise influence over matters submitted to our shareholders for approval.

Approvals for our product candidates may be delayed or become more difficult to obtain because of failure to pay FDA fees required, or if the FDA changes its approval requirements.

The FDA may institute changes to its ANDA approval requirements, which may make it more difficult or expensive for us to obtain approval for our new generic products. For instance, in July 2012, the Generic Drug User Fee Amendments of 2012 (“GDUFA”), was enacted into law. The GDUFA legislation implemented substantial fees for new ANDAs, Drug Master Files, and product and establishment fees. In return, the program is intended to provide faster and more predictable ANDA reviews by the FDA and more timely inspections of drug facilities. For the FDA’s fiscal year 2022, the annual facility fee is $210,012and the GDUFA fee is $153,686. Under GDUFA, generic product companies face significant penalties for failure to pay the new user fees, including rendering an ANDA not “substantially complete” until the fee is paid. Any failure by us or our suppliers to pay the fees or to comply with the other provisions of GDUFA may adversely impact or delay our ability to file ANDAs, obtain approvals for new generic products and generate revenues and thus may have a material adverse effect on our business, results of operations and financial condition.

We cannot ensure the availability of raw materials.

Certain raw materials necessary for the development and subsequent commercial manufacture of our product candidates may be proprietary products of other companies. While we attempt to manage the risk associated with such proprietary raw materials through contractual provisions in supply contracts, by management of inventory and by continuing to search for alternative authorized suppliers of such materials or their equivalents, if our efforts fail, or if there is a material shortage, contamination, and/or recall of such materials, the resulting scarcity, and scarcity as a result of any other reason (such as the novel coronavirus (COVID-19), could adversely affect our ability to develop or manufacture our product candidates. In addition, many third party suppliers are subject to governmental regulation and, accordingly, we are dependent on the regulatory compliance of, as well as on the strength, enforceability and terms of our various contracts with, these third party suppliers.

Further, the FDA requires identification of raw material suppliers in applications for approval of drug products. If raw materials are unavailable from a specified supplier, the supplier does not give us access to its technical information for our application or the supplier is not in compliance with FDA or other applicable requirements, FDA approval of the supplier could delay the manufacture of the drug involved. Any inability to obtain raw materials on a timely basis, or any significant price increases which cannot be passed on to our customers, could have a material adverse effect on our business, results of operations, financial condition and cash flows.

| 9 |

| Table of Contents |

Our product candidates may not be successfully developed or commercialized.

Successful development of our product candidates is highly uncertain and is dependent on numerous factors, many of which are beyond our control. Products that appear promising in research or early phases of development may fail to reach later stages of development or the market for several reasons including:

| · | for ANDA candidates, bioequivalence studies results may not meet regulatory requirements or guidelines for the demonstration of bioequivalence; |

|

|

|

| · | for NDA candidates, a product may not demonstrate acceptable large-scale clinical trial results, even though it demonstrated positive preclinical or initial clinical trial results; |

|

|

|

| · | for NDA candidates, a product may not be effective in treating a specified condition or illness; |

|

|

|

| · | a product may have harmful side effects on humans; |

|

|

|

| · | products may fail to receive the necessary regulatory approvals from the FDA or other regulatory bodies, or there may be delays in receiving such approvals; |

|

|

|

| · | changes in the approval process of the FDA or other regulatory bodies during the development period or changes in regulatory review for each submitted product application may also cause delays in the approval or result in rejection of an application; |

|

|

|

| · | difficulties may be encountered in formulating products, scaling up manufacturing processes or in getting approval for manufacturing; |

|

|

|

| · | difficulties may be encountered in the manufacture and/or packaging of our products; |

|

|

|

| · | once manufactured, our products may not meet prescribed quality assurance and stability tests; |

|

|

|

| · | manufacturing costs, pricing or reimbursement issues, other competitive therapeutics, or other commercial factors may make the product uneconomical; and |

|

|

|

| · | the proprietary rights of others, and their competing products and technologies, may prevent the product from being developed or commercialized. |

Further, success in preclinical and early clinical trials does not ensure that large-scale clinical trials will be successful, nor does success in preliminary studies for ANDA candidates or generic candidates in other jurisdictions ensure that bioequivalence studies will be successful. Results are frequently susceptible to varying interpretations that may delay, limit or prevent regulatory approvals. The length of time necessary to complete bioequivalence studies or clinical trials and to submit an application for marketing approval for a final decision by a regulatory authority varies significantly and may be difficult to predict.

As a result, there can be no assurance that any of our product candidates currently in development will ever be successfully commercialized and produce significant revenue for us.

Near-term revenue depends significantly on the success of our commercialized products.

Our ability to generate significant near-term revenue will depend upon successful commercialization of our ANDA products.

| 10 |

| Table of Contents |

Our ANDA product, a once daily generic Focalin XR® capsules, for which we received final approval from the FDA in November 2013 under the Company ANDA (as defined below) to launch the 15 and 30 mg strengths. Commercial sales of these strengths were launched immediately by our commercialization partner in the U.S., Par Pharmaceutical, Inc. (“Par”). Our 5, 10, 20 and 40 mg strengths were also then tentatively FDA approved, subject to the right of Teva Pharmaceuticals USA, Inc. (“Teva”) to 180 days of generic exclusivity from the date of first launch of such products. Teva launched its own 5, 10, 20 and 40 mg strengths of generic Focalin XR® capsules on November 11, 2014, February 2, 2015, June 22, 2015 and November 19, 2013, respectively. In January 2017, Par launched the 25 and 35 mg strengths of its generic Focalin XR® capsules in the U.S., and in May 2017, Par launched the 10 and 20 mg strengths, complementing the 15 and 30 mg strengths of our generic Focalin XR® marketed by Par. The FDA granted final approval under the Par ANDA (as defined in Item 4.B. below) for its generic Focalin XR® capsules in the 5, 10, 15, 20, 25, 30, 35 and 40 mg strengths. As the first filer of an ANDA for generic Focalin XR® in the 25 and 35 mg strengths, Par had 180 days of U.S. generic marketing exclusivity for those strengths. In November 2017, Par launched the remaining 5 and 40 mg strengths of generic Focalin XR®, complementing the 10, 15, 20, 25, 30 and 35 mg strengths previously launched and marketed by Par and providing us with the full line of general Focalin XR® strengths available in the U.S. market. Under the Par agreement (as defined below), we receive calendar quarterly profit-share payments on Par’s U.S. sales of generic Focalin XR®. There can be no assurance that commercialization of the product will produce significant revenue for us. We depend significantly on the actions of our marketing partner Par in the prosecution, regulatory approval and commercialization of our generic Focalin XR® capsules and on their timely payment to us of the contracted calendar quarterly payments as they come due. On August 15, 2019, we announced a license and commercial supply agreement with Tris Pharma, granting Tris Pharma the exclusive license to market, sell and distribute all strengths of generic Seroquel XR® (quetiapine fumarate extended-release tablets) in the United States. In May 2019, we received approval from the FDA for our ANDA for desvenlafaxine extended-release tablets in the 50 and 100 mg strengths and on September 5, 2019, we announced an agreement with Tris Pharma, granting Tris Pharma an exclusive license to market, sell and distribute that product in the United States. Our Venlafaxine hydrochloride extended-release capsules received final approval from the FDA in the 37.5, 75 and 150 mg strengths in November 2018; and the Company announced an exclusive licensing agreement with Tris Pharma to market, sell and distribute that product in the United States in November 2019.Product was never supplied nor distributed under this license. Effective May 5, 2021 the Company and Tris Pharma mutually terminated the license agreement. Termination of the exclusive agreements may provide opportunity for the Company to explore options of supplying the products to multiple sources on non-exclusive bases.

There can be no assurance that the products previously licensed to Tris Pharma will be successfully commercialized and produce significant revenues for us.

Our near-term ability to generate significant revenue will depend upon successful commercialization of our products in the U.S., where the branded products are in the market. Although we have some NDA 505(b)(2) product candidates in our pipeline, these are at early stages of development except Aximris XR that is still awaiting FDA decision. We have ANDAs still under review by the FDA and products that have been approved by the FDA that are not licensed.

Our significant expenditures on R&D may not lead to successful product introductions.

We conduct R&D primarily to enable us to manufacture and market pharmaceuticals in accordance with FDA regulations. Typically, research expenses related to the development of innovative compounds and the filing of NDAs are significantly greater than those expenses associated with ANDAs. As we continue to develop new products, our research expenses will likely increase. We are required to obtain FDA approval before marketing our drug products and the approval process is costly and time consuming. Because of the inherent risk associated with R&D efforts in our industry, particularly with respect to new drugs, our R&D expenditures may not result in the successful introduction of FDA approved new pharmaceuticals.

We may not have the ability to develop or license, or otherwise acquire, and introduce new products on a timely basis.

Product development is inherently risky, especially for new drugs for which safety and efficacy have not been established and the market is not yet proven. Likewise, product licensing involves inherent risks including uncertainties due to matters that may affect the achievement of milestones, as well as the possibility of contractual disagreements with regard to terms such as license scope or termination rights. The development and commercialization process, particularly with regard to new drugs, also requires substantial time, effort and financial resources. The process of obtaining FDA or other regulatory approval to manufacture and market new and generic pharmaceutical products is rigorous, time consuming, costly and largely unpredictable. We, or a partner, may not be successful in obtaining FDA or other required regulatory approval or in commercializing any of the product candidates that we are developing or licensing.

| 11 |

| Table of Contents |

Our business and operations are increasingly dependent on information technology and accordingly we would suffer in the event of computer system failures, cyber-attacks or a deficiency in cyber-security.

Our internal computer systems, and those of our vendors and current and/or future drug development or commercialization partners of ours, may be vulnerable to damage from cyber-attacks, computer viruses, malware, natural disasters, terrorism, war, telecommunication and electrical failures. The risk of a security breach or disruption, particularly through cyber-attacks, including by computer hackers, foreign governments, and cyber terrorists, has generally increased as the number, intensity and sophistication of attempted attacks and intrusions have increased. If such an event were to occur and cause interruptions in our operations or those of a drug development or commercialization partner, it could result in a material disruption of our product development programs. For example, the loss of clinical trial data from completed or ongoing or planned clinical trials could result in delays in our regulatory approval efforts and significantly increase our costs to recover or reproduce the data. To the extent that any disruption or security breach results in a loss of or damage to our data or applications, or inappropriate disclosure of confidential or proprietary information, we could incur significant liability and damage to our reputation. In addition, further development of our drug candidates could be adversely affected.

In addition, the unauthorized dissemination of sensitive personal information could expose us or other third parties to regulatory fines or penalties, litigation and potential liability, or otherwise harm our business.

Our business can be impacted by wholesaler buying patterns, increased generic competition and, to a lesser extent, seasonal fluctuations, which may cause our operating results to fluctuate.

We believe that the revenues derived from our generic Focalin XR® capsules and other licensed products are subject to wholesaler buying patterns, increased generic competition negatively impacting price, margins and market share consistent with industry post-exclusivity experience and, to a lesser extent, seasonal fluctuations in relation to generic Focalin XR® capsules (as these products are indicated for conditions including attention deficit hyperactivity disorder which we expect may see increases in prescription rates during the school term and declines in prescription rates during the summer months). Accordingly, these factors may cause our operating results to fluctuate.

We may not achieve our projected development goals in the time frames we announce and expect.

We set goals regarding the expected timing of meeting certain corporate objectives, such as the commencement and completion of clinical trials, anticipated regulatory approval and product launch dates. From time to time, we may make certain public statements regarding these goals. The actual timing of these events can vary dramatically due to, among other things, insufficient funding, delays or failures in our clinical trials or bioequivalence studies, the uncertainties inherent in the regulatory approval process, such as failure to secure appropriate product labeling approvals, requests for additional information, delays in achieving manufacturing or marketing arrangements necessary to commercialize our product candidates and failure by our collaborators, marketing and distribution partners, suppliers and other third parties to fulfill contractual obligations. In addition, the possibility of a patent infringement suit regarding one or more of our product candidates could delay final FDA approval of such candidates. If we fail to achieve one or more of these planned goals, the price of our common shares could decline.

We have limited manufacturing, sales, marketing or distribution capability and we must rely upon third parties for such.

While we have our own manufacturing facility in Toronto, we rely on third-party manufacturers to supply pharmaceutical ingredients, and we will be reliant upon a third-party manufacturer to produce certain of our products and product candidates. Third-party manufacturers may not be able to meet our deadlines or adhere to quality standards and specifications. Our reliance on third parties for the manufacture of pharmaceutical ingredients and finished products creates a dependency that could severely disrupt our research and development, our clinical testing, and ultimately our sales and marketing efforts if such third party manufacturers fail to perform satisfactorily, or do not adequately fulfill their obligations. If our manufacturing operation or any contracted manufacturing operation is unreliable or unavailable, we may not be able to move forward with our intended business operations and our entire business plan could fail. There is no assurance that our manufacturing operation or any third-party manufacturers will be able to meet commercialized scale production requirements in a timely manner or in accordance with applicable standards or current Good Manufacturing Practices (“cGMP”).

| 12 |

| Table of Contents |

If our manufacturing facility is unable to manufacture our product(s) or the manufacturing process is interrupted due to failure to comply with regulations or for other reasons, it could have a material adverse impact on our business.

If our manufacturing facility fails to comply with regulatory requirements or encounter other manufacturing difficulties, it could adversely affect our ability to supply products. All facilities and manufacturing processes used for the manufacture of pharmaceutical products are subject to inspection by regulatory agencies at any time and must be operated in conformity with the current cGMP regulations. Compliance with FDA and Health Canada cGMP requirements applies to both drug products seeking regulatory approval and to approved drug products. In complying with cGMP requirements, pharmaceutical manufacturing facilities must continually expend significant time, money and effort in production, record-keeping and quality assurance and control so that their products meet applicable specifications and other requirements for product safety, efficacy and quality. Failure to comply with applicable legal requirements subjects our manufacturing facility to possible legal or regulatory action, including shutdown, which may adversely affect our ability to manufacture product. If we are not able to manufacture products at our manufacturing facility because of regulatory, business or any other reasons, the manufacture and marketing of these products would be interrupted. This could have a material adverse impact on our business, results of operations, financial condition, cash flows and competitive position.

The use of legal and regulatory strategies by competitors with innovator products, including the filing of citizen petitions, may delay or prevent the introduction or approval of our product candidates, increase our costs associated with the introduction or marketing of our products, or significantly reduce the profit potential of our product candidates.

Companies with innovator drugs often pursue strategies that may serve to prevent or delay competition from alternatives to their innovator products. These strategies include, but are not limited to:

| · | filing “citizen petitions” with the FDA that may delay competition by causing delays of our product approvals; |

|

|

|

| · | seeking to establish regulatory and legal obstacles that would make it more difficult to demonstrate a product’s bioequivalence or “sameness” to the related innovator product; |

|

|

|

| · | filing suits for patent infringement that automatically delay FDA approval of products seeking approval based on the Section 505(b)(2) pathway; |

|

|

|

| · | obtaining extensions of market exclusivity by conducting clinical trials of innovator drugs in pediatric populations or by other methods; |

|

|

|

| · | persuading the FDA to withdraw the approval of innovator drugs for which the patents are about to expire, thus allowing the innovator company to develop and launch new patented products serving as substitutes for the withdrawn products; |

|

|

|

| · | seeking to obtain new patents on drugs for which patent protection is about to expire; and |

|

|

|

| · | initiating legislative and administrative efforts in various states to limit the substitution of innovator products by pharmacies. |

|

|

|

These strategies could delay, reduce or eliminate our entry into the market and our ability to generate revenues from our products and product candidates.

| 13 |

| Table of Contents |

Our products and product candidates, if approved for sale, may not gain acceptance among physicians, patients and the medical community, thereby limiting our potential to generate revenue.

Even if we are able to obtain regulatory approvals for our product candidates, the success of any of our products will be dependent upon market acceptance by physicians, healthcare professionals and third-party payers and our profitability and growth will depend on a number of factors, including:

| · | demonstration of safety and efficacy; |

|

|

|

| · | changes in the practice guidelines and the standard of care for the targeted indication; |

|

|

|

| · | relative convenience and ease of administration; |

|

|

|

| · | the prevalence and severity of any adverse side effects; |

|

|

|

| · | the availability of alternative products from competitors; |

|

|

|

| · | the prices of our products relative to those of our competitors; |

|

|

|

| · | pricing, reimbursement and cost effectiveness, which may be subject to regulatory control; |

|

|

|

| · | the number of competitive product entries, and the nature and extent of any aggressive pricing and rebate activities that may follow; |

|

|

|

| · | the timing of our market entry; |

|

|

|

| · | the ability to market our products effectively at the retail level; |

|

|

|

| · | the acceptance of our products by government and private formularies; and |

|

|

|

| · | the availability of adequate third-party insurance coverage or reimbursement. |

If any product candidate that we develop does not provide a treatment regimen that is as beneficial as, or is perceived as being as beneficial as, the current standard of care or otherwise does not provide patient benefit, that product candidate, if approved for commercial sale by the FDA or other regulatory authorities, likely will not achieve market acceptance. Our ability to effectively promote and sell any approved products will also depend on pricing and cost-effectiveness, including our ability to produce a product at a competitive price and our ability to obtain sufficient third-party coverage or reimbursement. If any product candidate is approved but does not achieve an adequate level of acceptance by physicians, patients and third-party payers, our ability to generate revenues from that product would be substantially reduced. In addition, our efforts to educate the medical community and third-party payers on the benefits of our product candidates may require significant resources, may be constrained by FDA rules and policies on product promotion, and may never be successful.

The risks and uncertainties inherent in conducting clinical trials could delay or prevent the development and commercialization of our own branded products, which could have a material adverse effect on our results of operations, liquidity, financial condition, and growth prospects.

There are a number of risks and uncertainties associated with clinical trials, which may be exacerbated by our relatively limited experience in conducting and supervising clinical trials and preparing NDAs. The results of initial clinical trials may not be indicative of results that would be obtained from large scale testing. Clinical trials are often conducted with patients having advanced stages of disease and, as a result, during the course of treatment these patients can die or suffer adverse medical effects for reasons that may not be related to the pharmaceutical agents being tested, but which nevertheless affect the clinical trial results. In addition, side effects experienced by the patients may cause delay of approval of our product candidates or a limited application of an approved product. Moreover, our clinical trials may not demonstrate sufficient safety and efficacy to obtain FDA approval.

| 14 |

| Table of Contents |

Failure can occur at any time during the clinical trial process and, in addition, the results from early clinical trials may not be predictive of results obtained in later and larger clinical trials, and product candidates in later clinical trials may fail to show the desired safety or efficacy despite having progressed successfully through earlier clinical testing. A number of companies in the pharmaceutical industry have suffered significant setbacks in clinical trials, even in advanced clinical trials after showing positive results in earlier clinical trials. In the future, the completion of clinical trials for our product candidates may be delayed or halted for many reasons, including those relating to the following:

| · | delays in patient enrollment, and variability in the number and types of patients available for clinical trials; |

|

|

|

| · | regulators or institutional review boards may not allow us to commence or continue a clinical trial; |

|

|

|

| · | our inability, or the inability of our partners, to manufacture or obtain from third parties materials sufficient to complete our clinical trials; |

|

|

|

| · | delays or failures in reaching agreement on acceptable clinical trial contracts or clinical trial protocols with prospective clinical trial sites; |

|

|

|

| · | risks associated with trial design, which may result in a failure of the trial to show statistically significant results even if the product candidate is effective; |

|

|

|

| · | difficulty in maintaining contact with patients after treatment commences, resulting in incomplete data; |

|

|

|

| · | poor effectiveness of product candidates during clinical trials; |

|

|

|

| · | safety issues, including adverse events associated with product candidates; |

|

|

|

| · | the failure of patients to complete clinical trials due to adverse side effects, dissatisfaction with the product candidate, or other reasons; |

|

|

|

| · | governmental or regulatory delays or changes in regulatory requirements, policy and guidelines; and |

|

|

|

| · | varying interpretation of data by the FDA or other applicable foreign regulatory agencies. |

In addition, our product candidates could be subject to competition for clinical study sites and patients from other therapies under development by other companies which may delay the enrollment in or initiation of our clinical trials. Many of these companies have significantly more resources than we do.

The FDA or other foreign regulatory authorities may require us to conduct unanticipated additional clinical trials, which could result in additional expense and delays in bringing our product candidates to market. Any failure or delay in completing clinical trials for our product candidates would prevent or delay the commercialization of our product candidates. There can be no assurance our expenses related to clinical trials will lead to the development of brand-name drugs which will generate revenues in the near future. Delays or failure in the development and commercialization of our own branded products could have a material adverse effect on our results of operations, liquidity, financial condition, and our growth prospects.

| 15 |

| Table of Contents |

We rely on third parties to conduct clinical trials for our product candidates, and if they do not properly and successfully perform their legal and regulatory obligations, as well as their contractual obligations to us, we may not be able to obtain regulatory approvals for our product candidates.

We design the clinical trials for our product candidates, but rely on contract research organizations and other third parties to assist us in managing, monitoring and otherwise carrying out these trials, including with respect to site selection, contract negotiation and data management. We do not control these third parties and, as a result, they may not treat our clinical studies as their highest priority, or in the manner in which we would prefer, which could result in delays. Although we rely on third parties to conduct our clinical trials, we are responsible for confirming that each of our clinical trials is conducted in accordance with our general investigational plan and protocol. Moreover, the FDA and foreign regulatory agencies require us to comply with regulations and standards, commonly referred to as good clinical practices (“good clinical practices”) for conducting, recording and reporting the results of clinical trials to ensure that the data and results are credible and accurate and that the trial participants are adequately protected. Our reliance on third parties does not relieve us of these responsibilities and requirements. The FDA enforces good clinical practices through periodic inspections of trial sponsors, principal investigators and trial sites. If we, our contract research organizations or our study sites fail to comply with applicable good clinical practices, the clinical data generated in our clinical trials may be deemed unreliable and the FDA may require us to perform additional clinical trials before approving our marketing applications. There can be no assurance that, upon inspection, the FDA will determine that any of our clinical trials comply with good clinical practices. In addition, our clinical trials must be conducted with product manufactured under the FDA’s cGMP regulations. Our failure, or the failure of our contract manufacturers, if any are involved in the process, to comply with these regulations may require us to repeat clinical trials, which would delay the regulatory approval process.