UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

(Mark One)

| ☒ |

QUARTERLY REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended June 30, 2020

| ☐ |

TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ____________ to ____________

Commission file number 001-37568

|

PDS Biotechnology Corporation

|

||

|

(Exact name of registrant as specified in its charter)

|

|

Delaware

|

26-4231384

|

|

|

(State or other jurisdiction of incorporation or organization)

|

(IRS Employer Identification No.)

|

|

25B Vreeland Road, Florham Park, NJ 07932

|

||

|

(Address of principal executive offices)

|

|

(800) 208-3343

|

||

|

(Registrant’s telephone number)

|

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class

|

Trading symbol(s)

|

Name of each exchange on which registered

|

||

|

Common Stock, par value $0.00033 per share

|

PDSB

|

Nasdaq Capital Market

|

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such

shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (Section 232.405 of this chapter)

during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the

definitions of “large accelerated filer”, “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Securities Exchange Act of 1934.

|

Large accelerated filer ☐

|

Accelerated filer ☐

|

Non-accelerated filer ☒

|

Smaller Reporting Company ☒

|

|

Emerging growth company ☒

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards

provided pursuant to Section 13(a) of the Exchange Act. ☒

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934). Yes ☐ No ☒

The number of shares of the registrant’s Common Stock, par value $0.00033 per share, outstanding as of August 6, 2020 was 15,361,619.

PDS BIOTECHNOLOGY CORPORATION

FORM 10-Q FOR THE QUARTER ENDED JUNE 30, 2020

INDEX

|

Page

|

|||

|

3

|

|||

|

Item 1.

|

3

|

||

|

3

|

|||

|

4

|

|||

|

5

|

|||

|

7

|

|||

|

8

|

|||

|

Item 2.

|

19

|

||

|

Item 3.

|

31

|

||

|

Item 4.

|

31

|

||

|

33

|

|||

|

Item 1.

|

33

|

||

|

Item 1A.

|

33

|

||

|

Item 2.

|

37

|

||

|

Item 3.

|

37

|

||

|

Item 4.

|

37

|

||

|

Item 5.

|

37

|

||

|

Item 6.

|

37

|

||

|

38

|

|||

|

39

|

|||

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARIES

|

June 30, 2020

|

December 31, 2019

|

|||||||

|

ASSETS

|

(unaudited)

|

|||||||

|

Current assets:

|

||||||||

|

Cash and cash equivalents

|

$

|

16,934,495

|

$

|

12,161,739

|

||||

|

Prepaid expenses and other

|

2,506,646

|

2,308,462

|

||||||

|

Total current assets

|

19,441,141

|

14,470,201

|

||||||

|

Property and equipment, net

|

13,247

|

21,051

|

||||||

|

Right-to-use asset

|

638,831

|

–

|

||||||

|

Total assets

|

$

|

20,093,219

|

$

|

14,491,252

|

||||

|

LIABILITIES AND STOCKHOLDERS’ EQUITY

|

||||||||

|

LIABILITIES

|

||||||||

|

Current liabilities:

|

||||||||

|

Accounts payable

|

$

|

1,092,527

|

$

|

1,197,720

|

||||

|

Accrued expenses

|

1,194,358

|

1,097,640

|

||||||

|

Restructuring reserve

|

126,862

|

498,185

|

||||||

|

Operating lease liability - short term

|

112,657

|

–

|

||||||

|

Total current liabilities

|

2,526,404

|

2,793,545

|

||||||

|

Noncurrent liability:

|

||||||||

|

Operating lease liability - long term

|

552,326

|

–

|

||||||

|

STOCKHOLDERS’ EQUITY

|

||||||||

|

Common stock, $0.00033 par value, 75,000,000 shares authorized at June 30, 2020 and December 31, 2019, 15,361,619 shares and 5,281,237 shares issued and outstanding

at June 30, 2020 and December 31, 2019, respectively

|

5,064

|

1,742

|

||||||

|

Additional paid-in capital

|

52,861,882

|

40,633,670

|

||||||

|

Accumulated deficit

|

(35,852,457

|

)

|

(28,937,705

|

)

|

||||

|

Total stockholders’ equity

|

17,014,489

|

11,697,707

|

||||||

|

Total liabilities and stockholders’ equity

|

$

|

20,093,219

|

$

|

14,491,252

|

||||

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARIES

(Unaudited)

|

Three Months Ended June 30,

|

Six Months Ended June 30,

|

|||||||||||||||

|

2020

|

2019

|

2020

|

2019

|

|||||||||||||

|

Operating expenses:

|

||||||||||||||||

|

Research and development expenses

|

$

|

1,414,225

|

$

|

1,886,934

|

$

|

3,385,904

|

$

|

2,916,937

|

||||||||

|

General and administrative expenses

|

1,521,736

|

2,383,972

|

3,581,884

|

6,289,848

|

||||||||||||

|

Total operating expenses

|

2,935,961

|

4,270,906

|

6,967,788

|

9,206,785

|

||||||||||||

|

Loss from operations

|

(2,935,961

|

)

|

(4,270,906

|

)

|

(6,967,788

|

)

|

(9,206,785

|

)

|

||||||||

|

Other income (expense):

|

||||||||||||||||

|

Gain on bargain purchase upon merger

|

–

|

209,449

|

–

|

11,939,331

|

||||||||||||

|

Interest income

|

6,617

|

175,605

|

53,036

|

198,907

|

||||||||||||

|

Interest expense

|

–

|

–

|

–

|

(606

|

)

|

|||||||||||

|

Net (loss) income and comprehensive (loss) income

|

(2,929,344

|

)

|

(3,885,852

|

)

|

(6,914,752

|

)

|

2,930,847

|

|||||||||

|

Per share information:

|

||||||||||||||||

|

Net (loss) income per share, basic

|

$

|

(0.19

|

)

|

$

|

(0.75

|

)

|

$

|

(0.54

|

)

|

$

|

0.66

|

|||||

|

Net (loss) income per share, diluted

|

$

|

(0.19

|

)

|

$

|

(0.75

|

)

|

$

|

(0.54

|

)

|

$

|

0.52

|

|||||

|

Weighted average common shares outstanding, basic

|

$

|

15,357,199

|

$

|

5,175,837

|

$

|

12,835,980

|

$

|

4,466,025

|

||||||||

|

Weighted average common shares outstanding, diluted

|

$

|

15,357,199

|

$

|

5,175,837

|

$

|

12,835,980

|

$

|

5,677,360

|

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARIES

(Unaudited)

|

Common Stock

|

Additional

Paid-in

Capital

|

Accumulated

|

Total

Equity

(Deficit)

|

|||||||||||||||||

|

Shares

Issued

|

Amount

|

Deficit

|

||||||||||||||||||

|

Balance - March 31, 2019

|

5,172,938

|

$

|

1,707

|

$

|

38,642,411

|

$

|

(14,196,475

|

)

|

$

|

24,447,643

|

||||||||||

|

Stock based compensation expense

|

–

|

–

|

18,580

|

–

|

18,580

|

|||||||||||||||

|

Issuance of common stock, net of issuance costs

|

4,549

|

2

|

25,242

|

–

|

25,244

|

|||||||||||||||

|

Net loss

|

–

|

–

|

–

|

(3,885,852

|

)

|

(3,885,852

|

)

|

|||||||||||||

|

Balance - June 30, 2019

|

5,177,487

|

$

|

1,709

|

$

|

38,686,233

|

$

|

(18,082,327

|

)

|

$

|

20,605,615

|

||||||||||

|

Common Stock

|

Additional

Paid-in

Capital

|

Accumulated

|

Total

Equity

(Deficit)

|

|||||||||||||||||

|

Shares

Issued

|

Amount

|

Deficit

|

||||||||||||||||||

|

Balance - March 31, 2020

|

15,350,445

|

$

|

5,064

|

$

|

52,805,601

|

$

|

(32,923,113

|

)

|

$

|

19,887,552

|

||||||||||

|

Stock-based compensation expense

|

–

|

–

|

46,113

|

–

|

46,113

|

|||||||||||||||

|

Issuance of common stock from 401K match

|

11,174

|

–

|

10,168

|

–

|

10,168

|

|||||||||||||||

|

Net loss

|

–

|

–

|

–

|

(2,929,344

|

)

|

(2,929,344

|

)

|

|||||||||||||

|

Balance - June 30, 2020

|

15,361,619

|

$

|

5,064

|

$

|

52,861,882

|

$

|

(35,852,457

|

)

|

$

|

17,014,489

|

||||||||||

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARIES

Condensed Consolidated Statements of Changes in Stockholders’ Equity (Deficit)

(Unaudited)

|

Common Stock

|

Additional

Paid-in

Capital

|

Accumulated

|

Total

Equity

(Deficit)

|

|||||||||||||||||

|

Shares

Issued

|

Amount

|

Deficit

|

||||||||||||||||||

|

Balance - December 31, 2018

|

3,417,187

|

$

|

1,128

|

$

|

19,311,529

|

$

|

(21,013,174

|

)

|

$

|

(1,700,517

|

)

|

|||||||||

|

Stock based compensation expense

|

–

|

–

|

2,773,451

|

–

|

2,773,451

|

|||||||||||||||

|

Issuance of common stock, net of issuance costs

|

48,930

|

16

|

749,984

|

–

|

750,000

|

|||||||||||||||

|

Issuance of common stock for antidilution

|

97,960

|

32

|

(32

|

)

|

–

|

–

|

||||||||||||||

|

Issuance of common stock for convertible debt

|

9,683

|

3

|

32,950

|

–

|

32,953

|

|||||||||||||||

|

Issuance of common stock from 401K match

|

4,549

|

2

|

25,241

|

–

|

25,243

|

|||||||||||||||

|

Equity from merger transaction

|

1,599,178

|

528

|

15,793,110

|

–

|

15,793,638

|

|||||||||||||||

|

Net income

|

–

|

–

|

–

|

2,930,847

|

2,930,847

|

|||||||||||||||

|

Balance - June 30, 2019

|

5,177,487

|

$

|

1,709

|

$

|

38,686,233

|

$

|

(18,082,327

|

)

|

$

|

20,605,615

|

||||||||||

|

Common Stock

|

Additional

Paid-in

Capital

|

Accumulated

|

Total

Equity

(Deficit)

|

|||||||||||||||||

|

Shares

Issued

|

Amount

|

Deficit

|

||||||||||||||||||

|

Balance - December 31, 2019

|

5,281,237

|

$

|

1,742

|

$

|

40,633,670

|

$

|

(28,937,705

|

)

|

$

|

11,697,707

|

||||||||||

|

Stock-based compensation expense

|

–

|

–

|

171,106

|

–

|

171,106

|

|||||||||||||||

|

Issuance of common stock, net of issuance costs

|

10,000,000

|

3,299

|

11,966,703

|

–

|

11,970,002

|

|||||||||||||||

|

Issuance of common stock for convertible debt

|

65,240

|

22

|

70,437

|

–

|

70,459

|

|||||||||||||||

|

Issuance of common stock from 401K match

|

15,142

|

1

|

19,966

|

–

|

19,967

|

|||||||||||||||

|

Net loss

|

–

|

–

|

–

|

(6,914,752

|

)

|

(6,914,752

|

)

|

|||||||||||||

|

Balance - June 30, 2020

|

15,361,619

|

$

|

5,064

|

$

|

52,861,882

|

$

|

(35,852,457

|

)

|

$

|

17,014,489

|

||||||||||

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARIES

(Unaudited)

|

Six Months Ended June 30,

|

||||||||

|

2020

|

2019

|

|||||||

|

Cash flows from operating activities:

|

||||||||

|

Net (loss) income

|

$

|

(6,914,752

|

)

|

$

|

2,930,847

|

|||

|

Adjustments to reconcile net (loss) income to net cash used in operating activities:

|

||||||||

|

Stock-based compensation expense

|

171,106

|

2,773,451

|

||||||

|

Stock-based 401K company common match

|

19,967

|

25,244

|

||||||

|

Depreciation expense

|

7,805

|

62,706

|

||||||

|

Amortization of the right-to-use asset

|

41,800

|

–

|

||||||

|

Bargain purchase gain from merger

|

–

|

(11,939,331

|

)

|

|||||

|

Changes in assets and liabilities:

|

||||||||

|

Prepaid expenses and other assets

|

(198,184

|

)

|

157,273

|

|||||

|

Accounts payable

|

(105,193

|

)

|

(1,157,171

|

)

|

||||

|

Accrued expenses

|

96,718

|

(292,678

|

)

|

|||||

|

Restructuring reserve

|

(371,323

|

)

|

(786,396

|

)

|

||||

|

Cash payments for expenses:

|

||||||||

|

Payments made for operating lease

|

(15,649

|

)

|

–

|

|||||

|

Net cash used in operating activities

|

(7,267,705

|

)

|

(8,226,055

|

)

|

||||

|

Cash flows from investing activities:

|

||||||||

|

Cash received in reverse merger transaction

|

–

|

29,106,512

|

||||||

|

Net cash provided by investing activities

|

–

|

29,106,512

|

||||||

|

Cash flows from financing activities:

|

||||||||

|

Proceeds from exercise of warrants

|

70,459

|

–

|

||||||

|

Proceeds from issuance of common stock, net of issuance costs

|

11,970,002

|

750,000

|

||||||

|

Net cash provided by financing activities

|

12,040,461

|

750,000

|

||||||

|

Net increase in cash and cash equivalents

|

4,772,756

|

21,630,457

|

||||||

|

Cash and cash equivalents at beginning of period

|

12,161,739

|

103,695

|

||||||

|

Cash and cash equivalents at end of period

|

$

|

16,934,495

|

$

|

21,734,152

|

||||

|

Supplemental disclosure of cash flow information:

|

||||||||

|

Cash paid for:

|

||||||||

|

Interest

|

$

|

–

|

$

|

606

|

||||

|

Supplemental cash flow information:

|

||||||||

|

Conversion of convertible notes and accrued interest into common stock

|

$

|

–

|

$

|

32,953

|

||||

|

Consideration in connection with reverse merger transaction

|

$

|

–

|

$

|

15,793,638

|

||||

See accompanying notes to the condensed consolidated financial statements.

PDS BIOTECHNOLOGY CORPORATION AND SUBSIDIARIES

Note 1 – Nature of Operations

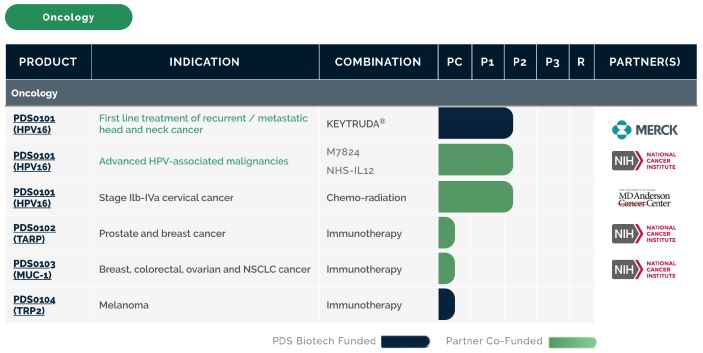

PDS Biotechnology Corporation, a Delaware corporation (the “Company,” “PDS,” or the “combined company”), PDS is a clinical-stage immunotherapy company

developing a growing pipeline of cancer immunotherapies and infectious disease vaccines designed to overcome the well-established limitations of current immunotherapy technologies. PDS owns Versamune®, a proprietary T-cell activating

platform designed to train the immune system to better attack and destroy disease. When paired with an antigen, a disease-related protein that is recognizable by the immune system, Versamune® has been shown to induce, in vivo, large quantities of high-quality, highly potent polyfunctional CD8+ killer T-cells, a specific sub-type of CD8+ killer T-cell that is more effective at killing infected or target cells. Our

immuno-oncology products can potentially be used as a component of combination products with other leading technologies to provide effective treatments across a range of cancer types, including Human Papillomavirus (HPV)-based cancers, melanoma,

colorectal, lung, breast and prostate cancers or as monotherapies in early-stage disease. PDS is working to expand its infectious disease pandemic development program, including novel vaccines for COVID-19 and universal influenza, in addition to

its previously announced tuberculosis development collaboration with Farmacore Biotechnology.

From the Company’s inception, it has devoted substantially all of its efforts to drug development, business planning, engaging regulatory, manufacturing and other technical consultants, acquiring

operating assets, planning and executing clinical trials and raising capital.

On March 15, 2019, the Company, then operating as Edge Therapeutics, Inc. (“Edge”), completed its reverse merger with privately held PDS Biotechnology Corporation

(“Private PDS”), pursuant to and in accordance with the terms of the Agreement and Plan of Merger (the “Merger Agreement”), dated as of November 23, 2018, as amended on January 24, 2019, by and among the

Company, Echos Merger Sub, a wholly-owned subsidiary of the Company (“Merger Sub”), and Private PDS, whereby Private PDS merged with and into Merger Sub, with Private PDS surviving as the Company’s wholly-owned subsidiary (the “Merger”). In connection with and immediately following completion of the Merger, the Company effected a 1-for-20 reverse stock split (the “Reverse Stock Split”) and changed its corporate name from Edge Therapeutics, Inc.

to PDS Biotechnology Corporation, and Private PDS changed its name to PDS Operating Corporation.

For accounting purposes, the Merger was treated as a “reverse acquisition” under generally accepted accounting principles in the United States (“U.S. GAAP”) and Private PDS is considered the

accounting acquirer. Accordingly, upon consummation of the Merger, the historical financial statements of Private PDS became the Company’s historical financial statements, and the historical financial statements of Private PDS are included in the

comparative prior periods. See “Note 4 – Reverse Merger” for more information on the Merger. As part of the Merger, the Company acquired all of Edge’s assets relating to current and future research and development.

In December 2019, a coronavirus known as SARS-CoV-2 was first detected in Wuhan, Hubei Province, People’s Republic of China, causing outbreaks of the coronavirus

disease, known as COVID-19, that has now spread globally. On January 30, 2020 the World Health Organization (WHO) declared COVID-19 a pandemic (the “COVID-19 Pandemic”). The Secretary of Health and Human Services declared a public health

emergency on January 31, 2020, under section 319 of the Public Health Service Act (42 U.S.C. 247d), in response to the COVID-19 Pandemic. The full impact of the COVID-19 Pandemic is unknown and rapidly evolving. To date, two of the three currently planned PDS0101 clinical trials have been delayed, specifically as a result of the adverse impact the COVID-19 Pandemic has had on clinical trial operations for cancer indications in the United

States.

Note 2 – Summary of Significant Accounting Policies

| (A) |

Unaudited interim financial statements:

|

The interim balance sheet at June 30, 2020, the statements of operations and comprehensive loss and changes in stockholders’ equity for the three and six months ended June 30, 2020

and 2019, and cash flows for the six months ended June 30, 2020 and 2019 are unaudited. The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with U.S. GAAP, in accordance with the requirements of

the Securities and Exchange Commission (“SEC”) for interim reporting. As permitted under those rules, certain footnotes or other financial information that are normally required by U.S. GAAP can be condensed or omitted. These condensed consolidated

financial statements have been prepared on the same basis as the Company’s annual financial statements and, in the opinion of management, reflect all adjustments, consisting only of normal recurring adjustments that are necessary for a fair

statement of its financial information. The results of operations for the three and six months ended June 30, 2020 are not necessarily indicative of the results to be expected for the year ending December 31, 2020 or for any other future annual or

interim period. The balance sheet as of December 31, 2019 included herein was derived from the audited condensed consolidated financial statements as of that date. These condensed consolidated financial statements should be read in conjunction with

the Company’s audited consolidated financial statements and notes thereto as of and for the year ended December 31, 2019, filed by the Company with the SEC in its Annual Report on Form 10-K on March 27, 2020.

|

(B)

|

Use of estimates:

|

The preparation of consolidated financial statements in conformity with U.S. GAAP requires management to make estimates and assumptions that affect the reported amounts of assets

and liabilities and the reported amounts of expenses at the date of the consolidated financial statements and during the reporting periods, and to disclose contingent assets and liabilities at the date of the consolidated financial statements.

Actual results could differ from those estimates.

| (C) |

Significant risks and uncertainties:

|

The Company’s operations are subject to a number of factors that may affect its operating results and financial condition. Such factors include, but are not limited to: the clinical

and regulatory development of its products, the Company’s ability to preserve its cash resources, the Company’s review of strategic alternatives, the Company’s ability to add product candidates to its pipeline, the Company’s intellectual property,

competition from products manufactured and sold or being developed by other companies, the price of, and demand for, Company products if approved for sale, the Company’s ability to negotiate favorable licensing or other manufacturing and marketing

agreements for its products, the Company’s ability to raise capital, and the effects of health epidemics, pandemics, or outbreaks of infectious diseases, including the recent COVID-19 pandemic.

The Company currently has no commercially approved products. As such, there can be no assurance that the Company’s future research and development programs will be successfully

commercialized. Developing and commercializing a product requires significant time and capital and is subject to regulatory review and approval as well as competition from other biotechnology and pharmaceutical companies. The Company operates in an

environment of rapid change and is dependent upon the continued services of its employees and consultants and obtaining and protecting its intellectual property.

| (D) |

Business acquisition:

|

The Company’s consolidated financial statements include the operations of an acquired business after the completion of the acquisition. We account for acquired businesses using

the acquisition method of accounting, which requires, among other things, that most assets acquired and liabilities assumed be recognized at their estimated fair values as of the acquisition date and that the fair value of IPR&D be recorded

on the balance sheet. Transaction costs are expensed as incurred.

The Company measures certain assets and liabilities at fair value, either upon initial recognition or for subsequent accounting or reporting. For example, we use fair value in the

initial recognition of net assets acquired in a business combination and when measuring impairment losses. We estimate fair value using an exit price approach, which requires, among other things, that we determine the price that would be received

to sell an asset or paid to transfer a liability in an orderly market. The determination of an exit price is considered from the perspective of market participants, considering the highest and best use of non-financial assets and, for liabilities,

assuming that the risk of non-performance will be the same before and after the transfer.

When estimating fair value, depending on the nature and complexity of the asset or liability, we may use one or all of the following techniques:

| ● |

Income approach, which is based on the present value of a future stream of net cash flows.

|

| ● |

Market approach, which is based on market prices and other information from market transactions involving identical or comparable assets or liabilities.

|

| ● |

Cost approach, which is based on the cost to acquire or construct comparable assets, less an allowance for functional and/or economic obsolescence.

|

Our fair value methodologies depend on the following types of inputs:

| ● |

Quoted prices for identical assets or liabilities in active markets (Level 1 inputs).

|

| ● |

Quoted prices for similar assets or liabilities in active markets, or quoted prices for identical or similar assets or liabilities in markets that are not active, or inputs other than quoted prices that are

directly or indirectly observable, or inputs that are derived principally from, or corroborated by, observable market data by correlation or other means (Level 2 inputs).

|

| ● |

Unobservable inputs that reflect estimates and assumptions (Level 3 inputs).

|

|

(E)

|

Cash equivalents and concentration of cash balance:

|

The Company considers all highly liquid securities with a maturity weighted average of less than three months to be cash equivalents. The Company’s cash and cash equivalents in bank

deposit accounts, at times, may exceed federally insured limits.

|

(F)

|

Research and development:

|

Costs incurred in connection with research and development activities are expensed as incurred. These costs include licensing fees to use certain technology in the Company’s

research and development projects as well as fees paid to consultants and entities that perform certain research and testing on behalf of the Company.

Costs for certain development activities, such as clinical trials, are recognized based on an evaluation of the progress to completion of specific tasks using data, such as patient

enrollment, clinical site activations or information provided by vendors on their actual costs incurred. Payments for these activities are based on the terms of the individual arrangements, which may differ from the pattern of costs incurred

| (G) |

Patent costs:

|

The Company expenses patent costs as incurred and classifies such costs as general and administrative expenses in the accompanying statements of operations and comprehensive loss.

| (H) |

Intangible asset and impairment:

|

As part of the reverse merger transaction on March 15, 2019, the Company acquired an in-process research and development (“IPR&D”) intangible asset valued at $2,974,000 using a discounted cash flow method. In determining the value of IPR&D, management considers, among other factors, the stage of completion of the project, the technological feasibility of the project, whether the project have an

alternative future use, and the estimated residual cash flows that could be generated from the various projects and technologies over their respective projected economic lives. The discount rate used is determined at the time of acquisition and

includes a rate of return which accounts for the time value of money, as well as risk factors reflecting the economic risk that the projected cash flows may not be realized.

The Company reviews all of its long-lived assets for impairment indicators throughout the year. The Company performs impairment testing for indefinite-lived intangible assets annually and for all other long-lived

assets whenever impairment indicators are present. When necessary, the Company records charges for impairments of long-lived assets for the amount by which the fair value is less than the carrying value of these assets.

| (I) |

Stock-based compensation:

|

The Company accounts for its stock-based compensation in accordance with ASC Topic 718, Compensation—Stock Compensation (“ASC 718”). ASC 718 requires all stock-based payments to employees,

directors and non-employees to be recognized as expense in the condensed statements of operations and comprehensive loss based on their grant date fair values. The Company estimates the fair value of options granted using the Black-Scholes option

pricing model for stock option grants to both employees and non-employees. This model requires the following assumptions: (1) the expected volatility of our stock is based on volatilities of a peer group of similar

companies in the biotechnology industry whose share prices are publicly available, (2) the expected term of the award is based on the simplified method, which is the midpoint between the requisite service

period and the contractual term of the option, as we have a limited history of being a public company from March 15, 2019 (the date of the Merger) to develop reasonable expectations about future exercise patterns and employment duration for our

options, (3) the risk-free interest rate based on U.S. Treasury notes with a term approximating the expected life of the option and (4) expected dividend yield of 0, since we have never paid cash dividends and have no present intention to pay

cash dividends.

The Company expenses the fair value of its stock-based compensation awards to employees, directors and non-employees on a straight-line basis over the requisite service period, which is generally

the vesting period. The Company recognizes forfeitures as they occur.

|

(J)

|

Net income (loss) per common share:

|

Basic net income (loss) per share attributable to common stockholders is computed by dividing net income (loss) attributable to common stockholders by the weighted-average number of

common shares outstanding during the period. All participating securities are excluded from basic weighted-average common shares outstanding. In computing both basic net income (loss) per share attributable to common stockholders and diluted net

income (loss) per share attributable to common stockholders, undistributed earnings are re-allocated to reflect the potential impact of dilutive securities, including stock options and warrants. Diluted net income (loss) per share attributable to

common stockholders is computed by dividing net income (loss) attributable to common stockholders by the weighted-average number of common equivalent shares outstanding for the period. Diluted net income (loss) per share attributable to common

stockholders includes any dilutive effect from outstanding stock options and warrants using the treasury stock method.

The common stock issuable upon the conversion or exercise of the following dilutive securities as of June 30, 2020 has been excluded from the diluted net loss per share attributable

to common stockholders calculation because their effect would have been antidilutive for the period presented.

The potentially dilutive securities excluded from the determination of diluted loss per share as their effect is antidilutive, are as follows:

|

As of June 30,

|

||||||||

|

2020

|

2019

|

|||||||

|

Stock options to purchase Common Stock

|

1,639,753

|

1,418,301

|

||||||

|

Warrants to purchase Common Stock

|

197,518

|

262,758

|

||||||

|

Total

|

1,837,271

|

1,681,059

|

||||||

The following is a reconciliation of the numerator (net income or loss) and the denominator (number of shares) used in the calculation of basic and diluted net income (loss) per

share attributable to common stockholders:

|

Three Months Ended June 30,

|

Six Months Ended June 30,

|

|||||||||||||||

|

2020

|

2019

|

2020

|

2019

|

|||||||||||||

|

Numerator

|

||||||||||||||||

|

Basic and diluted net (loss) income

|

$

|

(2,929,344

|

)

|

$

|

(3,885,852

|

)

|

$

|

(6,914,752

|

)

|

$

|

2,930,847

|

|||||

|

Denominator

|

||||||||||||||||

|

Shares used in computing basic net (loss) income per share

|

15,357,199

|

5,175,837

|

12,835,980

|

4,466,025

|

||||||||||||

|

Shares from dilutive securities

|

–

|

–

|

–

|

1,211,335

|

||||||||||||

|

Shares used in computing diluted net (loss) income per share

|

15,357,199

|

5,175,837

|

12,835,980

|

5,677,360

|

||||||||||||

|

Net (loss) income per share, basic

|

$

|

(0.19

|

)

|

$

|

(0.75

|

)

|

$

|

(0.54

|

)

|

$

|

0.66

|

|||||

|

Net (loss) income per share, diluted

|

$

|

(0.19

|

)

|

$

|

(0.75

|

)

|

$

|

(0.54

|

)

|

$

|

0.52

|

|||||

| (K) |

Accounting standards adopted:

|

In February 2016, the FASB issued ASU No. 2016-02, Leases (Topic 842) (“ASU 2016-02”), which sets out the principles for the recognition, measurement, presentation and disclosure

of leases for both lessees and lessors. The Company adopted the new lease standard, as of January 1, 2019, using the optional transition method under which comparative financial information will not be restated and continue to apply the

provisions of the previous lease standard in its annual disclosures for the comparative periods. In addition, the new lease standard provides a number of optional practical expedients in transition. The Company elected the package of practical

expedients. As such, the Company did not have to reassess whether expired or existing contracts are or contain a lease; did not have to reassess the lease classifications or reassess the initial direct costs associated with expired or existing

leases. Furthermore, the Company did not have any leases impacted by ASC 842 on the adoption date. As part of the purchase price allocation from the reverse merger, the Company recorded a Right of Use asset and Liability of $1.4 million for

office space located in Berkeley Heights, New Jersey. The lease for property in Berkeley Heights was subsequently terminated. As of March 5, 2020 the Company entered into a new sub lease for office space at Florham Park commencing May 1, 2020.

See note 6 for details.

The new lease standard also provides practical expedients for an entity’s ongoing accounting. The Company elected the short-term lease recognition exemption under which the Company

will not recognize right-of-use (“ROU”) assets or lease liabilities, and this includes not recognizing ROU assets or lease liabilities for existing short-term leases. The Company elected the practical expedient to not separate lease and non-lease

components for certain classes of assets (office building).

The Company determines if an arrangement is a lease at inception. Operating lease ROU assets and operating lease liabilities are recognized based on the present

value of the future minimum lease payments over the lease term. Operating lease expense is recognized on a straight-line basis over the lease term, subject to any changes in the lease or expectations regarding the terms. Variable lease costs

such as operating costs and property taxes are expensed as incurred. As of June 30, 2020, there is an active lease accounted for under ASC 842.

In August 2018, the FASB issued ASU No. 2018-13, Fair Value Measurement (Topic 820) (“ASU 2018-13”). ASU 2018-13 modifies

disclosure requirements related to fair value measurement. On January 1, 2020, the Company adopted ASU 2018-07 and there was no impact to its financial statements.

In August 2018, the FASB issued ASU No. 2018-15, Intangibles-Goodwill and Other-Internal-Use Software (Subtopic 350-40) (“ASU

2018-15”). ASU 2018-15 reduces complexity for the accounting for costs of implementing a cloud computing service arrangement and aligns the requirements for capitalizing implementation costs incurred in a hosting arrangement that is a service

contract with the requirements for capitalizing implementation costs incurred to develop or obtain internal-use software (and hosting arrangements that include an internal use software license). On January 1, 2020, the Company adopted ASU

2018-07 and there was no impact to its financial statements

Note 3 – Liquidity

As of June 30, 2020, the Company had $16.9 million of cash and cash equivalents, primarily provided by $29.1 million of pre-existing cash on Edge’s balance sheets that the Company obtained as a

result of the Merger and net proceeds of $12.8 million from the sale of our common stock. The Company’s primary uses of cash are to fund operating expenses, primarily research and development expenditures. Cash used to fund operating expenses is

impacted by the timing of when the Company pays these expenses, as reflected in the change to the Company’s outstanding accounts payable and accrued expenses.

In July 2019, the Company entered into a common stock purchase agreement, or the Aspire Purchase Agreement, with Aspire Capital, which provides that, upon the terms

and subject to the conditions and limitations set forth therein, at the Company’s discretion, Aspire Capital is committed to purchase up to an aggregate of $20.0 million of shares of the Company’s common stock (the “Purchased Shares”), over the

30-month term of the Aspire Purchase Agreement. The Company may sell an aggregate of 1,034,979 shares of its common stock (which represented 19.99% of the Company’s outstanding shares of common stock on the date of the Aspire Purchase

Agreement) without stockholder approval. The Company may sell additional shares of its common stock above the 19.99% limit provided that (i) it obtains stockholder approval or (ii) stockholder approval has not been obtained at any time the

1,034,979 share limitation is reached and at all times thereafter the average price paid for all shares issued under the Aspire Purchase Agreement, is equal to or greater than $5.76, which was the consolidated closing bid price of the Company’s

common stock on July 26, 2019. On July 29, 2019, the Company issued 100,654 shares of our common stock to Aspire Capital, as consideration for entering into the Aspire Purchase Agreement. As of June 30, 2020 no shares

have been sold to Aspire.

In February 2020, the Company completed an underwritten public offering, in which we sold 10,000,000 shares of common stock at a public offering price of $1.30 per share. The shares

sold included 769,230 shares issued upon the exercise by the underwriter of its option to purchase additional shares at the public offering price, minus underwriting discounts and commissions. The Company received gross proceeds of approximately

$13 million and net proceeds of approximately $11.9 million after deducting underwriting discounts and commissions.

On July 22, 2020, the Company filed a shelf registration statement (the “2020 Shelf Registration Statement”), with the SEC, for the issuance of common stock, preferred stock, warrants, rights, debt

securities and units (collectively, the “Shelf Securities”), up to an aggregate amount of $100 million. The 2020 Shelf Registration Statement was declared effective on July 31, 2020. On August 13, 2020, the Company sold 6,900,000 shares of its

common stock at a public offering price of $2.75 per share pursuant to the 2020 Shelf Registration Statement, which includes 900,000 shares issued upon the exercise by the underwriter of its option to purchase additional shares at the public

offering price, minus underwriting discounts and commissions. The Company received gross proceeds of approximately $19.0 million and net proceeds of approximately $17.1 million, after deducting underwriting discounts and offering expenses.

Approximately $81,000,000 of Shelf Securities remain available for future sale under the 2020 Shelf Registration Statement.

Our primary uses of cash are to fund operating expenses, primarily research and development expenditures. Cash used to fund operating expenses is impacted by the timing of when we pay these

expenses, as reflected in the change in our outstanding accounts payable and accrued expenses.

The Company evaluated whether there are any conditions and events, considered in the aggregate, that raise substantial doubt about its ability to continue as a going concern within

one year beyond the filing of this Quarterly Report on Form 10-Q. The Company’s budgeted cash requirements in 2020 and beyond include expenses related to continuing development and clinical studies. Based on the Company’s available cash resources

and cash flow projections as of the date the consolidated financial statements were available for issuance, the Company believes there are sufficient funds to continue operations and research and development programs for at least 12 months from the

date of this report. Until the Company can generate significant cash from its operations, the Company expects to continue to fund its operations with its available financial resources. These financial resources may not be adequate to sustain its

operations.

The Company plans to continue to fund its operations and capital funding needs through equity and/or debt financings. However, the Company cannot be certain that

additional financing will be available when needed or that, if available, financing will be obtained on terms favorable to the Company or its existing stockholders. The Company may also enter into government funding programs and consider

selectively partnering for clinical development and commercialization. The sale of additional equity would result in additional dilution to its stockholders. Incurring debt financing would result in debt service obligations, and the instruments

governing such debt could provide for operating and financing covenants that would restrict the Company’s operations. If the Company is unable to raise additional capital in sufficient amounts or on acceptable terms, it may be required to delay,

limit, reduce, or terminate its product development or future commercialization efforts or grant rights to develop and market immunotherapies that the Company would otherwise prefer to develop and market itself. Any of these actions could harm the

Company’s business, results of operations and prospects. Failure to obtain adequate financing also may adversely affect the Company’s ability to operate as a going concern.

Note 4 – Reverse Merger

On March 15, 2019, the Company (then operating as Edge), Merger Sub and Private PDS completed the Merger in accordance with the Plan of Merger and Reorganization, dated as of November 23, 2018, as

amended on January 24, 2019, pursuant to and in accordance with which Merger Sub merged with and into Private PDS, with Private PDS surviving as the Company’s wholly-owned subsidiary. Immediately following completion of the Merger, the Company

effected the Reverse Stock Split at a ratio of one new share for every twenty shares of its common stock then-outstanding, and changed its corporate name from Edge Therapeutics, Inc. to PDS Biotechnology Corporation, and Private PDS, now the

Company’s wholly-owned subsidiary, changed its name to PDS Operating Corporation. The Merger is intended to qualify for federal income tax purposes as a tax-free reorganization under the provisions of Section 368(a)

of the Internal Revenue Code of 1986, as amended.

In connection with the Merger, each share of Private PDS’s common stock outstanding immediately prior to the Merger was converted into 0.3262 shares (on a post-Reverse Stock Split basis) of the

Company’s common stock. As a result, the Company issued 3,573,760 shares of its common stock to the stockholders of Private PDS in exchange for all of the outstanding shares of common stock of Private PDS.

For accounting purposes, Private PDS is considered to be the accounting acquirer in the Merger because Private PDS’s stockholders owned approximately 70% of PDS’s common stock immediately following

the closing of the Merger. As the accounting acquirer, Private PDS’s assets and liabilities continue to be recorded at their historical carrying amounts and the historical operations that will be reflected in the Company’s financial statements will

be those of Private PDS. All references in the unaudited interim condensed consolidated financial statements to the number of shares and per share amounts of the Company’s common stock have been retroactively restated to reflect completion of the

Merger and the Reverse Stock Split.

Purchase Price

Pursuant to the Merger Agreement, Edge issued to Private PDS’s stockholders a number of shares of Edge’s common stock representing approximately 70% of the outstanding shares of common stock of the

combined company. The purchase price, which represents the consideration transferred to Edge’s stockholders in the Merger is calculated based on the number of shares of common stock of the combined company that Edge’s stockholders owned as of the

closing of the Merger on March 15, 2019, which consists of the following:

|

Number of shares of the combined company to be owned by Edge security holders (1)

|

1,600,166

|

|||

|

Multiplied by the price per share of Edge’s common stock as of March 15, 2019

|

$

|

9.87

|

||

|

Purchase price (in thousands)

|

$

|

15,794

|

| (1) |

The amount includes 1,576,916 shares of Edge’s common stock outstanding as of March 15, 2019 plus 23,250 stock options of Edge that were in the money and vested immediately upon closing of the Merger. At the

closing of the Merger, 753 of in-the-money options and 235 fractional shares paid out in cash to shareholders were not issued as common stock, resulting in 1,599,178 common shares issued.

|

Final Purchase Price Allocation

The Company completed its analysis of the allocation of the purchase price in the fourth quarter of 2019. The purchase price was allocated to the net assets acquired of Edge based upon their

preliminary estimated fair values as of March 15, 2019. The in-process research and development asset (“IPR&D”) that is recognized relates to Edge’s NEWTON 2 clinical trial for EG-1962 that has not reached

technological feasibility. The Company was actively looking to license out EG-1962 and had preliminary discussions with third parties who were actively looking at the data of EG-1962 during the prior year.

Accordingly, the IPR&D was initially capitalized as an indefinite-lived intangible asset and tested for impairment at least annually until it is determined that there is no future economic benefit from EG-1962. As a result of capitalizing the

IPR&D, the Company initially recognized an indefinite life deferred tax liability. During the three months ended June 30, 2019, two adjustments were made to the preliminary allocation. The first was for $275,000 relating to an offer to purchase

equipment that was given a value of $0 in the preliminary allocation. The second was for $65,551 relating to Edge’s bonus plan that was effective prior to the date of acquisition. During the three months ended December 31, 2019 two additional

adjustments were made to the preliminary valuation. The first was for an increase of $1,751,000 relating to the IPR&D in which the Company finalized the valuation of the IPR&D and as a result recognized an additional deferred tax liability

of $224,513. The second was for a write-off relating to a transition service arrangement that was effective prior to the date of the acquisition for $131,250. In accordance with ASC 805, Business Combinations any the excess of the fair value of the

acquired net assets over the purchase price has been recognized as a bargain purchase gain in the consolidated statement of operations and comprehensive loss. The Company has reassessed whether all the assets acquired, and the liabilities assumed

have been identified and recognized in the purchase price allocation.

The final allocation of the purchase price to the net assets of Edge, based on the fair values as of March 15, 2019, is as follows:

|

Cash and cash equivalents

|

$

|

29,106,513

|

||

|

Prepaid expense and other assets

|

1,585,482

|

|||

|

Right to use asset

|

1,384,810

|

|||

|

Intangible assets-IPR&D

|

2,974,000

|

|||

|

Total identifiable assets acquired

|

35,050,805

|

|||

|

Accounts payable, accrued expenses, other liabilities

|

(4,595,934

|

)

|

||

|

Lease liability

|

(945,152

|

)

|

||

|

Deferred tax liability

|

(381,513

|

)

|

||

|

Total liabilities assumed

|

(5,922,599

|

)

|

||

|

Net identifiable assets acquired

|

29,128,206

|

|||

|

Bargain purchase gain (1)

|

(13,334,568

|

)

|

||

|

Purchase price

|

$

|

15,793,638

|

| (1) |

Due to the aforementioned purchase price adjustments subsequent to March 31, 2019, the preliminary estimate of the bargain purchase gain was adjusted from $11,729,882 and finalized for the year ended December 31, 2019 at $13,334,568.

|

The fair value of the IPR&D was determined using the discounted cash flow method based on probability- adjusted cash flow success scenarios to develop EG-1962 into a commercial product,

estimating the revenue and costs. The rates utilized to discount the net cash flows to the present value are commensurate with the stage of development of the projects and uncertainties in the economic estimates used in the projections.

During the three months ended December 31, 2019, the Company determined that the intangible asset related to Edge’s NEWTON 2 clinical trial for EG-1962 was impaired

due to significantly reduced activity in the data room and a lack of new interest from third parties to purchase or license the product. Further the Company does not have the internal resources to pursue EG-1962 as an internal development

project and has stated publicly that it had intended to find a partner to fund and run the EG-1962 program. The drop off in interest from third parties and the lack of any new inbound interest has made this an extremely low probability of success.

As a result for the year ended December 31, 2019, the Company recorded an impairment charge - IPR&D of $2,974,000 for the estimated value of the IPR&D asset of $2,974,000 in its consolidated statement of

operations and comprehensive loss.

Note 5 – Fair Value of Financial Instruments

There were no transfers among Levels 1, 2, or 3 during 2020 or 2019.

|

Fair Value Measurements at Reporting Date Using

|

||||||||||||||||

|

Total

|

Quoted Prices in

Active Markets

(Level 1)

|

Quoted Prices in

Inactive Markets

(Level 2)

|

Significant

Unobservable Inputs

(Level 3)

|

|||||||||||||

|

As of June 30, 2020: (unaudited)

|

||||||||||||||||

|

Cash and cash equivalents

|

$

|

16,934,495

|

$

|

16,934,495

|

$

|

–

|

$

|

–

|

||||||||

|

As of December 31, 2019:

|

||||||||||||||||

|

Cash and cash equivalents

|

$

|

12,161,739

|

$

|

12,161,739

|

$

|

–

|

$

|

–

|

||||||||

Note 6 – Leases

On July 8, 2019, the Company entered into a lease termination agreement for its office space located at 300 Connell Drive, Suite 4000, Berkeley Heights, NJ 07922 effective August

31, 2019 (the “Lease Termination Agreement”). Pursuant to the Lease Termination Agreement, the Company was required to pay 50 percent of the remaining lease payments of $665,802 over three installments on September 1, 2019, December 1, 2019, and

March 1, 2020, which was recorded as lease termination costs in the third quarter of 2019. On August 31, 2019, the right-of-use asset of $1.2 million and operating lease liability of $1.2 million was written off. Leasehold improvements amounting to

approximately $0.3 million were also written off and are included in lease termination costs. The Company entered into a temporary month-to-month lease as of September 1, 2019 for office space located at 830 Morris Turnpike, Short Hills, NJ 07078

until the Company entered into a new lease for permanent office space. This lease was terminated on May 31, 2020.

Effective March 5, 2020, the Company entered into a sublease for approximately 11,200 square feet of office space located at 25B Vreeland Road, Florham Park, NJ. The sublease

commenced on May 1, 2020 and will continue for a term of forty (40) months with an option to renew through October 31, 2027. Upon inception of the lease, the Company recognized approximately $0.7 million of a ROU asset and operating lease

liabilities. The discount rate used to measure the operating lease liability as of May 1, 2020 was 9.15%. Throughout the period described above the Company has maintained, and continues to maintain, a month-to-month lease for its research

facilities at the Princeton Innovation Center BioLabs located at 303A College Road E, Princeton NJ, 08540.

|

Six Months Ended

June 30, 2020 |

||||

|

Cash paid for amounts included in measurement of lease liabilities:

|

||||

|

Operating cash outflows for operating lease

|

$

|

15,649

|

||

|

Right-of use asset obtained in exchange for new operating lease liability

|

$

|

638,831

|

||

|

Remaining lease term - operating lease liability

|

38.0

|

|||

|

Discount rate - operating lease

|

9.15

|

%

|

||

|

Reported as of June 30, 2020

|

||||

|

Current portion of operating lease liability

|

$

|

112,657

|

||

|

Operating leases, net of current portion

|

552,326

|

|||

|

Total

|

$

|

664,983

|

||

Note 7 – Accrued Expenses and Restructuring Reserve

Accrued expenses and other liabilities consist of the following:

|

As of

June 30, 2020

|

As of

December 31, 2019

|

|||||||

|

Accrued research and development costs

|

$

|

147,841

|

$

|

16,415

|

||||

|

Accrued professional fees

|

135,641

|

256,062

|

||||||

|

Accrued compensation

|

910,876

|

603,229

|

||||||

|

Accrued rent

|

–

|

221,934

|

||||||

|

Total

|

$

|

1,194,358

|

$

|

1,097,640

|

||||

Restructuring Reserve

|

As of

June 30, 2020

|

As of

December 31, 2019

|

|||||||

|

Restructuring reserve (1)

|

$

|

126,862

|

$

|

498,185

|

||||

|

Total

|

$

|

126,862

|

$

|

498,185

|

||||

|

(1)

|

Restructuring reserve relates to the severance costs incurred by Edge prior to the Merger and assumed by the Company as part of the purchase accounting, but not yet paid. The severance costs continue

through September 2020. For the six months ended June 30, 2020, the Company paid $371,323 of restructuring expense which was previously recorded on Edge’s financials.

|

Note 8 – Stock-Based Compensation

The Company has four equity compensation plans: the 2009 Amended Stock Option Plan, the 2010 Equity Incentive Plan, the 2014 Equity Incentive Plan and the 2018 Stock Incentive Plan

(the “Plans”). Originally, the Company was able to grant up to 27,410 of Common Stock as both incentive stock options (“ISOs”) and nonqualified stock options (“NQs”) under the 2010 Equity Incentive Plan. In 2013, the

Company’s stockholders approved an increase to 63,957 shares authorized for issuance under the 2010 Equity Incentive Plan. In 2014, the Board of Directors of the Company (the “Board”) approved an increase to 67,520 shares authorized for issuance

under the 2010 Equity Incentive Plan

In 2014, the Company’s stockholders approved the 2014 Equity Incentive Plan pursuant to which the Company may grant up to 91,367 shares as ISOs, NQs and restricted stock units

(“RSUs”), subject to increases as hereafter described (the “Plan Limit”). In addition, on January 1, 2015 and each January 1 thereafter prior to the termination of the 2014 Equity Incentive Plan, pursuant to the terms of the 2014 Equity Incentive

Plan, the Plan Limit was and shall be increased by the lesser of (x) 4% of the number of shares of Common Stock outstanding as of the immediately preceding December 31 and (y) such lesser number as the Board of Directors may determine in its

discretion. On January 1, 2016, 2017, 2018 and 2019 the Plan Limit was increased to 152,366 shares, 210,203 shares, 271,941 shares and 323,529 shares, respectively. In March 2019, the Plan was amended and restated which removed the annual increase

component and was limited to 826,292 shares.

In 2018, the Company’s stockholders approved the 2018 Stock Incentive Plan pursuant to which the Company may grant up to 558,071 shares as Stock Options, (ii) Stock Appreciation

Rights, (iii) Restricted Stock, (iv) Deferred Stock, (v) Stock Reload Options and/or (vi) Other Stock-Based Awards.

Pursuant to the terms of the Plans, ISOs have a term of ten years from the date of grant or such shorter term as may be provided in the option agreement. Unless specified otherwise

in an individual option agreement, ISOs generally vest over a four year term and NQs generally vest over a one to five year terms. Unless terminated by the Board, the Plans shall continue to remain effective for a term of ten years or until such

time as no further awards may be granted and all awards granted under the Plans are no longer outstanding. As of June 30, 2020 there were 190,799 shares available for grant under the 2018 Stock Incentive Plan.

On June 17, 2019, the Board adopted the 2019 Inducement Plan. The 2019 Inducement Plan provides for the grant of non-qualified stock options. The 2019 Inducement Plan was

recommended for approval by the Compensation Committee of the Board and subsequently approved and adopted by the Board without stockholder approval pursuant to Rule 5635(c)(4) of the Nasdaq Listing Rules.

The Board has reserved 200,000 shares of the Company’s common stock for issuance pursuant to non-qualified stock options granted under the 2019 Inducement Plan, and

the 2019 Inducement Plan will be administered by the Compensation Committee of the Board. In accordance with Rule 5635(c)(4) of the Nasdaq Listing Rules, non-qualified stock options under the 2019 Inducement Plan may only be made to an employee

who has not previously been an employee or member of the Board (or any parent or subsidiary of the Company), or following a bona fide period of non-employment by the Company (or a parent or subsidiary of the Company), if he or she is granted such

non-qualified stock options in connection with his or her commencement of employment with the Company or a subsidiary and such grant is an inducement material to his or her entering into employment with the Company or such subsidiary. As

of June 30, 2020, there were 121,500 shares available for grant under the 2019 Inducement Plan.

The Company’s stock-based compensation expense related to stock options was recognized in operating expense as follows:

|

Three Months Ended June 30,

|

Six Months Ended June 30,

|

|||||||||||||||

|

2020

|

2019

|

2020

|

2019

|

|||||||||||||

|

(unaudited)

|

(unaudited)

|

|||||||||||||||

|

Stock-Based Compensation

|

||||||||||||||||

|

Research and development

|

$

|

53,842

|

$

|

9,387

|

$

|

106,526

|

$

|

450,087

|

||||||||

|

General and administrative

|

(7,728

|

)

|

9,193

|

64,580

|

2,323,364

|

|||||||||||

|

Total

|

$

|

46,113

|

$

|

18,580

|

$

|

171,106

|

$

|

2,773,451

|

||||||||

The fair value of options granted during the three and six months ended June 30, 2020 and the three and six months ended June 30, 2019 was estimated using the Black-Scholes option valuation model

utilizing the following assumptions.

|

Three Months Ended June 30,

|

Six Months Ended June 30,

|

|||||||||||||||

|

2020

|

2019

|

2020

|

2019

|

|||||||||||||

|

Weighted Average

|

Weighted Average

|

Weighted Average

|

Weighted Average

|

|||||||||||||

|

(unaudited)

|

(unaudited)

|

|||||||||||||||

|

Volatility

|

97.13

|

%

|

94.43

|

%

|

97.00

|

%

|

88.87

|

%

|

||||||||

|

Risk-Free Interest Rate

|

0.34

|

%

|

2.19

|

%

|

0.38

|

%

|

2.34

|

%

|

||||||||

|

Expected Term in Years

|

6.07

|

6.08

|

6.07

|

6.17

|

||||||||||||

|

Dividend Rate

|

0.00

|

%

|

0.00

|

%

|

0.00

|

%

|

0.00

|

%

|

||||||||

|

Fair Value of Option on Grant Date

|

$

|

1.11

|

$

|

4.77

|

$

|

1.10

|

$

|

5.31

|

||||||||

The following table summarizes the number of options outstanding and the weighted average exercise price:

|

Number

of Shares

|

Weighted

Average

Exercise Price

|

Weighted Average

Remaining

Contractual

Life in Years

|

Aggregate

Intrinsic Value

|

|||||||||||||

|

Options outstanding at December 31, 2019

|

1,421,797

|

$

|

15.95

|

|||||||||||||

|

Granted

|

319,907

|

1.43

|

||||||||||||||

|

Exercised

|

–

|

–

|

||||||||||||||

|

Forfeited

|

(84,227

|

)

|

41.34

|

|||||||||||||

|

Expired

|

(17,724

|

)

|

4.69

|

|||||||||||||

|

Options outstanding at June 30, 2020

|

1,639,753

|

$

|

11.94

|

7.17

|

$

|

184,693–

|

||||||||||

|

Vested and expected to vest at June 30, 2020

|

1,639,753

|

$

|

11.94

|

7.17

|

$

|

184,693–

|

||||||||||

|

Exercisable at June 30, 2020

|

1,047,284

|

$

|

16.73

|

5.84

|

$

|

–

|

||||||||||

At June 30, 2020 there was approximately $1,554,689 of unamortized stock option compensation expense, which is expected to be recognized over a remaining average vesting period

of 3.39 years.

Note 9 – Income Taxes

In assessing the realizability of the net deferred tax assets, the Company considers all relevant positive and negative evidence to determine whether it is more likely than not that some portion or

all of the deferred income tax assets will not be realized. The realization of the gross deferred tax assets is dependent on several factors, including the generation of sufficient taxable income prior to the expiration of the net operating loss

carryforwards. The Company expects to have a loss for 2020 and there will be no current income tax expense. Additionally, there was a full valuation allowance against the net deferred tax assets as of June 30, 2020 and December 31, 2019. As

such, the Company recorded no income tax benefit due to realization uncertainties.

The Company’s U.S. statutory rate is 21%. The primary factor impacting the effective tax rate for the three and six months ended June 30, 2020 is the anticipated full year operating loss which

will require full valuation allowances against any associated net deferred tax assets.

Entities are also required to evaluate, measure, recognize and disclose any uncertain income tax provisions taken on their income tax returns. The Company has analyzed its tax

positions and has concluded that as of June 30, 2020, there were no uncertain positions. The Company’s U.S. federal and state net operating losses have occurred since its inception and as such, tax years subject to potential tax examination could

apply from that date because the utilization of net operating losses from prior years opens the relevant year to audit by the IRS and/or state taxing authorities. The Company did not have any unrecognized tax benefits and has not accrued any

interest or penalties for the three and six months ended June 30, 2020 and for the year ended December 31, 2019.

Note 10 – Commitments and Contingencies

Employment Matters

The Company has entered into employment agreements or offer letters with each of its executive officers. The employment agreements generally provide for, among other things, salary,

bonus and severance payments. The employment agreements generally provide for between 12 months and 24 months of severance benefits to be paid to an executive (as well as certain potential bonus, COBRA and equity award benefits), subject to the

effectiveness of a general release of claims, if the executive terminates his or her employment for good reason or if the Company terminates the executive’s employment without cause. Such severance payments may be provided for as long as 24 months

in connection with a termination following a change of control. The continued provision of severance benefits is conditioned on each executive’s compliance with the terms of the Company’s confidentiality and invention and assignment agreement as

well as his or her release of claims.

For month-to-month arrangements not impacted by the adoption of ASC 842, rent for the three and six months ended June 30, 2020 was $46,337 and $104,978 compared to the

three and six months ended June 30, 2019 of $11,400 and $ 20,300.

Note 11 – Retirement Plan

The Company has a 401(k) defined contribution plan as a benefit for all employees and permits voluntary contributions by employees subject to IRS-imposed

limitations. Employer 401K contributions for the three and six months ended June 30, 2020 was $10,168 and $19,966, respectively, compared to the three and six months ended June 30, 2019 of $25,242.

On August 13, 2020, the Company sold 6,900,000 shares of its common stock at a public offering price of $2.75 per share pursuant to the 2020 Shelf Registration Statement, which includes 900,000

shares issued upon the exercise by the underwriter of its option to purchase additional shares at the public offering price, minus underwriting discounts and commissions. The Company received gross proceeds of approximately $19.0 million and net

proceeds of approximately $17.1 million, after deducting underwriting discounts and offering expenses.

| ITEM 2. |

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with our unaudited interim

condensed consolidated financial statements and related notes thereto appearing elsewhere in this Quarterly Report on Form 10-Q (this “Quarterly Report”) and with the audited financial statements and notes

thereto of the Company as of and for the year ended December 31, 2019 on Form 10-K, filed with the Securities and Exchange Commission, or SEC, on March 27, 2020. As

further described in “Note 1 – Nature of Operations” and “Note 4 – Reverse Merger” in this Quarterly Report, Private PDS was determined to be the accounting acquirer in the Merger and, accordingly, the pre-Merger historical financial information

presented in this Quarterly Report reflects the standalone financial statements of Private PDS and, therefore, period-over-period comparisons may not be meaningful. Except as otherwise indicated herein or

as the context otherwise requires, references in this Quarterly Report to “PDS” “the Company,” “we,” “us” and “our” refer to PDS Biotechnology Corporation, a Delaware corporation, on a post-Merger basis,

and the term “Private PDS” refers to the business of privately held PDS Biotechnology Corporation prior to completion of the Merger.

Cautionary Note Regarding Forward-Looking Statements