0001466593falseFY2021http://fasb.org/us-gaap/2021-01-31#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2021-01-31#OtherAssetsNoncurrenthttp://fasb.org/us-gaap/2021-01-31#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2021-01-31#OtherLiabilitiesCurrenthttp://fasb.org/us-gaap/2021-01-31#OtherLiabilitiesNoncurrenthttp://fasb.org/us-gaap/2021-01-31#OtherLiabilitiesNoncurrentP3Y00014665932021-01-012021-12-3100014665932021-06-30iso4217:USD00014665932022-02-07xbrli:shares00014665932021-12-3100014665932020-12-31iso4217:USDxbrli:shares0001466593ottr:ElectricMember2021-01-012021-12-310001466593ottr:ElectricMember2020-01-012020-12-310001466593ottr:ElectricMember2019-01-012019-12-310001466593ottr:ProductSalesMember2021-01-012021-12-310001466593ottr:ProductSalesMember2020-01-012020-12-310001466593ottr:ProductSalesMember2019-01-012019-12-3100014665932020-01-012020-12-3100014665932019-01-012019-12-310001466593us-gaap:CommonStockMember2018-12-310001466593us-gaap:AdditionalPaidInCapitalMember2018-12-310001466593us-gaap:RetainedEarningsMember2018-12-310001466593us-gaap:AccumulatedOtherComprehensiveIncomeMember2018-12-3100014665932018-12-310001466593us-gaap:CommonStockMember2019-01-012019-12-310001466593us-gaap:AdditionalPaidInCapitalMember2019-01-012019-12-310001466593us-gaap:RetainedEarningsMember2019-01-012019-12-310001466593us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-01-012019-12-310001466593us-gaap:CommonStockMember2019-12-310001466593us-gaap:AdditionalPaidInCapitalMember2019-12-310001466593us-gaap:RetainedEarningsMember2019-12-310001466593us-gaap:AccumulatedOtherComprehensiveIncomeMember2019-12-3100014665932019-12-310001466593us-gaap:CommonStockMember2020-01-012020-12-310001466593us-gaap:AdditionalPaidInCapitalMember2020-01-012020-12-310001466593us-gaap:RetainedEarningsMember2020-01-012020-12-310001466593us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-01-012020-12-310001466593us-gaap:CommonStockMember2020-12-310001466593us-gaap:AdditionalPaidInCapitalMember2020-12-310001466593us-gaap:RetainedEarningsMember2020-12-310001466593us-gaap:AccumulatedOtherComprehensiveIncomeMember2020-12-310001466593us-gaap:CommonStockMember2021-01-012021-12-310001466593us-gaap:AdditionalPaidInCapitalMember2021-01-012021-12-310001466593us-gaap:RetainedEarningsMember2021-01-012021-12-310001466593us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-01-012021-12-310001466593us-gaap:CommonStockMember2021-12-310001466593us-gaap:AdditionalPaidInCapitalMember2021-12-310001466593us-gaap:RetainedEarningsMember2021-12-310001466593us-gaap:AccumulatedOtherComprehensiveIncomeMember2021-12-31ottr:segment0001466593ottr:ElectricPlantMember2021-01-012021-12-310001466593ottr:ElectricPlantMember2020-01-012020-12-310001466593ottr:ElectricPlantMember2019-01-012019-12-310001466593srt:MinimumMemberottr:ElectricPlantMemberus-gaap:EquipmentMember2021-01-012021-12-310001466593ottr:ElectricPlantMembersrt:MaximumMemberus-gaap:EquipmentMember2021-01-012021-12-310001466593srt:MinimumMemberus-gaap:EquipmentMemberottr:NonelectricPlantMember2021-01-012021-12-310001466593srt:MaximumMemberus-gaap:EquipmentMemberottr:NonelectricPlantMember2021-01-012021-12-310001466593srt:MinimumMemberottr:BuildingAndLeaseholdImprovementsMemberottr:NonelectricPlantMember2021-01-012021-12-310001466593ottr:BuildingAndLeaseholdImprovementsMembersrt:MaximumMemberottr:NonelectricPlantMember2021-01-012021-12-31ottr:plantottr:unit0001466593srt:MinimumMember2021-01-012021-12-310001466593srt:MaximumMember2021-01-012021-12-310001466593srt:MinimumMember2021-12-310001466593srt:MaximumMember2021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:CoyoteCreekMiningCompanyLLCCCMCMemberottr:LigniteSalesAgreementMember2021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:CoyoteCreekMiningCompanyLLCCCMCMemberottr:LigniteSalesAgreementMember2021-01-012021-12-31xbrli:pure0001466593us-gaap:OperatingSegmentsMemberottr:ElectricMember2021-01-012021-12-310001466593us-gaap:OperatingSegmentsMemberottr:ElectricMember2020-01-012020-12-310001466593us-gaap:OperatingSegmentsMemberottr:ElectricMember2019-01-012019-12-310001466593us-gaap:OperatingSegmentsMemberottr:ManufacturingMember2021-01-012021-12-310001466593us-gaap:OperatingSegmentsMemberottr:ManufacturingMember2020-01-012020-12-310001466593us-gaap:OperatingSegmentsMemberottr:ManufacturingMember2019-01-012019-12-310001466593us-gaap:OperatingSegmentsMemberottr:PlasticsMember2021-01-012021-12-310001466593us-gaap:OperatingSegmentsMemberottr:PlasticsMember2020-01-012020-12-310001466593us-gaap:OperatingSegmentsMemberottr:PlasticsMember2019-01-012019-12-310001466593us-gaap:CorporateNonSegmentMember2021-01-012021-12-310001466593us-gaap:CorporateNonSegmentMember2020-01-012020-12-310001466593us-gaap:CorporateNonSegmentMember2019-01-012019-12-310001466593us-gaap:OperatingSegmentsMemberottr:ElectricMember2021-12-310001466593us-gaap:OperatingSegmentsMemberottr:ElectricMember2020-12-310001466593us-gaap:OperatingSegmentsMemberottr:ManufacturingMember2021-12-310001466593us-gaap:OperatingSegmentsMemberottr:ManufacturingMember2020-12-310001466593us-gaap:OperatingSegmentsMemberottr:PlasticsMember2021-12-310001466593us-gaap:OperatingSegmentsMemberottr:PlasticsMember2020-12-310001466593us-gaap:CorporateNonSegmentMember2021-12-310001466593us-gaap:CorporateNonSegmentMember2020-12-310001466593ottr:ElectricMemberottr:RetailResidentialMember2021-01-012021-12-310001466593ottr:ElectricMemberottr:RetailResidentialMember2020-01-012020-12-310001466593ottr:ElectricMemberottr:RetailResidentialMember2019-01-012019-12-310001466593ottr:RetailCommercialAndIndustrialMemberottr:ElectricMember2021-01-012021-12-310001466593ottr:RetailCommercialAndIndustrialMemberottr:ElectricMember2020-01-012020-12-310001466593ottr:RetailCommercialAndIndustrialMemberottr:ElectricMember2019-01-012019-12-310001466593ottr:ElectricMemberottr:RetailOtherMember2021-01-012021-12-310001466593ottr:ElectricMemberottr:RetailOtherMember2020-01-012020-12-310001466593ottr:ElectricMemberottr:RetailOtherMember2019-01-012019-12-310001466593ottr:ElectronicProductRetailMemberottr:ElectricMember2021-01-012021-12-310001466593ottr:ElectronicProductRetailMemberottr:ElectricMember2020-01-012020-12-310001466593ottr:ElectronicProductRetailMemberottr:ElectricMember2019-01-012019-12-310001466593ottr:ElectricMemberus-gaap:ElectricTransmissionMember2021-01-012021-12-310001466593ottr:ElectricMemberus-gaap:ElectricTransmissionMember2020-01-012020-12-310001466593ottr:ElectricMemberus-gaap:ElectricTransmissionMember2019-01-012019-12-310001466593ottr:WholesaleMemberottr:ElectricMember2021-01-012021-12-310001466593ottr:WholesaleMemberottr:ElectricMember2020-01-012020-12-310001466593ottr:WholesaleMemberottr:ElectricMember2019-01-012019-12-310001466593ottr:ElectricMemberottr:ElectricProductOtherMember2021-01-012021-12-310001466593ottr:ElectricMemberottr:ElectricProductOtherMember2020-01-012020-12-310001466593ottr:ElectricMemberottr:ElectricProductOtherMember2019-01-012019-12-310001466593ottr:ElectricMember2021-01-012021-12-310001466593ottr:ElectricMember2020-01-012020-12-310001466593ottr:ElectricMember2019-01-012019-12-310001466593ottr:ManufacturingMemberottr:MetalPartsAndToolingMember2021-01-012021-12-310001466593ottr:ManufacturingMemberottr:MetalPartsAndToolingMember2020-01-012020-12-310001466593ottr:ManufacturingMemberottr:MetalPartsAndToolingMember2019-01-012019-12-310001466593ottr:ManufacturingMemberottr:PlasticProductsMember2021-01-012021-12-310001466593ottr:ManufacturingMemberottr:PlasticProductsMember2020-01-012020-12-310001466593ottr:ManufacturingMemberottr:PlasticProductsMember2019-01-012019-12-310001466593ottr:ManufacturingMemberus-gaap:ManufacturedProductOtherMember2021-01-012021-12-310001466593ottr:ManufacturingMemberus-gaap:ManufacturedProductOtherMember2020-01-012020-12-310001466593ottr:ManufacturingMemberus-gaap:ManufacturedProductOtherMember2019-01-012019-12-310001466593ottr:ManufacturingMember2021-01-012021-12-310001466593ottr:ManufacturingMember2020-01-012020-12-310001466593ottr:ManufacturingMember2019-01-012019-12-310001466593ottr:PlasticsMember2021-01-012021-12-310001466593ottr:PlasticsMember2020-01-012020-12-310001466593ottr:PlasticsMember2019-01-012019-12-310001466593ottr:PensionAndOtherPostretirementBenefitPlansMember2021-12-310001466593ottr:PensionAndOtherPostretirementBenefitPlansMember2020-12-310001466593ottr:AlternativeRevenueProgramRidersMember2021-01-012021-12-310001466593ottr:AlternativeRevenueProgramRidersMember2021-12-310001466593ottr:AlternativeRevenueProgramRidersMember2020-12-310001466593ottr:AssetRetirementObligationsMember2021-12-310001466593ottr:AssetRetirementObligationsMember2020-12-310001466593ottr:ISOCostRecoveryTrackersMember2021-01-012021-12-310001466593ottr:ISOCostRecoveryTrackersMember2021-12-310001466593ottr:ISOCostRecoveryTrackersMember2020-12-310001466593ottr:UnrecoveredProjectCostsMember2021-01-012021-12-310001466593ottr:UnrecoveredProjectCostsMember2021-12-310001466593ottr:UnrecoveredProjectCostsMember2020-12-310001466593ottr:DeferredRateCaseExpensesMember2021-12-310001466593ottr:DeferredRateCaseExpensesMember2020-12-310001466593ottr:DebtReacquisitionPremiumsMember2021-01-012021-12-310001466593ottr:DebtReacquisitionPremiumsMember2021-12-310001466593ottr:DebtReacquisitionPremiumsMember2020-12-310001466593ottr:FuelClauseAdjustmentsMember2021-01-012021-12-310001466593ottr:FuelClauseAdjustmentsMember2021-12-310001466593ottr:FuelClauseAdjustmentsMember2020-12-310001466593ottr:OtherRegulatoryAssetsMember2021-12-310001466593ottr:OtherRegulatoryAssetsMember2020-12-310001466593ottr:DeferredIncomeTaxesMember2021-12-310001466593ottr:DeferredIncomeTaxesMember2020-12-310001466593ottr:PlantRemovalObligationsMember2021-12-310001466593ottr:PlantRemovalObligationsMember2020-12-310001466593ottr:FuelClauseAdjustmentMember2021-01-012021-12-310001466593ottr:FuelClauseAdjustmentMember2021-12-310001466593ottr:FuelClauseAdjustmentMember2020-12-310001466593ottr:AlternativeRevenueProgramRidersMember2021-12-310001466593ottr:AlternativeRevenueProgramRidersMember2020-12-310001466593ottr:PensionAndOtherPostretirementBenefitPlansMember2021-01-012021-12-310001466593ottr:PensionAndOtherPostretirementBenefitPlansMember2021-12-310001466593ottr:PensionAndOtherPostretirementBenefitPlansMember2020-12-310001466593ottr:DerivativeLiabilitiesMember2021-01-012021-12-310001466593ottr:DerivativeLiabilitiesMember2021-12-310001466593ottr:DerivativeLiabilitiesMember2020-12-310001466593ottr:OtherRegulatoryLiabilitiesMember2021-12-310001466593ottr:OtherRegulatoryLiabilitiesMember2020-12-310001466593ottr:ElectricPlantMemberus-gaap:ElectricGenerationEquipmentMember2021-12-310001466593ottr:ElectricPlantMemberus-gaap:ElectricGenerationEquipmentMember2020-12-310001466593ottr:TransmissionPlantMemberottr:ElectricPlantMember2021-12-310001466593ottr:TransmissionPlantMemberottr:ElectricPlantMember2020-12-310001466593ottr:ElectricPlantMemberottr:DistributionPlantMember2021-12-310001466593ottr:ElectricPlantMemberottr:DistributionPlantMember2020-12-310001466593ottr:GeneralPlantMemberottr:ElectricPlantMember2021-12-310001466593ottr:GeneralPlantMemberottr:ElectricPlantMember2020-12-310001466593ottr:ElectricPlantMemberottr:ElectricPlantInServiceMember2021-12-310001466593ottr:ElectricPlantMemberottr:ElectricPlantInServiceMember2020-12-310001466593ottr:ElectricPlantMemberus-gaap:ConstructionInProgressMember2021-12-310001466593ottr:ElectricPlantMemberus-gaap:ConstructionInProgressMember2020-12-310001466593ottr:ElectricPlantMember2021-12-310001466593ottr:ElectricPlantMember2020-12-310001466593us-gaap:EquipmentMemberottr:NonelectricPlantMember2021-12-310001466593us-gaap:EquipmentMemberottr:NonelectricPlantMember2020-12-310001466593ottr:BuildingsAndLeaseholdImprovementsMemberottr:NonelectricPlantMember2021-12-310001466593ottr:BuildingsAndLeaseholdImprovementsMemberottr:NonelectricPlantMember2020-12-310001466593us-gaap:LandMemberottr:NonelectricPlantMember2021-12-310001466593us-gaap:LandMemberottr:NonelectricPlantMember2020-12-310001466593ottr:NonelectricOperationsPlantMemberottr:NonelectricPlantMember2021-12-310001466593ottr:NonelectricOperationsPlantMemberottr:NonelectricPlantMember2020-12-310001466593us-gaap:ConstructionInProgressMemberottr:NonelectricPlantMember2021-12-310001466593us-gaap:ConstructionInProgressMemberottr:NonelectricPlantMember2020-12-310001466593ottr:NonelectricPlantMember2021-12-310001466593ottr:NonelectricPlantMember2020-12-310001466593ottr:OtterTailPowerCompanyMemberottr:BigStonePlantMember2021-12-310001466593ottr:BigStonePlantMember2021-12-310001466593ottr:CoyoteStationMemberottr:OtterTailPowerCompanyMember2021-12-310001466593ottr:CoyoteStationMember2021-12-310001466593ottr:BigStoneSouthEllendaleMultiValueProjectMemberottr:OtterTailPowerCompanyMember2021-12-310001466593ottr:BigStoneSouthEllendaleMultiValueProjectMember2021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:FargoProjectMember2021-12-310001466593ottr:FargoProjectMember2021-12-310001466593ottr:BigStoneSouthBrookingsMultiValueProjectMemberottr:OtterTailPowerCompanyMember2021-12-310001466593ottr:BigStoneSouthBrookingsMultiValueProjectMember2021-12-310001466593ottr:BrookingsProjectMemberottr:OtterTailPowerCompanyMember2021-12-310001466593ottr:BrookingsProjectMember2021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:BemidjiProjectMember2021-12-310001466593ottr:BemidjiProjectMember2021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:BigStonePlantMember2020-12-310001466593ottr:BigStonePlantMember2020-12-310001466593ottr:CoyoteStationMemberottr:OtterTailPowerCompanyMember2020-12-310001466593ottr:CoyoteStationMember2020-12-310001466593ottr:BigStoneSouthEllendaleMultiValueProjectMemberottr:OtterTailPowerCompanyMember2020-12-310001466593ottr:BigStoneSouthEllendaleMultiValueProjectMember2020-12-310001466593ottr:OtterTailPowerCompanyMemberottr:FargoProjectMember2020-12-310001466593ottr:FargoProjectMember2020-12-310001466593ottr:BigStoneSouthBrookingsMultiValueProjectMemberottr:OtterTailPowerCompanyMember2020-12-310001466593ottr:BigStoneSouthBrookingsMultiValueProjectMember2020-12-310001466593ottr:BrookingsProjectMemberottr:OtterTailPowerCompanyMember2020-12-310001466593ottr:BrookingsProjectMember2020-12-310001466593ottr:OtterTailPowerCompanyMemberottr:BemidjiProjectMember2020-12-310001466593ottr:BemidjiProjectMember2020-12-310001466593ottr:ManufacturingMember2021-12-310001466593ottr:ManufacturingMember2020-12-310001466593ottr:PlasticsMember2021-12-310001466593ottr:PlasticsMember2020-12-310001466593us-gaap:CustomerRelationshipsMember2021-12-310001466593us-gaap:OtherIntangibleAssetsMember2021-12-310001466593us-gaap:CustomerRelationshipsMember2020-12-310001466593us-gaap:OtherIntangibleAssetsMember2020-12-310001466593srt:ParentCompanyMember2021-12-310001466593ottr:OtterTailPowerCompanyMember2021-12-310001466593srt:ParentCompanyMember2020-12-310001466593ottr:OtterTailPowerCompanyMember2020-12-310001466593ottr:OtterTailCorporationCreditAgreementMember2021-12-310001466593ottr:OtterTailCorporationCreditAgreementMember2020-12-310001466593ottr:OTPCreditAgreementMember2021-12-310001466593ottr:OTPCreditAgreementMember2020-12-310001466593ottr:OtterTailCorporationCreditAgreementMemberus-gaap:RevolvingCreditFacilityMember2021-12-310001466593us-gaap:RevolvingCreditFacilityMemberottr:OTPCreditAgreementMember2021-12-310001466593ottr:OtterTailCorporationCreditAgreementMemberus-gaap:LetterOfCreditMember2021-12-310001466593us-gaap:LetterOfCreditMemberottr:OTPCreditAgreementMember2021-12-310001466593srt:MinimumMemberottr:BenchmarkRateMember2021-01-012021-12-310001466593ottr:BenchmarkRateMembersrt:MaximumMember2021-01-012021-12-310001466593ottr:The355GuaranteedSeniorNotesDueDecember152026Member2021-12-310001466593ottr:The355GuaranteedSeniorNotesDueDecember152026Member2020-12-310001466593ottr:SeniorUnsecuredNotes463SeriesADueDecember12021Member2021-12-310001466593ottr:SeniorUnsecuredNotes463SeriesADueDecember12021Member2020-12-310001466593ottr:SeniorUnsecuredNotes615SeriesBDueAugust202022Member2021-12-310001466593ottr:SeniorUnsecuredNotes615SeriesBDueAugust202022Member2020-12-310001466593ottr:SeniorUnsecuredNotes637SeriesCDueAugust202027Member2021-12-310001466593ottr:SeniorUnsecuredNotes637SeriesCDueAugust202027Member2020-12-310001466593ottr:SeniorUnsecuredNotes468SeriesADueFebruary272029Member2021-12-310001466593ottr:SeniorUnsecuredNotes468SeriesADueFebruary272029Member2020-12-310001466593ottr:SeniorUnsecuredNotes307SeriesADueOctober102029Member2021-12-310001466593ottr:SeniorUnsecuredNotes307SeriesADueOctober102029Member2020-12-310001466593ottr:SeniorUnsecuredNotes307SeriesADueFebruary252030Member2021-12-310001466593ottr:SeniorUnsecuredNotes307SeriesADueFebruary252030Member2020-12-310001466593ottr:SeniorUnsecuredNotes322SeriesBDueAugust202030Member2021-12-310001466593ottr:SeniorUnsecuredNotes322SeriesBDueAugust202030Member2020-12-310001466593ottr:SeniorUnsecuredNotes274SeriesADueNovember292031Member2021-12-310001466593ottr:SeniorUnsecuredNotes274SeriesADueNovember292031Member2020-12-310001466593ottr:SeniorUnsecuredNotes647SeriesDDueAugust202037Member2021-12-310001466593ottr:SeniorUnsecuredNotes647SeriesDDueAugust202037Member2020-12-310001466593ottr:SeniorUnsecuredNotes352SeriesBDueOctober102039Member2021-12-310001466593ottr:SeniorUnsecuredNotes352SeriesBDueOctober102039Member2020-12-310001466593ottr:SeniorUnsecuredNotes362SeriesCDueFebruary252040Member2021-12-310001466593ottr:SeniorUnsecuredNotes362SeriesCDueFebruary252040Member2020-12-310001466593ottr:SeniorUnsecuredNotes547SeriesBDueFebruary272044Member2021-12-310001466593ottr:SeniorUnsecuredNotes547SeriesBDueFebruary272044Member2020-12-310001466593ottr:SeniorUnsecuredNotes407SeriesADueFebruary72048Member2021-12-310001466593ottr:SeniorUnsecuredNotes407SeriesADueFebruary72048Member2020-12-310001466593ottr:SeniorUnsecuredNotes382SeriesCDueOctober102049Member2021-12-310001466593ottr:SeniorUnsecuredNotes382SeriesCDueOctober102049Member2020-12-310001466593ottr:SeniorUnsecuredNotes392SeriesDDueFebruary252050Member2021-12-310001466593ottr:SeniorUnsecuredNotes392SeriesDDueFebruary252050Member2020-12-310001466593ottr:SeniorUnsecuredNotes369SeriesBDueNovember292051Member2021-12-310001466593ottr:SeniorUnsecuredNotes369SeriesBDueNovember292051Member2020-12-310001466593ottr:PartnershipInAssistingCommunityExpansionPaceNote254DueMarch182021Member2021-12-310001466593ottr:PartnershipInAssistingCommunityExpansionPaceNote254DueMarch182021Member2020-12-310001466593us-gaap:SeniorNotesMember2021-06-100001466593us-gaap:SeniorNotesMemberottr:SeniorUnsecuredNotes274SeriesADueNovember292031Member2021-06-100001466593us-gaap:SeniorNotesMemberottr:SeniorUnsecuredNotes369SeriesBDueNovember292051Member2021-06-100001466593us-gaap:SeniorNotesMemberottr:SeniorUnsecuredNotes377SeriesADueMay202052Member2021-06-100001466593us-gaap:SeniorNotesMember2021-01-012021-12-310001466593us-gaap:PensionPlansDefinedBenefitMember2021-01-012021-12-31ottr:year0001466593us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2021-01-012021-12-310001466593ottr:DefinedBenefitPlanReturnEnhancementMembersrt:MinimumMemberus-gaap:PensionPlansDefinedBenefitMemberottr:PermittedRange20To60PercentMember2021-12-310001466593ottr:DefinedBenefitPlanReturnEnhancementMemberus-gaap:PensionPlansDefinedBenefitMemberottr:PermittedRange20To60PercentMembersrt:MaximumMember2021-12-310001466593ottr:DefinedBenefitPlanReturnEnhancementMemberus-gaap:PensionPlansDefinedBenefitMember2021-12-310001466593ottr:DefinedBenefitPlanReturnEnhancementMemberus-gaap:PensionPlansDefinedBenefitMember2020-12-310001466593srt:MinimumMemberus-gaap:PensionPlansDefinedBenefitMemberottr:DefinedBenefitPlanRiskManagementMemberottr:PermittedRange40To80PercentMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:DefinedBenefitPlanRiskManagementMembersrt:MaximumMemberottr:PermittedRange40To80PercentMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:DefinedBenefitPlanRiskManagementMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:DefinedBenefitPlanRiskManagementMember2020-12-310001466593srt:MinimumMemberus-gaap:PensionPlansDefinedBenefitMemberottr:DefinedBenefitPlanAlternativesMemberottr:PermittedRange0To20PercentMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:DefinedBenefitPlanAlternativesMemberottr:PermittedRange0To20PercentMembersrt:MaximumMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:DefinedBenefitPlanAlternativesMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:DefinedBenefitPlanAlternativesMember2020-12-310001466593us-gaap:PensionPlansDefinedBenefitMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMember2020-12-310001466593us-gaap:DefinedBenefitPlanEquitySecuritiesMemberus-gaap:FairValueInputsLevel1Member2021-12-310001466593us-gaap:DefinedBenefitPlanEquitySecuritiesMemberus-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:DefinedBenefitPlanEquitySecuritiesMemberus-gaap:FairValueInputsLevel3Member2021-12-310001466593us-gaap:DefinedBenefitPlanEquitySecuritiesMember2021-12-310001466593us-gaap:FairValueInputsLevel1Memberus-gaap:FixedIncomeFundsMember2021-12-310001466593us-gaap:FixedIncomeFundsMemberus-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:FairValueInputsLevel3Memberus-gaap:FixedIncomeFundsMember2021-12-310001466593us-gaap:FixedIncomeFundsMember2021-12-310001466593us-gaap:FairValueInputsLevel1Memberottr:DefinedBenefitPlanHybridFundsMember2021-12-310001466593ottr:DefinedBenefitPlanHybridFundsMemberus-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:FairValueInputsLevel3Memberottr:DefinedBenefitPlanHybridFundsMember2021-12-310001466593ottr:DefinedBenefitPlanHybridFundsMember2021-12-310001466593us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel1Member2021-12-310001466593us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:USTreasuryAndGovernmentMemberus-gaap:FairValueInputsLevel3Member2021-12-310001466593us-gaap:USTreasuryAndGovernmentMember2021-12-310001466593ottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMemberus-gaap:FairValueInputsLevel1Member2021-12-310001466593ottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMemberus-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:FairValueInputsLevel3Memberottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMember2021-12-310001466593us-gaap:FairValueMeasuredAtNetAssetValuePerShareMemberottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMember2021-12-310001466593ottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMember2021-12-310001466593us-gaap:FairValueInputsLevel1Member2021-12-310001466593us-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:FairValueInputsLevel3Member2021-12-310001466593us-gaap:FairValueMeasuredAtNetAssetValuePerShareMember2021-12-310001466593us-gaap:FairValueInputsLevel1Memberus-gaap:DefinedBenefitPlanCashAndCashEquivalentsMember2020-12-310001466593us-gaap:FairValueInputsLevel2Memberus-gaap:DefinedBenefitPlanCashAndCashEquivalentsMember2020-12-310001466593us-gaap:FairValueInputsLevel3Memberus-gaap:DefinedBenefitPlanCashAndCashEquivalentsMember2020-12-310001466593us-gaap:DefinedBenefitPlanCashAndCashEquivalentsMember2020-12-310001466593us-gaap:DefinedBenefitPlanEquitySecuritiesMemberus-gaap:FairValueInputsLevel1Member2020-12-310001466593us-gaap:DefinedBenefitPlanEquitySecuritiesMemberus-gaap:FairValueInputsLevel2Member2020-12-310001466593us-gaap:DefinedBenefitPlanEquitySecuritiesMemberus-gaap:FairValueInputsLevel3Member2020-12-310001466593us-gaap:DefinedBenefitPlanEquitySecuritiesMember2020-12-310001466593us-gaap:FairValueInputsLevel1Memberus-gaap:FixedIncomeFundsMember2020-12-310001466593us-gaap:FixedIncomeFundsMemberus-gaap:FairValueInputsLevel2Member2020-12-310001466593us-gaap:FairValueInputsLevel3Memberus-gaap:FixedIncomeFundsMember2020-12-310001466593us-gaap:FixedIncomeFundsMember2020-12-310001466593us-gaap:FairValueInputsLevel1Memberottr:DefinedBenefitPlanHybridFundsMember2020-12-310001466593ottr:DefinedBenefitPlanHybridFundsMemberus-gaap:FairValueInputsLevel2Member2020-12-310001466593us-gaap:FairValueInputsLevel3Memberottr:DefinedBenefitPlanHybridFundsMember2020-12-310001466593ottr:DefinedBenefitPlanHybridFundsMember2020-12-310001466593ottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMemberus-gaap:FairValueInputsLevel1Member2020-12-310001466593ottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMemberus-gaap:FairValueInputsLevel2Member2020-12-310001466593us-gaap:FairValueInputsLevel3Memberottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMember2020-12-310001466593us-gaap:FairValueMeasuredAtNetAssetValuePerShareMemberottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMember2020-12-310001466593ottr:DefinedBenefitPlanOtherSEIEnergyDebtCollectiveFundMember2020-12-310001466593us-gaap:FairValueInputsLevel1Member2020-12-310001466593us-gaap:FairValueInputsLevel2Member2020-12-310001466593us-gaap:FairValueInputsLevel3Member2020-12-310001466593us-gaap:FairValueMeasuredAtNetAssetValuePerShareMember2020-12-310001466593us-gaap:PensionPlansDefinedBenefitMember2019-12-310001466593ottr:ExecutiveSurvivorAndSupplementalRetirementPlanMember2020-12-310001466593ottr:ExecutiveSurvivorAndSupplementalRetirementPlanMember2019-12-310001466593us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2020-12-310001466593us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2019-12-310001466593us-gaap:PensionPlansDefinedBenefitMember2020-01-012020-12-310001466593ottr:ExecutiveSurvivorAndSupplementalRetirementPlanMember2021-01-012021-12-310001466593ottr:ExecutiveSurvivorAndSupplementalRetirementPlanMember2020-01-012020-12-310001466593us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2020-01-012020-12-310001466593ottr:ExecutiveSurvivorAndSupplementalRetirementPlanMember2021-12-310001466593us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsToAge39Member2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsToAge39Member2020-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge40To49Member2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge40To49Member2020-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge50AndOlderMember2021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge50AndOlderMember2020-12-310001466593us-gaap:PensionPlansDefinedBenefitMember2019-01-012019-12-310001466593ottr:ExecutiveSurvivorAndSupplementalRetirementPlanMember2019-01-012019-12-310001466593us-gaap:OtherPostretirementBenefitPlansDefinedBenefitMember2019-01-012019-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsToAge39Member2021-01-012021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsToAge39Member2020-01-012020-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsToAge39Member2019-01-012019-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge40To49Member2021-01-012021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge40To49Member2020-01-012020-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge40To49Member2019-01-012019-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge50AndOlderMember2021-01-012021-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge50AndOlderMember2020-01-012020-12-310001466593us-gaap:PensionPlansDefinedBenefitMemberottr:ParticipantsAge50AndOlderMember2019-01-012019-12-310001466593us-gaap:SubsequentEventMember2022-02-012022-02-280001466593us-gaap:DomesticCountryMember2021-12-310001466593us-gaap:DomesticCountryMemberottr:TaxYears2022To2032Member2021-12-310001466593us-gaap:DomesticCountryMemberottr:TaxYears2033To2038Member2021-12-310001466593us-gaap:DomesticCountryMemberottr:TaxYears2039To2043Member2021-12-310001466593us-gaap:StateAndLocalJurisdictionMember2021-12-310001466593us-gaap:StateAndLocalJurisdictionMemberottr:TaxYears2022To2032Member2021-12-310001466593ottr:TaxYears2033To2038Memberus-gaap:StateAndLocalJurisdictionMember2021-12-310001466593us-gaap:StateAndLocalJurisdictionMemberottr:TaxYears2039To2043Member2021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:ConstructionProgramsMember2021-01-012021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:ConstructionProgramsMember2020-01-012020-12-310001466593ottr:OtterTailPowerCompanyMemberottr:ConstructionProgramsMember2019-01-012019-12-310001466593ottr:OtterTailPowerCompanyMemberottr:OTPLandEasementsMember2021-01-012021-12-310001466593ottr:ConstructionProgramAndOtherCommitmentsMembersrt:SubsidiariesMember2021-12-310001466593ottr:CapacityAndEnergyRequirementsMemberottr:OtterTailPowerCompanyMember2021-12-310001466593ottr:CoalPurchaseCommitmentsMemberottr:OtterTailPowerCompanyMember2021-12-310001466593ottr:OtterTailPowerCompanyMember2021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:FederalEnergyRegulatoryCommissionMember2020-12-310001466593ottr:WestmorelandArbitrationMemberus-gaap:PendingLitigationMember2021-01-012021-12-310001466593us-gaap:CumulativePreferredStockMember2021-12-310001466593ottr:CumulativePreferenceSharesMember2021-12-310001466593us-gaap:CumulativePreferredStockMember2020-12-310001466593ottr:SecondShelfRegistrationMember2021-05-032021-05-030001466593ottr:SecondShelfRegistrationMember2021-01-012021-12-310001466593ottr:SecondShelfRegistrationMember2021-12-310001466593srt:MinimumMemberottr:OtterTailPowerCompanyMemberottr:MinnesotaPublicUtilitiesCommissionMember2020-07-152020-07-150001466593ottr:OtterTailPowerCompanyMemberottr:MinnesotaPublicUtilitiesCommissionMembersrt:MaximumMember2020-07-152020-07-150001466593ottr:OtterTailPowerCompanyMember2021-01-012021-12-310001466593ottr:OtterTailPowerCompanyMembersrt:MaximumMember2021-12-310001466593srt:MinimumMemberottr:OtterTailPowerCompanyMemberus-gaap:SubsequentEventMemberottr:MinnesotaPublicUtilitiesCommissionMember2022-01-262022-01-260001466593ottr:OtterTailPowerCompanyMemberus-gaap:SubsequentEventMemberottr:MinnesotaPublicUtilitiesCommissionMembersrt:MaximumMember2022-01-262022-01-260001466593ottr:OtterTailPowerCompanyMemberus-gaap:SubsequentEventMembersrt:MaximumMember2022-01-260001466593us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2018-12-310001466593us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2018-12-310001466593us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-01-012019-12-310001466593us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2019-01-012019-12-310001466593us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2019-12-310001466593us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2019-12-310001466593us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-01-012020-12-310001466593us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2020-01-012020-12-310001466593us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2020-12-310001466593us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2020-12-310001466593us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-01-012021-12-310001466593us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2021-01-012021-12-310001466593us-gaap:AccumulatedDefinedBenefitPlansAdjustmentMember2021-12-310001466593us-gaap:AccumulatedNetUnrealizedInvestmentGainLossMember2021-12-310001466593ottr:The1999EmployeeStockPurchasePlanMember2021-12-310001466593ottr:The1999EmployeeStockPurchasePlanMember2021-01-012021-12-310001466593srt:MinimumMemberottr:The1999EmployeeStockPurchasePlanMember2021-01-012021-12-310001466593ottr:The1999EmployeeStockPurchasePlanMembersrt:MaximumMember2021-01-012021-12-310001466593ottr:The1999EmployeeStockPurchasePlanMember2018-01-012019-06-300001466593ottr:The1999EmployeeStockPurchasePlanMember2019-07-012021-12-310001466593ottr:The1999EmployeeStockPurchasePlanMember2020-01-012020-12-310001466593ottr:The1999EmployeeStockPurchasePlanMember2019-01-012019-12-310001466593ottr:The2014StockIncentivePlanMember2021-12-310001466593ottr:The2014StockIncentivePlanMember2021-01-012021-12-310001466593ottr:The2014StockIncentivePlanMember2020-01-012020-12-310001466593ottr:The2014StockIncentivePlanMember2019-01-012019-12-310001466593us-gaap:RestrictedStockMembersrt:MinimumMember2021-01-012021-12-310001466593us-gaap:RestrictedStockMembersrt:MaximumMember2021-01-012021-12-310001466593us-gaap:RestrictedStockMember2021-01-012021-12-310001466593us-gaap:RestrictedStockMember2020-12-310001466593us-gaap:RestrictedStockMember2021-12-310001466593us-gaap:RestrictedStockMember2020-01-012020-12-310001466593us-gaap:RestrictedStockMember2019-01-012019-12-310001466593us-gaap:PerformanceSharesMember2021-01-012021-12-310001466593srt:MinimumMemberus-gaap:PerformanceSharesMember2021-01-012021-12-310001466593srt:MaximumMemberus-gaap:PerformanceSharesMember2021-01-012021-12-310001466593us-gaap:PerformanceSharesMember2021-12-312021-12-310001466593us-gaap:PerformanceSharesMember2020-12-312020-12-310001466593us-gaap:PerformanceSharesMember2019-12-312019-12-310001466593us-gaap:PerformanceSharesMember2020-12-310001466593us-gaap:PerformanceSharesMember2021-12-310001466593us-gaap:PerformanceSharesMember2020-01-012020-12-310001466593us-gaap:PerformanceSharesMember2019-01-012019-12-310001466593us-gaap:EmployeeStockOptionMember2021-01-012021-12-310001466593us-gaap:EmployeeStockOptionMember2020-01-012020-12-310001466593us-gaap:EmployeeStockOptionMember2019-01-012019-12-310001466593us-gaap:SwapMember2021-12-312021-12-31utr:MWh0001466593us-gaap:SwapMember2021-12-310001466593us-gaap:SwapMember2021-01-012021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberottr:GovernmentBackedAndGovernmentSponsoredEnterprisesDebtSecuritiesMember2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberottr:GovernmentBackedAndGovernmentSponsoredEnterprisesDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberottr:GovernmentBackedAndGovernmentSponsoredEnterprisesDebtSecuritiesMember2021-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Member2020-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel2Member2020-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Member2020-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel1Member2020-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2020-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:CorporateDebtSecuritiesMemberus-gaap:FairValueInputsLevel3Member2020-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel1Memberottr:GovernmentBackedAndGovernmentSponsoredEnterprisesDebtSecuritiesMember2020-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberottr:GovernmentBackedAndGovernmentSponsoredEnterprisesDebtSecuritiesMemberus-gaap:FairValueInputsLevel2Member2020-12-310001466593us-gaap:FairValueMeasurementsRecurringMemberus-gaap:FairValueInputsLevel3Memberottr:GovernmentBackedAndGovernmentSponsoredEnterprisesDebtSecuritiesMember2020-12-310001466593us-gaap:CarryingReportedAmountFairValueDisclosureMember2021-12-310001466593us-gaap:EstimateOfFairValueFairValueDisclosureMember2021-12-310001466593us-gaap:CarryingReportedAmountFairValueDisclosureMember2020-12-310001466593us-gaap:EstimateOfFairValueFairValueDisclosureMember2020-12-310001466593srt:ParentCompanyMember2021-01-012021-12-310001466593srt:ParentCompanyMember2020-01-012020-12-310001466593srt:ParentCompanyMember2019-01-012019-12-310001466593srt:ParentCompanyMember2019-12-310001466593srt:ParentCompanyMember2018-12-310001466593ottr:OtterTailPowerCompanyMemberottr:OtterTailCorporationMember2021-12-310001466593ottr:NorthernPipeProductsIncMemberottr:OtterTailCorporationMember2021-12-310001466593ottr:VinyltechCorporationMemberottr:OtterTailCorporationMember2021-12-310001466593ottr:BTDManufacturingIncMemberottr:OtterTailCorporationMember2021-12-310001466593ottr:TOPlasticsIncMemberottr:OtterTailCorporationMember2021-12-310001466593ottr:VaristarCorporationMemberottr:OtterTailCorporationMember2021-12-310001466593ottr:OtterTailAssuranceLimitedMemberottr:OtterTailCorporationMember2021-12-310001466593ottr:OtterTailCorporationMember2021-12-310001466593ottr:OtterTailPowerCompanyMemberottr:OtterTailCorporationMember2020-12-310001466593ottr:NorthernPipeProductsIncMemberottr:OtterTailCorporationMember2020-12-310001466593ottr:VinyltechCorporationMemberottr:OtterTailCorporationMember2020-12-310001466593ottr:BTDManufacturingIncMemberottr:OtterTailCorporationMember2020-12-310001466593ottr:TOPlasticsIncMemberottr:OtterTailCorporationMember2020-12-310001466593ottr:VaristarCorporationMemberottr:OtterTailCorporationMember2020-12-310001466593ottr:OtterTailAssuranceLimitedMemberottr:OtterTailCorporationMember2020-12-310001466593ottr:OtterTailCorporationMember2020-12-310001466593us-gaap:AllowanceForCreditLossMember2020-12-310001466593us-gaap:AllowanceForCreditLossMember2021-01-012021-12-310001466593us-gaap:AllowanceForCreditLossMember2021-12-310001466593us-gaap:AllowanceForCreditLossMember2019-12-310001466593us-gaap:AllowanceForCreditLossMember2020-01-012020-12-310001466593us-gaap:AllowanceForCreditLossMember2018-12-310001466593us-gaap:AllowanceForCreditLossMember2019-01-012019-12-310001466593us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-12-310001466593us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-01-012021-12-310001466593us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2021-12-310001466593us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2019-12-310001466593us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2020-01-012020-12-310001466593us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2018-12-310001466593us-gaap:ValuationAllowanceOfDeferredTaxAssetsMember2019-01-012019-12-31

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

☒ Annual Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended December 31, 2021 or

☐ Transition Report pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Commission File Number 0-53713

OTTER TAIL CORPORATION

(Exact name of registrant as specified in its charter)

| | | | | |

Minnesota (State or other jurisdiction of incorporation or organization) | 27-0383995 (I.R.S. Employer Identification No.) |

| |

215 South Cascade Street, Box 496, Fergus Falls, Minnesota (Address of principal executive offices) | 56538-0496 (Zip Code) |

Registrant's telephone number, including area code: 866-410-8780

Securities registered pursuant to Section 12(b) of the Act:

| | | | | | | | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| Common Shares, par value $5.00 per share | OTTR | The Nasdaq Stock Market LLC |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☑ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☑

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | | | | | | | | | | | | |

| | Large Accelerated Filer ☑ | | Accelerated Filer ☐ | | |

| | Non-Accelerated Filer ☐ | | Smaller Reporting Company ☐ | | Emerging Growth Company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued

its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☑

As of June 30, 2021, the aggregate market value of common stock held by non-affiliates was 1,948,379,911.

Indicate the number of shares outstanding of each of the registrant's classes of common stock, as of the latest practicable date: 41,605,742 Common Shares ($5 par value) as of February 7, 2022.

DOCUMENTS INCORPORATED BY REFERENCE

The Registrant's definitive Proxy Statement for its 2022 Annual Meeting of Shareholders is incorporated by reference into Part III of this Form 10-K.

| | | | | | | | |

| | Description | Page |

| | |

| | | |

| | |

| | |

| | |

| ITEM 1. | | |

| ITEM 1A. | | |

| ITEM 1B. | | |

| ITEM 2. | | |

| ITEM 3. | | |

| ITEM 3A. | | |

| ITEM 4. | | |

| | |

| ITEM 5. | | |

| | |

| ITEM 7. | | |

| ITEM 7A. | | |

| ITEM 8. | | |

| | | |

| | |

| | |

| | | |

| | | |

| | | |

| | | |

| | |

| ITEM 9. | | |

| ITEM 9A. | | |

| ITEM 9B. | | |

| ITEM 9C. | | |

| | |

| ITEM 10. | | |

| ITEM 11. | | |

| ITEM 12. | | |

| ITEM 13. | | |

| ITEM 14. | | |

| | |

| ITEM 15. | | |

| ITEM 16. | | |

| | |

The following abbreviations or acronyms are used in the text. | | | | | | | | | | | | | | |

| ACE | Affordable Clean Energy | | kwh | kilowatt-hour |

| AFUDC | Allowance for Funds Used During Construction | | LIBOR | London Interbank Offered Rate |

| ARO | Asset Retirement Obligation | | LSA | Lignite Sales Agreement |

| ARP | Alternative Revenue Program | | Merricourt | Merricourt Wind Energy Center |

| Astoria | Astoria Station | | MISO | Midcontinent Independent System Operator, Inc. |

| BTD | BTD Manufacturing, Inc. | | MPUC | Minnesota Public Utilities Commission |

| CCMC | Coyote Creek Mining Company, L.L.C. | | NAV | Net Asset Value |

| CDD | Cooling Degree Day | | NDDEQ | North Dakota Department of Environmental Quality |

| CIP | Conservation Improvement Program | | NDPSC | North Dakota Public Service Commission |

CO2 | carbon dioxide | | NERC | North American Electric Reliability Corporation |

| COSO | Committee of Sponsoring Organizations of the Treadway Commission | | Northern Pipe | Northern Pipe Products, Inc. |

| ECR | Environmental Cost Recovery Rider | | OSHA | Occupational Safety and Health Administration |

| EEI | Edison Electric Institute | | OTC | Otter Tail Corporation |

| EEP | Energy Efficiency Plan | | OTP | Otter Tail Power Company |

| EPA | Environmental Protection Agency | | PACE | Partnership in Assisting Community Expansion |

| ERISA | Employee Retirement Income Security Act of 1974 | | PIR | Phase-in Rider |

| ESSRP | Executive Survivor and Supplemental Retirement Plan | | PTCs | Production tax credits |

| ETS | Emergency Temporary Standard | | PVC | Polyvinyl chloride |

| EUIC | Electric Utility Infrastructure Cost Recovery Rider | | RHR | Regional Haze Rule |

| FCA | Fuel Clause Adjustment | | ROE | Return on equity |

| FERC | Federal Energy Regulatory Commission | | RRR | Renewable Resource Rider |

| GCR | Generation Cost Recovery Rider | | SDPUC | South Dakota Public Utilities Commission |

| GHG | Greenhouse Gas | | SEC | Securities and Exchange Commission |

| HDD | Heating Degree Day | | SRECs | Solar renewable energy credits |

| ISO | Independent System Operator | | T.O. Plastics | T.O. Plastics, Inc. |

| IRP | Integrated Resource Plan | | TCR | Transmission Cost Recovery Rider |

| kV | kiloVolt | | Varistar | Varistar Corporation |

| kW | kiloWatt | | Vinyltech | Vinyltech Corporation |

| | | | |

| | | | | | | | |

| WHERE TO FIND MORE INFORMATION | | |

We make available free of charge at our website (www.ottertail.com) our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy and information statements, Forms 3, 4 and 5 filed on behalf of directors and executive officers and any amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as soon as reasonably practicable after such material is electronically filed with or furnished to the Securities and Exchange Commission (SEC). These reports are also available on the SEC's website (www.sec.gov). Information on our and the SEC's websites is not deemed to be incorporated by reference into this report on Form 10-K. | | |

| FORWARD-LOOKING INFORMATION |

This report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995 (the Act). When used in this Form 10-K and in future filings by the Company with the SEC, in the Company’s press releases and in oral statements, words such as “anticipate,” “believe,” “could,” “estimate,” “expect,” "goal," “intend,” “may,” “outlook,” “plan,” “possible,” “potential,” "probable," "projected," “should,” "target," “will,” “would” or similar expressions are intended to identify forward-looking statements within the meaning of the Act. Such statements are based on current expectations and assumptions and entail various risks and uncertainties that could cause actual results to differ materially from those expressed in such forward-looking statements. Such risks and uncertainties include the various factors set forth in Item 1A. Risk Factors of this report on Form 10-K and in our other SEC filings.

PART I

Otter Tail Corporation (OTC) has interests in diversified operations that include an electric utility and manufacturing and plastic pipe businesses with corporate offices located in Fergus Falls, Minnesota and Fargo, North Dakota.

We classify our five operating companies into three reportable segments consistent with our business strategy and management structure. The following table depicts our three segments and the subsidiary entities included within each segment:

| | | | | | | | | | | | | | |

| ELECTRIC SEGMENT | | MANUFACTURING SEGMENT | | PLASTICS SEGMENT |

| Otter Tail Power Company (OTP) | | BTD Manufacturing, Inc. (BTD) | | Northern Pipe Products, Inc. (Northern Pipe) |

| | T.O. Plastics, Inc. (T.O. Plastics) | | Vinyltech Corporation (Vinyltech) |

Electric includes the generation, purchase, transmission, distribution and sale of electric energy in western Minnesota, eastern North Dakota and northeastern South Dakota. OTP, our largest operating subsidiary and primary business since 1907, serves more than 133,000 customers in more than 400 communities across a predominantly rural and agricultural service territory.

Manufacturing consists of businesses in the following manufacturing activities: contract machining; metal parts stamping, fabrication and painting; and production of plastic thermoformed horticultural containers, life science and industrial packaging, material handling components and extruded raw material stock. These businesses have manufacturing facilities in Georgia, Illinois and Minnesota and sell products primarily in the United States.

Plastics consists of businesses producing polyvinyl chloride (PVC) pipe at plants in North Dakota and Arizona. The PVC pipe is sold primarily in the western half of the United States and Canada.

Throughout the remainder of this report, we use the terms "Company", "us", "our", or "we" to refer to OTC and its subsidiaries collectively. We will also refer to our Electric, Manufacturing and Plastics segments and our individual subsidiaries as indicated above.

INVESTMENT AND GROWTH STRATEGY

We maintain a moderate risk profile by investing in rate base growth opportunities in our Electric segment and organic growth opportunities in our Manufacturing and Plastics segments. This strategy and risk profile are designed to provide a more predictable earnings stream, maintain our credit quality and preserve our ability to fund our dividend payments. Our goal is to deliver annual growth in earnings per share between five and seven percent over the next several years, using 2020 diluted earnings per share as the base for measurement. We expect our earnings growth to come from rate base investments in our Electric segment and from existing capacities and planned investments within our Manufacturing and Plastics segments.

We will continue to review our business portfolio to identify additional opportunities to improve our risk profile, enhance our credit metrics and generate additional sources of cash to support the organic growth opportunities in our electric utility and manufacturing and plastics segments. We will also evaluate opportunities to allocate capital to potential acquisitions within our Manufacturing and Plastics segments. We are a committed long-term owner and do not acquire companies in pursuit of short-term gains. However, we will divest businesses which no longer fit into our strategy and risk profile over the long term.

We maintain a set of criteria used in evaluating the strategic fit of our operating businesses. The operating company should:

•Maintain a minimum level of net earnings and a return on invested capital in excess of the Company’s weighted average cost of capital,

•Have a strategic differentiation from competitors and a sustainable cost advantage,

•Operate within a stable and growing industry and be able to quickly adapt to changing economic cycles, and

•Have a strong management team committed to operational and commercial excellence.

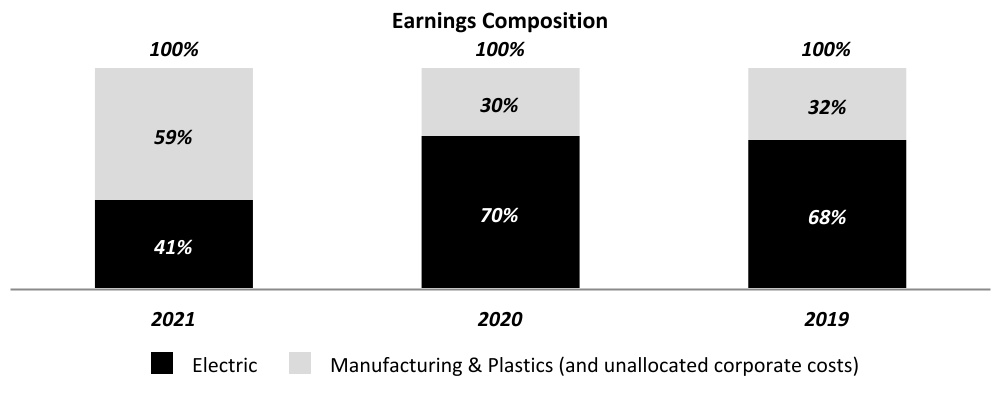

Over time, we expect our Electric segment will provide approximately 70% of our overall earnings and our Manufacturing and Plastics segments will collectively provide approximately 30% of our overall earnings and continue to be a fundamental part of our strategy.

Our actual mix of earnings for the years ended December 31, 2021, 2020, 2019 was as follows:

Our 2021 earnings mix was impacted by significantly higher earnings in our Plastics segment as unique supply and demand conditions during the year in the PVC pipe industry led to earnings levels not previously experienced. We expect our earnings mix to return back to our targeted mix of 70% from the Electric segment and 30% from the Manufacturing and Plastics segments over the long term as these industry conditions subside.

HUMAN CAPITAL

Our employees are a critical resource and an integral part of our success. We strive to provide an environment of opportunity and accountability where people are valued and empowered to do their best work. We are focused on the health and safety of our employees and creating a culture of inclusion, excellence and learning. Our human capital management efforts include monitoring various metrics and objectives associated with i) employee safety, ii) workforce stability, iii) management and workforce demographics, including gender, racial and ethnic diversity, iv) leadership development and succession planning and v) productivity. We have established the following programs in furtherance of these efforts:

Safety - Safety is one of our core values. In managing our business, we focus on the safety of our employees and have implemented safety programs and management practices to promote a culture of safety. Safety is also a metric used and evaluated in determining annual incentive compensation. We continually monitor the Occupational Safety and Health Administration (OSHA) Total Recordable Incident Rate (number of work-related injuries per 100 employees for a one-year period) and Lost Time Incident Rate (number of employees who lost time due to work-related injuries per 100 employees for a one-year period). New cases are reported and evaluated for corrective action during monthly safety meetings attended by safety professionals at all locations. Our 2021 Total Recordable Incident Rate was 1.86, compared to 1.42 in 2020 and our Lost Time Incident Rate was 0.57, compared to 0.55 in 2020. In both 2021 and 2020 these rates were favorable to the rates of our peers.

Leadership Development and Training Programs - We extend leadership development throughout the organization to build enterprise-wide understanding of our culture, strategy and processes. Annual succession planning, individual development planning, mentoring, and supervisory and leadership development programs all play a role in ensuring a capable leadership team now and in the future. Our skill progression and technical training programs help to retain a stable and skilled workforce.

Workforce Stability - Retaining and developing our employees is an important factor in our continued success and growth. We regularly evaluate our employee retention and turnover rates.

Employee Engagement - To enhance productivity and employee engagement, and to help our companies continue to be places where our employees choose to work and thrive, we have undertaken a multi-year series of employee engagement surveys. We use the feedback to help shape the future of our organization.

Code of Business Ethics - We communicate annually to all employees on our code of business ethics to reinforce our commitment to compliance with laws, regulations and values that guide who we are and how we do business.

Across our operating companies and including our corporate team as of December 31, 2021, we employed 2,487 full-time employees:

| | | | | |

| Segment/Organization | Employees |

| |

| Electric Segment | |

OTP (1) | 721 | |

| Manufacturing Segment | |

| BTD | 1,364 | |

| T.O. Plastics | 182 | |

| Segment Total | 1,546 | |

| Plastics Segment | |

| Northern Pipe | 104 | |

| Vinyltech | 78 | |

| Segment Total | 182 | |

| Corporate | 38 | |

| Total | 2,487 | |

(1) Includes all full-time employees of Otter Tail Power Company, including employees working at jointly-owned facilities. Labor costs associated with employees working at jointly-owned facilities are allocated to each of the co-owners based on their ownership interest. | |

At December 31, 2021, 358 employees of OTP are represented by local unions of the International Brotherhood of Electrical Workers under two separate collective bargaining agreements expiring on August 31, 2023 and October 31, 2023. OTP has not experienced any strike, work stoppage or strike vote, and considers its present relations with employees to be good. None of the employees of our other operating companies are represented by local unions.

The demographics of our workforce, including our Board of Directors, as of December 31, 2021 was as follows: | | | | | | | | | | | |

| % Female | | % Racially and Ethnically Diverse |

| | | |

Board of Directors(1) | 20 | % | | 10 | % |

| CEO Direct Reports | 33 | % | | — | % |

| Management | 22 | % | | 4 | % |

| Non-Management Employees | 17 | % | | 19 | % |

| | | |

(1) Includes the new director appointed to our Board effective January 1, 2022. | | | |

| | | | | |

| ELECTRIC | Contribution to Operating Revenues: 40% (2021), 50% (2020), 50% (2019) |

OTP, headquartered in Fergus Falls, Minnesota, is a vertically integrated, regulated utility with generation, transmission and distribution facilities to serve its more than 133,000 residential, industrial and commercial customers in a service area encompassing approximately 70,000 square miles of western Minnesota, eastern North Dakota and northeastern South Dakota.

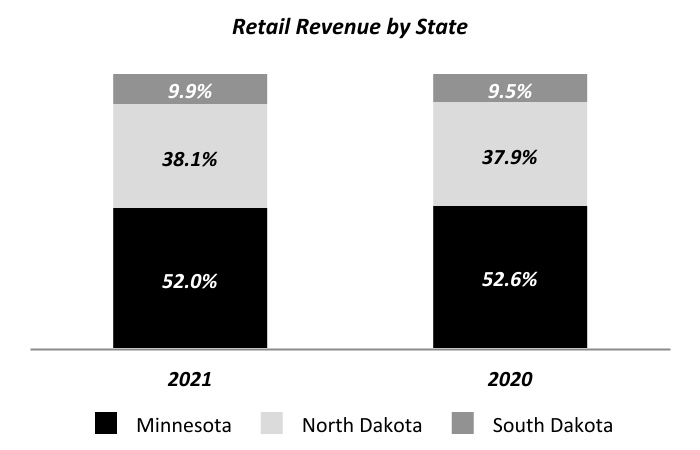

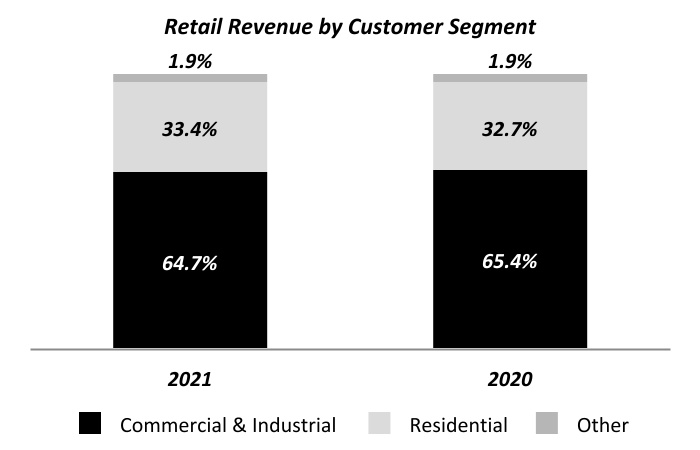

CUSTOMERS

Our service territory is predominantly rural and agricultural and includes over 400 communities, most of which have populations of less than 10,000. While our customer base includes relatively few large customers, sales to commercial and industrial customers are significant, with one industrial customer accounting for 10% of segment operating revenues for the year ended December 31, 2021.

The following charts summarize our retail electric revenues by state and by customer segment for the years ended December 31, 2021 and 2020:

In addition to retail revenue, our Electric segment also generates operating revenues from the transmission of electricity for others over the transmission assets we wholly or jointly own with other transmission service providers, and from the sale of electricity we generate and sell into the wholesale electricity market.

COMPETITIVE CONDITIONS

Retail electric sales are made to customers in assigned service territories. As a result, most retail customers do not have the ability to choose their electric supplier. Competition is present in some areas from municipally owned systems, rural electric cooperatives and, in certain respects, from on-site generators and co-generators. Electricity also competes with other forms of energy.

Competition also arises from customers supplying their own power through distributed generation, which is the generation of electricity on-site or close to where it is needed in small facilities designed to meet local needs. Distributed energy resources can include combined heat and power, solar photovoltaic, wind, battery storage, thermal storage and demand-response technologies.

The degree of competition may vary from time to time depending on relative costs and supplies of other forms of energy and advances in technology. Irrespective of the competitive environment, we are focused on providing value to our customers and ensuring our retail rates remain among the lowest in the region and in the nation.

The following table presents our average retail rate per kilowatt-hour (kwh) by customer class and in total for the years ended December 31, 2021 and 2020:

| | | | | | | | | | | |

| Revenue per kwh | 2021 | | 2020 |

| | | |

| Residential | 10.90 | ¢ | | 10.05 | ¢ |

| Commercial & Industrial | 7.52 | ¢ | | 7.40 | ¢ |

| Total Retail | 8.47 | ¢ | | 8.15 | ¢ |

Wholesale electricity markets are competitive under the Federal Energy Regulatory Commission (FERC) open access transmission tariffs, which require utilities to provide nondiscriminatory access to all wholesale users. In addition, the FERC has established a competitive process for the construction and operation of certain new electric transmission facilities whereby electric transmission providers, including the Midcontinent Independent System Operator, Inc. (MISO), of which OTP is a member, are required to remove from their tariffs a federal right of first refusal to construct transmission facilities selected in a regional transmission plan for purposes of cost allocation. The FERC is contemplating potential reforms for electric regional transmission planning, cost allocation and generator interconnection processes. While the ultimate regulatory outcome is uncertain at this time, changes to the regulatory framework could impact future transmission investments.

Franchises

OTP has franchises to operate as an electric utility in substantially all of the incorporated municipalities it serves. Franchise rights generally require periodic renewal. No franchises are required to serve unincorporated communities in any of the three states OTP serves.

GENERATION AND PURCHASED POWER

OTP primarily relies on company-owned generation, supplemented by purchase power agreements, to supply the energy to meet our customer needs. Wholesale market purchases and sales of electricity are used as necessary to balance supply and demand. Our mix of owned generation and wholesale market energy purchases to meet customer demand are impacted by wholesale energy prices and the relative cost of each energy source.

As of December 31, 2021, OTP’s wholly or jointly owned plants and facilities, as well as in place purchased power agreements, and their dependable kilowatt (kW) capacity were: | | | | | | | | |

| | Capacity /

Purchased Power

in kW |

| | |

| Owned Generation: | | |

| Baseload Plants | | |

Big Stone Plant(1) | | 257,700 | |

Coyote Station(2) | | 149,100 | |

| Total Baseload Plants | | 406,800 | |

| Combustion Turbine and Small Diesel Units | | |

| Astoria Station | | 249,700 | |

| All Other | | 102,800 | |

| Total Combustion Turbine and Small Diesel Units | | 352,500 | |

| Owned Wind Facilities (rated at nameplate) | | |

| Merricourt Wind Energy Center | | 150,000 | |

| Luverne Wind Farm | | 49,500 | |

| Ashtabula Wind Center | | 48,000 | |

| Langdon Wind Center | | 40,500 | |

| Total Owned Wind Facilities | | 288,000 | |

| Hydroelectric Facilities | | 2,600 | |

| Total Owned Generation Capacity | | 1,049,900 | |

| Purchased Power Agreements: | |

| Purchased Wind Power (rated at nameplate and greater than 2,000 kW) | |

| Ashtabula Wind III | | 62,400 | |

| Edgeley | | 21,000 | |

| Langdon | | 19,500 | |

| Total Purchased Wind | | 102,900 | |

| Total Generating Capacity | | 1,152,800 | |

(1) Reflects OTP's 53.9% ownership percentage of jointly-owned facility | | |

(2) Reflects OTP's 35.0% ownership percentage of jointly-owned facility | | |

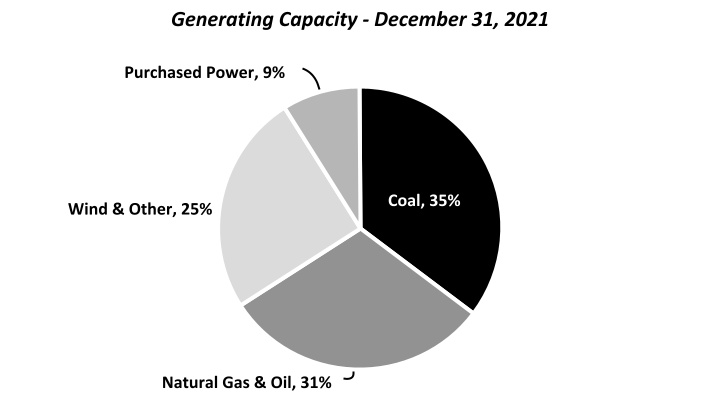

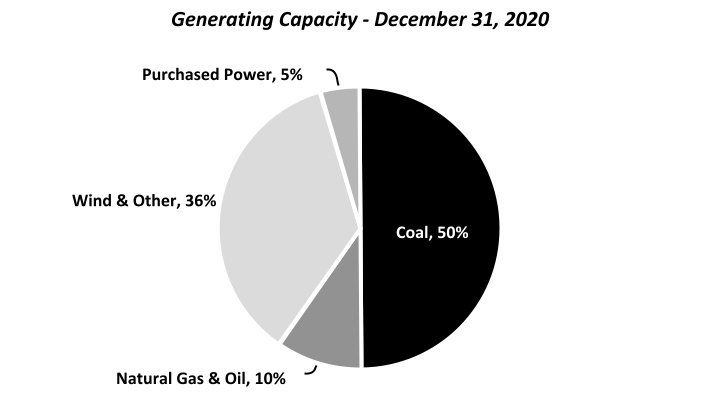

The following charts summarize the percentage of our generating capacity by source, including owned and jointly-owned facilities and through power purchase arrangements, as of December 31, 2021 and 2020:

Under MISO requirements, OTP is required to have sufficient capacity through wholly or jointly-owned generating capacity or purchased power agreements to meet its monthly weather-normalized forecast demand, plus a reserve obligation. OTP met its obligation for the 2020-2021 planning year and anticipates meeting this obligation prospectively.

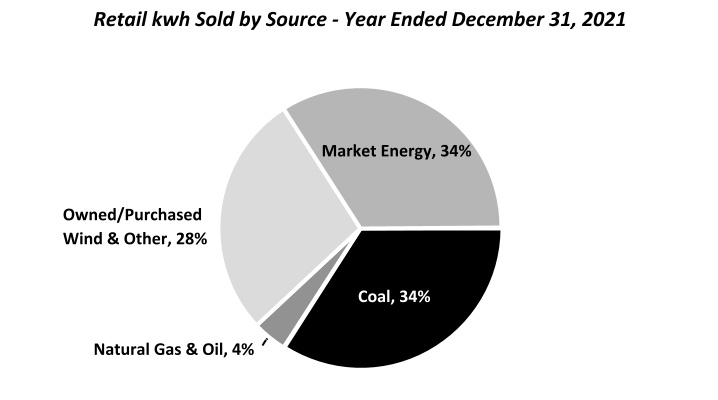

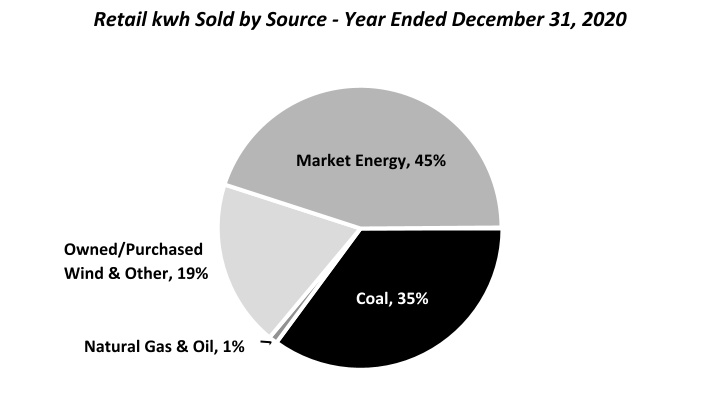

The following charts summarize the percentage of retail kilowatt-hours (kwh) sold by source during the years ended December 31, 2021 and 2020:

Capacity Retirements and Additions

Hoot Lake Plant, our 142-megawatt coal-fired power plant in Fergus Falls, Minnesota was retired in mid-2021.

As part of our investment plan to meet our future energy needs, we have the following significant projects at various stages of planning and construction or that have been recently completed:

Merricourt Wind Energy Center (Merricourt) is a 150-megawatt wind farm located in southeastern North Dakota. Construction of the wind farm commenced in 2019 and the facility was placed into commercial operation in December 2020, with a total cost of approximately $260 million.

Astoria Station Natural Gas Plant (Astoria) is a 245-megawatt simple cycle natural gas combustion turbine generation facility near Astoria, South Dakota. Construction commenced in 2019 and the facility was placed into commercial operation in February 2021, with a total cost of approximately $160 million.

Hoot Lake Solar is a 49-megawatt solar farm under development on land on and around our Hoot Lake Plant in Fergus Falls, Minnesota, with an anticipated cost of approximately $60 million. We anticipate the facility will be in commercial operation by the end of 2023.

ENERGY TRANSITION

Otter Tail Power is committed to transitioning to a lower-carbon and increasingly clean energy future, while maintaining low cost and reliable electricity to serve our customers. We have developed the following goals in the furtherance of our efforts to support the energy transition:

Provide 30% of energy generated from renewable resources to our customers by 2023.

Reduce carbon emissions from owned generation resources by 50% by 2025 from 2005 levels.

Reduce carbon emissions from owned generation resources by 97% by 2050 from 2005 levels.

To date, we have undertaken numerous initiatives to reduce our carbon footprint and mitigate greenhouse gas emissions in the process of generating electricity for our customers. Our initiatives include increasing the efficiency of our plants, adding renewable energy to our resource mix and sponsoring energy conservation programs.

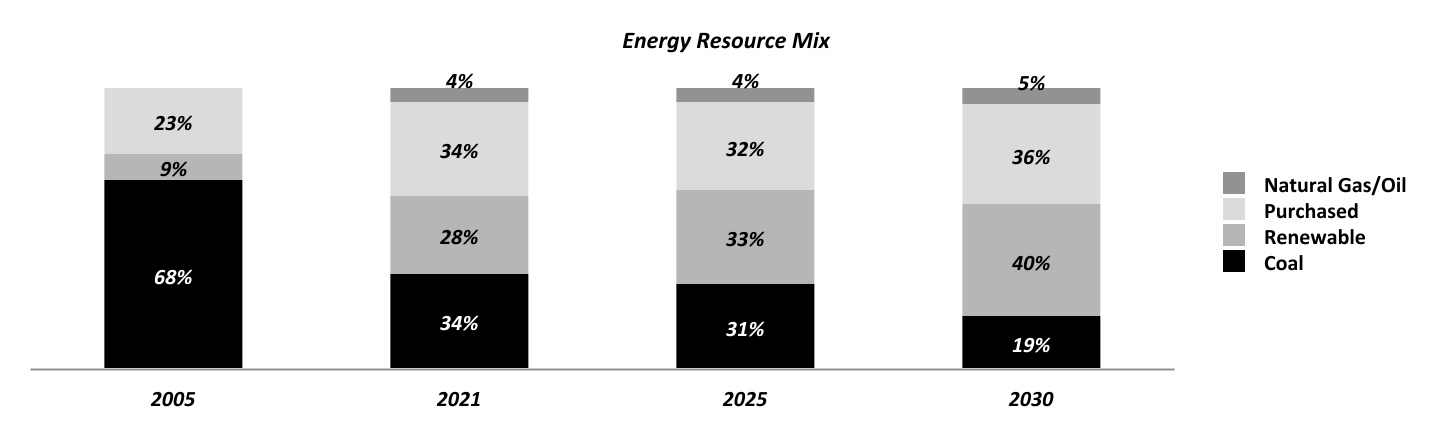

From 2005 through 2021, we have reduced our carbon dioxide emissions approximately 39% and increased the amount of renewable generation resources we own or contract through purchase power agreements by approximately 370 megawatts. Our future resource plans to deliver low-cost, reliable and increasingly clean energy to our customers include the addition of 49 megawatts of solar energy from Hoot Lake Solar in 2023 along with the resource additions as outlined in our Integrated Resource Plan, including the addition of 150 megawatts of solar generation and 100 megawatts of wind generation by 2027. Our resource plan also proposes to withdraw from Coyote Station, our jointly owned coal-fired generation facility by the end of 2028.

The following chart depicts our energy resource mix in 2005 and 2021 and the projected mix in 2025 and 2030 if our preferred plan within our Integrated Resource Plan is approved in each of the jurisdictions in which we operate. The amounts include energy generated from owned resources, procured through purchase power agreements and energy purchased in the wholesale market:

RESOURCE MATERIALS

Coal is the principal fuel burned at our jointly-owned Big Stone and Coyote Station generating plants. Coyote Station, a mine-mouth facility, burns North Dakota lignite coal. Big Stone Plant burns western subbituminous coal transported by rail. We source coal for our coal-fired power plants through requirements contracts which do not include minimum purchase requirements but do require all coal necessary for the operation of the respective plant to be purchased from the counterparty. Our coal supply contracts for our Big Stone Plant and Coyote Station have expiration dates in 2022 and 2040, respectively.

The supply agreement between the Coyote Station owners, including OTP, and the coal supplier includes provisions requiring the Coyote Station owners to purchase the membership interests and pay off or assume loan and lease obligations of the coal supplier, as well as complete mine closing and post-mining reclamation, in the event of certain early termination events and at the expiration of the coal supply agreement in 2040. See Note 1 to our consolidated financial statements included in this report on Form 10-K for additional information.

Coal is transported to our non-mine-mouth facility, Big Stone Plant, by rail and is provided under a common carrier rate which includes a mileage-based fuel surcharge.

We purchase natural gas for use at our combustion turbine facilities based on anticipated short-term resource needs. We procure natural gas from multiple vendors at spot prices in a liquid market primarily under firm delivery contracts.

TRANSMISSION AND DISTRIBUTION

Our transmission and distribution assets deliver energy from energy generation sources to our customers. In addition, we earn revenue from the transmission of electricity over our wholly or jointly owned transmission assets for others under approved rate tariffs. As of December 31, 2021, we were the sole or joint owner of over 9,000 miles of transmission and distribution lines.

Midcontinent Independent System Operator, Inc. (MISO)

MISO is an independent, non-profit organization that operates the transmission facilities owned by other entities, including OTP, within its regional jurisdiction and administers energy and generation capacity markets. MISO has operational control of our transmission facilities above 100 kiloVolts (kV). MISO seeks to optimize the efficiency of the interconnected system, provide solutions to regional planning needs and minimize risk to reliability through its security coordination, long-term regional planning, market monitoring, scheduling and tariff administration functions.

SEASONALITY

Electricity demand is affected by seasonal weather differences, with peak demand occurring in the summer and winter months. As a result, our Electric segment operating results regularly fluctuate on a seasonal basis. In addition, fluctuations in electricity demand within the same season but between years can impact our operating results. We monitor the level of heating and cooling degree days in a period to assess the impact of weather-related effects on our operating results between periods.

PUBLIC UTILITY REGULATION

OTP is subject to regulation of rates and other matters in each of the three states in which it operates and by the federal government for, among other matters, the interstate transmission of electricity. OTP operates under approved retail electric tariff rates in all three states it serves. Tariff rates are designed to recover plant investments, a return on those investments and operating costs. In addition to determining rate tariffs, state regulatory commissions also authorize return on equity (ROE), capital structure and depreciation rates of our plant investments. Decisions by our regulators significantly impact our operating results, financial position and cash flows.

Below is a summary of the regulatory agencies with jurisdiction of electric rates over OTP covered by each regulatory agency:

| | | | | | | | | | |

| Regulatory | | | | |

| Agency | | | | Areas of Regulation |

| | | | |

Minnesota Public Utilities Commission

(MPUC)

| | | | Retail rates, issuance of securities, depreciation rates, capital structure, public utility services, construction of major facilities, establishment of exclusive assigned service areas, contracts with subsidiaries and other affiliated interests and other matters. Selection or designation of sites for new generating plants (50,000 kW or more) and routes for transmission lines (100 kV or more). Review and approval of fifteen-year Integrated Resource Plan. |

North Dakota Public Service Commission

(NDPSC) | | | | Retail rates, certain issuances of securities, construction of major utility facilities and other matters. Approval of site and routes for new electric generating facilities (500 kW or more for wind generating facilities; 50,000 kW for non-wind generating facilities) and high voltage transmission lines (115 kV or more). Review and approval of ten-year facility plan and Integrated Resource Plan. |

South Dakota Public Utilities Commission

(SDPUC) | | | | Retail rates, public utility services, construction of major facilities, establishment of assigned service areas and other matters. Approval of sites and routes for new electric generating facilities (100,000 kW or more) and most transmission lines (115 kV or more). |

Federal Energy Regulatory Commission

(FERC) | | | | Wholesale electricity sales, transmission and sale of electric energy in interstate commerce, interconnection of facilities, hydroelectric licensing and accounting policies and practices. Compliance with North American Electric Reliability Corporation (NERC) reliability standards, including standards on cybersecurity and protection of critical infrastructure. |

In addition to base rates, which are established through periodic rate case proceedings within each state jurisdiction, there are other mechanisms for recovery of plant investments, including a return on investment and operating expenses, between rate cases. The following table summarizes these recovery mechanisms:

| | | | | | | | | | | | | | |

| Recovery Mechanism | | Jurisdiction(s) | | Additional Information |

| | | | |

| Fuel Clause Adjustment (FCA) | | MN, ND, SD | | Provides for periodic billing adjustments for changes in prudently incurred costs of fuel and purchased power. In North and South Dakota, fuel and purchased power costs are generally adjusted on a monthly basis with over or under collections from the previous month applied to the next monthly billing. In Minnesota, fuel and purchased power costs are estimated on an annual basis and the accumulated difference between actual and estimated cost per kwh are refunded or recovered, subject to regulatory approval, in subsequent periods. |

| Transmission Cost Recovery Rider (TCR) | | MN, ND, SD | | Provides for recovery of costs outside of a general rate case for investments in new or modified electric transmission or distribution assets. |

| Environmental Cost Recovery Rider (ECR) | | MN, ND, SD | | Provides for recovery of costs outside of a general rate case for investments in certain environmental improvement projects. |

| Renewable Resource Rider (RRR) | | MN, ND | | Provides for recovery of costs outside of a general rate case for investments in certain new renewable energy projects. |

| Conservation Improvement Program (CIP) | | MN | | Under Minnesota law, OTP is required to invest at least 1.5% of its gross operating revenues on energy conservation improvements. Recovery of these costs outside of a general rate case occurs through the CIP rider. |

| Electric Utility Infrastructure Costs Rider (EUIC) | | MN | | Provides for recovery of costs for investments made to replace or modify existing infrastructure if the replacement or modification conserves energy or uses energy more efficiently. |

| Generation Cost Recovery Rider (GCR) | | ND | | Provides for the recovery of costs outside of a general rate case for investments in new generation facilities. |

| Energy Efficiency Plan (EEP) | | SD | | Provides for the recovery of costs from energy efficiency investments. |

| Phase-In Rider (PIR) | | SD | | Provides for the recovery of costs outside of a general rate case for investments in new generation facilities. |

Renewable Energy Standard

Minnesota has a renewable energy standard requiring utilities to generate or procure sufficient renewable generation such that the following percentages of total retail electric sales to Minnesota customers come from qualifying renewable sources: 17% by 2016; 20% by 2020 and 25% by 2025. We met the current renewable sources requirements with a combination of owned renewable generation and purchases from renewable generation sources. Minnesota law also requires 1.5% of total Minnesota electric sales by public utilities to be supplied by solar energy. For a public utility with between 50,000 and 200,000 retail electric customers, such as OTP, at least 10% of the 1.5% requirement must be met by solar energy generated by or procured from solar photovoltaic devices with a nameplate capacity of 40 kWs or less. OTP plans to purchase Solar Renewable Energy Credits (SRECs) to meet its obligations until its Hoot Lake Solar and other solar projects are complete and operational. OTP plans to purchase SRECs to meet its 2021 obligation, for which compliance will be measured as of April 30, 2022.

Under certain circumstances and after consideration of costs and reliability issues, the MPUC may modify or delay implementation of the standards. We are evaluating potential options for maintaining compliance and meeting the solar energy standard beyond 2021.

Integrated Resource Plan (IRP)

Under Minnesota law, utilities are required to submit for approval by the MPUC a 15-year advance IRP. An IRP is a set of resource options a utility could use to meet the service needs of its customers over the forecast period, including an explanation of the utility’s supply and demand circumstances, and the extent to which each resource option would be used to meet those service needs. The MPUC’s findings of fact and conclusions regarding IRPs are considered to be prima facie evidence, subject to rebuttal, in future rate reviews and other proceedings. Typically, IRPs are submitted every two years.

In 2021, the North Dakota Legislative Assembly enacted a provision requiring investor-owned electric utilities to submit an IRP to the NDPSC and granted the NDPSC the authority to adopt rules and regulations for the preparation and submission of integrated resource plans. To date, the NDPSC has not established any formal rules and regulations.

On September 1, 2021, OTP filed its 2022 IRP concurrently with regulators in the three states where OTP operates, Minnesota, North Dakota and South Dakota. The 2022 IRP includes OTP’s preferred plan for meeting customers’ anticipated capacity and energy needs while maintaining system reliability and low electric service rates.

The components of OTP's preferred plan include:

•the addition of dual fuel capability at our Astoria Station natural gas plant, allowing for the plant to burn fuel oil in addition to natural gas;

•the addition of 150 megawatts of solar generation in 2025;

•the addition of 100 megawatts of wind generation in 2027;

•the commencement of the process of withdrawing from our 35 percent ownership interest in Coyote Station, a jointly owned, coal-fired generation plant, by December 31, 2028; and

•the addition of 50 megawatts of solar generation in 2033.