UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

[X] QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended: September 30, 2016

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from __________ to _________

Commission File Number 000-54333

XCELMOBILITY INC.

(Exact name of registrant as specified in its charter)

| Nevada | 98-1102006 | |

| (State or Other Jurisdiction of | (I.R.S. Employer | |

| Incorporation or Organization) | Identification Number) |

2225 East Bayshore Road, Suite 200, Palo Alto, CA 94303

(Address of principal executive offices) (Zip Code)

(650) 320-1728

(Registrant’s telephone number, including area code)

N/A

(Former address, if changed since last report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[X] Yes [ ] No

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files)

[X] Yes [ ] No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| [ ] Large accelerated filer | [ ] Accelerated filer | [ ] Non-accelerated filer | [X] Smaller reporting company |

| (Do not check if smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). [ ] Yes [X] No

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

| Class | Outstanding as of November 15, 2016 | ||||

| Common stock, $0.001 par value | 2,160,533,090 | ||||

XCELMOBILITY INC. FORM 10-Q

INDEX

| 2 |

FORWARD-LOOKING STATEMENTS

This Quarterly Report on Form 10-Q contains forward-looking statements within the meaning of the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. Reference is made in particular to the description of our plans and objectives for future operations, assumptions underlying such plans and objectives, and other forward-looking statements included in this report. Such statements may be identified by the use of forward-looking terminology such as “may,” “will,” “expect,” “believe,” “estimate,” “anticipate,” “intend,” “continue,” or similar terms, variations of such terms or the negative of such terms. Such statements are based on management’s current expectations and are subject to a number of factors and uncertainties, which could cause actual results to differ materially from those described in the forward-looking statements. Such statements address future events and conditions concerning, among others, capital expenditures, earnings, litigation, regulatory matters, liquidity and capital resources, and accounting matters. Actual results in each case could differ materially from those anticipated in such statements by reason of factors such as future economic conditions, changes in consumer demand, legislative, regulatory and competitive developments in markets in which we operate, results of litigation, other circumstances affecting anticipated revenues and costs, and the risk factors set forth in our Annual Report on Form 10-K filed on April 19, 2016.

The forward-looking statements made in this report on Form 10-Q relate only to events or information as of the date on which the statements are made in this report on Form 10-Q. Except as required by law, we undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events, or otherwise, after the date on which the statements are made or to reflect the occurrence of unanticipated events. You should read this report and the documents that we reference in this report, including documents referenced by incorporation, completely and with the understanding that our actual future results may be materially different from what we expect or hope.

YOU SHOULD NOT PLACE UNDUE RELIANCE ON THESE FORWARD LOOKING STATEMENTS.

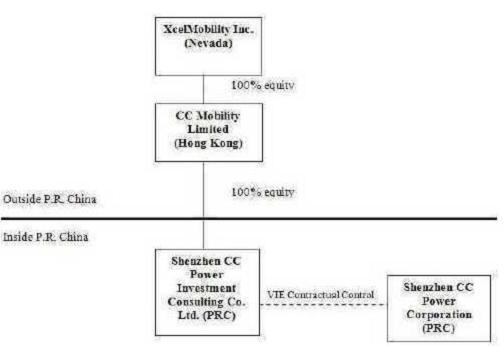

As used in this Quarterly Report on Form 10-Q, references to “dollars” and “$” are to United States dollars and, unless otherwise indicated, references to “we,” “our,” “us,” “Xcel,” “XCLL,” the “Company” or the “Registrant” refer to XcelMobility Inc., a Nevada corporation and its wholly owned subsidiaries, CC Mobility Limited (“CC Mobility”), a company organized under the laws of Hong Kong, Shenzhen CC Power Investment Consulting Co. Ltd. (“CC Investment”), a company organized under the laws of the People’s Republic of China, and a wholly-owned subsidiary of CC Mobility, and Shenzhen CC Power Corporation (“CC Power”), a company organized under the laws of the People’s Republic of China.

| 3 |

XCELMOBILITY INC. AND SUBSIDIARIES

FOR THE THREE MONTHS AND NINE MONTHS ENDED SEPTEMBER 30, 2016 AND 2015

INDEX TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

| 4 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| CONDENSED CONSOLIDATED BALANCE SHEETS |

| September 30, 2016 | December 31, 2015 | |||||||

| (unaudited) | (audited) | |||||||

| ASSETS | ||||||||

| Current Assets: | ||||||||

| Cash and cash equivalents | $ | 106,369 | $ | 37,774 | ||||

| Trade accounts receivable | 18,686 | 20,363 | ||||||

| Other receivables and prepayment | 18,374 | - | ||||||

| Inventory | 59,303 | 60,935 | ||||||

| Prepaid VAT | 4,064 | 9,670 | ||||||

| Total Current Assets | $ | 206,796 | $ | 128,742 | ||||

| Property, Plant and Equipment, net of accumulated depreciation of $142,932 and $119,328, respectively | 52,221 | 68,670 | ||||||

| TOTAL ASSETS | $ | 259,017 | $ | 197,412 | ||||

| LIABILITIES AND SHAREHOLDERS’ DEFICIT | ||||||||

| Current Liabilities: | ||||||||

| Amount due to a director | $ | - | $ | 599,318 | ||||

| Other payables and accrued expenses | 441,909 | 984,242 | ||||||

| Other taxes payable | 2,503 | 4,909 | ||||||

| Convertible notes, net of debt discount | 2,450,000 | 101 | ||||||

| Derivative liability | 429,111 | 279,071 | ||||||

| Accrued interest | 247,884 | 188,987 | ||||||

| Total Current Liabilities | $ | 3,571,407 | $ | 2,056,628 | ||||

| Convertible notes, net of debt discount | - | 993,505 | ||||||

| Accrued interest | 981 | 881 | ||||||

| Total Liabilities | $ | 3,572,388 | $ | 3,051,014 | ||||

| Shareholders’ Equity: | ||||||||

| Preferred stock, $0.001 par value, 20,000,000 shares authorized; 10,000,000 shares issued and outstanding at September 30, 2016 and December 31, 2015 | 10,000 | 10,000 | ||||||

| Common stock, $0.001 par value, 800,000,000 shares authorized; 660,533,090 and 568,582,680 shares issued and outstanding at September 30, 2016 and December 31, 2015 | 660,533 | 568,583 | ||||||

| Shares unissued | 486,500 | 486,500 | ||||||

| Additional paid in capital | 1,880,909 | 1,938,503 | ||||||

| Accumulated deficit | (7,324,211 | ) | (6,229,903 | ) | ||||

| Accumulated other comprehensive loss | 972,898 | 372,715 | ||||||

| Total Shareholders’ Equity | (3,313,371 | ) | (2,853,602 | ) | ||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | 259,017 | $ | 197,412 | ||||

The accompanying notes are an integral part of the condensed consolidated financial statements

| 5 |

XCELMOBILITY INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS AND COMPREHENSIVE LOSS

(UNAUDITED)

| For the Three Months Ended | For the Nine Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2016 | 2015 | 2016 | 2015 | |||||||||||||

| Revenue | $ | 80,128 | $ | 83,286 | $ | 183,842 | $ | 250,283 | ||||||||

| Cost of Revenue | 30,617 | 97,854 | 70,558 | 173,475 | ||||||||||||

| Gross Profit | 49,512 | (14,569 | ) | 113,284 | 76,808 | |||||||||||

| Operating Expenses: | ||||||||||||||||

| Selling expense | 48,442 | 73,338 | 90,452 | 187,250 | ||||||||||||

| General and administrative expense | 360,267 | 227,741 | 687,343 | 542,446 | ||||||||||||

| Total Operating Expenses | 408,709 | 301,079 | 777,795 | 729,696 | ||||||||||||

| Income (loss) from Operations | (359,198 | ) | (315,648 | ) | (664,511 | ) | (652,888 | ) | ||||||||

| Other Income (Expense): | ||||||||||||||||

| Interest income | 64 | 149 | 103 | 224 | ||||||||||||

| Interest expense | (291 | ) | (760 | ) | (123,404 | ) | (1,128 | ) | ||||||||

| Gain (loss) on derivative | 5,094 | (320,518 | ) | (30,160 | ) | 314,493 | ||||||||||

| Amortization of debt discount | (623,273 | ) | 131,093 | (621,611 | ) | (12,435 | ) | |||||||||

| Other income (expense) | (356,276 | ) | - | (356,276 | ) | - | ||||||||||

| Total Other Income (Expense) | (262,130 | ) | (190,036 | ) | (429,796 | ) | 301,154 | |||||||||

| Income (loss) Before Taxes | (621,328 | ) | (505,684 | ) | (1,094,307 | ) | (351,734 | ) | ||||||||

| Income tax expense | - | - | - | - | ||||||||||||

| Net Income (Loss) | (621,328 | ) | (505,684 | ) | (1,094,307 | ) | (351,734 | ) | ||||||||

| Foreign currency translation adjustment | (546,168 | ) | (315,637 | ) | (600,183 | ) | 340,971 | |||||||||

| Comprehensive (loss) income | (1,167,496 | ) | (821,321 | ) | (1,674,490 | ) | 10,763 | |||||||||

| Basic income (loss) per share: | $ | 0.00 | $ | 0.00 | $ | 0.00 | $ | 0.00 | ||||||||

| Diluted income (loss) per share: | $ | 0.00 | $ | 0.00 | $ | 0.00 | $ | 0.00 | ||||||||

| Basic weighted average number of shares outstanding | 333,925,553 | 253,896,191 | 333,925,553 | 253,896,191 | ||||||||||||

| Diluted weighted average number of shares outstanding | 333,925,553 | 253,896,191 | 333,925,553 | 253,896,191 | ||||||||||||

The accompanying notes are an integral part of the condensed consolidated financial statements

| 6 |

XCELMOBILITY INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(UNAUDITED)

| For the Nine Months Ended | ||||||||

| September 30, | ||||||||

| 2016 | 2015 | |||||||

| Cash Flows from Operating Activities: | ||||||||

| Net income (loss) | $ | (1,094,307 | ) | $ | (350,605 | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities | ||||||||

| Depreciation | 15,030 | 13,787 | ||||||

| Amortization of debt discount | - | 12,435 | ||||||

| Fair value adjustment on derivative liability | 632,611 | (314,493 | ) | |||||

| Changes in assets and liabilities: | ||||||||

| Trade accounts receivable, net | 1,677 | 19,350 | ||||||

| Other receivables and prepayment | (12,768 | ) | 88,736 | |||||

| Advances to suppliers | - | (3,059 | ) | |||||

| Inventory | 1,632 | (61,869 | ) | |||||

| Prepaid VAT | - | |||||||

| Account payable | (310,875 | ) | 92,720 | |||||

| Accrued interest | 58,997 | 2,676 | ||||||

| Other taxes payable | (2,406 | ) | (6,142 | ) | ||||

| Other payables and accrued expenses | (260,837 | ) | (260,958 | ) | ||||

| Deferred revenue | - | (19,135 | ) | |||||

| Net Cash Used In Operating Activities | (971,246 | ) | (786,827 | ) | ||||

| Cash Flows from Investing Activities: | ||||||||

| Purchase of property, plant and equipment, net of value added tax refunds received | (1,419 | ) | (40,992 | ) | ||||

| Net Cash Used In Investing Activities | (1,419 | ) | (40,992 | ) | ||||

| Cash Flows from Financing Activities: | ||||||||

| Payment for director’s loan | (356,846 | ) | - | |||||

| Proceeds from issuance of notes payable | 1,408,050 | 65,000 | ||||||

| Net Cash Provided By Financing Activities | 1,051,204 | 65,000 | ||||||

| Effect of Exchange Rate Changes on Cash and Cash Equivalents | (9,943 | ) | 638,865 | |||||

| Net Change in Cash and Cash Equivalents | 68,595 | (123,954 | ) | |||||

| Cash and Cash Equivalents at Beginning of Period | 37,774 | 159,628 | ||||||

| Cash and Cash Equivalents at End of Period | $ | 106,369 | $ | 35,674 | ||||

| Supplement Cash Flow Information | ||||||||

| Cash paid during the period for interest | $ | - | $ | - | ||||

| Cash received during the period for interest | 103 | 224 | ||||||

| Cash paid during the period for income taxes | $ | - | $ | - | ||||

The accompanying notes are an integral part of the condensed consolidated financial statements

| 7 |

XCELMOBILITY INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

1. Organization and Nature of Business

XcelMobility Inc.

XcelMobility Inc. (“Xcel” or the “Company”) was incorporated under the laws of the State of Nevada on December 27, 2007. Initial operations have included organization and incorporation, target market identification, marketing plans, and capital formation. The Company was no longer a development stage company after the Company started to generate revenues from various application of mobile device.

Share Cancellation

On August 11, 2011, Moses Carlo Supera Paez, a director and shareholder of the Company, surrendered 17,700,000 shares of common stock for cancellation. Further, on August 30, 2011, Mr. Paez surrendered an additional 7,350,000 shares of our common stock for cancellation and Mr. Jaime Brodeth, one of our former directors and a shareholder, surrendered 22,950,000 shares of our common stock for cancellation. As such, immediately prior to the Exchange Transaction as further discussed in detail later and after giving effect to the foregoing cancellations, the Company had 29,700,000 shares of common stock issued and outstanding. Immediately after the Exchange Transaction, the Company had 60,000,000 shares of common stock issued and outstanding.

CC Mobility Limited

CC Mobility Limited (“CC Mobility”), a company organized under the laws of Hong Kong, was formed on May 3, 2011 and has authorized capital of 10,000 shares with registered capital of HK$1,000 at HK$1 per share. At formation, CC Mobility Limited has issued 560 shares to CC Wireless Limited, a company organized under the laws of Hong Kong, and 440 shares to Sheen Ventures Limited, a company organized under the laws of Hong Kong. The Company is a holding company formed for the purpose of acquiring a target company to effect a reverse merger with a U.S. reporting company. The reverse merger was completed on August 30, 2011.

CC Power Investment Consulting Co. Ltd.

Shenzhen CC Power Investment Consulting Co. Ltd. (“CC Investment”), a wholly-owned subsidiary of CC Mobility, was incorporated on July 27, 2011 under the laws of the People’s Republic of China (“PRC”) as a wholly foreign owned limited liability company. The required registered capital is $2,000,000 and as of December 31, 2013, $400,000 of the registered capital has been contributed.

Shenzhen CC Power Corporation

Shenzhen CC Power Corporation (“CC Power”) is a Chinese enterprise organized in the PRC on March 13, 2003 in accordance with the Laws of the People’s Republic of China. The required registered capital of CC Power was approximately $1,547,000 (RMB 10,000,000) and as of December 31, 2013, CC Power has paid up approximately $346,000 (RMB2,526,000). In March 2011, Mr. Ryan Ge sold his 5% ownership in CC Power to the other shareholder, Xili Wang (“CC Power Shareholder”). Ms. Wang holds 100% ownership interest in CC Power at the end of the financial period.

CC Power is primarily engaged in the research, development and commercialization of applications for mobile devices that access the Internet utilizing mobile phone networks. CC Power’s principal activity is the design, testing sale and support of software to support mobile internet applications on cellular phones, smart phones, tablets and mobile computers in China. The principal product designed and built by CC Power is its Mach 5 Accelerator. This product has been independently tested by all 3 mobile phone carriers in China and accesses the internet 5 times faster than with other mobile browsers. The speed of the Mach 5 browser enables CC Power to develop other mobile software that can leverage off the Mach 5 products speed of processing. In order to support CC Power products the Company has built a series of server locations throughout China. CC Power sells its products to corporations directly, to individual users via the company’s website and retail locations, through distribution agents and through all three mobile phone carriers in China.

As noted above, the primary purpose of CC Power is to develop software that allows user faster access to the Internet. CC Power’s primary focus is in the mobile Internet market, with a focus on providing software that significantly increases the speed that users of smartphones, tablets and laptops can access the Internet over cellular phone networks. CC Power also uses their technology to increase the speed at which users of Virtual Private Networks can access data from their networks.

On September 22, 2014, XcelMobility Inc. entered into an Asset Purchase Agreement with CC Power, Xianjiang Silvercreek Digital Technology Co., Ltd. (“Silvercreek”) and the shareholders of Silvercreek (the “Selling Shareholders”). Pursuant to the terms of the Agreement, CC Power will acquire certain assets of Silvercreek relating to its online sports lottery business unit in exchange for the issuance of up to 80,000,000 shares of common stock of the Company to the Selling Shareholders. No Shares will be issued upon the closing date of the transaction. The Shares will be issued to the Selling Shareholders on a pro rata basis and upon achievement of the following milestones: (i) 10,000,000 Shares to be issued in the event that CC Power derives initial online lottery sales revenue (“Lottery Revenue”) of over 10,000 RMB per month from the business developed in connection with the Assets on or before October 1, 2014; (ii) 10,000,000 Shares to be issued in the event that CC Power derives Lottery Revenue of over 3,000,000 RMB per month from the business developed in connection with the Assets on or before March 31, 2016; (iii) 10,000,000 Shares to be issued in the event that CC Power derives initial online lottery sales revenue of over 20,000,000 RMB per month from the business developed in connection with the Assets on or before December 31, 2015; (iv) 40,000,000 Shares to be issued in the event that CC power obtains a lottery gaming license from the People’s Republic of China; and (v) 10,000,000 Shares to be issued based on the achievement of certain incentives as determined by the board of directors of the Company.

| 8 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

1. Organization and Nature of Business – Continued

Share Exchange Agreement

On August 30, 2011, the Company completed a voluntary share exchange transaction with Shenzhen CC Power Corporation, CC Mobility Limited and the shareholders of CC Mobility (“Selling Shareholders”) pursuant to a Share Exchange Agreement dated July 5, 2011 (the “Exchange Agreement”). In accordance with the terms of Exchange Agreement, on the Closing Date, Xcel issued 30,300,000 shares of its common stock to the Selling Shareholders in exchange for 100% of the issued and outstanding capital stock of CC Mobility (the “Exchange Transaction”). As a result of the Exchange Transaction, there was a change of control in the Company as the Selling Shareholders of CC Mobility acquired 50.5% of Xcel’s issued and outstanding common stock, CC Mobility became Xcel’s wholly-owned subsidiary, and Xcel acquired the business and operations of CC Mobility and CC Power.

For accounting purposes, the merger transaction is being accounted for as a reverse merger. The transaction has been treated as a recapitalization of CC Mobility and its subsidiaries, with Xcel (the legal acquirer of CC Mobility and its subsidiaries) considered the accounting acquiree and CC Mobility whose management took control of Xcel (the legal acquire of CC Mobility) considered the accounting acquirer.

CC Power is owned by an individual but controlled by CC Investment through a series of contractual arrangements that transferred all of the benefits and responsibilities for the operations of CC Power to CC Investment. CC Investment accounts for CC Power as a Variable Interest Entity (“VIE”) under ASC 810 “Consolidation.” Accordingly, CC Investment consolidates CC Power’s results, assets and liabilities.

Shenzhen Jifu Communication Technology Co., Ltd.

Shenzhen Jifu Communication Technology Co., Ltd (“Jifu”), was incorporated on April 16, 2001 under the laws of the People’s Republic of China (“PRC”) as a limited liability company. The required registered capital is RMB3,000,000 and all of the required registered capital has been contributed.

Jifu is primarily engaged in develops and distributes optical transmitters and receivers, electronic surveillance equipment, and other communications equipment. Jifu also engages in the purchase and sale of electronic products, network products, and communications equipment. In order to bolster its business, Jifu also engages in software research and development.

On May 7, 2013, the Company entered into and consummated a Stock Purchase Agreement (the “Agreement”) with Shenzhen CC Power Investment Consulting Co., Ltd., a company organized under the laws of the People’s Republic of China and an indirect wholly-owned subsidiary of the Company (“CC Power”), Shenzhen Jifu Communication Technology Co., Ltd. a company organized under the laws of the People’s Republic of China (“Jifu”) the shareholders of Jifu set forth in the signature page to the Agreement (the “Jifu Shareholders”) and Hui Luo.

Pursuant to the terms and conditions of the Agreement, the Company will issue an aggregate of 27,000,000 shares of the Company’s common stock (the “Purchase Shares”) to the Jifu Shareholders as consideration for Jifu entering into certain controlling agreements (the “VIE Agreement”) with CC Power. CC Power will effectively own Jifu through the various conditions prescribed in the VIE Agreements. The Company will also grant 3,000,000 shares (the “Luo Shares”, together with the Purchase Shares, the “Shares’”) to Mr. Luo.

The Shares will be released to the Jifu Shareholders and Mr. Luo after the Company has reviewed Jifu’s audited financial statements for the year ended December 31, 2013. If Jifu has achieved net revenue of $4,000,000 for the year ended December 31, 2013 (the “Target”), then the Company will release the Shares to the Jifu Shareholders and Mr. Luo in their full respective amounts. If Jifu has not achieved the Target by the end of the calendar year, the Company will decrease the amount of shares of common stock issued to the Jifu Shareholders and Mr. Luo in accordance with a formula set forth in the Agreement and release the Shares to the Jifu Shareholders and Mr. Luo in their respective decreased amounts. The Agreement has been approved by the boards of directors of the Company, CC Power, and Jifu, and the Jifu Shareholders.

On October 1, 2014, we entered into a Settlement Agreement, Waiver and Mutual Release with Jifu. Pursuant to the Release, the parties cancelled the Stock Purchase Agreement. We have completely transferred bac k the ownership of shares of Jifu to Jifu Shareholders without any further disputation and mutual accountability. In exchange, we have agreed to deliver 1,000,000 newly issued shares of our common stock to Jifu Shareholders.

| 9 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

1. Organization and Nature of Business – Continued

The organizational structure of the Company is as follows:

| 10 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

2. Summary of Significant Accounting Policies

Basis of presentation

The accompanying unaudited condensed consolidated financial statements of the Company and its subsidiaries at September 30, 2016 and for the nine months ended September 30, 2016 and 2015 reflect all adjustments (consisting only of normal recurring adjustments) that, in the opinion of management, are necessary to present fairly the financial position and results of operations of the Company for the periods presented. Operating results for the nine months ended September 30, 2016 are not necessarily indicative of the results that may be expected for the year ending December 31, 2016. The accompanying condensed consolidated financial statements should be read in conjunction with the audited financial statements and the notes thereto for the year ended December 31, 2015. The Company follows the same accounting policies in the preparation of interim reports. The Company’s accounting policies used in the preparation of the accompanying financial statements conform to accounting principles generally accepted in the United States of America (“US GAAP”)

The functional currency is the Chinese Renminbi, however the accompanying condensed consolidated financial statements have been translated and presented in United States Dollars ($). All significant inter-company balances and transactions have been eliminated in consolidation.

All dollars are rounded to nearest hundred except for share data.

| 11 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

2. Summary of Significant Accounting Policies - Continued

Use of estimates

In preparing financial statements in conformity with US GAAP, management is required to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and revenues and expenses during the reported periods. Actual results could differ from those estimates.

Significant Estimates

These financial statements include some amounts that are based on management’s best estimates and judgments. The most significant estimates relate to depreciation of property, plant and equipment, the valuation allowance for deferred taxes. It is reasonably possible that the above-mentioned estimates and others may be adjusted as more current information becomes available, and any adjustment could be significant in future reporting periods.

Variable Interest Entity

CC Power

The accounts of CC Power have been consolidated with the accounts of the Company because CC Power is a variable interest entity with respect to CC Investment, which is a wholly-owned subsidiary of the Company. CC Investment entered into five agreements dated August 22, 2011 with Xili Wang as the “CC Power Shareholder” and with CC Power pursuant to which CC Investment provides CC Power with exclusive technology consulting and management services (collectively referred to as the controlling agreements). On August 25, 2016, Mr. Wei, as the new “CC Power Shareholder” and CC Power revised these agreements pursuant to the transfer of ownership of CC Power from Xili Wang to Zhixiong Wei as set forth in the Agreement on Equity Transfer between Xili Wang and Zhixiong Wei. In summary, the new controlling agreements contain the following terms:

Entrusted Management Agreement. Pursuant to the Entrusted Management Service Agreement among CC Power, CC Investment, and the CC Power Shareholder, CC Investment agrees to provide, and CC Power agrees to accept, exclusive management services, including, without limitation, financial management services, business management services, advertising and marketing services, human resources management services, and internal control services. The Entrusted Management Service Agreement will remain in effect until the completion of an acquisition of all the assets or equity of CC Power by CC Investment or its designated third party, as more fully described in the Exclusive Purchase Option Agreement below.

Technical Services Agreement. Pursuant to the Technical Services Agreement among CC Power, CC Investment, and the CC Power Shareholder, CC Investment agrees to provide, and CC Power agrees to accept, exclusive technical services provided by CC Investment, including, without limitation, software and technology development services, computer system services, data analysis services, training, technical consulting services, and import and export consultancy services. The Technical Services Agreement will remain in effect until completion of an acquisition of all the assets or equity of CC Power by CC Investment or its designated third party, as more fully described in the Exclusive Purchase Option Agreement below.

Exclusive Purchase Option Agreement. . Pursuant to the Exclusive Purchase Option Agreement among CC Power, CC Investment, and the CC Power Shareholder, the CC Power Shareholder granted CC Investment an irrevocable and exclusive option to acquire either all or substantially all of the assets, or all or a part of the equity of CC Power, in each case for nominal consideration, plus the cancellation of all or part of the debt owing under the Loan Agreement described below. CC Investment may exercise its purchase option at any time.

Loan Agreement. Pursuant to the Loan Agreement between CC Investment and the CC Power Shareholder, CC Investment agreed to lend 10,000,000 RMB to the CC Power Shareholder. The loan is to be used solely for the operations of CC Power. As security for the loan, the CC Power Shareholder agreed to pledge his equity in CC Power, as more fully described in the Equity Pledge Agreement below.

| 12 |

XCELMOBILITY INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

2. Summary of Significant Accounting Policies – Continued

Equity Pledge Agreement. Pursuant to the Equity Pledge Agreement among CC Power, CC Investment, and the CC Power Shareholder, the CC Power Shareholder agreed to pledge all of his equity interest in CC Power to CC Investment as a guaranty of the performance of the obligations of the CC Power Shareholder and CC Power under the Loan Agreement, the Entrusted Management Service Agreement, the Technical Services Agreement, and the Exclusive Purchase Option Agreement. The Equity Pledge Agreement will remain in effect until all payments due and obligations under the foregoing agreements have been fulfilled by the CC Power Shareholder and/or CC Power. Pursuant to the terms of the Equity Pledge Agreement, the CC Power Shareholder shall not, among other things, sell, transfer, mortgage or otherwise dispose of or encumber the pledged equity interests without CC Investment’s prior written consent.

Assignment and Novation Agreement

In addition to revising the controlling agreements, CC Power, CC Investment, Xili Wang and Mr. Wei entered into an Assignment and Novation Agreement, under which the parties acknowledged that the new CC Power controlling agreements have replaced the original controlling agreements in their entirety, meaning that as of August 25, 2016, Xili Wang assigned to Mr. Wei all of the rights of the CC Power Shareholder under the CC Power controlling agreements, and Mr. Wei assumed from Xili Wang all of the obligations of the CC Power Shareholder under such agreements. The Assignment and Novation Agreement provides that the original controlling agreements have been terminated and replaced in their entirety by the updated controlling agreements. With respect to the Loan Agreement, the Assignment and Novation Agreement provides that the amount originally borrowed by Xili Wang under the original loan agreement, which was contributed to the bank account of CC Power, shall be treated as the amount received by Mr. Wei under the Loan Agreement, and that Mr. Wei shall assume the responsibility to repay the loan and fulfill all the obligations of the borrower under the Loan Agreement.

In sum, the agreements transfer to CC Investment all of the benefits and all of the risk arising from the operations of CC Power, as well as complete managerial authority over the operations of CC Power. Through these contractual arrangements, the Company has the ability to substantially influence CC Power’s daily operations and financial affairs, appoint its directors and senior executives, and approve all matters requiring board and/or shareholder approval. These contractual arrangements enable the Company to control CC Power and operate our business in the PRC through CC Investment. By reason of the relationship described in these agreements, CC Power is a variable interest entity with respect to CC Investment and CC Investment is considered the primary beneficiary of CC Power because the following characteristics identified in ASC 810-10-15-14 are present:

| - | The holder of the equity investment in CC Power lacks the direct or indirect ability to make decisions about the entity’s activities that have a significant effect on the success of CC Power, having assigned their voting rights and all managerial authority to CC Investment. (ASC 810-10-15-14(b)(1)). | |

| - | The holder of the equity investment in CC Power lacks the obligation to absorb the expected losses of CC Power, having assigned to CC Investment all revenue and responsibility for all payables. (ASC 810-10-15-14(b)(2). | |

| - | The holder of the equity investment in CC Power lacks the right to receive the expected residual returns of CC Power, having granted to CC Investment all revenue as well as an option to purchase the equity interests at a fixed price. (ASC 810-10-15-14(b)(3)). |

Accordingly, the Company’s condensed consolidated financial statements reflect the results of operations, assets and liabilities of CC Power. The carrying amount and classification of CC Power’s assets and liabilities included in the Condensed Consolidated Balance Sheets are as follows:

| September 30, 2016 | December 31, 2015 | |||||||

| Total current assets | $ | 1,883,503 | $ | 1,825,197 | ||||

| Total assets | 1,948,020 | 1,422,400 | ||||||

| Total current liabilities | 2,037,446 | 1,316,298 | ||||||

| Total liabilities | 2,037,446 | 1,316,298 | ||||||

| 13 |

XCELMOBILITY INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

2. Summary of Significant Accounting Policies – Continued

Jifu

The accounts of Jifu have been consolidated with the accounts of the Company because Jifu is a variable interest entity with respect to CC Investment, which is a wholly-owned subsidiary of the Company. CC Investment entered into five agreements dated May 7, 2013 with Jifu Shareholder and with Jifu pursuant to which CC Investment provides Jifu with exclusive technology consulting and management services. In summary, the five agreements contain the following terms:

Entrusted Management Agreement. Effective on May 7, 2013, CC Investment entered into an Entrusted Management Agreement with Jifu and the Jifu Shareholders, pursuant to which CC Investment agreed to provide, and Jifu agreed to accept, exclusive management services provided by CC Investment. Such management services include but are not limited to financial management, business management, marketing management, human resource management and internal control of Jifu. Jifu will pay a service fee to CC Investment on a quarterly basis, which fee will be a percentage of Jifu’s total operational income. The Entrusted Management Agreement will remain in effect until the acquisition of all the assets or equity of Jifu by CC Investment.

Technical Services Agreement. Effective on May 7, 2013, CC Investment entered into a Technical Services Agreement with Jifu and the Jifu Shareholders, pursuant to which CC Investment agreed to provide, and Jifu agreed to accept, exclusive technical services provided by CC Investment. Such technical services include but are not limited to software services, computer systems services, data analysis, training and other technical services. Jifu will pay a service fee to CC Investment on a quarterly basis, which fee shall be a percentage of Jifu’s total operational income. The Technical Service Agreement will remain in effect until the acquisition of all the assets or equity of Jifu by CC Investment.

Exclusive Purchase Option Agreement. Effective on May 7, 2013, CC Investment entered into an Exclusive Purchase Option Agreement with Jifu and the Jifu Shareholders, pursuant to which the Jifu Shareholders granted CC Investment an irrevocable and exclusive purchase option to acquire all of Jifu’s equity and/or assets at a nominal consideration. CC Investment may exercise the purchase option at any time. Until CC Investment has exercised its purchase option, Jifu is required to conduct its business in accordance with certain covenants as further described in the Exclusive Purchase Option Agreement.

Loan Agreement

Effective on May 7, 2013, CC Investment entered into a Loan Agreement with the Jifu Shareholders, pursuant to which CC Investment agreed to lend RMB 3,000,000 to the Jifu Shareholders, to be used solely for the operations of Jifu. The loan is interest free, unless the deemed value of the consideration for the equity purchase of Jifu or asset purchase of Jifu under the Exclusive Purchase Option Agreement is higher than the principal amount of the loan, in which case the excess will be deemed to be interest on the loan.

Equity Pledge Agreement

Effective on May 7, 2013, CC Investment entered into an Equity Pledge Agreement with Jifu and the Jifu Shareholders, pursuant to which the Jifu Shareholders pledged all of their equity interests in Jifu, including the proceeds thereof, to guarantee all of CC Investment’s rights and benefits under the Entrusted Management Agreement, the Technical Service Agreement, the Exclusive Purchase Option Agreement and the Loan Agreement. Prior to termination of the Equity Pledge Agreement, the pledged equity interests cannot be transferred without CC Investment’s prior consent. The Jifu Shareholders covenant to CC Investment that among other things, they will only appoint/elect candidates for the board of directors of Jifu and supervisor office of Jifu that were nominated by CC Investment.

| 14 |

XCELMOBILITY INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

2. Summary of Significant Accounting Policies – Continued

In sum, the agreements transfer to CC Investment all of the benefits and all of the risk arising from the operations of Jifu, as well as complete managerial authority over the operations of Jifu. Through these contractual arrangements, the Company has the ability to substantially influence Jifu’s daily operations and financial affairs, appoint its directors and senior executives, and approve all matters requiring board and/or shareholder approval. These contractual arrangements enable the Company to control Jifu and operate our business in the PRC through CC Investment. By reason of the relationship described in these agreements, Jifu is a variable interest entity with respect to CC Investment and CC Investment is considered the primary beneficiary of Jifu because the following characteristics identified in ASC 810-10-15-14 are present:

|

The holder of the equity investment in Jifu lacks the direct or indirect ability to make decisions about the entity’s activities that have a significant effect on the success of Jifu, having assigned their voting rights and all managerial authority to CC Investment. (ASC 810-10-15-14(b)(1)). | |

|

The holder of the equity investment in Jifu lacks the obligation to absorb the expected losses of Jifu, having assigned to CC Investment all revenue and responsibility for all payables. (ASC 810-10-15-14(b)(2). | |

|

The holder of the equity investment in Jifu lacks the right to receive the expected residual returns of Jifu, having granted to CC Investment all revenue as well as an option to purchase the equity interests at a fixed price. (ASC 810-10-15-14(b)(3)). |

On October 1, 2014, we entered into a Settlement Agreement, Waiver and Mutual Release with Jifu. Pursuant to the Release, the parties cancelled the Stock Purchase Agreement. We have completely transferred bac k the ownership of shares of Jifu to Jifu Shareholders without any further disputation and mutual accountability. In exchange, we have agreed to deliver 1,000,000 newly issued shares of our common stock to Jifu Shareholders.

Revenue recognition

Our source of revenues is from internet accelerator software, which includes new software license revenues and software plus hardware and maintenance arrangements, and the source of revenue of Jifu is from developing and distributing optical transmitters and receivers, electronic surveillance equipment, and other communications equipment; and trading of electronic products, network products, and communications equipment. We also engage in software research and development, GPS system development and website development projects along with maintenance arrangements.

We evaluate revenue recognition based on the criteria set forth in FASB ASC 985-605, Software: Revenue Recognition and Staff Accounting Bulletin (“SAB”) No. 101, Revenue Recognition in Financial Statements, as revised by SAB No. 104, Revenue Recognition.

| 15 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

2. Summary of Significant Accounting Policies - Continued

Revenue Recognition for Software Products (Software Elements)

New software license revenues represent fees earned from granting customers licenses to download our software products that aim at improving the internet connection speed of the mobile phone, computers or servers. The basis for software license revenue recognition is substantially governed by the accounting guidance contained in ASC 985-605, Software-Revenue Recognition. For software license that do not require significant modification or customization of the underlying software, we recognize new software license revenues when: (1) we enter into a legally binding arrangement with a customer for the license of software; (2) we deliver the products; (3) the sale price is fixed or determinable and free of contingencies or significant uncertainties; and (4) collection is probable. Revenues that are not recognized at the time of sale because the foregoing conditions are not met are recognized when those conditions are subsequently met.

Our software license arrangements do not include acceptance provisions, software license updates or product support contracts.

Revenue Recognition for Multiple-Element Arrangements - Software Products and Software Related Services(Software Arrangements)

We enter into arrangements with customers that purchase software related products that include one to three year product support service and a short training session (referred to as software related multiple-element arrangements). Such software related multiple-element arrangements include the sale of our software products, and product support contracts whereby software license delivery is followed by the subsequent delivery of the other elements. Our software license arrangements include acceptance provisions. We recognize revenue upon the receipt of written customer acceptance. The vast majority of our software license arrangements include software license updates and product support contracts. Software license updates provide customers with rights to unspecified software product upgrades during the term of the support period. Product support includes telephone access to technical support personnel or on-site support. For those software related multiple-element arrangements, we recognized revenue pursuant to ASC 985-605. Since we are unable to determine the fair value of the selling price for the undelivered elements in a multiple-element arrangement, which is the product support service and training, the entire arrangement consideration is deferred and is recognized ratably over the term of the arrangement, typically one year to three years.

Revenue Recognition for Multiple-Element Arrangements - Arrangements with Software and Hardware Elements

We also enter into multiple-element arrangements that may include a combination of our software installed in the hardware products we purchased from third parties and service offerings including purchased hardware , new software licenses, installation of the software in the hardware and one to three years product support. We adopted Accounting Standards Update (“ASU”) 2009-13, Revenue Recognition (Topic 605) : Multiple-Deliverable Revenue Arrangements . This guidance modifies the fair value requirements of FASB ASC subtopic 605-25, Revenue Recognition-Multiple Element Arrangements , by allowing the use of the “best estimate of selling price” in addition to vendor-specific objective evidence and third-party evidence for determining the selling price of a deliverable for non-software arrangements. This guidance establishes a selling price hierarchy for determining the selling price of a deliverable, which is based on: (a) vendor-specific objective evidence, (b) third-party evidence, or (c) estimated selling price. In addition, the residual method of allocating arrangement consideration is no longer permitted. In such arrangements, we first allocate the total arrangement consideration based on the relative selling prices of the software group of elements as a whole and to the hardware elements. We recognize the hardware element considerations upon delivery of the hardware. The consideration allocated to the software group which includes the software element and the product support is recognized in according to the software arrangements policy as described above.

Revenue Recognition for Lottery Revenue

Commission income is recognized when the lottery ticket is sold through its online system. Other service income is recognized when the service is provided.

Cost of Revenue

Cost of revenue primarily consists of direct costs of products, direct labor of technical staff, depreciation of computer equipment, and overhead associated with the technical department.

| 16 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

2. Summary of Significant Accounting Policies - Continued

Economic and political risks

The Company’s operations are mainly conducted in the PRC. Accordingly, the Company’s business, financial condition and results of operations in the PRC may be influenced by the political, economic and legal environment in the PRC, and by the general state of the PRC.

The Company’s major operations in the PRC are subject to special considerations and significant risks not typically associated with companies in North America. These include risks associated with, among others, the political, economic and legal environment and foreign currency exchange. The Company’s results may be adversely affected by changes in the political and social conditions in the PRC, and by changes in government administration, governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion, remittances abroad, and rates and methods of taxation, among other things.

Credit risk

The Company may be exposed to credit risk from its cash and fixed deposits at bank. No allowance has been made for estimated irrecoverable amounts determined by reference to past default experience and the current economic environment.

Property and equipment

Plant and equipment are carried at cost less accumulated depreciation. Depreciation is provided over their estimated useful lives, using the straight-line method. Estimated useful lives of the plant and equipment are as follows:

| Equipment | 5 years |

| Office equipment | 5 years |

| Leasehold improvements | Over the lease terms |

| Software | 5 years |

The cost and related accumulated depreciation of assets sold or otherwise retired are eliminated from the accounts and any gain or loss is included in the statement of income. The cost of maintenance and repairs is charged to income as incurred, whereas significant renewals and betterments are capitalized.

Accounting for the impairment of long-lived assets

Impairment of Long-Lived Assets is evaluated for impairment at a minimum on an annual basis whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable in accordance with ASC 360-10 “Impairments of Long-Lived Assets”. An asset is considered impaired if its carrying amount exceeds the future net cash flow the asset is expected to generate. If an asset is considered to be impaired, the impairment to be recognized is measured by the amount by which the carrying amount of the asset exceeds its fair market value. The recoverability of long-lived assets is assessed by determining whether the unamortized balances can be recovered through undiscounted future net cash flows of the related assets. The amount of impairment, if any, is measured based on projected discounted future net cash flows using a discount rate reflecting the Company’s average cost of capital.

| 17 |

XCELMOBILITY INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

2. Summary of Significant Accounting Policies – Continued

Inventories

Inventories are stated at the lower of cost or market value. Substantially all inventory costs are determined using the weighted average basis. The management regularly evaluates the composition of its inventory to identify slow-moving and obsolete inventories to determine if additional write-downs are required.

Accounts receivable

Accounts receivable consists of amounts due from customers. An allowance for doubtful accounts is established and determined based on management’s assessment of known requirements, aging of receivables, payment history, the customer’s current credit worthiness and the economic environment. As of September 30, 2016 and December 31, 2015, no allowance for doubtful accounts was deemed necessary based on management’s assessment.

Fair Value of Financial Instruments

FASB accounting standards require disclosing fair value to the extent practicable for financial instruments that are recognized or unrecognized in the balance sheet. The fair value of the financial instruments disclosed herein is not necessarily representative of the amount that could be realized or settled, nor does the fair value amount consider the tax consequences of realization or settlement.

For certain financial instruments, including cash, accounts payable, accruals and other payables, the carrying amounts approximate fair value because of the near term maturities of such obligations.

Patents

The Company has three patents as listed in the table below relating to its internet accelerator software products. Fees related to registering these patents were insignificant and have been expensed as incurred.

| Patent | Register Number | Issued By | ||||

| Mach5 Internet Acceleration Software V.6.0 | 2007SR09253 | National Copyright Administration of PRC | ||||

| Mach5 Enterprise Acceleration Software V.3.3 | 2009SR058767 | National Copyright Administration of PRC | ||||

| Mach5 Web Browser Software | 2010SR001089 | National Copyright Administration of PRC | ||||

Research and development and Software Development Costs

All research and development costs are expensed as incurred. Software development costs eligible for capitalization under ASC 985-20, Software-Costs of Software to be Sold, Leased or Marketed, were not material to our consolidated financial statements for the nine months ended September 30, 2016 and 2015. Research and development expenses amounted to $108,912 and $ 193,795 for the nine months ended September 30, 2016 and 2015, respectively, and were included in general and administrative expense.

Comprehensive income

Comprehensive income is defined as the change in equity of a company during a period from transactions and other events and circumstances excluding transactions resulting from investments from owners and distributions to owners. For the Company, comprehensive income for the periods presented includes net income and foreign currency translation adjustments.

Income taxes

Income taxes are provided on an asset and liability approach for financial accounting and reporting of income taxes. Current tax is based on the profit or loss from ordinary activities adjusted for items that are non-assessable or disallowable for income tax purpose and is calculated using tax rates that have been enacted or substantively enacted at the balance sheet date. Deferred income tax liabilities or assets are recorded to reflect the tax consequences in future differences between the tax basis of assets and liabilities and the financial reporting amounts at each year end. A valuation allowance is recognized if it is more likely than not that some portion, or all, of a deferred tax asset will not be realized.

| 18 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

2. Summary of Significant Accounting Policies - Continued

Foreign currency translation

Assets and liabilities of the Company’s subsidiaries with a functional currency other than US$ are translated into US$ using period end exchange rates. Income and expense items are translated at the average exchange rates in effect during the period. Foreign currency translation differences are included as a component of Accumulated Other Comprehensive Income in Shareholders’ Equity.

The exchange rates used to translate amounts in RMB into USD for the purposes of preparing the financial statements were as follows:

| September 30, 2016 | ||

| Balance sheet | RMB 6.6694 to US $1.00 | |

| Statement of income and other comprehensive income | RMB 6.5771 to US $1.00 |

| September 30, 2015 | ||

| Balance sheet | RMB 6.3561 to US $1.00 | |

| Statement of income and other comprehensive income | RMB 6.3568 to US $1.00 |

| December 31, 2015 | ||

| Balance sheet | RMB 6.4904 to US $1.00 | |

| Statement of income and other comprehensive income | RMB 6.2175 to US $1.00 |

The RMB is not freely convertible into foreign currency and all foreign exchange transactions must take place through authorized institutions. No representation is made that the RMB amounts could have been, or could be, converted into USD at the rates used in translation.

| 19 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

2. Summary of Significant Accounting Policies - Continued

Post-retirement and post-employment benefits

The Company contributes to a state pension plan in respect of its PRC employees. Other than the state pension plan, the Company does not provide any other post-retirement or post-employment benefits.

Recently Issued Accounting Pronouncements

The Financial Accounting Standards Board (“FASB”) has issued Accounting Standards Update (“ASU”) No. 2015-01 “Simplifying Income Statement Presentation by Eliminating the Concept of Extraordinary Items”. The objective is to reduce the cost and complexity of income statement presentation by eliminating the concept of extraordinary items while maintaining or improving the usefulness of the information provided to the users of financial statements. The extraordinary items must meet two criteria: unusual nature and infrequency of occurrence. If an event or transaction meets the criteria for extraordinary classification, an entity is required to segregate the extraordinary item from the results of ordinary operations and show the item separately in the income statement, net of tax, after income from continuing operations. The entity also is required to disclose applicable income taxes and either. This amendment will be effective for annual periods, and interim periods within those annual periods, beginning after December 15, 2015. The Board decided to permit early adoption provided that the guidance is applied from the beginning of the fiscal year of adoption.

The FASB has issued ASU No. 2015-03 “Simplifying the Presentation of Debt Issuance Costs”. The objective is to require that debt issuance costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts. The recognition and measurement guidance for debt issuance costs are not affected by the amendments in this update. For public business entities, the amendments in this update are effective for financial statements issued for fiscal years beginning after December 15, 2015, and interim periods within those fiscal years. For all other entities, the amendments in this update are effective for financial statements issued for fiscal years beginning after December 15, 2015, and interim periods within fiscal years beginning after December 15, 2016. Early adoption of the amendments in this update is permitted for financial statements that have not been previously issued.

The FASB has issued ASU No. 2015-05 “Intangibles-Goodwill and Other-Internal-Use Software”. The objective is to provide a guidance about whether a cloud computing arrangement includes a software license. If a cloud computing arrangement includes a software license, then the customer should account for the software license element of the arrangement consistent with the acquisition of other software licenses. If a cloud computing arrangement does not include a software license, the customer should account for the arrangement as a service contract. The amendment will not change GAAP for a customer accounting for service contracts. In addition, the guidance in this update supersedes paragraph 350-40-25-16. Consequently, all software licenses within the scope of Subtopic 350-40 will be accounted for consistent with other licenses of intangible assets. For public business entities, the FASB decided that the amendments will be effective for annual periods, including interim periods within those annual periods, beginning after December 15, 2015. For all other entities, the amendment will be effective for annual periods beginning after December 15, 2015, and interim periods in annual periods beginning after December 15, 2016. Early adoption is permitted for all entities.

Recently Issued Accounting Pronouncements

The FASB has issued ASU No. 2015-07 “Topic 820, Fair Value Measurement”, which permits a reporting entity, as a practical expedient, to measure the fair value of certain investments using the net asset value per share of the investment. The amendments in this update remove the requirement to categorize within the fair value hierarchy all investments for which fair value is measured using the net asset value per share practical expedient. The amendments also remove the requirement to make certain disclosures for all investments that are eligible to be measured at fair value using the net asset value per share practical expedient. Rather, those disclosures are limited to investments for which the entity has elected to measure the fair value using that practical expedient. The amendments in this update apply to reporting entities that elect to measure the fair value of an investment within the related scope by using the net asset value per share (or its equivalent) practical expedient.

| 20 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

2. Summary of Significant Accounting Policies – Continued

The FASB has issued No. 2015-10 “Technical Corrections and Improvements”, which aims to address feedback received from stakeholders on the Codification and make improvements to GAAP. The amendments in this update represent changes to clarify the Codification, correct unintended application of guidance, or make minor improvements to the Codification that are not expected to have a significant effect on current accounting practice or create a significant administrative cost to most entities. Some of the amendments will make the Codification easier to understand and apply by eliminating inconsistencies, providing needed clarifications, and improving the presentation of guidance in the Codification. The amendments in this update will apply to all reporting entities within the scope of the affected accounting guidance. The amendments in this update are effective for all entities for fiscal years, and interim periods within those fiscal years, beginning after December 15, 2015. Early adoption is permitted.

The FASB has issued No. 2015-11”Topic 330, Inventory”, which aims to simplify the measurement of inventory by changing the subsequent measurement guidance from the lower of cost or market to the lower of cost and net realizable value for inventory within the scope of this Update. The amendments in this update do not apply to inventory that is measured using last-in, first-out (LIFO) or the retail inventory method. The amendments apply to all other inventory, which includes inventory that is measured using first-in, first-out (FIFO) or average cost. An entity should measure inventory within the scope of this Update at the lower of cost and net realizable value. Subsequent measurement is unchanged for inventory measured using LIFO or the retail inventory method. For public business entities, the amendments in this update are effective for fiscal years beginning after December 15, 2016, including interim periods within those fiscal years. For all other entities, the amendments in this update are effective for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017.

The FASB has issued No. 2015-14”Topic 606, Revenue from Contracts with Customers”, which aims to respond to stakeholders’ requests to defer the effective date of the guidance in Update 2014-09 and to consider feedback received through extensive outreach with preparers, practitioners, and users of financial statements. The amendments in this update defer the effective date of Update 2014-09 for all entities by one year. Public business entities, certain not-for-profit entities, and certain employee benefit plans should apply the guidance in Update 2014-09 to annual reporting periods beginning after December 15, 2017, including interim reporting periods within that reporting period. Earlier application is permitted only as of annual reporting periods beginning after December 15, 2016, including interim reporting periods within that reporting period.

The FASB has issued No. 2015-15”Subtopic 835-30, Interest - Imputation of Interest”: Presentation and Subsequent Measurement of Debt Issuance Costs Associated with Line-of-Credit Arrangements - Amendments to SEC Paragraphs Pursuant to Staff Announcement at June 18, 2015 EITF Meeting. This amendment adds SEC paragraphs pursuant to the SEC Staff Announcement on June 18, 2015, Emerging Issues Task Force meeting about the presentation and subsequent measurement of debt issuance costs associated with line-of-credit arrangements.

Recently Issued Accounting Pronouncements

The FASB has issued No. 2015-16”Topic 805, Business Combinations”: Simplifying the Accounting for Measurement-Period Adjustments, which aims to identify, evaluate, and improve areas of GAAP for which cost and complexity can be reduced while maintaining or improving the usefulness of the information provided to users of financial statements. The amendments in this Update require that an acquirer recognize adjustments to provisional amounts that are identified during the measurement period in the reporting period in which the adjustment amounts are determined. The amendments in this update require that the acquirer record, in the same period’s financial statements, the effect on earnings of changes in depreciation, amortization, or other income effects, if any, as a result of the change to the provisional amounts, calculated as if the accounting had been completed at the acquisition date. The amendments in this update require an entity to present separately on the face of the income statement or disclose in the notes the portion of the amount recorded in current-period earnings by line item that would have been recorded in previous reporting periods if the adjustment to the provisional amounts had been recognized as of the acquisition date. For public business entities, the amendments in this update are effective for fiscal years beginning after December 15, 2015, including interim periods within those fiscal years. For all other entities, the amendments in this update are effective for fiscal years beginning after December 15, 2016, and interim periods within fiscal years beginning after December 15, 2017.

| 21 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

2. Summary of Significant Accounting Policies – Continued

The FASB has issued No. 2015-17”Topic 740, Income Taxes”: Balance Sheet Classification of Deferred Taxes, which aims to identify, evaluate, and improve areas of generally accepted accounting principles (GAAP) for which cost and complexity can be reduced while maintaining or improving the usefulness of the information provided to users of financial statements. The amendments in this update require that deferred tax liabilities and assets be classified as noncurrent in a classified statement of financial position. The amendments in this update apply to all entities that present a classified statement of financial position. The current requirement that deferred tax liabilities and assets of a tax-paying component of an entity be offset and presented as a single amount is not affected by the amendments in this Update. The amendments in this update will align the presentation of deferred income tax assets and liabilities with International Financial Reporting Standards (IFRS). For public business entities, the amendments in this Update are effective for financial statements issued for annual periods beginning after December 15, 2016, and interim periods within those annual periods. For all other entities, the amendments in this update are effective for financial statements issued for annual periods beginning after December 15, 2017, and interim periods within annual periods beginning after December 15, 2018. Earlier application is permitted for all entities as of the beginning of an interim or annual reporting period.

Other accounting standards that have been issued or proposed by the FASB or other standards-setting bodies that do not require adoption until a future date are not expected to have a material impact on the Company’s consolidated financial statements upon adoption

| 22 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

3. Going Concern

The Company has incurred negative operating cash flows during the six months ended September 30, 2016 and has an accumulated deficit at September 30, 2016 and has relied on the Company’s registered capital and issuance of convertible notes to fund operations. These conditions raise substantial doubt about the Company’s ability to continue as a going concern.

The financial statements have been prepared assuming that the Company will continue as a going concern and, accordingly, do not include any adjustments that might result from the outcome of this uncertainty. As of September 30, 2016, the Company had limited cash resources and management plans to continue its efforts to raise additional funds through debt or equity offerings which will be used to fund operations.

4. Property and Equipment, net

Property, plant and equipment, net consist of the following:

| September 30, 2016 | December 31, 2015 | |||||||

| Equipment | $ | 146,903 | $ | 148,305 | ||||

| Office equipment | 36,477 | 39,633 | ||||||

| Leasehold improvements | 11,773 | 8,634 | ||||||

| 195,153 | 196,572 | |||||||

| Less: Accumulated depreciation | (142,932 | ) | (127,902 | ) | ||||

| Property and equipment, net | $ | 52,221 | $ | 68,670 | ||||

During the nine months ended September 30, 2016 and 2015, depreciation expense was approximately $ 18,366 and $14,390, respectively.

| 23 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

5. Convertible Promissory Notes

Outstanding balances for the convertible promissory notes as of September 30, 2016 and December 31, 2015 are as follow:

| Lender | Date of Note | Maturity Date | Loan Amount | Interest Rate (p.a.) | Convertible Number of stock | September 30, 2016 | December 31, 2015 | |||||||||||||||||||

| Vantage Associates SA | April 15, 2011 | April 15, 2016 | $ | 150,000 | 5 | % | 600,000 | $ | 150,000 | $ | 150,000 | |||||||||||||||

| Empa Trading Ltd. | June 5, 2011 | June 5, 2016 | 100,000 | 5 | % | 400,000 | 100,000 | 100,000 | ||||||||||||||||||

| First Capital A.G. | July 14, 2011 | July 14, 2016 | 150,000 | 5 | % | 600,000 | 150,000 | 150,000 | ||||||||||||||||||

| First Capital A.G. | September 9, 2011 | September 9, 2016 | 200,000 | 5 | % | 800,000 | 200,000 | 200,000 | ||||||||||||||||||

| Vantage Associates SA | September 9, 2011 | September 9, 2016 | 200,000 | 5 | % | 800,000 | 200,000 | 200,000 | ||||||||||||||||||

| Vantage Associates SA | October 27, 2011 | October 27, 2016 | 50,000 | 5 | % | 200,000 | 50,000 | 50,000 | ||||||||||||||||||

| First Capital A.G. | December 1, 2011 | December 1, 2016 | 50,000 | 5 | % | 200,000 | 50,000 | 50,000 | ||||||||||||||||||

| First Capital A.G. | January 23, 2012 | January 23, 2017 | 50 000 | 5 | % | 200,000 | 50,000 | 50,000 | ||||||||||||||||||

| Magna Equities II, LLC (f/k/a Hanover Holdings I, LLC) | May 30, 2014 | May 30, 2016 | 150,000 | 8 | % | 10,632,951 | - | 350,000 | ||||||||||||||||||

| Vis Vires Group Inc. | June 1, 2015 | June 3, 2016 | 48,000 | 8 | % | 50,732,143 | - | 48,000 | ||||||||||||||||||

| Biz Wit Holdings Limited | May 6, 2016 | December 31, 2016 | 1,000,000 | 5 | % | 350,000,000 | 500,000 | - | ||||||||||||||||||

| Sino Secure International (Holdings) Limited | May 18, 2016 | December 31, 2016 | 700,000 | 5 | % | 700,000,000 | 700,000 | |||||||||||||||||||

| Lei Pan | May 18, 2016 | December 31, 2016 | 300,000 | 5 | % | 300,000,000 | 300,000 | |||||||||||||||||||

| $ | $ | 2,450,000 | $ | 1,348,000 | ||||||||||||||||||||||

| Less: | ||||||||||||||||||||||||||

| Debt discount | - | - | ||||||||||||||||||||||||

| from beneficial | - | - | ||||||||||||||||||||||||

| conversion feature | - | 354,394 | ||||||||||||||||||||||||

| 2,450,000 | 993,606 | |||||||||||||||||||||||||

| Less: | ||||||||||||||||||||||||||

| Current portion | 2,450,000 | 101 | ||||||||||||||||||||||||

| Non-current portion | $ | - | $ | 993,505 | ||||||||||||||||||||||

| 24 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

5. Convertible Promissory Notes- Continued

The debt discount was the beneficial conversion feature of the notes. It is being accreted as additional interest expense ratably over the term of the convertible notes.

Interest expenses for the three months ended September 30, 2016 and 2015 were $291 and $760 respectively. Interest expense for the nine months ended September 30, 2015 and 2014 was $123,404 and $1,128, respectively.

Amortization of the beneficial conversion feature for the nine months ended September 30, 2016 and 2015 were $nil and $12,435 respectively.

Except for the convertible promissory note of the $350,000 issued to Hanover Holdings I, LLC on May 30, 2014, and the $110,000 and $61,000 issued to KBM Worldwide, Inc. on August 14, 2014 and November 17, 2014 respectively, all the convertible promissory notes (the “Notes”) are convertible upon the occurrence of the following events:

(1) At any time, prior to the maturity date, the Company and the holder of the notes may mutually agree on a date to convert in whole or in part the notes into shares of common stock of the Company on the following terms: Holder of the note will be issued share units comprising of:

| (i) | one common share to be purchased at a price of $0.5, and | |

| (ii) | one warrant that is convertible into one common share at a price of $1.00, and expires two years from the date of the Exchange Transaction is completed, and | |

| (iii) | one warrant that is convertible into one common share at a price of $1.5, and expires three years from the date the Exchange Transaction is completed. |

(2) For the nine months ended September 30, 2016, prior to the maturity date, the Company and the holder of the notes may mutually agree on a date to convert in whole or in part the notes into shares of common stock of the Company on the following terms: Holder of the note will be issued share units comprising of:

| (i) | one common share to be purchased at a price of $0.001 |

(3) Unless earlier converted into common stock mentioned above, if within twelve months of the date hereof the Company completes a Qualified Financing, as defined by the respective convertible promissory notes, the holder agrees to exchange the notes simultaneously with the initial closing of such Qualified Financing as follows:

(a) In the event of a debt Qualified Financing (“Qualified Debt Financing”), the Holder may at its option exchange in whole or in part this Note for a promissory note (or other evidence of indebtedness) in the same form and with the same terms and conditions as those issued in such Qualified Debt Financing and in a principal amount equal to the then outstanding Debt.

(b) In the event of an equity Qualified Financing (“Qualified Equity Financing”), the Holder may at its option convert the Debt into shares of capital stock of the same class and series and with the same rights, preferences and privileges as those issued in such Qualified Equity Financing, at a price per share equal to the purchase price paid by investors in such Qualified Equity Financing.

| 25 |

| XCELMOBILITY INC. AND SUBSIDIARIES |

| NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS |

| (UNAUDITED) |

5. Convertible Promissory Notes – Continued

Convertible promissory note of $350,000 issued to Hanover Holdings I, LLC on May 30, 2014

On May 30, 2014, or the Closing Date, we entered into a securities purchase agreement dated as of the Closing Date (the “Purchase Agreement”) with Hanover Holdings I, LLC, a New York limited liability company (“Hanover”). Pursuant to the terms of the Purchase Agreement, Hanover purchased from us on the Closing Date (i) a senior convertible note with an initial principal amount of $350,000 (the “Convertible Note”) and (ii) a warrant to acquire up 3,716,091 shares of our common stock (the “Warrant”), for a total purchase price of $250,000. The Convertible Note was issued with an original issue discount of approximately 28.57%.

$40,000 of the outstanding principal amount of the Convertible Note (together with any accrued and unpaid interest with respect to such portion of the principal amount) shall be automatically extinguished (without any cash payment by us) if (i) we have properly filed a registration statement with the Securities and Exchange Commission, or SEC, on or prior to July 14, 2014, or the Filing Deadline, covering the resale by Hanover of the shares of common Stock issued or issuable upon conversion of the Convertible Note and (ii) no event of default or an event that with the passage of time or giving of notice would constitute an event of default has occurred on or prior to such date. Moreover, $60,000 of the outstanding principal amount of the Convertible Note (together with any accrued and unpaid interest with respect to such portion of the principal amount) shall be automatically extinguished (without any cash payment by us) if (i) the registration statement has been declared effective by the SEC on or prior to the earlier of (i) the 120th calendar day after the Closing Date and (ii) the fifth business day after the date we are notified by the SEC that such registration statement will not be reviewed or will not be subject to further review (the “Effectiveness Deadline”), and the prospectus contained therein is available for use by Hanover for the resale by Hanover of the shares of common stock issued or issuable upon conversion of the Convertible Note and (ii) no event of default or an event that with the passage of time or giving of notice would constitute an event of default has occurred on or prior to such date.