Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

Commission File Number: 001-34354

Altisource Portfolio Solutions S.A.

(Exact name of registrant as specified in its charter)

| Luxembourg | Not Applicable | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

291, Route d’Arlon

L-1150 Luxembourg

Grand Duchy of Luxembourg

(352) 24 69 79 00

(Address and telephone number, including area code, of registrant’s principal executive offices)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Name of each exchange on which registered | |

| Common Stock, $1.00 par value | NASDAQ Global Select Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulations S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein and will not be contained, to the best of the Registrant’s knowledge, in the definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer |

¨ |

Accelerated filer |

x | |||

| Non-accelerated filer |

¨ (Do not check if a smaller reporting company) |

Smaller reporting company |

¨ | |||

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ¨ No x

The aggregate market value of the voting stock held by nonaffiliates of the registrant as of June 30, 2011 was $662,418,290 based on the closing share price as quoted on the NASDAQ Global Market on that day and the assumption that all directors and executive officers of the Company, and their families, are affiliates. This determination of affiliate status is not necessarily a conclusive determination for any other purpose.

As of January 31, 2012, there were 23,405,123 outstanding shares of the Registrant’s shares of beneficial interest (excluding 2,007,625 shares held as treasury stock).

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement to be filed subsequent to the date hereof with the Commission pursuant to Regulation 14A in connection with the registrant’s 2011 Annual Meeting of Stockholders are incorporated by reference into Part III of this Report. Such Definitive Proxy Statement will be filed with the Securities and Exchange Commission not later than 120 days after the conclusion of the registrant’s fiscal year ended December 31, 2011.

Table of Contents

Table of Contents

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and certain information incorporated herein by reference contain forward-looking statements within the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. These statements may relate to, among other things, future events or our future performance or financial condition. Words such as “anticipate”, “intend”, “expect”, “may”, “could”, “should”, “would”, “plan”, “estimate”, “seek”, “believe” and similar expressions are intended to identify such forward-looking statements. Forward-looking statements are not guarantees of future performance and involve a number of assumptions, risks and uncertainties that could cause actual results to differ materially. Important factors that could cause actual results to differ materially from those suggested by the forward-looking statements include, but are not limited to, the risks discussed in Item 1A of Part 1 “Risk Factors”. We caution you not to place undue reliance on these forward-looking statements which reflect our view only as of the date of this report. We are under no obligation (and expressly disclaim any obligation) to update or alter any forward-looking statements contained herein to reflect any change in our expectations with regard thereto or change in events, conditions or circumstances on which any such statement is based.

Except as otherwise indicated or unless the context requires otherwise, “Altisource™,” “we,” “us,” “our” and the “Company” refer to Altisource Portfolio Solutions S.A., a Luxembourg société anonyme, or public limited company, and its wholly-owned subsidiaries.

| ITEM 1. | BUSINESS |

The Company

Altisource Portfolio Solutions S.A., together with its subsidiaries, is a provider of services focused on high value, technology-enabled, knowledge-based functions principally related to real estate and mortgage portfolio management, asset recovery and customer relationship management. We enable our clients to achieve their goals by leveraging our process management, innovative technology, econometrics and consumer behavior practice and high-quality, cost effective global human resources.

We are publicly traded on the NASDAQ Global Select Market under the symbol ASPS. We were incorporated under the laws of Luxembourg on November 4, 1999 as Ocwen Luxembourg S.à r.l., renamed Altisource Portfolio Solutions S.à r.l. on May 12, 2009 and converted into Altisource Portfolio Solutions S.A. on June 5, 2009. On August 10, 2009, we became a stand-alone public company in connection with our separation from Ocwen Financial Corporation (“Ocwen®”) (the “Separation”). Prior to the date of Separation, our businesses were wholly-owned subsidiaries of Ocwen.

2011 Achievements

During 2011, we achieved several milestones:

| • | Recognized revenue of $423.7 million, representing a 41% increase over the year-ended December 31, 2010. |

| • | Recognized Service Revenue of $334.8 million representing a 36% increase over the year-ended December 31, 2010. |

| • | Recognized diluted earnings per share of $2.77 representing a 47% increase over the year-ended December 31, 2010. |

| • | Generated $111.6 million of operating cash flow representing on average $0.33 for every dollar of Service Revenue generated. |

3

Table of Contents

In addition, we sought to strategically deploy cash generated during 2011 to either facilitate long-term growth or return such cash to shareholders:

| • | Returned $61.1 million to shareholders through the repurchase of 1.6 million shares under the stock repurchase program at an average price of $37.57 per share. |

| • | Expended $16.4 million on capital projects to facilitate the growth of operations, primarily as a result of the continued growth of the residential loan servicing portfolio of Ocwen, our largest customer. |

| • | Invested $15.0 million in Correspondent One S.A. (“Correspondent™”), an equity method investment. Correspondent One facilitates the purchase of closed conforming and government guaranteed residential mortgages from approved mortgage bankers. Correspondent One provides members of the Lenders One Mortgage Cooperative (“Lenders One®”), a national alliance of independent mortgage bankers which we manage, additional avenues to sell loans beyond Lenders One’s preferred investor arrangements and the members’ own network of loan buyers. |

| • | Acquired Springhouse, LLC (“Springhouse™”) an appraisal management company that utilizes a nationwide panel of appraisers to provide appraisals principally to mortgage originators and real estate managers. |

| • | Acquired the assembled workforce of a sub-contractor (“Tracmail”) in India that performs asset recovery services. |

Reportable Segments

We classify our businesses into three reportable segments:

| • | Mortgage Services consists of mortgage portfolio management services that span the mortgage lifecycle from origination through real estate owned (REO) asset management and sale; |

| • | Financial Services principally consists of unsecured asset recovery and customer relationship management; and |

| • | Technology Services consists of modular, comprehensive integrated technological solutions for loan servicing, vendor management and invoice presentment and payment as well as providing infrastructure support. |

In addition, our Corporate Items and Eliminations segment includes eliminations of transactions between the reporting segments and also includes costs recognized by us related to corporate support functions such as executive, finance, legal, human resources, vendor management and six sigma.

We conduct portions of our operations in all 50 states and in three countries outside of the United States.

Mortgage Services

Our Mortgage Services segment continues to be the primary driver of growth. This segment generates revenue principally by providing services that loan originators and loan servicers typically outsource to third parties. Our services are provided using our national platform and span the lifecycle of a mortgage loan. Our services are primarily centered on our relationship with Ocwen, but we also have longstanding relationships with some of the leading capital market firms, commercial banks, hedge funds, insurance companies and lending institutions.

Our services typically begin with a default management referral from a customer which results in a pre-foreclosure title search, property inspection services and non-legal back-office support services in connection with managing foreclosures. Upon receipt of an asset management referral after a property has been foreclosed, we provide REO preservation, REO asset management, REO valuation, REO brokerage, REO closing and REO title insurance services.

4

Table of Contents

While our initial focus has principally been related to default services, we are also committed to developing our services to support mortgage originators and correspondent lenders. In February 2010, we acquired the Mortgage Partnership of America, L.L.C. (“MPA™”). MPA is the manager of a national alliance of community mortgage bankers and correspondent lenders which does business as Lenders One. We believe MPA’s 210 plus member companies originated approximately 8% of the total U.S. residential mortgage originations in 2011. Further, in 2011, we co-formed Correspondent One which once fully operational will provide members of Lenders One additional avenues to sell their loans beyond Lenders One’s preferred investor arrangements and the members’ own network of loan buyers. We anticipate this will result in improved profitability for the members and facilitate the sale of our services to the members.

In 2011, we reorganized our reporting structure within this segment in that certain services originally part of Component Services and Other are now classified as part of Customer Relationship Management in our Financial Services segment. Following this change, Component Service and Other was renamed Origination Management Services. Prior periods have been recast to conform to the current year presentation.

The table below presents revenues for our Mortgage Services segment for the past three annual periods:

| For the Years Ended December 31, | ||||||||||||

| (in thousands) |

2011 | 2010 | 2009 | |||||||||

| Revenue: |

||||||||||||

| Asset Management Services |

$ | 141,486 | $ | 78,999 | $ | 30,464 | ||||||

| Origination Management Services |

25,566 | 22,835 | 3,899 | |||||||||

| Residential Property Valuation |

51,785 | 33,502 | 26,800 | |||||||||

| Closing and Insurance Services |

56,612 | 28,056 | 17,444 | |||||||||

| Default Management Services |

36,472 | 23,741 | 9,194 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total Revenue |

$ | 311,921 | $ | 187,133 | $ | 87,801 | ||||||

|

|

|

|

|

|

|

|||||||

| Transactions with Related Parties: |

||||||||||||

| Asset Management Services |

$ | 136,685 | $ | 78,999 | $ | 30,464 | ||||||

| Residential Property Valuation |

48,734 | 32,525 | 25,762 | |||||||||

| Closing and Insurance Services |

26,733 | 17,379 | 13,496 | |||||||||

| Default Management Services |

11,032 | 6,752 | 4,367 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

$ | 223,184 | $ | 135,655 | $ | 74,089 | ||||||

|

|

|

|

|

|

|

|||||||

| Reimbursable Expenses (included in Revenue)(1): |

||||||||||||

| Asset Management Services |

$ | 76,511 | $ | 41,920 | $ | 14,308 | ||||||

| Default Management Services |

3,497 | 2,328 | 1,769 | |||||||||

| Closing and Insurance Services |

116 | 302 | — | |||||||||

|

|

|

|

|

|

|

|||||||

| Total |

$ | 80,124 | $ | 44,550 | $ | 16,077 | ||||||

|

|

|

|

|

|

|

|||||||

| (1) | Reimbursable Expenses include costs we incur that we pass through to our customers without any mark-up. |

Asset Management Services. Principally includes property preservation, property inspection, REO asset management and REO brokerage. Asset Management Services has been the largest contributor to Service Revenue growth year to date which reflects an increase in the number of REO sold, the number of REO for which we provide property preservation services and an increase in pre-foreclosure inspection services.

Origination Management Services. Principally includes MPA, our contract underwriting business and our origination fulfillment operations currently under development.

5

Table of Contents

Residential Property Valuation Services. We provide our customers with traditional appraisal products through our licensed appraisal management company, working with our network of experienced appraisers and our exclusive ordering system. Customers may also order alternative valuation products through our system and network of real estate professionals. We also offer customers the ability to outsource all or part of their appraisal and valuation management oversight functions to us.

Closing and Insurance Services. We provide an array of closing services (e.g., document preparation) and title services (e.g., pre-foreclosure title search, title insurance) applicable to the residential foreclosure process and the sale of residential property. During 2011, we focused on increasing our referral capture rate in our operational states and rolling out insured title services nationwide, similar to what we accomplished with our title search and asset management businesses in 2010.

Default Management Services. We provide non-legal back-office support for foreclosure, bankruptcy and eviction attorneys as well as foreclosure trustee services. We do not execute or notarize foreclosure affidavits of debt or lost note affidavits.

Financial Services

Our Financial Services segment provides collection and customer relationship management services primarily to debt originators (e.g., credit card, auto loans, retail credit, mortgages) and the utility and insurance industries. Our leadership team for this segment is focused on disciplined floor management, delivering more services over our global delivery platform, expanding our quality and analytical initiatives and investing in new technology. Our global delivery platform consists of highly trained specialists in various geographic regions.

The following table represents revenues for our Financial Services segment for the past three annual periods:

| For the Years Ended December 31, | ||||||||||||

| (in thousands) |

2011 | 2010 | 2009 | |||||||||

| Revenue: |

||||||||||||

| Asset Recovery Management |

$ | 39,321 | $ | 48,050 | $ | 51,019 | ||||||

| Customer Relationship Management |

31,860 | 29,567 | 28,712 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total Revenue |

$ | 71,181 | $ | 77,617 | $ | 79,731 | ||||||

|

|

|

|

|

|

|

|||||||

| Transactions with Related Parties: |

||||||||||||

| Asset Recovery Management |

$ | 266 | $ | 166 | $ | 98 | ||||||

|

|

|

|

|

|

|

|||||||

| $ | 266 | $ | 166 | $ | 98 | |||||||

|

|

|

|

|

|

|

|||||||

| Reimbursable Expenses (included in Revenue)(1): |

||||||||||||

| Asset Recovery Management |

$ | 1,950 | $ | 2,899 | $ | — | ||||||

|

|

|

|

|

|

|

|||||||

| (1) | Reimbursable Expenses include costs we incur that we pass through to our customers without any mark-up. |

Asset Recovery Management. We provide post-charge-off consumer debt collection (e.g., credit cards, auto loans, second mortgages) on a contingent fee basis where we are paid a percentage of the recovered debt.

Customer Relationship Management. We provide customer care (e.g., connects/disconnects for utilities) and early stage collections services for which we are generally compensated on a per-call, per-person or per-minute basis. In addition, we provide insurance and claims processing, call center services and analytical support for which we are paid based upon the number of employees utilized.

6

Table of Contents

Technology Services

Technology Services comprises our REALSuite™ of applications as well as our IT infrastructure services. We only provide our IT infrastructure services to Ocwen and ourselves. In 2011, we began to report our Consumer Analytics group within Technology Services. Previously this group was included in Corporate.

Effective January 1, 2011, we modified our pricing for IT Infrastructure Services within our Technology Services segment from a model based principally on a rate card to a fully loaded costs plus mark-up methodology. This model applies to the infrastructure amounts charged to Ocwen as well as internal allocations of infrastructure costs.

Our Technology Services segment is primarily focused on supporting the growth of Mortgage Services and Ocwen. In addition, Technology Services is assisting in the cost reduction and quality initiatives on-going within the Financial Services segment.

The following table presents revenues for our Technology Services segment for the past three annual periods:

| For the Years Ended December 31, | ||||||||||||

| (in thousands) |

2011 | 2010 | 2009 | |||||||||

| Revenue: |

||||||||||||

| REALSuite |

$ | 34,926 | $ | 31,214 | $ | 25,784 | ||||||

| IT Infrastructure Services |

21,168 | 20,799 | 21,669 | |||||||||

|

|

|

|

|

|

|

|||||||

| Total Revenue |

$ | 56,094 | $ | 52,013 | $ | 47,453 | ||||||

|

|

|

|

|

|

|

|||||||

| Transactions with Related Parties: |

||||||||||||

| REALSuite |

$ | 13,253 | $ | 11,226 | $ | 9,899 | ||||||

| IT Infrastructure Services |

8,559 | 7,941 | 10,811 | |||||||||

|

|

|

|

|

|

|

|||||||

| $ | 21,812 | $ | 19,167 | $ | 20,710 | |||||||

|

|

|

|

|

|

|

|||||||

The REALSuite platform provides a fully integrated set of applications and technologies that manage the end-to-end lifecycle for residential and commercial servicing including the automated management and payment of a distributed network of vendors. A brief description of key components of the REALSuite is described below:

REALServicing® — an enterprise residential mortgage loan servicing product that offers an efficient and effective platform for loan servicing including default administration. This technology solution features automated workflows, a dialogue engine and robust reporting capabilities. The solution spans the loan servicing cycle from loan boarding to satisfaction including all collections, payment processing and reporting. We also offer REALSynergy®, an enterprise commercial loan servicing system.

REALTrans® — a patented electronic business-to-business exchange that automates and simplifies the ordering, tracking and fulfilling of vendor provided services principally related to mortgages. This technology solution, whether web-based or integrated into a servicing system, connects multiple service providers through a single platform and forms an efficient method for managing a large scale network of vendors.

REALRemit® — a patented electronic invoicing and payment system that provides vendors with the ability to submit invoices electronically for payment and to have invoice payments deposited directly to their respective bank accounts.

7

Table of Contents

IT Infrastructure Services. We provide a full suite of IT services (e.g., desktop management, application support, network management, telephony, data center management, disaster recovery, helpdesk and infrastructure security) for which we perform remote management of IT functions internally and for Ocwen.

Corporate Items and Eliminations

Corporate Items and Eliminations includes eliminations of transactions between the reporting segments and this segment also includes costs recognized by us related to corporate support functions such as executive, finance, legal, human resources, vendor management and six sigma. Prior to the date of Separation, this segment included expenditures recognized by us related to the Separation.

Customers

We provide services to some of the most respected organizations in their industries, including one of the U.S.’ largest sub-prime servicers, utility companies, commercial banks, servicers, investors, mortgage bankers, financial service companies and hedge funds across the U.S.

Our three largest customers in 2011 accounted for 71% of our total revenue. Our largest customer is Ocwen which accounted for 58% of Altisource’s total revenue in 2011. During 2011, Ocwen successfully grew its residential loan servicing portfolio primarily through acquisitions to $102.2 billion in unpaid principal balances as of December 31, 2011. In October 2011, Ocwen announced it had entered into a definitive agreement to acquire a portfolio from a subsidiary of Morgan Stanley Mortgage Capital Holdings, LLC which would result in a net gain of approximately $16.0 billion in unpaid principal balance (the “Saxon” portfolio). In November 2011, Ocwen entered into an agreement with JPMorgan Chase, N.A. (“JPMCB”) to acquire a portfolio of $15.0 billion in unpaid principal balance. Both of these transactions are expected to board in the first half of 2012. Additionally, Ocwen continues to evaluate additional servicing portfolio acquisitions.

Following the date of Separation, Ocwen is contractually obligated to purchase certain Mortgage Services and Technology Services from us under service agreements. These agreements extend until August 2017 subject to termination under certain provisions. Ocwen is not restricted from redeveloping these services. We settle amounts with Ocwen on a daily, weekly or monthly basis based upon the nature of the services and when the service is completed.

With respect to Ocwen, related party revenues consist of revenues earned directly from Ocwen and revenues earned from the loans serviced by Ocwen when Ocwen determines the service provider. We earn additional revenue on the loan portfolios serviced by Ocwen that are not considered related party revenues as Ocwen does not have the ability to decide the service provider. As a percentage of each of our segment revenues and as a percentage of consolidated revenues, related party revenue was as follows for the year ended December 31:

| For the Years Ended December 31, | ||||||||||||

| 2011 | 2010 | 2009 | ||||||||||

| Mortgage Services |

72 | % | 73 | % | 84 | % | ||||||

| Technology Services |

39 | 37 | 44 | |||||||||

| Financial Services |

< 1 | < 1 | < 1 | |||||||||

| Consolidated Revenues |

58 | % | 51 | % | 47 | % | ||||||

We record revenues we earn from Ocwen under the various long-term servicing contracts at rates we believe to be market rates as they are consistent with one or more of the following: the fees we charge to other customers for comparable services; the rates Ocwen pays to other service providers; fees commensurate with market surveys prepared by unaffiliated firms; and prices charged by our competitors.

8

Table of Contents

Sales and Marketing

We have experienced sales personnel and relationship managers with subject matter expertise. These individuals maintain relationships throughout the industry sectors we serve and play an important role in generating new client leads as well as identifying opportunities to expand our services with existing clients. Additional leads are also generated through request for proposal processes from key industry participants. Our sales team works collaboratively and is compensated principally with a base salary and commission for sales generated.

From a sales and marketing perspective, our primary focus is supporting the growth of our largest customer, Ocwen, expanding relationships with existing MPA members and targeting new customers that could have a material positive impact on our results of operations. Given the highly concentrated nature of the industries that we serve, the time and effort spent in expanding relationships or winning new relationships is significant.

Intellectual Property

We rely on a combination of contractual restrictions, internal security practices, patents, trademarks, copyrights, trade secrets and other intellectual property to establish and protect our software, technology and expertise. We also own or, as necessary and appropriate, have obtained licenses from third parties to intellectual property relating to our services, processes and business. These intellectual property rights are important factors in the success of our businesses.

As of December 31, 2011, we have been awarded one patent that expires in 2023 and three patents that expire in 2024. The U.S. Patent Office has also notified us of the allowance of a pending U.S. Patent Application. In addition, Altisource has registered trademarks or recently filed applications for registration of trademarks in a number of countries or groups of countries including the United States, the European Community, India and in eleven other countries or groups of countries. These trademarks generally can be renewed indefinitely.

We actively protect our rights and intend to continue our policy of taking all measures we deem reasonable and necessary to develop and protect our patents, copyrights, trade secrets, trademarks and other intellectual property rights.

Industry and Competition

The industry verticals in which we engage are highly competitive and generally consist of a few national vendors as well as a large number of regional or in-house providers resulting in a fragmented market with disparate service offerings. From an overall perspective, we compete with the global business process outsourcing firms. Our Mortgage Services segment competes with national and regional third party service providers and in-house servicing operations of large mortgage lenders and servicers. Our Financial Services segment competes with other large receivables management companies as well as a fragmented group of smaller companies and law firms focused on collections. Our Technology Services segment competes with data processing and software development companies.

Given the diverse nature of services that we and our competitors offer, we cannot determine our position in the market with certainty, but we believe that we represent only a small portion of very large sized markets. Given our size, some of our competitors may offer more diversified services, operate in broader geographic markets or have greater financial resources than we do. In addition, some of our larger customers retain multiple providers and continuously evaluate our performance against our competitors.

Competitive factors in our Mortgage Services business include the quality and timeliness of our services, the size and competence of our network of vendors and the breadth of the services we offer. For Financial Services, competitive factors include the ability to achieve a collection rate comparable to our competitors; the quality and personal nature of the service; the consistency and professionalism of the service and the recruitment, training and retention of our workforce. Competitive factors in our Technology Services business include the quality of the technology-based application or service; application features and functions; ease of delivery and integration; our ability to maintain, enhance and support the applications or services and the cost of obtaining, maintaining and enforcing of our patents.

9

Table of Contents

Employees

As of December 31, 2011, we had the following number of employees:

| United States | India | Other | Consolidated Altisource |

|||||||||||||

| Mortgage Services |

228 | 2,853 | 4 | 3,085 | ||||||||||||

| Financial Services |

593 | 1,678 | — | 2,271 | ||||||||||||

| Technology Services |

47 | 552 | — | 599 | ||||||||||||

| Corporate |

46 | 341 | 65 | 452 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Employees |

914 | 5,424 | 69 | 6,407 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

We have not experienced any work stoppages, and we consider our relations with employees to be good. We believe that our future success will depend, in part, on our ability to continue to attract, hire and retain skilled and experienced personnel.

Seasonality

Our revenues are seasonal. More specifically, Financial Services revenue tends to be higher in the first quarter, as borrowers may utilize tax refunds and bonuses to pay debts, and generally declines throughout the rest of the year. Mortgage Services revenue is impacted by REO sales which tend to be at their lowest level during fall and winter months and highest during spring and summer months.

Government Regulation

Our businesses are subject to extensive laws and regulations by federal, state and local governmental authorities including the Federal Trade Commission, the state agencies that license our mortgage services, collection entities and the SEC. We also must comply with a number of federal, state and local consumer protection laws including, among others, the Gramm-Leach-Bliley Act, the Fair Debt Collection Practices Act, the Real Estate Settlement Procedures Act (“RESPA”), the Truth in Lending Act (“TILA”), the Fair Credit Reporting Act, the Homeowners Protection Act and the SAFE Act. These requirements can and do change as statutes and regulations are enacted, promulgated or amended. One such recently enacted regulation is the Dodd-Frank Wall Street Reform and Consumer Protection Act (“Dodd-Frank Act”). The Dodd-Frank Act is extensive and includes reform of the regulation and supervision of financial institutions, as well as the regulation of derivatives, capital market activities and consumer financial services. Included in the Dodd Frank Act, among other things, is the creation of the Consumer Financial Protection Bureau, a new federal entity responsible for regulating consumer financial services and products. Title XIV of the Dodd-Frank Act contains the Mortgage Reform and Anti-Predatory Lending Act (“Mortgage Act”). The Mortgage Act imposes a number of additional requirements on lenders and servicers of residential mortgage loans by amending and expanding certain existing regulations. In some cases, penalties for noncompliance are significantly increased and could lead to settlements or consent orders on us or our customers that may curtail or restrict the business as it is currently conducted. The Mortgage Act generally requires that implementing regulations be issued before many of its provisions are effective. Therefore, many of these provisions in the Mortgage Act will not be effective until 2013 or early 2014.

We are subject to certain federal, state and local consumer protection provisions. We are also subject to licensing and regulation as a mortgage service provider and/or debt collector in a number of states. We are subject to audits and examinations that are conducted by the states. Our employees may be required to be licensed by various state commissions for the particular type of service delivered and to participate in regular continuing education programs. From time to time, we receive requests from state and other agencies for records, documents and information

10

Table of Contents

regarding our policies, procedures and practices regarding our mortgage services and debt collection business activities. We are also subject to the requirements of the Foreign Corrupt Practices Act and comparable foreign laws, due to our activities in foreign jurisdictions. We incur ongoing costs to comply with governmental laws and regulations.

Available Information

We file Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other information with the Securities and Exchange Commission (“SEC”). These filings are available to the public over the Internet at the SEC’s web site at http://www.sec.gov. You may also read and copy any document we file at the SEC’s public reference room located at 100 F Street, N.E., Washington, DC 20549. Please call the SEC at 1 800-SEC-0330 for further information on the public reference room.

Our principal Internet address is www.altisource.com and we encourage investors to use it as a way of easily finding information about us. We promptly make available on this website, free of charge, the reports that we file or furnish with the SEC, corporate governance information (including our Code of Business Conduct and Ethics) and select press releases. The contents of our website are available for informational purposes only and shall not be deemed incorporated by reference in this report.

| ITEM 1A. | RISK FACTORS |

The following risk factors and other information included in this Annual Report on Form 10-K should be carefully considered. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we presently deem less significant may also impair our business operations. If any of the following risks actually occur, our business, operating results and financial condition could be materially adversely affected.

Risks Related to Our Business and Industry

Our continuing relationship with Ocwen may inhibit our ability to obtain and retain other customers that compete with Ocwen.

As of December 31, 2011, our chairman owns or controls more than 13% of Ocwen’s common stock and 23% of our common stock. We derived 58% of our revenues in 2011 from Ocwen or the loan servicing portfolio managed by Ocwen. Given this close and continuing relationship with Ocwen, we may encounter difficulties in obtaining and retaining other customers who compete with Ocwen. Should these and other potential customers continue to view Altisource as part of Ocwen or as too closely related to or dependent upon Ocwen, they may be unwilling to utilize our services, and our growth could be inhibited as a result.

We are dependent on certain key customer relationships, the loss of or their inability to pay could affect our business and results of operations.

We currently generate approximately 58% of our revenue from Ocwen. Following the Separation, Ocwen is contractually obligated to purchase certain services from our Mortgage Services and Technology Services segments under service agreements that extend for eight years from the date of Separation subject to termination under certain provisions.

While no other individual client represents more than 10% of our consolidated revenues, we are exposed to customer concentration. Most of our customers are not contractually obligated to continue to use our services at historical levels or at all. The loss of any of these key customers or their failure to pay us could reduce our revenues and adversely affect results of operations.

11

Table of Contents

Our business is subject to substantial competition.

The markets for our services are very competitive. Our competitors vary in size and in the scope and breadth of the services they offer. We compete for existing and new customers against both third parties and the in-house capabilities of our customers. Some of our competitors have substantial resources and some have widely used technology platforms that they seek to use as a competitive advantage to drive sales of other products and services. In addition, we expect that the markets in which we compete will continue to attract new competitors and new technologies. These new technologies may render our existing technologies obsolete, resulting in operating inefficiencies and increased competitive pressure. There can be no assurance that we will be able to compete successfully against current or future competitors or that competitive pressures we face in the markets in which we operate will not materially adversely affect our business, financial condition and results of operations.

Our intellectual property rights are valuable and any inability to protect them could reduce the value of our services.

Our patents, trademarks, trade secrets, copyrights and other intellectual property rights are important assets. The efforts we have taken to protect these proprietary rights may not be sufficient or effective. The unauthorized use of our intellectual property or significant impairment of our intellectual property rights could harm our business, make it more expensive to do business or hurt our ability to compete. Protecting our intellectual property rights is costly and time consuming.

Although we seek to obtain patent protection for our innovations, it is possible we may not be able to protect some of these innovations. Changes in patent law, such as changes in the law regarding patentable subject matter, can also impact our ability to obtain patent protection for our innovations. In addition, given the costs of obtaining patent protection, we may choose not to protect certain innovations that later turn out to be important. Furthermore, there is always the possibility, despite our efforts, that the scope of the protection gained will be insufficient or that an issued patent may be deemed invalid or unenforceable.

Technology failures could damage our business operations and increase our costs.

System disruptions or failures may interrupt or delay our ability to provide services to our customers. Any sustained and repeated disruptions in these services may have an adverse impact on our results of operations.

The secure transmission of confidential information over the Internet is essential to maintaining consumer confidence. Security breaches and acts of vandalism could result in a compromise or breach of the technology that we use to protect our customers’ personal information and transaction data and could result in the assessment of penalties. Furthermore, Congress or individual states could enact new laws regulating electronic commerce that could adversely affect us and our results of operations.

Our technology solutions have a long sale cycle and are subject to development and obsolescence risks.

Many of our services in the Technology Services segment are based on sophisticated software and computing systems with long sales cycles. We may encounter delays when developing new technology solutions and services. We may experience difficulties in installing or integrating our technologies on platforms used by our customers. Further, defects in our technology solutions, errors or delays in the processing of electronic transactions, or other difficulties could result in interruption of business operations, delay in market acceptance, additional development and remediation costs, loss of customers, negative publicity or exposure to liability claims. Any one or more of the foregoing occurrences could have a material adverse effect on our business, financial condition or results of operations.

Our business is subject to extensive regulation, and failure to comply with existing or new regulations may adversely impact us.

Our business is subject to extensive regulation by federal, state and local governmental authorities including the Federal Trade Commission, the state agencies that license certain of our mortgage related services and collection services and the SEC. We also must comply with a number of federal, state and local consumer protection laws including, among others, the Gramm-Leach-Bliley Act, the Fair Debt Collection Practices Act, the Real Estate

12

Table of Contents

Settlement Procedures Act, the Truth in Lending Act, the Fair Credit Reporting Act, the Homeowners Protection Act, the SAFE Act, the Mortgage Act and the Foreign Corrupt Practices Act. These requirements can and do change as statutes and regulations are enacted, promulgated or amended.

The ongoing economic uncertainty and troubled housing market have resulted in increased regulatory scrutiny of all participants involved in the mortgage industry. This scrutiny has included federal and state governmental agency review of all aspects of the mortgage lending and servicing industries, including an increased legislative and regulatory focus on consumer protection practices. One such recently enacted regulation is the Dodd-Frank Act (see further description in Item 1. Business, Government Regulation section above). In some cases, penalties for noncompliance are significantly increased and could lead to settlements or consent orders on us or our customers that may curtail or restrict the business as it is currently conducted.

We are subject to additional certain federal, state and local consumer protection provisions. We also are subject to licensing and regulation as a mortgage services provider, valuation provider, appraisal management company, asset manager, property manager, title insurance agency, real estate broker and/or debt collector in a number of states. We are subject to audits and examinations that are conducted by the states in which we do business. Our employees and subsidiaries may be required to be licensed by various state commissions for the particular type of service sold and to participate in regular continuing education programs. From time to time, we receive requests from state and other agencies for records, documents and information regarding our policies, procedures and practices for our mortgage services and debt collection business activities. We incur significant ongoing costs to comply with governmental regulations.

The volume of new or modified laws and regulations has increased in recent years and, in addition, some individual municipalities have begun to enact laws that restrict mortgage services activities. If our regulators impose new or more restrictive requirements, we may incur significant additional costs to comply with such requirements which could further adversely affect our results of operations or financial condition. In addition, our failure to comply with these laws and regulations can possibly lead to civil and criminal liability, loss of licensure, damage to our reputation in the industry, fines and penalties, and litigation, including class action lawsuits or administrative enforcement actions. Any of these outcomes could harm our results of operations or financial condition.

If we fail to comply with privacy regulations imposed on providers of services to financial institutions, our business could be harmed.

As a provider of services to financial institutions, we are bound by the same limitations on disclosure of the information we receive from their customers that apply to the financial institutions themselves. If we fail to comply with these regulations, we could be exposed to lawsuits or to governmental proceedings, our customer relationships and reputation could be harmed and we could be inhibited in our ability to obtain new customers. In addition, the adoption of more restrictive privacy laws or rules in the future on the federal or state level could have an adverse impact on us.

We may be subject to claims of legal violations or wrongful conduct which may cause us to pay unexpected litigation costs or damages or modify our products or processes.

From time to time, we may be subject to costly and time-consuming legal proceedings that claim legal violations or wrongful conduct. These lawsuits may involve clients, vendors, competitors and / or other large groups of plaintiffs and, if resulting in findings of violations, could result in substantial damages. Alternatively, we may be forced to settle some claims out of court and change existing company practices, services and processes that are currently revenue generating. This could lead to unexpected costs or a loss of revenue.

If financial institutions at which we hold escrow funds fail, it could have a material adverse impact on our company.

We hold customers’ assets in escrow at various financial institutions, pending completion of certain real estate and debt collection activities. These amounts are held in escrow for limited periods of time, generally consisting of a few days. To the extent these assets are not co-mingled with our fees and are maintained in segregated bank accounts they are generally not included in the accompanying Consolidated Balance Sheets. Failure of one or more of these financial institutions may lead us to become liable for the funds owed to third parties, and there is no guarantee that we would recover the funds deposited, whether through Federal Deposit Insurance Corporation coverage, private insurance or otherwise.

13

Table of Contents

Risks Related to our Growth Strategy

Our ability to grow is affected by our ability to retain and expand our existing client relationships and our ability to attract new customers.

Our ability to grow is affected by our ability to retain and expand our existing client relationships and our ability to attract new customers. Our ability to retain existing customers and expand those relationships is subject to a number of risks including the risk that we do not:

| • | maintain or improve the quality of services that we provide to our customers; |

| • | maintain or improve the level of attention expected by our customers; and |

| • | successfully leverage our existing client relationships to sell additional services. |

If our efforts to retain and expand our client relationships and to attract new customers do not prove effective, it could have a material adverse effect on our business and results of operations and our ability to grow our operations.

If we do not adapt our services to changes in technology or in the marketplace, or if our ongoing efforts to upgrade our technology are not successful, we could lose customers and have difficulty attracting new customers for our services.

The markets for our services are characterized by constant technological change, frequent introduction of new services and evolving industry standards. Our future success will be significantly affected by our ability to enhance, primarily through use of automation, econometrics and behavioral science principles, our current services and develop and introduce new services that address the increasingly sophisticated needs of our customers and their customers. These initiatives carry the risks associated with any new service development effort including cost overruns, delays in delivery and performance effectiveness. There can be no assurance that we will be successful in developing, marketing and selling new services that meet these changing demands. In addition, we may experience difficulties that could delay or prevent the successful development, introduction and marketing of these services. Finally, our services and their enhancements may not adequately meet the demands of the marketplace and achieve market acceptance. Any of these results would have a negative impact on our financial condition and results of operations and our ability to grow our operations.

Our growth objectives are dependent on the timing and market acceptance of our new service offerings.

Our ability to grow may be adversely affected by difficulties or delays in service development or the inability to gain market acceptance of new services to existing and new customers. There are no guarantees that new services will prove to be commercially successful.

Our business is dependent on the trend toward outsourcing.

Our continued growth at historical rates is dependent on the industry trend toward outsourced services. There can be no assurance that this trend will continue, as organizations may elect to perform such services themselves or may be prevented from outsourcing services. A significant change in this trend could have a materially adverse effect on our continued growth.

Our strategy of growing through selective acquisitions and mergers involves potential risks.

We intend to consider acquisitions of other companies that could complement our business including the acquisition of entities offering greater access and expertise in other asset types and markets that are related but that we do not currently serve. If we do acquire other businesses, we may face a number of risks including diverting management’s

14

Table of Contents

attention from our daily operations, to the need for additional management, operational and financial resources along with system conversions and the inability to maintain key pre-acquisition relationships with customers, suppliers and employees. Moreover, any acquisition may result in the incurrence of additional amortization expense of related intangible assets which could reduce our profitability.

Risks Related to International Business

Our international operations subject us to additional risks which could have an adverse effect on our results of operations.

We have reduced our costs by utilizing lower cost labor in foreign countries such as India. For example, at December 31, 2011, over 5,400 of our employees were based in India. These countries are subject to relatively higher degrees of political and social instability and may lack the infrastructure to withstand political unrest or natural disasters. Such disruptions can decrease efficiency and increase our costs in these countries. Weakness of the U.S. dollar in relation to the currencies used in these foreign countries may also reduce the savings achievable through this strategy. Furthermore, the practice of utilizing labor based in foreign countries has come under increased scrutiny in the United States and, as a result, some of our customers may require us to use labor based in the United States. We may not be able to pass on the increased costs of higher-priced United States-based labor to our customers which ultimately could have an adverse effect on our results of operations.

In many foreign countries, particularly in those with developing economies, it is common to engage in business practices that are prohibited by laws and regulations applicable to us, such as the Foreign Corrupt Practices Act (“FCPA”). Any violations of the FCPA or local anti-corruption laws by us, our subsidiaries or our local agents, could have an adverse effect on our business and reputation and result in substantial financial penalties or other sanctions.

Any political or economic instability in these countries could result in our having to replace or reduce these labor sources which may increase our labor costs and have an adverse impact on our results of operations.

Altisource is a Luxembourg company, and it may be difficult to enforce judgments against it or its directors and executive officers.

Altisource is a public limited company organized under the laws of Luxembourg. As a result, Luxembourg law and the articles of incorporation govern the rights of shareholders. The rights of shareholders under Luxembourg law may differ from the rights of shareholders of companies incorporated in other jurisdictions. A significant portion of the assets of Altisource are located outside the United States. It may be difficult for investors to enforce, in the United States, judgments obtained in U.S. courts against Altisource or its directors based on the civil liability provisions of the U.S. securities laws or to enforce, in Luxembourg, judgments obtained in other jurisdictions including the United States.

Risks Related to Our Employees

Our inability to attract and retain skilled employees may adversely impact our business.

Our business is labor intensive and places significant importance on our ability to recruit, train and retain skilled employees. Additionally, demand for qualified technical professionals conversant in certain technologies may exceed supply as new and additional skills are required to keep pace with evolving computer technology. Our ability to locate and train employees is critical to achieving our growth objective. Our inability to attract and retain skilled employees or an increase in wages or other costs of attracting, training or retaining skilled employees could have a materially adverse effect on our business, financial condition and results of operations.

| ITEM 1B. | UNRESOLVED STAFF COMMENTS |

Not applicable.

15

Table of Contents

| ITEM 2. | PROPERTIES |

Our principal executive offices are located in leased office space in Luxembourg, Grand Duchy of Luxembourg. A summary of our principal leased office space as of December 31, 2011 and the segments primarily occupying each location is as follows:

| Corporate and Support Services |

Financial Services |

Mortgage Services |

Technology Services | |||||

| Luxembourg, Luxembourg |

X | X | ||||||

| United States |

||||||||

| Atlanta, GA |

X | X | X | X | ||||

| Irvine, CA |

X | |||||||

| Sacramento, CA |

X | |||||||

| St. Louis, MO |

X | |||||||

| Tempe, AZ |

X | |||||||

| Vestal, NY |

X | |||||||

| India |

||||||||

| Bangalore |

X | X | X | X | ||||

| Goa |

X | X | ||||||

| Mumbai |

X | X | ||||||

We do not own any real property. We consider these facilities to be suitable and adequate for the management and operations of our business.

| ITEM 3. | LEGAL PROCEEDINGS |

We are, from time to time, involved in legal proceedings arising in the ordinary course of business. We record a liability for litigation if an unfavorable outcome is probable and the amount of loss can be reasonably estimated, including expected insurance coverage. For proceedings where a range of loss is determined, we record a best estimate of loss within the range. When legal proceedings are material, we disclose the nature of the litigation and to the extent possible the estimate of loss or range of loss. In the opinion of management, after consultation with legal counsel and considering insurance coverage where applicable, the outcome of current legal proceedings both individually and in the aggregate will not have a material impact on our financial condition, results of operations or cash flows. Our businesses are also subject to extensive regulation which may result in regulatory proceedings against us. See “Item 1A. Risk Factors” above.

| ITEM 4. | MINE SAFETY DISCLOSURES |

Not applicable.

16

Table of Contents

| ITEM 5. | MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES |

Market Information

Our common stock is listed on the NASDAQ Global Select Market under the symbol of “ASPS”. The following table sets forth the high and low close of day sales prices for our common stock, for the periods indicated, as reported by the NASDAQ Global Select Market:

| 2011 | ||||||||

| Quarter Ended |

Low | High | ||||||

| December 31 |

$ | 34.41 | $ | 50.70 | ||||

| September 30 |

31.79 | 37.61 | ||||||

| June 30 |

30.49 | 36.89 | ||||||

| March 31 |

28.51 | 30.68 | ||||||

| 2010 | ||||||||

| Quarter Ended |

Low | High | ||||||

| December 31 |

$ | 24.40 | $ | 30.64 | ||||

| September 30 |

24.29 | 31.14 | ||||||

| June 30 |

21.84 | 28.19 | ||||||

| March 31 |

21.13 | 27.02 | ||||||

The number of holders of record of our common stock as of January 31, 2012 was 97. The number of beneficial stockholders is substantially greater than the number of holders as a large portion of our common stock is held through brokerage firms.

Dividends

We have never declared or paid cash dividends on our common stock, and we do not intend to pay dividends in the foreseeable future.

Issuer Purchases of Equity Securities

On May 19, 2010, our shareholders authorized us to purchase up to 3.8 million shares of our common stock in the open market. The following table presents information related to our repurchases of our equity securities during the three months ended December 31, 2011:

17

Table of Contents

| Period |

Total number of shares purchased(1) |

Weighted average price paid per share |

Total number of shares purchased as part of publicly announced plans or programs |

Maximum number of shares that may yet be purchased under the plans or programs |

||||||||||||

| Common Shares: |

||||||||||||||||

| October 1 – 31, 2011 |

128,923 | $ | 35.56 | 128,923 | 1,971,148 | |||||||||||

| November 1 – 30, 2011 |

300,373 | 45.71 | 300,373 | 1,670,775 | ||||||||||||

| December 1 – 31, 2011 |

170,000 | 49.10 | 170,000 | 1,500,775 | ||||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| Total Common Shares |

599,269 | $ | 44.49 | 599,269 | 1,500,775 | |||||||||||

|

|

|

|

|

|

|

|

|

|||||||||

| (1) | Includes shares withheld from employees to satisfy tax withholding obligations that arose from the exercise of stock options. |

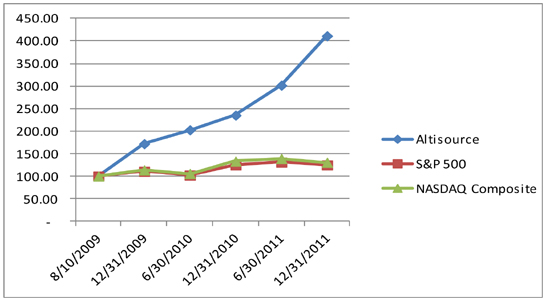

Stock Performance Graph

The information contained in Altisource Common Stock Comparative Performance Graph section shall not be deemed to be “soliciting material” or “filed” or incorporated by reference in future filings with the SEC, or subject to the liabilities of Section 18 of the Securities Exchange Act of 1934, as amended, except to the extent that we specifically request that it be treated as soliciting material or incorporate it by reference into a document filed under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended.

The graph below compares the cumulative total stockholder return on our common stock with the cumulative total return on the S&P’s 500 Index for the period commencing on August 10, 2009, the first trading day of our common stock, and ending on December 30, 2011, the last trading day of fiscal year 2011. The graph assumes an investment of $100 at the beginning of such period. The comparisons in the graphs below are based upon historical data and are not indicative of, nor intended to forecast, future performance of our common stock.

18

Table of Contents

| 8/10/2009 | 12/31/2009 | 06/30/10 | 12/31/10 | 06/30/11 | 12/31/11 | |||||||||||||||||||

| Altisource |

$ | 100.00 | $ | 172.05 | $ | 202.79 | $ | 235.33 | $ | 301.64 | $ | 411.31 | ||||||||||||

| S&P 500 |

100.00 | 110.72 | 101.94 | 124.38 | 131.13 | 124.87 | ||||||||||||||||||

| NASDAQ Composite |

100.00 | 113.90 | 105.87 | 133.16 | 139.22 | 130.76 | ||||||||||||||||||

| ITEM 6. | SELECTED CONSOLIDATED FINANCIAL DATA |

The following selected financial data as of and for the years ended December 31, 2011, 2010 and 2009 has been derived from our audited Consolidated Financial Statements. The following selected financial data as of and for the years ended December 31, 2008 and 2007 has been derived from our audited Combined Consolidated Financial Statements.

The historical results presented below may not be indicative of our future performance and do not necessarily reflect what our financial position and results of operations would have been had we operated as a separate, stand-alone entity for periods ending prior to August 9, 2009 (as discussed in Note 1 to the consolidated financial statements).

The selected consolidated financial data should be read in conjunction with the information contained in Item 7 of Part II, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and notes thereto in Item 8 of Part II, “Financial Statements and Supplementary Data”.

| Years Ended December 31, | ||||||||||||||||||||

| (in thousands, except per share data) |

2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||||||

| Revenue |

$ | 423,687 | $ | 301,378 | $ | 202,812 | $ | 160,363 | $ | 134,906 | ||||||||||

| Cost of Revenue |

275,849 | 189,059 | 126,797 | 115,048 | 96,954 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Gross Profit |

147,838 | 112,319 | 76,015 | 45,315 | 37,952 | |||||||||||||||

| Selling, General and Administrative Expenses |

62,131 | 57,352 | 39,473 | 28,088 | 27,930 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income from Operations |

85,707 | 54,967 | 36,542 | 17,227 | 10,022 | |||||||||||||||

| Other Income (Expense), net |

203 | 804 | 1,034 | (2,626 | ) | (1,743 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income Before Income Taxes |

85,910 | 55,771 | 37,576 | 14,601 | 8,279 | |||||||||||||||

| Income Tax Benefit (Provision) |

(7,943 | ) | 403 | (11,605 | ) | (5,382 | ) | (1,564 | ) | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Income |

77,967 | 56,174 | 25,971 | 9,219 | 6,715 | |||||||||||||||

| Net Income Attributable to Non-controlling Interests |

(6,855 | ) | (6,903 | ) | — | — | — | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Income Attributable to Altisource |

$ | 71,112 | $ | 49,271 | $ | 25,971 | $ | 9,219 | $ | 6,715 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Per Share: (1) |

||||||||||||||||||||

| Basic |

$ | 2.92 | $ | 1.96 | $ | 1.08 | $ | 0.38 | $ | 0.28 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Diluted |

$ | 2.77 | $ | 1.88 | $ | 1.07 | $ | 0.38 | $ | 0.28 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Transactions with Related Parties Included Above: |

||||||||||||||||||||

| Revenue |

$ | 245,262 | $ | 154,988 | $ | 94,897 | $ | 64,251 | $ | 59,350 | ||||||||||

| Selling, General and Administrative Expenses |

$ | 1,893 | $ | 1,056 | $ | 4,308 | $ | 6,208 | $ | 8,864 | ||||||||||

| Interest Expense |

$ | — | $ | — | $ | 1,290 | $ | 2,269 | $ | 965 | ||||||||||

19

Table of Contents

| Years Ended December 31, | ||||||||||||||||||||

| (in thousands) |

2011 | 2010 | 2009 | 2008 | 2007 | |||||||||||||||

| Cash and Cash Equivalents |

$ | 32,125 | $ | 22,134 | $ | 30,456 | $ | 6,988 | $ | 5,688 | ||||||||||

| Accounts Receivable, net |

52,005 | 53,495 | 30,497 | 9,077 | 16,770 | |||||||||||||||

| Premises and Equipment, net |

25,600 | 17,493 | 11,408 | 9,304 | 12,173 | |||||||||||||||

| Intangible Assets, net |

64,950 | 72,428 | 33,719 | 36,391 | 38,945 | |||||||||||||||

| Goodwill |

14,915 | 11,836 | 9,324 | 11,540 | 14,797 | |||||||||||||||

| Total Assets |

224,159 | 197,800 | 120,556 | 76,675 | 92,845 | |||||||||||||||

| Lines of Credit and Other Secured Borrowings |

— | — | — | 1,123 | 147 | |||||||||||||||

| Capital Lease Obligations |

836 | 1,532 | 664 | 1,356 | 3,631 | |||||||||||||||

| Total Liabilities |

58,216 | 45,902 | 34,208 | 16,129 | 17,171 | |||||||||||||||

| (1) | For all periods prior to the Separation, the number of shares originally issued of 24.1 million is being used for diluted earnings per share (“EPS”) and for basic EPS as no common stock of Altisource was traded prior to August 10, 2009 and no Altisource equity awards were outstanding prior to that date. |

20

Table of Contents

| ITEM 7. | MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS |

Management’s discussion and analysis of results of operations (“MD&A”) is a supplement to the accompanying consolidated financial statements and provides additional information on our businesses, current developments, financial condition, cash flows and results of operations. Significant sections of the MD&A are as follows:

Overview. This section, beginning on page 22, provides a description of recent developments we believe are important in understanding the results of operations and financial condition or in understanding anticipated future trends. In addition, a brief description is provided of significant transactions and events that affect the comparability of results being analyzed.

Consolidated Results of Operations. This section, beginning on page 24, provides an analysis of our consolidated results of operations for the three years ended December 31, 2011.

Segment Results of Operations. This section, beginning on page 29, provides an analysis of each business segment for the three years ended December 31, 2011 as well as our Corporate segment. In addition, we discuss significant transactions, events and trends that may affect the comparability of the results being analyzed.

Liquidity and Capital Resources. This section, beginning on page 41, provides an analysis of our cash flows for the three years ended December 31, 2011. We also discuss restrictions on cash movements, future commitments and capital resources.

Critical Accounting Judgments. This section, beginning on page 42, identifies those accounting principles we believe are most important to our financial results and that require significant judgment and estimates on the part of management in application. We provide all of our significant accounting policies in Note 2 to the accompanying consolidated financial statements.

Other Matters. This section, beginning on page 43, provides a discussion of off-balance sheet arrangements to the extent they exist. In addition, we provide a tabular discussion of contractual obligations and discuss any significant commitments or contingencies.

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K and certain information incorporated herein by reference contain forward-looking statements within the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995. These statements may relate to, among other things, future events or our future performance or financial condition. Words such as “anticipate”, “intend”, “expect”, “may”, “could”, “should”, “would”, “plan”, “estimate”, “seek”, “believe” and similar expressions are intended to identify such forward-looking statements. Forward-looking statements are not guarantees of future performance and involve a number of assumptions, risks and uncertainties that could cause actual results to differ materially. Important factors that could cause actual results to differ materially from those suggested by the forward-looking statements include, but are not limited to, the risks discussed in Item 1A of Part 1 “Risk Factors”. We caution you not to place undue reliance on these forward-looking statements which reflect our view only as of the date of this report. We are under no obligation (and expressly disclaim any obligation) to update or alter any forward-looking statements contained herein to reflect any change in our expectations with regard thereto or change in events, conditions or circumstances on which any such statement is based.

21

Table of Contents

OVERVIEW

Our Business

We are a provider of services focused on high value, technology-enabled, knowledge-based functions principally related to real estate and mortgage portfolio management, asset recovery and customer relationship management.

We classify our businesses into three reportable segments:

| • | Mortgage Services consists of mortgage portfolio management services that span the mortgage lifecycle from origination through REO asset management and sale; |

| • | Financial Services principally consists of unsecured asset recovery and customer relationship management; and |

| • | Technology Services consists of modular, comprehensive integrated technological solutions for loan servicing, vendor management and invoice presentment and payment as well as providing infrastructure support. |

In addition, our Corporate Items and Eliminations segment includes eliminations of transactions between the reporting segments and also includes costs recognized by us related to corporate support functions such as executive, finance, legal, human resources, vendor management and six sigma.

In evaluating our performance, we utilize Service Revenue which consists of amounts attributable to our fee based services. Reimbursable Expenses and Cooperative Non-controlling Interests are pass-through items for which we earn no margin. Reimbursable Expenses consists of amounts that we incur on behalf of our customers in performing our fee based services, but we pass such costs directly on to our customers without any additional markup.

Further discussion regarding our business may be found under Part I, Item 1, “Business”.

Strategic Update

For 2011, we focused our efforts on strategically supporting Ocwen as its portfolio of loans serviced continued to grow at an accelerated pace. To support such growth, we invested significantly in hiring and training new personnel (increasing our global staffing by 66%), developed and expanded some of the newer services (primarily insurance related services) and continued to add to the geographic footprint for existing services where it made economic sense.

Through Ocwen’s growth and our focused efforts to capture more revenue per loan serviced by Ocwen, we recognized $334.8 million of Service Revenue, a 36% increase over the year-ended December 31, 2010. In addition, although we made significant investments in personnel and related costs months in advance of loans boarding, we achieved gross margins based on Service Revenue of 44%, comparable to 2010 levels, and improved income from operations as a percent of Service Revenue to 26%, up from 22% in 2010.

From a cash perspective, we generated $111.6 million in operating cash flow which represents $0.33 for every dollar of Service Revenue. We sought to strategically deploy cash principally in three ways. First, we returned $61.1 million to shareholders through the repurchase of 1.6 million shares under the stock repurchase program. Second, we invested $16.4 million in technology and facilities to support our rapid growth. Third, we continued to invest in mortgage origination services with our $15.0 million investment in Correspondent One and our acquisition of Springhouse.

Looking ahead to 2012, we expect to remain focused on a few key initiatives that we believe will allow us to continue to deliver superior results for our customers and shareholders:

Support Ocwen’s growth. Our primary focus for next year will be the continued support of Ocwen. Ocwen’s growth in loans serviced, including loans boarded in the second half of 2011 and the additional 0.2 million loans we expect Ocwen to board in early 2012, will be the principal driver of our expected growth in 2012. Furthermore, we believe Ocwen will remain a leader in the on-going consolidation of high touch residential loan servicers.

Improve operating effectiveness. We must deliver high quality, regulatory compliant services that meet or exceed customers’ performance expectations. This requires us to intelligently and persistently invest in an array of broad based competencies including technology, quality assurance, compliance, econometrics and behavioral science among others.

22

Table of Contents

Service Offerings. We intend to capture additional revenue per loan from the loans boarded on our systems as well as develop a more balanced portfolio of service offerings that we believe will enable us to generate long-term consistent revenue and earnings growth, with faster growth in 2012. In 2012, we will expand our offering of mortgage origination services, principally to the members of Lenders One, as well as begin implementation of our next generation of REALSuite technologies.

Bring Financial Services to Profitability. Our Financial Services segment improved in 2011 posting $4.4 million in pre-tax income, which compares to $0.3 million in 2010, although revenue declined 8% to $71.2 million. We remain committed to this segment as we believe that significant market opportunities exist in assisting clients in the areas of customer relationship and asset recovery management services. We continue to believe that investments in areas such as optimal resolution models deployed through dynamic scripts will enable us to take advantage of these opportunities over an extended time period.

Basis of Presentation

We have prepared our consolidated financial statements in accordance with accounting principles generally accepted in the United States of America (“GAAP”). For periods prior to the Separation, our results include revenues and expenses directly attributable to our operations and allocations of expense from Ocwen which may not necessarily reflect what our consolidated results of operations, financial position and cash flows would have been had we operated as an independent company during that entire period.

Stock Repurchase Plan

In May 2010, our shareholders authorized us to purchase 15% of our outstanding share capital, or 3.8 million shares of common stock, in the open market. From authorization through December 31, 2011, we have purchased 2.3 million shares of common stock on the open market at an average price of $34.55 per share leaving 1.5 million shares available for purchase under the program.

Acquisitions

In April 2011, we acquired Springhouse, an appraisal management company that utilizes a nationwide panel of appraisers to provide real estate appraisals principally to mortgage originators, including the members of Lenders One, and real estate asset managers. In July 2011, we acquired the assembled workforce of a sub-contractor in India that performs asset recovery services. See Note 4 to the consolidated financial statements for additional information.

Factors Affecting Comparability

The following items may impact the comparability of our results:

| • | Effective January 2011, we modified our pricing for IT Infrastructure Services within our Technology Services segment from a rate card model primarily based on headcount to a fully loaded cost plus mark-up methodology. This new model applies to the infrastructure amounts charged to Ocwen as well as internal allocations of infrastructure cost. The impact of this change is discussed further in the Technology Services segment; |

| • | To further align the interests of management with shareholders, we expanded our use of equity compensation. For the years ended December 31, 2011, 2010 and 2009, we have recognized equity compensation expense of $4.0 million, $3.1 million and $0.3 million, respectively. Contributing to the increase was the attainment of certain market performance criteria in 2011 and 2010 which triggered vesting of a portion of the awards and acceleration in the expense recognition of these grants; |

| • | In the fourth quarter of 2010, we recognized $2.8 million of goodwill impairment related to the Financial Services segment; |

23

Table of Contents