UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

ý ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission file number 001-36157

ESSENT GROUP LTD.

(Exact name of registrant as specified in its charter)

Bermuda | Not Applicable | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |

Clarendon House 2 Church Street Hamilton HM11, Bermuda (Address of principal executive offices and zip code) (441) 297-9901 (Registrant’s telephone number, including area code) | ||

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Shares, $0.015 par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ý No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232-405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files.) Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer ý | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company o | |||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No ý

As of June 30, 2015, the last business day of the registrant's most recently completed second fiscal quarter, the aggregate market value of common shares held by non-affiliates of the registrant was approximately $1,960,432,848 (based upon the last reported sales price on The New York Stock Exchange).

The number of the registrant's common shares outstanding as of February 22, 2016 was 93,064,030.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant's proxy statement for the 2016 Annual General Meeting of Shareholders are incorporated by reference into Part III of this Annual Report on Form 10-K where indicated. Such Proxy Statement will be filed with the Securities and Exchange Commission within 120 days of the registrant's fiscal year ended December 31, 2015.

TABLE OF CONTENTS

Page | ||

i

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K, or Annual Report, includes forward-looking statements pursuant to the "safe harbor" provisions of the Private Securities Litigation Reform Act of 1995. Forward-looking statements relate to expectations, beliefs, projections, future plans and strategies, anticipated events or trends and similar expressions concerning matters that are not historical facts or present facts or conditions, such as statements regarding our future financial condition or results of operations, our prospects and strategies for future growth, the introduction of new products and services, and the implementation of our marketing and branding strategies. In many cases, you can identify forward-looking statements by terms such as "may," "will," "should," "expects," "plans," "anticipates," "believes," "estimates," "predicts," "potential" or the negative of these terms or other comparable terminology.

The forward-looking statements contained in this Annual Report reflect our views as of the date of this Annual Report about future events and are subject to risks, uncertainties, assumptions and changes in circumstances that may cause events or our actual activities or results to differ significantly from those expressed in any forward-looking statement. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future events, results, actions, levels of activity, performance or achievements. A number of important factors could cause actual results to differ materially from those indicated by the forward-looking statements, including, but not limited to, those factors described below, in Part I, Item 1A "Risk Factors," and in Part II, Item 7 "Management's Discussion and Analysis of Financial Condition and Results of Operations." These factors include, without limitation, the following:

• | changes in or to Fannie Mae and Freddie Mac, which we refer to collectively as the GSEs, whether through Federal legislation, restructurings or a shift in business practices; |

• | failure to continue to meet the mortgage insurer eligibility requirements of the GSEs; |

• | competition for our customers or the loss of a significant customer; |

• | lenders or investors seeking alternatives to private mortgage insurance; |

• | increase in the number of loans insured through Federal government mortgage insurance programs, including those offered by the Federal Housing Administration; |

• | decline in the volume of low down payment mortgage originations; |

• | uncertainty of loss reserve estimates; |

• | decrease in the length of time our insurance policies are in force; |

• | deteriorating economic conditions; |

• | the definition of "Qualified Mortgage" reducing the size of the mortgage origination market or creating incentives to use government mortgage insurance programs; |

• | the definition of "Qualified Residential Mortgage" reducing the number of low down payment loans or lenders and investors seeking alternatives to private mortgage insurance; |

• | the implementation of the Basel III Capital Accord, which may discourage the use of private mortgage insurance; |

• | management of risk in our investment portfolio; |

• | fluctuations in interest rates; |

• | inadequacy of the premiums we charge to compensate for our losses incurred; |

• | dependence on management team and qualified personnel; |

• | disturbance to our information technology systems; |

• | change in our customers' capital requirements discouraging the use of mortgage insurance; |

ii

• | declines in the value of borrowers' homes; |

• | limited availability of capital; |

• | unanticipated claims arise under and risks associated with our contract underwriting program; |

• | industry practice that loss reserves are established only upon a loan default; |

• | disruption in mortgage loan servicing; |

• | risk of future legal proceedings; |

• | customers' technological demands; |

• | our non-U.S. operations becoming subject to U.S. Federal income taxation; |

• | becoming considered a passive foreign investment company for U.S. Federal income tax purposes; and |

• | potential inability of our insurance subsidiaries to pay dividends. |

Readers are urged to consider these factors carefully in evaluating the forward-looking statements and are cautioned not to place undue reliance on these forward-looking statements. All of the forward-looking statements we have included in this Annual Report are based on information available to us on the date of this Annual Report. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise, except as otherwise required by law.

iii

Unless the context otherwise indicates or requires, the terms "we," "our," "us," "Essent," and the "Company," as used in this Annual Report, refer to Essent Group Ltd. and its directly and indirectly owned subsidiaries, including our primary operating subsidiaries, Essent Guaranty, Inc. and Essent Reinsurance Ltd., as a combined entity, except where otherwise stated or where it is clear that the terms mean only Essent Group Ltd. exclusive of its subsidiaries. Except as otherwise indicated, "Market Share" as used in this Annual Report means our market share as measured by our share of total new insurance written ("NIW") on a flow basis (in which loans are insured in individual, loan-by-loan transactions) in the private mortgage insurance industry, and excludes NIW under the Home Affordable Refinance Program ("HARP" and such NIW, the "HARP NIW") and bulk insurance that we write (in which each loan in a portfolio of loans is insured in a single transaction).

PART I

ITEM 1. BUSINESS

Overview

We are an established and growing private mortgage insurance company. We were formed to serve the U.S. housing finance industry at a time when the demands of the financial crisis and a rapidly changing business environment created the need for a new, privately funded mortgage insurance company. We had an estimated 12.0% Market Share for the year ended December 31, 2015. We believe that our success in acquiring customers and growing our insurance in force has been driven by the unique opportunity we offer lenders to partner with a well-capitalized mortgage insurer, unencumbered by business originated prior to the financial crisis, that provides fair and transparent claims payment practices, and consistency and speed of service.

Private mortgage insurance plays a critical role in the U.S. housing finance system. Essent and other private mortgage insurers provide credit protection to lenders and mortgage investors by covering a portion of the unpaid principal balance of a mortgage and certain related expenses in the event of a default. In doing so, we provide private capital to mitigate mortgage credit risk, allowing lenders to make additional mortgage financing available to prospective homeowners.

Private mortgage insurance helps extend affordable home ownership by facilitating the sale of low down payment loans into the secondary market. Two U.S. Federal government-sponsored enterprises, Fannie Mae and Freddie Mac, which we refer to collectively as the GSEs, purchase residential mortgages from banks and other lenders and guaranty mortgage-backed securities that are offered to investors in the secondary mortgage market. The GSEs are restricted by their charters from purchasing or guaranteeing low down payment loans, defined as loans with less than a 20% down payment, that are not covered by certain credit protections. Private mortgage insurance satisfies the GSEs' credit protection requirements for low down payment loans, supporting a robust secondary mortgage market in the United States.

Our primary U.S. mortgage insurance subsidiary, Essent Guaranty, Inc., received its certificate of authority from the Pennsylvania Insurance Department in July 2009. We subsequently acquired our mortgage insurance platform from a former private mortgage insurance industry participant and in 2010, became the first private mortgage insurer to be approved by the GSEs since 1995. We are licensed to write mortgage guaranty coverage in all 50 states and the District of Columbia.

We had master policy relationships with approximately 1,300 customers as of December 31, 2015. Our top ten customers represented approximately 36.6%, 42.6% and 49.6% of our NIW on a flow basis for the years ended December 31, 2015, 2014 and 2013, respectively. We have a highly experienced, talented team of 366 employees as of December 31, 2015. Our holding company is domiciled in Bermuda and our U.S. insurance business is headquartered in Radnor, Pennsylvania. We operate additional underwriting and service centers in Winston-Salem, North Carolina and Irvine, California.

For the years ended December 31, 2015, 2014 and 2013, we generated NIW of approximately $26.2 billion (including approximately $0.3 billion in NIW written on a bulk basis), $24.8 billion (including approximately $1.8 billion in NIW written on a bulk basis) and $21.2 billion, respectively, and as of December 31, 2015, we had approximately $65.2 billion of insurance in force. The insurer financial strength rating of Essent Guaranty, Inc. is Baa2 with a stable outlook by Moody's Investors Service and BBB+ with a stable outlook by Standard & Poor's Rating Services.

We also offer mortgage-related insurance and reinsurance through our wholly-owned Bermuda-based subsidiary, Essent Reinsurance Ltd., which we refer to as "Essent Re." As of December 31, 2015, Essent Re provided insurance and reinsurance in connection with GSE risk-share transactions covering approximately $156.3 million of risk on mortgage loans in reference pools associated with Freddie Mac's Agency Credit Insurance Structure (ACIS) and Fannie Mae's Credit Insurance Risk Transfer (CIRT) programs. Essent Re has also reinsured 25% of Essent Guaranty, Inc.'s GSE-eligible mortgage insurance NIW originated since July 1, 2014 under a quota share reinsurance agreement.

1

Our Industry

U.S. Mortgage Market

The U.S. residential mortgage market is one of the largest in the world, with over $9.95 trillion of debt outstanding as of September 30, 2015, and includes a range of private and government-sponsored participants. Private industry participants include mortgage banks, mortgage brokers, commercial, regional and investment banks, savings institutions, credit unions, REITs, mortgage insurers and other financial institutions. Public participants include government agencies such as the Federal Housing Administration, or FHA, the Veterans Administration, or VA, the U.S. Department of Agriculture Rural Development program and the Government National Mortgage Association, or Ginnie Mae, as well as government-sponsored enterprises such as Fannie Mae and Freddie Mac. The overall U.S. residential mortgage market encompasses both primary and secondary markets. The primary market consists of lenders originating home loans to borrowers, and includes loans made to support home purchases, which are referred to as purchase originations, and loans made to refinance existing mortgages, which are referred to as refinancing originations. The secondary market includes institutions buying and selling mortgages in the form of whole loans or securitized assets, such as mortgage-backed securities.

GSEs

The GSEs are the largest participants in the secondary mortgage market, buying residential mortgages from banks and other primary lenders as part of their government mandate to provide liquidity and stability in the U.S. housing finance system. According to the Federal Reserve, the GSEs held or guaranteed approximately $4.5 trillion, or 45.3%, of total U.S. residential mortgage debt as of September 30, 2015. Their charters generally prohibit the GSEs from purchasing a low down payment loan unless that loan is insured by a GSE-approved mortgage insurer, the mortgage seller retains at least a 10% participation in the loan or the seller agrees to repurchase or replace the loan in the event of a default. Historically, private mortgage insurance has been the preferred method utilized to meet this GSE charter requirement. As a result, the private mortgage insurance industry in the United States is driven in large part by the business practices and mortgage insurance requirements of the GSEs.

Mortgage Insurance

Mortgage insurance plays a critical role in the U.S. residential mortgage market by facilitating secondary market sales and by providing lenders and investors a means to diversify their exposures and mitigate mortgage credit risk. Mortgage insurance is provided by both private companies, such as Essent, and government agencies, such as the FHA and the VA. From 1996 through 2015, an average of 22.3% of total annual mortgage origination volume utilized mortgage insurance.

Mortgage insurance industry volumes are influenced by total mortgage originations, and the mix between purchase and refinancing originations. Historically, mortgage insurance utilization has been meaningfully higher in purchase originations compared to refinancing originations. In 2015, total U.S. residential mortgage origination volume was estimated at $1.63 trillion, comprised of $881 billion of purchase originations and $749 billion of refinancing originations. In recent years, historically low interest rates and special refinance programs, such as HARP, have caused refinancing volume to significantly outpace purchase originations. Purchase originations are expected to account for an increasing percentage of the overall mortgage market as the economic recovery and favorable housing market fundamentals stimulate growth in home buying activity, and a rising interest rate environment slows refinancing volume.

The following graph provides detail on trends in total residential mortgage originations and the breakdown of the market between purchase and refinancing volume.

2

Residential Purchase vs. Refinancing Mortgage Originations ($ in billions)

_______________________________________________________________________________

Source: Mortgage Bankers Association

Financial Crisis and Recovery

The severe economic and housing market dislocation experienced during the recent financial crisis had a profound impact on our industry. Incumbent insurers experienced record high claims activity and sustained significant financial losses, resulting in depleted capital positions. Three private mortgage insurers who wrote more than $125 billion of NIW, accounting for approximately 36% of total private mortgage insurance market NIW in 2007, have since exited the market, and several other insurers were forced to raise capital to repair their balance sheets and remain in operation. Although certain remaining incumbent insurers continue to deal with legacy challenges, the ongoing improvement of housing market fundamentals and the high credit quality of post-crisis new business are expected to support improved growth and profitability in the private mortgage insurance sector post-crisis.

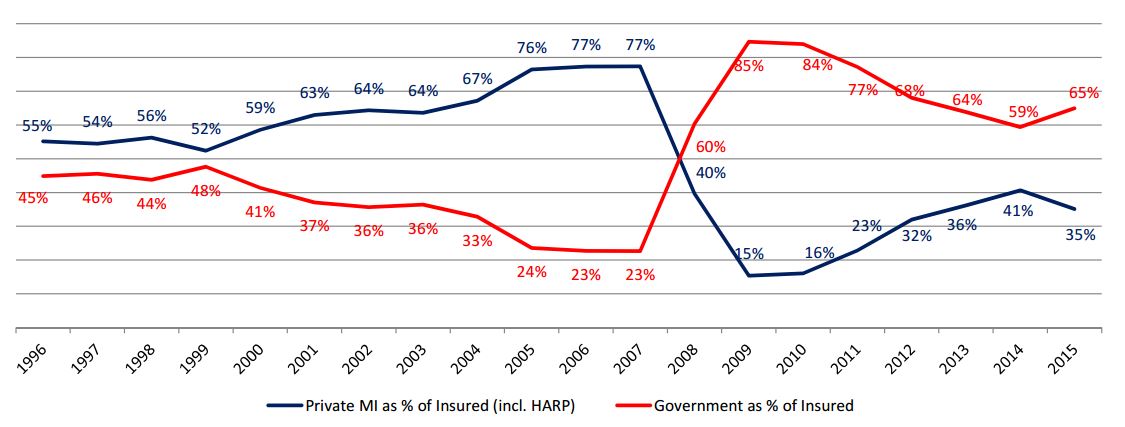

Prior to the financial crisis, private mortgage insurers accounted for the majority of the insured mortgage origination market. In 2007, private mortgage insurance represented 77.3% of insured mortgages and covered 15.5% of the total residential mortgage origination volume. During the financial crisis, government agencies began to insure an increasing percentage of the market as incumbent private insurers came under significant financial stress. By 2009, private mortgage insurance represented only 15.4% of the insured mortgage market and covered 4.1% of the total residential mortgage origination volume.

The private mortgage insurance industry, however, has continued to recover, more than doubling its share of the total insured market since 2009 and thereby leading to higher private mortgage insurance penetration of the total mortgage origination market. In 2015, private mortgage insurance increased to an estimated 35% of the total insured market and covered 14% of the total mortgage origination volume. These gains have been driven in part by the improved financial position of incumbent insurers, the influx of private capital into the sector to support post-crisis entrants such as Essent, and aggregate increase since 2010 in the mortgage insurance premium rates and upfront fees charged for FHA insurance, even after giving effect to the 50 basis point decrease in FHA mortgage insurance rates announced in January 2015.

The charts below detail the relative share of the insured mortgage market covered by public and private participants, and historical NIW trends in the mortgage insurance market and private mortgage insurance penetration rates, which represents private mortgage insurance NIW to total U.S. residential mortgage origination volume.

3

Relative Share of Private and Public Mortgage Insurance

_______________________________________________________________________________

Source: Inside Mortgage Finance

Private mortgage insurance NIW ($ in billions)

_______________________________________________________________________________

Source: Inside Mortgage Finance, except for total originations for the purpose of calculating private mortgage insurance penetration, which is based on Mortgage Bankers Association. For 2011 through 2015, private mortgage insurance penetration includes private mortgage insurance HARP NIW.

We view HARP as a modification of the coverage on existing insurance in force, and therefore when estimating our Market Share based on NIW, we exclude HARP NIW from total industry NIW. However, HARP is included as part of total industry NIW when showing private mortgage insurance penetration for the industry.

Competition

The private mortgage insurance industry is highly competitive. Private mortgage insurers generally compete on the basis of underwriting guidelines, pricing, terms and conditions, financial strength, reputation, customer relationships, the strength of management and field organizations, the effective use of technology, and innovation in the delivery and servicing of insurance products. The private mortgage insurance industry currently consists of seven active private mortgage insurers, including Essent and each of Arch Mortgage Insurance Company, Genworth Financial Inc., Mortgage Guaranty Insurance Corporation, National Mortgage Insurance Corporation, Radian Guaranty Inc. and United Guaranty Corporation.

We and other private mortgage insurers compete directly with Federal and state governmental and quasi-governmental agencies that provide mortgage insurance, principally, the FHA and, to a lesser degree, the VA. As discussed above, the FHA's

4

share of the mortgage insurance market increased as a result of the financial crisis and since 2009 has decreased as the private mortgage insurance industry has recovered and FHA premiums have increased in the aggregate. In addition to competition from the FHA and the VA, we and other private mortgage insurers currently face limited competition from state-sponsored mortgage insurance funds in several states, including California and New York. From time to time, other state legislatures and agencies consider expanding the authority of their state governments to insure residential mortgages.

Our industry also competes with products designed to eliminate the need for private mortgage insurance, such as "piggyback loans," which combine a first lien loan with a second lien in order to meet the 80% loan-to-value threshold required for sale to the GSEs without certain credit protections. In addition, we compete with investors willing to hold credit risk on their own balance sheets without credit enhancement and, in some markets, with alternative forms of credit enhancement such as structured finance products and derivatives.

Our Products and Services

Mortgage Insurance

In general, there are two principal types of private mortgage insurance, primary and pool.

Primary Mortgage Insurance

Primary mortgage insurance provides protection on individual loans at specified coverage percentages. Primary mortgage insurance is typically offered to customers on individual loans at the time of origination on a flow (i.e., loan-by-loan) basis, but can also be written in bulk transactions (in which each loan in a portfolio of loans is insured in a single transaction). A substantial majority of our policies are primary mortgage insurance.

Customers that purchase our primary mortgage insurance select a specific coverage level for each insured loan. To be eligible for purchase by a GSE, a low down payment loan must comply with the coverage percentages established by that GSE. For loans not sold to the GSEs, the customer determines its desired coverage percentage. Generally, our risk across all policies written is approximately 25% of the underlying primary insurance in force, but may vary from policy to policy between 6% and 35% coverage.

We file our premium rates with the insurance departments of the 50 states and the District of Columbia as required. Premium rates cannot be changed after the issuance of coverage and premiums applicable to an individual loan are based on a broad spectrum of risk variables including coverage percentages, loan-to-value, or LTV, loan and property attributes, and borrower risk characteristics. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Factors Affecting Our Results of Operations—Net Premiums Written and Earned" and "—Key Performance Indicators—Average Premium Rate."

Premium payments for primary mortgage insurance coverage are typically made by the borrower. Mortgage insurance paid directly by the borrower is referred to as borrower-paid mortgage insurance, or "BPMI." If the borrower is not required to pay the premium, then the premium is paid by the lender, who may recover the premium through an increase in the note rate on the mortgage or higher origination fees. Loans for which premiums are paid by the lender are referred to as lender-paid mortgage insurance, or "LPMI." In either case, the payment of premium to us generally is the legal responsibility of the insured.

Premiums are generally calculated as a percentage of the original principal balance and may be paid as follows:

•monthly, where premiums are collected on a monthly basis over the life of the policy;

•in a single payment, where the entire premium is paid upfront at the time the mortgage loan is originated;

•annually, where premiums are paid in advance for the subsequent 12 months; or

•on a "split" basis, where an initial premium is paid upfront along with subsequent monthly payments.

As of December 31, 2015, substantially all of our policies are monthly or single premium policies.

In general, we may not terminate mortgage insurance coverage except in the event there is non-payment of premiums or certain material violations of our mortgage insurance policies. The insured may cancel mortgage insurance coverage at any time at their option or upon mortgage repayment. GSE guidelines generally provide that a borrower meeting certain conditions may require the mortgage servicer to cancel mortgage insurance coverage upon the borrower's request when the principal balance of the loan is 80% or less of the property's current value. The Homeowners Protection Act of 1998, or HOPA, also requires the automatic termination of BPMI on most loans when the LTV ratio, based upon the original property value and

5

amortized loan balance, reaches 78%, and provides for cancellation of BPMI upon a borrower's request when the LTV ratio, based on the current value of the property, reaches 80%, upon satisfaction of the conditions set forth in HOPA. In addition, some states impose their own mortgage insurance notice and cancellation requirements on mortgage loan servicers.

Pool Insurance

Pool insurance is typically used to provide additional credit enhancement for certain secondary market and other mortgage transactions. Pool insurance generally covers the excess of the loss on a defaulted mortgage loan that exceeds the claim payment under the primary coverage, if such loan has primary coverage, as well as the total loss on a defaulted mortgage loan that did not have primary coverage. Pool insurance may have a stated aggregate loss limit for a pool of loans and may also have a deductible under which no losses are paid by the insurer until losses on the pool of loans exceed the deductible. In another variation, generally referred to as modified pool insurance, policies are structured to include an exposure limit for each individual loan as well as an aggregate loss limit or a deductible for the entire pool.

Master Policy

We issue a master policy to each customer approved as a counterparty by our risk department before accepting their applications for insurance. The master policy, along with its related endorsements and certificates, sets forth the general terms and conditions of our mortgage insurance coverage, including loan eligibility requirements, coverage terms, policy administration, premium payment obligations, exclusions or reductions in coverage, conditions precedent to payment of a claim, claim payment requirements, subrogation and other matters attendant to our coverage.

Mortgage insurance master policies generally protect mortgage insurers from the risk of material misrepresentations and fraud in the origination of an insured loan by establishing the right to rescind coverage in such event. Effective for mortgage insurance applications received after October 10, 2014, the GSEs, in coordination with the Federal Housing Finance Agency, or FHFA, have instituted new minimum standards for mortgage insurer master policies. Under these new minimum standards, master policies must provide rescission relief for loans that remain current up to 36 months after origination and that have not experienced more than two late payments of 30 days or more and have never been 60 days late, and are permitted to provide rescission relief after 12 payments provided the mortgage insurer can independently validate the representations for which it intends to give rescission relief. The standards require that the master policies reserve rescission rights with respect to fraud committed by the insured or those under its control and certain patterns of fraud. Our master policy forms satisfy these standards. See "Risk Factors—Risks Relating to Our Business—Changes in the business practices of the GSEs, including actions or decisions to decrease or discontinue the use of mortgage insurance or changes in the GSEs' eligibility requirements for mortgage insurers, could reduce our revenues or adversely affect our profitability and returns" elsewhere in this Annual Report and "—Regulation—Direct U.S. Regulation—GSE Qualified Mortgage Insurer Requirements" below.

Contract Underwriting

In addition to offering mortgage insurance, we provide contract underwriting services on a limited basis. As a part of these services, we assess whether data provided by the customer relating to a mortgage application complies with the customer's loan underwriting guidelines. These services are provided for loans that require private mortgage insurance, as well as for loans that do not require private mortgage insurance. Under the terms of our contract underwriting agreements with customers and subject to contractual limitations on liability, we agree to indemnify the customer against losses incurred in the event that we make an underwriting error which materially restricts or impairs the saleability of a loan, results in a material reduction in the value of a loan or results in the customer being required to repurchase a loan. The indemnification may be in the form of monetary or other remedies, subject to per loan and annual limitations. See "Risk Factors—Risks Relating to Our Business—We face risks associated with our contract underwriting business."

Bermuda-Based Insurance and Reinsurance

We offer mortgage-related insurance and reinsurance through Essent Re, a Class 3A insurance company licensed pursuant to Section 4 of the Bermuda Insurance Act 1978. As of December 31, 2015, Essent Re provided insurance or reinsurance in connection with GSE risk-share transactions covering approximately $156.3 million of risk on mortgage loans in reference pools associated with ACIS and CIRT programs. Essent Re has also reinsured 25% of Essent Guaranty, Inc.'s GSE-eligible mortgage insurance NIW originated since July 1, 2014 under a quota share reinsurance agreement.

Our Mortgage Insurance Portfolio

All of our policies in force were written since May 2010. The following data presents information on our mortgage insurance portfolio for policies written by Essent Guaranty, Inc.

6

Insurance in Force by Policy Year

The following table sets forth our insurance in force, or IIF, as of December 31, 2015, by year of policy origination. IIF refers to the unpaid principal balance of mortgage loans that we insure.

($ in thousands) | $ | % | |||||

2015 | $ | 25,292,660 | 38.8 | % | |||

2014 | 19,896,191 | 30.5 | |||||

2013 | 13,552,397 | 20.8 | |||||

2012 | 5,566,258 | 8.5 | |||||

2011 | 886,106 | 1.3 | |||||

2010 | 48,841 | 0.1 | |||||

$ | 65,242,453 | 100.0 | % | ||||

Portfolio Characteristics

The following tables reflect our IIF and risk in force, or RIF, amounts by borrower credit scores at origination, LTV at origination, and loan type and amortization as of December 31, 2015 and 2014. RIF refers to the product of the coverage percentage applied to the unpaid principal balance of mortgage loans that we insure.

Portfolio by Credit Score

December 31, | ||||||||||||||

Total IIF by FICO score ($ in thousands) | 2015 | 2014 | ||||||||||||

>=760 | $ | 30,174,460 | 46.2 | % | $ | 24,546,571 | 48.4 | % | ||||||

740-759 | 11,019,729 | 16.9 | 8,804,454 | 17.3 | ||||||||||

720-739 | 9,398,659 | 14.4 | 7,185,175 | 14.2 | ||||||||||

700-719 | 6,507,454 | 10.0 | 4,849,412 | 9.6 | ||||||||||

680-699 | 5,030,169 | 7.7 | 3,540,811 | 7.0 | ||||||||||

<=679 | 3,111,982 | 4.8 | 1,836,171 | 3.5 | ||||||||||

Total | $ | 65,242,453 | 100.0 | % | $ | 50,762,594 | 100.0 | % | ||||||

December 31, | ||||||||||||||

Total RIF by FICO score ($ in thousands) | 2015 | 2014 | ||||||||||||

>=760 | $ | 7,379,053 | 45.9 | % | $ | 5,900,373 | 48.3 | % | ||||||

740-759 | 2,735,754 | 17.0 | 2,135,891 | 17.4 | ||||||||||

720-739 | 2,346,971 | 14.6 | 1,750,232 | 14.3 | ||||||||||

700-719 | 1,592,463 | 9.9 | 1,145,431 | 9.4 | ||||||||||

680-699 | 1,255,734 | 7.8 | 859,436 | 7.0 | ||||||||||

<=679 | 763,199 | 4.8 | 435,907 | 3.6 | ||||||||||

Total | $ | 16,073,174 | 100.0 | % | $ | 12,227,270 | 100.0 | % | ||||||

7

Portfolio by LTV

December 31, | ||||||||||||||

Total IIF by LTV ($ in thousands) | 2015 | 2014 | ||||||||||||

85.00% and below | $ | 7,341,316 | 11.3 | % | $ | 6,100,274 | 12.0 | % | ||||||

85.01% to 90.00% | 22,337,975 | 34.2 | 17,719,816 | 34.9 | ||||||||||

90.01% to 95.00% | 34,035,682 | 52.2 | 25,832,106 | 50.9 | ||||||||||

95.01% and above | 1,527,480 | 2.3 | 1,110,398 | 2.2 | ||||||||||

Total | $ | 65,242,453 | 100.0 | % | $ | 50,762,594 | 100.0 | % | ||||||

December 31, | ||||||||||||||

Total RIF by LTV ($ in thousands) | 2015 | 2014 | ||||||||||||

85.00% and below | $ | 826,531 | 5.2 | % | $ | 681,908 | 5.6 | % | ||||||

85.01% to 90.00% | 5,310,050 | 33.0 | 4,174,743 | 34.1 | ||||||||||

90.01% to 95.00% | 9,646,406 | 60.0 | 7,203,270 | 58.9 | ||||||||||

95.01% and above | 290,187 | 1.8 | 167,349 | 1.4 | ||||||||||

Total | $ | 16,073,174 | 100.0 | % | $ | 12,227,270 | 100.0 | % | ||||||

Portfolio by Loan Amortization Period

December 31, | ||||||||||||||

Total IIF by Loan Amortization Period ($ in thousands) | 2015 | 2014 | ||||||||||||

FRM 30 years and higher | $ | 58,344,666 | 89.4 | % | $ | 44,503,607 | 87.7 | % | ||||||

FRM 20-25 years | 1,515,756 | 2.3 | 1,273,086 | 2.5 | ||||||||||

FRM 15 years | 2,702,723 | 4.2 | 2,637,970 | 5.2 | ||||||||||

ARM 5 years and higher | 2,679,308 | 4.1 | 2,347,931 | 4.6 | ||||||||||

Total | $ | 65,242,453 | 100.0 | % | $ | 50,762,594 | 100.0 | % | ||||||

Portfolio by Geography

Our in force portfolio is geographically diverse. As of December 31, 2015, only three states accounted for greater than 5% of our portfolio and no single metropolitan statistical area accounted for greater than 3% of our portfolio, as measured by either IIF or RIF. The following tables provide detail of the IIF and RIF in our top ten most concentrated states and our top ten most concentrated U.S. metropolitan statistical areas as of December 31, 2015 and 2014.

8

Top Ten States

December 31, | ||||||

2015 | 2014 | |||||

IIF by State | ||||||

CA | 9.6 | % | 10.2 | % | ||

TX | 8.3 | 8.3 | ||||

FL | 6.2 | 5.3 | ||||

WA | 4.6 | 4.3 | ||||

IL | 4.1 | 3.9 | ||||

NC | 3.9 | 4.0 | ||||

NJ | 3.4 | 3.4 | ||||

GA | 3.3 | 3.3 | ||||

PA | 3.3 | 3.4 | ||||

AZ | 3.2 | 3.3 | ||||

All Others | 50.1 | 50.6 | ||||

Total | 100.0 | % | 100.0 | % | ||

December 31, | |||||

2015 | 2014 | ||||

RIF by State | |||||

CA | 9.2 | % | 9.8 | % | |

TX | 8.6 | 8.5 | |||

FL | 6.4 | 5.6 | |||

WA | 4.8 | 4.4 | |||

IL | 4.1 | 4.0 | |||

NC | 4.0 | 4.2 | |||

GA | 3.5 | 3.5 | |||

NJ | 3.3 | 3.4 | |||

AZ | 3.2 | 3.2 | |||

PA | 3.1 | 3.2 | |||

All Others | 49.8 | 50.2 | |||

Total | 100.0 | % | 100.0 | % | |

9

Top Ten Metropolitan Statistical Areas

December 31, | ||||||

2015 | 2014 | |||||

IIF by Metropolitan Statistical Area | ||||||

Chicago-Naperville-Arlington Heights, IL | 2.9 | % | 3.1 | % | ||

New York-Jersey City-White Plains, NY-NJ | 2.7 | 1.8 | ||||

Houston-The Woodlands-Sugar Land, TX | 2.7 | 2.8 | ||||

Phoenix-Mesa-Scottsdale, AZ | 2.5 | 2.6 | ||||

Minneapolis-St. Paul-Bloomington, MN-WI | 2.5 | 2.4 | ||||

Atlanta-Sandy Springs-Roswell, GA | 2.5 | 2.5 | ||||

Seattle-Bellevue-Everett, WA | 2.3 | 2.3 | ||||

Los Angeles-Long Beach-Glendale, CA | 2.1 | 2.3 | ||||

Dallas-Plano-Irving, TX | 2.0 | 2.0 | ||||

Washington-Arlington-Alexandria, DC-VA-MD-WV | 2.0 | 2.0 | ||||

All Others | 75.8 | 76.2 | ||||

Total | 100.0 | % | 100.0 | % | ||

December 31, | ||||||

2015 | 2014 | |||||

RIF by Metropolitan Statistical Area | ||||||

Chicago-Naperville-Arlington Heights, IL | 2.9 | % | 3.1 | % | ||

Houston-The Woodlands-Sugar Land, TX | 2.7 | 2.9 | ||||

New York-Jersey City-White Plains, NY-NJ | 2.7 | 1.7 | ||||

Atlanta-Sandy Springs-Roswell, GA | 2.6 | 2.6 | ||||

Minneapolis-St. Paul-Bloomington, MN-WI | 2.6 | 2.5 | ||||

Phoenix-Mesa-Scottsdale, AZ | 2.5 | 2.5 | ||||

Seattle-Bellevue-Everett, WA | 2.3 | 2.4 | ||||

Dallas-Plano-Irving, TX | 2.0 | 2.0 | ||||

Los Angeles-Long Beach-Glendale, CA | 2.0 | 2.2 | ||||

Washington-Arlington-Alexandria, DC-VA-MD-WV | 1.9 | 2.0 | ||||

All Others | 75.8 | 76.1 | ||||

Total | 100.0 | % | 100.0 | % | ||

Customers

Our customers consist of originators of residential mortgage loans, such as regulated depository institutions, mortgage banks, credit unions and other lenders. We classify our customers into two broad categories and target our marketing efforts based on the customer's operating model and whether decisions to select a mortgage insurance provider are made centrally, or at the field or customer branch level:

• | Centralized—Centralized customers make decisions regarding the placement and allocation of mortgage insurance among their approved private mortgage insurers at the corporate level. Generally, these customers consist of the larger, national mortgage originators which originate loans across multiple states, but there are several regional and mid-size lenders which use this method as well. |

• | Decentralized—Decentralized customers make mortgage insurance purchasing decisions at the field or branch level. These customers generally are more prevalent with regional and mid-size lenders which originate mortgages in a smaller geographic footprint, but are also seen, on a limited basis, among some national lenders. |

10

We seek to maintain strong institutional relationships with all our customers. We provide them with ongoing risk, sales, training, service and product development support. We maintain regular and ongoing dialogue with our customers to develop an in-depth understanding of their strategies and needs, to share market perspectives and industry best practices, and to offer tailored solutions and training where necessary on a local level.

The following table provides detail on the percentage of our total NIW generated by centralized and decentralized customers, respectively, during the years ended December 31, 2015, 2014 and 2013.

Year Ended December 31, | |||||||||

2015 | 2014 | 2013 | |||||||

Centralized | 38.3 | % | 48.2 | % | 56.0 | % | |||

Decentralized | 61.7 | 51.8 | 44.0 | ||||||

Total | 100.0 | % | 100.0 | % | 100.0 | % | |||

We had master policy relationships with approximately 1,300 customers as of December 31, 2015.

As we have grown, we have successfully diversified our customer base. Our top ten customers generated 36.6% of our NIW on a flow basis during the year ended December 31, 2015, compared to 42.6% and 49.6% for the years ended December 31, 2014 and 2013, respectively. For the year ended December 31, 2015, one customer, Wells Fargo, exceeded 10% of our consolidated revenue. The loss of any of our larger customers could have a material adverse impact on us and our business. See "Risk Factors—Risks Relating to Our Business—Our revenues, profitability and returns would decline if we lose a significant customer."

Sales and Marketing

Our sales and marketing efforts are designed to help us establish and maintain in-depth, quality customer relationships. We organize our sales and marketing efforts based on our centralized and decentralized customer segmentation, giving additional consideration to a customer's geographic location and whether its lending footprint is national or regional in nature.

We emphasize a collaborative approach with our customers that includes a number of educational offerings and joint product development and marketing initiatives:

• | Regular Portfolio and Risk Management Reviews. We conduct periodic insured mortgage portfolio reviews with customers, including detailed loan performance metrics. |

• | Joint Product Development and Marketing Initiatives. We emphasize the development of specialized products and programs that provide increased opportunities for customers and address targeted segments of the market. We recognize the value in developing new products collaboratively with our customers. We also work closely with customers to understand their strategic priorities and business objectives while identifying opportunities that will enhance and complement the customers' marketing activities. |

• | Customer Service, Support and Trainings. We have an experienced and knowledgeable customer services team that strives to provide premier service to our customers. We dedicate service representatives to our customers so they can establish relationships with their customer peers and become thoroughly familiar with unique customer systems, processes and service needs. We have developed mortgage industry training courses that are offered to our customers as a value added service. We have an experienced team that maintains the course materials so that they are relevant and current and who facilitate training sessions for our customers. |

We have an experienced team of national and regional account managers strategically deployed nationwide that markets our mortgage insurance products and support services.

We assign national account managers to each of the national lenders, providing a point of communication between us and the customer's senior management team. These professionals are responsible for the development and execution of sales and marketing strategies aimed at growing customer volumes and ensuring each customer's needs are understood and helping them to pursue their strategies. The national account managers also coordinate the direct communication of customers with our underwriting and risk management groups to provide a continual flow of information between the organizations.

11

We also have regional account managers and dedicated support staff operating in eight defined geographic regions. Our regional account managers play a similar role to our national account managers with respect to customer relationship management, education and customer training, serving as our primary point of contact for small and mid-sized regional lenders operating in a given territory. Regional account managers also support our national account team by assisting with our efforts to directly market and service the branch locations of certain national lenders.

We support our national and regional sales force, and improve their effectiveness in acquiring new customers, by raising our brand awareness through advertising and marketing campaigns, website enhancements, electronic communication strategies and sponsorship of industry and educational events.

We continue to build our sales force by hiring qualified mortgage professionals who generally have well-established relationships with industry-leading lenders and significant experience in both mortgage insurance and mortgage lending. Our approach is reflected in and supported by our compensation structure, pursuant to which we have successfully implemented a non-commission-based structure that includes an equity ownership program, which we believe aligns their efforts with our long-term corporate objectives, including providing better customer service and better risk selection.

Information Technology

We have a highly automated business that relies on information technology. We accept insurance applications through electronic submission and issue electronic insurance approvals. In order to facilitate this process, we establish direct connections to the origination and servicing systems of our customers and servicers, which may require a significant upfront investment. We also provide our customers secure access to our web-based mortgage insurance ordering and servicing systems to facilitate transactions.

We continue to upgrade and enhance our systems and technology, including:

• | investing in new customer-facing technology that enables our customers to transact business faster and easier, whether over an internet browser or through direct system-to-system interfacing with our customers' loan origination and servicing systems; |

• | integrating our platform with third-party technology providers used by our customers in their loan origination process and for ordering mortgage insurance; |

• | developing and implementing a business rules engine that automatically enforces our eligibility guidelines and pricing rules at the time the mortgage insurance application is submitted; and |

• | implementing advanced business process management software that focuses on improving our underwriting productivity and that may also be used to improve our quality assurance and loss management functions. |

We believe that our technology, together with our information technology team, greatly enhances our operating efficiency and creates competitive advantages. This team is experienced in large-scale project delivery, including mortgage insurance administration systems and the development of web-enabled servicing capabilities. Technology costs are managed by standardizing our technology infrastructure, consolidating application systems, managing project execution risks and using contract employees as needed.

Underwriting

We have established underwriting guidelines that we believe protect our balance sheet and result in the insurance of high quality business. Most applications for mortgage insurance are submitted to us electronically, and we rely upon the lender's representations and warranties that the data submitted is true and correct when making our insurance decision. Our underwriting guidelines incorporate credit eligibility requirements that, among other things, restrict our coverage to mortgages that meet our requirements with respect to borrower FICO scores, maximum debt-to-income levels, maximum LTV ratios and documentation requirements. Our underwriting guidelines also limit the coverage we provide for mortgages made with certain high risk features, including those for cash-out refinance, second homes or investment properties.

We regularly seek to enhance our underwriting guidelines through extensive data gathering, detailed loan level risk analysis, and assessments of trends in key macroeconomic factors such as housing prices, interest rates and employment. We utilize proprietary models that enable us to assess individual loan risks with a high degree of granularity and set pricing for our

12

policies within a risk-adjusted return framework. See "—Risk Management" below. We have adopted a balanced underwriting approach, which considers our risk analysis, return objectives and market factors.

At present, our underwriting guidelines are broadly consistent with those of the GSEs. Many of our customers use the GSEs' automated loan underwriting systems, Desktop Underwriter® and Loan Prospector®, for making credit determinations. We accept the underwriting decisions made by the GSEs' underwriting systems, subject to certain additional limitations and requirements. We monitor the GSEs for updates to these systems, and may engage in a deeper review for the more substantive releases. Our reviews may result in the maintenance or implementation of additional eligibility requirements. In addition, the performance results of loans scored via automated underwriting systems are monitored within our portfolio management protocols.

Our primary mortgage insurance policies are issued through one of two programs:

• | Delegated Underwriting. We delegate to eligible customers the ability to underwrite the loans based on agreed-upon underwriting guidelines. To perform delegated underwriting, customers must be approved by our risk management group. See "—Risk Management—Loan Life Cycle Risk Management" below. Some customers prefer to assume underwriting responsibilities because it is more efficient within their loan origination process. Because this delegated underwriting is performed by third parties, we regularly perform quality assurance reviews on a sample of delegated loans to assess compliance with our guidelines. As of December 31, 2015, approximately 62% of our insurance in force had been originated on a delegated basis, compared to 65% as of December 31, 2014. See "Risk Factors—Risks Relating to Our Business—Our delegated underwriting program may subject our mortgage insurance business to unanticipated claims." |

• | Non-Delegated Underwriting. Customers who choose not to participate in, or do not qualify for, our delegated underwriting program submit loan files to us so that we may reach a decision as to whether we will insure the loan. In addition, customers participating in our delegated underwriting program may choose not to use their delegated authority, and instead may submit loans for our independent underwriting. Some customers prefer our non-delegated program because we assume underwriting responsibility and will not rescind coverage if we make an underwriting error, subject to the terms of our master policy. We seek to ensure that our employees properly underwrite our loans through quality assurance sampling, loan performance monitoring and training. As of December 31, 2015, approximately 38% of our insurance in force had been originated on a non-delegated basis, compared to 35% as of December 31, 2014. |

We maintain primary underwriting centers in Radnor, Pennsylvania, Winston-Salem, North Carolina and Irvine, California. We believe that the geographical distribution of our underwriting staff allows us to make underwriting determinations across different time zones and to best serve customers across the United States. Although our employees conduct the substantial majority of our non-delegated underwriting, we engage underwriters on an outsourced basis from time to time in order to provide temporary underwriting capacity.

Risk Management

We have established risk management controls throughout our organization and have a risk management framework that we believe reduces the volatility of our financial results and capital position. The risk committee of our board of directors has formal oversight responsibility for the risks associated with our business and is supported by a management risk committee, chaired by our Chief Risk Officer, comprised of all senior members of our executive management team.

We believe that our risk management framework encompasses all of the major risks we face, including our mortgage insurance portfolio, investment risk, liquidity risk and regulatory compliance risk, among others. The majority of our risk analysis is directed toward the risks embedded in our mortgage insurance portfolio. As such, we have established a risk management approach that analyzes the risk across the full life cycle of a mortgage, into what we term the "loan life cycle."

Loan Life Cycle Risk Management

We generally break down the loan life cycle risk management process into three components:

• | Customer qualification—customer review and approval process; |

• | Policy acquisition—loan underwriting, valuation and risk approval; and |

13

• | Portfolio management—loan performance and lender monitoring with continuous oversight through the settlement of a claim. |

Customer qualification involves a process in which we diligence a potential customer's financial resources, operational practices, management experience and track record of originating quality mortgages prior to formalizing a customer relationship. We leverage the experience of our management team to pre-screen lenders prior to formally engaging and performing a lender qualification review. Once engaged, our counterparty risk management team conducts a lender qualification review with oversight from the management risk committee. Approved lenders are subject to clear parameters regarding underwriting delegation status, credit guideline requirements and variances and collateral thresholds and volume mix expectations for loan diversification.

The policy acquisition process involves the establishment of underwriting guidelines, pricing schedules and aggregate risk limits. See "—Underwriting" above. These guidelines and schedules are coded in our credit risk rule engine which is utilized to screen each loan underwritten, and are constructed to ensure prudent risk acquisition with adequate return on capital. These guidelines and schedules are maintained and periodically reviewed by our risk management team and adjusted to reflect the most current risk assessment based on ongoing experience in the insurance portfolio as well as industry loan quality trends.

The portfolio management process involves two main functions, quality assurance, or QA, reviews, and a comprehensive surveillance protocol, in order to provide customers timely feedback that fosters high quality loan production. Through our QA process, we review a statistically significant sample of individual mortgages from our customers to ensure that the loans accepted through our underwriting process meet our pre-determined eligibility and underwriting criteria. The QA process allows us to identify trends in lender underwriting and origination practices, as well as to back-test underlying reasons for delinquencies, defaults and claims within our portfolio. The information gathered from the QA process is incorporated into our policy acquisition function and is intended to prevent continued aggregation of underperforming risks. Our surveillance protocol maintains oversight over customer and vendor activities, industry dynamics, production trends and portfolio performance. The portfolio management process also involves loss mitigation aimed to reduce both frequency and severity of non-performing risk. See "—Defaults and Claims" below.

Modeling and Analytics

Our risk management professionals are supported by substantial data analysis and sophisticated risk models. We have a dedicated modeling and analytics team which is responsible for delivering actionable models, tools, analysis and reporting to inform our credit underwriting and pricing decisions. The team analyzes mortgage, financial, economic and housing data to develop proprietary behavioral models that help us assess credit, prepayment and loss severity trends and collateral valuation models to help inform business decisions. Performance and profitability are evaluated across customers and products to identify the emergence of potential weaknesses and adverse risks. Geographic housing market analysis also is utilized in establishing market restrictions for certain products and segments. We utilize an economic capital framework to evaluate risk-adjusted returns. We also perform stress tests on our portfolio to analyze how our book of business may perform under adverse scenarios. We believe that our economic capital framework and stress testing analysis helps to inform our optimal capitalization targets, allowing us to prudently manage and protect our balance sheet.

Defaults and Claims

Defaults

The default and claim cycle for a mortgage insurance policy begins with receipt of a default notice from the servicer. We consider a loan to be in default when we are notified by the servicer that the borrower has missed at least two consecutive monthly payments. Defaults may occur for a variety of reasons including death or illness, divorce or other family problems, unemployment, changes in economic conditions, declines in property values that cause the outstanding mortgage amount to exceed the value of a home or other events.

We expect servicers to make timely collection efforts on borrowers who have defaulted, and to attempt to restore the defaulted mortgage, and our mortgage insurance coverage, to current status. If the servicer cannot restore a borrower to current status, the servicer may be able to offer the borrower a forbearance or loan modification alternatives. Where these alternatives cannot cure the default, the servicer is responsible for pursuing remedies for the default, including foreclosure or acceptable foreclosure alternatives, certain of which, such as short sales and deeds in lieu of foreclosure, require our prior approval under the terms of our master policy. We have delegated limited authority to the GSEs' and their servicers to exercise some of these alternatives. Among other requirements, servicers operate under protocols established by the GSEs. See "Risk Factors—Risks

14

Relating to Our Business—If servicers fail to adhere to appropriate servicing standards or experience disruptions to their businesses, our losses could unexpectedly increase."

The following table shows the number of primary insured loans and the percentage of loans insured by us that are in default as of December 31, 2015 and 2014:

Number of Loans in Default and Default Rate

December 31, | ||||||

2015 | 2014 | |||||

Number of policies in force | 297,437 | 229,721 | ||||

Loans in default | 1,028 | 457 | ||||

Percentage of loans in default | 0.35 | % | 0.20 | % | ||

Loan Defaults by Originating Year

December 31, 2015 | December 31, 2014 | |||||||||||||||||||

Originating Year | Loans in Default | Percentage of policies written in period | Defaulted RIF (in thousands) | Loans in Default | Percentage of policies written in period | Defaulted RIF (in thousands) | ||||||||||||||

2010 | 4 | 0.3 | % | $ | 186 | 1 | 0.1 | % | $ | 16 | ||||||||||

2011 | 45 | 0.3 | 1,886 | 55 | 0.4 | 2,155 | ||||||||||||||

2012 | 154 | 0.3 | 7,639 | 119 | 0.2 | 5,672 | ||||||||||||||

2013 | 303 | 0.3 | 15,209 | 206 | 0.2 | 10,879 | ||||||||||||||

2014 | 421 | 0.4 | 24,525 | 76 | 0.1 | 4,398 | ||||||||||||||

2015 | 101 | 0.1 | 5,526 | N/A | N/A | N/A | ||||||||||||||

Total | 1,028 | $ | 54,971 | 457 | $ | 23,120 | ||||||||||||||

We have experienced a low level of defaults to date. This is due, in part, to the weighted average life of our mortgage insurance portfolio being 17.3 months as of December 31, 2015, whereas the peak default period for insured mortgage loans has historically been three to six years after loan origination. As a result, we do expect default levels to increase as our portfolio seasons. We believe that in recent years the underwriting practices in the industry have improved substantially and that the quality of mortgage loans originated has been high. Consequently, we expect that the default rate and losses on the business we have underwritten to date will be favorable in comparison to the default rate and losses experienced by the mortgage insurers that wrote business in 2009 and prior years.

Claims

Defaulted mortgages that are not cured turn into claims. The insured customer must acquire title to the property before submitting a claim. The time in which a customer may acquire title to a property through foreclosure varies, depending on the state in which the property is located. Historically, on average, mortgage insurers do not receive a request for claim payment until approximately 18 months following a default on a first-lien mortgage. This time lag has increased in recent years as the industry has experienced a slowdown in foreclosures (and, consequently, a slowdown in claims submitted to mortgage insurers) largely due to foreclosure moratoriums imposed by various government entities and lenders and increased scrutiny within the mortgage servicing industry on the foreclosure process.

Upon review and determination that a claim is valid, we generally have the following three settlement options:

• | Percentage option—determined by multiplying the claim amount by the applicable coverage percentage, with the customer retaining title to the property. The claim amount is defined in the master policy as consisting of the unpaid loan principal, plus past due interest, subject to a defined maximum, and certain expenses associated with the default; |

15

• | Third-party sale option—pay the amount of the claim required to make the customer whole, commonly referred to as the "actual loss amount" (not to exceed our maximum liability as outlined under the percentage option), following an approved sale; or |

• | Acquisition option—pay the full claim amount and acquire title to the property. |

We believe there are opportunities to mitigate losses between the time a loan defaults and the ultimate loss we may experience. Because of the small number of defaults and filed claims in our insurance portfolio to date, our opportunities to pursue these activities have been limited. However, we expect both defaulted loan counts and claim filings to increase as our portfolio grows and matures, expanding the potential benefit from these loss mitigation activities. Our loss mitigation and claims area is led by seasoned personnel supported by default tracking and claims processing capabilities within our integrated platform. Our loss mitigation staff is also actively engaged with our servicers and the GSEs with regard to appropriate servicing and loss mitigation practices.

Investment Portfolio

Our investment portfolio, including cash, comprises the largest single component of our balance sheet, representing 88.6% of our total assets at December 31, 2015. Our primary objectives with respect to our investment portfolio are to preserve capital, generate investment income and maintain sufficient liquidity to cover operating expenses and pay future insurance claims. As of December 31, 2015, predominately all of our investment securities were rated investment-grade.

We have adopted and our board of directors has approved an investment policy that defines specific limits for asset sectors, single issuer, credit rating, asset duration, industry and geographic concentration and eligible and ineligible investments. Our senior management is responsible for the execution of our investment strategy and compliance with the adopted investment policy, and review investment performance and strategy with the investment committee of the board of directors on a quarterly basis.

Our current strategy for the investment portfolio is focused primarily on the following: selecting investment-grade, fixed income securities; maintaining sufficient liquidity to meet expected and unexpected financial obligations; mitigating interest rate risk through management of asset durations; continuously monitoring investment quality; and restricting investments to assets that are highly correlated to the residential mortgage market.

We engage external asset managers to assist with the trading, investment research, investment due diligence and portfolio allocation within the guidelines that we have set. Approximately 92.3% of our investment assets, excluding cash, were managed by external managers as of December 31, 2015. Assets not managed by external managers include securities on deposit with state regulatory agencies in connection with the insurance licenses and bonds issued by the U.S. Treasury and U.S. government agencies. To date, we have not used any derivatives to hedge any investment or business risks that we are currently assuming. We measure investment performance against market benchmarks on both total return and return volatility dimensions.

See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Financial Condition—Investments" for information regarding the performance of our investment portfolio.

Regulation

Direct U.S. Regulation

We are subject to comprehensive, detailed regulation by Federal regulators and state insurance departments. State regulations are principally designed for the protection of the public and our insured policyholders, rather than for the benefit of investors. Although their scope varies, state insurance laws generally grant broad supervisory powers to agencies or to officials to examine insurance companies and to enforce rules or to exercise discretion affecting almost every significant aspect of the insurance business.

GSE Qualified Mortgage Insurer Requirements

Pursuant to their charters, Fannie Mae and Freddie Mac purchase or guaranty low down payment loans insured by entities that they determine to be qualified mortgage insurance companies. Our primary insurance subsidiary, Essent Guaranty, Inc., is currently approved by both Fannie Mae and Freddie Mac as a mortgage insurer.

16

The FHFA, as the conservator of the GSEs, has the authority to establish the priorities of the GSEs and to control and direct their operations. The FHFA has established a strategic plan for the GSEs, including the development by the GSEs of aligned counterparty risk management standards for mortgage insurers that include uniform master policy and eligibility requirements.

Effective for mortgage insurance applications received after October 10, 2014, the GSEs have instituted minimum standards for mortgage insurer master policies, including standards relating to limitations of a mortgage insurer's rescission rights. We have received all necessary state approvals and have implemented our new master policy forms as required by the GSEs. See "—Our Products and Services—Mortgage Insurance—Master Policy" above.

Effective December 31, 2015, Fannie Mae and Freddie Mac, at the direction of the FHFA, implemented new coordinated Private Mortgage Insurer Eligibility Requirements, which we refer to as the "PMIERs." The PMIERs represent the standards by which private mortgage insurers are eligible to provide mortgage insurance on loans owned or guaranteed by Fannie Mae and Freddie Mac. The PMIERs include financial strength requirements incorporating a risk-based framework that require approved insurers to have a sufficient level of liquid assets from which to pay claims. The PMIERs also include enhanced operational performance expectations and define remedial actions that apply should an approved insurer fail to comply with these requirements. As of December 31, 2015, Essent Guaranty, Inc., our GSE-approved mortgage insurance company, was in compliance with the PMIERs.

State Insurance Regulation

Our U.S. insurance subsidiaries are required by the insurance regulatory authority of its state of domicile, and the insurance regulatory authority of each other jurisdiction in which they are licensed to transact business, to make various filings with those insurance regulatory authorities and with the National Association of Insurance Commissioners, or NAIC, including quarterly and annual financial statements prepared in accordance with statutory accounting principles. We are licensed to write mortgage insurance in all 50 states and the District of Columbia. Most states also regulate transactions between insurance companies and their affiliates and have restrictions on transactions that have the effect of inducing lenders to place business with the insurer. For a description of limits on dividends payable to Essent Group Ltd. from our insurance subsidiaries, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources" and Note 10 to our consolidated financial statements entitled "Dividends Restrictions" included elsewhere in this Annual Report.

In general, state regulation of our insurance business relates to:

• | licenses to transact business; |

• | producer licensing; |

• | approval of policy forms; |

• | approval of premium rates; |

• | limits on insurable loans; |

• | quarterly, annual and other reports on our financial condition; |

• | the basis upon which assets and liabilities must be stated; |

• | requirements regarding contingency reserves; |

• | minimum capital levels and adequacy ratios; |

• | limitations on the types of investment instruments which may be held in our investment portfolio; |

• | special deposits of securities; |

• | limits on dividends payable; |

• | advertising compliance; |

17

• | establishment of reserves; |

• | claims handling; |

• | hazardous financial condition; and |

• | enterprise risk management. |

Mortgage insurance premium rates are regulated to protect policyholders against the adverse effects of excessive, inadequate or unfairly discriminatory rates and to encourage competition in the insurance marketplace. Any increase in premium rates must be actuarially justified, generally on the basis of the insurer's loss experience, expenses and future trend analysis. The general mortgage default experience may also be considered. Premium rates are subject to review and approval protocols maintained, and may be the subject of examination, by state regulators. See "Management's Discussion and Analysis—Liquidity and Capital Resources" for information about regulations governing our capital adequacy, information about our current capital and our expectations regarding our future capital position.

The insurance holding company laws and regulations of Pennsylvania, the state in which our U.S. insurance subsidiaries are domiciled, regulate, among other things, certain transactions between Essent Group Ltd., our insurance subsidiaries and other parties affiliated with us and certain transactions involving our common shares, including transactions that constitute a change of control of Essent Group Ltd. and, consequently, a change of control of our insurance subsidiaries. Specifically, these laws and regulations require that, before a person can acquire direct or indirect control of an insurer domiciled in the state, prior written approval must be obtained from the Pennsylvania Insurance Department. The Pennsylvania Insurance Department is required to consider various factors, including the financial strength of the acquirer, the integrity and management experience of the acquirer's board of directors and executive officers, and the acquirer's plans for the future operations of the reinsurer or insurer. Pursuant to applicable laws and regulations, "control" over an insurer is generally presumed to exist if any person, directly or indirectly, owns, controls, holds the power to vote or holds proxies representing, 10% or more of the voting securities of that reinsurer or insurer. Indirect ownership includes ownership of our common shares.

State insurance law, and not Federal bankruptcy law, would apply to any insolvency or financially hazardous condition of our U.S. insurance subsidiaries.

During 2012, the NAIC established a Mortgage Guaranty Insurance Working Group, which we refer to as the "MGIWG," to determine and make recommendations to the NAIC's Financial Condition Committee regarding what, if any, changes are deemed necessary to the solvency regulation of mortgage guaranty insurers. The MGIWG has advanced a draft revised Model Act and has engaged with certain industry members developing a risk-sensitive analytical model to assess and establish capital adequacy levels. The MGIWG has advised us that it would like to conclude its work in 2016.

Statutory Accounting

The preparation of financial statements in conformity with state-regulated statutory accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities. It also requires disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the period. Actual results could differ from those estimates.

We are required to establish statutory accounting contingency loss reserves in an amount equal to 50% of our net earned premiums. These amounts generally cannot be withdrawn for a period of 10 years, except as permitted by applicable insurance law and regulations. With regulatory approval, a mortgage guaranty insurance company may make early withdrawals from the contingency reserve when incurred losses exceed 35% of net premiums earned in a calendar year. For further information, see Note 16 to our consolidated financial statements entitled "Statutory Accounting" included elsewhere in this Annual Report.

Federal Mortgage-Related Laws and Regulations

Certain Federal laws directly or indirectly affect private mortgage insurers. Private mortgage insurers are impacted indirectly by Federal laws and regulations affecting mortgage originators and lenders, purchasers of mortgage loans, such as the GSEs, and governmental insurers such as the FHA and the VA. For example, changes in Federal housing laws and regulation or other laws and regulations that affect the demand for private mortgage insurance may have a material adverse effect on us. In addition, mortgage origination and servicing transactions are subject to compliance with various Federal and state laws, including the Real Estate Settlement Procedures Act, or RESPA, the Equal Credit Opportunity Act, the Fair Housing Act, the

18

Truth In Lending Act, or TILA, the Homeowners Protection Act of 1998, or HOPA, the Fair Credit Reporting Act of 1970 and the Fair Debt Collection Practices Act. Among other things, these laws and their implementing regulations prohibit payments for referrals of settlement service business, require fairness and non-discrimination in granting or facilitating the granting of credit, govern the circumstances under which companies may obtain and use consumer credit information, define the manner in which companies may pursue collection activities, and provide for other consumer protections.

Dodd-Frank Act

The Dodd-Frank Act Wall Street Reform and Consumer Protection Act of 2010, which we refer to as the Dodd-Frank Act, amended certain provisions of TILA and RESPA that may have a significant impact on our business prospects. The Consumer Financial Protection Bureau, or CFPB, a Federal agency created by the Dodd-Frank Act, is charged with implementation and enforcement of these provisions. On January 10, 2014, the CFPB implemented a final rule regarding ability-to-repay, or ATR, and Qualified Mortgage, or QM, standards. Effective December 24, 2015, the Office of the Comptroller of the Currency, the Federal Reserve Board, the Federal Deposit Insurance Commission, the Federal Housing Finance Agency, the Securities and Exchange Commission and the Department of Housing and Urban Development adopted a joint final rule to implement the Qualified Residential Mortgage, or QRM, regulations as required by the Dodd-Frank Act. The CFPB has also published final residential mortgage servicing rules providing for amendments to Regulation Z (promulgated pursuant to TILA) and RESPA.

Qualified Mortgage Regulations—Ability To Repay Requirements

The Dodd-Frank Act established the CFPB to regulate the offering and provision of consumer financial products and services under Federal law, including residential mortgages. Under the Dodd-Frank Act, the CFPB is authorized to issue regulations governing a loan originator's determination that, at the time a loan is originated, the consumer has a reasonable ability to repay the loan. The Dodd-Frank Act provides for a statutory presumption that a borrower will have the ability to repay a loan if the loan has characteristics satisfying the QM definition. Creditors who violate the ATR standard can be liable for all interest and fees paid by the borrower as well as actual and statutory damages. Furthermore, the borrower may assert this as a defense by recoupment or set off without regard to any statute of limitation in any foreclosure action initiated by or on behalf of the creditor, assignee or any holder of the mortgage.

Pursuant to the CFPB's final rule regarding QMs, which we refer to as the QM Rule, a loan is deemed to be a QM if it meets certain specified requirements, including if:

• | the term of the mortgage is less than or equal to 30 years; |