UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

____________________

FORM 10-Q

| (Mark One) | |

| [X] | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For quarterly period ended March 31, 2020 | |

|

|

|

| [ ] | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 000-54653

BULLFROG GOLD CORP.

(Exact name of registrant as specified in its charter)

| Delaware | 41-2252162 |

| (State or other jurisdiction of | (I.R.S. Employer |

| incorporation or organization) | Identification No.) |

|

|

|

| 897 Quail Run Drive |

|

| Grand Junction, Colorado | 81505 |

| (Address of principal executive offices) | (Zip Code) |

(970) 628-1670

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act: None.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes [X] No [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | [ ] |

| Accelerated filer | [ ] |

| Non-accelerated filer | [X] |

| Smaller reporting company | [X] |

|

|

|

| Emerging growth company | [ ] |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. [ ]

Indicate by check mark whether the registrant is a shell company (as defined in 12b-2 of the Exchange Act.) Yes [ ] No [X]

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date: 157,230,237 shares of common stock, par value $0.0001, were outstanding on May 12, 2020.

BULLFROG GOLD CORP.

TABLE OF CONTENTS TO FORM 10-Q

2

ITEM 1 - CONSOLIDATED FINANCIAL STATEMENTS (UNAUDITED)

BULLFROG GOLD CORP.

CONSOLIDATED BALANCE SHEETS

MARCH 31, 2020 AND DECEMBER 31, 2019

(unaudited)

|

| 3/31/20 | 12/31/19 |

| Assets |

|

|

| Current assets |

|

|

| Cash | $1,255,130 | $44,595 |

| Prepaids | 28,805 | 26,042 |

| Deposits | 116,783 | 116,783 |

| Total current assets | 1,400,718 | 187,420 |

|

|

|

|

| Other assets |

|

|

| Mineral properties | 210,425 | 210,425 |

|

|

|

|

| Total assets | $1,611,143 | $397,845 |

|

|

|

|

| Liabilities and Stockholders' Equity (Deficit) |

|

|

| Current liabilities |

|

|

| Accounts payable | $23,261 | $21,308 |

| Related party payable | 637,292 | 635,775 |

| Total current liabilities | 660,553 | 657,083 |

|

|

|

|

| Long term liabilities |

|

|

| Warrant liability | 269,519 | 0 |

|

|

|

|

| Total liabilities | 930,072 | 657,083 |

|

|

|

|

| Stockholders' deficit |

|

|

| Preferred stock, 250,000,000 shares authorized, 200,000,000 undesignated, zero issued and outstanding, $.0001 par value | 0 | 0 |

| Preferred stock series A, 5,000,000 shares designated and authorized, $.0001 par value; zero issued and outstanding as of 3/31/20 and 12/31/19 | 0 | 0 |

| Preferred stock series B, 45,000,000 shares designated and authorized, $.0001 par value; 20,229,166 issued and outstanding as of 3/31/20 and 25,520,833 issued and outstanding as of 12/31/19 | 2,023 | 2,552 |

| Common stock, 750,000,000 shares authorized, $.0001 par value 157,230,237 share issued and outstanding as of 03/31/20 and 136,553,955 shares issued and outstanding as of 12/31/19 | 15,723 | 13,655 |

| Additional paid in capital | 12,404,684 | 11,390,844 |

| Accumulated deficit | (11,741,359) | (11,666,289) |

|

|

|

|

| Total stockholders' deficit | 681,071 | (259,238) |

|

|

|

|

| Total liabilities and stockholders' deficit | $1,611,143 | $397,845 |

See accompanying notes to consolidated financial statements

3

BULLFROG GOLD CORP.

CONSOLIDATED STATEMENTS OF OPERATIONS

FOR THE THREE MONTHS ENDED MARCH 31, 2020 AND 2019

(unaudited)

|

| Three Months Ended | ||

|

| 3/31/20 |

| 3/31/19 |

|

|

|

|

|

| Revenue | $0 |

| $0 |

|

|

|

|

|

| Operating expenses |

|

|

|

| General and administrative | 183,808 |

| 317,231 |

| Exploration, evaluation and project expense | 43,689 |

| 45,691 |

|

|

|

|

|

| Total operating expenses | 227,497 |

| 362,922 |

|

|

|

|

|

| Net operating loss | (227,497) |

| (362,922) |

|

|

|

|

|

| Interest expense | (19,064) |

| (17,242) |

| Revaluation of warrant liability | 171,491 |

| 0 |

|

|

|

|

|

| Net loss | $(75,070) |

| $(380,164) |

|

|

|

|

|

| Weighted average common shares outstanding - basic and diluted | 151,424,059 |

| 113,198,118 |

|

|

|

|

|

| Loss per common share - basic and diluted | $0.00 |

| $0.00 |

See accompanying notes to consolidated financial statements

4

BULLFROG GOLD CORP.

CONSOLIDATED STATEMENTS OF STOCKHOLDERS' EQUITY (DEFICIT)

FOR THE THREE MONTHS ENDED MARCH 31, 2020 AND 2019

(unaudited)

|

| Preferred Stock Shares Issued |

| Preferred Stock |

| Common Stock Shares Issued |

| Common Stock |

| Additional Paid In Capital |

| Deficit Accumulated During the Exploration Stage |

| Total Stockholders' Equity (Deficit) |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| December 31, 2018 | 30,187,500 |

| $3,018 |

| 104,107,096 |

| $10,411 |

| $9,589,037 |

| $(10,070,364) |

| $(467,898) |

| Stock-based compensation, March 2019 | - |

| - |

| 900,000 |

| 90 |

| 80,910 |

| - |

| 81,000 |

| Private placement issued, February 2019 | - |

| - |

| 16,700,000 |

| 1,670 |

| 833,330 |

| - |

| 835,000 |

| Private placement issued, March 2019 | - |

| - |

| 5,848,000 |

| 584 |

| 291,816 |

| - |

| 292,400 |

| Net loss | - |

| - |

| - |

| - |

| - |

| (380,164) |

| (380,164) |

| March 31, 2019 | 30,187,500 |

| $3,018 |

| 127,555,096 |

| $12,755 |

| $10,795,093 |

| $(10,450,528) |

| $360,338 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| December 31, 2019 | 25,520,833 |

| $2,552 |

| 136,553,955 |

| $13,655 |

| $11,390,844 |

| $(11,666,289) |

| $(259,238) |

| Private placement issued, January 2020 | - |

| - |

| 15,384,615 |

| 1,539 |

| 1,418,151 |

| - |

| 1,419,690 |

| Warrant liability, January 2020 | - |

| - |

| - |

| - |

| (441,010) |

| - |

| (441,010) |

| Conversion of preferred stock, January 2020 | (1,000,000) |

| (100) |

| 1,000,000 |

| 100 |

| - |

| - |

| - |

| Stock options issued, January 2020 | - |

| - |

| - |

| - |

| 36,699 |

| - |

| 36,699 |

| Conversion of preferred stock, February 2020 | (4,291,667) |

| (429) |

| 4,291,667 |

| 429 |

| - |

| - |

| - |

| Net loss |

|

|

|

|

|

|

|

|

|

| (75,070) |

| (75,070) |

| March 31, 2020 | 20,229,166 |

| $2,023 |

| 157,230,237 |

| $15,723 |

| $12,404,684 |

| $(11,741,359) |

| $681,071 |

See accompanying notes to consolidated financial statements

5

BULLFROG GOLD CORP.

CONSOLIDATED STATEMENTS OF CASH FLOWS

FOR THE THREE MONTHS ENDED MARCH 31, 2020 AND 2019

(unaudited)

|

| Three Months Ended | ||

|

| 3/31/20 |

| 3/31/19 |

|

|

|

|

|

| Cash flows from operating activities |

|

|

|

| Net loss | $(75,070) |

| $(380,164) |

| Adjustments to reconcile net loss to net cash used in operating activities |

|

|

|

| Revaluation of warrant liability | (171,491) |

| 0 |

| Stock/options issued for services | 36,699 |

| 81,000 |

| Change in operating assets and liabilities: |

|

|

|

| Deposits | (2,763) |

| 0 |

| Other assets | 0 |

| (90,000) |

| Accounts payable | 1,953 |

| (165) |

| Related party payable | 1,517 |

| 2,550 |

| Net cash used in operating activities | (209,155) |

| (386,779) |

|

|

|

|

|

| Cash flows from financing activities |

|

|

|

| Proceeds from private placement of stock | 1,419,690 |

| 432,400 |

|

|

|

|

|

| Net decrease in cash | 1,210,535 |

| 45,621 |

|

|

|

|

|

| Cash, beginning of period | 44,595 |

| 620,949 |

|

|

|

|

|

| Cash, end of period | $1,255,130 |

| $666,570 |

See accompanying notes to consolidated financial statements

6

BULLFROG GOLD CORP.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

(unaudited)

NOTE 1 - NATURE OF BUSINESS AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Nature of Business

Bullfrog Gold Corp. (the “Company”) is a junior exploration company engaged in the acquisition and exploration of properties that may contain gold, silver and other metals in the United States. The Company’s target properties are those that have been the subject of historical exploration. The Company owns, controls or has acquired mineral rights on Federal patented and unpatented mining claims in the state of Nevada for the purpose of exploration and potential development of gold, silver and other metals on a total of approximately 5,250 acres. The Company plans to review opportunities and acquire additional mineral properties with current or historic precious and base metal mineralization with meaningful exploration potential.

The Company’s properties do not have any reserves. The Company plans to conduct exploration programs on these properties with the objective of ascertaining whether any of its properties contain economic concentrations of precious and base metals that are prospective for mining.

In March 2020 the World Health Organization declared coronavirus COVID-19 a global pandemic. This contagious disease outbreak, which has continued to spread, and any related adverse public health developments, has adversely affected workforces, economies, and financial markets globally, potentially leading to an economic downturn. It is not possible for the Company to predict the duration or magnitude of the adverse results of the outbreak and its effects on the Company’s business or ability to raise funds.

Basis of Presentation

The consolidated unaudited financial statements included in this Form 10-Q have been prepared in accordance with generally accepted accounting principles in the United States of America for interim financial information and with the instructions to Form 10-Q. Accordingly, these financial statements do not include all the disclosures required by U.S. generally accepted accounting principles for complete financial statements. These consolidated unaudited interim financial statements should be read in conjunction with the audited financial statements for the fiscal year ended December 31, 2018 in our Annual Report on Form 10-K. The financial information furnished herein reflects all adjustments consisting of normal, recurring adjustments which, in the opinion of management, are necessary for a fair presentation of our financial position, the results of operations and cash flows for the periods presented. Operating results for the three months ended March 31, 2020 are not necessarily indicative of results for future quarters or periods in the fiscal year ending December 31, 2020.

Principles of Consolidation

The consolidated financial statements include the accounts of Bullfrog Gold Corp. and its wholly owned subsidiaries, Standard Gold Corp. (“Standard Gold”) a Nevada corporation and Rocky Mountain Minerals Corp. (“Rocky Mountain Minerals” or “RMM”) a Nevada corporation. All significant inter-entity balances and transactions have been eliminated in consolidation.

Going Concern and Management’s Plans

The Company has incurred losses from operations since inception and has an accumulated deficit of approximately $11,741,000 as of March 31, 2020. The Company’s consolidated financial statements have been prepared on the basis that it is a going concern, which contemplates the realization of assets and the satisfaction of liabilities in the normal course of business. The Company’s continuation as a going concern is dependent upon attaining profitable operations which will require generating revenue. This raises substantial doubt about the Company's ability to continue as a going concern within one year from the issuance of these consolidated financial statements.

The Company has not generated any revenues since its inception and does not expect to generate any revenues in 2020. Should we be unable to continue as a going concern, we may be unable to realize the carrying value of our assets and to meet our obligations as they become due. To continue as a going concern, we will need to raise additional capital. However, we have no commitment from any party to provide additional capital and there is no assurance that such funding will be available when needed, or if available, that its terms will be favorable or acceptable to us.

7

Cash and Concentration

The Company considers all highly liquid investments with a maturity of three months or less when acquired to be cash equivalents. The Company places its cash with a high credit quality financial institution. The Company’s account at this institution is insured by the Federal Deposit Insurance Corporation up to $250,000. At March 31, 2020, the Company’s cash balance was approximately $1,255,000. To reduce its risk associated with the failure of such financial institution, the Company will evaluate at least annually the rating of the financial institution in which it holds deposits.

Use of Estimates

The preparation of financial statements in conformity with accounting principles generally accepted in the United States of America requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Mineral Property Acquisition and Exploration Costs

Mineral property exploration costs are expensed as incurred until economic reserves are quantified. To date, the Company has not established any proven or probable reserves on its mineral properties. Costs of lease, exploration, carrying and retaining unproven mineral lease properties are expensed as incurred. The Company has chosen to expense all mineral exploration costs as incurred given that it is still in the exploration stage. Once the Company has identified proven and probable reserves in its investigation of its properties and upon development of a plan for operating a mine, it would enter the development stage and capitalize future costs until production is established. When a property reaches the production stage, the related capitalized costs will be amortized over the estimated life of the probable-proven reserves. When the Company has capitalized mineral properties, these properties will be periodically assessed for impairment of value and any diminution in value. To date, the Company has not established the commercial feasibility of any exploration prospects; therefore, all exploration costs are being expensed. Costs of property acquisitions are being capitalized.

Fair Value of Financial Instruments

Fair value is defined as the exchange price that would be received for an asset or paid to transfer a liability (an exit price) in the principal or most advantageous market for the asset or liability in an orderly transaction between market participants on the measurement date. There are three levels of inputs that may be used to measure fair value:

Level 1 - Valuation based on quoted market prices in active markets for identical assets and liabilities.

Level 2 - Valuation based on quoted market prices for similar assets and liabilities in active markets.

Level 3 - Valuation based on unobservable inputs that are supported by little or no market activity, therefore requiring management’s best estimate of what market participants would use as fair value.

Income Taxes

Income taxes are accounted for under the asset and liability method in accordance with ASC 740, “Income Taxes”. Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial carrying amounts of existing assets and liabilities and their respective tax bases as well as operating loss and tax credit carry forwards. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the periods in which those temporary differences are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in income in the period that includes the enactment date. Deferred tax assets are reduced by a valuation allowance to the extent that the recoverability of the asset is unlikely to be recognized.

The Company reports a liability, if any, for unrecognized tax benefits resulting from uncertain tax positions taken, or expected to be taken, in an income tax return. The Company has elected to classify interest and penalties related to unrecognized income tax benefits, if and when required, as part of income tax expense in the statement of operations. No liability has been recorded for uncertain income tax positions, or related interest or penalties as of March 31, 2020 and December 31, 2019. The periods ended December 31, 2019, 2018, 2017 and 2016 are open to examination by taxing authorities.

8

Long Lived Assets

The Company assesses the impairment of long-lived assets whenever events or changes in circumstances indicate that the carrying value may not be recoverable. When the Company determines that the carrying value of long-lived assets may not be recoverable based upon the existence of one or more indicators of impairment and the carrying value of the asset cannot be recovered from projected undiscounted cash flows, the Company records an impairment charge. The Company measures any impairment based on a projected discounted cash flow method using a discount rate determined by management to be commensurate with the risk inherent in the current business model. Significant management judgment is required in determining whether an indicator of impairment exists and in projecting cash flows.

Preferred Stock

The Company accounts for its preferred stock under the provisions of the ASC on Distinguishing Liabilities from Equity, which sets forth the standards for how an issuer classifies and measures certain financial instruments with characteristics of both liabilities and equity. This standard requires an issuer to classify a financial instrument that is within the scope of the standard as a liability if such financial instrument embodies an unconditional obligation to redeem the instrument at a specified date and/or upon an event certain to occur. The Company has determined that its preferred stock does not meet the criteria requiring liability classification as its obligation to redeem these instruments is not based on an event certain to occur. Future changes in the certainty of the Company’s obligation to redeem these instruments could result in a change in classification.

Stock-Based Compensation

Stock-based compensation is accounted for based on the requirements of the Share-Based Payment Topic of ASC 718 which requires recognition in the consolidated financial statements of the cost of employee and director services received in exchange for an award of equity instruments over the period the employee or director is required to perform the services in exchange for the award (presumptively, the vesting period). This ASC also requires measurement of the cost of employee and director services received in exchange for an award based on the grant-date fair value of the award.

The estimated fair value of each stock option as of the date of grant was calculated using the Black-Scholes pricing model. The Company estimates the volatility of its common stock at the date of grant based on Company stock price history. The Company determines the expected life based on the simplified method given that its own historical share option exercise experience does not provide a reasonable basis for estimating expected term. The Company uses the risk-free interest rate on the implied yield currently available on U.S. Treasury issues with an equivalent remaining term approximately equal to the expected life of the award. The Company has never paid any cash dividends on its common stock and does not anticipate paying any cash dividends in the foreseeable future. The shares of common stock subject to the stock-based compensation plan shall consist of unissued shares, treasury shares or previously issued shares held by any subsidiary of the Company, and such number of shares of common stock are reserved for such purpose.

Derivative Financial Instruments

The Company accounts for derivative instruments in accordance with Financial Accounting Standards Board (“FASB”) ASC 815, Derivatives and Hedging (“ASC 815”), which requires additional disclosures about the Company’s objectives and strategies for using derivative instruments, how the derivative instruments and related hedged items are accounted for, and how the derivative instruments and related hedging items affect the financial statements. The Company does not use derivative instruments to hedge exposures to cash flow, market or foreign currency risk. Terms of convertible debt and equity instruments are reviewed to determine whether or not they contain embedded derivative instruments that are required under ASC 815 to be accounted for separately from the host contract, and recorded on the balance sheet at fair value. The fair value of derivative liabilities, if any, is required to be revalued at each reporting date, with corresponding changes in fair value recorded in current period operating results. Pursuant to ASC 815, an evaluation of specifically identified conditions is made to determine whether the fair value of warrants issued is required to be classified as equity or as a derivative liability.

9

Net Loss per Common Share

The Company incurred net losses during the three months ended March 31, 2020 and 2019. As such, the Company excluded the following from computation as the effect would be anti-dilutive:

|

| 3/31/20 |

| 3/31/19 |

| Stock options | 9,850,000 |

| 9,500,000 |

| Warrants | 30,081,058 |

| 21,474,000 |

| Preferred stock | 20,229,166 |

| 25,520,833 |

Risks and Uncertainties

Since our formation, we have not generated any revenues. As an early stage company, we are subject to all the risks inherent in the initial organization, financing, expenditures, complications and delays inherent in a new business. Our business is dependent upon the implementation of our business plan. There can be no assurance that our efforts will be successful or that we will ultimately be able to generate revenue or attain profitability.

Natural resource exploration, and exploring for gold, is a business that by its nature is very speculative. There is a strong possibility that we will not discover gold or any other mineralization which can be mined or extracted at a profit. Even if we do discover gold or other deposits, the deposit may not be of the quality or size necessary for us or a potential purchaser of the property to make a profit from mining it. Few properties that are explored are ultimately developed into producing mines. Unusual or unexpected geological formations, geological formation pressures, fires, power outages, labor disruptions, flooding, explosions, cave-ins, landslides and the inability to obtain suitable or adequate machinery, equipment or labor are just some of the many risks involved in mineral exploration programs and the subsequent development of gold deposits.

Our business is exploring for gold and other minerals. In the event that we discover commercially exploitable gold or other deposits, we will not be able to generate any revenue from such discoveries unless the gold or other minerals are actually mined, or we sell all or a part of our interest. Accordingly, we will need to find some other entity to mine our properties on our behalf, mine them ourselves or sell our rights to mine to third parties.

Mining operations in the United States are subject to many different federal, state and local laws and regulations, including stringent environmental, health and safety laws. In the event we assume any operational responsibility for mining our properties, we may be unable to comply with current or future laws and regulations, which can change at any time. Changes to these laws may adversely affect any of our potential mining operations. Moreover, compliance with such laws may cause substantial delays and require capital outlays greater than those we anticipate, adversely affecting any potential mining operations. Our future mining operations, if any, may also be subject to liability for pollution or other environmental damage. We may choose to not be insured against this risk because of high insurance costs or other reasons.

Recent Accounting Pronouncements

There are several new accounting pronouncements issued by the FASB which are not yet effective. Management does not believe any of these accounting pronouncements will be applicable and therefore will not have a material impact on the Company's financial position or operating results.

NOTE 2 - STOCKHOLDER’S EQUITY

Recent Sales of Unregistered Securities

On February 12, 2019 and March 27, 2019, the Company sold an aggregate of 16,700,000 Units and 5,848,000 Units, respectively, for gross proceeds to the Company of $835,000 ($695,000 of which was received in 2018 and included in liabilities on the consolidated balance sheet) and $292,400, respectively to accredited investors pursuant to a subscription agreement. Each Unit was sold for a purchase price of $0.05 per Unit and consisted of: (i) one share of the Company’s common stock and (ii) a two-year warrant to purchase 50% of the number of shares of common stock purchased at an exercise price of $0.10 per share. The warrants were evaluated for purposes of classification between liability and equity. The warrants do not contain features that would require a liability classification and are therefore considered equity.

10

The Black Scholes pricing model was used to estimate the fair value of $415,019 of the warrants with the following inputs:

| Warrants | Exercise Price | Term | Volatility | Risk Free Interest Rate | Fair Value |

| 11,274,000 | $0.10 | 2 years | 109.0% | 2.5% | $415,019 |

Using the fair value calculation, the relative fair value between the common stock and the warrants was calculated to determine the warrants’ recorded equity amount of $232,287 accounted for in additional paid in capital.

In March 2019, the Company issued 900,000 shares of common stock for consulting services performed in the three months ended March 31, 2019 valued at $0.09 per share and an aggregate of $81,000.

In April 2019, the Company issued 900,000 shares of common stock for consulting services performed in the three months ended June 30, 2019 valued at $0.14 per share and an aggregate of $126,000.

In August 2019, the Company issued 900,000 shares of common stock for consulting services performed in the three months ended September 30, 2019 valued at $0.11 per share and an aggregate of $99,000.

In October 2019, the Company issued 1,500,000 shares of common stock for executive and director services valued at $0.17 per share, for an aggregate of $255,000.

In October 2019, the Company issued 132,192 shares of common stock for consulting services performed valued at $0.13 per share and an aggregate of $17,185.

In November 2019, the Company issued 900,000 shares of common stock for consulting services performed in the three months ended December 31, 2019 valued at $0.11 per share and an aggregate of $99,000.

On January 16, 2020, the Company sold an aggregate of 15,384,615 Units for gross proceeds to the Company of CAD$2,000,000 to accredited investors pursuant to a subscription agreement. Each Unit was sold for a purchase price of CAD$0.13 per Unit and consisted of: (i) one share of the Company’s common stock and (ii) a two-year warrant (the “2020 Warrants”) to purchase 50% of the number of shares of common stock purchased at an exercise price of CAD$0.20 per share. In addition, the Company paid a total of CAD$118,918 for finder's fees on subscriptions under the Offering, together with 914,750 share purchase warrants (the “Finder Warrants”). Each Finder Warrant entitles the holder to acquire one share of common stock at an exercise price of CAD$0.20 per share for a period of 24 months from the date of issuance.

The Finder Warrants were evaluated for purposes of classification between liability and equity. The warrants do not contain features that would require a liability classification and are therefore considered equity. The Black Scholes pricing model was calculated in US dollars to estimate the fair value of $44,858 of the warrants with the following inputs:

| Warrants | Exercise Price | Term | Volatility | Risk Free Interest Rate | Fair Value |

| 914,750 | $0.15 | 2 years | 113.5% | 1.6% | $44,858 |

Convertible Preferred Stock

In August 2011, the Board of Directors designated 5,000,000 shares of Preferred Stock as Series A Preferred Stock. Each share of Series A Preferred Stock is convertible into one share of common stock at the option of the preferred holder. The Series A Preferred Stock is not entitled to receive dividends and does not possess redemption rights. The Company is prohibited from effecting the conversion of the Series A Preferred Stock to the extent that, as a result of the conversion, the holder of such shares would beneficially own more than 4.99% (or, if this limitation is waived by the holder upon no less than 61 days prior notice to us, 9.99%) in the aggregate of the issued and outstanding shares of our common stock. The holders of the Company’s Series A Preferred Stock are also entitled to certain liquidation preferences upon the liquidation, dissolution or winding up of the business of the Company.

11

In October 2012, the Board of Directors designated 5,000,000 shares of Preferred Stock as Series B Preferred Stock. In July 2016, the Board of Directors increased the total Series B Preferred Stock designated to 45,000,000. Each share of Series B Preferred Stock is convertible into one share of common stock at the option of the preferred holder. The Series B Preferred Stock is not entitled to receive dividends and does not possess redemption rights. The Company is prohibited from effecting the conversion of the Series B Preferred Stock to the extent that, as a result of the conversion, the holder of such shares would beneficially own more than 4.99% (or, if this limitation is waived by the holder upon no less than 61 days prior notice to us, 9.99%) in the aggregate of the issued and outstanding shares of our common stock. For a period of 24 months from the issue date, the holder of Series B Preferred Stock is entitled to price protection as determined in the subscription agreement. The Company has evaluated this embedded lower price issuance feature in accordance with ASC 815 and determined that is clearly and closely related to the host contract and is therefore accounted for as an equity instrument.

As of March 31, 2020, the Company had outstanding 20,229,166 shares of Series B Preferred Stock.

Common Stock Options

There were a total of 350,000 options granted in January 2020 to Tyler Minnick, CFO. These options issued are nonqualified stock options and were 100% vested on grant date. All expense related to these stock options has been recognized in 2020.

The Black Scholes option pricing model was used to estimate the aggregate fair value of $36,699 with the following inputs:

| Options | Exercise Price | Term | Volatility | Risk Free Interest Rate | Fair Value |

| 350,000 | $0.11 | 6 years | 160.4% | 1.83% | $36,699 |

A summary of the stock options as of March 31, 2020 and changes during the periods are presented below:

|

| Number of Options | Weighted Average Exercise Price | Weighted Average Remaining Contractual Life (Years) | Aggregate Intrinsic Value |

| Balance at December 31, 2018 | 9,500,000 | $0.083 | 7.70 | - |

| Granted | - | - | - | - |

| Exercised | - | - | - | - |

| Forfeited | - | - | - | - |

| Canceled | - | - | - | - |

| Balance at December 31, 2019 | 9,500,000 | $0.083 | 6.70 | $382,500 |

| Exercised | - | - | - | - |

| Forfeited | - | - | - | - |

| Canceled | - | - | - | - |

| Issued | 350,000 | - | - | - |

| Balance at March 31, 2020 | 9,850,000 | $0.084 | 6.46 | $247,500 |

| Options exercisable at March 31, 2020 | 9,850,000 | $0.084 | 6.46 | $247,500 |

Total outstanding warrants of 30,081,058 as of March 31, 2020 were as follows:

| Warrants Issued | Exercise Price | Expiration Date |

| 10,200,000 | $0.15 | May 2020 |

| 8,350,000 | $0.10 | February 2021 |

| 2,924,000 | $0.10 | March 2021 |

| 8,607,058 | CAD$0.20 | January 2022 |

12

NOTE 3 - DERIVATIVE FINANCIAL INSTRUMENTS

The 2020 Warrants have an exercise price in Canadian dollars while the Company’s functional currency is US dollars. Therefore, in accordance with ASU 815 - Derivatives and Hedging, the 2020 Warrants have a derivative liability value.

The value of the 2020 Warrants of $441,010 has been calculated on the date of issuance of January 16, 2020 using Black-Scholes valuation technique. During the three months ended March 31, 2020, there was a gain on the warrant liability of $171,491 and the value was reduced to $269,519 with the following assumptions:

|

| 1/16/20 | 3/31/20 |

| Fair market value of common stock | $0.11 | $0.08 |

| Exercise price | $0.15 | $0.14 |

| Term | 2 Years | 1.8 Years |

| Volatility range | 113.5% | 119.6% |

| Risk-free rate | 1.58% | 0.23% |

NOTE 4 - RELATED PARTY

As of March 31, 2020, and December 31, 2019, the Company has a related party payable with David Beling, CEO and President, of $637,292 and $635,775, respectively. This amount at March 31, 2020 consists of $195,902 of expense reports plus interest of $161,781 and salary of $191,667 plus interest of $87,942. Interest is accrued at a rate of 1% per month.

On January 7, 2020, the Board of Directors approved issuance of 350,000 stock options to Tyler Minnick, CFO, with an exercise price of $0.11 per share determined by the closing price of the Company’s common stock as of January 7, 2020. The options are 100% percent vested as of the grant date. In addition, Mr. Minnick received approximately $13,000 in consulting fees from the Company.

NOTE 5 - COMMITMENTS

On March 23, 2015, Rocky Mountain Minerals Corp. (“RMM”) a wholly owned subsidiary of the Company, entered into a Mineral Lease and Option to Purchase Agreement (the “Barrick Agreement”) with Barrick Bullfrog Inc. (“Barrick Bullfrog”) involving patented mining claims, unpatented mining claims, and mill site claims (collectively, the “Properties”) located approximately four miles west of Beatty, Nevada. In order for RMM to exercise the option to acquire a 100% interest in and to the properties, RMM must provide thirty-days advance notice to Barrick Bullfrog and, thereafter, at the mutually agreed upon closing date, the Company will issue to Barrick Gold 3,230,000 shares of its common stock. The Company has not exercised the option to date. These Properties are strategically located adjacent to the Company’s Bullfrog Gold Project and include two patents that cover the southwest half of the Montgomery-Shoshone (M-S) open pit gold mine. In October 2014 the Company optioned the northeast half of the M-S pit and now controls the entire pit, however no payment is due to Barrick Bullfrog for this.

RMM shall expend as minimum work commitments (the “Project Work Commitments”) for the benefit of the Properties prior to the 5th anniversary of the effective date per the schedule below. As the Properties are part of a logical land and mining unit, work performed on any of the Properties will be counted toward Rocky Mountain’s Project Work Commitment. In any given year, if Rocky Mountain incurs Project Work Commitment expenditures in excess of the Project Work Commitment for that year, then up to 20% of the excess expenditures, as measured against the Project Work Commitment for that year, shall be credited toward the minimum Project Work Commitment expenditures for the following years. In any given year, if Rocky Mountain incurs expenditures below the required Project Work Commitment for that year, then up to 20% of the expenditure shortfall, as measured against the Project Work Commitment for that year, may be carried forward by Rocky Mountain and added to the minimum Project Work Commitment expenditures for the following year. In such case, Rocky Mountain shall make cash payments to Barrick Bullfrog equal to the remaining expenditure shortfall for the year.

13

Further, if Rocky Mountain incurs expenditures below the required Project Work Commitment for a given year but elects not to carry forward any shortfall to the subsequent year, then Rocky Mountain shall make cash payments to Barrick Bullfrog equal to the expenditure shortfall for the year; provided however, that if Rocky Mountain elects not to carry forward any shortfall such payment shall not be due if Rocky Mountain terminates the agreement before the end of the year with the expenditure shortfall. If a party fails to keep or perform any covenant or condition of the agreement to be kept or performed by that party, the other party may provide written notice to first party specifying such default. If the Company does not, within 15 days after it has received notice of default with respect to the share delivery, or any party within 30 days after it has received notice of any other default, cure the default, the party issuing the notice of default may terminate the agreement by delivering to the other party written notice of such termination and exercising any other rights and remedies permitted by law or equity. These work commitments, as of March 31, 2020, have been satisfactorily met and include a 5% management fee, but exclude corporate expenses of RMM.

| Anniversary of Effective Date | Minimum Project Work Commitment ($) |

| First (March 2016) | 100,000 |

| Second (March 2017) | 200,000 |

| Third (March 2018) | 300,000 |

| Fourth (March 2019) | 400,000 |

| Fifth (March 2020) | 500,000 (amended to September 23, 2020) |

On May 21, 2019 the Barrick Agreement was amended whereby work commitments for the fifth anniversary and the total of $1.5 million were extended to September 23, 2020. The Company has paid the required work commitments with a final work commitment of $561,762.

On July 1, 2017, RMM entered a 30-year Mineral Lease (the “Lunar Lease”) with Lunar Landing, LLC (“Lunar”) involving 24 patented mining claims situated in the Bullfrog Mining District, Nye County, Nevada. Lunar owns a 100% undivided interest in the mining claims.

Under the Lunar Lease, RMM shall expend as minimum work commitments of $50,000 per year starting in 2017 until a cumulative of $500,000 of expense has been incurred. If RMM fails to perform its obligations under the Lunar Lease, and in particular fails to make any payment due to Lunar thereunder, Lunar may declare RMM in default by giving RMM written notice of default which specifies the obligation(s) which RMM has failed to perform. If RMM fails to remedy a default in payment within fifteen (15) days of receiving the notice of default or fails to remedy or commence to remedy any other default within thirty (30) days of receiving notice, Lunar may terminate the Lunar Lease and RMM shall peaceably surrender possession of the properties to Lunar. Notice of default or of termination shall be in writing and served in accordance with the Lunar Lease. RMM has made all required payments and has paid Lunar $58,000 as of March 31, 2020 and makes lease payments on the following schedule:

| Years Ending December 31 | Annual Lease Payment ($) |

| 2019-2022 | 16,000 |

| 2023-2027 | 21,000 |

| 2028-2032 | 25,000 |

| 2033-2037 | 30,000 |

| 2038-2042 | 40,000 |

| 2043-2047 | 45,000 |

On October 29, 2014, RMM entered into an Option Agreement (the “Mojave Option”) with Mojave Gold Mining Corporation (“Mojave”). Mojave holds the purchase rights to 100% of 12 patented mining claims located in Nye County, Nevada. This property is contiguous to the Company’s Bullfrog Project and covers approximately 156 acres, including the northeast half of the Montgomery-Shoshone (M-S) pit mined by Barrick Gold in the 1990’s.

Mojave granted to RMM the sole and immediate working right and option with respect to the property until the 10th anniversary of the closing date, to earn a 100% interest in and to the property free and clear of all charges encumbrances and claims, except a sliding scale Net smelter return (or NSR) royalty.

14

In order to maintain in force, the working right and option granted to it, and to exercise the Mojave Option, RMM issued Mojave 750,000 shares of Company common stock and paid $16,000 in October 2014, and RMM must pay to Mojave a total of $190,000 over the next 10 years of which the Company has made all required payments and paid $80,000 as of December 31, 2019. Future payments will be due as follows:

| Due Date | Amount |

| October 2019 | $20,000 |

| October 2020 | $25,000 |

| October 2021 | $25,000 |

| October 2022 | $30,000 |

| October 2023 | $30,000 |

NOTE 6 - SUBSEQUENT EVENTS

None.

15

ITEM 2 - MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Certain statements in this Management's Discussion and Analysis (“MD&A”), other than purely historical information, including estimates, projections, statements relating to our business plans, objectives and expected operating results, and the assumptions upon which those statements are based, are “forward-looking statements”. Forward-looking statements generally can be identified by the use of forward-looking terminology such as “may,” “would,” “expect,” “intend,” “could,” “estimate,” “should,” “anticipate,” or “believe,” and similar expressions. Forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties which may cause actual results to differ materially from the forward-looking statements. We undertake no obligation to update or revise publicly any forward-looking statements, whether as a result of new information, future events, or otherwise, except as may be required under applicable law. Readers should carefully review the risk factors and related notes included under Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2019 filed with the Securities and Exchange Commission on March 13, 2020.

The following MD&A is intended to help readers understand the results of our operation and financial condition, and is provided as a supplement to, and should be read in conjunction with, our Interim Unaudited Financial Statements and the accompanying Notes to Interim Unaudited Financial Statements under Part 1, Item 1 of this Quarterly Report on Form 10-Q.

Unless otherwise indicated or unless the context otherwise requires, all references in this document to “we,” “us,” “our,” the “Company,” and similar expressions refer to Bullfrog Gold Corp., and depending on the context, its subsidiaries.

Company History and Recent Events

Bullfrog Gold Corp. was incorporated under the laws of the State of Delaware on July 23, 2007 as Kopr Resources Corp. On July 21, 2011, the Company changed its name to “Bullfrog Gold Corp.” The Company is in the exploration stage of its business.

Company Overview

We are an exploration stage company engaged in the acquisition and exploration of properties that may contain gold and other mineralization primarily in the United States.

Bullfrog Project

The Bullfrog Gold Project lies approximately 4 miles west of the town of Beatty, Nevada and 120 miles northwest of Las Vegas, Nevada. In 2011, Standard Gold Corp. (“Standard Gold”) a wholly owned subsidiary of the Company, initially acquired a 100% right, title and interest in 79 lode claims and 2 patented claims that contain approximately 1,600 acres subject to a 3% net smelter royalty.

On October 29, 2014, Rocky Mountain Minerals Corp. (“RMM”) a wholly owned subsidiary of the Company, entered into an Option Agreement (the “Option”) with Mojave Gold Mining Corporation (“Mojave”). Mojave holds the purchase rights to 100% of 12 patented mining claims located in Nye County, Nevada. This property is contiguous to the Company’s Bullfrog Project and covers approximately 156 acres, including the northeast half of the Montgomery-Shoshone (M-S) pit mined by Barrick Gold in the 1990’s.

Mojave granted to RMM the sole and immediate working right and option with respect to the property until the 10th anniversary of the closing date, to earn a 100% interest in and to the property free and clear of all charges encumbrances and claims, except a sliding scale Net smelter return (or NSR) royalty.

In order to maintain in force, the working right and Option granted to it, and to exercise the Option, the Company issued Mojave 750,000 shares of common stock and paid Mojave $16,000 in October 2014. In addition, to exercise the option, RMM must pay to Mojave a total of $190,000 over the next 10 years. For reference, Barrick Bullfrog Inc. (“Barrick”) terminated a lease on these patents after they ceased operations in late 1999.

16

On March 23, 2015, RMM entered into a Mineral Lease and Option to Purchase Agreement with Barrick involving 6 patented mining claims, 20 unpatented mining claims, and 8 mill site claims located approximately four miles west of Beatty, Nevada and covering approximately 444 acres (the “Barrick Properties”). These Barrick Properties are strategically located adjacent to the Company’s Bullfrog Gold Project and include two patents that cover the southwest half of the M-S open pit from which Barrick produced approximately 220,000 ounces of gold by the late 1990’s. Underground mining in the early 1900’s produced approximately 70,000 ounces of gold from the M-S deposit. Also included in the agreement is the northern one third of the main Bullfrog deposit where Barrick mined approximately 2.1 million additional ounces by open pit and underground methods. In addition to prospective adjacent lands, these acquisitions provide the potential to expand the M-S deposit along strike and at depth and in the northern part of the main Bullfrog deposit.

The Company also has access to Barrick’s substantial data base within a 1.5-mile radius of the leased lands to further advance its exploration and development programs. To maintain the lease and option, the Company was required to spend $1.5 million dollars within five years on the Barrick Properties and to exercise the option the Company must issue to Barrick 3.25 million shares of the Company’s common stock. On May 21, 2019 the Barrick Agreement was amended whereby work commitments for the fifth anniversary and the total of $1.5 million were extended to September 23, 2020. The final work commitment has been accounted at $561,762. The Company will also provide a 2% gross royalty on production from the Barrick Properties. Overriding royalties of 5% net smelter returns and 5% gross proceeds are respectively limited to three claims and two patents in the main Bullfrog pit area. Barrick has retained a back-in right to reacquire a 51% interest in the Barrick Properties, subject to definition of a mineral resource on the Barrick Properties meeting certain criteria and reimbursing the Company in an amount equal to two and one-half times Company expenditures on the Barrick Properties.

On July 1, 2017, RMM entered a 30-year Mineral Lease (the “Lunar Lease”) with Lunar Landing, LLC. (“Lunar”), the owner of 24 patented mining claims situated in the Bullfrog Mining District, Nye County, Nevada.

On January 29, 2018 the Company purchased two patented claims, thereby eliminating minor constraints to expand the Bullfrog pit to the north.

In August 2018 and December 2018, the Company staked and duly recorded an additional 46 unpatented claims, for a total of 134 claims staked by the Company.

Significant drilling is required to test projections of mineralized trends and structures that extend for considerable distances to the north and east of the M-S pit on the original lands acquired by the Company in 2011. Located east of the M-S pit is an area 700 meters by 1,300 meters in which there is only one shallow hole from which there is no data available. Only a small portion of this area may be prospective, but we believe the area warrants additional study and exploration drilling.

There is only one drill hole located about 150 meters northeast of the M-S pit limit and another hole 1,000 meters northeast of the pit along strike of a major geologic structure. In this regard, the Company’s lands extend nearly 5,000 meters north-northeast of the pit and there has been very little drilling in this area, even though several structures have been mapped by Barrick and others.

17

Barrick drilled twelve deep holes in the M-S area ranging from 318 meters to 549 meters. Notable mineral intercepts from four holes below the central part of the pit are summarized below:

|

| Intercept Data, Meters | Gold | |

| Hole No. | Thickness | Under Pit | g/t |

| 717 | 51.8 | 70 | 1.35 |

|

| 18.3 | 135 | 0.59 |

|

| 15.2 | 150 | 0.68 |

|

| 160.0 | 180 | 0.96 |

| 732 | 10.7 | 200 | 0.84 |

|

| 79.2 | 330 | 0.74 |

| 733 | 12.2 | 130 | 1.14 |

|

| 13.7 | 220 | 0.75 |

|

| 29.0 | 250 | 0.70 |

| 734 | 4.6 | 15 | 6.03 |

|

| 21.3 | 70 | 1.43 |

|

| 22.9 | 130 | 0.89 |

|

| 4.6 | 190 | 1.04 |

These results demonstrate that substantial amounts of gold occur in an exceptionally large epithermal system that has good potential for expansion and possibly higher grades at depth. Three of these intercepts are less than 75 meters below the existing pit. Two holes located 40 meters and 90 meters east of the 160-meter interval in hole #717 contained no significant mineralization at this depth, whereas the 29 meters of mineral in hole #733 is 60 meters west and the mineral zone is open to the north, south and west.

For reference, Barrick terminated all mining and milling operations in the autumn of 1999 when their cash production costs exceeded gold prices that averaged less than $300 per ounce for the year and reached a low of $258/oz in August 1999. The economic margins for heap leaching lower grades at current gold prices near $1500/oz are deemed better than in 1999, and we believe the Company is positioned to explore such opportunities. Furthermore, Barrick never controlled or had access to a patented claim on the immediate east and north limits of the M-S pit, but this patent is owned by the Company.

Starting in 2015, the Company has studied Barrick’s entire electronic data base and much of their paper data base obtained from their Elko, Nevada and Salt Lake City, Utah offices. On August 9, 2017, an independent engineering firm issued estimates of mineralized materials totally contained on Company controlled lands. In January 2018 the Company purchased a patent that removed all remaining constraints for pit mining the mineralization, see summary below:

Mineralized Material Estimates

|

| Cutoff | Mineral T | Grade | Gold Oz | Grade | Silver Oz | Waste T | W : Min. |

| Deposit | Gold g/t | Millions | Gold g/t | 000's | Silver g/t | 000's | Millions | Ratio |

| Bullfrog | 0.20 | 26.4 | 0.69 | 585 | 1.85 | 1,569 | 110 | 3.5 |

|

| 0.36 | 14.9 | 1.02 | 489 | 2.50 | 1,198 | 124 | 7.0 |

|

|

|

|

|

|

|

|

|

|

| M-S | 0.20 | 1.4 | 0.84 | 39 | 3.48 | 162 | 11 | 7.8 |

|

| 0.36 | 1.1 | 1.00 | 36 | 4.02 | 146 | 11 | 10.1 |

|

|

|

|

|

|

|

|

|

|

| Total | 0.20 | 27.8 | 0.70 | 624 | 1.93 | 1,731 | 121 | 4.3 |

|

| 0.36 | 16.0 | 1.02 | 525 | 2.60 | 1,344 | 135 | 8.4 |

“Mineralized material” as used in this quarterly report on Form 10-Q, although permissible under the Securities and Exchange Commission (“SEC”) Guide 7, does not indicate “reserves” by SEC standards. We cannot be certain that any part of the Company’s deposits will ever be confirmed or converted into SEC Industry Guide 7 compliant “reserves.” Investors are cautioned not to assume that all or any part of the mineralized material will be confirmed or converted into reserves or that mineralized material can be economically or legally extracted.

18

Input parameters used in the estimates are tabulated below:

Estimate Input Parameters

| Parameter | Input | Unit |

| Mining Cost - M & W | 2.25 | $/t |

| Processing Cost | 6.00 | $/t |

| General & Admin. | 1.60 | $/t |

| Refining Sales | 0.05 | $/t |

| Sell Cost | 10 | $/tr oz |

| Gold Recovery | 72 | % |

| Silver Recovery | 20 | % |

| Gold Price (3-yr average) | 1200 | $/tr oz |

| Pit Slopes | 45 | degrees |

Mineral estimates are in place and do not include recoveries from a proposed downstream heap leach/processing operation. The mineral estimates herein are consistent with the policies and standards of Canadian National Instrument 43-101 (“NI 43-101”).

The data base used for the estimates included 1,262 holes containing 155 miles of coring and drilling completed from 1983 through 1996 by Barrick and its predecessors. Assaying was performed by several accredited laboratories. Tetra Tech, Inc. (“Tetra Tech”) a recognized global provider of engineering, technical and construction management services with particular expertise in the mining sector, reviewed the data base in detail and found it to be of sufficient quality and quantity to estimate mineralized materials. A final NI 43-101 Technical Report is posted on the Company’s website.

The mineralized materials were estimated by the Golden, Colorado office of Tetra Tech. The estimates were prepared in accordance with requirements of NI 43-101 Standards of Disclosure for Mineral Projects. The technical work, analysis and findings were completed or directly supervised by Rex Bryan, PhD, who is as an independent "Qualified Person" as defined by NI 43-101. Mr. Bryan has also reviewed and approved the information in the June 27, 2017 news release.

An internal pit cutoff ranging between 0.20 to 0.36 g/t in the same base case pit shell provides an additional 99,000 ounces of gold averaging 0.26 g/t that is planned to be heap leached at a run-of-mine or uncrushed size. Thus, 624,000 ounces of mineralized materials grading 0.70 g/t are within this base case pit. From June 2017 through December 2018 the Company leased 24 patents and staked 134 mining claims to cover exploration targets and potential sites for leach pads and other project facilities.

For reference, the Company estimated in April 2016 a preliminary mineral inventory of 470,000 ounces grading 0.89 g/t using a nominal 0.3 g/t cutoff. In comparison, the mineralized materials of 624,000 ounces represents a 33% increase in gold ounces. As the existing pit slopes are up to 52 degrees and stable after 21 years of no mining, the 45-degree input by Tetra Tech is conservative and provides upside in final pit designs. It is also noted that Barrick terminated all mining by the end of 1998 and mill production in early 1999 when gold prices were less than $300 per ounce. However, economic margins for gold mining in general are now much better, particularly with the application of low-cost heap leaching methods. Barrick also used gold cut-off grades of 0.5 g/t in the pits and 3.0 g/t in the underground mine.

Metallurgy

In addition to extensive testing and operations using conventional milling at a fine size of -100 mesh, the following relevant test work was completed with respect to heap leaching.

In 1986 St Joe column leached a 22-ton composite of minus 12-inch material grading 0.037 gold opt to simulate heap leaching material at a coarse run-of-mine (“ROM”) size and recovered 49% in 59 days of leaching, which they projected to 54% for leaching 90 days.

19

In 1994 Kappes Cassiday of Reno, NV performed simulated heap leach column tests on 250 kg samples with results as follows:

| Size, inch | -1.5 | -3/8 |

| Calc. Head, gold opt | .035 | .029 |

| Rec., % | 71.4 | 75.9 |

| Leach time, days | 41 | 41 |

In 1995, Barrick performed a pilot heap leach test on 844 tons that were crushed to -½ inch and averaged 0.019 gold opt. In only 41 days of leaching, 67% of the gold was recovered while cyanide and lime consumptions were exceptionally low.

In 1986 St Joe column leached a 22-ton composite of minus 12-inch material grading 0.037 gold opt to simulate heap leaching material at a coarse run-of-mine (“ROM”) size and recovered 49% in 59 days of leaching, which they projected to 54% for leaching 90 days.

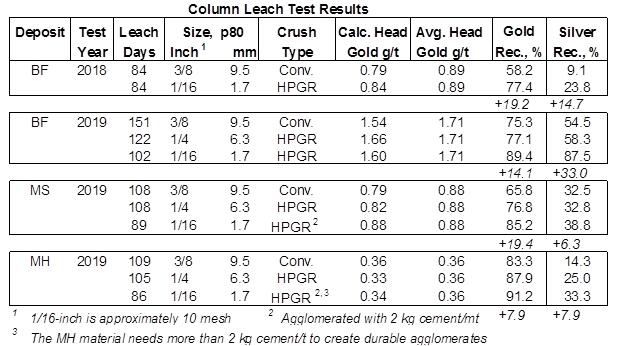

Starting in February 2018, the Company collected four bulk samples from the North Bullfrog and Montgomery-Shoshone pits and conducted extensive metallurgical tests using high pressure grinding rolls (HPGR’s) to compare leaching with conventional crushing equipment. HPGR’s are designed to produce a much finer product that also has much more micro-fractures in the particles thereby increasing leach recovery.

Below is a summary of BFGC’s four column leach test programs performed on the four bulk samples.

The HPGR column test programs on -1/16” leach feed recovered an average 85.8% of the gold compared to 70.7% from the conventional crushed tests sized at -3/8 inch. Results from hydraulic conductivity (load/permeability) testing of column leach residues from programs two and three indicate that cement agglomeration would not be required for heap leaching up to 200 feet high for a size coarser than 80%-1/16 inch feed. However, cement agglomeration is required for leaching 80% -1/16-inch up to 200 feet high.

It is notable that the brittle, rhyolite-hosted deposits in the BF area have very low clay contents that do not generate much additional fines during the sizing stages and they are particularly amenable to leaching fine sizes compared to most other epithermal gold deposits.

20

Results of Operations

Three Months Ended March 31, 2020 Compared to March 31, 2019

|

| Three Months Ended | ||

|

| 3/31/20 |

| 3/31/19 |

|

|

|

|

|

| Revenue | $0 |

| $0 |

|

|

|

|

|

| Operating expenses |

|

|

|

| General and administrative | 183,808 |

| 317,231 |

| Exploration, evaluation and project expense | 43,689 |

| 45,691 |

|

|

|

|

|

| Total operating expenses | 227,497 |

| 362,922 |

|

|

|

|

|

| Net operating loss | (227,497) |

| (362,922) |

|

|

|

|

|

| Interest expense | (19,064) |

| (17,242) |

| Revaluation of warrant liability | 171,491 |

| - |

|

|

|

|

|

| Net loss | $(75,070) |

| $(380,164) |

We are still in the exploration stage and have generated no revenues to date.

For the three months ending March 31, we incurred professional fees comprised of (1) accounting fees for annual audit and consulting for a total of $33,000 in 2020 compared to $28,000 in 2019, (2) legal fees for review of quarterly filings and general services for a total of $3,000 in 2020 and $0 in 2019 and (3) marketing and corporate services of $50,000 in 2020 compared to $230,000 spent in 2019. The 2019 marketing and corporate services includes 900,000 common shares the Company issued valued at $0.09 per share for a non-cash transaction valued at $81,000; and marketing and corporate development services of $149,000 to consultants. In addition, there was payroll expense of $27,000 for both 2020 and 2019.

The 2020 Warrants have an exercise price in Canadian dollars while the Company’s functional currency is US dollars. Therefore, in accordance with ASU 815 - Derivatives and Hedging, the 2020 Warrants have a derivative liability value. This liability value has no effect on the cash flow of the Company and does not represent a cash payment of any kind.

The value of the 2020 Warrants of $441,010 has been calculated on the date of issuance of January 16, 2020 using Black-Scholes valuation technique. During the three months ended March 31, 2020, there was a gain on the warrant liability of $171,491 and the value was reduced to $269,519.

There was a total of 350,000 options granted in January 2020 to Tyler Minnick, CFO. These options issued are nonqualified stock options and were 100% vested on grant date. All expense related to these stock options has been recognized in 2020.

The Black Scholes option pricing model was used to estimate the aggregate fair value of $36,699

For the three months ending March 31, exploration, evaluation and project expense costs included professional consulting services for a total of approximately $44,000 in 2020 compared to $46,000 in 2019. Included in the expense is continued payments for lab testing and project review.

As of March 31, 2020, and December 31, 2019, the Company has a related party payable with David Beling, CEO and President, of $637,292 and $635,775, respectively. This amount at March 31, 2020 consists of $195,902 of expense reports plus interest of $161,781 and salary of $191,667 plus interest of $87,942. Interest is accrued at a rate of 1% per month. This resulted in $19,000 of interest expense in 2020 versus $17,000 in 2019.

21

Liquidity and Capital Resources

To continue as a going concern, the Company will need to raise additional funds and attain profitable operations. The Company has no committed sources of capital and additional funding may not be available on terms acceptable to the Company, or at all.

On January 16, 2020, the Company entered into subscription agreements (“Subscription Agreements”) pursuant to which the Company sold an aggregate of 15,384,615 Units (the “Units”) with gross proceeds to the Company of CAD$2,000,000 to certain accredited investors. The proceeds from this offering will be used for general corporate purposes.

Each Unit was sold for a purchase price of CAD$0.13 per Unit and consisted of one share of the Company’s common stock and a two year warrant to purchase fifty percent (50% or one-half warrant) of the number of Units purchased in the offering at a per share exercise price of CAD$0.20. In connection with the offering, the Company issued an aggregate of 15,384,615 shares of its common stock.

The Company paid a total of CAD$118,918 for finder's fees on subscriptions under the Offering, together with 914,750 share purchase warrants (the “Finder Warrants”). Each Finder Warrant entitles the holder to acquire one share of common stock at an exercise price of CAD$0.20 per share for a period of 24 months from the date of issuance.

On October 29, 2014, Rocky Mountain Minerals Corp. a wholly owned subsidiary of the Company, entered into an Option Agreement (the “Option”) with Mojave Gold Mining Corporation (“Mojave”). Mojave holds and possesses the purchase rights to 100% of 12 patented mining claims located in Nye County, Nevada. This property is contiguous to the Company’s Bullfrog Project and covers approximately 156 acres, including the northeast half of the Montgomery-Shoshone (M-S) pit mined by Barrick Gold in the 1990’s.

Mojave granted to RMM the sole and immediate working right and option with respect to the property until the 10th anniversary of the closing date, to earn a 100% interest in and to the property free and clear of all charges encumbrances and claims, save and except a sliding scale Net smelter return (or NSR) royalty.

In order to maintain in force, the working right and Option granted to it, and to exercise the Option, RMM granted Mojave 750,000 shares of common stock and paid $16,000. In addition, to exercise the option, RMM must pay to Mojave a total of $190,000 over the next 10 years. For reference, Barrick Bullfrog Inc. (“Barrick”) terminated a lease on these patents after they ceased operations in late 1999.

On March 23, 2015, RMM the 100% owned subsidiary of the Company entered into a Mineral Lease and Option to Purchase Agreement with Barrick Bullfrog involving patented mining claims, unpatented mining claims, and mill site claims (“Properties”) located approximately four miles west of Beatty, Nevada. These Properties are strategically located adjacent to the Company’s Bullfrog Gold Project and include two patents that cover the southwest half of the Montgomery-Shoshone (M-S) open pit gold mine. In October 2014 the Company optioned the northeast half of the M-S pit and now controls the entire pit.

On May 21, 2019 the Barrick Agreement was amended whereby work commitments for the fifth anniversary and the total of $1.5 million were extended to September 23, 2020. The final work commitment has been accounted at $561,762.

On October 29, 2014, RMM entered into an Option Agreement (the “Option”) with Mojave Gold Mining Corporation (“Mojave”). Mojave holds and possesses the purchase rights to 100% of 12 patented mining claims located in Nye County, Nevada. This property is contiguous to the Company’s Bullfrog Project and covers approximately 156 acres, including the northeast half of the Montgomery-Shoshone (M-S) pit mined by Barrick Gold in the 1990’s.

Mojave granted to RMM the sole and immediate working right and option with respect to the property until the 10th anniversary of the closing date, to earn a 100% interest in and to the property free and clear of all charges encumbrances and claims, save and except a sliding scale Net Smelter Return (or NSR) royalty.

22

To maintain in force, the working right and Option granted to it, and to exercise the Option, RMM granted Mojave 750,000 shares of common stock and paid $16,000 in October 2014. In addition, to exercise the option, RMM must pay to Mojave a total of $190,000 over the next 10 years of which the Company has paid $80,000. Future payments due as follows:

| Due Date | Amount |

| October 2020 | $25,000 |

| October 2021 | $25,000 |

| October 2022 | $30,000 |

| October 2023 | $30,000 |

On July 1, 2017, RMM entered a 30-year Mineral Lease (the “Lunar Lease”) with Lunar Landing, LLC. (“Lunar”), the owner of 24 patented mining claims situated in the Bullfrog Mining District, Nye County, Nevada. RMM shall expend as minimum work commitments of $50,000 per year until a cumulative of $500,000 of expense has been incurred. RMM paid Lunar $26,000 on the Effective Date and makes lease payments on the following schedule:

| Years Ending December 31 | Annual Lease Payment ($) |

| 2018-2022 | 16,000 |

| 2023-2027 | 21,000 |

| 2028-2032 | 25,000 |

| 2033-2037 | 30,000 |

| 2038-2042 | 40,000 |

| 2043-2047 | 45,000 |

In August 2018 and December 2018, the Company staked and recorded an additional 46 unpatented claims, for a total of 134 claims staked by the Company.

In March 2019, the Company completed the final closing of a $1,127,400 private placement of equity. The subscriptions were priced at $0.05 per unit, which consisted of one share of the Company’s common stock and a two-year warrant to purchase a one-half share at a price of $0.10 per share. The initial closing of $835,000 was completed on February 11, 2019.

The consolidated financial statements have been prepared on a going concern basis, which contemplates the realization of assets and satisfaction of liabilities and commitments in the normal course of business. In the event that we are unable to continue as a going concern, we may be unable to realize the carrying value of our assets and to meet our obligations as they become due. To continue as a going concern, we will need to raise additional capital. However, we have no commitment from any party to provide additional capital and there is no assurance that such funding will be available when needed, or if available, that its terms will be favorable or acceptable to us. Furthermore, if we issue additional equity or debt securities, stockholders may experience additional dilution or the new equity securities may have rights, preferences or privileges senior to those of existing holders of our common stock.

If we are unable to raise additional financing, we may have to substantially reduce or cease operations.

Off Balance Sheet Arrangements

We do not engage in any activities involving variable interest entities or off-balance sheet arrangements.

Critical Accounting Policies and Use of Estimates

Stock based compensation is measured at grant date, based on the fair value of the award, and is recognized as an expense over the employee’s requisite service period. We estimate the fair value of each stock option as of the date of grant using the Black-Scholes pricing model. The Company determines the expected life based on historical experience with similar awards, giving consideration to the contractual terms, vesting schedules and post-vesting forfeitures. The Company uses the risk-free interest rate on the implied yield currently available on U.S. Treasury issues with an equivalent remaining term approximately equal to the expected life of the award. The Company has never paid any cash dividends on its common stock and does not anticipate paying any cash dividends in the foreseeable future.

23

Mineral property exploration costs are expensed as incurred until such time as economic reserves are quantified. To date, the Company has not established any proven or probable reserves on its mineral properties. Costs of lease, exploration, carrying and retaining unproven mineral lease properties are expensed as incurred. The Company has chosen to expense all mineral exploration costs as incurred given that it is still in the exploration stage. Once the Company has identified proven and probable reserves in its investigation of its properties and upon development of a plan for operating a mine, it would enter the development stage and capitalize future costs until production is established. When a property reaches the production stage, the related capitalized costs will be amortized over the estimated life of the probable-proven reserves. When the Company has capitalized mineral properties, these properties will be periodically assessed for impairment of value and any diminution in value. To date, the Company has not established the commercial feasibility of any exploration prospects; therefore, all exploration costs are being expensed. Costs of property acquisitions are being capitalized, and a required payment of $20,000 was made in 2018 to Mojave Gold Mining Corporation (“Mojave”) as part of the Option to Purchase Agreement (“Option”).

ITEM 3 - QUANTITATIVE AND QUALITATIVE DISCLOSURES AND MARKET RISK

This information is not required because we are a smaller reporting company.

ITEM 4 - CONTROLS AND PROCEDURES

Disclosure Controls and Procedures

As required by Rule 13a-15 under the Securities Exchange Act of 1934, as amended (the “Exchange Act”) our management conducted an evaluation of the effectiveness of the design and operation of our disclosure controls and procedures as of March 31, 2020.

Disclosure controls and procedures refer to controls and other procedures designed to ensure that information required to be disclosed in the reports we file or submit under the Exchange Act is recorded, processed, summarized and reported within the time periods specified in the rules and forms of the SEC and that such information is accumulated and communicated to our management, including our chief executive officer and chief financial officer, as appropriate, to allow timely decisions regarding required disclosure. In designing and evaluating our disclosure controls and procedures, management recognizes that any controls and procedures, no matter how well designed and operated, can provide only reasonable assurance of achieving the desired control objectives, and management is required to apply its judgment in evaluating and implementing possible controls and procedures.

Our management does not expect that our disclosure controls and procedures will prevent all error and all fraud. A control system, no matter how well designed and operated, can provide only reasonable, not absolute, assurance that the control system’s objectives will be met. Further, the design of a control system must reflect the fact that there are resource constraints, and the benefits of controls must be considered relative to their costs. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of simple error or mistake. The design of any system of controls is based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions.

With respect to the quarterly period ending March 31, 2020, under the supervision and with the participation of our management, we conducted an evaluation of the effectiveness of the design and operations of our disclosure controls and procedures, as defined in Rules 13a-15(e) and 15d-15(e) promulgated under the Exchange Act. Based upon our evaluation regarding the quarterly period ending March 31, 2020, our management, including our chief executive officer and chief financial officer, has concluded that its disclosure controls and procedures were effective.

Changes in Internal Controls

There have been no changes in the Company’s internal control over financial reporting during the three months ended March 31, 2020 that have materially affected, or are reasonably likely to materially affect, the Company’s internal controls over financial reporting.

24

We know of no material, active or pending legal proceedings against the Company, nor are we involved as a plaintiff in any material proceeding or pending litigation. There are no proceedings in which any of our directors, officers or affiliates, or any registered or beneficial shareholder, is an adverse party or has a material interest adverse to our interest.

There have been no material changes to the risk factors set forth in our Annual Report on Form 10-K for the fiscal year ended December 31, 2019.

ITEM 2 - UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

None.

ITEM 3 - DEFAULTS UPON SENIOR SECURITIES

None

ITEM 4 - MINE SAFETY DISCLOSURES

None

None

Exhibit Number | Description |

|

|

|

| Certification of Chief Executive Officer filed pursuant to Section 302 of the Sarbanes-Oxley Act of 2002* | |

| Certification of Chief Financial Officer filed pursuant to Section 302 of the Sarbanes-Oxley Act of 2002* | |

| Certification of Chief Executive Officer and Chief Financial Officer filed pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002* | |

| 101.ins | XBRL Instance Document * |

| 101.sch | XBRL Taxonomy Schema Document * |

| 101.cal | XBRL Taxonomy Calculation Document * |