Document

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_________________________________

FORM 10-K

_________________________________

(Mark One)

|

| |

ý | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017

OR

|

| |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 000-54376

_________________________________

STRATEGIC REALTY TRUST, INC.

(Exact name of registrant as specified in its charter)

_________________________________

|

| |

Maryland | 90-0413866 |

(State or Other Jurisdiction of Incorporation or Organization) | (I.R.S. Employer Identification No.) |

| |

66 Bovet Road, Suite 100 San Mateo, California, 94402 | (650) 343-9300 |

(Address of Principal Executive Offices; Zip Code) | (Registrant’s Telephone Number, Including Area Code) |

_________________________________

|

| | | | |

Securities registered pursuant to Section 12(b) of the Act: |

| | | | |

Title of Each Class | | Name of Each Exchange on Which Registered |

None | | None |

| | | | |

Securities registered pursuant to Section 12(g) of the Act: |

Common Stock, $0.01 par value per share |

_________________________________

Indicate by check mark whether the registrant is a well-known season issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark whether the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of the Form 10-K or any amendment of this Form 10-K. ý

Indicate by check mark whether the registrant is a large accelerated filed, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

|

| | | |

Large accelerated filer | ¨ | Accelerated filer | ¨ |

| | | |

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ý |

| | | |

| | Emerging growth company | ¨ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

There is no established trading market for the registrant’s common stock. On August 2, 2017, the registrant’s board of directors approved an estimated value per share of the registrant’s common stock of $6.27 per share based on (i) the estimated value of the registrant’s real estate assets as of June 30, 2017, plus the estimated value of the registrant’s tangible other assets as of April 30, 2017, less the estimated value of the registrant’s liabilities as of April 30, 2017, divided by (ii) the number of shares and operating partnership units outstanding as of April 30, 2017. For a full description of the methodologies used to value the registrant’s assets and liabilities in connection with the calculation of the estimated value per share as of April 30, 2017, see Part II, Item 5, “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities – Market Information” of this Annual Report on Form 10-K.

As of June 30, 2017, the last business day of the Company’s most recently completed second fiscal quarter, 10,629,677 shares of its common stock were held by non-affiliates.

As of March 20, 2018, there were 10,988,438 shares of the registrant’s common stock issued and outstanding.

STRATEGIC REALTY TRUST, INC. AND SUBSIDIARIES

TABLE OF CONTENTS

|

| | |

| Page |

| |

| |

| |

PART I | |

Item 1. | | |

Item 1A. | | |

Item 1B. | | |

Item 2. | | |

Item 3. | | |

Item 4. | | |

| | |

PART II | |

Item 5. | | |

Item 6. | | |

Item 7. | | |

Item 7A. | | |

Item 8. | | |

Item 9. | | |

Item 9A. | | |

Item 9B. | | |

| | |

PART III | |

Item 10. | | |

Item 11. | | |

Item 12. | | |

Item 13. | | |

Item 14. | | |

| | |

PART IV | |

Item 15. | | |

| | |

| |

| |

| |

Special Note Regarding Forward-Looking Statements

Certain statements included in this Annual Report on Form 10-K (“this Annual Report”) that are not historical facts (including any statements concerning investment objectives, other plans and objectives of management for future operations or economic performance, or assumptions or forecasts related thereto) are forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements are only predictions. We caution that forward-looking statements are not guarantees. Actual events or our investments and results of operations could differ materially from those expressed or implied in any forward-looking statements. Forward-looking statements are typically identified by the use of terms such as “may,” “should,” “expect,” “could,” “intend,” “plan,” “anticipate,” “estimate,” “believe,” “continue,” “predict,” “potential” or the negative of such terms and other comparable terminology.

The forward-looking statements included herein are based upon our current expectations, plans, estimates, assumptions and beliefs, which involve numerous risks and uncertainties. Assumptions relating to the foregoing involve judgments with respect to, among other things, future economic, competitive and market conditions and future business decisions, all of which are difficult or impossible to predict accurately and many of which are beyond our control. Although we believe that the expectations reflected in such forward-looking statements are based on reasonable assumptions, our actual results and performance could differ materially from those set forth in the forward-looking statements. The following are some of the risks and uncertainties, although not all of the risks and uncertainties, that could cause our actual results to differ materially from those presented in our forward-looking statements:

| |

• | Our executive officers and certain other key real estate professionals are also officers, directors, managers, key professionals and/or holders of a direct or indirect controlling interest in our advisor. As a result, they face conflicts of interest, including conflicts created by our advisor’s compensation arrangements with us and conflicts in allocating time among us and other programs and business activities. |

| |

• | We are uncertain of our sources for funding our future capital needs. If we cannot obtain debt or equity financing on acceptable terms, our ability to continue to acquire real properties or other real estate-related assets, fund or expand our operations and pay distributions to our stockholders will be adversely affected. |

| |

• | We depend on tenants for our revenue and, accordingly, our revenue is dependent upon the success and economic viability of our tenants. Revenues from our properties could decrease due to a reduction in tenants (caused by factors including, but not limited to, tenant defaults, tenant insolvency, early termination of tenant leases and non-renewal of existing tenant leases) and/or lower rental rates, making it more difficult for us to meet our financial obligations, including debt service and our ability to pay distributions to our stockholders. |

| |

• | Our current and future investments in real estate and other real estate-related investments may be affected by unfavorable real estate market and general economic conditions, which could decrease the value of those assets and reduce the investment return to our stockholders. Revenues from our properties could decrease. Such events would make it more difficult for us to meet our debt service obligations and limit our ability to pay distributions to our stockholders. |

| |

• | Certain of our debt obligations have variable interest rates with interest and related payments that vary with the movement of LIBOR or other indices. Increases in these indices could increase the amount of our debt payments and limit our ability to pay distributions to our stockholders. |

All forward-looking statements should be read in light of the risks identified in Part I, Item 1A of this Annual Report. Any of the assumptions underlying the forward-looking statements included herein could be inaccurate, and undue reliance should not be placed upon on any forward-looking statements included herein. All forward-looking statements are made as of the date of this Annual Report, and the risk that actual results will differ materially from the expectations expressed herein will increase with the passage of time. Except as otherwise required by the federal securities laws, we undertake no obligation to publicly update or revise any forward-looking statements made after the date of this Annual Report, whether as a result of new information, future events, changed circumstances or any other reason. In light of the significant uncertainties inherent in the forward-looking statements included in this Annual Report, and the risks described in Part I, Item 1A, the inclusion of such forward-looking statements should not be regarded as a representation by us or any other person that the objectives and plans set forth in this Annual Report will be achieved.

PART I

ITEM 1. BUSINESS

Overview

Strategic Realty Trust, Inc., is a Maryland corporation formed on September 18, 2008 to invest in and manage a portfolio of income-producing retail properties, located in the United States, real estate-owning entities and real estate-related assets, including the investment in or origination of mortgage, mezzanine, bridge and other loans related to commercial real estate. We have elected to be taxed as a real estate investment trust, or REIT, for federal income tax purposes, commencing with the taxable year ended December 31, 2009. As used herein, the terms “we” “our” “us” and “Company” refer to Strategic Realty Trust, Inc., and, as required by context, Strategic Realty Operating Partnership, L.P., a Delaware limited partnership, which we refer to as our “operating partnership” or “OP”, and to their respective subsidiaries. References to “shares” and “our common stock” refer to the shares of our common stock. We own substantially all of our assets and conduct our operations through our operating partnership, of which we are the sole general partner. We also own a majority of the outstanding limited partner interests in the operating partnership.

On November 4, 2008, we filed a registration statement on Form S-11 with the Securities and Exchange Commission (the “SEC”) to offer a maximum of 100,000,000 shares of our common stock to the public in our primary offering at $10.00 per share and up to 10,526,316 shares of our common stock to our stockholders at $9.50 per share pursuant to our distribution reinvestment plan (“DRIP”) (collectively, the “Offering”). On August 7, 2009, the SEC declared the registration statement effective and we commenced the Offering. On February 7, 2013, we terminated the Offering and ceased offering shares of common stock in the primary offering and under the DRIP.

As of February 2013 when we terminated the Offering, we had accepted subscriptions for, and issued, 10,688,940 shares of common stock in the Offering for gross offering proceeds of approximately $104.7 million, and 391,182 shares of common stock pursuant to the DRIP for gross offering proceeds of approximately $3.6 million. We have also granted 50,000 shares of restricted stock and we issued 273,729 shares of common stock to pay a portion of a special distribution on November 4, 2015.

On April 1, 2015, our board of directors approved the reinstatement of the share redemption program and adopted the Amended and Restated Share Redemption Program (the “SRP”). The program was previously suspended, effective as of January 15, 2013. Under the SRP, only shares submitted for repurchase in connection with the death or “qualifying disability” (as defined in the SRP) of a stockholder are eligible for repurchase by us. For more information regarding our share redemption program, refer to Part II, Item 5, “Market for Registrant’s Common Equity, Related Shareholder Matters and Issuer Purchases of Equity Securities - Share Redemption Program.” Cumulatively, through December 31, 2017, we have redeemed 612,115 shares of common stock sold in the Offering and/or the DRIP for approximately $4.6 million.

Since our inception, our business has been managed by an external advisor. We do not have direct employees and all management and administrative personnel responsible for conducting our business are employed by our advisor. Currently we are externally managed and advised by SRT Advisor, LLC, a Delaware limited liability company (the “Advisor”) pursuant to an advisory agreement with the Advisor (the “Advisory Agreement”) initially executed on August 10, 2013, and subsequently renewed every year through 2017. The current term of the Advisory Agreement terminates on August 10, 2018. The Advisor is an affiliate of Glenborough, LLC (together with its affiliates, “Glenborough”), a privately held full-service real estate investment and management company focused on the acquisition, management and leasing of commercial properties.

Our office is located at 66 Bovet Road, Suite 100, San Mateo, California 94402, and our main telephone number is (650) 343-9300.

Investment Objectives

Our investment objectives are to:

| |

• | preserve, protect and return stockholders’ capital contributions; |

| |

• | pay predictable and sustainable cash distributions to stockholders; and |

| |

• | realize capital appreciation upon the ultimate sale of the real estate assets. |

Business Strategy

On February 7, 2013, as a result of the termination of the Offering, we ceased offering shares of our common stock in our primary offering and under our DRIP. Additionally, in March 2013, we filed an application with the SEC to withdraw our registration statement on Form S-11 for a contemplated follow-on public offering of our common stock. Prior to the termination of the Offering, we funded our investments in real properties and other real-estate related assets primarily with the proceeds

from the Offering and debt financing. Since the termination of the Offering, we intend to fund our future cash needs, including any future investments, with debt financing, cash from operations, proceeds to us from asset sales, cash flows from investments in joint ventures and the proceeds from any offerings of our securities that we may conduct in the future. As a result of the termination of the Offering and the resulting decrease in our capital resources, we expect our investment activity to be reduced until we are able to engage in an offering of our securities or are able to identify other significant sources of financing.

We intend to continue to focus on investments in income-producing retail properties. Specifically, we are focused on acquiring high quality urban retail properties in major west coast markets and building a joint venture platform with institutional investors to invest in value–add retail properties. Our investments may include urban store front retail buildings, free standing single tenant buildings, neighborhood, community, power and lifestyle shopping centers, and multi-tenant shopping centers. We may also invest in real estate loans or real estate-related assets that we believe meet our investment objectives.

Investment Portfolio

As of December 31, 2017, our portfolio included 10 properties, including 3 properties classified as held for sale, which we refer to as “our properties” or “our portfolio,” comprising an aggregate of approximately 303,000 square feet of single and multi-tenant commercial retail space located in four states, which we purchased for an aggregate purchase price of approximately $73.4 million. Refer to Item 2, “Properties” for additional information on our portfolio. In addition to the properties, in 2015 we invested in two joint ventures with an institutional partner. These ventures acquired two portfolios comprising 19 properties and approximately 1,447,000 square feet. As of December 31, 2017, these ventures own in aggregate, 8 properties, comprising an aggregate of approximately 599,000 square feet and located in four states. During the first quarter of 2016, we invested, through joint ventures, in two significant retail projects under development.

Borrowing Policies

We use, and may continue to use in the future, secured and unsecured debt as a means of providing additional funds for the acquisition of real property, real estate-related loans, and other real estate-related assets. Our use of leverage increases the risk of default on loan payments and the resulting foreclosure on a particular asset. In addition, lenders may have recourse to assets other than those specifically securing the repayment of our indebtedness. As of December 31, 2017, our aggregate outstanding indebtedness, excluding outstanding indebtedness included in liabilities related to assets held for sale, and including deferred financing costs, net of accumulated amortization, totaled approximately $42.2 million, or 46.3% of the book value of our total assets, excluding assets held for sale.

Our aggregate borrowings, secured and unsecured, are reviewed by our board of directors at least quarterly. Under our Articles of Amendment and Restatement, as amended, which we refer to as our “charter,” we are prohibited from borrowing in excess of 300% of the value of our net assets. Net assets for purposes of this calculation is defined to be our total assets (other than intangibles), valued at cost prior to deducting depreciation, reserves for bad debts and other non-cash reserves, less total liabilities. The preceding calculation is generally expected to approximate 75% of the aggregate cost of our assets before non-cash reserves and depreciation. However, we may temporarily borrow in excess of these amounts if such excess is approved by a majority of the independent directors and disclosed to stockholders in our next quarterly report, along with an explanation for such excess. As of December 31, 2017 and 2016, our borrowings, excluding line of credit balances which have been classified as held for sale, were approximately 93.0% and 73.6%, respectively, of the book value of our net assets, excluding assets held for sale.

Our Advisor uses its best efforts to obtain financing on the most favorable terms available to us and will seek to refinance assets during the term of a loan only in limited circumstances, such as when a decline in interest rates makes it beneficial to prepay an existing loan, when an existing loan matures or if an attractive investment becomes available and the proceeds from the refinancing can be used to purchase such an investment. The benefits of any such refinancing may include increased cash flow resulting from reduced debt service requirements, an increase in distributions from proceeds of the refinancing and an increase in diversification and assets owned if all or a portion of the refinancing proceeds are reinvested.

Economic Dependency

We are dependent on our Advisor and its affiliates for certain services that are essential to us, including the disposition of real estate and real estate-related investments and, to the extent we acquire additional assets, the identification, evaluation, negotiation and purchase of these assets, management of the daily operations of our real estate and real estate-related investment portfolio, and other general and administrative responsibilities. In the event that our Advisor is unable to provide such services to us, we will be required to obtain such services from other sources.

Competitive Market Factors

To the extent that we acquire additional real estate investments in the future, we will be subject to significant competition in seeking real estate investments and tenants. We compete with many third-parties engaged in real estate investment activities, including other REITs, other real estate limited partnerships, banks, mortgage bankers, insurance companies, mutual funds, institutional investors, investment banking firms, lenders, hedge funds, governmental bodies, and other entities. Some of our competitors may have substantially greater financial and other resources than we have and may have substantially more operating experience than us. The marketplace for real estate equity and financing can be volatile. There is no guarantee that in the future we will be able to obtain financing or additional equity on favorable terms, if at all. Lack of available financing or additional equity could result in a further reduction of suitable investment opportunities and create a competitive advantage for other entities that have greater financial resources than we do.

Tax Status

We elected to be taxed as a REIT for U.S. federal income tax purposes under Sections 856 through 860 of the Internal Revenue Code of 1986, as amended, or the Internal Revenue Code, beginning with the taxable year ended December 31, 2009. We believe we are organized and operate in such a manner as to qualify for taxation as a REIT under the Internal Revenue Code, and we intend to continue to operate in such a manner, but no assurance can be given that we will operate in a manner so as to qualify or remain qualified as a REIT. As a REIT, we generally are not subject to federal income tax on our taxable income that is currently distributed to our stockholders, provided that distributions to our stockholders equal at least 90% of our taxable income, subject to certain adjustments. If we fail to qualify as a REIT in any taxable year without the benefit of certain relief provisions, we will be subject to federal income taxes on our taxable income at regular corporate income tax rates. We may also be subject to certain state or local income taxes, or franchise taxes.

We have elected to treat one of our subsidiaries as a taxable REIT subsidiary, which we refer to as a TRS. In general, a TRS may engage in any real estate business and certain non-real estate businesses, subject to certain limitations under the Internal Revenue Code. A TRS is subject to federal and state income taxes.

Environmental Matters

All real property investments and the operations conducted in connection with such investments are subject to federal, state and local laws and regulations relating to environmental protection and human health and safety. Some of these laws and regulations may impose joint and several liability on customers, owners or operators for the costs to investigate or remediate contaminated properties, regardless of fault or whether the acts causing the contamination were legal.

Under various federal, state and local environmental laws, a current or previous owner or operator of real property may be liable for the cost of removing or remediating hazardous or toxic substances on a real property. Such laws often impose liability whether or not the owner or operator knew of, or was responsible for, the presence of such hazardous or toxic substances. In addition, the presence of hazardous substances, or the failure to properly remediate these substances, may adversely affect our ability to sell, rent or pledge such real property as collateral for future borrowings. Environmental laws also may impose restrictions on the manner in which real property may be used or businesses may be operated. Some of these laws and regulations have been amended so as to require compliance with new or more stringent standards as of future dates. Compliance with new or more stringent laws or regulations or stricter interpretations of existing laws may require us to incur material expenditures or may impose material environmental liability. Additionally, tenants’ operations, the existing condition of land when we buy it, operations in the vicinity of our real properties, such as the presence of underground storage tanks, or activities of unrelated third-parties may affect our real properties. There are also various local, state and federal fire, health, life-safety and similar regulations with which we may be required to comply and which may subject us to liability in the form of fines or damages for noncompliance. In connection with the acquisition and ownership of real properties, we may be exposed to such costs in connection with such regulations. The cost of defending against environmental claims, of any damages or fines we must pay, of compliance with environmental regulatory requirements or of remediating any contaminated real property could materially and adversely affect our business, lower the value of our assets or results of operations and, consequently, lower the amounts available for distribution to our stockholders.

We do not believe that compliance with existing environmental laws will have a material adverse effect on our consolidated financial condition or results of operations. However, we cannot predict the impact of unforeseen environmental contingencies or new or changed laws or regulations on properties in which we hold an interest, or on properties that may be acquired directly or indirectly in the future.

Employees

We have no paid employees. The employees of our Advisor and its affiliates provide management, acquisition, disposition, advisory and certain administrative services for us.

Available Information

We are subject to the reporting and information requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and, as a result, file our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements and other information with the SEC. The SEC maintains a website (http://www.sec.gov) that contains our annual, quarterly and current reports, proxy and information statements and other information we file electronically with the SEC. Access to these filings is free of charge on the SEC’s website as well as on our website (www.srtreit.com).

ITEM 1A. RISK FACTORS

The following are some of the risks and uncertainties that could cause our actual results to differ materially from those presented in our forward-looking statements. The risks and uncertainties described below are not the only ones we face but do represent those risks and uncertainties that we believe are material to us. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also harm our business.

Risks Related to an Investment in Us

The estimated value per share of our common stock may not reflect the value that stockholders will receive for their investment.

On August 2, 2017, our board of directors approved an estimated value per share of our common stock of $6.27 per share based on the estimated value of the our real estate assets as of June 30, 2017 plus the estimated value of our tangible other assets less the estimated value of our liabilities divided by the number of shares and operating partnership units outstanding, as of April 30, 2017. We provided this estimated value per share to assist broker-dealers that participated in the Offering in meeting their customer account statement reporting obligations under the rules of National Association of Securities Dealers Conduct Rule 2340 as required by the Financial Industry Regulatory Authority (“FINRA”).

FINRA rules provide no guidance on the methodology an issuer must use to determine its estimated value per share. As with any valuation methodology, our Advisor’s methodology is based upon a number of estimates and assumptions that may not be accurate or complete. Different parties with different assumptions and estimates could derive a different estimated value per share, and these differences could be significant. The estimated value per share is not audited and does not represent the fair value of our assets or liabilities according to generally accepted accounting principles (“GAAP”). Accordingly, with respect to the estimated value per share, we can give no assurance that:

| |

• | a stockholder would be able to resell his or her shares at this estimated value; |

| |

• | a stockholder would ultimately realize distributions per share equal to our estimated value per share upon liquidation of our assets and settlement of our liabilities or a sale of the company; |

| |

• | our shares of common stock would trade at the estimated value per share on a national securities exchange; |

| |

• | an independent third-party appraiser or other third-party valuation firm would agree with our estimated value per share; or |

| |

• | the methodology used to estimate our value per share would or would not be acceptable to FINRA or for compliance with ERISA reporting requirements. |

The value of our shares will fluctuate over time in response to developments related to individual assets in our portfolio and the management of those assets and in response to the real estate and finance markets. As such, the estimated value per share does not take into account estimated disposition costs and fees for real estate properties that are not held for sale, debt prepayment penalties that could apply upon the prepayment of certain of our debt obligations or the impact of restrictions on the assumption of debt. For a description of the methodologies used to value our assets and liabilities in connection with the calculation of the estimated value per share, refer to Part II, Item 5, “Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities—Market Information”.

Our business could be negatively affected as a result of stockholder activities. Proxy contests threatened or commenced against us could be disruptive and costly and the possibility that stockholders may wage proxy contests or gain representation on or control of our board of directors could cause uncertainty about our strategic direction.

Campaigns by stockholders to effect changes at public companies are sometimes led by investors seeking to increase stockholder value through actions such as financial restructuring, corporate governance changes, special dividends, stock repurchases or sales of assets or the entire company. Proxy contests, if any, could be costly and time-consuming, disrupt our operations and divert the attention of management and our employees from executing our strategic plan. Additionally, perceived uncertainties as to our future direction as a result of stockholder activities or changes to the composition of the board of directors may lead to the perception of a change in the direction of the business, instability or lack of continuity which may be exploited by our competitors, cause concern to our current or potential customers, and make it more difficult to attract and retain qualified personnel. If such perceived uncertainties result in delay, deferral or reduction in transactions with us or transactions with our competitors instead of us because of any such issues, then our revenue, earnings and operating cash flows could be adversely affected.

Failure to maintain effective disclosure controls and procedures and internal controls over financial reporting could have an adverse effect on our operations.

Section 404 of the Sarbanes-Oxley Act of 2002 requires annual management assessments of the effectiveness of the Company’s internal control over financial reporting. If we fail to maintain the adequacy of our internal control over financial reporting, we may not be able to ensure that we can conclude on an ongoing basis that we have an effective internal control over financial reporting in accordance with Section 404 of the Sarbanes-Oxley Act of 2002. Moreover, effective internal controls over financial reporting are necessary for us to produce reliable financial reports and to maintain our qualification as a REIT and are important in helping to prevent financial fraud. If we cannot provide reliable financial reports or prevent fraud, our business and operating results could be harmed, REIT qualification could be jeopardized, and investors could lose confidence in our reported financial information.

There is no trading market for shares of our common stock, and we are not required to effectuate a liquidity event by a certain date. As a result, it will be difficult for you to sell your shares of common stock and, if you are able to sell your shares, you are likely to sell them at a substantial discount.

There is no current public market for the shares of our common stock and we have no obligation to list our shares on any public securities market or provide any other type of liquidity to our stockholders. It will therefore be difficult for you to sell your shares of common stock promptly, or at all. Even if you are able to sell your shares of common stock, the absence of a public market may cause the price received for any shares of our common stock sold to be less than what you paid or less than your proportionate value of the assets we own. We have adopted the Amended and Restated SRP, but only shares submitted for repurchase in connection with the death or “qualifying disability” (as defined in the Amended and Restated SRP) of a stockholder are eligible for repurchase under the Amended and Restated SRP and the number of shares to be redeemed under the Amended and Restated SRP is limited to the lesser of (i) a total of $3,500,000 for redemptions sought upon a stockholder’s death and a total of $1,000,000 for redemptions sought upon a stockholder’s qualifying disability, and (ii) 5% of the weighted average of the number of shares of our common stock outstanding during the prior calendar year. Additionally, our charter does not require that we consummate a transaction to provide liquidity to stockholders on any date certain or at all. As a result, you should be prepared to hold your shares for an indefinite length of time.

You are limited in your ability to sell your shares of common stock pursuant to the Amended and Restated SRP. You may not be able to sell any of your shares of our common stock back to us, and if you do sell your shares, you may not receive the price you paid upon subscription.

The Amended and Restated SRP may provide you with an opportunity to have your shares of common stock redeemed by us. However, our share redemption program contains certain restrictions and limitations. Only shares submitted for repurchase in connection with the death or “qualifying disability” (as defined in the Amended and Restated SRP) of a stockholder are eligible for repurchase under the Amended and Restated SRP. Further, we limit the number of shares to be redeemed under the Amended and Restated SRP to the lesser of (i) a total of $3,500,000 for redemptions sought upon a stockholder’s death and a total of $1,000,000 for redemptions sought upon a stockholder’s qualifying disability, and (ii) 5% of the weighted average of the number of shares of our common stock outstanding during the prior calendar year. In addition, our board of directors reserves the right to reject any redemption request for any reason or to amend or terminate the Amended and Restated SRP at any time. Therefore, you may not have the opportunity to make a redemption request prior to a potential termination of the Amended and Restated SRP and you may not be able to sell any of your shares of common stock back to us pursuant to the Amended and Restated SRP. Moreover, if you do sell your shares of common stock back to us pursuant to the Amended and Restated SRP, you may not receive the price you paid for any shares of our common stock being redeemed.

Distributions are not guaranteed, may fluctuate, and may constitute a return of capital or taxable gain from the sale or exchange of property.

From August 2009 to December 2012, our board of directors declared monthly cash distributions. Due to short-term liquidity issues and defaults under certain of our loan agreements, effective January 15, 2013, our board of directors determined to pay future distributions on a quarterly basis (as opposed to monthly). However, our board of directors did not declare or pay a distribution for the first three quarters of 2013. On December 9, 2013, our board of directors re-established a quarterly distribution that has continued through 2017. Refer to Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Distributions” for additional information regarding distributions.

The actual amount and timing of any future distributions will be determined by our board of directors and typically will depend upon, among other things, the amount of funds available for distribution, which will depend on items such as current and projected cash requirements and tax considerations. As a result, our distribution rate and payment frequency may vary from time to time.

To the extent that we are unable to consistently fund distributions to our stockholders entirely from our funds from operations, the value of your shares upon a listing of our common stock, the sale of our assets or any other liquidity event will likely be reduced. Further, if the aggregate amount of cash distributed in any given year exceeds the amount of our “REIT taxable income” generated during the year, the excess amount will either be (1) a return of capital or (2) gain from the sale or exchange of property to the extent that a stockholder’s basis in our common stock equals or is reduced to zero as the result of our current or prior year distributions. In addition, to the extent we make distributions to stockholders with sources other than funds from operations, the amount of cash that is distributed from such sources will limit the amount of investments that we can make, which will in turn negatively impact our ability to achieve our investment objectives and limit our ability to make future distributions.

Because we are dependent upon our Advisor and its affiliates to conduct our operations, any adverse changes in the financial health of our Advisor or its affiliates or our relationship with them could hinder our operating performance and the return on our stockholders’ investment.

We are dependent on our Advisor to manage our operations and our portfolio of real estate and real estate-related assets. Our Advisor depends on fees and other compensation that it receives from us in connection with the purchase, management and sale of assets to conduct its operations. Any adverse changes in the financial condition of our Advisor or our relationship with our Advisor could hinder our Advisor’s ability to successfully manage our operations and our portfolio of investments. If our Advisor is unable to provide services to us, we may spend substantial resources in identifying alternative service providers to provide advisory functions.

If we internalize our management functions, your interest in us could be diluted and we could incur other significant costs associated with being self-managed.

Our board of directors may decide in the future to internalize our management functions. If we do so, we may elect to negotiate the acquisition of our Advisor’s assets and personnel. At this time, we cannot anticipate the form or amount of consideration or other terms relating to any such acquisition. Such consideration could take many forms, including cash payments, promissory notes and shares of our common stock. The payment of such consideration could result in dilution of your interests as a stockholder and could reduce the earnings per share and funds from operations per share attributable to your investment.

Additionally, while we would no longer bear the costs of the various fees and expenses we pay to our Advisor under the Advisory Agreement, our direct expenses would include general and administrative costs, including legal, accounting and other expenses related to corporate governance, SEC reporting and compliance. We would also be required to employ personnel and would be subject to potential liabilities commonly faced by employers, such as workers disability and compensation claims, potential labor disputes and other employee-related liabilities and grievances as well as incur the compensation and benefits costs of our officers and other employees and consultants that were being paid by our Advisor or its affiliates. We may issue equity awards to officers, employees and consultants, which awards would decrease net income and funds from operations and may further dilute your investment. We cannot reasonably estimate the amount of fees to our Advisor that we would save or the costs that we would incur if we became self-managed. If the expenses we assume as a result of an internalization are higher than the expenses we avoid paying to our Advisor, our earnings per share and funds from operations per share would be lower as a result of the internalization than they otherwise would have been, potentially decreasing the amount of funds available to distribute to our stockholders and the value of our shares.

Internalization transactions involving the acquisition of advisors or property managers affiliated with entity sponsors have also, in some cases, been the subject of litigation. Even if these claims are without merit, we could be forced to spend

significant amounts of money defending claims which would reduce the amount of funds available for us to invest in properties or other investments or to pay distributions.

If we internalize our management functions, we could have difficulty integrating these functions as a stand-alone entity. Currently, our Advisor and its affiliates perform asset management and general and administrative functions, including accounting and financial reporting, for multiple entities. These personnel have substantial know-how and experience which provides us with economies of scale. We may fail to properly identify the appropriate mix of personnel and capital needs to operate as a stand-alone entity. An inability to manage an internalization transaction effectively could thus result in our incurring excess costs and suffering potential deficiencies in our disclosure controls and procedures or our internal control over financial reporting. Such deficiencies could cause us to incur additional costs, and our management’s attention could be diverted from most effectively managing our real properties and other real estate-related assets.

Provisions of the Maryland General Corporation Law may limit the ability of a third party to acquire control of us and may prevent our stockholders from receiving a premium price for their stock in connection with a business combination.

Our board of directors has elected for us to be subject to certain provisions of the Maryland General Corporation Law (the “MGCL”) relating to corporate governance that may have the effect of delaying, deferring or preventing a transaction or a change of control of us that might involve a premium to the market price of our common stock or otherwise be in our stockholders' best interests. Pursuant to Subtitle 8 of Title 3 of the MGCL, our board of directors has implemented (i) a classified board of directors having staggered three year terms and (ii) a requirement that a vacancy on the board be filled only by the remaining directors. Such provisions may have the effect of discouraging offers to acquire us and of increasing the difficulty of consummating any such offers, even if the acquisition would be in our stockholders’ best interests, and may therefore prevent our stockholders from receiving a premium price for their stock in connection with a business combination.

Risks Related To Our Business

We are uncertain of our sources for funding our future capital needs and our cash and cash equivalents on hand is limited. If we cannot obtain debt or equity financing on acceptable terms, our ability to acquire real properties or other real estate-related assets, fund or expand our operations and pay distributions to our stockholders will be adversely affected.

Our cash and cash equivalents on hand are currently limited. In the event that we develop a need for additional capital in the future for investments, the improvement of our real properties or for any other reason, sources of funding may not be available to us. If we cannot establish reserves out of cash flow generated by our investments or out of net sale proceeds in non-liquidating sale transactions, or obtain debt or equity financing on acceptable terms, our ability to acquire real properties and other real estate-related assets, to expand our operations and make distributions to our stockholders will be adversely affected. Furthermore, if our liquidity were to become severely limited it could jeopardize our ability to continue as a going concern or to make the annual distributions required to continue to qualify as a REIT, which would adversely affect the value of our stockholders’ investment in us.

Uninsured losses or premiums for insurance coverage relating to real property may adversely affect your returns.

We attempt to adequately insure all of our real properties against casualty losses. There are types of losses, generally catastrophic in nature, such as losses due to wars, acts of terrorism, earthquakes, floods, hurricanes, pollution or environmental matters that are uninsurable or not economically insurable, or may be insured subject to limitations, such as large deductibles or co-payments. Additionally, mortgage lenders sometimes require commercial property owners to purchase specific coverage against terrorism as a condition for providing mortgage loans. These policies may not be available at a reasonable cost, if at all, which could inhibit our ability to finance or refinance our real properties. In such instances, we may be required to provide other financial support, either through financial assurances or self-insurance, to cover potential losses. Changes in the cost or availability of insurance could expose us to uninsured casualty losses. In the event that any of our real properties incurs a casualty loss which is not fully covered by insurance, the value of our assets will be reduced by any such uninsured loss. In addition, we cannot assure you that funding will be available to us for repair or reconstruction of damaged real property in the future.

Risks Relating to Our Organizational Structure

The limit on the percentage of shares of our common stock that any person may own may discourage a takeover or business combination that may benefit our stockholders.

Our charter restricts the direct or indirect ownership by one person or entity to no more than 9.8% of the value of our then outstanding capital stock (which includes common stock and any preferred stock we may issue) and no more than 9.8% of the value or number of shares, whichever is more restrictive, of our then outstanding common stock unless exempted by our board of directors. This restriction may discourage a change of control of us and may deter individuals or entities from making tender

offers for shares of our common stock on terms that might be financially attractive to stockholders or which may cause a change in our management. In addition to deterring potential transactions that may be favorable to our stockholders, these provisions may also decrease your ability to sell your shares of our common stock.

We may issue preferred stock or other classes of common stock, which could adversely affect the holders of our common stock.

Our stockholders do not have preemptive rights to any shares issued by us in the future. We may issue, without stockholder approval, preferred stock or other classes of common stock with rights that could dilute the value of your shares of common stock. However, the issuance of preferred stock must also be approved by a majority of our independent directors not otherwise interested in the transaction, who will have access, at our expense, to our legal counsel or to independent legal counsel. In some instances, the issuance of preferred stock or other classes of common stock would increase the number of stockholders entitled to distributions without simultaneously increasing the size of our asset base.

Our charter authorizes us to issue 450,000,000 shares of capital stock, of which 400,000,000 shares of capital stock are designated as common stock and 50,000,000 shares of capital stock are designated as preferred stock. Our board of directors may amend our charter to increase the aggregate number of authorized shares of capital stock or the number of authorized shares of capital stock of any class or series without stockholder approval. If we ever create and issue preferred stock with a distribution preference over common stock, payment of any distribution preferences of outstanding preferred stock would reduce the amount of funds available for the payment of distributions on our common stock. Further, holders of preferred stock are normally entitled to receive a preference payment in the event we liquidate, dissolve or wind up before any payment is made to our common stockholders, likely reducing the amount common stockholders would otherwise receive upon such an occurrence. In addition, under certain circumstances, the issuance of preferred stock or a separate class or series of common stock may render more difficult or tend to discourage:

| |

• | a merger, tender offer or proxy contest; |

| |

• | the assumption of control by a holder of a large block of our securities; and |

| |

• | the removal of incumbent management. |

Actions of joint venture partners could negatively impact our performance.

We have entered into and may enter into joint ventures with third-parties, including with entities that are affiliated with our Advisor. We may also purchase and develop properties in joint ventures or in partnerships, co-tenancies or other co-ownership arrangements with the sellers of the properties, affiliates of the sellers, developers or other persons. Such investments may involve risks not otherwise present with a direct investment in real estate, including, for example:

| |

• | the possibility that our venture partner or co-tenant in an investment might become bankrupt; |

| |

• | that the venture partner or co-tenant may at any time have economic or business interests or goals which are, or which become, inconsistent with our business interests or goals; |

| |

• | that such venture partner or co-tenant may be in a position to take action contrary to our instructions or requests or contrary to our policies or objectives; |

| |

• | the possibility that we may incur liabilities as a result of an action taken by such venture partner; |

| |

• | that disputes between us and a venture partner may result in litigation or arbitration that would increase our expenses and prevent our officers and directors from focusing their time and effort on our business; |

| |

• | the possibility that if we have a right of first refusal or buy/sell right to buy out a co-venturer, co-owner or partner, we may be unable to finance such a buy-out if it becomes exercisable or we may be required to purchase such interest at a time when it would not otherwise be in our best interest to do so; or |

| |

• | the possibility that we may not be able to sell our interest in the joint venture if we desire to exit the joint venture. |

Under certain joint venture arrangements, one or all of the venture partners may have limited powers to control the venture and an impasse could be reached, which might have a negative influence on the joint venture and decrease potential returns to you. In addition, to the extent that our venture partner or co-tenant is an affiliate of our Advisor, certain conflicts of interest will exist.

Risks Related To Conflicts of Interest

We may compete with other affiliates of our Advisor for opportunities to acquire or sell investments, which may have an adverse impact on our operations.

We may compete with other affiliates of our Advisor for opportunities to acquire or sell real properties and other real estate-related assets. We may also buy or sell real properties and other real estate-related assets at the same time as other affiliates are considering buying or selling similar assets. In this regard, there is a risk that our Advisor will select for us investments that provide lower returns to us than investments purchased by another affiliate. Certain of our Advisor’s affiliates may own or manage real properties in geographical areas in which we may expect to own real properties. As a result of our potential competition with other affiliates of our Advisor, certain investment opportunities that would otherwise be available to us may not in fact be available. This competition may also result in conflicts of interest that are not resolved in our favor.

The time and resources that our Advisor and some of its affiliates, including our officers and directors, devote to us may be diverted, and we may face additional competition due to the fact that affiliates of our Advisor are not prohibited from raising money for, or managing, another entity that makes the same types of investments that we target.

Our Advisor and some of its affiliates, including our officers and directors, are not prohibited from raising money for, or managing, another investment entity that makes the same types of investments as those we target. For example, our Advisor’s management currently manages several privately offered real estate programs sponsored by affiliates of our Advisor. As a result, the time and resources they could devote to us may be diverted. In addition, we may compete with any such investment entity for the same investors and investment opportunities. We may also co-invest with any such investment entity. Even though all such co-investments will be subject to approval by our independent directors, they could be on terms not as favorable to us as those we could achieve co-investing with a third-party.

Our Advisor and its affiliates, including certain of our officers and directors, face conflicts of interest caused by compensation arrangements with us and other affiliates, which could result in actions that are not in the best interests of our stockholders.

Our Advisor and its affiliates receive substantial fees from us in return for their services and these fees could influence the advice provided to us. Among other matters, the compensation arrangements could affect their judgment with respect to:

| |

• | acquisitions of property and other investments and originations of loans, which entitle our Advisor to acquisition or origination fees and management fees; and, in the case of acquisitions of investments from other programs sponsored by Glenborough, may entitle affiliates of our Advisor to disposition or other fees from the seller; |

| |

• | real property sales, since the asset management fees payable to our Advisor will decrease; |

| |

• | incurring or refinancing debt and originating loans, which would increase the acquisition, financing, origination and management fees payable to our Advisor; and |

| |

• | whether and when we seek to sell the company or its assets or to list our common stock on a national securities exchange, which would entitle the Advisor and/or its affiliates to incentive fees. |

Further, our Advisor may recommend that we invest in a particular asset or pay a higher purchase price for the asset than it would otherwise recommend if it did not receive an acquisition fee. Certain acquisition fees and asset management fees payable to our Advisor and property management fees payable to the property manager are payable irrespective of the quality of the underlying real estate or property management services during the term of the related agreement. These fees may influence our Advisor to recommend transactions with respect to the sale of a property or properties that may not be in our best interest at the time. Investments with higher net operating income growth potential are generally riskier or more speculative. In addition, the premature sale of an asset may add concentration risk to the portfolio or may be at a price lower than if we held on to the asset. Moreover, our Advisor has considerable discretion with respect to the terms and timing of acquisition, disposition, refinancing and leasing transactions. In evaluating investments and other management strategies, the opportunity to earn these fees may lead our Advisor to place undue emphasis on criteria relating to its compensation at the expense of other criteria, such as the preservation of capital, to achieve higher short-term compensation. Considerations relating to our affiliates’ compensation from us and other affiliates of our Advisor could result in decisions that are not in the best interests of our stockholders, which could hurt our ability to pay you distributions or result in a decline in the value of your investment.

We may purchase real property and other real estate-related assets from third-parties who have existing or previous business relationships with affiliates of our Advisor, and, as a result, in any such transaction, we may not have the benefit of arm’s-length negotiations of the type normally conducted between unrelated parties.

We may purchase real property and other real estate-related assets from third-parties that have existing or previous business relationships with affiliates of our Advisor. The officers, directors or employees of our Advisor and its affiliates and the principals of our Advisor who also perform services for other affiliates of our Advisor may have a conflict in representing our interests in these transactions on the one hand and preserving or furthering their respective relationships on the other hand. In any such transaction, we will not have the benefit of arm’s-length negotiations of the type normally conducted between unrelated parties, and the purchase price or fees paid by us may be in excess of amounts that we would otherwise pay to third-parties.

Risks Associated with Retail Property

Our retail properties are subject to property taxes that may increase in the future, which could adversely affect our cash flow.

Our real properties are subject to real and personal property taxes that may increase as tax rates change and as the real properties are assessed or reassessed by taxing authorities. Certain of our leases provide that the property taxes, or increases therein, are charged to the lessees as an expense related to the real properties that they occupy, while other leases provide that we are responsible for such taxes. In any case, as the owner of the properties, we are ultimately responsible for payment of the taxes to the applicable government authorities. If real property taxes increase, our tenants may be unable to make the required tax payments, ultimately requiring us to pay the taxes even if otherwise stated under the terms of the lease. If we fail to pay any such taxes, the applicable taxing authority may place a lien on the real property and the real property may be subject to a tax sale. In addition, we will generally be responsible for real property taxes related to any vacant space.

An economic downturn in the United States may have an adverse impact on the retail industry generally. Slow or negative growth in the retail industry may result in defaults by retail tenants which could have an adverse impact on our financial operations.

An economic downturn in the United States may have an adverse impact on the retail industry generally. As a result, the retail industry may face reductions in sales revenues and increased bankruptcies. Adverse economic conditions may result in an increase in distressed or bankrupt retail companies, which in turn could result in an increase in defaults by tenants at our commercial properties. Additionally, slow economic growth is likely to hinder new entrants in the retail market which may make it difficult for us to fully lease our properties. Tenant defaults and decreased demand for retail space would have an adverse impact on the value of our retail properties and our results of operations.

Our properties consist of retail properties. Our performance, therefore, is linked to the market for retail space generally.

As of December 31, 2017, we owned 10 properties, including three properties held for sale, each of which is a retail property and the majority of which have multiple tenants. The joint ventures in which we have invested also own retail centers. The market for retail space has been and in the future could be adversely affected by weaknesses in the national, regional and local economies, the adverse financial condition of some large retailing companies, consolidation in the retail sector, excess amounts of retail space in a number of markets and competition for tenants with other shopping centers in our markets. Customer traffic to these shopping areas may be adversely affected by the closing of stores in the same shopping center, or by a reduction in traffic to such stores resulting from a regional economic downturn, a general downturn in the local area where our retail center is located, or a decline in the desirability of the shopping environment of a particular shopping center. Such a reduction in customer traffic could have a material adverse effect on our business, financial condition and results of operations.

Our retail tenants face competition from numerous retail channels, which may reduce our profitability and ability to pay distributions.

Retailers at our current retail properties and at any retail property we may acquire in the future face continued competition from discount or value retailers, factory outlet centers, wholesale clubs, mail order catalogs and operators, television shopping networks and shopping via the Internet. Such competition could adversely affect our tenants and, consequently, our revenues and funds available for distribution.

Retail conditions may adversely affect our base rent and subsequently, our income.

Some of our leases may provide for base rent plus contractual base rent increases. A number of our retail leases may also include a percentage rent clause for additional rent above the base amount based upon a specified percentage of the sales our tenants generate. Under those leases that contain percentage rent clauses, our revenue from tenants may increase as the sales of

our tenants increase. Generally, retailers face declining revenues during downturns in the economy. As a result, the portion of our revenue that we may derive from percentage rent leases could decline upon a general economic downturn.

Our revenue will be impacted by the success and economic viability of our anchor retail tenants. Our reliance on single or significant tenants in certain buildings may decrease our ability to lease vacated space and adversely affect the returns on your investment.

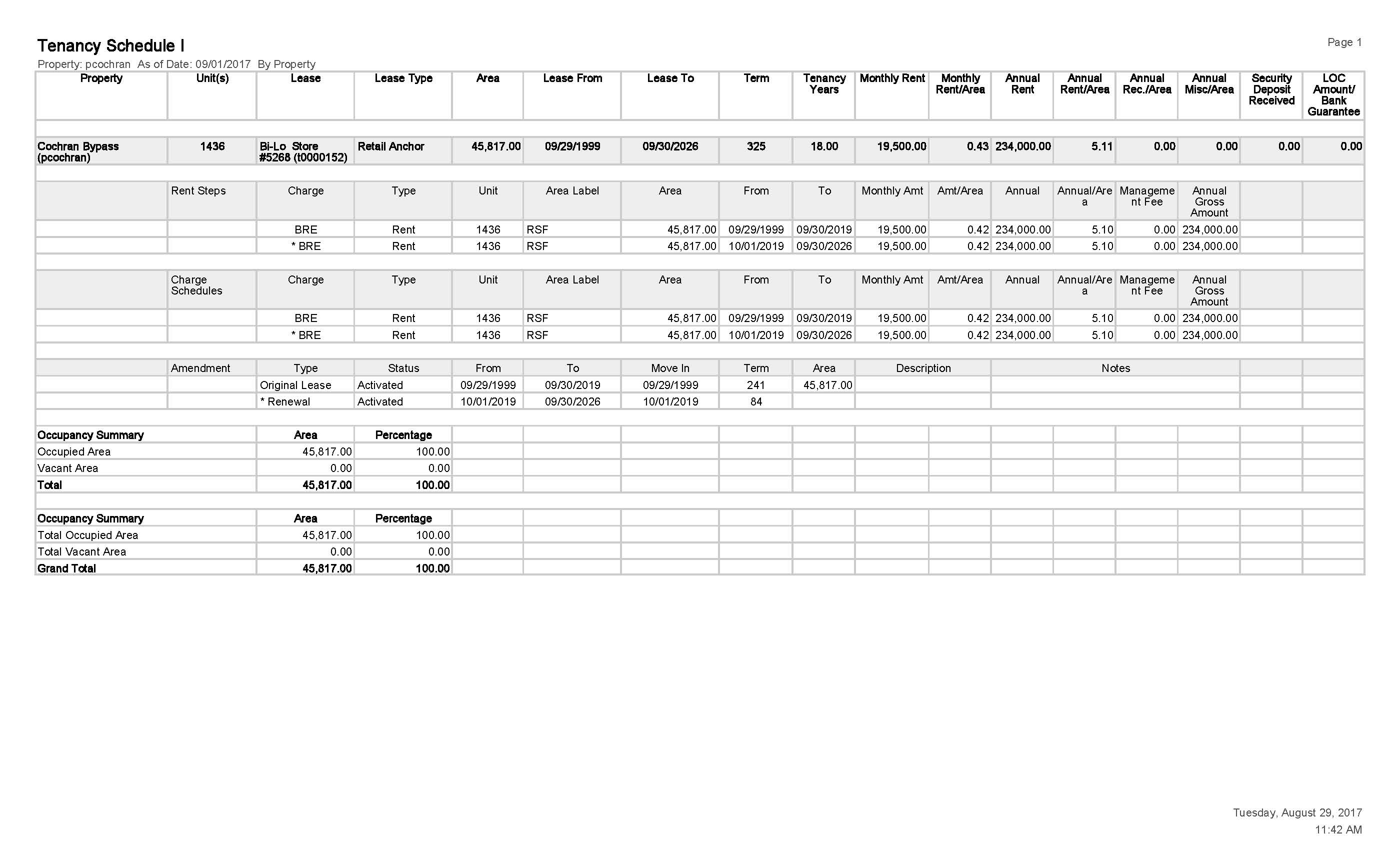

In the retail sector, a tenant occupying all or a large portion of the gross leasable area of a retail center, commonly referred to as an “anchor tenant,” may become insolvent, may suffer a downturn in business, or may decide not to renew its lease. Any of these events at one of our properties or any retail property we may acquire in the future would result in a reduction or cessation in rental payments to us and would adversely affect our financial condition. A lease termination by an anchor tenant at one of our properties or any retail property we may acquire in the future could result in lease terminations or reductions in rent by other tenants whose leases may permit cancellation or rent reduction if another tenant’s lease is terminated. In such event, we may be unable to re-lease the vacated space. Similarly, the leases of some anchor tenants may permit the anchor tenant to transfer its lease to another retailer. The transfer of a lease to a new anchor tenant could cause customer traffic in the retail center to decrease and thereby reduce the income generated by that retail center. A lease transfer to a new anchor tenant could also allow other tenants to make reduced rental payments or to terminate their leases. In the event that we are unable to re-lease vacated space at one of our properties or any retail property we may acquire in the future to a new anchor tenant, we may incur additional expenses in order to re-model the space to be able to re-lease the space to more than one tenant. As of December 31, 2017, excluding properties classified as held for sale, Clover Juice accounted for more than 10% of our annual minimum rent.

One of our tenants accounts for a meaningful portion of the gross leasable area of our portfolio and/or our annual minimum rent, and the inability of of this tenant to make its contractual rent payments to us could expose us to potential losses in rental revenue, expense recoveries, and percentage rent.

A concentration of credit risk may arise in our business when a nationally or regionally-based tenant is responsible for a substantial amount of rent in multiple properties owned by us. In that event, if the tenant suffers a significant downturn in its business, it may become unable to make its contractual rent payments to us, exposing us to potential losses in rental revenue, expense recoveries, and percentage rent. Further, the impact may be magnified if the tenant is renting space in multiple locations. Generally, we do not obtain security from nationally-based or regionally-based tenants in support of their lease obligations to us. As of December 31, 2017, excluding properties classified as held for sale, Clover Juice accounted for more than 10% of our annual minimum rent.

The bankruptcy or insolvency of a major tenant may adversely impact our operations and our ability to pay distributions.

The bankruptcy or insolvency of a significant tenant or a number of smaller tenants at one of our properties or any retail property we may acquire in the future may have an adverse impact on our income and our ability to pay distributions. Generally, under bankruptcy law, a debtor tenant has 120 days to exercise the option of assuming or rejecting the obligations under any unexpired lease for nonresidential real property, which period may be extended once by the bankruptcy court. If the tenant assumes its lease, the tenant must cure all defaults under the lease and may be required to provide adequate assurance of its future performance under the lease. If the tenant rejects the lease, we will have a claim against the tenant’s bankruptcy estate. Although rent owing for the period between filing for bankruptcy and rejection of the lease may be afforded administrative expense priority and paid in full, pre-bankruptcy arrears and amounts owing under the remaining term of the lease will be afforded general unsecured claim status (absent collateral securing the claim). Moreover, amounts owing under the remaining term of the lease will be capped. Other than equity and subordinated claims, general unsecured claims are the last claims paid in a bankruptcy and therefore funds may not be available to pay such claims in full.

The costs of complying with governmental laws and regulations related to environmental protection and human health and safety may be high.

All real property investments and the operations conducted in connection with such investments are subject to federal, state and local laws and regulations relating to environmental protection and human health and safety. Some of these laws and regulations may impose joint and several liability on customers, owners or operators for the costs to investigate or remediate contaminated properties, regardless of fault or whether the acts causing the contamination were legal. Under various federal, state and local environmental laws, a current or previous owner or operator of real property may be liable for the cost of removing or remediating hazardous or toxic substances on such real property. Such laws often impose liability whether or not the owner or operator knew of, or was responsible for, the presence of such hazardous or toxic substances. In addition, the presence of hazardous substances, or the failure to properly remediate these substances, may adversely affect our ability to sell, rent or pledge such real property as collateral for future borrowings. Environmental laws also may impose restrictions on the manner in which real property may be used or businesses may be operated. Some of these laws and regulations have been

amended so as to require compliance with new or more stringent standards as of future dates. Compliance with new or more stringent laws or regulations or stricter interpretation of existing laws may require us to incur material expenditures. Future laws, ordinances or regulations may impose material environmental liability. Additionally, our tenants’ operations, the existing condition of land when we buy it, operations in the vicinity of our real properties, such as the presence of underground storage tanks, or activities of unrelated third-parties may affect our real properties. There are also various local, state and federal fire, health, life-safety and similar regulations with which we may be required to comply and which may subject us to liability in the form of fines or damages for noncompliance. In connection with the acquisition and ownership of our real properties, we may be exposed to such costs in connection with such regulations. The cost of defending against environmental claims, of any damages or fines we must pay, of compliance with environmental regulatory requirements or of remediating any contaminated real property could materially and adversely affect our business, lower the value of our assets or results of operations and, consequently, lower the amounts available for distribution to you.

The costs associated with complying with the Americans with Disabilities Act may reduce the amount of cash available for distribution to our stockholders.

Investment in real properties may also be subject to the Americans with Disabilities Act of 1990, as amended, or “ADA”. Under the ADA, all places of public accommodation are required to comply with federal requirements related to access and use by disabled persons. We are committed to complying with the act to the extent to which it applies. The ADA has separate compliance requirements for “public accommodations” and “commercial facilities” that generally require that buildings and services be made accessible and available to people with disabilities. With respect to the properties we acquire, the ADA’s requirements could require us to remove access barriers and could result in the imposition of injunctive relief, monetary penalties or, in some cases, an award of damages. We will attempt to acquire properties that comply with the ADA or place the burden on the seller or other third-party, such as a tenant, to ensure compliance with the ADA. We cannot assure you that we will be able to acquire properties or allocate responsibilities in this manner. Any monies we use to comply with the ADA will reduce the amount of cash available for distribution to our stockholders.

Real properties are illiquid investments, and we may be unable to adjust our portfolio in response to changes in economic or other conditions or sell a property if or when we decide to do so.

Real properties are illiquid investments. We may be unable to adjust our portfolio in response to changes in economic or other conditions. In addition, the real estate market is affected by many factors, such as general economic conditions, availability of financing, interest rates and supply and demand that are beyond our control. We cannot predict whether we will be able to sell any real property for the price or on the terms set by us, or whether any price or other terms offered by a prospective purchaser would be acceptable to us. We cannot predict the length of time needed to find a willing purchaser and to close the sale of a real property. Also, we may acquire real properties that are subject to contractual “lock-out” provisions that could restrict our ability to dispose of the real property for a period of time. We may be required to expend funds to correct defects or to make improvements before a property can be sold. We cannot assure you that we will have funds available to correct such defects or to make such improvements.

In acquiring a real property, we may agree to restrictions that prohibit the sale of that real property for a period of time or impose other restrictions, such as a limitation on the amount of debt that can be placed or repaid on that real property. Our real properties may also be subject to resale restrictions. All these provisions would restrict our ability to sell a property, which could reduce the amount of cash available for distribution to our stockholders.

Risks Associated With Debt Financing

Restrictions imposed by our loan agreements may limit our ability to execute our business strategy and could limit our ability to make distributions to our stockholders.

We are a party to loan agreements that contain a variety of restrictive covenants. These covenants include requirements to maintain certain financial ratios and requirements to maintain compliance with applicable laws. A lender could impose restrictions on us that affect our ability to incur additional debt and our distribution and operating policies. In general, we expect our loan agreements to restrict our ability to encumber or otherwise transfer our interest in the respective property without the prior consent of the lender. Loan documents we enter may contain other customary negative covenants that may limit our ability to further mortgage the property, discontinue insurance coverage, replace our Advisor or impose other limitations. Any such restriction or limitation may have an adverse effect on our operations and our ability to make distributions to you.

We will incur mortgage indebtedness and other borrowings, which may increase our business risks, could hinder our ability to make distributions and could decrease the value of your investment.

We have, and may in the future, obtain lines of credit and long-term financing that may be secured by our real properties and other assets. Under our charter, we are prohibited from borrowing in excess of 300% of the value of our net assets. Net assets for purposes of this calculation are defined to be our total assets (other than intangibles), valued at cost prior to deducting depreciation, reserves for bad debts or other non-cash reserves, less total liabilities. Generally speaking, the preceding calculation is expected to approximate 75% of the aggregate cost of our investments before non-cash reserves and depreciation. Our charter allows us to borrow in excess of these amounts if such excess is approved by a majority of the independent directors and is disclosed to stockholders in our next quarterly report, along with justification for such excess. As of December 31, 2017, our aggregate borrowings did not exceed 300% of the value of our net assets. Also, we may incur mortgage debt and pledge some or all of our investments as security for that debt to obtain funds to acquire additional investments or for working capital. We may also borrow funds as necessary or advisable to ensure we maintain our REIT tax qualification, including the requirement that we distribute at least 90% of our annual REIT taxable income to our stockholders (computed without regard to the distribution paid deduction and excluding net capital gains). Furthermore, we may borrow if we otherwise deem it necessary or advisable to ensure that we maintain our qualification as a REIT for federal income tax purposes.