UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_______________

FORM 10-Q

_______________

(Mark One)

|

x

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended June 30, 2014

OR

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ___________ to ___________

RETROPHIN, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

000-53293

|

27-4842691

|

||

|

(State or other jurisdiction of

incorporation or organization)

|

(Commission File No.)

|

(I.R.S. Employer

Identification No.)

|

777 Third Avenue, 22nd Floor, New York, NY, 10017

(Address of Principal Executive Offices)

_______________

(646) 837-5863

(Issuer Telephone number)

_______________

(Former Name or Former Address if Changed Since Last Report)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes þ No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company.

|

Large accelerated filer

|

¨

|

Accelerated filer

|

¨

|

|

Non-accelerated filer

|

¨

|

Smaller reporting company

|

þ

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No þ

The number of shares of outstanding common stock, par value $0.0001 per share, of the Registrant as of August 12, 2014 was 26,681,514.

RETROPHIN, INC. AND SUBSIDIARIES

Form 10-Q

June 30, 2014

Page No.

|

PART I – FINANCIAL INFORMATION

|

||

|

Item 1. Financial Statements

|

||

|

4

|

||

|

5

|

||

|

6

|

||

|

7

|

||

|

8

|

||

|

24

|

||

|

32

|

||

|

32

|

||

|

PART II – OTHER INFORMATION

|

||

|

33

|

||

|

33

|

||

|

36

|

||

|

36

|

||

|

36

|

||

|

36

|

FORWARD LOOKING STATEMENTS

This report contains forward-looking statements regarding our business, financial condition, results of operations and prospects. Words such as “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates” and similar expressions or variations of such words are intended to identify forward-looking statements, but are not deemed to represent an all-inclusive means of identifying forward-looking statements as denoted in this report. Additionally, statements concerning future matters are forward-looking statements.

Although forward-looking statements in this report reflect the good faith judgment of our management, such statements can only be based on facts and factors currently known by us. Consequently, forward-looking statements are inherently subject to risks and uncertainties and actual results and outcomes may differ materially from the results and outcomes discussed in or anticipated by the forward-looking statements. Factors that could cause or contribute to such differences in results and outcomes include, without limitation, those specifically addressed under the headings “Risks Factors” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in our annual report on Form 10-K for the fiscal year ended December 31, 2013, in “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this Form 10-Q and information contained in other reports that we file with the Securities and Exchange Commission (the “SEC”). You are urged not to place undue reliance on these forward-looking statements, which speak only as of the date of this report.

We file reports with the SEC. The SEC maintains a website (www.sec.gov) that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, including us. You can also read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. You can obtain additional information about the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330.

We undertake no obligation to revise or update any forward-looking statements in order to reflect any event or circumstance that may arise after the date of this report, except as required by law. Readers are urged to carefully review and consider the various disclosures made throughout the entirety of this quarterly report, which are designed to advise interested parties of the risks and factors that may affect our business, financial condition, results of operations and prospects.

|

PART I-FINANCIAL INFORMATION

|

|

Item 1. Financial Statements

|

|

RETROPHIN, INC. AND SUBSIDIARIES

|

|

June 30, 2014

|

December 31, 2013

|

|||||||

|

(Unaudited)

|

||||||||

|

Assets

|

||||||||

|

Current assets:

|

||||||||

|

Cash

|

$ | 39,880,286 | $ | 5,997,307 | ||||

|

Marketable securities

|

3,563,914 | 132,994 | ||||||

|

Accounts receivable

|

1,600,769 | - | ||||||

|

Other receivable

|

5,963,889 | - | ||||||

|

Inventory

|

496,685 | - | ||||||

|

Prepaid expenses and other current assets

|

1,891,433 | 1,370,943 | ||||||

|

Total current assets

|

53,396,976 | 7,501,244 | ||||||

|

Property and equipment, net

|

511,275 | 127,427 | ||||||

|

Security deposits

|

288,997 | 244,058 | ||||||

|

Restricted cash

|

40,000 | 40,000 | ||||||

|

Other asset

|

1,927,757 | - | ||||||

|

Investment

|

400,000 | - | ||||||

|

Intangible assets, net

|

98,034,363 | 12,586,150 | ||||||

|

Goodwill

|

935,935 | - | ||||||

|

Total assets

|

$ | 155,535,303 | $ | 20,498,879 | ||||

|

Liabilities and Stockholders' Equity (Deficit)

|

||||||||

|

Current liabilities:

|

||||||||

|

Deferred technology purchase liability, current portion

|

$ | 1,500,000 | $ | 1,634,630 | ||||

|

Accounts payable

|

10,625,117 | 3,553,567 | ||||||

|

Accrued expenses

|

7,233,493 | 3,526,434 | ||||||

|

Securities sold, not yet purchased

|

144,850 | 1,457,901 | ||||||

|

Other liability

|

588,601 | - | ||||||

|

Contingent consideration, current portion

|

3,053,486 | - | ||||||

|

Derivative financial instruments, warrants

|

24,839,144 | 25,037,346 | ||||||

|

Total current liabilities

|

47,984,691 | 35,209,878 | ||||||

|

Note payable

|

39,834,960 | - | ||||||

|

Convertible debt

|

42,978,042 | - | ||||||

|

Other liability

|

12,783,110 | - | ||||||

|

Contingent consideration

|

9,746,515 | - | ||||||

|

Deferred technology purchase liability

|

1,000,000 | 1,000,000 | ||||||

|

Deferred income tax liability, net

|

141,151 | 2,600,899 | ||||||

|

Total liabilities

|

154,468,469 | 38,810,777 | ||||||

|

Commitments and contingencies

|

||||||||

|

Stockholders' Equity (Deficit):

|

||||||||

|

Preferred stock Series A $0.001 par value; 20,000,000 shares authorized; 0 issued and outstanding

|

- | - | ||||||

|

Common stock $0.0001 par value; 100,000,000 shares authorized; 26,681,514 and 18,546,363 issued and 26,301,923 and 18,415,573 outstanding, respectively

|

2,668 | 1,855 | ||||||

|

Additional paid-in capital

|

133,448,275 | 50,189,127 | ||||||

|

Treasury stock, at cost, 379,591 and 130,790, respectively

|

(3,214,608 | ) | (957,272 | ) | ||||

|

Accumulated deficit

|

(129,578,400 | ) | (67,435,621 | ) | ||||

|

Accumulated other comprehensive income (loss)

|

408,899 | (109,987 | ) | |||||

|

Total stockholders' equity (deficit)

|

1,066,834 | (18,311,898 | ) | |||||

|

Total liabilities and stockholders' equity (deficit)

|

$ | 155,535,303 | $ | 20,498,879 | ||||

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

|

||||||||

|

RETROPHIN, INC. AND SUBSIDIARIES

|

|

(Unaudited)

|

|

Three Months Ended June 30,

|

Six Months Ended June 30,

|

|||||||||||||||

|

2014

|

2013

|

2014

|

2013

|

|||||||||||||

|

Net product sales

|

$ | 5,741,734 | $ | - | $ | 5,769,634 | $ | - | ||||||||

|

Operating expenses:

|

||||||||||||||||

|

Cost of goods sold

|

1,207,395 | - | 1,208,295 | - | ||||||||||||

|

Research and development

|

13,697,991 | 605,203 | 20,584,717 | 713,937 | ||||||||||||

|

Selling, general and administrative

|

11,340,071 | 4,494,699 | 21,432,093 | 6,636,449 | ||||||||||||

|

Total operating expenses

|

26,245,457 | 5,099,902 | 43,225,105 | 7,350,386 | ||||||||||||

|

Operating loss

|

(20,503,723 | ) | (5,099,902 | ) | (37,455,471 | ) | (7,350,386 | ) | ||||||||

|

Other income (expenses):

|

||||||||||||||||

|

Interest income (expense), net

|

(2,178,937 | ) | 5 | (2,178,401 | ) | (41,558 | ) | |||||||||

|

Finance expense

|

(4,708,280 | ) | - | (4,708,280 | ) | - | ||||||||||

|

Realized gain on sale of marketable securities, net

|

370,177 | - | 374,841 | - | ||||||||||||

|

Change in fair value of derivative instruments - gain (loss)

|

32,978,586 | 56,041 | (20,635,216 | ) | (2,395,618 | ) | ||||||||||

|

Loss on transaction denominated in foreign currencies

|

- | (4,657 | ) | - | (3,873 | ) | ||||||||||

|

Total other income (expense), net

|

26,461,546 | 51,389 | (27,147,056 | ) | (2,441,049 | ) | ||||||||||

|

Income (loss) before provision for income taxes

|

5,957,823 | (5,048,513 | ) | (64,602,527 | ) | (9,791,435 | ) | |||||||||

|

Income tax benefit

|

2,525,124 | - | 2,459,748 | - | ||||||||||||

|

Net income (loss)

|

$ | 8,482,947 | $ | (5,048,513 | ) | $ | (62,142,779 | ) | $ | (9,791,435 | ) | |||||

|

Net income (loss) per common share, basic

|

$ | 0.33 | $ | (0.41 | ) | $ | (2.54 | ) | $ | (0.85 | ) | |||||

|

Net loss per common share, diluted

|

$ | (0.90 | ) | $ | (0.41 | ) | $ | (2.54 | ) | $ | (0.85 | ) | ||||

|

Weighted average common shares outstanding, basic

|

25,635,277 | 12,253,599 | 24,491,477 | 11,492,475 | ||||||||||||

|

Weighted average common shares outstanding, diluted

|

27,326,442 | 12,253,599 | 24,491,477 | 11,492,475 | ||||||||||||

|

Comprehensive Income (Loss):

|

||||||||||||||||

|

Net income (loss)

|

$ | 8,482,947 | $ | (5,048,513 | ) | $ | (62,142,779 | ) | $ | (9,791,435 | ) | |||||

|

Unrealized gain (loss)

|

(103,190 | ) | - | 518,886 | - | |||||||||||

|

Comprehensive income (loss)

|

$ | 8,379,757 | $ | (5,048,513 | ) | $ | (61,623,893 | ) | $ | (9,791,435 | ) | |||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

RETROPHIN, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENT OF CHANGES IN STOCKHOLDERS' DEFICIT

FOR THE PERIOD FROM DECEMBER 31, 2013 THROUGH JUNE 30, 2014

(Unaudited)

|

Common stock

|

Common stock in treasury

|

Additional paid | Accumulated other comprehensive | Accumulated | Total Stockholders' | |||||||||||||||||||||||||||

|

Shares

|

Amount

|

Shares

|

Amount

|

in capital

|

loss

|

deficit

|

deficit

|

|||||||||||||||||||||||||

|

Balance - December 31, 2013

|

18,546,363 | $ | 1,855 | (130,790 | ) | $ | (957,272 | ) | $ | 50,189,127 | $ | (109,987 | ) | $ | (67,435,621 | ) | $ | (18,311,898 | ) | |||||||||||||

|

Share based compensation

|

1,065,845 | 106 | - | - | 10,014,520 | - | - | 10,014,626 | ||||||||||||||||||||||||

|

Issuance of common stock in connection with January 2014 public offering at $8.50 per share, net of fees of $3,164,990

|

4,705,882 | 471 | - | - | 36,834,536 | - | - | 36,835,007 | ||||||||||||||||||||||||

|

Exercise of warrants and reclassification of the

derivative liability

|

1,962,377 | 196 | - | - | 31,701,852 | - | - | 31,702,048 | ||||||||||||||||||||||||

|

Treasury stock

|

- | - | (248,801 | ) | (2,257,336 | ) | - | - | - | (2,257,336 | ) | |||||||||||||||||||||

|

Issuance of common stock to convertible debt holders

|

401,047 | 40 | - | - | 4,708,240 | - | - | 4,708,280 | ||||||||||||||||||||||||

|

Unrealized gain

|

- | - | - | - | - | 518,886 | - | 518,886 | ||||||||||||||||||||||||

|

Net loss

|

- | - | - | - | - | - | (62,142,779 | ) | (62,142,779 | ) | ||||||||||||||||||||||

|

Balance - June 30, 2014

|

26,681,514 | $ | 2,668 | (379,591 | ) | $ | (3,214,608 | ) | $ | 133,448,275 | $ | 408,899 | $ | (129,578,400 | ) | $ | 1,066,834 | |||||||||||||||

The accompanying notes are an integral part of these condensed consolidated financial statements.

|

RETROPHIN, INC. AND SUBSIDIARIES

|

|

(Unaudited)

|

|

For the six months ended June 30,

|

||||||||

|

2014

|

2013

|

|||||||

|

Cash Flows From Operating Activities:

|

||||||||

|

Net loss

|

$ | (62,142,779 | ) | $ | (9,791,435 | ) | ||

|

Adjustments to reconcile net loss to net cash used in operating activities:

|

||||||||

|

Depreciation and amortization

|

1,692,606 | 105,307 | ||||||

|

Amortization of deferred financing costs

|

3,503 | |||||||

|

Amortization of debt discount

|

53,873 | |||||||

|

Realized gain on marketable securities

|

(374,841 | ) | - | |||||

|

Share based compensation

|

10,014,626 | 287,592 | ||||||

|

Change in estimated fair value of liability classified warrants

|

20,635,216 | 2,395,618 | ||||||

|

Non-cash financing cost

|

4,708,280 | |||||||

|

Changes in operating assets and liabilities, net of acquisitions:

|

||||||||

|

Accounts receivable

|

(1,600,769 | ) | - | |||||

|

Inventory

|

21,320 | - | ||||||

|

Prepaid expenses and other assets

|

(814,204 | ) | (96,065 | ) | ||||

|

Accounts payable and accrued expenses

|

6,547,781 | 312,001 | ||||||

|

Net cash used in operating activities

|

(21,255,388 | ) | (6,786,982 | ) | ||||

|

Cash Flows From Investing Activities:

|

||||||||

|

Purchase of fixed assets

|

(423,482 | ) | (9,693 | ) | ||||

|

Purchase of intangible asset

|

(3,301,534 | ) | (5,700 | ) | ||||

|

Repayment of technology license liability

|

- | (1,300,000 | ) | |||||

|

Security deposits

|

(44,939 | ) | - | |||||

|

Proceeds from the sale of marketable securities

|

1,884,584 | - | ||||||

|

Purchase of marketable securities

|

(4,887,184 | ) | - | |||||

|

Proceeds from securities sold, not yet purchased

|

4,462,144 | - | ||||||

|

Cover securities sold, not yet purchased

|

(5,309,791 | ) | - | |||||

|

Cash paid for investment

|

(400,000 | ) | - | |||||

|

Cash paid upon acquisition, net of cash acquired

|

(29,150,000 | ) | - | |||||

|

Net cash used in investing activities

|

(37,170,202 | ) | (1,315,393 | ) | ||||

|

Cash Flows From Financing Activities:

|

||||||||

|

Repayment of net amounts due to related parties

|

- | (13,200 | ) | |||||

|

Repayment of note payable - related party

|

- | (884,764 | ) | |||||

|

Proceeds from Credit Agreement

|

38,752,321 | - | ||||||

|

Proceeds from Note Purchase Agreement

|

41,924,169 | - | ||||||

|

Proceeds from the exercise of warrants

|

8,337,380 | - | ||||||

|

Proceeds received from issuance of common stock, net

|

36,835,007 | 9,275,465 | ||||||

|

Repayment of Manchester Note payable

|

(31,282,972 | ) | ||||||

|

Purchase of treasury stock, at cost

|

(2,257,336 | ) | - | |||||

|

Net cash provided by financing activities

|

92,308,569 | 8,377,501 | ||||||

|

Net (decrease) increase in cash

|

33,882,979 | 275,126 | ||||||

|

Cash, beginning of year

|

5,997,307 | 11,388 | ||||||

|

Cash, end of period

|

$ | 39,880,286 | $ | 286,514 | ||||

|

Supplemental Disclosure of Cash Flow Information:

|

||||||||

|

Cash paid for interest

|

$ | 1,832,984 | $ | 28,263 | ||||

|

Non-cash investing and financing activities:

|

||||||||

|

Reclassification of derivative liability to equity due to exercise of warrants

|

$ | 23,364,668 | $ | - | ||||

|

Present value of contingent consideration payable to sellers of Manchester Pharmaceuticals LLC

|

$ | 12,800,000 | $ | - | ||||

|

Present value of guaranteed minimum royalty payable to sellers of Thiola

|

$ | 11,849,648 | $ | - | ||||

|

Note payable entered into upon consummation of Manchester Pharmaceuticals LLC

|

$ | 31,282,972 | $ | - | ||||

|

Unrealized gain on marketable securities

|

$ | 1,858,744 | $ | - | ||||

|

Unrealized loss on securities sold, not yet purchased

|

$ | (1,339,858 | ) | $ | - | |||

|

Allocation of proceeds from issuance of common stock to registration payment obligation

|

$ | - | $ | 360,000 | ||||

|

Share issued on behalf of related party

|

$ | - | $ | 44,400 | ||||

|

Cost incurred related to debt financing not yet paid

|

$ | 1,882,128 | $ | - | ||||

|

The accompanying notes are an integral part of these condensed consolidated financial statements.

|

RETROPHIN, INC. AND SUBSIDIARIES

NOTES TO UNAUDITED CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

Organization and Description of Business

Retrophin, Inc. and its subsidiaries (the “Company”) is a fully integrated biopharmaceutical company focused on the development, acquisition and commercialization of therapies for the treatment of serious, catastrophic or rare diseases.

Acquisition of Manchester Pharmaceuticals LLC

On March 26, 2014, the Company completed its acquisition of all of the membership interests of Manchester Pharmaceuticals LLC, a privately-held specialty pharmaceutical company that focuses on treatments for rare diseases. The acquisition expands the Company’s ability to address the special needs of patients with rare diseases.

Thiola® License

On May 29, 2014, the Company entered into a license agreement with Mission Pharmacal Company (“Mission”), a privately-held healthcare medications and treatments provider, for the U.S. marketing rights to Thiola. The license adds Thiola to the Company’s product line. In July 2014, the Company amended the license agreement with Mission to secure the Canadian marketing rights to the product.

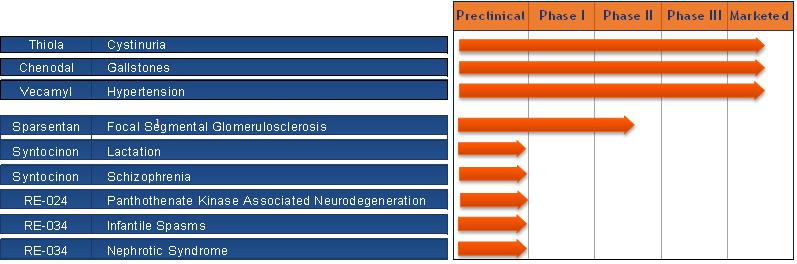

The Company currently sells the three following products:

|

·

|

Chenodal®, which is available in the United States for the treatment of patients suffering from gallstones in whom surgery poses an unacceptable health risk due to disease or advanced age.

|

|

·

|

Vecamyl®, which is available in the United States for the treatment of moderately severe to severe essential hypertension and uncomplicated cases of malignant hypertension.

|

|

·

|

Thiola, which is available in the United States for the prevention of cysteine (kidney) stone formation in patients with severe homozygous cystinuria.

|

The Company is developing RE-024, a novel small molecule, as a potential treatment for pantothenate kinase-associated neurodegeneration, or PKAN. Also, the Company is developing sparsentan, formerly known as RE-021, a dual acting receptor antagonist of angiotensin and endothelin receptors, for the treatment of focal segmental glomerulosclerosis, or FSGS. The Company is developing SyntocinonTM Nasal Spray in the United States to assist initial postpartum milk ejection, and for the treatment of Schizophrenia. Syntocinon Nasal Spray is currently marketed by Novartis and Sigma-Tau in Europe and other countries for aiding milk let-down. In addition, the Company is developing RE-034, a synthetic hormone analogue that is composed of the first 24 amino acids of the 39 amino acids contained in ACTH for the treatment of Infantile Spasms, or IS, and Nephrotic Syndrome, or NS. The Company also has several additional programs in preclinical development, including RE-001, a therapy for the treatment of Duchenne muscular dystrophy, or DMD.

NOTE 2. BASIS OF PRESENTATION

The accompanying unaudited condensed consolidated financial statements of the Company should be read in conjunction with the audited consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2013 (the “2013 10-K”) filed with the Securities and Exchange Commission (the “SEC”) on March 28, 2014. The accompanying condensed consolidated financial statements have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”) for interim financial information, the instructions to Form 10-Q and the rules and regulations of the SEC. Accordingly, since they are interim statements, the accompanying condensed consolidated financial statements do not include all of the information and notes required by GAAP for annual financial statements, but reflect all adjustments consisting of normal, recurring adjustments, that are necessary for a fair presentation of the financial position, results of operations and cash flows for the interim periods presented. Interim results are not necessarily indicative of results for a full year. The December 31, 2013 balance sheet information was derived from the audited financial statements as of that date.

NOTE 3. LIQUIDITY AND FINANCIAL CONDITION AND MANAGEMENT’S PLANS

The Company incurred a net loss of approximately $62.1 million, which includes a charge for the change in fair value of derivative instruments in the amount of $20.6 million, for the six months ended June 30, 2014. At June 30, 2014, the Company had a cash balance of approximately $39.9 million and working capital of approximately $5.4 million. The Company’s accumulated deficit amounted to approximately $129.6 million as of June 30, 2014.

The Company has principally financed its operations from inception using proceeds from sales of its equity securities in a series of private placement transactions and the issuance of debt. On January 9, 2014, the Company completed a public offering of 4,705,882 shares of common stock at a price of $8.50 per share. The Company received net proceeds from the offering of approximately $36.8 million, after deducting the underwriting fees and other offering costs.

On May 29, 2014, the Company entered into a Note Purchase Agreement (the “Note Purchase Agreement”) relating to the private placement of $46 million aggregate principal senior convertible notes with an interest rate of 4.50% due 2019 (the “Notes”). The Company received net funds from the Note Purchase Agreement of approximately $41.9 million. As of June 30, 2014, the Company has recorded $1 million as other receivable related to the Note Purchase Agreement due to a principal amount an investor agreed to purchase. As of the date of this filing, the $1 million has not been received, but the Company expects to receive such payment in the third quarter.

On June 30, 2014, the Company entered into a $45 million Credit Agreement (the “Credit Agreement”) which matures on June 30, 2018 and bears interest at an annual rate of (i) the Adjusted LIBOR Rate plus 10% or (ii) in certain circumstances, the Base Rate (as such term defined in the Credit Agreement) plus 9.00%. The Company received net funds from the Credit Agreement of approximately $38.8 million. As of June 30, 2014, the Company recorded approximately $5 million as other receivable related to the Credit Agreement due to funding received in July 2014.

On June 30, 2014, the Company made the final payment of $33 million to the sellers of Manchester Pharmaceuticals LLC (“Manchester”) in full satisfaction of the outstanding amount owed (see Note 5).

Management believes the Company’s ability to continue its operations depends on its ability to raise capital. The Company’s future depends on the costs, timing, and outcome of regulatory reviews of its product candidates, ongoing research and development, the funding of planned or potential acquisitions, other planned operating activities, and the costs of commercialization activities, including ongoing, product marketing, sales and distribution. The Company expects to continue to finance its cash needs through additional private and public equity offerings and debt financings, corporate collaboration and licensing arrangements and grants from patient advocacy groups, foundations and government agencies. Although management believes that the Company has access to capital resources, there are no commitments for financing in place at this time, nor can management provide any assurance that such financing will be available on commercially acceptable terms, if at all.

These conditions raise substantial doubt about the Company’s ability to continue as a going concern. These unaudited condensed consolidated financial statements do not include any adjustments relating to the recovery of assets or the classification of liabilities that might be necessary should the Company be unable to continue as a going concern.

NOTE 4. SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

A summary of the significant accounting policies applied in the preparation of the accompanying condensed consolidated financial statements follows:

Principles of Consolidation

The unaudited condensed consolidated financial statements represent the consolidation of the accounts of the Company and its subsidiaries in conformity with GAAP. All intercompany accounts and transactions have been eliminated in consolidation.

Accounts Receivable – Trade

The Company's trade accounts receivable represents amounts due from customers. The Company monitors the financial performance and credit worthiness of its customers so that it can properly assess and respond to changes in their credit profile. The Company provides reserves against trade receivables for estimated losses that may result from a customer's inability to pay. Amounts determined to be uncollectible are written-off against the reserve.

Inventory

Inventories are stated at the lower of cost or estimated realizable value. The Company determines the cost of inventory using the first-in, first-out, or FIFO, method. The Company periodically analyzes its inventory levels to identify inventory that may expire prior to expected sale or has a cost basis in excess of its estimated realizable value, and write down such inventories as appropriate. In addition, the Company's products are subject to strict quality control and monitoring which the Company’s manufacturers perform throughout their manufacturing process.

Inventory consists of the following at June 30, 2014:

|

June 30, 2014

|

||||

|

Raw material

|

$ | 375,875 | ||

|

Finished goods

|

120,810 | |||

|

Total inventory

|

$ | 496,685 | ||

Income Taxes

The Company follows FASB ASC 740, Income Taxes, which requires recognition of deferred tax assets and liabilities for the expected future tax consequences of events that have been included in the financial statements or tax returns. Under this method, deferred tax assets and liabilities are based on the differences between the financial statement and tax bases of assets and liabilities using enacted tax rates in effect for the year in which the differences are expected to reverse. Deferred tax assets are reduced by a valuation allowance to the extent management concludes it is more likely than not that the asset will not be realized. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences are expected to be recovered or settled.

The standard addresses the determination of whether tax benefits claimed or expected to be claimed on a tax return should be recorded in the financial statements. Under FASB ASC 740, the Company may recognize the tax benefit from an uncertain tax position only if it is more likely than not that the tax position will be sustained on examination by the tax authorities, based on the technical merits of the position. The tax benefits recognized in the financial statements from such a position should be measured based on the largest benefit that has a greater than fifty percent likelihood of being realized upon ultimate settlement. FASB ASC 740 also provides guidance on de-recognition, classification, interest and penalties on income taxes, accounting in interim periods and requires increased disclosures. As of June 30, 2014 and December 31, 2013, the Company has $1,522,063, and $0, respectively, recorded as a liability for unrecognized tax uncertainties, included in other liability-long term in the condensed consolidated balance sheet.

Revenue Recognition

Product sales consist of U.S. sales of Chenodal, Vecamyl, and Thiola. Revenue from product sales is recognized when persuasive evidence of an arrangement exists, title to product and associated risk of loss have passed to the customer, the price is fixed or determinable, collection from the customer is reasonably assured, the Company has no further performance obligations, and returns can be reasonably estimated. The Company records revenue from product sales upon delivery to its customers. The Company sells Chenodal and Vecamyl in the United States to a specialty pharmacy. Under this distribution model, the specialty pharmacy takes title of the inventory FOB shipping point and sells directly to patients. The Company sells Thiola in the United States and Canada through a specialty distributor. Under this model, the Company will record revenues once the distributor ships products to customers and such customers take title of the inventory FOB shipping point.

Government Rebates and Chargebacks: The Company estimates reductions to product sales for Medicaid programs, and for certain other qualifying federal and state government programs. Based upon the Company's contracts with government agencies, statutorily-defined discounts applicable to government-funded programs, historical experience, and estimated payer mix, the Company estimates and records an allowance for rebates and chargebacks as a reduction in sales. The Company's liability for Medicaid rebates consists of estimates for claims that a state will make for a current quarter, claims for prior quarters that have been estimated for which an invoice has not been received, and invoices received for claims from prior quarters that have not been paid. The Company's customers charge the Company for the difference between what they pay for the products and the ultimate selling price.

Distribution-Related Fees: The Company has written contracts with its customer that include terms for distribution-related fees. The Company estimates and records distribution and related fees due to its customer based on gross sales. Distribution-related fees amounted to $56,912 and $57,191 for the three and six months ended June 30, 2014, respectively, and are recorded as general and administrative expense in our condensed consolidated financial statements. Distribution-related fees were not incurred in 2013.

Prompt Pay Discounts: The Company offers discounts to its customers for prompt payments. The Company estimates these discounts based on customer terms and historical experience, and expect that its customer will always take advantage of this discount. Therefore, the Company accrues 100% of the prompt pay discount that is based on the gross amount of each invoice, at the time of sale.

Product Returns: Consistent with industry practice, the Company offers its customers a limited right to return product purchased directly from the Company, which is principally based upon the product's expiration date. Product returned is generally not resalable given the nature of the Company's products and method of administration. The Company develops estimates for product returns based upon historical experience, inventory levels in the distribution channel, shelf life of the product, and other relevant factors. The Company monitors product supply levels in the distribution channel, as well as sales by its customers to patients using product-specific data provided by its customers. If necessary, the Company's estimates of product returns may be adjusted in the future based on actual returns experience, known or expected changes in the marketplace, or other factors.

During the three and six months ended June 30, 2014, one customer accounted for 99% of the Company’s revenues. As of June 30, 2014 one customer accounted for 98% of accounts receivable.

Earnings (Loss) per Share

The Company adopted ASC 260, "Earnings Per Share" ("EPS"), which requires presentation of basic and diluted EPS on the face of the income statement for all entities with complex capital structures, and requires a reconciliation of the numerator and denominator of the basic EPS computation to the numerator and denominator of the diluted EPS computation. In the accompanying financial statements, basic earnings (loss) per share is computed by dividing net income (loss) by the weighted average number of shares of common stock outstanding during the period. Diluted EPS excluded all dilutive potential shares if their effect is anti-dilutive.

The following sets forth the computation of diluted EPS for the three months ended June 30, 2014:

|

Three months ended June 30, 2014

|

||||||||||||

|

Net income (loss) (Numerator)

|

Shares (Denominator)

|

Per Share Amount

|

||||||||||

|

Basic EPS

|

$ | 8,482,947 | 25,635,277 | $ | 0.33 | |||||||

|

Change in fair value of derivative instruments

|

(32,978,586 | ) | - | |||||||||

|

Dilutive shares related to warrants

|

- | 1,691,165 | ||||||||||

|

Dilutive EPS

|

$ | (24,495,639 | ) | 27,326,442 | $ | (0.90 | ) | |||||

Basic net income (loss) per share is based on the weighted average number of common and common equivalent shares outstanding. Potential common shares includable in the computation of fully diluted per share results are not presented for the six month ended June 30, 2014 and the periods ended June 30, 2013 in the condensed consolidated financial statements as their effect would be anti-dilutive. The total number of shares issuable upon exercise of options that were not included in dilutive earnings per share for the three and six months ended June 30, 2014 were 2,852,500. The total number of shares issuable upon conversion of debt that were not included in dilutive earnings per share for the three and six months ended June 30, 2014 were 2,642,160. The total number of shares issuable upon exercise of options that were not included in dilutive earnings per share for the three and six months ended June 30, 2013 were 120,000. The total number of shares issuable upon exercise of warrants that were not included in dilutive earnings per share for the three and six months ended June 30, 2013 were 1,917,792.

Financial Instruments and Fair Value

The Company accounts for financial instruments in accordance with ASC 820, “Fair Value Measurements and Disclosures” (“ASC 820”). ASC 820 establishes a fair value hierarchy that prioritizes the inputs to valuation techniques used to measure fair value. The hierarchy gives the highest priority to unadjusted quoted prices in active markets for identical assets or liabilities (Level 1 measurements) and the lowest priority to unobservable inputs (Level 3 measurements). The three levels of the fair value hierarchy under ASC 820 are described below:

Level 1 – Unadjusted quoted prices in active markets that are accessible at the measurement date for identical, unrestricted assets or liabilities;

Level 2 – Quoted prices in markets that are not active or financial instruments for which all significant inputs are observable, either directly or indirectly; and

Level 3 – Prices or valuations that require inputs that are both significant to the fair value measurement and unobservable.

In estimating the fair value of the Company’s marketable securities available-for-sale and securities sold, not yet purchased, the Company used quoted prices in active markets (see Note 6 and Note 8).

In estimating the fair value of the Company’s derivative liabilities, the Company used the Binomial Lattice options pricing model at inception and on each subsequent valuation date (see Note 7 and Note 8).

In estimating the fair value of the Company’s contingent consideration, the Company used the comparable uncontrolled transaction (“CUT”) method for royalty payments based on projected revenues. Based on the fair value hierarchy, the Company classified contingent consideration within Level 3 because valuation inputs are based on projected revenues discounted to a present value (see Note 8).

Financial instruments with carrying values approximating fair value include cash as well as accounts receivable, deposits on license agreements, and accounts payable.

New Accounting Standards

In May 2014, the Financial Accounting Standards Board (“FASB”) issued ASU 2014-09, "Revenue from Contracts with Customers (Topic 606)," which is the new comprehensive revenue recognition standard that will supersede all existing revenue recognition guidance under GAAP. The standard's core principle is that a company will recognize revenue when it transfers promised goods or services to a customer in an amount that reflects the consideration to which the company expects to be entitled in exchange for those goods or services. This ASU is effective for annual and interim periods beginning on or after December 15, 2016, and early adoption is not permitted. Companies will have the option of using either a full retrospective approach or a modified approach to adopt the guidance in the ASU. We are currently evaluating the impact of adopting this guidance.

Note 5. BUSINESS COMBINATION

Manchester Pharmaceuticals LLC

On March 26, 2014 (the “Manchester Closing Date”), the Company acquired 100% of the outstanding membership interests of Manchester. Under the terms of the agreement, the Company paid $29.5 million upon consummation of the transaction, of which $3.2 million was paid by Retrophin Therapeutics International LLC, a newly formed indirect wholly owned subsidiary, for rights of product sales outside of the United States. Acquisition costs amounted to approximately $0.3 million and have been recorded as selling, general, and administrative expense in the accompanying condensed consolidated financial statements. The Company entered into a promissory note with Manchester principals for $33 million which was discounted to $31.3 million to be paid in three equal installments of $11 million within three, six, and nine months after the Manchester Closing Date. On June 30, 2014, the Company paid the sellers of Manchester $33 million in full satisfaction of the outstanding amount owed.

In addition, the Company agreed to make contractual payments based on 10% of net sales of the products Chenodal and Vecamyl to the former members of Manchester. Additional contingent payments will be made based on 5% of net sales from new products derived from the existing products. Contingent consideration will be revalued at each reporting period and any change in valuation will be recorded in the Company’s statement of operations.

The acquisition was accounted for under the purchase method of accounting in accordance with ASC 805, with the excess purchase price over the fair market value of the assets acquired and liabilities assumed allocated to goodwill. Based on the preliminary purchase price allocation, the purchase price of $73.23 million has resulted in goodwill of $0.9 million and is primarily attributed to the synergies expected to arise after the acquisition. The $0.9 million of goodwill resulting from the acquisition is deductible for income tax purposes.

The fair value of assets acquired and liabilities assumed was based upon a preliminary valuation and the Company’s estimates and assumptions are subject to change within the measurement period. Critical estimates in valuing certain intangible assets include but are not limited to future expected cash flows from customer relationships and developed technology, present value and discount rates. Management’s estimates of fair value are based upon assumptions believed to be reasonable, but which are inherently uncertain and unpredictable and, as a result, actual results may differ from estimates.

The purchase included $72 million of intangible assets with definite lives related to product rights, trade names, and customer relationships with values of $71.4 million, $0.2 million, and $0.4 million, respectively. The useful lives related to the acquired product rights, trade names, and customer relationships are expected to be approximately 16, 1 and 10 years, respectively. Under the terms of the agreement, the sellers agreed to indemnify the Company for uncertain tax liabilities, any breach of any representation or warranty the sellers made to the purchaser, failure of the sellers to perform any covenants or obligations made to the purchaser, and third party claims relating to the operation of the Company and events occurring prior to the Manchester Closing Date. As of June 30, 2014, the Company has recorded an indemnification asset with a corresponding liability in the amount of $1.5 million related to uncertain tax liabilities.

The purchase price allocation of $73.23 million was as follows:

|

Amount (in thousands)

|

||||

|

Cash paid upon consummation, net

|

$ | 29,150 | ||

|

Secured promissory note

|

31,283 | |||

|

Fair value of contingent consideration

|

12,800 | |||

|

Total purchase price

|

$ | 73,233 | ||

|

Prepaid expenses

|

116 | |||

|

Inventory

|

517 | |||

|

Product rights

|

71,372 | |||

|

Trade names

|

175 | |||

|

Customer relationship

|

403 | |||

|

Goodwill

|

936 | |||

|

Other asset

|

1,522 | |||

|

Accounts payable and accrued expenses

|

(286 | ) | ||

|

Other liability

|

(1,522 | ) | ||

|

Total allocation of purchase price consideration

|

$ | 73,233 | ||

Pro Forma Operating Results

The following table provides unaudited pro forma results of operations for the three and six months ended June 30, 2014 and 2013, as if the March 26, 2014 acquisition had occurred on January 1, 2013. The pro forma results of operations were prepared for comparative purposes only and do not purport to be indicative of what would have occurred had the acquisitions been made as of January 1, 2013 or of results that may occur in the future.

|

Pro Forma (Unaudited)

|

||||||||||||||||

|

Three months ended June 30,

(in thousands, except per share data)

|

Six months ended June 30,

(in thousands, except per share data)

|

|||||||||||||||

|

2014

|

2013

|

2014

|

2013

|

|||||||||||||

|

Net Sales

|

$ | 5,742 | $ | 1,098 | $ | 6,988 | $ | 2,197 | ||||||||

|

Net income (loss)

|

$ | 8,483 | $ | (4,184 | ) | $ | (61,524 | ) | $ | (8,063 | ) | |||||

|

Net income (loss) per common share, basic

|

$ | 0.33 | $ | (0.34 | ) | $ | (2.51 | ) | $ | (0.70 | ) | |||||

|

Net loss per common share, diluted

|

$ | (0.90 | ) | $ | (0.34 | ) | $ | (2.51 | ) | $ | (0.70 | ) | ||||

NOTE 6. MARKETABLE SECURITIES AND SECURITIES SOLD, NOT YET PURCHASED

The Company measures marketable securities and securities sold, not yet purchased on a recurring basis. Generally, the types of securities the Company invests in are traded on a market such as the NASDAQ Global Market, which the Company considers to be Level 1 measurements.

Marketable securities and securities sold, not yet purchased at June 30, 2014 consisted of the following:

|

Cost

|

Unrealized Gains

|

Unrealized Losses

|

Estimated Fair Value

|

|||||||||||||

|

Marketable securities

available-for-sale:

|

$ | 3,157,355 | $ | 406,826 | $ | 267 | $ | 3,563,914 | ||||||||

|

Securities sold, not yet purchased

|

$ | 147,190 | $ | 2,340 | $ | - | $ | 144,850 | ||||||||

Marketable securities and securities sold, not yet purchased at December 31, 2013 consisted of the following:

|

Cost

|

Unrealized Gains

|

Unrealized Losses

|

Estimated Fair Value

|

|||||||||||||

|

Marketable securities

available-for-sale:

|

$ | 129,702 | $ | 3,292 | $ | - | $ | 132,994 | ||||||||

|

Securities sold, not yet purchased

|

$ | 1,344,622 | $ | 13,256 | $ | 126,535 | $ | 1,457,901 | ||||||||

NOTE 7. DERIVATIVE FINANCIAL INSTRUMENTS

The Company accounts for derivative financial instruments in accordance with ASC 815-40, “Derivative and Hedging – Contracts in Entity’s Own Equity” (“ASC 815-40”), instruments which do not have fixed settlement provisions are deemed to be derivative instruments. The Company’s warrants are classified as liability instruments due to an anti-dilution provision that provides for a reduction to the exercise price of the warrants if the Company issues additional equity or equity linked instruments in the future at an effective price per share less than the exercise price then in effect.

The warrants are re-measured at each balance sheet date based on estimated fair value. Changes in estimated fair value are recorded as non-cash valuation adjustments within other income (expense) in the Company’s accompanying condensed consolidated statements of operations. The Company recorded a gain on a change in the estimated fair value of warrants of $33 million and $0.06 million during the three months ended June 30, 2014 and 2013, respectively. The Company recorded a loss on a change in the estimated fair value of warrants of $20.6 million and $2.4 million during the six months ended June 30, 2014 and 2013, respectively.

The Company calculated the fair value of the warrants using the Binomial Lattice options pricing model at inception and on each subsequent valuation date. The assumptions used at June 30, 2014 and December 31, 2013 are as follows:

|

As of

|

||||||

|

December 31, 2013

|

June 30, 2014

|

|||||

|

Fair market price of common stock

|

$7.00 | $11.74 | ||||

|

Expected life (in years), represents the weighted average period until next liquidity event

|

4.12-4.62 years

|

.36 – 3.63 years

|

||||

|

Risk-free interest rate

|

1.39% | 1.11% - 1.62% | ||||

|

Expected volatility

|

93-97% | 85% | ||||

|

Dividend yield

|

0.00% | 0.00% | ||||

Expected volatility is based on analysis of the Company’s volatility, as well as the volatilities of guideline companies. The risk free interest rate is based on the U.S. Treasury security rates for the remaining term of the warrants at the measurement date.

NOTE 8. FAIR VALUE MEASUREMENTS

The following table presents the Company’s asset and liabilities that are measured and recognized at fair value on a recurring basis classified under the appropriate level of the fair value hierarchy as of June 30, 2014:

|

As of June 30, 2014

|

Fair Value Hierarchy at June 30, 2014

|

|||||||||||||||

|

Total carrying and estimated fair value

|

Quoted prices in active markets (Level 1)

|

Significant other observable inputs (Level 2)

|

Significant unobservable inputs (Level 3)

|

|||||||||||||

|

Asset:

|

||||||||||||||||

|

Marketable securities, available-for-sale

|

$ | 3,563,914 | $ | 3,563,914 | $ | - | ||||||||||

|

Liabilities:

|

||||||||||||||||

|

Derivative liability related to

warrants

|

$ | 24,839,144 | $ | - | $ | - | $ | 24,839,144 | ||||||||

|

Securities sold, not yet purchased

|

$ | 144,850 | $ | 144,850 | $ | - | $ | - | ||||||||

|

Contingent consideration

|

$ | 12,800,000 | $ | - | $ | - | $ | 12,800,000 | ||||||||

The following table presents the Company’s asset and liabilities that are measured and recognized at fair value on a recurring basis classified under the appropriate level of the fair value hierarchy as of December 31, 2013:

|

As of December 31, 2013

|

Fair Value Hierarchy at December 31, 2013

|

|||||||||||||||

|

Total carrying and estimated fair value

|

Quoted prices in active markets (Level 1)

|

Significant other observable inputs (Level 2)

|

Significant unobservable inputs (Level 3)

|

|||||||||||||

|

Asset:

|

||||||||||||||||

|

Marketable securities, available-for-sale

|

$ | 132,994 | $ | 132,994 | $ | - | $ | - | ||||||||

|

Liability:

|

||||||||||||||||

|

Derivative liability related to warrants

|

$ | 25,037,346 | $ | - | $ | - | $ | 25,037,346 | ||||||||

|

Securities sold, not yet purchased

|

$ | 1,457,901 | $ | 1,457,901 | $ | - | $ | - | ||||||||

The following table sets forth a summary of changes in the estimated fair value of the Company’s derivative financial instruments, warrants liability for the period from January 1, 2014 through June 30, 2014:

|

Fair Value Measurements of Common Stock Warrants Using Significant Unobservable Inputs (Level 3)

|

||||

|

Balance at January 1, 2013

|

$ | - | ||

|

Issuance of common stock warrants:

|

||||

|

February 14, 2013

|

5,407,372 | |||

|

August 14, 2013

|

328,561 | |||

|

August 15, 2013

|

9,201,487 | |||

|

Total value upon issuance

|

14,937,420 | |||

|

Change in fair value of common stock warrant liability

|

10,099,926 | |||

|

Balance at December 31, 2013

|

25,037,346 | |||

|

Issuance of common stock warrants, June 30, 2014 (Note 12)

|

2,531,250 | |||

|

Reclassification of derivative liability to equity upon exercise of warrants

|

(23,364,668 | ) | ||

|

Change in estimated fair value of liability classified warrants

|

20,635,216 | |||

|

Balance at June 30, 2014

|

$ | 24,839,144 | ||

A financial instrument’s level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. At each reporting period, the Company performs a detailed analysis of the assets and liabilities that are subject to ASC 820.

The following table sets forth a summary of changes in the estimated contingent consideration for the period from January 1, 2014 through June 30, 2014:

|

Fair Value Measurements of

Contingent Consideration

|

||||

|

Balance at January 1, 2014

|

$ | - | ||

|

Present value of contractual payments, contingent consideration upon acquisition

|

12,800,000 | |||

|

Balance at June 30, 2014

|

$ | 12,800,000 | ||

NOTE 9. INTANGIBLE ASSETS

Amortizable intangible assets

Ligand License Agreement

On February 16, 2012, the Company entered into an agreement for a worldwide sublicense for $2.5 million to develop, manufacture and commercialize a drug technology which is referred to as DARA (the “Ligand License Agreement”). The cost of the Ligand License Agreement, which is presented net of amortization in the accompanying condensed consolidated balance sheet as other amortizable intangible asset, is being amortized to research and development on a straight-line basis through September 30, 2023.

Syntocinon License Agreement

On December 12, 2013, the Company entered into an agreement with Novartis Pharma AG and Novartis AG pursuant to which Novartis Pharma AG and Novartis AG agreed to grant the Company an exclusive, perpetual, and royalty-bearing license for the manufacture, development and commercialization of Syntocinon and related intranasal products in the United States (the “Syntocinon License Agreement”). Under the Syntocinon License Agreement, Novartis Pharma AG and Novartis AG are obligated to transfer to the Company certain information that is necessary for or related to the development or commercialization of Syntocinon. As consideration for the Syntocinon License Agreement, the Company paid to Novartis Pharma AG and Novartis AG, and capitalized, a $5 million upfront fee. The intellectual property underlying the Syntocinon License Agreement is held in perpetuity. The Company has examined the Syntocinon License Agreement and has capitalized the license fee in accordance with ASC 350 due to future alternative uses such as re-licensing of the technology to other third parties, the sale of the licensed technology to other life science companies, and the potential development of various ingestible drug products using the licensed technologies.

During the quarter ended June 30, 2014, certain key underlying assumptions regarding the estimated useful life of the Syntocinon License Agreement changed resulting in the Company changing the estimated useful life from indefinite-lived to definite lived, starting in the second quarter of 2014. Such changes relate to the regulatory requirements needed to re-introduce the product for the treatment of lactation deficiency. Management determined the development program approximates seven to eight years and the use patent exclusivity and/or commercial viability period upon approval will be eleven to twelve years. Management assigned a life of twenty (20) years to the asset and is being amortized to research and development on a straight-line basis through December 2033.

Kyalin - Carbetocin Technology Purchase

On December 23, 2013, the Company entered into a stock purchase agreement with Kyalin to acquire substantially all of Kyalin’s assets which include patents, patent applications, contracts and data related to the intranasal formulation of the compound Carbetocin (collectively, the “Carbetocin Assets”). Carbetocin, similar to Oxytocin, has potential utility for the treatment of milk let-down in post pregnant women, inducing contractions during labor, postpartum hemorrhage, as well as for schizophrenia.

The Company capitalized $3 million of fixed minimum payments and closing costs. For tax purposes, intangible assets are subject to different amortization allowances than for book purposes. FASB ASC 740-10-55 (“ASC 740”) addresses the accounting treatment when an asset is acquired outside of a business combination, and the tax basis of that asset differs from the amount paid. For the year ended December 31, 2013, pursuant to the guidance in ASC 740, the Company has stepped-up the basis of its intangible assets by $2.5 million and has recorded a deferred tax liability in the same amount, to account for the book/tax basis difference resulting from the Kyalin acquisition.

During the quarter ended June 30, 2014, certain underlying assumptions regarding the estimated useful life of the Carbetocin Assets changed resulting in the Company changing the estimated useful life from indefinite-lived to definite lived, starting in the second quarter of 2014. Such changes relate to the regulatory requirements needed to develop the Carbetocin Assets, as well as the departure of key personnel responsible for the development of the Carbetocin Assets. Management determined the development program approximates five to seven years and commercial viability will be five to seven years. Management assigned a life of ten (10) years to the assets and is being amortized to research and development on a straight-line basis through December 2023.

The change in estimated useful life in the current quarter also resulted in reversal of the deferred tax liability and recording a tax benefit of $2.5 million, as it was no longer necessary to account for the book/tax difference of Kyalin.

Manchester Pharmaceuticals LLC

Upon the completion of the Company’s acquisition of Manchester on March 26, 2014, it acquired intangible assets with definite lives related to product rights, trade names, and customer relationships with the values of $71.4 million, $0.2 million, and $0.4 million, respectively. The useful lives related to the acquired product rights, trade names, and customer relationships are expected to be approximately 16, 1 and, 10 years, respectively. Amortization of product rights is being recorded as cost of goods sold and amortization of trade names and customer relationships is being recorded as general and administrative expense over their respective lives.

Thiola License Agreement

On May 29, 2014, the Company entered into a license agreement with Mission Pharmacal Company (“Mission”), pursuant to which Mission agreed to grant the Company an exclusive, royalty-bearing license to market, sell and commercialize Thiola in the United States and a non-exclusive license to use know-how relating to Thiola to the extent necessary to market Thiola. In July 2014, the Company amended the license agreement with Mission to secure the Canadian marketing rights to the product for no additional consideration.

Upon execution of the agreement, the Company paid Mission an up-front license fee of $3 million. In addition, the Company shall pay guaranteed minimum royalties during each calendar year the greater of $2 million or twenty percent (20%) of the Company’s net sales of Thiola through June 30, 2024. As of June 30, 2014, the present value of guaranteed minimum royalties payable is $11.8 million using a discount rate of approximately 11% based on the Company’s current borrowing rate. As of June 30, 2014, the guaranteed minimum royalties’ current and long term liability is approximately $.6 million and $11.2 million, respectively, and is recorded as other liability in the condensed consolidated balance sheet. The Company capitalized $15 million related to the Thiola asset which consists of the up-front license fee, professional fees, and the present value of the guaranteed minimum royalties.

As of June 30, 2014, amortizable intangible assets were approximately $98 million. Amortization expense recorded as research and development amounted to $255,430 and $305,386 for the three and six months ended June 30, 2014, respectively. Amortization expense recorded as research and development amounted to $0 for the three and six months ended June 30, 2013. Amortization expense recorded as general and administrative amounted to $172,203 and $175,151 for the three and six months ended June 30, 2014, and $50,511 and $100,466 for the three and six months ended June 30, 2013, respectively. Amortization expense recorded as cost of goods sold amounted to $1,111,371 and $1,172,435 for the three and six months ended June 30, 2014, respectively. Amortization expense recorded as cost of goods sold amounted to $0 for each of the three and six months ended June 30, 2013.

Amortizable intangible assets as of June 30, 2014 and December 31, 2013 consist of the following:

| June 30, 2014 | ||||||||||||

|

Gross Carrying Amount

|

Accumulated Amortization

|

Net Book Value

|

||||||||||

|

Product Rights

|

$ | 71,372,000 | $ | (1,172,435 | ) | $ | 70,199,565 | |||||

|

Thiola License

|

15,049,647 | (118,533 | ) | 14,931,114 | ||||||||

|

Carbetocin Assets*

|

5,567,736 | (141,074 | ) | 5,426,662 | ||||||||

|

Syntocinon License*

|

5,000,000 | (62,552 | ) | 4,937,448 | ||||||||

|

Ligand License

|

2,300,000 | (424,447 | ) | 1,875,553 | ||||||||

|

Customer Relationships

|

403,000 | (10,591 | ) | 392,409 | ||||||||

|

Trade Name

|

175,000 | (46,027 | ) | 128,973 | ||||||||

|

Patent Costs

|

143,928 | (1,289 | ) | 142,639 | ||||||||

|

Total

|

$ | 100,011,311 | $ | (1,976,948 | ) | $ | 98,034,363 | |||||

* The Company commenced amortization in the current quarter due to change in estimate.

| December 31, 2013 | ||||||||||||

|

Gross Carrying

Amount

|

Accumulated Amortization

|

Net Book Value

|

||||||||||

|

Ligand License

|

$ | 2,300,000 | $ | (323,980 | ) | $ | 1,976,020 | |||||

|

Patent Costs

|

49,775 | - | 49,775 | |||||||||

|

Total

|

$ | 2,349,775 | $ | (323,980 | ) | $ | 2,025,795 | |||||

Amortization expense for the years ended December 31, 2014, 2015, 2016, 2017, and 2018 is expected to be $5,281,810, $7,064,263, $7,042,752, $7,023,509, and $7,023,509 respectively.

NOTE 10. RESEARCH AND DEVELOPMENT

Research and development expenses consist of the following for the three and six months ended June 30, 2014 and 2013:

|

Three Months Ended June 30

|

Six Months Ended June 30

|

|||||||||||||||

|

2014

|

2013

|

2014

|

2013

|

|||||||||||||

|

External service provider costs:

|

||||||||||||||||

|

Sparsentan

|

$ | 2,647,735 | $ | 356,238 | $ | 3,577,175 | $ | 464,973 | ||||||||

|

RE-024

|

3,745,059 | - | 6,110,068 | - | ||||||||||||

|

Syntocinon

|

517,899 | - | 642,765 | - | ||||||||||||

|

RE-034

|

602,129 | - | 1,177,815 | - | ||||||||||||

|

General

|

2,036,756 | - | 3,118,476 | - | ||||||||||||

|

Other product candidates

|

312,275 | - | 610,677 | - | ||||||||||||

|

Amortization

|

255,430 | - | 305,386 | - | ||||||||||||

|

Total external service provider costs:

|

10,117,283 | 356,238 | 15,542,362 | 464,973 | ||||||||||||

|

Internal personnel costs:

|

3,580,708 | 248,965 | 5,042,355 | 248,964 | ||||||||||||

|

Total research and development

|

$ | 13,697,991 | $ | 605,203 | $ | 20,584,717 | $ | 713,937 | ||||||||

NOTE 11. SELLING, GENERAL, AND ADMINISTRATIVE

Selling, general, and administrative expenses consist of the following for the three and six months ended June 30, 2014 and 2013, respectively:

|

Three Months Ended June 30

|

Six Months Ended June 30

|

|||||||||||||||

|

2014

|

2013

|

2014

|

2013

|

|||||||||||||

|

Professional fees

|

$ | 4,913,393 | $ | 1,595,026 | $ | 11,068,778 | $ | 1,928,868 | ||||||||

|

Compensation and related costs

|

3,847,879 | 358,167 | 5,931,468 | 1,288,454 | ||||||||||||

|

Depreciation and amortization

|

198,619 | 53,139 | 214,785 | 105,307 | ||||||||||||

|

Other

|

2,380,180 | 2,488,367 | 4,217,062 | 3,313,820 | ||||||||||||

|

Total selling, general, and administrative expenses

|

$ | 11,340,071 | $ | 4,494,699 | $ | 21,432,093 | $ | 6,636,449 | ||||||||

NOTE 12. NOTES PAYABLE

Total interest expense recognized for the three and six months ended June 30, 2014 aggregated to $2,178,937 and $2,178,401, respectively. Total interest income (expense) recognized for the three and six months ended June 30, 2013 aggregated to $5 and ($41,558), respectively.

Note Payable – Manchester Pharmaceuticals, LLC

On March 26, 2014 upon the acquisition of Manchester, the Company entered into a note payable in the amount of $33 million. The note is non-interest bearing and therefore the Company recorded the loan at present value of $31.2 million using the effective interest rate of approximately 11%, which is the Company’s current borrowing rate. The note was due and payable in three consecutive payments, each in the amount of $11 million payable on June 26, 2014, September 26, 2014, and December 12, 2014 (the maturity date). On June 30, 2014, the Company paid off the note in its entirety. The Company accelerated interest expense in the amount of $1.7 million for the difference between the present value of the loan and the loan balance paid.

Convertible Notes Payable

On May 29, 2014, the Company entered into a Note Purchase Agreement with the investors thereunder (the “Investors”) relating to a private placement by the Company of $46 million aggregate principal senior convertible notes due 2019 (the “Notes”), which are convertible into shares of the Company’s common stock at an initial conversion price of $17.41 per share. The conversion price is subject to customary anti-dilution protection. The Notes bear interest at a rate of 4.5% per annum, payable semiannually in arrears on May 15 and November 15 of each year, beginning on November 15. The Notes mature on May 30, 2019 unless earlier converted or repurchased in accordance with the terms. The aggregate carrying value of the Notes on their issuance was $43 million, which was net of the $3 million debt discount. The debt discount is being amortized to interest expense over the term of the Notes under the effective interest method. As of June 30, 2014, accrued interest amounted to $0.2 million related to the convertible notes payable.

On June 30, 2014, the Company issued 401,047 shares of Common Stock to the Investors and such Investors granted the Company a release of certain claims they may have had in connection with the Company's sale of the Notes or certain statements made by the Company in connection with such sale. The Company recorded finance expense as other expense in the amount of $4,708,280 in relation to the shares issued based on the fair market value of the stock on the date of issuance.

Note Payable with Detachable Warrants

On June 30, 2014, the Company entered into a $45 million Credit Agreement which matures on June 30, 2018 and bears interest at an annual rate of (i) the Adjusted LIBOR Rate (as such term is defined in the Credit Agreement) plus 10.00% or (ii) in certain circumstances, the Base Rate (as such term is defined in the Credit Agreement) plus 9.00%. The Credit Agreement contains certain covenants, including those limiting the Company's and its subsidiaries' abilities to incur indebtedness, incur liens, sell or acquire assets or businesses, change the nature of their businesses, engage in transactions with related parties, make certain investments or pay dividends. In addition, the Credit Agreement requires the Company and its subsidiaries to meet certain financial quarterly requirements commencing in September 2014. Failure by the Company or its subsidiaries to comply with any of these covenants or financial tests could result in the acceleration of the loans under the Credit Agreement. The aggregate carrying value of the convertible notes on their issuance was $39.8 million, which was net of the $5.2 million debt discount. The debt discount is being amortized to interest expense over the term of the notes under the effective interest method. No interest expense was incurred during the quarter ended June 30, 2014 related to the Note Payable.

In connection with the execution of the Credit Agreement, the Company issued warrants (the "Warrants") to the Lenders under the Credit Agreement, initially exercisable to purchase up to an aggregate of 337,500 shares of common stock of the Company. The Warrants will be exercisable in whole or in part, at an initial exercise price per share of $12.76 per share, which is subject to weighted-average anti-dilution protections. The Warrants may be exercised at any time upon the election of the holder, beginning on the date of issuance and ending on the fifth anniversary of the date of issuance. The issuance of the Warrants was not registered under the Securities Act of 1933, as amended (the "Securities Act") as such issuance was exempt from registration under Section 4(2) of the Securities Act.

The total grant date fair value of the Warrants is $2.5 million and was recorded as a derivative liability and is included in the debt discount to the Note Payable. The Company calculates the fair value of the warrants using the Binomial Lattice pricing model using the following assumptions:

|

Risk free rate

|

1.62%

|

|

|

Expected volatility

|

85%

|

|

|

Expected life (in years), represents the weighted average period until next liquidity event

|

0.36

|

|

|

Expected dividend yield

|

-

|

|

|

Exercise Price

|

$12.76

|

Debt Maturities

The stated maturities of the Company’s long-term debt at December 31 are as follows (in millions):

|

2014

|

$ | - | ||

|

2015

|

- | |||

|

2016

|

- | |||

|

2017

|

- | |||

|

2018

|

45 | |||

|

Thereafter

|

46 | |||

|

|

$ | 91 |

NOTE 13. COMMITMENTS AND CONTINGENCIES

Leases and Sublease

On February 28, 2014, the Company amended its lease agreement for its offices located in Carlsbad, California. The Company increased its Carlsbad office space for approximately $110,000 of additional annual base rent plus rent escalations, common area maintenance, insurance, and real estate taxes under a lease agreement expiring in June 2017.

On April 10, 2014, the Company entered into an amended lease agreement at its principal offices in New York, New York and is responsible for additional rent of approximately $537,264 annually plus rent escalations through April 2015.

Research Collaboration and Licensing Agreements

As part of the Company's research and development efforts, the Company enters into research collaboration and licensing agreements with unrelated companies, scientific collaborators, universities, and consultants. These agreements contain varying terms and provisions which include fees and milestones to be paid by the Company, services to be provided, and ownership rights to certain proprietary technology developed under the agreements. Some of these agreements contain provisions which require the Company to pay royalties in the event the Company sells or licenses any proprietary products developed under the respective agreements.

Contract Commitments

The following table summarizes our principal contractual commitments, excluding open orders that support normal operations, as of June 30, 2014:

|

Year Ending December 31,

|

Research and Development and

other Charitable Donations

|

Consultants

|

Operating Leases

|

|||||||||

|

2014

|

$ | 5,332,827 | $ | 220,830 | $ | 1,133,034 | ||||||

|

2015

|

4,941,144 | - | 1,054,961 | |||||||||

|

2016

|

- | - | 836,978 | |||||||||

|

2017

|

- | - | 70,504 | |||||||||

|

Total

|

$ | 10,273,971 | $ | 220,830 | $ | 3,095,477 | ||||||

Legal Proceedings

In Charles Schwab & Co., Inc. v. Retrophin, Inc., et. al., Case No. 14 CV 4294 (S.D.N.Y.), the plaintiff, Charles Schwab & Co., Inc. (“Schwab”), asserts that it was misled by two of its customers, Jackson Su (“Su”), and Chun Yi “George” Huang (“Huang”), who are former employees of the Company, and who induced Schwab to wrongfully execute sales of their restricted shares of the Company’s common stock (the “Shares”). Schwab has also alleged that certain agents of the Company provided incorrect information to Schwab in connection with the sale of the Shares. Schwab has alleged that as a result of its detrimental reliance on the incorrect information provided to it by the Company’s agents, it has incurred in excess of $2 million in damages. Su and Huang have asserted “cross-claims” against the Company for alleged fraud and negligent misrepresentation premised upon the Company’s alleged failure to inform them of restrictions on the sale of their Shares. The Company believes that it has valid defenses against all claims and that it is not responsible for any losses incurred by the other parties. The Company cannot predict the timing or outcome of this litigation.

From time to time the Company is involved in legal proceedings arising in the ordinary course of business. The Company believes there is no other litigation pending that could have, individually or in the aggregate, a material adverse effect on its results of operations or financial condition.

NOTE 14. STOCKHOLDERS’ DEFICIT

Common Stock

The Company is currently authorized to issue up to 100,000,000 shares of $0.0001 par value common stock. All issued shares of common stock are entitled to vote on a 1 share/1 vote basis.

Preferred Stock

The Company is currently authorized to issue up to 20,000,000 shares of $0.001 preferred stock, of which 1,000 shares are designated Class "A" Preferred shares, $0.001 par value. Class A Preferred Shares are not entitled to interest, have certain liquidation preferences, special voting rights and other provisions. No Preferred Shares have been issued to date.

Issuances

Public Offering - 2014

On January 9, 2014, the Company completed a public offering of 4,705,882 shares of common stock at a price of $8.50 per share. The Company received net proceeds from the offering of $36,835,007, after deducting the underwriting fees and other offering costs of $3,164,990, which were recorded against additional paid in capital.

Restricted Shares