Exhibit 3.4(i)

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

EXCHANGE ACT OF 1934

For

the quarterly period ended

or

EXCHANGE ACT OF 1934

Commission

File Number:

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation)

(Commission File Number) |

(IRS Employer Identification No.) |

| (Address of principal executive offices) | (Zip Code) |

Registrant’s

telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||

| OTC QB |

Indicate by check mark if the registrant is a well-known seasoned issuer as defined in Rule 405 of the Securities Act.

Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this form 10-K or any amendment to this form 10-K.

Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer ☐ | Accelerated filer ☐ |

| Smaller

reporting company | |

| Emerging

Growth Company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes

☐ No

APPLICABLE ONLY TO ISSUERS INVOLVED IN BANKRUPTCY PROCEEDINGS DURING THE PRECEDING FIVE YEARS:

Indicate by check mark whether the registrant has filed all documents and reports required to be filed by Sections 12, 13 or 15(d) of the Securities Exchange Act of 1934 subsequent to the distribution of securities under a plan confirmed by a court.

Yes ☐ No ☐

APPLICABLE ONLY TO CORPORATE ISSUERS:

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

As of the date of this filing, there were shares of the Issuer’s common stock issued and outstanding and held by approximately 138 shareholders, six of which are deemed affiliates within the meaning of Rule 12b-2 under the Exchange Act.

As of the date of this filing, there were 20,000 shares of the Issuer’s preferred stock issued and outstanding.

CyberloQ Technologies, Inc.

FORM 10-Q

For The Fiscal Quarter Ended March 31, 2024

TABLE OF CONTENTS

| 2 |

PART I

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This quarterly report on Form 10-Q and the documents incorporated by reference herein contain forward-looking statements that are not statements of historical fact and may involve a number of risks and uncertainties. These statements related to analyses and other information that are based on forecasts of future results and estimates of amounts not yet determinable. These statements may also relate to our future prospects, developments and business strategies. These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance, or achievements expressed or implied by forward-looking statements.

In some cases, you can identify forward-looking statements by terminology such as “may,” “should,” “expects,” “plans,” “anticipates,” “believes,” “estimates,” “predicts,” “potential,” “proposed,” “intended,” or “continue” or the negative of these terms or other comparable terminology. You should read statements that contain these words carefully, because they discuss our expectations about our future operating results or our future financial condition or state other “forward-looking” information. There may be events in the future that we are not able to accurately predict or control. Before you invest in our securities, you should be aware that the occurrence of any of the events described in this quarterly report could substantially harm our business, results of operations and financial condition, and that upon the occurrence of any of these events, the trading price of our securities could decline and you could lose all or part of your investment. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, growth rates, levels of activity, performance or achievements. We are under no duty to update any of the forward-looking statements after the date of this Annual Report to conform these statements to actual results.

The following factors are among those that may cause actual results to differ materially from our forward-looking statements:

| ● | General economic and industry conditions; | |

| ● | Out history of losses, deficits and negative operating cash flows; | |

| ● | Our limited operating history; | |

| ● | Industry competition; | |

| ● | Environmental and governmental regulation; | |

| ● | Protection and defense of our intellectual property rights; | |

| ● | Reliance on, and the ability to attract, key personnel; | |

| ● | Other factors including those discussed in “Risk Factors” in this quarterly report on Form 10-Q and our incorporated documents. |

You should keep in mind that any forward-looking statement made by us in this quarterly report or elsewhere speaks only as of the date on which we make it. New risks and uncertainties arise from time to time, and it is impossible for us to predict these events or how they may affect us. We have no duty to, and do not intend to, update or revise the forward-looking statements in this annual report after the date of filing, except as may be required by law. In light of these risks and uncertainties, you should keep in mind that any forward-looking statement made in this annual report or elsewhere might not occur.

In this quarterly report on Form 10-Q, the terms “CLOQ,” “Company,” “we,” “us” and “our” refer to CyberloQ Technologies, Inc. and its wholly-owned subsidiary CyberloQ Technologies, LTD.

| 3 |

Item 1. FINANCIAL STATEMENTS

CyberloQ Technologies, Inc.

CONSOLIDATED CONDENSED BALANCE SHEETS

| March 31, 2024 | December 31, 2023 | |||||||

| (unaudited) | ||||||||

| ASSETS | ||||||||

| Current Assets | ||||||||

| Cash | $ | $ | ||||||

| Accounts receivable | ||||||||

| Deposits and prepaids | ||||||||

| Total Current Assets | ||||||||

| Fixed Assets | ||||||||

| Cyberloq platform | ||||||||

| Website | ||||||||

| Total Fixed Assets | ||||||||

| Total Assets | $ | $ | ||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||

| Current Liabilities | ||||||||

| Accounts Payable and Accrued Expenses | $ | $ | ||||||

| Accrued interest | ||||||||

| Note Payable – Stockholders | ||||||||

| Note Payable – Related Party | ||||||||

| Convertible debt – Stockholders, net | ||||||||

| Loan payable - SBA | ||||||||

| Total Current Liabilities | ||||||||

| Long Term Liabilities | ||||||||

| SBA Loan Payable | ||||||||

| Total Long Term Liabilities | ||||||||

| Total Liabilities | ||||||||

| Commitments and Contingencies | ||||||||

| Stockholders’ Equity | ||||||||

| Common stock: $ par value, shares authorized; and shares issued and outstanding, respectively | ||||||||

| Preferred Stock $ per value - shares authorized; issued and outstanding | ||||||||

| Treasury stock | ( | ) | ( | ) | ||||

| Shares to be Issued: and common shares respectively | ||||||||

| Additional Paid in Capital | ||||||||

| Accumulated Deficit | ( | ) | ( | ) | ||||

| Total Stockholders’ Equity | ||||||||

| Total Liabilities and Stockholders’ Equity | $ | $ | ||||||

See accompanying notes to financial statements

| F-1 |

CyberloQ Technologies, Inc.

CONSOLIDATED CONDENSED STATEMENTS OF OPERATIONS

| For the Three Months Ended March 31, | ||||||||

| 2024 | 2023 | |||||||

| (unaudited) | (unaudited) | |||||||

| Revenue | ||||||||

| Service Revenue | $ | $ | ||||||

| License fees | ||||||||

| Total Revenue | ||||||||

| Operational Expense | ||||||||

| Professional Fees | ||||||||

| Officer’s Compensation | ||||||||

| Travel and Entertainment | ||||||||

| Rent | ||||||||

| Computer and Internet | ||||||||

| Office Supplies and Expenses | ||||||||

| Other Operating Expenses | ||||||||

| Total Operating Expenses | ||||||||

| Loss from Operations | ( | ) | ( | ) | ||||

| Other Income (Expense) | ||||||||

| Interest | ( | ) | ( | ) | ||||

| Amortization of debt discount | ( | ) | ( | ) | ||||

| Total Other Income (Expenses) | ( | ) | ( | ) | ||||

| Provision for Income Taxes | ||||||||

| Net Loss | $ | ( | ) | $ | ( | ) | ||

| Loss per common share-Basic and diluted | $ | ) | $ | ) | ||||

| Weighted Average Number of Common Shares Outstanding Basic and diluted | ||||||||

See accompanying notes to financial statements

| F-2 |

CyberloQ Technologies, Inc.

CONSOLIDATED STATEMENTS OF CHANGES IN STOCKHOLDERS’ EQUITY (DEFICIT)

(unaudited)

From January 1, 2023 to March 31, 2024

| Common (Issued) | Common (Unissued) | Preferred Stock | Add’l Paid-In | Treasury | Accum. | |||||||||||||||||||||||||||||||||||

| Shares | Amount | Shares | Amount | Shares | Amount | Capital | Stock | Deficit | Total | |||||||||||||||||||||||||||||||

| Balance, December 31, 2022 | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | ||||||||||||||||||||||||||||||

| Common stock issued for cash | - | - | ||||||||||||||||||||||||||||||||||||||

| Beneficial conversion feature of convertible debt | - | - | - | |||||||||||||||||||||||||||||||||||||

| Net loss for quarter ending March 31, 2023 | - | - | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||||||

| Balance, March 31, 2023 | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||||||||||||

| Common stock issued for cash | - | - | ||||||||||||||||||||||||||||||||||||||

| Beneficial conversion feature of convertible debt | - | - | - | |||||||||||||||||||||||||||||||||||||

| Net loss for period ended June 30, 2023 | - | - | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||||||

| Balance, June 30, 2023 | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ||||||||||||||||||||||||||||||

| Common stock issued for cash | - | - | ||||||||||||||||||||||||||||||||||||||

| Beneficial conversion feature of convertible debt | - | - | - | |||||||||||||||||||||||||||||||||||||

| Net loss for period ended September 30, 2023 | - | - | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||||||

| Balance, September 30, 2023 | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | |||||||||||||||||||||||||||||

| Common stock issued for cash | - | - | ||||||||||||||||||||||||||||||||||||||

| Common stock issued for services | - | - | ||||||||||||||||||||||||||||||||||||||

| Beneficial conversion feature of convertible debt | - | - | - | |||||||||||||||||||||||||||||||||||||

| Net loss for period ended December 31, 2023 | - | - | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||||||

| Balance, December 31, 2023 | ( | ) | ( | ) | ||||||||||||||||||||||||||||||||||||

| Common stock issued for cash | - | - | ||||||||||||||||||||||||||||||||||||||

| Common stock issued for services | ||||||||||||||||||||||||||||||||||||||||

| Beneficial conversion feature of convertible debt | - | - | - | |||||||||||||||||||||||||||||||||||||

| Net loss for period ended March 31, 2024 | - | - | - | ( | ) | ( | ) | |||||||||||||||||||||||||||||||||

| Balance, March 31, 2024 | $ | $ | $ | $ | $ | $ | ( | ) | $ | ( | ) | $ | ||||||||||||||||||||||||||||

See accompanying notes to financial statements

| F-3 |

CyberloQ Technologies, Inc.

CONSOLIDATED CONDENSED STATEMENTS OF CASH FLOWS

For the Three Months Ended March 31,

| 2024 | 2023 | |||||||

| (unaudited) | (unaudited) | |||||||

| OPERATING ACTIVITIES | ||||||||

| Net loss | $ | ( | ) | $ | ( | ) | ||

| Adjustments to reconcile net loss to net cash used in operating activities: | ||||||||

| Amortization of debt discount | ||||||||

| Stock compensation | ||||||||

| Change in Operating Assets and Liabilities: | ||||||||

| Decrease (increase) in accounts receivable | ( | ) | ||||||

| Decrease (increase) in deposits and prepaids | ( | ) | ||||||

| Increase (decrease) in accounts payable and accrued expenses | ( | ) | ( | ) | ||||

| Increase (decrease) in accrued interest | ||||||||

| Net Cash Used in Operating Activities | ( | ) | ( | ) | ||||

| INVESTING ACTIVITIES | ||||||||

| Software | ( | ) | ( | ) | ||||

| Website | ( | ) | ||||||

| Net cash provided by (used) in investing activities | ( | ) | ( | ) | ||||

| FINANCING ACTIVITIES | ||||||||

| Proceeds from sale of common stock issuance | ||||||||

| Proceeds from convertible debt | ||||||||

| Net Cash Provided by Financing Activities | ||||||||

| Net Increase (Decrease) in Cash and Equivalents | ( | ) | ||||||

| Cash and Equivalents at Beginning of the Period | ||||||||

| Cash and Equivalents at End of the Period | $ | $ | ||||||

| SUPPLEMENTAL CASH FLOW INFORMATION | ||||||||

| Interest Paid | $ | $ | ||||||

| Income Taxes Paid | $ | $ | ||||||

| NON-CASH DISCLOSURES | ||||||||

| Beneficial conversion feature | $ | $ | ||||||

See accompanying notes to financial statements

| F-4 |

CyberloQ Technologies, Inc.

NOTES TO CONSOLIDATED CONDENSED FINANCIAL STATEMENTS (unaudited)

NOTE 1 – SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Organization and Nature of Business

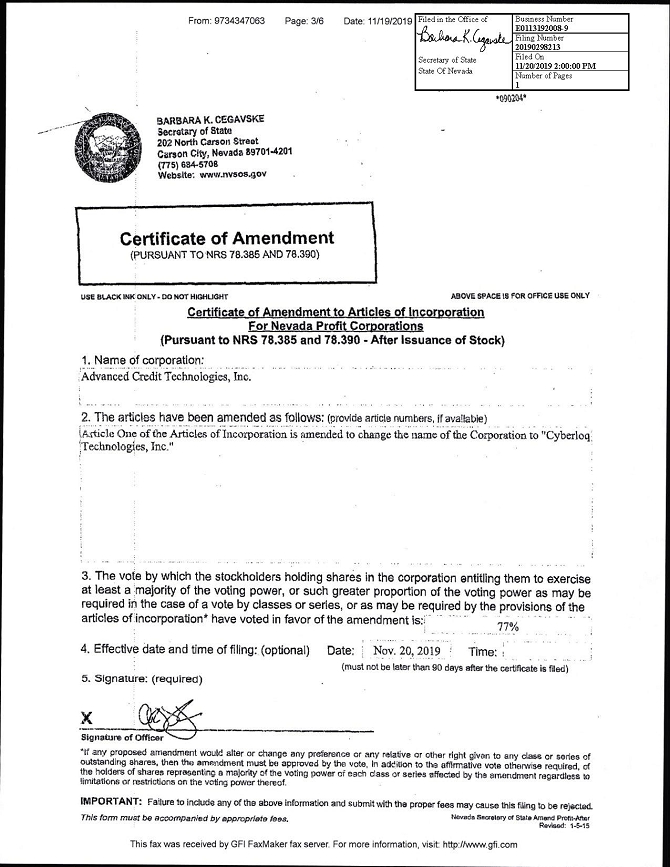

CyberloQ Technologies Inc. (“CLOQ”, ‘We” or the “Company”) is a development-stage technology company focused on fraud prevention and credit management. The Company was originally incorporated as Advanced Credit Technologies, Inc. in the State of Nevada on February 25, 2008. On November 20, 2019, the Company changed its name from Advanced Credit Technologies, Inc. to CyberloQ Technologies, Inc.

The Company offers a proprietary software platform branded as CyberloQ®. While previously the Company licensed CyberloQ, in the third quarter of 2017, the Company acquired the CyberloQ technology and is now the exclusive owner of CyberloQ.

CyberloQ is a banking fraud prevention technology that is offered to institutional clients in order to combat fraudulent transactions and unauthorized access to customer accounts. Through the use of a customer’s smart-phone, CyberloQ uses a multi-factor authentication system to control access to a bank card, transaction type or amount, website, database or digital service. The mobile applications for CyberloQ have been built, and have been successfully integrated into the banking ecosystem.

The CyberloQ Vault is a “cloud based’ security protocol that allows clients the ability to send/receive secure data without having to use traditional e-mail which is prone to a breach. This CyberloQ service uses cloud-based encryption and a secure web portal to send/receive confidential data, the sender and receiver both must have authenticated their position within the prescribed geo coordinates as well as authenticate their mobile devices prior to sending/receiving any data. Thus, rendering a hack or breach utterly useless for the encrypted data is unusable without the CyberloQ authentication component.

In addition to CyberloQ, the Company offers a web-based proprietary software platform under the brand name Turnscor® which allows customers to monitor and manage their credit from the privacy of their own homes. Although individuals can sign-up for Turnscor on their own, the Company also intends to market Turnscor to certain institutional clients, where appropriate, in conjunction with CyberloQ as a value-added benefit to offer their customers.

Basis of Presentation

The financial statements of the Company have been prepared using the accrual basis of accounting in accordance with generally accepted accounting principles in the United States of America and the rules of the Securities and Exchange Commission. All amounts are presented in U.S. dollars. The Company has adopted a December 31 fiscal year end.

Certain information and note disclosures normally included in our annual financial statements prepared in accordance with generally accepted accounting principles have been condensed or omitted. These consolidated financial statements should be read in conjunction with a reading of the financial statements and notes thereto included in our Annual Report on Form 10-K for the fiscal year ended December 31, 2023, as filed with the U.S. Securities and Exchange Commission.

Principles of Consolidation – The consolidated financial statements include the accounts of the Company and its wholly-owned or controlled operating subsidiaries. All intercompany accounts and transactions have been eliminated.

Use of Estimates

In preparing these financial statements, management makes estimates and assumptions that affect the reported amounts of assets and liabilities in the balance sheets and revenues and expenses during the year reported. Actual results may differ from these estimates. The Company bases its estimates and assumptions on current facts, historical experience and various other factors that it believes to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities and the accrual of costs and expenses that are not readily apparent from other sources. The actual results experienced by the Company may differ materially and adversely from the Company’s estimates. To the extent there are material differences between the estimates and the actual results, future results of operations will be affected.

| F-5 |

Cash and Cash Equivalents

Cash

equivalents are comprised of certain highly liquid investments with maturities of three months or less when purchased. The Company maintains

its cash in bank deposit accounts, which at times, may exceed federally insured limits. As of March 31, 2024, and December 31, 2023,

the Company had

Research and Development, Software Development Costs, and Internal Use Software Development Costs

Software development costs are accounted for in accordance with ASC Topic No. 985. Software development costs are capitalized once technological feasibility of a product is established and such costs are determined to be recoverable. For products where proven technology exists, this may occur very early in the development cycle. Factors we consider in determining when technological feasibility has been established include (i) whether a proven technology exists; (ii) the quality and experience levels of the individuals developing the software; (iii) whether the software is similar to previously developed software which has used the same or similar technology; and (iv) whether the software is being developed with a proven underlying engine. Technological feasibility is evaluated on a product-by-product basis. Capitalized costs for those products that are canceled or abandoned are charged immediately to cost of sales. The recoverability of capitalized software development costs is evaluated on the expected performance of the specific products for which the costs relate.

During

the three months ended March 31, 2024 and 2023, we capitalized $

Internal use software development costs are accounted for in accordance with ASC Topic No. 350 which requires the capitalization of certain external and internal computer software costs incurred during the application development stage. The application development stage is characterized by software design and configuration activities, coding, testing and installation. Training costs and maintenance are expensed as incurred, while upgrades and enhancements are capitalized if it is probable that such expenditures will result in additional functionality.

In

accounting for website software development costs, we have adopted the provisions of ASC Topic No. 350. ASC Topic No. 350 provides that

certain planning and training costs incurred in the development of website software be expensed as incurred, while application development

stage costs are to be capitalized. During the period ended September 30, 2023 the Company began capitalizing website development costs,

for the three month period ended March 31, 2023, we capitalized $

Fixed Assets, Intangibles and Long-Lived Assets

The Company records its fixed assets at historical cost. The Company expenses maintenance and repairs as incurred. Upon disposition of fixed assets, the gross cost and accumulated depreciation are written off and the difference between the proceeds and the net book value is recorded as a gain or loss on sale of assets. The Company depreciates its fixed assets over their respective estimated useful lives ranging from three to fifteen years.

The

Company follows FASB ASC 360-10, “Property, Plant, and Equipment,” which established a “primary asset”

approach to determine the cash flow estimation period for a group of assets and liabilities that represents the unit of accounting for

a long-lived asset to be held and used. Long-lived assets to be held and used are reviewed for impairment whenever events or changes

in circumstances indicate that the carrying amount of an asset may not be recoverable. The carrying amount of a long-lived asset is not

recoverable if it exceeds the sum of the undiscounted cash flows expected to result from the use and eventual disposition of the asset.

Long-lived assets to be disposed of are reported at the lower of carrying amount or fair value less cost to sell. As of December 31,

2020, the Company wrote-off the book value of the Cyberloq technology software fixed asset and recorded software impairment expense of

$

| F-6 |

Revenue Recognition

Effective January 1, 2018, the Company adopted the requirements of ASU No. 2014-09, Revenue from Contracts with Customers: Topic 606 (ASU 2014-09 or ASC 606). The adoption of ASC 606 resulted in changes to the Company’s accounting policies for revenue recognition previously recognized under ASC 605 (Legacy GAAP), as detailed below. However, since the Company had not earned any revenue prior to adopting ASC 606, this policy change had no effect on any financial statements from prior periods, thus no adjustments have been made to any prior periods related to the adoption of ASC 606.

Revenue Recognition Policy

Under ASC 606, the Company recognizes revenue upon transfer of control of promised products or services to customers in an amount that reflects the consideration the Company expects to receive in exchange for those products or services. To achieve the core principle of ASC 606, the Company performs the following steps:

| 1) | Identify the contract(s) with a customer; | |

| 2) | Identify the performance obligations in the contract; | |

| 3) | Determine the transaction price; | |

| 4) | Allocate the transaction price to the performance obligations in the contract; and | |

| 5) | Recognize revenue when (or as) we satisfy a performance obligation. |

The Company derives its revenue from development, customization and user fees for the CyberloQ banking fraud technology products, including CyberloQ Vault, and from licensing fees for the TurnScor product.

The revenue derived from the CyberloQ banking fraud technology products are comprised of two components. First, there is a development and customization fee paid to the Company to integrate CyberloQ with the banking institution or program manager’s ecosystem in order to add the CyberloQ authentication to the bank’s payment cards, website or digital service. This fee is customarily paid in multiple payments based upon the Company reaching certain milestones as set forth in the scope of work for each customer. Since completion of a milestone is subject to each customer’s approval, there are significant judgments involved in the determination of timing and satisfaction of performance obligations and the payments are recognized as revenue upon the completion of each milestone. Second, where the Company’s agreement is with a processor as opposed to an end user customer, there is an API license fee that is accrued monthly. Third, revenue from user fees are accrued monthly based over the number of individual card users each month.

The revenue derived from CyberloQ Vault is also comprised of two components. First, there is a development and customization fee paid to the Company to build a customized cloud-based encryption and a secure web portal to send/receive confidential data. This fee is customarily paid in multiple payments based upon the Company reaching certain milestones as set forth in the scope of work for each customer. Since completion of a milestone is subject to each customer’s approval, there are significant judgments involved in the determination of timing and satisfaction of performance obligations and the payments are recognized as revenue over the completion of each milestone. Second, revenue from a monthly user fee is accrued monthly based upon the number of individual users of the product each month.

License fees generated by the nonexclusive licensing of the Company’s TurnScor product are accrued monthly.

As

of March 31, 2024, and December 31, 2023, the Company had $

Accounts Receivable

The Company extends credit to customers in the normal course of business. The allowance for doubtful accounts represents the Company’s best estimate of the amount of profitable credit losses in the Company’s existing accounts receivable. The Company determines the allowance based on specific customer information, historical write-off experience and current industry and economic data. Account balances are charged off against the allowance when the Company believes that it is probable that the receivable will not be recovered. Management believes that there are no concentrations of credit risk for which an allowance has not been established. Although management believes that the allowance is adequate, it is possible that the estimated amount of cash collections with respect to accounts receivable could change.

| F-7 |

Fair Value Measurements

For certain financial instruments, including accounts receivable, accounts payable, accrued expenses, interest payable, advances payable and notes payable, the carrying amounts approximate fair value due to their relatively short maturities.

The Company has adopted FASB ASC 820-10, “Fair Value Measurements and Disclosures.” FASB ASC 820-10 defines fair value, and establishes a three-level valuation hierarchy for disclosures of fair value measurement that enhances disclosure requirements for fair value measures. The carrying amounts reported in the consolidated balance sheets for receivables and current liabilities each qualify as financial instruments and are a reasonable estimate of their fair values because of the short period of time between the origination of such instruments and their expected realization and their current market rate of interest. The three levels of valuation hierarchy are defined as follows:

| ● | Level 1 inputs to the valuation methodology are quoted prices for identical assets or liabilities in active markets. |

| ● | Level 2 inputs to the valuation methodology include quoted prices for similar assets and liabilities in active markets, and inputs that are observable for the asset or liability, either directly or indirectly, for substantially the full term of the financial instrument. |

| ● | Level 3 inputs to the valuation methodology are unobservable and significant to the fair value measurement. |

The Company did not identify any other non-recurring assets and liabilities that are required to be presented in the balance sheets at fair value in accordance with FASB ASC 815.

Segment Reporting

FASB

ASC 280, “Segment Reporting” requires use of the “management approach” model for segment reporting. The

management approach model is based on the way a company’s management organizes segments within the company for making operating

decisions and assessing performance. The Company determined it has

Advertising

Advertising

costs are expensed as incurred. Advertising expense for the three-months ended March 31, 2024 and 2023 were $

Income Taxes

Deferred income taxes are provided using the liability method (in accordance with ASC 740) whereby deferred tax assets are recognized for deductible temporary differences and operating loss and tax credit carry forwards, and deferred tax liabilities are recognized for taxable temporary differences. Temporary differences are the differences between the reported amounts of assets and liabilities and their tax bases. Deferred tax assets are reduced by a valuation allowance when, in the opinion of management, it is more likely than not that some portion or all-of the deferred tax assets will not be realized. Deferred tax assets and liabilities are adjusted for the effects of the changes in tax laws and rates of the date of enactment.

When tax returns are filed, it is highly certain that some positions taken would be sustained upon examination by the taxing authorities, while others are subject to uncertainty about the merits of the position taken or the amount of the position that would be ultimately sustained. The benefit of a tax position is recognized in the financial statements in the period during which, based on all available evidence, management believes it is more likely than not that the position will be sustained upon examination, including the resolution of appeals or litigation processes, if any. Tax positions taken are not offset or aggregated with other positions. Tax positions that meet the more-likely-than-not recognition threshold are measured as the largest amount of tax benefit that is more than 50 percent likely of being realized upon settlement with the applicable taxing authority. The portion of the benefits associated with tax positions taken that exceeds the amount measured as described above is reflected as a liability for unrecognized tax benefits in the accompanying balance sheets along with any associated interest and penalties that would be payable to the taxing authorities upon examination. Applicable interest and penalties associated with unrecognized tax benefits are classified as additional income taxes in the statements of operations. The Company is not aware of uncertain tax positions.

| F-8 |

Earnings per share is calculated in accordance with the FASB ASC 260-10, “Earnings Per Share.” Basic earnings (loss) per share is based upon the weighted average number of common shares outstanding. Diluted earnings (loss) per share is based on the assumption that all dilutive convertible shares and stock options were converted or exercised. Dilution is computed by applying the treasury stock method. Under this method, options and warrants are assumed to be exercised at the beginning of the period (or at the time of issuance, if later), and as if funds obtained thereby were used to purchase common stock at the average market price during the period.

At March 31, 2024 and December 31, 2023, the Company has warrants or options outstanding, and had and convertible debt shares irrespectively that could have been exercised and could have been dilutive to the existing number of shares issued and outstanding. The convertible debt shares were not included in the weighted average shares outstanding as they were anti-dilutive.

The computation of earnings per share of common stock is based on the weighted average number of shares outstanding at the date of the financial statements.

The Company adopted FASB ASC Topic 718 – Compensation – Stock Compensation (formerly SFAS 123R), which establishes the use of the fair value-based method of accounting for stock-based compensation arrangements under which compensation cost is determined using the fair value of stock-based compensation determined as of the date of grant and is recognized over the periods in which the related services are rendered. For stock-based compensation, the Company recognizes an expense in accordance with FASB ASC Topic 718 and values the equity securities based on the fair value of the security on the date of grant. Stock option and warrant awards are valued using the Black-Scholes option-pricing model, which according to ASC 820-10 is a level 3 value on the hierarchy.

Leases

FASB issued ASU No. 2016-02, Leases (Topic 842), which establishes a comprehensive new lease accounting model. The new standard: (a) clarifies the definition of a lease; (b) requires a dual approach to lease classification similar to current lease classifications; and, (c) causes lessees to recognize leases on the balance sheet as a lease liability with a corresponding right-of-use asset for leases. The standard became effective for calendar years beginning after December 15, 2018.

The Company has made an accounting policy election not to recognize right of use assets and lease liabilities that arise from short term leases for any class of asset.

NOTE 2 – FIXED ASSETS

Software and computer equipment, recorded at cost, consisted of the following:

| March 31, 2024 | December 31, 2023 | |||||||

| Cyberloq platform | $ | $ | ||||||

| Website | ||||||||

| Software and computer equipment | ||||||||

| Less: accumulated amortization | ||||||||

| Fixed assets, net | $ | $ | ||||||

Amortization

expense was $

| F-9 |

NOTE 3 – GOING CONCERN

The

Company has incurred losses since Inception resulting in an accumulated deficit of $

The accompanying financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America, which contemplate continuation of the Company as a going concern. The financial statements do not include any adjustments relating to the recoverability and classification of recorded asset amounts or the amounts and classification of liabilities that could result from the outcome of this uncertainty.

The ability to continue as a going concern is dependent upon the Company generating profitable operations in the future and, or, obtaining the necessary financing to meet its obligations and repay its liabilities arising from normal business operations when they come due.

Management anticipates that the Company will be dependent, for the near future, on additional investment capital to fund operating expenses. The Company intends to position itself so that it may be able to raise additional funds through the capital markets. In light of management’s efforts, there are no assurances that the Company will be successful in this or any of its endeavors or become financially viable and continue as a going concern.

NOTE 4 – SERVICES AGREEMENT

On

September 25, 2023, the Company entered into a Services Agreement with QRails, Inc to integrate the features of CyberloQ® and its

multi-factor security protocol into QRails’ processing platform. As a result of the integration, anyone who has their card processing

services through QRails will have the option to utilize the features of CyberloQ in conjunction with their card programs. The agreement

also includes the integration of CyberloQ into the card network of XTM, Inc. Under the terms of the Agreement, the Company will pay $

NOTE 5 – SETTLEMENT AGREEMENT

On February 28, 2022, the Company signed a Separation and Release of Claims Agreement with an employee, officer and director of the Company. The terms of the agreement are as follows:

| ● | The employee resigned from the Company’s Board of Directors | |

| ● | The employee resigned his position as an officer of the Company, and his employment agreement was terminated | |

| ● | The employee assigned and transferred shares of preferred stock to be canceled and extinguished by the Company. A loss of $ was recorded | |

| ● | The

Company will pay the $ | |

| ● | The

Company and the employee entered into a Common Stock Redemption Agreement by which the Company will purchase shares of

the Company’s common stock owned by the employee at $ per share for a total of $ |

| ○ | Payments under the Common Stock Redemption Agreement are as follows: |

| Date | Amount | Shares Redeemed | ||||||

| 02/28/22 | $ | |||||||

| 09/01/22 | ||||||||

| 03/01/23 | ||||||||

| 09/01/23 | ||||||||

| 9/13/22 Termination of Agreement | $ | ( | ) | ( | ) | |||

| Balance as of 9/30/22 | ||||||||

| F-10 |

On

September 1, 2022, the Company failed to make the stock redemption payment of $

NOTE 6 – STOCKHOLDERS’ EQUITY

Common Stock

The Company has shares of $ par value common stock authorized as of March 31, 2024 and December 31, 2023.

During

the quarter ended March 31, 2024, the Company received $

During

the quarter ended March 31, 2023, the Company received $

Treasury Stock

The

Company entered into a settlement agreement with a prior employee, officer and director resulting in treasury stock of shares

valued at $

Preferred Stock

The

Company did not have any preferred stock prior to 2017. In April of 2017, the Company amended its articles of incorporation to create

a new class of stock designated Series A Super Voting Preferred Stock consisting of thirty-thousand () shares at par value of $

per share. Certain rights, preferences, privileges and restrictions were established for the Series A Preferred Stock as follows: (a)

the amount to be represented in stated capital at all times for each share of Series A Preferred Stock shall be its par value of $

per share; (b) except as otherwise required by law,

On February 28, 2022, the Series A Preferred Stock held by Mark Carten were redeemed by the Company and returned to treasury.

Incentive Stock Options

The

employment contracts for Christopher Jackson and Enrico Giordano include performance incentive stock options based upon the Company meeting

certain performance conditions that can potentially result in the issuance of stock option awards of up to shares each in the

event that the Company reaches certain performance goals. Specifically,

| F-11 |

NOTE 7 – SBA EIDL Loan

On

June 9, 2020, the Company received an Economic Injury Disaster Loan from the Small Business Administration in the amount of $

| Payment Obligations | ||||

| Amount | ||||

| 2024 | ||||

| 2025 | ||||

| 2026 | ||||

| 2027 | ||||

| 2028 to 2050 | ||||

| Total | $ | |||

NOTE 8 – COMMITMENTS

In

April 2023, the Company signed a new lease for office space at its existing location at 4837 Swift Rd Sarasota, FL 34231 at a rate of

$

The Company has commission agreements as follows:

| ● | An agreement with a shareholder and director of the Company stating that the executive will be entitled to a two-and-a half-percent (%) commission of the gross revenue recorded by the Company for any customer contracts that are closed by the Company at the time of and during the duration of the agreement. These commissions are payable quarterly upon receipt of customer revenues. | |

| ● | An

agreement with two sales managers granting each manager a |

NOTE 9 – RELATED PARTY TRANSACTIONS

Related Parties and Stockholders Notes Payable

The following is a summary of related party notes payable:

| For the Periods Ended | ||||||||

| March 31, 2024 | December 31, 2023 | |||||||

| Notes payable – stockholders | $ | $ | ||||||

| Convertible debt - stockholders | ||||||||

| Notes payable – related parties | $ | $ | ||||||

Notes Payable - Stockholders

On

December 29, 2014, the Company entered into a partially-convertible promissory note with a stockholder in the amount of $

| F-12 |

Convertible Debt - Stockholders

March 31, 2024 | December 31, 2023 | |||||||

| Principal | $ | $ | ||||||

| Beneficial Conversion Feature | ( | ) | ( | ) | ||||

| Amortization of Debt Discount | ||||||||

| Convertible Debt - Stockholders, net | $ | $ | ||||||

On

December 8, 2022, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

December 14, 2022, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

January 13, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

| F-13 |

On

February 2, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

February 3, 2023, the Company entered into a convertible promissory note with a different stockholder in the amount of $

On

February 10, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

February 21, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

April 4, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

May 17, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

| F-14 |

On

May 17, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

June 2, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

June 5, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

August 2, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

August 3, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

August 18, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

| F-15 |

On

August 24, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

October 11, 2023, the Company entered into five convertible promissory notes with stockholders in the amount of $

On

October 23, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

November 16, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

December 18, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

| F-16 |

On

December 19, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

December 20, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

December 21, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

December 22, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

On

December 26, 2023, the Company entered into a convertible promissory note with a stockholder in the amount of $

| F-17 |

On

January 9, 2024, the Company entered into a convertible promissory note with a stockholder in the amount of $

Notes Payable - Related Parties

On

December 31, 2021, the Company entered into a loan modification agreement with a director which consolidated three outstanding promissory

notes dated August 8, 2020, September 9, 2020, and December 28, 2020 into one loan. The total amount borrowed is $

On

February 23, 2022, the Company received a loan from a director in the amount of $

On

February 23, 2022, the Company received a convertible debt note from a different director in the amount of $

NOTE 10 – SUBSEQUENT EVENTS

On April 1, 2024, the Company entered into a promissory

note with a stockholder in the amount of $

On April 1, 2024, the Company entered into a promissory

note with a stockholder in the amount of $

The Company is not aware of any other subsequent events through the date of this filing that require disclosure or recognition in these financial statements.

| F-18 |

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

The following discussion is intended to assist you in understanding our business and the results of our operations. It should be read in conjunction with the Condensed Financial Statements and the related notes that appear elsewhere in this report as well as our Report on Form 10K filed with the Securities and Exchange Commission for the period ending December 31, 2023. Statements made in this Form 10-Q that are not historical or current facts are “forward-looking statements”. These statements often can be identified by the use of terms such as “may,” “will,” “expect,” “believe,” “anticipate,” “estimate,” “approximate” or “continue,” or the negative thereof. We wish to caution readers not to place undue reliance on any such forward-looking statements, which speak only as of the date made. Any forward-looking statements represent management’s best judgment as to what may occur in the future. However, forward-looking statements are subject to risks, uncertainties and important factors beyond our control that could cause actual results and events to differ materially from historical results of operations and events and those presently anticipated or projected. We disclaim any obligation subsequently to revise any forward-looking statements to reflect events or circumstances after the date of such statement or to reflect the occurrence of anticipated or unanticipated events.

Company History

CyberloQ Technologies Inc. (“CLOQ”, ‘We” or the “Company”) was incorporated in Nevada on February 5, 2008 as Advanced Credit Technologies, Inc. The Company changed its name to CyberloQ Technologies, Inc. on November 20, 2019. The Company has never been the subject of any bankruptcy, receivership or similar proceeding. The Company has never been involved in any material reclassification, merger, or consolidation.

On June 15, 2017, the Company created a private limited company in the United Kingdom named CyberloQ Technologies LTD. CyberloQ Technologies LTD is a wholly-owned subsidiary of the Company, and any business that the Company has in the United Kingdom will be transacted through CyberloQ Technologies LTD. However, to date CyberloQ Technologies LTD has had no activity, operational or otherwise and is now dissolved.

Current Overview of the Company

The Company is a development-stage technology company focused on fraud prevention and credit management.

The Company offers a proprietary software platform branded as CyberloQ®. While previously the Company licensed CyberloQ, in the third quarter of 2017, the Company acquired the CyberloQ technology and is now the exclusive owner of CyberloQ.

CyberloQ is a MFA (Multi Factor Authentication) protocol technology that is offered to institutional clients in order to combat fraudulent transactions and unauthorized access to customer accounts or any digital asset. Through the use of a customer’s smart-phone, CyberloQ uses a multi-factor authentication system to control access to a bank card, transaction type or amount, website, database or digital service. The mobile applications for CyberloQ have been built, and have been successfully integrated into the banking ecosystem. The Company has also updated the entire infrastructure, UI/UX and streamlined the deliverable services per strategic partnerships with clients in multiple channels in order to increase the scalability of the original platform.

In addition to CyberloQ, the Company offers a web-based proprietary software platform under the brand name TurnScor® which allows customers to monitor and manage their credit from the privacy of their own homes. Although individuals can sign-up for TurnScor on their own, the Company also intends to market TurnScor to certain institutional clients, where appropriate, in conjunction with CyberloQ as a value-added benefit to offer their customers.

| 4 |

The CyberloQ Vault is a “cloud based’ security protocol that allows clients the ability to send/receive secure data without having to use traditional e-mail which is prone to a breach. This CyberloQ service uses cloud-based encryption and a secure web portal to send/receive confidential data, the sender and receiver both must have authenticated their position within the prescribed geo coordinates as well as authenticate their mobile devices prior to sending/receiving any data. Thus, rendering a hack or breach utterly useless for the encrypted data is unusable without the CyberloQ authentication component.

The Company currently has two full-time employees — its President and Vice-President. There are no other employees of the Company at this time.

The Company also has a Board of Advisors comprised of individuals from the banking, business development, and technical sectors to advise the Company as it moves forward with its business strategy. The Board of Advisors does not have any decision-making authority.

Liquidity, Capital Resources and Material Changes in Financial Condition

As of March 31, 2024, the Company’s assets were $1,410,170 compared to $1,458,565 in assets as of December 31, 2023.

This change in the Company’s financial condition can be primarily attributed to the Company’s cash assets being $127,148 as of March 31, 2024 as opposed to $307,174 as of December 31, 2023. This decrease in cash assets was partially offset by an increase in fixed assets of $92,464 due to the capitalization of the Cyberloq Platform and website development, an increase in the Company’s prepaid expense from $44,564 to $68,731, and an increase in the company’s accounts receivable from $10,000 to $25,000.

As of March 31, 2024, the Company’s liabilities were $1,321,203 compared to $1,021,359 in liabilities as of December 31, 2023. This change in the Company’s financial condition can be primarily attributed to an increase in convertible debt of $290,431, net of beneficial conversion costs, related to the Company raising operating capital through the issuance of convertible notes. In addition, there was a decrease of $40,838 in accounts payable and accrued expenses, along with an increase of $50,251 in accrued interest.

Net cash used in operating activities for the three-month period ending March 31, 2024 was $197,562 compared to $90,700 for 2023. Cash provided by or used by operating activities is driven by our net loss and adjusted by non-cash items as well as changes in operating assets and liabilities. At March 31, 2024, there was $290,431 in amortization of debt discount and $79,000 in stock compensation.

Net cash used by investing activities was $92,464 for the three months ended March 31, 2024 as compared to $168,700 for 2023.

Net cash provided by financing activities was $110,000 for the three months ended March 31, 2024 as compared to $274,000 for 2023.

The Company had gross revenue of $15,000 for the three months ended March 31, 2024 compared to gross revenue of $993 for the three months ended March 31, 2023, and is currently reliant on its ability to raise additional capital to continue execution of its business plan to move the Company forward towards profitability. The Company does not anticipate any significant decrease in its operating expenses for the remainder of 2024. Unless the Company begins to generate operational revenue, it will be reliant on its ability to raise additional capital in order to continue its operations.

Results of Operations for the Three Months Ended March 31, 2024 and 2023

Company revenue was $15,000 in the three months ended March 31, 2024 as compared to $993 for the three months ended March 31, 2023. This increase in revenue was related to the agreement with QRails, Inc. to integrate the features of CyberloQ® and its multi-factor security protocol into QRails’ processing platform that was entered into in September of 2023.

| 5 |

The Company’s operating expenses were $211,035 for the three months ended March 31, 2024 as compared to $97,707 for the three months ended March 31, 2023. This increase in operating expenses was primarily due to an increase in officer compensation which was $62,500 for the three months ended March 31, 2024, compared to $45,000 for the three months ended March 31, 2023 due to the Board of Directors approving a salary increase for the Company’s President, and an increase in professional fees which was $114,774 for the three Months ended March 31, 2024 compared to $33,819 for the three months ended March 31, 2023. this increase of $80,955 was due to the issuance of common stock for services.

In addition, the Company experienced changes in expense categories as noted below.

Other operating expenses were $21,382 for the three months ended March 31, 2024 as compared to $11,341 for the three months ended March 31, 2023. This increase in other operating expenses was due to an increase in OTC Market fees.

Computer and internet expenses were $5,711 for the three months ended March 31, 2024 as compared to $3,548 for the three months ended March 31, 2023.

Finally, there were no material changes in the Company’s office supplies and expenses, rent and travel expenses in the three months ended March 31, 2024 as compared to the three months ended March 31, 2023.

As a result of the foregoing, the Company experienced a net loss from operations of $196,035 in the three months ended March 31, 2024 compared to a net loss from operations of $96,714 in the three months ended March 31, 2023

Item 3. Quantitative and Qualitative Disclosures About Market Risk

The Company qualifies as a smaller reporting company as defined by §229.10(f)(1) and therefore is not required to provide the information required by this Item.

ITEM 4. CONTROLS AND PROCEDURES

Our management is responsible for establishing and maintaining a system of disclosure controls and procedures (as defined in Rule 13a-15(e) and 15d-15(e) under the Exchange Act) that is designed to ensure that information required to be disclosed by us in the reports that we file or submit under the Exchange Act is recorded, processed, summarized and reported, within the time periods specified in the Commission’s rules and forms. Disclosure controls and procedures include, without limitation, controls and procedures designed to ensure that information required to be disclosed by an issuer in the reports that it files or submits under the Exchange Act is accumulated and communicated to the issuer’s management, including its principal executive officer or officers and principal financial officer or officers, or persons performing similar functions, as appropriate to allow timely decisions regarding required disclosure.

An evaluation was conducted under the supervision and with the participation of our management of the effectiveness of the design and operation of our disclosure controls and procedures as of March 31, 2024 in accordance with Committee of Sponsoring Organizations of the Treadway Commission’s 2013 Integrated Framework. Based on that evaluation, our management concluded that our disclosure controls and procedures were not effective as of such date to ensure that information required to be disclosed in the reports that we file or submit under the Exchange Act, is recorded, processed, summarized and reported within the time periods specified in SEC rules and forms. In addition, due to its current size, the Company currently does not have sufficient staff to maintain appropriate segregation of duties, as it pertains to application and oversight of internal control processes. Material weaknesses have previously been identified, including lack of segregation of duties and lack of formal written policies and procedures surrounding financial close and reporting. However, the Company anticipates that as it grows and formalizes its internal control processes and procedures, it will add sufficient staff to perform internal control processes, as well as adequately provided oversight to ensure processes are working as designed. Such officer also confirmed that there was no change in our internal control over financial reporting during the three-month period ended March 31,2024 that has materially affected, or is reasonably likely to materially affect, our internal control over financial reporting.

| 6 |

PART II

OTHER INFORMATION

Item 1. Legal Proceedings

The Company is not currently a party to any other legal proceedings, nor is the Company a party to any administrative proceedings.

In addition, the Company’s officers and directors have not been convicted in any criminal proceedings nor have they been permanently or temporarily enjoined, barred, suspended or otherwise limited from involvement in any type of securities or banking activities.

Item 1A. Risk Factors

The Company qualifies as a smaller reporting company as defined by §229.10(f)(1) and therefore is not required to provide the information required by this Item. However, the Company does acknowledge that there are risks associated with the business of the Company.

We will be competing with a variety of companies, many of which have significantly greater financial, technical, marketing and other resources than us. If we fail to attract and retain a large base of customers for our products, or if our competitors establish a more prominent market position relative to ours, this will inhibit our ability to grow and successfully execute our business plan. For example, Wells Fargo has introduced an “on/off” feature for their customers, Discover Card has “Freeze It” functionality, and Ondot Systems has already been operating in the mobile card security space for quite some time. However, the Company believes that the multi-purpose functionality of CyberloQ, along with its multi-purpose applications will give the Company a distinct advantage by comparison. CyberloQ can be used in the banking system to protect debit/credit cards, in the health care industry to protect PII (Personal Identifying Information) now that medical records are kept digitally, and can protect corporate data bases in any industry from outside intrusion via geo-fencing. The Company believes that these distinct features, along with the ability to “White Label” the technology for marketing partners, give the Company a distinction in the marketplace. However, there can be no assurance that we will be able to successfully compete with other companies in the marketplace.

In addition, the Company could incur increased costs, decreased revenue, or suffer reputational damage in the event of a cyber-attack. The Company’s business involves the collection, storage, processing and transmission of customers’ personal data, including financial information. In the event that the Company’s security measures are breached due to human error, malfeasance, system errors or vulnerabilities, or other irregularities, such breach could adversely affect our business through possible interruption of the Company’s operations, improper disclosure of data, damage to the Company’s reputation, and/or legal exposure.

Finally, management has evaluated whether or not COVID-19 has had any material impact on the Company. The Company is a technology-based company with personnel already working remotely prior to COVID-19. Therefore, the Company has not been impacted by any stay-at-home orders or travel restrictions. Likewise, the Company has continued to have access to capital and funding sources, and COVID-19 has had no material effect on the demand for the Company’s services. Consequently, to date COVID-19 has not impacted the Company’s financial condition or the results of its operations, and the Company does not anticipate that there be any material impact in the future.

| 7 |

Item 2. UNREGISTERED SALES OF EQUITY SECURITIES AND USE OF PROCEEDS

During the first three months of 2024, the Company raised $100,000 for the operations of the Company through the unregistered sale of 2,000,000 shares of restricted common stock.

All of the shares described above were issued by the Company in reliance upon an exemption from the registration requirements of the Securities Act of 1933, as amended, provided by Section 4(2). All of the purchasers of the unregistered securities were all known to us and our management, through pre-existing business relationships, as long standing business associates, friends, and employees. All purchasers were provided access to all public material information, which they requested, and all information necessary to verify such information and were afforded access to our management in connection with their purchases. All purchasers of the unregistered securities acquired such securities for investment and not with a view toward distribution, acknowledging such intent to us. All certificates or agreements representing such securities that were issued contained restrictive legends, prohibiting further transfer of the certificates or agreements representing such securities, without such securities either being first registered or otherwise exempt from registration in any further resale or disposition.

ITEM 3. DEFAULTS UPON SENIOR SECURITIES

The Company is not in default on any financing arrangements at this time.

ITEM 4. OTHER INFORMATION

There exists no information required to be disclosed by us in a report on Form 8-K during the three-months ended March 31, 2024, but not reported.

ITEM 5. EXHIBITS

Exhibits have been filed separately with the United States Securities and Exchange Commission in connection with the quarterly report on Form 10-Q or have been incorporated into the report by reference.

| Exhibit | Description | |

| 3.1(i) | Articles of Incorporation* | |

| 3.2(i) | Amended Articles of Incorporation dated May 4, 2010* | |

| 3.3(i) | Amended Articles of Incorporation dated May 5, 2017** | |

| 3.4(i) | Amended Articles of Incorporation dated November 20, 2019 | |

| 3.4(ii) | By-Laws**** | |

| 14.1 | Code of Ethics**** | |

| 14.2 | Related-Party Transactions Policy**** | |

| 14.3 | Anti-Corruption Policy**** | |

| 16.1 | Letter re Change in Certifying Accountant ***** | |

| 31.1 | Rule 13a-14(a) / 15d-14(a) Certification of Principal Executive Officer & Principal Financial Officer.****** | |

| 32.1 | Section 1350 Certification of the Principal Executive Officer & Principal Financial Officer.****** | |

| 101.1 | Interactive data files pursuant to Rule 405 of Regulation S-T.******* | |

| 101.INS | Inline XBRL Instance Document | |

| 101.SCH | Inline XBRL Taxonomy Extension Schema Document | |

| 101.CAL | Inline XBRL Taxonomy Extension Calculation Linkbase Document | |

| 101.DEF | Inline XBRL Taxonomy Extension Definition Linkbase Document | |

| 101.LAB | Inline XBRL Taxonomy Extension Label Linkbase Document | |

| 101.PRE | Inline XBRL Taxonomy Extension Presentation Linkbase Document | |

| 104 | Cover Page Interactive Data File (embedded within the Inline XBRL document) | |

| * | Incorporated by reference through the Registration Statement on form S-1 filed with the Commission on October 26, 2010. (101141203) | |

| ** | Incorporated by reference through the Quarterly Report on form 10-Q filed with the Commission on May 11, 2017. (17832815) | |

| **** | Incorporated by reference through the Current Report on form 8-K filed with the Commission on November 6, 2017. | |

| ***** | Incorporated by reference through the Current Report on form 8-K filed with the Commission on May 19, 2017. | |

| ****** | Filed herewith. In addition, in accordance with SEC Release 33-8238, Exhibits 32.1 and 32.2 are being furnished and not filed. | |

| ******* | Furnished herewith. XBRL (Extensible Business Reporting Language) information is furnished and not filed for purposes of Sections 11 or 12 of the Securities Act of 1933, as amended, is deemed not filed for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, and otherwise is not subject to liability under these sections. |

| 8 |

SIGNATURES

In accordance with Section 13 or 15(d) of the Exchange Act, the registrant caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| CYBERLOQ TECHNOLOGIES, INC. | ||

| By: | /s/ Christopher Jackson | |

| Christopher Jackson | ||

| President, Secretary, Treasurer and Director | ||

| Principal Executive Officer | ||

| Principal Financial Officer | ||

| Date: May 15, 2024 | ||

Pursuant to the requirements of the Securities Act of 1933, this report has been signed by the following persons in the capacities and on the dates indicated.

| CYBERLOQ TECHNOLOGIES, INC. | ||

| By: | /s/ Enrico Giordano | |

| Enrico Giordano, Director | ||

| Date: May 15, 2024 | ||

| By: | /s/ Leon Hurst | |

| Leon Hurst, Director | ||

| Date: May 15, 2024 | ||

| By: | /s/ Christopher Jackson | |

| Christopher Jackson, Director | ||

| Date: May 15, 2024 | ||

| By: | /s/ Rex Schuette | |

| Rex Schuette, Director | ||

| Date: May 15, 2024 | ||

| 9 |

Exhibit 3.4(i)

Exhibit 31.1

CERTIFICATION PURSUANT TO SECTION 302 OF THE SARBANES OXLEY ACT OF

2002 AND RULE 13A-14 OF THE EXCHANGE ACT OF 1934

I, Christopher Jackson, certify that:

| 1. | I have reviewed this 1st quarterly report on Form 10-Q of CyberloQ Technologies, Inc.; |

| 2. | Based on my knowledge, this report does not contain any untrue statement of a material fact or omit to state a material fact necessary to make the statement made, in light of the circumstances under which such statements were made, not misleading with respect to the period covered by this report; |

| 3. | Based on my knowledge, the financial statements, and other financial information included in this report, fairly present in all material respects the financial condition, results of operations and cash flows of the registrant as of, and for, the periods presented in this report; |

| 4. | As certifying officer, I am responsible for establishing and maintaining disclosure controls and procedures (as defined in Exchange Act Rules 13a-15(e) and 15d-15(e)) and internal controls over financial reporting (as defined in Exchange Act Rules 13a-15(f) and 15d015f)) for the registrant and have: |

| (a) | designed such disclosure controls and procedures, or caused such internal control over financial reporting to be designed under our supervision, to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to us by others within those entities, particularly during the period in which this report is being prepared; | |

| (b) | designed such internal control over financial reporting, or caused such internal control over financial reporting to be designed under our supervision, to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance with generally accepted accounting principles; | |

| (c) | evaluated the effectiveness of the registrant’s disclosure controls and procedures and presented in this report our conclusions about the effectiveness of the disclosure controls and procedures, as of the end of the period covered by this report based on such evaluation; and | |

| (d) | disclosed in this report any change in the registrant’s internal control over financial reporting that occurred during the registrant’s most recent fiscal quarter (the registrant’s fourth fiscal quarter in the case of an annual report) that has materially affected, or is reasonably likely to materially affect, the registrant’s internal control over financial reporting; and |

| 5. | As certifying officer, I have disclosed, based on our most recent evaluation of internal control over financial reporting, to the registrant’s auditors and the audit committee of the registrant’s board of directors (or persons performing the equivalent functions): |

| (a) | all significant deficiencies and material weaknesses in the design or operation of internal controls over financial reporting which are reasonably likely; and | |

| (b) | any fraud, whether or not material, that involves management or other employees who have a significant role in the Registrant’s internal control over financial reporting. |

| CYBERLOQ TECHNOLOGIES, INC. | ||

| By: | /s/ Christopher Jackson | |

| Christopher Jackson | ||

| President, Treasurer, Secretary, Principal Executive Officer and Principal Financial Officer | ||

| Date: Date: May 15, 2024 | ||

Exhibit 32.1

CERTIFICATION OF THE CHIEF EXECUTIVE OFFICER

PURSUANT TO 18 U.S. C. SECTION 1350

AS ADOPTED PURSUANT TO

SECTION 906 OF THE SARBANES-OXLEY ACT OF 2002

In connection with the Annual Report of CyberloQ Technologies, Inc., (the “Company”) on Form 10-Q for the period ended March 31, 2024 as filed with the Securities and Exchange Commission on the date hereof (the “Report”), I, Christopher Jackson, President, Treasurer, Secretary and Principal Executive Officer of the Company, certify, pursuant to 18 U.S.C. Section 1350, as adopted pursuant to Section 906 of the Sarbanes-Oxley Act of 2002, that, to my knowledge:

| 1. | The Report fully complies with the requirements of Section 13 (a) or 15 (d) of the Securities Exchange Act of 1934; and |

| 2. | The information contained in the Report fairly presents, in all material respects, the financial condition and results of operations of the Company. |

| CYBERLOQ TECHNOLOGIES, INC. | ||

| By: | /s/ Christopher Jackson | |

| Christopher Jackson | ||

| President, Treasurer, Secretary, Principal Executive Officer and Principal Financial Officer | ||

| Date: Date: May 15, 2024 | ||

QCC.:C;_@R\_P""9!4X

M_: _;MWE0NY_B3\"7&2_F2E@?V<@[>9(%8 R?+M ^85_7I10!_(*/^#+G_@F

M? WWK<.WDM]Z//RD#BMCP]_P3^_83\*:E#J_A

MG]BG]DKPYJ<%_#JD&I:#^SG\']*OX-2MK34K&VOX+NQ\'07,5Y;V6L:M907$

M