UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

For the fiscal year ended December 31 , 2023

or

For the transition period from ___ to ___

Commission File Number 001-34481

(Exact name of registrant as specified in its charter)

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification Number) | |||||||

(Address of principal executive offices) (Zip Code)

(609 ) 716-4000

(Registrant's telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ý No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.:

Large accelerated filer o | x | ||||||||||

Non-accelerated filer o | Smaller reporting company | ||||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. Yes ☐ No ý

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant's executive officers during the relevant recovery period pursuant to § 240.10D-1(b). Yes ☐ No ý

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ý

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant, based on the closing price of $7.72 on June 30, 2023, the last business day of the registrant's most recently completed second fiscal quarter, as reported on the New York Stock Exchange, was approximately $158.4 million.

As of March 6, 2024, the Registrant had 30,634,785 shares of common stock outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Information required by Part III (Items 10, 11, 12, 13 and 14) is incorporated by reference to portions of the registrant’s definitive proxy statement for its 2024 annual meeting of stockholders (the “Proxy Statement”), which is expected to be filed not later than 120 days after the registrant’s fiscal year ended December 31, 2023. Except as expressly incorporated by reference, the Proxy Statement shall not be deemed to be a part of this report on Form 10-K.

Auditor Name: PricewaterhouseCoopers LLP Auditor Location: Philadelphia, Pennsylvania Auditor Firm ID: 238

1

MISTRAS GROUP, INC.

ANNUAL REPORT ON FORM 10-K

TABLE OF CONTENTS

DISCLOSURES REGARDING FOREIGN JURISDICTIONS THAT PREVENT INSPECTIONS | |||||||||||

2

ITEM 1. BUSINESS

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (this "Annual Report") contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), regarding Mistras Group, Inc. ("Mistras," "MISTRAS," "the Company," "us," "we," "our" and similar expressions) and our business, financial condition, results of operations and prospects. Such forward-looking statements include those that express plans, anticipation, intent, contingency, goals, targets or future development and/or otherwise are not statements of historical fact. These forward-looking statements are based on our current expectations and projections about future events and they are subject to risks and uncertainties known and unknown that could cause actual results and developments to differ materially from those expressed or implied in such statements.

In some cases, you can identify forward-looking statements by terminology, such as “goals,” “expects,” “anticipates,” “intends,” “plans,” “believes,” “seeks,” “estimates,” “may,” “could,” “should,” “would,” “predicts,” “appears,” “projects,” or the negative of such terms or other similar expressions, although the absence of such words does not mean that a statement is not forward-looking. Factors that could cause or contribute to differences in results and outcomes from those in our forward-looking statements include, without limitation, those discussed elsewhere in this Annual Report in Part I, Item 1A. “Risk Factors,” Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and in this Item 1. We undertake no obligation to (and expressly disclaim any obligation to) revise or update any forward-looking statements made herein whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws. However, you should consult any further disclosures we may make on these or related topics in our reports on Form 8-K or Form 10-Q filed with the Securities and Exchange Commission ("SEC").

The following discussions should be read in conjunction with the sections of this Annual Report entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Risk Factors.”

OUR BUSINESS

Overview

Mistras Group, Inc. is a leading "one source" multinational provider of integrated technology-enabled asset protection solutions, helping to maximize the safety and operational uptime for civilization’s most critical industrial and civil assets.

Backed by an innovative, data-driven asset protection portfolio, proprietary technologies, and a decades-long legacy of industry leadership, the Company helps customers with asset-intensive infrastructure in the oil and gas, petrochemical, aerospace and defense, industrials, power generation and transmission (including alternative and renewable energy), other process industries and infrastructure, research and engineering and other industries towards achieving and maintaining operational excellence. By supporting these customers that help fuel our vehicles and power our society; inspecting components that are trusted for commercial, defense, and private space; and building monitoring equipment to help avoid catastrophic incidents, the Company helps the world at large.

The Company enhances value for its customers by providing data driven solutions that digitalize the asset protection process and provide valuable insights to our customers that maximize uptime of the assets monitored. Our data analytical solutions offerings, coupled with the traditional non-destructive testing ("NDT"), provide us a competitive advantage over our competitors. With our ability to integrate asset protection throughout supply chains and centralizing data management, we are able to provide insights and actionable recommendations to our customers through a suite of Industrial Internet of Things ("IoT")-connected digital software and monitoring solutions, including OneSuite™, which serves as an ecosystem platform, pulling together all of the Company’s software and data services capabilities, for the benefit of its customers.

The Company’s core capabilities also include NDT field inspections enhanced by advanced robotics, laboratory quality control, laboratory materials services, shop laboratory assurance testing, sensing technologies and NDT equipment, asset and mechanical integrity engineering services, and light mechanical maintenance and access services.

Given the role our solutions play in enhancing the safe and efficient operation of our customers' infrastructure, we have historically provided a majority of our solutions to our customers on a regular, recurring basis. We perform these services largely at our customers’ facilities, while primarily servicing our aerospace customers at our network of state-of-the-art, in-house laboratories. These solutions typically include NDT and inspection services, and can also include a wide range of

3

mechanical services, including heat tracing, pre-inspection insulation stripping, coating applications, re-insulation, engineering assessments and long-term condition-monitoring. Our traditional NDT solutions, coupled with our data analytical solutions offerings, allow us to provide accessible and easily understood data to our customers that allows them to identify when an asset may fail, in order to prioritize inspections and repair.

Under our business model, many customers outsource their inspection to us on a “run and maintain” basis. We have established long-term relationships as a critical solutions provider to many of the leading companies with asset-intensive infrastructure in our target markets. These markets include companies in the oil and gas, aerospace and defense, industrials, power generation and transmission (including alternative and renewable energy), other process industries and infrastructure, research and engineering and other industries.

We have focused on providing our advanced asset protection solutions to our customers using proprietary, technology-enabled software and testing instruments, including those developed by our Products and Systems segment. In the past, we have made numerous acquisitions in an effort to grow our base of experienced, certified personnel, expand our service lines and technical capabilities, increase our geographical reach, complement our existing offerings, and leverage our fixed costs. We have increased our capabilities and the size of our customer base through the development of applied technologies and managed support services, organic growth and the integration of acquired companies. These acquisitions have provided us with additional service lines, technologies, resources and customers, which we believe will enhance our advantages over our competition.

We believe long-term growth can be realized in our target markets. Our business and financial results are impacted by world-wide macro- and micro-economic conditions generally, as well as those within our target markets. Among other things, we expect the timing of our oil and gas customers inspection expenditures to be impacted by oil price fluctuations.

We have continued providing our customers with an innovative asset protection software ecosystem through our MISTRAS OneSuite platform. The OneSuite platform offers functions of MISTRAS' software and services brands as integrated applications on a cloud environment. OneSuite serves as a single access portal for customers' data activities and provides access to 90 plus applications being offered on one centralized platform.

We have established long-term relationships as a critical solutions provider to many of the leading companies with asset-intensive infrastructure in our target markets. These markets primarily consist of:

•Oil and Gas (Downstream, Midstream and Upstream)

•Aerospace and Defense

•Industrial

•Power Generation and Transmission

•Infrastructure, Research and Engineering

•Other Process Industries

•Petrochemical

A majority of our revenues are generated by deploying technicians at our customers' locations. A majority of our revenues from aerospace and defense as well as certain manufacturing customers are generated by performing inspections and testing at our various in-house laboratories.

We generated revenues of $705.5 million, $687.4 million and $677.1 million for the years ended December 31, 2023, 2022 and 2021, respectively. We generated net loss of $17.4 million, a net income of $6.6 million and net loss of $3.9 million for the years ended December 31, 2023, 2022, and 2021, respectively. For the years ended December 31, 2023, 2022 and 2021, we generated approximately 82%, 83% and 82%, respectively, of our revenues from our North America segment. Our revenues are diversified, with our top ten customers accounting for approximately 35%, 33% and 33% of our revenues during the years ended December 31, 2023, 2022 and 2021, respectively, with no customer accounting for greater than 10% of our revenues in any such year.

OUR SPECIALIZED SOLUTIONS

As a provider of asset protection solutions, we combine our industry-leading services, products, data management and analytical solutions technologies to provide a unique and custom-tailored solution for each customer’s individual asset protection needs, ranging from routine inspections to complex, plant-wide asset integrity management programs.

Field Inspections

4

Our field inspections portfolio includes traditional and advanced NDT techniques and inline inspection for pipelines. We offer these solutions on an individual basis, or as parts of enterprise inspection and testing programs.

NDT is the examination of an asset without materially impacting its structural integrity. The ability to inspect infrastructure assets and not interfere with their operating performance makes NDT a highly-attractive alternative to many traditional techniques, which may require shutting down an asset or entire facility. Typical issues for which our technicians inspect include potential corrosion, cracking, pitting, leaking, faults and flaws in piping, storage tanks and pressure vessels, as well as a wide range of other industrial assets and public infrastructure.

Our automated data acquisition solutions utilize smart sensing and monitoring, robotic inspection systems, and digitized spot inspections to provide asset integrity data with greater insight into current and potentially future asset conditions.

Field inspection services lend themselves to integration with our other offerings, and as such have often served as the initial entry point to more advanced customer engagements that require additional solutions. After an initial field inspection is performed, we are able to provide multiple supplemental solutions, such as maintenance services, engineering consulting and data analytical solutions services we provide, that further serve to solidify our relationships with our customers and drive additional revenue.

Data Analytical Solutions

The asset protection solutions that we provide throughout our customers’ asset lifecycles generate mechanical integrity data that needs to be effectively archived, managed, and analyzed. A common difficulty that our customers face is the ability to easily access and analyze large volumes of data from multiple data collection and input sources. We recognize that this data is most valuable to our customers when it is accessible and integrated (regardless of vendor, tool, or facility), and we have taken significant steps to digitalizing asset protection processes through our data analytical solutions product offerings.

Our data acquisition capabilities capture asset data to help our customers follow regulatory compliance, ensure mechanical integrity, and reduce unplanned outages. We capture data using manned and automated techniques that minimize the impact on our customers' operations. Customers can access our collected data for all facilities, structures, and assets that we manage from one easy to use dashboard, which enables customers to evaluate trending and benchmarking across multiple sites seamlessly.

Customer data is managed in our asset protection software ecosystem, OneSuite. Our OneSuite software platform offers functions of our popular software and services brands as integrated applications in a cloud environment. Our OneSuite software platform serves as a single access portal for customers' data activities and provides access to 90 plus integrated applications being offered in one centralized platform.

Many customers take advantage of our data analytics capabilities that utilize technology to automatically generate insights and actionable recommendations that can be implemented to improve our customers' overall productivity. Our managed services integrate our data capabilities with data analysts, field personnel and engineers to provide a comprehensive solution to our customers that reduces our customers' overall costs.

Our customers within the oil and gas and petrochemical industries take advantage of our industry-leading application Plant Condition Management Software (PCMS®). This application is one of the most widely used asset integrity management systems (“AIMS”). We estimate that our PCMS application is currently used by approximately 50% of the U.S. refiners, as well as by leading midstream pipeline energy companies and major oil and gas companies in Canada and Europe. This allows us to provide our customers with industry-leading insights across all their facilities and enables us to provide additional software and solutions to these customers and perform recurring maintenance where necessary.

Our pipeline customers utilize our Onstream® services and New Century® software platform to capture, manage and analyze pipeline integrity data in the midstream and upstream sectors of the oil and gas industry. We provide among the most comprehensive, data-driven pipeline protection solutions available to the industry. Our proprietary pipeline data analysis solutions enable deep integration of inline inspection ("ILI") big data with real-time risk analytics and business intelligence ("BI") to provide capabilities for supporting pipeline integrity, which we believe provides us with an important competitive advantage.

Our wind, power and infrastructure customers implement our online condition-monitoring solutions that provide real-time reports and analysis of infrastructure to alert facility personnel to damages before critical failures occur, while our flexible, IIoT compatible, cloud-based online monitoring portal centralizes and analyzes all collected monitoring data. These monitoring solutions are often installed in hazardous or hard-to-reach locations, helping to enhance safety by reducing the need to send technicians into unsafe locations.

5

Laboratory Testing

Our network of in-house laboratories located across North America and Europe offers quality assurance and quality control ("QA/QC") solutions for new and existing metal and alloy components, materials, and composites.

Our in-house laboratories work with our customers to test and measure utilized components throughout their lifetimes, from preparation and production to post-processing and in-service component monitoring. Our laboratory QA/QC solutions help to meet customer needs throughout their manufacturing cycles, with a focus on optimizing production logistics. Our in-house laboratory solutions include:

•Non-destructive evaluation/inspection ("NDE"/"NDI")

•Destructive testing ("DT")

•Metallurgical testing

•Chemical analysis testing

•Mechanical services

•Machining services

•Pre-machining

•Casting repair solutions

•Finishing services

We often inspect and test components prior to assembly to screen for defects and discontinuities introduced in the manufacturing process. We also inspect existing components to ensure they remain fit-for-purpose.

Our laboratories hold a wide variety of certifications, such as: Nadcap (formerly NADCAP, the National Aerospace and Defense Contractors Accreditation Program), AS9100/ISO-9001, Federal Aviation Administration Repair Station, and the International Traffic in Arms Regulations/Export Administration Regulations, that allow us to perform inspections which meet or exceed stringent regulatory and manufacturers' requirements. With these certifications come a comprehensive range of approvals from prime contractors of major projects, militaries and internationally-renowned original equipment manufacturers ("OEMs") from many of our key markets, including the oil and gas, aerospace and defense, power generation and industrial markets.

Maintenance

We perform maintenance and light mechanical services to prepare assets for inspection and to return them to working condition post inspection. These services include corrosion removal, mitigation and prevention; insulation installation and removal; electrical services; heat tracing, industrial cleaning; pipefitting; and welding. Our light mechanical services are often offered as complementary, value-added solutions to inspections, such as removing insulation in order to inspect piping, then re-installing insulation.

Our multi-disciplined technicians offer maintenance and light mechanical services in hard-to-access areas, in combination with rope access or diving strategies.

Mechanical services are still a small part of our business, and we carefully try to avoid providing any such services that conflict with our inspection services.

Engineering Consulting

We provide a broad range of engineering consulting services, primarily for process equipment, technologies and facilities. Our engineering consultations include plant operations and management support, turnaround/shutdown planning, profit improvement, facilities planning studies, engineering design, process safety reviews, energy optimization evaluations, benchmarking/key performance indicator development and technical training.

Our Asset Integrity Management ("AIMS") and Mechanical Integrity ("MI") services help improve asset reliability and regulatory compliance through a systematic, engineering-based approach to ensure the ongoing integrity and safety of equipment and industrial facilities. AIMS/MI services can include conducting an inventory of infrastructure assets; developing, implementing and training personnel in executing inspection and maintenance procedures; and managing MI programs. We help to identify gaps between existing and desired practices and establish quality assurance standards for fabrication, engineering and installation of infrastructure assets.

Access

6

Much of our work is conducted in hard-to-access locations, including those in at-height, subsea and confined locations. We utilize scaffolding and rope access to access at-height and confined assets; certified divers for subsea inspection and maintenance; and unmanned (drone) aerial, land-based and subsea systems to deliver a wide range of inspection applications, with an emphasis on minimizing at-height access and confined space entry.

Equipment

We design and manufacture portable, handheld, wireless and turnkey NDT equipment, along with corresponding data acquisition sensors and software, for spot inspections and long-term, unattended monitoring applications.

We sell these solutions as individual components, or as complete systems, which include a combination of sensors, amplifiers, signal processing electronics, knowledge-based software and decision and feedback electronics. We also sell integrated service-and-system technology packages, in which our field technicians utilize our proprietary and specialized testing procedures and hardware, advanced pattern recognition, neural network software and databases to compare test results against our prior testing data or industry standards.

We provide a range of acoustic emission ("AE") products and are a leader in the design and manufacture of AE sensors, instruments and turnkey systems used for monitoring and testing materials, pressure components, processes, and structures. We also design and manufacture ultrasonic testing ("UT") equipment.

Most of our hardware products are fabricated, assembled and tested in our ISO-9001-certified facility in Princeton Junction, New Jersey. We also design and manufacture automated ultrasonic systems and scanners in France.

Centers of Excellence

Another differentiator in our business model is our Centers of Excellence ("COEs"), which offer support for asset, technology or industry-specific solutions. Our subject matter experts engage in strategic sales opportunities to offer customers value-added solutions using advanced technologies and methods. The COEs help to standardize our approach to common problems in our key market segments. Our COEs include:

•Acoustic Emission

•American Petroleum Institute ("API") Turnarounds

•AIMS/MI/Engineering

•Automated Ultrasonics

•Fossil Power

•Guided Wave Ultrasonics

•Mechanical Services

•Nuclear Power

•Phased Array

•Rope Access

•Wind

•Tank Inspection

•Tube Inspection

•Unmanned Systems

ASSET PROTECTION INDUSTRY OVERVIEW

Asset protection plays a crucial role in assuring the integrity and reliability of critical infrastructure. As an asset protection solutions provider, we seek to maximize the uptime and safety of critical infrastructure, by helping customers to detect, locate, mitigate, and prevent damages such as corrosion, cracks, leaks, manufacturing flaws and other concerns to operating and structural integrity. In addition to these core utilities, the storage and analysis of collected inspection and MI data is also a key aspect of asset protection.

NDT has historically been a prominent solution in the asset protection industry due to its capacity to detect defects without compromising the structural integrity of the tested materials or equipment. Traditionally, the supply of NDT inspection services has been provided by many relatively small vendors, who provide services in a more localized geographic region. A trend has emerged, however, for customers to increasingly engage a select few vendors capable of providing a wider spectrum of asset protection solutions for global infrastructure, in addition to an increased demand for advanced non-destructive testing ("ANDT") solutions and data acquisition software, both of which require a highly-trained workforce.

Due to these trends, those vendors offering integrated solutions, scalable operations, skilled personnel and a global footprint are expected to have a distinct competitive advantage. Moreover, we believe that vendors that are able to effectively deliver both

7

advanced solutions and data analytics, by virtue of their access to customers’ data, create a significant barrier to entry for competitors, leading to the opportunity to further create significant recurring revenues.

Key Dynamics of the Asset Protection Industry

We believe the following represent key dynamics of the asset protection industry, and that the market available to us will continue to grow as these macro-market trends continue to develop:

Digital Transformation of Asset Protection. Plants in the oil and gas, petrochemical and other process industries are recognizing the need to evolve their traditional, paper-based mechanical integrity programs in favor of digitalized solutions. The rise of big data intelligence, and our data analytical solutions offerings, provide our customers with actionable insights from raw asset integrity data. The growing digitization of asset protection provides opportunities for contractors with a wide range of asset protection expertise and integrated data platforms to provide customers with data analytical solutions to help customers maximize uptime while controlling costs.

Extending the Useful Life of Aging Infrastructure While Increasing Utilization. Due to the prohibitive costs and challenges of building new infrastructure, many companies have chosen to extend the useful life of existing assets through enhancements, rather than replacing these assets. This has resulted in the significant aging and increased utilization of existing infrastructure in our target markets. Because aging infrastructure requires more frequent inspection and maintenance in comparison to new infrastructure, companies and public authorities continue to spend on asset protection to ensure their aging infrastructure assets continue to operate effectively.

Outsourcing of Non-Core Activities and Technical Resource Constraints. Due to the increasing sophistication and automation of NDT programs, a decreasing supply of skilled professionals and increasing governmental regulations, companies are increasingly outsourcing NDT to third-party providers with advanced solution portfolios, engineering expertise and trained workforces.

Increasing Corrosion from Low-Quality Inputs. The increased availability and low cost of crude oil from areas such as shale plays and oil sands resources have led to the use of lower-grade raw materials and feedstock. This leads to higher rates of corrosion, especially in refining processes involving petroleum with higher sulfur content, which increases the need for asset protection solutions to detect and/or proactively prevent corrosion-related issues.

Increasing Use of Advanced Materials. Customers in various target markets - particularly aerospace and defense - are increasingly utilizing advanced materials, such as composites and other unique technologies in their assets. These materials often cannot be tested using traditional NDT techniques. We believe that demand for more advanced testing and assessment solutions will increase as the utilization of these advanced materials increases during the design, manufacturing, operating and quality control phases.

Meeting Safety Regulations. Owners and operators of refineries, pipelines and petrochemical and chemical plants increasingly face strict government regulations and more stringent process safety enforcement standards. This includes the continued implementation of the Occupational Safety and Health Administration’s National Emphasis Program. Failure to meet these standards can result in significant financial liabilities, increased scrutiny by government and industry regulators, higher insurance premiums and tarnished corporate brand value. As a result, these owners and operators are seeking highly-reliable asset protection suppliers with a track record of assisting customers in meeting increasingly stringent regulations. Our customers benefit from our extensive engineering consulting base that supports them in devising mechanical integrity programs that both meet regulatory compliance standards and enable enhanced safety and uptime at the customer's facilities.

Expanding Addressable End-Markets. The continued emergence of and advances in asset protection technologies and software-based systems are increasing the demand for asset protection solutions in applications where existing techniques were previously ineffective.

Expanding Aerospace and Defense Industry. We believe that increased demand will continue to come over the next several years from the commercial industry due to the approximately decade-long backlog for next-generation commercial aircraft to be built, driving the need for advanced solutions that drive cost and quality efficiencies. Demand continues to be stable in the defense industry while demand in the private space industry is growing.

Crude Oil Prices. Volatility in the energy sector has been profound during the 2015-2022 period with moderation occurring during 2023. The collapse of world oil prices in 2015 and 2016 undermined industry expansion. While energy prices recovered in 2017 and 2018, they once more declined, and subsequently rebounded in the second half of 2021 and the first half of 2022 with near record high prices and crack spreads. This resulted in refineries delaying turnarounds during 2022 until oil prices decreased and stabilized in the second half of 2022. The stabilization continued throughout 2023 without major peaks and fluctuations as seen in prior periods. The on-going war in Ukraine and the conflict in the Middle East between Israel and

8

Hamas, coupled with continued macroeconomic uncertainty in 2024, are expected to continue to significantly influence oil prices for the foreseeable future.

Expanding Pipeline Integrity Regulations: The United States Pipeline & Hazardous Materials Safety Administration’s “Mega Rule” adopted in October 2019, expands pipeline integrity regulations on more than 500,000 miles of pipelines that carry natural gas, oil and other hazardous materials throughout the United States. Some of these requirements will take operators decades to fulfill. These regulations require inspection and integrity data records throughout a pipeline’s lifetime to be “reliable, traceable, verifiable, and complete,” increasing the demand for integrated inspection, engineering, monitoring, and data management and analysis solutions.

Consolidation of Refineries: Consolidation of refinery ownership will create both pressure on refinery service providers due to increased customer purchasing power and provide an opportunity to those same refinery service providers to become preferred providers to these larger customers.

Our Competitive Strengths

We believe the following competitive strengths contribute to our being a leading provider of asset protection solutions and will allow us to further capitalize on growth opportunities in our industry:

OneSource Provider for Asset Protection Solutions. We believe we have one of the most comprehensive portfolios of integrated asset protection solutions worldwide, which positions us to be a leading single-source provider for our customers’ asset protection requirements. This is particularly a competitive strength in regards to turnarounds and shutdowns - during which facilities temporarily cease portions of their operations in order to perform plant-wide inspections, maintenance and repairs - as the services being requested and performed during these work stoppages make up significant portions of refinery, process and power plant maintenance budgets. Demand for our solutions increases during these outages, as facilities seek third-party providers to perform a wide spectrum of asset protection operations while the plant is offline. In addition, as companies are increasingly outsourcing their NDT needs to third-party providers, we believe that the ability to offer a comprehensive package of solutions provides us with a competitive advantage.

Integrated Data Management: Our expertise and proprietary research and development in data analytical solutions throughout the asset protection cycle provides a competitive advantage. With solutions for integrated data acquisition, storage, visualization and analytics, our integrated data analytical solutions well-position us for the oil and gas increasing movement towards digitalizing and centralizing asset protection to fewer, highly-skilled and multi-disciplined vendors. Many of our data analytical solutions are platform-agnostic, allowing us to integrate into customers' existing operations, and thereby expanding the potential customer pool for our solutions. Our expertise and experience also allow us to tailor our offerings to meet specific customer needs, which sets us apart from our competitors. Our presence in our customers’ operations throughout their asset lifecycles also ideally positions us to be their primary vendor to centralize their asset integrity data collection, management and analysis, creating mutually-beneficial opportunities to scale our relationships.

Long-Standing Trusted Provider to a Diversified and Growing Customer Base. We have become a trusted partner to a large and growing customer base across numerous global markets through our proven, decades-long track record of successful operations. Our customers include some of the largest and most well-recognized firms in the oil and gas, chemicals, power generation and transmission and aerospace and defense industries, as well as public authorities.

Repository of Customer-Specific Inspection Data. Through our world-class enterprise data management and analysis software, PCMS, we have accumulated extensive, proprietary process data that allows us to provide our customers with value-added services, such as benchmarking, "RBI" and reliability-centered maintenance.

Proprietary Products, Software and Technology Packages. Our deep knowledge base in asset protection services and equipment enables us to offer technology packages, in which our field technicians utilize our proprietary and specialized testing procedures and hardware, advanced pattern recognition, neural network software and databases to compare test results against our prior testing data or national and international structural integrity standards.

Deep Domain Knowledge and Extensive Industry Experience. We have extensive asset protection experience and data, dating back several decades of operations. We have gained this through our industry leadership in developing advanced asset protection solutions, including research and development of advanced NDT technologies and applications, process engineering technologies, online plant asset integrity management with sensor fusion; and enterprise software solutions for plant-wide and fleet-wide inspection data archiving and management.

Technological Research and Development. The NDT industry continues to move towards more advanced, automated solutions, requiring service providers to find safer and more cost-efficient inspection techniques. We believe that we remain ahead of the

9

technological curve by backing our extensive industry expertise with the investment of resources in research and development. Some of the advanced inspection technologies developed by our internal research and development teams include an automated radiographic testing ("aRT") crawler for corrosion under insulation ("CUI") inspections in above ground pipelines and piping; our Large Structure Inspection ("LSI") scanner, and our real-time radiography ("RTR") crawler for 360° inspections of pipeline girth welds.

Collaborating with Our Customers. We have historically expanded our asset protection solution portfolio in response to our customers’ unique performance specifications. Our technology packages have often been developed in close cooperation and partnership with key customers and industry organizations.

Experienced Management Team. Our management team has a track record of asset protection organizational leadership. These individuals also have successfully driven operational growth organically and through acquisitions, which we believe is important to facilitate future growth in the asset protection industry.

Our Growth Strategy

Our growth strategy emphasizes the following key elements:

Continue to Digitalize Asset Protection Data and Processes. We place a data-centric focus on asset protection, enabling our customers to ease some of their biggest areas of concern (particularly the timely and accurate transfer of asset integrity data from the field to their IDMS, as well as the data’s visibility and accessibility once uploaded). We expect that the demand for our data analytical solutions which provides big data intelligence and remote data visibility will continue to grow, and we are investing in data analytical solutions that help our customers visualize and generate actionable insight from their asset integrity data, regardless of data input. We are also actively seeking to optimize our customers’ asset protection workflows and processes, by creating digital paths between data applications to increase data visibility and reduce manual data entry and human error.

Expand Our Focus in the Aerospace and Defense Industries. We believe that the introduction of next-generation airframes and aircraft engines has created an inherent demand for inspection, testing, machining and mechanical services required for the production of parts. The recent interest in the use of additive manufacturing techniques to create components also necessitates advanced inspection and testing solutions.

Expand Our Focus in the Pipeline Integrity Industry. We intend to continue broadening our solutions for the pipeline market. Recent industry regulations significantly expanded pipeline integrity management regulations, requiring pipeline owner/operators to inspect, document, and assess the risk of operating conditions for existing lines. This provides us with the opportunity to provide asset protection solutions for both the new construction and integrity phases. In 2019, we acquired a company that provides pipeline integrity management software and services to energy transportation companies. We acquired an inline inspection provider in 2018 and have implemented our PCMS software for several pipeline operators to support their integrity data management.

Expanding our Mechanical Services Portfolio. We believe that performing mechanical services to complement inspections, such as removing and reapplying insulation or preparing surfaces for coating or painting, is an important market differentiator for us. This is particularly true, for example, when considering the cost-efficiencies our customers realize when our rope access technicians perform these services at height without the use of scaffolding. Many of our customers already require these services, but utilize multiple vendors to do so, creating an opportunity for us to provide greater value to a customer base that increasingly requires enhanced speed and efficiency.

Continue to Develop Technology-Enabled and Digital Asset Protection Solutions. We intend to maintain and enhance our technological leadership by continuing to invest in developing new technology, applications and data services. The release of our OneSuite ecosystem underscores our dedication to continue deepening synergies between our solutions to provide our customers with uniquely-integrated offerings, which we believe makes us a more attractive vendor for customers seeking to centralize their asset protection. We have actively continued to develop technologies that enhance the flow of data throughout multiple operational phases and facilities, through our integrated pipeline integrity data portfolio, and our cloud-based monitoring data portal.

Expand our Solution Offerings to Existing Customers. We believe that branching into adjacent, complementary services, such as mechanical services, increases our value proposition and our ability to capture additional business. Many of our customers are multinational corporations with asset protection requirements at multiple locations. We believe that expanding our solution offerings and merging and visualizing data across facilities for enterprise data analysis, combined with the trend of customers outsourcing asset protection to service providers with integrated offerings, provides opportunities for significant additional recurring revenues.

10

Continue to Expand Our Customer Base into New End Markets. We believe we have significant opportunities to expand our customer base in relatively new end markets, including the renewable energy industry, specifically, wind and other alternative energy, natural gas transportation industries, pipeline integrity and additive manufacturing. The expansion of our addressable markets is being driven by the increased recognition and adoption of advanced asset protection technologies (such as unmanned drone inspection devices, robotics, etc.) that are supplanting traditional methods.

Capitalize on Acquisitions. We have completed several acquisitions to supplement and enhance our solutions, add new customers, expand our sales channels and accelerate our expected growth. Due to our current debt levels and restrictions related to the debt covenants in our credit facility, we do not expect to make any acquisitions in 2024 other than small acquisitions with the banks’ approval. However, once we reduce our debt, we expect to make selective acquisitions beyond 2024.

Our Segments

We have three operating segments: (i) North America (which we previously referred to as our Services segment), (ii) International and (iii) Products and Systems:

North America provides asset protection solutions with the largest concentration in the United States, followed by Canada, consisting primarily of NDT, inspection, mechanical and engineering services that are used to evaluate the structural integrity and reliability of critical energy, industrial and public infrastructure and commercial aerospace components. Software, digital and data services are included in this segment.

International offers services, products and systems similar to those of the other segments to select markets within Europe, the Middle East, Africa, Asia and South America, but not to customers in China and South Korea, which are served by the Products and Systems segment

Products and Systems designs, manufactures, sells, installs and services the Company’s asset protection products and systems, including equipment and instrumentation, predominantly in the United States.

For a discussion of segment revenues, operating results and other financial information, including geographic areas in which we generated revenues, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in Item 7, as well as Note 2-Revenue and Note 19-Segment Disclosure in the notes to our audited consolidated financial statements in Item 8 of this Annual Report.

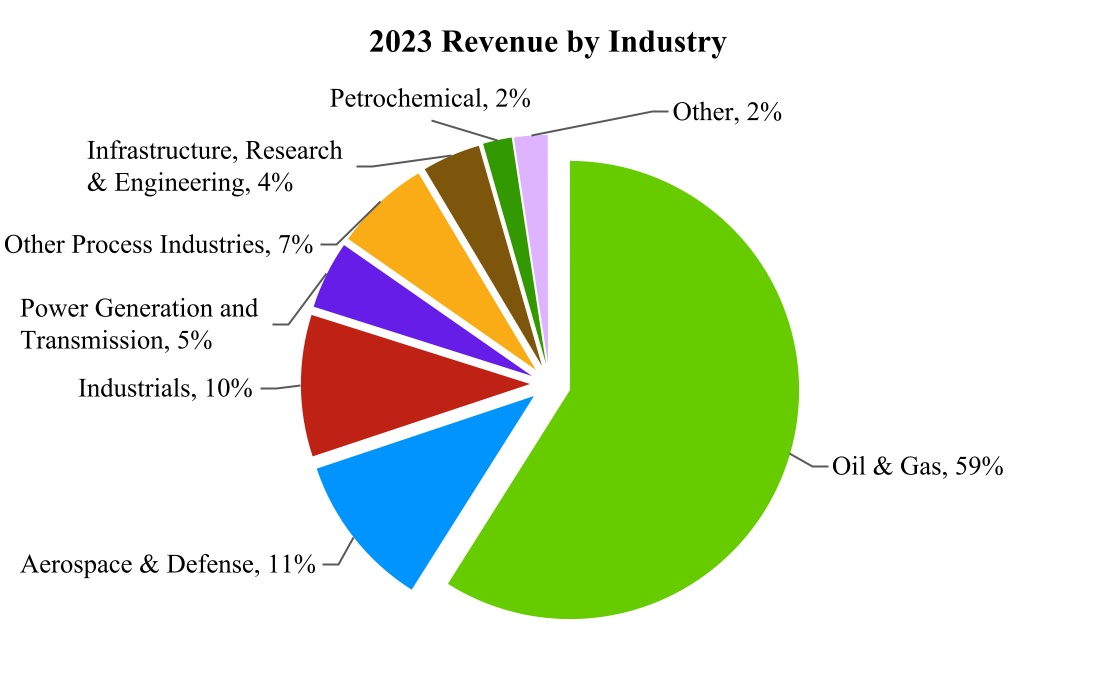

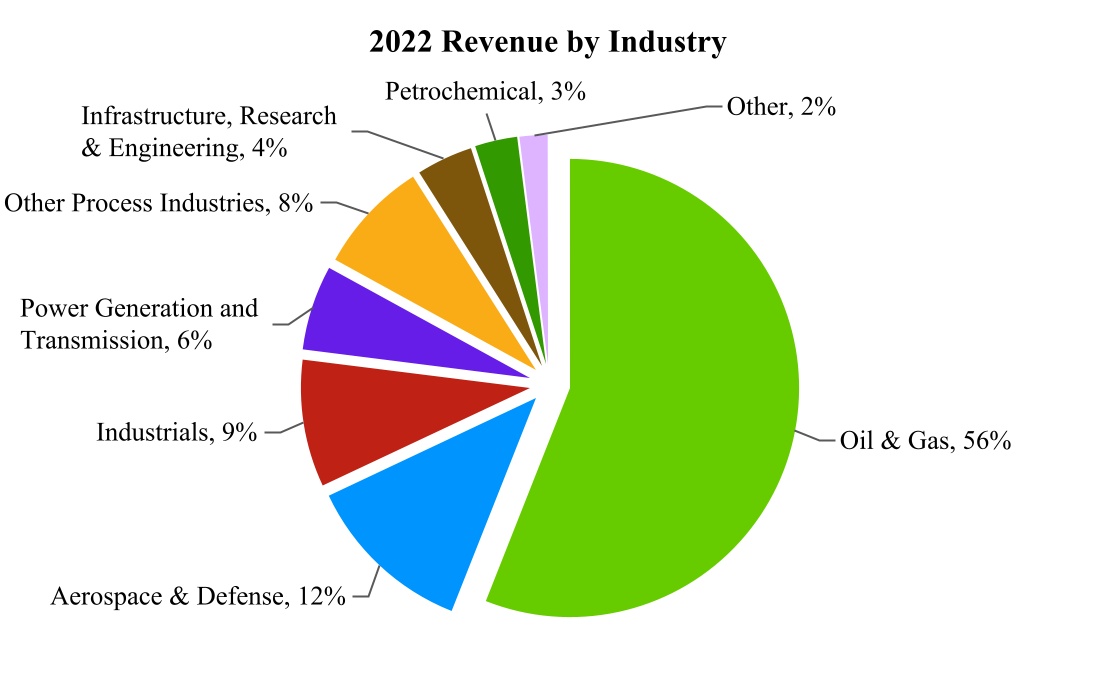

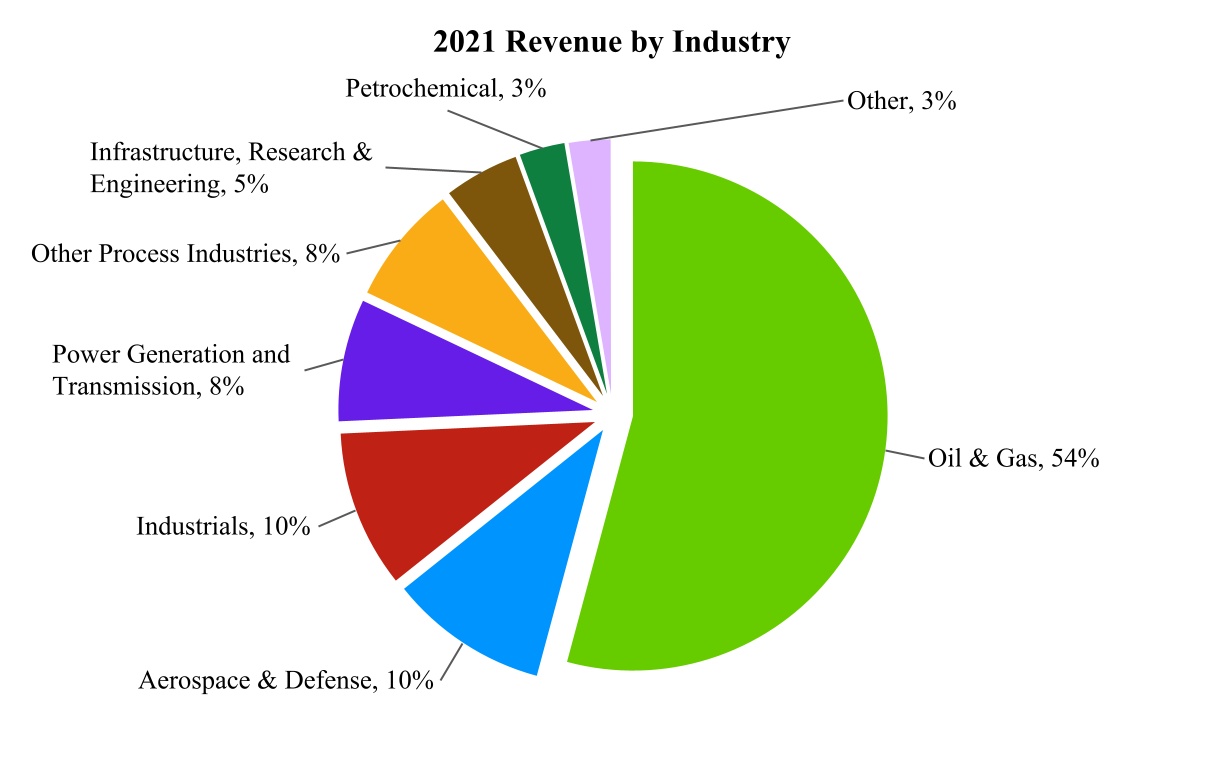

Revenue Overview

Revenue by Industry

The following charts represent our disaggregated revenue by industry for the years ended December 31, 2023, 2022 and 2021.

11

12

Our Target Markets

Overview

We operate in a highly competitive, but fragmented market. Domestically, the market is serviced by several national competitors and many regional and/or local companies. Internationally, our primary competitors are divisions of large companies, with additional competition from small independent local companies which may be limited to a specific product, service or technology and focused on a niche market or geographic region. We focus our strategic sales, marketing and product development efforts on a range of infrastructure-intensive based industries and governmental authorities. We view energy-related infrastructure and commercial aerospace as our largest market opportunities. We perform inspection and mechanical services for customers in both industries.

Our revenues are comprised of services offerings at our laboratories and at customer facilities. Data Analytical Solutions revenues are comprised of revenue derived from data software sales & subscriptions, implementation services and analytics that offer insights and recommendations to improve asset integrity. Data Analytical Solutions revenue is derived from work performed by Mistras employees in our facilities, or at customer locations, using our proprietary portfolio of software applications. Field Services revenues are comprised of revenue derived primarily by technicians performing asset inspections and maintenance services for our customers at locations other than Mistras properties. Shop Laboratory revenues are comprised of quality assurance inspections of components and materials at our Mistras in-house laboratory facilities. Other revenues are comprised of locations that perform both asset inspection services and testing of components and materials at in-house Mistras laboratories.

There are a number of economic factors which drive the aerospace market, including:

•The multi-year backlog for next generation commercial aircraft to be built, including several large and mid-sized aircraft built by Boeing and Airbus, among other manufacturers; and

•The continuing regulatory scrutiny to ensure public safety serves to ensure the continued need for inspection and mechanical services to be performed.

In the energy market, there are various economic indicators that drive our business, especially in the U.S. domestic markets. It is unclear what the short and long term effects of the war between Russia and Ukraine is likely to have on the world economy and certain of our target markets, including particularly the oil and gas market. Excerpted below are forecasts from various Energy Information Administration (EIA) outlook reports, which are subject to change based on these factors:

13

Electricity generation from coal is projected to fall throughout the mid 2020s and the decrease will be partially offset by an increase in the forecast of combined utility-scale solar and wind generation.

The EIA noted U.S. crude oil production averaged 11.9 million barrels per day (bpd) in 2022 and rose to an average 12.9 million bpd in 2023. The EIA forecasts production to continue to increase to an average 13.3 million bpd in 2024 and further increase to 13.5 million bpd in 2025.

Oil and Gas

We supply oil and gas asset protection solutions to downstream (refining), midstream (transportation and storage) and upstream (exploration and production) operations.

We use our vast solutions portfolio to help identify current and future asset performance, and actively prevent, mitigate or otherwise address potential issues, including corrosion, cracking, leaking and other damages that may lead to safety, productivity or environmental concerns. Our solutions help identify conditions that if not remedied, could lead to potential catastrophic failures in tanks, vessels, valves, buried and above ground pipelines, pumps, motors, compressors and other critical assets found throughout the oil and gas production and delivery supply chain.

We actively seek to evolve our solutions through technological enhancements and research and development to discover new applications. Online monitoring and permanently-mounted sensors, as well as the use of drones and other alternative delivery devices, are all being considered as oil and gas infrastructure owners look to “smart” technologies that reduce human intervention while delivering highly-accurate inspection and integrity data. We also have actively sought to further enhance our integrated approach to asset protection, through the development of our complementary mechanical service portfolio.

In general, the oil and gas market is poised to leverage digital solutions to facilitate process improvements as well as increase plant reliability and improve process and personnel safety. This provides an opportunity for us to synergistically leverage our digital asset protection solutions. Digital transmission of data in various industry sectors, with built-in analytic functions, will allow our customers to better leverage inspection data that is being generated in the field.

While we expect off-stream inspection of critical assets to remain a routine practice, we anticipate an increase in the demand for non-invasive or on-stream inspections. Non-invasive inspections enable companies to minimize the costs associated with shutting down equipment during testing, while enabling the economic and safety advantages of advanced planning and/or predictive maintenance.

Aerospace and Defense

The aerospace industry continued to rebound from COVID-19 throughout 2023 with backlog and production levels approaching and exceeding pre-pandemic levels for certain OEMs for the first time since the pandemic. We serve this rapidly growing target market by providing a full range of inspection, testing, machining, mechanical, finishing, additive manufacturing and equipment solutions, for which we are Nadcap certified. Our state-of-the-art in-house laboratories maintain numerous accreditations from industry organizations, including Nadcap, and some of the largest manufacturers in the world, such as Boeing, Safran, Airbus, Bombardier and Embraer.

Advanced composite materials found in new classes of aircraft require advanced asset protection solutions, including x-ray of critical engine components, ultrasonic fatigue testing of complete aircraft structures and corrosion detection and other critical components. Many OEMs are shifting towards condition-based maintenance utilizing embedded monitoring sensors to track component structural and operational integrity over time as opposed to performing maintenance on time-based intervals. We expect demand for our solutions to increase with the adoption of these new-age materials and distributed online sensor networks. We also expect demand for asset protection solutions to increase with the continued adoption of additive manufacturing techniques.

Industrials

The quality control requirements driven by the need for zero-to-low-defect component tolerance within automated, robotic-intensive industries such as automotive, consumer electronics and medical industries serve as key drivers for increased demand in asset protection, particularly for in-house inspection and testing. We expect that increasingly stringent quality-control requirements and competitive forces will drive the demand for more-costly finishing and polishing which, in turn, creates opportunities for integrated partnerships between us and our customers throughout the production lifecycle.

Power Generation and Transmission

14

We provide asset protection solutions for customers in the combined cycle, fossil, nuclear, transmission and distribution and wind/alternative energy industries. We believe that in recent years, acceptance of asset protection solutions has grown in this industry due to the aging of critical power generation and transmission infrastructure.

The growing availability of cheap natural gas, along with environmental concerns with coal, has stimulated the construction of new natural gas-fired power plants across North America, creating opportunities for us to provide specialized solutions in multiple phases. These include facility design consultations, NDT services during construction and plant operations and long-term condition monitoring. We anticipate sharp growth in these types of plants as natural gas pricing remains low, and the environmental impacts of coal remain unattractive to the public.

We also offer solutions for inspection, maintenance, monitoring and data services for wind turbines and their components. These include NDT services — often performed through rope and/or drone access — to identify corrosion, cracking, and other defects that can affect the safety and operational effectiveness of wind turbines, along with remedial solutions to repair minor damages identified during inspections.

Other Process Industries

Our asset protection solutions are crucial for process industries, or industries in which raw materials are treated or prepared in a series of stages, including chemicals, pharmaceuticals, food processing, pulp and paper and metals and mining. As the process facilities are increasingly facing aging infrastructure, high utilization, growing capacity constraints and increasing capital costs, we believe asset protection solutions will continue to grow in importance in maintenance planning, quality and cost control and prevention of catastrophic failure.

Infrastructure, Research and Engineering

We believe that high-profile infrastructure catastrophes have caused public authorities to more actively seek ways to prevent similar events from occurring. Public authorities tasked with new construction and maintenance of existing public infrastructure increasingly use asset protection solutions to inspect these assets, including the use of embedded sensors to enable online monitoring throughout the life of the asset.

We have provided testing and structural health monitoring and data analytical solutions on bridges and structures worldwide, including some of the largest and most well-known bridges in the United States and United Kingdom. Our sensors continuously monitor these assets, alerting owner/operators when defects are detected. Our monitoring teams also provide regular reports that include early warnings of suspect areas before an alarm is generated.

Petrochemical

We provide asset protection NDT services for customers within the petrochemical industry, as they transform byproducts into goods which are utilized in many end products such as plastics, soaps, fertilizers, synthetic fibers and rubber. Our solutions help identify conditions that if not remedied, could lead to potential catastrophic failures in tanks, vessels, valves, buried and above ground pipelines, pumps, motors, compressors and other critical assets found throughout the petrochemical production process.

We actively seek to evolve our solutions through technological enhancements and R&D to discover new applications. Online monitoring and permanently-mounted sensors provide real-time data to petrochemical owners and operators and provide an opportunity for us to synergistically leverage our asset protection solutions into our MISTRAS Digital platform, OneSuite. Digital transmission of data in various industry sectors, with built-in analytic functions, will allow our customers to better leverage inspection data that is being generated in the field. We also have actively sought to further enhance our integrated approach to asset protection, through the development of our complementary mechanical service portfolio.

Customers

We provide our asset protection solutions to a global customer base of diverse companies primarily in our target markets. No customer represented 10% or more of our revenue in any of the years ended December 31, 2023, 2022 or 2021.

Geographic Areas

We have operations in 10 countries and occasionally conduct business in a few other countries. Most of our revenues are derived from our U.S., Canadian and European operations and we do not have operations in Russia, and we do not do business in Russia, Ukraine or other areas which are impacted by the Russian invasion of Ukraine. See Note 2-Revenue and Note 19-Segment Disclosure to our audited consolidated financial statements in this Annual Report for further disclosure of our revenues, long-lived assets and other financial information regarding our international operations.

15

Sales and Marketing

We sell our asset protection solutions through our direct sales and marketing activities worldwide. In addition, our project and laboratory managers, as well as our management, are trained on our solutions and often are the source of sales leads and customer contacts. Our direct sales and marketing teams work closely with our customers to demonstrate the benefits and capabilities of our asset protection solutions, refine our asset protection solutions based on changing market and customer needs and identify potential opportunities. We divide our sales and marketing efforts into services sales, products and systems sales and marketing and utilize marketing automation and customer relationship management ("CRM") systems to collect, manage and collaborate customer information with our teams globally. Our CRM systems also provide critical data to provide accurate forecasting and reporting.

Manufacturing

Most of our hardware products are manufactured in our Princeton Junction, New Jersey facility. This facility includes the capabilities and personnel to fully produce all of our AE products and NDT Automation Ultrasonic equipment. We also design and manufacture automated ultrasonic systems and scanners in France.

Human Capital

As of December 31, 2023, we had approximately 4,800 employees worldwide, of which 3,200 were located in the United States, 500 in Canada and 1,100 in our other non-U.S. locations. Our employees include full and part time employees throughout our organization. As described below, we value our employees and have established various programs to promote the satisfaction, health and safety of our employees. Less than 0.01% of our employees in the United States are unionized.

Our employees are key to achieving our goals and strategy. We have committed resources throughout our organization to ensure that we are attracting, developing, and retaining talented employees needed to support all aspects of our activities. Our core values and business ethics guide and direct all activities undertaken by us.

The health and safety of our employees is paramount. We have also developed key initiatives and strategies regarding our talent and people initiatives. Below, we describe some of the key initiatives and values around health and safety. Management regularly updates our Board of Directors with regards to our safety and people strategy and how we are performing in these areas. In 2020, our Board established the Environmental, Social and Safety Committee. This Committee, which consists of independent directors, monitors and oversees the strategic direction of our initiatives in support of our core values and our environmental, social and governance initiatives.

Talent, Leadership and Employee Development

Employee development and engagement begins with our senior management team, which has considerable industry experience and expertise. Leveraging this experience and expertise, our senior management team is able to continuously review our organizational structure and provide opportunities for the growth and development for our employees.

As part of our continued commitment to our employees, we have established various programs to promote lifelong learning and development opportunities for our employees. These include a mix of voluntary and mandatory training programs, which are provided in-person, virtually or on the job. We also provide employees the ability to continue to gain additional professional certifications to contribute to their career advancement. We utilize a web-based training center which is available to field technicians for career advancement and includes over 500 web-based classes. In addition, we are committed to ensuring all employees are compensated at a living wage. All local minimum wage requirements are met and where no wage laws are in place, employees are compensated competitively, in accordance with industry standards.

Our human rights policy places a high priority on diversity and equal opportunity and provides our employees with management’s expectations related to human rights and labor practices.

Another program we instituted focuses on our connection by a common thread of caring – about one another, our customers, the environment, and the work we do. We seek to foster a culture of togetherness, safety, respect, and contribution which enables each individual member to feel that he or she is a part of something bigger. A community of caring professionals with a genuine passion for helping people and making a difference together – that is the heart of the program we call “Caring Connects.”

16

Our Safety-Conscious Culture

We consider safety the backbone of our operations. Our asset protection solutions aim to ensure that industrial assets and facilities remain in safe, reliable working condition, which in turn enhances safety for our customers, the public, and the environment. Our laboratory and field personnel are trained to operate according to strict safety and quality standards so that our processes and procedures regarding hazardous materials, worker safety, and accident prevention are sound and effective. Further to this, we are constantly evaluating these processes and procedures to ensure that they remain of high quality and are effective, and we consider changes in the manner in which work is performed or lessons that have been learned from any sources, such as industry data. We work to help ensure that our customers are in full compliance with all federal, state, and local regulations. Our practices, policies and procedures are designed to help ensure we perform our duties through the use of safe, industry-best practices, seeking to minimize risk wherever possible.

We emphasize a “MISTRAS’ safety-conscious” culture with the intent that it becomes embedded in the day-to-day work of all our employees. We use various training tools and other practices to instill attitudes, beliefs, perceptions, and values that all employees share in the mandate to create and maintain a safe work environment for all.

We continuously monitor our safety performance through analysis of our company-wide safety statistics, which help us to determine behavioral trends while also instilling a culture of proactivity. For the year ended December 31, 2023, our Total Recordable Incident Rate ("TRIR") was 0.3 while Days Away, Restricted and Transferred Rate was 0.18 and Lost Work Day Rate remained 0.12. For the year ended December 31, 2022, our TRIR was 0.41.

Seasonality

Our business is seasonal. This seasonality relates primarily to our oil and gas target market, and to a lesser extent within our other target markets. U.S. refineries’ non-peak periods are generally in the fall, when they are retooling to produce more heating oil for winter, and in the spring, when they are retooling to produce more gasoline for summer. The peak periods for these customers are the summer and winter months, when they run at peak capacity and are not retooling or performing turnarounds or shut downs. As a result, our revenues in the summer and winter months are typically lower than our revenues in the fall and spring, when demand for our asset protection solutions from the oil and gas as well as the fossil power industries increases during their non-peak production periods. Because we are increasing our work in the fall and spring, our cash flows are lower in those quarters than in the summer and winter, as collections of receivables lag behind revenues. We expect that this seasonality will continue.

Competition

We operate in a highly competitive, but fragmented, market. Our primary competitors include large public and private companies, divisions of large companies and various small companies which generally are limited to a specific product or technology and focused on a niche market or geographic region. We believe that few, if any, of our competitors currently provide the full range of asset protection and NDT products, enterprise software ("PCMS") and the traditional and advanced services solutions that we offer. Our competition with respect to NDT services include Acuren, SGS Group, the Team IHT Segment and APPLUS RTD. Our competition with respect to our PCMS software includes UltraPIPE, Lloyd’s Register Capstone, Inc. and Meridium Systems. In the traditional NDT market, we believe the principal competitive factors include project management, availability of qualified personnel, execution, price, reputation and quality, whereas in the advanced NDT market, reputation, quality and size tend to be the most significant competitive factors. We believe that the NDT market has significant barriers to entry which would make it difficult for new competitors to enter the market. These barriers include: (i) having to acquire or develop advanced NDT services, products and systems technologies, which in our case occurred over many years of customer engagements and at significant internal research and development expense, (ii) complex regulations and safety codes that require significant industry experience, (iii) license requirements and evolved quality and safety programs, (iv) costly and time-consuming certification processes, (v) capital requirements and (vi) emphasis by large customers on size and critical mass, length of relationship and past service record.

Research and Development

Our research and development is principally conducted by engineers and scientists at our Princeton Junction, New Jersey headquarters, and supplemented by other employees in the United States and throughout the world, including Canada, France, Greece the United Kingdom, Brazil and the Netherlands. Our total professional staff includes employees who hold Ph.D.’s and engineers and employees who hold Level III certification, the highest level of certification from the American Society of Non-Destructive Testing (ASNT).

17

We make strategic research and development investments in our data analytical solutions technologies that support integration with our other solution offerings to enhance cost- and time-efficiencies, maximize uptime and safety and improve the flow of data from field technicians to inspection databases. These strategic investments enable us to enhance our service offerings to customers and provide valuable insights and predictive analysis.

We have also invested significant research and development in pre-machining and advanced testing technologies in a purpose-built facility for an aerospace customer, with the goal of reducing the customer’s production cycle logistics and costs.

We also work with customers to develop new products or applications for our technology, including:

•Testing of new composites

•Detecting crack propagation

•Wireless and communications technologies

•Development of permanently embedded inspection systems to provide continuous, online, in-service monitoring of critical structural components

Research and development expenses are reflected in our Consolidated Statements of Income (Loss) as research and engineering expenses. Our company-sponsored research and engineering expenses were approximately $1.7 million, $2.0 million and $2.5 million for the years ended December 31, 2023, 2022 and 2021, respectively. While we have historically funded most of our research and development expenditures, from time to time we also receive customer-sponsored research and development funding. Most of the projects are in our target markets, however, a few of the projects could lead to other future market opportunities.

Intellectual Property

Our success depends, in part, on our ability to maintain and protect our proprietary technology and to conduct our business without infringing on the proprietary rights of others. We utilize a combination of intellectual property safeguards, including patents, copyrights, trademarks and trade secrets, as well as employee and third-party confidentiality agreements, to protect our intellectual property.

As of December 31, 2023, we held 12 U.S. patents by direct ownership and 5 patent applications pending in the United States. All the patent applications pending have been filed since 2018. While we do not rely on these patents or licenses to provide a majority of our proprietary asset protection solutions, certain of these patents do provide us with a competitive advantage and we believe they will be an asset to our growth strategy. Our trademarks and service marks provide us and our solutions with a certain amount of brand recognition in our markets. We do not consider any single patent, trademark or service mark material to our financial condition or results of operations.

As of December 31, 2023, the primary trademarks and service marks that we held in the United States included MISTRAS®, our stylized globe design and our tag line "One Source for Asset Protection Solutions". Other key trademarks or service marks that we utilize in localized markets or product advertising include:

•Onstream® (word and logo)

•PCMS® (word and logo)

•Ropeworks®

•MISTRAS Digital®

•OneSuite™

•Sensoria™

•OneSource™

•CALIPERAY™ (word and logo)

•Physical Acoustics PAC logo

•Streamview™

•Sensor Highway™

•TankPAC®

•VPAC™

•Transformer Clinic™

•FieldCal™

•UTwin®

•AEwin®

•Pocket AE®

•Pocket UT®

18

Many elements of our asset protection solutions involve proprietary know-how, technology or data that are not covered by patents or patent applications because they are not patentable or would be difficult to enforce, including technical processes, algorithms and procedures. We believe that this proprietary know-how, technology and data is the most important component of our intellectual property used in our asset protection solutions and is a primary differentiator of our solutions from those of our competitors. We rely on various trade secret protection techniques and agreements with our customers, service providers and vendors to protect these assets. All of our employees are subject to confidentiality requirements through our employee handbook. In addition, many of our employees have entered into confidentiality and proprietary information agreements with us. Our employee handbook and these agreements require our employees not to use or disclose our confidential information and to assign to us all the inventions, designs and technologies they develop during the course of employment with us, as well as addressing other intellectual property protection issues. We also seek confidentiality agreements from our customers and business partners before we disclose any sensitive aspects of our technologies or business strategies. We are not currently involved in any material intellectual property claims.

Governmental Regulations

We are subject to numerous environmental, legal and regulatory requirements related to our operations worldwide. In the United States, these laws and regulations include, among others: the Comprehensive Environmental Response, Compensation, and Liability Act, the Resources Conservation and Recovery Act, the Clean Air Act, the Federal Water Pollution Control Act, the Toxic Substances Control Act, the Atomic Energy Act, the Energy Reorganization Act of 1974, and applicable regulations. In addition to the federal laws and regulations, states and other countries where we do business often have numerous environmental, legal and regulatory requirements by which we must abide. We evaluate and address the environmental impact of our operations by assessing properties in order to avoid future liabilities and comply with environmental, legal and regulatory requirements.

Executive Officers

The following were our executive officers for the year ended December 31, 2023 and their background and experience.

| Name | Age | Position | ||||||||||||

| Manuel N. Stamatakis | 76 | Chairman of the Board and Interim President and Chief Executive Officer | ||||||||||||

| Edward J. Prajzner | 57 | Senior Executive Vice President and Chief Financial Officer | ||||||||||||

| Gennaro D'Alterio | 52 | Executive Vice President, Chief Commercial Officer | ||||||||||||

| Michael C. Keefe | 67 | Executive Vice President, General Counsel and Secretary | ||||||||||||

| Michael J. Lange | 63 | Senior Group Executive Vice President | ||||||||||||

| John A. Smith | 54 | Executive Vice President and President of Services | ||||||||||||

Manuel "Manny" N. Stamatakis joined Mistras Board of Directors in 2002, became the Chair of the Governance Committee as well as a member of the Audit Committee and Compensation Committee in 2009 and Lead Director in 2010. On October 9, 2023, Mr. Stamatakis became the Chairman of the Board, and on the same day became our Interim President Chief Executive Officer to replace our prior President and Chief Executive Officer, Dennis Bertolotti. At that same time, Mr. Stamatakis resigned from all the committees of the Board and as our lead director. Mr. Stamatakis currently chairs the Project Phoenix Steering Committee, an initiative for which he is both the chief architect and driving force.

An accomplished entrepreneur for over 30 years, Mr. Stamatakis is an executive officer of Capital Management Enterprises, Inc., a financial services and employee benefits consulting firm based in Pennsylvania. Mr. Stamatakis has held multiple board and chairmanship positions over the years, including Chairman of the Delaware River Port Authority, The Drexel College of Medicine, the Pennsylvania Supreme Court Investment Advisory Board, and the Philadelphia Shipyard Development Corporation which was the catalyst to bringing shipbuilding back to the Philadelphia region. He earned a B.S. in Industrial Engineering from Pennsylvania State University and received an honorary Doctor of Business Administration from Drexel University.

19

Edward J. Prajzner joined Mistras in January 2018 as our Senior Vice President, Chief Financial Officer and Treasurer, was subsequently promoted to Executive Vice President and on March 26, 2023, was promoted to become our Senior Executive Vice President and Chief Financial Officer. Prior to joining Mistras, Mr. Prajzner worked at CECO Environmental Corp., a global service provider to environmental, energy and filtration industries, and served as Chief Financial Officer and Secretary from 2014 to 2017, Vice President of Finance and Chief Accounting Officer from 2013 until his appointment as Chief Financial Officer in 2014, and Corporate Controller and Chief Accounting Officer from 2012 to 2013. Mr. Prajzner also served in senior finance roles at CDI Corporation (now AE Industrial Partners) and American Infrastructure (now Allan Myers). Mr. Prajzner began his career in public accounting at Ernst & Young, received his B.S. in accountancy from Villanova University, his MBA in finance from Temple University and is a certified public accountant.