UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

_____________________________________________________________

FORM 10-Q

_____________________________________________________________

(Mark One)

| QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the quarterly period ended June 30, 2023

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from _______________ to _______________

Commission File Number: 001-37756

______________________________________________________________

(Exact Name of Registrant as Specified in its Charter)

______________________________________________________________

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

Registrant’s telephone number, including area code: (480 ) 360-7775

Securities registered pursuant to Section 12(b) of the Act:

______________________________________________________________

| Title of each class | Trading Symbol | Name of each exchange on which registered | ||||||

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. x Yes ☐ No

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). x Yes ☐ No

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☐ | |||||||||||||||||

| x | Smaller reporting company | |||||||||||||||||||

| Emerging growth company | ||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). ☐ Yes x No

As of August 9, 2023, the registrant had 24,170,517 shares of common stock, $0.01 par value per share, outstanding.

-1-

TABLE OF CONTENTS

| PART I. | ||||||||

| Item 1. | Financial Statements (Unaudited) | |||||||

Condensed Consolidated Balance Sheets | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| PART II. | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

-2-

ITEM 1.FINANCIAL STATEMENTS

GLOBAL WATER RESOURCES, INC.

CONDENSED CONSOLIDATED BALANCE SHEET

(in thousands, except share and per share amounts)

(Unaudited)

| June 30, 2023 | December 31, 2022 | ||||||||||

| ASSETS | |||||||||||

| PROPERTY, PLANT AND EQUIPMENT: | |||||||||||

| Land | $ | $ | |||||||||

| Depreciable property, plant and equipment | |||||||||||

| Construction work-in-progress | |||||||||||

| Other | |||||||||||

| Less accumulated depreciation | ( | ( | |||||||||

| Net property, plant and equipment | |||||||||||

| CURRENT ASSETS: | |||||||||||

| Cash and cash equivalents | |||||||||||

| Accounts receivable — net | |||||||||||

| Customer payments in-transit | |||||||||||

| Unbilled revenue | |||||||||||

| Taxes, prepaid expenses, and other current assets | |||||||||||

| Total current assets | |||||||||||

| OTHER ASSETS: | |||||||||||

| Goodwill | |||||||||||

| Intangible assets — net | |||||||||||

| Regulatory asset | |||||||||||

| Restricted cash | |||||||||||

| Right-of -use asset | |||||||||||

| Other noncurrent assets | |||||||||||

| Total other assets | |||||||||||

| TOTAL ASSETS | $ | $ | |||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY | |||||||||||

| CURRENT LIABILITIES: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Customer and meter deposits | |||||||||||

| Long-term debt — current portion | |||||||||||

| Leases — current portion | |||||||||||

| Total current liabilities | |||||||||||

| NONCURRENT LIABILITIES: | |||||||||||

| Line of credit | |||||||||||

| Long-term debt | |||||||||||

| Long-term lease liabilities | |||||||||||

| Deferred revenue - ICFA | |||||||||||

| Regulatory liability | |||||||||||

| Advances in aid of construction | |||||||||||

| Contributions in aid of construction — net | |||||||||||

| Deferred income tax liabilities, net | |||||||||||

| Acquisition liability | |||||||||||

| Other noncurrent liabilities | |||||||||||

| Total noncurrent liabilities | |||||||||||

| Total liabilities | |||||||||||

| Commitments and contingencies (Refer to Note 16) | |||||||||||

| SHAREHOLDERS’ EQUITY: | |||||||||||

Common stock, $ | |||||||||||

Treasury stock, | ( | ( | |||||||||

| Paid in capital | |||||||||||

| Retained earnings | |||||||||||

| Total shareholders’ equity | |||||||||||

| TOTAL LIABILITIES AND SHAREHOLDERS’ EQUITY | $ | $ | |||||||||

See accompanying notes to the condensed consolidated financial statements

-3-

GLOBAL WATER RESOURCES, INC.

CONDENSED CONSOLIDATED STATEMENTS OPERATIONS

(in thousands, except share and per share amounts)

(Unaudited)

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| REVENUES: | |||||||||||||||||||||||

| Water services | $ | $ | $ | $ | |||||||||||||||||||

| Wastewater and recycled water services | |||||||||||||||||||||||

| Unregulated revenues | |||||||||||||||||||||||

| Total revenues | |||||||||||||||||||||||

| OPERATING EXPENSES: | |||||||||||||||||||||||

| Operations and maintenance | |||||||||||||||||||||||

| General and administrative | |||||||||||||||||||||||

| Depreciation and amortization | |||||||||||||||||||||||

| Total operating expenses | |||||||||||||||||||||||

| OPERATING INCOME | |||||||||||||||||||||||

| OTHER INCOME (EXPENSE): | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | |||||||||||||||||||

| Allowance for equity funds used during construction | |||||||||||||||||||||||

| Other - Net | |||||||||||||||||||||||

| Total other expense | ( | ( | ( | ( | |||||||||||||||||||

| INCOME BEFORE INCOME TAXES | |||||||||||||||||||||||

| INCOME TAX BENEFIT (EXPENSE) | ( | ( | ( | ||||||||||||||||||||

| NET INCOME | $ | $ | $ | $ | |||||||||||||||||||

| Basic earnings per common share | $ | $ | $ | $ | |||||||||||||||||||

| Diluted earnings per common share | $ | $ | $ | $ | |||||||||||||||||||

| Dividends declared per common share | $ | $ | $ | $ | |||||||||||||||||||

| Weighted average number of common shares used in the determination of: | |||||||||||||||||||||||

| Basic | |||||||||||||||||||||||

| Diluted | |||||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements

-4-

GLOBAL WATER RESOURCES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF SHAREHOLDERS’ EQUITY

(in thousands, except share and per share amounts)

(Unaudited)

| Common Stock Shares | Common Stock | Treasury Stock Shares | Treasury Stock | Paid-in Capital | Retained Earnings | Total Equity | |||||||||||||||||||||||||||||||||||

| BALANCE - December 31, 2021 | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||

Dividend declared $ | — | — | — | — | ( | ( | ( | ||||||||||||||||||||||||||||||||||

| Stock option exercise | — | — | — | — | |||||||||||||||||||||||||||||||||||||

| Stock compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| BALANCE - March 31, 2022 | ( | ( | |||||||||||||||||||||||||||||||||||||||

Dividend declared $ | — | — | — | — | ( | ( | |||||||||||||||||||||||||||||||||||

| Treasury stock | — | — | ( | — | ( | — | ( | ||||||||||||||||||||||||||||||||||

| Stock option exercise | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||

| Stock compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| BALANCE - June 30, 2022 | ( | ( | |||||||||||||||||||||||||||||||||||||||

| BALANCE - December 31, 2022 | ( | ( | |||||||||||||||||||||||||||||||||||||||

Dividend declared $ | — | — | — | — | — | ( | ( | ||||||||||||||||||||||||||||||||||

| Stock compensation | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| BALANCE - March 31, 2023 | ( | ( | |||||||||||||||||||||||||||||||||||||||

Dividend declared $ | — | — | — | — | ( | ( | ( | ||||||||||||||||||||||||||||||||||

| Issuance of Common Stock | — | — | — | ||||||||||||||||||||||||||||||||||||||

| Treasury stock | — | — | ( | — | — | — | — | ||||||||||||||||||||||||||||||||||

| Stock option exercise | — | — | — | — | — | — | |||||||||||||||||||||||||||||||||||

| Stock compensation | — | — | — | — | ( | — | ( | ||||||||||||||||||||||||||||||||||

| Net income | — | — | — | — | — | ||||||||||||||||||||||||||||||||||||

| BALANCE - June 30, 2023 | $ | ( | $ | ( | $ | $ | $ | ||||||||||||||||||||||||||||||||||

See accompanying notes to the condensed consolidated financial statements

-5-

GLOBAL WATER RESOURCES, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(Unaudited, in thousands)

| Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| CASH FLOWS FROM OPERATING ACTIVITIES: | |||||||||||

| Net income | $ | ||||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Deferred compensation | |||||||||||

| Depreciation and amortization | |||||||||||

| Right of use amortization | |||||||||||

| Amortization of deferred debt issuance costs and discounts | |||||||||||

| (Gain) Loss on disposal of fixed assets | ( | ( | |||||||||

| Provision for credit losses | |||||||||||

| Deferred income tax expense | |||||||||||

| Changes in assets and liabilities | |||||||||||

| Accounts receivable | ( | ( | |||||||||

| Other current assets | ( | ||||||||||

| Accounts payable and other current liabilities | ( | ||||||||||

| Other noncurrent assets | ( | ||||||||||

| Other noncurrent liabilities | |||||||||||

| Net cash provided by operating activities | |||||||||||

| CASH FLOWS FROM INVESTING ACTIVITIES: | |||||||||||

| Capital expenditures | ( | ( | |||||||||

| Cash paid for acquisitions, net of cash acquired | ( | ( | |||||||||

| Other cash flows from investing activities | ( | ||||||||||

| Net cash used in investing activities | ( | ( | |||||||||

| CASH FLOWS FROM FINANCING ACTIVITIES: | |||||||||||

| Dividends paid | ( | ( | |||||||||

| Advances in aid of construction | |||||||||||

| Refunds of advances for construction | ( | ||||||||||

| Refunds of developer taxes | ( | ||||||||||

| Proceeds from stock option exercise | |||||||||||

| Payments for taxes related to net shares settlement of equity awards | ( | ||||||||||

| Principal payments under finance lease | ( | ( | |||||||||

| Line of credit borrowings, net | |||||||||||

| Loan borrowings | |||||||||||

| Loan repayments | ( | ||||||||||

| Repayments of bond | ( | ( | |||||||||

| Proceeds from sale of stock | |||||||||||

| Net cash provided by (used in) financing activities | ( | ||||||||||

| INCREASE (DECREASE) IN CASH, CASH EQUIVALENTS, AND RESTRICTED CASH | ( | ( | |||||||||

| CASH, CASH EQUIVALENTS, AND RESTRICTED CASH — Beginning of period | |||||||||||

| CASH, CASH EQUIVALENTS, AND RESTRICTED CASH – End of period | |||||||||||

See accompanying notes to the condensed consolidated financial statements

Supplemental disclosure of cash flow information:

| Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted Cash | |||||||||||

| Total cash, cash equivalents, and restricted cash | $ | $ | |||||||||

-6-

GLOBAL WATER RESOURCES, INC.

Notes to the Condensed Consolidated Financial Statements (Unaudited)

1. BASIS OF PRESENTATION, CORPORATE TRANSACTIONS, SIGNIFICANT ACCOUNTING POLICIES, AND RECENT ACCOUNTING PRONOUNCEMENTS

Basis of Presentation and Principles of Consolidation

Arizona Corporation Commission (“ACC”) Rate Case

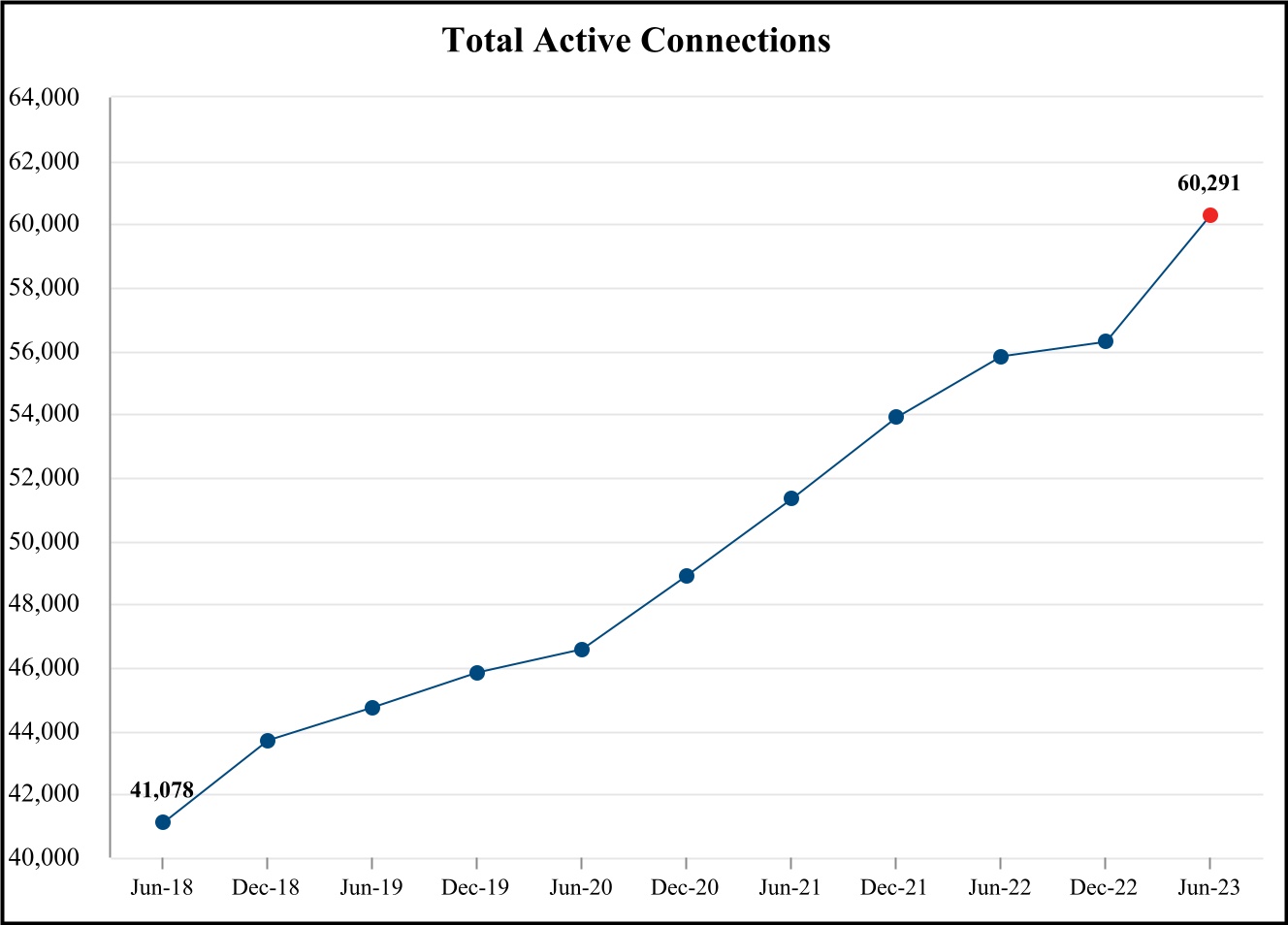

On June 27, 2023, seven of the Company’s 13 regulated utilities each filed a rate case application with the ACC for water rates based on a 2022 test year. In addition to a rate increase, the Company requested, among other things, the consolidation of water rates for certain of its utilities, including Global Water-Mirabell Water Company, Inc. (“Mirabell”), Global Water-Lyn Lee Water Company, Inc. (“Lyn Lee”), Global Water-Francesca Water Company, Inc. (“Francesca”), Global Water-Tortolita Water Company, Inc. (“Tortolita”), Global Water-Rincon Water Company, Inc. (“Rincon”), Global Water-Las Quintas Serenas Water Company, Inc. (“Las Quintas Serenas”), and Global Water-Red Rock Water Company, Inc. (“Red Rock”), each located in Pima County. Of the Company’s utilities, these utilities filing rate applications make up approximately 3 % of the Company’s active service connections. There can be no assurance that the ACC will approve the requested rate increase or any increase or the consolidation of water rates described above, and the ACC could take other actions as a result of the rate case. Further, it is possible that the ACC may determine to decrease future rates. There can also be no assurance as to the timing of when an approved rate increase (if any) would go into effect.

On July 27, 2022, the ACC issued Rate Decision No. 78644 relating to the Company’s previous rate case. Pursuant to Rate Decision No. 78644, the ACC approved, among other things, a collective annual revenue requirement increase of approximately $2.2 million (including the acquisition premiums discussed below) based on 2019 test year service connections, and phased-in over approximately two years .

The ACC also approved: (i) the consolidation of water and/or wastewater rates to create economies of scale that are beneficial to all customers when rates are consolidated; (ii) acquisition premiums relating to the Company’s acquisitions of its Red Rock and Global Water-Turner Ranches Irrigation, Inc. (“Turner Ranches”) utilities, which increase the rate base for such utilities and result in an increase in the annual collective revenue requirement ; (iii) the Company’s ability to annually adjust rates to flow through certain changes in tax expense, primarily related to income taxes, without the necessity of a rate case proceeding; and (iv) a sustainable water surcharge, which will allow semiannual surcharges to be added to customer bills based on verified costs of new water resources.

Refer to Note 2 – “Regulatory Decision and Related Accounting and Policy Changes” for additional information.

-7-

Private Placement Offering of Common Stock

On June 8, 2023, the Company entered into a securities purchase agreement for the issuance and sale by the Company of an aggregate of 230,000 shares of the Company’s common stock at a purchase price of $12.07 per share in an offering exempt from registration pursuant to Section 4(a)(2) of the Securities Act of 1933, as amended (the “Securities Act”), and Rule 506 promulgated thereunder. The Company received gross proceeds of approximately $2.8 million from the offering. One of the Company’s directors purchased an aggregate of 30,000 shares of common stock in the offering at the purchase price.

Public Offering of Common Stock

On August 1, 2022, the Company completed a public offering of 1,150,000 shares of common stock at a public offering price of $13.50 per share, which included 150,000 shares issued and sold to the underwriter following the exercise in full of its option to purchase additional shares of common stock. The Company received net proceeds of approximately $14.9 million from the offering after deducting underwriting discounts and commissions and offering expenses paid by the Company. Certain of the Company’s directors and/or their affiliates purchased an aggregate of 652,000 shares of common stock at the public offering price.

Stipulated Condemnation of the Operations and Assets of Valencia Water Company, Inc.

On July 14, 2015, the Company closed the stipulated condemnation to transfer the operations and assets of Valencia Water Company, Inc. (“Valencia”) to the City of Buckeye. Terms of the condemnation were agreed upon through a settlement agreement and stipulated final judgment of condemnation wherein the City of Buckeye acquired all the operations and assets of Valencia and assumed operation of the utility upon close. The City of Buckeye is obligated to pay the Company a growth premium equal to $3,000 for each new water meter installed within Valencia’s prior service areas in the City of Buckeye, for a 20-year period ending December 31, 2034, subject to a maximum payout of $45.0 million over the term of the agreement. The Company received growth premiums of $0.5 million for both the three months ended June 30, 2023 and 2022 and $0.9 million and $1.6 million for the six months ended June 30, 2023 and 2022, respectively.

Significant Accounting Policies

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| (In thousands) | 2023 | 2022 | 2023 | 2022 | |||||||||||||||||||

| Basic weighted average common shares outstanding | |||||||||||||||||||||||

| Effect of dilutive securities: | |||||||||||||||||||||||

| 2017 Option grant | |||||||||||||||||||||||

| 2019 Option grant | |||||||||||||||||||||||

| 2020 Restricted stock awards | |||||||||||||||||||||||

| 2021 Restricted stock awards | |||||||||||||||||||||||

| Total dilutive securities | |||||||||||||||||||||||

| Diluted weighted average common shares outstanding | |||||||||||||||||||||||

| Anti-dilutive shares excluded from earnings per diluted shares (1) | |||||||||||||||||||||||

Recent Accounting Pronouncements

Recently Adopted Accounting Standards

-8-

In June 2016, the Financial Accounting Standards Board (“FASB”) issued Accounting Standards Update (“ASU”) 2016-13, Financial Instruments—Credit Losses (Topic 326): Measurement of Credit Losses on Financial Instruments, which changed the impairment model for certain financial assets that have a contractual right to receive cash, including trade and loan receivables. The new model required recognition based upon an estimation of expected credit losses rather than recognition of losses based on the probability of occurrence.

The Company is a public business entity that qualifies as a smaller reporting company, and therefore ASU 2016-13 was effective for annual reporting periods beginning after December 15, 2022. The Company adopted the standard utilizing the modified retrospective method for its trade receivables and unbilled revenue on January 1, 2023. Based on the composition of the Company’s trade receivables and unbilled revenue, and expected future losses, the adoption of ASU 2016-13 did not have a material impact on its consolidated financial statements.

2. REGULATORY DECISION AND RELATED ACCOUNTING AND POLICY CHANGES

The Company’s regulated utilities and certain other balances are subject to regulation by the ACC and meet the requirements for regulatory accounting found within Accounting Standards Codification (“ASC 980”), Regulated Operations.

In accordance with ASC 980, rates charged to utility customers are intended to recover the costs of the provision of service plus a reasonable return in the same period. Changes to the rates are made through formal rate applications with the ACC, which the Company has done for all of the operating utilities and which are described below.

On or after July 1, 2023, the water processing facility and part of the wastewater processing facility of the Southwest Plant was placed in service with the remaining parts of the plant to be placed in service once sufficient flows are established. The Southwest Plant was substantially constructed prior to 2009 to process water, wastewater, and recycled water for the area southwest of the City of Maricopa. Due to the unprecedented collapse of the housing market during the Great Recession, the nearly completed plant remained idle for well over a decade. The total cost of the plant was approximately $38.4 million. Also, on July 3, 2023, Global Water-Palo Verde Utilities Company, Inc. (“Palo Verde”) and Global Water-Santa Cruz Water Company, Inc. (“Santa Cruz”) filed an application with the ACC for approval of an accounting order to defer and record as a regulatory asset the depreciation expense recorded for the Southwest Plant, plus the carrying cost at the authorized rate of return set in Palo Verde’s and Santa Cruz’s most recent rate order, until the plant is considered for recovery in the utilities’ next rate case. There can be no assurance, however, that the ACC will approve the application as submitted and the ACC could take other actions regarding the application.

On June 27, 2023, seven of the Company’s 13 regulated utilities each filed a rate case application with the ACC for water rates based on a 2022 test year. In addition to a rate increase, the Company requested, among other things, the consolidation of water rates for certain of its utilities, including Mirabell, Lyn Lee, Francesca, Tortolita, Rincon, Las Quintas Serenas, and Red Rock, each located in Pima County. Of the Company’s utilities, these utilities filing rate applications make up approximately 3 % of the Company’s active service connections. There can be no assurance that the ACC will approve the requested rate increase or any increase or the consolidation of water rates described above, and the ACC could take other actions as a result of the rate case. Further, it is possible that the ACC may determine to decrease future rates. There can also be no assurance as to the timing of when an approved rate increase (if any) would go into effect.

On July 27, 2022, the ACC issued Rate Decision No. 78644 relating to the Company’s previous rate case. Pursuant to Rate Decision No. 78644, the ACC approved, among other things, a collective annual revenue requirement increase of approximately $2.2 million (including the acquisition premiums discussed below) based on 2019 test year service connections, and phased-in over approximately two years, as follows:

| Incremental | Cumulative | ||||||||||

| August 1, 2022 | $ | $ | |||||||||

| January 1, 2023 | $ | $ | |||||||||

| January 1, 2024 | $ | $ | |||||||||

To the extent that the number of active service connections has increased and continues to increase from 2019 levels, the additional revenues may be greater than the amounts set forth above. On the other hand, if active connections decrease or the Company experiences declining usage per customer, the Company may not realize all of the anticipated revenues.

Rate Decision No. 78644 also addressed the primary impacts of the Federal Tax Cuts and Jobs Act (the “TCJA”) on the Company, which is the reduction of the federal income tax rate from 35 percent to 21 percent beginning on January 1, 2018. The TCJA required the Company to re-measure all existing deferred income tax assets and liabilities to reflect the reduction in the federal tax rate. For the Company’s regulated entities, substantially all of the change in deferred income taxes is recorded as

-9-

an offset to either a regulatory asset or liability because the impact of changes in the rates are expected to be recovered from or refunded to customers.

On September 20, 2018, the ACC issued Rate Decision No. 76901, which set forth the reductions in revenue for the Santa Cruz, Palo Verde, Greater Tonopah, and Northern Scottsdale utilities due to the TCJA. Rate Decision No. 76901 adopted a phase-in approach for the reductions to match the phase-in of the revenue requirements under Rate Decision No. 74364. In 2021, the final year of the phase-in, the aggregate annual reductions in revenue for the Santa Cruz, Palo Verde, Greater Tonopah, and Northern Scottsdale utilities were approximately $415,000 , $669,000 , $16,000 , and $5,000 , respectively. The ACC also approved a carrying cost of 4.25 % on regulatory liabilities resulting from the difference of the fully phased-in rates to be applied in 2021 versus the years leading up to 2021 (i.e., 2018 through 2020).

Rate Decision No. 76901, however, did not address the impacts of the TCJA on accumulated deferred income taxes (“ADIT”), including excess ADIT (“EADIT”). Subsequently, Rate Decision No. 78644 approved an adjustor mechanism for income taxes. The adjustor mechanism permits the Company to flow through potential changes to state and federal income tax rates as well as refund or collect funds related to TCJA.

The ACC also approved:

(i) the consolidation of water and/or wastewater rates to create economies of scale that are beneficial to all customers when rates are consolidated;

(ii) acquisition premiums relating to the Company’s acquisitions of its Red Rock and Turner Ranches utilities, which increase the rate base for such utilities and result in an increase in the annual collective revenue requirement included in the table above;

(iii) the Company’s ability to annually adjust rates to flow through certain changes in tax expense, primarily related to income taxes, without the necessity of a rate case proceeding; and

(iv) a sustainable water surcharge, which will allow semiannual surcharges to be added to customer bills based on verified costs of new water resources.

Finally, Rate Decision No. 78644 requires the Company to work with ACC staff and the Residential Utility Consumer Office to prepare a Private Letter Ruling request to the Internal Revenue Service (“IRS”) to clarify whether the failure to eliminate the deferred taxes attributable to assets condemned in a transaction governed by Section 1033 of the Internal Revenue Code (“IRC”) would violate the normalization provisions of Section 168(i)(9) of the IRC. If the IRS accepts the request and issues its ruling, a copy must be provided to the ACC. Within 90 days after providing the ruling to the ACC, ACC Staff shall prepare, for ACC consideration, a memorandum and proposed order regarding guidance issued within the Private Letter Ruling. This may result in further action by the ACC, which the Company is unable to predict due to the uncertainties involved, that could have an adverse impact on its financial condition, results of operations and cash flows.

Certain accounting implications related to Rate Decision No. 78644 were recognized and recorded as of June 30, 2022, and are as follows:

•Reclassification of Red Rock Water, Red Rock Wastewater, and Turner Ranches acquisition premiums of approximately $0.8 million in the aggregate from goodwill to regulatory assets to be included in rate base. The premiums are to be amortized over 25 years.

•Reversal of the 2017 TCJA tax reform regulatory liability of approximately $0.8 million, which was recorded as a reduction to income tax expense for approximately $0.7 million, and as a reduction to interest expense for approximately $0.1 million.

•Write-off of approximately $0.3 million in capitalized rate case costs.

Infrastructure Coordination and Financing Agreements

Infrastructure Coordination and Financing Agreements (“ICFAs”) are agreements with developers and homebuilders where the Company provides services to plan, coordinate, and finance the water and wastewater infrastructure that would otherwise be required to be performed or subcontracted by the developer or homebuilder. Rate Decision No. 74364, issued by the ACC in February 2014, established the policy for the treatment of ICFA funds and also prohibited the Company from entering into any new ICFAs. Rate Decision No. 74364 requires a hook-up fee (“HUF”) tariff to be established for all ICFAs that come due and are paid subsequent to December 31, 2013, which is a set amount per equivalent dwelling unit determined by the ACC based on

-10-

the utility and meter size. In addition, since ICFA funds are generally received in installments, Rate Decision No. 74364 prescribes that 70 % of funds received must be recorded as a HUF liability, with the remaining 30 % to be recorded as deferred revenue, until the HUF liability is fully funded. The Company is responsible for assuring that the full HUF tariff, which is the set amount determined by the rate decision, is funded in the HUF liability, even if it results in recording less than 30% of the overall ICFA funds as deferred revenue. Refer to Note 3 – “Revenue Recognition - Unregulated Revenue” for additional information.

The Company accounts for the portion allocated to the HUF as a contribution in aid of construction (“CIAC”). However, in accordance with the ACC directives, the CIAC is not deducted from rate base until the HUF funds are expended for utility plant. Such funds are segregated in a separate bank account and used for plant.

A HUF liability is established and amortized as a reduction of depreciation expense over the useful life of the related plant once the HUF funds are utilized for the construction of plant. For facilities required under a HUF or ICFA, the utilities must first use the HUF moneys received, after which, it may use debt or equity financing for the remainder of construction.

Regulatory Assets and Liabilities

Regulatory assets and liabilities are the result of operating in a regulated environment in which the ACC establish rates that are designed to permit the recovery of the cost of service and a return on investment. The Company capitalizes and records regulatory assets for costs that would otherwise be charged to expense if it is probable that the incurred costs will be recovered in future rates. Regulatory assets are amortized over the future periods that the costs are expected to be recovered. Final determination of whether a regulatory asset can be recovered is decided by the ACC in regulatory proceedings. If the Company determines that a portion of the regulatory assets is not recoverable in customer rates, the Company would be required to recognize the loss of the assets disallowed.

If costs expected to be incurred in the future are currently being recovered through rates, the Company records those expected future costs as regulatory liabilities.

The Company’s regulatory assets and liabilities consist of the following (in thousands):

| Recovery Period | June 30, 2023 | December 31, 2022 | |||||||||||||||

| Regulatory Assets | |||||||||||||||||

Income taxes recoverable through future rates (1) | Various | $ | |||||||||||||||

Rate case expense surcharge(2) | |||||||||||||||||

Acquisition premiums(3) | |||||||||||||||||

| Total regulatory assets | $ | $ | |||||||||||||||

| Regulatory Liabilities | |||||||||||||||||

Income taxes payable through future rates(1) | |||||||||||||||||

Acquired ICFAs(4) | |||||||||||||||||

| Total regulatory liabilities | $ | $ | |||||||||||||||

(1) The TCJA required the Company to re-measure all existing deferred income tax assets and liabilities to reflect the reduction in the federal tax rate. For the Company’s regulated entities, substantially all of the change in deferred income taxes is recorded as an offset to either a regulatory asset or liability because the impact of changes in the rates are expected to be recovered from or refunded to customers.

(2) Rate Decision No. 78743, issued on October 24, 2022, approved approximately $0.5 million in rate case expenses to be recovered through a rate case expense surcharge over a two-year period.

(3) Decision No. 78319, issued on December 3, 2021, approved an acquisition premium to be amortized over 25 years related to the acquisition of its Rincon Utility. Amortization will begin once the Company receives a decision on the recently filed rate case and the acquisition premium is approved to be included in customer rates. The acquisition premium balance as of June 30, 2023 was approximately $0.5 million.

Rate Decision No. 78644 approved acquisition premiums of approximately $0.8 million related to the acquisitions of its Turner Ranches and Red Rock utilities. Amortization began in 2022 as the acquisition premiums were included in customer rates as approved in the decision.

-11-

3. REVENUE RECOGNITION

Regulated Revenue

The Company’s operating revenues are primarily attributable to regulated services based upon tariff rates approved by the ACC. Regulated service revenues consist of amounts billed to customers based on approved fixed monthly fees and consumption fees, as well as unbilled revenues estimated from the last meter reading date to the end of the accounting period utilizing historical customer data recorded as accrued revenue. The measurement of sales to customers is generally based on the reading of their meters, which occurs on a systematic basis throughout the month. At the end of each month, the Company estimates consumption since the date of the last meter reading and a corresponding unbilled revenue is recognized. The unbilled revenue estimate is based upon the number of unbilled days that month and the average daily customer billing rate from the previous month (which fluctuates based upon customer usage). The Company applies the invoice practical expedient and recognizes revenue from contracts with customers in the amount for which the Company has a right to invoice. The Company has the right to invoice for the volume of consumption, service charge, and other authorized charges.

The Company satisfies its performance obligation to provide water, wastewater, and recycled water services over time as the services are rendered. Regulated services may be terminated by the customers at will, and, as a result, no separate financing component is recognized for the Company’s collections from customers, which generally require payment within 15 days of billing. The Company applies judgment, based principally on historical payment experience, in estimating its customers’ ability to pay.

Total revenues do not include sales tax as the Company considers itself a pass-through conduit for collecting and remitting sales taxes.

Unregulated Revenue

Unregulated revenues represent those revenues that are not subject to the ratemaking process of the ACC. For the three and six months ended June 30, 2023 and June 30, 2022, unregulated revenues primarily related to the revenues recognized on a portion of ICFA funds received.

ICFAs are agreements with developers and homebuilders where the Company provides services to plan, coordinate, and finance the water and wastewater infrastructure that would otherwise be required to be performed or subcontracted by the developer or homebuilder. Services provided within these agreements include coordination of construction services for water and wastewater treatment facilities as well as financing, arranging, and coordinating the provision of utility services. In return, the developers and homebuilders pay the Company an agreed-upon amount per dwelling unit for the land legally described in the agreement, or a portion thereof. Under ICFA agreements, the Company has a contractual obligation to ensure physical capacity exists through its regulated utilities for the provision of water and wastewater utility service to the land when needed. This obligation persists regardless of connection growth.

As these arrangements are with developers and not with the end water or wastewater customer, revenue recognition coincides with the completion of the Company’s performance obligations under the agreement with the developer and the regulated utilities’ ability to provide fitted capacity for water and wastewater service.

Fees for these services are typically a negotiated amount per equivalent dwelling unit for the for the land legally described in the agreement, or a portion thereof. Payments are generally due in installments, with a portion due upon signing of the agreement, a portion due upon completion of certain milestones, and the final payment due upon final plat approval or sale of the subdivision. The payments are non-refundable. The agreements are generally recorded against the land with the appropriate recorder’s office and must be assumed in the event of a sale or transfer of the land. The regional planning and coordination of the infrastructure in the various service areas has been an important part of the Company’s business model.

Rate Decision No. 74364 requires a hook-up fee (“HUF”) tariff to be established for all ICFAs that come due and are paid subsequent to December 31, 2013, which is a set amount per equivalent dwelling unit determined by the ACC based on the utility and meter size. As ICFA funds are generally received in installments, Rate Decision No. 74364 prescribes that 70% of funds received must be recorded as a HUF liability, with the remaining 30% to be recorded as deferred revenue, until the HUF liability is fully funded. The Company is responsible for assuring that the full HUF tariff, which is the set amount determined

-12-

by the rate decision, is funded in the HUF liability, even if it results in recording less than 30% of the overall ICFA funds as deferred revenue.

Refer to Note 2 – “Regulatory Decision and Related Accounting and Policy Changes” for additional information on the accounting treatment of HUF.

The Company believes that these services are not distinct in the context of the contract because they are highly interdependent with the regulated utilities’ ability to provide fitted capacity for water and wastewater services. The Company concluded that the goods and services provided under ICFA contracts constitute a single performance obligation.

ICFA revenue is recognized at a point in time when the regulated utilities have the necessary capacity in place within their infrastructure to provide water/wastewater services to the developer. The Company exercises judgment when estimating the number of equivalent dwelling units that the regulated utilities have capacity to serve.

As of June 30, 2023 and December 31, 2022, ICFA deferred revenue recorded on the consolidated balance sheet totaled $19.4 million and $21.0 million, respectively, which represents deferred revenue recorded for ICFA funds received on contracts. For the six months ended June 30, 2023, ICFA revenue recognized totaled $2.3 million. No

Disaggregated Revenues

For the three and six months ended June 30, 2023 and 2022, disaggregated revenues from contracts with customers by major source and customer class are as follows (in thousands):

| Three Months Ended June 30, | Six Months Ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| REGULATED REVENUE | |||||||||||||||||||||||

| Water Services | |||||||||||||||||||||||

| Residential | $ | $ | $ | $ | |||||||||||||||||||

| Irrigation | |||||||||||||||||||||||

| Commercial | |||||||||||||||||||||||

| Construction | |||||||||||||||||||||||

| Other water revenues | |||||||||||||||||||||||

| Total water revenues | |||||||||||||||||||||||

| Wastewater and recycled water services | |||||||||||||||||||||||

| Residential | |||||||||||||||||||||||

| Commercial | |||||||||||||||||||||||

| Recycled water revenues | |||||||||||||||||||||||

| Other wastewater revenues | |||||||||||||||||||||||

| Total wastewater and recycled water revenues | |||||||||||||||||||||||

| TOTAL REGULATED REVENUE | |||||||||||||||||||||||

| UNREGULATED REVENUE | |||||||||||||||||||||||

| ICFA revenues | |||||||||||||||||||||||

| Rental revenues | |||||||||||||||||||||||

| TOTAL UNREGULATED REVENUE | |||||||||||||||||||||||

| TOTAL REVENUE | $ | $ | $ | $ | |||||||||||||||||||

Contract Balances

-13-

| June 30, 2023 | December 31, 2022 | ||||||||||

| CONTRACT ASSETS | |||||||||||

| Accounts receivable | |||||||||||

| Water services | $ | $ | |||||||||

| Wastewater and recycled water services | |||||||||||

Total contract assets(1) | $ | $ | |||||||||

| CONTRACT LIABILITIES | |||||||||||

| Deferred revenue - ICFA | $ | $ | |||||||||

| Total contract liabilities | $ | $ | |||||||||

Remaining Performance Obligations

Revenue allocated to remaining performance obligations represents contracted revenue that has not yet been recognized, which includes deferred revenue and amounts that will be invoiced and recognized as revenue in future periods. Contracted revenue expected to be recognized in future periods was approximately $19.4 million and $21.0 million at June 30, 2023 and December 31, 2022, respectively. Deferred revenue - ICFA is recognized as revenue once the obligations specified within the applicable ICFA are met, including construction of sufficient operating capacity to serve the customers for which revenue was deferred. Due to the uncertainty of future events, the Company is unable to estimate when to expect recognition of deferred revenue - ICFA.

4. LEASES

The Company measures the lease liability at the present value of future lease payments, excluding variable payments based on usage or performance, and calculates the present value using implicit rates. Leases with an initial term of twelve months or less are not recorded on the balance sheet.

During the year ended December 31, 2022, the Company entered into nine new finance leases for vehicles with either 48 or 60 month terms, all of which include a purchase option.

In January 2022, the Company entered into a five-year finance lease for office equipment which expires on January 31, 2027. There is no purchase option in the lease agreement but the Company controls and obtains substantially all of the benefit from the identified asset.

In December 2021, the Company entered into a new five-year corporate office lease agreement with a commencement date of May 1, 2022. The new monthly rent expense increased to $23,750 for each full calendar month commencing on May 1, 2022 through April 30, 2025 and will increase to $41,572 for each calendar month commencing on May 1, 2025 through April 30, 2027. On March 1, 2022 the Company amended the terms of the lease to incorporate construction of tenant improvements.

-14-

Rent expense arising from the operating leases totaled approximately $98,000 and $71,000 for the three months ended June 30, 2023 and 2022, respectively. Rent expense arising from the operating leases totaled approximately $195,000 and $127,000 for the six months ended June 30, 2023 and 2022, respectively.

The right-of-use (“ROU”) asset recorded represents the Company’s right to use an underlying asset for the lease term and ROU lease liability represents the Company’s obligation to make lease payments arising from the lease. Lease ROU assets and liabilities are recognized at commencement date based on the present value of lease payments over the lease term.

ROU assets at June 30, 2023 and December 31, 2022 consist of the following (in thousands):

| June 30, 2023 | December 31, 2022 | |||||||||||||

| $ | $ | |||||||||||||

| Total | $ | $ | ||||||||||||

Lease liabilities at June 30, 2023 and December 31, 2022 consist of the following (in thousands):

| June 30, 2023 | December 31, 2022 | |||||||||||||

| $ | $ | |||||||||||||

| Total | $ | $ | ||||||||||||

At June 30, 2023, the remaining aggregate annual minimum lease payments are as follows (in thousands):

| Finance Lease Obligations | Operating Lease Obligations | ||||||||||

| 2023 (remaining period) | $ | $ | |||||||||

| 2024 | |||||||||||

| 2025 | |||||||||||

| 2026 | |||||||||||

| 2027 | |||||||||||

| Thereafter | |||||||||||

| Subtotal | |||||||||||

| Less: amount representing interest | ( | ( | |||||||||

| Total | $ | $ | |||||||||

5. PROPERTY, PLANT AND EQUIPMENT

Depreciable property, plant, and equipment at June 30, 2023 and December 31, 2022 consist of the following (in thousands):

| June 30, 2023 | December 31, 2022 | |||||||||||||

| Equipment | $ | $ | ||||||||||||

| Office buildings and other structures | ||||||||||||||

| Transmission and distribution plant | ||||||||||||||

| Total property, plant, and equipment | $ | $ | ||||||||||||

Depreciation of property, plant and equipment is computed based on the estimated useful lives as follows:

| Useful Lives | ||||||||

| Equipment | ||||||||

| Office buildings and other structures | ||||||||

| Transmission and distribution plant | ||||||||

6. ACCOUNTS RECEIVABLE

-15-

| June 30, 2023 | December 31, 2022 | ||||||||||

| Billed receivables | $ | $ | |||||||||

| Less provision for credit losses | ( | ( | |||||||||

| Accounts receivable — net | $ | $ | |||||||||

7. GOODWILL AND INTANGIBLE ASSETS

Goodwill

The goodwill balance was $10.9 million at June 30, 2023 and is related to the Turner, Red Rock, Mirabell, Francesca, Tortolita, Lyn Lee, Las Quintas Serenas, Rincon, Twin Hawks, and Farmers acquisitions. As of June 30, 2022, the Company reclassified approximately $0.8 million of goodwill to regulatory assets related to Red Rock Water, Red Rock Wastewater, and Turner Ranches acquisition premiums as a result of Rate Decision No. 78644 (refer to Note 2 - “Regulatory Decision and Related Accounting and Policy Changes” for additional information). The Farmers acquisition contributed approximately $6.0 million to the change in the goodwill balance (refer to Note 15 - “Acquisitions” for additional information). There were no indicators of impairment identified as a result of the Company’s review of events and circumstances related to its goodwill subsequent to the acquisitions.

As of June 30, 2023 and December 31, 2022, the goodwill balance consisted of the following (in thousands):

| December 31, 2022 Balance | Acquisition Activity | Adjustments Subsequent to Acquisition Date | June 30, 2023 Balance | |||||||||||||||||||||||

| Goodwill | $ | $ | $ | $ | ||||||||||||||||||||||

Intangible Assets

As of June 30, 2023 and December 31, 2022, intangible assets consisted of the following (in thousands):

| June 30, 2023 | December 31, 2022 | ||||||||||||||||||||||||||||||||||

| Gross Amount | Accumulated Amortization | Net Amount | Gross Amount | Accumulated Amortization | Net Amount | ||||||||||||||||||||||||||||||

| INDEFINITE LIVED INTANGIBLE ASSETS: | |||||||||||||||||||||||||||||||||||

| CP Water Certificate of Convenience & Necessity service area | $ | $ | $ | ||||||||||||||||||||||||||||||||

| Intangible trademark | |||||||||||||||||||||||||||||||||||

| Franchise contract rights | |||||||||||||||||||||||||||||||||||

| Organizational costs | |||||||||||||||||||||||||||||||||||

| Total indefinite lived intangible assets | |||||||||||||||||||||||||||||||||||

| DEFINITE LIVED INTANGIBLE ASSETS: | |||||||||||||||||||||||||||||||||||

| Acquired ICFAs | ( | ( | |||||||||||||||||||||||||||||||||

| Sonoran contract rights | ( | ( | |||||||||||||||||||||||||||||||||

| Total definite lived intangible assets | ( | ( | |||||||||||||||||||||||||||||||||

| Total intangible assets | $ | $ | ( | $ | $ | $ | ( | $ | |||||||||||||||||||||||||||

A Certificate of Convenience & Necessity (“CC&N”) is a permit issued by the ACC allowing a public service corporation to serve a specified area, and preventing other public service corporations from offering the same services within the specified area. The CP Water CC&N intangible asset was acquired through the acquisition of CP Water Company in 2006. This CC&N permit has no outstanding conditions that would require renewal.

-16-

8. TRANSACTIONS WITH RELATED PARTIES

9. ACCRUED EXPENSES

Accrued expenses at June 30, 2023 and December 31, 2022 consist of the following (in thousands):

| June 30, 2023 | December 31, 2022 | ||||||||||

| Accrued project liabilities | $ | $ | |||||||||

| Property taxes | |||||||||||

| Asset retirement obligations | |||||||||||

| Customer prepayments | |||||||||||

| Accrued Bonus | |||||||||||

| Dividend payable | |||||||||||

| Deferred compensation | |||||||||||

| Interest | |||||||||||

| Other taxes | |||||||||||

| Accrued professional fees | |||||||||||

| Accrued sales taxes | |||||||||||

| Accrued payroll | |||||||||||

| Other accrued liabilities | |||||||||||

| Total accrued expenses | $ | $ | |||||||||

10. FAIR VALUE

Fair Value of Financial Instruments

FASB ASC 820, Fair Value Measurement, establishes a fair value hierarchy that distinguishes between assumptions based on market data (observable inputs) and the Company’s assumptions (unobservable inputs). The hierarchy consists of three levels, as follows:

•Level 1 - Quoted market prices in active markets for identical assets or liabilities.

•Level 2 - Inputs other than Level 1 that are either directly or indirectly observable.

-17-

•Level 3 - Unobservable inputs developed using the Company’s estimates and assumptions, which reflect those that the Company believes market participants would use.

Financial assets and liabilities measured at fair value on a recurring basis as of June 30, 2023 and December 31, 2022 were as follows (in thousands):

| June 30, 2023 | December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | |||||||||||||||||||||||||||||||||||||||||||

| Asset/Liability Type: | ||||||||||||||||||||||||||||||||||||||||||||||||||

HUF Funds - restricted cash(1) | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

Demand Deposit(2) | ||||||||||||||||||||||||||||||||||||||||||||||||||

Certificate of Deposit - Restricted(1) | ||||||||||||||||||||||||||||||||||||||||||||||||||

Acquisition Liability(3) | ||||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||

(1) HUF Funds - restricted cash and Certificate of Deposit - Restricted are presented on the Restricted cash line item of the Company’s consolidated balance sheets and are valued at amortized cost, which approximates fair value. The increase was primarily driven by additional funds received in growth areas of several utilities.

(2) Demand Deposit is presented on the Cash and cash equivalents line item of the Company’s consolidated balance sheets and is valued at amortized cost, which approximates fair value.

(3) As part of the Red Rock acquisition, the Company is required to pay to the seller a growth premium equal to $750 (not in thousands) for each new account established within three specified growth premium areas, commencing in each area on the date of the first meter installation and ending on the earlier of ten years after such first installation date, or twenty years from the acquisition date. The fair value of the acquisition liability was calculated using a discounted cash flow technique which utilized unobservable inputs developed using the Company’s estimates and assumptions. Significant inputs used in the fair value calculation are as follows: year of the first meter installation, total new accounts per year, years to complete full build out, and discount rate.

In addition, as part of the Farmers acquisition, the Company is required to pay the seller a growth premium equal to $1,000 (not in thousands) for each new account established in the service area, up to a total aggregate growth premium of $3.5 million. The obligation period of the growth premium commences on the closing date of the acquisition and ends ten years after the first new account for residential purposes is established on land that is, at the time of the closing date of the acquisition, undeveloped or unplatted and owned by the seller within the service area or ten years after the date of closing if a new account (as previously described) has not been established.

11. DEBT

The outstanding balances and maturity dates for short-term (including the current portion of long-term debt) and long-term debt as of June 30, 2023 and December 31, 2022 are as follows (in thousands):

| June 30, 2023 | December 31, 2022 | ||||||||||||||||||||||

| Short-term | Long-term | Short-term | Long-term | ||||||||||||||||||||

| BONDS AND NOTES PAYABLE - | |||||||||||||||||||||||

| $ | $ | $ | |||||||||||||||||||||

| OTHER | |||||||||||||||||||||||

| Debt issuance costs | ( | ( | |||||||||||||||||||||

| Loan Payable | |||||||||||||||||||||||

| Total debt | $ | $ | $ | $ | |||||||||||||||||||

Debt is measured at fair value on a recurring basis as of June 30, 2023 and December 31, 2022 as follows (in thousands):

| June 30, 2023 | December 31, 2022 | |||||||||||||||||||||||||||||||||||||||||||||||||

| Level 1 | Level 2 | Level 3 | Total | Level 1 | Level 2 | Level 3 | Total | |||||||||||||||||||||||||||||||||||||||||||

Long-term debt(3) | ||||||||||||||||||||||||||||||||||||||||||||||||||

-18-

2016 Senior Secured Notes

On June 24, 2016, the Company issued two series of senior secured notes with an aggregate total principal balance of $115.0 million at a blended interest rate of 4.55 %. Series A carries a principal balance of $28.8 million and bears an interest rate of 4.38 % over a twelve-year term, with the principal payment due on June 15, 2028. Series B carries a principal balance of $78.6 million and bears an interest rate of 4.58 % over a 20 -year term. Series B was interest only for the first five years, with $1.9 million principal payments paid semiannually thereafter beginning December 2021. The senior secured notes are collateralized by a security interest in the Company’s equity interest in its subsidiaries, including all payments representing profits and qualifying distributions.

The senior secured notes require the Company to maintain a debt service coverage ratio of consolidated EBITDA to consolidated debt service of at least 1.10 to 1.00. Consolidated EBITDA is calculated as net income plus depreciation and amortization, taxes, interest and other non-cash charges net of non-cash income. Consolidated debt service is calculated as interest expense, principal payments, and dividend or stock repurchases. The senior secured notes also contain a provision limiting the payment of dividends if the Company falls below a debt service ratio of 1.25 . However, for the quarter ended June 30, 2021 through the quarter ending March 31, 2024, the debt service ratio drops to 1.20 . The debt service ratio increases to 1.25 for any fiscal quarter during the period from and after June 30, 2024. As of June 30, 2023, the Company was in compliance with its financial debt covenants.

Revolving Credit Line

On April 30, 2020, the Company entered into an agreement with Northern Trust for a two-year revolving line of credit initially up to $10.0 million with an initial maturity date of April 30, 2022 (as amended, the “Northern Trust Loan Agreement”). This credit facility, which may be used to refinance existing indebtedness, to acquire assets to use in and/or expand the Company’s business, and for general corporate purposes, initially bore an interest rate equal to London Interbank Offered Rate (LIBOR) plus 2.00 % and had no unused line fee.

On April 30, 2021, the Company and Northern Trust entered into an amendment to the Northern Trust Loan Agreement pursuant to which, among other things, the maturity date for the Company’s revolving credit line was extended from April 30, 2022 to April 30, 2024.

On July 26, 2022, the Company and Northern Trust entered into a second amendment to the Northern Trust Loan Agreement, which, among other things, further extended the scheduled maturity date for the revolving line of credit from April 30, 2024 to July 1, 2024, increased the maximum principal amount available for borrowing from $10.0 million to $15.0 million, and replaced the LIBOR interest rate provisions with provisions based on the Secured Overnight Financing Rate (SOFR).

On June 28, 2023, the Company and Northern Trust entered into a third amendment to the Northern Trust Loan Agreement, which, among other things, (i) further amended the scheduled maturity date for the revolving line of credit from July 1, 2024 to July 1, 2025 and (ii) added a quarterly facility fee equal to 0.35 % of the average daily unused amount of the revolving line of credit.

The Northern Trust Loan Agreement requires the Company to maintain a debt service coverage ratio of consolidated EBITDA to consolidated debt service of at least 1.10 to 1.00. The Northern Trust 1.25 . However, for the quarter ending June 30, 2021 through the quarter ending March 31, 2024, the ratio drops to 1.20 . As of June 30, 2023, the Company was in compliance with its financial debt covenants.

As of June 30, 2023 and December 31, 2022, the outstanding borrowings on this credit line were $6.8 million and $0 , respectively. There were approximately $6,000 and $9,812 unamortized debt issuance costs as of June 30, 2023 and December 31, 2022, respectively.

In 2020, ASU 2020-04 was issued establishing ASC 848, Reference Rate Reform, and in 2021 ASU 2021-01, Reference Rate Reform (Topic 848): Scope was issued (collectively, “ASC 848”). ASC 848 contains practical expedients for reference rate reform related activities that impact debt, leases, derivatives and other contracts. The guidance in ASC 848 is optional and may be elected over time as reference rate reform activities occur. In 2022, ASU 2022-06, Deferral of the Sunset Date of Topic 848 (ASU 2022-06) was issued to defer the sunset date of ASC 848 to December 31, 2024. ASU 2022-06 is effective immediately for all companies. The Company continues to evaluate the impact of ASC 848.

-19-

| Debt | |||||

| 2023 (remaining period) | $ | ||||

| 2024 | |||||

| 2025 | |||||

| 2026 | |||||

| 2027 | |||||

| Thereafter | |||||

| Subtotal | |||||

| Less: amount representing interest | — | ||||

| Total | $ | ||||

12. INCOME TAXES

For the three months ended June 30, 2023, the Company recorded tax expense of $0.7 million calculated on pre-tax income of $2.5 million. For the three months ended June 30, 2022, tax expense of $0.5 million was calculated on pre-tax income of $2.0 million, which was offset by approximately $0.7 million from the reversal of the regulatory liability related to Rate Decision No. 78622 (refer to Note 2 — “Regulatory Decision and Related Accounting and Policy Changes” for additional information) resulting in a net tax benefit of $0.2 million.

For the six months ended June 30, 2023, the Company recorded tax expense of $1.6 million calculated on pre-tax income of $5.8 million. For the six months ended June 30, 2022, the tax expense of $0.2 million was calculated on pre-tax income of $3.2 million, which was partially offset by approximately $0.7 million from the reversal of the regulatory liability related to Rate Decision No. 78622 as described above.

13. DEFERRED COMPENSATION AWARDS

Stock-based compensation

Stock-based compensation related to option awards is measured based on the fair value of the award. The fair value of stock option awards is determined using a Black-Scholes option-pricing model. The Company recognizes compensation expense associated with the options over the vesting period.

2017 stock option grant

In August 2017, GWRI’s Board of Directors granted stock options to acquire 465,000 shares of GWRI’s common stock to employees throughout the Company. The options were granted with an exercise price of $9.40 , the market price of the Company’s common shares on the NASDAQ Global Market at the close of business on August 10, 2017. The options vested over a four-year period, with 25 % having vested in August 2018, 25 % having vested in August 2019, 25 % having vested in August 2020, and 25 % having vested in August 2021. The options have a 10 -year life. The Company expensed the $1.1 million fair value of the stock option grant ratably over the four-year vesting period. As of August 2021, these options were fully expensed. As of June 30, 2023, 127,454 options have been exercised and 64,625 options have been forfeited with 268,321 options outstanding.

2019 stock option grant

In August 2019, GWRI’s Board of directors granted stock options to acquire 250,000 shares of GWRI’s common stock to employees throughout the Company. The options were granted with an exercise price of $11.26 , the market price of the Company’s common shares on the NASDAQ Global Market at the close of business on August 13, 2019. The options vest over a four-year period, with 25 % having vested in August 2020, 25 % having vested in August 2021, 25 % having vested in August 2022, and 25 % vesting in August 2023. The options have a 10-year life. The Company will expense the $0.8 million fair value of the stock option grant ratably over the four-year vesting period. Stock-based compensation expense of $29,000 and $45,000 was recorded for the three months ended June 30, 2023 and 2022, respectively, and $72,000 and $90,000 was recorded for the six months ended June 30, 2023 and 2022, respectively. As of June 30, 2023, 42,217 options have been exercised and 28,782 options have been forfeited with 179,001 options outstanding.

-20-

Phantom stock/Restricted stock units compensation

Restricted stock units are granted in the first quarter based on the prior year’s performance and vest over a three year period. The units are credited quarterly using the closing price of the Company’s common stock on the applicable record date for the respective quarter. The following table details total awards granted and the number of units outstanding as of June 30, 2023, along with the amounts paid to holders of the phantom stock units (“PSUs”) and/or restricted stock units (“RSUs”) for the years ended June 30, 2023 and 2022 (in thousands, except unit amounts):

| Amounts Paid For the Three Months Ended June 30, | Amounts Paid For the Six Months Ended June 30, | |||||||||||||||||||||||||||||||||||||

| Grant Date | Units Granted | Units Outstanding | 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||||||||||||||

| Q1 2019 | — | $ | — | $ | — | $ | — | $ | ||||||||||||||||||||||||||||||

| Q1 2020 | — | — | — | |||||||||||||||||||||||||||||||||||

Q1 2021(1) | ||||||||||||||||||||||||||||||||||||||

Q1 2022(1) | ||||||||||||||||||||||||||||||||||||||

Q1 2023(1) | — | — | ||||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||

Stock appreciation rights compensation

The following table details the recipients of the stock appreciation rights (“SARs”) awards, the grant date, units granted, exercise price, outstanding units as of June 30, 2023 and amounts paid during the three and six months ended June 30, 2023 and 2022 (in thousands, except unit and per unit amounts):

| Amounts Paid For the Three Months Ended June 30, | Amounts Paid For the Six Months Ended June 30, | |||||||||||||||||||||||||||||||||||||||||||||||||

| Recipients | Grant Date | Units Granted | Exercise Price | Units Outstanding | 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||||||||||||||||||||||||

Members of Management (1)(2) | Q1 2015 | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||

Members of Management (1)(3) | Q3 2017 | $ | ||||||||||||||||||||||||||||||||||||||||||||||||

Members of Management (1)(4) | Q1 2018 | $ | ||||||||||||||||||||||||||||||||||||||||||||||||

| Total | $ | $ | $ | $ | ||||||||||||||||||||||||||||||||||||||||||||||

(1)The SARs vest ratably over 16 quarters from the grant date.

(2)The exercise price was determined to be the fair market value of one share of GWRC stock on the grant date of February 11, 2015.

(3)The exercise price was determined to be the fair market value of one share of GWRI stock on the grant date of August 10, 2017.

(4)The exercise price was determined to be the fair market value of one share of GWRI stock on the grant date of March 12, 2018.

For the three months ended June 30, 2023 and 2022, the Company recorded approximately $0.1 million and $0.1 million of compensation expense related to the PSUs/RSUs and SARs, respectively. These are liability awards, so when the stock price decreases, cumulative compensation expense is reduced, which can lead to negative compensation in a given period. Based on GWRI’s closing share price on June 30, 2023 (the last trading date of the quarter), deferred compensation expense to be recognized over future periods is estimated for the years ending December 31 as follows (in thousands):

| RSUs / PSUs | |||||

| 2023 | $ | ||||

| 2024 | |||||

| 2025 | |||||

| Total | $ | ||||

Restricted stock compensation

-21-

14. SUPPLEMENTAL CASH FLOW INFORMATION

| For the Six Months Ended June 30, | |||||||||||

| 2023 | 2022 | ||||||||||

| Supplemental cash flow information: | |||||||||||

| Cash paid for interest | $ | $ | |||||||||

| Non-cash financing and investing activities: | |||||||||||

| Capital expenditures included in accounts payable and accrued liabilities | $ | $ | |||||||||

| Business acquisition through issuance of contingent consideration payable | $ | $ | |||||||||

15. ACQUISITIONS

Acquisition of Farmers Water Company

On February 1, 2023, the Company acquired all of the equity of Farmers, an operator of a water utility with service area in Pima County, Arizona, for a total consideration of $7.6 million consisting of $6.2 million in cash plus a growth premium estimated at $1.4 million. The acquisition added approximately 3,300 active water service connections and approximately 21.5 square miles of service area in Sahuarita, Arizona and the surrounding unincorporated area of Pima County.

The acquisition was accounted for as a business combination under ASC 805, “Business Combinations” and the purchase price was allocated to the acquired utility assets and liabilities based on the acquisition-date fair values. Fair values are determined in accordance with ASC 820 “Fair Value Measurement,” which allows for the characteristics of the acquired assets and liabilities to be considered, particularly restrictions on the use of the asset and liabilities. Regulation is considered both a restriction on the use of the assets and liabilities, as it relates to inclusion in rate base, and a fundamental input to measuring the fair value in a business combination. Substantially all the Company’s operations are subject to the rate-setting authority of the ACC and are accounted for pursuant to accounting guidance for regulated operations. The rate-setting and cost recovery provisions currently in place for the Company’s regulated operations provide revenues derived from costs, including a return on investment of assets and liabilities included in rate base. As such, the fair value of the Company’s assets and liabilities subject to these rate-setting provisions approximates the pre-acquisition carrying values and does not reflect any net valuation adjustments.

Under the terms of the purchase agreement, the Company is obligated to pay the seller a growth premium equal to $1,000 for each new account established in the service area, up to a total aggregate growth premium of $3.5 million. The obligation period of the growth premium commences on the closing date of the acquisition and ends (i) ten years after the first new account for residential purposes is established on land that is, at the time of the closing date of the acquisition, undeveloped or unplatted and owned by the seller within the service area or (ii) ten years after the date of closing if a new account (as described above) has not been established.

-22-

A preliminary purchase price allocation of the net assets acquired in the transaction is as follows (in thousands):

| Net assets acquired: | |||||

| Cash | $ | ||||

| Accounts receivable | |||||

| Property, plant and equipment | |||||

| Construction work-in-progress | |||||

| Prepaids | |||||

Intangibles(1) | |||||

| Other taxes | ( | ||||

| Other accrued liabilities | ( | ||||

| Developer deposits | ( | ||||

| AIAC | ( | ||||

| CIAC | ( | ||||

| Total net assets assumed | |||||

| Goodwill | |||||

| Total purchase price | $ | ||||

(1) Intangibles consist of franchise contract rights and organization costs. Refer to Note 7 — “Goodwill & Intangible Assets” for additional information regarding the intangibles.

The goodwill reflects the value paid primarily for the long-term potential for connection growth as a result of the Company’s increased scale and diversity, opportunities for synergies, and an improved risk profile.

16. COMMITMENTS AND CONTINGENCIES

Commitments

The Company has operating and finance leases for vehicles, office equipment, and office space. Refer to Note 4 – “Leases” for additional information.

On October 16, 2018, the Company completed the acquisition of Red Rock, an operator of a water and a wastewater utility with service areas in the Pima and Pinal counties of Arizona. Under the terms of the purchase agreement, the Company is obligated to pay to the seller a growth premium equal to $750 for each new account established within three specified growth premium areas, commencing in each area on the date of the first meter installation and ending on the earlier of ten years after such first installation date or twenty years from the acquisition date. As of June 30, 2023, no meters have been installed and no accounts have been established in any of the three growth premium areas.

Contingencies

From time to time, in the ordinary course of business, the Company may be subject to pending or threatened lawsuits in which claims for monetary damages are asserted. Management is not aware of any legal proceeding of which the ultimate resolution could materially affect the Company’s financial position, results of operations, or cash flows.

-23-

ITEM 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following management’s discussion and analysis of Global Water Resources, Inc.’s (the “Company”, “GWRI”, “we”, or “us”) financial condition and results of operations (“MD&A”) relate to the three and six months ended June 30, 2023 and should be read together with the consolidated financial statements and accompanying notes included in Part I, Item 1 of this report.

Cautionary Statement Regarding Forward-Looking Statements

Certain statements in this Quarterly Report on Form 10-Q are forward-looking in nature and may constitute “forward-looking information” within the meaning of applicable securities laws. Often, but not always, forward-looking statements can be identified by the words “believes”, “anticipates”, “plans”, “expects”, “intends”, “projects”, “estimates”, “objective”, “goal”, “focus”, “aim”, “should”, “could”, “may”, and similar expressions. These forward-looking statements include future estimates described in “Business Outlook”, “Factors Affecting our Results of Operations”, and “Liquidity and Capital Resources”. These forward-looking statements include, but are not limited to, statements about our strategies; expectations about future business plans, prospective performance, growth, and opportunities; future financial performance; regulatory and Arizona Corporation Commission (“ACC”) proceedings and approvals, such as the anticipated benefits resulting from Rate Decision No. 78644, including our expected collective revenue increase due to new water and wastewater rates and benefits from consolidation of rates; our Private Letter Ruling request in connection with our previous rate case and possible further action that may be taken by the ACC following such request; acquisition plans and our ability to complete additional acquisitions; population and growth projections; technologies, including expected benefits from implementing such technologies; revenues; metrics; operating expenses; trends relating to our industry, market, population growth, and housing permits; the adequacy of our water supply to service our current demand and growth for the foreseeable future; liquidity; plans and expectations for capital expenditures; cash flows and uses of cash; dividends; depreciation and amortization; tax payments; our ability to repay indebtedness and invest in initiatives; the anticipated impact and resolutions of legal matters; the anticipated impact of new or proposed laws, including regulatory requirements, tax changes, and judicial decisions; the anticipated impact of accounting changes and other pronouncements.

Forward-looking statements should not be read as a guarantee of future performance or results. They are based on numerous assumptions that we believe are reasonable, but they are open to a wide range of uncertainties and business risks. Consequently, actual results may vary materially from what is contained in a forward-looking statement. Investors are cautioned not to place undue reliance on forward-looking information. A number of factors could cause actual results to differ materially from the results discussed in the forward-looking statements, including risks related to legal, regulatory, and legislative matters; risks related to our business and operations; risks related to market and financial matters; risk related to technology; risks related to the ownership of our common stock; and certain general risks, which could have a material adverse effect on our business, financial condition, results of operations and cash flows. These and other factors are discussed in the risk factors described in Part I, Item 1A “Risk Factors” in our Annual Report on Form 10-K for the year ended December 31, 2022 (the “2022 Form 10-K”). Additionally, there may be other risks described from time to time in the reports that we file with the Securities and Exchange Commission (the “SEC”). Any forward-looking statement speaks only as of the date of this report. Except as required by law, we undertake no obligation to publicly release the results of any revision to these forward-looking statements that may be made to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Overview

GWRI is a water resource management company that owns, operates, and manages twenty-nine water, wastewater, and recycled water systems in strategically located communities, principally in metropolitan Phoenix and Tucson, Arizona. The Company seeks to deploy an integrated approach, referred to as “Total Water Management.” Total Water Management is a comprehensive approach to water utility management that reduces demand on scarce non-renewable water sources and costly renewable water supplies, in a manner that ensures sustainability and greatly benefits communities both environmentally and economically. This approach employs a series of principles and practices that can be tailored to each community:

•Reuse of recycled water, either directly or to non-potable uses, through aquifer recharge, or possibly direct potable reuse in the future;

•Regional planning;

•Use of advanced technology and data;

•Employing respected subject matter experts and retaining thought and application leaders;

-24-

•Leading outreach and educational initiatives to ensure all stakeholders including customers, development partners, regulators, and utility staff are knowledgeable on the principles and practices of the Total Water Management approach; and

•Establishing partnerships with communities, developers, and industry stakeholders to gain support of the Total Water Management principles and practices.

Business Outlook